JK Tyre summer internship report on two wheeler tyre segment

Russia

Andrei PantioukhovVP, Russian operations

Capital Markets Day 2015

1. Operational review

(market / business / production)

2. Strategy update and long-range plan

Contents

2

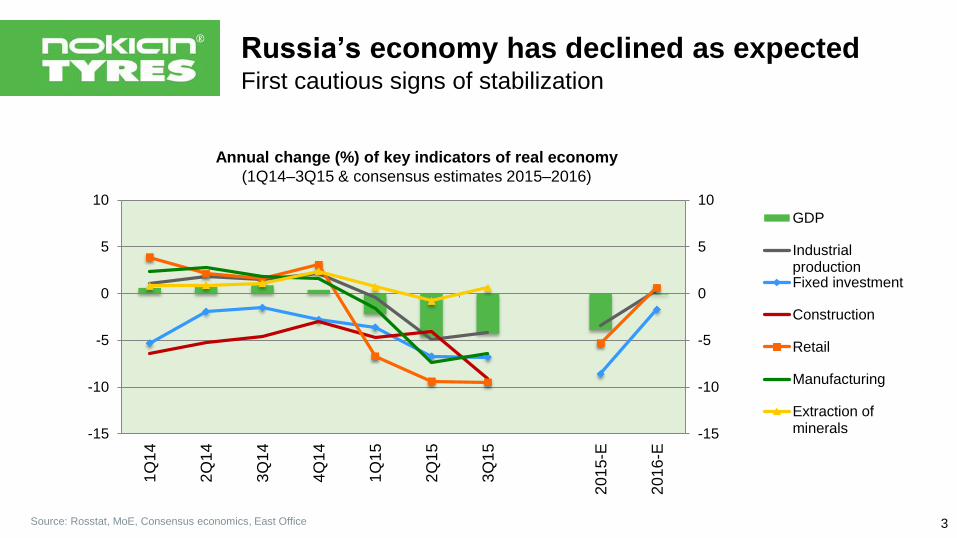

Russia’s economy has declined as expectedFirst cautious signs of stabilization

Source: Rosstat, MoE, Consensus economics, East Office

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

201

5-E

201

6-E

GDP

IndustrialproductionFixed investment

Construction

Retail

Manufacturing

Extraction ofminerals

Annual change (%) of key indicators of real economy

(1Q14–3Q15 & consensus estimates 2015–2016)

3

Ruble clearly follows oil priceImpact of other exchange rate factors limited

2000

3000

4000

5000

6000

7000

8000

9000

20

30

40

50

60

70

80

90

RUB/EUR (LHS) RUB/USD (LHS)

Brent RUB/bbl (RHS) Budget 2016

Oil price impact on RUB exchange rate

Urals oil price USD/bbl RUB/USD

40 77-80

50 61-65

60 52-55

Source: CBR, EIA, East Office 4

Inflation is slowing downGiven no further devaluation, it should be under control

Sep 2015 % YoY

CPI* +15.7

Food +17.4

Non-food +15.2

Services +13.8

Source: CBR, Consensus Economics, gazeta.ru, East Office

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Russia's CPI inflation % YoY, Russia’s Central Bank key rate

CPI

Consensus Forecast(Oct-2015)

