ECONOMICS, MONEY MARKETS AND BANKING - Graduate School of Banking …€¦ · ·...

46

Lecture Materials TOPIC 4: THE FEDERAL RESERVE, THE TREASURY AND . . . US MONETARY POLICY ECONOMICS, MONEY MARKETS AND BANKING James M. Johannes Interim Associate Dean for Executive and Evening MBA Programs Aschenbrener Chair of Banking & Finance Graduate School of Banking-Prochnow Professor of Banking Director, Puelicher Center for Banking Education Director, Officer Education Program University of Wisconsin-Madison Madison, Wisconsin [email protected] 608-265-2323 August 2-5, 2016

Transcript of ECONOMICS, MONEY MARKETS AND BANKING - Graduate School of Banking …€¦ · ·...

Lecture Materials

TOPIC 4:

THE FEDERAL RESERVE, THE TREASURY AND . . . US MONETARY POLICY

ECONOMICS, MONEY MARKETS AND BANKING

James M. Johannes Interim Associate Dean for Executive and Evening MBA Programs

Aschenbrener Chair of Banking & Finance Graduate School of Banking-Prochnow Professor of Banking

Director, Puelicher Center for Banking Education Director, Officer Education Program

University of Wisconsin-Madison Madison, Wisconsin

[email protected] 608-265-2323

August 2-5, 2016

Topic 4:The Federal Reserve, the Treasury and…

Janet Yellen Jacob Lew

…US Monetary Policy

2

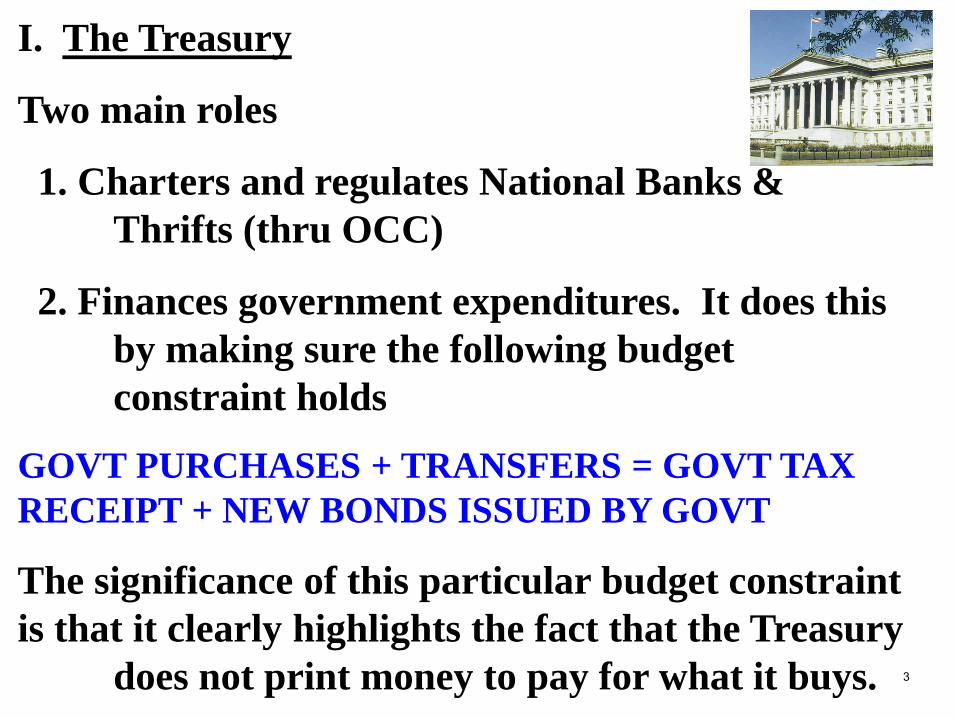

I. The Treasury

Two main roles

1. Charters and regulates National Banks &Thrifts (thru OCC)

2. Finances government expenditures. It does thisby making sure the following budget constraint holds

GOVT PURCHASES + TRANSFERS = GOVT TAX RECEIPT + NEW BONDS ISSUED BY GOVT

The significance of this particular budget constraint is that it clearly highlights the fact that the Treasury

does not print money to pay for what it buys. 3

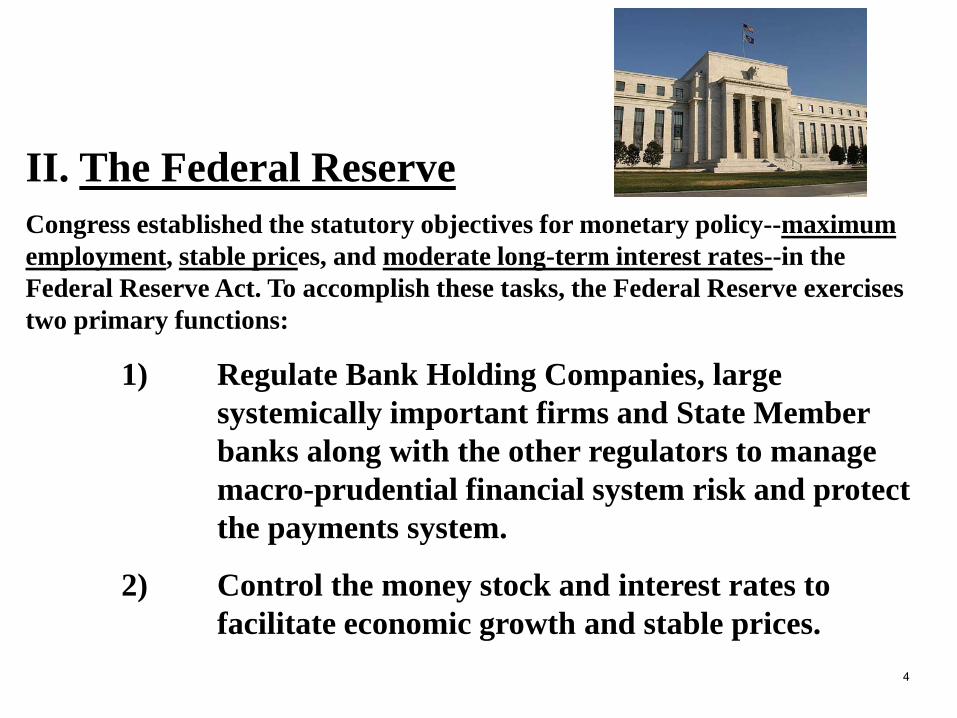

II. The Federal ReserveCongress established the statutory objectives for monetary policy--maximum employment, stable prices, and moderate long-term interest rates--in the Federal Reserve Act. To accomplish these tasks, the Federal Reserve exercises two primary functions:

1) Regulate Bank Holding Companies, largesystemically important firms and State Memberbanks along with the other regulators to managemacro-prudential financial system risk and protectthe payments system.

2) Control the money stock and interest rates tofacilitate economic growth and stable prices.

4

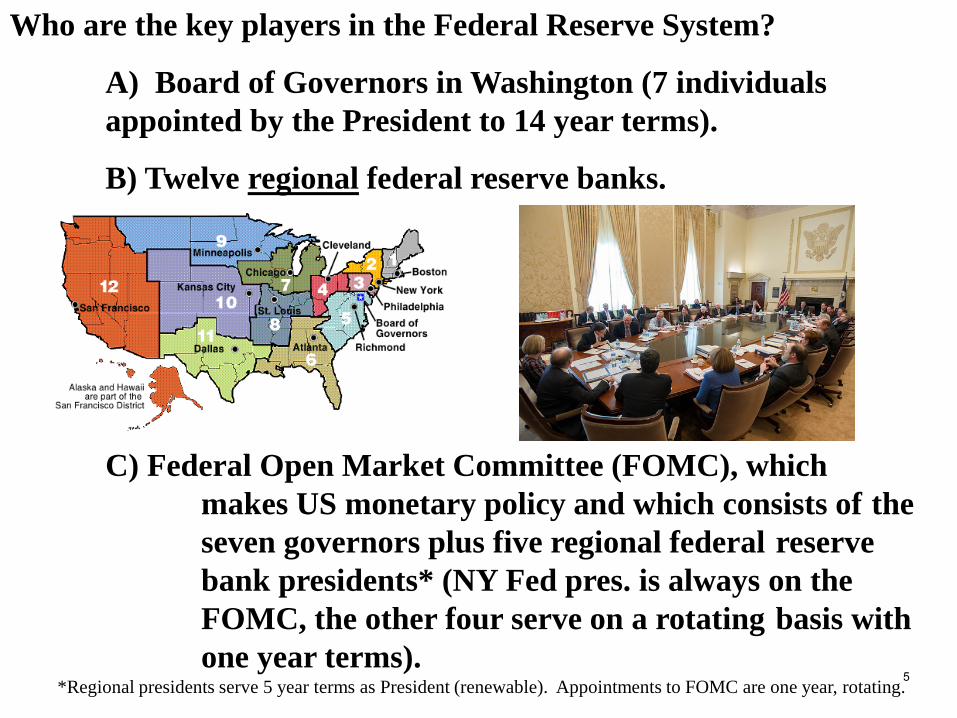

Who are the key players in the Federal Reserve System?

A) Board of Governors in Washington (7 individualsappointed by the President to 14 year terms).

B) Twelve regional federal reserve banks.

C) Federal Open Market Committee (FOMC), whichmakes US monetary policy and which consists of the seven governors plus five regional federal reserve bank presidents* (NY Fed pres. is always on the FOMC, the other four serve on a rotating basis with one year terms).

*Regional presidents serve 5 year terms as President (renewable). Appointments to FOMC are one year, rotating.5

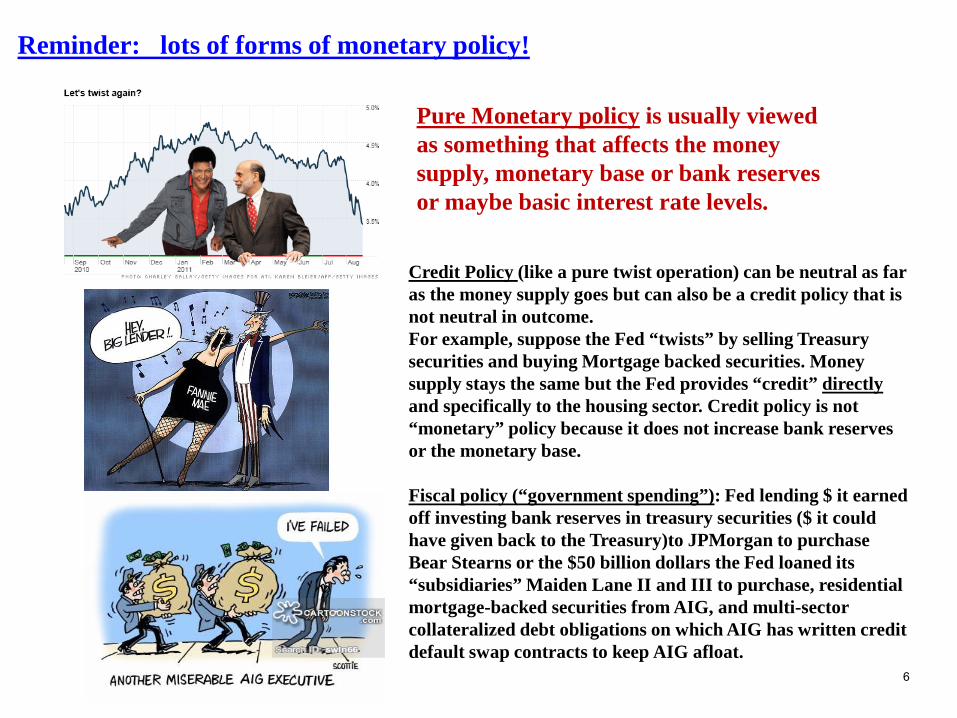

Credit Policy (like a pure twist operation) can be neutral as far as the money supply goes but can also be a credit policy that is not neutral in outcome. For example, suppose the Fed “twists” by selling Treasury securities and buying Mortgage backed securities. Money supply stays the same but the Fed provides “credit” directlyand specifically to the housing sector. Credit policy is not “monetary” policy because it does not increase bank reserves or the monetary base.

