Economy, Retail & Beer - Arena International

45

Economy, Retail & Beer By Matthias Queck Research Director Copenhagen, 29 May 2012 How the economy shapes retail channel development and product ranges A Service

Transcript of Economy, Retail & Beer - Arena International

Economy Retail amp Beer

By Matthias Queck Research Director

Copenhagen 29 May 2012

How the economy shapes retail channel development and product ranges

A Service

2

Contents

1 Economic Development

2 Retail Evolution

3 Big Plans for Small Stores

4 Smaller Plans for Bigger Stores

5 Polarisation Discounting amp Private Label

6 Summary

3

About Planet Retail

4

1 Economic Development

2 Retail Evolution

5

Europe continues to be divided economically

Positive outlook for countries benefiting from emerging markets growth and featuring stable domestic economy

Difficult outlook for countries struck by public and household debt crises (UK Ireland Spain Greece Portugal) with most problems coming from the inside Several countries will lose a full decade

Consumer confidence is key in countries with high dependence on domestic consumption (UK Portugal)

Structural adaptations in retail will be accordingly deep amp fast there

But not all structural change in retail is economy-led Further drivers are demographic trends and channel development

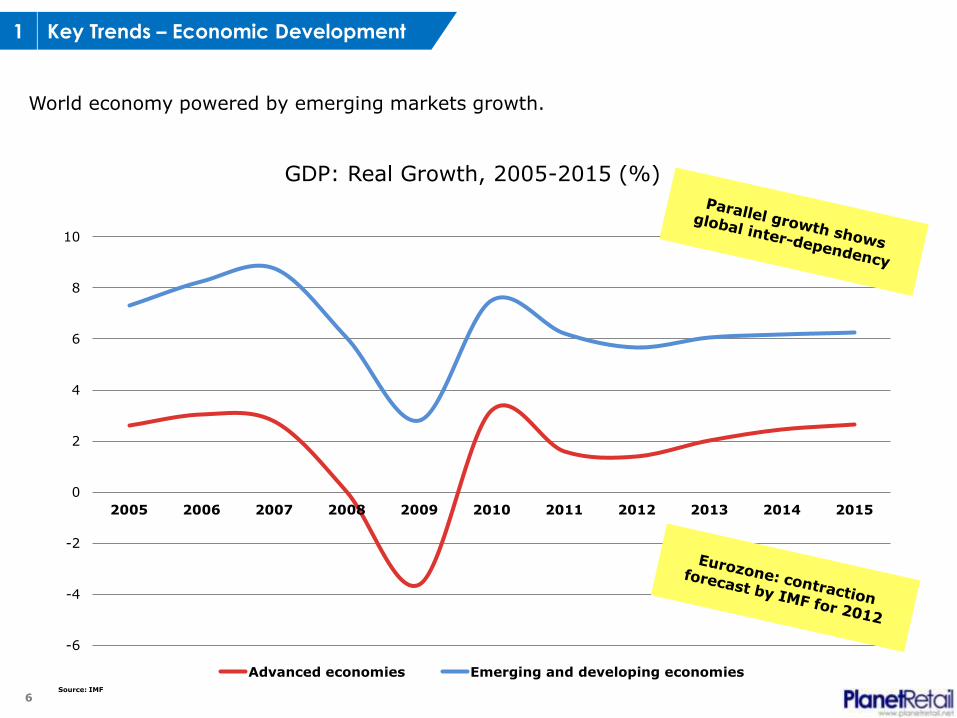

X Key Trends ndash Economic Development 1

6

GDP Real Growth 2005-2015 ()

Source IMF

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Advanced economies Emerging and developing economies

World economy powered by emerging markets growth

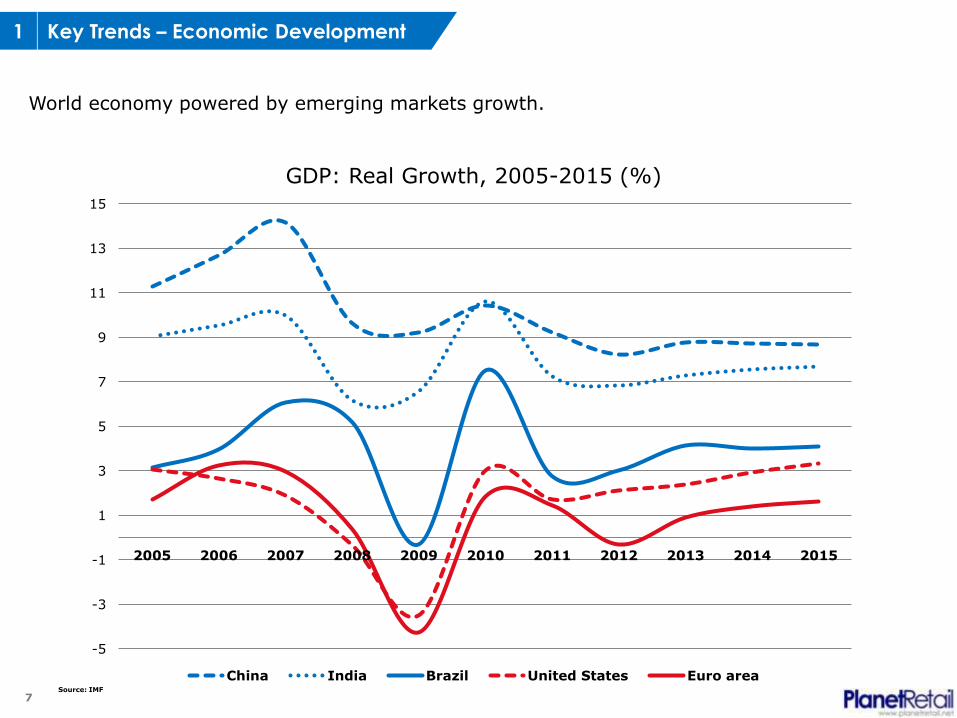

X Key Trends ndash Economic Development 1

7

GDP Real Growth 2005-2015 ()

Source IMF

-5

-3

-1

1

3

5

7

9

11

13

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China India Brazil United States Euro area

World economy powered by emerging markets growth

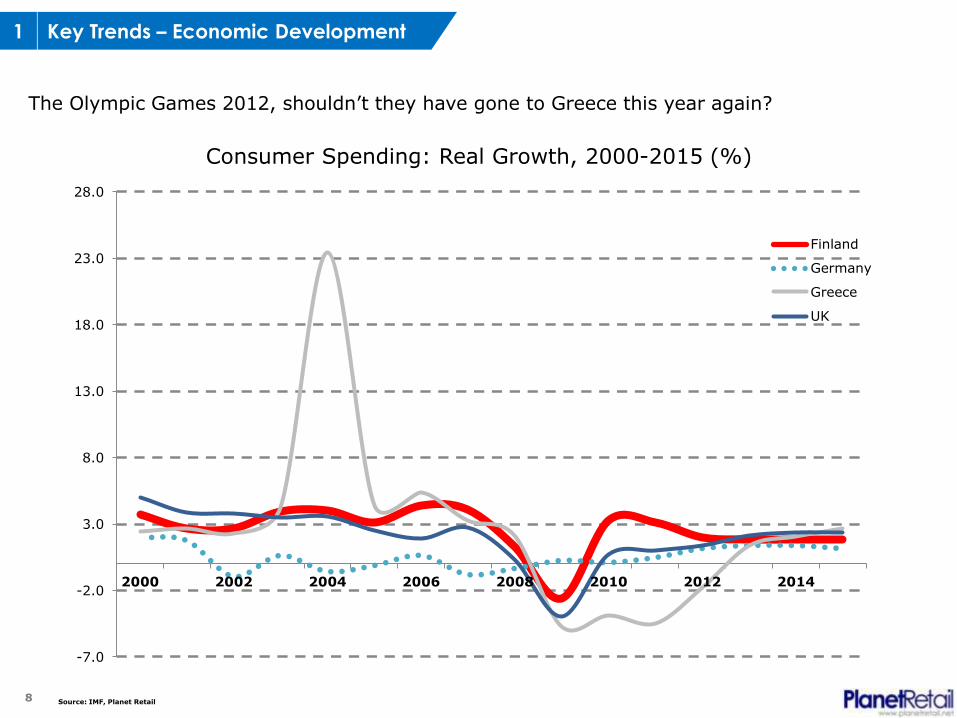

X Key Trends ndash Economic Development 1

8

Consumer Spending Real Growth 2000-2015 ()

Source IMF Planet Retail

-70

-20

30

80

130

180

230

280

2000 2002 2004 2006 2008 2010 2012 2014

Finland

Germany

Greece

UK

X Key Trends ndash Economic Development 1

The Olympic Games 2012 shouldnrsquot they have gone to Greece this year again

9

800

900

1000

1100

2007 2008 2009 2010 2011 2012 2013 2014 2015

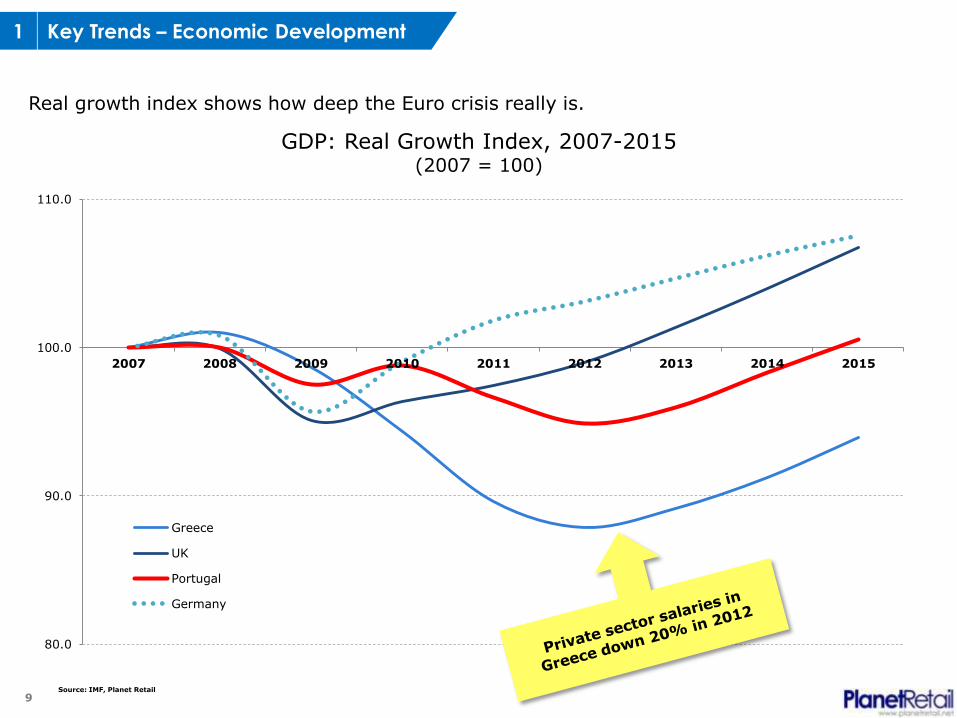

Greece

UK

Portugal

Germany

GDP Real Growth Index 2007-2015 (2007 = 100)

Source IMF Planet Retail

Real growth index shows how deep the Euro crisis really is

X Key Trends ndash Economic Development 1

10

79

7

46

3

60

6

39

3

46

1

36

6

36

8

36

2

29

8

26

5

74

6

69

9

65

0

48

3

46

6

45

2

43

6

42

1

38

7

29

9

77

5

98

8

80

9

64

8

48

4

49

6

50

2

52

2

49

3

34

1

0

20

40

60

80

100

120

Carrefour Schwarz Group Tesco Auchan Metro Group Edeka Aldi Rewe Group Leclerc ITM(Intermarcheacute)

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

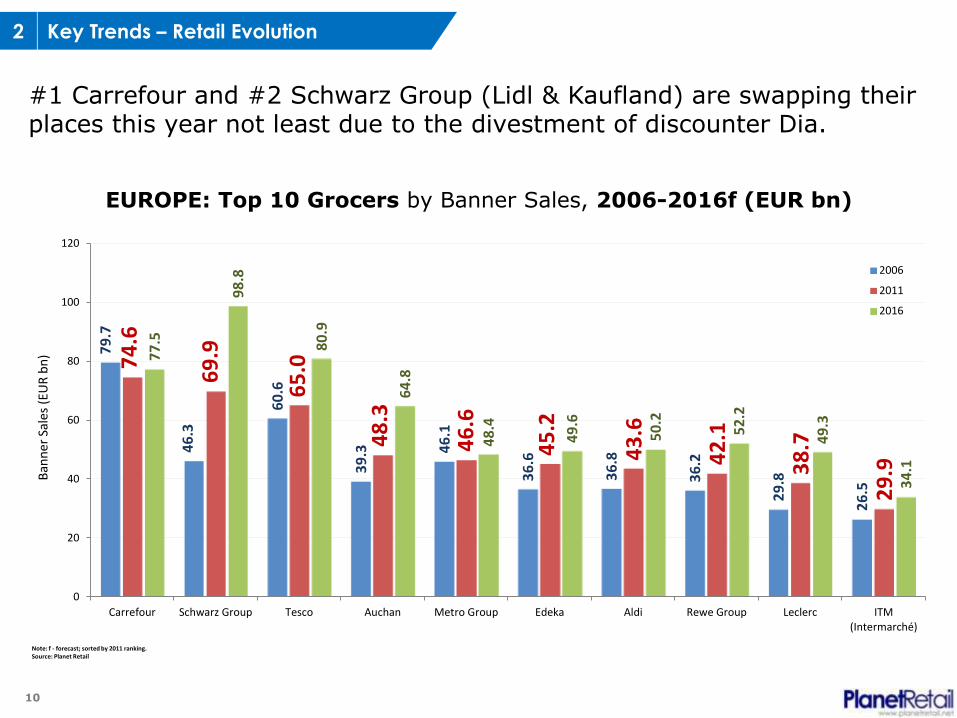

EUROPE Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

1 Carrefour and 2 Schwarz Group (Lidl amp Kaufland) are swapping their places this year not least due to the divestment of discounter Dia

