Economic Outlook & SME Focus Through Big Data - … · Economic Outlook & SME Focus Through Big...

22

Economic Outlook & SME Focus Through Big Data Prepared by: TMB Analytics Date: 31 May 2017

Transcript of Economic Outlook & SME Focus Through Big Data - … · Economic Outlook & SME Focus Through Big...

Economic Outlook &

SME Focus Through Big Data

Prepared by: TMB Analytics

Date: 31 May 2017

-2-

Global Economy 01

Global Economy

Interest Rate Outlook

FX Trend

3

GDP growth

Inflation rate

Unemployment rate

GDP growth

Inflation rate

Data source : Minute of FOMC March 14-15 ,2017 ; Bank of Thailand, CEIC, and TMB Analytics, as of May 2017

2.0%

2.0%

4.5%

Fed’s Projection

GDP on growth

momentum.

(1.8% long run growth)

Inflation reaches

Fed’s target at 2%.

Unemployment rate

continues to drop.

(4.8% long run

unemployment rate)

3.3%

Key Factors for Policy Rate Direction

3.7%

1.7% 2.2%

TMBA’s Projection

2017 2018-19

GDP gains momentum in 2018-2019, triggering inflationary pressure.

Strong demand recovery in 2018

Key Factors for Policy Rate Direction

2018-2019

4.5%

2.0%

2.1%

2017

Brighter Economic Outlook Leads to Hawkish Policies

-3-

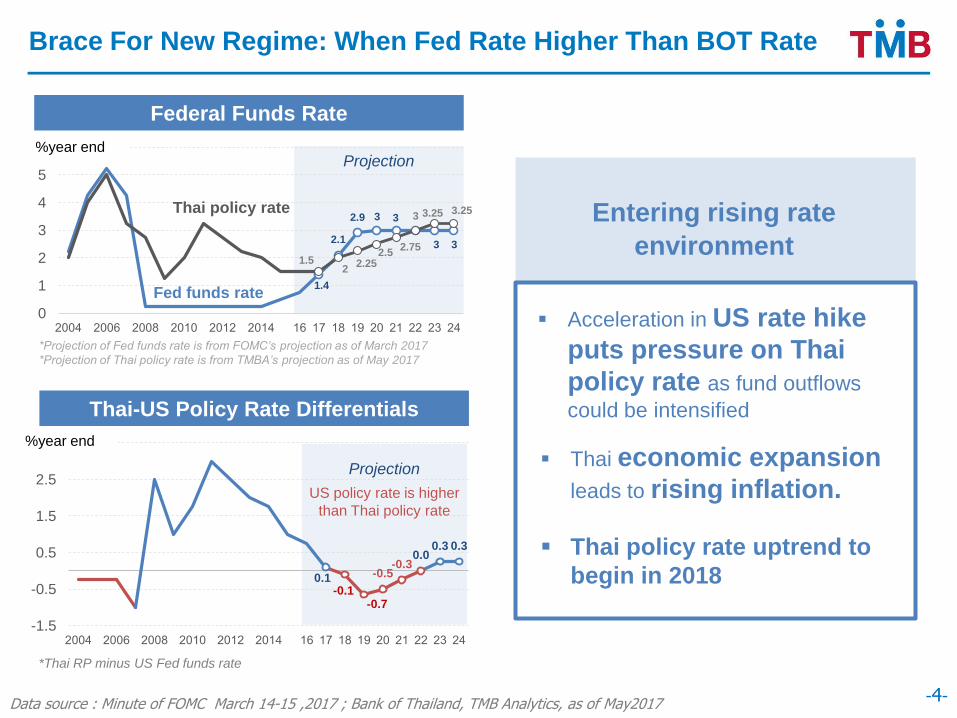

4

1.4

2.1

2.9 3 3

3 3

1.5 2

2.25 2.5

2.75

3 3.25 3.25

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014 16 17 18 19 20 21 22 23 24

0.1 -0.1

-0.7

-0.5 -0.3

0.0 0.3 0.3

-1.5

-0.5

0.5

1.5

2.5

3.5

2004 2006 2008 2010 2012 2014 16 17 18 19 20 21 22 23 24

Data source : Minute of FOMC March 14-15 ,2017 ; Bank of Thailand, TMB Analytics, as of May2017

Federal Funds Rate

Entering rising rate

environment

*Projection of Fed funds rate is from FOMC’s projection as of March 2017

*Projection of Thai policy rate is from TMBA’s projection as of May 2017

Projection %year end

%year end

Thai-US Policy Rate Differentials

Projection

*Thai RP minus US Fed funds rate

Thai economic expansion

leads to rising inflation.

