ECONOMIC DEVELOPMENTS & BUSINESS OPPORTUNITIES

25

THE PHILIPPINES: ECONOMIC DEVELOPMENTS & BUSINESS OPPORTUNITIES By: ANTONIO A. MORALES Consul General To be presented by: GERMINIA V. AGUILAR-USUDAN Deputy Consul General Philippine Consulate General in Hong Kong

Transcript of ECONOMIC DEVELOPMENTS & BUSINESS OPPORTUNITIES

THE PHILIPPINES:ECONOMIC

DEVELOPMENTS &

BUSINESS

OPPORTUNITIESBy: ANTONIO A. MORALES

Consul General

To be presented by: GERMINIA V. AGUILAR-USUDAN

Deputy Consul General

Philippine Consulate General in Hong Kong

Resilience Amidst

External Shocks

6.2 percent GDP growth rate in 2018

* 6.9 percent growth in Industry

* 6.3 percent growth in Services

* 1.7 percent growth in Agriculture

PH: a Bright Spot in Asia

Steady Investment Inflows

* Php 105.19 million BOI-PEZA Approved Investments

PH: a Bright Spot in Asia

1.12.0

3.2 3.7

5.7 5.6

8.2

10.19.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2010 2011 2012 2013 2014 2015 2016 2017 2018

(in US$ billion)

19.29% Ave. annual growth rate (2016-2018)

GR

OW

THSource: BSP

PH: a Bright Spot in Asia

Robust inward FDI

Credit Ratings

PH: a Bright Spot in Asia

7

The Gross International Reserves reached approximately US$79.2 billion in 2018

Merchandise Exports

2018: US$67.49 billion(1.8% lower than 2017)

2017: US$68.71 billion

Service Exports

2018: US$43.96 billion(11.2% higher than 2017)

2017: US$39 billion

Source: DTI and BSP

PH:a Bright Spot in Asia

Steady Export

THE PH FACTOR

100.98MPopulation

(as of Aug 2015)

FILIPINOS ARE YOUNGER COMPARED TO THE REST OF THE WORLD

The median age in the Philippines is 24.1 years old.This is equivalent to the age of someone who

recently graduated from college.

EU-28

Thailand

USA

Australia

China

UAE

Vietnam

Philippines

42.6

37.8

37.6

37.4

37.0

33.4

30.4

24.1

PH in Demographic Sweet Spot

Our workforce is:• Highly educated and English Proficient• Strongly customer-oriented• Highly trainable with fast learning curve• Adaptable to universal cultures• High level of commitment and loyalty

We produced over 708,000 college graduates in AY 2017-2018 across a wide range of disciplines.

Breakdown of Graduates by Priority Discipline (AY 2017-18)

Agriculture, Forestry, Veterinary Medicine 25.421

Architectural and Town Planning 4,392

Education 145,421

Engineering and Technology 86,934

IT Related 86,933

Mathematics 3,104

Maritime 25,996

Medicine and Health Related 43,188

Sciences 7,827

Others 279,229

TOTAL GRADUATES 708,445 Source: CHED

0

200,000

400,000

600,000

800,000

2015-16 2016-17 2017-18

276,240 304,674 317,392

309,048 327,402 328,581

Higher Education Graduates

AY 2015 - 2018

Private Public

Rich Talent Pool

11

JapanTokyo

South KoreaSeoul

Shanghai

C h i n a

TaiwanTaipei

Hong Kong

ThailandBangkok

MalaysiaKuala Lumpur

Singapore

IndonesiaJakarta

3.25 hrs.

2 hrs.

3 hrs.

The country’s location is acritical entry point to over 600million people in the ASEANMarket and a natural gateway tothe East- Asian economies.

The country is likewise placed atthe crossroads of internationalshipping and airlines.

Within Asia, the Philippines isreachable within 3 to 4 hours byplane.

