ECONOMIC OUTLOOK 2017 03-Mar-2017 - AXYS · PDF fileECONOMIC OUTLOOK 2017 03-Mar-2017 A: AXYS...

17

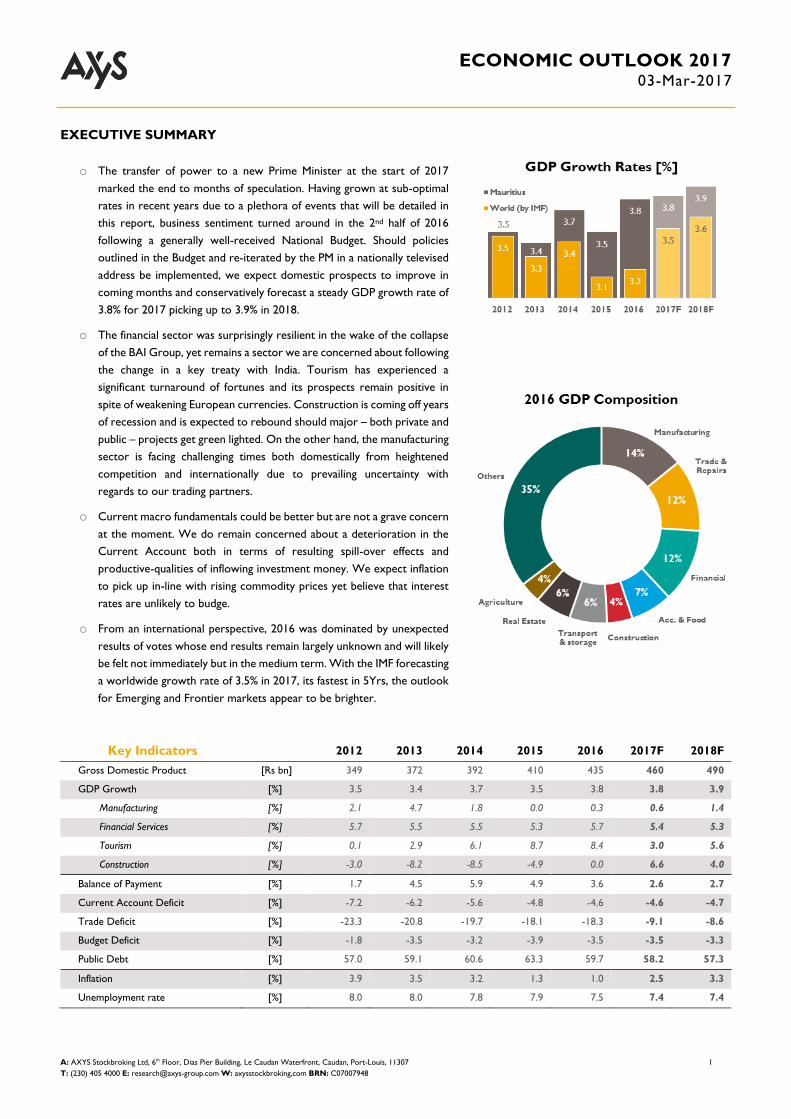

ECONOMIC OUTLOOK 2017 03-Mar-2017 A: AXYS Stockbroking Ltd, 6 th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 1 T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948 EXECUTIVE SUMMARY o The transfer of power to a new Prime Minister at the start of 2017 marked the end to months of speculation. Having grown at sub-optimal rates in recent years due to a plethora of events that will be detailed in this report, business sentiment turned around in the 2 nd half of 2016 following a generally well-received National Budget. Should policies outlined in the Budget and re-iterated by the PM in a nationally televised address be implemented, we expect domestic prospects to improve in coming months and conservatively forecast a steady GDP growth rate of 3.8% for 2017 picking up to 3.9% in 2018. o The financial sector was surprisingly resilient in the wake of the collapse of the BAI Group, yet remains a sector we are concerned about following the change in a key treaty with India. Tourism has experienced a significant turnaround of fortunes and its prospects remain positive in spite of weakening European currencies. Construction is coming off years of recession and is expected to rebound should major – both private and public – projects get green lighted. On the other hand, the manufacturing sector is facing challenging times both domestically from heightened competition and internationally due to prevailing uncertainty with regards to our trading partners. o Current macro fundamentals could be better but are not a grave concern at the moment. We do remain concerned about a deterioration in the Current Account both in terms of resulting spill-over effects and productive-qualities of inflowing investment money. We expect inflation to pick up in-line with rising commodity prices yet believe that interest rates are unlikely to budge. o From an international perspective, 2016 was dominated by unexpected results of votes whose end results remain largely unknown and will likely be felt not immediately but in the medium term. With the IMF forecasting a worldwide growth rate of 3.5% in 2017, its fastest in 5Yrs, the outlook for Emerging and Frontier markets appear to be brighter. Key Indicators 2012 2013 2014 2015 2016 2017F 2018F Gross Domestic Product [Rs bn] 349 372 392 410 435 460 490 GDP Growth [%] 3.5 3.4 3.7 3.5 3.8 3.8 3.9 Manufacturing [%] 2.1 4.7 1.8 0.0 0.3 0.6 1.4 Financial Services [%] 5.7 5.5 5.5 5.3 5.7 5.4 5.3 Tourism [%] 0.1 2.9 6.1 8.7 8.4 3.0 5.6 Construction [%] -3.0 -8.2 -8.5 -4.9 0.0 6.6 4.0 Balance of Payment [%] 1.7 4.5 5.9 4.9 3.6 2.6 2.7 Current Account Deficit [%] -7.2 -6.2 -5.6 -4.8 -4.6 -4.6 -4.7 Trade Deficit [%] -23.3 -20.8 -19.7 -18.1 -18.3 -9.1 -8.6 Budget Deficit [%] -1.8 -3.5 -3.2 -3.9 -3.5 -3.5 -3.3 Public Debt [%] 57.0 59.1 60.6 63.3 59.7 58.2 57.3 Inflation [%] 3.9 3.5 3.2 1.3 1.0 2.5 3.3 Unemployment rate [%] 8.0 8.0 7.8 7.9 7.5 7.4 7.4

Transcript of ECONOMIC OUTLOOK 2017 03-Mar-2017 - AXYS · PDF fileECONOMIC OUTLOOK 2017 03-Mar-2017 A: AXYS...

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 1

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

EXECUTIVE SUMMARY

o The transfer of power to a new Prime Minister at the start of 2017

marked the end to months of speculation. Having grown at sub-optimal

rates in recent years due to a plethora of events that will be detailed in

this report, business sentiment turned around in the 2nd half of 2016

following a generally well-received National Budget. Should policies

outlined in the Budget and re-iterated by the PM in a nationally televised

address be implemented, we expect domestic prospects to improve in

coming months and conservatively forecast a steady GDP growth rate of

3.8% for 2017 picking up to 3.9% in 2018.

o The financial sector was surprisingly resilient in the wake of the collapse

of the BAI Group, yet remains a sector we are concerned about following

the change in a key treaty with India. Tourism has experienced a

significant turnaround of fortunes and its prospects remain positive in

spite of weakening European currencies. Construction is coming off years

of recession and is expected to rebound should major – both private and

public – projects get green lighted. On the other hand, the manufacturing

sector is facing challenging times both domestically from heightened

competition and internationally due to prevailing uncertainty with

regards to our trading partners.

o Current macro fundamentals could be better but are not a grave concern

at the moment. We do remain concerned about a deterioration in the

Current Account both in terms of resulting spill-over effects and

productive-qualities of inflowing investment money. We expect inflation

to pick up in-line with rising commodity prices yet believe that interest

rates are unlikely to budge.

o From an international perspective, 2016 was dominated by unexpected

results of votes whose end results remain largely unknown and will likely

be felt not immediately but in the medium term. With the IMF forecasting

a worldwide growth rate of 3.5% in 2017, its fastest in 5Yrs, the outlook

for Emerging and Frontier markets appear to be brighter.

