Economic Nationalism in Mergers and...

44

THE JOURNAL OF FINANCE • VOL. LXVIII, NO. 6 • DECEMBER 2013 Economic Nationalism in Mergers and Acquisitions I. SERDAR DINC and ISIL EREL ∗ ABSTRACT This paper studies government reactions to large corporate merger attempts in the European Union during 1997 to 2006 using hand-collected data. We document widespread economic nationalism in which the government prefers that target com- panies remain domestically owned rather than foreign-owned. This preference is stronger in times and countries with strong far-right parties and weak governments. Nationalist government reactions have both direct and indirect economic impacts on mergers. In particular, these reactions not only affect the outcome of the mergers that they target but also deter foreign companies from bidding for other companies in that country in the future. “Come sta?” 1 CORPORATE MERGERS AND ACQUISITIONS are an important part of a market econ- omy. Large firms often enter into a new market through acquisitions of local firms. If there is excess capacity in a sector, weak firms often exit the economy, not necessarily through bankruptcy, but by being acquired by another firm. When such mergers take place between companies from different countries, national economies become more integrated. Yet, the reaction of governments to merger attempts often seems to be motivated by concerns other than compe- tition. In particular, government interventions often appear to depend on the “nationality” of the acquiring company. Nationalist interventions by domestic governments do not simply take the form of opposition to foreign acquirers. They also include support for domestic ∗ Serdar Dinc is with Rutgers Business School and Isil Erel is with the Ohio State University, Fisher College of Business. We would like to thank L. Iv´ an Alfaro, Ji-Woong Chung, and John Sedunov for providing excellent research assistance. We are grateful to Christopher Wendt for sharing his voting data. We also would like to thank the referee; the Associate Editor; Kenneth Ahern; Campbell Harvey (the Editor); Randall Morck; John Parsons; Roberto Rigobon; Paola Sapienza; Antoinette Schoar; Ren´ e Stulz; Michael Weisbach; Christopher Wendt; and seminar participants at 2012 American Finance Association Meetings, Brandeis University, Chicago Fed, Federal Reserve Board of Governors, Georgetown University, MIT, Ohio State University, Philadel- phia Fed, Rutgers University, and University of Houston for comments. The usual disclaimer applies. 1 This quote is French President Charles de Gaulle’s greeting in Italian to Franc ¸ois Michelin, who was summoned to the presidential office upon rumors that he was about to sell the French carmaker Citroen he controlled to Italian Fiat. Shortly thereafter it was arranged that Peugeot, another French carmaker, would acquire Citroen (see Betts (2001)). DOI: 10.1111/jofi.12086 2471

Transcript of Economic Nationalism in Mergers and...

THE JOURNAL OF FINANCE • VOL. LXVIII, NO. 6 • DECEMBER 2013

Economic Nationalism in Mergersand Acquisitions

I. SERDAR DINC and ISIL EREL∗

ABSTRACT

This paper studies government reactions to large corporate merger attempts inthe European Union during 1997 to 2006 using hand-collected data. We documentwidespread economic nationalism in which the government prefers that target com-panies remain domestically owned rather than foreign-owned. This preference isstronger in times and countries with strong far-right parties and weak governments.Nationalist government reactions have both direct and indirect economic impacts onmergers. In particular, these reactions not only affect the outcome of the mergers thatthey target but also deter foreign companies from bidding for other companies in thatcountry in the future.

“Come sta?”1

CORPORATE MERGERS AND ACQUISITIONS are an important part of a market econ-omy. Large firms often enter into a new market through acquisitions of localfirms. If there is excess capacity in a sector, weak firms often exit the economy,not necessarily through bankruptcy, but by being acquired by another firm.When such mergers take place between companies from different countries,national economies become more integrated. Yet, the reaction of governmentsto merger attempts often seems to be motivated by concerns other than compe-tition. In particular, government interventions often appear to depend on the“nationality” of the acquiring company.

Nationalist interventions by domestic governments do not simply take theform of opposition to foreign acquirers. They also include support for domestic

∗Serdar Dinc is with Rutgers Business School and Isil Erel is with the Ohio State University,Fisher College of Business. We would like to thank L. Ivan Alfaro, Ji-Woong Chung, and JohnSedunov for providing excellent research assistance. We are grateful to Christopher Wendt forsharing his voting data. We also would like to thank the referee; the Associate Editor; KennethAhern; Campbell Harvey (the Editor); Randall Morck; John Parsons; Roberto Rigobon; PaolaSapienza; Antoinette Schoar; Rene Stulz; Michael Weisbach; Christopher Wendt; and seminarparticipants at 2012 American Finance Association Meetings, Brandeis University, Chicago Fed,Federal Reserve Board of Governors, Georgetown University, MIT, Ohio State University, Philadel-phia Fed, Rutgers University, and University of Houston for comments. The usual disclaimerapplies.

1 This quote is French President Charles de Gaulle’s greeting in Italian to Francois Michelin,who was summoned to the presidential office upon rumors that he was about to sell the Frenchcarmaker Citroen he controlled to Italian Fiat. Shortly thereafter it was arranged that Peugeot,another French carmaker, would acquire Citroen (see Betts (2001)).

DOI: 10.1111/jofi.12086

2471

2472 The Journal of Finance R©

acquirers to create domestic companies that are considered too big to be ac-quired by foreigners. For instance, consider the following comment by formerfinance minister Dominique Strauss-Cahn about the French government’s sup-port for the merger of two French oil companies, Elf and Total Fina:

[The merger will create] a French oil group that is almost at the level ofthe three world leaders and therefore really protected from any takeoverattempt by an Anglo Saxon or American [company].2

The anecdotal evidence about nationalist behavior raises several empiricalquestions. Do governments really resist the acquisition of domestic companiesby foreign companies? If so, are such reactions just political statements or dothey have real economic effects on mergers and acquisitions? For instance, doeseconomic nationalism impede capital flows and investment by deterring futureacquisition attempts by foreign firms, or do the government interventions affectthe premiums offered to target shareholders? Furthermore, what are the eco-nomic, political, and sociological factors behind nationalism in mergers? Theseare some of the questions that this paper addresses.

Our study of economic nationalism uses hand-collected data on governmentreactions to individual merger attempts in the 15 European Union (EU) coun-tries (as of 1996) from 1997 to 2006. We show that domestic governments aremore likely to support domestic acquirers and oppose foreign ones even thoughthe EU treaty does not leave them with jurisdiction to rule in merger attemptson the basis of nationality. These results are robust to controlling for target,acquirer, and bid characteristics; macroeconomic conditions; as well as targetindustry, target country, and year fixed effects. We also demonstrate that na-tionalism has not only a direct impact on the outcome of the merger for whichit is targeted, but also, and perhaps more importantly, an indirect deterrenteffect on future foreign bids for other firms in that country. In other words,nationalism affects international investment and capital flows even if they arenot the direct targets of a particular nationalist intervention.

We further show that nationalist interventions are more frequent when pref-erences for natives over foreigners in both the social and the economic domainsare stronger. We measure the importance of such preferences by the vote shareof extreme right parties, for which preferences for natives and against foreign-ers are defining issues in Europe, and by survey evidence. We also find thatnationalist reactions are stronger under weaker governments, in countriesholding the rotational presidency of the EU, and against firms in countries forwhich the people in the target country have little trust or affinity. Interest-ingly, we do not find a significant effect for unemployment, GDP growth, or theideology of the prime minister in the target country.

The study of nationalism in economics has a long history, and we follow anold tradition in using the term “economic nationalism” to refer to the preference

2 Owen (1999).

Economic Nationalism in M&As 2473

for natives over foreigners in economic activities.3 Of this earlier literature, thepaper closest to our own might be Golay (1958), who studies the impact of suchpreferences on the ownership of firms in postcolonial Southeast Asia.4 Much ofthis literature focuses on trade protectionism. Interestingly, EU countries, onwhich we focus, have some of the most liberal policies in the world with respectto the flow of goods and capital, at least among themselves. Furthermore, ourstudy focuses on some of the richest countries in the world, unlike recent workon economic nationalism that focuses on less developed countries.5

While economic nationalism is unlikely to be restricted to Europe only,6 wechose to focus on large merger attempts in the EU because the EU providesan ideal setting for a study of this kind for several reasons. First, for largemergers across national borders in the EU, the European Commission, not thenational governments, is the antitrust authority. Hence, a nationalist policy bydomestic governments cannot be disguised as procompetition policy. In fact, aswe explain later when we discuss the legal background, the member countriesof the EU rarely have de jure power to block any merger based on the acquirer’snationality; instead, they have to rely on their de facto power. Second, Europe-wide economic integration is unlikely to be complete. Indeed there still seem tobe many opportunities for cross-border mergers, especially following the recentfinancial crisis. A study of the impediments to this integration is thereforeimportant. Third, there have been a sufficient number of domestic and cross-border merger attempts within the EU to allow for statistical analysis. Finally,a large body of anecdotal evidence points to economic nationalism in the EU.