Acceleration in US rate hike

puts pressure on Thai

policy rate as fund outflows

could be intensified

Thai policy rate

Fed funds rate

US policy rate is higher

than Thai policy rate

Thai policy rate uptrend to

begin in 2018

Brace For New Regime: When Fed Rate Higher Than BOT Rate

-4-

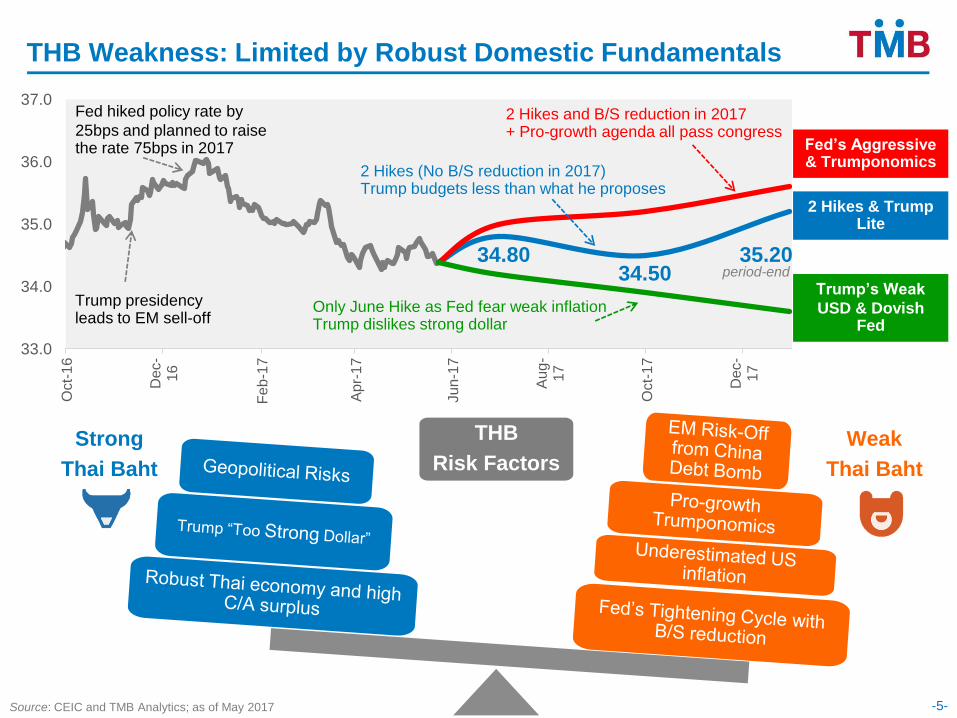

THB Weakness: Limited by Robust Domestic Fundamentals

Source: CEIC and TMB Analytics; as of May 2017 -5-

33.0

34.0

35.0

36.0

37.0

Oct-

16

De

c-

16

Feb-1

7

Ap

r-17

Ju

n-1

7

Au

g-

17

Oct-

17

De

c-

17

Trump presidency leads to EM sell-off

2 Hikes & Trump Lite

34.80 35.20

Fed hiked policy rate by

25bps and planned to raise the rate 75bps in 2017

period-end

Fed’s Aggressive & Trumponomics

Strong

Thai Baht

Weak

Thai Baht

THB

Risk Factors

Trump’s Weak

USD & Dovish Fed

2 Hikes and B/S reduction in 2017 + Pro-growth agenda all pass congress

34.50

2 Hikes (No B/S reduction in 2017) Trump budgets less than what he proposes

Only June Hike as Fed fear weak inflation Trump dislikes strong dollar

-6-

Domestic Economy 02

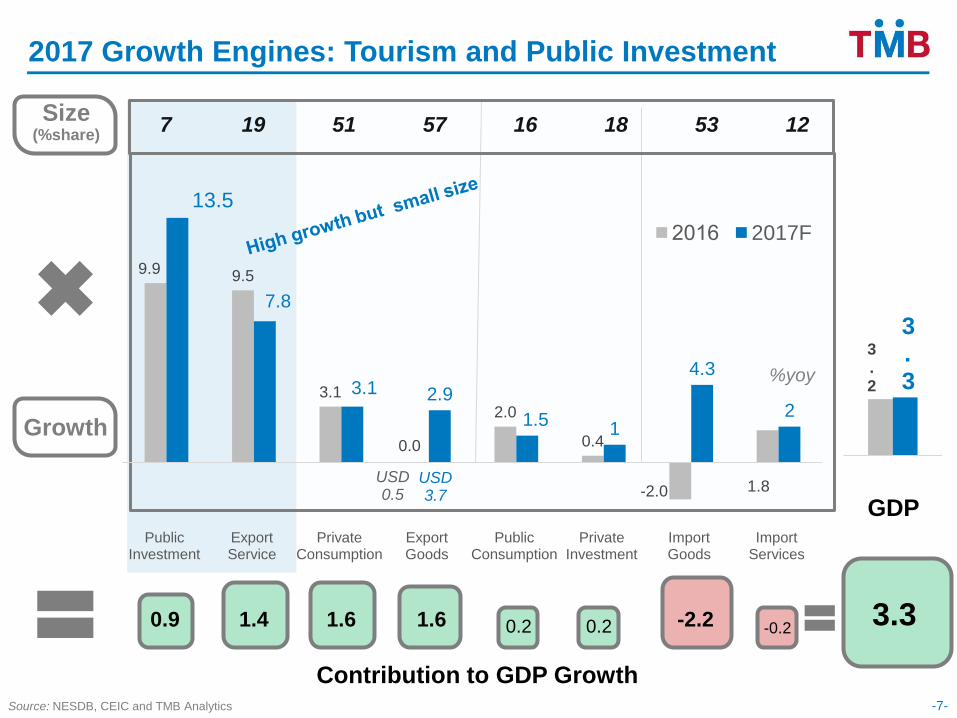

Growth Engines

2017 Export Trend

9.9 9.5

3.1

0.0

2.0

0.4

-2.0 1.8

13.5

7.8

3.1 2.9

1.5 1

4.3

2

Public Investment

Export Service

Private Consumption

Export Goods

Public Consumption

Private Investment

Import Goods

Import Services

2016 2017F

2017 Growth Engines: Tourism and Public Investment

Source: NESDB, CEIC and TMB Analytics -7-

USD 0.5

USD 3.7

%yoy

Contribution to GDP Growth

7 19 51 57 16 18 53 12 Size (%share)

Growth

0.9 1.4 1.6 1.6 0.2 0.2 -2.2 -0.2 3.3

3.2

3.3

GDP GDP

CLMV

(2016 -0.2)

+6.5

Rubber +38.5 (2016 -3.8)

-8- Source: MOC CEIC and TMB Analytics

What is 2017 outlook for Thai Export?

