Economic & Commercial Real Estate Outlooksites.cassidyturley.com/SORE/images/Kevin...

32

Kevin Thorpe, Chief Economist March 11 th 2013 Economic & Commercial Real Estate Outlook

Transcript of Economic & Commercial Real Estate Outlooksites.cassidyturley.com/SORE/images/Kevin...

Kevin Thorpe, Chief Economist

March 11th 2013

Economic & Commercial

Real Estate Outlook

2013 - 2014 Baseline Forecast

2012 2013 Annual

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2012 2013 2014

US Economy

Real GDP Growth, % 2.0 1.3 3.1 0.1 2.0 2.3 3.1 2.7 2.2 2.5 3.6

Job Growth, ths. 771 451 409 537 471 512 451 484 2,168 1,919 2,230

Office-using Job Growth,

ths. 231 172 129 138 114 124 109 117 670 464 541

Unemployment Rate 8.3 8.2 8.0 7.8 7.8 7.7 7.6 7.6 8.1 7.7 7.2

Retail Services Growth, % 6.5 -0.6 5.3 6.1 3.8 5.6 4.7 8.0 4.3 5.5 6.0

Inflation, % 2.5 0.8 2.3 2.1 1.9 2.1 2.2 2.2 1.9 2.1 2.9

CCI 68 65 65 70 73 75 78 80 67 77 85

Fed Funds Rate 0.1 0.2 0.1 0.2 0.1 0.1 0.1 0.1 0.1 0.1 0.1

10-year Gov't Bond 2.0 1.8 1.6 1.7 1.9 2.1 2.2 2.4 1.8 2.1 3.1

ISM Manufacturing Index 53.0 52.3 50.9 50.6 53 54 55 55 51.7 54 57

West Texas Intermediate 103 93 92 88 89 92 95 97 94 93 95

Office Sector

Net Absorption, msf 7.20 13.81 7.18 20.01 8.2 13.1 11.8 16.8 48.2 50.0 60.3

Vacancy 16.0% 15.8% 15.7% 15.4% 15.3% 15.2% 15.0% 14.9% 15.7% 15.1% 14.3%

Asking Rents $21.65 $21.72 $21.72 $21.69 $21.83 $21.92 $22.02 $22.13 $21.70 $21.98 $22.42

Industrial Sector

Net Absorption, msf 19.12 20.36 24.62 40.89 18.4 21.3 24.8 34.7 105.0 99.2 108.1

Vacancy 9.3% 9.3% 9.1% 8.9% 8.8% 8.6% 8.4% 8.3% 9.1% 8.5% 7.9%

Asking Rents $5.05 $5.04 $5.04 $5.00 $5.03 $5.06 $5.09 $5.12 $5.03 $5.07 $5.12

Retail Sector

Net Absorption, msf 3.47 2.27 1.50 2.29 3.7 4.6 2.1 3.5 9.5 13.8 16.0

Vacancy 10.9% 10.8% 10.8% 10.7% 10.6% 10.4% 10.4% 10.3% 10.8% 10.4% 10.1%

Asking Rents $19.00 $19.03 $19.05 $19.08 $19.09 $19.11 $19.12 $19.14 $19.04 $19.12 $19.17

Apartment Sector

Net Absorption, ths. sf 36.02 32.03 25.10 46.99 25.0 31.0 43.3 42.7 140.1 142.0 159.8

Vacancy 5.0% 4.8% 4.7% 4.5% 4.5% 4.5% 4.4% 4.4% 4.8% 4.5% 4.5%

Asking Rents $1,070 $1,082 $1,091 $1,097 $1,104 $1,122 $1,127 $1,136 $1,085 $1,122 $1,160

Exposure To Sequestration

2011 Federal Spending as % of GDP

39.9%

34.9%

29.3%

26.5%

23.5%

22.4%

22.0%

21.7%

21.3%

20.0%

19.5%

18.8%

17.6%

17.3%

15.9%

15.2%

14.9%

14.6%

14.3%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Washington, DC

Sacramento, CA

Baltimore, MD

St. Louis, MO

Tampa, FL

Riverside, CA

Louisville, KY

San Diego, CA

Los Angeles, CA

Raleigh, NC

Columbus, OH

Nashville, TN

Phoenix, AZ

Cincinnati, OH

Indianapolis, IN

San Francisco, CA

Atlanta, GA

Milwaukee, WI

Denver, CO

Source: U.S. Bureau of Economic Analysis (BEA); Consolidated Federal Funds Report, 2010

Sequester: Why Slash This?