Key Indicators 2012 2013 2014 2015 2016 2017F 2018F

Gross Domestic Product [Rs bn] 349 372 392 410 435 460 490

GDP Growth [%] 3.5 3.4 3.7 3.5 3.8 3.8 3.9

Manufacturing [%] 2.1 4.7 1.8 0.0 0.3 0.6 1.4

Financial Services [%] 5.7 5.5 5.5 5.3 5.7 5.4 5.3

Tourism [%] 0.1 2.9 6.1 8.7 8.4 3.0 5.6

Construction [%] -3.0 -8.2 -8.5 -4.9 0.0 6.6 4.0

Balance of Payment [%] 1.7 4.5 5.9 4.9 3.6 2.6 2.7

Current Account Deficit [%] -7.2 -6.2 -5.6 -4.8 -4.6 -4.6 -4.7

Trade Deficit [%] -23.3 -20.8 -19.7 -18.1 -18.3 -9.1 -8.6

Budget Deficit [%] -1.8 -3.5 -3.2 -3.9 -3.5 -3.5 -3.3

Public Debt [%] 57.0 59.1 60.6 63.3 59.7 58.2 57.3

Inflation [%] 3.9 3.5 3.2 1.3 1.0 2.5 3.3

Unemployment rate [%] 8.0 8.0 7.8 7.9 7.5 7.4 7.4

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 2

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

BIRD’S EYE VIEW

The Mauritian economy grew at a sub-optimal average rate of

3.6% during the past five years. On the bright side, the change in

leadership at the helm of Government ended months of speculation

bringing added clarity to forward policies which is expected to be

beneficial for business.

Factors having afflicted growth momentum include: stimulus

packages reaching “maturity” upon project completion; private

investment slowing down in 2014 ahead of general elections in a

year dominated by political manoeuvres which then extended into

2015 amid shifting policies. The collapse of the BAI Group that same

year fuelled a reversal in business sentiment. The mood in the first

half of 2016 remained weak as a consequence of the renegotiated

Indo-Mauritian DTA, government-level bottlenecks, as well as intra-

cabinet bickering which led to a mini-cabinet re-shuffling. Sentiment

eventually turned around in the second half of 2016 following a

generally well received National Budget.

Figure 1. A Breakdown of the Mauritian Economy

The composition of the Mauritian economy remained more-or-less

the same. Construction, as a share of the economy, shrank by 47bps

annually which in turn resulted in lower demand for Credit. Weak

growth in Mauritius’ main trading partners hurt manufacturing

which also shed some 32bps annually. An unexpected observation

was the annualised 10bps growth in share of GDP for Trade which

appears to have been propped by lower petrol and food prices

instead of being curtailed – as anticipated – following the collapse

of the BAI Group. Other similarly appreciable gains were witnessed

mostly in Government-driven sectors e.g. Defence, Education,

Health and other support services.

1 On the back of inflated assets

Rankings

Mauritius – having consistently been within the Top 25 until 2014 –

tumbled to the 49th position in the World Bank’s 2017 Doing

Business ranking; although it retains its Top Spot in Sub-Saharan

Africa. Mauritius lost Doing Business ranks in most sub-segments

including “Starting a Business”, “Getting Electricity”, and

“Protecting Minority Investors”. With regards to the Ibrahim

Index of African Governance, Mauritius held on to the top spot

which it has never conceded.

Figure 2. Ease of Doing Business Ranking

SECTORIAL PERSPECTIVES

Finance

The Financial Sector has remained spectacularly resilient averaging

a 5.5% growth rate these past five years. This amazing feat becomes

more impressive given the collapse of one of the island’s largest Life

Insurers1 and a fairly small retail bank; as well as Mauritius finally

giving in to India’s demand of being allowed to apply its capital gains

tax on portfolio flows. It appears that Government intervention –

which created an unwelcome precedent of “Moral Hazard” –

propped the industry and prevented contagion. The entire debacle

paints a picture of poor oversight.

Figure 3. Financial Industry Growth Rate

Banks have seen a deterioration of their asset quality which coupled

with sluggish demand for Credit has resulted in weakened PAT

growth. On the plus side, should Government deliver on its

promise to kick-start major infrastructure projects in 2017, we

believe lending will pick up; in addition to the fact that banks are

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 3

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

increasingly diversifying into fee-driven operations such as Wealth

Management.

Our earnest concerns lie with Global Business following the

renegotiation of the Indo-Mauritian DTA. Since then, India has also

renegotiated other bilateral DTAs with various countries. The

Mauritian jurisdiction remains the most advantageous, yet flows are

unlikely to remain the same. Counter to intuition, the expected

reduction in flows will have an impact2 on the National Current

Account (C/A) and Overall Balance of Payments (BoP) whose

deterioration – from current positive levels – could hurt the MUR.

A depreciation of our national currency would fuel inflation which

would in turn affect highly leveraged companies should the logical

interest rate hike follow. In addition to the above, the spill-over

effects from fewer licensees and flows is poised to affect

Professional services such as Auditing, Secretarial, Legal and other

Support services. Although we paint a bleak picture, Mauritius has

a positive track-record of re-inventing troubled sectors.

Consequently, we believe that focusing efforts in cementing

Mauritius as a well-regulated Financial Centre will help companies

diversify both their lines of business and markets. While we shall

lose some players in the short term, the Mauritian entrepreneur

has often forsaken short-term gains in favour of long-term growth.

It is with this very mind-set that we believe local players will

successfully diversify and expand their business internationally.

Travel & Leisure

Following years of stagnation, the Tourism Industry has registered

high growth rates north of 8% during the last two years. Both

Tourism Receipts at Rs56bn and Arrivals at 1.275M have grown by

11% in 2016. This stellar performance however, has not been seen

in the financials of listed hoteliers for reasons specific to each

group’s strategy and to some extent a weak post-Brexit GBP. Island

wide Occupancy rates are expected to have stood ~300bps higher

in 2016 setting a new national record.

Figure 4. Tourist Arrivals & Receipts

This fresh growth spurt has been essentially driven by improved air

connectivity with both Europe and Asia. A majority of the new

flights are operated by Charters. This suits local hotel groups which

2 Daily transient flows represent a few percentage points of GDP

have grown accustomed to the Tour Operator model. Although

the industry is doing well, the major downside risk of such an

approach can result in lower occupancies in the event that the

Charter chooses to cease flights as has been the case of China

Southern Airlines and most recently low-cost operator, Air Asia X,

after just six months. Further, the lifting of the moratorium on new

hotel developments and Government’s intent to maintain an

“appropriate” air connectivity policy to foster diversification

suggest prospects for the hospitality industry are promising.

