Economics ppt

33

Abhishek Mishra Bishwarup Mitra Vivek Rajan Sanket Kabra Sidharth VD Hiral Shah Automobile Industry

-

Upload

abhishek31m -

Category

Business

-

view

1.440 -

download

0

Transcript of Economics ppt

Abhishek MishraBishwarup Mitra

Vivek RajanSanket KabraSidharth VDHiral Shah

Automobile Industry

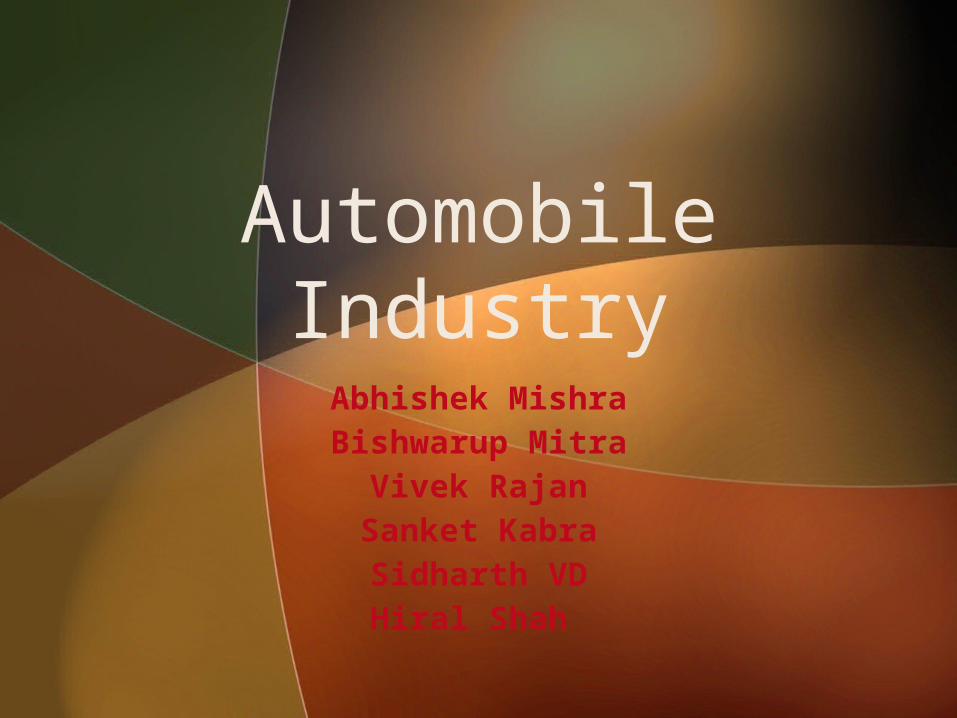

History of the automobile begins as early as 1769, with the creation of steam-powered automobiles capable of human transport In 1806.

The first cars powered by internal combustion engines running on fuel gas appeared, which led to the introduction in 1885 of the ubiquitous modern gasoline or petrol-fueled internal combustion engine.

The design of the Cugnot Steam Trolley (1769)

Automobile History in brief

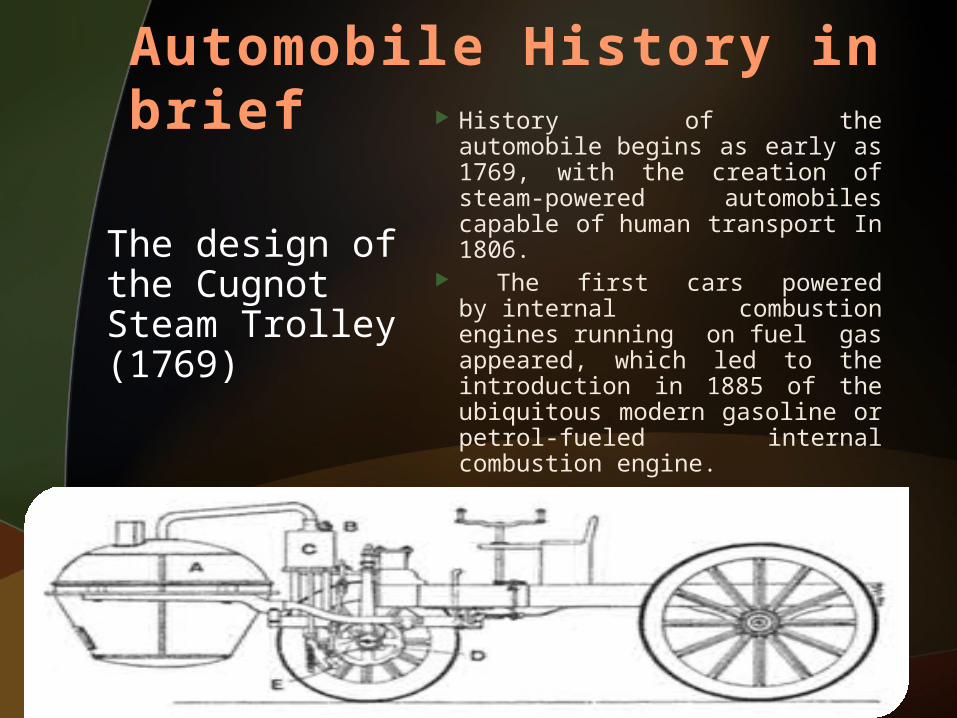

AUTOMOBILE

2 WHEELER 3 WHEELERPASSENGER

VEHICLECOMMERCIAL

VEHICLE

MOTORCYCLE SCOOTERS SCOOTERETTES MOPEDS

L.C.V. M.C.V. H.C.V.

