Networks of organizational learning and adaptation in retail TNCs

Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:A Micro Level AnalysisA Micro Level AnalysisA Micro Level AnalysisA Micro Level AnalysisA Micro Level Analysis

Arvind BadigerG.K. Kadekodi

Nayanatara S.N.

Series Editors:Aasha Kapur Mehta, Pradeep Sharma

Sujata Singh, R.K.TiwariP.R. Panchamukhi

2006

Table of ContentsTable of ContentsTable of ContentsTable of ContentsTable of Contents

Introduction 1

A Macro View of the Sector 2

A Micro View of the Sector 4

Drug Policy in India 5

Patent Scenario 9

Economic Reforms of 1990s, Implications of WTO Commitments andTrade Liberalisation 13

Evaluation of the Reforms Process in India 18

The New Patent Bill: Some Observations 20

Medecins Sans Frontieres’ (MSF) Views on India’s Role in the Provision of Drugs:Expressions on the Indian Patent Bill, 2005 22

Summary and Conclusions 23

Insight for Policy Initiatives 24

Annexures 25

References 26

4

1

2

3

5

6

7

8

9

10

11

Chhattisgarh Infrastructure Report

1. WPI of Medicines 2

2. Number of Drugs Under DPCO 3

3. Expenditure on Medicines as % of Per Capita Income 9

4. Export of Pharmaceuticals from India- 1998 10

5. Production of formulations and Bulk Drug in India 11

List of Figures

1. Drug Production in Response to Price Policy ( percent) 5

2. Price Difference Between TNCs and Indigenous Firms in 1978 & 1982 6

3. Comparative Contributions of Major MNCs and National Companies in Antibioticand Simple Remedies Segments 6

4. Impact of DPCO 1995 7

5. Wholesale Price Index of Selected Components for Different Time Periods 7

6. Growth Rate of Drug Prices from 1982-2002 8

7. Comparative Prices of Selected Drugs 10

8. R & D Expenditure by MNCs in 1996 (millions of US $) 10

9. Time Lag Between Originator and Indian National Firms in Introducinga New Drug in the World Market 14

10. Comparative Picture of Indian and other Developing Country Prices Before

Introduction of Product Patenting 14

11. Prices of Zantac in 1999 15

12. Reduction in the Work Force in Pharmaceuticals Industries 16

13. Some Top Pharma Company Mergers in the World 17

List of Tables

List of Tables and FiguresList of Tables and FiguresList of Tables and FiguresList of Tables and FiguresList of Tables and Figures

1

IntroductionIntroductionIntroductionIntroductionIntroduction1

Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:Economic Reforms and Drug Policy:A Micro Level AnalysisA Micro Level AnalysisA Micro Level AnalysisA Micro Level AnalysisA Micro Level Analysis

* The present paper is the outcome of a detailed empirical exercise carried out by the Centre for Multi Disciplinary Development Research (CMDR),Dharwad as part of its UNDP sponsored project “Economic Reforms and Health Sector in India”. The views expressed in this paper are those of theauthors and do not necessarily reflect the views of GOI, UNDP, IIPA or the collaborating institutions.

The drugs and pharmaceuticals sector has a direct link withthe health care system. Drugs are used to protect, maintainand restore the health of people. The pharmaceuticals in-dustry therefore plays an important role in the provisionof health care. The Indian pharmaceuticals industry is grow-ing and there is increased demand for Indian bulk drugsand generics in other countries. This sector has a long his-tory of internal reforms and has also been affected bygeneral reforms in other sectors. The Indian pharmaceuti-cals industry benefited from the process patent that hadexisted in India since 1970, because companies were ableto produce new drugs introduced by foreign companiesby reverse engineering or by using a different process.However, Indian companies will no longer be able to pro-duce new drugs patented by other companies because, theIndian government has introduced the Indian Patent Bill2005, which recognises product patents. The new Bill islikely to bring in many changes in the pharmaceuticals sec-tor. Though there may not be any major immediate changes,in the long run there could be adverse effects in terms of

price rise, non-availability of new drugs to the poor andmonopoly by foreign companies. This paper addressessome of the issues that influenced the development ofthe pharmaceuticals industry during the reforms period. Abrief discussion on the new Patent Bill is presented in thelatter part of the paper.

The objectives of the paper are to:

Study the challenges to the Indian pharmaceuticals in-dustry in the current era of liberalisation;

Look at the micro level effects of globalisation on theIndian pharmaceuticals industry;

Study the impacts of the dilution of DPCO (DrugPrice Control Order) from time to time since 1986;

Analyse the policy frameworks of DPCO and WTOin relation to the accessibility and availability of thedrugs in India; and

Discuss the overall implications of the product patentregime on the Indian drug sector.

Aravind Badiger, G.K. Kadekodi, Nayanatara S.N. *

2

Economic Reforms and Drug Policy : A Micro Level Analysis

A Macro View of the SectorA Macro View of the SectorA Macro View of the SectorA Macro View of the SectorA Macro View of the Sector

2

The drugs and pharmaceuticals sector is one of the largestcomponents in the category of chemical industries. Outof the total contribution of the chemicals sector to theGDP of India, the share of drugs and pharmaceuticalssector is 35 percent. Since Independence, and more so sincethe 1960s, this sector has had the highest trade advantagecompared to most other chemical sectors1. Compared tothe international situation, life-saving and other drugs wereavailable in India at much lower and affordable prices tothe Indian masses. Pharmaceuticals exports werejust 0.55 percent of the value of total Indian ex-ports in the 1970s and rose to 4.5 percent by theturn of the century. India’s share of the value ofworld pharmaceuticals exports was just about 0.4percent in the 1970s, and rose to over one percentby 19982. Over the last 40 years there has been arising trend in the export of pharmaceuticals fromIndia. Since the 1960s, despite liberalisation, drugprices within India were kept under control throughvarious orders. More importantly, with the estab-lishment of the Drug Price Control Office in 1970,the prices of essential drugs were frozen. Subse-quently all the drugs were categorised as life-sav-ing, essential, less essential and non-essential drugs.Different price control regimes were introducedto provide the Indian population with some secu-rity for health. The trend in the wholesale price in-

dex of drugs and medicines makes it very clear that drugprice control has maintained a steady growth in prices till1998, as can be seen from Figure 1.

The Indian pharmaceuticals industry, which used to de-pend solely on imported medicines and intermediates dur-ing 1950-60, has now emerged as a leader among the de-veloping countries.

How did Indian drug industry make such remarkable

1 Most other important exportables (e.g., gems and jewellery) either enjoyed a monopoly or are based on cultural and traditional linkages.2 All other merchandise exports have been stagnating around 0.6% of world merchandise exports.

Figure 1: WPI of Medicines

Source: Business Beacon, 2001, Centre for Monitoring Indian Economy Pvt.Ltd., Mumbai

3

3 For more details, see Kumar, Nagesh and Jaya Prakash Pradhan (2002).4 This trend has however increased over time.

progress? Was there a reforms process within the drugsand pharmaceuticals sector in India even before the 1990s?A variety of policy instruments were introduced from timeto time to make this industry competitive and yet providehealth care support. Some of the major macro level poli-cies introduced were3:

Introducing IPR (Intellectual Property Rights) for thepharmaceuticals sector in the 1948 Industrial PolicyResolution.

The pharmaceuticals industry was in Schedule B ofthe 1956 Industrial Policy Resolution (where both thestate and private sectors can operate).

Under the Industrial Licensing Policy of 1973, MNCshad permission to retain upto 74 percent of owner-ship (against the general limit of 40% for all otherindustries).

The Hathi Committee recommendations were imple-mented in toto, with a new drug policy from 1978.The major policy implications were: self-reliance indrug technology, self-sufficiency in drug productionand accessibility of quality drugs at affordable prices.In a sense, the 1978 policy constituted land-mark re-forms for the Indian drug sector. All these broughtnew technologies, a shift in production from bulk toformulations and the growth of MNCs in India.

The most important aspect of reform policies wasprice control. A large number of price control or-ders were issued (starting from 1960), to ensure, (a)the welfare of the consumers and (b) encourage theproducers. For instance, while the prices of essentialdrugs were reduced, the producers were given the free-dom to earn reasonable profits on other drugs.

The establishment of DPCO in 1970 was yet anothermajor policy reform (modified in 1979). As many as347 major drugs came under the perview of DPCO.It encouraged small scale enterprises. New bulk drugswere encouraged through R&D (Research and De-velopment). Fiscal incentives such as income tax reliefon in-house R&D expenditure4, capital subsidy viahigher depreciation rates, etc., were introduced.

Finally, as the sector is quite competitive, modifica-tions in DPCO orders were carried out from time totime. In 1987 the scope of DPCO was reduced to166 drugs, in 1995 to 75 and in 2002 to only 39, mak-ing price controls applicable to a smaller number ofdrugs (Figure 2).

Figure 2: Number of Drugs Under DPCO

A Macro View of the Sector

Against this background of the on-going macro-level re-forms process in the drugs and pharamaceuticals sector,this study addresses several micro level issues.

Source: DPCO (1975-1995), Pharma pulse

4

Economic Reforms and Drug Policy : A Micro Level Analysis

A Micro View of the SectorA Micro View of the SectorA Micro View of the SectorA Micro View of the SectorA Micro View of the Sector

3

The industry was established with the birth of BengalChemicals and Pharmaceuticals in 1901. By the turn of thecentury it had grown in size to 21,000 manufacturing units.About 75,000 formulations are being marketed indig-enously. The growth of the Indian pharmaceuticals indus-try was the result of some major policy decisions. Thebiggest source of support to the industry was the decisionto practice process patent regime in India (Indian PatentAct 1970). Further, the decision to have regular controlover the retail price of important drugs through the DPCOchecked any uneven hikes in prices and controlled mo-nopolistic tendencies.