Fiscal policy (“government spending”): Fed lending $ it earned off investing bank reserves in treasury securities ($ it could have given back to the Treasury)to JPMorgan to purchase Bear Stearns or the $50 billion dollars the Fed loaned its “subsidiaries” Maiden Lane II and III to purchase, residential mortgage-backed securities from AIG, and multi-sector collateralized debt obligations on which AIG has written credit default swap contracts to keep AIG afloat.

Reminder: lots of forms of monetary policy!

Pure Monetary policy is usually viewed as something that affects the money supply, monetary base or bank reserves or maybe basic interest rate levels.

6

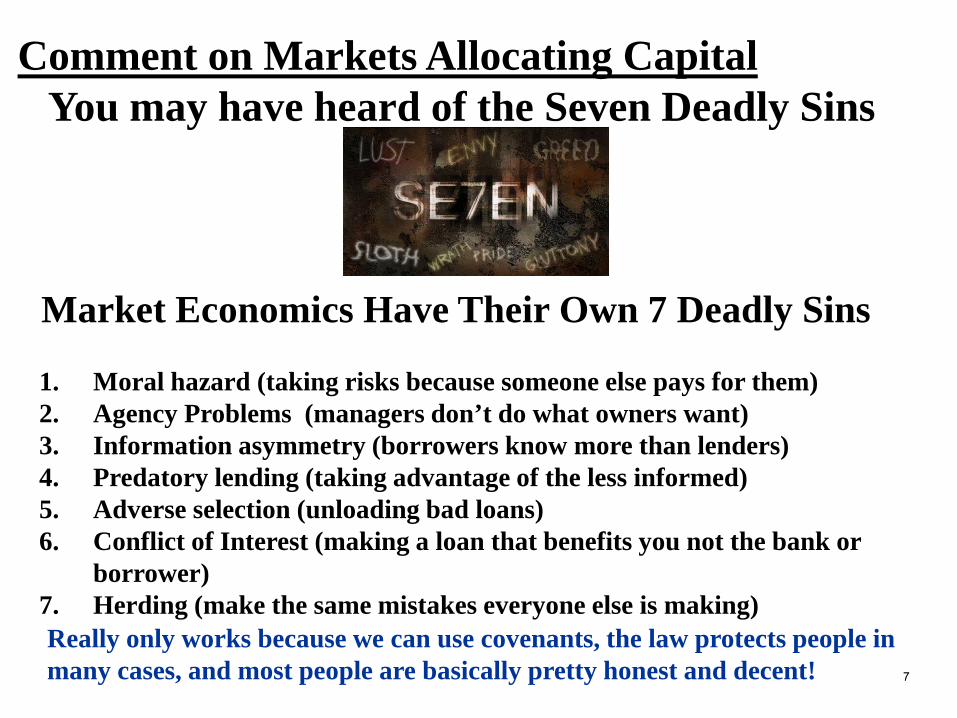

Comment on Markets Allocating CapitalYou may have heard of the Seven Deadly Sins

Market Economics Have Their Own 7 Deadly Sins

1. Moral hazard (taking risks because someone else pays for them)2. Agency Problems (managers don’t do what owners want)3. Information asymmetry (borrowers know more than lenders)4. Predatory lending (taking advantage of the less informed)5. Adverse selection (unloading bad loans)6. Conflict of Interest (making a loan that benefits you not the bank or

borrower)7. Herding (make the same mistakes everyone else is making)Really only works because we can use covenants, the law protects people inmany cases, and most people are basically pretty honest and decent! 7

III. Bank’s Role in Monetary Policy:Money Stock Determination

What is Money?Money is something that serves three

purposes1. medium of exchange2. standard of value (unit of account)3. store of value

8

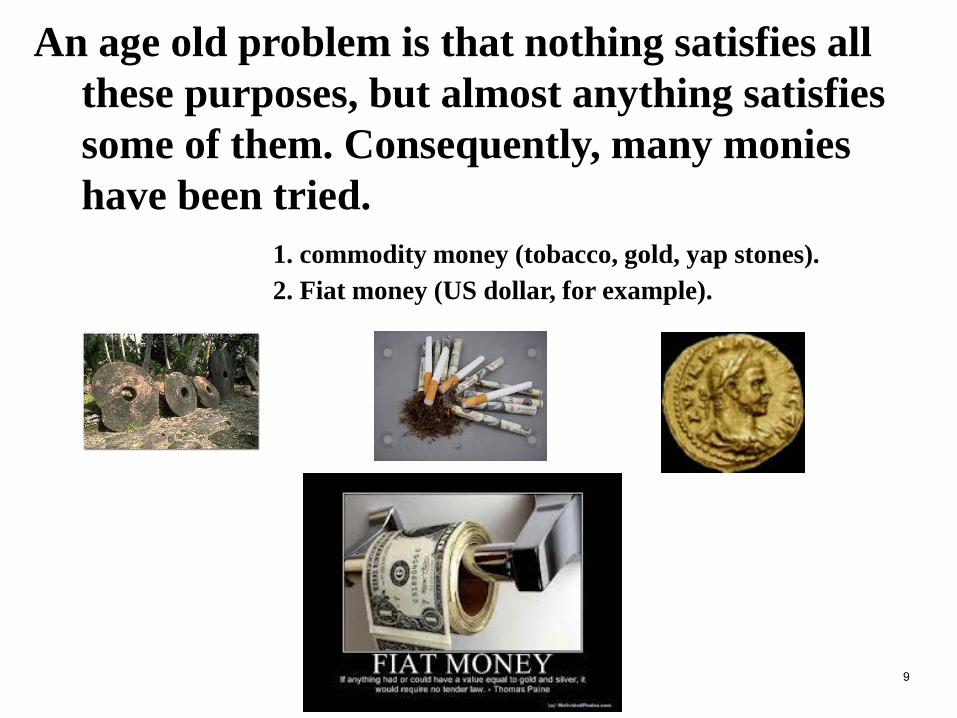

An age old problem is that nothing satisfies all these purposes, but almost anything satisfies some of them. Consequently, many monies have been tried.

1. commodity money (tobacco, gold, yap stones).2. Fiat money (US dollar, for example).

9

German Joachim’sthaler: thaleris a silver coin with same value asa gold coin

Spanish 8 Real Silver Coin=The Spanish version of theSilver Thaler, i.e. the Spanish Thaler.

“Thaler” became “Dollar”

Abbreviated as $ which became the symbol for US currency

10

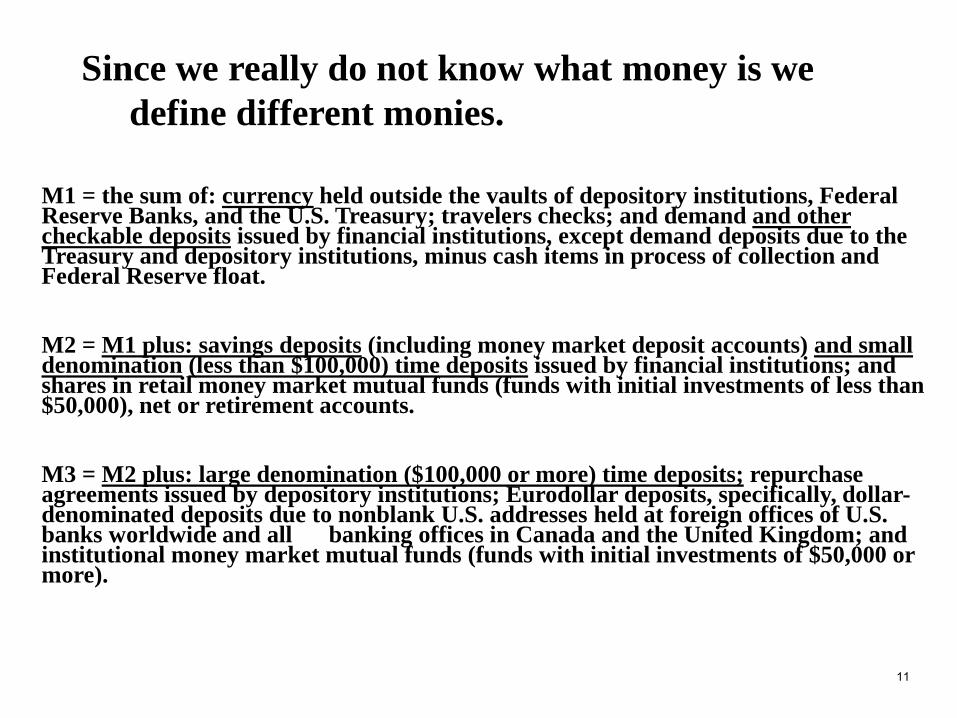

M1 = the sum of: currency held outside the vaults of depository institutions, Federal Reserve Banks, and the U.S. Treasury; travelers checks; and demand and other checkable deposits issued by financial institutions, except demand deposits due to the Treasury and depository institutions, minus cash items in process of collection and Federal Reserve float.

M2 = M1 plus: savings deposits (including money market deposit accounts) and small denomination (less than $100,000) time deposits issued by financial institutions; and shares in retail money market mutual funds (funds with initial investments of less than $50,000), net or retirement accounts.

M3 = M2 plus: large denomination ($100,000 or more) time deposits; repurchase agreements issued by depository institutions; Eurodollar deposits, specifically, dollar-denominated deposits due to nonblank U.S. addresses held at foreign offices of U.S. banks worldwide and all banking offices in Canada and the United Kingdom; and institutional money market mutual funds (funds with initial investments of $50,000 or more).

Since we really do not know what money is we define different monies.