Total

(2016 +0.5)

+3.7

ASEAN5

(2016 -1.4)

+2.2 Japan

(2016 +2.4)

+2.8 China

(2016 -0.8)

+9.3 USA

(2016 +1.7)

+3.5 EU

(2016 +0.5)

+2.4

Able to grow from

global demand

recovery despite higher

uncertainty from

political and geopolitical risk

Strong

consumption demand

Oil price

recovery helps

raw mat and commodities

Recovered

investment in Asia

help supply chain with Japan

Continual

economic recovery

Protectionism

unlikely to take

full effect this year

Thai Export: Recovery … Not A Significant Boost

Computer &Parts

+6.3 (2016 -2.0)

Beverages +0.5

(2016 +5.8)

Electrical appliances

+5.4 (2016 -1.3)

Rising demand

for tire mfg from

China and price increase

Drop comes

mainly from

middle east market

Global economic recovery and increase in

oil price which is expected to be 57 dollar per barrel at the end of 2017

Energy drink

market growth

contributes to overall growth

Market

Product

High

economic growth

Vehicles -0.9

(2016 +4.6)

Chemical +8.3

(2016 -7.5)

90

100

110

14Q1 14Q3 15Q1 15Q3 16Q1 16Q3 17Q1 17Q3

Source: BOT, CEIC and TMB Analytics

70

75

80

2015 2016 2017

-9-

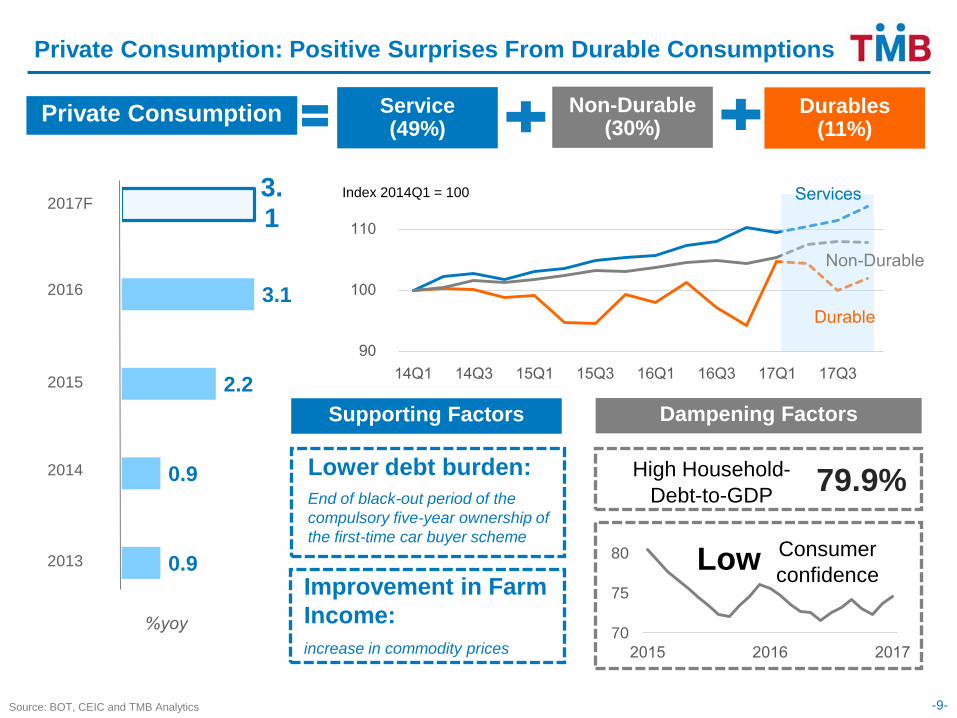

0.9

0.9

2.2

3.1

3.1

2017F

2016

2015

2014

2013

%yoy

Private Consumption

Lower debt burden:

End of black-out period of the

compulsory five-year ownership of

the first-time car buyer scheme

Improvement in Farm

Income:

increase in commodity prices

High Household-

Debt-to-GDP

Consumer

confidence

Supporting Factors

Index 2014Q1 = 100

Dampening Factors

Service (49%)

Non-Durable (30%)

Durables (11%)