Unrivalled Access to Key Markets

ASEAN (10 members)

ASEAN Partners: China, Japan, South Korea,

India, Australia, New Zealand, Hong Kong

Europe: EFTA (Switzerland,

Norway Iceland and

Liechtenstein) & EU (GSP+)

United States

Market Size• PH - 104 M

• ASEAN - 629 M

• ASEAN+6 - 3.5 B (1/2 of World Population)

- $22.4 T (1/3 of World Economy)

Unrivalled Access to Key Markets

• EU - duty-free access for 6,274 tariff lines

under GSP+ Program

• PH, only ASEAN country with GSP+

• US – 70% of PH exports enter the US duty-

free (GSP & MFN)

Access to EU and the US

BUILD. BUILD. BUILD

• The Duterte Administration’s Build Build BuildProgram amounts to PhP8.4 trillion (~US$168B) in total for the 6-year period.

• The Build Build Build Program is composed ofhigh impact projects or the 75 flagship projectsof the current administration

Infrastructure Development

15

15

*as of 30 April 2016

http://www.peza.gov.ph/index.php/economic-zones

ECONOMIC ZONES and IPAs

• 18 IPAs• 74 Manufacturing

EcoZones• 262 IT Parks and Centers • 22 Agro-Industrial

EcoZones• 19 Tourism EcoZones• 2 Medical Tourism Zones

PPP and other Infrastructure Projects (in the pipeline)

• LRT Line 6 Project• New Manila Int’l Airport• East-West Rail Project• Manila Bay Integrated Flood

Control, Coastal Defense and Expressway Project

Completed and Operational Projects

• Daang Hari-SLEX Link Road• NAIA Expressway (Phase II)

Projects under Construction

• Metro Manila Skyway Stage 3 Project

• MRT Line 7 Project

*as of 30 November 2017 Sources: PEZA and PPP Center

Infrastructure Development

Business Opportunities:

2017 Investments Priorities Plan

Philippine Investment Priority Plan (IPP)

• 1. Regular List

• 2. Export Activities

• 3. Mandatory List

• 4. ARMM List

17

INCENTIVE

Board of Investments (BOI)

(Executive Order No. 226, as

amended)

Philippine Economic Zone Authority

(PEZA)

(Republic Act No. 7916, as amended)

Income Tax Holiday (ITH) 4 – 6 years (max of 8 years)

