Economic Outlook for Calhoun County 2014-15 - Battle Creek Area

53

2014–2015 Forecast for Calhoun County 2013 was an “OK” year George A. Erickcek Brian Pittelko W.E. Upjohn Institute for Employment Research January 16, 2014

Transcript of Economic Outlook for Calhoun County 2014-15 - Battle Creek Area

2014–2015 Forecast for Calhoun County

2013 was an “OK” year

George A. Erickcek Brian Pittelko

W.E. Upjohn Institute for Employment Research

January 16, 2014

Thanks to Our Sponsors

1

Outline

• Most think that the economy is stronger than it looks—only 74,000 new jobs in December

• The state economy continues to be driven by the car industry

• Calhoun County had a positive but disappointing year

• Forecast: more employment growth

2

GDP grew by 4.1 percent in the third quarter, and the forecast is positive

-10

-8

-6

-4

-2

0

2

4

6

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percent change in GDP (average annual rate)

3

The last quarter of the year is expected to be slow as businesses work off unwanted inventories.

Capacity utilization has not yet fully recovered but business confidence is up

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

30

35

40

45

50

55

60

65

70

2006 2007 2008 2009 2010 2011 2012 2013

Pe

rce

nt

uti

lizat

ion

(%)

PM

I (>5

0 =

exp

ansi

on

; <5

0 =

co

ntr

acti

on

)

Purchasing Managers’ Index for Manufacturing and Industrial Capacity Utilization

Manufacturing PMI Capacity utilization

4

Employment conditions have improved; however, the number of job seekers per opening

is still double what it was in 2008

5

Employment has been slow to recover

94

96

98

100

102

104

106

108

110

-24 -18 -12 -6 0 6 12 18 24 30 36 42 48 54

Months from the trough

Employment Index (100 = Trough)

Current

6

Yes, we are coming off a bad one

54 months since the trough and we are still off more than a million jobs in the nation.

7

Recession Employment Loss in

Recession Employment Gains

in Expansion Net Change

Current -7,464 6,299 -1,165

2001 -1,593 4,933 3,340

1991 -1,242 9,287 8,045

Unemployment is falling, but there are still too many long-term unemployed workers

0

5

10

15

20

25

30

35

40

45

50

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013

Perc

enta

ge u

nem

plo

yed

27

wee

ks o

r m

ore

Un

emp

loym

ent

rate

U.S. Unemployment Rate and Long-Term Unemployment

Unemployment rate Percentage unemployed 27 weeks or more

In December, the unemployment rate dropped because 347,000 individuals left the workforce.

8

Consumers appear to be holding more debt and not feeling that good about it

9 Source: Conference Board and the Federal Reserve.

0

20

40

60

80

100

120

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

2006 2007 2008 2009 2010 2011 2012 2013

Ind

ex: 1

99

5 =

10

0

Bill

ion

s ($

)

Consumer Confidence and Change in Consumer Debt

Consumer debt Consumer confidence

Interest rates and inflation are moving upward but are still at historically low levels

10

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2008 2009 2010 2011 2012 2013

An

nu

al p

erce

nta

ge r

ate

Interest Rates and Inflation

30-year mortgages 10-year Treasury bill

3-month Treasury

12-month change in CPI-U

There isn’t a lot of demand for loans

-100

-80

-60

-40

-20

0

20

40

60

80

100

2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1

Net

per

cen

tage

of

resp

on

den

ts

Federal Reserve Senior Loan Officers Survey: Demand and Lending Standards for Commercial and Industrial

Loans by Medium-to-Large Firms

Reporting tightening standards

Reporting stronger loan demand

11

So let’s sum up

• The economy is expected to grow faster in 2014 than last year, but will still be below what we want

• The major problem is the lack of demand as seen in our capacity utilization rates and loan demand

• This means the number of job seekers per job will remain too high

• Don’t expect anything from Congress and the Fed will slowly—and I mean slowly—tighten the money supply

But there is something else as well 12

Starting in 1981 and continuing until today, most of the nation’s income growth has been

earned by the top 5 percent

0

20

40

60

80

100

120

140

160

180

200

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

Ho

use

ho

ld in

com

e ($

00

0s)

Income Level Quintiles, 2012 Dollars

Lowest Second Third Fourth Lower limit of top 5 percent

Source: Census Historic Income. 13

Why does it matter?