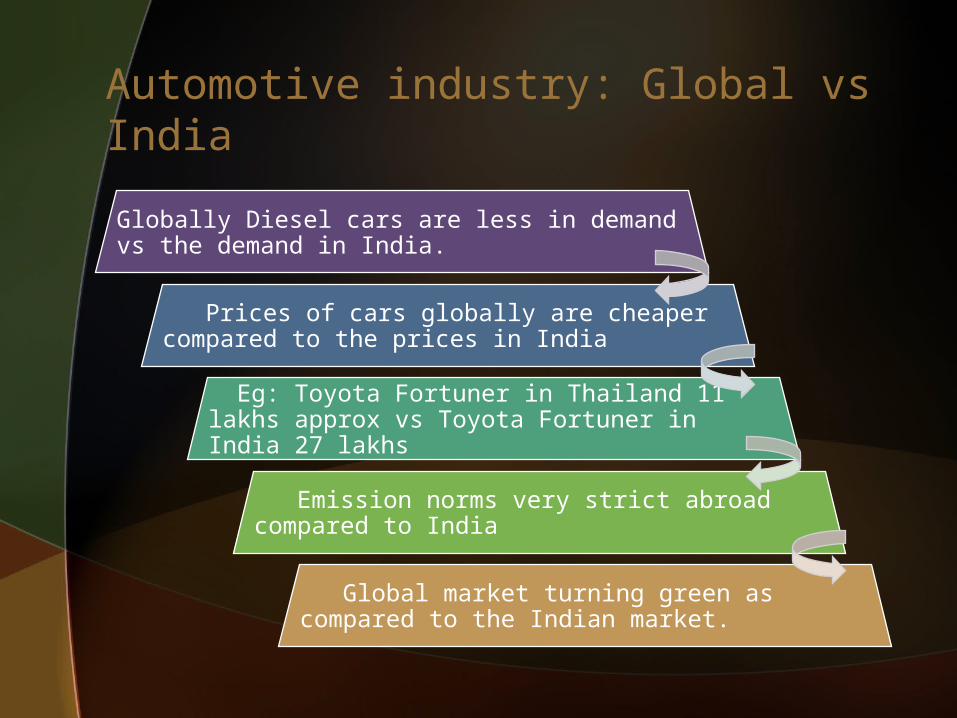

Globally Diesel cars are less in demand vs the demand in India.

Prices of cars globally are cheaper compared to the prices in India

Eg: Toyota Fortuner in Thailand 11 lakhs approx vs Toyota Fortuner in India 27 lakhs

Emission norms very strict abroad compared to India

Global market turning green as compared to the Indian market.

Automotive industry: Global vs India

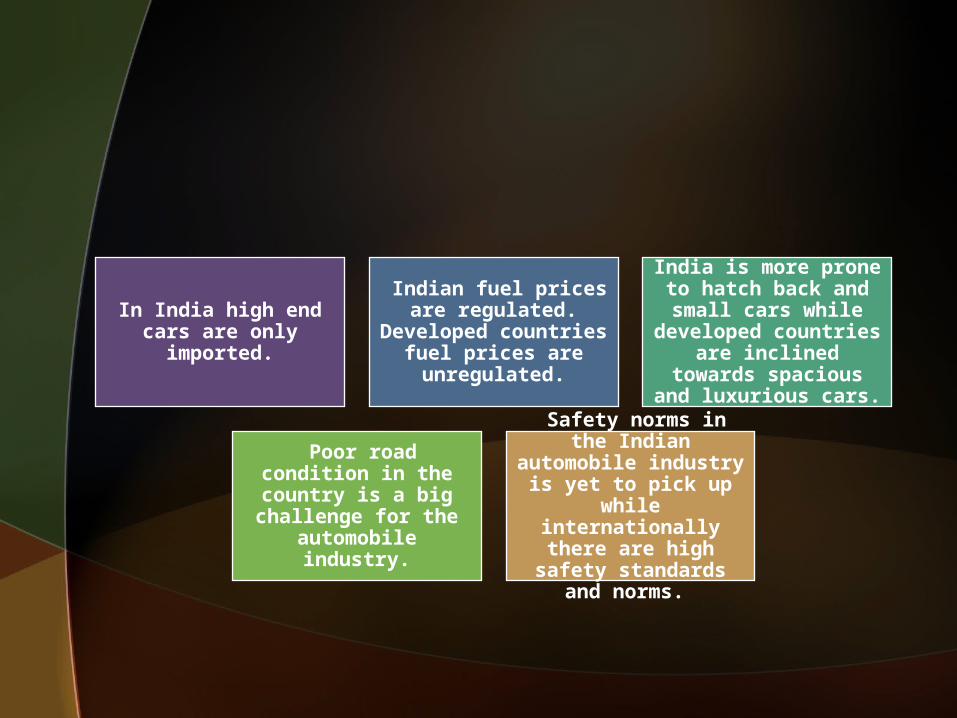

In India high end cars are only

imported.

Indian fuel prices are regulated.

Developed countries fuel prices are unregulated.

India is more prone to hatch back and small cars while

developed countries are inclined towards

spacious and luxurious cars.

Poor road condition in the country is a

big challenge for the automobile industry.

Safety norms in the Indian automobile industry is yet to

pick up while internationally there

are high safety standards and

norms.

