Economic Impact Assessment - Berths 203 to 205 Expansion … … · ECONOMIC IMPACT ASSESSMENT FOR...

41

Economic Impact Assessment For the proposed deepening of berths 203, 204 and 205 of the Durban Container Terminal (DCT). Developed for Transnet Ports Authority by Urban-Econ (PTY) Ltd Year: 2012

Transcript of Economic Impact Assessment - Berths 203 to 205 Expansion … … · ECONOMIC IMPACT ASSESSMENT FOR...

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

1

Economic

Impact

Assessment For the proposed deepening

of berths 203, 204 and 205

of the Durban Container

Terminal (DCT).

Developed for Transnet Ports Authority

by Urban-Econ (PTY) Ltd

Year: 2012

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

2

Table of Contents Table of Acronyms and Definitions ............................................................................................... 3

Executive Summary ...................................................................................................................... 4

Section 1: Introduction ................................................................................................................. 7

1.1 Description of the Expansion ........................................................................................................ 7

1.2 Motivation for the Expansion ....................................................................................................... 8

1.3 Methodology ................................................................................................................................. 9

1.4 Structure of the Report ............................................................................................................... 10

Section 2: Current Trade and Container Shipping Trends ............................................................. 11

2.1 National Production and Trade Trends ....................................................................................... 11

2.2 Durban Port Container Trends .................................................................................................... 12

2.3 Berths 203-205 Container Trends ............................................................................................... 14

2.4 Global Containership Trends ....................................................................................................... 15

Section 3: Economic Impacts ...................................................................................................... 19

3.1 Input-Output Economic Model ................................................................................................... 19

3.2 CAPEX Impact Modelling ............................................................................................................. 19

3.3 OPEX Impact Modelling .............................................................................................................. 22

3.4 Berth Deepening Scenarios and Associated Impacts .................................................................. 25

3.5 Concluding Comments ................................................................................................................ 28

Section 4: Scoped Socio-Economic Impacts ................................................................................. 29

4.1 Subsistence Fishing (Includes Commercial and Recreational) .................................................... 29

4.2. Beach Tourism ............................................................................................................................ 31

4.3 Traffic .......................................................................................................................................... 33

Section 5: Integrated Impact Tables ............................................................................................ 35

Section 6: Conclusion ................................................................................................................. 40

6.1 Summary of Findings ................................................................................................................... 40

6.2 Recommendations ...................................................................................................................... 41

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

3

Table of Acronyms and Definitions

GVA Gross Value Added. A measure of the value of goods and services produced in

an economy. In this report GVA is calculated using factor costs. It includes

remuneration and gross operating surplus.

TEU Twenty-foot equivalent unit. One TEU represents the cargo capacity of a

standard intermodal container, 20 feet (6.1 m) long and 8 feet (2.44 m) wide.

Deepsea A shipment coming from or going to an international port

Transhipped The shipment of goods or containers to an intermediate destination, and then

from there to yet another destination.

Coastwise From one domestic coastal port to another (e.g. Cape Town to Durban)

gt Gross tonnage measures a ships overall internal volume

LOA Length Overall is the maximum length of a vessel's hull measured parallel to the

waterline.

VLCS Very large container ship is a container vessel able to carry 8000 and more TEU

CRM data Customer Relationship Management data from Transnet

SAECS trades Southern Africa Europe Container Services

TNPA Transnet National Port Authority

TPT Transnet Port Terminals

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

4

Executive Summary

1: Introduction

This report describes the Economic Impact of the proposed expansion of the Durban Container

Terminal at Durban Port. In particular, the expansion includes the deepening and widening of

berths 203 to 205 which will allow larger vessels to safely berth, thus increasing the overall

economic production gained from the terminal.

2: Current Trade and Container Shipping Trends

Productive industries (i.e. manufacturing, agriculture and mining) have shown recovery since the

2009 recession; hence exports and imports have recovered to 2008 levels and continue to show

strong growth (11%) placing increasing demand on the port. Volumes of containers handled have

increased by 7% on average annually, and also superseded 2008 levels in 2011. Evidence shows

continued growth in 2012. Berths 203-205 handle 37% of these containers and are therefore critical

to the port. It is therefore, evident that the volume of traffic at these berths is increasing.

Furthermore, regardless of demand for containers, ship sizes are increasing and will continue to do

so into the near future to a point where 3,000-6,000 TEU range ships are phased out and replaced

with medium and large sized vessels of 8,000-10,000TEUs. Currently, the terminal can only

accommodate ships up to 9,000TEUs (not fully laden) at high tide. If the expansion does not occur,

Durban Port will be unable to accommodate an increasing number of containerships and, thus,

regional competitiveness of KZN will be reduced. In the long term, this reduced competitiveness will

be significant and detrimental to trade in the province and will raise cost of exports by incurring an

additional feedering service to a port that can handle larger vessel sizes.

3: Economic Impacts

Economic impact refers to the effects on the level of economic activity in a given area as result of

some form of external intervention in the economy. The intervention can be in the form of new

investment in for example, transport facilities, social developments, housing, business development,

the establishment of a new or the expansion of existing production capacity. In this instance, it is the

expansion of the Durban Container Terminal.

3.1 CAPEX

The economic impact during the construction phase is shown for each of the three construction

options. The construction options are Caisson, Deck on Piles, and Sheet Piles (which has the highest

component of off-shore expenditure)1. For all options, only the local capital spend has been

modelled and all dredging costs have been excluded.

The temporary benefits of the construction process have been shown to include:

R3050m to R5494m in new business sales

R1083m to R1952m in Gross Value Added

R963m to R535m in income multipliers locally (KZN)

5 222 to 9 406 temporary work opportunities created through the port construction

process.

1 The share of off-shore capital spend associated with the purchase of sheetpile material and backs has been

excluded from the modelled data. Only the South African on-shore capture of spend is reflected.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

5

3.2 OPEX

The operational benefits of the expansion to year 2025 have been shown as follows:

Using the projections of TEU volumes from TNPA from 2012/13 – 2017/18 and a

medium term growth rate of 8% (post-recession growth) from 2017/18 – 2024/25, by

2025 TEU traffic projections on these berths reaches over 5 million TEU per annum. This

relates to spend of R27 088m first round and a further spend of R21 671 induced into

supporting services. Employment related to this traffic base is 21 506 persons.

3.3 Two further scenarios show:

3.3.1 The losses in benefits if the berths were only deepened but not lengthened by 170m were

shown to include:

a loss of direct spend of R16 653m, induced spend of R21 671m and port related

employment loss of 5 547 jobs and total employment loss of 13 221 jobs over the four years

of construction.

a loss of direct spend of R1 523m, induced spend of R2119m and port related employment

loss of 507 jobs and total employment loss of 1225 jobs over the operational seven years. If

the capacity for the Dig-Out Port comes on line, in accordance with the anticipated planning

horizon, by 2021 then this loss is reduced to: a loss in direct spend of R554m, a loss in

induced spend of R443m and port related employment loss of 185 jobs and total

employment loss of 446 jobs over the operational three year period between the end of

construction and the availability of initial capacity at the dig-out port.

3.3.2 The losses in benefits if the expansion does not occur at all were shown to include:

No loss of trade for the first 5 years, absolute loss of all CAPEX investment benefit.

This equates to a loss of handling capacity of 284 108 TEUS carried on vessels too large to be

berthed if the depth at berths 203 – 205 is not increased in the short term, until available

capacity at the dig-out port becomes available.

Which has a direct spend loss impact of R1961m, induced spend of R1569m, port related

employment loss of 852 jobs and total employment loss of 3530 over the period of 2016 –

2020.

4 Scoped Socio-economic Impacts

The impact on subsistence fishing, beach tourism, and traffic were flagged as part of the scoping

report and raised during public meetings by interested and affected parties.