The Indian pharmaceuticals industry today produces acomplete range of formulations i.e., medicines ready forconsumption by patients and about 350 bulk drugs i.e.,chemicals having therapeutic value and used for the pro-duction of the country’s requirement of bulk drugs andalmost all the demands for formulations. India’s total medi-cine market is estimated to be Rs. 127 billion, of which theretail formulations market is Rs. 105 billion. The produc-

tion of bulk drugs and formulations has risen from Rs.38.40 billion in 1990-91 to an estimated Rs.197.37 billionin the year 1999-2000.

With the introduction of economic reforms since the 1990s,there are two major concerns at the manufacturing unit orfirm level. First, whether Indian manufacturing units willbe able to produce the medicines at the present range ofprices with a minimum of expenditure on research. Second,what will be the time lag in making these drugs available tothe Indian masses, once they are brought under liberalisationand WTO regimentation.

This study outlines the micro level effects of globalisationon the Indian pharmaceuticals industry. It aims to studythe impact of the dilution of DPCO from time to timesince 1986. Further, there is an attempt to revoke the policyframework of DPCO and WTO in relation to the acces-sibility and availability of the drugs in India. Essentially, thestudy focuses on the micro-product and unit levels, ratherthan the sectoral levels.

5

Drug Policy in IndiaDrug Policy in IndiaDrug Policy in IndiaDrug Policy in IndiaDrug Policy in India

4

Drug policy in India began with the establishment of theHathi Committee to look into price trends, the competi-tiveness and feasibility of making Indian drug units self-sufficient. There were two major concerns. First, India waslargely dependent on western countries for its supply ofmedicines and intermediates. While the basic drugs wereproduced mainly by foreign units, Indian units producedonly formulations. There was a lack of R&D both in thepublic and private sector. The growing monopoly ofMNCs (multinational companies) in the pharmaceuticalsindustry was a concern. Second, though Indian drug priceswere quite low relative to international prices, the MNCstried to produce many non-essential drugs and kept theprices of essential drugs high relative to the purchasingpower of the Indian masses.

Based on the recommendations of the Hathi Committee,the DPCOs of 1978 and 1979 were established. For thefirst time, a comprehensive price control was introducedin the drug industry (though a few measures had alreadybeen in force since 1970). The new DPCO then groupedthe drugs into four categories:

1. Category – I (Life saving)

2. Category – II (Essential)

3. Category – III (Less essential)

4. Category – IV (Non-essential / simple remedies)

Among these, the prices of the first three categories werecontrolled with mark up (profits allowed) of 40 percent,

55 percent and 100 percent, respectively. In all, 347 drugs(about 90%) came under these price control categories.The philosophy behind the graded system was to makeessential drugs cheaper. This approach of control on theprice of essential drugs resulted in a shift in the productionpattern and this made it more difficult to avail essentialmedicines (Table 1).

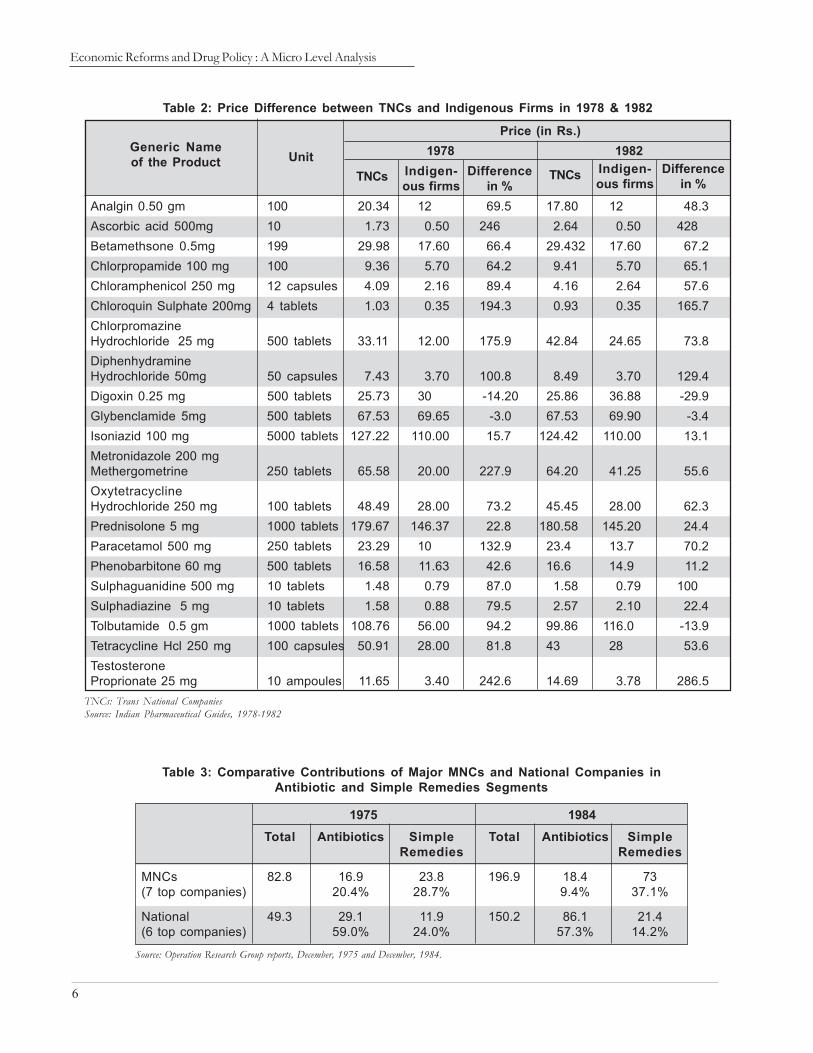

A second major reform at the manufacturing unit leveltook place around the same time with the liberalisationprocess. The MNCs pressurised the government to re-duce the number of drugs under the DPCO. The govern-ment decontrolled some of the drugs from the purviewof the DPCO in 1987, reducing them to 166. There was ahike in the price of a few decontrolled drugs. Further, theprice difference between drugs supplied by TNCs andindigenous firms became very significant (Table 2).

From 1975 to 1984 there was an increase in the manufac-ture of non-essential drugs by the MNCs as the profitmargin was higher in this segment than in essential drugsfalling under the DPCO (Table 3).

Table 1: Drug Production in Response toPrice Policy (percent)

Source: T. L.Narayana (1982).

DPCO Category 1978 1979 1980

I Life saving 4.5 4.2 3.6II Essential 16.7 14.8 13.2III Marginal 67.1 67.0 68.6IV Decontrolled 11.7 13.2 14.6

6

Economic Reforms and Drug Policy : A Micro Level Analysis

Analgin 0.50 gm 100 20.34 12 69.5 17.80 12 48.3Ascorbic acid 500mg 10 1.73 0.50 246 2.64 0.50 428Betamethsone 0.5mg 199 29.98 17.60 66.4 29.432 17.60 67.2Chlorpropamide 100 mg 100 9.36 5.70 64.2 9.41 5.70 65.1Chloramphenicol 250 mg 12 capsules 4.09 2.16 89.4 4.16 2.64 57.6Chloroquin Sulphate 200mg 4 tablets 1.03 0.35 194.3 0.93 0.35 165.7ChlorpromazineHydrochloride 25 mg 500 tablets 33.11 12.00 175.9 42.84 24.65 73.8DiphenhydramineHydrochloride 50mg 50 capsules 7.43 3.70 100.8 8.49 3.70 129.4Digoxin 0.25 mg 500 tablets 25.73 30 -14.20 25.86 36.88 -29.9Glybenclamide 5mg 500 tablets 67.53 69.65 -3.0 67.53 69.90 -3.4Isoniazid 100 mg 5000 tablets 127.22 110.00 15.7 124.42 110.00 13.1Metronidazole 200 mgMethergometrine 250 tablets 65.58 20.00 227.9 64.20 41.25 55.6OxytetracyclineHydrochloride 250 mg 100 tablets 48.49 28.00 73.2 45.45 28.00 62.3Prednisolone 5 mg 1000 tablets 179.67 146.37 22.8 180.58 145.20 24.4Paracetamol 500 mg 250 tablets 23.29 10 132.9 23.4 13.7 70.2Phenobarbitone 60 mg 500 tablets 16.58 11.63 42.6 16.6 14.9 11.2Sulphaguanidine 500 mg 10 tablets 1.48 0.79 87.0 1.58 0.79 100Sulphadiazine 5 mg 10 tablets 1.58 0.88 79.5 2.57 2.10 22.4Tolbutamide 0.5 gm 1000 tablets 108.76 56.00 94.2 99.86 116.0 -13.9Tetracycline Hcl 250 mg 100 capsules 50.91 28.00 81.8 43 28 53.6TestosteroneProprionate 25 mg 10 ampoules 11.65 3.40 242.6 14.69 3.78 286.5

Price (in Rs.)1978 1982Generic Name

of the Product UnitTNCs Indigen-

ous firmsDifference

in %TNCs Indigen-

ous firmsDifference

in %

TNCs: Trans National CompaniesSource: Indian Pharmaceutical Guides, 1978-1982

Table 2: Price Difference between TNCs and Indigenous Firms in 1978 & 1982

Table 3: Comparative Contributions of Major MNCs and National Companies inAntibiotic and Simple Remedies Segments

1975 1984Total Antibiotics Simple Total Antibiotics Simple

Remedies Remedies

MNCs 82.8 16.9 23.8 196.9 18.4 73(7 top companies) 20.4% 28.7% 9.4% 37.1%

National 49.3 29.1 11.9 150.2 86.1 21.4(6 top companies) 59.0% 24.0% 57.3% 14.2%

Source: Operation Research Group reports, December, 1975 and December, 1984.