X Key Trends ndash Retail Evolution 2

11

29

05

97

7

68

9

46

3

51

7

50

7

43

5

45

1

41

4

48

7

34

83

10

70

80

5

69

9

69

0

62

6

58

1

57

2

51

8

51

1

49

42

12

98

10

87

98

8

83

7

89

0

86

1

71

4

67

7

59

2

0

50

100

150

200

250

300

350

400

450

500

Walmart Carrefour Tesco Schwarz Group Seven amp I Costco Auchan Aldi Casino Metro Group

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

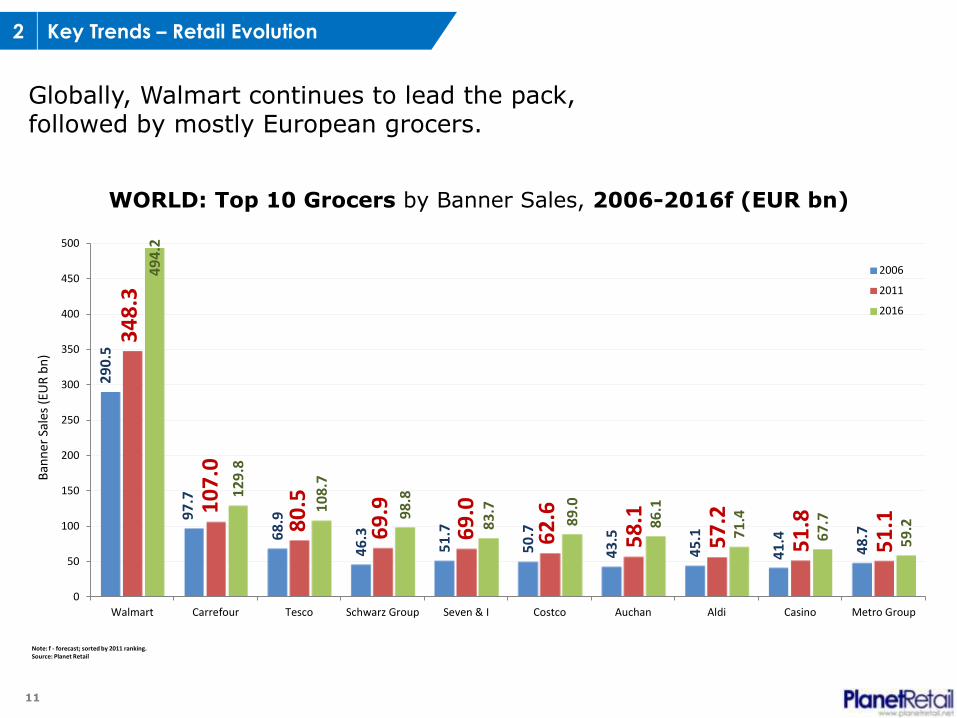

WORLD Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

Globally Walmart continues to lead the pack followed by mostly European grocers

X Key Trends ndash Retail Evolution 2

12

0

10

20

30

40

50

60

70

80

90

100

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

Sale

s (

)

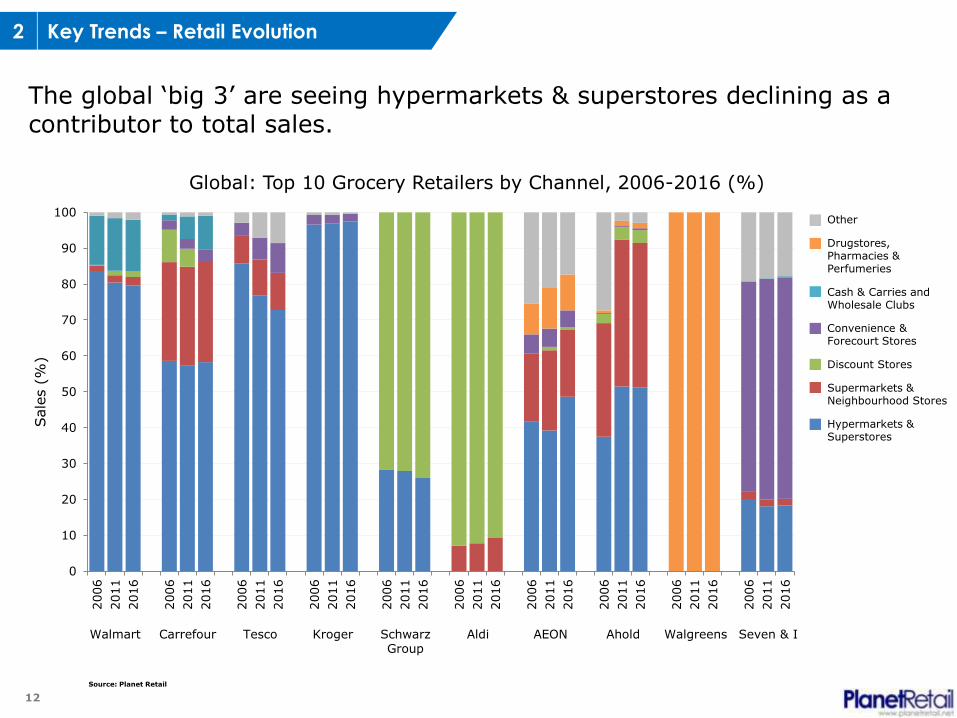

Global Top 10 Grocery Retailers by Channel 2006-2016 ()

The global lsquobig 3rsquo are seeing hypermarkets amp superstores declining as a contributor to total sales

Source Planet Retail

Walmart Carrefour Schwarz Group

Tesco Kroger Aldi AEON Ahold Walgreens Seven amp I

Other

Drugstores Pharmacies amp Perfumeries

Cash amp Carries and Wholesale Clubs

Convenience amp Forecourt Stores

Discount Stores

Supermarkets amp Neighbourhood Stores

Hypermarkets amp Superstores

X Key Trends ndash Retail Evolution 2

13

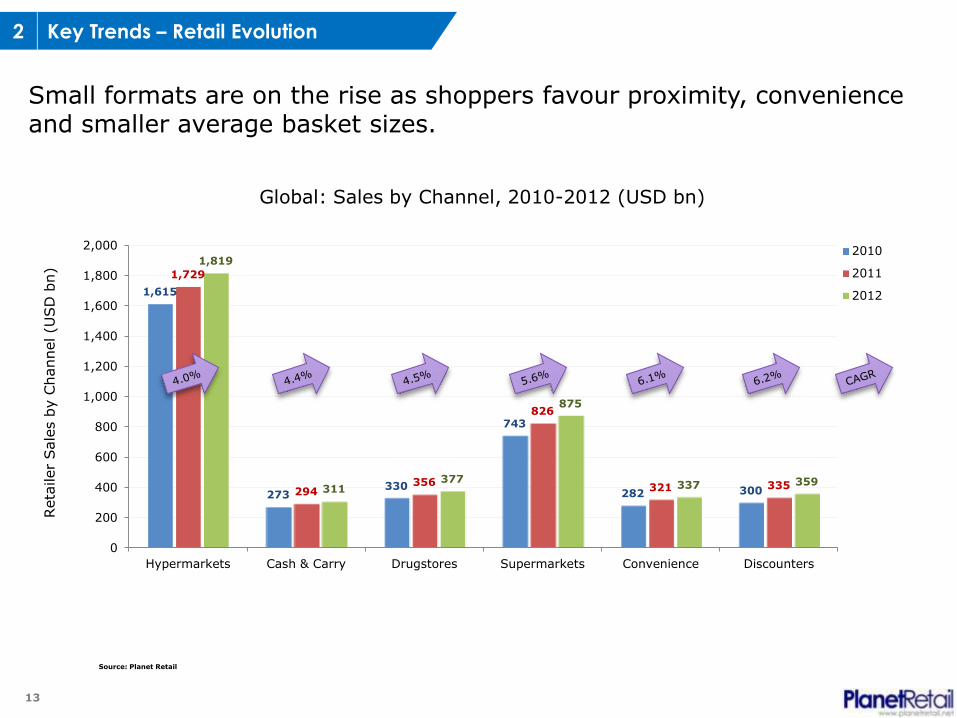

Small formats are on the rise as shoppers favour proximity convenience and smaller average basket sizes

1615

273 330

743

282 300

1729

294 356

826

321 335

1819

311 377

875

337 359

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Hypermarkets Cash amp Carry Drugstores Supermarkets Convenience Discounters

Reta

iler

Sale

s b

y C

hannel (U

SD

bn)

Global Sales by Channel 2010-2012 (USD bn)

2010

2011

2012

Source Planet Retail

X Key Trends ndash Retail Evolution 2

14

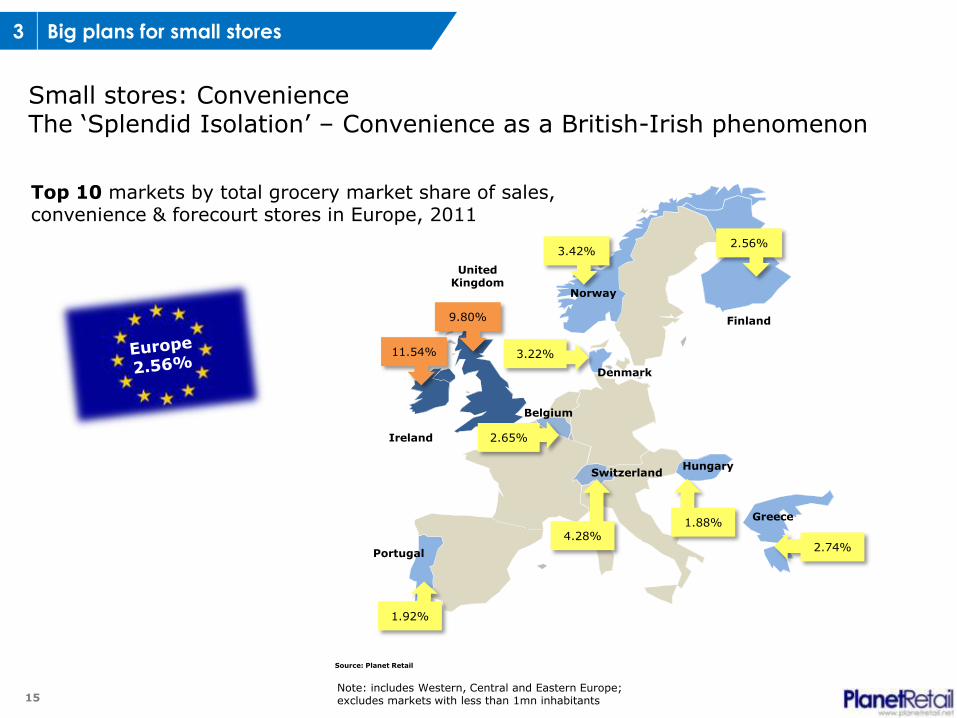

15

Ireland

United Kingdom

Portugal

Belgium

Switzerland

Denmark

Norway

Finland

Hungary

Small stores Convenience The lsquoSplendid Isolationrsquo ndash Convenience as a British-Irish phenomenon

1154

980

256

428

342

322

Greece 188

192

265

274

Note includes Western Central and Eastern Europe excludes markets with less than 1mn inhabitants

Source Planet Retail

Top 10 markets by total grocery market share of sales convenience amp forecourt stores in Europe 2011