Figure 5. Hotels Growth Rate

Consumer Staples and Discretionary

Trade & Repairs

With a share of GDP averaging just short of 12% over the past five

years, Trade is on par with Financial Services in terms of size,

however growth has averaged ~3.0%. While we would have

expected the collapse of the BAI Group to hurt consumer

confidence resulting in a drop in trade, the effect appears to have

been limited. It would therefore seem fair to conclude that retailers,

many of whom said that business had been slow in 2014 & 2015,

were rather affected by greater competition following a

proliferation of medium to large sized malls across the island. We

believe record low inflation rates kept consumption rolling. The

recent ~10% increase in petrol and diesel prices however, might

curtail consumption in 2017. Consumption might be affected more

strongly in the following year when professionals with medium-to-

high disposable incomes become the collateral casualties of the

altered DTA.

Figure 6. Trade & Repairs Growth Rate

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 4

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

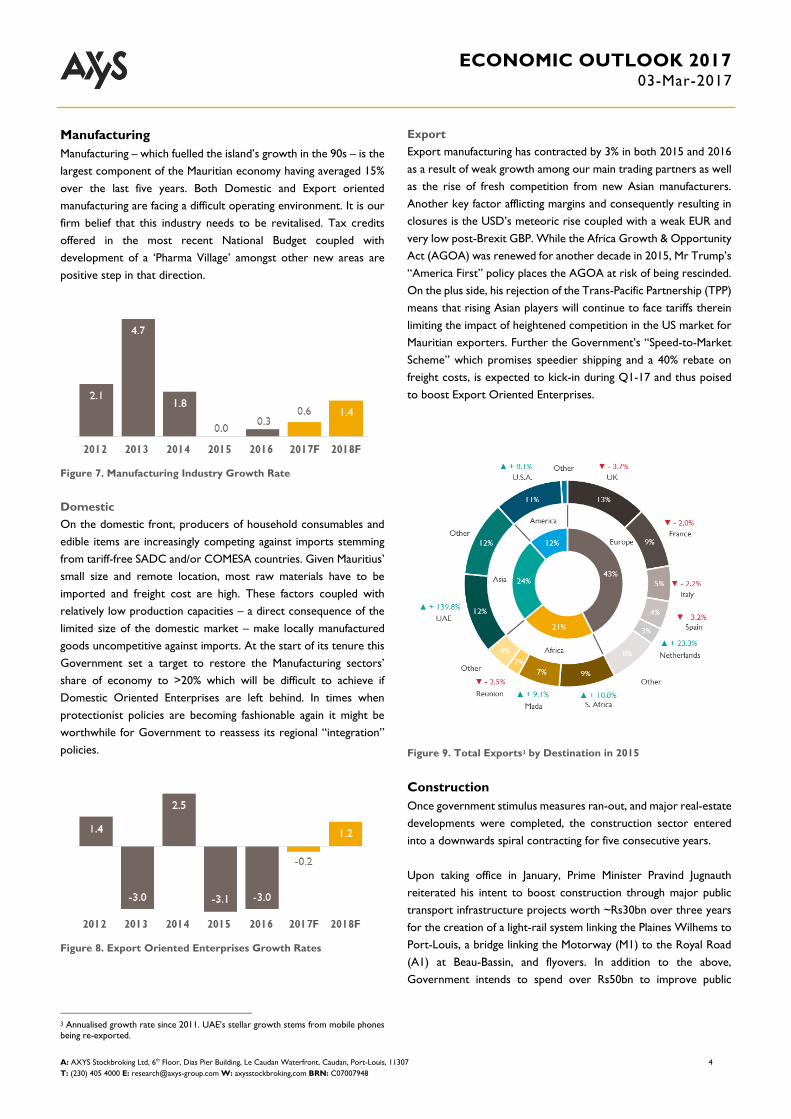

Manufacturing

Manufacturing – which fuelled the island’s growth in the 90s – is the

largest component of the Mauritian economy having averaged 15%

over the last five years. Both Domestic and Export oriented

manufacturing are facing a difficult operating environment. It is our

firm belief that this industry needs to be revitalised. Tax credits

offered in the most recent National Budget coupled with

development of a ‘Pharma Village’ amongst other new areas are

positive step in that direction.

Figure 7. Manufacturing Industry Growth Rate

Domestic

On the domestic front, producers of household consumables and

edible items are increasingly competing against imports stemming

from tariff-free SADC and/or COMESA countries. Given Mauritius’

small size and remote location, most raw materials have to be

imported and freight cost are high. These factors coupled with

relatively low production capacities – a direct consequence of the

limited size of the domestic market – make locally manufactured

goods uncompetitive against imports. At the start of its tenure this

Government set a target to restore the Manufacturing sectors’

share of economy to >20% which will be difficult to achieve if

Domestic Oriented Enterprises are left behind. In times when

protectionist policies are becoming fashionable again it might be

worthwhile for Government to reassess its regional “integration”

policies.

Figure 8. Export Oriented Enterprises Growth Rates

3 Annualised growth rate since 2011. UAE’s stellar growth stems from mobile phones

being re-exported.

Export

Export manufacturing has contracted by 3% in both 2015 and 2016

as a result of weak growth among our main trading partners as well

as the rise of fresh competition from new Asian manufacturers.

Another key factor afflicting margins and consequently resulting in

closures is the USD’s meteoric rise coupled with a weak EUR and

very low post-Brexit GBP. While the Africa Growth & Opportunity

Act (AGOA) was renewed for another decade in 2015, Mr Trump’s

“America First” policy places the AGOA at risk of being rescinded.

On the plus side, his rejection of the Trans-Pacific Partnership (TPP)

means that rising Asian players will continue to face tariffs therein

limiting the impact of heightened competition in the US market for

Mauritian exporters. Further the Government’s “Speed-to-Market

Scheme” which promises speedier shipping and a 40% rebate on

freight costs, is expected to kick-in during Q1-17 and thus poised

to boost Export Oriented Enterprises.

Figure 9. Total Exports3 by Destination in 2015

Construction

Once government stimulus measures ran-out, and major real-estate

developments were completed, the construction sector entered

into a downwards spiral contracting for five consecutive years.

Upon taking office in January, Prime Minister Pravind Jugnauth

reiterated his intent to boost construction through major public

transport infrastructure projects worth ~Rs30bn over three years

for the creation of a light-rail system linking the Plaines Wilhems to

Port-Louis, a bridge linking the Motorway (M1) to the Royal Road

(A1) at Beau-Bassin, and flyovers. In addition to the above,

Government intends to spend over Rs50bn to improve public

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 5

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

utilities infrastructure with a focus on renewable energy sources,

and replacement of leaky water pipes. Once kick-started such

medium-term projects are poised to stimulate growth for years to

come.

Figure 10. Construction Growth Rates

From a Private Sector perspective, weakened demand for high-end

real estate and moratorium on new hotels dampened Construction.

However, a little over a year following the introduction of ‘Smart-

City’ and ‘Property Development Schemes’, we expect

development permits granted to be on the rise and the process

simplified in coming years with a view to restore Mauritius’ Doing

Business Rank within the Top 25. Consequently, we believe this

industry will return to growth in years to come.

Figure 11. Location of Smart Cities

Property

Real Estate as a share of GDP has averaged 6.0% these last five years

but has experienced attenuated growth rates. The large supply of

new office buildings, commercial centres and residential apartments

has created a glut which is impacting rental on some properties, but

not for a select few well-positioned ones. Although we expect

rentals to remain stable in real terms over the years, the upcoming

developments should bring fresh impetus to the sector.

