EGYPTIAN AUTOMOTIVE MARKET - amicegypt.comamicegypt.com/Data/amic_april2010_report.pdf ·...

45

EGYPTIAN AUTOMOTIVE AMIC APRIL 2010 REPORT MARKET Sponsored By:

Transcript of EGYPTIAN AUTOMOTIVE MARKET - amicegypt.comamicegypt.com/Data/amic_april2010_report.pdf ·...

EGYPTIAN AUTOMOTIVE

AMIC APRIL 2010 REPORT

MARKET

Sponsored By:

Sponsored by:

1. Preface 3

2.. Local industry analysis 4

2.1. Total market 5

2.2. Passenger cars market 11

2.3. Buses market 27

2.4. Trucks market 35

3. Monthly news flash 15th to 15th 43

3.1. Egypt macro flash 44

3.2. Automotive industry local news clips 45

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

2

Sponsored by:

1. PREFACE

The methodology, used in this report is mainly relying on the following steps:

* Gathering primary and secondary data from AMIC Egypt members.

* Validating missing data and cross checking of data from different sources

* Processing, Analyzing and presenting data in a useful way to AMIC Egypt

members.

* Gathering Macro Economic and Automotive industry news from: Newspapers

and other sources

Confidentiality Clause:

This report as well as the attached Excel sheet are the Exclusive property

of AMIC Egypt and its members and should not be reproduced or distributed

to outsider parties.

This report was prepared and developed by:

Integrated Management Consultancy – IMC, which is a Management Consultancy

Office with specific areas of strengths in:

* Marketing – Specially Business to Business,

* Human Resources – Specifically in Learning Organizations,

* Six Sigma Methodology - Manufacturing.

* SME Upgrading and Training - World bank / Business Edge Partner

* On the Job Coaching.

IMC

TEL. /FAX: + (202) 2690 1472 / + (202) 2690 1476 / + (202) 258 4015

MOBILE: + (2010) 19 757 11

Rami Y. Camel-Toueg & Associates22 RASHID ST. OFF EL OROUBA ST. 1ST FLOOR, SUITE # 6,

11341 HELIOPOLIS, CAIRO, EGYPT.

Email: [email protected]

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

3

Sponsored by:

2. LOCAL INDUSTRY ANALYSIS

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

4

Sponsored by:

2.1. TOTAL AUTOMOTIVE MARKET

Total Market split April 2009 - April 2010 in volume

Total Market volume for the month of April 2010 was higher than April 2009

sales by to units.

The Passenger cars segment had a volume increase of in units, when

comparing April 09 to April 10; the Buses segment had a volume increase

of , and the Trucks segment had a volume decrease of

19,34115,601Total Market Volume

from

Total Market Volume

36%

3% -8%

24% 15,601 19,341

11,086

Buses

Passenger Cars Passenger Cars

Buses2,8851,420

15,036

1,384Trucks3,131Trucks

PC, 11,086 ,

71%

Buses, 1,384 , 9%

Trucks, 3,131 , 20%

April 09

PC, 15,036 , 78%

Buses, 1,420 , 7%

Trucks, 2,885 , 15%

April 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

5

Sponsored by:

Total Market split YTD 09 – YTD 10 in volume

Total Market volume for the YTD 2010 was higher than YTD 2009 sales by

to units.

The Passenger cars segment had a volume increase of almost 52% in units,

when comparing YTD 2010 to YTD 2009; the Buses segment had a volume growth of 9%

12,403

Passenger Cars

4,703 Buses

59,595

11,018 TrucksTrucksBuses

Passenger Cars39,169

5,110

54,890Total Market Volume 77,108

77,108

and the Trucks segment had a volume increase of

40%

13%

Total Market Volume

54,890

PC, 39,169 , 71%

Buses, 4,703 , 9%

Trucks, 11,018 , 20%

YTD 2009

PC, 59,595 , 77%

Buses, 5,110 , 7%

Trucks, 12,403 , 16%

YTD 2010

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

6

Sponsored by:

Total Market April 10 sales analysis in volume

This chart is developed in order to assist in giving a comparative view of current

month results to all directly relevant previous results, which could have impact on

future market performance projections and/or demand forecasts.

This chart has been developed consistently for all 3 sectors.

* April 2010 sales are higher than 2010 YTD average by

* April 2010 sales are higher than 2009 YTD average by

* April 2010 sales are higher than 2009 average by

* April 2010 sales are higher than April 2009 by

* April 2010 sales are lower than March 2010 by

Performance in April 2010 is higher than the YTD 2009 average,

April 2009, and the YTD 2010 average but lower than March 2010.

24.0%

-6.0%

0.3%

40.9%

12.9%

17,551

19,647 20,569

19,341

10,765

13,148

15,376 15,601

15,931

19,536 19,616

18,944 17,711

19,756 18,723

20,414

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010

2009

2010 YTD Avg

2009 YTD Avg

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

7

Sponsored by:

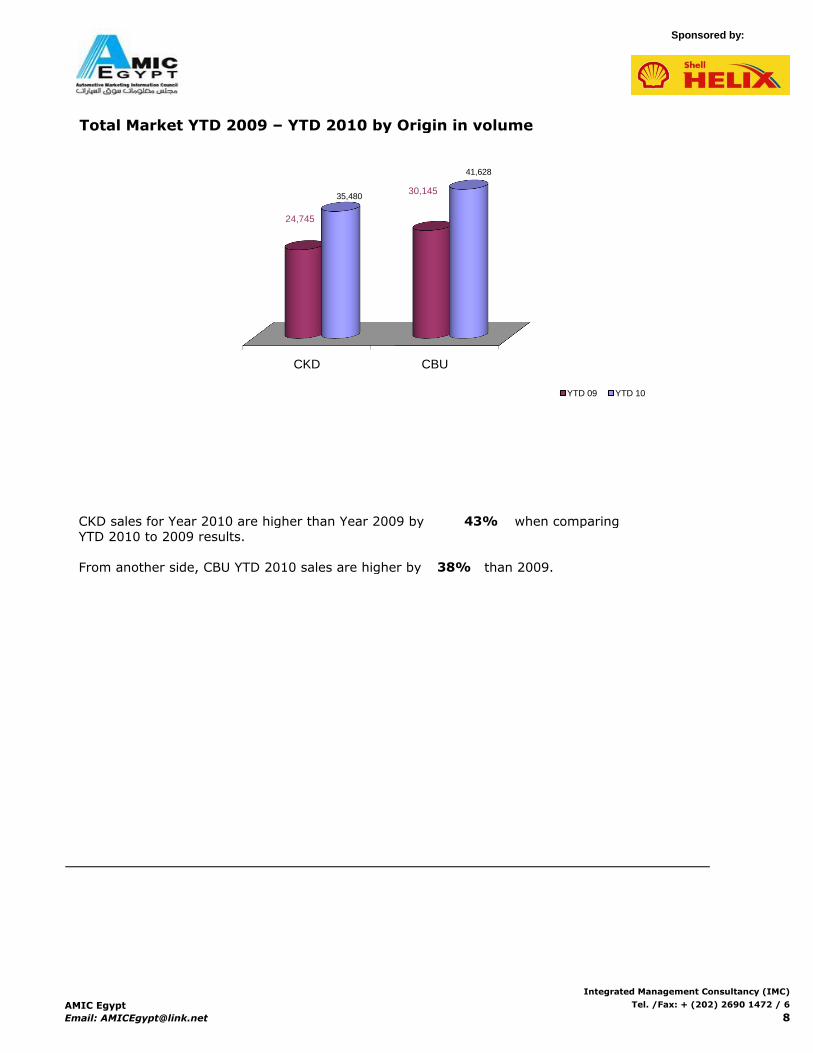

Total Market YTD 2009 – YTD 2010 by Origin in volume

CKD sales for Year 2010 are higher than Year 2009 by when comparing

YTD 2010 to 2009 results.

From another side, CBU YTD 2010 sales are higher by than 2009.38%

43%

CKD CBU

24,745

30,145 35,480

41,628

YTD 09 YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

8

Sponsored by:

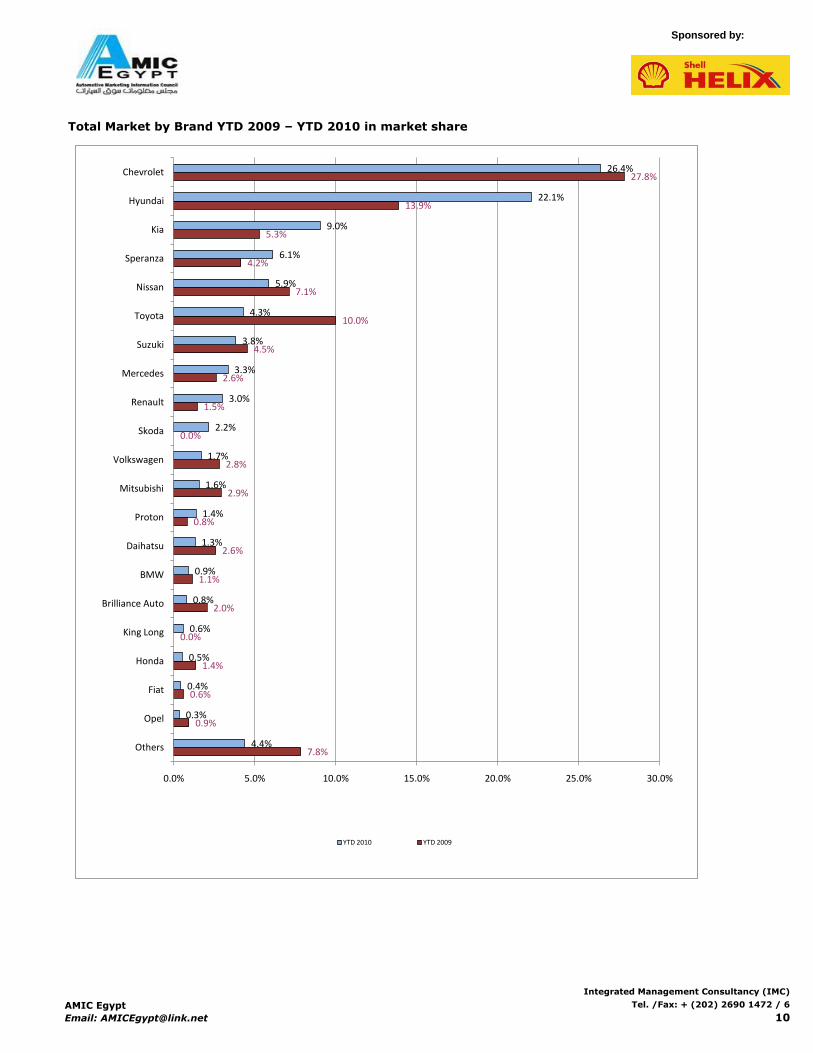

Total Market by Brand YTD 2009 – YTD 2010 in volume

4,303

514

332

748

0

1,124

631

1,424

454

1,607

1,546

0

799

1,440

2,492

5,495

3,908

2,279

2,902

7,623

15,269

3,377

267

334

408

449

606

692

1,018

1,062

1,198

1,303

1,663

2,321

2,581

2,954

3,309

4,523

4,718

6,976

17,031

20,318

0 5,000 10,000 15,000 20,000 25,000

Others

Opel

Fiat

Honda

King Long

Brilliance Auto

BMW

Daihatsu

Proton

Mitsubishi

Volkswagen

Skoda

Renault

Mercedes

Suzuki

Toyota

Nissan

Speranza

Kia

Hyundai

Chevrolet

YTD 2010 YTD 2009

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

9

Sponsored by:

Total Market by Brand YTD 2009 – YTD 2010 in market share

7.8%

0.9%

0.6%

1.4%

0.0%

2.0%

1.1%

2.6%

0.8%

2.9%

2.8%

0.0%

1.5%

2.6%

4.5%

10.0%

7.1%

4.2%

5.3%

13.9%

27.8%

4.4%

0.3%

0.4%

0.5%

0.6%

0.8%

0.9%

1.3%

1.4%

1.6%

1.7%

2.2%

3.0%

3.3%

3.8%

4.3%

5.9%

6.1%

9.0%

22.1%

26.4%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Others

Opel

Fiat

Honda

King Long

Brilliance Auto

BMW

Daihatsu

Proton

Mitsubishi

Volkswagen

Skoda

Renault

Mercedes

Suzuki

Toyota

Nissan

Speranza

Kia

Hyundai

Chevrolet

YTD 2010 YTD 2009

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

10

Sponsored by:

2.2 PASSENGER CARS

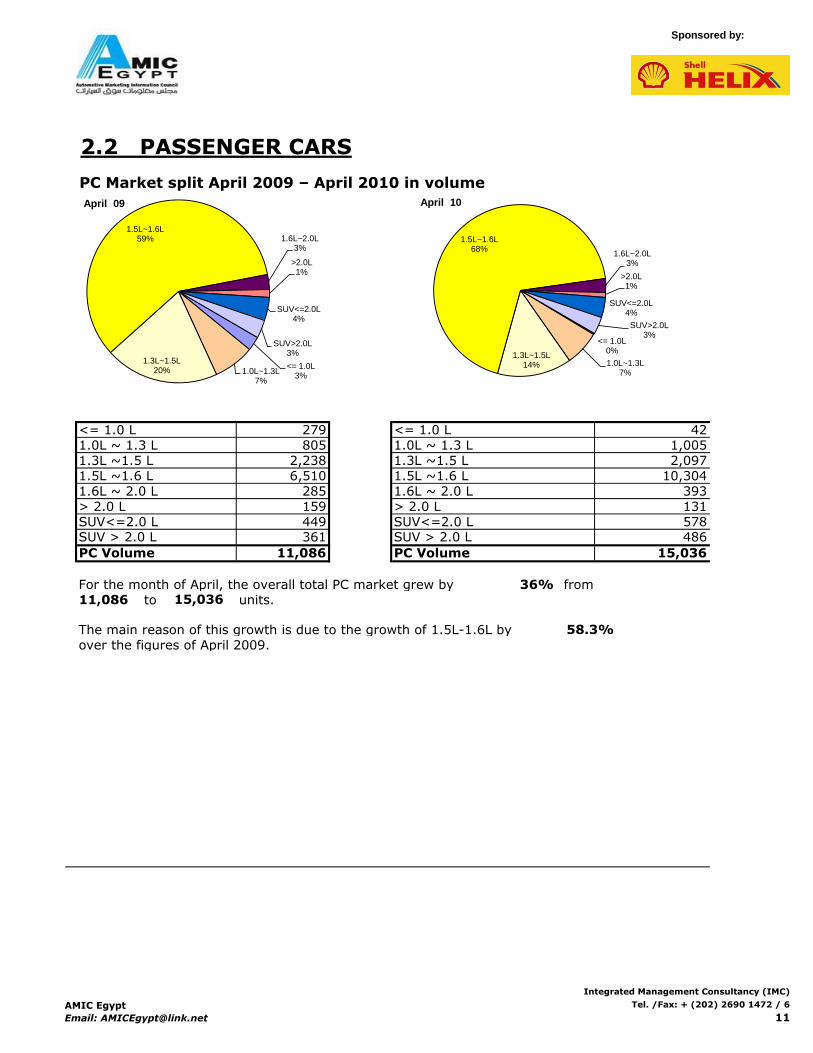

PC Market split April 2009 – April 2010 in volume

For the month of April, the overall total PC market grew by 36% from

to units.

The main reason of this growth is due to the growth of 1.5L-1.6L by

over the figures of April 2009.

1,005

<= 1.0 L

2,238

1.0L ~ 1.3 L

42

805

2,097

131

285

1.0L ~ 1.3 L

279<= 1.0 L

1.3L ~1.5 L

> 2.0 L

15,036

> 2.0 L

PC Volume

SUV<=2.0 L 449

1.6L ~ 2.0 L

SUV<=2.0 LSUV > 2.0 L

PC Volume

1.3L ~1.5 L

578

15,036

1.5L ~1.6 L

159

11,086

1.5L ~1.6 L

58.3%

10,3046,510

1.6L ~ 2.0 L

486361

393

SUV > 2.0 L

11,086

<= 1.0L3%

1.0L~1.3L7%

1.3L~1.5L20%

1.5L~1.6L59% 1.6L~2.0L

3%

>2.0L1%

SUV<=2.0L4%

SUV>2.0L3%

April 09

<= 1.0L0%

1.0L~1.3L7%

1.3L~1.5L14%

1.5L~1.6L68%

1.6L~2.0L3%

>2.0L1%

SUV<=2.0L4%

SUV>2.0L3%

April 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

11

Sponsored by:

PC Market split YTD 2009 – YTD 2010 in volume

The overall total PC market grew by 52% from units to

units.

The main reason of this growth is due to the 1.5L-1.6L which has respective growth

of over the figures of 2009.

<= 1.0 L 1,332

PC Volume 59,595

<= 1.0 L 925

1.0L ~ 1.3 L 3,635 1.0L ~ 1.3 L 3,391

1.3L ~1.5 L 8,755

540

SUV > 2.0 L2,4991,894

39,460

9,511

1,282

SUV<=2.0 L

633

1.3L ~1.5 L

1.5L ~1.6 L1.5L ~1.6 L

59,59539,169

-31%

-7%

9%

95%

27%

95%

PC Volume

1.6L ~ 2.0 L 1,008

1,851

39,169

> 2.0 L 17%

38%2%

SUV<=2.0 L 1,812

1.6L ~ 2.0 L

SUV > 2.0 L

20,236

> 2.0 L

52%

<= 1.0L3%

1.0L~1.3L9%

1.3L~1.5L22%

1.5L~1.6L52%

1.6L~2.0L3%

>2.0L1%

SUV<=2.0L5%

SUV>2.0L5%

YTD 09

<= 1.0L2%1.0L~1.3L

6%1.3L~1.5L

16%

1.5L~1.6L66%

1.6L~2.0L2%

>2.0L1%

SUV<=2.0L4%

SUV>2.0L3%

YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

12

Sponsored by:

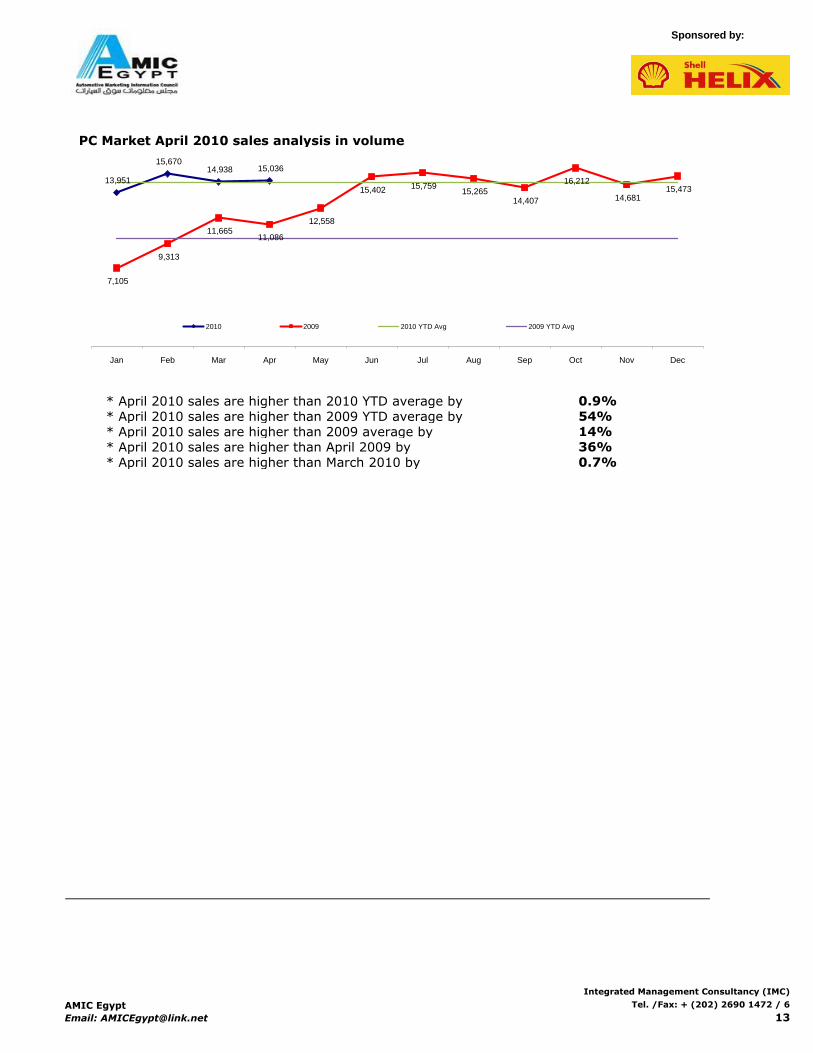

PC Market April 2010 sales analysis in volume

* April 2010 sales are higher than 2010 YTD average by

* April 2010 sales are higher than 2009 YTD average by

* April 2010 sales are higher than 2009 average by

* April 2010 sales are higher than April 2009 by

* April 2010 sales are higher than March 2010 by

14%

54%

36%

0.7%

0.9%

13,951

15,670 14,938 15,036

7,105

9,313

11,665 11,086

12,558

15,402 15,759 15,265

14,407

16,212

14,681 15,473

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2009 2010 YTD Avg 2009 YTD Avg

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

13

Sponsored by:

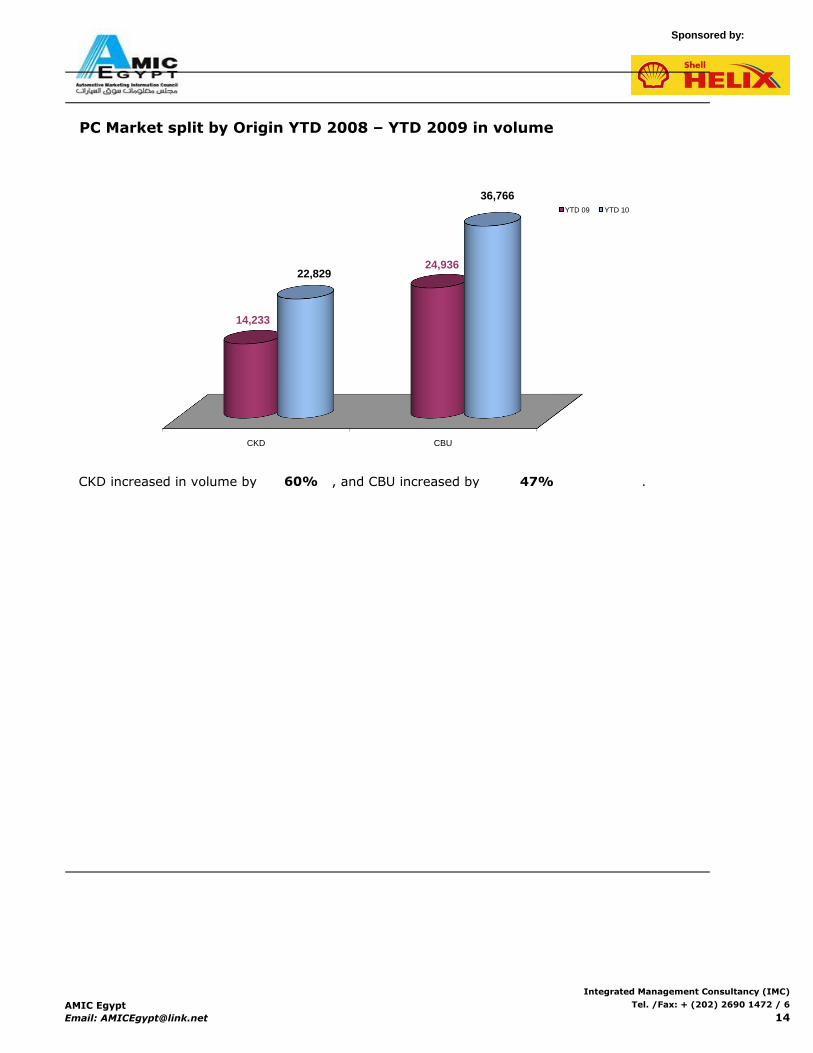

PC Market split by Origin YTD 2008 – YTD 2009 in volume

CKD increased in volume by , and CBU increased by 47% .60%

CKD CBU

14,233

24,936 22,829

36,766

YTD 09 YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

14

Sponsored by:

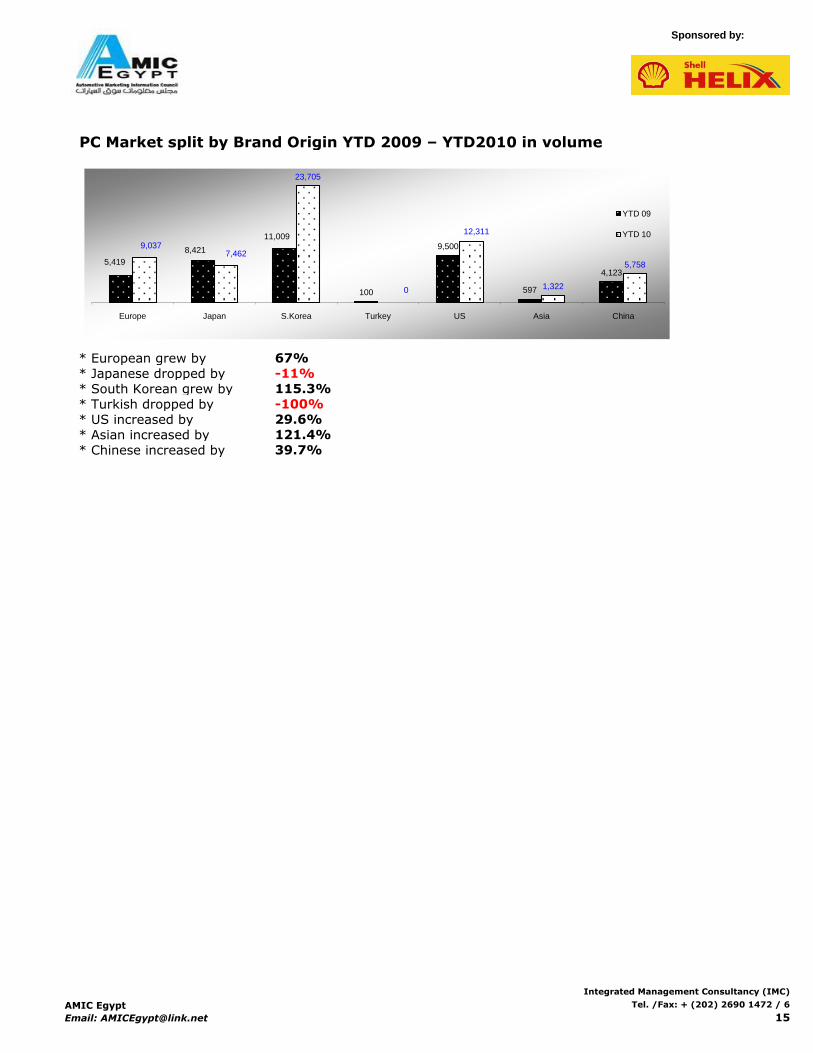

PC Market split by Brand Origin YTD 2009 – YTD2010 in volume

* European grew by

* Japanese dropped by

* South Korean grew by

* Turkish dropped by

* US increased by

* Asian increased by

* Chinese increased by

29.6%

67%

-11%

115.3%

-100%

121.4%

39.7%

5,419

8,421

11,009

100

9,500

597

4,123

9,037 7,462

23,705

0

12,311

1,322

5,758

Europe Japan S.Korea Turkey US Asia China

YTD 09

YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

15

Sponsored by:

PC Market by Brand YTD 2009 – YTD2010 in volume

2,794

100

516

182

514

714

329

748

996

1,024

631

893

454

1,483

2,285

-

1,116

753

2,402

2,279

2,902

8,645

7,591

2,606

-

-

258

267

295

334

408

449

688

692

979

1,062

1,292

1,346

1,663

1,682

2,321

3,487

4,718

6,976

11,601

16,729

Others

TOFAS

DAEWOO

Geely

OPEL

BRILLIANCE

FIAT

Honda

MITSUBISHI

DAIHATSU

BMW

Suzuki

Proton

VW

TOYOTA

SKODA

MERCEDES

RENAULT

Nissan

Speranza

KIA

Chevrolet

HYUNDAI

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

16

Sponsored by:

PC Market by Brand YTD 2008 – YTD2009 in Market Share

8%

0%

1%

1%

1%

2%

1%

2%

3%

3%

2%

3%

1%

4%

6%

0%

3%

2%

7%

6%

8%

24%

21%

4.37%

0.00%

0.00%

0.43%

0.45%

0.50%

0.56%

0.68%

0.75%

1.15%

1.16%

1.64%

1.78%

2.17%

2.26%

2.79%

2.82%

3.89%

5.85%

7.92%

11.71%

19.47%

28.07%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

Others

TOFAS

DAEWOO

Geely

OPEL

BRILLIANCE

FIAT

Honda

MITSUBISHI

DAIHATSU

BMW

Suzuki

Proton

VW

TOYOTA

SKODA

MERCEDES

RENAULT

Nissan

Speranza

KIA

Chevrolet

HYUNDAI

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

17

Sponsored by:

PC Brands by Origin versus CKD & CBU YTD 2009 – YTD2010 (Volume)

CKD

* Hyundai increased by

* Chevrolet increased by

* Speranza increased by

* Mercedes increased by 56%

* BMW sales increased by 11%

* Nissan increased by 56%

* Komodo dropped by -66%

* Mahindra decreased by -58%

* Brilliance Auto dropped by -50%

CBU

* Hyundai grew by

* Kia increased by

* Chevrolet increased by

* Renault increased by

* Skoda increased from Zero sales

* Toyota dropped by

* VW dropped by

* Proton increased by

* Suzuki increased by

* Daihatsu decreased by

* Mercedes increased by

* Nissan increased by

* Mitsubishi decreased by

* Honda decreased by

* Seat increased by

* Fiat increased by

* Geely increased by

* Brilliance Auto dropped by

* Opel decreased by -64%

* BMW increased by

78%

-41%

-55%

208%

56%

-13%

229%

110%

16%

-45%

4%

44%

10%

134%

-33%

42%

-60%

6%

140%

202%

2%

110

104

143

592

505

486

654

1,897

2,246

4,766

2,112

248

52

60

200

462

541

1,019

2,954

4,718

5,535

6,957

Others

BRILLIANCE Auto

MAHINDRA

KOMODO

JEEP

BMW

MERCEDES

Nissan

Speranza

Chevrolet

HYUNDAI

YTD 10

YTD 09

1,142

145

512

610

182

329

120

748

996

505

462

1,024

893

454

1,483

2,285

0

753

3,879

2,902

5,479

1,016

151

184

243

258

334

362

408

449

533

663

688

979

1,062

1,292

1,346

1,663

2,321

6,066

6,976

9,772

Others

BMW

OPEL

BRILLIANCE Auto

Geely

FIAT

SEAT

HONDA

MITSUBISHI

Nissan

MERCEDES

DAIHATSU

Suzuki

Proton

VW

TOYOTA

SKODA

RENAULT

Chevrolet

KIA

HYUNDAI

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

18

Sponsored by:

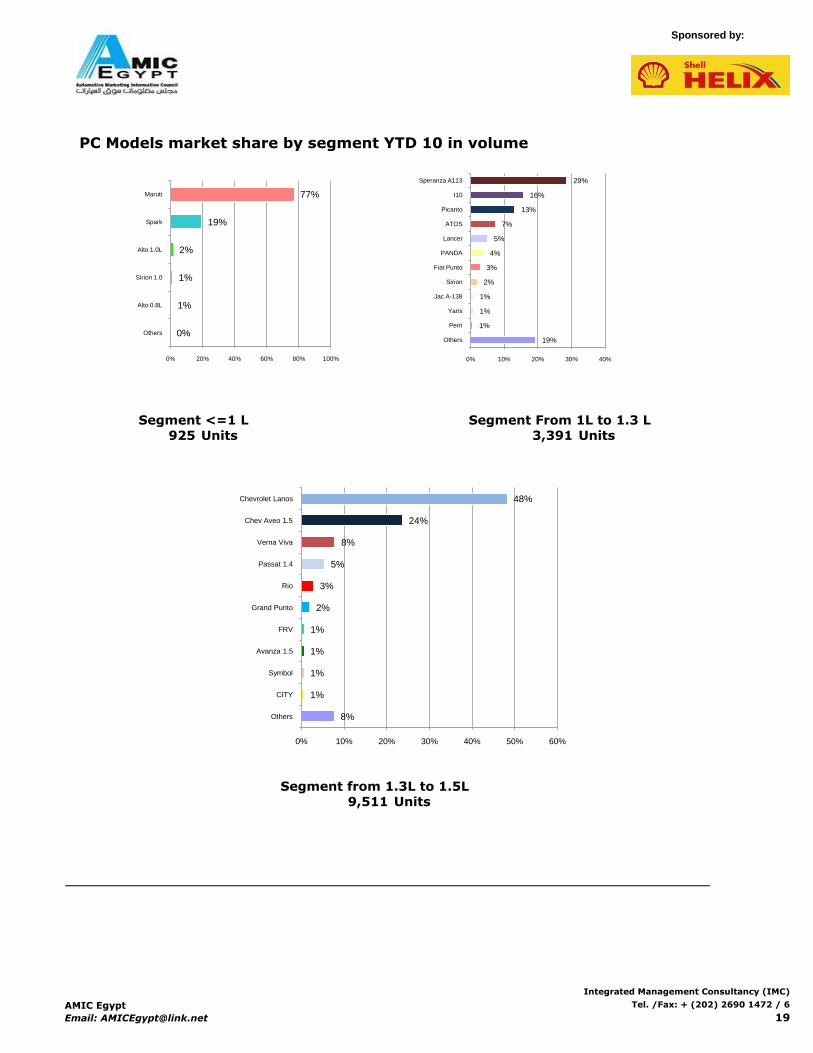

PC Models market share by segment YTD 10 in volume

925

Segment From 1L to 1.3 L

UnitsUnits 3,391

Units

Segment <=1 L

Segment from 1.3L to 1.5L

9,511

0%

1%

1%

2%

19%

77%

0% 20% 40% 60% 80% 100%

Others

Alto 0.8L

Sirion 1.0

Alto 1.0L

Spark

Maruti

19%

1%

1%

1%

2%

3%

4%

5%

7%

13%

16%

29%

0% 10% 20% 30% 40%

Others

Perri

Yaris

Jac A-138

Sirion

Fiat Punto

PANDA

Lancer

ATOS

Picanto

I10

Speranza A113

8%

1%

1%

1%

1%

2%

3%

5%

8%

24%

48%

0% 10% 20% 30% 40% 50% 60%

Others

CITY

Symbol

Avanza 1.5

FRV

Grand Punto

Rio

Passat 1.4

Verna Viva

Chev Aveo 1.5

Chevrolet Lanos

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

19

Sponsored by:

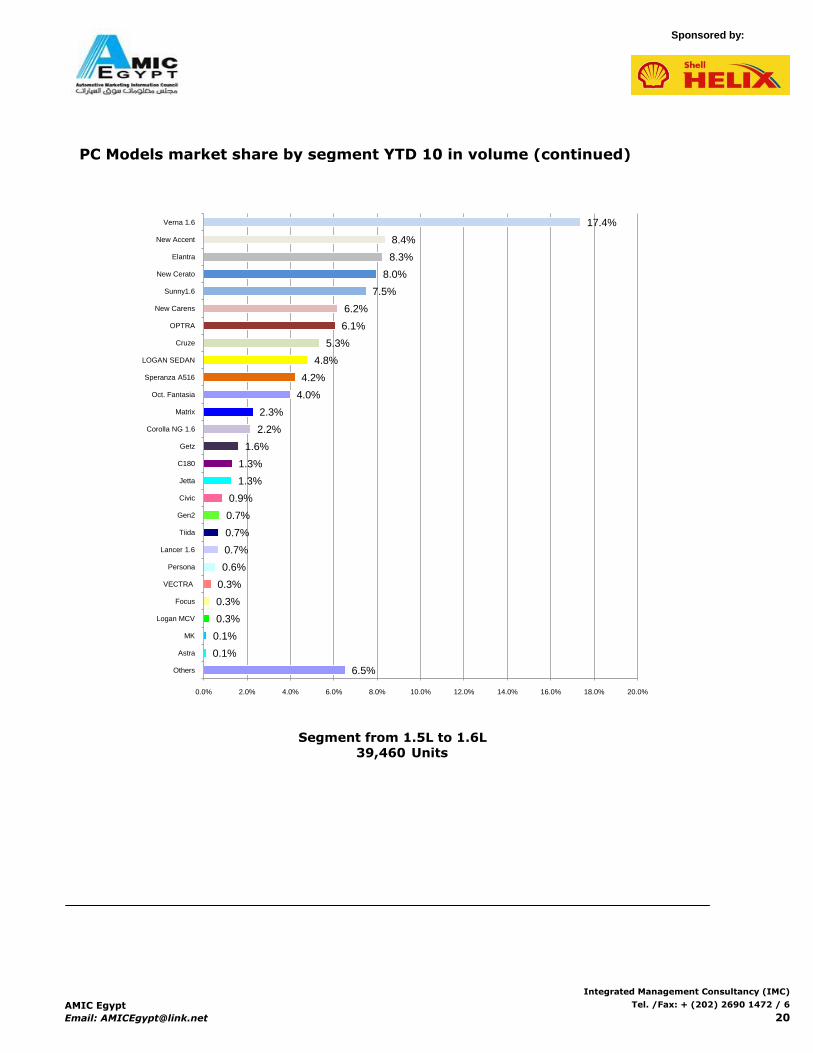

PC Models market share by segment YTD 10 in volume (continued)

