EEC SlideDeck 02072013 Public v3 - Hart...

34

Sponsored by: Global Refining: Fueling Profitability in the Turbulent Times Ahead

Transcript of EEC SlideDeck 02072013 Public v3 - Hart...

Sponsored by:

Global Refining: Fueling Profitability in the Turbulent Times Ahead

The Outlook for Energy:A View to 2040

Roland L. MoreauExxonMobil Upstream Research CompanyHart Energy Breakfast ClubFebruary 7, 2013

This presentation includes forward-looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply) could differ materially due to changes in technology, the development of new supply sources, political events, demographic changes, and other factors discussed herein and under the heading "Factors Affecting Future Results" in the Investors section of our website at: www.exxonmobil.com. The information provided includes ExxonMobil's internal estimates and forecasts based upon internal data and analyses as well as publically-available information from external sources including the International Energy Agency. This material is not to be used or reproduced without the permission of Exxon Mobil Corporation. All rights reserved.

0

3

6

9

2010 2020 2030 2040

PopulationBillion

Population Trends Impacts Energy Use

0

1

2

3

4

5

6

7

8

1960 1980 2000 2020 2040

OECDAfricaChinaIndiaSoutheast AsiaLatin America

Fertility Rate*Children per Woman

* Source: World Bank & United Nations

OECD

Other Non OECD

China

India