4.1 Subsistence Fishing: There are approximately 4000 true subsistence fishers on the East Coast

of South Africa, but none of these are registered within eThekwini region according to Ezemvelo

Wildlife, who maintains the registry. Fishers in eThekwini comprise of small scale commercial and

recreational participants. This is, however, an important part of locals’ livelihoods and Durban’s

economy. Ecology studies show that there will be no long term impact on line-fish in the bay with

mitigation, and during construction there will be a displacement of 50% of the fish within the

turbidity plume only (within the bay). There will therefore be an impact on fishers within the bay

and slightly along the coast during construction; however, the exact impact is unknown. There is no

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

6

associated impact on subsistence activities per se, as these fishers do not fall into this catchment

area.

4.2 Beach tourism: The economic value of the beach to Durban is R260 million for non-resident

tourists alone. This figure would be in the billions of rand per year if a resident spend was included.

The beach is considered the most important draw-card to Durban for tourists and residents. Any

impact on the beaches would be detrimental to Durban’s economy. Specialist studies have found,

however, that there will be no impact on the beaches or the quality of the water.

4.3 Traffic: Any increase in landed containers will result in an increase in trucks on eThekwini roads.

Currently there are 3000 trucks leaving the port in a day. However, planning for this additional

volume of road freight traffic on domestic roads adjacent the port precinct is mitigated by

eThekwini’s freight plan and TNPAs projects to increase road capacity, which has taken into account

projected growth in port traffic in line with Transnet’s projections. Furthermore, the economic

impact on increased truck business and related truck servicing and production industries will be

positive.

5 Recommendations

5.1. The results of the Economic Impact Assessment show that the economic benefits for

extending and deepening the berths at Pier 2 are significant and, therefore, warrant full

development to go ahead.

5.2. The benefits are equal across the three construction types in the operational phase and the

variation between the three options during construction phase is not significant enough to

warrant a preference.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

7

Section 1: Introduction This report describes the Economic Impact of the proposed expansion of the Durban Container

Terminal at Durban Port. In particular, the expansion includes the deepening and widening of

berths 203 to 205 which will allow larger vessels to safely berth, thus increasing the overall

economic production gained from the terminal.

1.1 Description of the Expansion The map below shows the location of the relevant berths within the port.

FIGURE 1 MAP SHOWING LOCATION OF BERTHS 203 TO 205

Source: Nemai Consulting (May 2012) ‘Deepening, Lengthening and Widening of Berth 203 to 205, Pier , Container

Terminal, Port of Durban, FINAL SCOPING REPORT’

The proposed upgrade would include the following activities:

1. The westward lengthening of Berth 205 by 170m; 2. The eastward lengthening of Berth 203 by 100m; 3. The seaward widening of Berths 203 to 205 by 50m; 4. The deepening of the berth channel, approach channel and vessel turning basin from the

current -12.8m CDP to -16.5m CDP; 5. Three technical options will be considered namely, the Deck on Pile option, Sheet Pile option

and the Caisson option. For the Caisson option, a trench will need to be excavated to -19m CDP;

6. The precasting of beams; storage of sheet piles or construction of caissons (for the Deck on Pile, Sheet Pile and Caisson option respectively) would take place at Bayhead Lot 10;

7. The offshore disposal of dredge material;

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

8

8. The offshore sand winning for infill material; and 9. The installation of new Ship to Shore (STS) cranes and associated infrastructure.

1.2 Motivation for the Expansion Providing operating capacity ahead of the demand has become an essential element of managing

national logistics capability in a fast changing and competitive global economic environment.

Included in these commitments will be the necessity of providing major container capacity

enhancements along the highest demand logistics corridor in the country in the form of increasing

container handling capacity at the Port of Durban. The proposed expansion of the DCT offers this in

line with existing market provision of extensive logistics capabilities.

The Port of Durban is the gateway port in the South African ports system which plays an important

role in facilitating the import and export needs for much of South Africa. The existing Blockwork

Quay wall structure along Pier 2 Berth 203 to 205 was designed in the 1970s, to support dockside

cranes with a lifting capacity of 4 tonnes and a water depth of -12.8m Chart Datum Port (CDP). This

allowed for the safe berthing of vessels with a fully laden draft (vertical distance between the

waterline and the bottom of the hull) not greater than -11.8m CDP. At present the existing quay wall

structure is operated beyond its original design parameters. Recent studies have concluded that the

existing quay walls do not meet the minimum Eurocode 7 Safety Standards and that there is a risk of

potential quay wall failure2.

Current trends show the number of containers handled at the port increasing by 7% on average each

year over the previous decade (albeit with a recession in growth over 2008/9)3. In addition, vessel

sizes have increased since the original terminal was constructed and Berth 203 to 205 cannot

therefore safely accommodate fully laden new generation container vessels due to insufficient water

depth at these berths. At present these vessels enter and exit the Port partially laden and during the

high tide window. This is an unsafe operating condition and the risk exists that vessels could run

aground. Transnet National Ports Authority (TNPA) has proposed the deepening, lengthening and

widening of Berth 203 to 205 in order to improve the safety of the berths as well as to improve the

efficiency of the Port4.

Given the positive relationship between economic growth and trade, it is expected that the trade

resulting from the economic activity within the port system have a significant positive economic

impact on both the local regional economy as well as on the wider hinterland economies serviced by

the total system – and hence at a national level. The Port System is a hub of numerous and diverse

economic activities involving a range of economic actors. Once vessels call at port, or when cargo

passes through wharf side, the economic activity is energised in a myriad of areas. The economic

impact of improved efficiency at the port, therefore, will not be confined to the port alone but will

have a significant impact on the local economy as a whole. The value chain of a container terminal is

extensive, and the economic impact is, therefore, equally extensive. The next section describes the

methodology used to measure the extent of this impact.

2 Prestedge Retief Dresner Wijnberg (PRDW) (2011). Pre-Feasibility Study Report for the Proposed Berth Deepening of Berths 203 to 205 at DCT. PRDW Report No. 1079/0/003/REV01. 3 National Port Authority of South Africa container traffic recorded as per cargo due issues

4 Nemai Consulting (May 2012) ‘Deepening, Lengthening and Widening of Berth 203 to 205, Pier , Container

Terminal, Port of Durban, FINAL SCOPING REPORT’

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

9

1.3 Methodology

The economic impact of the ports on their hinterlands and local economies is not measured in tons

of cargo, in TEUs (twenty foot equivalent unit) or in gross tonnage (gt) of vessels utilising the port,

rather, it is measured in terms of persons employed in port-related economic activity, and in cycles

of expenditure that originate in the port, and reverberate through the economy of the region.

Importantly, it examines the linkages that are forged between the maritime cluster and other

commercial and industrial groupings within the economy.

For instance, ships make use of marine infrastructure and marine services provided by the port

authority, they utilise a range of port terminals that are provided by Transnet and by a number of

private terminal operators, they require the ships’ husbandry services made available by ships’

agents, ship chandlers and bunker suppliers, their crews need transport services, medical services

and recreation, and they provide custom from time to time for local ship repairers, with their deep

and rich linkages into the steel fabrication, engineering, painting and outfitting industries. A much

broader array of economic activities surrounds the cargo handling and logistics process. Cargo is

handled physically in port terminals and by stevedores, it is distributed by road, rail and by pipeline,

its documentation, financing and on-carriage is facilitated by the employment-rich clearing &

forwarding industry, it requires storage in warehousing facilities, it is scrutinised by customs officials,

and its seamless progress to consignees and from suppliers is tracked by freight logistics

professionals5.

In order to calculate the economic impact of increased number of calls and containers handled at

berths 203-205, each of these ship services need to be taken into account. In this case, the spend of

an average call at pier 2 on each of these services was calculated in order to determine the injection

into the economy per call. Economic multipliers that calculate the increase in sales, income, gross

value added (production) and jobs generated per R1 spent are used to transfer the total call spend

into a measure of the impact on the economy. An average call at pier 2 handles 2300 TEUs

(one TEU represents the cargo capacity of a standard intermodal container) according to TPT, with a

calculated related spend impact of R12.3million through the local and regional economy. The

expansion of pier 2 will allow for this average call rate to increase, and hence the injection into the

economy will be able increase accordingly. This is referred to OPEX (operational expenditure)

economic modelling.