Segment from 1.5L to 1.6L

39,460 Units

6.5%

0.1%

0.1%

0.3%

0.3%

0.3%

0.6%

0.7%

0.7%

0.7%

0.9%

1.3%

1.3%

1.6%

2.2%

2.3%

4.0%

4.2%

4.8%

5.3%

6.1%

6.2%

7.5%

8.0%

8.3%

8.4%

17.4%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0%

Others

Astra

MK

Logan MCV

Focus

VECTRA

Persona

Lancer 1.6

Tiida

Gen2

Civic

Jetta

C180

Getz

Corolla NG 1.6

Matrix

Oct. Fantasia

Speranza A516

LOGAN SEDAN

Cruze

OPTRA

New Carens

Sunny1.6

New Cerato

Elantra

New Accent

Verna 1.6

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

20

Sponsored by:

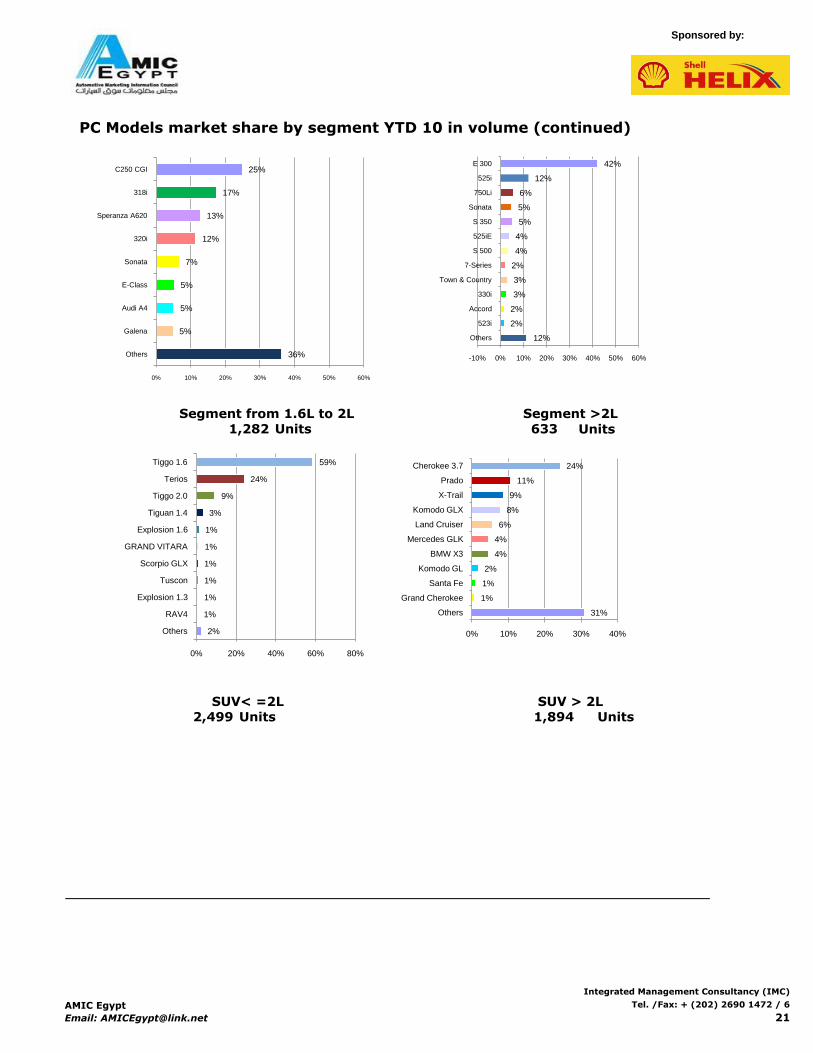

PC Models market share by segment YTD 10 in volume (continued)

Units

SUV > 2L

2,499 Units Units

SUV< =2L

Units

Segment >2LSegment from 1.6L to 2L

1,282 633

1,894

36%

5%

5%

5%

7%

12%

13%

17%

25%

0% 10% 20% 30% 40% 50% 60%

Others

Galena

Audi A4

E-Class

Sonata

320i

Speranza A620

318i

C250 CGI

12%

2%

2%

3%

3%

2%

4%

4%

5%

5%

6%

12%

42%

-10% 0% 10% 20% 30% 40% 50% 60%

Others

523i

Accord

330i

Town & Country

7-Series

S 500

525iE

S 350

Sonata

750Li

525i

E 300

2%

1%

1%

1%

1%

1%

1%

3%

9%

24%

59%

0% 20% 40% 60% 80%

Others

RAV4

Explosion 1.3

Tuscon

Scorpio GLX

GRAND VITARA

Explosion 1.6

Tiguan 1.4

Tiggo 2.0

Terios

Tiggo 1.6

31%

1%

1%

2%

4%

4%

6%

8%

9%

11%

24%

0% 10% 20% 30% 40%

Others

Grand Cherokee

Santa Fe

Komodo GL

BMW X3

Mercedes GLK

Land Cruiser

Komodo GLX

X-Trail

Prado

Cherokee 3.7

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

21

Sponsored by:

PC by Model YTD 2009 – YTD 2010 in volume (>800 cars)

14,211

20

31

234

485

-

255

394

167

662

704

221

604

1,105

505

372

528

780

384

669

672

1,287

1,187

624

-

-

886

191

-

2,008

159

1,897

809

2,108

1060

3,579

2,064

12,210

-

-

-

-

-

27

135

170

228

262

295

343

445

462

512

533

585

638

713

746

860

900

949

971

1,431

1,575

1,662

1,896

2,109

2,392

2,440

2,954

3,146

3,261

3,304

4,586

6,855

Others

SHAHIN 1.4

LANOS 1.5

New Passat

NUBIRA

OCTAVIA A5

Yaris

VECTRA

LANCER 1.3

Tiggo 2.0

LANCER 1.6

Gen 2

Civic 1.6

Picanto

CHEROKEE 3.7

Jetta

i10

Terios

GETZ 1.6

Suzuki Maruti

Verna Viva

COROLLA NG 1.6

MATRIX

AVEO 1.5

Speranza A113

Tiggo 1.6

Oct. Fantasia

Speranza A516

LOGAN SEDAN

Cruze

OPTRA

New Carens

SUNNY

New Cerato

ELANTRA

New Accent 1.6

Chevrolet Lanos

Verna 1.6

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

22

Sponsored by:

PC YTD Volume by Price Segment

- <= 50,000 EGP

- >50,000 EGP ~ <= 70,000 EGP

- >70,000 EGP ~ <= 100,000 EGP

- >100,000 EGP ~ <= 150,000 EGP

- >150,000 EGP ~ <= 300,000 EGP

- >300,000 EGP ~ <= 500,000 EGP

- >500,000 EGP

The following graphs show segmentation for the PC market according to Price segment in EGP.

Both volume in units and market share in percentage are presented in seven segments:

18,538

16,49515,018

5,580

1,289 1,264 713

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

50,000 - 70,000 70,000 - 100,000 100,000 - 150,000 150,000 - 300,000 300,000 - 500,000 >500,000 <=50,000

Un

its

EGP

The above graph shows that the (50,000 EGP ~ 70,000 EGP) segment has the highest volume

with 18,538 units, followed by the (70,000 EGP ~ 100,000 EGP) segment with 16,495 units. The least segment is the (<=50,000 EGP) with 713 units followed by the (>500,000 EGP) segment with 1,264 units.

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

23

Sponsored by:

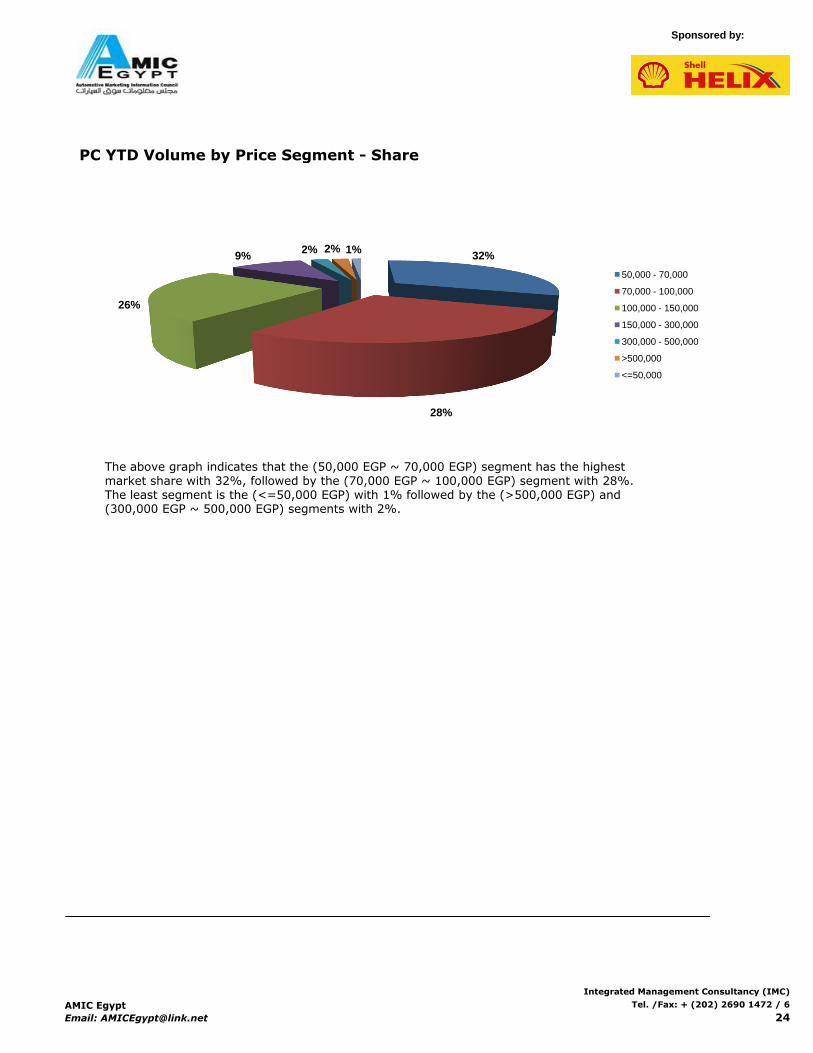

PC YTD Volume by Price Segment - Share

32%

28%

26%

9%2% 2% 1%

50,000 - 70,000

70,000 - 100,000

100,000 - 150,000

150,000 - 300,000

300,000 - 500,000

>500,000

<=50,000

The above graph indicates that the (50,000 EGP ~ 70,000 EGP) segment has the highest market share with 32%, followed by the (70,000 EGP ~ 100,000 EGP) segment with 28%. The least segment is the (<=50,000 EGP) with 1% followed by the (>500,000 EGP) and (300,000 EGP ~ 500,000 EGP) segments with 2%.

