Econ 721 lec 1 - UMass Amherstpeople.umass.edu/econ721/Econ_721_lec 1_s_07.pdf · Raghuram G. Rajan...

98

Economics 721 International Finance

Transcript of Econ 721 lec 1 - UMass Amherstpeople.umass.edu/econ721/Econ_721_lec 1_s_07.pdf · Raghuram G. Rajan...

Economics 721

International Finance

Week I

Lecture 1: Introduction

What is financial globalization?

• The increasing importance and even dominance of international financial transactions in the global economy.

• This affects economic growth, stability and equality.

What has been the Impact of Financial Globalization?

• Economic growth• Inequality• Instability• Distribution of power – classes, nations• Trajectory of national economics and

world economy

What are the contradictions and trajectories of this phase of global

capitalist development?

What has been the impact on the ability of national institutions – the state to chart their own courses?

Fred Block:

• Distinction between open and closed economies

Distinction between open and closed

• NOT whether there are international flows of goods or finance, but whether these are dominated by international capitalist markets and institutions, as opposed to national capitalists states or other non-capitalist institutions

Block: Goals of US in post wwIIreconstruction

• To get other countries to adopt “open”economies

• Not just fighting communism but also national capitalist economies in europeand elsewhere

US Capitalists, and economy benefit

• But finance dominated by industry

Eric Helleiner

• Over post-war period, finance makes a come back. Increase financial power over the period.

• Now, many argue that the power of finance supreme (Dumenil and Levy, Crotty)