X Big plans for small stores 3

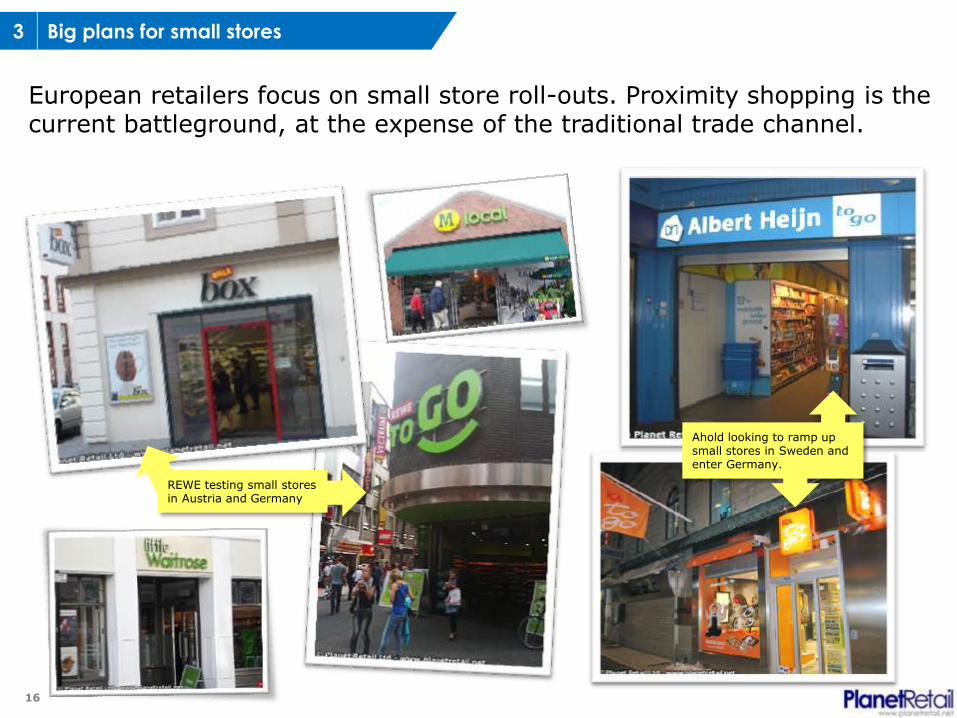

16

European retailers focus on small store roll-outs Proximity shopping is the current battleground at the expense of the traditional trade channel

X Big plans for small stores 3

Ahold looking to ramp up small stores in Sweden and enter Germany

REWE testing small stores in Austria and Germany

17

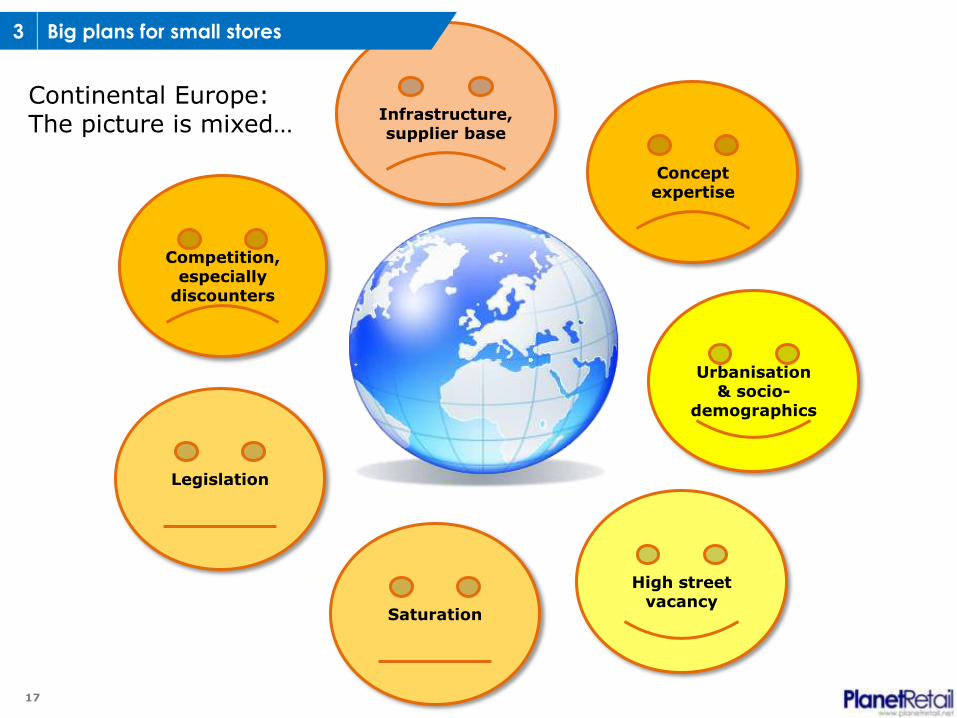

Legislation

High street

vacancy

Infrastructure supplier base

Urbanisation

amp socio-demographics

Competition

especially discounters

Concept

expertise

Saturation

Continental Europe The picture is mixedhellip

X Big plans for small stores 3

18

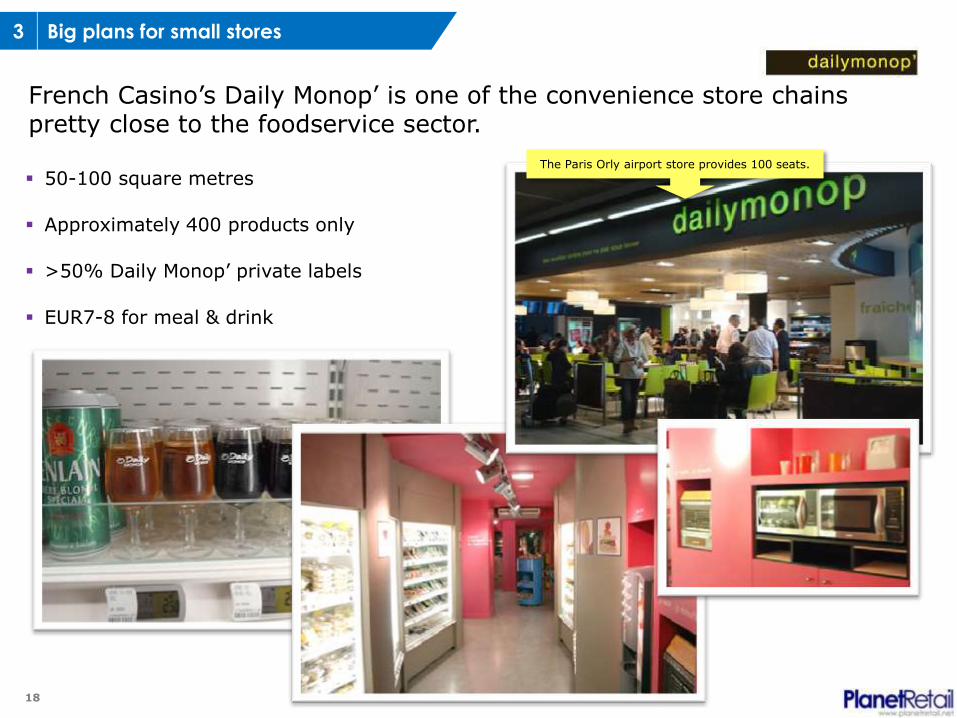

French Casinorsquos Daily Monoprsquo is one of the convenience store chains pretty close to the foodservice sector

50-100 square metres

Approximately 400 products only

gt50 Daily Monoprsquo private labels

EUR7-8 for meal amp drink

The Paris Orly airport store provides 100 seats

X Big plans for small stores 3

19

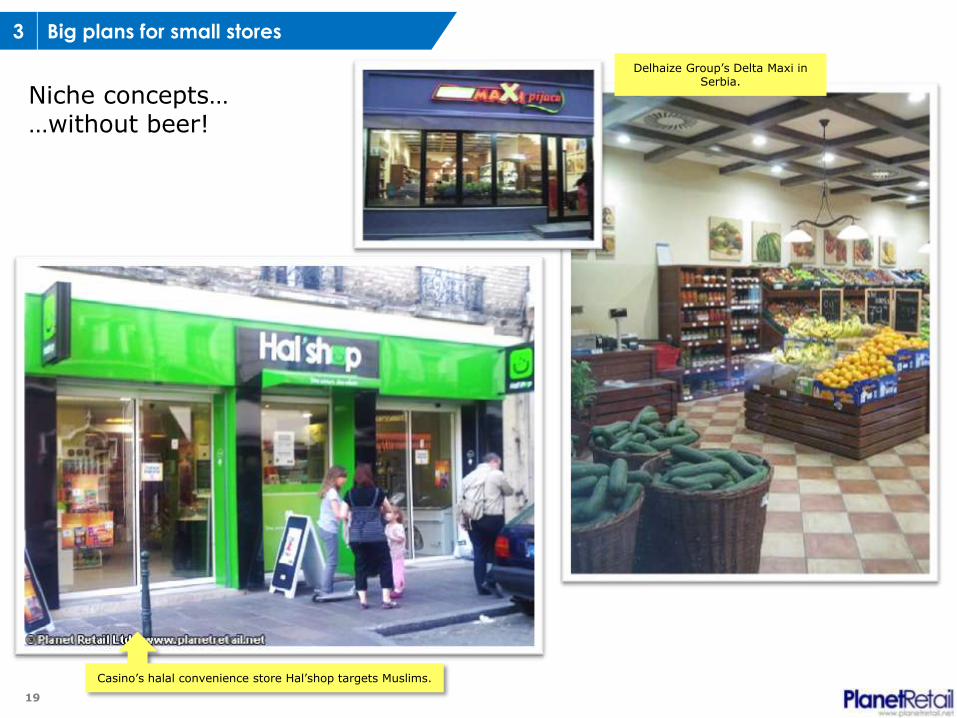

Casinorsquos halal convenience store Halrsquoshop targets Muslims

X Big plans for small stores 3

Delhaize Grouprsquos Delta Maxi in Serbia

Niche conceptshellip hellipwithout beer

20

Discounters and convenience

Customers have learned private label quality does not have to be expensive

Small city-centre locations make shopping convenient

Limited assortment means pre-selection

X Big plans for small stores 3

ldquoSnacks to gordquo at German Edekarsquos Netto discount store

Convenience products from discounter Aldi Germany

21

Is there a future for hypermarkets

22

-40

-30

-20

-10

00

10

20

30

40

50

60

Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3

Walmart US

Metro Group Real

Sonae MC

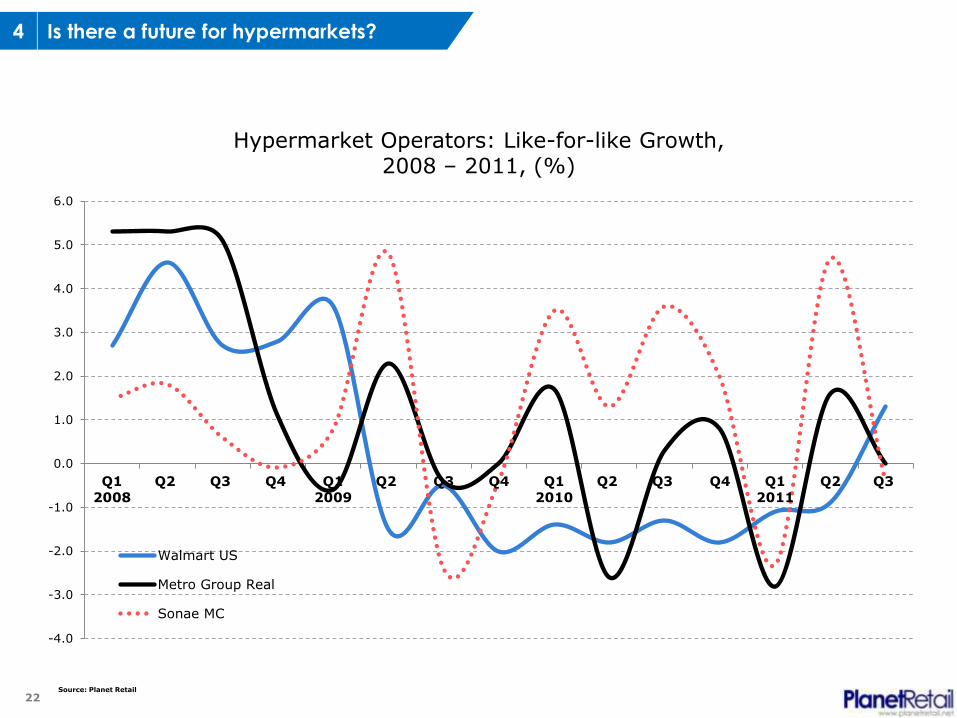

Hypermarket Operators Like-for-like Growth 2008 ndash 2011 ()

Source Planet Retail

Is there a future for hypermarkets 4

23

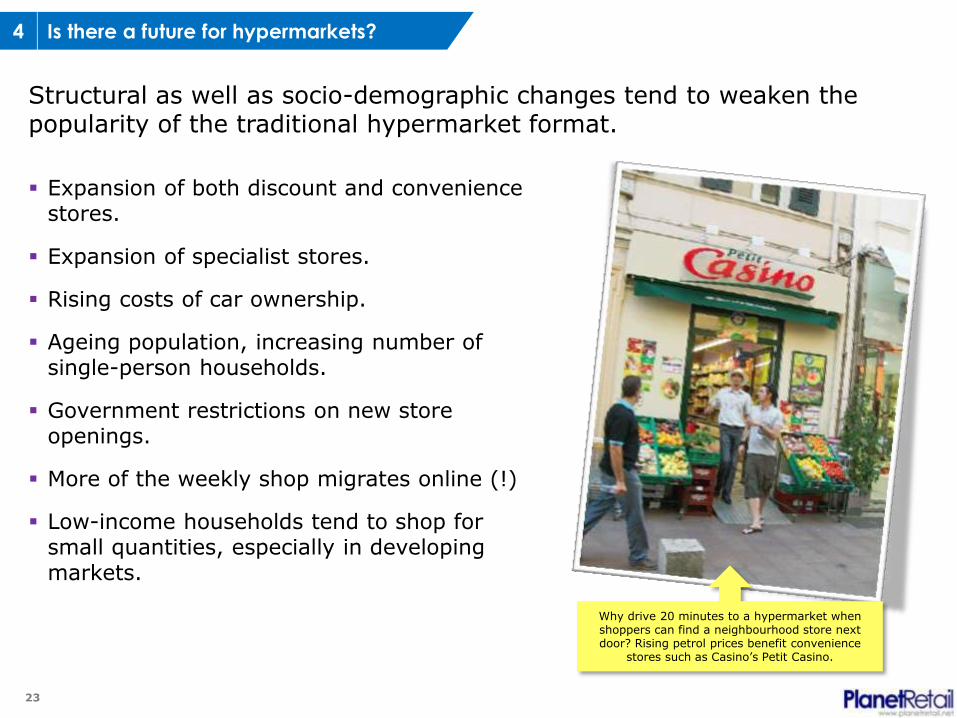

Structural as well as socio-demographic changes tend to weaken the popularity of the traditional hypermarket format