11

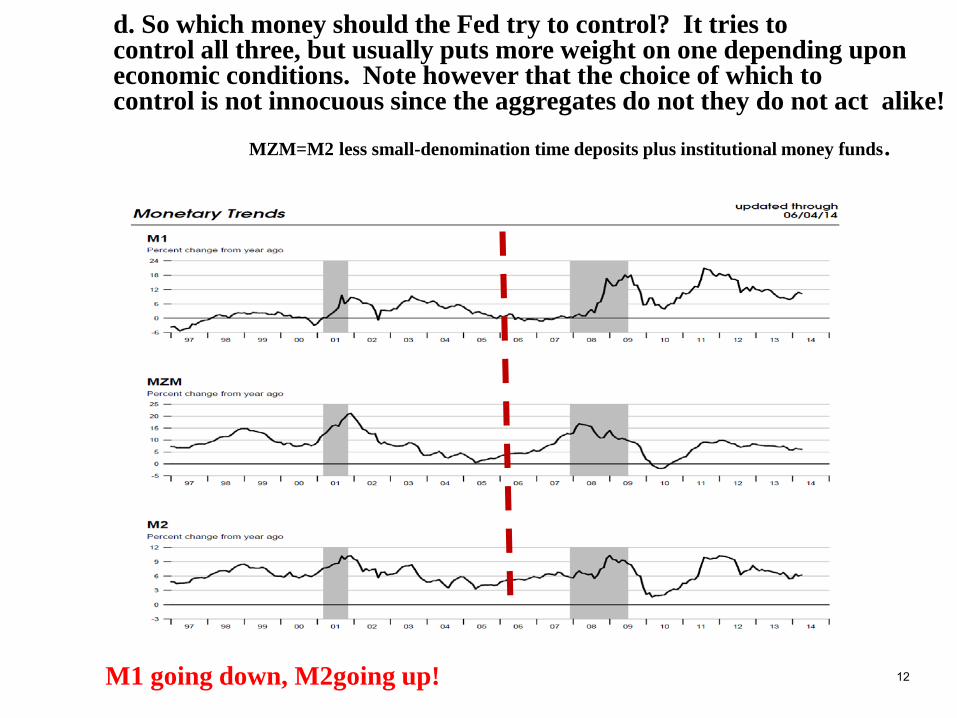

d. So which money should the Fed try to control? It tries to control all three, but usually puts more weight on one depending upon economic conditions. Note however that the choice of which to control is not innocuous since the aggregates do not they do not act alike!

MZM=M2 less small-denomination time deposits plus institutional money funds.

M1 going down, M2going up! 12

Most economists believe that the “best” definition of money is the one

A) most readily controlled by the Fed

B) that has the most stable and predictablerelationship to the thing the Fed ultimately wants to control-GDP, that is the money with the most stable and predictable VELOCITY.

Before 1982 M1 was the aggregate of choice. Since 1982 M2 is the preferred aggregate.

13

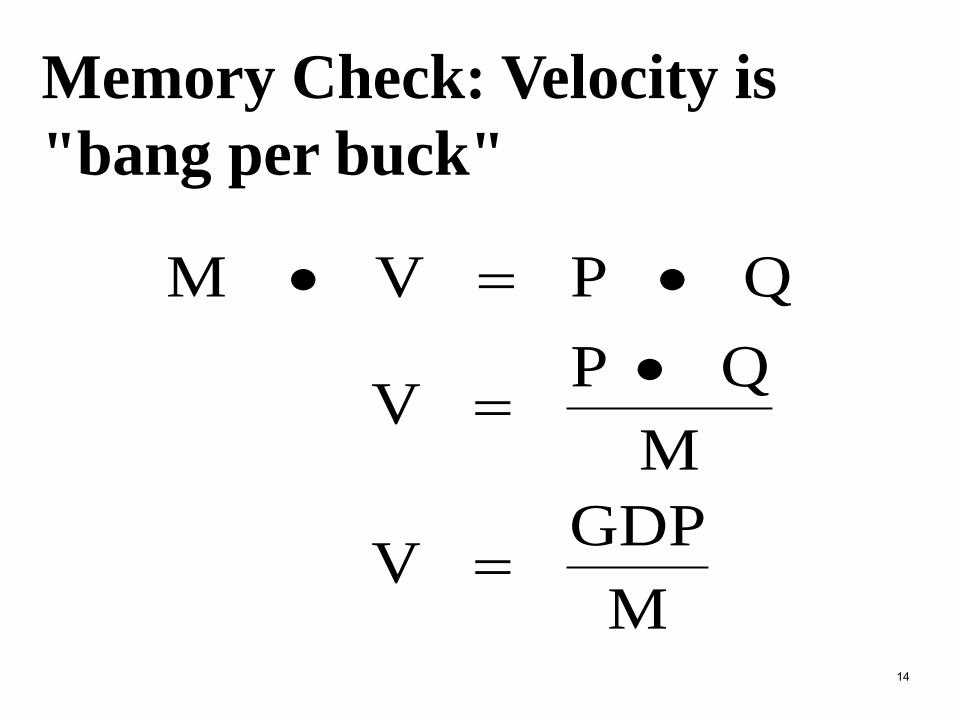

Memory Check: Velocity is "bang per buck"

MGDPV

MQPV

QPVM

=

•=

•=•

14

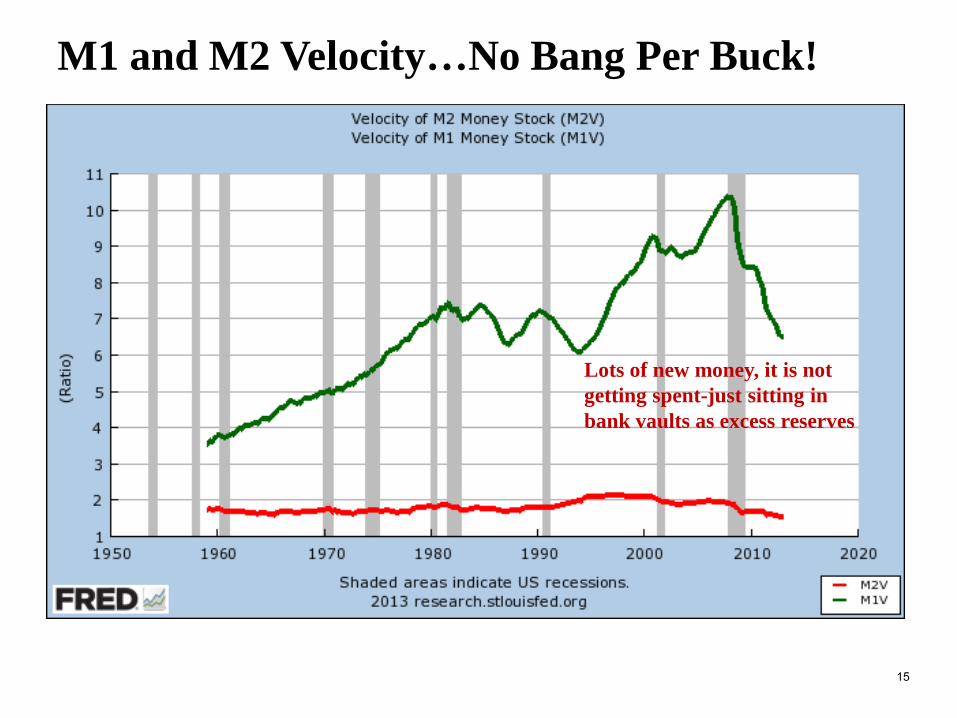

M1 and M2 Velocity…No Bang Per Buck!

Lots of new money, it is not getting spent-just sitting in bank vaults as excess reserves

15

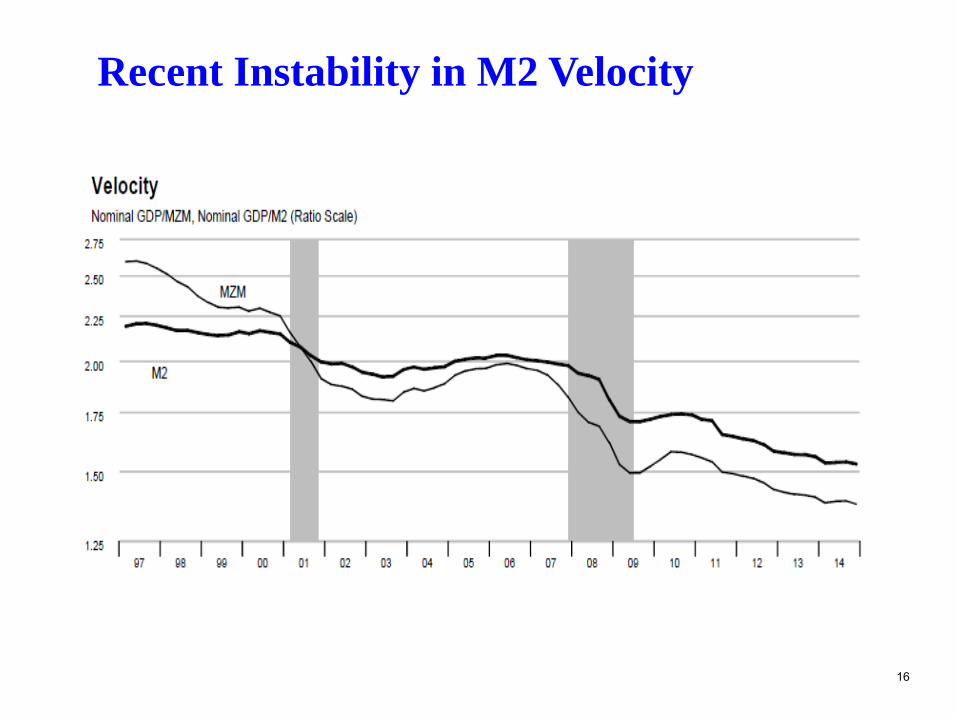

Recent Instability in M2 Velocity

16

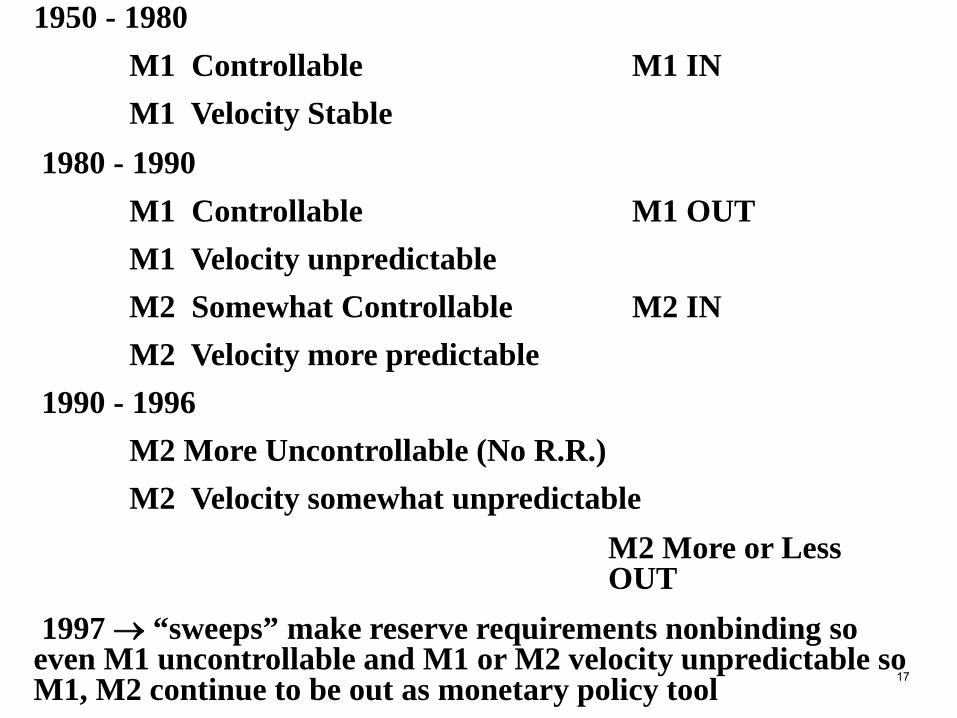

1950 - 1980M1 Controllable M1 INM1 Velocity Stable

1980 - 1990M1 Controllable M1 OUTM1 Velocity unpredictableM2 Somewhat Controllable M2 INM2 Velocity more predictable