79.9%

Durable

Non-Durable

Services

Private Consumption: Positive Surprises From Durable Consumptions

Low

Index 2014Q1 = 100

Source: NESDB, BOT, CEIC and TMB Analytics

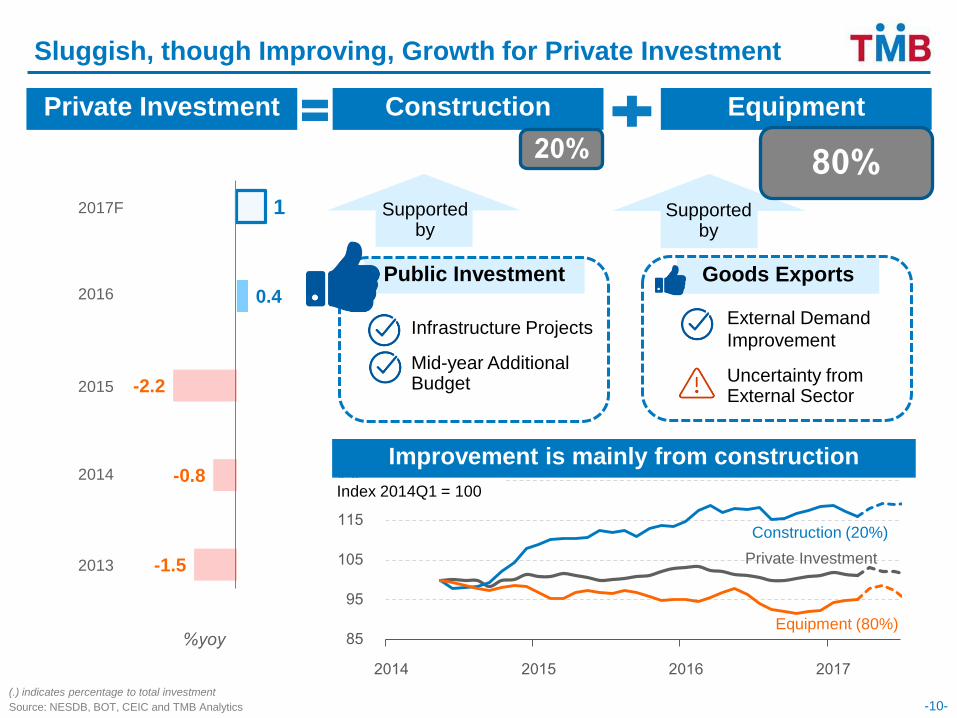

Private Investment

(.) indicates percentage to total investment

-10-

Construction Equipment

20% 80%

Public Investment Goods Exports

Supported by

Infrastructure Projects

Mid-year Additional Budget

External Demand

Improvement

Uncertainty from External Sector

-1.5

-0.8

-2.2

0.4

1 2017F

2016

2015

2014

2013

%yoy 85

95

105

115

125

2014 2015 2016 2017

Private Investment

Construction (20%)

Equipment (80%)

Supported by

Index 2014Q1 = 100

Sluggish, though Improving, Growth for Private Investment

Improvement is mainly from construction

-11-

SME Focus Through

Big Data 03

Regional

Businesses

SME

Landscape

Future SME

Businesses

-12-

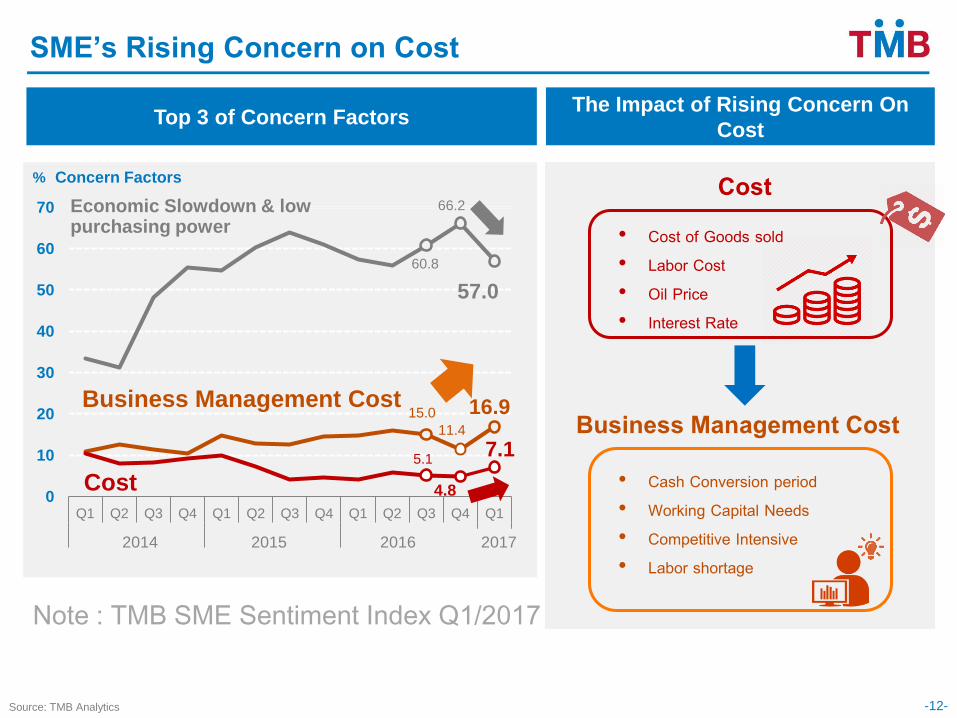

60.8

66.2

57.0

15.0

11.4

16.9

5.1

4.8

7.1

0

10

20

30

40

50

60

70

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2557 2558 2559 2560

% Concern Factors

2014 2015 2016 2017

SME’s Rising Concern on Cost

Top 3 of Concern Factors

Economic Slowdown & low purchasing power

Business Management Cost

Cost

• Cost of Goods sold • Labor Cost • Oil Price • Interest Rate

• Cash Conversion period • Working Capital Needs • Competitive Intensive • Labor shortage

Cost

The Impact of Rising Concern On

Cost

Business Management Cost

Note : TMB SME Sentiment Index Q1/2017

Source: TMB Analytics

-13-

Landscape of Thai SME: Glimpse Into Firm Level Characters

95

90

85

80

75

70

65

60

55

50

45

40

35

30

25

20

15

10

5

0

-5

-10

-15

-20

-25

-30

-35

-40

-45

-50

-55

-60

-65

-70

-75

-80

-85

-90

-95

-4.75

-4.50

-4.25

-4.00

-3.75

-3.50

-3.25

-3.00

-2.75

-2.50

-2.25

-2.00

-1.75

-1.50

-1.25

-1.00

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

Ne

t P

rofi

t M

arg

in (

%)