Why drive 20 minutes to a hypermarket when shoppers can find a neighbourhood store next door Rising petrol prices benefit convenience

stores such as Casinorsquos Petit Casino

Expansion of both discount and convenience stores

Expansion of specialist stores

Rising costs of car ownership

Ageing population increasing number of single-person households

Government restrictions on new store openings

More of the weekly shop migrates online ()

Low-income households tend to shop for small quantities especially in developing markets

Is there a future for hypermarkets 4

24

Going small Compact stores offer numerous benefits for the retailer as well as for the shopper

Higher flexibility smaller catchment areas

Is there a future for hypermarkets 4

25

Polarisation Trading up ndash or trading down

Self-discount

department with loose

goods at Auchan in

France

hellipand at Auchanrsquos

Jumbo hypermarkets in

Portugal

Carrefour Planet

in France

Is there a future for hypermarkets 4

26

27

gtgtThe lsquotwo nationsrsquo phenomenon is also seen in the alcohol market with premium brands increasing in popularity The

UKs top five lsquoworld beerrsquo brands ndash San Miguel Peroni Tuborg Cobra and Tiger ndash have seen sales rise by 201 in the past year 2011 despite total lager volume sales falling

by 7ltlt

UK The Grocer

Polarisation in store formats

Polarisation in shopping behaviour

Polarisation in brands

Polarisation in private labels

Polarisation ndash Discounting ndash Private Label 5

28

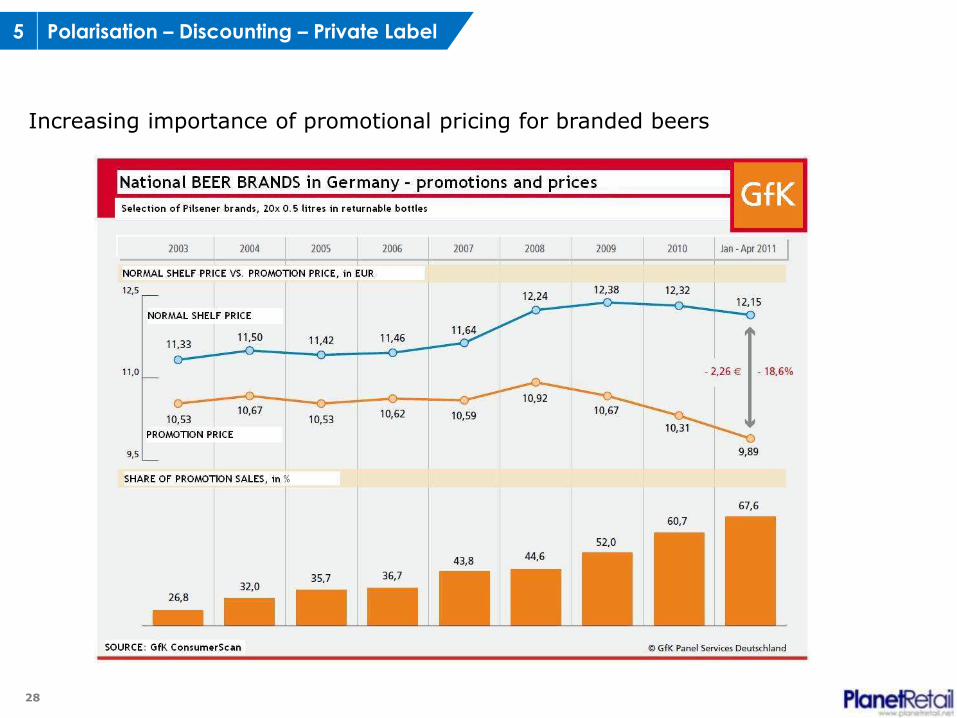

Increasing importance of promotional pricing for branded beers

Polarisation ndash Discounting ndash Private Label 5

29

Discounters Lidl continues to promote the lowest price segment

Polarisation ndash Discounting ndash Private Label 5

30

hellipand competitor Netto (Edeka) goes even lower

Polarisation ndash Discounting ndash Private Label 5

31

hellipwhile Aldi seems undecided whether to give up on the category (Aldi Suumld) allow brands (Aldi Nord) exclusive brand agreements (USA) or develop premium private labels (UK) ldquoDiscounter Aldi Suumld in the UK has appointed Clarion Communications to handle its consumer public relations to promote its range of beers wines and spirits The agency has reportedly been tasked with conveying the quality and value for money proposition and plans to use endorsements awards and creative news generation to achieve this goalrdquo

Polarisation ndash Discounting ndash Private Label 5

32

Source Planet Retail Ltd - wwwplanetretailnet

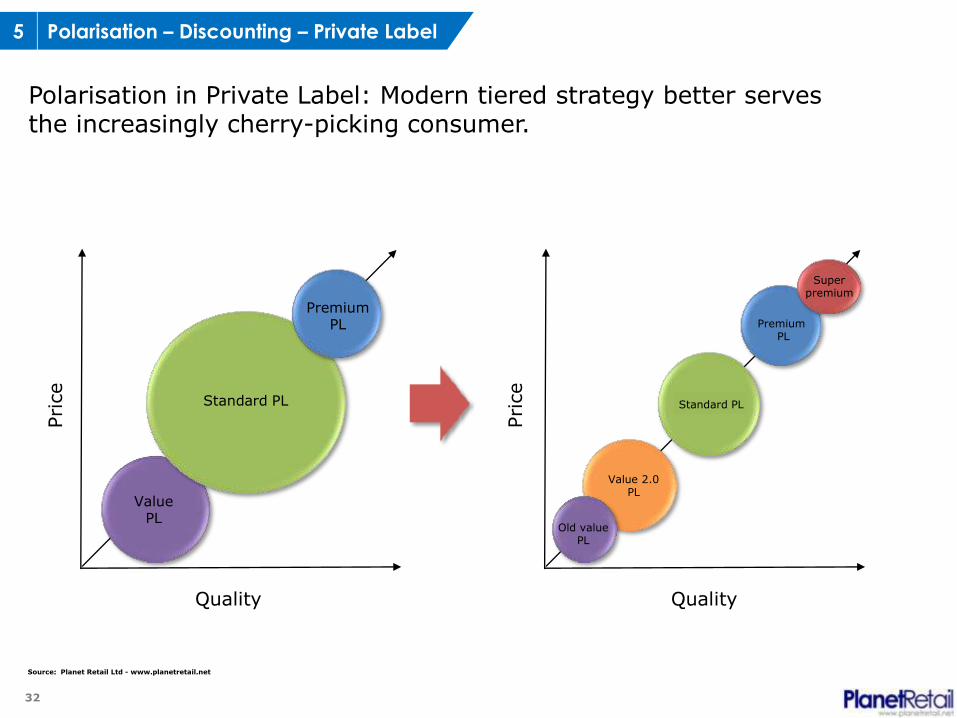

Polarisation in Private Label Modern tiered strategy better serves the increasingly cherry-picking consumer

Value PL

Standard PL

Premium PL

Pri

ce

Quality

Value 20 PL

Standard PL

Premium PL

Super premium

Old value PL

Pri

ce

Quality

Polarisation ndash Discounting ndash Private Label 5

33

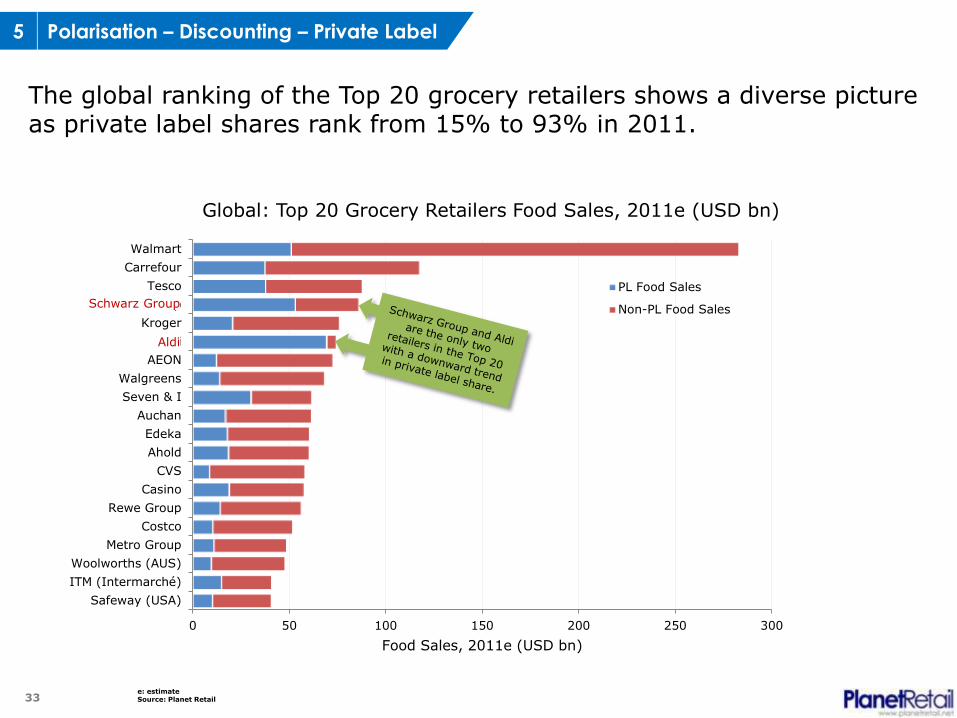

The global ranking of the Top 20 grocery retailers shows a diverse picture as private label shares rank from 15 to 93 in 2011

0 50 100 150 200 250 300

Safeway (USA)

ITM (Intermarcheacute)

Woolworths (AUS)

Metro Group

Costco

Rewe Group

Casino

CVS

Ahold

Edeka

Auchan

Seven amp I

Walgreens

AEON

Aldi

Kroger

Schwarz Group

Tesco

Carrefour

Walmart

Food Sales 2011e (USD bn)

Global Top 20 Grocery Retailers Food Sales 2011e (USD bn)

PL Food Sales

Non-PL Food Sales

e estimate Source Planet Retail

Schwarz Group

Aldi

Polarisation ndash Discounting ndash Private Label 5

34

Increasing importance of private label even in brand-driven categories

+++ January 2011

US-based drugstore

operator Walgreens

launches lsquoFlats

1901rsquo+++

+++ February 2011

US grocery operator

SuperValu launches

Buck Range Light

beer line +++

+++ June 2011

Delhaize Group

introduces limited-

edition premium

private label beer

lsquoSingle Hoprsquo in

Belgium +++

+++ Autumn 2011

US grocer Harris

Teeter introduces

Barrel Trolley

range +++

+++ August 2011

Japanese retailer

AEON introduces

Topvalu Barreal

Lager Beer +++

Polarisation ndash Discounting ndash Private Label 5

35

Zielpunktrsquos Mundl Beer in Austria ndash Tegutrsquos Josefs Kellerbier in Germany