Africa

0

3

6

9

2010 2020 2030 2040

Global Demographics*Billion

Age 0-14

Age 65+

Age 15-64

ExxonMobil 2013 Outlook for Energy

0

25

50

75

100

125

2000 2020 2040

Energy Demand

Economic Growth Drives Energy DemandGDPTrillion 2005$

China

United States

2010-2040 AAGR %

5.6%

2.3%

1.8%Other OECD

Other Non

OECD

3.9%World2.8%

ExxonMobil 2013 Outlook for Energy

0

250

500

750

1000

1250

2000 2020 2040

Quadrillion BTUs

2010-2040 AAGR %World1.0%

0

250

500

750

1000

1250

2000 2020 2040

Energy DemandQuadrillion BTUs

Energy Saved ~500

2010-2040 AAGR %World1.0%

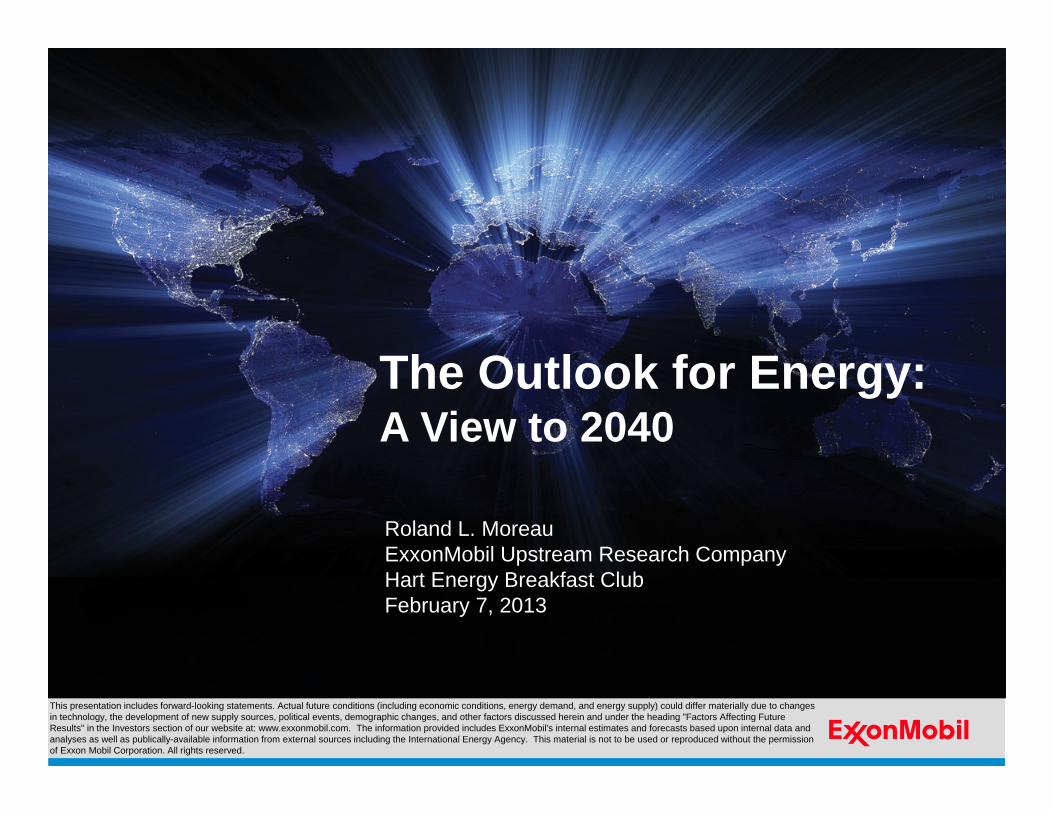

0

50

100

150

200

250

300

ElectricityGeneration

Industrial Transportation Res/Comm

Energy Demand by SectorQuadrillion BTUs

2010

2025

2040

Electricity Generation Leads Growth

ExxonMobil 2013 Outlook for Energy

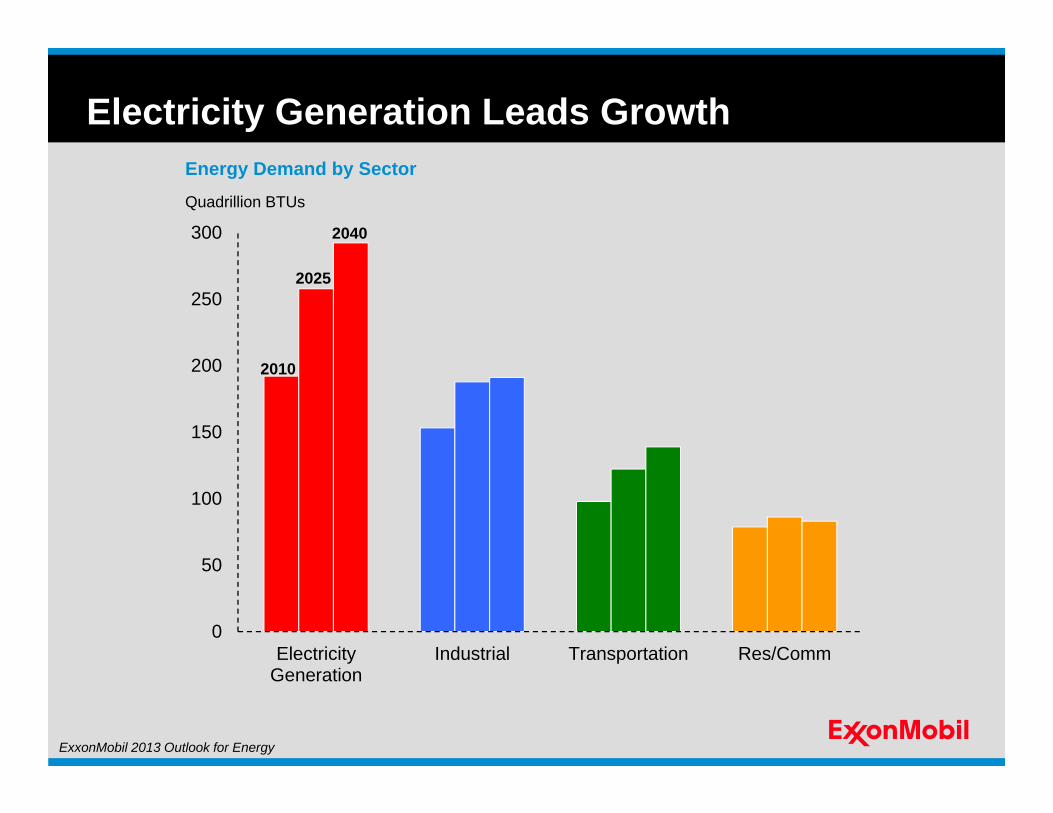

0

25

50

75

100

125

150

2000 2020 2040

Residential/Commercial Outlook

0

5

10

15

20

25

30

35

2000 2020 2040

Residential Energy IntensityMillion BTUs per Person

Japan

North America

Europe OECD

China

India

By SectorQuadrillion BTUs

Commercial

Residential

0

25

50

75

100

125

150

2000 2020 2040

Fuel DemandQuadrillion BTUs

Electricity

Coal

Oil

Gas

Biomass

Other

ExxonMobil 2013 Outlook for Energy

0

50

100

150

200

250

1990 2015 2040

Industry Energy Demand Increases

Chemicals