The economic impact of CAPEX (capital expenditure) is calculated by applying these multipliers to

the level of investment made by Transnet during the construction of the expansion. The direct and

indirect impacts of the OPEX and CAPEX make up the total economic impact of a given project, in

this case, the expansion of the Durban Container Terminal.

Once the operational and capital expenditure impact have been calculated, the socio-economic costs

can be incorporated. These impacts have been raised as part of the Scoping Report and as part of

the public participation process. Particular impacts flagged include the impact on subsistence

fishermen and recreational users of the port. The full set of socio-economic benefits and costs are

then assessed in table format. The diagram below outlines the steps in the methodology.

5 Urban-Econ, 2009, ‘South African Ports Sector Review’; developed for the National Ports Regulator of South

Africa.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

10

FIGURE 2 METHODOLOGY

Source: Urban-Econ 2012

1.4 Structure of the Report Given the above methodology, the structure of the report is as follows:

Section 1: Introduction

Section 2: Current Trade and Container Shipping Trends o This includes national trade trends, current container volumes being experienced at

the DCT and at pier 2 specifically, as well as, global trends in the size of container ships.

Section 3: Economic Impact o This includes the IO Modelling on CAPEX and OPEX as described in the methodology.

Section 4: Scoped Socio-Economic Impacts o This includes a brief description of the relevant socio-economic impacts as raised in

the scoping report and by various members of the public.

Section 5: Integrated Impact Table o This table provides a summary of all the social and economic impact considered as

part of this economic impact assessment.

Section 6: Conclusion o This includes the recommendations

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

11

Section 2: Current Trade and Container Shipping Trends The following section describes the container shipping trends at Durban Port, at the relevant berths

(203-205) and internationally. It also describes current trade trends and how they relate to

production in South Africa and KZN. This allows us to understand the economic value of the industry

and the reasons for infrastructure development, given current growth trends.

2.1 National Production and Trade Trends The graph below describes export and import trends in South Africa for the previous 11 years. In

this time, imports and exports have grown by 12% and 11% respectively. Similarly, growth in

production measured using GVA (gross value added) has grown by 11% in this time. The trend lines

in the graph below show how both the primary and secondary sector correlate with the level of

imports and exports (trade). Trade and production rely on each other. The majority of this trade is

done through Durban Port and therefore, as production increases, so will demand for the port.

FIGURE 3 EXPORT TRENDS FOR SOUTH AFRICA, 2000 - 2011

Source: Quantec Dataset, 2011

The graph below shows trade trends for KwaZulu-Natal, of which the significant majority (over two-

thirds) is derived from activity eThekwini’s economy. KZN is slightly different to the rest of the

country in that its trade is generated primarily by the secondary sector (manufacturing) and to a

lesser by the primary sector (agriculture and mining). Since 2009, the manufacturing sector has

been showing good recovery, and thus, in 2011, exports and imports have reached 2008 levels once

again. This positive growth in GVA and trade indicates a growing demand for port infrastructure.

-

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

2 0

11

Ran

d M

illio

ns

Export Trends for South Africa

South Africa Primary sector

South Africa Secondary sector

South Africa Imports

South Africa Exports

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

12

FIGURE 4 EXPORT TRENDS FOR KZN, 2000 -2011

Source: Quantec Dataset, 2011

2.2 Durban Port Container Trends The graph below gives the number of TEUs (one TEU represents the cargo capacity of a standard

intermodal container) that landed at Durban Port between 2003 and 2011. The trend shows that

the majority of containers are deepsea, and these deapsea incoming shipments have been growing

on average annually at 7.7% since 2003. Transhipped containers have grown at 6% on average

annually, although have reduced for the previous two years. The volume of coastwise containers is

significantly less than the other two categories and has experienced a negative growth rate of -7.9%

since 2003. Overall, the number of landed containers has grown at an average annual growth rate

of 7.2% over the period.

-

20 000

40 000

60 000

80 000

100 000

120 000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

2 0

11

Ran

d M

illio

ns

Export Trends for KZN

Kwazulu-Natal Primary sector

Kwazulu-Natal Secondary sector

Kwazulu-Natal Imports

Kwazulu-Natal Exports

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

13

FIGURE 5 CONTAINERS LANDED IN DURBAN, 2003 - 2011

Source: National Port Authority of South Africa

The graph below shows the number of containers (measured in TEUs) shipped from Durban Port.

The trend for container shipments is similar to that of containers landed at Durban Port. Deepsea

shipments make up the majority of all shipments, and have been growing at an average annual rate

of 6.7%. Transhipments have been growing at 8.4% and Coastwise shipments at 3.9%. Overall, the

number of shipped containers has grown at an average annual rate of 6.9% over the period.

FIGURE 6 CONTAINERS SHIPPED FROM DURBAN, 2003 - 2011

Source: National Port Authority of South Africa

The following table describes the volumes of containers handled at Durban Port across various

categories in 2011. The total number of TEUs handled in 2011 was 2 720 915. Due to the recovery

in the manufacturing sector and the KZN economy in general, volumes of containers shipped have

reached 2008 levels and both shipped and landed containers continue to grow. The proportion of

TEUs shipped versus landed in 2011 was exactly 50/50 and the proportion of TEUs that were full was

76%, and empty was 24%.

-

200 000

400 000

600 000

800 000

1 000 000

1 200 000

2003 2004 2005 2006 2007 2008 2009 2010 2011

6M

Un

its

(TEU

s)

Containers Landed in Durban Port, 2003-2011

DEEPSEA

COASTWISE

TRANSHIPPED

-

200 000

400 000

600 000

800 000

1 000 000

1 200 000

2003 2004 2005 2006 2007 2008 2009 2010 2011

6M

Un

its

(TEU

s)

Containers Shipped from Durban Port, 2003-2011

DEEPSEA

COASTWISE

TRANSHIPPED

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

14

TABLE 1 DURBAN PORT STATISTICS EXPRESSED IN 6M UNITS (TEUS), 2011

FULL EMPTY TOTAL

LANDED:

DEEPSEA 1 004 104 103 229 1 107 333

COASTWISE 2 753 6 125 8 878

TRANSHIPPED 200 933 43 094 244 027

TOTAL LANDED 1 207 790 152 448 1 360 238

SHIPPED:

DEEPSEA 627 731 422 242 1 049 973

COASTWISE 13 457 12 814 26 271

TRANSHIPPED 217 725 48 708 266 433

TOTAL SHIPPED 858 913 483 764 1 342 677

GRAND TOTAL 2 066 703 636 212 2 720 915

Source: National Port Authority of South Africa

The following graph gives a comparison of the period January to May for 2010, 2011 and 2012. The

graph reflects that the positive trends described above are continuing thus far in 2012, with only the

number of transhipped containers reducing in 2012.

FIGURE 7 CONTAINERS HANDLED, Q1 2010, 2011, 2012

2.3 Berths 203-205 Container Trends 37% of all containers handled at the port are handled at berths 203-205 which indicates the

importance of these berths to the container handling capacity of the port. These berths are located

on pier two which is the only area that has direct access to rail (Gauteng bound). The graph below

shows that berth 205 handles 51% of all containers at pier 2, while berths 203 and 204 handle 25%

each.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

15

FIGURE 8 TEUS HANDLED AT PIER 2, BERTHS 203, 204 AND 205

Source: Transnet Ports Authority

While the existing profile of vessels berthing at berths 203-205 is described by the liner trade as

“feeder –sized”, with an average gross tonnage of a vessel at these berths is 26 000gt (gross tonnage

measures a ships overall internal volume) and the average length overall is 180m6 (length overall is

the maximum length of a vessel's hull measured parallel to the waterline). These berths do

accommodate large vessels up to 345m LOA and it is for this reason that the expansion has been

proposed. The expansion is particularly important if, as expected, the average vessel size is going to

increase significantly over the next 10 to 20 years – this is described in detail in the following section.

