Implementation Guidance on MSRB Rule G-18, on Best Execution

Education and Outreach Seminar

July 29, 2014 | Chicago, IL

2 Municipal Securities Rulemaking Board 2

About the MSRB

• A self-regulatory organization created by Congress in 1975

• Protects investors, municipal entities including issuers of

municipal securities, obligated persons and the public

interest

• Promotes a fair and efficient municipal market

3 Municipal Securities Rulemaking Board 3

• Regulates municipal securities dealers and

municipal advisors

• Operates market transparency systems including

the EMMA® website

• Conducts education, outreach and market

leadership

How the MSRB Fulfills its Mission

4 Municipal Securities Rulemaking Board 4

Today’s Agenda

• Municipal Advisor Regulation Post July 1, 2014

• Update on Market Structure Improvements and

Enhancing Transparency

• New Tools on EMMA: Price Discovery and Trade

Price Enhancements

5 Municipal Securities Rulemaking Board 5

Presenters

• Dan Heimowitz, MSRB Board Chair

• Lynnette Kelly, Executive Director

• Ritta McLaughlin, Chief Education Officer

• Michael L. Post, Deputy General Counsel

• Justin Pica, Director of Product Management –

Market Transparency

Guest Panelists

• Ben Watkins, Government Finance Officers Association

• Steve Apfelbacher, National Association of Independent

Public Finance Advisors

–

Opening Remarks

Dan Heimowitz

Chair, Municipal Securities Rulemaking Board

Municipal Advisor Regulation, Post July 1

Lynnette Kelly, MSRB Executive Director

Ben Watkins, GFOA

Steve Apfelbacher, NAIPFA

8 Municipal Securities Rulemaking Board 8

3 “Rs” of Municipal Advisor Regulation

• What is the role of a municipal advisor?

• What are the responsibilities of a municipal advisor?

• What relationships does a municipal advisor have

that could affect provision of their services?

9 Municipal Securities Rulemaking Board 9

Origins of Municipal Advisor Regulation

• Dodd-Frank Wall Street Reform and Consumer

Protection Act of 2010 charged MSRB with

developing regulatory framework for municipal

advisors to:

– Protect state and local governments and other municipal

entities that engage the services of a municipal advisor

– Promote a fair and efficient market

– Preserve municipal market integrity

10 Municipal Securities Rulemaking Board 10

Key Obligations of Municipal Advisors

• Federal fiduciary duty to state and local government

clients

• Fair dealing with all persons

• Registration with SEC and MSRB

11 Municipal Securities Rulemaking Board 11

Regulatory Framework

• MSRB is developing a comprehensive regulatory

framework that includes:

– Development of rules governing the professional conduct of

municipal advisors

– Establishment of a professional qualifications program that

ensures municipal advisors are qualified in their duties

– Extensive education and outreach to municipal advisors on duties

and obligations

12 Municipal Securities Rulemaking Board 12

MSRB Draft Rules for Municipal Advisors

• Core standards of conduct rule (MSRB Rule G-42)

• Supervision and compliance obligations (MSRB Rule G-44)

• Professional qualifications for municipal advisors (MSRB Rule G-3)

• Pay-to-play rule (forthcoming draft amended MSRB Rule G-37)

• Gifts and gratuities (forthcoming draft amended MSRB Rule G-20)

MSRB Education and Outreach Seminar

Chicago

July 29, 2014

“The Securities and Exchange Commission’s

New Municipal Advisor (MA) Rule”

Ben Watkins, Director

Florida Division of Bond Finance

Chair, GFOA Debt Committee

13

MA Rule – Critique

• Regulatory Quagmire

• No Bright Lines

• Far Too Complicated / Cumbersome

• Thank Goodness for FAQs

14

MA Rule – GFOA Alert

• Educates Issuers With Overview of Rule

• Highlights Key Points

• Focus on Mitigating Adverse Impact of MA Rule on Communication / Interaction with Dealers