Polarisation ndash Discounting ndash Private Label 5

36

Polarisation ndash Discounting ndash Private Label 5

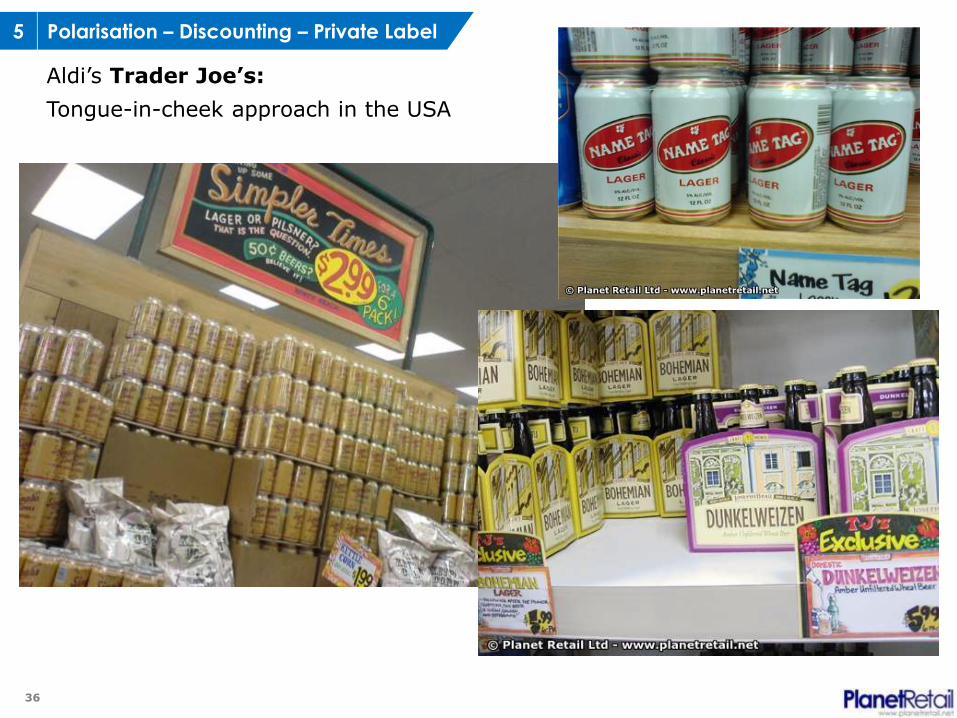

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA

37

Polarisation ndash Discounting ndash Private Label 5

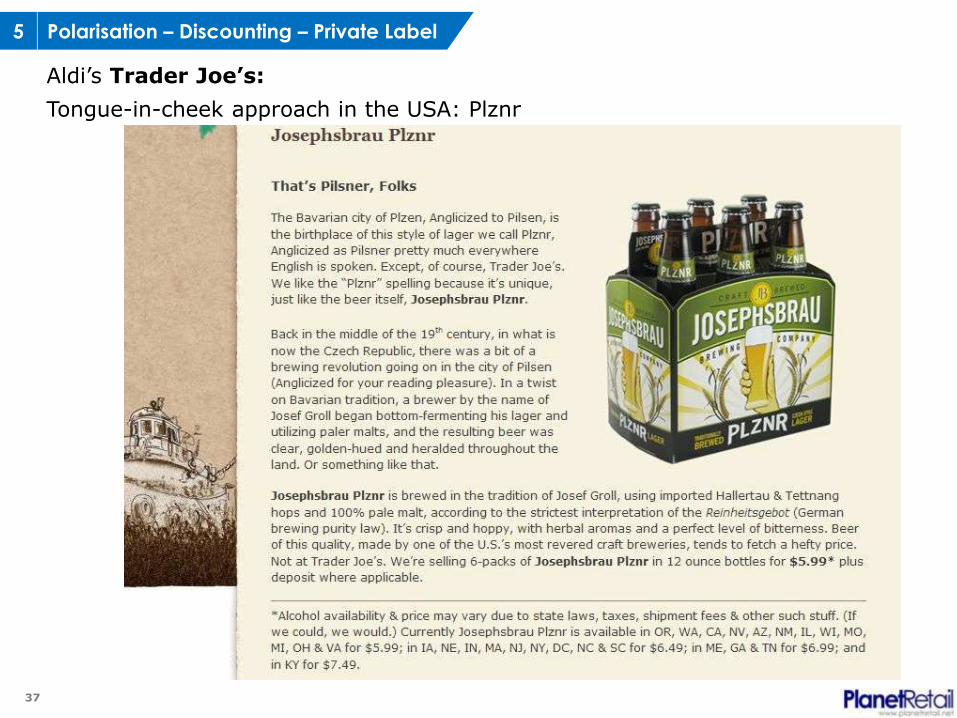

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA Plznr

38

Provenance amp Transparency Regional is the new sustainable Regionality gives brands a face

Polarisation ndash Discounting ndash Private Label 5

39

Shopper democracy amp customer engagement Private label allows retailers to directly liaise with shoppers ndash not only in-store but also online via social media

Polarisation ndash Discounting ndash Private Label 5

40

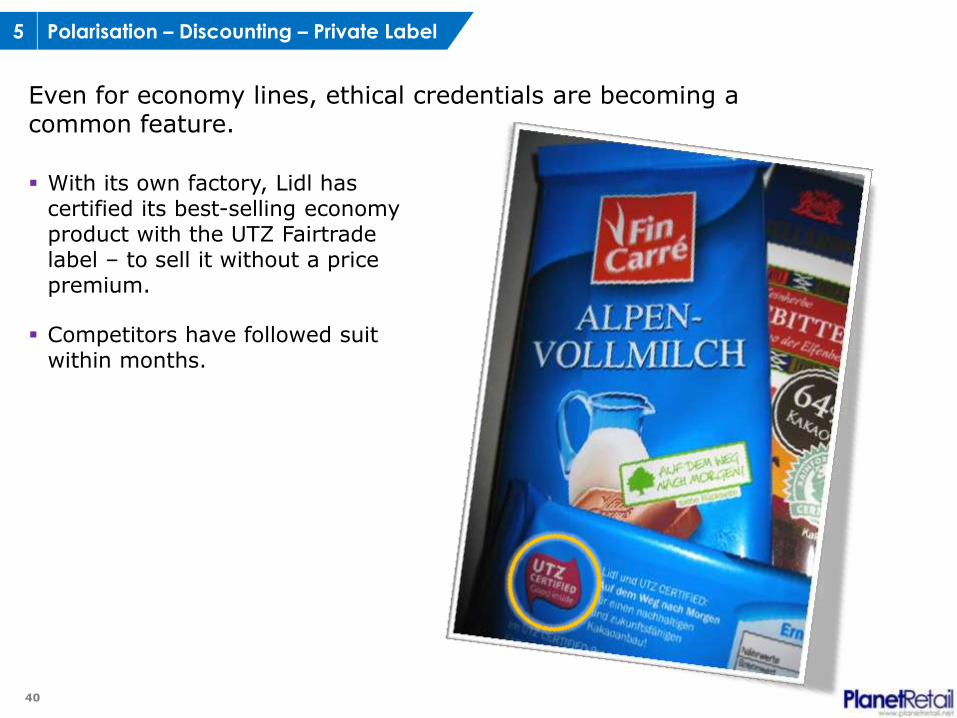

Even for economy lines ethical credentials are becoming a common feature

With its own factory Lidl has certified its best-selling economy product with the UTZ Fairtrade label ndash to sell it without a price premium

Competitors have followed suit within months

Polarisation ndash Discounting ndash Private Label 5

41

Vertical integration Retailers are investing in production facilities to gain independence of increasingly volatile commodity markets

Migros Coop CH Morrisons Lidl etc

Cutting out the middleman

Access to commodity markets

Expertise for annual range reviews

Control from farm to fork

Long-term planning

But Creates dependence

Polarisation ndash Discounting ndash Private Label 5

42

43

Europe continues to be divided economically

Small stores will continue to outperform larger stores globally not least due to polarisation

Polarisation store formats shopping behaviour (cherry-picking) brands private labels

Hypermarkets are on the rocky path from providing lsquoeverything for everyonersquo to becoming the lsquospecialist for everyonersquo

Rising fuel prices high flexibility of small formats the expansion of specialists a trend towards smaller families more single households and an ageing population and changing shopping habits benefit small stores online and necessitate compact hypermarkets

Summary 6

44

Shopper engagement and transparency will instil trust and loyalty among brand and private label shoppers alike But thanks to their general distribution function retailers are closer to consumers than manufacturers ndash not only in-store but also via social media

There are opportunities for additional investment in premium and niche private label ranges ndash even at discounters

Summary 6

United Kingdom

Greater London House

Hampstead Road

London

NW1 7EJ

United Kingdom

T +44 (0)207 728 5600

F +44 (0)207 728 4999

Germany

Dreieichstrasse 59

D-60594 Frankfurt am Main

Germany

T +49 (0) 69 96 21 75-6

F +49 (0) 69 96 21 75-70

Japan

co INSIGHT INC

Atami Plaza 1401

Kasuga-cho 16-45 Atami-shi

Shizuoka 413-0005

Japan

T +81 (0) 557 35 9102

F +81 (0) 557 35 9103

China

10-1-202

88 Tongxing Road

Qingdao 266034

China

T +86 (0)532 85981272

F +86 (0)532 85989372

USA

1450 American Lane

Suite 1400

Schaumburg

IL 60173

USA

Tel + (1) 224 698 2601

Fax + (1) 224 698 9230

twittercomPlanetRetail

facebookcomPlanetRetail

tinyurlcomPR-linkedin

Researched and published by Planet Retail Limited

Company No 3994702 (England amp Wales) - Registered Office 66 Wigmore Street London W1U 2SB

Terms of use and copyright conditions

This document is copyrighted All rights reserved and no part of this publication may be reproduced stored in a retrieval system or transmitted in any

form without the prior permission of the publishers We have taken every precaution to ensure that details provided in this document are accurate

The publishers are not liable for any omissions errors or incorrect insertions nor for any interpretations made from the document

A Service

Thank you

2

Contents

1 Economic Development

2 Retail Evolution

3 Big Plans for Small Stores

4 Smaller Plans for Bigger Stores

5 Polarisation Discounting amp Private Label

6 Summary

3

About Planet Retail

4

1 Economic Development

2 Retail Evolution

5

Europe continues to be divided economically

Positive outlook for countries benefiting from emerging markets growth and featuring stable domestic economy

Difficult outlook for countries struck by public and household debt crises (UK Ireland Spain Greece Portugal) with most problems coming from the inside Several countries will lose a full decade

Consumer confidence is key in countries with high dependence on domestic consumption (UK Portugal)

Structural adaptations in retail will be accordingly deep amp fast there

But not all structural change in retail is economy-led Further drivers are demographic trends and channel development

X Key Trends ndash Economic Development 1

6

GDP Real Growth 2005-2015 ()

Source IMF

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Advanced economies Emerging and developing economies

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

7

GDP Real Growth 2005-2015 ()

Source IMF

-5

-3

-1

1

3

5

7

9

11

13

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China India Brazil United States Euro area

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

8

Consumer Spending Real Growth 2000-2015 ()

Source IMF Planet Retail

-70

-20

30

80

130

180

230

280

2000 2002 2004 2006 2008 2010 2012 2014

Finland

Germany

Greece

UK

X Key Trends ndash Economic Development 1

The Olympic Games 2012 shouldnrsquot they have gone to Greece this year again

9

800

900

1000

1100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Greece

UK

Portugal

Germany

GDP Real Growth Index 2007-2015 (2007 = 100)

Source IMF Planet Retail

Real growth index shows how deep the Euro crisis really is

X Key Trends ndash Economic Development 1

10

79

7

46

3

60

6

39

3

46

1

36

6

36

8

36

2

29

8

26

5

74

6

69

9

65

0

48

3

46

6

45

2

43

6

42

1

38

7

29

9

77

5

98

8

80

9

64

8

48

4

49

6

50

2

52

2

49

3

34

1

0

20

40

60

80

100

120

Carrefour Schwarz Group Tesco Auchan Metro Group Edeka Aldi Rewe Group Leclerc ITM(Intermarcheacute)

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

EUROPE Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

1 Carrefour and 2 Schwarz Group (Lidl amp Kaufland) are swapping their places this year not least due to the divestment of discounter Dia

X Key Trends ndash Retail Evolution 2

11

29

05

97

7

68

9

46

3

51

7

50

7

43

5

45

1

41

4

48

7

34

83

10

70

80

5

69

9

69

0

62

6

58

1

57

2

51

8

51

1

49

42

12

98

10

87

98

8

83

7

89

0

86

1

71

4

67

7

59

2

0

50

100

150

200

250

300

350

400

450

500

Walmart Carrefour Tesco Schwarz Group Seven amp I Costco Auchan Aldi Casino Metro Group

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

WORLD Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

Globally Walmart continues to lead the pack followed by mostly European grocers

X Key Trends ndash Retail Evolution 2

12

0

10

20

30

40

50

60

70

80

90

100

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

Sale

s (

)

Global Top 10 Grocery Retailers by Channel 2006-2016 ()

The global lsquobig 3rsquo are seeing hypermarkets amp superstores declining as a contributor to total sales

Source Planet Retail

Walmart Carrefour Schwarz Group

Tesco Kroger Aldi AEON Ahold Walgreens Seven amp I

Other

Drugstores Pharmacies amp Perfumeries

Cash amp Carries and Wholesale Clubs

Convenience amp Forecourt Stores

Discount Stores

Supermarkets amp Neighbourhood Stores

Hypermarkets amp Superstores

X Key Trends ndash Retail Evolution 2

13

Small formats are on the rise as shoppers favour proximity convenience and smaller average basket sizes

1615

273 330

743

282 300

1729

294 356

826

321 335

1819

311 377

875

337 359

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Hypermarkets Cash amp Carry Drugstores Supermarkets Convenience Discounters

Reta

iler

Sale

s b

y C

hannel (U

SD

bn)

Global Sales by Channel 2010-2012 (USD bn)

2010

2011

2012

Source Planet Retail

X Key Trends ndash Retail Evolution 2

14

15

Ireland

United Kingdom

Portugal

Belgium

Switzerland

Denmark

Norway

Finland

Hungary

Small stores Convenience The lsquoSplendid Isolationrsquo ndash Convenience as a British-Irish phenomenon