Figure 12. Property Growth Rate

MACROECONOMIC PERSPECTIVES

Monetary Policy

Figure 13. Headline Inflation Evolution

Headline inflation has fallen to record lows in recent years in-line

with sliding food and energy commodity prices which in turn gave

room for the Monetary Policy Committee (MPC) to lower the

Repo Rate by 40bps – largest cut in six years – to a record low 4.0%

in July 2016. Faced with now rising commodity prices, we expect

headline inflation to exceed 2% at the end of 2017 and 3% in 2018.

Given the fragility of the local economy and uncertain political and

economic climate in Europe, we do not believe that the MPC will

increase the Repo Rate this year. On the contrary, should the

EUR/USD fall below 1.05 and begin converging to parity, we believe

that the probability of a rate cut would increase significantly.

Figure 14. Key Repo Rate Evolution

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 6

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Yields

The Bank of Mauritius (BoM) initiated a programme – after it was

agreed that the sterilised funds would not form part of statutory

debt ceiling computations – to mop-up excess liquidity in the

system which was in part a consequence of reduced investment.

This has had a positive effect with Sovereign (T-Bill, Notes & Bonds)

Yields coming-off record lows and in turn boosting investment

income for banks and investment funds. Starting Mar 1st 2017, BoM

has trimmed the number of Primary Dealers down to four (MCB,

SBM, Barclays & AfrAsia) with the intention of boosting the

Secondary market. The fewer number of bidders is also expected

to contribute in pulling the yield curve upwards.

Figure 15. Mauritian Sovereign Yields Evolution

Government Finances

We note that the Budget Deficit – which we would prefer to see

contained under 3% – has oscillated between 3% to 4% but, given

the need to stimulate growth through Government spending in

infrastructure, we remain content at under 4% until the situation

improves. Although the Public Sector debt currently exceeds the

legal ceiling of 60%, it is not debilitating. We are therefore not

apprehensive of so long as the borrowed funds are used to

invigorate growth.

Figure 16. Budget Deficit and Debt Evolution

Balance of Payments

The latest Balance of Payments (BoP) and Current Account (C/A)

figures have been fundamentally improved to capture transiting

Global Business flows which was previously lost in “errors and

omissions”. Having highlighted our key concerns for these two

metrics going forward in our discussion on the possible outcome of

DTA renegotiation, we remain comfortable with a C/A Deficit

under 5% and a positive BoP.

Figure 17. CAD and BoP Evolution

Foreign Direct Investment

BoP has now remained positive for 10 consecutive years a feat

which has been accompanied by a surge in Foreign Direct

Investment (FDI) since the mid-noughties. FDI in 2015 and 2016

have hovered at ~Rs10bn coming off peaks of Rs20bn and Rs18bn

achieved in 2012 and 2014 respectively. The flows have remained

geared towards Real Estate – which has a new moniker “PDS”

replacing “IRS & RES” – which as investments in non-productive

asset impacts the quality of FDI. A shift in FDI mix with an increase

in “Manufacturing” and “Tourism” would for starters be a leading

indicator that strong economic growth might be on the way.

Figure 18. FDI Evolution in Rs bn

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 7

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Foreign Exchange

Figure 19. Currencies Evolution vs MUR

Given the large inward FDI and a positive BoP, it should not be a

surprise that the Rupee experiences consistent pressures towards

“strength” which the Central Bank alleviates through regular

monthly interventions on the foreign exchange market. Governor

Bheenick appears to have targeted a stable MUR Index4 through a

timely purchases of both USD and EUR whereas Governor Basant

Roi appears to be targeting5 a stable MUR/EUR rate exclusively and

rightly so through purchases of US Dollars. In the transition period

between Governors, the MUR depreciated by ~15% vis-à-vis peers

albeit with a slight lag – in-line with the Greenback’s surge – and

has since “gained” strength as a consequence of weakness in the

Single-currency and the Sterling.

Figure 20. MUR’s Evolution + BoM Interventions

This managed currency regime aids local companies which have

significant cross-border trade of goods and/or services.

Nonetheless, we often hear kvetching about the Rupee’s “super

strength”. If we were to apply the Economist’s light-hearted “Big

Mac Index” approach, with a Big Mac being sold at Rs94 compared

to $5.06 in USA, we discover that the MUR is undervalued by a

whopping 49% against the USD with an implied purchasing-power

parity exchange of Rs18.58. Wouldn’t that be a “super strong”

Rupee?

4 against a weighted basket of peer currencies 5 A policy aimed at helping exporters

Figure 21. Under v/s Over-valued currencies according to BigMac

Index

Labour

The unemployment rate which has averaged 7.9% over the

preceding five years is expected to drop to 7.4% in 2016. While this

improvement is welcome, we have not been particularly concerned

by the unemployment rate. As a country moving up the ladder in

terms of wealth per person and the high level of education

attainment, Mauritius is undergoing a transformation: the younger

generation has little interest in menial jobs. We believe that

imported labour is not replacing local labour, but rather filling the

vacuum created by locals not willing to take up some jobs.

Figure 22. Unemployment Evolution

The fact that youth unemployment is high is a signal for

Government to ensure that the new generation is given career

guidance to acquire skills-sets in the appropriate fields as well as

encouraging establishment of companies that would naturally

attract the millennials. The initiation of a “National Skills

Development Programme” is a positive step towards addressing the

more fundamental issue6 of jobs v/s skills mis-match.