1990 - 1996M2 More Uncontrollable (No R.R.)M2 Velocity somewhat unpredictable

M2 More or Less OUT

1997 → “sweeps” make reserve requirements nonbinding so even M1 uncontrollable and M1 or M2 velocity unpredictable so M1, M2 continue to be out as monetary policy tool 17

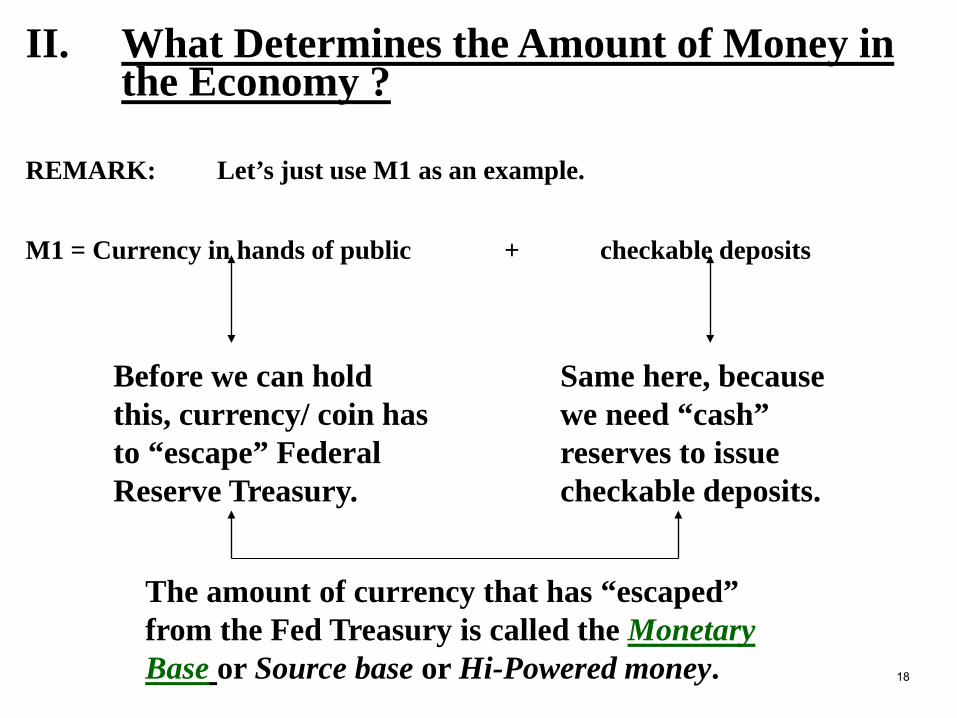

II. What Determines the Amount of Money in the Economy ?

REMARK: Let’s just use M1 as an example.

M1 = Currency in hands of public + checkable deposits

Before we can hold this, currency/ coin has to “escape” Federal Reserve Treasury.

Same here, because we need “cash” reserves to issue checkable deposits.

The amount of currency that has “escaped” from the Fed Treasury is called the Monetary Base or Source base or Hi-Powered money. 18

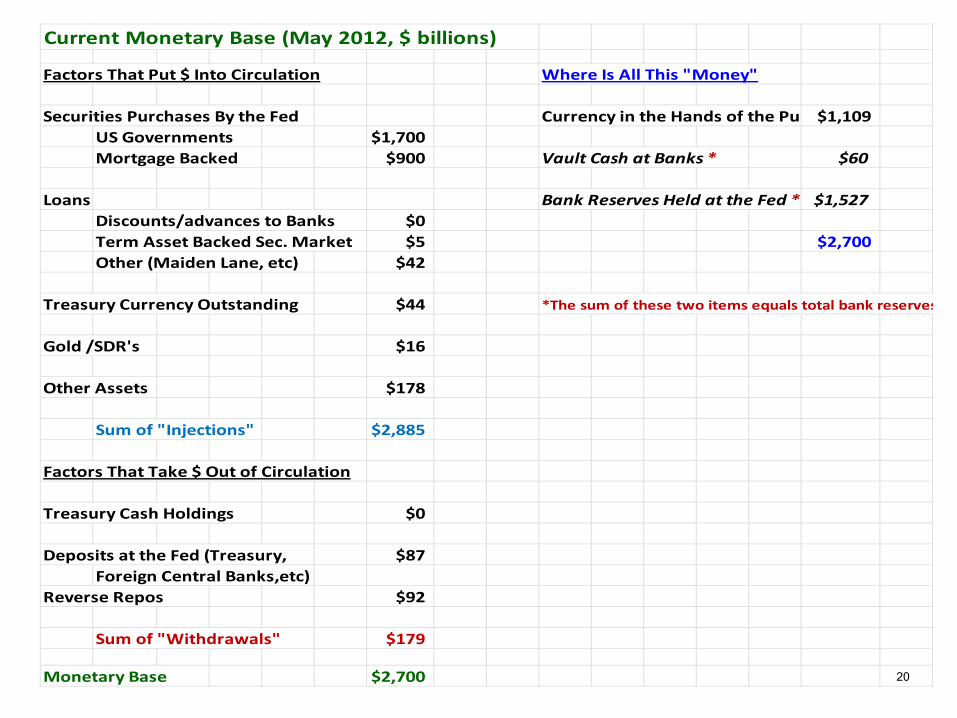

The Monetary Base Today

Highlights all the unusual Monetary policyactions lately

19

Current Monetary Base (May 2012, $ billions)

Factors That Put $ Into Circulation Where Is All This "Money"

Securities Purchases By the Fed Currency in the Hands of the Pu $1,109US Governments $1,700Mortgage Backed $900 Vault Cash at Banks * $60

Loans Bank Reserves Held at the Fed * $1,527Discounts/advances to Banks $0Term Asset Backed Sec. Market $5 $2,700Other (Maiden Lane, etc) $42

Treasury Currency Outstanding $44 *The sum of these two items equals total bank reserves

Gold /SDR's $16

Other Assets $178

Sum of "Injections" $2,885

Factors That Take $ Out of Circulation

Treasury Cash Holdings $0

Deposits at the Fed (Treasury, $87Foreign Central Banks,etc)

Reverse Repos $92

Sum of "Withdrawals" $179

Monetary Base $2,700 20

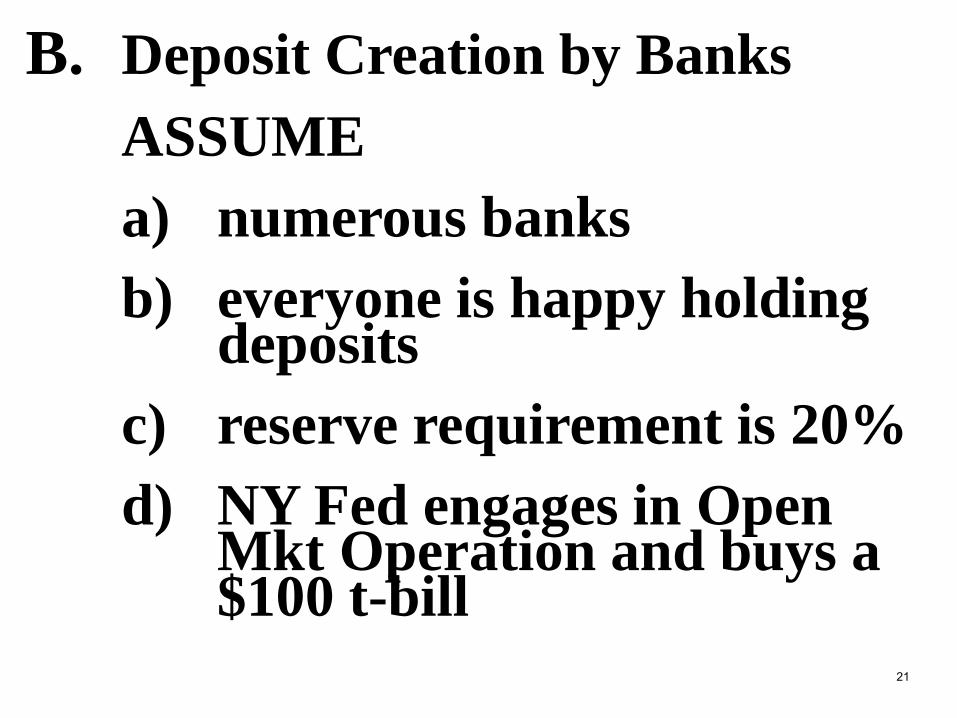

B. Deposit Creation by BanksASSUMEa) numerous banksb) everyone is happy holding

depositsc) reserve requirement is 20%d) NY Fed engages in Open

Mkt Operation and buys a $100 t-bill

21

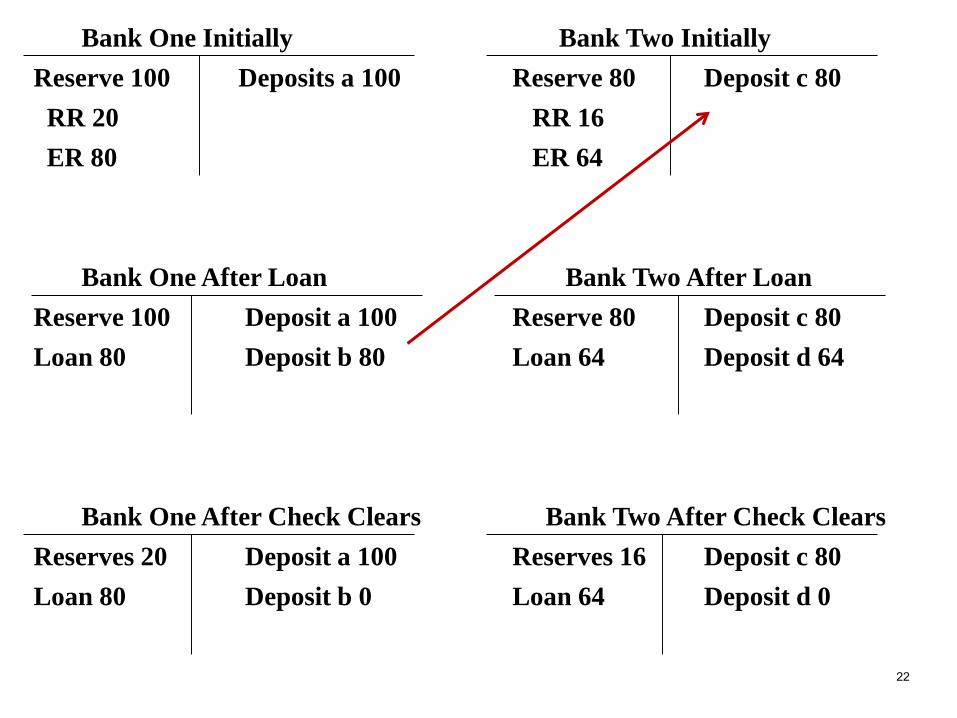

Bank One Initially Bank Two InitiallyReserve 100 Deposits a 100 Reserve 80 Deposit c 80RR 20 RR 16ER 80 ER 64

Bank One After Loan Bank Two After LoanReserve 100 Deposit a 100 Reserve 80 Deposit c 80Loan 80 Deposit b 80 Loan 64 Deposit d 64