0

10

20

30

40

0

10

20

30

40

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080 2085

Discretionary Spending Revenue

Percent of GDP

Source: Congressional Budget Office (The 2012 Long-Term Budget Outlook)

Entitlements Will Bankrupt The U.S.

0

10

20

30

40

0

10

20

30

40

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080 2085

Discretionary & Other Spending Entitlement Programs Revenue

Percent of GDP

Source: Congressional Budget Office (The 2012 Long-Term Budget Outlook)

Clear Bright Spots

Equity markets & housing

160

163

166

169

172

175

178

181

184

187

10500

11000

11500

12000

12500

13000

13500

14000

14500

Share Price Index: World - Dow Jones Industrial Average, (Index, NSA) for United States

Median Sales Price of Existing Homes: Single-Family & Coo & Co-op, (Ths. $, SA) for United States

Confidence Rising, Despite Threats

$3.30

$3.40

$3.50

$3.60

$3.70

$3.80

$3.90

52

54

56

58

60

62

64

66

68

70

72

Jan 2013 Feb 2013

CCI Gas Prices

Consumer Confidence vs. Gas Prices

7

Payroll taxes go up

Euro-zone less stable

Sequester approaching

Gas prices jump 50 cents

Source: Conference Board, Cassidy Turley Research

0

20

40

60

80

100

120

Retail (msf) Office (msf) Industrial (msf) Apartment (000's)

2012 Absorption

Pre-recession Average

CRE Demand Metrics

8

Net Absorption in 2012 vs. Pre-recession Annual Averages

Shifts in Commercial Space Usage

9

• The Rise of Creative Office Space • Adaptable “hackable” space • Space no longer homogenous • Repurposed space (warehouse as

office space, rooftops as gardens) • Strong identity exteriors

• Edgy Architecture

• Wireless environments • Green space a plus

Capital Markets

Capital Markets

$0

$100

$200

$300

$400

$500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

$210 $252

Sales Volume, $bil.

Sales Volume, All Product Types, $billions

11

Source: Real Capital Analytics

Bank Lending Trends

12

Loan Volume for CRE, y/y % chg.

Source: Federal Reserve

Bank Lending Trends

13

Loan Volume for CRE, y/y % chg.

Inflection Point

Source: Federal Reserve

Excess Reserves Still Huge

Aggregate Reserves of Depository Institutions

14

-$0.4

$0.0

$0.4

$0.8

$1.2

$1.6

Ja

n 2

00

0A

pr

200

0Ju

l 200

0O

ct

20

00

Ja

n 2

00

1A

pr

200

1Ju

l 200

1O

ct

20

01

Ja

n 2

00

2A

pr

200

2Ju

l 200

2O

ct

20

02

Ja

n 2

00

3A

pr

200

3Ju

l 200

3O

ct

20

03

Ja

n 2

00

4A

pr

200

4Ju

l 200

4O

ct

20

04

Ja

n 2

00

5A

pr

200

5Ju

l 200

5O

ct

20

05

Ja

n 2

00

6A

pr

200

6Ju

l 200

6O

ct

20

06

Ja

n 2

00

7A

pr

200

7Ju

l 200

7O

ct

20

07

Ja

n 2

00

8A

pr

200

8Ju

l 200

8O

ct

20

08

Ja

n 2

00

9A

pr

200

9Ju

l 200

9O

ct

20

09

Ja

n 2

01

0A

pr

201

0J

ul

20

10

Oct

20

10

Ja

n 2

01

1A

pr

201

1Ju

l 201

1O

ct

20

11

Ja

n 2

01

2A

pr

201

2Ju

l 201

2O

ct

20

12

Excess Reserves, $T

Source: Federal Reserve

CMBS Gaining Momentum

15

Source: Commercial Mortgage Alert

Fed Senior Loan Survey

-80

-60

-40

-20

0

20

40

60

80

100

Net % of Banks Tightening

Net % of banks reporting stronger demand

Percent of banks reporting stronger demand for CRE loans

16

Source: Federal Reserve

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

3,000

US Monetary Base (US $bn., LHS)