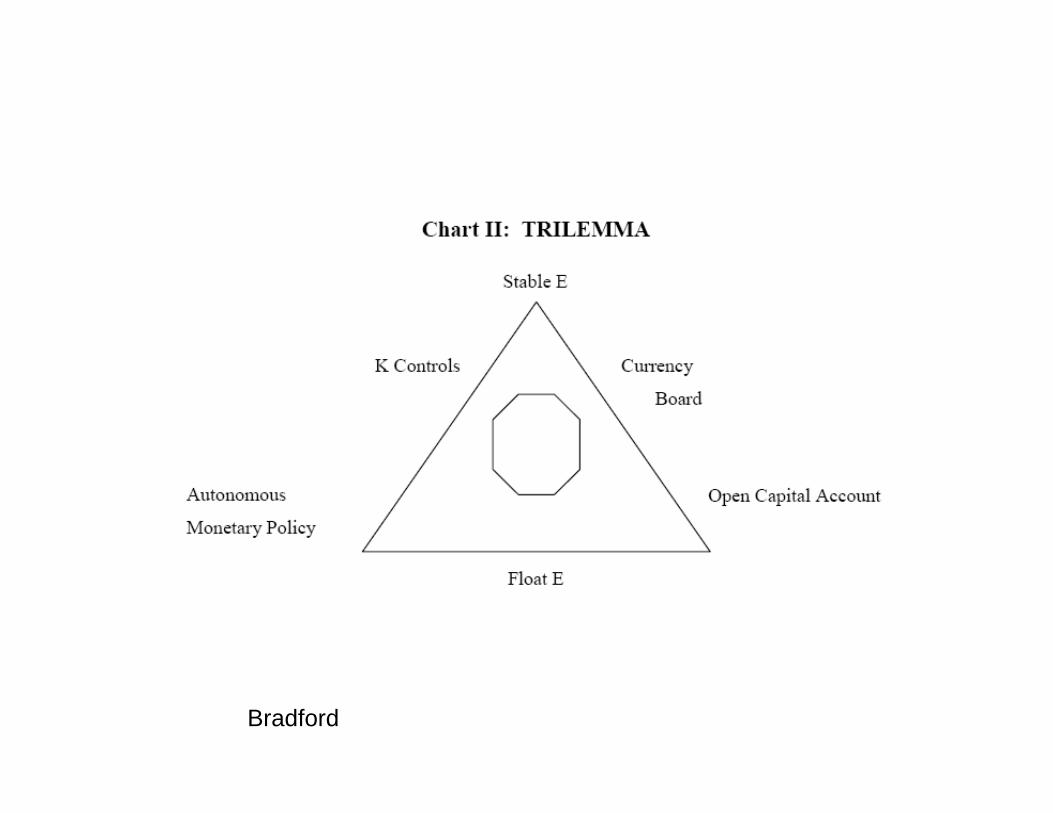

Obstfeld and Taylor

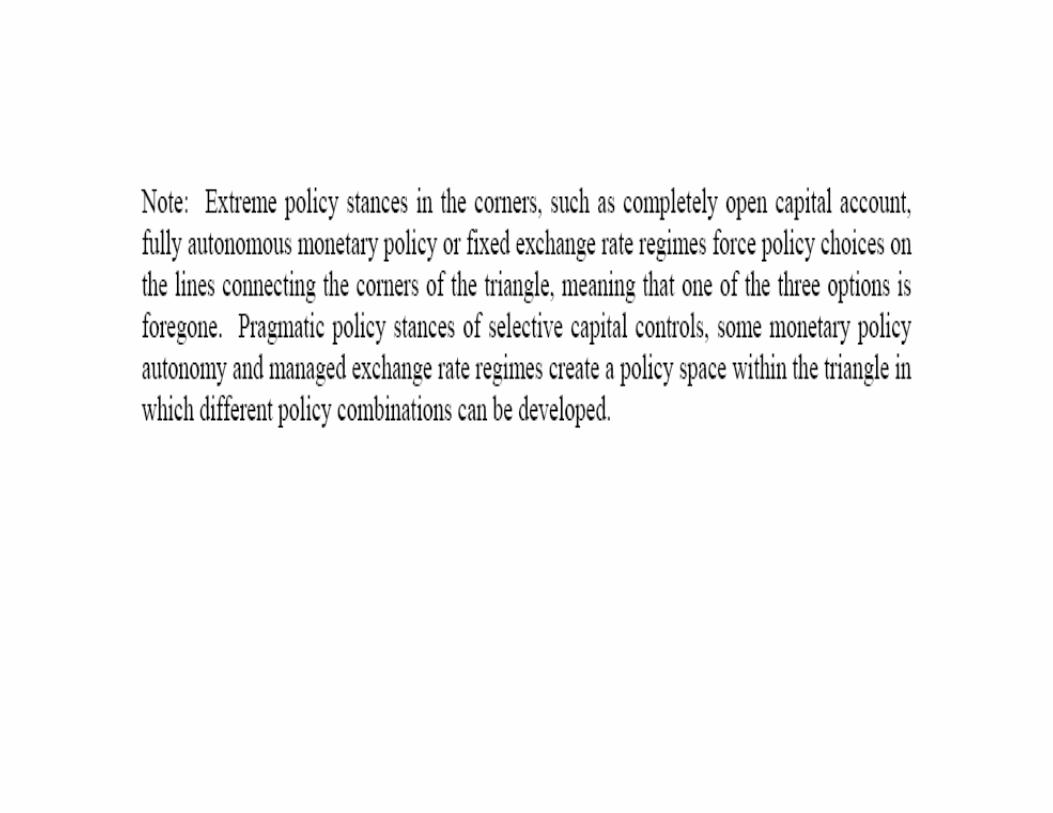

• Organize their history by idea of “trilemma”in international economy.

Bradford

Questions about Trilemma

• How do governments choose where on triangle to be?

• What are the role of class forces and coalitions?

• What is the role of underlying productive structre?

Questions about Trilemma

• What are the impacts of different choices in terms of income distribution, economic growth, class power?

• Where do IMF/World Bank push countries to be and why?

• Domestic capitalists? What are their interests?

Capital Mobility and Financialization

• Finance push for financial liberalization and capital mobility

• What are impacts?

