UNIT II MG2452 Engineering Economics and Financial Accounting Notes

Economics /Management 4 Financial Accounting

A First Course in Financial Accounting for:

Producers (accountants) and

Users (analysts & economists)

L-1

Course Objectives

1. Learn the Language of accounting. 2. Become a sophisticated Financial

Statement user. 3. Be able to differentiate between

Economic information and Accounting information.

Grading

o One Quiz 10 percent o Midterm #1 20 percent o Midterm #2 20 percent o Final Exam 45 percent o Participation 5 percent

Final “letter” Grades will be curved. You need 55 percent for a “C- / P”.

Grading Extras • There will be one A+, regardless of score. • Up to 10%, of students will receive an “A”. • There will be as many “A-’s” as practical where

there is a gap in scores. For example, in Winter 2016, the lowest A- had a score of 73.01, the highest B+ had a score of 72.30. Thus 0.71 points was The Gap.

• The student ranked #1 at the beginning of 10th week will be excused from the final exam, with an “A” grade for the course.

Grade Insurance

During the quarter, unannounced, there will be at least two A- grade insurance exercises. These exercises will be challenging in scope with only a little allotted time. Should you solve the exercise perfectly, or near perfectly, you will receive: • an “A-” guarantee , or a “B+” guarantee,

respectively • regardless of end of term scores as long as you

get a 60% score on the final exam.

Reminders • Read the Syllabus. • Bring a couple of 3x5 index cards to class each

day. This is how I will record “participation”.

• Participation? Get involved with the subject.

• Start looking for a Partner for Midterm #1.

• All exams are M/C. You will need Scantrons. • You may use your Reader during exams; write in

it but add no separate sheets of paper. • The Quiz will be a crossword puzzle. Reader

Chapters 1-2, Slides L-1 and L-2.

Attitude

Keep an open mind. Accounting is simple, relatively deterministic, but it has a few nuances.

Attend lectures and visit the TA’s regularly. Practice. Set your standards high - have zero tolerance

for error; limited tolerance for mistakes. Read the Reader. Stay awake in class. Accounting is a professional

art, so practice being professional.

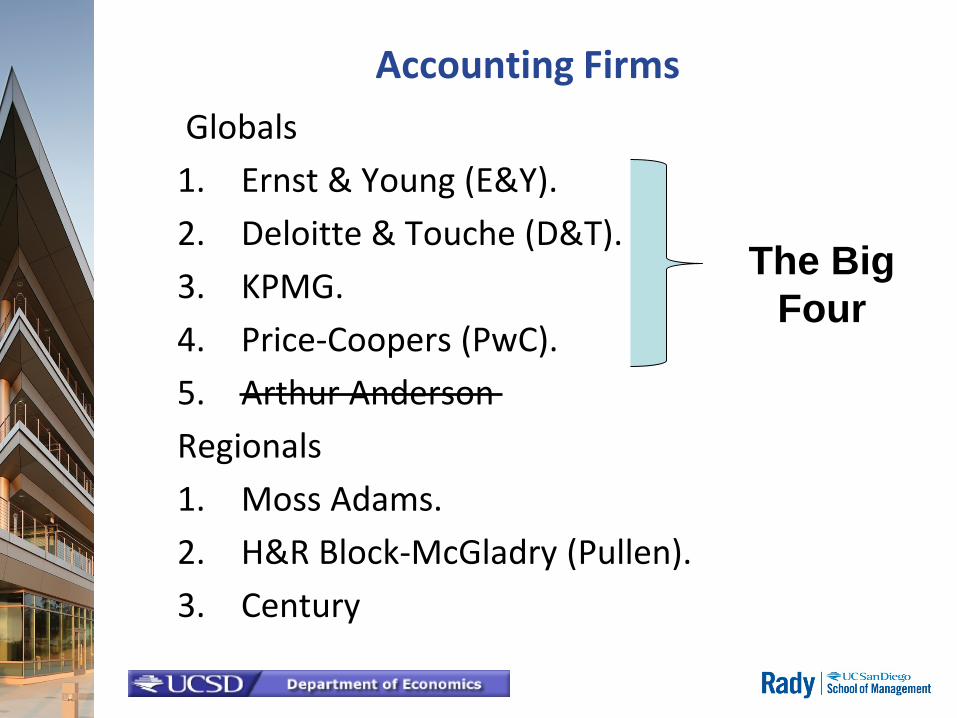

Accounting Firms Globals 1. Ernst & Young (E&Y). 2. Deloitte & Touche (D&T). 3. KPMG. 4. Price-Coopers (PwC). 5. Arthur Anderson Regionals 1. Moss Adams. 2. H&R Block-McGladry (Pullen). 3. Century