7

1982 1992 1994 2002

Drugs and Medicines 53.6 85.7 100 252.5Pencillins 49.9 95.9 100 129.6Vitamin Liquid 47 64.3 100 103.2Ayurvedic Medicines 31.1 80.9 100 190.3Antibiotics NA NA 100 127.7

Table 5: Wholesale Price Index of SelectedComponents for Different Time Periods

Source: Business Beacon (2001), Centre for Monitoring Indian Economy Pvt.Ltd., Mumbai.

The liberalisation policy contin-ued and there was a further re-duction in drugs under the con-trol of the DPCO. By 1995, asfew as 73 and by 2002 only 39drugs remained under the pur-view of the DPCO (Figure 2).The outcome of the dilution ofthe DPCO was evident in theincrease in drug prices in India(Table 4), particularly in the caseof decontrolled drugs. The av-erage increase in price of 18 ma-jor drugs was observed to be44.6 percent during 1993-1999.The average change in this pe-riod was mainly due to decon-trolled drugs, which contributedto the extent of 70.9 percentwhile the controlled drugs con-tributed only18.2 percent. Theliberalisation policy highlightedthe significance of the PatentAct 1970, which helped the In-dian pharmaceuticals industrydevelop generic versions of theexisting drugs.

Figure 1 and Tables 5 and 6show the wholesale price indexand its growth rate during the period 1982 - 2002.Therate of growth in drugs and medicine prices was 11percent after the recent reforms.

Invariably, fixing the criteria for keeping or withdraw-ing drugs from the DPCO was the most difficult task.It was observed that every time the drugs were broughtout of the DPCO, their prices increased. This was mainlydue to the criteria used by DPCO. The DPCO consid-ers the total sale, monopoly and competition in theproduction and marketing of a particular drug. The con-cept of essentiality is misquoted in this context. Any drugwhich has sales less than the prescribed quantity (based on

demand) automatically comes out of the purview of theDPCO. Prices of drugs under the DPCO have often beenless than the ceiling price fixed by DPCO/NPPA (Na-

Name of the drug Retail prices in Rupees % Change1993 1999

Controlled drugs

Chloroquin phosphate tablet 150 mg. 0.52 0.90 73.0Cloxacillin capsule 500 mg. 3.80 4.50 18.4Ciprofloxacin tablet 250 mg. 7.10 3.56 -49.8Doxycycline tablet 100 mg. 2.10 3.20 52.4Erythromycin tablet 250 mg. 2.92 3.50 19.8Famotidine tablet 20 mg. 2.10 0.60 -71.4Griseofulvin 250 mg. 1.55 2.10 35.5Penicillin G tablet 500 mg. 0.80 1.00 25.0Tetracycline tablet 250 mg. 0.90 1.45 61.1

Average Change 18.2Decontrolled drugs

Amoxycilline Capsule 250 mg. 2.43 3.40 39.9Ampicillin capsule 250 mg. 1.69 2.95 74.5Albendazole tablet 400 mg. 5.89 11.80 100.3Cephalexin capsule 250 mg. 4.10 5.80 41.4Co-trimaxazole DS tablet 0.80 1.55 93.7Diclofenac sodium tablet 50 mg. 0.71 0.90 26.8Paracetamol 500 mg. 0.29 0.50 72.4Nifedipine tablet 10 mg. 0.58 0.90 55.2Vitamin B complex tablet 0.49 1.15 134.7

Average Change 70.9 Average change (All) 44.60

Source: CIMS, Sep-Dec,1993 and Sep-Dec,1999.

Change in Retail price of 18 drugs 1993-1999

Table 4: Impact of DPCO 1995

A Macro View of the Sector

8

Economic Reforms and Drug Policy : A Micro Level Analysis

1982-2002 Before During RecentReforms Reforms

Drugs and Medicines 8.05 4.5 11Pencillins 4.8 7.5 2.5Antibiotics - - 3.1

Table 6: Growth Rate of Drug Prices from 1982-2002

tional Pharmaceutical Pricing Authority). The system ofceiling price is slowly becoming obsolete due to market-driven prices. Thus the role of the DPCO is effective onlyif the producer charges monopoly prices over and abovethe ceiling prices. Thus, two forces acted simultaneously.While the prices of drugs going out of the DPCO’s con-trol increased, the competition driven market succeeded inkeeping the prices of such drugs below the level fixed bythe DPCO/NPPA. Competition among the decontrolleddrugs emerged due to the process patent, which permitsany manufacturer to produce any drug by opting for some

alternative processes. Furthermore, it is the func-tion of the NPPA to keep a watch on the pricesof drugs and to fix the ceiling price for newdrugs/dosage forms.

The DPCO was also finding it increasingly diffi-cult to fix the drug prices due to the increasing

number of formulations (about 75,000) resulting from therelaxation in the patenting system. Also, the time taken bythe authorities to fix a ceiling price for the formulations andthe bulk drug was too long, leading to problems in theproduction of the required drugs. Further, the need for theDPCO’s intervention to control prices occurred only ifmonopoly prices were charged. However, the process patentsystem enabled India to develop into a technologically ad-vanced country in the field of bulk drugs. The followingsection therefore reviews the patent system in India.

9

Patent ScenarioPatent ScenarioPatent ScenarioPatent ScenarioPatent Scenario

5

Source: http://www.indioppi.com/keystat.htm and Human Development Report (2000), UNDP, P.No.178.

Figure 3: Expenditure on Medicines as % of Per Capita Income

India has been practising the process patent system in whichone can patent the process, but not the product. In otherwords, a producer can produce a given product through adifferent process. The policy helped the Indian pharma-ceuticals industry in many ways. India is the only countrythat had the option to reverse engineer patented drugs andproduce generic versions. The generic version will alwaysbe available at a lower price because it requires less time,money and energy to produce the molecule. Further, themanufacturer will not be paying royalty to the patent holder.Moreover the system makes it possible for individuals topatent the reverse engineered scheme.

As a result, India is enjoyinglow cost medicines comparedto the rest of the world. Inthe context of the purchas-ing power or the income perhead, the expenditure onmedicine in India can be con-sidered to be relatively low(Figure 3 and Annexure I).

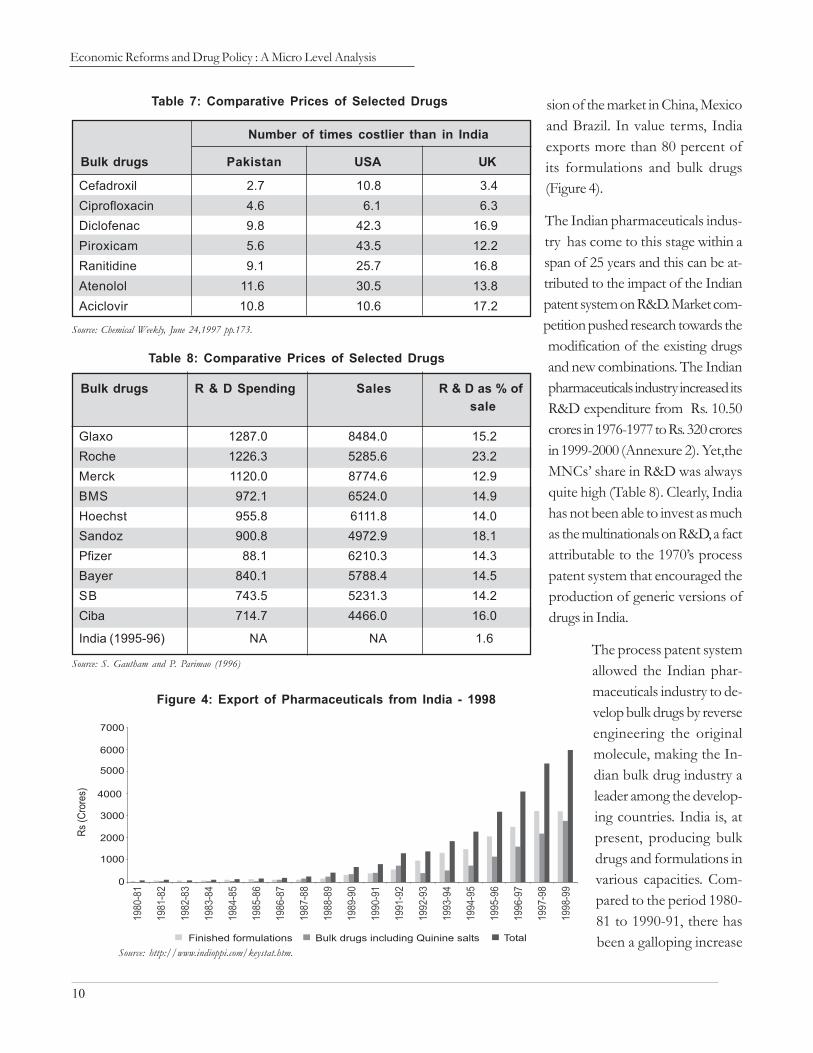

It can be safely inferred thatIndians can access medi-cines at much lower pricesthan other countries likeUSA, UK, Pakistan, etc.(Table 7). There has been acontinuous decline in theshare of medicines and

pharmaceuticals in total imports from 1991 onwards. Thisshows that the Indian pharmaceuticals industry is becom-ing self-sufficient and is capable of making indigenouspreparations. In fact, the export data clearly reveals theemerging technological hold that India has due to which itis supplying drugs to most of the developing and devel-oped countries in various capacities. Between 1994 and2001, India exported medicines and pharmaceuticals mainlyto USA (10 to 12%), Russia (11 to 6%), Germany (11 to5%), Hongkong (4 to 5%), Netherlands (4 to 2%) andNigeria (3.5 to 4%). Exports to Russia, Germany, Nether-lands, Italy and Japan have declined, while there is expan-