The recent crisis has only increased the importance of economic nationalism.Many firms are distressed and likely to exit their industry. Given widespreadweaknesses in a given country, a potential acquirer may be more likely to befound in other countries. Yet calls for political intervention in the economyin general and for protectionism in particular have increased in the popularpress.7 Considering the role of protectionism in deepening and spreading the

3 See, for example, Feiler (1935), Knight (1935), von Hayek (1937), von Mises ([1943] 1990), Seers(1983), Olson (1987), and Helleiner and Pickel (2005). Breton (1964, p. 377) defines nationalism as“the investment of present scarce resources for the alteration of the interethnic and internationaldistribution of ownership.” The different treatment of foreign acquiring firms from domestic onesthat this paper demonstrates is also related to the discrimination literature that starts with Becker(1957).

4 With respect to our use of the vote share of extreme right parties as a proxy for nationalistsentiments, it is also interesting to note that Knight (1935) focuses on “fascist nationalism” in hisstudy of economic theory and nationalism.

5 See, for example, Macesich (1985) and Burnell (1986).6 Dubai Port’s attempt to acquire a Florida port and the attempt by Chinese oil company CNOOC

to acquire U.S. oil company Unocal are some of the better-known examples. Both were withdrawnafter political opposition. It is interesting to note that China retaliated by not allowing Coca Colato acquire one of its bottlers in China (see, for example, Petrusic (2006) The Economist (March 5,2009), and Timmons (2006)).

7 See the discussion in Schuman (2009), and The Economist (February 5, 2009a), among others.

2474 The Journal of Finance R©

Great Depression around the world (Irwin (1998)), an analysis of economicnationalism and its impact is timely.8

Our paper is related to several recent studies that examine the role of mergerregulations in the European context. Aktas, de Bodt, and Roll (2004), Carletti,Hartmann, and Ongena (2012), and Duso, Neven, and Roller (2007) study thestock market response to regulatory decisions or legislative actions using eventstudy methodology. Our focus and methodology, however, are different. Guiso,Sapienza, and Zingales (2009) and Bottazzi, Da Rin, and Hellmann (2008)demonstrate the importance of trust in cross-border financial investmentsby using macroeconomic and venture capital investment data, respectively.Ahern, Daminelli, and Fracassi (2012) also use macroeconomic data and findthat the volume of cross-border mergers is smaller when countries are moreculturally distant. In contrast, we focus on nationalism and use microlevelmergers and acquisitions data as well as hand-collected data on actual gov-ernment reactions.9 Finally, Morse and Shive (2010) find that country-levelpatriotism is significantly related to the home bias in equity investments, andGupta and Yu (2009) show that bilateral capital flows reflect bilateral politicalrelations. Unlike these studies, our study is at the micro level.

This paper is structured as follows. Section I summarizes the institutionalbackground. Section II describes our data and sample. In Section III, we presentour main findings on economic nationalism in government reactions to mergerattempts. Section IV studies the sociological and political factors behind nation-alism. Section V examines the direct impact of nationalism on merger outcomes.In Section VI, we study the indirect impact of nationalism, namely, whetherit deters future foreign acquisition attempts in that country. Section VIIconcludes.

I. Institutional Background

Mergers above a certain size threshold with a sufficiently large representa-tion across the EU are deemed to have a “European Community Dimension,”in which case the relevant competition authority for these mergers is the EU.Exceptions as discussed below notwithstanding, member countries have to im-plement the ruling made by the European Commission on a merger case. Anyappeal can be made only at the European Court. This section first reviewsthe regulation in the EU, and then discusses how the governments of membercountries implement nationalist policies within this legal framework.

8 Note that we do not study nationalizations in which the government takes an ownership stakein firms.

9 For studies on European mergers and acquisitions but without a political economy focus,see, for example, Rossi and Volpin (2004), Faccio and Masulis (2005), Ferreira, Massa, and Matos(2007), Bris and Cabolis (2008), and Erel, Jang, and Weisbach (2012). See Erel, Liao, and Weisbach(2012) for the determinants of cross-border mergers and acquisitions around the world.

Economic Nationalism in M&As 2475

A. Regulation in the EU

For most of our sample period, the EU’s approach to mergers and acquisitionswas determined by the EU Merger Regulation of 1989, as amended in 1997.10

The European Commission, as opposed to the individual countries, had theauthority to rule on mergers if the mergers were deemed to have a communitydimension, which is defined as follows:

� The aggregate worldwide turnover of all the merging parties is more than5 billion euros.11

� The aggregate community-wide turnover of each of at least two mergingparties is more than 250 million euros.12

The main exception to these size and breadth thresholds is that, if more thantwo-thirds of the turnovers of each merging party take place in one and thesame member state, the competition authority is the government of that mem-ber country. The implication of this community dimension rule is that mergersbetween large companies from different countries within the EU typically fallwithin the jurisdiction of the European Commission, while mergers betweenlarge companies from the same country may satisfy the exception to the com-munity dimension rule. This distinction will prove to be important in allowingthe creation of “national champions” as discussed below.13

If a merger satisfies the community dimension, a member state can still take“appropriate measures” to protect the following legitimate interests:14 publicsecurity, plurality of media, prudential rules for financial companies, and otherpublic interests that are recognized by the European Commission. In otherwords, nationalism in defense and media companies is explicitly allowed, somergers involving those companies are excluded from this study. However,beyond these two industries, the EU’s Merger Regulation leaves little de jure

10 See Council Regulation (EEC) No. 4064/89 as amended by Council Regulation (EC) No.1310/97 and hereafter referred to as the EC Merger Regulation. This was replaced by Council Regu-lation (EC) No. 139/2004 but the definition of “community dimension” in Article 1 that determinedthe scope of the European Commission’s jurisdiction did not change. In general, the changesbrought by the latter regulation were minor (see Hinds (2006)).

11 For banks, “turnover” is calculated as the sum of interest income, income from securities,commission income, net profit on financial operations, and other income; for insurance companies,it is the value of gross premiums on policies written; see Article 5 of the EC Merger Regulation.

12 The 1997 amendment accepted a lower threshold of 2.5 billion euros of aggregate turnover if(1) in each of the three-member states, the aggregate turnover of the merging parties is more than100 million euros; and (2) the aggregate community-wide turnover of each merging party is morethan 100 million euros.

13 Although it is beyond the scope of this paper, notice that mergers between two companies withmain operations located outside of Europe may still satisfy the community dimension rule and,hence, require the European Commission’s approval. The case of the proposed merger betweenGeneral Electric and Honeywell, which was approved by U.S. regulators but rejected by Europeanregulators, is a good example of the implications of this rule for non-European companies (seeEvans (2002)).

14 See Article 21 of the EC Merger Regulation.

2476 The Journal of Finance R©

power to individual countries to implement their economic nationalism. So wenow turn to their de facto power in implementing such policies.

B. Common Methods of Implementing Nationalism in M&As

We define a company’s nationality as its—or its ultimate parent’s—countryof registration, which we discuss in more detail in the Data section. Belowwe review common methods used by individual countries in implementingnationalist policies in mergers in our sample. Multiple methods are typicallyused simultaneously. Appendix B provides several examples of governmentinterventions.

B.1. Prudential Rules for Financial Companies

The EC’s Merger Regulation allows domestic governments to oppose an ac-quisition of a financial company based on prudential rules even if the commu-nity dimension is satisfied. This exception allows governments to implementnationalist policies under the rubric of prudential rules. This ability, how-ever, has been relatively restricted since the Champalimaud case in 1999, inwhich the European Commission took Portugal to the European Court becausethe Portuguese government vetoed the acquisition of a Portuguese bank by aSpanish bank based on the nationality of the acquirer (Gerard (2008)). Theprudential rules exception often serves as a way for the government to gaintime while searching for a “white knight” for the domestic target instead ofvetoing an acquisition outright.