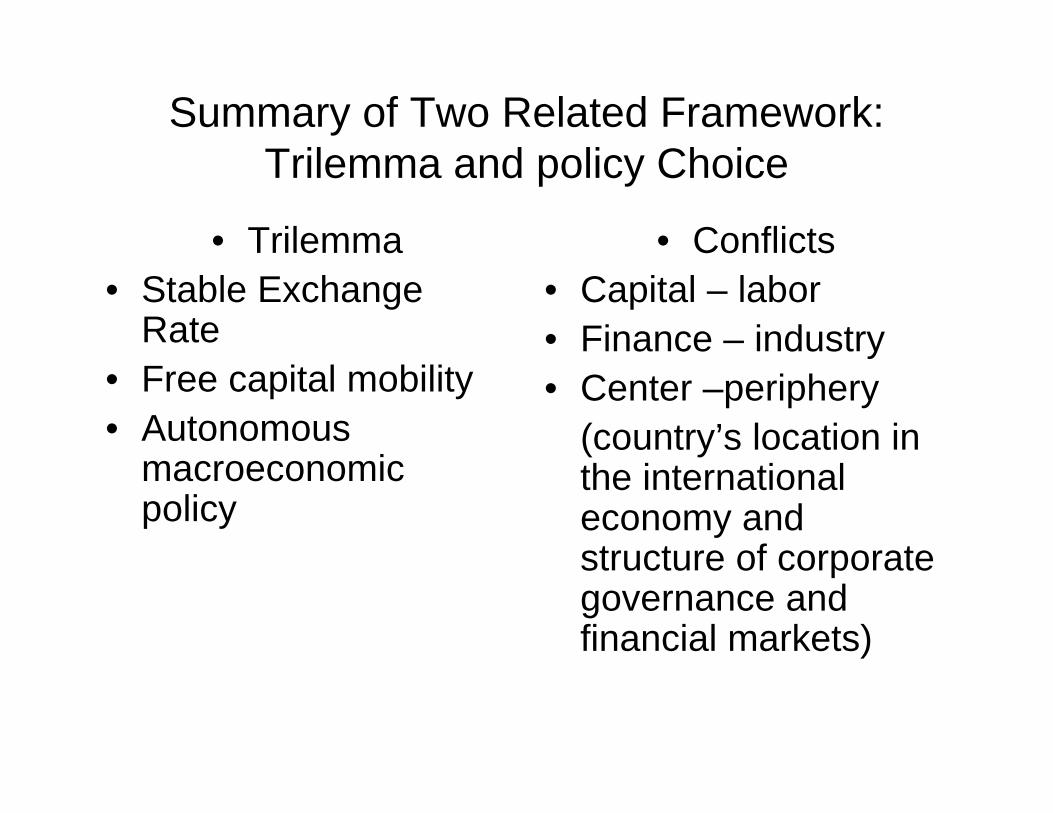

Summary of Two Related Framework: Trilemma and policy Choice

• Trilemma• Stable Exchange

Rate• Free capital mobility• Autonomous

macroeconomic policy

• Conflicts• Capital – labor• Finance – industry• Center –periphery

(country’s location in the international economy and structure of corporate governance and financial markets)

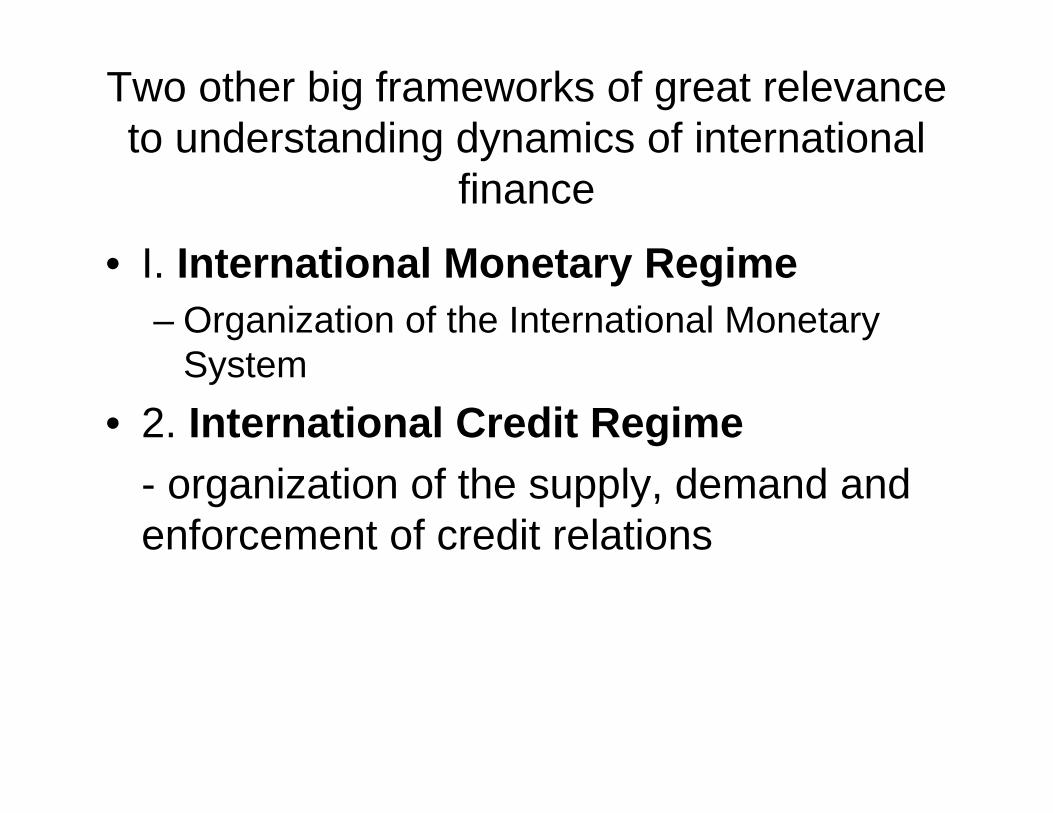

Two other big frameworks of great relevance to understanding dynamics of international