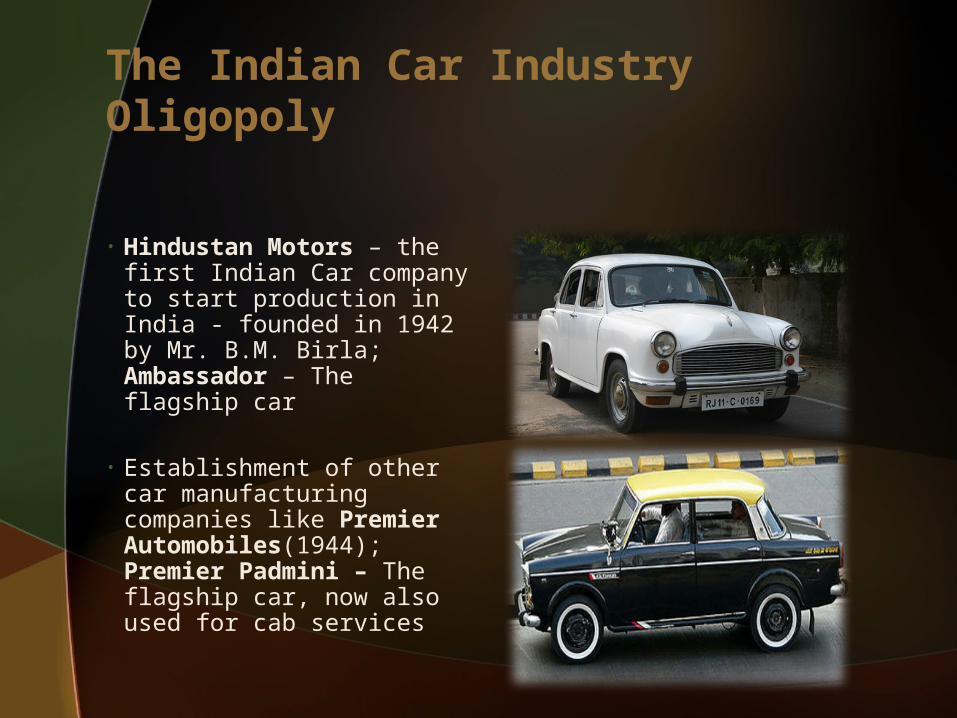

• Hindustan Motors – the first Indian Car company to start production in India - founded in 1942 by Mr. B.M. Birla; Ambassador – The flagship car

• Establishment of other car manufacturing companies like Premier Automobiles(1944); Premier Padmini – The flagship car, now also used for cab services

The Indian Car Industry Oligopoly

Growth very slow because of Low Demand and Low Economic Status of the country

Government restrictions provided no motivation or incentive for firms to do technological upgradation.

Supply was low and there weren’t many competitors

Impact on Consumers –Consumers did not have many choices; the Demand was fairly low as Cars were still a Luxury and availability of

same models

Impact of Oligopoly structure and License Raj

• Sanjay Gandhi owned Maruti Technical Services Limited which was liquidated

• After his death, Indira Gandhi government collaborated with Suzuki Motors, a Japanese firm, for collaboration – Formation of Maruti Udyog Limited and renamed later Maruti Suzuki in 2007

+ =

The Causes of Transformation – The First Big Step

• Policy changes introduced in 2 doses:1. Partial de-regulation in 1985 – eased

licensing requirements, allowed selective capacity-expansion, partial relaxation of controls with regard to foreign collaboration, imports.

However, trade and investment regulations continued, constraining growth of big business houses.

2. 1991 policy changes – Dispensed with bulk controls and regulations

• Partial de-regulation allowed technology inflow into India

The Causes of Transformation

• New Industrial Policy in July 1991 by Congress Government led by Mr. Narsimha Rao:

It introduced Liberalization policies – Abolishment of License Raj

• April 1993 – Government removed motor cars from list of industries reserved for compulsory licensing

The Causes of Transformation (contd..)

• New firms, including foreign players, entered with modern engineering, efficient processes and modern shop-floor layouts

• Indian automobile industry grew at 14.31% per annum in post-1991 era compared to 8.56% per annum during 1985-91

• Delicencing of sector attracted many major Global OEMs (GM, Ford, Honda, Hyundai etc.) to start assembly in India

Effects of the Transformation

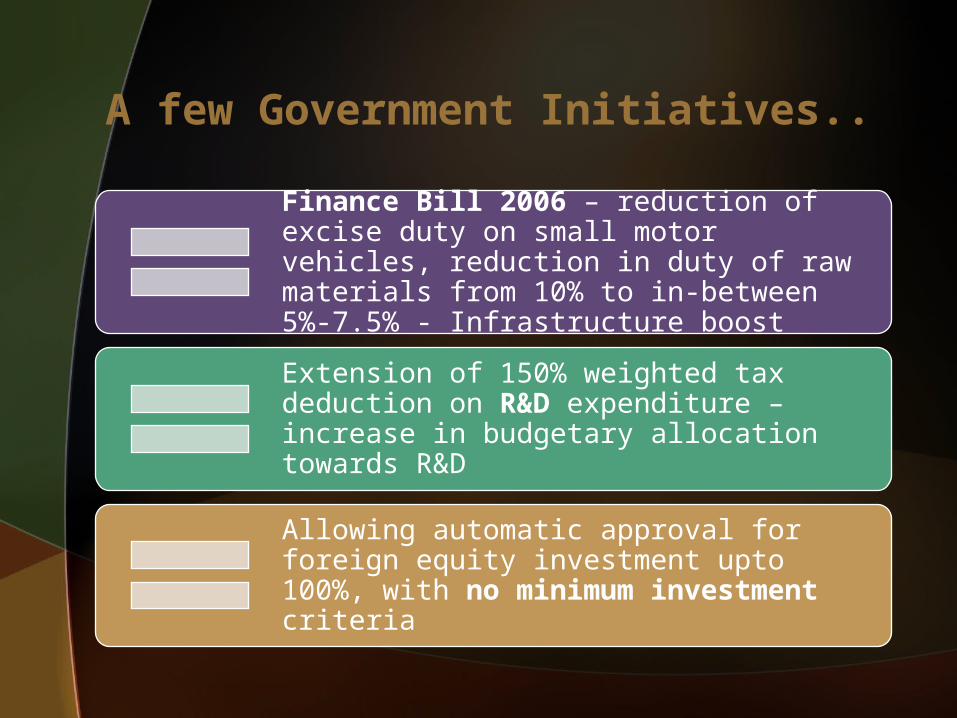

Finance Bill 2006 – reduction of excise duty on small motor vehicles, reduction in duty of raw materials from 10% to in-between 5%-7.5% - Infrastructure boost

Extension of 150% weighted tax deduction on R&D expenditure – increase in budgetary allocation towards R&D

Allowing automatic approval for foreign equity investment upto 100%, with no minimum investment criteria

A few Government Initiatives..