2.4 Global Containership Trends After a capacity increase of 7.9% in 2010, cellular containership capacity is expected to grow by 8.1%

in 2012 and 10.3% in 2013, based on BRS-Alphaliner projections, with net global fleet increases of

1.4m TEU in 2012 and 1.8m TEU in 2013. The table below shows the number of existing container

ships and their capacity (measured in TEUs), as well as the number of containerships on order. It is

clear in the table that the capacity growth is unevenly distributed, with ships over 4,000 TEU

representing 87%-90% of the total capacity delivered during these two years. Half of the expected

6 CRM data provided from Transnet National Port Authorities

-

50 000

100 000

150 000

200 000

250 000

300 000

203 204 205

TEU

s

Berths

TEUs Handled at Berths 203-205

TEUS Landed

TEUS Shipped

SUMMARY BOX: Trends in allied economic and port performance

Productive industries (i.e. manufacturing, agriculture and mining) have shown recovery since the 2009 recession; hence exports and imports have recovered to 2008 levels and continue to show strong growth (11%) placing increasing demand on the port.

Volumes of containers handled have increased by 7% on average annually, and also superseded 2008 levels in 2011. Evidence shows continued growth in 2012.

Berths 203-205 handle 37% of the entire ports containers and are therefore critical to the port.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

16

capacity to be delivered in 2012 involves ships above 10,000 TEU. This trend is likely to continue as

large fixed port costs and high fuel oil prices, hovering at $600-700 per tonne, actually encourage the

use of the largest possible units on long haul routes as they allow operators to spread prohibitively

high port and fuel oil costs over a larger number of containers. This gives an impetus to carriers

employing such ships, and put those without them at a disadvantage. Some carriers, notably

Evergreen, may return to the shipyards in 2012 to order larger ships for this reason.

TABLE 2 EXISTING ORDER BOOK AS AT DECEMBER 2011

Source: Barry Rogliano Salles Annual Review 2012

Most of these large ships are earmarked for deployment on the Far East-Europe route. As a

consequence, medium-size VLCS of 8,000-9,000 TEU displaced by 10,000+ TEU ships are increasingly

finding their way onto north-south trades (emerging markets such as Africa being affected in this

way). Furthermore, the 8.1% fleet growth expected for 2012 presents a serious challenge for the

industry, as the demand growth is expected to weaken to 6.5%, against almost 8% growth in 2011.

This imbalance is leading to a build-up of excess ships. The 3,000-6,000 TEU range is likely to be the

most affected. Many ships in this size range are expected to be displaced by larger ships, with no

ready market to fully absorb large chunks of this redundant tonnage7.

At present, a typical caller to DCT is approximately 36 000gt, with a typical capacity of 34 00 TEU, this

is derived from the CRM data provided from Transnet National Port Authorities. However, the

indications are clear that the global phenomenon of larger vessels is becoming a reality on the

southern trade, with local liner operators anticipating the downward cascading of larger vessels

currently on the Europe-Asia and Europe-North America routes. Industry insiders reflect that there

is a 5 – 10 year window until Durban can expect average callers to be sized 7 000-10 000 TEU, this he

sees as a cascade down from their Europe-Asia and Europe-North America trade fleets. It is

anticipated that the SAECS trades, which have purpose built vessels will be slower to change. As

markets continue to expand in Africa, there will be a need to use larger vessels. For this trade, it is

not anticipated that the liner trade will require carriers of 10 000 – 12 000 TEU category for the next

decade. Currently, DCT does handle callers at the 10 000 TEU threshold, however, these vessels are

not operating fully laden.

7 Barry Rogliano Salles Annual Review 2012

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

17

Liner comment also reflected that if DCT doesn’t deepen sufficiently to meet new draught

requirements of larger vessels, then it is likely that the trade would consider in the medium term

calling at Coega and feedering cargo onto the Port of Durban. The impact of this is that there would

likely be higher cost passed onto the cargo owner per TEU and in addition, it could be anticipated

that given the close proximity (14hrs) by road, that container traffic could be redirected onto road

which would reduce absolute port caller numbers.

The cost per TEU of ship-time in port is an increasing function of ship size8. Figure 2 below shows

that as vessel size increases, average costs decrease (line) but total costs increase (histogram). As

mentioned, the average costs decrease due to the large fixed port and fuel costs making it

advantageous to increase ship capacity. The total costs increase with vessel size, however, because

turnaround times at the port increase. It is, therefore, vital that capacity at the DCT is increased to

match the increase in large vessels through infrastructure investment such as this berth expansion

project and the current increase in capacity of the crane configuration in the port which is seeing 30

staff being added to pier 2 alone. If this does not occur, it will become increasingly cost inefficient

for vessels to use Durban Port resulting in increased shipping prices for local importers and exporters

in particular.

FIGURE 9 INCREASE IN TOTAL COSTS (HISTOGRAM) AND DECREASE IN AVERAGE COSTS

(LINE) PER DAY AS A FUNCTION OF CONTAINERSHIP SIZE IN 1997

Source: Cariou and Haralambides (1999), Cariou (2000)

The following table describes the recorded average vessel and port turnaround time at pier 2 from

April to December 2011. It also shows the key performance indicator for each of these. The average

turnaround time for a container vessel calling at Pier 2 is 60 hours (2 and a half days)9, and the

8 Haralambides E. H., Benacchio M., Cariou P. (2002) Costs, Benefits and Pricing of Dedicated Container Terminals,

International Journal of Maritime Economics Vol. 4-1, March, pp. 21-34 9 If the vessel arrives 2 or 3 days earlier than the ETA given to the terminal then this time is not included in the calculation.

If there are transhipment connections which the Line needs to take place and the on-carrying vessel arrives before the pre-carrying vessel so cannot be worked then this time is also not included in the calculation.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

18

average port turnaround time is 141 hours (just less than 6 days). However, the key performance

indicator for both these is 40 hours (less than 2 days). It is vital for trade in South Africa that the

port is efficient. Efficiency will determine Durban Port’s ability to remain competitive as vessel sizes

and volumes increase.

TABLE 3 KEY PERFORMANCE INDICATORS FOR PIER 2, DCT

Indicator April May June July Aug Sept Oct Nov Dec Target

Vessel Turnaround Time

53.0 51.2 54.1 61.8 72.8 70.7 64.1 52.5 55.1 40 Hours

Port Turnaround Time

165.4 131.8 141.1 128.2 183.7 194.3 137.8 87.0 104.1 40 Hours

Source: Durban Container Terminals, DPC presentation, December 2011

Currently, the average call-size is 1,770 moves (using information from 1 April 2012 to-date). Several

cranes have been purchased by Transnet in order to increase the number of moves. The crane

configuration after January 2013 will be:

North Quay (Berths 203-205): 2 Liebherr twin lift cranes, 1 Impsa single lift carne and 7

ZPMC tandem lift cranes = 10

East Quay(Berths 200+202): 6 Noell single lift cranes

South Quay Berth (108/9): 4 Liebherr twin lift cranes

Pier 1(Berths 105+107): 6 Liebherr single lift cranes.

The 7 new tandem lift cranes will assist reduce handling inefficiencies, and support faster

turnaround times for vessels. This is anticipated to a 10% gain in efficiency, which will reduce vessel

turnaround times by 9 hours10.

10

TPT estimates, 201

SUMMARY BOX: Relevance of current container shipping trends to DCT

The consequence of these factors for the Durban Container Terminal is that, regardless of demand

for containers, ship sizes are increasing and will continue to do so into the near future to a point

where 3,000-6,000 teu range ships are phased out and replaced with medium and large sized

vessels of 8,000-10,000teus. Currently, the terminal can only accommodate ships up to 9,000teus

(not fully laden) at high tide. If the expansion does not occur, Durban Port will be unable to

accommodate an increasing number of containerships and, thus, regional competitiveness of KZN

will be reduced. In the long term, this reduced competitiveness will be significant and detrimental

to trade in the province and will raise cost of exports by incurring an additional feedering service,

at best, to a port that can handle larger vessel sizes and at worst, losing out on the trades to other

ports on the eastern sea-board of Africa that are undertaking these necessary in-situ upgrades.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

19

Section 3: Economic Impacts This section provides an initial quantification of the economic impact of the proposed expansion of

berths 203 – 205 at the DCT.