The Big Four

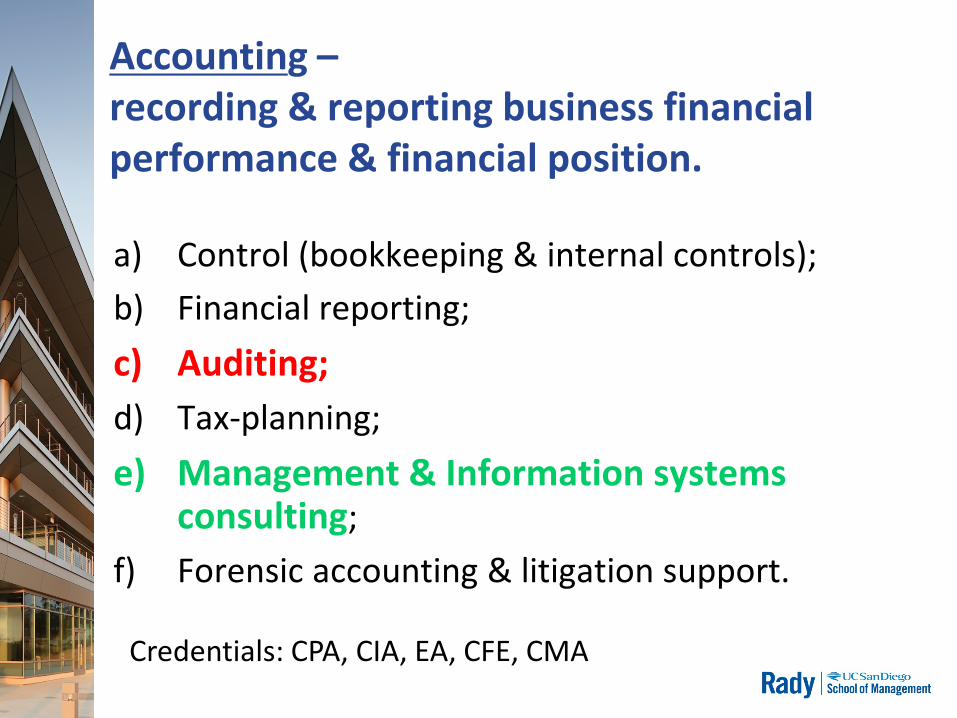

Accounting – recording & reporting business financial performance & financial position. a) Control (bookkeeping & internal controls); b) Financial reporting; c) Auditing; d) Tax-planning; e) Management & Information systems

consulting; f) Forensic accounting & litigation support.