DE Ratio

0

30

60

90

120

150

0 0.5 1 1.5 2 2.5 3 Net P

rofit M

arg

in (

%)

Debt To Equity Ratio

Manufacturing

0

30

60

90

120

150

0 0.5 1 1.5 2 2.5 3

Net

Pro

fit

Mar

gin

(%

)

Debt To Equity Ratio

Services

0

30

60

90

120

150

0 0.5 1 1.5 2 2.5 3

Net

Pro

fit

Mar

gin

(%

)

Debt To Equity Ratio

Trade

Juristic SMEs: 350K+ firms

9,500 firms

1,500 firms

17,000 firms

Cream SMEs:

28K firms

(8%)

Only 8% of SMEs Are Cream Services Have Higher Net Profit Margin

Source : DSS and TMB Analytics

-14-

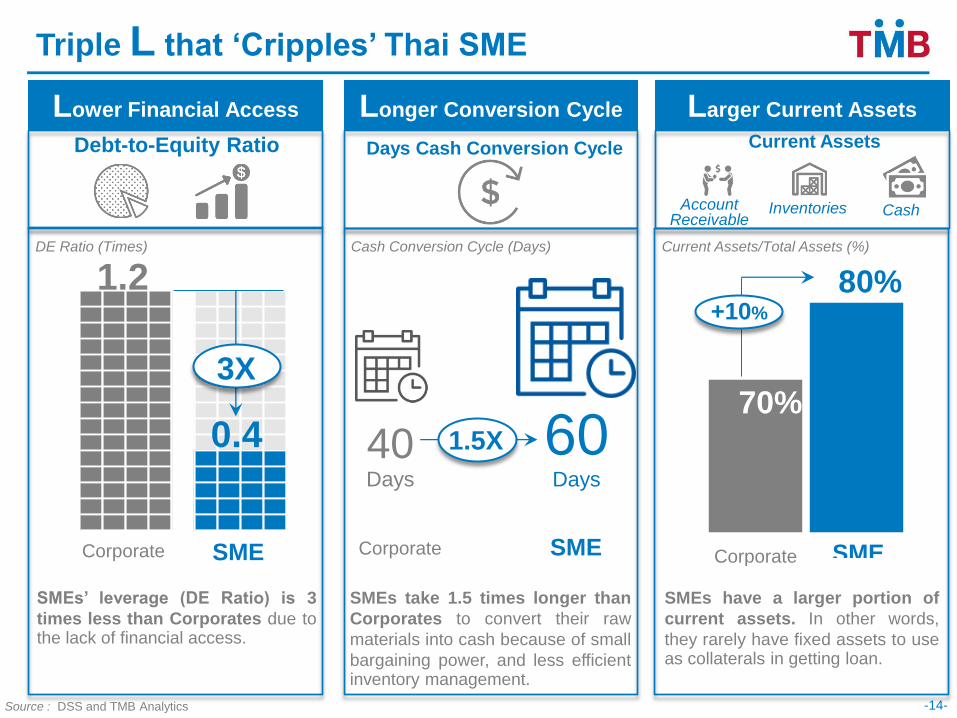

Triple L that ‘Cripples’ Thai SME

Lower Financial Access Longer Conversion Cycle Larger Current Assets

SMEs’ leverage (DE Ratio) is 3

times less than Corporates due to the lack of financial access.

Account Receivable

Inventories Cash

70%

80%

Corporate SME SME

+10%

1.2

0.4

3X

Corporate SME

SMEs take 1.5 times longer than

Corporates to convert their raw

materials into cash because of small

bargaining power, and less efficient inventory management.

Corporate SME

60 Days

40 Days

DE Ratio (Times) Current Assets/Total Assets (%)

Debt-to-Equity Ratio Days Cash Conversion Cycle

SMEs have a larger portion of

current assets. In other words,

they rarely have fixed assets to use as collaterals in getting loan.

Cash Conversion Cycle (Days)