B.2. Public Interest

The EU Merger Regulation also allows domestic governments to oppose amerger in order to protect public interests, which are left undefined in theMerger Regulation. Although this might seem to be a catch-all clause thatcan be invoked at will by individual governments to block a merger, its use isactually limited in practice because any public interest must first be recognizedas such by the European Commission.

B.3. Moral Persuasion

Moral persuasion is especially common when governments try to stop amerger at the rumor stage by stating that they are against it. Although theymay have no de jure power to stop a merger, the implicit threat is that the ac-quiring company will be dealing with a hostile domestic government on manyregulatory issues if the acquisition goes through. This implicit threat is morepowerful if the government is also a major customer, as the case may be for apharmaceutical company.

Economic Nationalism in M&As 2477

B.4. Golden Shares in Privatized Companies

In many privatized companies, domestic governments still hold “goldenshares,” or the right to veto major corporate changes, such as the decisionto be acquired. This can be a major deterrent to foreign acquirers even thoughsuch rights are increasingly in a legal gray area because they are frequentlyrejected in the European Court when challenged (Adolff (2002)).

B.5. Playing for Time

Apart from the prudential rules for financial companies as mentioned above,requirements for the stock market regulator to approve any tender offer and/orapprovals necessary from various commissions (such as energy boards) to clearpotential mergers are often used by the domestic government. In this way,governments gain time to find and/or fund a friendly bidder for the target.However, politicians’ control over such regulators varies across countries andtime.

B.6. Providing Financing to Domestic Bidders

Domestic governments often support domestic bidders by providing financingto complete the acquisition. Direct aid from the government budget, however,is rarely used. Instead, public pension funds and government-owned bankslend to the acquirer or invest in the merged company. There are typicallyfewer restrictions on these financial institutions’ investment choices than therestrictions placed on individual governments by the EC Merger Regulation.Given the limited effectiveness and questionable legality of other methods,this method may be observed even more frequently in the future, especially ifgovernments start creating sovereign wealth funds that can be used to preventthe acquisition of domestic companies by foreign companies, as advocated byformer French president Nicolas Sarkozy (Hall (2008)).

B.7. Finding White Knights

This is one of the most effective methods to block an unwanted acquirer. Whileusing other methods to gain time, the government and/or target managementtry to find a friendly acquirer (white knight) or a friendly blocking minorityholder (white squire). Advantageous financing through government-controlledfinancial institutions often follows as discussed above.

B.8. Creating National Champions

This involves supporting the merger of two domestic companies in the hope ofcreating a new company that is too big to be taken over by foreign firms. Targetsize is often a good deterrent of foreign acquisitions and this preemptive moveis very common.

2478 The Journal of Finance R©

II. Data and Sample Description

Our sample contains the largest 25 merger targets by market capitalizationof target firms in each of the first 15 EU countries (as of 1996) from 1997 to 2006.These countries are Austria, Belgium, Denmark, Finland, France, Germany,Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden,and the United Kingdom. All firms in our sample are publicly listed. We definethe nationality of a company as its country of registration or, if it is majority-owned, as its parent’s country of registration.

We use Thomson Financial’s SDC Mergers and Acquisitions database for non-U.S. targets to identify merger attempts and their characteristics. We includea merger bid in our sample if the acquiring firm aims, with the proposed acqui-sition, to become the majority owner or to cross the 20% ownership thresholdto become the largest shareholder. If there are multiple bidders for the sametarget firm, we keep all of them. For Luxembourg, there are only 10 mergerattempts during this time period. All other countries have 25 observations ormore due to multiple bids, forming a sample size of 415 merger bids for 15countries. Spain has the largest number of observations at 35. These mergerbids are made by firms in the same country as the target firm as well as byforeign firms from all around the world. Our sample comprises 197 domesticbids and 218 foreign bids.

Facing an acquisition bid, the target firm’s government has three choices:support the bid, oppose the bid, or be neutral/do nothing. To identify govern-ment reactions to the merger bids, we search newspaper articles about eachmerger attempt using Factiva. We use a large set of key words to identify ar-ticles likely to be relevant and read all of them.15 Based on these newspaperarticles, especially using quotes from government representatives, we identifya government’s reaction to a merger bid as support, opposition, or neutral/no re-action. We use only quotes by prime ministers and cabinet ministers—and theirspokespersons—as well as actions taken by them. For targets in banking, wealso include central banks, which typically examine any bank merger. No othergovernment agency or politicians, including those that belong to the governingparty, are used to classify the data. Any possible disagreements among cabinetministers do not appear to be made public. If the domestic government has theanticompetition jurisdiction on a domestic merger and the cabinet follows therecommendation of the agency in charge of the anticompetition examination,the government action is not considered an intervention for our purposes. Themanual search for government actions was, by far, the most time-consumingaspect of our study.

There are both advantages and disadvantages to our approach. The maindisadvantage is that we underestimate economic nationalism in mergers and

15 The following are the key words that we use to search the body of articles in order to iden-tify relevant articles: government, minister, politic*, national assembly, parliament, central bank,nationalism, patriotism, protectionism, champion, industrial jewel, national jewel, industrial sym-bol, national symbol, icon, national security, strategic interest, strategic sector, strategic industry,public interest, national interest, municipal, state-owned, and patriotic.

Economic Nationalism in M&As 2479

Figure 1. Government support/opposition for domestic and foreign acquisition at-tempts. This figure shows the reaction (support vs. opposition) of the target country’s governmentto merger bids. The sample contains the 25 largest merger bids by market capitalization in each ofthe 15 EU countries as of 1996. These countries are Austria, Belgium, Denmark, Finland, France,Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, and theUnited Kingdom. If there are multiple bidders for the same target, all bids are included. There are415 merger attempts in total. The sample period is 1997 to 2006.

acquisitions by looking at the government reaction to actual or rumored bids.For example, if a country’s government is known to oppose foreign acquirers,potential foreign acquirers will fail to materialize in the first place and thegovernment will not need to oppose openly any foreign bids. In this case, wewill not capture a nationalist reaction by that country’s government, and thusour method is likely to underestimate nationalism in cross-sectional analysis.16

The main advantage of our approach is that it focuses on direct governmentreactions rather than surveys of nationalist sentiment or the ideology of theruling party, which may or may not be correlated with actual actions. Thismethod also allows us to exploit the timing of government reactions and studytheir subsequent deterrent effect on future merger attempts.

Simple frequency counts of government reaction provide initial evidence thatwhether the bidder is foreign or domestic is an important factor behind govern-ment reactions. Governments are more likely to support a domestic acquisitionand oppose a foreign acquisition of a domestic company. Figure 1 illustrates this

16 This is less of a problem in time-series analysis, where we study the impact of nationalism onforeign merger bids in the years that immediately followed. If a country has at least one nationalistreaction, time-series analysis can be performed and the overwhelming majority of the countries inour sample have at least one nationalist reaction in our sample period.

2480 The Journal of Finance R©

Table IGovernment Reaction to Domestic and Foreign Merger Bids

This table reports the reaction of the target country’s government to merger bids. The samplecontains the largest 25 merger targets by market capitalization in each of the 15 EU countries asof 1996. If there are competing bidders for the same target, all bids are included so a country’stotal may exceed 25. These countries are Austria, Belgium, Denmark, Finland, France, Germany,Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, and the UnitedKingdom. The sample period is 1997 to 2006. Pearson Chi-squared tests the equality of distribu-tions between domestic bids and foreign bids across government reactions.

Government Reaction

Opposition Neutral Support Total

Domestic Bids 9 154 34 197Foreign Bids 28 183 7 218Total 37 337 41 415

Note: Pearson’s Chi-squared p-value < 0.001.

difference visually and Table I provides a more detailed tabulation. AlthoughTable I indicates that governments stay neutral, or do not show any reaction,to the majority of bids, the Pearson chi-squared test provides evidence againstthe equality of distributions for government reactions by the nationality of theacquiring company at a significance level better than 1%.

There are large differences across countries in the degree of interventionism.France, Italy, and Spain, followed by Portugal, have the most interventions onmerger attempts in our sample, where Greece and the United Kingdom haveno interventions in our sample. In Section IV, we study the sociological andpolitical factors behind nationalism.