• Major Emphasis on Implementing Exemptions

15

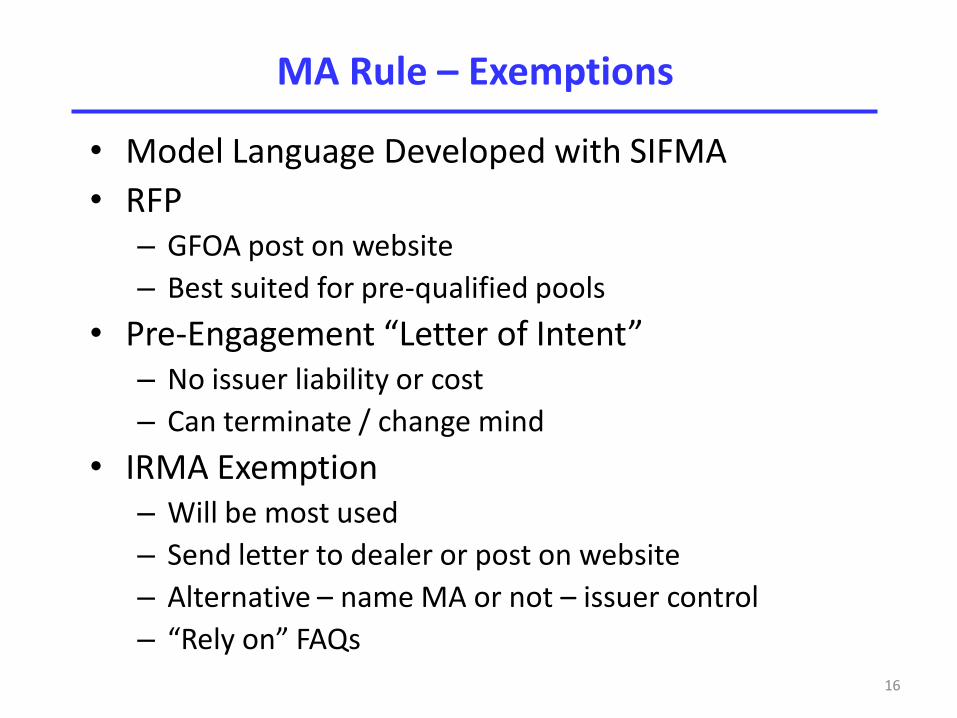

MA Rule – Exemptions

• Model Language Developed with SIFMA

• RFP – GFOA post on website

– Best suited for pre-qualified pools

• Pre-Engagement “Letter of Intent” – No issuer liability or cost

– Can terminate / change mind

• IRMA Exemption – Will be most used

– Send letter to dealer or post on website

– Alternative – name MA or not – issuer control

– “Rely on” FAQs

16

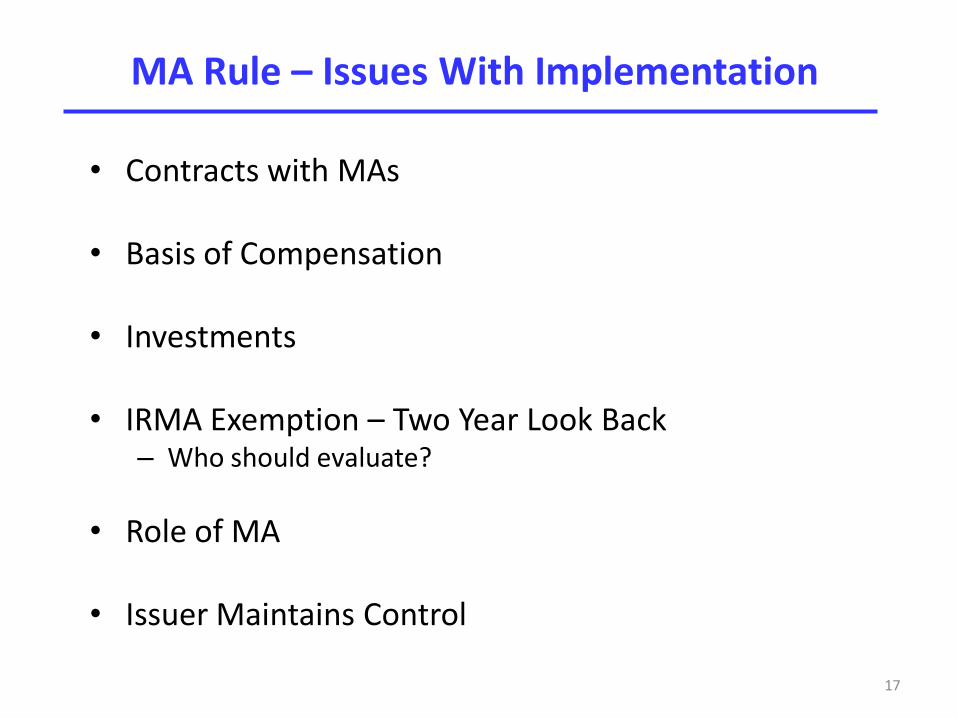

MA Rule – Issues With Implementation

• Contracts with MAs • Basis of Compensation

• Investments

• IRMA Exemption – Two Year Look Back

– Who should evaluate?