Manufacturing & Industry

Energy Industry

Other

PlasticsPlasticsFertilizerFertilizer

PaintPaint

SteelSteel

AutomobilesAutomobiles TextilesTextiles

Liquid FuelsLiquid Fuels

CoalCoalNatural GasNatural Gas

AgricultureAgriculture

LubricantsLubricants AsphaltAsphalt

Quadrillion BTUs

ExxonMobil 2013 Outlook for Energy

Transportation Sectors

Light Duty Vehicles

CarsCars

SUVsSUVs

Pickup TrucksPickup Trucks

Heavy Duty Vehicles

18-wheelers18-wheelers

BusesBuses

Delivery TrucksDelivery Trucks

ExxonMobil 2013 Outlook for Energy

0

15

30

45

60

75

2000 2020 2040

Sector DemandMBDOE

Light Duty

Marine

Rail

Heavy Duty

Aviation

Transportation Demand

ExxonMobil 2013 Outlook for Energy

0

5

10

15

20

25

30

AP NA Europe LA ME ROW

Demand by RegionMBDOE

‘40

‘25

‘10

0

25

50

75

100

125

150

2010 2015 2020 2025 2030 2040

Elec/PHV

Full Hybrid

Natural Gas

Conv. Diesel

Conv. Gasoline

Light Duty Vehicle Sales & Efficiency

0

5

10

15

20

2010 2020 2030 2040

Incremental Vehicle Efficiency GainsMiles per Gallon

Powertrain

Body & Accessories

Vehicle Size

Hybrid

Average27 MPG

47 MPG

Annual New Car Sales by TypeMillion Cars

ExxonMobil 2013 Outlook for Energy

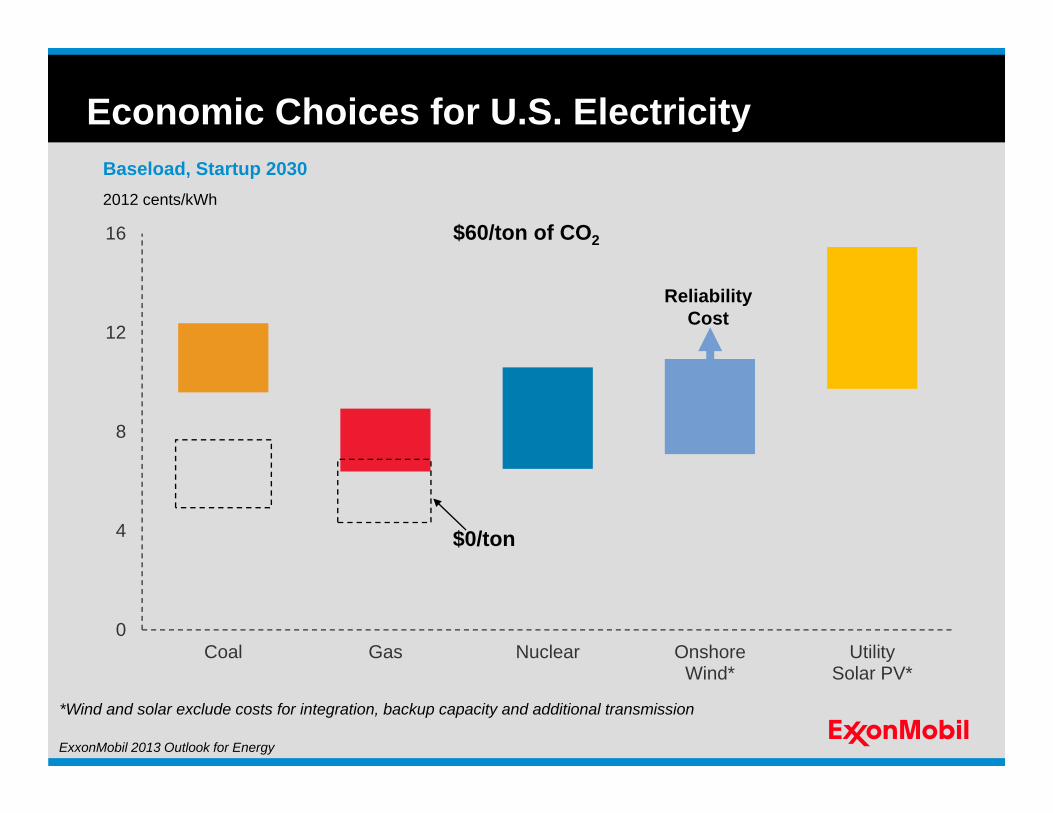

0

4

8

12

16

Coal Gas Nuclear OnshoreWind*

UtilitySolar PV*

Baseload, Startup 20302012 cents/kWh

*Wind and solar exclude costs for integration, backup capacity and additional transmission