1154

980

256

428

342

322

Greece 188

192

265

274

Note includes Western Central and Eastern Europe excludes markets with less than 1mn inhabitants

Source Planet Retail

Top 10 markets by total grocery market share of sales convenience amp forecourt stores in Europe 2011

X Big plans for small stores 3

16

European retailers focus on small store roll-outs Proximity shopping is the current battleground at the expense of the traditional trade channel

X Big plans for small stores 3

Ahold looking to ramp up small stores in Sweden and enter Germany

REWE testing small stores in Austria and Germany

17

Legislation

High street

vacancy

Infrastructure supplier base

Urbanisation

amp socio-demographics

Competition

especially discounters

Concept

expertise

Saturation

Continental Europe The picture is mixedhellip

X Big plans for small stores 3

18

French Casinorsquos Daily Monoprsquo is one of the convenience store chains pretty close to the foodservice sector

50-100 square metres

Approximately 400 products only

gt50 Daily Monoprsquo private labels

EUR7-8 for meal amp drink

The Paris Orly airport store provides 100 seats

X Big plans for small stores 3

19

Casinorsquos halal convenience store Halrsquoshop targets Muslims

X Big plans for small stores 3

Delhaize Grouprsquos Delta Maxi in Serbia

Niche conceptshellip hellipwithout beer

20

Discounters and convenience

Customers have learned private label quality does not have to be expensive

Small city-centre locations make shopping convenient

Limited assortment means pre-selection

X Big plans for small stores 3

ldquoSnacks to gordquo at German Edekarsquos Netto discount store

Convenience products from discounter Aldi Germany

21

Is there a future for hypermarkets

22

-40

-30

-20

-10

00

10

20

30

40

50

60

Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3

Walmart US

Metro Group Real

Sonae MC

Hypermarket Operators Like-for-like Growth 2008 ndash 2011 ()

Source Planet Retail

Is there a future for hypermarkets 4

23

Structural as well as socio-demographic changes tend to weaken the popularity of the traditional hypermarket format

Why drive 20 minutes to a hypermarket when shoppers can find a neighbourhood store next door Rising petrol prices benefit convenience

stores such as Casinorsquos Petit Casino

Expansion of both discount and convenience stores

Expansion of specialist stores

Rising costs of car ownership

Ageing population increasing number of single-person households

Government restrictions on new store openings

More of the weekly shop migrates online ()

Low-income households tend to shop for small quantities especially in developing markets

Is there a future for hypermarkets 4

24

Going small Compact stores offer numerous benefits for the retailer as well as for the shopper

Higher flexibility smaller catchment areas

Is there a future for hypermarkets 4

25

Polarisation Trading up ndash or trading down

Self-discount

department with loose

goods at Auchan in

France

hellipand at Auchanrsquos

Jumbo hypermarkets in

Portugal

Carrefour Planet

in France

Is there a future for hypermarkets 4

26

27

gtgtThe lsquotwo nationsrsquo phenomenon is also seen in the alcohol market with premium brands increasing in popularity The

UKs top five lsquoworld beerrsquo brands ndash San Miguel Peroni Tuborg Cobra and Tiger ndash have seen sales rise by 201 in the past year 2011 despite total lager volume sales falling

by 7ltlt

UK The Grocer

Polarisation in store formats

Polarisation in shopping behaviour

Polarisation in brands

Polarisation in private labels

Polarisation ndash Discounting ndash Private Label 5

28

Increasing importance of promotional pricing for branded beers

Polarisation ndash Discounting ndash Private Label 5

29

Discounters Lidl continues to promote the lowest price segment

Polarisation ndash Discounting ndash Private Label 5

30

hellipand competitor Netto (Edeka) goes even lower

Polarisation ndash Discounting ndash Private Label 5

31

hellipwhile Aldi seems undecided whether to give up on the category (Aldi Suumld) allow brands (Aldi Nord) exclusive brand agreements (USA) or develop premium private labels (UK) ldquoDiscounter Aldi Suumld in the UK has appointed Clarion Communications to handle its consumer public relations to promote its range of beers wines and spirits The agency has reportedly been tasked with conveying the quality and value for money proposition and plans to use endorsements awards and creative news generation to achieve this goalrdquo

Polarisation ndash Discounting ndash Private Label 5

32

Source Planet Retail Ltd - wwwplanetretailnet

Polarisation in Private Label Modern tiered strategy better serves the increasingly cherry-picking consumer

Value PL

Standard PL

Premium PL

Pri

ce

Quality

Value 20 PL

Standard PL

Premium PL

Super premium

Old value PL

Pri

ce

Quality

Polarisation ndash Discounting ndash Private Label 5

33

The global ranking of the Top 20 grocery retailers shows a diverse picture as private label shares rank from 15 to 93 in 2011

0 50 100 150 200 250 300

Safeway (USA)

ITM (Intermarcheacute)

Woolworths (AUS)

Metro Group

Costco

Rewe Group

Casino

CVS

Ahold

Edeka

Auchan

Seven amp I

Walgreens

AEON

Aldi

Kroger

Schwarz Group

Tesco

Carrefour

Walmart

Food Sales 2011e (USD bn)

Global Top 20 Grocery Retailers Food Sales 2011e (USD bn)

PL Food Sales

Non-PL Food Sales

e estimate Source Planet Retail

Schwarz Group

Aldi

Polarisation ndash Discounting ndash Private Label 5

34

Increasing importance of private label even in brand-driven categories

+++ January 2011

US-based drugstore

operator Walgreens

launches lsquoFlats

1901rsquo+++

+++ February 2011

US grocery operator

SuperValu launches

Buck Range Light

beer line +++

+++ June 2011

Delhaize Group

introduces limited-

edition premium

private label beer

lsquoSingle Hoprsquo in

Belgium +++

+++ Autumn 2011

US grocer Harris

Teeter introduces

Barrel Trolley

range +++

+++ August 2011

Japanese retailer

AEON introduces

Topvalu Barreal

Lager Beer +++

Polarisation ndash Discounting ndash Private Label 5

35

Zielpunktrsquos Mundl Beer in Austria ndash Tegutrsquos Josefs Kellerbier in Germany

Polarisation ndash Discounting ndash Private Label 5

36

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA

37

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA Plznr

38

Provenance amp Transparency Regional is the new sustainable Regionality gives brands a face

Polarisation ndash Discounting ndash Private Label 5

39

Shopper democracy amp customer engagement Private label allows retailers to directly liaise with shoppers ndash not only in-store but also online via social media

Polarisation ndash Discounting ndash Private Label 5

40

Even for economy lines ethical credentials are becoming a common feature

With its own factory Lidl has certified its best-selling economy product with the UTZ Fairtrade label ndash to sell it without a price premium

Competitors have followed suit within months

Polarisation ndash Discounting ndash Private Label 5

41

Vertical integration Retailers are investing in production facilities to gain independence of increasingly volatile commodity markets

Migros Coop CH Morrisons Lidl etc

Cutting out the middleman

Access to commodity markets

Expertise for annual range reviews

Control from farm to fork

Long-term planning

But Creates dependence

Polarisation ndash Discounting ndash Private Label 5

42

43

Europe continues to be divided economically

Small stores will continue to outperform larger stores globally not least due to polarisation

Polarisation store formats shopping behaviour (cherry-picking) brands private labels

Hypermarkets are on the rocky path from providing lsquoeverything for everyonersquo to becoming the lsquospecialist for everyonersquo

Rising fuel prices high flexibility of small formats the expansion of specialists a trend towards smaller families more single households and an ageing population and changing shopping habits benefit small stores online and necessitate compact hypermarkets

Summary 6

44

Shopper engagement and transparency will instil trust and loyalty among brand and private label shoppers alike But thanks to their general distribution function retailers are closer to consumers than manufacturers ndash not only in-store but also via social media

There are opportunities for additional investment in premium and niche private label ranges ndash even at discounters

Summary 6

United Kingdom

Greater London House

Hampstead Road

London

NW1 7EJ

United Kingdom

T +44 (0)207 728 5600

F +44 (0)207 728 4999

Germany

Dreieichstrasse 59

D-60594 Frankfurt am Main

Germany

T +49 (0) 69 96 21 75-6

F +49 (0) 69 96 21 75-70

Japan

co INSIGHT INC

Atami Plaza 1401

Kasuga-cho 16-45 Atami-shi

Shizuoka 413-0005

Japan

T +81 (0) 557 35 9102

F +81 (0) 557 35 9103

China

10-1-202

88 Tongxing Road

Qingdao 266034

China

T +86 (0)532 85981272

F +86 (0)532 85989372

USA

1450 American Lane

Suite 1400

Schaumburg

IL 60173

USA

Tel + (1) 224 698 2601

Fax + (1) 224 698 9230

twittercomPlanetRetail

facebookcomPlanetRetail

tinyurlcomPR-linkedin

Researched and published by Planet Retail Limited

Company No 3994702 (England amp Wales) - Registered Office 66 Wigmore Street London W1U 2SB

Terms of use and copyright conditions

This document is copyrighted All rights reserved and no part of this publication may be reproduced stored in a retrieval system or transmitted in any

form without the prior permission of the publishers We have taken every precaution to ensure that details provided in this document are accurate

The publishers are not liable for any omissions errors or incorrect insertions nor for any interpretations made from the document

A Service

Thank you

3

About Planet Retail

4

1 Economic Development

2 Retail Evolution

5

Europe continues to be divided economically

Positive outlook for countries benefiting from emerging markets growth and featuring stable domestic economy

Difficult outlook for countries struck by public and household debt crises (UK Ireland Spain Greece Portugal) with most problems coming from the inside Several countries will lose a full decade

Consumer confidence is key in countries with high dependence on domestic consumption (UK Portugal)

Structural adaptations in retail will be accordingly deep amp fast there

But not all structural change in retail is economy-led Further drivers are demographic trends and channel development

X Key Trends ndash Economic Development 1

6

GDP Real Growth 2005-2015 ()

Source IMF

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Advanced economies Emerging and developing economies

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

7

GDP Real Growth 2005-2015 ()

Source IMF

-5

-3

-1

1

3

5

7

9

11

13

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China India Brazil United States Euro area

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

8

Consumer Spending Real Growth 2000-2015 ()

Source IMF Planet Retail

-70

-20

30

80

130

180

230

280

2000 2002 2004 2006 2008 2010 2012 2014

Finland

Germany

Greece

UK

X Key Trends ndash Economic Development 1

The Olympic Games 2012 shouldnrsquot they have gone to Greece this year again

9

800

900

1000

1100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Greece

UK

Portugal

Germany

GDP Real Growth Index 2007-2015 (2007 = 100)

Source IMF Planet Retail

Real growth index shows how deep the Euro crisis really is

X Key Trends ndash Economic Development 1

10

79

7

46

3

60

6

39

3

46

1

36

6

36

8

36

2

29

8

26

5

74

6

69

9

65

0

48

3

46

6

45

2

43

6

42

1

38

7

29

9

77

5

98

8

80

9

64

8

48

4

49

6

50

2

52

2

49

3

34

1

0

20

40

60

80

100

120

Carrefour Schwarz Group Tesco Auchan Metro Group Edeka Aldi Rewe Group Leclerc ITM(Intermarcheacute)

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

EUROPE Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

1 Carrefour and 2 Schwarz Group (Lidl amp Kaufland) are swapping their places this year not least due to the divestment of discounter Dia

X Key Trends ndash Retail Evolution 2

11

29

05

97

7

68

9

46

3

51

7

50

7

43

5

45

1

41

4

48

7

34

83

10

70

80

5

69

9

69

0

62

6

58

1

57

2

51

8

51

1

49

42

12

98

10

87

98

8

83

7

89

0

86

1

71

4

67

7

59

2

0

50

100

150

200

250

300

350

400

450

500

Walmart Carrefour Tesco Schwarz Group Seven amp I Costco Auchan Aldi Casino Metro Group

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

WORLD Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

Globally Walmart continues to lead the pack followed by mostly European grocers

X Key Trends ndash Retail Evolution 2

12

0

10

20

30

40

50

60

70

80

90

100

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

Sale

s (

)

Global Top 10 Grocery Retailers by Channel 2006-2016 ()

The global lsquobig 3rsquo are seeing hypermarkets amp superstores declining as a contributor to total sales

Source Planet Retail

Walmart Carrefour Schwarz Group

Tesco Kroger Aldi AEON Ahold Walgreens Seven amp I

Other

Drugstores Pharmacies amp Perfumeries

Cash amp Carries and Wholesale Clubs

Convenience amp Forecourt Stores

Discount Stores

Supermarkets amp Neighbourhood Stores

Hypermarkets amp Superstores

X Key Trends ndash Retail Evolution 2

13

Small formats are on the rise as shoppers favour proximity convenience and smaller average basket sizes

1615

273 330

743

282 300

1729

294 356

826

321 335

1819

311 377

875

337 359

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Hypermarkets Cash amp Carry Drugstores Supermarkets Convenience Discounters

Reta

iler

Sale

s b

y C

hannel (U

SD

bn)