10

Economic Reforms and Drug Policy : A Micro Level Analysis

Source: S. Gautham and P. Parimao (1996)

Table 8: Comparative Prices of Selected Drugs

Glaxo 1287.0 8484.0 15.2Roche 1226.3 5285.6 23.2Merck 1120.0 8774.6 12.9BMS 972.1 6524.0 14.9Hoechst 955.8 6111.8 14.0Sandoz 900.8 4972.9 18.1Pfizer 88.1 6210.3 14.3Bayer 840.1 5788.4 14.5SB 743.5 5231.3 14.2Ciba 714.7 4466.0 16.0

India (1995-96) NA NA 1.6

Bulk drugs R & D Spending Sales R & D as % ofsale

sion of the market in China, Mexicoand Brazil. In value terms, Indiaexports more than 80 percent ofits formulations and bulk drugs(Figure 4).

The Indian pharmaceuticals indus-try has come to this stage within aspan of 25 years and this can be at-tributed to the impact of the Indianpatent system on R&D. Market com-petition pushed research towards themodification of the existing drugsand new combinations. The Indianpharmaceuticals industry increased itsR&D expenditure from Rs. 10.50crores in 1976-1977 to Rs. 320 croresin 1999-2000 (Annexure 2). Yet,theMNCs’ share in R&D was alwaysquite high (Table 8). Clearly, Indiahas not been able to invest as muchas the multinationals on R&D, a factattributable to the 1970’s processpatent system that encouraged theproduction of generic versions ofdrugs in India.

The process patent systemallowed the Indian phar-maceuticals industry to de-velop bulk drugs by reverseengineering the originalmolecule, making the In-dian bulk drug industry aleader among the develop-ing countries. India is, atpresent, producing bulkdrugs and formulations invarious capacities. Com-pared to the period 1980-81 to 1990-91, there hasbeen a galloping increase

Source: Chemical Weekly, June 24,1997 pp.173.

Table 7: Comparative Prices of Selected Drugs

Cefadroxil 2.7 10.8 3.4Ciprofloxacin 4.6 6.1 6.3Diclofenac 9.8 42.3 16.9Piroxicam 5.6 43.5 12.2Ranitidine 9.1 25.7 16.8Atenolol 11.6 30.5 13.8Aciclovir 10.8 10.6 17.2

Bulk drugs Pakistan USA UK

Number of times costlier than in India

Figure 4: Export of Pharmaceuticals from India - 1998

Source: http://www.indioppi.com/keystat.htm.

11

Patent Scenario

in the production of formulationsand bulk drugs (Figure 5). Thegrowth in bulk drug productionpushed the formulations as well.

5.1 Why Do We5.1 Why Do We5.1 Why Do We5.1 Why Do We5.1 Why Do WeNeed a System ofNeed a System ofNeed a System ofNeed a System ofNeed a System ofPatents?Patents?Patents?Patents?Patents?

In the context of examining thereforms process it is worthwhileto discuss certain basic aspects ofthe patent system. First of all, arepatents really essential? What istheir impact on developing coun-tries like India? Is the present sys-tem beneficial to the people inIndia? How are we going to copewith issues such as upcoming chal-lenges by MNCs?

IPRs are a subset of property rights. A number of theo-ries have been put forward to explain why patents areneeded. The natural rights theory suggests that the creatoris entitled to the intellectual fruits of his or her labour, en-abling him or her to either prohibit others or charge aroyalty for using the outcome of the creator’s labour. Theprospect theory of patents (Kitch, 1977) posits that therationale for granting patents is not so much a reward forpast innovative activity, but an incentive for (future) devel-opmental activity. This perspective is consistent with con-siderations such as commercial success.

Patent laws are not free from social costs. First, higher pricesmay be charged for patented products. There are also highertransaction costs due to inefficiencies caused by patents oninventions that would have been made without patent pro-tection. Further, there are the costs of patent administra-tion and patent application. The costs incurred by the patentadministration system include the cost of processing ap-plications, the cost of granting applications and the costof adjudicating disputes. Costs incurred by patent appli-

cants include the cost of maintaining corporate patent de-partments, cost of patent counsel and lobbying activitiestoward influencing patent policy.

Patents in the pharmaceuticals industry play a particularlyimportant role. Pharmaceutical innovation is quite costly.Development of a new drug can take 10 to 15 years andcost more than $500 million (Sudarshan, 2002). Moreover,the success rates for the complete process of drug devel-opment from synthesis to market approval have been es-timated at less than 0.1 percent. While development ofdrugs is a lengthy and expensive process, their imitation isoften simple and inexpensive, leading to significant rev-enue loss for innovating firms. A study by the Pharmaceu-tical Manufacturers Association reported that in 1984,unauthorised sales of patented U.S. pharmaceuticals by localfirms in just five foreign countries amounted to $192 mil-lion, while the concomitant sales by U.S. firms were $162million (Mossinghoff, 1987). Therefore, effective patentprotection is a necessary incentive to pharmaceutical andchemical research.

Figure 5: Production of Formulations and Bulk Drugs in India

Source: http://www.indioppi.com/keystat.htm.

12

Economic Reforms and Drug Policy : A Micro Level Analysis

5.25.25.25.25.2 Arguments Against Patents inArguments Against Patents inArguments Against Patents inArguments Against Patents inArguments Against Patents inPharmaceuticalsPharmaceuticalsPharmaceuticalsPharmaceuticalsPharmaceuticals

There are some cogent arguments against patents for phar-maceutical products. First, while patents are needed forpharmaceutical innovation, prices are higher for patentedpharmaceutical drugs. This price differential becomes evi-dent when drugs lose their patent protection. For instance,Griliches and Cockburn (1994, p.1214) noted that whenthe patent on the incumbent firm’s product expires, sev-eral generic versions appear relatively quickly, selling at muchlower prices, typically 30 to 50 percent cheaper than theoriginal versions. Second, availability of patents for certainpharmaceutical products, and their higher prices, may makethe pharmaceuticals industry less enthused to develop non-patented products that are necessary from a public healthpolicy perspective, but are not profitable to the innovator.Third, patents may polarise the market in favour of largerfirms, which have the resources to invest in R&D and driveout smaller firms, which have essentially been producingcopies of drugs. In a developing economy, this might meanthat foreign multinationals supplement indigenous manu-facturers, as the latter cannot afford to invest huge resourcesin R&D. The absence of product patents may provide an

environment conducive to indigenous participation in thepharmaceuticals industry. Redwood (1994) points out that,in the 23 years since the introduction of the Indian PatentsAct in 1970, Indian ownership of drug firms increasedfrom 20 percent in 1970 to 61 percent in 1993. Fourth, it isnot clear that granting product patents will encourage fur-ther investment in pharmaceutical R&D. Deardorff (1992)argues that the availability of product patents for drugs isnot likely to substantially encourage new pharmaceuticalR&D, given diminishing returns in new drug development.Hamied also supports this view (cited in Cherukuri, Ravi,1999). Finally, on humanitarian grounds, it can be arguedthat essential drugs should be available to fight life-threat-ening diseases irrespective of the patients’ ability to pay.

Even though the Indian pharmaceuticals industry is enjoy-ing the existing patent system, it will have to change tocomply with WTO regulations. A large section of the In-dian population lives below the poverty line and will notbe able to afford the high cost of medicines that will enterthe market with enforcement of product patents. Obser-vation of developing countries with product patents makesit apparent that this is an area of concern.

13

Economic Reforms of 1990s, Implications ofEconomic Reforms of 1990s, Implications ofEconomic Reforms of 1990s, Implications ofEconomic Reforms of 1990s, Implications ofEconomic Reforms of 1990s, Implications ofWTO Commitments and TWTO Commitments and TWTO Commitments and TWTO Commitments and TWTO Commitments and Trade Liberalisationrade Liberalisationrade Liberalisationrade Liberalisationrade Liberalisation

6

The New Economic Policy was introduced in India in June1991. The Industrial Policy was also reformed in July 1991.GATT regulations were modified in 1994. WTO was es-tablished in January 1995. All these internal and externalreforms have influenced the performance of the drug andpharmaceuticals sector during the 1990s.

Under WTO, several objectives were incorporated (fol-lowing from the Uruguay Round in 1995). Among them,the Agreement on Trade Related Aspects of IntellectualProperty Rights (TRIPS), Agreement on Subsidies andCountervailing Measures, Sanitary and Phyto-sanitary Regu-lations and Agreement on Technical Barriers are directlyrelevant for this sector. The major changes introduced inIndia under WTO are:

A two-tier tariff structure, making essential drugs avail-able at zero tariff and countervailing duty rates; whereasall other drugs are at 30 percent tariff and 16 percentcountervailing duty.