CBR Key rate

Minfin Estimate

* CPI – consumer price index

5

Weak consumer confidence and retail turnoverDriven by low purchasing power

2013

Consumer confidence index

Quarters

2007 2008 2009 2010 2011 2012 2013 2014 2015

Retail turnover development

as a % to monthly average of 2012

total turnover eliminated seasonality trend

Source: Rosstat

2014 2015

6

Sales of new cars remain sluggishMonthly sales on 2009 level

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0

50 000

100 000

150 000

200 000

250 000

20

09

/1

20

09

/3

20

09

/5

20

09

/7

20

09

/9

20

09

/11

20

10

/1

20

10

/3

20

10

/5

20

10

/7

20

10

/9

20

10

/11

20

11

/1

20

11

/3

20

11

/5

20

11

/7

20

11

/9

20

11

/11

20

12

/1

20

12

/3

20

12

/5

20

12

/7

20

12

/9

20

12

/11

20

13

/1

20

13

/3

20

13

/5

20

13

/7

20

13

/9

20

13

/11

20

14

/1

20

14

/3

20

14

/5

20

14

/7

20

14

/9

20

14

/11

20

15

/1

20

15

/3

20

15

/5

20

15

/7

20

15

/9

un

its

MONTHLY CAR AND LCV SALES

Foreign brands

Local brands

Foreign change y-o-y

Local change y-o-y

0

1 000 000

2 000 000

3 000 000

4 000 000

2009 2010 2011 2012 2013 2014 2015 e

un

its

ANNUAL CAR AND LCV SALES

Local brands

Foreign brands

Source: AEB, Global Insight 7

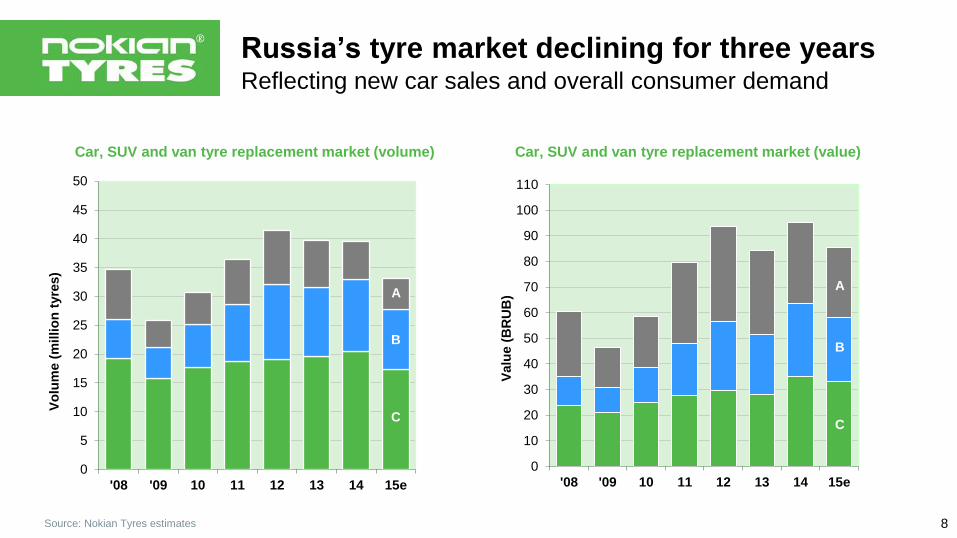

Russia’s tyre market declining for three yearsReflecting new car sales and overall consumer demand

0

5

10

15

20

25

30

35

40

45

50

'08 '09 10 11 12 13 14 15e

Vo

lum

e (

millio

n t

yre

s)

x

0

10

20

30

40

50

60

70

80

90

100

110

'08 '09 10 11 12 13 14 15e

Valu

e (

BR

UB

)

Car, SUV and van tyre replacement market (volume) Car, SUV and van tyre replacement market (value)

C

B

A

C

B

A

Source: Nokian Tyres estimates 8

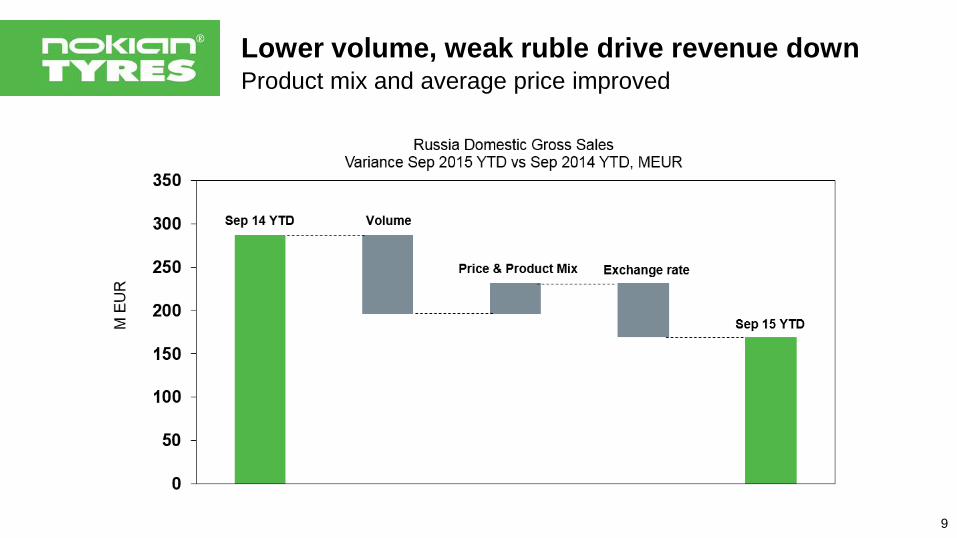

Lower volume, weak ruble drive revenue downProduct mix and average price improved