Global Sales by Channel 2010-2012 (USD bn)

2010

2011

2012

Source Planet Retail

X Key Trends ndash Retail Evolution 2

14

15

Ireland

United Kingdom

Portugal

Belgium

Switzerland

Denmark

Norway

Finland

Hungary

Small stores Convenience The lsquoSplendid Isolationrsquo ndash Convenience as a British-Irish phenomenon

1154

980

256

428

342

322

Greece 188

192

265

274

Note includes Western Central and Eastern Europe excludes markets with less than 1mn inhabitants

Source Planet Retail

Top 10 markets by total grocery market share of sales convenience amp forecourt stores in Europe 2011

X Big plans for small stores 3

16

European retailers focus on small store roll-outs Proximity shopping is the current battleground at the expense of the traditional trade channel

X Big plans for small stores 3

Ahold looking to ramp up small stores in Sweden and enter Germany

REWE testing small stores in Austria and Germany

17

Legislation

High street

vacancy

Infrastructure supplier base

Urbanisation

amp socio-demographics

Competition

especially discounters

Concept

expertise

Saturation

Continental Europe The picture is mixedhellip

X Big plans for small stores 3

18

French Casinorsquos Daily Monoprsquo is one of the convenience store chains pretty close to the foodservice sector

50-100 square metres

Approximately 400 products only

gt50 Daily Monoprsquo private labels

EUR7-8 for meal amp drink

The Paris Orly airport store provides 100 seats

X Big plans for small stores 3

19

Casinorsquos halal convenience store Halrsquoshop targets Muslims

X Big plans for small stores 3

Delhaize Grouprsquos Delta Maxi in Serbia

Niche conceptshellip hellipwithout beer

20

Discounters and convenience

Customers have learned private label quality does not have to be expensive

Small city-centre locations make shopping convenient

Limited assortment means pre-selection

X Big plans for small stores 3

ldquoSnacks to gordquo at German Edekarsquos Netto discount store

Convenience products from discounter Aldi Germany

21

Is there a future for hypermarkets

22

-40

-30

-20

-10

00

10

20

30

40

50

60

Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3

Walmart US

Metro Group Real

Sonae MC

Hypermarket Operators Like-for-like Growth 2008 ndash 2011 ()

Source Planet Retail

Is there a future for hypermarkets 4

23

Structural as well as socio-demographic changes tend to weaken the popularity of the traditional hypermarket format

Why drive 20 minutes to a hypermarket when shoppers can find a neighbourhood store next door Rising petrol prices benefit convenience

stores such as Casinorsquos Petit Casino

Expansion of both discount and convenience stores

Expansion of specialist stores

Rising costs of car ownership

Ageing population increasing number of single-person households

Government restrictions on new store openings

More of the weekly shop migrates online ()

Low-income households tend to shop for small quantities especially in developing markets

Is there a future for hypermarkets 4

24

Going small Compact stores offer numerous benefits for the retailer as well as for the shopper

Higher flexibility smaller catchment areas

Is there a future for hypermarkets 4

25

Polarisation Trading up ndash or trading down

Self-discount

department with loose

goods at Auchan in

France

hellipand at Auchanrsquos

Jumbo hypermarkets in

Portugal

Carrefour Planet

in France

Is there a future for hypermarkets 4

26

27

gtgtThe lsquotwo nationsrsquo phenomenon is also seen in the alcohol market with premium brands increasing in popularity The

UKs top five lsquoworld beerrsquo brands ndash San Miguel Peroni Tuborg Cobra and Tiger ndash have seen sales rise by 201 in the past year 2011 despite total lager volume sales falling

by 7ltlt

UK The Grocer

Polarisation in store formats

Polarisation in shopping behaviour

Polarisation in brands

Polarisation in private labels

Polarisation ndash Discounting ndash Private Label 5

28

Increasing importance of promotional pricing for branded beers

Polarisation ndash Discounting ndash Private Label 5

29

Discounters Lidl continues to promote the lowest price segment

Polarisation ndash Discounting ndash Private Label 5

30

hellipand competitor Netto (Edeka) goes even lower

Polarisation ndash Discounting ndash Private Label 5

31

hellipwhile Aldi seems undecided whether to give up on the category (Aldi Suumld) allow brands (Aldi Nord) exclusive brand agreements (USA) or develop premium private labels (UK) ldquoDiscounter Aldi Suumld in the UK has appointed Clarion Communications to handle its consumer public relations to promote its range of beers wines and spirits The agency has reportedly been tasked with conveying the quality and value for money proposition and plans to use endorsements awards and creative news generation to achieve this goalrdquo

Polarisation ndash Discounting ndash Private Label 5

32

Source Planet Retail Ltd - wwwplanetretailnet

Polarisation in Private Label Modern tiered strategy better serves the increasingly cherry-picking consumer

Value PL

Standard PL

Premium PL

Pri

ce

Quality

Value 20 PL

Standard PL

Premium PL

Super premium

Old value PL

Pri

ce

Quality

Polarisation ndash Discounting ndash Private Label 5

33

The global ranking of the Top 20 grocery retailers shows a diverse picture as private label shares rank from 15 to 93 in 2011

0 50 100 150 200 250 300

Safeway (USA)

ITM (Intermarcheacute)

Woolworths (AUS)

Metro Group

Costco

Rewe Group

Casino

CVS

Ahold

Edeka

Auchan

Seven amp I

Walgreens

AEON

Aldi

Kroger

Schwarz Group

Tesco

Carrefour

Walmart

Food Sales 2011e (USD bn)

Global Top 20 Grocery Retailers Food Sales 2011e (USD bn)

PL Food Sales

Non-PL Food Sales

e estimate Source Planet Retail

Schwarz Group

Aldi

Polarisation ndash Discounting ndash Private Label 5

34

Increasing importance of private label even in brand-driven categories

+++ January 2011

US-based drugstore

operator Walgreens

launches lsquoFlats

1901rsquo+++

+++ February 2011

US grocery operator

SuperValu launches

Buck Range Light

beer line +++

+++ June 2011

Delhaize Group

introduces limited-

edition premium

private label beer

lsquoSingle Hoprsquo in

Belgium +++

+++ Autumn 2011

US grocer Harris

Teeter introduces

Barrel Trolley

range +++

+++ August 2011

Japanese retailer

AEON introduces

Topvalu Barreal

Lager Beer +++

Polarisation ndash Discounting ndash Private Label 5

35

Zielpunktrsquos Mundl Beer in Austria ndash Tegutrsquos Josefs Kellerbier in Germany

Polarisation ndash Discounting ndash Private Label 5

36

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA

37

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA Plznr

38

Provenance amp Transparency Regional is the new sustainable Regionality gives brands a face

Polarisation ndash Discounting ndash Private Label 5

39

Shopper democracy amp customer engagement Private label allows retailers to directly liaise with shoppers ndash not only in-store but also online via social media

Polarisation ndash Discounting ndash Private Label 5

40

Even for economy lines ethical credentials are becoming a common feature

With its own factory Lidl has certified its best-selling economy product with the UTZ Fairtrade label ndash to sell it without a price premium

Competitors have followed suit within months

Polarisation ndash Discounting ndash Private Label 5

41

Vertical integration Retailers are investing in production facilities to gain independence of increasingly volatile commodity markets

Migros Coop CH Morrisons Lidl etc

Cutting out the middleman

Access to commodity markets

Expertise for annual range reviews

Control from farm to fork

Long-term planning

But Creates dependence

Polarisation ndash Discounting ndash Private Label 5

42

43

Europe continues to be divided economically

Small stores will continue to outperform larger stores globally not least due to polarisation

Polarisation store formats shopping behaviour (cherry-picking) brands private labels

Hypermarkets are on the rocky path from providing lsquoeverything for everyonersquo to becoming the lsquospecialist for everyonersquo

Rising fuel prices high flexibility of small formats the expansion of specialists a trend towards smaller families more single households and an ageing population and changing shopping habits benefit small stores online and necessitate compact hypermarkets

Summary 6

44

Shopper engagement and transparency will instil trust and loyalty among brand and private label shoppers alike But thanks to their general distribution function retailers are closer to consumers than manufacturers ndash not only in-store but also via social media

There are opportunities for additional investment in premium and niche private label ranges ndash even at discounters

Summary 6

United Kingdom

Greater London House

Hampstead Road

London

NW1 7EJ

United Kingdom

T +44 (0)207 728 5600

F +44 (0)207 728 4999

Germany

Dreieichstrasse 59

D-60594 Frankfurt am Main

Germany

T +49 (0) 69 96 21 75-6

F +49 (0) 69 96 21 75-70

Japan

co INSIGHT INC

Atami Plaza 1401

Kasuga-cho 16-45 Atami-shi

Shizuoka 413-0005

Japan

T +81 (0) 557 35 9102

F +81 (0) 557 35 9103

China

10-1-202

88 Tongxing Road

Qingdao 266034

China

T +86 (0)532 85981272

F +86 (0)532 85989372

USA

1450 American Lane

Suite 1400

Schaumburg

IL 60173

USA

Tel + (1) 224 698 2601

Fax + (1) 224 698 9230

twittercomPlanetRetail

facebookcomPlanetRetail

tinyurlcomPR-linkedin

Researched and published by Planet Retail Limited

Company No 3994702 (England amp Wales) - Registered Office 66 Wigmore Street London W1U 2SB

Terms of use and copyright conditions

This document is copyrighted All rights reserved and no part of this publication may be reproduced stored in a retrieval system or transmitted in any

form without the prior permission of the publishers We have taken every precaution to ensure that details provided in this document are accurate

The publishers are not liable for any omissions errors or incorrect insertions nor for any interpretations made from the document

A Service

Thank you

4

1 Economic Development

2 Retail Evolution

5

Europe continues to be divided economically

Positive outlook for countries benefiting from emerging markets growth and featuring stable domestic economy

Difficult outlook for countries struck by public and household debt crises (UK Ireland Spain Greece Portugal) with most problems coming from the inside Several countries will lose a full decade

Consumer confidence is key in countries with high dependence on domestic consumption (UK Portugal)

Structural adaptations in retail will be accordingly deep amp fast there

But not all structural change in retail is economy-led Further drivers are demographic trends and channel development

X Key Trends ndash Economic Development 1

6

GDP Real Growth 2005-2015 ()

Source IMF

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Advanced economies Emerging and developing economies

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

7

GDP Real Growth 2005-2015 ()

Source IMF

-5

-3

-1

1

3

5

7

9

11

13

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China India Brazil United States Euro area

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

8

Consumer Spending Real Growth 2000-2015 ()

Source IMF Planet Retail

-70

-20

30

80

130

180

230

280

2000 2002 2004 2006 2008 2010 2012 2014

Finland

Germany

Greece

UK

X Key Trends ndash Economic Development 1

The Olympic Games 2012 shouldnrsquot they have gone to Greece this year again

9

800

900

1000

1100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Greece

UK

Portugal

Germany

GDP Real Growth Index 2007-2015 (2007 = 100)

Source IMF Planet Retail

Real growth index shows how deep the Euro crisis really is

X Key Trends ndash Economic Development 1

10

79

7

46

3

60

6

39

3

46

1

36

6

36

8

36

2

29

8

26

5

74

6

69

9

65

0

48

3

46

6

45

2

43

6

42

1

38

7

29

9

77

5

98

8

80

9

64

8

48

4

49

6

50

2

52

2

49

3

34

1

0

20

40

60

80

100

120

Carrefour Schwarz Group Tesco Auchan Metro Group Edeka Aldi Rewe Group Leclerc ITM(Intermarcheacute)

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

EUROPE Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

1 Carrefour and 2 Schwarz Group (Lidl amp Kaufland) are swapping their places this year not least due to the divestment of discounter Dia

X Key Trends ndash Retail Evolution 2

11

29

05

97

7

68

9

46

3

51

7

50

7

43

5

45

1

41

4

48

7

34

83

10

70

80

5

69

9

69

0

62

6

58

1

57

2

51

8

51

1

49

42

12

98

10

87

98

8

83

7

89

0

86

1

71

4

67

7

59

2

0

50

100

150

200

250

300

350

400

450

500

Walmart Carrefour Tesco Schwarz Group Seven amp I Costco Auchan Aldi Casino Metro Group

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

WORLD Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

Globally Walmart continues to lead the pack followed by mostly European grocers

X Key Trends ndash Retail Evolution 2

12

0

10

20

30

40

50

60

70

80

90

100

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

Sale

s (

)

Global Top 10 Grocery Retailers by Channel 2006-2016 ()

The global lsquobig 3rsquo are seeing hypermarkets amp superstores declining as a contributor to total sales

Source Planet Retail

Walmart Carrefour Schwarz Group

Tesco Kroger Aldi AEON Ahold Walgreens Seven amp I

Other

Drugstores Pharmacies amp Perfumeries

Cash amp Carries and Wholesale Clubs

Convenience amp Forecourt Stores

Discount Stores

Supermarkets amp Neighbourhood Stores

Hypermarkets amp Superstores

X Key Trends ndash Retail Evolution 2

13

Small formats are on the rise as shoppers favour proximity convenience and smaller average basket sizes