End of

QE1

End of

QE2

QE3

Source: U.S. Board of Governors of the Federal Reserve System

Monetary Policy

Characterization of Fed Officials & Votes

Source: Capital Economics

Ratings 2013 Vote

2014 Vote

Permanent Voters

Ben Bernanke Dove D D

William Dudley Unknown ? ?

Elizabeth Duke Moderate M M

Jerome Powell Moderate M M

Sara Bloom Raskin Unknown ? ?

Jeremy Stein Hawk H H

Daniel Tarullo Dove D D

Janet Yellen Dove D D

Rotating Regional Voters

James Bullard, St. Louis Moderate M

Charles Evans, Chicago Dover D

Esther George, Kansas City Hawk H

Eric Rosengren, Boston Dove D

Sandra Pianalto, Cleveland Hawk H

Charles Plosser, Philadelphia Hawk H

Richard Fisher, Dallas Hawk H

Narayana Kocherlakota, Min. Dover D

Dennis Lockhart, Atlanta Moderate

Jeffery Lacker, Richmond Hawk

John Williams, San Francisco Dove

Summary

Doves 7 5 4

Moderates 4 3 2

Hawks 6 2 4

Unknown 2 2 2

Total 19 12 12

Atlanta

29 35

-150

-100

-50

0

50

100

150

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Atlanta Making Progress

Job Growth/Losses, 000’s

Source: BLS

Historical Average = 33,000

Atlanta – Employment

2,439

2,345

1500

1600

1700

1800

1900

2000

2100

2200

2300

2400

2500

Dec 1

990

Au

g 1

99

1

Ap

r 1

99

2

Dec 1

992

Au

g 1

99

3

Ap

r 1

99

4

Dec 1

994

Au

g 1

99

5

Ap

r 1

99

6

Dec 1

996

Au

g 1

99

7

Ap

r 1

99

8

Dec 1

998

Au

g 1

99

9

Ap

r 2

00

0

Dec 2

000

Au

g 2

00

1

Ap

r 2

00

2

Dec 2

002

Au

g 2

00

3

Ap

r 2

00

4

Dec 2

004

Au

g 2

00

5

Ap

r 2

00

6

Dec 2

006

Au

g 2

00

7

Ap

r 2

00

8

Dec 2

008

Au

g 2

00

9

Ap

r 2

01

0

Dec 2

010

Au

g 2

01

1

Ap

r 2

01

2

Dec 2

012

Total Nonfarm, 000's

Atlanta MSA

Source: BLS

Office-using Job Growth

Jan 2010/Dec 2012, 000’s

Source: BLS

-20

0

20

40

60

80

100

120

140

Ne

w Y

ork

, N

Y

Da

lla

s-F

ort

Wo

rth

, T

X

Lo

s A

ng

ele

s, C

A

Ch

ica

go

, IL

Atl

an

ta, G

A

Sa

n J

ose

, C

A

Ho

us

ton

, T

X

Sa

n F

ran

cis

co

, C

A

Ta

mp

a, F

L

Min

neap

olis, M

N

Sa

nta

Ba

rba

ra, C

A

Milw

au

ke

e, W

I

Po

rtla

nd

, O

R

Oa

kla

nd

, C

A

Ind

ian

ap

olis

, IN

Sa

n A

nto

nio

, T

X

Orl

an

do

, F

L

Sa

cra

me

nto

, C

A

Co

lora

do

Sp

rin

gs, C

O

La

s V

eg

as

, N

V

Top 10 Bottom 10

Atlanta Office Market

23

Overall Market: Net Absorption and Vacancy

0%

5%

10%

15%

20%

25%

-4

-2

0

2

4

6

8

MS

F

Net Absorption (MSF) Vacancy Rate

Source: Cassidy Turley Research

Atlanta Industrial Market

24

Overall Market: Net Absorption and Vacancy

0%

4%

8%

12%

16%

-8

-4

0

4

8

12

16

MS

F

Net Absorption (MSF) Vacancy (%)Source: Cassidy Turley Research

Top 20 Industrial Markets

25

Industrial Sector Net Absorption 2011 + 2012, msf

0.00 5.00 10.00 15.00 20.00 25.00

Dayton

Pittsburgh

Denver

Portland, OR

San Antonio

Baltimore

Miami

Los Angeles

Seattle

Charlotte

Detroit

Central NJ

Milwaukee

Houston

Nashville

Indianapolis

Atlanta

Phoenix

Chicago

Dallas 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Source: Cassidy Turley Research