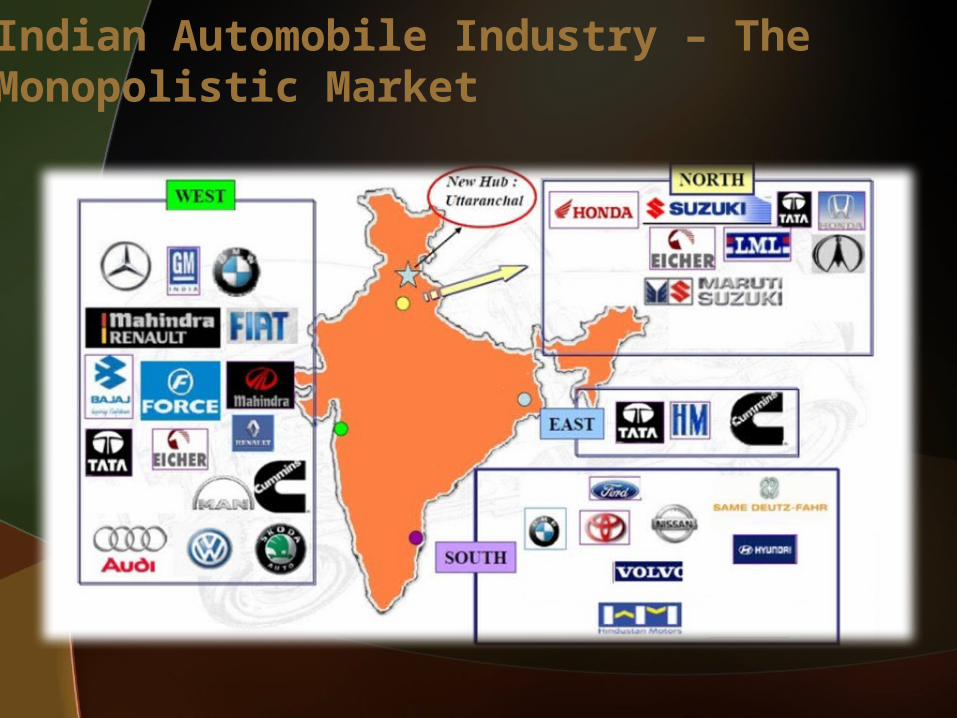

Indian Automobile Industry – The Monopolistic Market

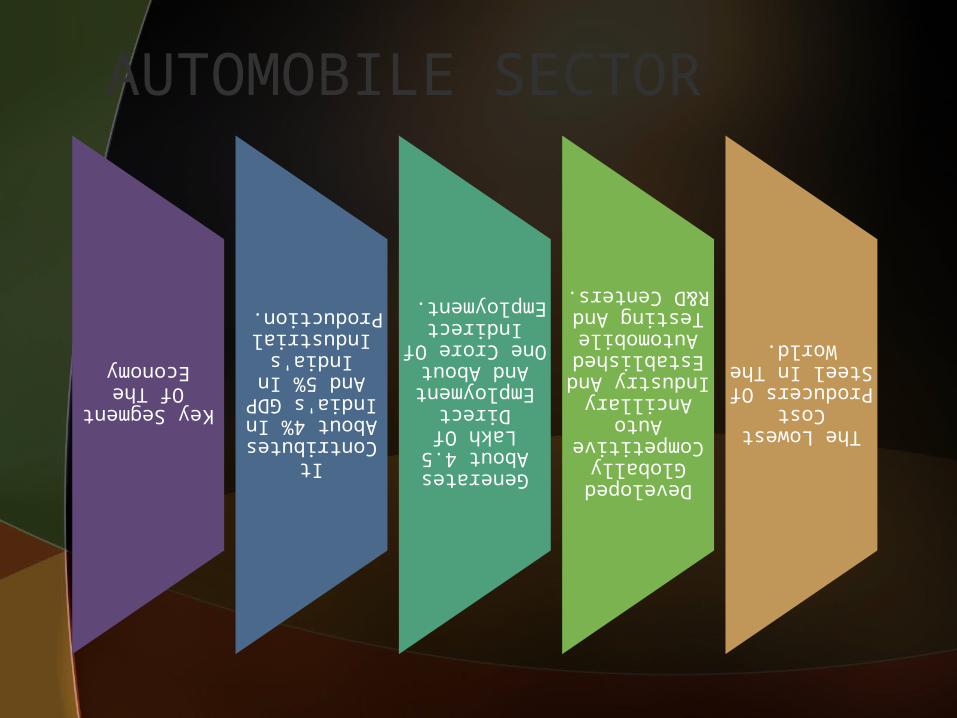

Key Segment Of The Economy It Contributes About 4% In India's GDP And 5% In India's Industrial Production.

Generates About 4.5 Lakh Of Direct Employment And About One Crore Of Indirect Employment.

Developed Globally Competitive Auto Ancillary Industry And Established Automobile Testing And

R&D Centers.The Lowest Cost Producers Of Steel In The World.