Credentials: CPA, CIA, EA, CFE, CMA

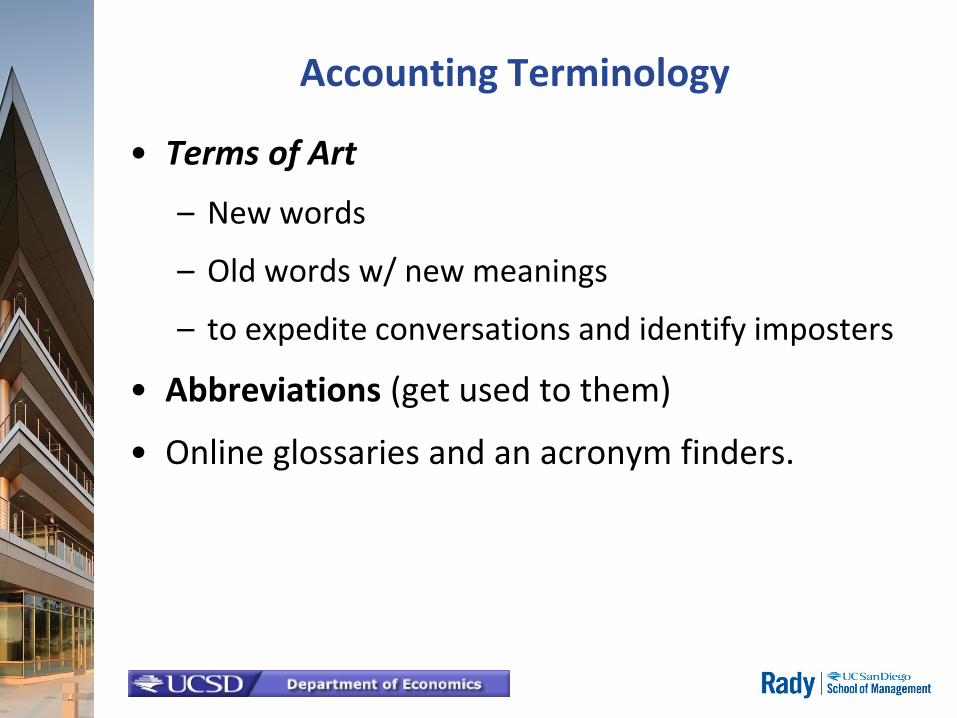

Accounting Terminology

• Terms of Art

– New words

– Old words w/ new meanings

– to expedite conversations and identify imposters

• Abbreviations (get used to them)

• Online glossaries and an acronym finders.

Firms Need Cash (to acquire Assets),

so they create Financial Capital

• Financial Capital represents the Cash raised when firms sell Financial Securities