• Inequality limits consumer expending and, hence, slows the economy

• Research suggests that historical trends in upward mobility are declining

• Consumer confidence surveys indicate that households’ future expectations are at record lows

14

What should be done? That is the question

• Very little political will to make the tax code more progressive

• Increasing educational opportunities is a standard response but it is a long-term solution

• Current efforts are to increase the minimum wage

15

The state’s minimum wage of $7.40 has not changed since 2008

0

1

2

3

4

5

6

7

8

9

10

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Wag

e ($

)

Minimum Wage, 1980–2013, Nominal

Michigan US

16

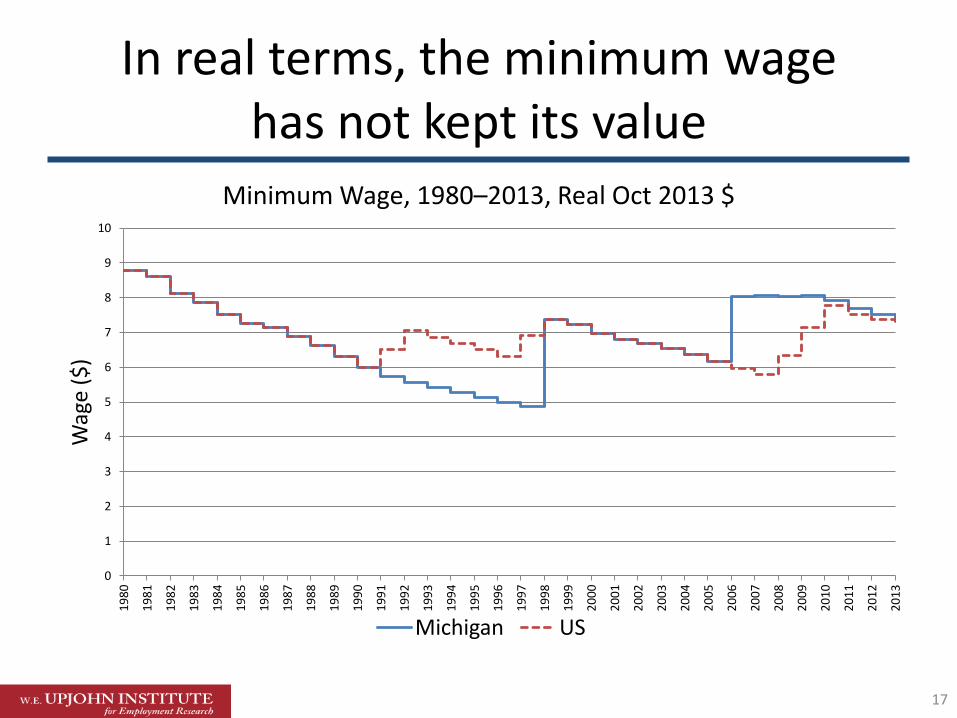

In real terms, the minimum wage has not kept its value

0

1

2

3

4

5

6

7

8

9

10

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Wag

e ($

)

Minimum Wage, 1980–2013, Real Oct 2013 $

Michigan US

17

So should we increase the minimum wage?

• Worries:

– Negatively impact employment – Recent research indicates that this may not be the case

– Some individuals who earn the minimum wage do not live in low-income households. This is true.

• My preferred solution is to increase the Earned Income Tax Credit

• Bottom line: this issue will not go away

18

Turning to Michigan

• 2013 Employment Growth Estimates: 59.480 total jobs created, up 1.4%

17,570 manufacturing jobs, up 3.3%

• U of M’s Forecast is positive

66,730 additional jobs in 2014

65,050 additional jobs in 2015

19 Source: University of Michigan.

During the past four quarters, the state’s employment has increased by 64,400

-10 0 10 20 30 40 50 60 70

Government Other services

Leisure & hospitality Education & health

Business & professional Financial

Information Transportation & utilities

Retail Wholesale

Manufacturing Construction

Total

Employment (in 000s)

Employment Change, 3rd Quarter 2012 to 3rd Quarter 2013

20 Source: Michigan Labor Market Information, CES.

Implied manufacturing multiplier is 3.9 which is a bit too high.