6 Rather than raw unemployment

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 8

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

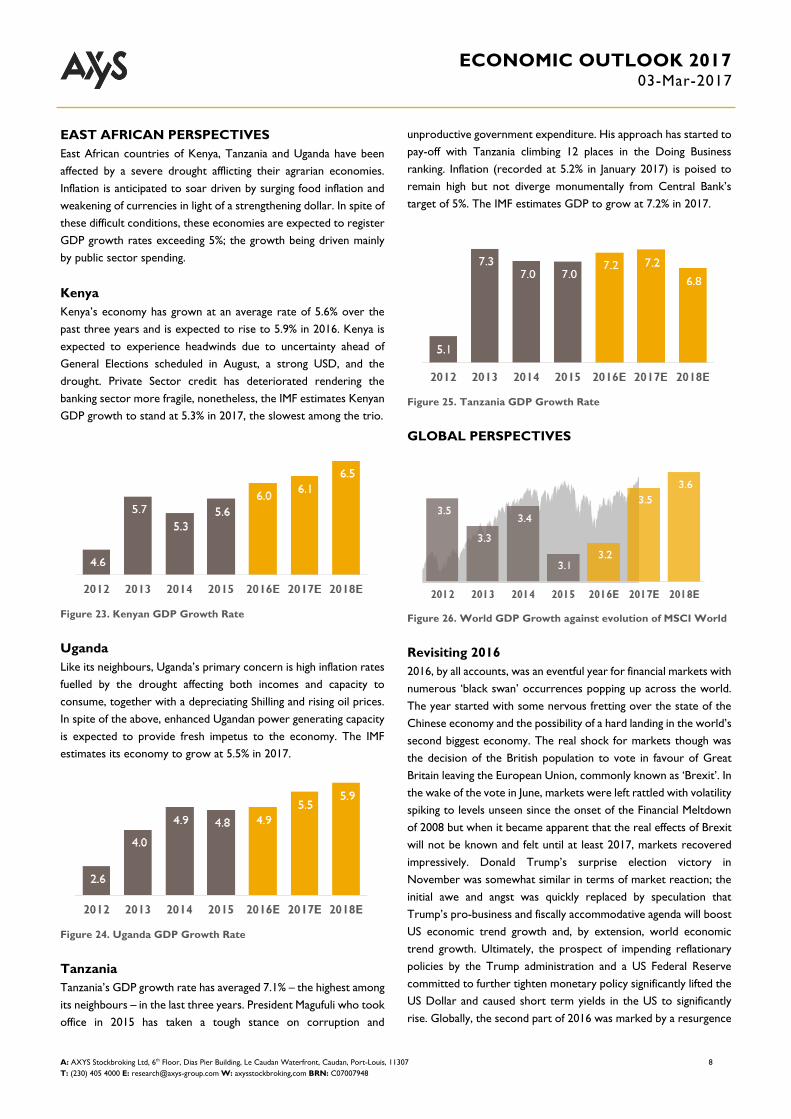

EAST AFRICAN PERSPECTIVES

East African countries of Kenya, Tanzania and Uganda have been

affected by a severe drought afflicting their agrarian economies.

Inflation is anticipated to soar driven by surging food inflation and

weakening of currencies in light of a strengthening dollar. In spite of

these difficult conditions, these economies are expected to register

GDP growth rates exceeding 5%; the growth being driven mainly

by public sector spending.

Kenya

Kenya’s economy has grown at an average rate of 5.6% over the

past three years and is expected to rise to 5.9% in 2016. Kenya is

expected to experience headwinds due to uncertainty ahead of

General Elections scheduled in August, a strong USD, and the

drought. Private Sector credit has deteriorated rendering the

banking sector more fragile, nonetheless, the IMF estimates Kenyan

GDP growth to stand at 5.3% in 2017, the slowest among the trio.

Figure 23. Kenyan GDP Growth Rate

Uganda

Like its neighbours, Uganda’s primary concern is high inflation rates

fuelled by the drought affecting both incomes and capacity to

consume, together with a depreciating Shilling and rising oil prices.

In spite of the above, enhanced Ugandan power generating capacity

is expected to provide fresh impetus to the economy. The IMF

estimates its economy to grow at 5.5% in 2017.

Figure 24. Uganda GDP Growth Rate

Tanzania

Tanzania’s GDP growth rate has averaged 7.1% – the highest among

its neighbours – in the last three years. President Magufuli who took

office in 2015 has taken a tough stance on corruption and

unproductive government expenditure. His approach has started to

pay-off with Tanzania climbing 12 places in the Doing Business

ranking. Inflation (recorded at 5.2% in January 2017) is poised to

remain high but not diverge monumentally from Central Bank’s

target of 5%. The IMF estimates GDP to grow at 7.2% in 2017.

Figure 25. Tanzania GDP Growth Rate

GLOBAL PERSPECTIVES

Figure 26. World GDP Growth against evolution of MSCI World

Revisiting 2016

2016, by all accounts, was an eventful year for financial markets with

numerous ‘black swan’ occurrences popping up across the world.

The year started with some nervous fretting over the state of the

Chinese economy and the possibility of a hard landing in the world’s

second biggest economy. The real shock for markets though was

the decision of the British population to vote in favour of Great

Britain leaving the European Union, commonly known as ‘Brexit’. In

the wake of the vote in June, markets were left rattled with volatility

spiking to levels unseen since the onset of the Financial Meltdown

of 2008 but when it became apparent that the real effects of Brexit

will not be known and felt until at least 2017, markets recovered

impressively. Donald Trump’s surprise election victory in

November was somewhat similar in terms of market reaction; the

initial awe and angst was quickly replaced by speculation that

Trump’s pro-business and fiscally accommodative agenda will boost

US economic trend growth and, by extension, world economic

trend growth. Ultimately, the prospect of impending reflationary

policies by the Trump administration and a US Federal Reserve

committed to further tighten monetary policy significantly lifted the

US Dollar and caused short term yields in the US to significantly

rise. Globally, the second part of 2016 was marked by a resurgence

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 9

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

in economic activity as the Eurozone and China witnessed a pick up

in the pace of expansion of their respective manufacturing and

services sectors.

Figure 27. SSA Growth against evolution of MSCI Frontier

Looking Ahead

Financial markets are riding high on optimism going into 2017 as

most expect the feel good sentiment surrounding the US economy

to propagate worldwide at some point this year. Market

participants have already mostly priced in an improved growth story

for the US and it remains to be seen whether Trump can transform

his ‘populist’ rhetoric into concrete policies. Equally important is an

objective assessment of the spill over effects of Trump-ism on other

economies, particularly China. According to numerous economists,

2016 was the start of a ‘de-globalisation’ trend; it remains to be

seen whether 2017 confirms this new state of affairs. In Europe, the

resurgent economy is somewhat clouded by a busy political

calendar. More than half a dozen European countries head to the

polls in 2017 with important elections being held in Germany,

France and to some extent Italy. Should the Eurozone be able to

navigate through this delicate year unscathed politically, its equity

markets are likely to post significant returns as economic growth

prospects are encouraging - courtesy of the ongoing European

Quantitative Easing (QE). Inflationary pressures are likely to come

to the fore in the United Kingdom as the effects of the significantly

depreciated Pound Sterling (GBP) on imported prices are felt

broadly across the UK economy and booming economic activities

also add to inflationary pressures. Last but not least, Emerging

Markets should continue to recover with a positive outlook for

both their respective currencies and equity markets. For instance,

Brazil was the standout performer last year, with its equity index,

the Bovespa Index rising by more than 60% in USD terms. Should

the world economy be effectively in a cyclical upturn as recent

economic figures suggest, the outlook for Emerging Markets will

brighten further.

CONCLUDING REMARKS

The freshly re-constituted cabinet combined with clearer policies

render the outlook for coming appreciably brighter than in recent

years. Government intends to boost the economy through major

infrastructure projects which should improve the velocity of money

which in turn signals an economy in bloom. Nonetheless,

headwinds, exist: we have expressed our concerns for the financial

sector which will require both transformation and stronger

regulation in order to diversify and develop fresh lines of business

as well as potential; and we have also discussed the repercussions

of rising inflation and currency volatility on our economy in times

of cries for greater protectionism abroad. Should this

administration deliver on its renewed promises, we expect

prospects to remain positive with a GDP growth rate of 3.8% in

2017 increasing to 3.9% in 2018.

Figure 28. Mauritius Growth against evolution of SEM

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 10

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

APPENDIX A – MAURITIUS KEY INFO

Country Information

Appellation Republic of Mauritius

Independence | Rep. March 12, 1968 | 1992

Government Westminster Dem.