$60/ton of CO2

$0/ton

Economic Choices for U.S. Electricity

Reliability Cost

ExxonMobil 2013 Outlook for Energy

0

25

50

75

100

125

150

175

200

225

Oil Gas Coal Nuclear Biomass Solar / Wind /Biofuels

Hydro / Geo

Energy Mix Continues to EvolveQuadrillion BTUs

Average Growth / Yr. 2010 - 2040

1.0%

2040

2010

0.8%

1.7%

-0.1%

2.4% 0.4%

5.8% 1.8%

ExxonMobil 2013 Outlook for Energy

0

20

40

60

80

100

120

2000 2010 2020 2030 2040

Liquids Supply

MBDOE

Supply by Type

Other LiquidsBiofuels

Conventional Crude & Condensate

Tight OilOil Sands

NGLs

Deepwater

0

1

2

3

4

5

6

2040

Resource*TBO

Remaining Resource

Cumulative Production

* Source: IEAExxonMobil 2013 Outlook for Energy

0

10

20

30

40

50

2010 2025 2040

0

10

20

30

40

50

2010 2025 2040

North America Energy Balance

Oil

Regional Supply

Gas

Quadrillion BTUs

Net ImportsNet Imports

Net Exports

Regional Supply

Net Exports

ExxonMobil 2013 Outlook for Energy

0

25

50

75

100

125

2010 2025 2040

Regional Supply

Total Energy BalanceNet Exports

Net ImportsNet Imports

Conclusions

ExxonMobil 2013 Outlook for Energy

Global Crude, Refining and Clean Fuels Outlook to 2035

Executive Energy Club

Rodrigo FavelaExecutive Director

Refining, Planning and EvaluationHart Energy

February 7, 2013

All rights reserved © 2013

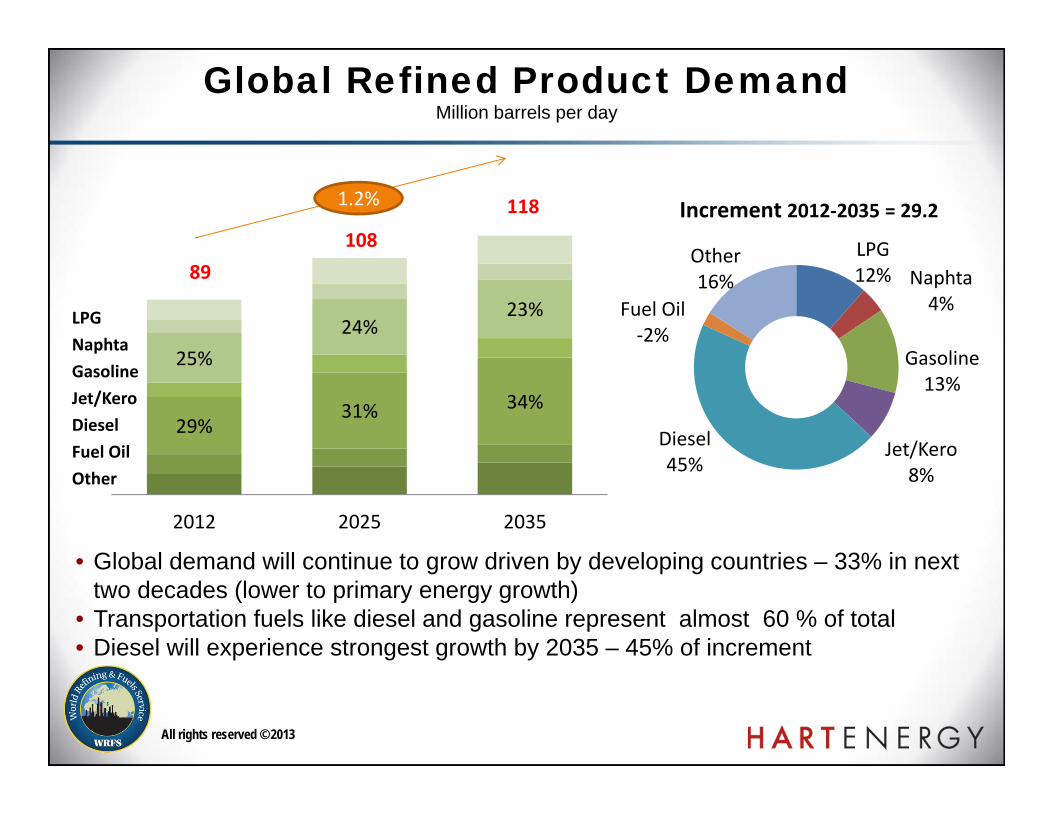

Global Refined Product DemandMillion barrels per day

• Global demand will continue to grow driven by developing countries – 33% in next two decades (lower to primary energy growth)

• Transportation fuels like diesel and gasoline represent almost 60 % of total• Diesel will experience strongest growth by 2035 – 45% of increment

LPGNaphtaGasolineJet/KeroDieselFuel OilOther

Increment 2012‐2035 = 29.2

29%31% 34%

25%24%

23%

2012 2025 2035

LPG12% Naphta

4%

Gasoline13%

Jet/Kero8%

Diesel45%

Fuel Oil‐2%

Other16%89

108

1181.2%

All rights reserved © 2013

Regional Petroleum Product Demand Growth 2012-2035

Source: Hart Energy analysis and forecast (2013)

Asia-Pacific highest volume Middle East highest growth North America will decrease by 0.2%