Auto sales continue to pick up and are forecast to drive past 16 million units in 2014

21 Source: BEA.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

15.5 million units in 2013

The auto outlook is promising

• The current fleet on the road is old, very old–11.4 years

• Incentives are back

• New selections – there will be 40 new launches in 2014

• Financing is available

22

Construction activity has a long way to go

0

10,000

20,000

30,000

40,000

50,000

60,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Number of Building Permits Issued*

Total units Single family

Source: U.S. Census. 23

*2013 is an estimate

Calhoun County

• Modest employment gains and a declining unemployment rate

• Lagging retail market

• Still, it has out-performed comparison MSAs

• Talent attraction remains a challenge

• Forecast: continued growth

24

Employment gains have been modest: 370 jobs in the four-quarter period, 0.7% increase.

-150 -100 -50 0 50 100 150 200 250

Government

Other Services

Leisure & hospitality

Education & Health

Prof. and Business

Financial

Trade, Transport., and Util.

Manufacturing

Mining, Logging, Const.

Employment Change, Q3 2012 to Q3 2013

Source: BLS CES.

Given a 2.3 employment multiplier, manufacturing employment can be credited for powering the entire economy forwared.

25

The lack of linkage between manufacturing and trade is troublesome

Mining, Logging, Const.

Manufacturing

Trade, Transport., and

Util. Financial

Prof. and Business

Education & Health

Leisure & hospitality

Other Services

Government

-150

-100

-50

0

50

100

150

200

250

Employment Change, Q3 2012 to Q3 2013

Source: BLS CES. 26

The good news is that county’s unemployment rate is dropping; the bad news is that it is for

the wrong reason

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Unemployment Rate for Calhoun County

27 Source: BLS LAUS and Upjohn Institute.

November-to-November Change

Year Labor Force Change Employment

Change Unemployment

Change

2011 -1,281 353 -1,634

2012 -685 110 -795

2013 519 209 310

Source: MI Labor Market Indicators, Local Area Unemployment Statistics.

Unfortunately, too many people have been dropping out the labor force

28

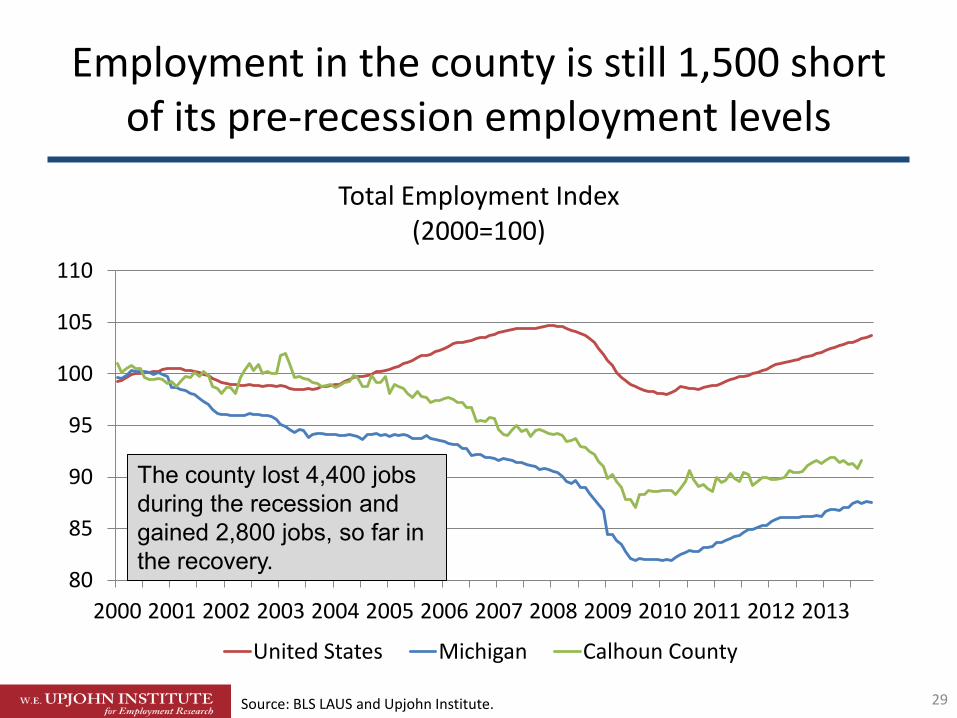

Employment in the county is still 1,500 short of its pre-recession employment levels

80

85

90

95

100

105

110

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Total Employment Index (2000=100)

United States Michigan Calhoun County

29 Source: BLS LAUS and Upjohn Institute.

The county lost 4,400 jobs during the recession and gained 2,800 jobs, so far in the recovery.