1.5X

Source : DSS and TMB Analytics

Current Assets

Future

SME Business

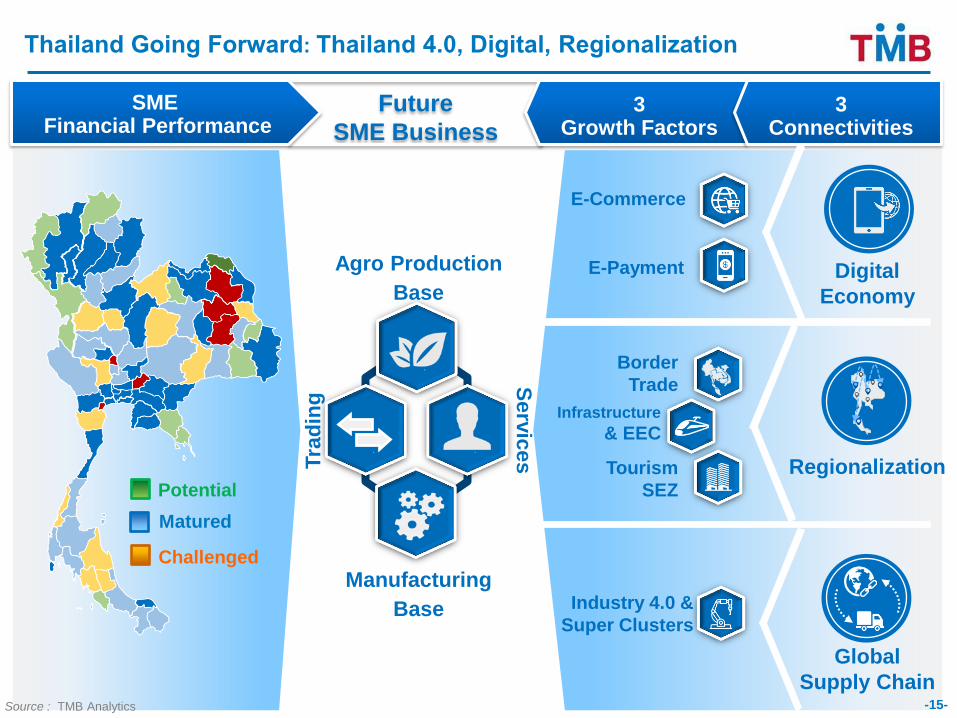

Thailand Going Forward: Thailand 4.0, Digital, Regionalization

Source : TMB Analytics

Industry 4.0 &

Super Clusters

Infrastructure

& EEC

Border

Trade

Tourism

SEZ

E-Commerce

Global

Supply Chain

Regionalization

3 Growth Factors

E-Payment Digital

Economy

SME Financial Performance

Potential

Matured

Challenged

3 Connectivities

Agro Production

Base

Manufacturing

Base

Serv

ices

Tra

din

g

-15-

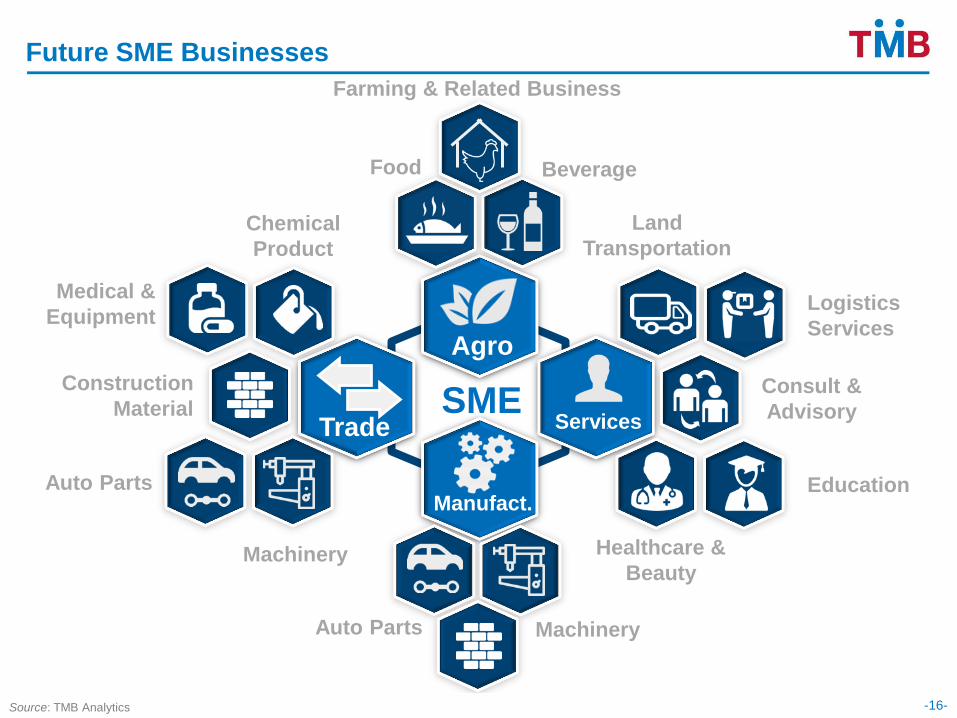

SME

Auto Parts Machinery

Construction Material

Food

Farming & Related Business

Beverage

Land

Transportation

Logistics

Services

Consult &

Advisory

Healthcare &

Beauty

Education Auto Parts

Machinery

Construction

Material

Medical &

Equipment

Chemical

Product

Future SME Businesses

Trade

Agro

Services

Manufact.

Source: TMB Analytics -16-

THANK YOU

Disclaimer

This document is issued by TMB Analytics, a division of TMB Bank PCL. All analyses are based on information available to

the public. Although the information contained herein is believed to be gathered from reliable sources, TMB makes no

guarantee to its accuracy and completeness. TMB may have issued, and may in the future issue, other reports that are

inconsistent with, and reach different conclusions from, the information presented in this report. Opinions or predictions

expressed herein reflect the authors’ views, not that of TMB, as of date of the analysis and are subject to change without

notice. TMB shall not be responsible for the use of contents and its implication.