Bank One After Check Clears Bank Two After Check ClearsReserves 20 Deposit a 100 Reserves 16 Deposit c 80Loan 80 Deposit b 0 Loan 64 Deposit d 0

22

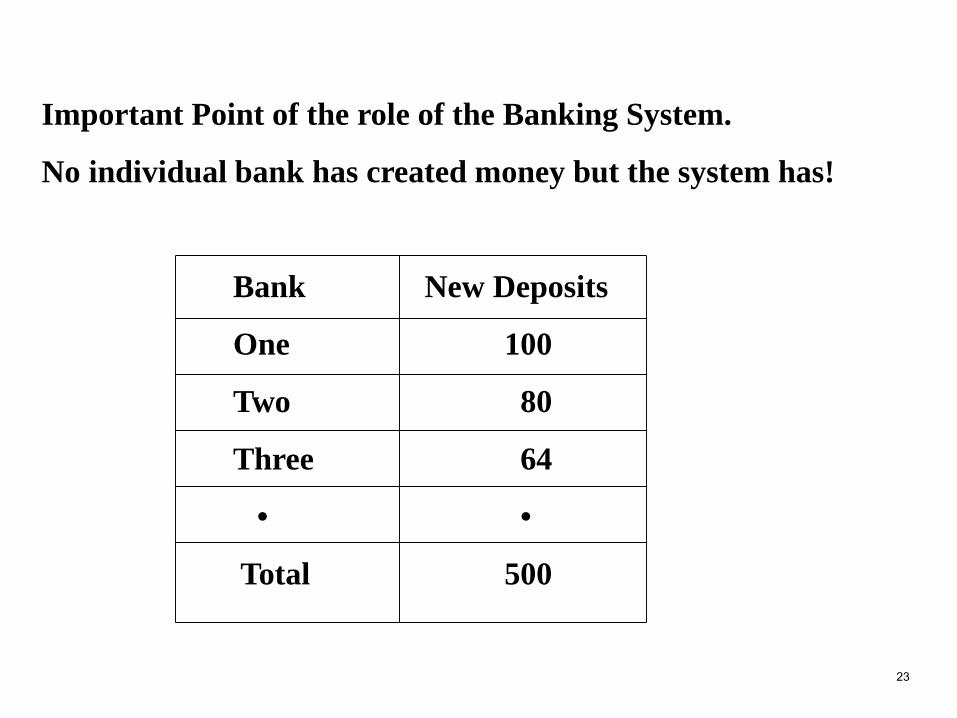

Important Point of the role of the Banking System.

No individual bank has created money but the system has!

Bank New Deposits

One 100

Two 80

Three 64

• •

Total 500

23

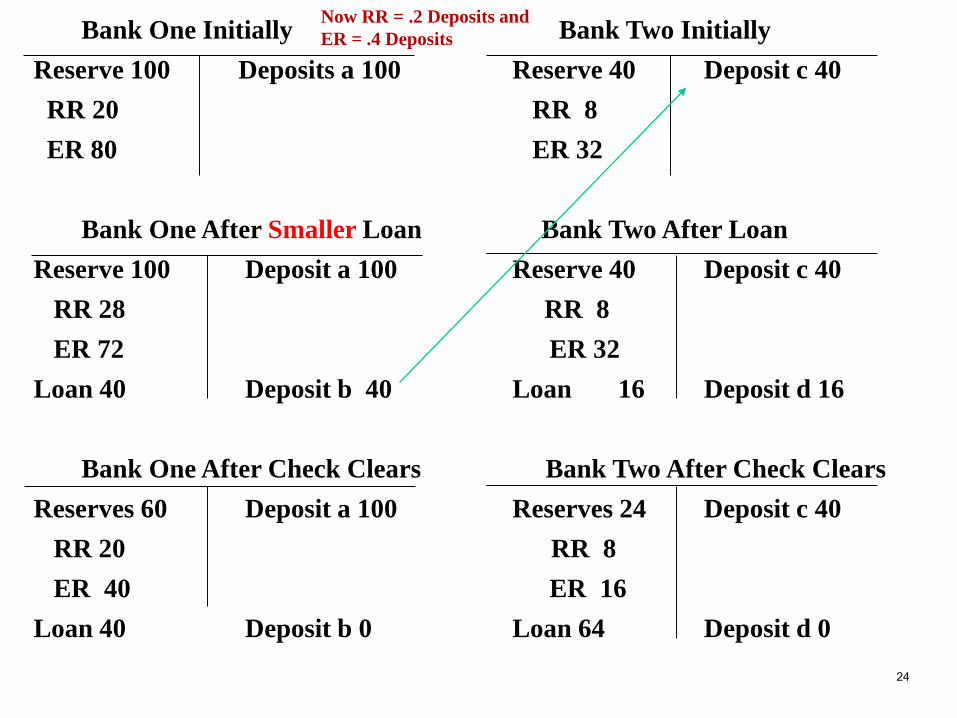

Bank One Initially Bank Two InitiallyReserve 100 Deposits a 100 Reserve 40 Deposit c 40RR 20 RR 8ER 80 ER 32

Bank One After Smaller Loan Bank Two After LoanReserve 100 Deposit a 100 Reserve 40 Deposit c 40

RR 28 RR 8ER 72 ER 32

Loan 40 Deposit b 40 Loan 16 Deposit d 16

Bank One After Check Clears Bank Two After Check ClearsReserves 60 Deposit a 100 Reserves 24 Deposit c 40

RR 20 RR 8ER 40 ER 16

Loan 40 Deposit b 0 Loan 64 Deposit d 0

Now RR = .2 Deposits andER = .4 Deposits

24

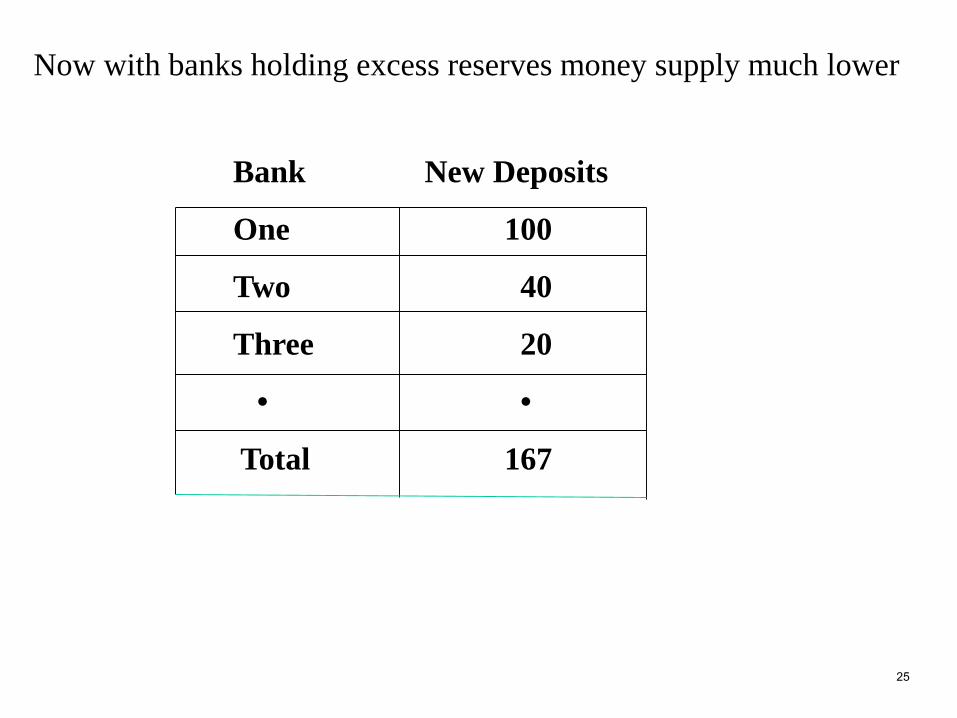

Bank New Deposits

One 100

Two 40

Three 20

• •

Total 167

Now with banks holding excess reserves money supply much lower

25

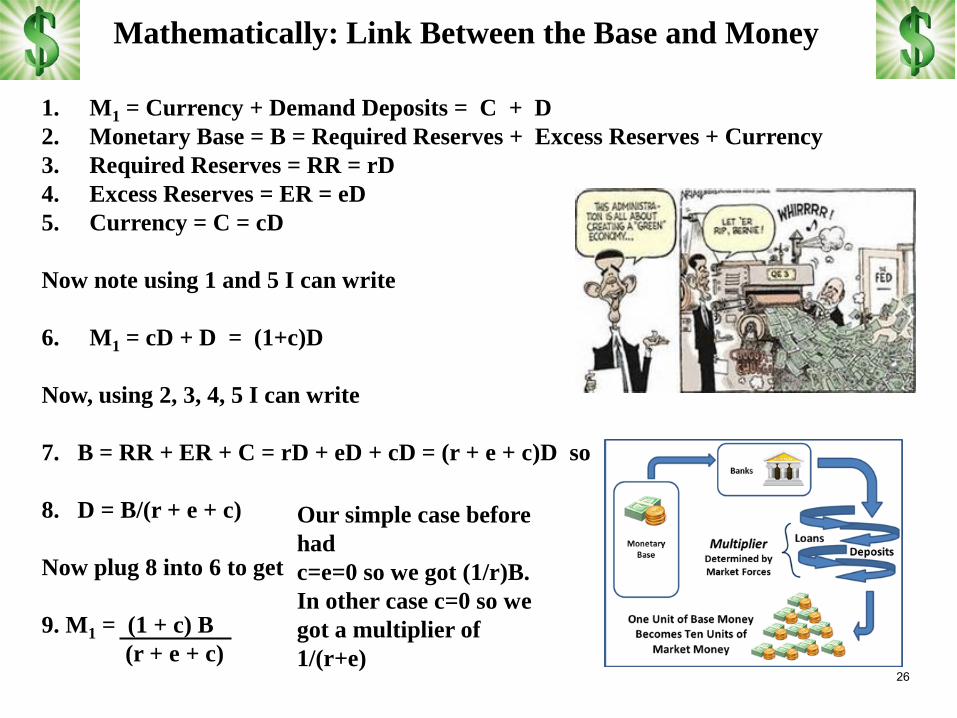

Mathematically: Link Between the Base and Money

1. M1 = Currency + Demand Deposits = C + D2. Monetary Base = B = Required Reserves + Excess Reserves + Currency3. Required Reserves = RR = rD4. Excess Reserves = ER = eD5. Currency = C = cD

Now note using 1 and 5 I can write

6. M1 = cD + D = (1+c)D

Now, using 2, 3, 4, 5 I can write

7. B = RR + ER + C = rD + eD + cD = (r + e + c)D so

8. D = B/(r + e + c)

Now plug 8 into 6 to get

9. M1 = (1 + c) B (r + e + c)

Our simple case before hadc=e=0 so we got (1/r)B. In other case c=0 so we got a multiplier of 1/(r+e)

26

So Who Determines the Money Stock?1. Federal Reserve

A) Open Market Operations change the base or reservesB) Set reserve requirements and hence affect multiplierC) Set discount rate and thereby affect the base or reservesD) Set rate paid on reserves