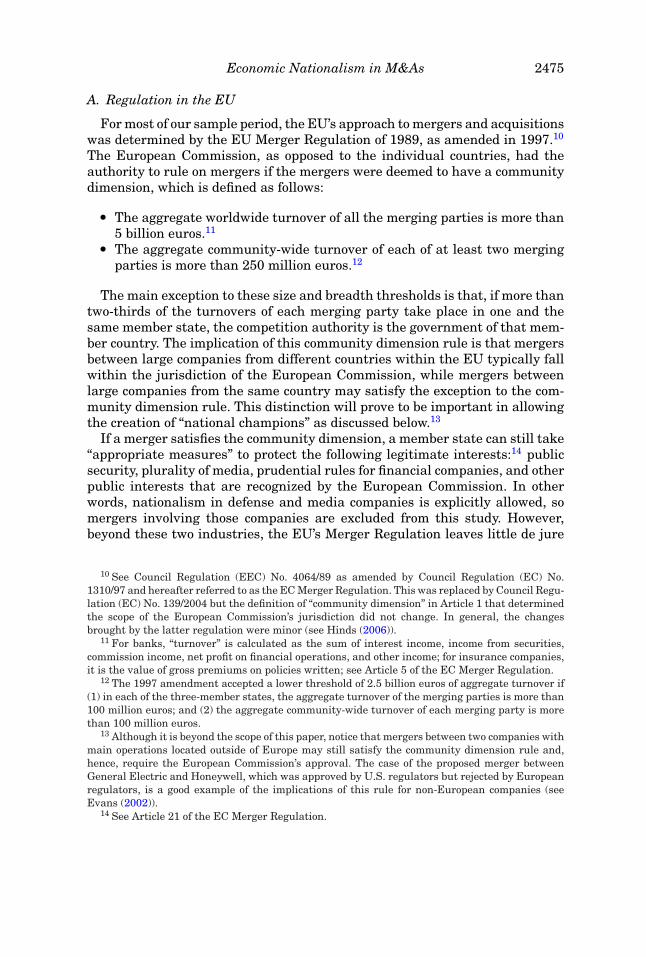

We obtain firm-level data such as market capitalization and net income fortarget firms from Datastream and Global Compustat. Table II, Panel A, reportssummary statistics on target firms and the merger bids that they receive fromdomestic and foreign acquirers. Based on a comparison of sample statistics,there is no statistically significant difference across targets based on whetherthe acquirer is foreign or domestic.

Table II, Panel B tabulates similar characteristics by the reaction of thetarget country’s government. We see more differences based on governmentreaction. Compared to the median merger bid that gets a neutral or no reactionfrom the government (1.4 billion euros), the median bid that the governmentopposes or supports is larger (6.3 and 6.6 billion euros for opposition and sup-port, respectively). Governments also tend to oppose hostile or unsolicited bidsmuch more frequently. Most importantly for our analysis, 75.7% of all mergerattempts that are resisted by the government are initiated by foreign acquirerswhile only 17.1% of the bids supported by the government are foreign bids.This difference is statistically significant at the 1% level.

For robustness checks in multivariate analysis, we also employ country-levelcontrols. GDP growth and the unemployment rate, which is reported as the per-centage of the labor force, come from the International Monetary Fund (IMF)

Economic Nationalism in M&As 2481

Table IISample Statistics for Merger Bids

The statistics describe target firms and merger bids that they receive by whether the acquireris foreign or domestic (Panel A) and by the reaction of the target country’s government (PanelB). Our sample contains the 25 largest targets in each of the first 15 EU countries (as of 1996)between 1997 and 2006. Market Cap. is the market capitalization of target firms in real euros as of4 weeks before the merger bid. Net Income/Market Cap is the ratio of the target firm’s net incomeover market capitalization as of the most recent fiscal year-end before the bid is announced.Hostile/Unsolicited Bid Dummy takes a value of one if the bid is classified as hostile and/orunsolicited, and zero otherwise. The last row in each panel reports the number of observations for allvariables except the number of observations for Net Income/Market Cap, which is in parentheses.p-values from Wilcoxon rank-sum tests for the medians and mean difference tests for the means(between opposition and support samples in Panel B) are reported. The symbols ***, **, and *indicate significance at the 1%, 5%, and 10% levels, respectively.

Panel A: Nationality of the Acquirer

Statistic Domestic Bidder Foreign Bidder p-Value All

Market Cap. (Billions euro) Median 2.91 1.69 0.40 2.49Net Income/Market Cap Median 5.8% 5.9% 0.895 5.8%Hostile/Unsolicited Bid Dummy Mean 16.8% 12.4% 0.21 14.5%

N 197 (196) 218 (217) 415 (413)

Panel B: Government Reaction

Statistic Opposition Support p-Value Neutral All

Market Cap. (Billions euro) Median 6.3 6.6 0.645 1.4 2.5Net Income/Market Cap Median 5.8% 5.6% 0.76 5.8% 5.8%Hostile/Unsolicited Bid Dummy Mean 43.2% 17.1% 0.012** 11.0% 14.5%Foreign Bidder Dummy Mean 75.7% 17.1% 0.00*** 54.3% 52.5%

N 37 41 337 (335) 415 (413)

database. The political affiliation of the ruling party comes from rulers.org, andthe election dates come from electionguide.org and other Internet sources.

III. Multivariate Analysis of Economic Nationalism in M&As

A. Specification

To study the government reactions to merger bids, we employ a discrete-choice model that estimates the likelihood of a particular government reactionto a given merger bid. When the target firm receives a merger bid, the govern-ment has three choices: oppose, support, or do nothing/stay neutral. Given thenumber of choices, a multinomial logit model allows us to estimate the effect ofbid-, firm-, and macro-level factors on the government’s reaction to the mergerbid (see McFadden (2001) and Train (2003) for an overview). A different setof coefficients is estimated for different outcomes within the same regression.These estimates are relative to the base outcome, which is taken to be do-ing nothing or staying neutral, as this outcome is the observed reaction in themajority of cases. We provide average marginal effects with heteroskedasticity-robust standard errors corrected for clustering at the target country level.

2482 The Journal of Finance R©

Table IIINationalism in Mergers and Acquisitions: Main Regressions

This table reports average marginal effect estimates for a multinomial logit model. The depen-dent variable is the government reaction, which can be opposition, support, or the base outcome,no/neutral reaction. Foreign Acquirer Dummy is equal to one if the bidder is not from the samecountry as the target firm and zero otherwise. Ln (Market Cap) is the natural logarithm of the targetfirm’s market capitalization and Net Income/Market Cap is the ratio of its net income over marketcap as of the most recent fiscal year-end before the bid is announced. Competing Bid Dummy isequal to one if there is a competing bid for the target and zero otherwise. Hostile/Unsolicited BidDummy is equal to one if the bid is classified as hostile and/or unsolicited. Far Right Vote Shareis the share of votes obtained by extreme right parties in the most recent election in the targetcountry before the bid was announced. Heteroskedasticity-robust standard errors, corrected forclustering of observations at the target country level, are in parentheses. The symbols ***, **, and* indicate significance at the 1%, 5%, and 10% levels, respectively.

Government Reaction

(1) (2) (3)

Opposition Support Opposition Support Opposition Support

Foreign Acquirer 0.151*** −0.136*** 0.113*** −0.125***

Dummy (0.039) (0.016) (0.036) (0.019)Far Right Vote Share 0.005** 0.004***

(0.002) (0.001)Foreign Acquirer 0.006* −0.008***

Dummy * Far RightVote Share

(0.003) (0.002)

Ln(Market Cap) 0.019*** 0.032*** 0.016** 0.039*** 0.017*** 0.024***

(0.006) (0.011) (0.006) (0.011) (0.005) (0.008)Net Income/Market 0.136 0.012 0.134 0.008 0.146 0.037

Cap (0.160) (0.271) (0.131) (0.255) (0.123) (0.239)Competing Bid 0.065* 0.073** 0.080** 0.065* 0.040 0.061*

Dummy (0.039) (0.032) (0.036) (0.039) (0.036) (0.033)Hostile/Unsolicited 0.083** −0.005 0.094*** −0.013 0.104*** −0.014

Bid Dummy (0.039) (0.024) (0.026) (0.039) (0.034) (0.029)Year FEs Yes Yes Yes Yes Yes YesTarget Country FEs Yes Yes Yes Yes No NoTarget Industry FEs Yes Yes Yes Yes Yes Yes

413 413 4110.339 0.417 0.295

B. Results

Table III provides estimates of our main multinomial logit model. The es-timates are for two possible outcomes, namely, government opposition andgovernment support, and are relative to the base case of no reaction/stayingneutral. The first model serves as a benchmark and includes characteristics atthe bid and target firm levels but excludes the Foreign Acquirer Dummy, ourmain variable of interest.