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

24

Sponsored by:

Taxi Project Sales

Taxi Project Sales as Percentage of Total PC Sales

441

1297

2028

1777 1795

13551429

1633 16851573

1423

363

141

0

500

1000

1500

2000

2500

Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10

Total Taxi

3.98%

10.33%

13.17%

11.28%11.76%

9.41%8.81%

11.12%

10.89%

11.28%

9.08%

2.43%

0.94%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10

Percentage of Total PC

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

25

Sponsored by:

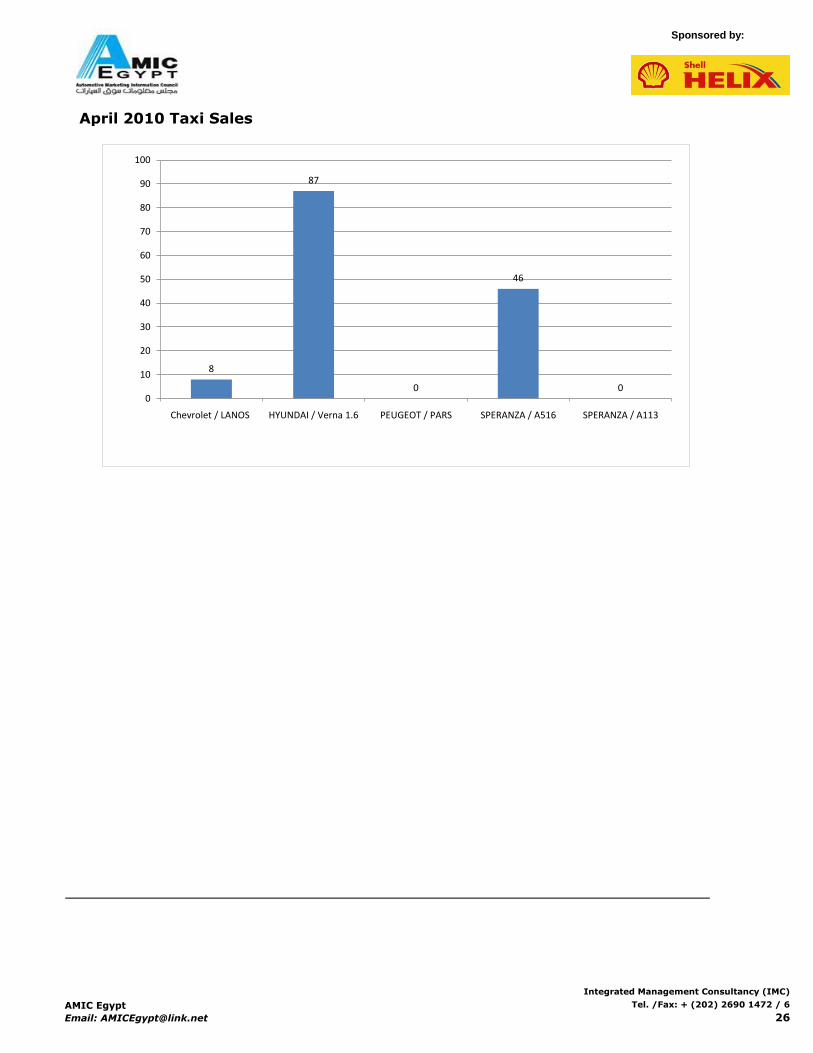

April 2010 Taxi Sales

8

87

0

46

00

10

20

30

40

50

60

70

80

90

100

Chevrolet / LANOS HYUNDAI / Verna 1.6 PEUGEOT / PARS SPERANZA / A516 SPERANZA / A113

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

26

Sponsored by:

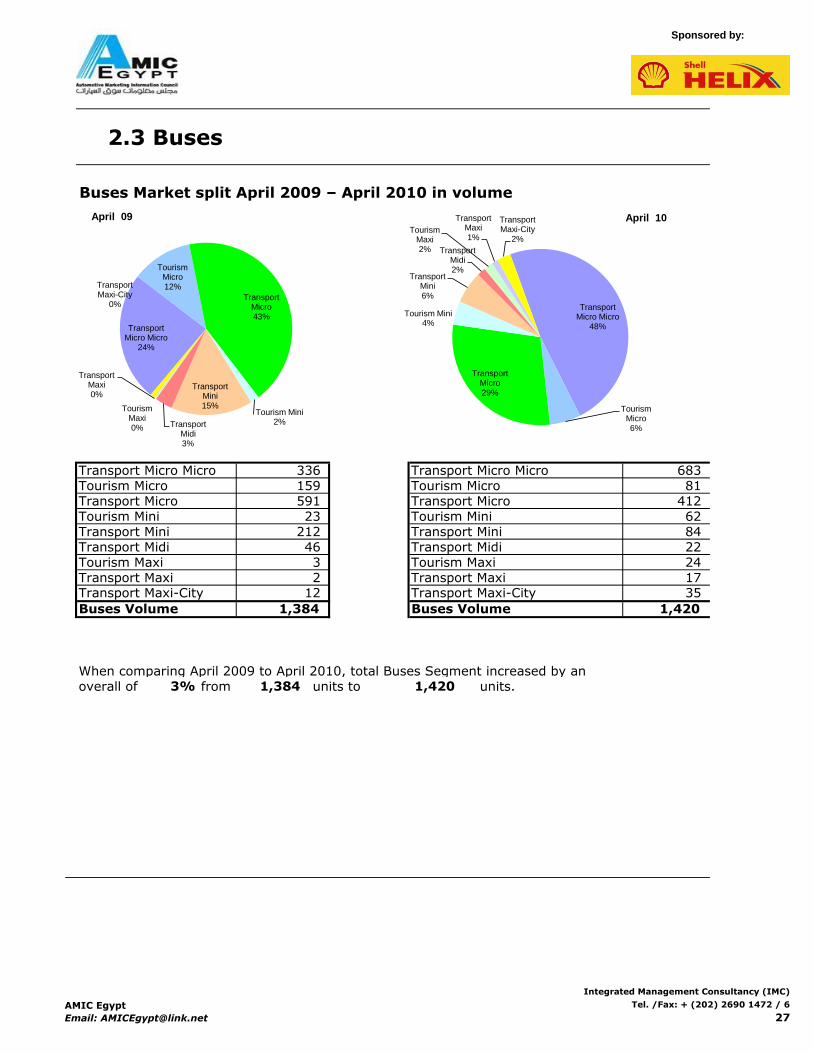

2.3 Buses

Buses Market split April 2009 – April 2010 in volume

When comparing April 2009 to April 2010, total Buses Segment increased by an

overall of from units to units.

Transport Micro Micro 336 683 Transport Micro Micro

Tourism Mini

84

22

Tourism Maxi

212

46

Transport Mini

Tourism Micro

Transport Micro

Tourism Mini

Tourism Micro

23

Transport Maxi-City12

Buses Volume

1,384

1,384

Transport Mini

412

Transport Midi

Transport Maxi

24

159

591

81

Transport Micro

3

62

17

1,420

Transport Midi

35

1,420

Tourism Maxi

Buses Volume

Transport Maxi

3%

2 Transport Maxi-City

Transport Micro Micro

24%

Tourism Micro12%

Transport Micro43%

Tourism Mini2%

Transport Mini15%

Transport Midi3%

Tourism Maxi0%

Transport Maxi0%

Transport Maxi-City

0%

April 09

Transport Micro Micro

48%

Tourism Micro6%

Transport Micro29%

Tourism Mini4%

Transport Mini6%

Transport Midi2%

Tourism Maxi2%

Transport Maxi1%

Transport Maxi-City

2%

April 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

27

Sponsored by:

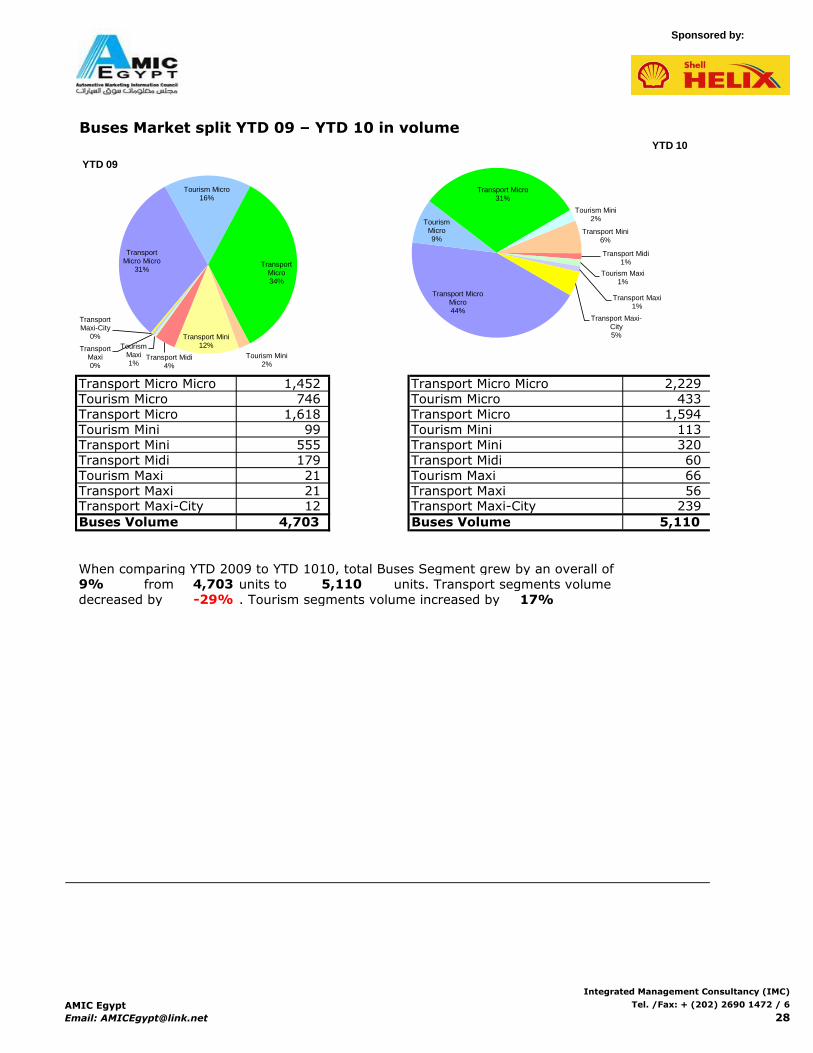

Buses Market split YTD 09 – YTD 10 in volume

When comparing YTD 2009 to YTD 1010, total Buses Segment grew by an overall of

from units to units. Transport segments volume

decreased by . Tourism segments volume increased by 17%

Transport Micro Micro

320

Transport Midi

113

Transport Micro 1,594

Buses Volume

Tourism Maxi

2,229

555

Transport Midi

Transport Micro Micro

Transport Maxi-City

4,703

1,452

60

Transport Maxi

179

Transport Micro

21

433 Tourism MicroTourism Micro

1,618

746

Tourism Mini

56

Transport Mini

99

Tourism Maxi 66

Transport Mini

Transport Maxi 21

Tourism Mini

4,703

-29%

12

Buses Volume 5,110

5,110

239 Transport Maxi-City

9%

Transport Micro Micro

31%

Tourism Micro16%

Transport Micro34%

Tourism Mini2%

Transport Mini12%

Transport Midi4%

Tourism Maxi1%

Transport Maxi0%

Transport Maxi-City

0%

YTD 09

Transport Micro Micro44%

Tourism Micro9%

Transport Micro31%

Tourism Mini2%

Transport Mini6%

Transport Midi1%

Tourism Maxi1%

Transport Maxi1%

Transport Maxi-City5%

YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

28

Sponsored by:

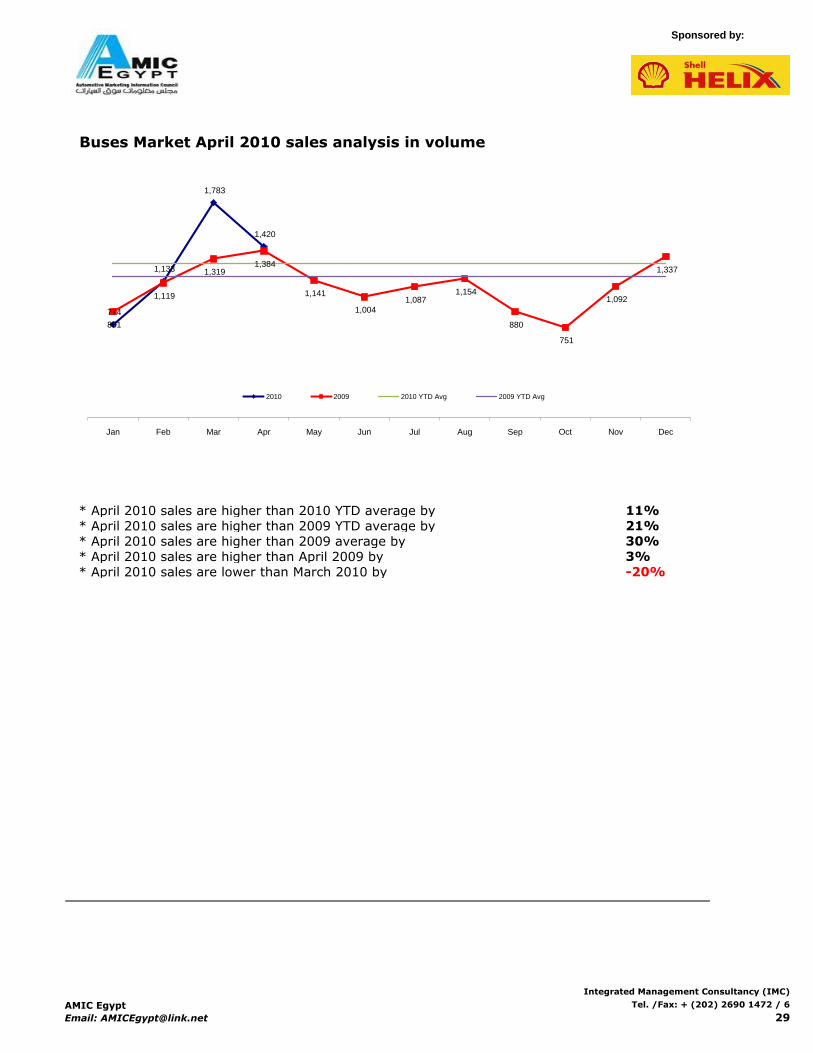

Buses Market April 2010 sales analysis in volume

* April 2010 sales are higher than 2010 YTD average by

* April 2010 sales are higher than 2009 YTD average by

* April 2010 sales are higher than 2009 average by

* April 2010 sales are higher than April 2009 by

* April 2010 sales are lower than March 2010 by

21%

30%

11%

3%

-20%

774

1,133

1,783

1,420

881

1,119

1,319 1,384

1,141

1,004

1,087 1,154

880

751

1,092

1,337

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2009 2010 YTD Avg 2009 YTD Avg

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

29

Sponsored by:

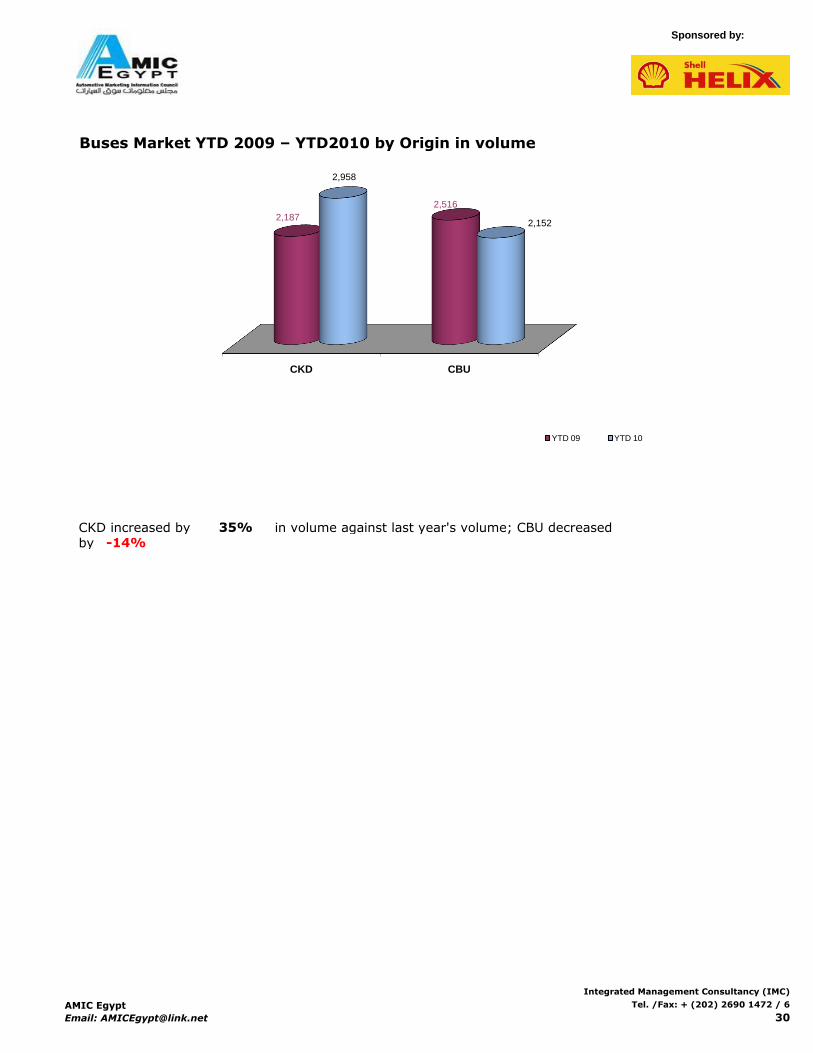

Buses Market YTD 2009 – YTD2010 by Origin in volume

CKD increased by in volume against last year's volume; CBU decreased

by

35%

-14%

CKD CBU

2,187

2,516

2,958

2,152

YTD 09 YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

30

Sponsored by:

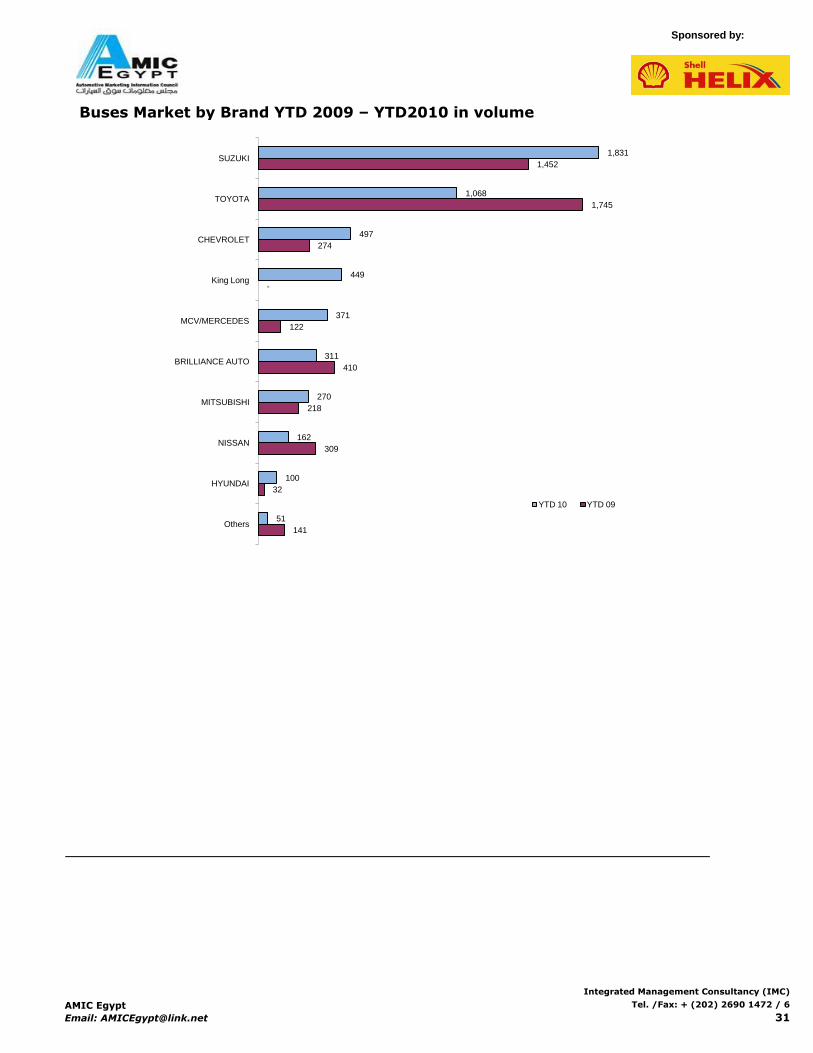

Buses Market by Brand YTD 2009 – YTD2010 in volume

141

32

309

218

410

122

-

274

1,745

1,452

51

100

162

270

311

371

449

497

1,068

1,831

Others

HYUNDAI

NISSAN

MITSUBISHI

BRILLIANCE AUTO

MCV/MERCEDES

King Long

CHEVROLET

TOYOTA

SUZUKI

YTD 10 YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

31

Sponsored by:

Buses Market by Brand YTD 2009 – YTD2010 in Percentage

3%

1%

7%

5%

9%

3%

0%

6%

37%

31%

1.0%

2.0%

3.2%

5.3%

6.1%

7.3%

8.8%

9.7%

20.9%

35.8%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Others

HYUNDAI

NISSAN

MITSUBISHI

BRILLIANCE AUTO

MCV/MERCEDES

King Long

CHEVROLET

TOYOTA

SUZUKI

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

32

Sponsored by:

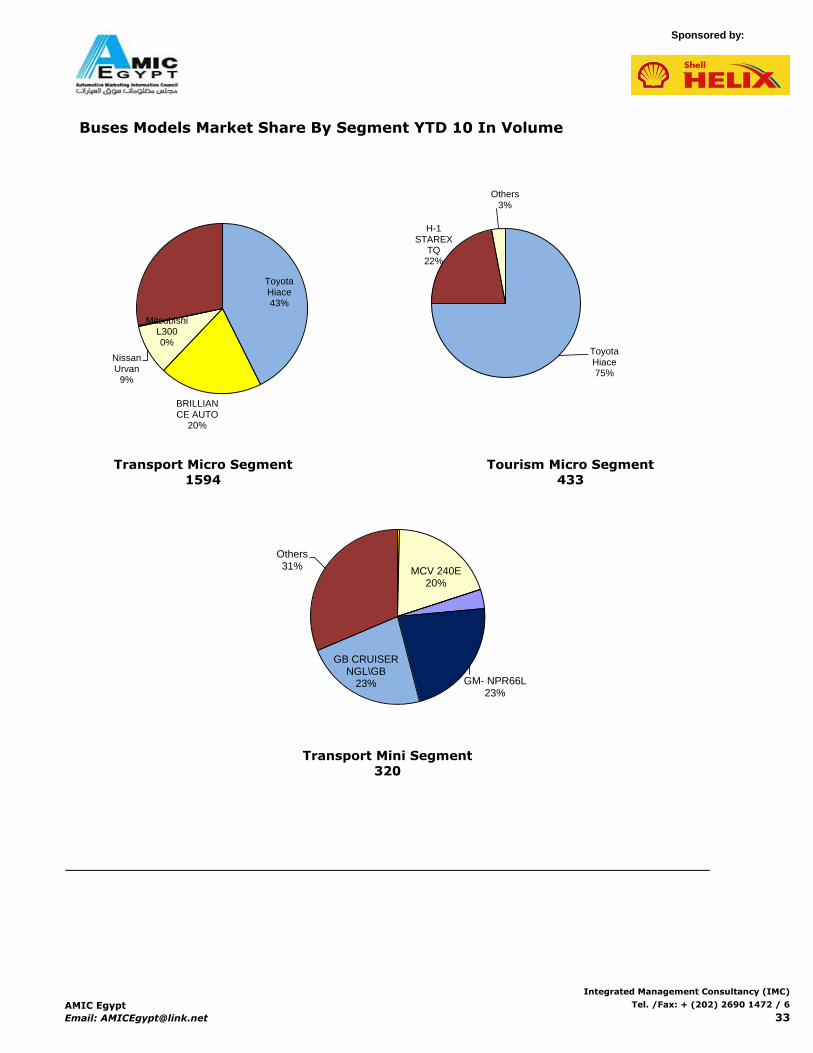

Buses Models Market Share By Segment YTD 10 In Volume

433

Transport Mini Segment

Transport Micro Segment

1594

320

Tourism Micro Segment

Toyota Hiace43%

BRILLIANCE AUTO

20%

Nissan Urvan

9%

Mitsubishi L3000%

Toyota Hiace75%

H-1 STAREX

TQ22%

Others3%

MCV 240E20%

GM- NPR66L23%

GB CRUISER NGL\GB

23%

Others31%

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

33

Sponsored by:

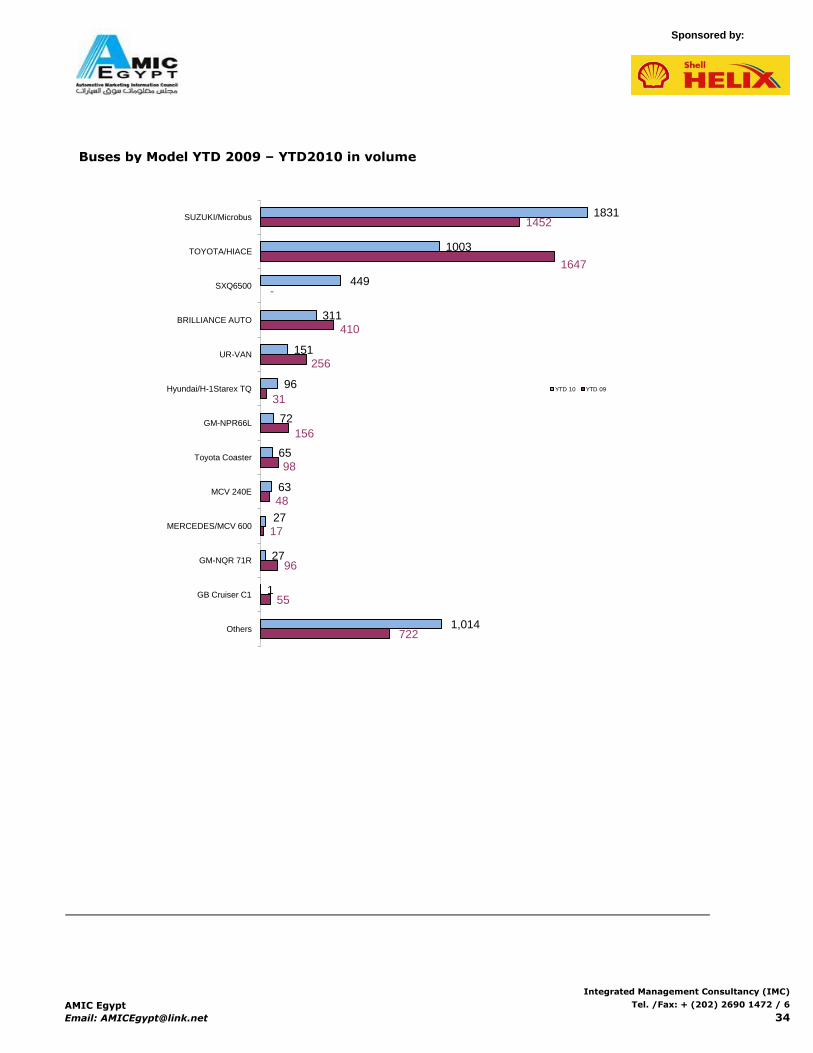

Buses by Model YTD 2009 – YTD2010 in volume

722

55

96

17

48

98

156

31

256

410

-

1647

1452

1,014

1

27

27

63

65

72

96

151

311

449

1003

1831

Others

GB Cruiser C1

GM-NQR 71R

MERCEDES/MCV 600

MCV 240E

Toyota Coaster

GM-NPR66L

Hyundai/H-1Starex TQ

UR-VAN

BRILLIANCE AUTO

SXQ6500

TOYOTA/HIACE

SUZUKI/Microbus

YTD 10 YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

34

Sponsored by:

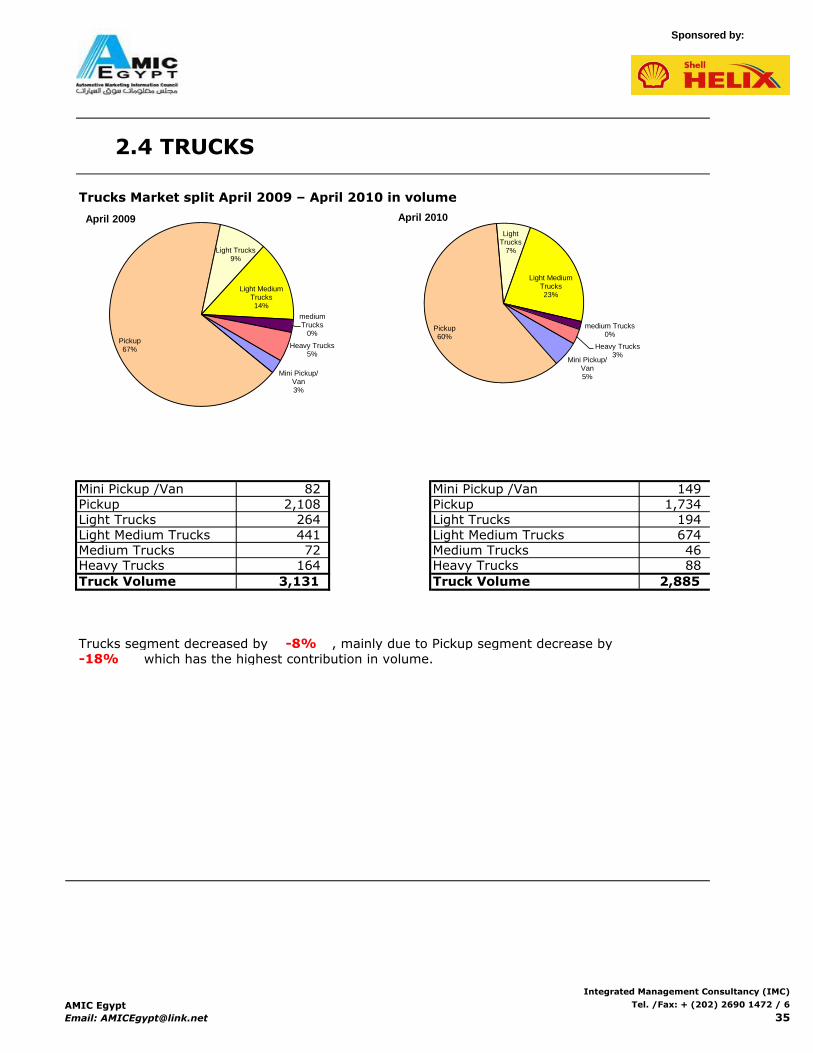

2.4 TRUCKS

Trucks Market split April 2009 – April 2010 in volume

Trucks segment decreased by , mainly due to Pickup segment decrease by

which has the highest contribution in volume.

Light Medium Trucks

Pickup

264

Medium Trucks164

Medium Trucks

Light Trucks 194 Light Trucks

149 Mini Pickup /Van

1,734 2,108

Heavy Trucks

674 441

Pickup

-8%

2,885

Heavy Trucks

Light Medium Trucks

72

Truck Volume Truck Volume

46 88

3,131

-18%

Mini Pickup /Van 82

Mini Pickup/ Van5%

Pickup60%

Light Trucks

7%

Light Medium Trucks23%

medium Trucks0%

Heavy Trucks3%

April 2010

Mini Pickup/ Van3%

Pickup67%

Light Trucks9%

Light Medium Trucks14%

medium Trucks

0%

Heavy Trucks5%

April 2009

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

35

Sponsored by:

Trucks Market split YTD 09 – YTD 10 in volume

Mini Pickup /Van 679

Pickup

Light Trucks

Light Medium Trucks

Medium TrucksHeavy Trucks

Trucks segment grew by , mainly due to Pickup segment growth of by

which has the highest contribution in volume.

324117

712

12.6%

3.6%

11,018

Medium Trucks

Truck Volume 12,403 Truck Volume

Light Medium Trucks

409Heavy Trucks

Mini Pickup /Van

2404

Light Trucks

195

250

690

8111

1700

Pickup 7830

Mini Pickup /Van2%

Pickup71%

Light Trucks

7%

Light Medium Trucks15%

Medium Trucks1%

Heavy Trucks4%

YTD 09

Mini Pickup /Van5%

Pickup65%

Light Trucks6%

Light Medium Trucks19%

Medium Trucks2%

Heavy Trucks3%

YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

36

Sponsored by:

Trucks Market April 2010 sales analysis in volume

* April 2010 sales are Lower than 2010 YTD average by

* April 2010 sales are higher than 2009 YTD average by

* April 2010 sales are higher than 2009 average by

* April 2010 sales are Lower than April 2009 by

* April 2010 sales are lower than March 2010 by -25.0%

-7.0%

4.7%

3.5%

-7.9%

2,826 2,844

3,848

2,885 2,779 2,716

2,392

3,131

2,232

3,130

2,770

2,525 2,424

2,793 2,950

3,604

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2009 2010 YTD Avg 2009 YTD Avg

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

37

Sponsored by:

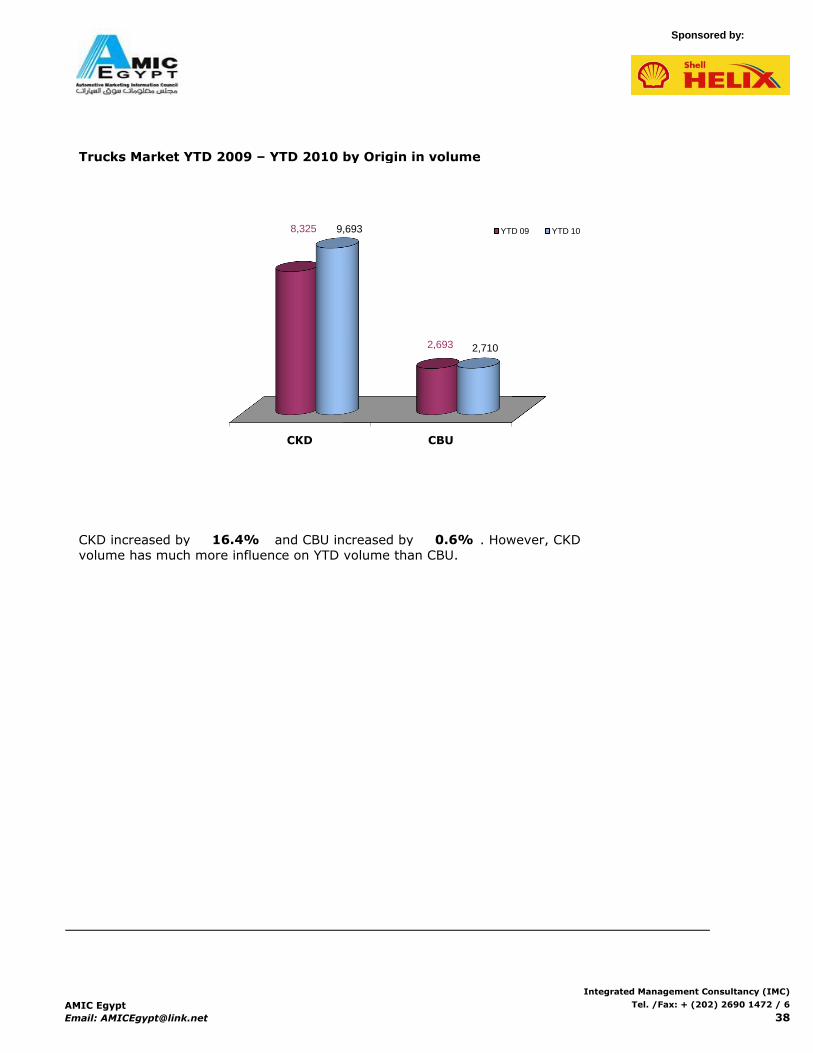

Trucks Market YTD 2009 – YTD 2010 by Origin in volume

CKD increased by and CBU increased by . However, CKD

volume has much more influence on YTD volume than CBU.