President Dr Gurib-Fakim, Ameenah

Prime Minister Jugnauth, Pravind

Suffrage Universal, >18yrs

Off. & Biz. Language English & French

Geography

Area 2,040 km2

Excl. economic zone 1.9M km2

Capital Port-Louis

Location 20° 10' S; 57° 30' E

Time Zone GMT +4 hrs

Climate Sub-tropical

Tel. country code 230

Intnet country code .mu

Demographics

Population 1,263,500

Popn growth rate 0.24%

Median age 35.3 yrs

Life expectancy 75.4 yrs

Workforce 613,900

Unemployment 7.5%

Literacy 90.6% (2015)

Poverty 9.4% (2012)

Currency

Nomenclature Mauritian Rupee

Symbol/code Rs / MUR

Exchange rate (Mid) USD Rs 31.47 per USD

Exchange rate (Mid) EUR Rs 40.77 per EUR

Economy (2016)

GDP growth rate 3.8%

GDP at mkt price Rs 434.6bn

GDP per capita Rs 344,000

GDP ppp $ 25.9bn (138st)

GDP ppp per capita $ 20,500 (86th)

Budget deficit 3.5% of GDP

Public debt 59.7% of GDP

Current A/C deficit 4.6% of GDP

Headline Inflation 0.98%

Reserves 12.1 Months

Stock Exchange (2016)

Stocks | Fix Inc | ETFs 94 | 27 | 5

Key Indices Semdex | Alex 20

Market Cap Rs 279bn [64% of GDP]

Mean daily turnover Rs 60.2M [$ 1.88M]

Market PER | DY 16.42x | 3.08%

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 11

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

APPENDIX B – LISTED STOCKS BY SECTOR

Financial Services

Direct LCP @ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

MCB ▲ 226.50 7.2 8.2x 3.9% Comm. Banking

SBM ▲ 7.02 3.2 7.7x 4.3% Comm. Banking

ABCB ▲ 27.70 58.3 12.0x 1.9% Comm. Banking

MEI ▲ 83.00 -0.9 6.8x 2.7% Gen. Insurance

MUA ▲ 61.00 1.7 16.5x 4.1% Gen. Insurance

SWAN ▲ 305.00 -20.3 10.9x 3.9% Gen. Insurance

SWANL ▲ 1,250.00 30.9 34.3x 3.7% Life Insurance

CIM ▲ 7.68 2.4 9.4x 4.4% Global Biz. & Cons Fin.

FINC ▲ 21.10 -3.9 27.2x 2.8% Leasing

IBL ▲ 36.20 48.1 565.8x 1.0% Glob Biz., Insu, Leasing & Banking

ROGE ▲ 28.75 0.5 68.5x 3.1% Glob Biz. & Insurance

UTIN ▼ 9.50 -25.4 ▬ 0.0% Glob Biz., Leasing, Wealth

CIEL ▲ 6.38 -0.3 12.1x 2.8% Glob Biz, Banking, Wealth

Indirect LCP @ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

TERRA ▲ 32.15 5.4 17.4x 2.6% SWAN, SWANL, & UTIN

NITL ▲ 23.90 29.2 9.4x 3.7% SICOM

BMHL ▼ 27.60 2.0 48.7x 2.9% IBL & AfrAsia

ENLL ▲ 43.40 -7.7 #### 2.9% ROGE

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% ENLL

EUDC ▲ 18.00 16.1 16.3x 4.4% SWAN

Travel & Leisure

Arts & Entertainment

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

LOTO ▼ 5.72 68.2 21.6x 4.7% Lotto

ASL ▲ 59.00 57.8 7.3x 6.8% Sports Betting

MEDL ▼ 63.00 4.1 46.3x 2.7% Theme Park (Casela)

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

GAMMA ▼ 24.65 7.2 10.2x 3.7% LOTO

o Banks MCB, and SBM should be on your watch

list for their attractive PERs. Their lower Loan-

Deposit Ratios than in recent years suggests

room to improve Interest Income once the

economy re-ignites.

o Companies with an appreciable fraction of their

Global Business operations geared towards India

are poised to face turbulent times ahead while

opportunities are expected to be in Africa.

o Gaming companies LOTO and ASL that have

experienced a rough spell following a shift in

Government policies, which appear to have

stabilized.

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 12

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Travel & Leisure

Accommodation & Food Services

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

NMHL ▲ 20.95 -1.6 ▬ 0.0% Mtius, Sey, Moroc. (★ 4-5+)

LUX ▼ 58.00 -0.8 18.4x 2.0% Indian Ocean, Mid East, China (★ 3-5)

SUN ▲ 39.30 14.7 ▬ 0.0% Mtius, Mdves (★ 4-5)

CHSL ▲ 34.25 6.2 93.6x 1.9% Mtius, Sey, Mdves (★ 5-5+)

SCT ▲ 5.00 -9.1 32.4x 0.0% Mtius (★ 4)

MOLI ▬ 41.20 -1.4 ▬ 0.0% Hilton Mtius (★ 5)

TPL ▼ 6.10 5.5 35.2x 0.9% Indigo {Biz. Hotel} (★ 4-5)

ROGE ▲ 28.75 0.5 68.5x 3.1% VLH & NMHL (★ 3-5)

UTIN ▼ 9.50 -25.4 ▬ 0.0% Attitude (★ 3-5)

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

HTLS ▼ 30.90 -9.1 56.2x 2.0% CHSL

CIEL ▲ 6.38 -0.3 12.1x 2.8% SUN

MEDL ▼ 63.00 4.1 46.3x 2.7% Tamarina (★ 4)

EUDC ▲ 18.00 16.1 16.3x 4.4% Palmeraie (★ 4)

GAMMA ▼ 24.65 7.2 10.2x 3.7% MOLI

UNSE ▼ 26.00 -23.5 ▬ 0.0% SCT

LFL ▲ 31.50 17.8 7.1x 3.8% TPL

LMLC ▲ 215.00 26.3 9.8x 3.7% TPL

PAD ▲ 97.75 2.9 21.1x 3.3% TPL, MEDL

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% TPL, VLH, NMHL

ENLL ▲ 43.40 -7.7 #### 2.9% NMHL, VLH, TPL

Transport & ICT

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

MK ▲ 14.55 7.8 1.3x 0.0% Airline

RHT ▬ 25.25 -6.5 68.7x 4.4% Public Transport (Bus)

UBS ▬ 36.35 12.5 9.9x 2.8% Public Transport (Bus)

MFD ▬ 9.84 -6.3 11.1x 2.0% Freeport & Logistics

ROGE ▲ 28.75 0.5 68.5x 3.1% Logistics

IBL ▲ 36.20 48.1 565.8x 1.0% Logistics

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

PAD ▲ 97.75 2.9 21.1x 3.3% MFD

ENLL ▲ 43.40 -7.7 #### 2.9% ROGE

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% ENLL

o With Tourism having picked up momentum, we

expect hoteliers to improve their bottom lines

through higher room rates in spite of high

indebtedness. On the flip side, weaker EUR and

GBP could impact revenue as will planned

renovations of hotels in the coming low season.

SUN, CHSL, and TPL are likely to experience the

least disruptive low-seasons from renovations.

o Logistics companies MFD, ROGE and IBL

are expected to fare substantially better in

the medium term should the planned

enhancement in port infrastructure

materialize. On the other hand, public

transport companies RHT and UBS could

face rough times if they do not alter their

existing operating models once the Metro

becomes live.