Employment in the county’s service sector has hit a plateau

80

85

90

95

100

105

110

115

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Private Services Employment Index (2000=100)

United States Michigan Calhoun County

30 Source: BLS LAUS and Upjohn Institute.

The county manufacturers have added 1,500 jobs since the recession

45

55

65

75

85

95

105

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Manufacturing Employment Index (2000=100)

United States Michigan Calhoun County

31 Source: BLS LAUS and Upjohn Institute.

Employment gains are clearly auto driven

Food Printing

Chemical

Plastics & Rubber

Nonmetallic Mineral

Primary Metal

Fabricated Metal

Machinery Electrical

Equip.

Transportation

Misc.

-400

-300

-200

-100

0

100

200

300

400

500

600

Employment Change, Q1 2012 to Q1 2013

Source: BLS QCEW. 32

Construction activity is still flat

0

50

100

150

200

250

300

350

400

450

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Construction Permits Issued, Calhoun Co.

Total, All Structure Types Single Family Houses

33 Source: U.S. Census. •Year to date, November 2013

And evidence suggests that housing prices are stable at best

0

20

40

60

80

100

120

140

160

180

200

FHFA Housing Price Index (1995=100)

Battle Creek

Source: FHFA Housing Index. 34

Comparison Analysis

• Altoona, PA

• Anderson, IN

• Jackson, MI

• Johnstown, PA

• Lebanon, PA

• Mansfield, OH

• Monroe, MI

• Muncie, IN

• Springfield, OH

• Wausau, WI

• Williamsport, PA

Comparison Areas:

35

Comparison Criteria

• All one-county metropolitan areas

• Within Midwest region

• Not college town or state capitol

• All within 15% population of Calhoun County (plus Jackson)

36

All of the comparison areas are experiencing lackluster employment growth

-1.1% -0.7%

-0.5% -0.3%

-0.2% -0.1%

0.1% 0.2%

0.3% 0.6%

1.6% 0.0%

1.0%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

Mansfield, OH Wausau, WI Monroe, MI

Springfield, OH Johnstown, PA

Jackson, MI Muncie, IN

Altoona, PA Lebanon, PA

Williamsport, PA Anderson, IN

Comparison Average Battle Creek, MI

Percent Change in Total Employment, Jan–Nov 2012 through Jan–Nov 2013

Source: BLS. 37

Calhoun County’s manufacturing sector is doing better than average . . .

-2.1% -1.9%

-0.9% -0.7%

-0.2% 1.1%

1.6% 1.7%

1.8% 2.7%

4.7% 0.7%

2.7%

-4% -2% 0% 2% 4% 6%

Johnstown, PA Williamsport, PA

Wausau, WI Lebanon, PA

Mansfield, OH Muncie, IN

Anderson, IN Altoona, PA Jackson, MI Monroe, MI

Springfield, OH Comparison Average

Battle Creek, MI

Percent Change in Manufacturing Employment, Jan–Nov 2012 through Jan–Nov 2013

Source: BLS. 38

. . . as are its service sectors

-1.1% -1.1%

-0.7% -0.6% -0.6%

-0.4% -0.2% -0.2%

0.0% 0.1%

1.6% -0.3%

0.7%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

Mansfield, OH Springfield, OH

Wausau, WI Monroe, MI Lebanon, PA Jackson, MI Altoona, PA

Johnstown, PA Williamsport, PA

Muncie, IN Anderson, IN

Comparison Average Battle Creek, MI

Percent Change in Service Providing Employment, Jan–Nov 2012 through Jan–Nov 2013