Economic impact refers to the effects on the level of economic activity in a given area as result of

some form of external intervention in the economy. The intervention can be in the form of new

investment in for example, transport facilities, social developments, housing, business development,

the establishment of a new or the expansion of existing production capacity. In this instance, it is the

expansion of the Durban Container Terminal.

3.1 Input-Output Economic Model In order to quantify the economic impact of the proposed expansion, an input/output model was

used. The model contains information on inter-sector relations, including tables that describe, for

each sector included in the model, the amount of input the sector requires from other sectors to

produce one unit of output. It is thus a set of equations describing the relationships that link the

output of one industry with all other industries in an economy.

These models are able to estimate impacts within each industry in the model and thereby provide

much more information than simple total economic impacts on income, output, and employment.

Using, for example, new investment or operational expense data, multipliers are calculated to

estimate different impacts of development investment and its ripple effects through the economy.

Measures of input also take into account imports and exports to and from the specific geographic

area.

Impact Measurement – Direct and Indirect: The economic impact in this regard is defined as effects

on the level of economic activity in South Africa and the benefit to the economy, such as the

generation of additional jobs, business sales, and/or disposable income. To quantify the most likely

economic impact of a new business or expansion of an existing activity into a specific area, two types

of economic impact can be measured, namely, direct and multiplicative impacts.

The direct economic effects are generated when the new business creates new jobs and purchase

additional goods and services to operate the new facility.

The multiplicative effects can be grouped into two distinct effects: indirect and induced.

The indirect economic effects occur when the suppliers of goods and services to the new business

experience larger markets and potential to expand. Induced impacts: The induced impacts are the

impacts on goods and services demanded due to increased expenditure by households from income

earned due at the project.

3.2 CAPEX Impact Modelling The economic impact during the construction phase is shown for each of the three construction

options. The construction options are Caisson, Deck on Piles, and Sheet Piles (which has the highest

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

20

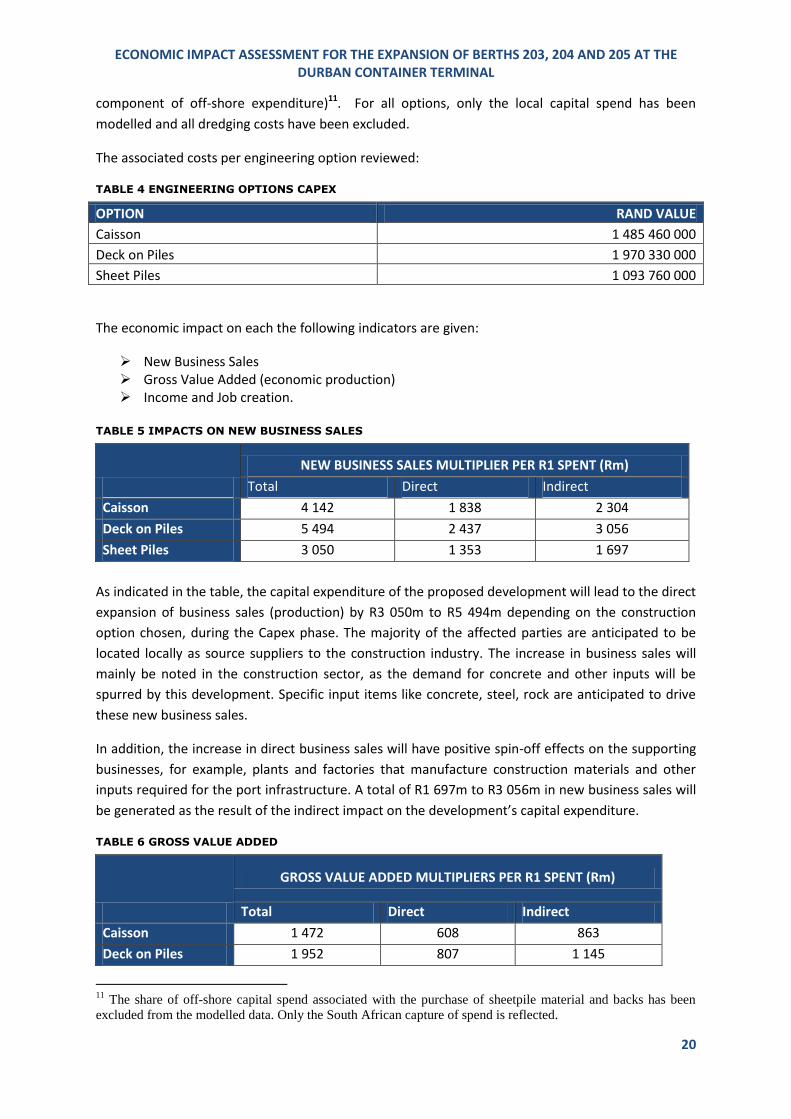

component of off-shore expenditure)11. For all options, only the local capital spend has been

modelled and all dredging costs have been excluded.

The associated costs per engineering option reviewed:

TABLE 4 ENGINEERING OPTIONS CAPEX

OPTION RAND VALUE

Caisson 1 485 460 000

Deck on Piles 1 970 330 000

Sheet Piles 1 093 760 000

The economic impact on each the following indicators are given:

New Business Sales Gross Value Added (economic production) Income and Job creation.

TABLE 5 IMPACTS ON NEW BUSINESS SALES

NEW BUSINESS SALES MULTIPLIER PER R1 SPENT (Rm)

Total Direct Indirect

Caisson 4 142 1 838 2 304

Deck on Piles 5 494 2 437 3 056

Sheet Piles 3 050 1 353 1 697

As indicated in the table, the capital expenditure of the proposed development will lead to the direct

expansion of business sales (production) by R3 050m to R5 494m depending on the construction

option chosen, during the Capex phase. The majority of the affected parties are anticipated to be

located locally as source suppliers to the construction industry. The increase in business sales will

mainly be noted in the construction sector, as the demand for concrete and other inputs will be

spurred by this development. Specific input items like concrete, steel, rock are anticipated to drive

these new business sales.

In addition, the increase in direct business sales will have positive spin-off effects on the supporting

businesses, for example, plants and factories that manufacture construction materials and other

inputs required for the port infrastructure. A total of R1 697m to R3 056m in new business sales will

be generated as the result of the indirect impact on the development’s capital expenditure.

TABLE 6 GROSS VALUE ADDED

GROSS VALUE ADDED MULTIPLIERS PER R1 SPENT (Rm)

Total Direct Indirect

Caisson 1 472 608 863

Deck on Piles 1 952 807 1 145

11

The share of off-shore capital spend associated with the purchase of sheetpile material and backs has been

excluded from the modelled data. Only the South African capture of spend is reflected.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

21

Sheet Piles 1 083 448 636

Gross Value Added reflects the rand values for the goods and services produced (less the cost of raw

materials and inputs). The measure provides the basis for determining impact on gross domestic

product – as it provides a mechanism to measure the additional output produced as a result of the

economic intervention of expanding DCT.

As reflected in the table above, GVA indicates a direct impact of R448m to R807m as a result of the

Capex spend on the Pier 2 expansion, and a further indirect/induced impact of R636m to R1145m. In

total this provides a GVA impact of R1 083m to R1 952m depending on which option is chosen.