finance

• I. International Monetary Regime– Organization of the International Monetary

System• 2. International Credit Regime

- organization of the supply, demand and enforcement of credit relations

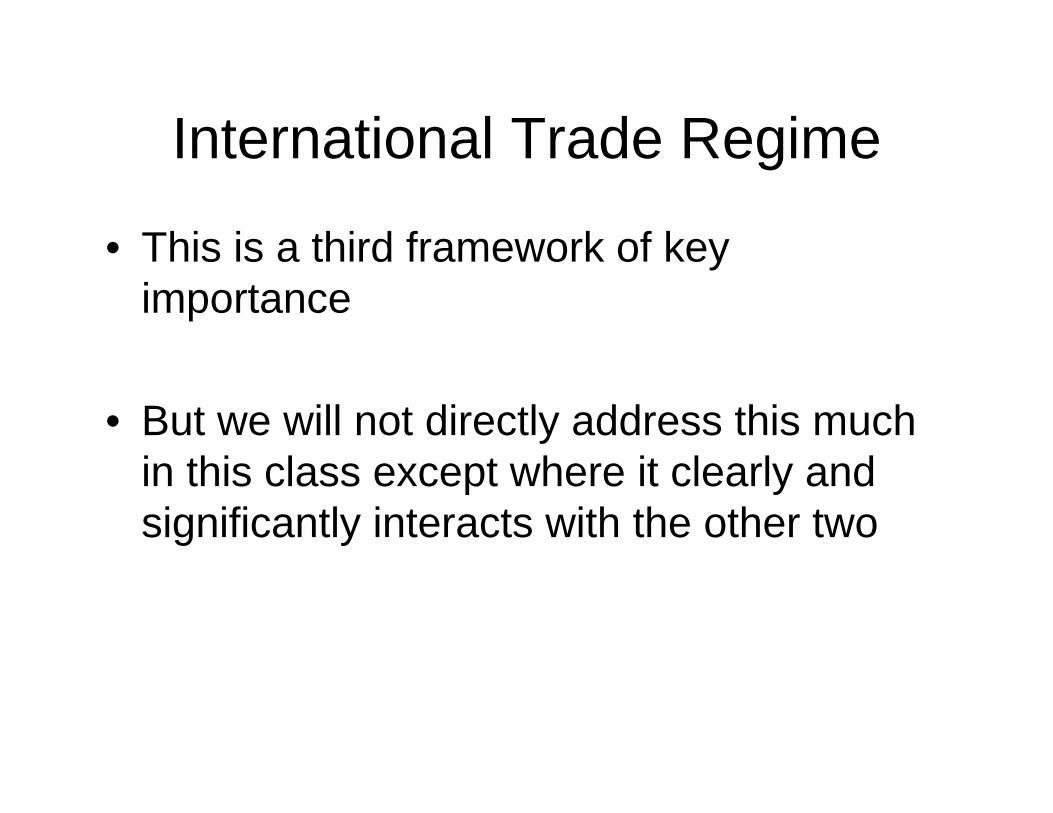

International Trade Regime

• This is a third framework of key importance

• But we will not directly address this much in this class except where it clearly and significantly interacts with the other two