2. The BanksA) Decide how many excess reserves to hold which affects the

multiplierB) Decide how many reserves to borrow at the Fed which affects

the base

3. The PublicA) Set currency and time deposit ratios which affect the

multiplier

4. The TreasuryA) Set amount of currency they want to hold in tax and loan

accounts which affects the base27

0.0000

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

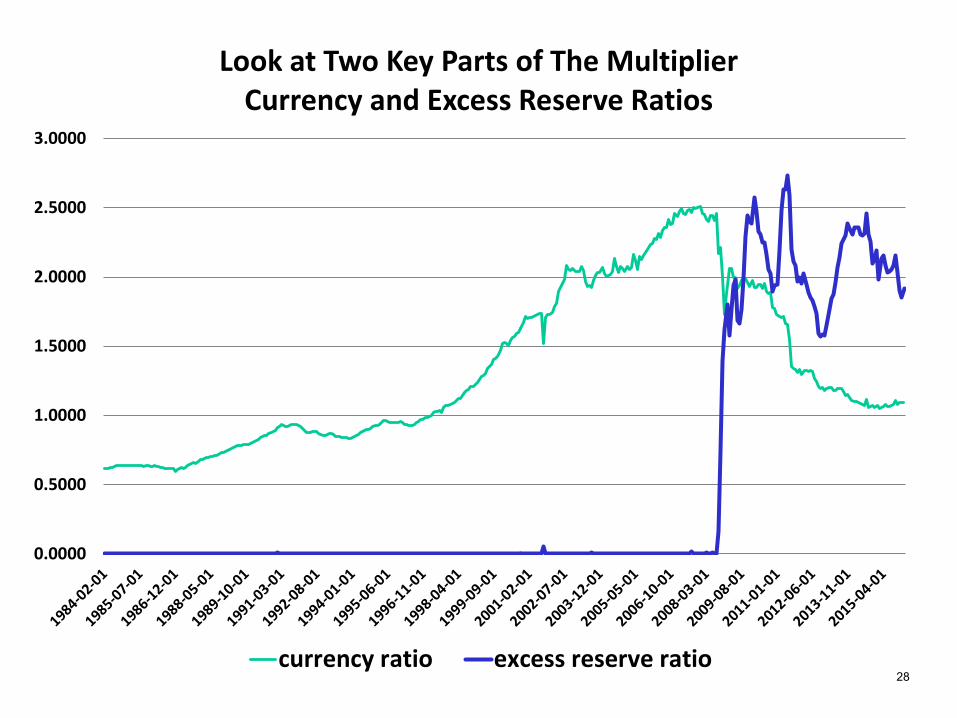

Look at Two Key Parts of The MultiplierCurrency and Excess Reserve Ratios

currency ratio excess reserve ratio28

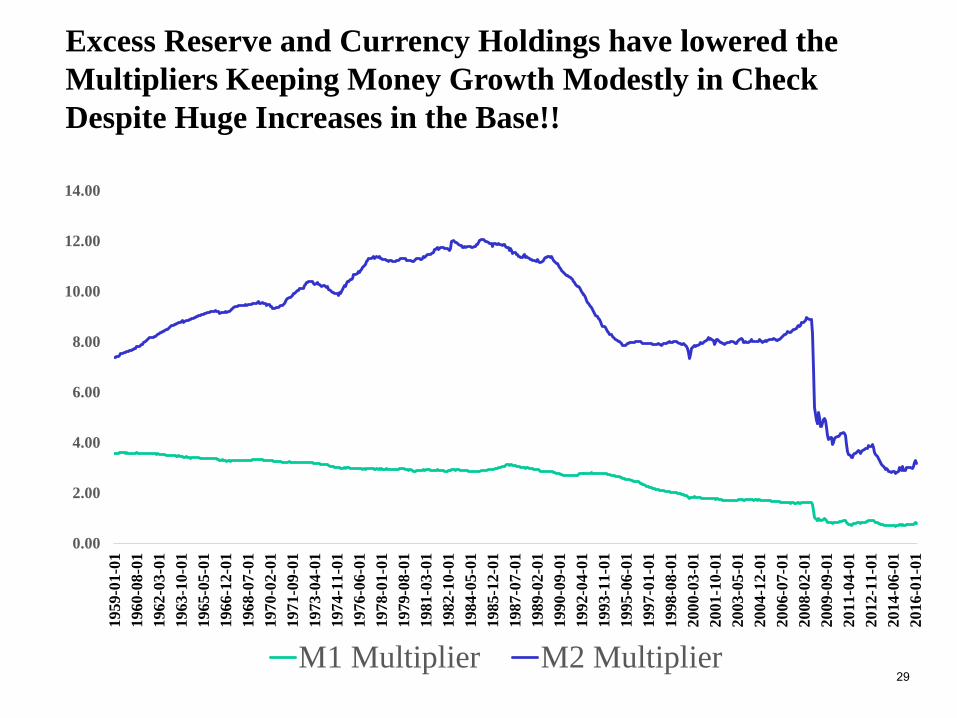

Excess Reserve and Currency Holdings have lowered the Multipliers Keeping Money Growth Modestly in Check Despite Huge Increases in the Base!!

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1959

-01-

0119

60-0

8-01

1962

-03-

0119

63-1

0-01

1965

-05-

0119

66-1

2-01

1968

-07-

0119

70-0

2-01

1971

-09-

0119

73-0

4-01

1974

-11-

0119

76-0

6-01

1978

-01-

0119

79-0

8-01

1981

-03-

0119

82-1

0-01

1984

-05-

0119

85-1

2-01

1987

-07-

0119

89-0

2-01

1990

-09-

0119

92-0

4-01

1993

-11-

0119

95-0

6-01

1997

-01-

0119

98-0

8-01

2000

-03-

0120

01-1

0-01

2003

-05-

0120

04-1

2-01

2006

-07-

0120

08-0

2-01

2009

-09-

0120

11-0

4-01

2012

-11-

0120

14-0

6-01

2016

-01-

01

M1 Multiplier M2 Multiplier29

0

500000

1000000

1500000

2000000

2500000

3000000

0.000

2000.000

4000.000

6000.000

8000.000

10000.000

12000.000

14000.00020

00-0

1-01

2000

-07-

0120

01-0

1-01

2001

-07-

0120

02-0

1-01

2002

-07-

0120

03-0

1-01

2003

-07-

0120

04-0

1-01

2004

-07-

0120

05-0

1-01

2005

-07-

0120

06-0

1-01

2006

-07-

0120

07-0

1-01

2007

-07-

0120

08-0

1-01

2008

-07-

0120

09-0

1-01

2009

-07-

0120

10-0

1-01

2010

-07-

0120

11-0

1-01

2011

-07-

0120

12-0

1-01

2012

-07-

0120

13-0

1-01

2013

-07-

0120

14-0

1-01

2014

-07-

0120

15-0

1-01

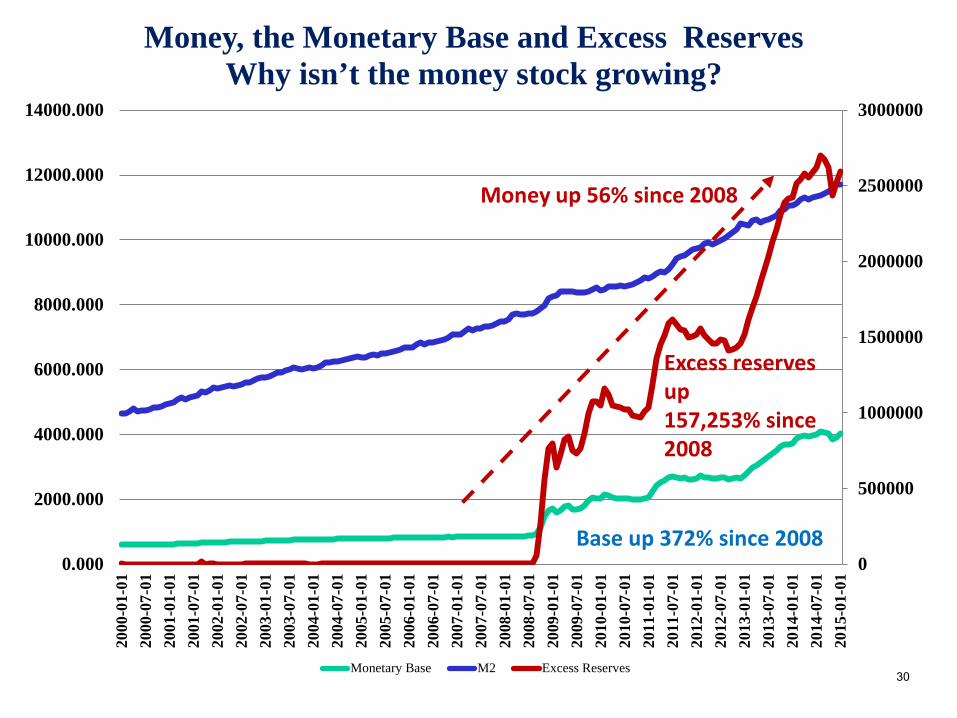

Money, the Monetary Base and Excess ReservesWhy isn’t the money stock growing?

Monetary Base M2 Excess Reserves

Base up 372% since 2008

Money up 56% since 2008

Excess reserves up157,253% since 2008

30

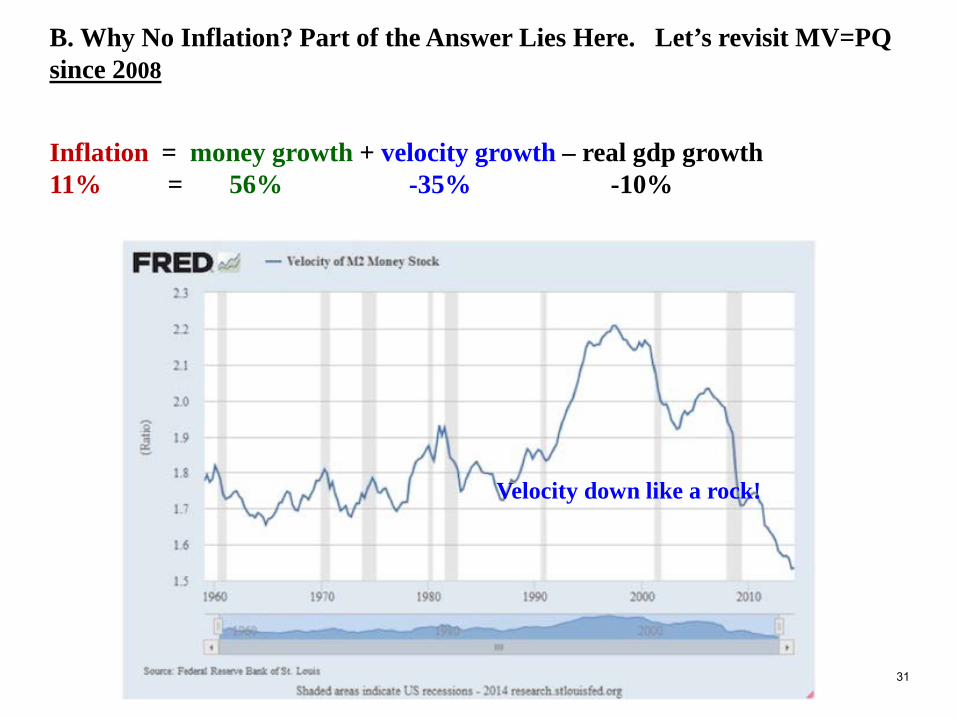

B. Why No Inflation? Part of the Answer Lies Here. Let’s revisit MV=PQ since 2008

Inflation = money growth + velocity growth – real gdp growth11% = 56% -35% -10%

Velocity down like a rock!