Atlanta: Home Prices Rebounding

-30

-25

-20

-15

-10

-5

0

5

10

15

20

2000

Q1

2001

Q1

2002

Q1

2003

Q1

2004

Q1

2005

Q1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

Home prices, y/y % change

Atlanta, existing sf home price, y/y % change

26

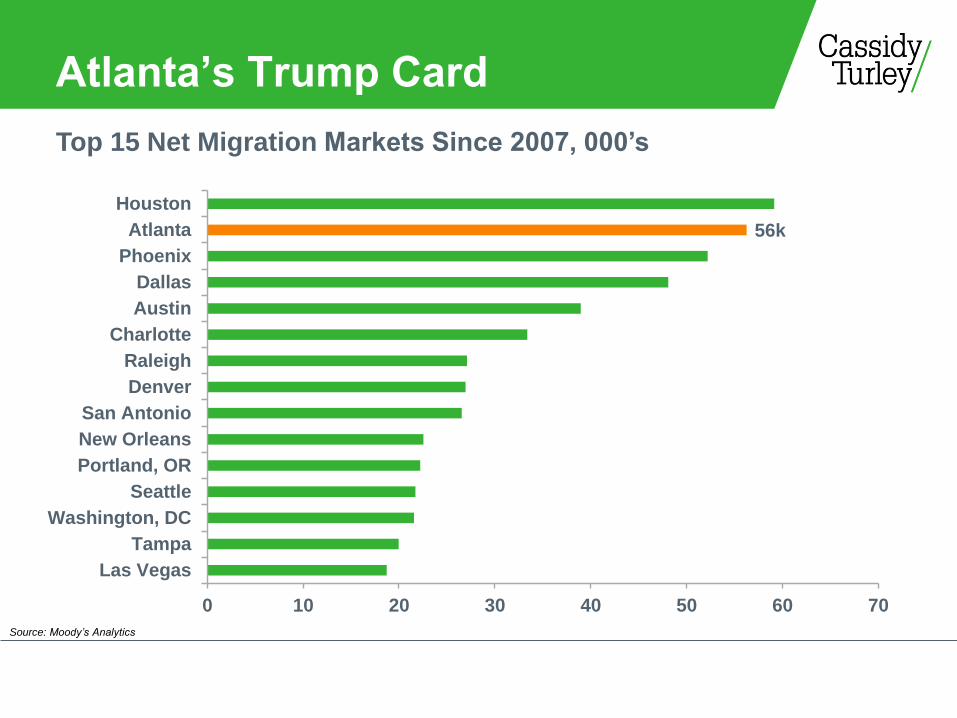

Atlanta’s Trump Card

Top 15 Net Migration Markets Since 2007, 000’s

Source: Moody’s Analytics

56k

0 10 20 30 40 50 60 70

Las Vegas

Tampa

Washington, DC

Seattle

Portland, OR

New Orleans

San Antonio

Denver

Raleigh

Charlotte

Austin

Dallas

Phoenix

Atlanta

Houston

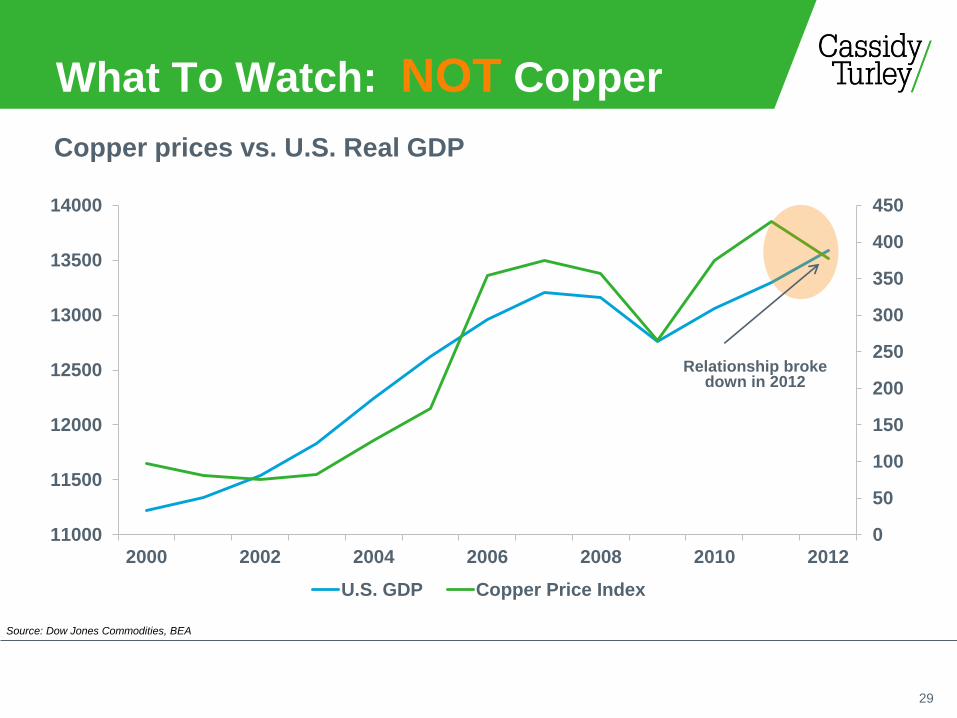

What To Watch

What To Watch: NOT Copper

0

50

100

150

200

250

300

350

400

450

11000

11500

12000

12500

13000

13500

14000

2000 2002 2004 2006 2008 2010 2012

U.S. GDP Copper Price Index

Copper prices vs. U.S. Real GDP

29

Relationship broke down in 2012

Source: Dow Jones Commodities, BEA

What To Watch: Confidence