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 13

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Agriculture

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

CSE ▲ 105.00 2.9 11.9x 4.3% Farming (Sugar, Lifestock)

UNSE ▼ 26.00 -23.5 ▬ 0.0% Farming (Sugar, Crops)

INNO ▲ 40.00 -5.9 17.7x 4.6% Farming (Poultry)

ALTEO ▲ 30.50 8.9 23.8x 2.7% Farming (Sugar)

TERRA ▲ 32.15 5.4 17.4x 2.6% Farming (Sugar)

OMNI ▲ 63.00 -10.6 ▬ 3.2% Farming (Sugar)

MEDL ▼ 63.00 4.1 46.3x 2.7% Farming (Sugar)

ENLL ▲ 43.40 -7.7 #### 2.9% Farming (Sugar) & Foods

ROGE ▲ 28.75 0.5 68.5x 3.1% Farming (Sugar)

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% ENLL & Eclosia

CIEL ▲ 6.38 -0.3 12.1x 2.8% ALTEO

PAD ▲ 97.75 2.9 21.1x 3.3% MEDL

IBL ▲ 36.20 48.1 565.8x 1.0% Fishing + ALTEO

Manufacturing

Staples

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

INNO ▲ 40.00 -5.9 17.7x 4.6% Dairy & Yogurt

MOR ▲ 28.00 11.1 17.7x 4.6% Edible Oils

PBL ▬ 420.00 16.7 18.5x 2.3% Beverages

QBL ▲ 8.90 34.8 3.4x 11.2% Beverages (Soft only)

LMLC ▲ 215.00 26.3 9.8x 3.7% Flour

LFL ▲ 31.50 17.8 7.1x 3.8% Livestock feeds

MIL ▬ 923.00 0.0 28.7x 2.2% Margarine

SAIL ▲ 18.60 -7.0 3.9x 5.4% Soap & Detergents

MCOS ▬ 25.00 -16.7 ▬ 2.0% Cosmetics

PCCL ▬ 25.00 0.0 6.7x 2.0% Tissue & Toilet Paper

ALTEO ▲ 30.50 8.9 23.8x 2.7% Milling/Refining (Sugar)

TERRA ▲ 32.15 5.4 17.4x 2.6% Milling (Special Sugars)

OMNI ▲ 63.00 -10.6 ▬ 3.2% Milling/Refining (Sugar)

MEDL ▼ 63.00 4.1 46.3x 2.7% Milling (Sugar)

IBL ▲ 36.20 48.1 565.8x 1.0% Fish Processing

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

IBL ▲ 36.20 48.1 565.8x 1.0% Fishing & Proc. + PBL

PHIN ▲ 268.75 16.8 13.5x 3.1% PBL

CIEL ▲ 6.38 -0.3 12.1x 2.8% ALTEO

o The Primary sector, once the lifeline of Mauritius,

has been relegated to 3rd place. Sugarcane fields

are increasingly being abandoned or turned into

property developments. Although Government is

encouraging growing increasingly “bio” vegetables

locally to ensure subsistence, these are unlikely to

bring in massive profits. Sugarcane farmers,

ALTEO, TERRA, OMNI, MEDL, ENLL, UNSE,

CSE will experience cyclical swings in profitability

in-line with sugar prices. Fishing (IBL) is also a

cyclical activity with Mauritius facing stiff

completion from Latin American and Asian

countries when attempting to penetrate

developed markets.

o Like traders, manufacturers of edible and

household items, MOR, QBL, MIL, SAIL, MCOS,

& PCCL, aimed at the local market are finding it

increasingly difficult to grow margins due to tariff-

free imports produced in SADC/COMESA

increasingly find their way on shelves. Sugar

millers/refiners (ALTEO, TERRA, OMNI) and

seafood companies (IBL) on the other hand face

cyclical up-turns and downturns. While higher

sugar prices bode well for sugar conglomerates,

the end of the EU quota system this year will bring

forth a fresh set of challenges.

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 14

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Manufacturing

Discretionary

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

CTL ▼ 42.00 6.6 7.0x 7.7% Textiles

PIM ▲ 65.00 4.8 8.8x 5.4% Plastics

GAZ ▲ 65.00 -15.6 19.5x 4.2% Gases (Medical & Industrial)

MCFI ▼ 17.40 -4.1 93.0x 0.0% Fertilizers + CHEM

CHEM ▼ 17.20 1.2 11.4x 6.4% Chemicals

BYCH ▼ 4.02 -19.6 83.1x 2.0% Chemicals

ENLC ▲ 14.30 -19.7 ▬ 0.0% Goods + Bldg Mat

EUDC ▲ 18.00 16.1 16.3x 4.4% Distillery

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

HML ▼ 66.00 -21.4 63.5x 2.7% MCFI, BYCH, CHEM

UTIN ▼ 9.50 -25.4 ▬ 0.0% Liquid Fertilizers + GAZ

PAD ▲ 97.75 2.9 21.1x 3.3% EUDC

CIEL ▲ 6.38 -0.3 12.1x 2.8% CTL

Trade & Repairs

Direct LCP @ Δ [%] Key Ratios

3-Mar YoY PER DY Activity

INNO ▲ 40.00 -5.9 17.7x 4.6% Foods & Diapers

CMPL ▼ 8.50 -40.5 ▬ 0.0% Supermarket Chain

ENLC ▲ 14.30 -19.2 ▬ 0.0% Car dealerships

ABC ▲ 92.00 8.2 5.7x 2.4% Car dealerships

ACC ▲ 145.50 -4.9 5.6x 2.7% Trye & Spare Parts

MSIL ▬ 30.65 -3.0 7.6x 3.3% Tyre re-threader

VEM ▲ 119.00 32.2 12.3x 2.5% Petrol stations

IBL ▲ 36.20 47.7 565.8x 1.0% Retail (Supermarkets)

TERRA ▲ 32.15 5.4 17.4x 2.6% Specialised stores + HML

HML ▼ 66.00 -21.4 63.5x 2.7% Technology + CMPL

o Manufacturers focusing on exports (CTL) are

hurting from uncertainty in their export markets

and weak currencies while those producing for

the local market (MCFI, CHEM, BYCH, PIM) are

impacted by both slowing demand for their goods

and imports.

o Consumption has been surprisingly resilient in

recent years. Despite a pick-up in inflation, we

expect consumption to maintain its momentum

but will unlikely translate to profits for listed retail

focused entities who have seen margins shrink as

a consequence of an increasingly fractionated

market with more and more players competing

for a limited market.

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 15

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

Construction

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Activity

UBP ▲ 103.00 32.1 19.5x 2.9% Bldg Materials

GAMMA ▼ 24.65 7.2 10.2x 3.7% Bldg Materials & Contracting

BEEP ▲ 17.00 -6.1 ▬ 0.0% Bldg Materials

IBL ▲ 36.20 48.1 565.8x 1.0% Civil Engineering, M&E

ENLL ▲ 43.40 -7.7 #### 2.9% Contracting

FORT ▼ 141.50 1.3 4.0x 5.3% Engineering

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

TERRA ▲ 32.15 5.4 17.4x 2.6% Rehm Grinaker, Terrarock

HML ▼ 66.00 -21.4 63.5x 2.7% Rehm Grinaker

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% ENLL

Real Estate

Direct

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

ASCE ▼ 12.00 -9.8 26.8x 3.2% Retail & Offices

CAUD ▲ 0.99 -2.0 51.9x 0.0% Retail & Offices

CIMO ▼ 429.00 -3.4 13.8x 4.9% Retail

NOVUS ▬ 9.20 22.7 20.8x 4.9% Industrial & Office

APL ▬ 10.00 -0.5 24.4x 6.9% Hotel

COVI ▲ 6.26 0.6 17.9x 0.0% Hotel

UTDL ▲ 56.25 -19.6 59.5x 0.0% Offices & Land

BLFE ▼ 2.28 -34.5 ▬ 0.0% Property Development

ALTEO ▲ 30.50 8.9 23.8x 2.7% Property Development

MEDL ▼ 63.00 4.1 46.3x 2.7% Education focused Smart City

ENLL ▲ 43.40 -7.7 #### 2.9% Property Development

ROGE ▲ 28.75 0.5 68.5x 3.1% Property Development

OMNI ▲ 63.00 -10.6 ▬ 3.2% Airport focused Smart City

TERRA ▲ 32.15 5.4 17.4x 2.6% Upcoming Property Development

Indirect

LCP

@ Δ [%] Key Ratios

2-Mar YoY PER DY Through investment in

CIEL ▲ 6.38 -0.3 12.1x 2.8% ALTEO

PAD ▲ 97.75 2.9 21.1x 3.3% MEDL, CAUD

ENL(P) ▲ 26.00 -4.6 131.4x 3.0% ENLL, ROGE

o Companies producing construction materials

(UBP, GAMMA) and involved in contracting

(GAMMA, ENLL, TERRA, HML) are expected to

see appreciable improvements in coming years.