Source: BLS. 39

The Calhoun County unemployment situation is slightly better than average

9.6

9.3

8.8

8.7

8.3

8.1

7.9

7.2

6.9

6.9

6.2

8.0

7.3

0 2 4 6 8 10 12

Anderson, IN

Muncie, IN

Johnstown, PA

Jackson, MI

Mansfield, OH

Monroe, MI

Williamsport, PA

Springfield, OH

Altoona, PA

Wausau, WI

Lebanon, PA

Comparison

Battle Creek

Average Unemployment Rate, Jan–Nov 2013

Source: BLS. 40

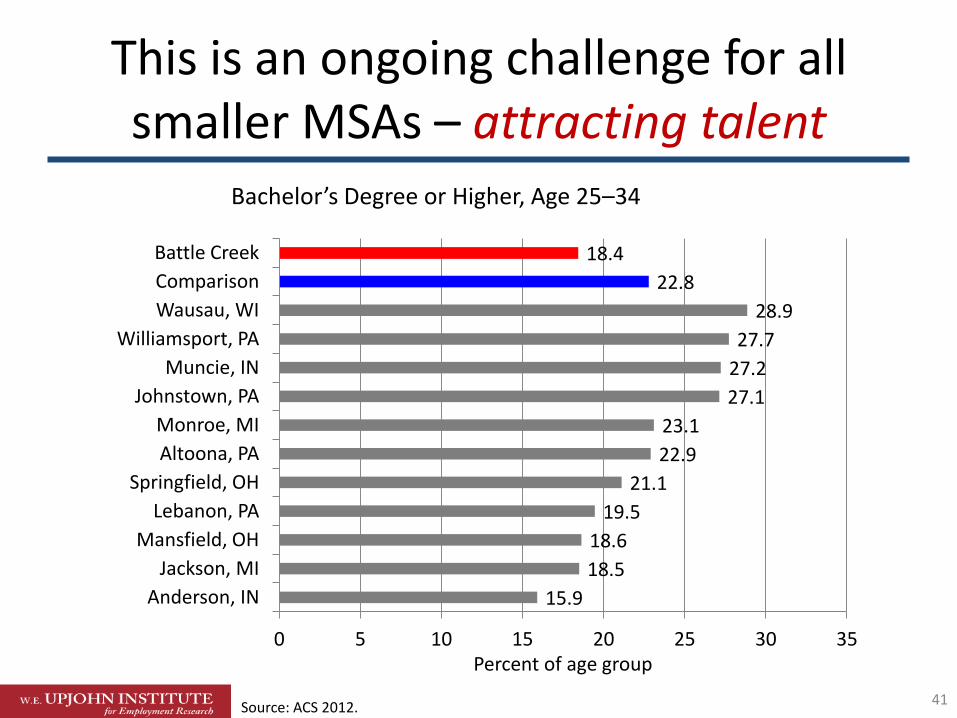

This is an ongoing challenge for all smaller MSAs – attracting talent

15.9

18.5

18.6

19.5

21.1

22.9

23.1

27.1

27.2

27.7

28.9

22.8

18.4

0 5 10 15 20 25 30 35

Anderson, IN

Jackson, MI

Mansfield, OH

Lebanon, PA

Springfield, OH

Altoona, PA

Monroe, MI

Johnstown, PA

Muncie, IN

Williamsport, PA

Wausau, WI

Comparison

Battle Creek

Percent of age group

Bachelor’s Degree or Higher, Age 25–34

Source: ACS 2012. 41

Nevertheless, knowledge-based entrepreneurship

is a strength of the county

15.3

15.3

16.3

16.3

17.3

17.4

18.1

19.3

20.1

23.1

26.6

18.7

24.6

0 5 10 15 20 25 30

Johnstown, PA

Wausau, WI

Lebanon, PA

Altoona, PA

Muncie, IN

Williamsport, PA

Springfield, OH

Jackson, MI

Mansfield, OH

Anderson, IN

Monroe, MI

Comparison

Battle Creek

Percent of industry

Self-Employed Professional, Scientific Technical Employed

Source: ACS 2012. 42

Just a reminder that education matters

0

10

20

30

40

50

60

70

Less than HS High school Some college

Associate's Bachelor's Graduate

Inco

me

($0

00

’s)

Annual Income by Educational Attainment

Source: IPUMS USA 2012. 43

Change in the number of job postings, 2012 to 2013

-4 -2 0 2 4 6 8 10

Public Administration Other Services

Accommodation and Food Arts, Ent., and Rec.