AUTOMOBILE SECTOR

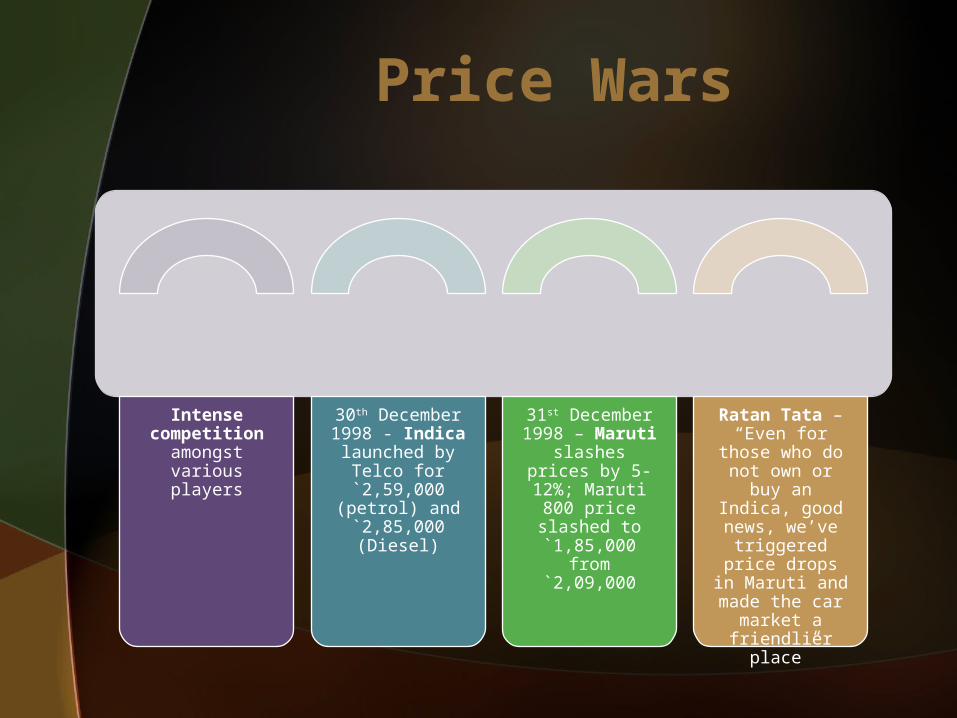

Intense competition

amongst various players

30th December 1998 - Indica

launched by Telco for `2,59,000 (petrol) and `2,85,000 (Diesel)

31st December 1998 – Maruti

slashes prices by 5-12%; Maruti

800 price slashed to `1,85,000 from

`2,09,000

Ratan Tata – “Even for those who do not own or buy an Indica, good news, we’ve

triggered price drops in Maruti

and made the car market a

friendlier place”

Price Wars

• Tata has come up with ` 1 Lakh car – Tata Nano

• This again has created price war

• Nissan-Renault to develop a $3000 car using India’s “frugal engineering expertise”

• Bajaj to experiment with the idea of a small car

Current Trends

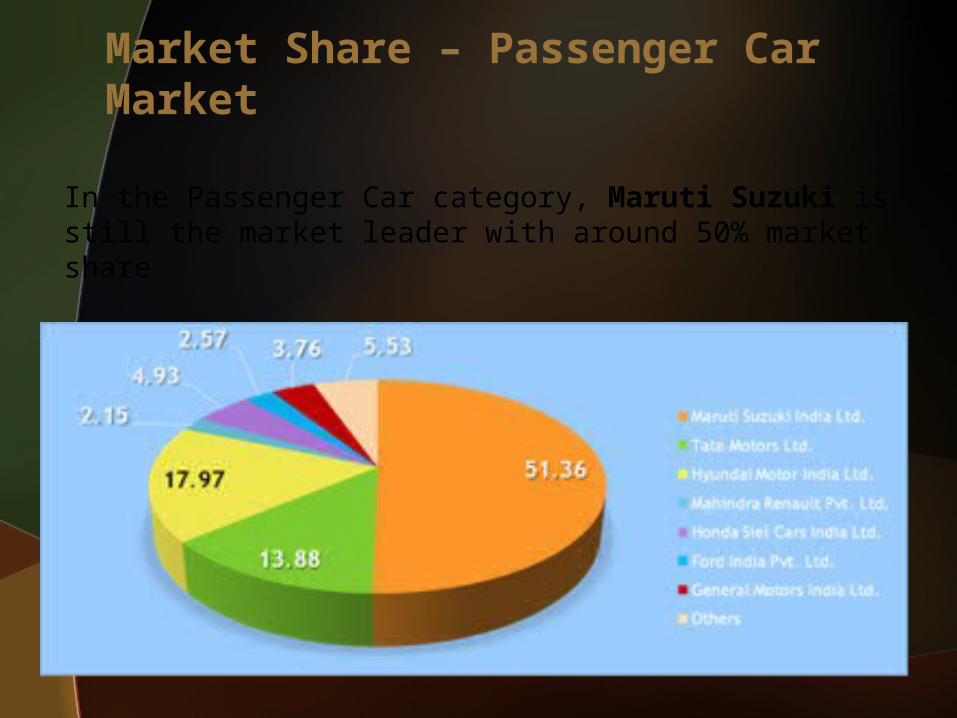

Market Share – Passenger Car Market

In the Passenger Car category, Maruti Suzuki is still the market leader with around 50% market share