‐2 0 2 4 6 8 10 12 14 16

North America

Europe

Africa

CIS

Latin America

Middle East

Asia‐Pacific

‐0.2%0.2%

2.0%

1.9%

1.8%

2.6%

1.8%

Million barrels per day

All rights reserved © 2013

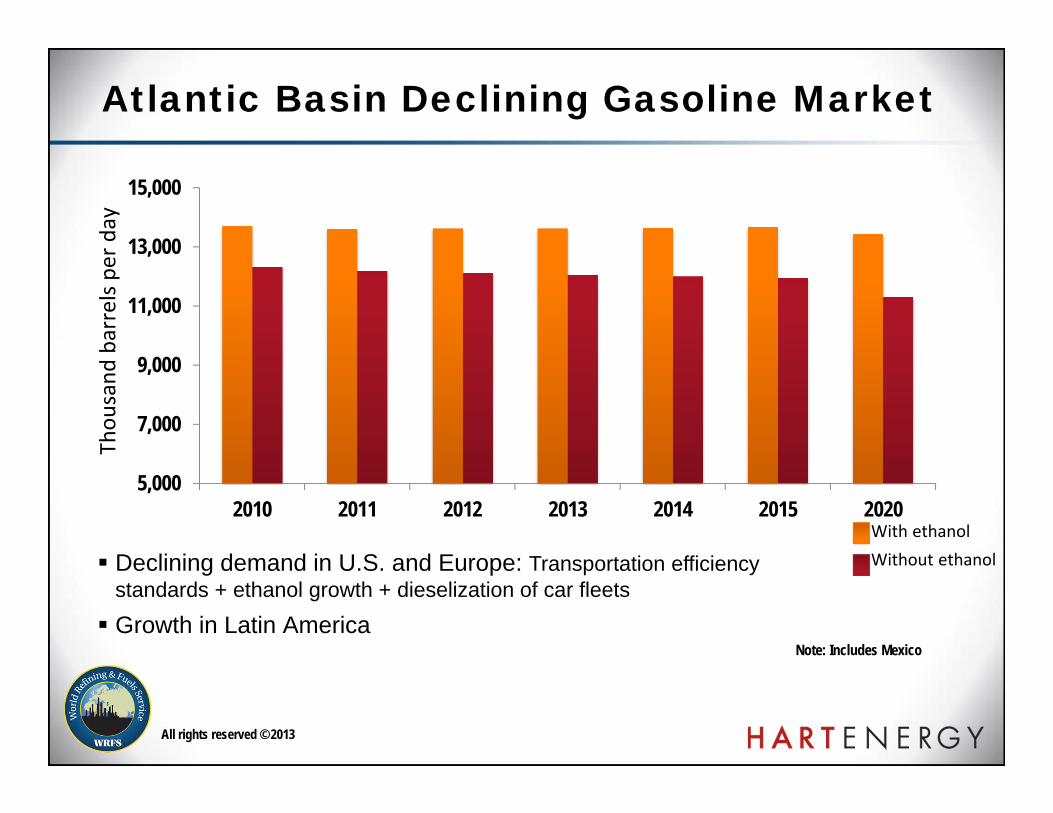

Atlantic Basin Declining Gasoline Market

5,000

7,000

9,000

11,000

13,000

15,000

2010 2011 2012 2013 2014 2015 2020

Note: Includes Mexico

Declining demand in U.S. and Europe: Transportation efficiency standards + ethanol growth + dieselization of car fleets