• Role of MA

• Issuer Maintains Control

17

MA Rule – Considerations Going Forward

• Dealer Compliance Policies and Procedures

• Additional Cost to Executing Business

• MSRB Rules – Oversight / Enforcement

• Changes in Market Practices

• Need for Sophisticated Issuer Exemption

18

The Municipal Advisor Rule:

Post July 1, 2014

Steve Apfelbacher

Ehlers President

On Behalf of the National Association of Independent Public

Finance Advisors

19

7/28/2014

Dodd-Frank Act

• NAIPFA supports Congressional action to legislate

Municipal Advisors

• Why?

History of municipal market participants using their

issuer relationship for their self gain at the expense of

taxpayers and ratepayers

• Municipal Advisors have fiduciary duty to issuers which

establishes clarity in who issuers can trust

• Securities Exchange Commission (SEC) since

determined Municipal Advisor Registration Requirements

20

Municipal Advisor (MA) Definition Observations

• Frequent issuers and infrequent issuers equally

impacted

• Rule does not just impact MA’s

• Rule impacts all market participants including issuers

• New behaviors/practices will need to be established

• Parts of the rule will have more significant impact in

different states and markets

• Limits “advice” by other professionals unless exemption

utilized • Bond Counsel

• Engineers

• Accountants

• Local bankers

• Vendors recommending financing options

21

Municipal Advisor (MA) Definition Observations

• Advice Underwriter is able to provide more limited also

– Can not provide advice on certain topics

– Can not provide advice unless retained

– Can not provide advice unless an exemption used

• Request For Proposal (RFP to 3 or more underwriters)

• Independent Registered Municipal Advisor (IRMA)

• Over time all underwriters will be selected more for

capabilities and not just relationship

• Yet unclear the final impact of various Municipal

Securities Rulemaking Board (MSRB) MA Rules

22

MA Firm Requirements

• How do MA firms comply?

• What client service is MA advice?

• Who at the firm is a MA?

• Security and Exchange Commission (SEC)

– Registration of MA Firm and MA I’s

– Maintain specific Books and Records

• Municipal Securities Rulemaking Board (MSRB)

– Duties of Non-Solicitor MA’s (Contracts, Disclosures)

• Fiduciary Duty (Duty of Care and Duty of Loyalty)

• Client Suitability

• Know Your Client

23

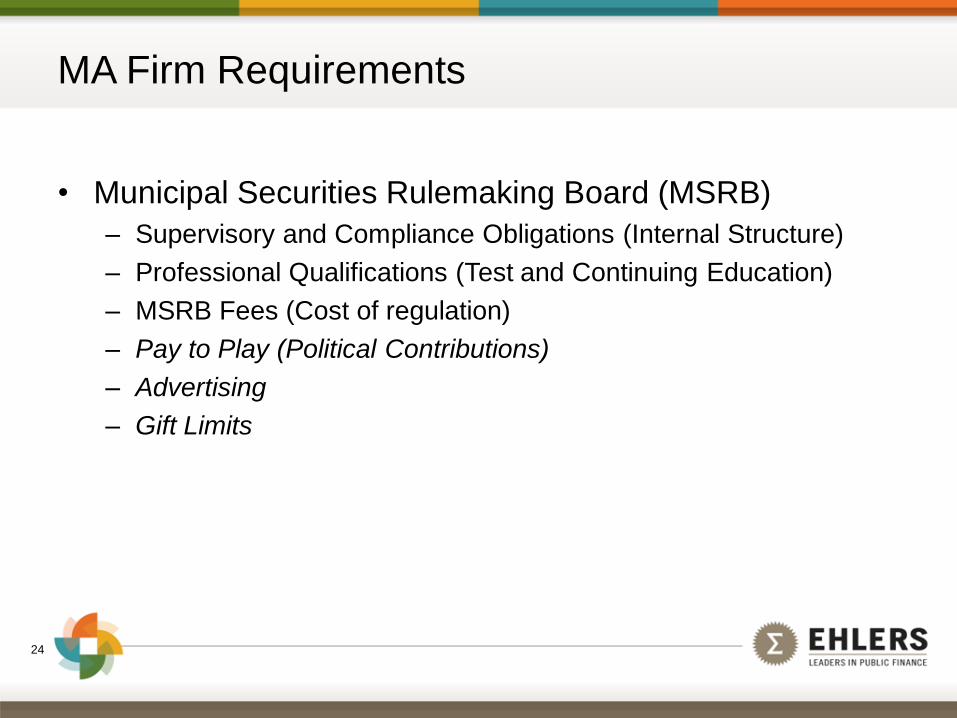

MA Firm Requirements

• Municipal Securities Rulemaking Board (MSRB)