The benchmark regression shows a statistically significant size effect: a 10%increase in target size increases the probability of opposition by 0.19 percentage

Economic Nationalism in M&As 2483

points and that of support by 0.32 percentage points on average, compared toa 10% unconditional probability for either outcome. This effect is significant atthe 1% level for both outcomes. European governments are also more likely tooppose a bid by 8.3 percentage points on average if it is hostile or unsolicited.

The second regression adds Foreign Acquirer Dummy, our main variableof interest, to the explanatory variables. This variable has a large averagemarginal effect that is significant at the 1% level for both types of intervention.European governments are 15.1 percentage points more likely to oppose and13.6 percentage points less likely to support a foreign acquirer, on average.This is a very strong preference for domestic owners and against foreign ownersgiven that the unconditional probability is about 10% for both outcomes andonly about half of the sample acquirers are foreign companies.

As mentioned in the introduction, we follow an old tradition in economicsand use the term nationalism to denote the preference for natives againstforeigners. A natural question to ask is whether the nationalism we find aboveis stronger when such nationalist sentiment is strong. However, it is not trivialto measure such sentiment or to find a proxy for it. We consult the recentpolitical science literature that studies the rise of extreme right parties inEurope in the 1990s and thereafter. Three main findings of this literature areimportant for our analysis.17

First, a common theme of these European parties is their advocacy andpreferences for natives over foreigners and immigrants. For example, Mudde(1996) finds that, among the 26 different academic studies surveyed, the fol-lowing five features are mentioned by at least half of the studies: nationalism,racism, xenophobia, antidemocracy, and strong state.

Second, despite the free market origins of some of these extreme right parties,by the 1990s most of them adopted economic policies that are protectionistand economic nationalist, and against globalization (see, for example, Betzand Swank (2003), Mudde (2007, pp. 119–137, 184–197), Zaslove (2008), andHainsworth (2008, pp. 85–89)).

Third, although extreme right parties rarely came to power on their own,their impact on European politics has been large as they have forced other par-ties to move to the right and they have dominated the discussion on foreigners(see, for example, Bale (2003), Schain (2006), Hainsworth (2008, pp. 111–121)).

Following the findings of this literature, we use the vote share of extremeright parties as identified by Golder (2003) and updated by Wendt (2009) as aproxy for the strength of nationalist sentiment.18 We test for whether the im-pact of foreign ownership of the acquirer on the government decision increasesas the vote share of extreme right parties also increases. We are not aware ofany other empirical study that uses this proxy but we are certainly not the first

17 See, for example, Hagtvet (1994), van Der Brug, Fennema, and Tillie (2000), Golder (2003),Givens (2005, esp. pp 68–86), Bjørklund (2007), Wendt (2009), and the references cited below.In this voluminous literature, Hainsworth (2008) provides a concise book-length treatment andfurther references.

18 We thank Christopher Wendt for sharing these data.

2484 The Journal of Finance R©

in economics to link extreme right ideology to economic nationalism (see, forexample, Knight (1935)).

This test is essentially a test for the interaction effect between the ForeignAcquirer Dummy and Far Right Vote Share. In a usual linear estimation, thiswould be straightforward—the coefficient on the interaction term would imme-diately give the interaction effect. However, in a nonlinear estimation such asthe multinomial logit model here, Ai and Norton (2003) show that the calcula-tion of the interaction effect is more complicated, and that it typically dependsalso on coefficients other than that on the interaction term as well as on the val-ues that the independent variables take. In Appendix A, we provide details onhow the average marginal effects are derived and calculated for the interactioneffects in the multinomial logit estimation.

The third regression reported in Table III is the same as the second regressionexcept that Far Right Vote Share and its interaction with Foreign AcquirerDummy are included. Country fixed effects, on the other hand, are omittedas the vote share of extreme right parties changes only in election years. Theresults show that European governments are more likely to intervene, bothin support of or opposition to a merger, where and when the extreme rightparties are strong; this effect is statistically significant at the 5% level. Theaverage marginal effect of foreign acquirer is somewhat smaller than, thoughstill comparable to, the values reported above and significant at the same 1%level.

Our main interest, the interaction effect, is also economically significant. Aone percentage point increase in the extreme right vote share increases theprobability that the domestic government opposes a foreign acquirer by 0.6percentage points, on average; this effect is significant at the 10% level. Toput this effect in perspective, the vote share of extreme right parties is in lowsingle digits where and when they are weak but increases to low double dig-its when they are strong. Hence, a 10 percentage point increase in the voteshare increases the probability of opposition to a foreign acquirer by 6 percent-age points, which is more than half the unconditional probability. Similarly,a 10 percentage point increase in the extreme right vote share decreases theprobability of support for a foreign acquirer by 8 percentage points, which isclose to the unconditional probability. This effect is significant at the 1% level.

To summarize, the nationalist preference of governments for domestic ownersover foreign owners is stronger when the nationalist sentiment of voters is alsostrong. The next subsection provides robustness tests of our main result andthis interaction effect.

C. Robustness

C.1. Macroeconomics

Macroeconomic factors may also affect government decisions. In particular,the effect of the extreme right vote share documented above may simply bea reflection of macroeconomic factors, especially unemployment, rather than

Economic Nationalism in M&As 2485

the role of nationalist sentiment in that country.19 In Table IV, Panel A, werepeat the third regression in Table III by substituting the extreme right voteshare first with the GDP growth rate, and then with the unemployment rate.Neither of these terms has a statistically significant effect either alone or in-teracted with the foreign acquirer dummy. Hence, the extreme right vote shareis not capturing any effect of macroeconomic factors, especially of unemploy-ment. Furthermore, the foreign ownership of the acquirer continues to have aneconomically and statistically significant effect.

C.2. Acquirer and Bid Characteristics

We check the robustness of our results to controlling for acquirer size andprofitability, using, respectively, the natural logarithm of the acquirer’s mar-ket capitalization and its net income over market capitalization. These datacome from Datastream as of the most recent fiscal year-end before the bid isannounced. Unfortunately, we only have data on acquirer size for 255 bids, orabout two-thirds of the sample. The results are reported in the first regressionof Table IV, Panel B. Neither acquirer size nor profitability has a statisticallysignificant effect, but the foreign ownership of the acquirer continues to havea statistically and economically significant effect.

We check the robustness of our results to whether the bid consists only of cashor includes the stock of the acquiring company (second regression of Table IV,Panel B). We have data for only 342 bids for this robustness check. We findthat governments are more likely to support a bid that includes the acquiringcompany’s stock. Our main variable of interest, the foreign ownership of theacquirer, remains statistically and economically significant.

C.3. Other Robustness Checks

We also perform additional robustness checks and present them in detailin the Internet Appendix.20 Our mergers and acquisitions data include somemerger rumors but the selection of rumors, unlike formal merger bids, mayincorporate subjective criteria by the data provider, and, in particular, maychange across countries and over time. Hence, we repeat our main regressionafter excluding rumors from the sample. This amounts to excluding 23 datapoints, or about 5% of the full sample from the analysis. We find that theeconomic nationalism found above remains robust to the exclusion of theseacquisition rumors.

In some companies, the domestic government owns golden shares, the rightto veto a major decision, including mergers. We search Factiva to identify the

19 Unlike the antiforeign preferences of these parties, the role of unemployment in the strengthof these parties is mixed in the political science literature. Arzheimer and Carter (2006) finda positive correlation while Bjørklund (2007) finds a negative one. Golder (2003) documents apositive correlation only when the immigrant population in that country is also high.

20 The Internet Appendix may be found in the online version of this article.

2486 The Journal of Finance R©

Table IVNationalism in Mergers and Acquisitions: Robustness

This table reports average marginal effect estimates for a multinomial logit model. Panel A includetests for robustness to macroeconomic factors. Panel B includes tests for robustness to acquirer andbid characteristics. The dependent variable is the government’s reaction, which can be opposition,support, or the base outcome, no/neutral reaction. Foreign Acquirer Dummy is equal to one ifthe bidder is not from the same country as the target firm and zero otherwise. Macroeconomiccontrols are the target country’s GDP Growth and Unemployment Rate as a percentage of totallabor force (both as of the previous year-end). Other control variables included but not reportedare Ln(Market Cap, Net Income/Market Cap, Competing Bid Dummy, Hostile/Unsolicited BidDummy, Year FEs, and Target Industry FEs (both in Panels A and B) and Target Nation FEs (onlyin Panel B). Heteroskedasticity-robust standard errors, corrected for clustering of observations atthe target country level, are in parentheses. The symbols ***, **, and * indicate significance at the1%, 5%, and 10% levels, respectively.