Growth in Latin America

Thou

sand

barrelsp

er day

With ethanolWithout ethanol

All rights reserved © 2013

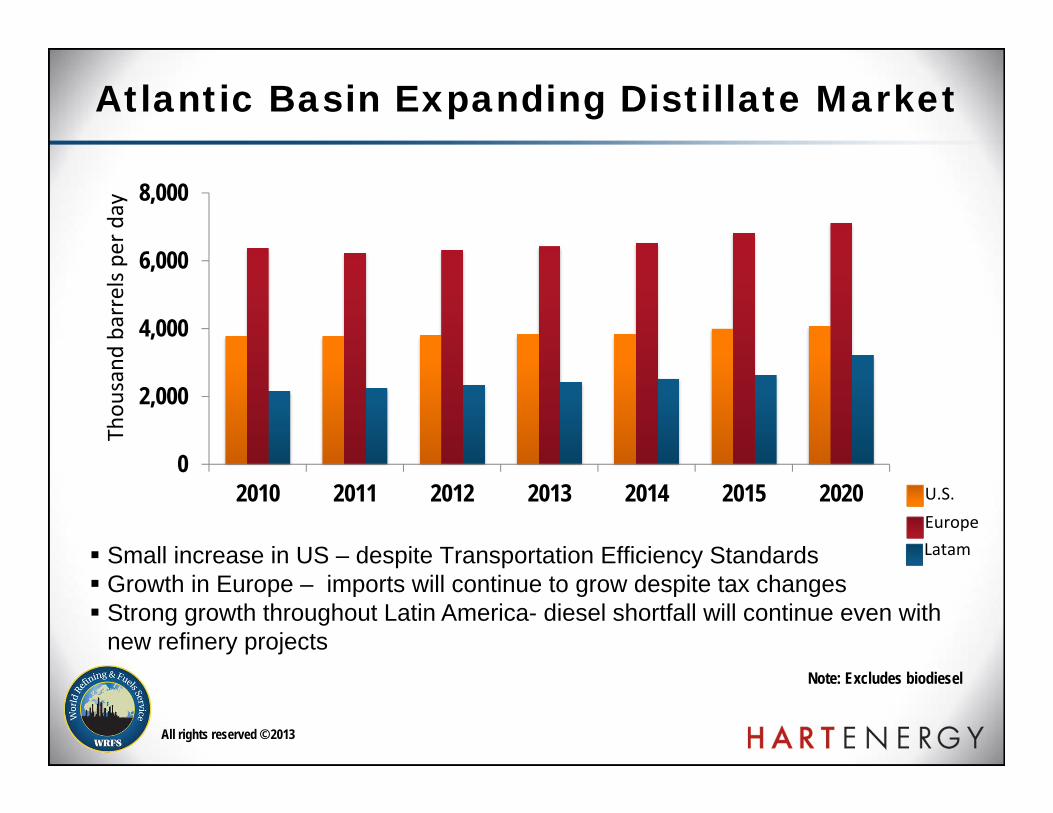

Atlantic Basin Expanding Distillate Market

Note: Excludes biodiesel

0

2,000

4,000

6,000

8,000

2010 2011 2012 2013 2014 2015 2020

Small increase in US – despite Transportation Efficiency Standards Growth in Europe – imports will continue to grow despite tax changes Strong growth throughout Latin America- diesel shortfall will continue even with

new refinery projects

Thou

sand

barrelsp

er day

U.S.EuropeLatam

All rights reserved © 2013

Transportation Fuel Quality

0

5

10

15

20

25

30

2011 2015 2020 2025 2030

<10 ppm 10-50 ppm 51-500 ppm >500 ppm

05

1015202530354045

2011 2015 2020 2025 2030<10 ppm 11-50 ppm 51-500 ppm501-2000 ppm >2000 ppm

Gasoline and on-road diesel markets to less than 10 ppm ULS fuels Lower sulfur in off-road diesel and marine fuels:

500 ppm for on-road diesel by 2015 & below 100 ppm by 2025 500 ppm for marine fuels before middle next decade.

Source: Hart Energy analysis and forecast (2013)

Million barrels per day

Gasoline Diesel

All rights reserved © 2013

0 20 40 60 80 100 120 140

Crude Distillation

Coking

Catalytic Cracking

Hydrocracking +74%

+19%

+66%

+28%

Capacity Expansion, 2012-2035

Million barrels per day

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

Changes in Product Trade Patterns

Escalating gasoline and distillate imbalance in Europe and North America