Health Care and Social Asst. Educational Services

Admin, Support, Waste Management

Prof., Sci., Tech Real Estate

Finance and Insurance Information

Transport. And Warehousing Retail Trade

Wholesale Trade Manufacturing

Construction Utilities

Ratio to total growth

Job Posting Index, 2012 to 2013 All Industries

Source: Burning Glass Labor Insight. 44

Job postings for knowledge-based workers lag in nearly all MSAs in the state

-6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0

Bay City Benton Harbor

Saginaw Flint

Detroit Lansing Holland

Ann Arbor Muskegon

Jackson Battle Creek

Monroe Kalamazoo

Grand Rapids

Ratio to total growth

Job Posting Index, 2012 to 2013 Architecture and Engineering Occupations

Source: Burning Glass Labor Insight. 45

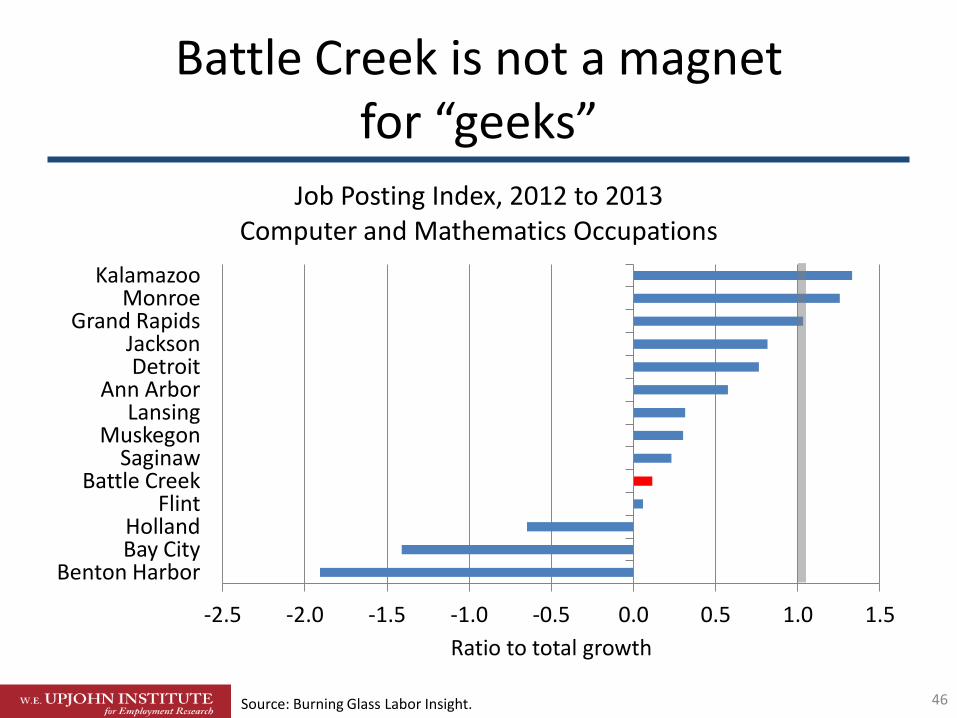

Battle Creek is not a magnet for “geeks”

-2.5 -2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Benton Harbor Bay City Holland

Flint Battle Creek

Saginaw Muskegon

Lansing Ann Arbor

Detroit Jackson

Grand Rapids Monroe

Kalamazoo

Ratio to total growth

Job Posting Index, 2012 to 2013 Computer and Mathematics Occupations

Source: Burning Glass Labor Insight. 46

On to the 2014 and 2015 forecast

Not so fast, how good was your last year’s forecast?

The focus group blew it again!