TABLE 7 INCOME MULTIPLIERS

KZN Impact

INCOME MULTIPLIERS PER R1 SPENT (Rm)

Total Direct Indirect

Caisson 726 322 404

Deck on Piles 963 427 536

Sheet Piles 535 237 298

The income multipliers above reflect the KZN anticipated impact12. Additional income generated as

a result of the construction phase of the development is totalled at R 535m to R963m. The directly

attributed wage bill – for work both on site and for immediate first round impacts is estimated at

R237m to R427m. Many of these jobs are likely to be filled by local residents as the closest source of

labour, which will significantly increase the disposable income levels within the Durban area.

Additional income of R298m to R536m is likely to be generated through indirect mechanisms.

TABLE 8 TOTAL TEMPORARY EMPLOYMENT OPPORTUNITES DURING CONSTRUCTION PHASE

Total Temporary Job Opportunities

Total Direct Indirect

Caisson 7 091 3 991 3 100

Deck on Piles 9 406 5 294 4 112

Sheet Piles 5 222 2 939 2 283

Lastly, the number of temporary employment opportunities is provided. It is anticipated that 5 222

to 9 406 temporary job opportunities will be created depending on what option is chosen. Directly

related employment is likely to rise by 2 939 to 5 294 persons – and this impact is most likely to be

felt in the construction sector. In addition, 2 283 to 4 112 positions will be created through indirect

impact, and these are likely to be in the manufacturing and tertiary sectors.

Typically, employment is equated solely to the number of jobs generated, however in measuring the

impact of large scale capital projects such as the Pier 2 deepening additional considerations must be

included: the capital intensive nature, due to the engineering requirements, and the phasing in

distinct phases where part-time and/or contract workers are likely to be used must be considered in

the model, otherwise there is a potential to create a misleading assessment resulting in an

12

This figure has been derived using the KZN I-O model, and is provided as there is a higher level of certainty

with the regional impact than the national impact with regard to anticipated income changes at household level.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

22

exaggeration of economic impact. The model takes the nature of the development and the local

spend consideration into account in deriving the job opportunities.

In this model, employment impacts are measured in terms of the number of temporary jobs

generated over the capital construction period, these are referred to as temporary as the these

opportunities are likely to be taken up by equally over the phased development time frame.

Permanent employment opportunities are measured based on increased operational (OPEX) output,

and are described in the following section.

3.3 OPEX Impact Modelling A considered method for measuring the economic impact of the port at the operational impact

modelling level focuses on expenditure flows associated with additional port activity. To this end,

the operational impact has been modelled using a typical spend profile of a 2300 TEU container call

by an average sized 36 680 gt vessel13. The following assumptions about intermodal and destination:

an 85%/15% road/rail split of cargo distribution and 35%/65% split of container volumes across

Durban/non-Durban cargo owners14. To reduce the double count on the road split, the figures in the

table allows for short-haulage to a de-stuffing warehousing and re-parcelling of container goods.

This method takes a representative container vessel working 2300 TEU of container cargo by

traditional stevedoring services over a typical 4 day port visit15. A conservative view is taken of

expenditure flows, as these are limited to direct port-ancillary activities16, without considering

expenditure generated in the family of locally-based cargo owners (importers and exporters); and

expenditure flows are expressed initially in direct, first-round terms, without taking account of

multiplier effects. The port is consequently seen purely as a cargo-handling interface without regard

for the origins and destinations of cargo.

The typical spend profile per vessel is shown on below in table 7.

TABLE 9 PROFILE OF CONTAINER VESSEL SPENDING, EXCL CARGO DUES, CURRENT TRAFFIC AND

TARIFF LEVELS, 2012

Item/Service Expenditure R

% total

TNPA marine infrastructure & services 180 524 1.46

TPT Terminal charges 2 665 700 21.62

Stevedoring & Lashing/Securing 80 500 0.65

Ships Agency 4 840 0.04

Ship Chandlers 63 600 0.52

Clearing & Forwarding and Warehousing 1 235 850 10.02

Container depots, logistics etc 360 400 2.92

Road haulage 3 519 000 28.54

Rail charges 2 208 000 17.91

13

Based on TNPA CMR data for 2011 and year to date 2012. 14

Based on industry inputs from clearing and forwarding industry and haulier industry provided during June 2012. 15

Average turnaround time for a container vessel calling at Pier 1 or Pier 2 is around 62 hours with and average call-size of about 1,770 moves (TNPA: 22 June 2012) 16

It should be stressed that this relates solely to port-ancillary activities – that is, to economics activities that would not exist in the absence of a port of Durban – and do not include port-using cargo owners, however intimately many of these might be dependent upon the port.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

23

Ship repair services 106 400 0.86

Bunkers & fuel 1 861 798 15.10

Miscellaneous medical, crew transfers etc 44 000 0.36

TOTAL EXPENDITURE PER CALL PER VESSEL DIRECTLY RELATED SPEND

12 330 611

100

Source: Urban-Econ: Based on Industry Interviews, June 2012.

The table indicates a total direct spend of R12 330 611 per visit by container vessels, this includes

bunker (fuel) spend. This spend is then circulated through the multiplier effect to a range of indirect

and induced beneficiaries in supporting industries, promoting employment opportunities in allied

industries that support the port cluster, industries ranging from manufacturing through to business

services.

In order to present the impact of the port over the lifetime of the infrastructural asset base, the

spend profile impacts is shown for specific years of the operational phase of the expanded berths.

This shows a depth of linkages between port traffic levels and associated (port and petroleum) as

well as non-port industry.

The induced spends indicate the multiplier effect impact. Importantly, the traffic growth supports

broad employment opportunities.

The TEU figure is derived using the proposed TNPA model for the expansion plan, and the spend per

TEU is based on vessel spend for an average 2300 TEU container vessel.

Direct first round post cluster spend reflects spend to port related businesses.

Induced spend makes use of the transport sector multipliers

Total spend is the sum of direct and induced spend.

Port Related Petroleum Industry Employment was derived using a petroleum multiplier,

weighted for the percentage of bunker trade as a share of total sector

Wider economy employment examines the induced employment provided by the increase in

port traffic figures.

Total employment is the sum of all three employment categories.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

24

TABLE 10 SPEND PROFILE IMPACTS FOR PROJECTED NEXT 13 YEARS (2012/13 – 2024/25) FOR THE OPERATIONAL PHASE IF THE FULL DEEPENING IS

ACHIEVED17

Year TEU PROJECTIONS at PIER 2, BERTHS 203 - 205

First round port cluster spend (Rm)

Induced supporting services spend (Rm)

Total Port Cluster Employment

Port Related Petroleum Industry Employment

Wider Economy Employment

Total Employment

2012/13 1 977 010 10 599 8 479 19 078 3 530 214 4 670 8 415

2013/14 2 095 631 11 235 8 988 20 223 3 742 227 4 950 8 920

2014/15 2 244 411 12 033 9 626 21 659 4 008 243 5 302 9 553

2015/16 2 449 633 13 133 10 506 23 639 4 374 265 5 787 10 426

2016/17 2 622 929 14 062 11 250 25 311 4 684 284 6 196 11 164

2017/18 2 948 214 15 806 12 645 28 450 5 265 319 6 964 12 548

2018/19 3 184 071 17 070 13 656 30 726 5 686 345 7 522 13 552

2019/20 3 438 797 18 436 14 749 33 185 6 141 372 8 123 14 636

2020/21 3 713 901 19 911 15 929 35 839 6 632 402 8 773 15 807

2021/22 4 011 013 21 504 17 203 38 706 7 163 434 9 475 17 072

2022/23 4 331 894 23 224 18 579 41 803 7 736 469 10 233 18 438

2023/24 4 678 446 25 082 20 065 45 147 8 354 507 11 052 19 913

2024/25 5 052 721 27 088 21 671 48 759 9 023 547 11 936 21 506

17 TNPA projections provided to 2018. Urban-Econ projections (medium growth) scenario applied from 2018 – 2025.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

25

Using the projections of TEU volumes from TNPA from 2012/13 – 2017/18 the following is evident:

First round impact spend equates to R10 599m in the local economy, and a further induced spend of

R8 479m in 2012/13. This has an overall impact of employment of 8 415 persons. Using this growth

rate in TEU, by 2017/18 the traffic base in TEUs is estimated at just under 3m TEU, with an

equivalent impact of R28 450m (direct and induced spend) and an employment profile of 12 548

persons.