-18-

United States Eurozone

Source: Bloomberg, and TMB Analytics’ projection

Japan China

2016

1.6%

2017

2.3%

GDP growth

2016

2.0%

2017

2.0%

2016

1.0%

2017

1.2%

2016

6.7%

2017

6.6%

GDP growth

GDP growth

GDP growth

Manufacturing sector keeps

expanding but strong dollar

could be an obstacle

Economy is projected to

expand 2.3% in 2017 from

1.6% in 2016

Global Recovery: Improving But Uneven

Stronger expansion among

manufacturing and service

sectors support EU recovery

Growth in 2017 is expected

to recover by 2.0% same as

+2.0% in 2016

GDP is likely to grow by

6.6% in 2017 where growth

story still broadly unchanged

Rebound in industrial sector

galvanize rising profits and

debt-repayment ability

High corporate debt to GDP

(156%) remains a terrifying

risk

Economy is likely to

sustain above 1.0%

expansion in 2017

Inflation and consumer

spending gradually improve

Weak yen boosts Exports

and imports and strengthen

recovery

80

90

100

110

120

130

Jan-16 Jul-16 Jan-17

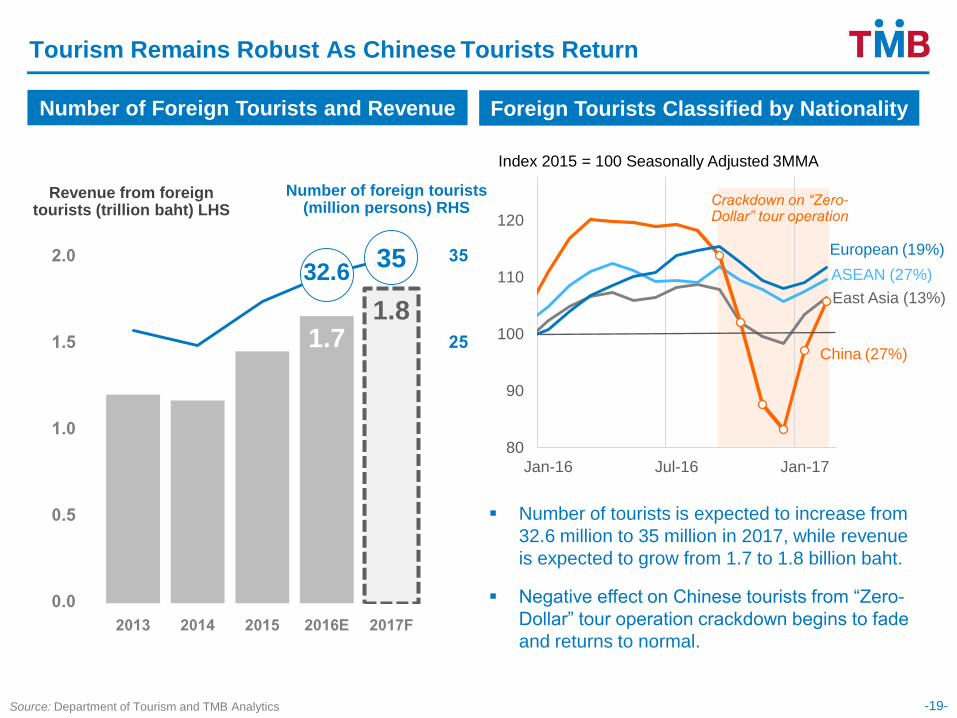

Number of Foreign Tourists and Revenue

1.7 1.8

32.6 35

-5

5

15

25

35

0.0

0.5

1.0

1.5

2.0

2013 2014 2015 2016E 2017F

Source: Department of Tourism and TMB Analytics -19-

Tourism Remains Robust As Chinese Tourists Return

Number of foreign tourists (million persons) RHS

Revenue from foreign tourists (trillion baht) LHS

Foreign Tourists Classified by Nationality

Number of tourists is expected to increase from

32.6 million to 35 million in 2017, while revenue

is expected to grow from 1.7 to 1.8 billion baht.

Negative effect on Chinese tourists from “Zero-

Dollar” tour operation crackdown begins to fade

and returns to normal.

Index 2015 = 100 Seasonally Adjusted 3MMA

East Asia (13%)

China (27%)

European (19%)

ASEAN (27%)

Crackdown on “Zero-Dollar” tour operation

-20-

Infrastructure Projects

Government Capital

Expenditure

2017 Money injected FY2017 Budget:

Provincial Cluster

Total 75 Bn

Source: FPO and TMB Analytics

> 4.5 bn

4.0 - 4.5 bn

< 4.0 bn

687 Bn 240 Bn

Money Invested in Infrastructure Projects 2017-2023

Land transport

Double track

Mass transit

240

483 549 516

271 142

35

17F 18F 19F 20F 21F 22F 23F

Total 2.24 trillion

(15.6% of GDP)