– Supervisory and Compliance Obligations (Internal Structure)

– Professional Qualifications (Test and Continuing Education)

– MSRB Fees (Cost of regulation)

– Pay to Play (Political Contributions)

– Advertising

– Gift Limits

24

How SEC/MSRB Rules Affects Issuers

• MA’s engagements will be more formal

– Written engagement with scope of service defined/compensation

– Written/ongoing disclosure of conflicts and affiliations

• Unless excluded by written engagement, MA’s likely be

obligated to review options and make suitability

recommendation

• Independent Registered Municipal Advisor(IRMA)

Prediction- IRMA will become common practice for those

the use a MA but MA needs to be engaged to use IRMA

25

How SEC/MSRB Rule Affects Issuers

• What exemptions will you use? How will the issuer

execute those exemptions?

• What is the role of the MA if an IRMA exemption is used?

If MA is not participating in all advice discussions, how

do you keep the MA informed to meet their regulatory

obligation?

• Will issuer have point person who has authority to bind

issuer for:

– MA written agreement and ongoing MA disclosures?

– Underwriter engagement (Final and preliminary)?

– IRMA or RFP exemption?

26

How SEC/MSRB Rule Affects Issuers

• Bond purchaser cannot invest bond proceeds so what

does an issuer do to avoid this problem?

• Is a MA involved earlier in your project because of the

limitations the rule puts on advice from other

professionals?

• Should issuers use an underwriter MA for a competitive

sale knowing that they will lose a bidder on their

competitive sale?

27

Summary

• All municipal market participants need to be aware of the

MA rule and change our behavior/practice

• There were significant abuses the rule is attempting to

correct

• These changes are in the best interests of most of the

50,000 municipal market debt issuers

• This is good for taxpayers and ratepayers

28

Municipal Advisor Regulation

Post July 1, 2014

Lynnette Kelly, MSRB Executive Director

Ben Watkins, GFOA

Steve Apfelbacher, NAIPFA

Break

Rulemaking Update on Market Structure

Improvements and Enhancing Transparency

Michael L. Post, MSRB Deputy General Counsel

32

Improving Municipal Market Structure and

Transparency

• Developing best-execution standard for municipal

securities transactions

• Considering disclosure of pricing reference

information related to “matched trades” and

alternatives

33

Best Execution

• Benefits of complementing existing fair pricing

obligations of municipal securities dealers with a

best-execution standard:

– Buttress pricing protections

– Bolster obligations

– Improve execution quality for customers

– Promote fair competition among dealers resulting in

increased market efficiency

34

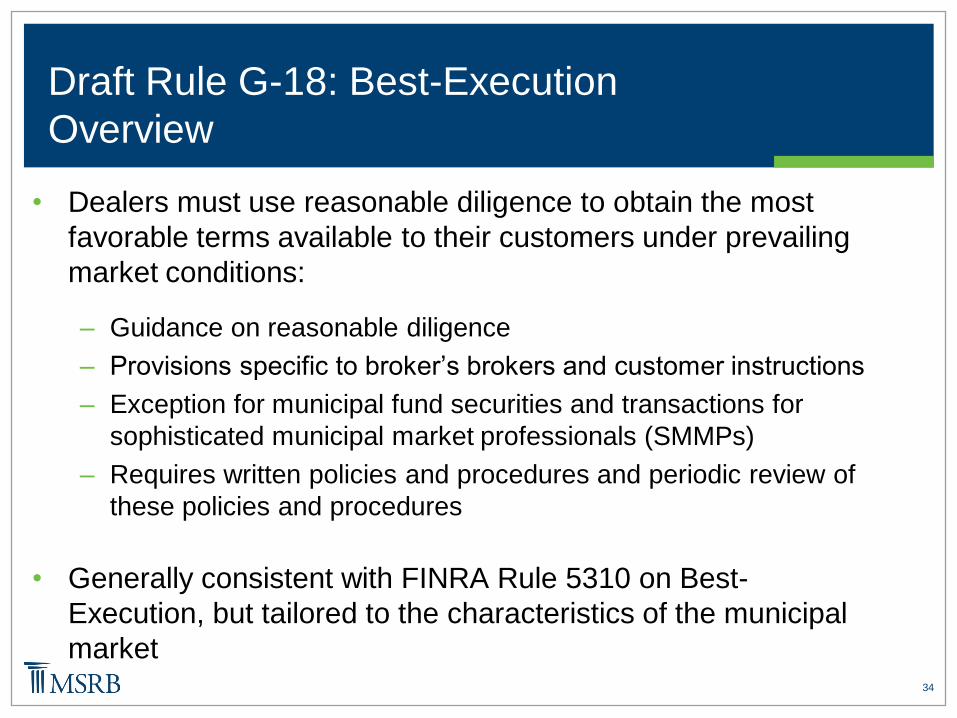

Draft Rule G-18: Best-Execution

Overview

• Dealers must use reasonable diligence to obtain the most

favorable terms available to their customers under prevailing

market conditions:

– Guidance on reasonable diligence

– Provisions specific to broker’s brokers and customer instructions

– Exception for municipal fund securities and transactions for

sophisticated municipal market professionals (SMMPs)

– Requires written policies and procedures and periodic review of

these policies and procedures

• Generally consistent with FINRA Rule 5310 on Best-

Execution, but tailored to the characteristics of the municipal

market

35

Best-Execution Obligation

• Use reasonable diligence to ascertain the best market for

the security

– “Market” may include broker’s brokers, alternative trading systems

or platforms or other counterparties, including a dealer itself acting

as a principal, among others

• Buy or sell in that market so that the price to the customer

is as favorable as possible under prevailing market

conditions

36

Reasonable Diligence

• Factors used to determine whether a dealer has used

“reasonable diligence” include:

– Character of the market for the security

– Size and type of transaction

– Number of markets checked

– Information reviewed to determine the current market for the

security or similar securities

– Accessibility of quotations

– Terms and conditions of the customer’s inquiry or order

37

Reasonable Diligence (continued)

• Factors in draft Rule G-18 generally conform to the factors

in FINRA’s best execution rule (FINRA Rule 5310)

– Exception: Information reviewed to determine the current market

for the security or similar securities is an additional factor not found

in FINRA Rule 5310

• Factors in draft Rule G-18 also guide the use of reasonable

diligence when there are no available quotations for a

security

38

Reasonable Diligence (continued)

• Failure to obtain the most favorable price does not

necessarily mean that a dealer failed to use reasonable

diligence

• A dealer’s failure to maintain adequate resources is not an

excuse for executing away from the best available market

• The level of resources required to be maintained will

depend on the nature of the dealer’s municipal securities

business, taking into account its level of sales and trading

activity

39

Best-Execution Policies and Procedures

• Dealers must have written policies and procedures that

address how best-execution determinations will be made

for securities with limited pricing information or

quotations

• Dealers must document compliance with their policies

and procedures

• Dealers must conduct periodic reviews of their policies

and procedures for determining the best available market

for execution of retail customer transactions

40

An Analogy

41

Other Elements of Best-Execution Draft Rule

• Interpositioning

• Timing

• Principal and Agency Transactions

• Executing Brokers

• Customer Instructions

• Sophisticated Municipal Market Professionals (SMMPs)

• Municipal Fund Securities

42

Pricing Reference Information

• Discussing regulatory approaches to enhance investor

access to information about transaction pricing and the

market

• Working closely with FINRA and SEC to develop an

approach taking into account increased transparency for

investors and the need for fair dealer compensation

Rulemaking Update on Market Structure

Improvements and Enhancing Transparency

Questions

New Tools on EMMA®

Justin Pica, MSRB Director of Product Management –

Market Transparency

45

The EMMA® Website

• Launched by the MSRB in 2008

• Serves as official, free and public source of trade

data and disclosure information on virtually all

municipal securities

• Provides a platform for issuers to communicate

with investors

emma.msrb.org

46

Information Available on EMMA

• Official Statements

• Trade Prices and Yields

• Ongoing Financial Disclosures

• Event Notices

• Advance Refunding

Documents

• Credit Ratings

• Variable Rate Securities

Information

– Interest rate resets

– Credit enhancement documents

• Market Statistics

– New issuance

– Trade statistics

– Disclosure statistics

• 529 Plan Disclosure

• Political contribution disclosure

47

Navigating EMMA

• Browse for

information

by:

– Issuer

– Security

– CUSIP

• View real-

time market

data

48

Issuer Homepages

Municipal Securities Rulemaking Board 48

• Pilot! EMMA® Issuer Homepages display issuer

information in a single location

− Geographic search

− More intuitive access to

information on issuers

for EMMA® users

− emma.msrb.org/

IssuerHomePage

49

Issuer Homepage Features

• Listing of bond issues

• Trade activity

• Pre-sale documents

• Official statements

• Financial and event

disclosures

• Refunding escrows

50

Manage Issuer Homepages

• Customize and consolidate issuer information in a

single location on EMMA®

− Customize plain-English name of issuer and bond issues

− Edit issue list, contact information and website links

− Minimal annual maintenance needed – receive email

alert when new issue is added to an issuer homepage

51

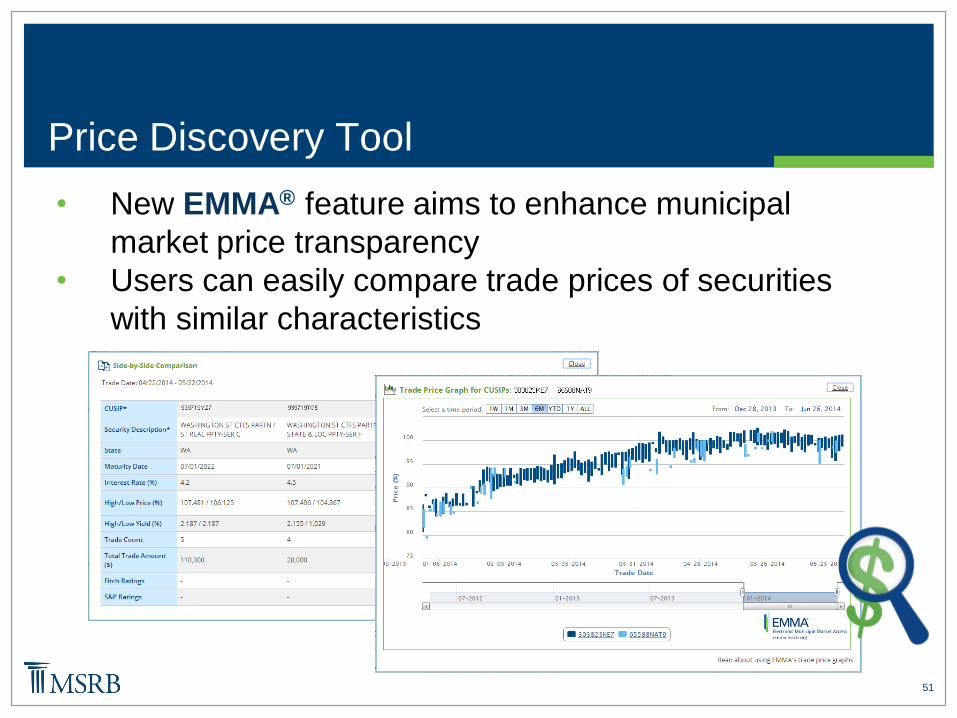

Price Discovery Tool

• New EMMA® feature aims to enhance municipal

market price transparency

• Users can easily compare trade prices of securities

with similar characteristics

52

Enhanced Trade Data Display

• See daily high and low price for individual securities

• Visualize historical trading trends for every security

53 Municipal Securities Rulemaking Board 53

• Seeking to expand pricing-related data available on

EMMA® by developing a proposed framework for

collecting additional post-trade information for public

display

• Exploring an approach for collecting and disseminating

relevant pre-trade data

Future Enhancements to Price

Transparency on EMMA

Municipal Securities Rulemaking Board 53

Demonstration of New Tools on EMMA®

MuniPriceDiscovery.org

Closing

Ritta McLaughlin, MSRB Chief Education Officer

56 Municipal Securities Rulemaking Board 56

• New single location for free educational resources on

the municipal market

• Available on msrb.org

• Access videos, fact sheets and resources about:

– Understanding the municipal market

– Using EMMA® to make informed decisions

– Issuing municipal securities

MSRB Education Center

Municipal Securities Rulemaking Board 56

57

Contact the MSRB

MSRB Online

msrb.org

emma.msrb.org

MSRB Support

703-797-6668

Hours of Operation:

7:30 a.m. - 6:30 p.m. ET

MSRB Email Updates

– Subscribe at msrb.org

Follow the MSRB on Twitter

@MSRB_News