31

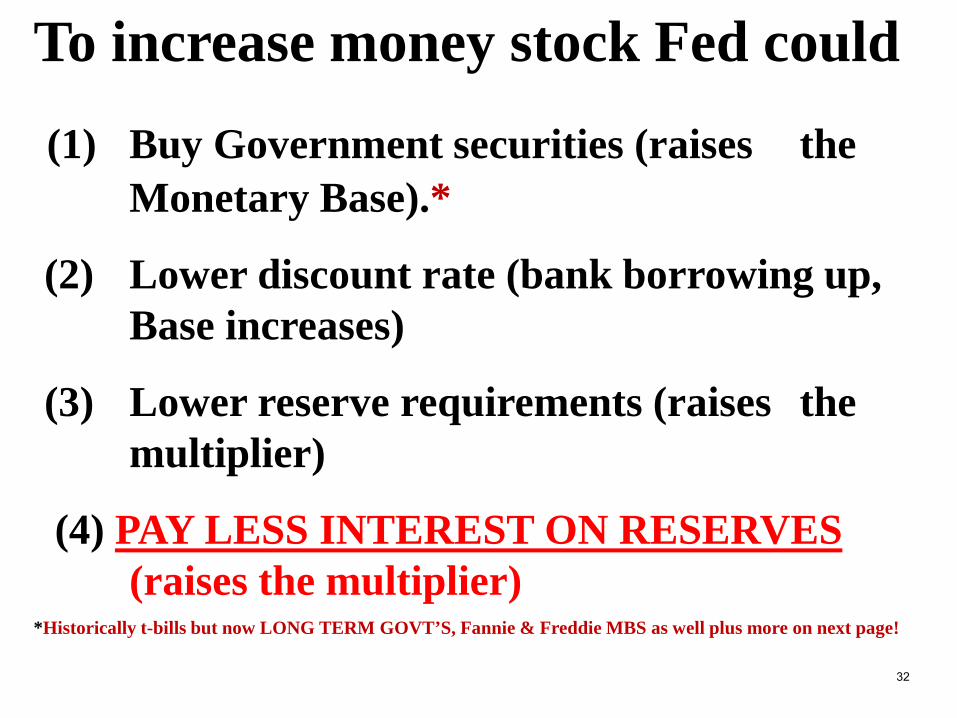

To increase money stock Fed could

(1) Buy Government securities (raises the Monetary Base).*

(2) Lower discount rate (bank borrowing up, Base increases)

(3) Lower reserve requirements (raises the multiplier)

(4) PAY LESS INTEREST ON RESERVES (raises the multiplier)

*Historically t-bills but now LONG TERM GOVT’S, Fannie & Freddie MBS as well plus more on next page!

32

Let’s revisit monetary policy in general

33

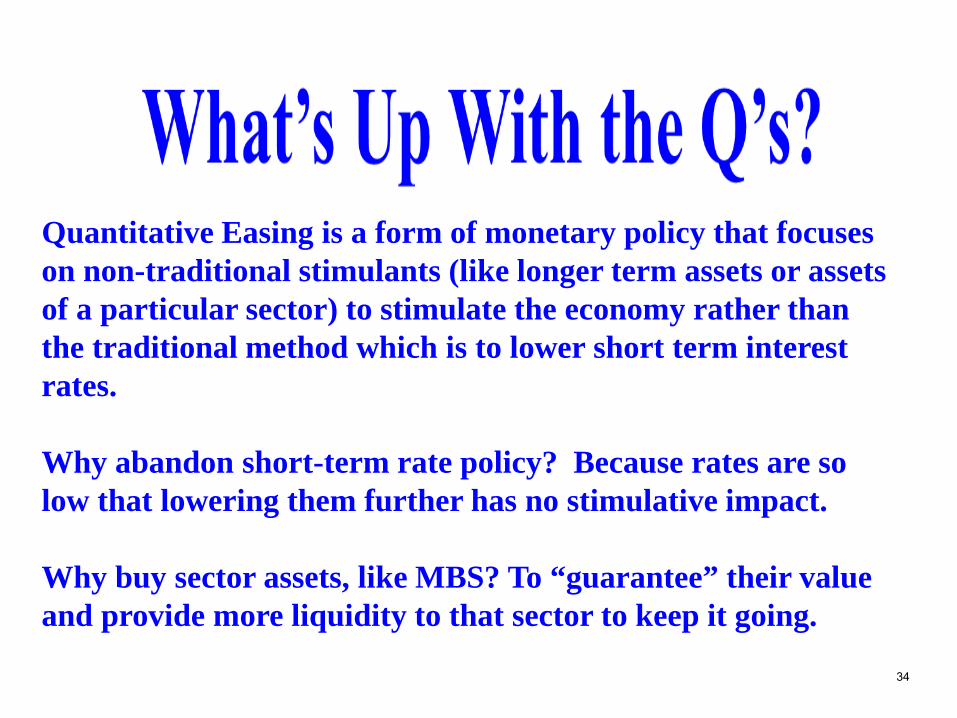

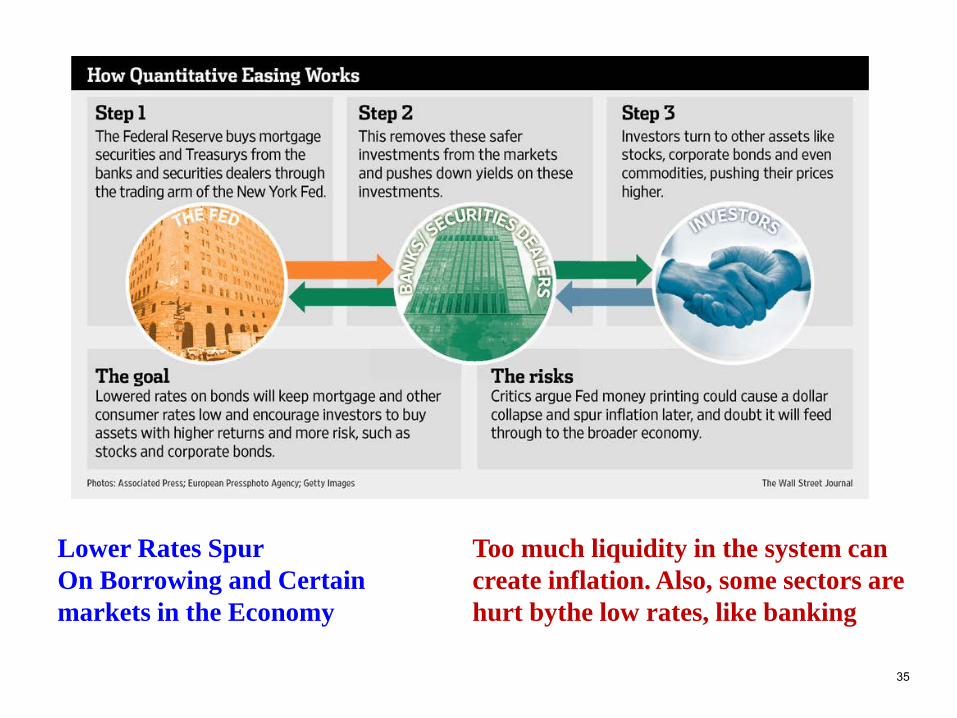

Quantitative Easing is a form of monetary policy that focuses on non-traditional stimulants (like longer term assets or assets of a particular sector) to stimulate the economy rather than the traditional method which is to lower short term interest rates.

Why abandon short-term rate policy? Because rates are so low that lowering them further has no stimulative impact.

Why buy sector assets, like MBS? To “guarantee” their value and provide more liquidity to that sector to keep it going.

34

Lower Rates Spur On Borrowing and Certain markets in the Economy

Too much liquidity in the system can create inflation. Also, some sectors are hurt bythe low rates, like banking

35

Difference Between QE Policies and Operation TwistQE policies create new money and increase the monetary base and potentially the money stock.

Twist exercises do not change the money stock so are less inflationary. You just take $X out and put it right back in. 36

THREE POINTS1. The Fed can use monetary policy to

control different things.

2. If they try to control one thing, something bad might happen to another thing.

3. So, monetary policy is not so simple or straightforward.

37

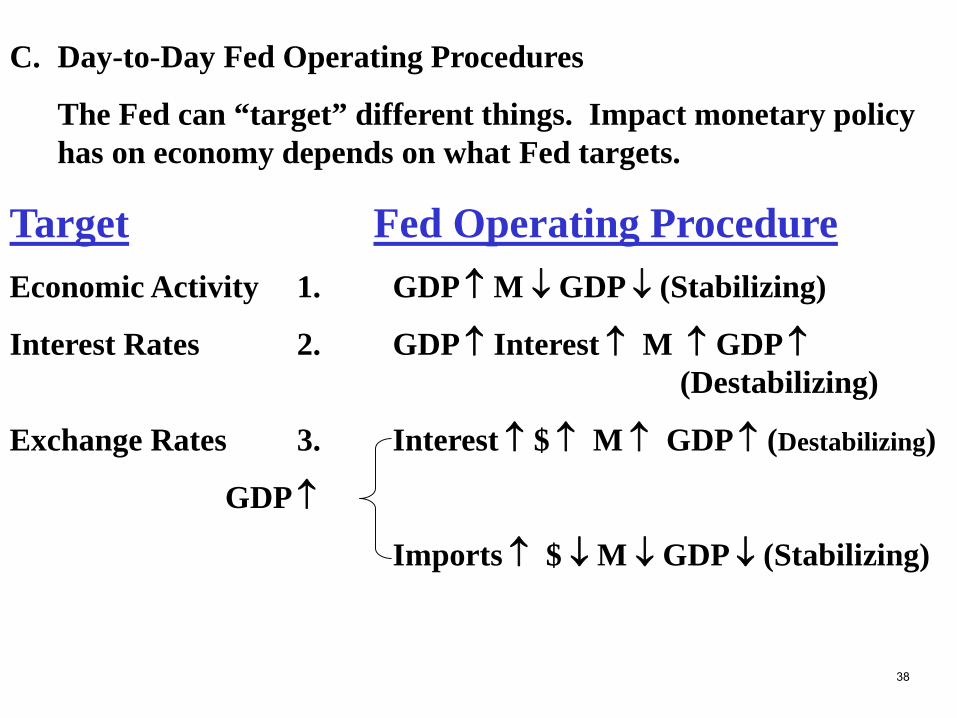

C. Day-to-Day Fed Operating Procedures

The Fed can “target” different things. Impact monetary policy has on economy depends on what Fed targets.