Pattaya-Maptaput

Bangpa-In - Korat

Bang Yai - Kanchanaburi

Thai-China

Mabkabao-Jira

Nakhonpathom-Huahin

Lopburi-Paknumpoe Prachub-Chumporn

Jira-Khonkaen

Pink

Yellow

Dark Red

Orange

Purple

Light Red

Public Investment: More Broad-based Distribution

Classification: Confidential (C-3) -21-

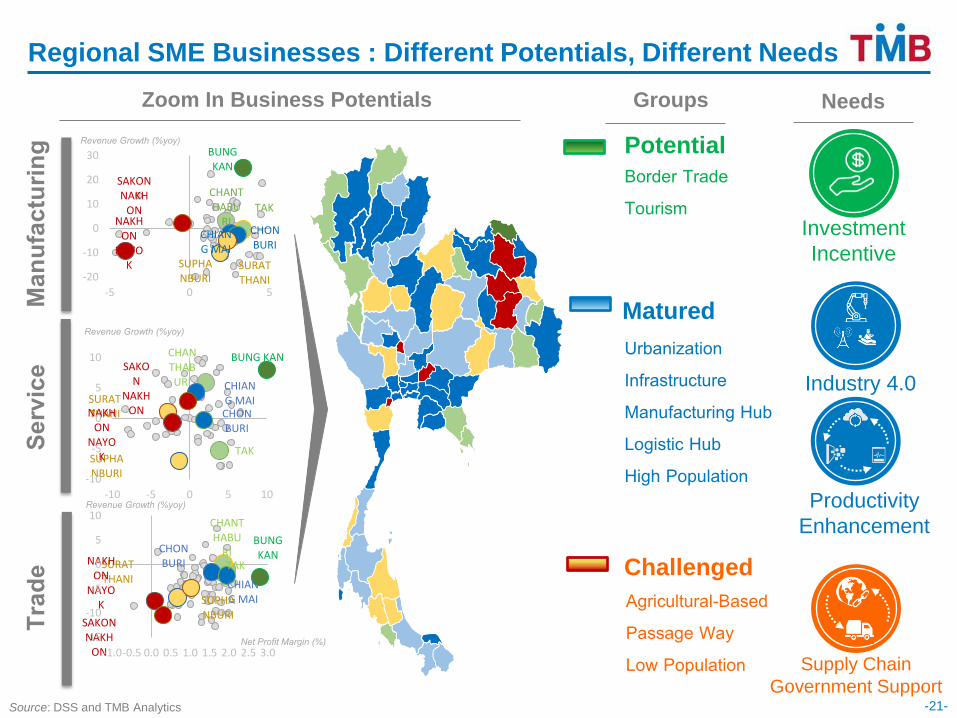

BUNG KAN

CHANTHABU

RI TAK

CHIANG MAI

CHON BURI

SUPHANBURI

SURAT THANI

NAKHON

NAYOK

SAKON NAKH

ON

-20

-10

0

10

20

30

-5 0 5 Manu

fact

urin

g Se

rvice

Tr

ade

BUNG KAN CHANTHABURI

TAK

CHIANG MAI CHON BURI

SUPHANBURI

SURAT THANI NAKHON

NAYOK

SAKON

NAKHON

-10

-5

0

5

10

-10 -5 0 5 10

BUNG KAN

CHANTHABU

RI TAK

CHIANG MAI

CHON BURI

SUPHANBURI

SURAT THANI

NAKHON

NAYOK

SAKON NAKH

ON -15

-10

-5

0

5

10

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

Revenue Growth (%yoy)

Revenue Growth (%yoy)

Revenue Growth (%yoy)

Net Profit Margin (%)

Potential Border Trade Tourism

Matured

Urbanization Infrastructure Manufacturing Hub Logistic Hub High Population

Challenged Agricultural-Based Passage Way Low Population Supply Chain

Government Support

Investment

Incentive

Industry 4.0

Groups Needs

Productivity

Enhancement

Regional SME Businesses : Different Potentials, Different Needs

Zoom In Business Potentials

Source: DSS and TMB Analytics

Source: DSS, OSMEP and TMB Analytics -22-

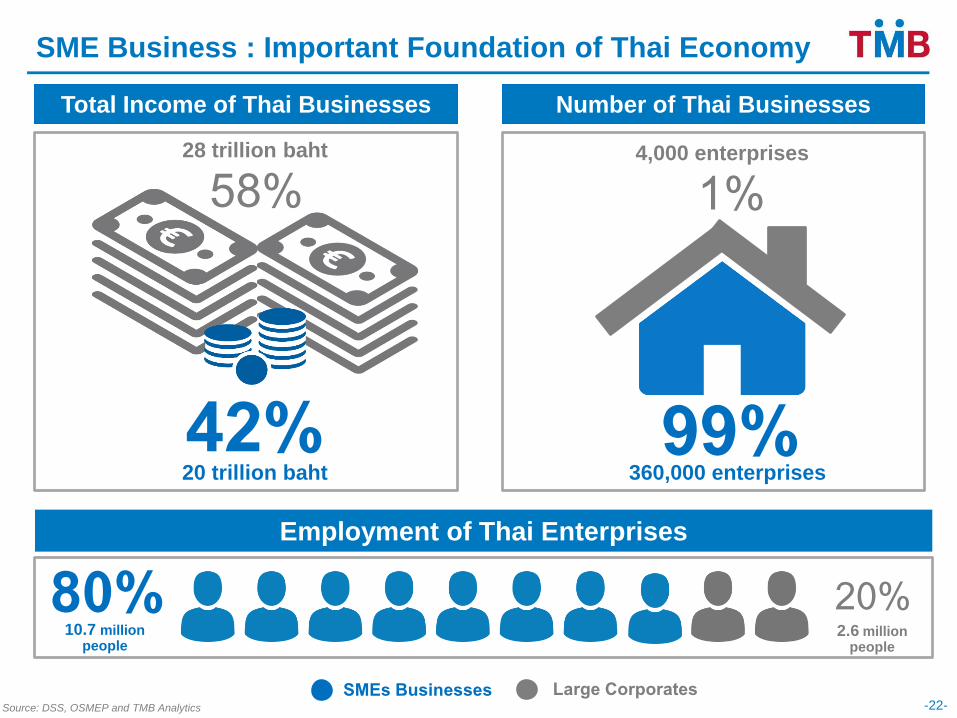

Total Income of Thai Businesses

58% 28 trillion baht

42% 20 trillion baht

80% Employment of Thai Enterprises

10.7 million people

20% 2.6 million

people

Number of Thai Businesses

1% 4,000 enterprises

99% 360,000 enterprises

SME Business : Important Foundation of Thai Economy

SMEs Businesses Large Corporates