ITH Bonus 3 years provided the firm meets certain conditions

Special Tax Rate of 5% on

Gross IncomeNone Special Tax Rate of 5% on Gross Income

Importation of Capital

Equipment, Spare Parts and

Supplies

0% Duty Tax and Duty-Free

Importation of Raw Materials

& Supplies used in ExportTax Credit Tax & Duty-Free

Value Added Tax Zero Rating for

Exports 0%

Employment of Foreign

Nationals

Special Non-Immigrant Working Visa within 5 years from project’s registration

including spouse and unmarried children under 21 years of age

Competitive Investment Incentives

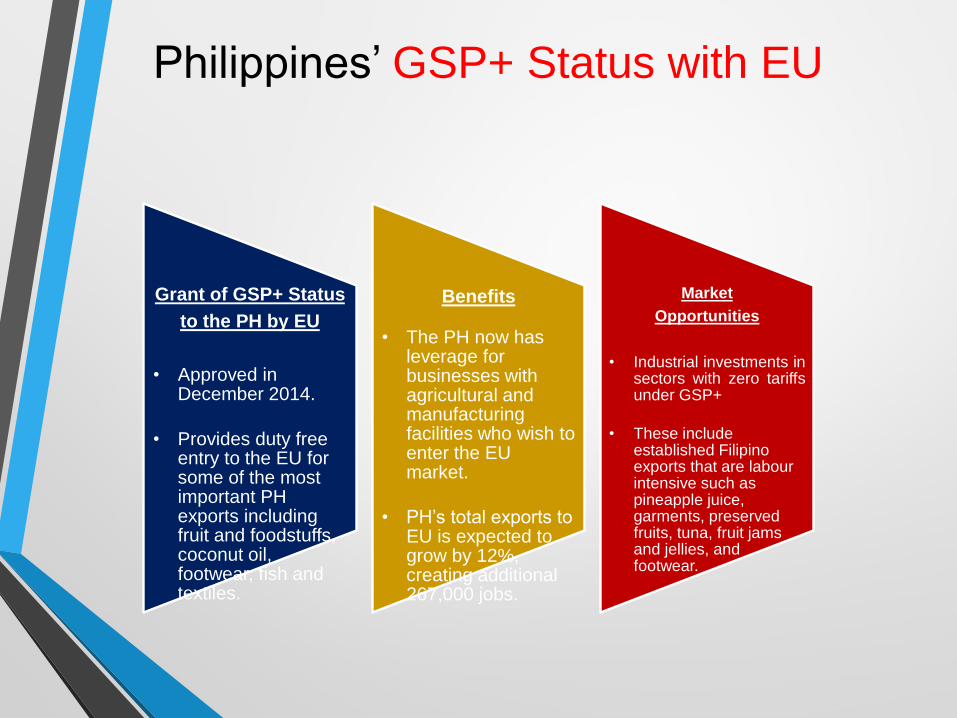

Grant of GSP+ Status

to the PH by EU

• Approved in December 2014.

• Provides duty free entry to the EU for some of the most important PH exports including fruit and foodstuffs, coconut oil, footwear, fish and textiles.

Benefits

• The PH now has leverage for businesses with agricultural and manufacturing facilities who wish to enter the EU market.

• PH’s total exports to EU is expected to grow by 12%, creating additional 267,000 jobs.

Market

Opportunities

• Industrial investments insectors with zero tariffsunder GSP+

• These include established Filipino exports that are labourintensive such as pineapple juice, garments, preserved fruits, tuna, fruit jams and jellies, and footwear.

Philippines’ GSP+ Status with EU

Strategic Initiatives:

Reforms that Transform

Manufacturing Resurgence Program 2014 - 2025

• Upgrade and transform the manufacturing industry to one that addresses the most binding constraints to manufacturing growth, strengthen industries and improve the business environment within which they operate

21

Phase 1

(2014-2017)

• Rebuild capacity of

existing industries

• Strengthen emerging

industries

• Maintain competitiveness

of comparative

advantage

industries

Phase 3

(2022 - 2025)

• Deepen participation in

regional integration by

serving as hubs in

production networks for

industries like auto,

electronics, machinery

garments, food

Phase 2

(2018 - 2021)

• Shift to high value added

activities

• Investments in upstream

industries

• Link and integrate

industries

Strategic Shift of Strategy to Industry Development

Transforming the PH economy

in the new digital age

◆ Build innovation & entrepreneurship ecosystem -> upgrade & develop new industries

◆ Remove obstacles to growth -> attract investments

◆ Strengthen domestic supply chains & deepen participation in global/regional value chains

New Industrial Strategy

Ease of Doing Business and Efficient Delivery of

Government Services Act of 2018 (an amendment of the

Anti-Red Tape Act of 2007)

• Promotes transparency and simplified requirements and procedures to reduce

red tape and expedite business and non-business related transactions in the

government

• Prescribed processing time for transactions– 3 days: Simple, 7 days:

Complex, 20 days: Highly Technical

• Penalty – 2-strike policy

23

REFORMS TO IMPROVE THE BUSINESS

ENVIRONMENT

Strategic Initiatives

Philippine Competition Act (Anti-Trust/Competition Policy )

Telecommuting Act

Allows private sector employees to work from an alternative

workplace with the use of current technology and

telecommunications

Foreign Investments Negative List (FINL)

Revised Corporation Code of the Philippines (RA 11232)

Minimum of 1 person may form a private corporation

24

REFORMS TO IMPROVE THE BUSINESS

ENVIRONMENT

Strategic Initiatives

Thank you very much!

Doh jeh sai!

Maraming salamat po!