Target Fed Operating ProcedureEconomic Activity 1. GDP ↑ M ↓ GDP ↓ (Stabilizing)

Interest Rates 2. GDP ↑ Interest ↑ M ↑ GDP ↑(Destabilizing)

Exchange Rates 3. Interest ↑ $ ↑ M ↑ GDP ↑ (Destabilizing)

GDP ↑

Imports ↑ $ ↓ M ↓ GDP ↓ (Stabilizing)

38

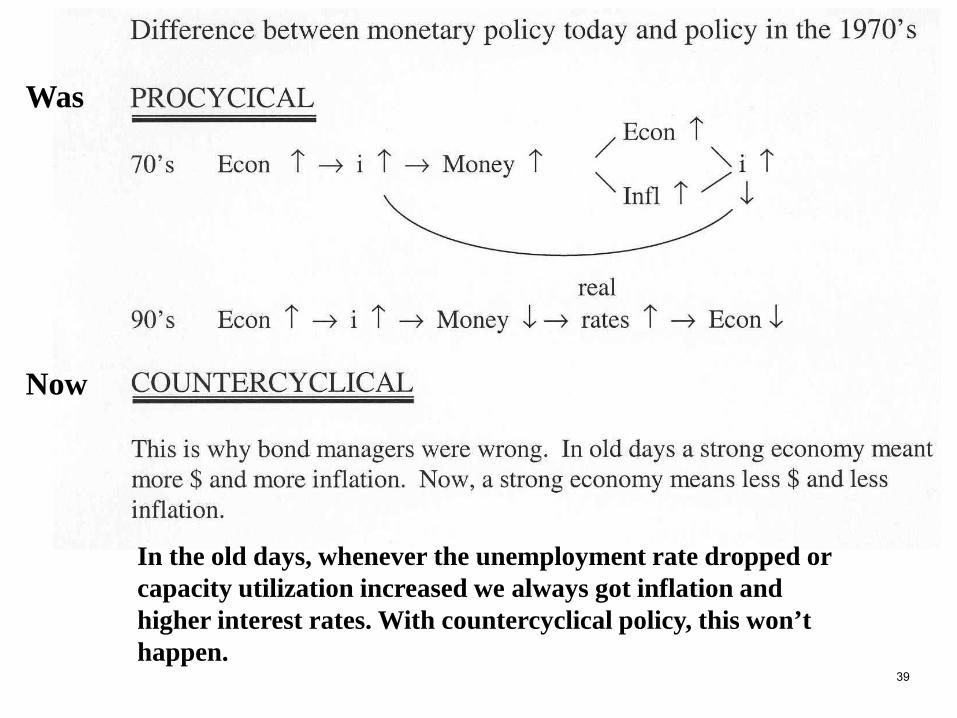

Was

Now

In the old days, whenever the unemployment rate dropped or capacity utilization increased we always got inflation and higher interest rates. With countercyclical policy, this won’t happen.

39

Advanced topic

New policy works as long as demand stocks dominate

S

D

P

Output

40

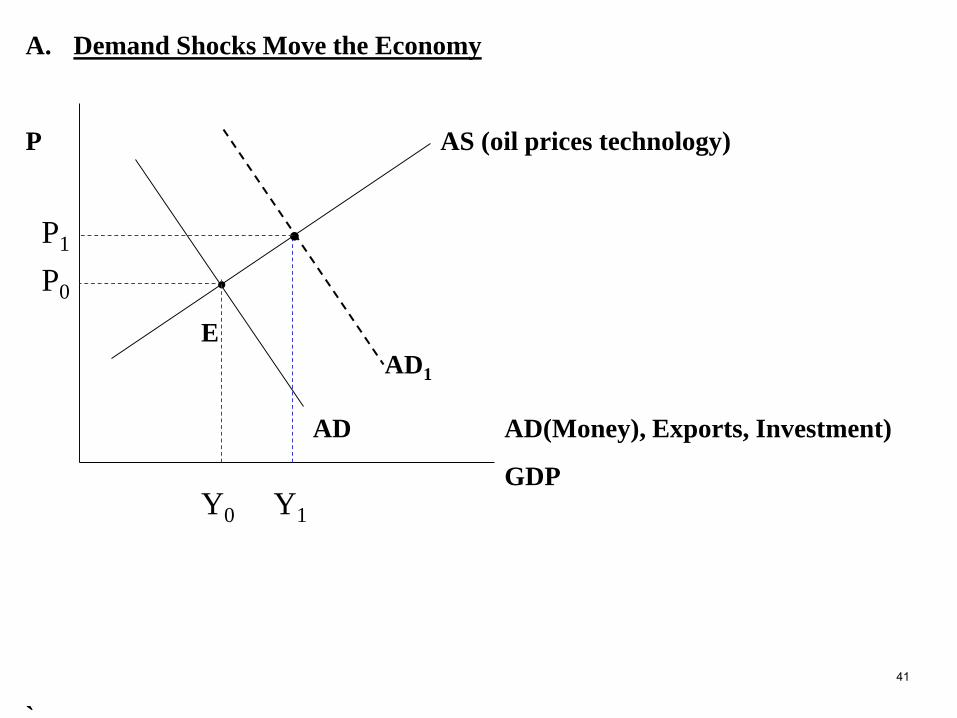

A. Demand Shocks Move the Economy

P AS (oil prices technology)

•

E

AD AD(Money), Exports, Investment)

GDP

`

Y0 Y1

P1

P0

AD1

•

41

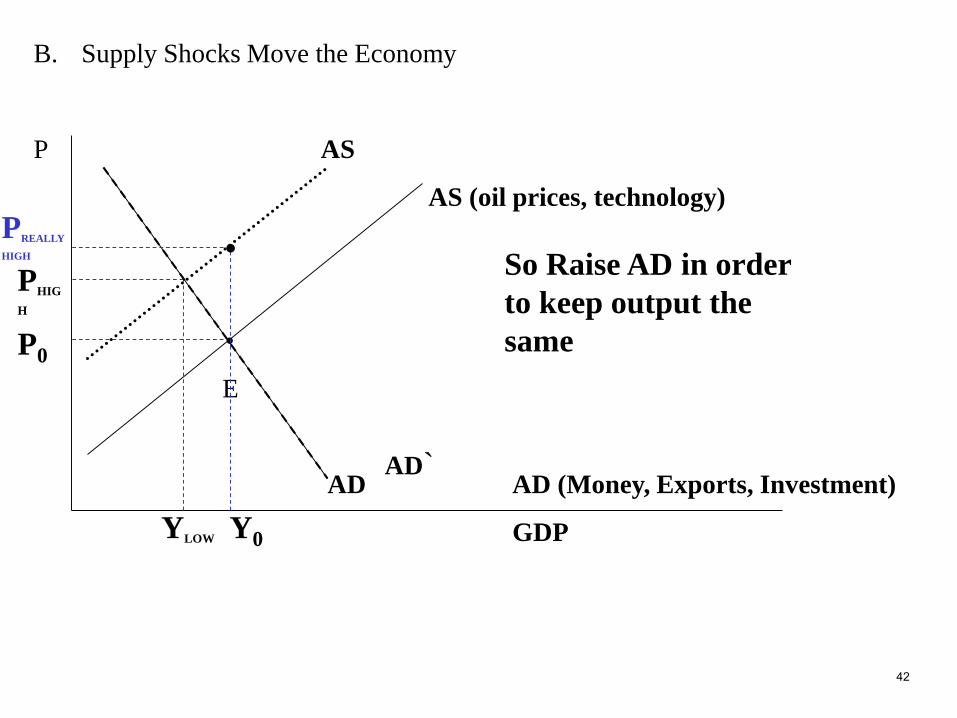

B. Supply Shocks Move the Economy

P AS

AS (oil prices, technology)

•

E

AD AD (Money, Exports, Investment)

GDPYLOW Y0

PHIGH

P0

AD`

PREALLY

HIGH • So Raise AD in order to keep output the same

42

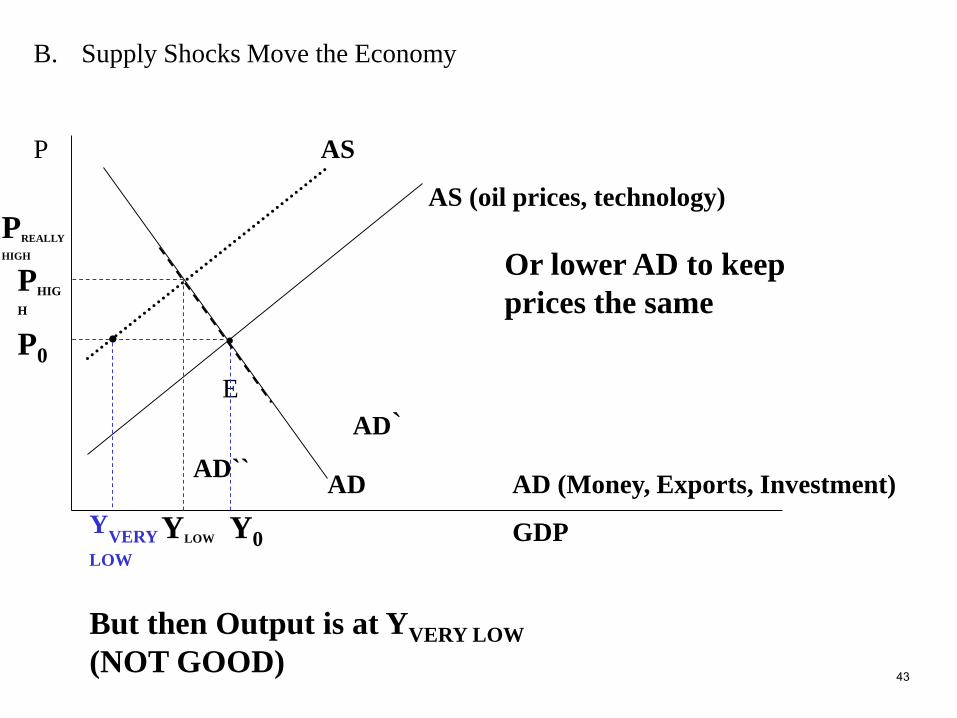

B. Supply Shocks Move the Economy

P AS

AS (oil prices, technology)

•

E

AD AD (Money, Exports, Investment)

GDPYLOW Y0

PHIGH

P0

AD`

PREALLY

HIGH Or lower AD to keep prices the same

•

AD``

But then Output is at YVERY LOW (NOT GOOD)

YVERY LOW

43

It’s Not the Fed: Structural Obstacles to US Growth

1. Aging population (not as bad as Japan’s or China’s)

2. Horrible immigration policy or lack thereof

3. Productivity declines caused by -lack or capital formation-lack of organic growth (as opposed to M&A activity that does not grow the pie but simply

slices it up differently to get market share, etc)- over regulation, too much focus on oversight/compliance which might not be productive or

bank regulation focused on asset liquidity or risk based capital

4. Failing educational system

5. Bad fiscal policy decisions -Focused on redistribution of the pie not growth of the pie-Debilitating Tax system

6. Rising health costs consuming more disposable income.

7. Globalization has exported the middle class (“off-shoring” is a symptom of demand for cheaper goods that will ultimately be met by technology)

44

More of Bad Tax Code & Tax Policy

• Way too Complex• Since self reported Income is taxed it incents evasion and inversion (fear a Greek

equilibrium as gov’t relies on tax revenue-everyone cheats because everyone else cheats…not American way)

• Taxing Income (since income is spent or saved) taxes saving, which means it taxes investment

• Deductions, like interest, bias capital structure towards debt not equity • Corporate tax > 0 causes geographic dislocation, higher prices for consumers, lower

wages to workers and lower returns to investors• Deductions reward the rich at 40% the poor at 0 or 10%

45