TRIPS agreements on technical matters extended to20 years from the existing seven and 14 years.

India agreeing to opt for switching to product pat-enting from 2005.

As part of TRIPS, the Drug Development Promo-tion Foundation, Pharmaceutical Research and Devel-opment Support Fund, and National PharmaceuticalPricing Authority (NPPA in 1997) have come intoexistence since 2002 in place of DPCO.

The new economic policy (1991) also changed the restric-tions on foreign ownership, by raising the ceiling on for-eign equity holding to 51 percent, which was further raisedto 100 percent by December 2001. Till the NPPA cameinto existence, DPCO kept reducing the number of drugsunder price control based on the annual turnover. Similarmodifications were made for the units in formulations.

Under the WTO norms imposed from 2005 onwards,drugs can no longer be produced generically. This willchange the drug supply considerably, as access to inexpen-sive medicines, relative to the rest of the world, will nolonger be available. Since the prevailing process patent re-gime allows the industries to market the reverse engineeredform of the patented drugs without paying any penalty,firms were able to reproduce the drug in three to fouryears without violating the Process Patent Laws (Table 9).

6.16.16.16.16.1 Effect of WTO/TRIPS: SomeEffect of WTO/TRIPS: SomeEffect of WTO/TRIPS: SomeEffect of WTO/TRIPS: SomeEffect of WTO/TRIPS: SomeCase StudiesCase StudiesCase StudiesCase StudiesCase Studies

There is a fear that implementation of WTO and TRIPSregulations will worsen access to the health care systems indeveloping countries. Watal (2000; 2001) has analysed thisusing several case studies.

WTO implementation can worsen the situation throughTRIPS regulations, which may ultimately result in increasedprices. Indian companies including Cipla and Cadila cameup with the generic version of sildanafil citrate and Pfizer

14

Economic Reforms and Drug Policy : A Micro Level Analysis

the innovator of the drug went out of the Indian market.Indian companies marketed the drug at a considerablylower price, based on low costs due to reverse engineer-ing. Table 10 shows that Indian companies are selling thepatented drugs at a rate far lower than other developingcountries and the world market. In fact, Indian firms areexporting the medicines to countries like Thailand. WillIndian firms be able to give the drugs at the same priceafter 2005? Prices are expected to go up by over 100 per-cent after product patenting is introduced.

The WTO rules are complex and appear to permit some

Source: B.K. Keayla (1998)

Table 9: Time Lag Between Originator and Indian National Firms inIntroducing a New Drug in the World Market

Captopril 1981 1985Ranitidine 1983 1985Acyclovir 1985 1988

Ciprofloxacin 1985 1989

By originator in the By Indian national firmsin the world market in the world market

Drug Year introduced

Acyclovir 200 mg Glaxo-Welcome/Zovirax Tongo 50 Indonesia 371 1:7Acyclovir 800 mg Glaxo- Welcome/Zovirax India 94 South Africa 790 1:8Atenolol 25 mg Zenaca/Tenormin India 03 Camerom 53 1:18Ciprofloxacin 500 mg Bayer/Ciproxin India 15 Mozambique 740 1:49Diclofenac 50 mg Novartis/Voltarin India 02 Argentina 118 1:59Nifedipine 20 mg Seneca/ Adalat

Bayer Corporation India 03 Peru 96 1:32Omeprazole 20 mg Astra/ Losec Zambia 30 Brazil 477 1:11Ranitidine 150 mg Glaxo- Welcome/Zantac India 20 South Africa 116 1:58Zidovudine 100 mg Glaxo-Welcome Pakistan 81 Argentina 316 1:4

Source: Bala K. and Kiran Sagoo (2000)

Table 10: Comparative Picture of Indian and other Developing Country PricesBefore Introduction of Product Patenting

Generic nameof drug

Originator/Proprietaryname

Country Price Country Price

Lowest Highest

Retail prices of 100 units in USD Ratioof

low :high

Comment: Comparison of lowest and highest retail prices in USD for 100 units of proprietary brands of nine drugs in developing countries.

exceptions, with countries able to“adopt measures necessary toprotect public health and nutri-tion.” This is supposed to allowthe granting of “compulsorylicenses” for the production ofvital drugs. It is also supposed toallow “parallel importing” ofpatented drugs, i.e., their purchasefrom whoever sells them thecheapest. The difficulty is beingable to utilise the rules permitting

exceptions. Most developing countries, including India, donot have a pharmaceuticals industry that is capable of pro-duction on a scale that can act on the basis of such ‘excep-tions’ and bring down drug prices. They are only allowedto import cheap “generic” drugs (copies of expensive drugspatented by Western companies), usually produced in coun-tries such as India, Brazil and Thailand, if a compulsorylicense has been issued in the exporting country. Even inthis case, the TRIPS agreement specifies that a compulsorylicense can only be issued for “predominantly” domesticneeds. What is more, compulsory licensing can only beobtained after efforts have been made to obtain a regular

15

license from the patent holder on commercial terms andif the patent holder is compensated. The WTO rules ef-fectively mean, ‘Governments will no longer be permittedto allow local companies to produce, market and exportcopies of patented drugs’. At present, there are a range ofexamples of the staggering difference in prices betweenpatented and generic drugs. Zantac, used to treat gastriculcers, costs between 15 and 50 times more in the US andEurope respectively, than its generic version made in In-dia5. When WTO rules are applied in India, drug pricescould rise significantly as a result of patenting (Table 11).

There are newer problems arising now. Oxfam (2001)points to the vast increase of new strains of diseases, in-cluding malaria and tuberculosis, which can only be treatedby recently developed patented drugs. For example, aWorld Health Organisation (WHO) study has shown thatin the case of pneumonia, which kills 3.5 million peopleannually, medications that were formerly effective now failin 70 percent of cases because of drug resistance. A newrange of antibiotics is being patented that will beunaffordable in developing countries. To ensure that thepoorer countries do not find ways of using compulsorylicensing or parallel importing to avoid WTO rules, themajor pharmaceutical companies are using what is describedas “armies of lawyers” to press their case.6 In 1997, theSouth African government passed a law sanctioning theuse of compulsory purchasing and parallel importing forAIDS drugs and other medicines. Introduced in 1988, the“Special 301” provision of the US government is used toimpose trade sanctions on countries to enforce compli-ance with WTO rules. India, the Dominican Republic, Ar-gentina, Vietnam and Thailand all face Special 301 sanc-tions by the US over patenting rules for medicines.

6.2 Patent Barriers to Access to6.2 Patent Barriers to Access to6.2 Patent Barriers to Access to6.2 Patent Barriers to Access to6.2 Patent Barriers to Access toMedicines at WTO: A ReviewMedicines at WTO: A ReviewMedicines at WTO: A ReviewMedicines at WTO: A ReviewMedicines at WTO: A Review

Since the provisions under WTO allow protection of 20years for the patented product, it is likely that patent hold-ers will have a monopoly over the market, which ultimately

may lead to an increase in prices of the patented products.The patent system is likely to affect availability of new drugs,particularly for the treatment of cancer, AIDS, blood pres-sure, diabetes, TB, etc. So a poor man cannot afford treat-ment involving new medicines even, if it is necessary orbeneficial. Yet, the new patent system or WTO provisionsmay not affect the availability of basic or essential drugs,which are already in the market and those which are non-patented or for which the patent period is over. Indiancompanies can produce generic versions of drugs patentedbefore 1995, the year in which India adopted the TRIPSagreement.

Indians may have access to new drugs, if Indian compa-nies can reverse-engineer new patented drugs, brought undercompulsory licensing by the government because of theirsignificance to public health. In the past, Indian companieshave shown that they can produce patented drugs within ashort period. This may also be beneficial to other devel-oping countries, which do not have a strong pharmaceuti-cals industry base. However, this depends on the stage atwhich compulsory licensing is issued by the governmentand at what price (payment of royalty) it is available toIndian companies. The other option to minimise the im-pact of WTO on the availability of new drugs is to pro-

Note: The ratio of the lowest to the highest price of a multi-source drug, Zantacin developing countries is 1:58. It is US $2 per 100 units in India and Nepalwhile it is $116 in South Africa.

Table 11: Prices of Zantac in 1999

India 2Nepal 2Pakistan 21Korea 61Zambia 82Bolivia 94Senegal 100Burkina Faso 105South Africa 116

Countries Price in USD

5 If a country can import the drug fluconazole used in the treatment of cryptococcal meningitis, (an infection associated with AIDS) from Thailand,the annual cost of treatment would be $104. However, Pfizer, the company owning the patent on the drug, charges $3,000 for an annual course oftreatment and is applying pressure through the WTO to stop Thailand from exporting the drug.

Economic Reforms of 1990s, Implications of WTOCommitments and Trade Liberalisation

6 An indicator of the vast economic power of transnational corporations is Pfizer’s whose earnings are greater than the Gross Domestic Product ofmost developing countries.

16

Economic Reforms and Drug Policy : A Micro Level Analysis

duce alternative medicines for the treatment of diseasesfor which patented drugs are available. Government in-centives in the nature of provision of infrastructure andremoval of administrative hurdles are also necessary forpromoting R&D in the pharmaceuticals sector.

We need to watch how India will overcome the challengesof monopoly and price rise that are likely to be broughtabout by the new patent system.