European gasoline exports to North America will decline by 50%

The distillate shortfall in Europe:

CIS less volume

Middle East and other regions incremental supply

Asia-Pacific will increase gasoline and distillate exports but will fall short in long term due to increased internal demand

Middle East is projected to become the world marginal refined product supply center.

All rights reserved © 2013

Increased Crude/LiquidsGlobal Crude Oil Quality TrendsAPI°, %Sulfur

Global Crude Oil Outlook

Crude quality will remain similar in average …but Heavy crude oil, condensate/NGL, Light/Medium and Unconventional

Oil will have the largest contribution to liquid supply – Impact on dieselyield

1.00

1.10

1.20

1.30

1.40

31.532.032.533.033.534.034.535.0

2011 2015 2025 2035

API

Sulfur

Light/Medium23%

Unconventional15%

SCO6%

Heavy Oil28%

NGL15%

Biofuels8%

GTL/CTL5%

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

North America: Supply Landscape

Unconventional Tight Oil (Shale) will add 4 million b/d. (Sweet light) Logistic constraints – emerging crude-by-rail infrastructure Canadian oil sand

Turn up in production – 2+ million b/d increase 2012 to 2020 Additional 0.8 million b/d 2021- 2025

Increasing supply of condensate and NGL

0%10%20%30%40%50%60%70%

0.01.02.03.04.05.06.07.08.09.0

10.0

2011 2012 2015 2020 2025 2030 2035Tight Oil Oil Sands % of Total

Million barrels per day

All rights reserved © 2013

USGC Natural Gas Prices and Refining Differentials

Source: Hart Energy analysis and forecast (2013)