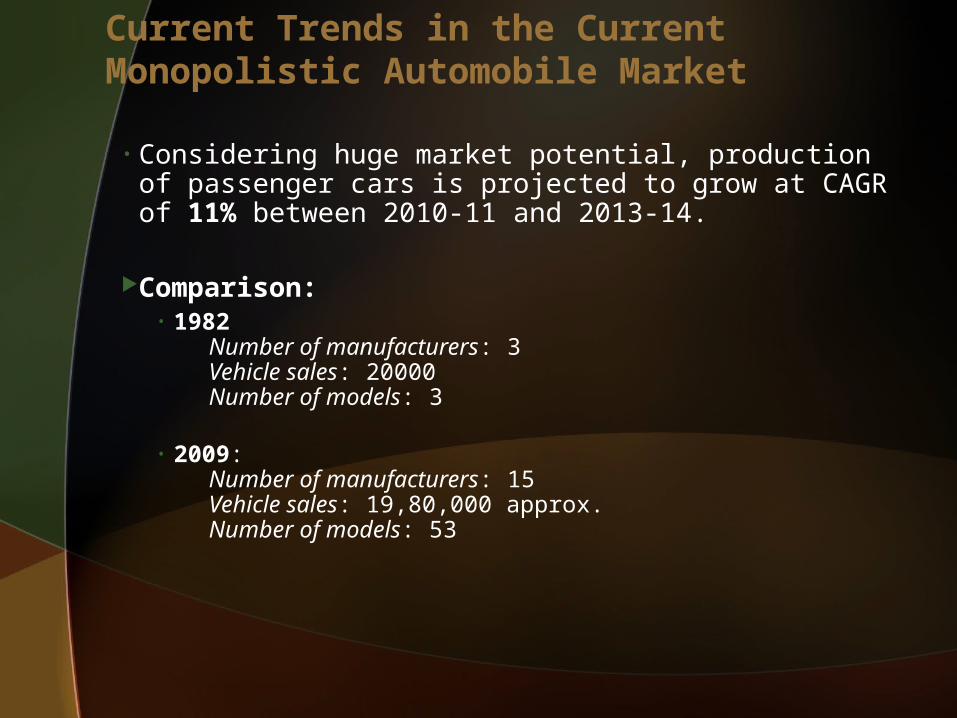

• Considering huge market potential, production of passenger cars is projected to grow at CAGR of 11% between 2010-11 and 2013-14.

Comparison:• 1982

Number of manufacturers: 3Vehicle sales: 20000Number of models: 3

• 2009:Number of manufacturers: 15Vehicle sales: 19,80,000 approx.Number of models: 53

Current Trends in the Current Monopolistic Automobile Market

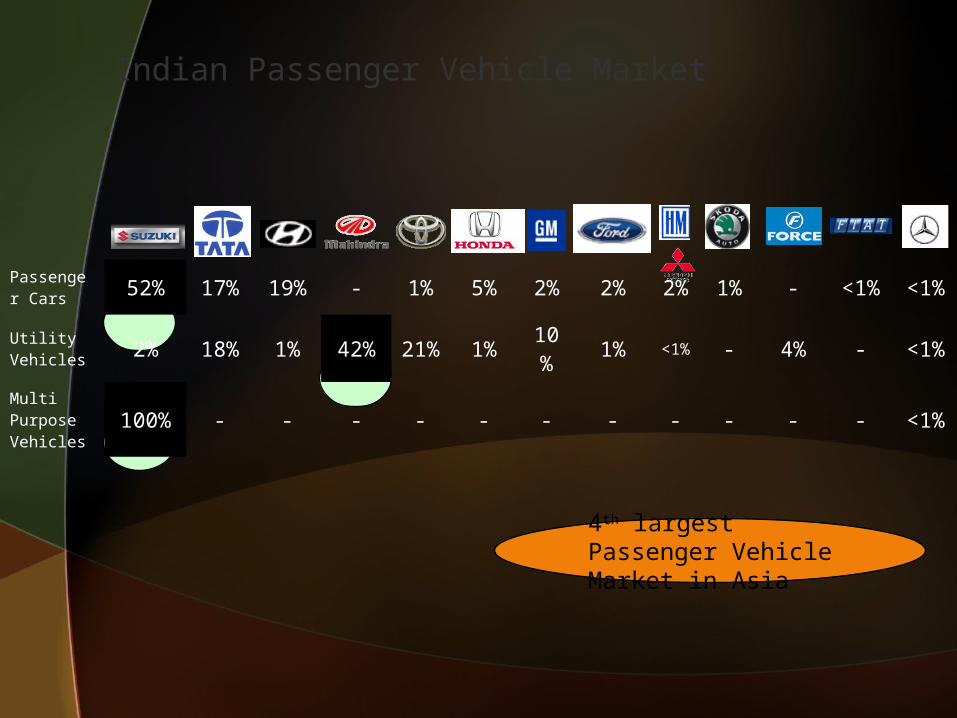

Passenger Cars 52% 17% 19% - 1% 5% 2% 2% 2

% 1% - <1%

<1%

Utility Vehicles 2% 18% 1% 42% 21

% 1% 10% 1% <1

% - 4% - <1%

Multi Purpose Vehicles

100% - - - - - - - - - - - <1%

Indian Passenger Vehicle Market

4th largest Passenger Vehicle Market in Asia

Petrol Vs Diesel

Diesel car or a Petrol car?

Important for consumers to know they're getting value for money when they buy a car.

Petrol car running cost is Rs.5/KM where as Diesel car running cost is Rs.2.5/Km.

Continued..

Less KM Run people prefer Petrol cars and for more KM Run people prefer Diesel cars.

Petrol car users= 1/ KM Run.