The timing of the boost is of course a function of

how fast or late Government will green-light the

various projects that have been announced in last

year’s budget.

o REIT-Type “Rental Income” focused companies

(APL, NOVUS, ASCE, COVI, CAUD and CIMO),

including GBL1s, are likely to remain good

sources of yields. In spite of a mushrooming of

malls, rentals are stable if not firming and usually

carry inflation linked escalation clauses.

o Property developers on the other hand

experienced cyclical phases of high losses

followed by an excellent year when the

development is delivered. ENLL and ROGE have

experienced slowing sales in Bel Ombre while

ALTEO is poised to deliver Amalthea in coming

months as will BLFE in Azuri phase 2. All of MEDL,

ENLL, OMNI and TERRA have projects in their

pipelines and are therefore expected to register

the resulting initial losses in coming years.

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 16

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

REFERENCES

International Monetary Fund, ‘World Economic Outlook October

2016’, <http://www.imf.org/external/pubs/ft/weo/2016/02/>. [October

2016].

International Monetary Fund, ‘World Economic Outlook Update

January 2017’,

<https://www.imf.org/external/pubs/ft/weo/2017/update/01>. [January

2017].

International Monetary Fund, ‘2015 Article IV Consultation -

Mauritius’, <http://www.imf.org/external/country/mus/>. [March

2016].

Minister of Finance and Economic Development, ‘Budget 2016-

2017’, < http://budget.mof.govmu.org/>. [July 2016].

Statistics Mauritius, ‘Digest of External Trade Statistics 2015’,

<http://statsmauritius.govmu.org/English/StatsbySubj/Pages/External-

Trade.aspx>. [October 2016].

Statistics Mauritius, ‘International Travel & Tourism’,

<http://statsmauritius.govmu.org/English/StatsbySubj/Pages/International

-Travel-and-Tourism.aspx>. [December 2016].

Statistics Mauritius, ‘Labour – Labour Force, Employment and

Unemployment’,

<http://statsmauritius.govmu.org/English/StatsbySubj/Pages/Labour.aspx

>. [May 2016].

Statistics Mauritius, ‘National Account and Investments’,

<http://statsmauritius.govmu.org/English/StatsbySubj/Pages/National-

Accounts.aspx>. [December 2016].

Board of Investment, ‘Speed to Market Scheme’,

<http://www.investmauritius.com/news-room/latest-news/mauritius-

launches-speed-to-market-scheme-to-boost-exports-to-the-european-

union.aspx>. [January 2017].

Board of Investment, ‘BOI issues first Smart City Certificate -

Omnicane’, <http://www.investmauritius.com/news-room/latest-

news/boi-issues-first-smart-city-certificate.aspx>. [September 2016].

Board of Investment, ‘BOI issues Smart City Certificate to Cap

Tamarin Ltée’ & ‘Letter of Intent for City of Moka’,

<http://www.investmauritius.com/news-room/latest-news/boi-issues-

smart-city-certificate-to-cap-tamarin-lt%C3%A9e.aspx>. [October

2016].

Mauritius JinFei Economic Trade and Cooperation Zone Co., Ltd,

‘Obtention of Letter of Intent for Smart City Scheme (SCS)

Certificate’, <http://www.jfjmy.5dlc.com/newsdefault/1996/19176>.

[October 2016].

Defi Media, ‘Projets: Medine investit Rs 1,3 Mddans sa Smart City

en 2017’, <http://defimedia.info/projets-medine-investit-rs-13-

mddans-sa-smart-city-en-2017>. [December 2016].

Defi Media,’16 «smart cities» sur le plan de travail’,

<http://defimedia.info/16-smart-cities-sur-le-plan-de-travail>.

[December 2015].

Bank of Mauritius 2017, ‘Monthly Statistical Bulletin January 2017’,

<https://www.bom.mu/publications-statistics/monthly-statistical-bulletin>.

[January 2017].

Bank of Mauritius 2017, ‘Key Repo Rate February 2017’,

<https://www.bom.mu/repo-rate>. [20 February 2017].

Bank of Mauritius 2017, ‘Consolidated Indicative Exchange Rates’,

<https://www.bom.mu/markets/foreign-exchange/consolidated-

indicative-exchange-rates>. [28 February 2017].

Bank of Mauritius 2017, ‘Government of Mauritius Treasury Bills

(GMTB)’, <https://www.bom.mu/markets/money-markets/gmtb>.

[February 2017].

ECONOMIC OUTLOOK 2017 03-Mar-2017

A: AXYS Stockbroking Ltd, 6th Floor, Dias Pier Building, Le Caudan Waterfront, Caudan, Port-Louis, 11307 17

T: (230) 405 4000 E: [email protected] W: axysstockbroking,com BRN: C07007948

DISCLAIMER

AXYS Stockbroking Ltd has issued this document without

consideration of the investment objectives, financial situation or

particular needs of any individual recipient. Recipients should not

act or rely on any recommendation in this document without

consulting their financial adviser to determine whether the

recommendation is appropriate to their investment of this

document.

This document is not, and should not be construed as, an offer to

sell or the solicitation of an offer to purchase or subscribe for any

investment. This document has been based on information obtained

from sources believed to be reliable but which have not been

independently verified.

AXYS Stockbroking Ltd makes no guarantee, representation or

warranty and accepts no responsibility or liability as to its accuracy

or completeness. AXYS Stockbroking Ltd and its officers, directors

and representatives may have positions in securities mentioned in

this document, or in related investments, and may from time to

time add to or dispose of such securities or investments. AXYS

Stockbroking Ltd is a member of the Stock Exchange of Mauritius

and is licensed by the Financial Services Commission.

AUTHORS

Bhavik Desai

Head of Research

Prerna Cheekhooree

Research Analyst

Alexis Corson

Investment Analyst

ACKNOWLEDGEMENTS

Kugan Parapen

Portfolio Manager

AXYS Investment Partners

Joy D’Souza

Head of Research

ApexAfrica Capital Ltd (part of AXYS Group)

Abizer Shafarali

Senior Research Analyst

ApexAfrica Capital Ltd (part of AXYS Group)

Harrison Ngugi

Research Analyst

ApexAfrica Capital Ltd (part of AXYS Group)

Jason Theeroovengadum

Chief Dealer

AXYS Leasing

Melvyn Chung Kai To

Managing Director

AXYS Stockbroking