9

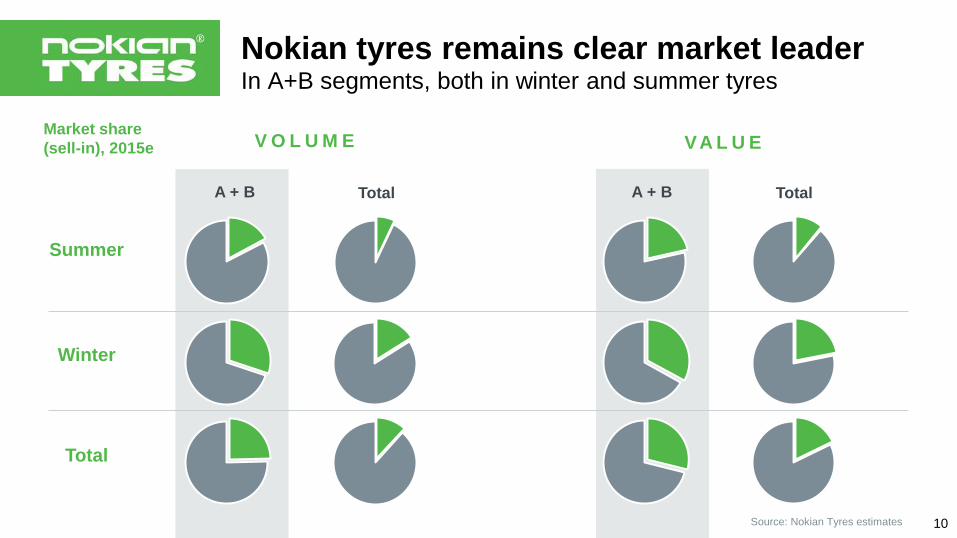

Nokian tyres remains clear market leaderIn A+B segments, both in winter and summer tyres

Market share

(sell-in), 2015e V O L U M E VA L U E

Summer

A + B Total

Winter

Total

A + B Total

10Source: Nokian Tyres estimates

Marketing and sell-out support programAimed at keeping market share on sell-out level

LIFE-LONG EXTENDED GUARANTEEFOR ALL HAKKAPELIITTA PRODUCTSCONVINCING MAGAZINE TEST VICTORIES

‘TYRE MOUNTING FOR FREE’ CAMPAIGNSEFFECTIVE ADVERTISING

11

Vsevolozhsk factory – main production base10 years of success

Production capacity increased from 1 m

(2005) to 15.5. m units / year

Biggest car tyre factory in Russia: over 70

million tyres produced since 2005

The most modern tyre factory in Europe:

high level of automation

The best efficiency in the industry: only

~1,000 employees at the factory

Wide product range for all markets: over

1,300 SKUs in production

Export to over 40 countries: ~70% of the

factory’s production output in 2015

Biggest exporter of consumer goods in

Russia

Significant tax benefits

12

1. Operational review

(market / business / production)

2. Strategy update and long-range plan

Contents

13

Strategic goal intact: continue to be #1Keep market leader position and outperform market

Sales volume >5 Mpcs / revenue >20 BRUB

Market share total >14%, A+B >28%

Profitability: EBIT margin (local sales) >40%

Market leader in A+B segments,

consumers’ ultimate choice of high-quality tyres,

and best partner for customers

Comprehensive product

portfolio with balanced price

positioning

Highest brand awareness and

intent to buy among

consumers

Committed, loyal distribution;

highest earning potential for

partners

One of the most attractive

employers with highly

engaged and effective

personnel

Strategic cornerstones

Vision Mid-term strategic objectives (2018)

14

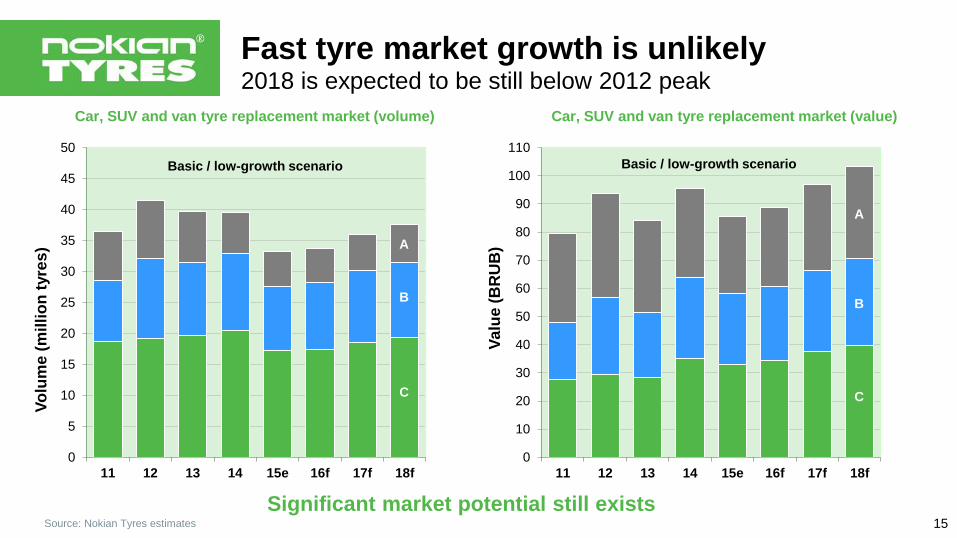

Fast tyre market growth is unlikely2018 is expected to be still below 2012 peak

Significant market potential still exists15Source: Nokian Tyres estimates

0

5

10

15

20

25

30

35

40

45

50

11 12 13 14 15e 16f 17f 18f

Vo

lum

e (

milli

on

tyre

s)