Using a medium term growth rate of 8% of (post recession growth), by 2025 TEU traffic projections

on these berths reaches over 5 million TEU per annum. This relates to spend of R27 088m first round

and a further spend of R21 671 induced into supporting services. Employment related to this traffic

base is 21 506 persons.

3.4 Berth Deepening Scenarios and Associated Impacts The following section relates this growth rate projected in 3.3 above to three scenarios of

development, and tests whether or not this economic activity will be able to be captured in the

regional economy as anticipated if the deepening of the nominated three berths does not occur as

per Transnet planning in this EIA submission.

Currently, Pier 2 is 914m in length. A standard large vessel caller to Pier 2 is 350m in length and a

typical feeder (smaller) vessel is 220m in length. Each large vessel requires 40m on either side in

order to safely berth – therefore each larger caller actually requires 430m. During construction it

will be necessary to decommission 1 berth and keep two berths operational at any time.

The three scenarios:

Full development takes place; Limited development, deepening but no extension to Pier 2 at berth 205 by the proposed

170m; and

No development takes place

These scenarios are detailed in the table, and take into account that there is a 4 year construction

period (mid 2013 to end 2017) anticipated for the deepening of berths 203, 204 and 205. In addition,

these scenarios take into account the anticipated Durban Dig-Out Port depth capacity becoming

available by 2020.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

26

Scenario De-Commissioning of Berth During Construction (mid 2013-2017) Impact

Post Construction (2018 onwards) Impact

Full development

No loss of handling facilities as single berth decommissioning can be accommodated during this period in other parts of the port.

No loss of handling anticipated.

No Extension to Berth 205

During construction it will be necessary to decommission 1 berth and keep two berths operational at any time. If we do not have expansion of 170m, and decommission one berth then there will be an effective quay side of 484m operational for the duration of the construction period (4 years). This means only one larger or one smaller vessel will be able to berth at any time. Effectively reducing the number of TEUs handled at Pier 2 during this period by a third (or 12% in the port of Durban as these berths handle 37%) of the total container traffic base. This equates to 3 106 159 lost TEUs. This equates to a loss of direct spend of R16 653m, induced spend of R21 671m and port related employment loss of 5 547 jobs and total employment loss of 13 221 jobs over the four years.

In the short term the port is in the process of recovery and is yet to reach the volumes and growth that was being experienced at the peak of 2008. Thus, in the short term it is unlikely that this will cause any loss in trade. However, in the long term the opportunity cost increases substantially if the port is unable to accommodate increasing volumes of large vessels servicing the Africa-Far East trade and the Africa-Near East trade. Specifically, if the rate of change of 3% on vessel size upwards is applied, a loss in TEU handling of 284 108 is anticipated from 2018 to 2020 (after which time, it is assumed that the Dig-Out Port will be operational). The loss in handling capacity is due to the effective inability to berth three larger vessels simultaneously at these berths. It is anticipated that due to the additional draught requirements of these larger vessels they will not be easily accommodated within the port. While it may appear a small number of containers however this equates to a loss of direct spend of R554m, induced spend of R443m and port related employment loss of 185 jobs and total employment loss of 446 jobs over the three years before the Dig-Out Port comes on line. This rate of change in vessel size will grow more rapidly after 2025 and losses incurred due to the lack of extension could result in zero rate of traffic growth to the terminal before the full capacity of the proposed dig-out port is available.

No During this recovery period (continuing through construction Significant loss of TEU traffic (1 019 460 TEU) is anticipated from 2016

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

27

development takes place

phase) this will not cause any loss in trade. The anticipated shift towards larger vessels is to occur in a five year time frame, at a changeover rate of 3% per annum on the Southern trades, therefore, no direct impact anticipated during construction on the loss of handling within the Port of Durban. However, and absolute loss off all anticipated impacts derived from the CAPEX phase occurs, this equates to a loss of:

R3050m to R5494m in new business sales

R1083m to R1952m in Gross Value Added

R963m to R535m in income multipliers locally (KZN)

5 222 to 9 406 temporary work opportunities created

through the port construction process.

to 2025 if the deepening of the berths is not undertaken. This ten year period reflects the anticipated short term transition to larger vessel stock in the Southern trades. This equates to a loss of handling capacity of 284 108 TEUS carried on vessels to large to be berthed if the depth at berths 203 – 205 is not increased in the short term, until available capacity at the dig-out port becomes available. Which has a direct spend loss impact of R1961m, induced spend of R1569m, port related employment loss of 852 jobs and total employment loss of 3530 over the period of 2016 – 2020.

NO DEVELOPMENT SCENARIO - LOSS DUE CHANGE IN VESSEL SIZE DURING OPERATIONAL PHASE ONLY

Year

TEU projections at Pier 2, Berths

203-205

First round port cluster spend (Rm)

Induced supporting

services spend (Rm)

Total (Rm) Port Cluster

Employment ( no of jobs)

Port Related Petroleum Industry

Employment (no of jobs)

Wider Economy

Employment (no of jobs)

Total Employment (no of jobs)

2016/17 78,688 422 337 759 141 9 186 335

2017/18 88,446 474 379 854 158 10 209 376

2018/19 95,522 512 410 922 171 10 226 407

2019/20 103,164 553 442 996 184 11 244 439

2020/21 111,417 597 478 1,075 199 12 263 474

2021/22 120,330 645 516 1,161 215 13 284 512

2022/23 129,957 697 557 1,254 232 14 307 553

2023/24 140,353 752 602 1,354 251 15 332 597

2024/25 151,582 813 650 1,463 271 16 358 645

TOTAL LOSS (NO DEV)

1,019,460 5,465 4,372 9,838 1,820 110 2,408 4,339

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

28

3.5 Concluding Comments 1. The temporary benefits of the construction process have been shown to include:

R3050m to R5494m in new business sales

R1083m to R1952m in Gross Value Added

R963m to R535m in income multipliers locally (KZN)

5 222 to 9 406 temporary work opportunities created through the port construction

process.

2. The operational benefits of the expansion to year 2025 have been shown as follows:

Using the projections of TEU volumes from TNPA from 2012/13 – 2017/18 and a

medium term growth rate of 8% (post-recession growth) from 2017/18 – 2024/25, by

2025 TEU traffic projections on these berths reaches over 5 million TEU per annum. This

relates to spend of R27 088m first round and a further spend of R21 671 induced into

supporting services. Employment related to this traffic base is 21 506 persons.

3. The losses in benefits if the berths were only deepened but not lengthened by 170m were

shown to include:

a loss of direct spend of R16 653m, induced spend of R21 671m and port related

employment loss of 5 547 jobs and total employment loss of 13 221 jobs over the four

years of construction.

a loss of direct spend of R1 523m, induced spend of R2119m and port related

employment loss of 507 jobs and total employment loss of 1225 jobs over the

operational seven years. If the capacity for the Dig-Out Port comes on line, in

accordance with the anticipated planning horizon, by 2021 then this loss is reduced to: a

loss in direct spend of R554m, a loss in induced spend of R443m and port related

employment loss of 185 jobs and total employment loss of 446 jobs over the operational

three year period between the end of construction and the availability of initial capacity

at the dig-out port.

4. The losses in benefits if the expansion does not occur at all were shown to include:

No loss of trade for the first 5 years, absolute loss of all CAPEX investment benefit.

This equates to a loss of handling capacity of 284 108 TEUS carried on vessels too large to be berthed if the depth at berths 203 – 205 is not increased in the short term, until available capacity at the dig-out port becomes available.

Which has a direct spend loss impact of R1961m, induced spend of R1569m, port related employment loss of 852 jobs and total employment loss of 3530 over the period of 2016 – 2020.

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

29

Section 4: Scoped Socio-Economic Impacts The impact on subsistence fishing, beach tourism, and traffic were flagged as part of the scoping

report and raised during public meetings by interested and affected parties. Each of these is

discussed in the following sections.