Panel A: Robustness to Macroeconomic Factors

Government Reaction

(1) (2)

Opposition Support Opposition Support

Foreign Acquirer Dummy 0.109*** −0.126*** 0.117*** −0.127***

(0.040) (0.036) (0.035) (0.039)GDP Growth Rate −0.017 0.009

(0.017) (0.008)Foreign Acquirer * GDP Growth −0.027 0.005

(0.023) (0.024)Unemployment Rate 0.007 −0.000

(0.007) (0.005)Foreign Acquirer * Unemployment −0.004 0.003

(0.012) (0.009)Observations 413 413Pseudo-R2 0.260 0.267

Panel B: Robustness to Some Acquirer and Bid Characteristics

Government Reaction

(1) (2)

Oppose Support Oppose Support

Foreign Acquirer Dummy 0.173*** −0.185*** 0.149*** −0.136***

(0.040) (0.040) (0.040) (0.032)Ln(Acquirer Market Cap) −0.005 −0.009

(0.012) (0.014)Acq. Net Income/Mrkt Cap 0.088 −0.349

(0.171) (0.510)Stock/Hybrid Payment 0.036 0.101***

(0.031) (0.016)Observations 255 342Pseudo-R2 0.468 0.477

Economic Nationalism in M&As 2487

target companies in which the domestic government has golden shares andexclude the bids to those target companies, about 5% of our sample, from ouranalysis. Our results are robust to the exclusion of those targets.

IV. Factors behind Economic Nationalism in Mergers andAcquisitions

In this section, we study the factors that strengthen or mitigate nationalistreactions in mergers and acquisitions. We study both sociological and politicalfactors. While the former change only slowly, the latter tend to vary from oneelectoral cycle to the next. We find that both types of factors play a role ingovernment reactions.

A. Sociological Factors

As another measure of the attitude of people in target countries towardforeigners, we use the answers to a question in Eurobarometer survey #47 ad-ministered in the EU in 1997 about the foreigners living in the respondent’scountry. The question asks respondents to choose the statement with whichthey agree. We use the proportion of respondents who agreed with the state-ment “there are too many foreigners [in my country]” as a measure of the targetcountry’s attitude toward foreigners.21 The first regression in Table V, PanelA provides the results. We find that governments are more likely to opposea foreign acquirer in target countries where more people think there are toomany foreigners.

Guiso, Sapienza, and Zingales (2009) and Bottazzi, Da Rin, and Hellmann(2008) find that trust is an important factor behind international investment,so we also check whether government reactions are different if people in thetarget country trust people in the acquirer’s country to a greater extent. Inregression (2) of Table V, we include a measure of the trust that target countrycitizens feel for others, including people in their own country, as well as theinteraction between this variable and Foreign Acquirer Dummy.22 We findthat trust plays a role in government reactions to mergers and acquisitions.Government opposition is weaker if the foreign acquirer is from a country forwhich the people in the target country have a higher level of trust. Similarly,government support for acquirers from those countries is more likely.

21 The use of such a survey question as a measure of attitude is not without problems, however.In addition to the usual concern that people may not behave as they say, the survey we use wasonly administered to young Europeans between 15 and 24 years old. Hence, its results may not berepresentative of the population at large. However, this is the best survey question that we couldfind that covered our sample period.

22 We use the median trust value based on the 1996 survey; see Guiso, Sapienza, and Zingales(2009) for details about the construction of this variable. We thank Luigi Guiso, Paola Sapienza,and Luigi Zingales for sharing their data, which include some non-European acquirers such asJapan and the United States. Note that participants were asked to report trust scores for peoplein their own country as well. Also note that 86.5% of the acquirers in our sample are from Europe(including the domestic acquirers).

2488 The Journal of Finance R©

Tab

leV

Soc

iolo

gica

lF

acto

rsb

ehin

dN

atio

nal

ism

Th

ista

ble

repo

rts

aver

age

mar

gin

alef

fect

esti

mat

esfo

ra

mu

ltin

omia

llog

itm

odel

.Th

ede

pen

den

tva

riab

leis

the

gove

rnm

ent’s

reac

tion

,wh

ich

can

beop

posi

tion

,su

ppor

t,or

the

base

outc

ome,

no/

neu

tral

reac

tion

.For

eign

Acq

uir

erD

um

my

iseq

ual

toon

eif

the

bidd

eris

not

from

the

sam

eco

un

try

asth

eta

rget

firm

and

zero

oth

erw

ise.

Inea

chre

gres

sion

,For

eign

Acq

uir

erD

um

my

isin

tera

cted

wit

hon

eof

the

soci

olog

ical

fact

ors.

Too

Man

yF

orei

gner

sis

the

leve

lofp

erce

nt

ofpe

ople

wh

oag

ree

wit

hth

est

atem

ent

“Th

ere

are

Too

Man

yF

orei

gner

sin

my

cou

ntr

y”in

a19

97E

uro

baro

met

ersu

rvey

;Tru

stis

the

med

ian

tru

stfe

ltby

the

peop

leof

the

targ

etco

un

try

for

the

acqu

irin

gfi

rm’s

cou

ntr

yfo

llow

ing

Gu

iso,

Sap

ien

za,a

nd

Zin

gale

s(2

009)

;an

dL

n(L

agge

dE

uro

visi

onVo

tes)

isth

en

atu

rall

ogar

ith

mof

the

vote

sth

eac

quir

ing

firm

’sco

un

try

rece

ived

from

the

targ

etco

un

try

inth

eE

uro

visi

onso

ng

con

test

inth

epr

evio

us

year

.Sam

eL

angu

age

(Rel

igio

n)

Du

mm

yeq

ual

son

eif

the

peop

lein

the

targ

etan

dac

quir

erco

un

trie

ssp

eak

the

sam

ela

ngu

age

(sh

are

the

sam

ere

ligi

on)u

sin

gda

tafr

omS

tulz

and

Wil

liam

son

(200

3).C

omm

onB

ord

erD

um

my

take

sa

valu

eof

one

ifth

eta

rget

and

the

acqu

irer

cou

ntr

ies

shar

ea

lan

dbo

rder

orar

ese

para

ted

by24

mil

esof

wat

eror

less

(htt

p://w

ww

.cor

rela

teso

fwar

.org

/CO

W2%

20D

ata/

Dir

ectC

onti

guit

y/D

CV

3des

c.h

tm).

Het

eros

keda

stic

ity-

robu

stst

anda

rder

rors

,cor

rect

edfo

rcl

ust

erin

gof

obse

rvat

ion

sat

the

targ

etco

un

try

leve

l,ar

ein

pare

nth

eses

.Th

esy

mbo

ls**

*,**

,an

d*

indi

cate

sign

ifica

nce

atth

e1%

,5%

,an

d10

%le

vels

,res

pect

ivel

y.

Too

Man

yF

orei

gner

sTr

ust

Ln

(Lag

ged

Eu

rovi

sion

Vote

s)

Gov

ern

men

tR

eact

ion

(1)

(2)

(3)

Soc

iolo

gica

lF

acto

r:O

ppos

itio

nS

upp

ort

Opp

osit

ion

Su

ppor

tO

ppos

itio

nS

upp

ort

For

eign

Acq

uir

erD

um

my

0.11

0***

−0.1

39**

*0.

136**

*−0

.135

***

0.07

2*−0

.100

***

(0.0

36)

(0.0

37)

(0.0

17)

(0.0

42)

(0.0

42)

(0.0

33)

For

eign

Acq

.Du

mm

y*S

ocio

logi

calF

acto

r0.

007**

*−0

.002

−0.1

43**

*0.

201*

−0.0

52**

*0.

020

0.00

30.

003

(0.0

42)

(0.1

05)

(0.0

19)

(0.0

35)

Soc

iolo

gica

lFac

tor

0.00

30.

001

0.02

0−0

.036

(0.0

02)

(0.0

02)

(0.0

51)

(0.0

50)

Targ

et-

and

Bid

-Lev

elC

ontr

ols

Yes

Yes

Yes

Year

FE

sYe

sYe

sYe

sTa

rget

Nat

ion

FE

sN

oYe

sYe

sIn

dust

ryF

Es

Yes

Yes

Yes

Obs

erva

tion

s39

439

530

4P

seu

do-R

20.