x

0

10

20

30

40

50

60

70

80

90

100

110

11 12 13 14 15e 16f 17f 18f

Va

lue

(B

RU

B)

x

Car, SUV and van tyre replacement market (volume) Car, SUV and van tyre replacement market (value)

C

B

A

C

B

A

Basic / low-growth scenario Basic / low-growth scenario

0

5

10

15

20

25

30

35

40

45

50

11 12 13 14 15e 16f 17f 18f

Vo

lum

e (

milli

on

tyre

s)

x

0

5

10

15

20

25

30

35

40

45

50

11 12 13 14 15e 16f 17f 18f

Vo

lum

e (

milli

on

tyre

s)

x

Car, SUV and van tyre replacement market (volume) Car, SUV and van tyre replacement market (volume)

C

B

A

C

B

A

16

Pessimistic / stagnant scenario Optimistic / modest growth scenario

Source: Nokian Tyres estimates

Growth may vary depending on scenarioVariation between optimistic and pessimistic up to 20%

Competition has clearly intensifiedKey players are committed to the Russian market

Tight pricing environment, aggressive pricing policies by some competitors;

Launch of local production facilities affecting the approach and level of activity of competitors;

Localized production and extended product range becoming key factors in shaping competitive

landscape;

Role of Japanese and Korean players growing due to increased focus and competitive pricing;

Competitive threat from Chinese and other Asian players, not established in Russia directly,

weakening due to ruble devaluation;

Russian producers gaining share due to lower competition from China;

Emerging overcapacity situation resulting in further pricing pressure.

17

Target to outperform market in any scenarioMarket share in A+B segments to grow from 25% to 30%

10,0

11,0

12,0

13,0

14,0

15,0

2015e 2016f 2017f 2018f

basic optimistic pessimisticScenarios:

20,021,022,023,024,025,026,027,028,029,030,0

2015e 2016f 2017f 2018f

basic optimistic pessimisticScenarios:

Market

share, %

(volume)

Market

share, %

(volume)

A + B segments Total market

Source: Nokian Tyres estimates18

Optimal product mix and price positioning keyTarget to maximize revenue and profit

Segments

A:

B:

A:

B:

19

New business models in distribution evolvingPlan to pilot various consignment schemes

Manufacturer Distributor Retailer Consumer

Consignment sales

Logistics Service

Now

Meantime

Future

20

New business concepts in B2B2C e-commerceProactive approach to digital disruption

B2B

New web shop for business-to-

business customers

State-of-the-art e-commerce platform

enabling deep integration to corporate

ERP systems and making new

features and tools available for

boosting B2B online sales

Scalable and extendable solution

adjusted to specific B2B needs

B2C

Up-to-date web shop for direct sales

from the manufacturer to end

consumers

The new e-commerce platform

bringing better user experience to

online consumers

Strong prerequisite for owning the

end consumer and leveraging B2C

sales

vianor.ru

Sustainable, flexible and user-friendly

marketplace adjusted to business

needs of Vianor partners and

preferences of online consumers

Marketplace concept expanding

opportunities in selling products and

services

Significant step in strategic

evolvement of B2B2C model in line

with strong trends in online sales

21

Nokian tyres set to remain market leaderExecutive summary

Period of Russia’s tyre market fast growth is over: by 2018 the total market will still be below the

peak levels of 2012 with a clearly weaker structure of segments. However, significant market

potential still exists.

Competition has clearly intensified, with major manufacturers expanding their product ranges into

cheaper segments, adopting aggressive pricing strategies and localizing their production.

Russia remains a key market for Nokian Tyres. The strategic target will remain intact: outperform

the market and keep the market leader position.

Key strategic dimension for Nokian Tyres is the optimal product portfolio, i.e. product range and

price positioning within and across A and B segments.

Big changes are taking place in the area of distribution: new concepts based on consignment

approach are being developed and piloted.

Focus on consumer is increasingly important; changing consumer behavior and growing role of

ecommerce will have a big impact on marketing strategies and business concepts.

22

Thank you!