6.36.36.36.36.3 Globalisation: A ThreatGlobalisation: A ThreatGlobalisation: A ThreatGlobalisation: A ThreatGlobalisation: A Threat

The effect of globalisation on the pharmaceuticals sectorneeds to be examined. Case studies have already provedthat the medicines that are going to be invented after 2005will be expensive and inaccessible. Added to this is the factthat the pharmaceuticals industry in India will have to facestiff competition from the multinationals, which have a stra-tegic plan to introduce their products in the Indian market.

One strategy has been to shift production to third partymanufacturing units. In their attempt to do this, HindustanCiba Geigy, Roche, Abbot, Boehringer Mannheim, Boots,

Park Davis, Unichem, etc., have already offered a volun-tary retirement scheme to workers, closed their factoriesand sold their factory premises at premium prices. Pfizer,Rhone Poulnec, Hoechst, Glaxo, etc., have reduced theirwork force. Crores of rupees have been spent on volun-tary retirement schemes. These companies are manufac-turing their products with the help of loan licences. Someof them have opened smaller factories in new places andappointed workers with lower wages and heavierworkloads. More casual workers are being appointed. Inthe Mumbai-Thane region of Maharashtra, around 30,000workers have lost their jobs in the pharmaceuticals indus-try in the last two years.

In addition, the distribution workers are gradually beingreplaced by the cost and freight agency system. Under thissystem, the original company does not have any responsi-bility towards the workers. They are employed by agentsand have heavier workloads and lower wages. In the lastdecade, around 15,000 distribution workers have lost theirjobs in the pharmaceuticals industry (Table 12). Moreover,because of the agency system, the government is deprivedof sales tax.

In marketing too, the field workers or the sales promo-tion employees are facing tremendous pressure in the nameof franchise, co-marketing, appointment of communica-tors, etc. Many permanent sales promotion employees arelosing their jobs. Many others are appointed as so-calledexecutives to remove them from the fold of the union.More casual and contractual workers are being recruited.

The total payment on voluntary retirement schemes byfirms like Glaxo, Hoechst, Pfizer, Knoll Pharma, RhonePoulenc, Park Davis, Smith Kline Beecham, Duphar, Bayer,etc., is more than Rs. 200 crores in the last three financialyears. Employment opportunities in these units have beenreduced permanently.

6.46.46.46.46.4 Mergers and AcquisitionsMergers and AcquisitionsMergers and AcquisitionsMergers and AcquisitionsMergers and Acquisitions

International and national level mergers, acquisitions andtakeovers have now become a common phenomenon in

Source: Annual reports of respective companies and interaction with the office bearers ofunions

Glaxo 1995 1564Hoechst 1996 10429Knoll Pharma (Boots) 1995 600 (All workers)Smith Kline Beecham 1995 208E.Merck 1995 194Rhone Poulnec 1996 700Hindustan Ciba Geigy 1993 907Duphar Interferan 1996 154Bayer 1996 590Abbott 1996 All workersRoche 1996 All 320 workersPark-Davis 1997 All 650 workersPfizer 1995 215Unichem 1997 All workers

Company Year Reduction of workforce

Table 12: Reduction in the Work Force inPharmaceuticals Industries

17

the pharmaceuticals industry. Inter-nationally, American Home Prod-uct merged with Cyanamid, SKB(Smith Kline Beecham) with Ster-ling, Rhone Poulenc with Fashions,BSF with Boots, Glaxo withBurroughs Welcome, Ciba Geigywith Sandoz, Warner Hindustanwith Parke Davis, Hoechst withRhone Poulenc, etc. These are someof the examples of big takeovers.Through mergers and acquisitions,these companies became evenlarger, with more financial powerat their disposal relative to theircompetitors (Table 13).

In the coming days, with the helpof international financial compa-nies, the MNCs will capture andtake control of Indian companiesin order to control the Indianmarket.

Companies in India are adopting the international meth-ods of mergers and takeovers. For example, Wockhardttook over Merind and Tata Pharma, Ranbaxy took overCrosslands, Nicholas Piramal took over Roche, Boehringer,Sumitra Pharma. The inevitable result is loss of jobs. Be-cause of overlapping of jobs, a large number of workersare declared surplus. After their merger, Glaxo-Welcomeand Ciba-Sandoz announced a worldwide reduction of15,000 and 10,000 respectively in their work force. Upjohnand Pharmacia decided to close 24 of their 57 plants indifferent countries after their merger.

Some countries are adopting the ‘buy and grow’ method.They are taking over some popular brands and increasing

Source: Compiled from reports published in various newspapers.

Dow Chemicals Marion Labs 1986 6.21Bristol Myers Squibb Corp 1989 12.09Beecham group Smith, Kline & French 1989 7.9American Home Products American Cynamide 1994 9.7Hoffman La Roche Syntex Lab. 1994 5.3Eli Lyly PCS Health System 1994 4Sandoz Gerber 1994 3.7Smith Kline Beecham Sterling 1994 2.9Glaxo Burroughs Wellcome 1995 14.2Hoechst MMD Roussel 1995 7.2Pharmacia Upjohn 1995 7BASF Boots 1995 1.3Ciba Geigy Sandoz 1996 30.1Hoffman La Roche Comage Ltd. 1997 11Astra Zeneca 1998 67

Company Merger Year

Table 13: Some Top Pharma Company Mergers in the World

Value ofMerged

Company(US $)

7 Such mergers are more predominantly observed during the reforms period in the sector and also in the chemical sector in general.

their business. SKB took over Crocin from Duphar,Ranbaxy took over seven leading brands from Gufic, andDr. Reddy’s Lab purchased six products of Dolphin and twoeach from Pfimex and SOL Pharma. Sun Pharma purchasedall the leading brands of NATCO. After selling their popularbrands companies are becoming sick and having to down theirshutters, making the workers jobless.

Government permission to the MNCs to come to India with100 percent equity has threatened the existing companies andtheir workers. Through the process of mergers, acquisitionsand takeovers, MNCs will gradually increase their grip on theIndian industry by creating a limited number of mega compa-nies that have monopoly control and worldwide domination.In the absence of competition, people will have to pay exorbi-tant prices, as happens in a sellers market7.

Economic Reforms of 1990s, Implications of WTOCommitments and Trade Liberalisation

18

Economic Reforms and Drug Policy : A Micro Level Analysis

Evaluation of the Reforms Process in IndiaEvaluation of the Reforms Process in IndiaEvaluation of the Reforms Process in IndiaEvaluation of the Reforms Process in IndiaEvaluation of the Reforms Process in India

7

There is already sufficient evidence to indicate that compe-tition has forced the multinationals to lower their prices tocompete with Indian firms. Interestingly, when faced withcompetition, multinationals do not leave the market. Theylower their prices and stay on to compete with the nation-als. This is due to the size of the Indian market.8 The bestway for the Indian firms to compete is to produce thedrug at very low costs. It takes a few years for manufac-turers to copy products by reverse engineering and enterthe market (Table 9). A short period of three to fouryears is not sufficient for them to capture a sizeable worldmarket share, increase production volume, lower pro-duction costs and effectively compete on price. In thepast, Indian firms were able to market these drugs at abouthalf to one-fourth of the lowest prices of the originatorsof the proprietary drugs. Then, the Indian manufacturershad adequate time to capture a considerable market share,increase production volume, lower production costs andoffer low-priced drugs to consumers.

Time is crucial in introducing generic equivalents of essen-tial drugs, soon after new drugs are put into the market.This enables them to enter into price competition by skil-ful promotion, well before the originators secure brandloyalty for their products. Many of the African countries(where no patent protection exists) surveyed had only theoriginators’ proprietary brands, which are monopoly mar-kets for eight multi-source drugs, while generic equivalentsof these drugs were available in the world market at lowerprices. It will be in the interest of public health to have

low-priced generic drugs available in every developingcountry. This is critical since price is one of the criteria usedby developing countries for selecting drugs for their na-tional list of essential drugs. High cost drugs, for examplesome of the new anti-retroviral drugs for the treatmentof HIV/AIDS, because of their high prices, are not in-cluded in the lists of essential drugs in many developingcountries.

The case studies and Indian data clearly show that there isneed for national policies on the intellectual property sys-tem with provisions to enable national firms to initiate pro-duction of new drugs as early as possible. Indian firmswere able to do this by a process of reverse engineering.This was possible because the Indian national legislationon patents did not provide patent protection for prod-ucts. However, this will change now.

With the TRIPS Agreement taking effect, all member coun-tries of the WTO will have to provide patent protectionfor products and processes for 20 years. The only waynational firms can initiate production is by compulsory li-censing, which is allowed under the TRIPS Agreement.Nevertheless, only a few of the technically advanced de-veloping countries can use compulsory licensing to manu-facture new drugs. The vast majority of developing coun-tries do not have the technical specialisation to producepharmaceuticals. These countries depend on imports ofraw materials and finished products. They can have accessto lower priced drugs produced in the more advanced

8 Another example comes from Bolivia where 100 units of 100 mg of Retrovir (zidovudine) were priced at US$626 in 1997. Prices dropped to US$258in 1998 when the competitor’s product of zidovudine was made available and sold at US$427

19

developing countries or by generic manufacturers in somedeveloped countries only by parallel importing. Parallelimport or trade in patented articles is governed by the ‘ex-haustion of rights’ doctrine, which stipulates that once theproducer of a patented item has sold the product, thepatent holders’ right to determine the conditions underwhich the product is resold are exhausted (Misra et al 2003).Parallel importing arises due to differential pricing of pat-ented products in different markets. Parallel importing en-ables the sale of patented products from a country whereit is cheaper, to other countries where the prices may be

higher. This is also allowed under the TRIPS Agreement.This study shows that India can take advantage of thissituation (Tables 10 and 11).