1. Stocks – shares of the Firm sold to investors, also called Share-holders – Equity Capital

2. Bonds – loans from creditors, bond-holders – Debt

Capital

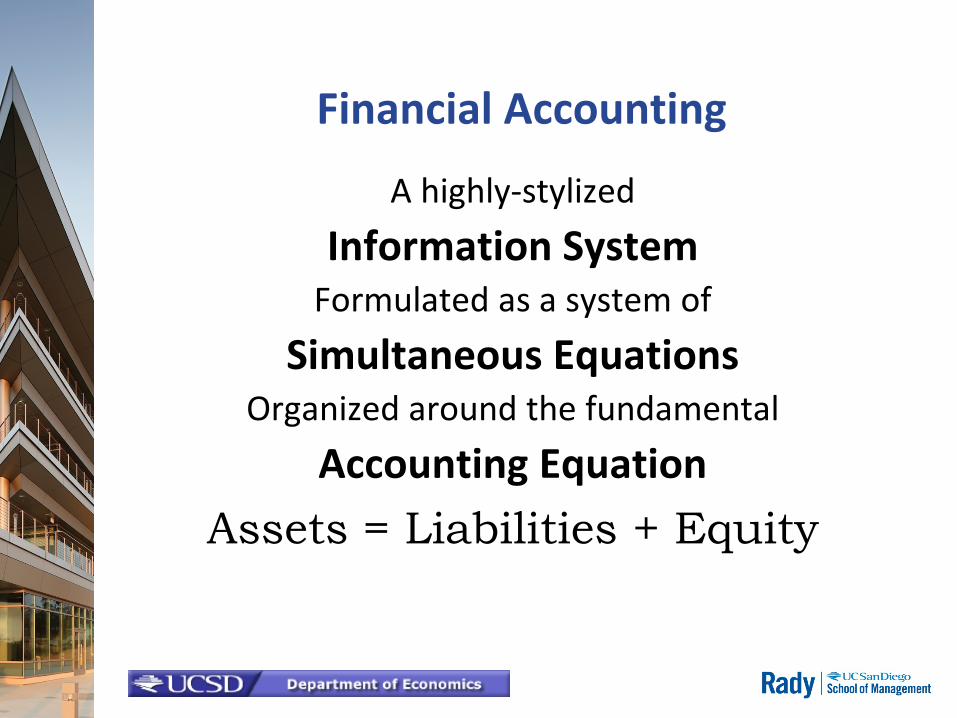

Financial Accounting

A highly-stylized Information System

Formulated as a system of Simultaneous Equations

Organized around the fundamental Accounting Equation

Assets = Liabilities + Equity

The Fundamental Equation of Accounting

Assets = Liabilities + Equity

What we OWN “Assets” must have a Source =

Liabilities are what we owe to others Equity is what we owe to ourselves

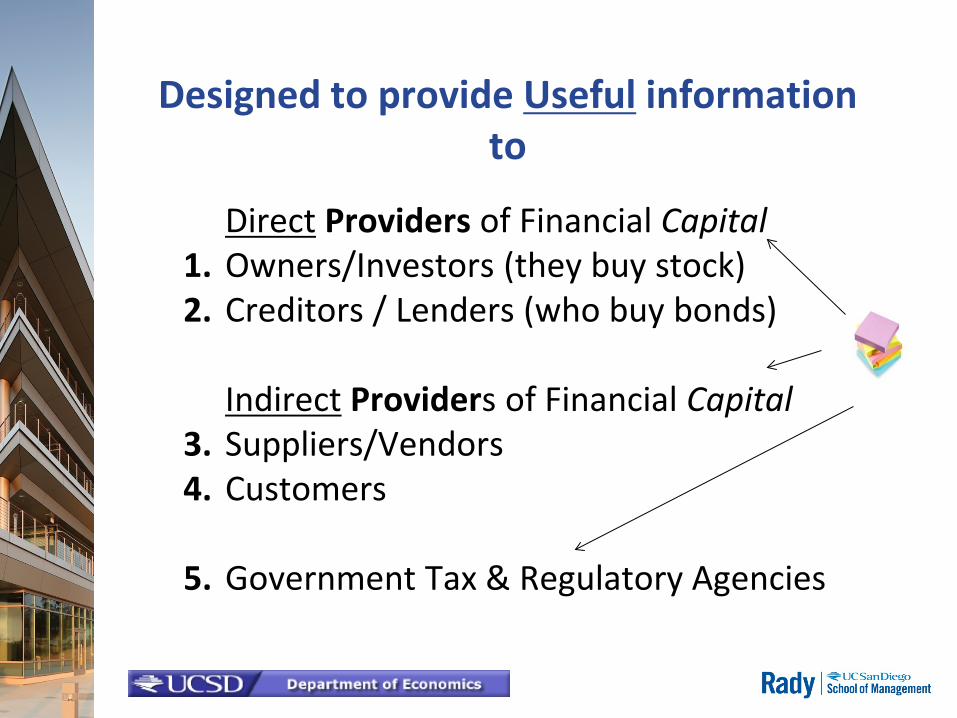

Designed to provide Useful information to

Direct Providers of Financial Capital 1. Owners/Investors (they buy stock) 2. Creditors / Lenders (who buy bonds) Indirect Providers of Financial Capital 3. Suppliers/Vendors 4. Customers 5. Government Tax & Regulatory Agencies

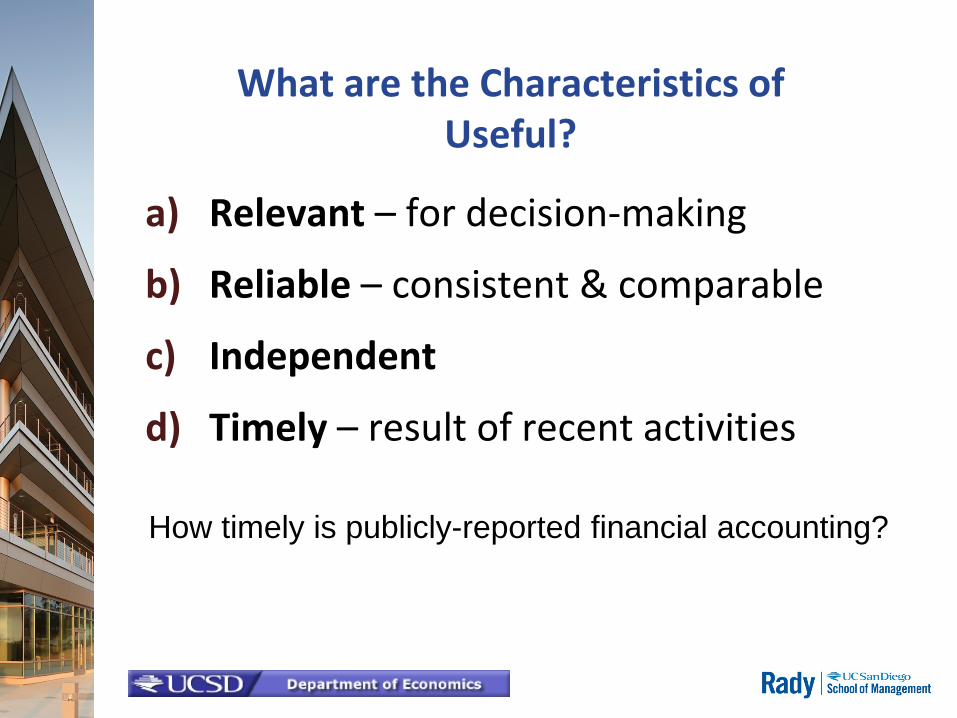

What are the Characteristics of Useful?

a) Relevant – for decision-making

b) Reliable – consistent & comparable

c) Independent

d) Timely – result of recent activities How timely is publicly-reported financial accounting?