Business class prefer Diesel car more than Petrol Cars, Where as Service class prefer more petrol car than diesel car

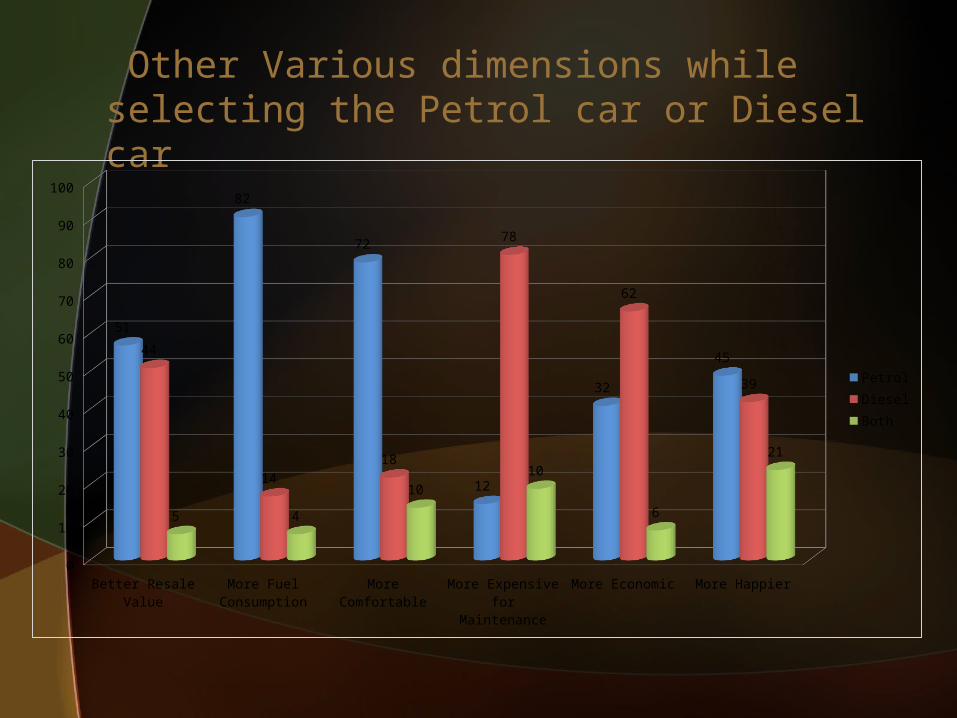

Other Various dimensions while selecting the Petrol car or Diesel car

Better

Resale

Value

More Fu

el Consu

mption

More Comforta

ble

More Ex

pensiv

e for M

ainten

ance

More Eco

nomic

More Hap

pier0

10

20

30

40

50

60

70

80

90

100

51

82

72

12

32

4544

1418

78

62

39

5 4

1010

6

21PetrolDieselBoth

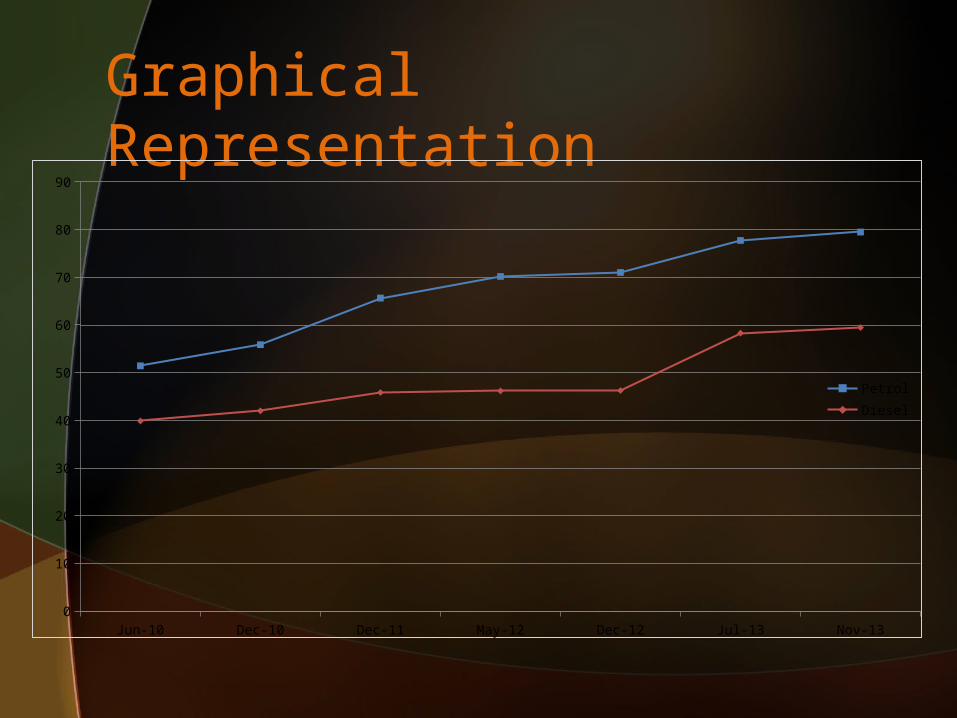

Price Fluctuations

Year Petrol Price Diesel Price

Jun-10 51.43 39.88

Dec-10 55.87 41.98

Dec-11 65.64 45.84

May-12 70.18 46.17

Dec-12 71.02 46.25

Jul-13 77.73 58.29

Nov-13 79.49 59.46

Graphical Representation

Jun-10 Dec-10 Dec-11 May-12 Dec-12 Jul-13 Nov-130

10

20

30

40

50

60

70

80

90

PetrolDiesel

Analysis

Customer like to go for Petrol vehicle for advantage of less maintenance cost and less Purchase price

Customer like to go for Diesel vehicle for getting the advantage of extra Mileage & better features

Customer buying a Diesel vehicle is not much bothered about the price of the vehicle

Customer buying Petrol vehicle is not much bothered about the mileage of the vehicle