16.4% 0.6%

CKD CBU

8,325

2,693

9,693

2,710

YTD 09 YTD 10

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

38

Sponsored by:

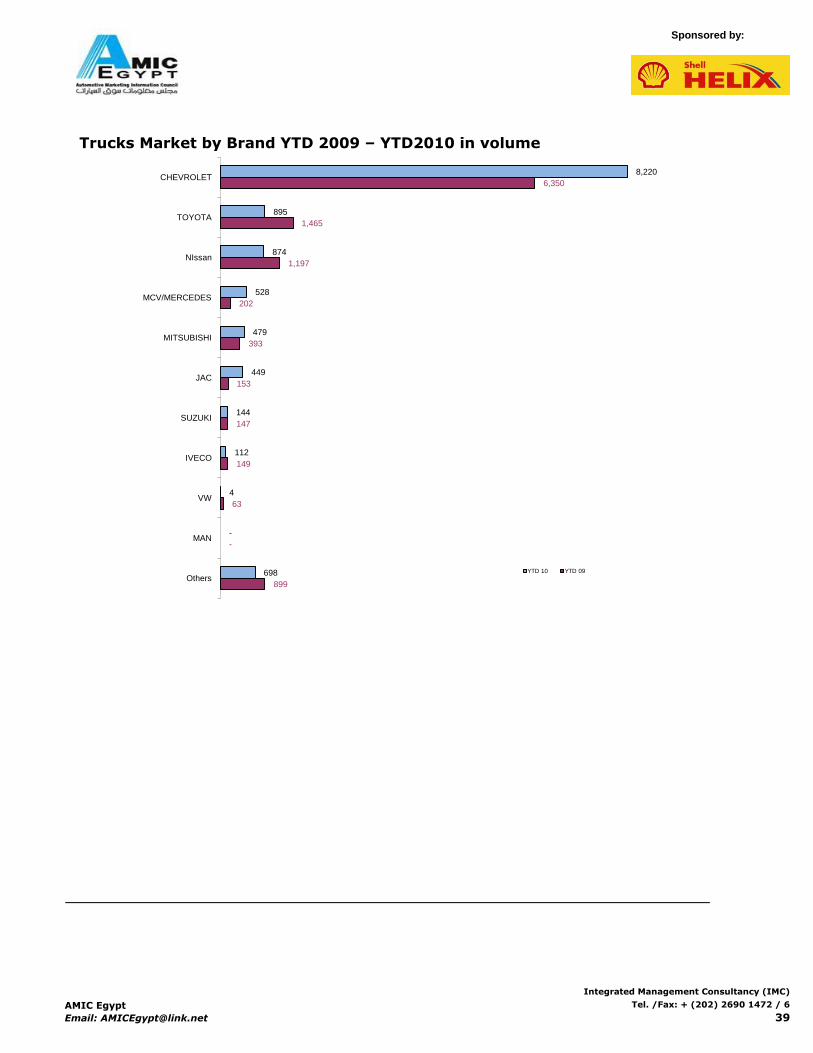

Trucks Market by Brand YTD 2009 – YTD2010 in volume

899

-

63

149

147

153

393

202

1,197

1,465

6,350

698

-

4

112

144

449

479

528

874

895

8,220

Others

MAN

VW

IVECO

SUZUKI

JAC

MITSUBISHI

MCV/MERCEDES

NIssan

TOYOTA

CHEVROLET

YTD 10 YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

39

Sponsored by:

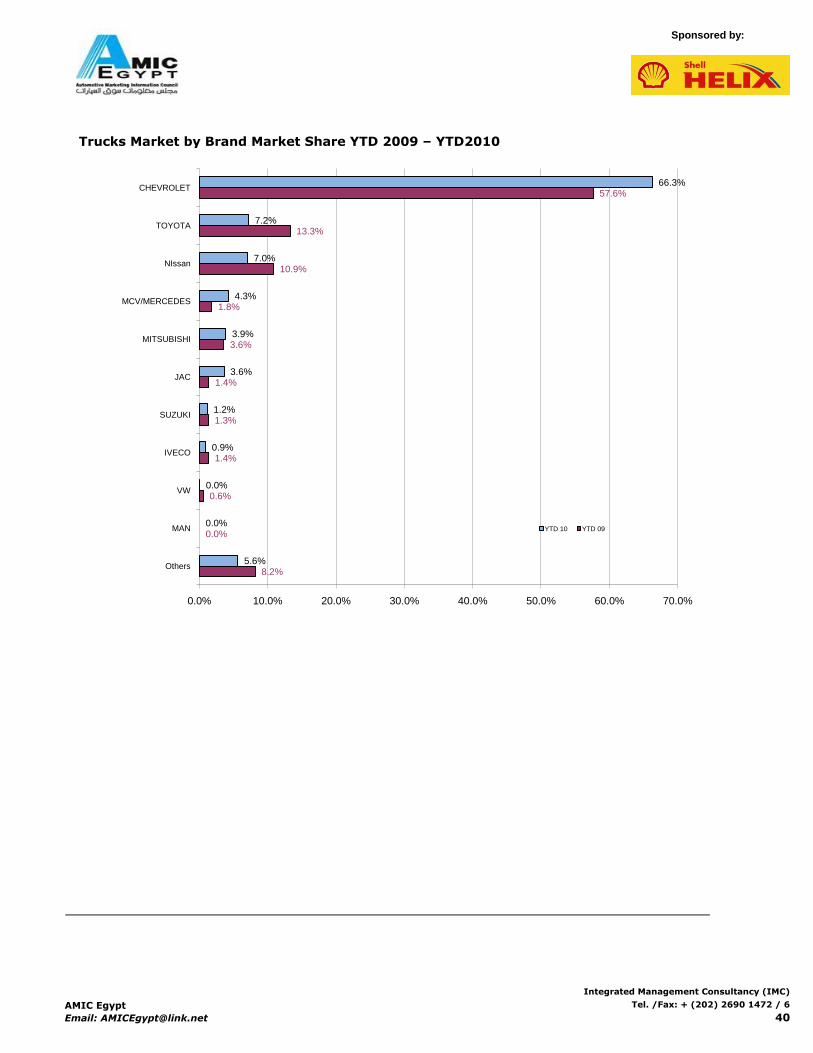

Trucks Market by Brand Market Share YTD 2009 – YTD2010

8.2%

0.0%

0.6%

1.4%

1.3%

1.4%

3.6%

1.8%

10.9%

13.3%

57.6%

5.6%

0.0%

0.0%

0.9%

1.2%

3.6%

3.9%

4.3%

7.0%

7.2%

66.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Others

MAN

VW

IVECO

SUZUKI

JAC

MITSUBISHI

MCV/MERCEDES

NIssan

TOYOTA

CHEVROLET

YTD 10 YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

40

Sponsored by:

Trucks Models Market Share By Segment YTD 10 in Volume

8111

Light Medium Trucks Segment

2404

Pickup Segment

Heavy Trucks Segment

324

TFR SINGLE

CAB74%

HILUX11%

Nissan Pickup S/C

11%

Others4%

NPR 66 TRK62%

NQR 71 TRK12%

CANTER12%

Others14%

IVECO AT720T42TH1%

IVECO AD-N410T42H

14%MERCEDES

ACTROS 20408%

MERCEDES ACTROS 3340

6%

MERCEDES ACTROS 4048 S/L

9%

MERCEDES 4048K-MPII

9%

MITSUBISHI MITSUBISHI

FUSO HL6%

JAC HFCHT2%

MERCEDES 4140B8%

Others37%

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

41

Sponsored by:

Trucks by Model YTD 2009 – YTD2010 in volume

1,305

234

1

4

3

67

144

266

57

248

157

300

916

1,436

1,087

4,793

1,624

-

2

17

46

86

98

151

246

284

287

297

864

873

1,482

6,046

Others

Nissan PickupD/C

VW Crafter

Mitsubishi L200

Suzuki Van

JAC HFCM

Suzuki Pickup

Daihatsu V 118

JAC HFCL

Chevrolet NKR55

Chevrolet/NQR 71

Mitsubishi CANTER

Nissan Pickup S/C

Toyota/Hilux

Chevrolet NPR 66

Chevrolet TFR

YTD 10

YTD 09

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

42

Sponsored by:

------------------------------------------------3. MONTHLY NEWS FLASH 15TH TO 15TH

------------------------------------------------

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

43

Sponsored by:

PETROLEUM MINISTER TO REVISE ENERGY SUBSIDIES

Source: Zawya, April 19, 2010

A senior government official indicated that the Prime Minister has asked the Minister of Petroleum to

present several scenarios involving a reduction in subsidies on energy products within one month for

review by the Cabinet, reported Al-Masry Al-Youm.

The objective of the request is to reduce the size of energy subsidies, which are expected to reach LE

62 billion in the fiscal year, around 80 percent of total subsides in the budget.

Diesel is currently subsidized by LE17.5 billion, or 52 percent of energy subsidies, butane gas by LE 7.7

billion or 23 percent of energy subsidies, gasoline by LE5.7 billion or 17 percent of energy subsidies and

natural gas by LE1.6 billion or 4.6 percent of total energy subsidies, according to the newspaper as

cited by Beltone Financials daily market report.

The government is already planning to raise the prices of natural gas and electricity for non-energy

intensive industries in July 2010. The move is not expected to have a significant impact on companies

in these industries, but could raise average annual headline inflation from 11 percent to 13 percent.

MINISTRY OF TRADE CHANGES EXPORT REBATE SYSTEM

Source: Daily News, April 26, 2010

The Ministry of Trade and Industry has decided to start in July 2010 applying the new methodology for

granting export rebates (also considered a form of subsidy) using a value-added-based system,

reported local newspapers.

The current system grants exports a percentage of their value in rebates, according to Beltone

Financial’s daily market report.

Different industries benefit from the export rebate system, including textiles and some manufacturing

industries. The change in methodology aims to encourage the use of local components in production.

The Export Development Fund, disbursing the subsidy, has a budget of LE4 billion.

SUDAN CUTS TARIFFS BY 80% ON EGYPTIAN GOODS

Source: Beltone, April 27, 2010

The Sudanese government agreed to implement the Arab Free Trade and COMESA free trade

agreements on Egyptian products exported to Sudan, cutting customs rates on 53 Egyptian products by

80%, following three months of negotiations, reported Al Ahram newspaper. The products subject to

the lower tariffs include vehicles, furniture, appliances, food products, textiles and apparel. The

Sudanese government had previously exempted five products from customs duties in 2004, out of the

58 Egyptian products which it taxes.

CHINA CURBS COMMODITY EXPORTS TO EGYPT

Source: Arab Finance, April 27, 2010

China is taking steps to curb the shipment of goods to Egypt, according to the state-run General

Organization for Export and Import Control (GOEIC) (link here).

The move comes as part of a deal between Egypt and China aimed at imposing tighter control measures

on the bilateral commodity trade, reported Al-Masry Al-Youm.

GOEIC chief Mohamed Shafiq told the newspaper that China had halted the shipment of Egypt-bound

cargos from July to December of last year. He went on to say that both sides had agreed that the

GOEIC would be notified every six months about blocked shipments.

Shafiq explained that, according to the terms of the agreement, goods exported to Egypt would be

monitored by the Chinese government so that the latter could verify that all goods listed on shipping

lists and those prepped for export were the same. This, he said, was in order to combat smuggling.

_____________________________________3.1 EGYPT MACRO FLASH

_____________________________________

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

44

Sponsored by:

______________________________________3.2. AUTOMOTIVE INDUSTRY LOCAL NEWS CLIPS

________________________________________

New Buses save 250 Million EGP

Al Sayarat -Al Ahram – 7th of May 2010

Mr. Salah Farag, CEO of the public transportation body, have declared that the new buses which are operating

in Cairo area will be saving 250 Million EGP over the coming 3 years which is representing 30% of the subsidy

given to the transportation body which adding to a yearly amount of 690 Million EGP this year.

He also added that due to the bad traffic situation in Cairo, the buses are only doing 6 rounds instead of 10 daily

and transport around 3.2 Million passenger daily.

He also added that the new buses, which are running, now are 200 units and another 300 units will be added in

next October.

Nissan Egypt celebrates 5 years in Egypt

Al Sayarat -Al Ahram – 7th of May 2010

Nissan Egypt is celebrating five years in Egypt by launching a large maintenance campaign from Saturday the

8th of May till Tuesday the 8th of June 2010.

Knowing that Nissan Egypt is owning the only Nissan training center in North Africa.

El Rawas and Mitsubishi

Al Sayarat -Al Ahram – 7th of May 2010

New negotiations round will be held between El Rawas and Mitsubishi Dubai, to re-discuss the possibility of

renewing the agency contract after responding to the main request of Mitsubishi which is mainly renovating and

maintenance centers.

Mazda is back to the Egyptian market with GB Auto

El Sayarat -Akhbar El Youm– 8th of May 2010

GB auto is considered the exclusive agent of Mazda in Africa and the middle east.

Mazda will witness a new era in the Egyptian market after signing the exclusive agreement with GB auto, which

will assure after sales services through a new service center in “Abu Rawash”, few KM away from Hyundai after

sales service center. In addition a hotline 16670 will be available to answer all client requests and questions 24

hours 7 days a week.

A test Drive for Wrangler Unlimited 2010

El Sayarat -Akhbar El Youm– 15th of May 2010

A test drive for Wrangler Unlimited 2010 in Sinai mountains area “Wadi bawbaw” which is blocked by rocks.

For 6 hours over a distance of 10 KM covered with rough rocks and very difficult track the Wrangler Unlimited

proved to be more than adequate for such very difficult tracks.

AMIC Egypt

Email: [email protected]

Integrated Management Consultancy (IMC)

Tel. /Fax: + (202) 2690 1472 / 6

45