4.1 Subsistence Fishing (Includes Commercial and Recreational) An organisation called the KZN Subsistence Fisherman Forum has raised concern that the DCT

expansion is going to impact on their livelihoods. Eleven fishermen from the forum came forward,

however, it is uncertain how many subsistence fishermen are utilising the port; as Ezemvelo Wildlife

stated that there are no registered subsistence fishermen formally recorded on their register for the

eThekwini area. The closest registered and recognised subsistence fisher groups are located in

Umgababa (south coast) and Nonoti (north coast). Furthermore, officially, there is no port access

allowed to fishermen by the TNPA. Regardless, it seems that subsistence fishing is occurring within

the port and along the coast north and south of the port and there is a possibility that this may be

impacted by the expansion and deepening of berths 203-205. There is also a possibility that the

impact on the Durban port estuary habitat will affect fish populations along the east coast which

might also affect commercial and recreational fishers.

4.1.1 An overview of subsistence fishing in KZN and Durban Bay

True subsistence fishing is not a chosen activity but one carried out to obtain the basics for survival

when there are no alternatives. It can produce extra resources, which occasionally may be sold or

bartered, but the basic aim is not to sell the resources. The following description of subsistence

fishing is provided by Ezemvelo KZN Wildlife’s Craig Mulqueeny18.

Many communities in KZN have been formally identified, by Ezemvelo and MCM, as containing true

“subsistence fishers” and most of these have been formalized with permits issued and the fishing

monitored. No subsistence fishing licenses have been issued to fishermen within eThekwini’s

borders. According to Ezemvelo, in almost all cases identified so far, there has been a drastic decline

over the last few years in the numbers of people carrying out subsistence fishing. This is usually

ascribed to the advent of and improvement in social grants which now supply most of the poorest

people in the province with much of their basic needs. In 2011 approximately 6% of all shore anglers

in KZN could be considered true subsistence fishers (this translates to approximately 4 000 people)19.

Most of the difficulties with subsistence fishing have arisen where there is a blending of true

subsistence fishing and commercial interests. Where people really were trying to obtain their basic

needs these have now mostly been made available through the grants. There are serious challenges

due to the sale of resources collected under the “umbrella” of subsistence fishing as many of the

resources may not legally be sold and the resources cannot sustain increased use levels. If any

dispensation was to be made for these fishers then it could not be for “subsistence fishing” but for

a commercial enterprise20.

18

http://sancor.nrf.ac.za/newsletters/past-issues/issue-188/the-exclusion-of-subsistence-fishers-from-public-spaces-in-durban 19

Dunlop SW (2011) An assessment of the shore-based and off-shore boat linefishers of KwaZulu-Natal, South Africa, Unpublished thesis of UKZN 20

Ezemvelo KZN Wildlife, Craig MulQueeny, Sancor Newsletter

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

30

4.1.2 Recreational and Commercial Fishing in KZN

According to research conducted by ORI over 2010/2011 there are approximately 70 000 shore

fishers in KZN and this number has remained fairly constant over the previous 10 to 15 years. They

all operate under recreational licenses. It is estimated that the total recreational shore catch per

annum in KZN is 250 tons. At R40 per ton this equates to R10 million per annum (Dunlop 2011)21.

However, due the recreational nature of this fishing, it is not expected that all of this catch is sold

(perhaps 50%). It should be noted that the value of recreational fishing due to tourism and retail

spend is significant. CIC International estimate that 30% of commercial catch is estuary-dependent

and that of this, 13% is attributable to the Durban Bay. This equates to R390 000.

Many anglers fish on the Durban beachfront throughout the year. It is a renowned venue for

recreational anglers from all the provinces of South Africa and overseas and good catches can still be

made from the beaches and piers. Monitoring shows that the most common species

caught, accounting for well over half the fish, is shad. Shad are a ‘recreational” list species which

may not be sold in KZN. Many thousands of visitors come to KZN annually to fish along the shore and

shad are the greatest drawcard. This industry is of immense importance to the economy of the

province and each shad caught effectively brings in much more revenue than would be obtained

from catching and selling the fish. Any marked reduction in shad abundance would undoubtedly

impact negatively on tourism22.

There are 52 commercial line boat rights available in KZN but only approximately 42 commercial line

boats currently operating on the KZN coast. It is estimated that 1487 metric tonnes of fish is caught

per annum by commercial line boats. Of this 457 tonnes is recreational, 245 by charter boats, and

785 is for commercial fishing (Dunlop 2011). The value of the total catch is approximately R60

million, and the value of the commercial catch alone is R31,4 million. It should be noted that the

value of recreational fishing due to tourism and retail spend is significant. CIC International estimate

that 45% of commercial catch is estuary-dependent and that of this, 13% is attributable to the

Durban Bay. This equates to R2 million.

4.1.3 Impact of the widening and extending of berths 203-205 on fishers in KZN

Based the above assessment we can conclude that there is little to no ‘true’ subsistence fishing in

the Durban area (albeit some in KZN) but that there is substantial commercial and recreational

fishing occurring. The proposed expansion could impact the line-fish population and bait harvests in

Durban Bay which would both have a negative impact on fishermen in the area and the economic

value of tourism to Durban. Furthermore, according to the CIC International Environmental

Resource Evaluation study all estuaries along the east coast form a metacommunitiy which relies on

each other to absorb shocks and provide breeding areas for fish. Therefore, any impact on the

Durban bay with impact proportionally (13%) on this East Coast metacommunity23. For these

reasons it is important to understand the impact that the widening and extending of berths 203-205

will have on line fish.

21

Dunlop SW (2011) An assessment of the shore-based and off-shore boat linefishers of KwaZulu-Natal, South Africa, Unpublished thesis of UKZN 22

Ezemvelo KZN Wildlife, Craig MulQueeny, Sancor Newsletter 23

CIC International (2007) Environmental Resource Economic Evaluation for Durban Bay

ECONOMIC IMPACT ASSESSMENT FOR THE EXPANSION OF BERTHS 203, 204 AND 205 AT THE DURBAN CONTAINER TERMINAL

31

According to the Estuarine Biodiversity Study conducted for this EIA, the central sand bank which will

be affected by the proposed project is particularly prevalent with high densities of sand prawn

Callianasa kraussi, higher than for most of the other sand banks in the Port (Newman et al. 2008).

These crustaceans are a very important food source for fish. Any destruction of the sandbank will

have a proportional impact on the fish in the estuary and therefore on the catch in the estuary and

along the coast. Furthermore, disturbance and/or displacement of linefish as a result of the

dredging operations is also considered likely. These effects may be reduced only by strict adherence

to a suite of proposed mitigation measures that include refilling/backfilling and enlarging of the

Centre Bank sand flat in addition to strict operating rules pertaining to dredging such that the extent

of any turbidity plumes are minimised and do not exceed specified threshold levels24.

Post construction, if mitigation measures are adopted in full and recreation of the habitat lost is

successful (specifically the offset created needs to fulfil the same function as the sand bank lost and

sand prawn in particular need to migrate effectively) then the resulting impact on line-fish will be

positive25. However, during construction, the disturbance created by dredging and other

construction will cause 50% of the linefish to be displaced within the extent of the dredge plume.

The impact on fishers within the bay will be medium to high during this time; however, the impact

outside of the plume extent is seen to be zero (Anchor Environmental).

4.2. Beach Tourism Interested and affected parties noted concern that there will be an impact on water quality and

wave size (turbidity and bed shear stress levels) which would affect prime beach areas at Ushaka and

Bluff. These beaches are used for various tourism activities and act as the major draw-card for

domestic tourism especially in Durban. Durban’s tourism industry provides an income for thousands

of people and contributes 4.8% to the city’s GVA. Any negative impact on the beaches would cause

a large knock-on effect in the economy of the city. The following sub-section discusses the value of

the beaches in Durban, to Durban’s economy.