Factors Influencing the Sales Rise Convergence of government policiesEconomy’s growthIncrease in People’s purchasing power.Pursuit of better lifestyleGrowth in the road infrastructure

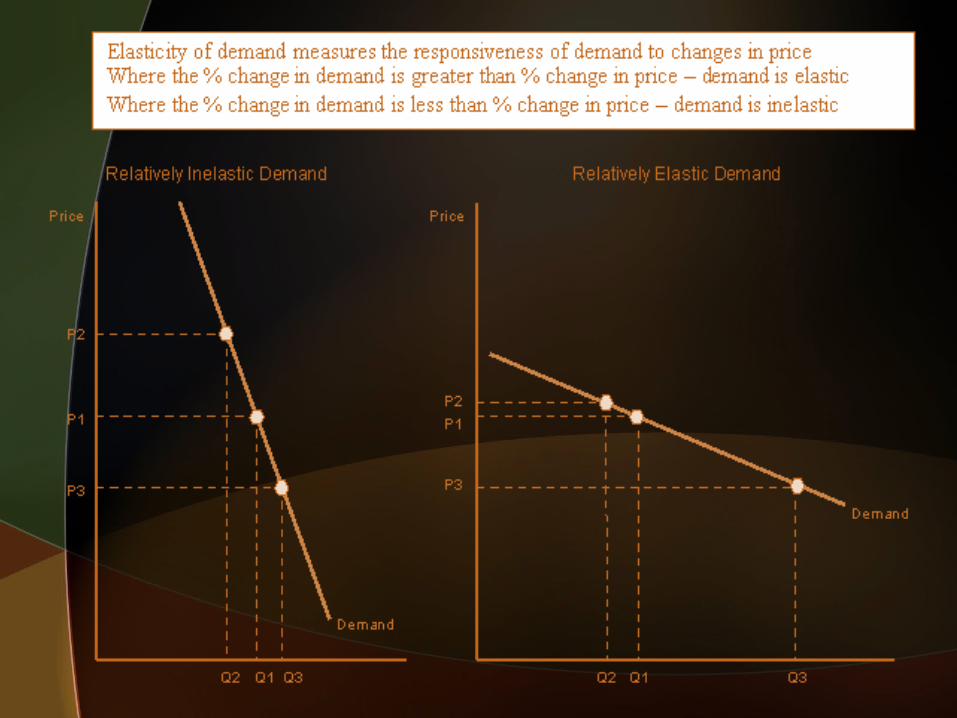

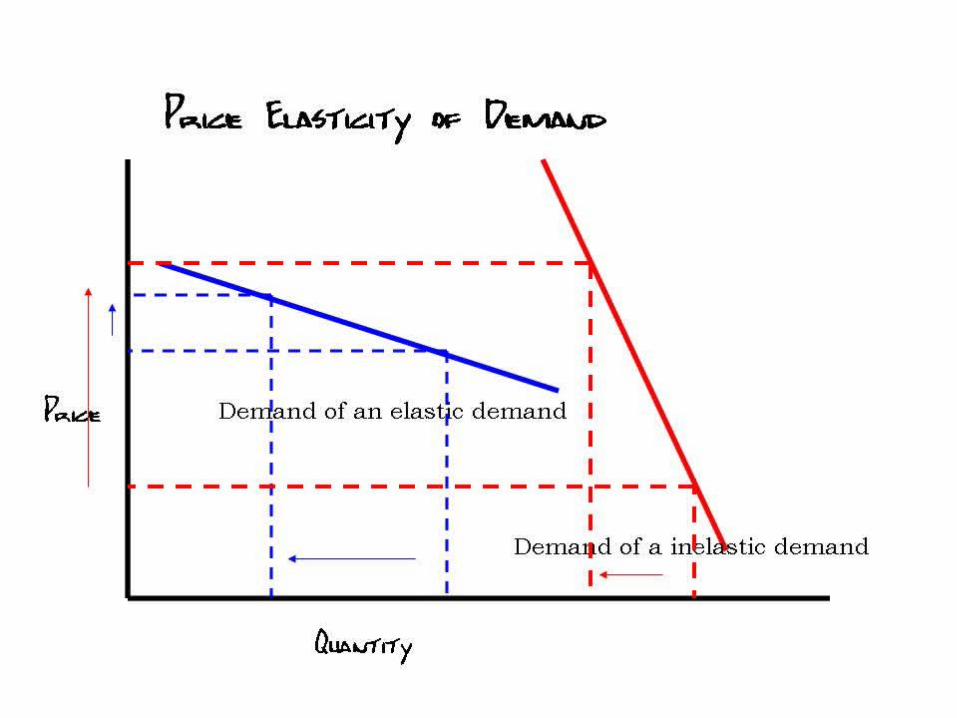

PRICE ELASTICITY OF DEMANDRelatively inelastic demand for

Mercedes car owner compared to a Maruti Suzuki car owner who will have a relatively elastic demand

when it comes to charging him for service .

This is because owner of mercedes wont mind in paying higher amount.

This effect explains that the automobile market in India is highly price sensitive when it comes to middle level segment cars.

The change in price of Honda Jazz from 7,25,000 to 6,10,000 in 2012 lead to substantial increase in quantity demanded for Jazz from 316 units in 2009 to 1209 units in 2012.

APPLICATION OF PED

The increase in price of Audi A6 in India from 50,25,000 to 51,90,000 in 2012 lead to very small decrease in quantity demanded for Audi A6 from 712 units in 2011 to 689 units in 2012.

This shows that consumers are very less price sensitive when it comes to luxury cars.

CRISIL Reports

http://auto.indiamart.com/

http://www.wikinvest.com

http://india-reports.in

http://wheelsunplugged.in/

http://en.wikipedia.org

References