Light – Heavy Differential (USD/Bbl) Natural gas prices ($/Mcf)

0.0

2.0

4.0

6.0

8.0

10.0

Jul‐0

8De

c‐09

Apr‐11

Sep‐12

Jan‐14

Jun‐15

Oct‐16

Mar‐18

Jul‐1

9

Discounts will depend if USGC exports allowed: ($7‐$8/barrel vs $2‐$3)

Natural gas prices sustained at $4‐$5/Mcf

‐20.0

0.0

20.0

40.0

60.0

80.0

Jun‐08

Jun‐09

Jun‐10

Jun‐11

Jun‐12

Jun‐13

Jun‐14

Jun‐15

Jun‐16

Jun‐17

Jun‐18

Jun‐19

Product – (ULR+DSL)/2‐HSF

LLS – MAY

WTI – MAY

All rights reserved © 2013

U.S.: Favorable Refining Position

US refining with $2‐3 US/bbl advantage over other regions. US Midcontinent / USGC Capacity Additions ‐ surplus capacity with minimal rationalization. Exports to Latin‐American have helped to maintain process Capacity rationalization focused on Europe and to a lesser extent in US East Coast

70

75

80

85

90

95

100Refinery Utilization (%)

0100200300400500600

2008 2009 2010 2011 2012

Gasoline Distillate

US Exports to Latin America(thousand barrels per day)

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

Diesel – Gasoline Differential Outlook

Diesel ‐ Gasoline Differential (USD/bbl)

0

2

4

6

8

10

12

14

16

18

20

2006 2007 2008 2009 2010 2011 2012 2014 2016 2018 2020 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Condensate NGL

2,500

1,500

Growth in condensate will depress light naphtha and eventually gasoline market Naphtha/Gasoline market vulnerable to ethanol requirements volatility initiatives. Gasoline prices will decline relative to crude and diesel.

Condensate & NGL (1000 b/d)

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

Latin America: Refined Product Demand

Demand will grow by 52% Diesel and gasoline represent 60% of total demand and contribute 80% of increment LPG and fuel oil participation higher than other regions Brazil and Mexico represent 60% of total demand Major countries will reach less than 30 ppm fuel specs before 2016

LPGNaphthaGasolineJet/KeroDieselFuel OilOther

1.8%MILLION b/d Increment 2012‐2035

02468101214

2012 2025 2035

LPG, 7%Naphta, 2%

Gasoline, 37%

Jet/Kero, 5%

Diesel, 41%

Fuel Oil, 0%

Other, 9%

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

Crude Quality – heavier and sourer than other regions Capacity will increase 42% increment (Brazil, Mexico, Cuba, Argentina and Colombia) Investment in conversion, hydrocracking, and hydroprocessing will increase above

50% (70%,103%,91%)

Latin America: Refining Capacity Expansion

(million barrels per day)

2.53.4

4.23.0

5.26.1

0.8 1.2 1.6

7.79.4

10.9

2012 2020 2030

Conversion Hydroprocessing Light Oil Processing Crude Distillation

Source: Hart Energy analysis and forecast (2013)

All rights reserved © 2013

•Global refining markets have become more volatile, diesel will be the fuel with the strongest growth in all regions

•Gasoline will continue to grow in developing countries but will experience a decline in the US and Europe

•Strong growth in Latin America/Middle East/Asia Pacific. Larger countries will achieve nationwide ultra‐low sulfur fuels quality by 2016.

•Aggressive capacity expansion will be required to keep pace with demand and lower quality indigenous crude.

•Middle East emerging as the marginal producer of diesel. •Unconventional gas and crude will foster US refineries competitiveness in the Atlantic Basin – affecting European refining industry and possibly some Latin American refining projects – new opportunities will arise for petrochemicals based on condensates for the region

Final Remarks

All rights reserved © 2013

Rodrigo FavelaExecutive Director

Refining, Planning and EvaluationHart Energy

Global Crude, Refining and Clean Fuels Outlook to 2035

All rights reserved © 2013