1615

273 330

743

282 300

1729

294 356

826

321 335

1819

311 377

875

337 359

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Hypermarkets Cash amp Carry Drugstores Supermarkets Convenience Discounters

Reta

iler

Sale

s b

y C

hannel (U

SD

bn)

Global Sales by Channel 2010-2012 (USD bn)

2010

2011

2012

Source Planet Retail

X Key Trends ndash Retail Evolution 2

14

15

Ireland

United Kingdom

Portugal

Belgium

Switzerland

Denmark

Norway

Finland

Hungary

Small stores Convenience The lsquoSplendid Isolationrsquo ndash Convenience as a British-Irish phenomenon

1154

980

256

428

342

322

Greece 188

192

265

274

Note includes Western Central and Eastern Europe excludes markets with less than 1mn inhabitants

Source Planet Retail

Top 10 markets by total grocery market share of sales convenience amp forecourt stores in Europe 2011

X Big plans for small stores 3

16

European retailers focus on small store roll-outs Proximity shopping is the current battleground at the expense of the traditional trade channel

X Big plans for small stores 3

Ahold looking to ramp up small stores in Sweden and enter Germany

REWE testing small stores in Austria and Germany

17

Legislation

High street

vacancy

Infrastructure supplier base

Urbanisation

amp socio-demographics

Competition

especially discounters

Concept

expertise

Saturation

Continental Europe The picture is mixedhellip

X Big plans for small stores 3

18

French Casinorsquos Daily Monoprsquo is one of the convenience store chains pretty close to the foodservice sector

50-100 square metres

Approximately 400 products only

gt50 Daily Monoprsquo private labels

EUR7-8 for meal amp drink

The Paris Orly airport store provides 100 seats

X Big plans for small stores 3

19

Casinorsquos halal convenience store Halrsquoshop targets Muslims

X Big plans for small stores 3

Delhaize Grouprsquos Delta Maxi in Serbia

Niche conceptshellip hellipwithout beer

20

Discounters and convenience

Customers have learned private label quality does not have to be expensive

Small city-centre locations make shopping convenient

Limited assortment means pre-selection

X Big plans for small stores 3

ldquoSnacks to gordquo at German Edekarsquos Netto discount store

Convenience products from discounter Aldi Germany

21

Is there a future for hypermarkets

22

-40

-30

-20

-10

00

10

20

30

40

50

60

Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3

Walmart US

Metro Group Real

Sonae MC

Hypermarket Operators Like-for-like Growth 2008 ndash 2011 ()

Source Planet Retail

Is there a future for hypermarkets 4

23

Structural as well as socio-demographic changes tend to weaken the popularity of the traditional hypermarket format

Why drive 20 minutes to a hypermarket when shoppers can find a neighbourhood store next door Rising petrol prices benefit convenience

stores such as Casinorsquos Petit Casino

Expansion of both discount and convenience stores

Expansion of specialist stores

Rising costs of car ownership

Ageing population increasing number of single-person households

Government restrictions on new store openings

More of the weekly shop migrates online ()

Low-income households tend to shop for small quantities especially in developing markets

Is there a future for hypermarkets 4

24

Going small Compact stores offer numerous benefits for the retailer as well as for the shopper

Higher flexibility smaller catchment areas

Is there a future for hypermarkets 4

25

Polarisation Trading up ndash or trading down

Self-discount

department with loose

goods at Auchan in

France

hellipand at Auchanrsquos

Jumbo hypermarkets in

Portugal

Carrefour Planet

in France

Is there a future for hypermarkets 4

26

27

gtgtThe lsquotwo nationsrsquo phenomenon is also seen in the alcohol market with premium brands increasing in popularity The

UKs top five lsquoworld beerrsquo brands ndash San Miguel Peroni Tuborg Cobra and Tiger ndash have seen sales rise by 201 in the past year 2011 despite total lager volume sales falling

by 7ltlt

UK The Grocer

Polarisation in store formats

Polarisation in shopping behaviour

Polarisation in brands

Polarisation in private labels

Polarisation ndash Discounting ndash Private Label 5

28

Increasing importance of promotional pricing for branded beers

Polarisation ndash Discounting ndash Private Label 5

29

Discounters Lidl continues to promote the lowest price segment

Polarisation ndash Discounting ndash Private Label 5

30

hellipand competitor Netto (Edeka) goes even lower

Polarisation ndash Discounting ndash Private Label 5

31

hellipwhile Aldi seems undecided whether to give up on the category (Aldi Suumld) allow brands (Aldi Nord) exclusive brand agreements (USA) or develop premium private labels (UK) ldquoDiscounter Aldi Suumld in the UK has appointed Clarion Communications to handle its consumer public relations to promote its range of beers wines and spirits The agency has reportedly been tasked with conveying the quality and value for money proposition and plans to use endorsements awards and creative news generation to achieve this goalrdquo

Polarisation ndash Discounting ndash Private Label 5

32

Source Planet Retail Ltd - wwwplanetretailnet

Polarisation in Private Label Modern tiered strategy better serves the increasingly cherry-picking consumer

Value PL

Standard PL

Premium PL

Pri

ce

Quality

Value 20 PL

Standard PL

Premium PL

Super premium

Old value PL

Pri

ce

Quality

Polarisation ndash Discounting ndash Private Label 5

33

The global ranking of the Top 20 grocery retailers shows a diverse picture as private label shares rank from 15 to 93 in 2011

0 50 100 150 200 250 300

Safeway (USA)

ITM (Intermarcheacute)

Woolworths (AUS)

Metro Group

Costco

Rewe Group

Casino

CVS

Ahold

Edeka

Auchan

Seven amp I

Walgreens

AEON

Aldi

Kroger

Schwarz Group

Tesco

Carrefour

Walmart

Food Sales 2011e (USD bn)

Global Top 20 Grocery Retailers Food Sales 2011e (USD bn)

PL Food Sales

Non-PL Food Sales

e estimate Source Planet Retail

Schwarz Group

Aldi

Polarisation ndash Discounting ndash Private Label 5

34

Increasing importance of private label even in brand-driven categories

+++ January 2011

US-based drugstore

operator Walgreens

launches lsquoFlats

1901rsquo+++

+++ February 2011

US grocery operator

SuperValu launches

Buck Range Light

beer line +++

+++ June 2011

Delhaize Group

introduces limited-

edition premium

private label beer

lsquoSingle Hoprsquo in

Belgium +++

+++ Autumn 2011

US grocer Harris

Teeter introduces

Barrel Trolley

range +++

+++ August 2011

Japanese retailer

AEON introduces

Topvalu Barreal

Lager Beer +++

Polarisation ndash Discounting ndash Private Label 5

35

Zielpunktrsquos Mundl Beer in Austria ndash Tegutrsquos Josefs Kellerbier in Germany

Polarisation ndash Discounting ndash Private Label 5

36

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA

37

Polarisation ndash Discounting ndash Private Label 5

Aldirsquos Trader Joersquos

Tongue-in-cheek approach in the USA Plznr

38

Provenance amp Transparency Regional is the new sustainable Regionality gives brands a face

Polarisation ndash Discounting ndash Private Label 5

39

Shopper democracy amp customer engagement Private label allows retailers to directly liaise with shoppers ndash not only in-store but also online via social media

Polarisation ndash Discounting ndash Private Label 5

40

Even for economy lines ethical credentials are becoming a common feature

With its own factory Lidl has certified its best-selling economy product with the UTZ Fairtrade label ndash to sell it without a price premium

Competitors have followed suit within months

Polarisation ndash Discounting ndash Private Label 5

41

Vertical integration Retailers are investing in production facilities to gain independence of increasingly volatile commodity markets

Migros Coop CH Morrisons Lidl etc

Cutting out the middleman

Access to commodity markets

Expertise for annual range reviews

Control from farm to fork

Long-term planning

But Creates dependence

Polarisation ndash Discounting ndash Private Label 5

42

43

Europe continues to be divided economically

Small stores will continue to outperform larger stores globally not least due to polarisation

Polarisation store formats shopping behaviour (cherry-picking) brands private labels

Hypermarkets are on the rocky path from providing lsquoeverything for everyonersquo to becoming the lsquospecialist for everyonersquo

Rising fuel prices high flexibility of small formats the expansion of specialists a trend towards smaller families more single households and an ageing population and changing shopping habits benefit small stores online and necessitate compact hypermarkets

Summary 6

44

Shopper engagement and transparency will instil trust and loyalty among brand and private label shoppers alike But thanks to their general distribution function retailers are closer to consumers than manufacturers ndash not only in-store but also via social media

There are opportunities for additional investment in premium and niche private label ranges ndash even at discounters

Summary 6

United Kingdom

Greater London House

Hampstead Road

London

NW1 7EJ

United Kingdom

T +44 (0)207 728 5600

F +44 (0)207 728 4999

Germany

Dreieichstrasse 59

D-60594 Frankfurt am Main

Germany

T +49 (0) 69 96 21 75-6

F +49 (0) 69 96 21 75-70

Japan

co INSIGHT INC

Atami Plaza 1401

Kasuga-cho 16-45 Atami-shi

Shizuoka 413-0005

Japan

T +81 (0) 557 35 9102

F +81 (0) 557 35 9103

China

10-1-202

88 Tongxing Road

Qingdao 266034

China

T +86 (0)532 85981272

F +86 (0)532 85989372

USA

1450 American Lane

Suite 1400

Schaumburg

IL 60173

USA

Tel + (1) 224 698 2601

Fax + (1) 224 698 9230

twittercomPlanetRetail

facebookcomPlanetRetail

tinyurlcomPR-linkedin

Researched and published by Planet Retail Limited

Company No 3994702 (England amp Wales) - Registered Office 66 Wigmore Street London W1U 2SB

Terms of use and copyright conditions

This document is copyrighted All rights reserved and no part of this publication may be reproduced stored in a retrieval system or transmitted in any

form without the prior permission of the publishers We have taken every precaution to ensure that details provided in this document are accurate

The publishers are not liable for any omissions errors or incorrect insertions nor for any interpretations made from the document

A Service

Thank you

5

Europe continues to be divided economically

Positive outlook for countries benefiting from emerging markets growth and featuring stable domestic economy

Difficult outlook for countries struck by public and household debt crises (UK Ireland Spain Greece Portugal) with most problems coming from the inside Several countries will lose a full decade

Consumer confidence is key in countries with high dependence on domestic consumption (UK Portugal)

Structural adaptations in retail will be accordingly deep amp fast there

But not all structural change in retail is economy-led Further drivers are demographic trends and channel development

X Key Trends ndash Economic Development 1

6

GDP Real Growth 2005-2015 ()

Source IMF

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Advanced economies Emerging and developing economies

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

7

GDP Real Growth 2005-2015 ()

Source IMF

-5

-3

-1

1

3

5

7

9

11

13

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China India Brazil United States Euro area

World economy powered by emerging markets growth

X Key Trends ndash Economic Development 1

8

Consumer Spending Real Growth 2000-2015 ()

Source IMF Planet Retail

-70

-20

30

80

130

180

230

280

2000 2002 2004 2006 2008 2010 2012 2014

Finland

Germany

Greece

UK

X Key Trends ndash Economic Development 1

The Olympic Games 2012 shouldnrsquot they have gone to Greece this year again

9

800

900

1000

1100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Greece

UK

Portugal

Germany

GDP Real Growth Index 2007-2015 (2007 = 100)

Source IMF Planet Retail

Real growth index shows how deep the Euro crisis really is

X Key Trends ndash Economic Development 1

10

79

7

46

3

60

6

39

3

46

1

36

6

36

8

36

2

29

8

26

5

74

6

69

9

65

0

48

3

46

6

45

2

43

6

42

1

38

7

29

9

77

5

98

8

80

9

64

8

48

4

49

6

50

2

52

2

49

3

34

1

0

20

40

60

80

100

120

Carrefour Schwarz Group Tesco Auchan Metro Group Edeka Aldi Rewe Group Leclerc ITM(Intermarcheacute)

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

EUROPE Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

1 Carrefour and 2 Schwarz Group (Lidl amp Kaufland) are swapping their places this year not least due to the divestment of discounter Dia

X Key Trends ndash Retail Evolution 2

11

29

05

97

7

68

9

46

3

51

7

50

7

43

5

45

1

41

4

48

7

34

83

10

70

80

5

69

9

69

0

62

6

58

1

57

2

51

8

51

1

49

42

12

98

10

87

98

8

83

7

89

0

86

1

71

4

67

7

59

2

0

50

100

150

200

250

300

350

400

450

500

Walmart Carrefour Tesco Schwarz Group Seven amp I Costco Auchan Aldi Casino Metro Group

Ban

ner

Sal

es (

EUR

bn

)

2006

2011

2016

Note f - forecast sorted by 2011 ranking Source Planet Retail

WORLD Top 10 Grocers by Banner Sales 2006-2016f (EUR bn)

Globally Walmart continues to lead the pack followed by mostly European grocers

X Key Trends ndash Retail Evolution 2

12

0

10

20

30

40

50

60

70

80

90

100

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

2006

2011

2016

Sale

s (

)

Global Top 10 Grocery Retailers by Channel 2006-2016 ()