266

0.45

80.

476 (C

onti

nu

ed)

Economic Nationalism in M&As 2489

Tab

leV

—C

onti

nu

ed

Sam

eL

angu

age

Sam

eR

elig

ion

Com

mon

Bor

der

Du

mm

yD

um

my

Du

mm

y

Gov

ern

men

tR

eact

ion

(1)

(2)

(3)

Soc

iolo

gica

lF

acto

r:O

ppos

itio

nS

upp

ort

Opp

osit

ion

Su

ppor

tO

ppos

itio

nS

upp

ort

For

eign

Acq

uir

erD

um

my

0.15

2***

−0.1

33**

*0.

157**

*−0

.132

***

0.14

8***

−0.1

26**

*

(0.0

45)

(0.0

20)

(0.0

34)

(0.0

14)

(0.0

35)

(0.0

18)

For

eign

Acq

.Du

mm

y*S

ocio

logi

calF

acto

r0.

017

−0.0

030.

076

−0.0

050.

021

0.04

3(0

.070

)(0

.030

)(0

.071

)(0

.021

)(0

.059

)(0

.027

)Ta

rget

-an

dB

id-L

evel

Con

trol

sYe

sYe

sYe

sYe

arF

Es

Yes

Yes

Yes

Targ

etN

atio

nF

Es

Yes

Yes

Yes

Indu

stry

FE

sYe

sYe

sYe

sO

bser

vati

ons

413

413

413

Pse

udo

-R2

0.41

70.

421

0.42

3

2490 The Journal of Finance R©

Following Bottazzi, Da Rin, and Hellmann (2008), we also use the pointsgiven by the target country in the Eurovision song contest as an alternativemeasure of the target country’s affinity for the acquirer’s country. We constructa time series of Eurovision votes covering our sample period for the mergerbids where both the target and the acquirer are from Europe. The variableLn (1 + Lagged Eurovision Votes) is the natural logarithm of the votes thatthe acquiring firm’s country received from the target country in the Eurovisionsong contest in the previous year.23 We report these results in Table V, PanelA. We find that government opposition is weaker if people in the target countryhave greater affinity for the acquirer’s country. We also check whether sharinga common border, language, or religion play a role. In Table V, Panel B, we donot find any evidence that these factors affect government reactions to mergersand acquisitions.

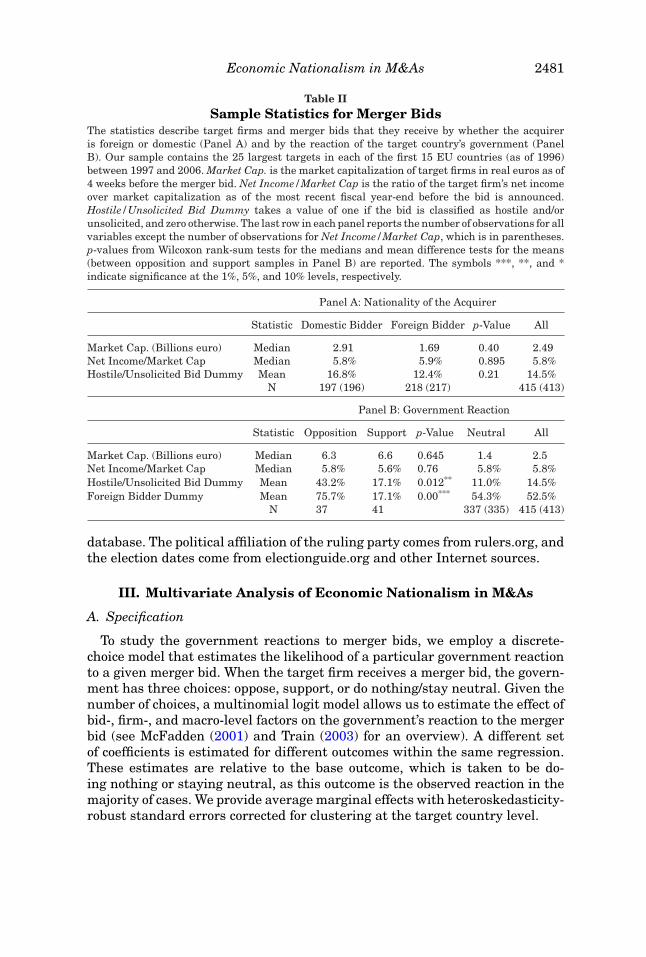

B. Political Factors

We study the role of both domestic and EU politics. The results are reportedin Table VI. We start with the ideology of the prime minister’s party in thetarget country on the announcement date. We use the ideological classificationby Volkens et al. (2010) using party programs. The variable Right Leaningness(the “rile” measure in their data set) is a continuous measure where higherlevels indicate more rightist positions. Leftist parties tend to have negativelevels of this measure. An overwhelming majority of ruling parties has a center-right or center-left ideology. We interact Right Leaningness with the ForeignAcquirer Dummy. The interaction terms do not have significant coefficients.24

Interest groups may be able to influence weak governments more easily, sowe also study whether weak governments are more likely to have nationalistreactions. Coalition governments tend to include smaller parties and may bemore easily captured by interest group politics. We interact the Foreign Ac-quirer Dummy with the binary variable Coalition Government, which takesthe value of one if the target country is ruled by a coalition government onthe announcement date. We find that the coefficient on the interaction termhas the same sign as the Foreign Acquirer Dummy and is statistically signifi-cant for government support. This result indicates that coalition governments,which tend to be weaker than single-party governments, are more likely to takenationalist actions.

We further check this result by interacting the Foreign Acquirer Dummywith Government Vote Share, which is the total vote share obtained by partiesforming the government in the most recent election before the announcement

23 The data source is http://www.eurovisioncovers.co.uk/. A given country can cast 1–8, 10, or12 votes. One complicating econometric issue in using the points given in the Eurovision contestis that countries cannot vote for themselves. We assumed they all give themselves the maximumpoints to keep the domestic mergers in the sample and included Ln(Lagged Eurovision Votes) onlyas an interaction term.

24 We repeated the analysis with a binary variable for a leftist Prime Minister. We did not findstatistically significant effect.

Economic Nationalism in M&As 2491

Tab

leV

IP

olit

ical

Fac

tors

beh

ind

Nat

ion

alis

mT

his

tabl

ere

port

sav

erag

em

argi

nal

effe

ctes

tim

ates

for

am

ult

inom

ial

logi

tm

odel

.Th

ede

pen

den

tva

riab

leis

the

gove

rnm

ent’s

reac

tion

,wh

ich

can

beop

posi

tion

,su

ppor

t,or

the

base

outc

ome,

no/

neu

tral

reac

tion

.For

eign

Acq

uir

erD

um

my

iseq

ual

toon

eif

the

bidd

eris

not

from

the

sam

eco

un

try

asth

eta

rget

firm

and

zero

oth

erw

ise.

Inea

chre

gres

sion

,For

eign

Acq

uir

erD

um

my

isin

tera

cted

wit

hon

eof

the

poli

tica

lfa

ctor

s.R

igh

tL

ean

ingn

ess

isth

eid

eolo

gyof

the

prim

em

inis

ter’

spa

rty

acco

rdin

gto

Vol

ken

set

al.

(201

0);

Coa

liti

onG

over

nm

ent

isa

bin

ary

vari

able

that

ison

eif

the

ruli

ng

gove

rnm

ent

isa

mu

ltip

arty

coal

itio

n;

Gov

ern

men

tVo

teS

har

eis

the

tota

lvo

tesh

are

ofth

ego

vern

ing

part

ies

inth

em

ost

rece

nt

parl

iam

enta

ryel

ecti

ons;

EU

Rot

atio

nal

Pre

sid

ency

isa

bin

ary

vari

able

that

ison

eif

the

targ

etco

un

try

hol

dsth

e6-

mon

thro

tati

onal

pres

iden

cyof

the

EU

wh

enth

ebi

dis

ann

oun

ced;

the

Eu

rope

anC

omm

issi

onP

resi

den

cyis

abi

nar

yva

riab

leth

atis

one

ifth

epr

esid

ent

ofth

eE

uro

pean

Com

mis

sion

isa

nat

ion

alof

the

targ

etco

un

try

atth

eti

me

the

bid

isan

nou

nce

d.H

eter

oske

dast

icit

y-ro

bust

stan

dard

erro

rs,c

orre

cted

for

clu

ster

ing

ofob

serv

atio

ns

atth

eta

rget

cou

ntr

yle

vel,

are

inpa

ren

thes

es.T

he

sym

bols

***,

**,a

nd

*in

dica

tesi

gnifi

can

ceat

the

1%,5

%,a

nd

10%

leve

ls,r

espe

ctiv

ely.