47

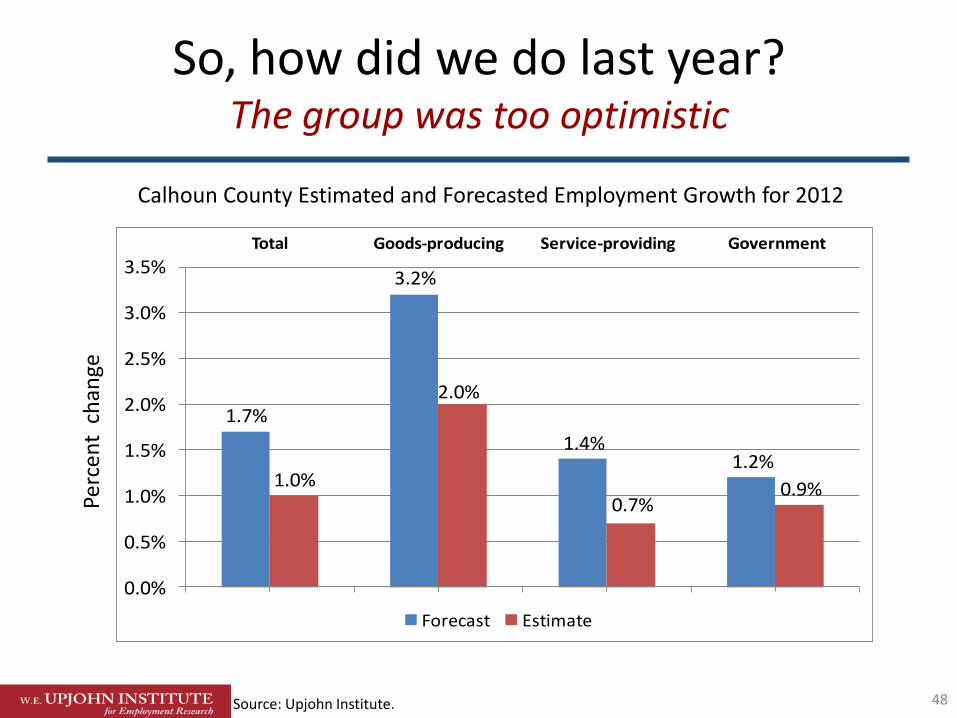

So, how did we do last year? The group was too optimistic

1.7%

3.2%

1.4%1.2%

1.0%

2.0%

0.7%0.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%Total Goods-producing Service-providing Government

Forecast Estimate

Perc

ent

ch

ange

Source: Upjohn Institute.

Calhoun County Estimated and Forecasted Employment Growth for 2012

48

Recent business reports have been robust

• Bleistahl

• Cosma Castings Michigan

• Denso

• Janesville Acoustics

• Post Cereal

• TRMI Inc

49

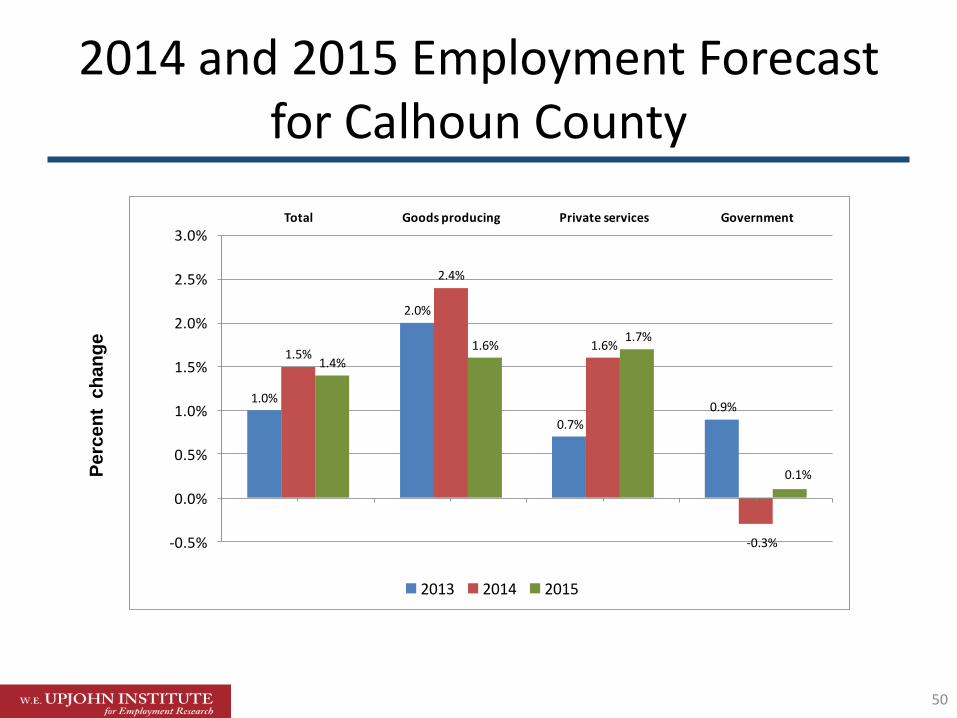

2014 and 2015 Employment Forecast for Calhoun County

1.0%

2.0%

0.7%

0.9%

1.5%

2.4%

1.6%

-0.3%

1.4%

1.6%1.7%

0.1%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%Total Goods producing Private services Government

2013 2014 2015

Perc

en

t c

han

ge

50

Last words

• 2013 was a good year for Calhoun County

• Still, the drop in the area’s unemployment rate was due largely because individuals were leaving the workforce

• The link between the area’s manufacturing sector and its service sectors is very weak, suggesting strong retail leakage from the county

• Again, I believe 2014 will be a better year—however, this has been the fourth year in a row that our forecast has been too robust

51

2014–2015 Forecast for Calhoun County

2013 was an “OK” year

George A. Erickcek Brian Pittelko

W.E. Upjohn Institute for Employment Research

January 16, 2014