Furthermore, in the interest of all developing countries in-cluding India, compulsory licensing and parallel imports aretwo provisions, which should be included in all national leg-islations on IPRs. The TRIPS Agreement allows these provi-sions to be included in the national legislation on prices. Thiswill enable developing countries to have regular access togood quality essential drugs at affordable prices.

Evaluation of the Reforms Process in India

20

Economic Reforms and Drug Policy : A Micro Level Analysis

The New Patent Bill: Some ObserThe New Patent Bill: Some ObserThe New Patent Bill: Some ObserThe New Patent Bill: Some ObserThe New Patent Bill: Some Observationsvationsvationsvationsvations

8

The Indian Patent Amendment Bill,The Indian Patent Amendment Bill,The Indian Patent Amendment Bill,The Indian Patent Amendment Bill,The Indian Patent Amendment Bill,20052005200520052005

The Indian Patent Amendment Bill, 2005 was passed inParliament on 22nd March, 2005 reflecting India’s supportto the WTO product patent regime. The new patent re-gime is applicable from January 1st, 2005. Under the newpatent regime, India shifted from process patent to prod-uct patent, making it illegal for domestic companies to makegeneric copies of patented drugs. The Bill enables the In-dian government to grant product patents to pharmaceu-tical and agrochemical inventions. The patent mailbox al-ready has 8,926 applications in it for the period 1995-2005.Around 84 percent of these applications are from foreigncompanies.

Important Provisions of Patent Bill, 2005A patented product has to be a new entity, involvingone or more innovative steps.

The new Act restricts ‘ever-greening’ i.e., there is noprovision for placing new-use patents for the alreadypatented drugs.

A system of automatic licensing, which allows genericmanufacturers already producing and marketing a drugthat gets a patent from the Indian Patent Office tocontinue production after paying a ‘reasonable roy-alty’ to the patent holder.

Provision for ‘compulsory licensing’ allowing compa-nies other than the patent holder to manufacture pat-ented drugs under license. The government has the

power to issue a ‘compulsory license’ in the public in-terest.

Generic manufacturers have to wait three years after apatent is granted to a particular medicine before theycan apply for a compulsory license to manufacture it.

There is provision for allowing the patent holder tocontest ‘compulsory licensing’.

Patent protection is applicable for a period of 20 years.

The introduction of the Indian Patent Amendment Bill,2005 has made India shift from process patent to productpatent as per the provisions of WTO. Article 28 of theTRIPS Agreement removes the distinction between prod-uct and process patent and recognises only product patent,wherein the process for making the product is implicitlypatented. As such, no manufacturer can produce the pat-ented product using different methods or processes. Thenew Patent Bill in India provides patent protection for aperiod of 20 years, up from the existing period of sevenyears. Under the process patent, manufacturers adopteddifferent processes to produce a patented product, butproduct patent does not allow manufacturing and sale ofpatented products without proper authorisation. Productpatent is supposed to be an incentive to pharmaceuticalcompanies who make huge investments in research and islikely to boost research on the treatment of various dis-eases. A majority of the companies that have applied forpatents in India are foreign. Exceptions include Dr. Reddy’sLaboratories who have also applied for patents in India.

21

The new Patent Bill provides for some precautionary mea-sures to prevent misuse of patents. The Bill specifies “newentity”, which does not allow “ever greening” of patentsby companies trying to extend the period of a patenteddrug by introducing the same product with minor changes.

Companies have to show one or more inventive steps inthe production of the new drug. The Bill also provides forcompulsory licensing, which may be issued by the govern-ment in the case of high prices of patented drugs and inthe interest of public health.

The New Patent Bill: Some Observations

22

Economic Reforms and Drug Policy : A Micro Level Analysis

Medecins Sans Frontieres’ (MSF) Views onMedecins Sans Frontieres’ (MSF) Views onMedecins Sans Frontieres’ (MSF) Views onMedecins Sans Frontieres’ (MSF) Views onMedecins Sans Frontieres’ (MSF) Views onIndia’India’India’India’India’s Role in the Prs Role in the Prs Role in the Prs Role in the Prs Role in the Provision of Drovision of Drovision of Drovision of Drovision of Drugs:ugs:ugs:ugs:ugs:

Expressions on the Indian Patent Bill, 2005Expressions on the Indian Patent Bill, 2005Expressions on the Indian Patent Bill, 2005Expressions on the Indian Patent Bill, 2005Expressions on the Indian Patent Bill, 2005

9

Examining the amendments that were proposed un-der the Indian Patents Act, 1970, MSF reacted by say-ing that they will restrict and prevent the productionand supply of vital therapies by Indian pharmaceuti-cal companies to other developing countries.

MSF has recognised India’s role in treating AIDS indeveloping countries. In its letter to the President ofIndia, MSF writes that out of 7,00,000 people whoreceive antiretroviral treatment in developing countries,an estimated 50 percent rely on Indian generic pro-duction and 70 percent of the AIDS patients treatedby MSF in 27 countries around the world use medi-cines that originate in India. These drugs cost aboutfive percent of the price of similar drugs sold by phar-maceutical companies in the US and the European

Union. MSF has warned that the new patent law couldthreaten the supply of affordable and essential drugs.

MSF urged the Indian policy makers to ensure that thenew Act incorporates the full flexibilities and safeguardsof the TRIPS Agreement and reflects the outcome ofthe Doha declaration on TRIPS and public health, whichaffirmed that the TRIPS Agreement can and should beinterpreted and implemented in a manner supportiveof WTO members’ rights to protect public health andin particular, to promote access to medicines for all.

Expressing its concern over the developments, MSFhopes that the new patent law will safeguard not onlythe citizens of India, but also the millions of children,women and men in the developing world whose livesdepend on access to affordable generic medicines.

23

SummarSummarSummarSummarSummary and Conclusionsy and Conclusionsy and Conclusionsy and Conclusionsy and Conclusions

10

Technological advancement has enabled India to becomeone of the leading pharmaceutical manufacturers that pro-duces drugs at the lowest prices available internationally.Although prices have increased with the new liberalisationpolicies, Indians still have access to the latest drugs with theminimum time lag at costs that are 10 to 100 times lessthan those prevailing in foreign countries.

The wholesale price data indicates that the overall growthin prices of medicines is largely due to the rise in prices ofnon-essential drugs. The effect of the DPCO 1995 alsoindicates that the price of decontrolled drugs contributesto most of the increase in the drug prices. The reformsprocess has reduced the controls by DPCO. The net im-pact has been a large increase in the basket of drugs.

Further, Indian R&D is advanced in process research, whichgives it a leading edge in developing drugs that are presentlyavailable. However, it faces some drawbacks in not research-ing new molecules. Much of the R&D by large pharmaceu-tical companies is not aimed at developing “new” drugs,but is targeted at the development of substitutes for com-petitors’ drugs with little or no contribution to the pool ofavailable therapies, or to minor changes in existing productsand processes. In many cases these are intended to extendthe term of the monopolistic position that patents confer.

It is worth mentioning that India has always shown that it ispossible to provide access to generic drugs within two tothree years of the introduction of the original drugs in theworld market.

Indian companies can no longer enjoy the benefits of pro-cess patent. The new Patent Bill puts an end to the produc-tion of generic versions of a patented drug. Increasedinvestment on R&D in the drug sector, formalising anddocumenting the medicinal properties of plants by manu-facturers and patenting ayurvedic drugs, framing a nationalforum of Indian Medical Association, pharmaceuticalmanufacturers and health officials to promote productsof Indian manufacturers and, negotiating with foreign drugcompanies manufacturing in India to supply patented medi-cines for the treatment of diseases like AIDS at an afford-able cost for bulk purchase are some of the measures thatcan be taken in the interest of public health.

The mergers and acquisitions taking place on a large scalein this industry have been of some concern. Many job lossesare reported due to the mega mergers. The profiteeringattitude of the MNCs has resulted in a reduction in theworkforce and is a threat to the small-scale industries, whichmainly practice generic manufacturing. This is a matter ofvery serious concern. Apart from loss of employment oftechnical manpower, the tendency for mergers will createmore monopoly power in the industry.

In short, the drug and pharmaceuticals industry in Indiawill have to face the challenges of economic reforms,WTO and TRIPS regulations while trying to ensure thatthe welfare of the people, or the public health care systemis not compromised in any significant way. Otherwise, thecomparative advantage established till the 1980s could belost in the coming years.

24

Economic Reforms and Drug Policy : A Micro Level Analysis

Encourage development of new drugs via fiscalincentives.

Control prices of selected life saving drugs and basicdrugs used in primary health care.

Sign agreements with MNCs established in India forthe supply of new drugs (particularly for treatment ofdiseases like TB, Malaria, AIDS, Hepatitis A & B) atconcessional rates to Public Health Centres.

Regulation of drugs:

i) Restrict marketing of banned drugs

ii) Use of restricted components in drug manufacturing

iii) Quality control

Create a platform for using compulsory licensing orparallel importing to have access to patented drugsfor curing TB, malaria, AIDS, pneumonia, etc.