Pan

elA

.Dom

esti

cP

olit

ics

Rig

ht

Lea

nin

gnes

sC

oali

tion

Gov

ern

men

tG

over

nm

ent

Vote

Sh

are

Gov

ern

men

tR

eact

ion

(1)

(2)

(3)

Pol

itic

alF

acto

r:O

ppos

itio

nS

upp

ort

Opp

osit

ion

Su

ppor

tO

ppos

itio

nS

upp

ort

For

eign

Acq

uir

erD

um

my

0.14

4***

−0.1

31**

*0.

143**

*−0

.136

***

0.14

3***

−0.1

33**

*

(0.0

33)

(0.0

14)

(0.0

33)

(0.0

18)

(0.0

34)

(0.0

13)

For

eign

Acq

.Du

mm

y*

Pol

itic

alF

acto

r−0

.002

0.00

00.

054

−0.1

34**

*−0

.002

0.00

9***

(0.0

02)

(0.0

01)

(0.0

38)

0.02

9(0

.005

)(0

.003

)P

olit

ical

Fac

tor

0.00

30.

001

−0.4

81**

*0.

079**

*0.

002

−0.0

08**

(0.0

02)

(0.0

02)

(0.0

08)

(0.0

18)

(0.0

03)

(0.0

03)

Targ

et-

and

Bid

-Lev

elC

ontr

ols

Yes

Yes

Yes

Year

FE

sYe

sYe

sYe

sTa

rget

Nat

ion

FE

sYe

sYe

sYe

sIn

dust

ryF

Es

Yes

Yes

Yes

Obs

erva

tion

s41

341

341

3P

seu

do-R

20.

420

0.42

00.

429 (C

onti

nu

ed)

2492 The Journal of Finance R©

Tab

leV

I—C

onti

nu

ed

Pan

elB

.Eu

rope

anU

nio

nP

olit

ics

EU

Rot

atio

nal

Pre

sid

ency

Eu

rope

anC

omm

issi

onP

resi

den

cy

Gov

ern

men

tR

eact

ion

(1)

(2)

Pol

itic

alF

acto

r:O

ppos

itio

nS

upp

ort

Opp

osit

ion

Su

ppor

t

For

eign

Acq

uir

erD

um

my

0.14

5***

−0.1

32**

*0.

137**

*−0

.134

***

(0.0

34)

(0.0

15)

(0.0

30)

(0.0

15)

For

eign

Acq

.Du

mm

y*

Pol

itic

alF

acto

r0.

176**

−0.1

87−0

.053

0.08

8***

(0.0

86)

(0.1

18)

(0.1

25)

(0.0

21)

Pol

itic

alF

acto

r0.

051

0.06

3−0

.068

−0.0

78**

*

(0.0

48)

(0.0

55)

(0.0

47)

(0.0

12)

Targ

et-

and

Bid

-Lev

elC

ontr

ols

Yes

Yes

Year

FE

sYe

sYe

sTa

rget

Nat

ion

FE

sYe

sYe

sIn

dust

ryF

Es

Yes

Yes

Obs

erva

tion

s41

341

3P

seu

do-R

20.

423

0.43

7

Economic Nationalism in M&As 2493

date in the target country. We find that the coefficient on the interaction termhas the opposite sign as the Foreign Acquirer Dummy and is statistically sig-nificant for government support. This confirms that strong governments areless likely to act nationalistically. This result is similar to that in Dinc andGupta (2011), who find that governments are more likely to undertake priva-tizations where they are stronger. These results also indicate that nationalistinterventions are unlikely to be taken by governments following an industrialpolicy with a long horizon.

We also study the role of EU politics. Every EU country assumes the EUpresidency for 6 months on a rotating schedule. Target countries may act lessnationalist during their presidency as they lead the EU, or the power of pres-idency may induce them to become bolder during that time. To test whicheffect dominates, we interact the Foreign Acquirer Dummy with EU RotationalPresidency, which takes the value of one if the target country has the rota-tional presidency on the announcement date. We find that the coefficient onthe interaction term has the same sign as the Foreign Acquirer Dummy andis statistically significant for government opposition. This suggests that targetcountries act more nationalist when they hold the rotational EU presidency.

We also study whether the nationality of the European Commission presi-dent matters. The European Commission is the executive branch of the EU andits president is regarded as the most powerful EU official. The president of theEuropean Commission is nominated by the European Council, which containsthe head of government of every EU member, and is approved by the EuropeanParliament for 5-year terms. As with the EU presidency, target countries mayact more or less nationalistically if the European Commission president is fromtheir country. To test for this effect, we interact the Foreign Acquirer Dummywith EU Commission Presidency, which takes the value of one if the EuropeanCommission president is from the target country on the announcement date.We find that the coefficient on the interaction term has the opposite sign as theForeign Acquirer Dummy and the coefficient on the government opposition isstatistically significant. This suggests that target countries become more reluc-tant to act nationalistically when one of their nationals holds the presidencyof the European Commission. In an earlier version, we also studied the role ofelections following Brown and Dinc (2005) and Dinc (2005) but did not find anystatistically significant effect.

V. Direct Impact of Nationalism

The next important question to address is whether nationalism has anyeconomic impact. After all, government opposition or support may simply be amanifestation of political posturing with little real economic influence. In thissection, we study the direct impact of government intervention. More precisely,we examine whether a merger bid is more (less) likely to succeed when thegovernment supports (opposes) it. We then analyze the effect of governmentopposition on the premiums offered or received, taking the endogeneity of themerger premium into account.

2494 The Journal of Finance R©

Table VIIImpact of Nationalism on Merger Outcomes: Univariate Analysis

This table reports the reaction (opposition, neutral/no reaction, and support) of the target country’sgovernment and the success/failure of the merger bids. The sample contains the 25 largest mergertargets by market capitalization in each of the 15 EU countries as of 1996. If there are multiplebidders for the same target, all bids are included so a country’s total may exceed 25. The sampleperiod is 1997 to 2006. Pearson Chi-squared tests the equality of distributions between failed bidsand successful bids across the government reactions.

Government Reaction

Opposition Neutral Support Total

Failed Bids 26 120 11 157Successful Bids 11 217 30 258Total 37 337 41 415

Pearson’s Chi-squared p-value < 0.001.

A. Direct Impact of Nationalism on Merger Outcome

We first perform a univariate comparison of the success/failure of the mergerattempts that receive different government reactions. Table VII shows that,of 37 merger bids that the government resists, 26 (70%) eventually fail. Of 41merger bids that the government supports, only 11 (27%) fail. The difference ofdistributions is significant at the 1% level as indicated by Pearson’s chi-squaredtest. This univariate analysis suggests that government interventions have adirect economic impact. Of course, government interventions may simply be aproxy for foreign acquirers. If cross-border merger attempts, once announced,are inherently more difficult to complete, then these univariate statistics mayjust reflect that difficulty. We therefore turn to the regression analysis next.

We employ a binary choice framework—a logistic regression—where the de-pendent variable is equal to one if the merger takes place and zero if the mergerfails. Table VIII reports the results. The first model is the base model withthe Foreign Acquirer Dummy as well as controls at the bid and firm levels.The model also includes the target industry and target country fixed effects.The regression analysis indicates that acquisition attempts that target largercompanies, that attract multiple bids, and that are hostile are less likely to besuccessful. The coefficient on the Foreign Acquirer Dummy is negative but notstatistically significant. This suggests that bidders seem to internalize possibledifficulties in completing a cross-border merger when they attempt the merger.

The second regression adds Government Opposition and Government Sup-port, two dummy variables that identify government reactions. (Recall thatthe government does not react, or stays neutral, in the majority of mergerattempts, so both of these dummy variables are zero for the majority of obser-vations.) The coefficient on Government Opposition is negative and significantat the 10% level whereas the coefficient on the Government Support is positiveand significant at the 5% level. Notice that the Foreign Acquirer dummy is

Economic Nationalism in M&As 2495

Table VIIIImpact of Nationalism on Merger Outcomes