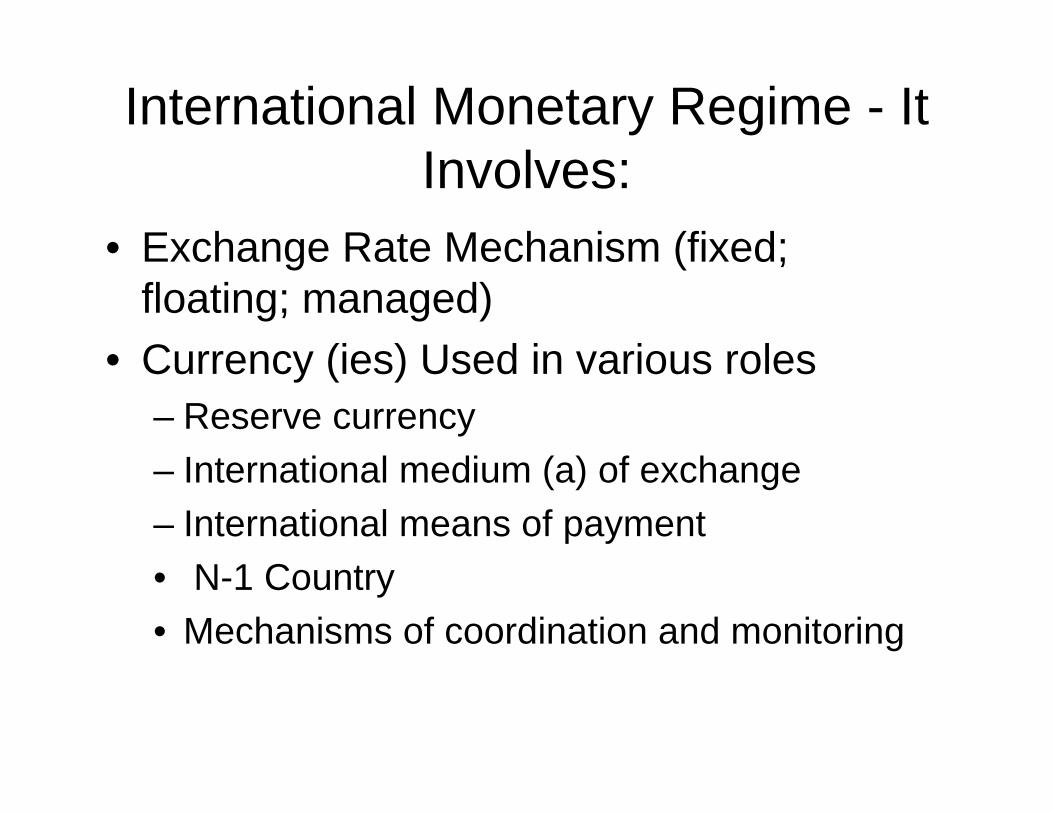

International Monetary Regime - It Involves:

• Exchange Rate Mechanism (fixed; floating; managed)

• Currency (ies) Used in various roles– Reserve currency– International medium (a) of exchange– International means of payment• N-1 Country• Mechanisms of coordination and monitoring

Which Countries can issue hard currencies

• Key divide in global economy (medium of exchange, and means of payment –dollars; pesos ?)

Key Currencies

• Store of value (reserves)• Medium of exchange (vehicle currency)• Intervention currency (intervene in foreign

exchange markets)• Means of payment (service debts)