Insights for Policy InitiativesInsights for Policy InitiativesInsights for Policy InitiativesInsights for Policy InitiativesInsights for Policy Initiatives

11

Introduce a system (maybe a panel of experts) to screenthe existing drugs, which could help in banning irratio-nal, ineffective (therapeutically) and harmful drugs.

Protect the interests of the poor in the light of thenew patent regime. The MNCs operating in the coun-try may be asked to set aside at least 25 percent oftheir production for essential drugs. Issue public no-tices at all the health centres on banned drugs, sideeffects of major essential drugs and drugs not to beused under self-medication. Ethics in production, mar-keting and prescription of medicines is what is requiredtoday in a country with mass illiteracy, poverty andwide prevalence of morbidity, but this cannot be im-posed. It has to come out of self-decision on the partof the respective players in the field. State interventionthrough monitoring, guidelines and regulation can becomplementary measures.

25

ANNEXURESANNEXURESANNEXURESANNEXURESANNEXURES

Countries Per Capita Drug Per CapitaExpenditure(US$) Income PPP

Japan 412 23257

Germany 222 22169

United States 191 29605

Canada 124 23582

United Kingdom 97 20336

Norway 89 26342

Costa Rica 37 5987

Chile 30 8787

Mexico 28 7704

Turkey 21 6492

Morocco 17 3305

Brazil 16 6625

Philippines 11 3555

Ghana 10 1735

China 7 3105

Pakistan 7 1715

Indonesia 5 2651

Kenya 4 980

India 3 2077

Bangladesh 2 1361

Mozambique 2 782

Annexure-I

Per capita drug expenditure and per capitaincome in 1998

Source: http://www.indioppi.com/keystat.htm. and Human Development Report(2000), pp. 178

Annexure-II

Years Rs in crores1976-77 10.501978-79 12.001979-80 14.751981-82 29.301983-84 40.001985-86 48.001986-87 50.001993-94 125.001994-95 140.001995-96 160.001996-97 185.001997-98 220.001998-99 260.001999-00 320.00

R&D Expenditure as % 2.0%of sales 2.0%

R & D Expenditure in India

Source. http://www.indioppi.com/keystat.htm.

26

Economic Reforms and Drug Policy : A Micro Level Analysis

Bala, K. and Sagoo, Kiran 2000. ‘Patents and prices’, Hainews, No.112.

Cherukuri, Ravi 1999. ‘In an interview with Mr. Y. K. Hamid,Chairman and Managing Director of Cipla, cited in ProductPatents: A Bitter Sweet Pill’, Capital Market, Vol. 13, No. 22, pp.4-11.

Current Index of Medical Specialities (CIMS) 1993. ‘Bio-GuardMedical Specialities’, Vol. 18, No. 3.

Current Index of Medical Specialities (CIMS) 1999. ‘Bio-GuardMedical Specialities’, Vol. 19, No. 4.

Deardoff, Alan V. 1992. ‘Welfare effects of global patent protection’,Economica, Vol. 59, pp. 35-51.

Drug Price Control Order (DPCO) 1975-1995, Government ofIndia.

Drug Price Control Order (DPCO) 2002, Government of India.

Gautam, S. and Parimao, P. 1996. ‘Challenges and opportunitiesfor pharma industry’, The Eastern Pharmacist, Vol. 39, No. 462,pp. 53-ff.

Griliches, Zvi and Cockburn, Iain 1994. ‘Generics and new goodsin pharmaceutical price indexes’, American Economic Review, Vol.84, No. 5, pp. 1213-1232.

Human Development Report 2000. pp. 178-ff.

Jayasekera, Deepal 2001. ‘AIDS becomes a serious health problemin India’, WSWS, May 14.

Kadekodi, G.K.and Kulkarni, Keerti 2002. ‘Status of Health andMedical Care in India: A Macro Perspective’, Centre for Multi-disciplinary Development Research, Dharwad, (Monograph no. 38).

Keayla, B. K 1998. ‘Conquest by patents - TRIPs Agreement onPatent Laws: Impact on Pharmaceuticals and Health for All’,

REFERENCESREFERENCESREFERENCESREFERENCESREFERENCES

Centre for Study of Global Trade System and Development,New Delhi, India.

Kitch, Edmund W. 1977. ‘The nature and function of the patentsystem’, Journal of Law and Economic Times, pp. 265-300.

Kumar, Nagesh and Pradhan, Jaya Prakash Undated. ‘EconomicReforms, WTO and Indian Drug Pharmaceuticals Industry:Inplications of Emerging Trends’, Centre for Multi-disciplinaryDevelopment Research, Dharwad, Monograph no. 42.

Mossinghoff, Gerald J. 1987. ‘Research-based pharmaceuticalcompanies: the need for improved patent protectionworldwide’, Journal of Law and Technology, Vol. 2, No. 6, pp.307-324.

Narayana, T. L. 1982. ‘The Indian Pharmaceutical Industry Problemsand Prospects’, National Council of Applied EconomicResearch, New Delhi.

Operation Research Group Reports, December 1975 and December1984.

People’s Democracy, Vol. 22, No. 50,December 1998, pp. 7-ff.

Rajiv, Misra; Chatterjee, Rachel and Rao, Sujata 2003. India HealthReport, Oxford University Press, New York.

Redwood, H. 1994. New Horizones in India-the consequences of patentprotection, Oldwicks press Ltd.

Sehgal, J. M. 1998. ‘Opportunities and challenges in the drug sector’,The Eastern Pharmacist, Vol. 41, No. 486, pp. 22-ff.

Sengupta, Amit 1996. ‘Economic reforms, health andpharmaceuticals: conferring legitimacy to the market’, Economicand Political Weekly, Vol. 31, No. 48, pp. 3135-3145.

Seth, P. D.; Razdan, Renu and Bhalla, Sandhya 2000. ’Pharmacist infight against AIDS in India’, The Eastern Pharmacist, Vol. 43,No. 515, pp. 37-45.

27

References

Sudarshan, V. 2002. ‘Where all those cheaper drugs gone?’, ExpressPharma Pulse, Vol.8, No.11, p.8.

Talbot, Chris Undated. ‘Adverse Health Impact of Drug Patentson Developing Countries’, Oxfam Reports, World SocialistWebsite.

Watal, Jayashree 2001. Intellectual Property rights in the WTO andDeveloping Countries, Oxford University Press, New York.

WTO OMC Fact Sheet, April 2001.

Relevant Websites:

http://www.indioppi.com/keystat.htm.

www.medindia.net/buy_n_sell/pharm_industry/ph_rdindia.asp

http://www.oxfam.org/

About the Series EditorsAbout the Series EditorsAbout the Series EditorsAbout the Series EditorsAbout the Series Editors

Aasha Kapur Mehta is Professor of Economics at the Indian Institute of Public Administration, New Delhi and leads theChronic Poverty Research Centre’s work in India. She has a Masters from Delhi School of Economics, an M.Phil fromJawaharlal Nehru University and a PhD from Iowa State University, USA. She has been teaching since 1975, initially ata college of Delhi University and then at IIPA since 1986. She is a Fulbright scholar and a McNamara fellow. Her areaof research is now entirely focused on poverty reduction and equity related issues.

Pradeep Sharma is an Assistant Resident Representative and heads the Public Policy and Local Governance Unit inthe India Country Office of United Nations Development Programme (UNDP). A post-graduate from University of EastAnglia (UK) and Doctorate from Jawaharlal Nehru University, he has held several advisory positions in the Governmentof India and has taught economic policy at LBS National Academy of Administration, Mussoorie. He has severalpublications to his credit.

Sujata Singh is an Associate Professor at the Indian Institute of Public Administration. She completed her doctoralstudies in Public Administration and Public Policy at Auburn University, USA. Her primary research interests are in thearea of Comparative and Development Administration, Public Policy Analysis, Organizational Theory and Evaluation ofRural Development Programmes.

R.K. Tiwari is Senior Consultant, Centre for Public Policy and Governance, Institute of Applied Manpower Research,Delhi. He was formerly Professor of Public Administration at the Indian Institute of Public Administration (IIPA), NewDelhi. He received his education at Gwalior, Allahabad and Delhi. He has undertaken a number of research studies inDevelopment Administration, Rural Development, Personnel Administration, Tribal Development, Human Rights andPublic Policy. He has conducted consultancy assignments for the Department of Posts and in the Ministry of RuralDevelopment, Government of India; and for the Government of Orissa and the Narmada Planning Agency, Governmentof Madhya Pradesh. He has published several books.

P.R. Panchamukhi, is Professor Emeritus, Centre for Multi-disciplinary Development Research (CMDR), Dharwad,where he was Founder-Director. He has a doctorate in Pubic Finance from Bombay University. He has beenawarded a number of coveted scholarships and prizes including Seth Mangaldas Jeshingbhai Economics prize forstanding first in the Bombay University and V.K.R.V.Rao Award for significant original research contribution. He hasheld the CN Vakil Chair in General Economics of Bombay University and has worked as Director, Indian Institute ofEducation, Pune. He been Advisor to the Planning Commission and has served on a number of committees of Govt.of India, Govt. of Karnataka, and Maharashtra, and been a consultant/adviser to international agencies like TheWorld Bank, UNICEF, UNESCO, Columbia University, WHO-Geneva, ESCAP-Bangkok, Indo-French Round Table.He has been Chief Editor /Editor of different national level journals. He has authored 15 major research works andhas more than 89 research papers in national and international publications in the areas of Education, Health,Public Finance and Developmental Economics.