20

40

60

80

100

120

140

160

80%

82%

84%

86%

88%

90%

92%

94%

200

0Q

1

200

0Q

3

200

1Q

1

200

1Q

3

200

2Q

1

200

2Q

3

200

3Q

1

200

3Q

3

200

4Q

1

200

4Q

3

200

5Q

1

200

5Q

3

200

6Q

1

200

6Q

3

200

7Q

1

200

7Q

3

200

8Q

1

200

8Q

3

200

9Q

1

200

9Q

3

201

0Q

1

201

0Q

3

201

1Q

1

201

1Q

3

201

2Q

1

201

2Q

3

201

3Q

1

Office Occupancy (LHS) CCI

Consumer Confidence vs. Office Occupancy

30

Source: Conference Board, Cassidy Turley

What to Watch: Airline Passengers

31

-20

-15

-10

-5

0

5

10

15

20

-40

-30

-20

-10

0

10

20

30

40

50

19931Q

19943Q

19961Q

19973Q

19991Q

20003Q

20021Q

20033Q

20051Q

20063Q

20081Q

20093Q

2011Q1

2012Q3

Net Absorption, MSF Passenger enplanements, Yr/Yr % Chg.

Source: U.S. Bureau of Transportation Statistics; Cassidy Turley Research

Kevin Thorpe, Chief Economist

March 11th 2013

Economic & Commercial

Real Estate Outlook