International Monetary Systems

See next slide

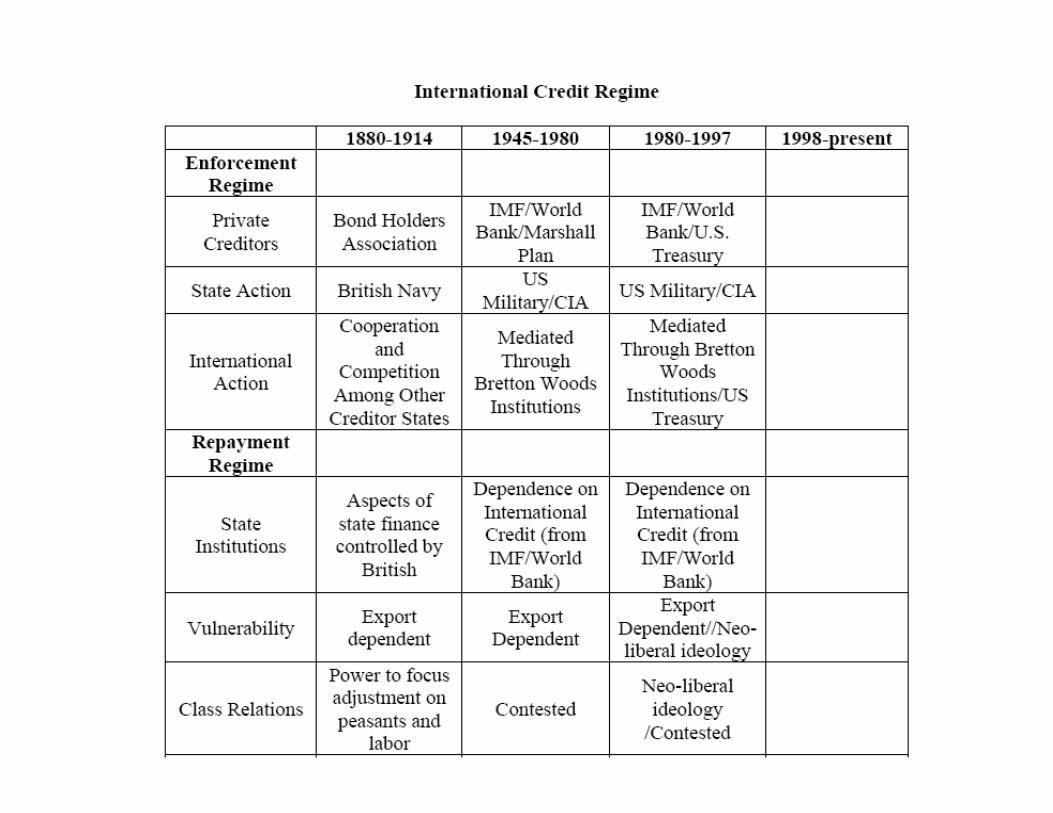

International Credit Regime: Has Two Components Operating in Tandem

• Enforcement Regime: The institutions and policies implemented by creditors to punish non-payment and reward payment

• Repayment Regime: the institutions and policies implemented by debtors to credibly signal that they will repay

International Credit Regime has a Third Component Working in Tension with the

Other Two

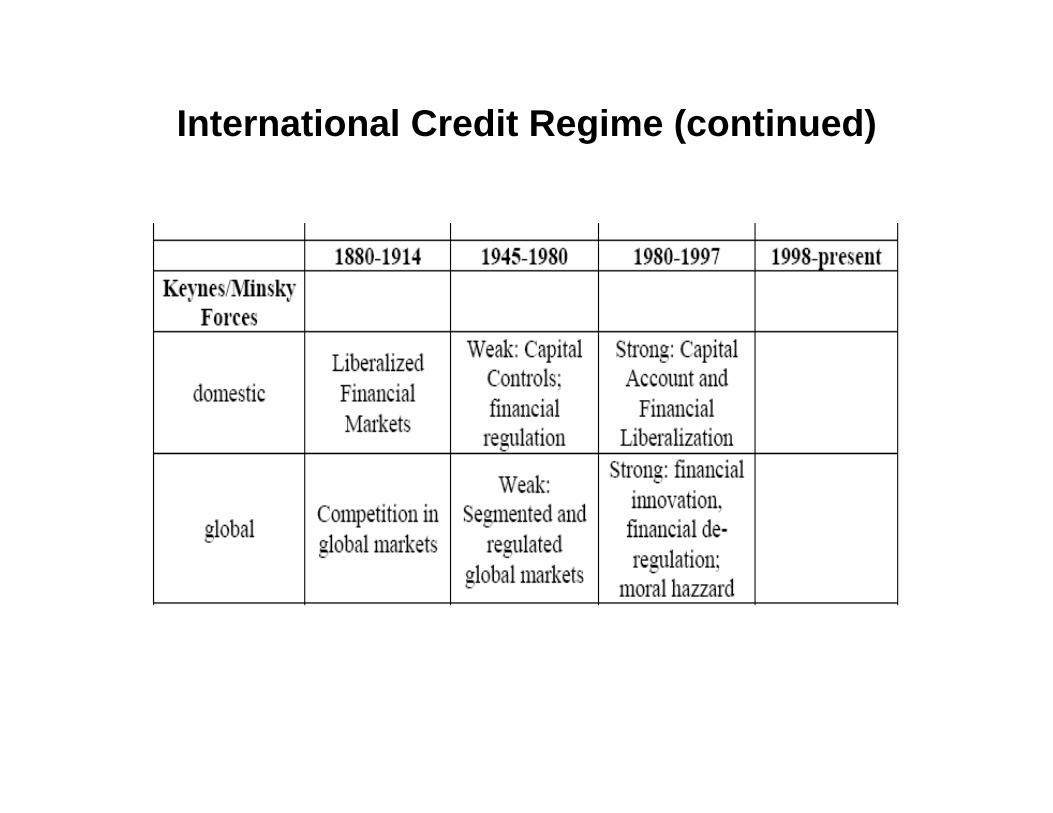

• The Keynesian/Mynskian Imperative:Competition, behavioral aspects, and fundamental uncertainty: Excessive lending and bubbles

Enforcement Regime in Tension and Contradiction

• Enforcement Regime• Repayment Regime• Keynsian/Minskian Imperatives

Current Aspects of International Credit Regime

International Credit Regime (continued)

Implicit in These are Different Theories/Models of International

Capital Markets

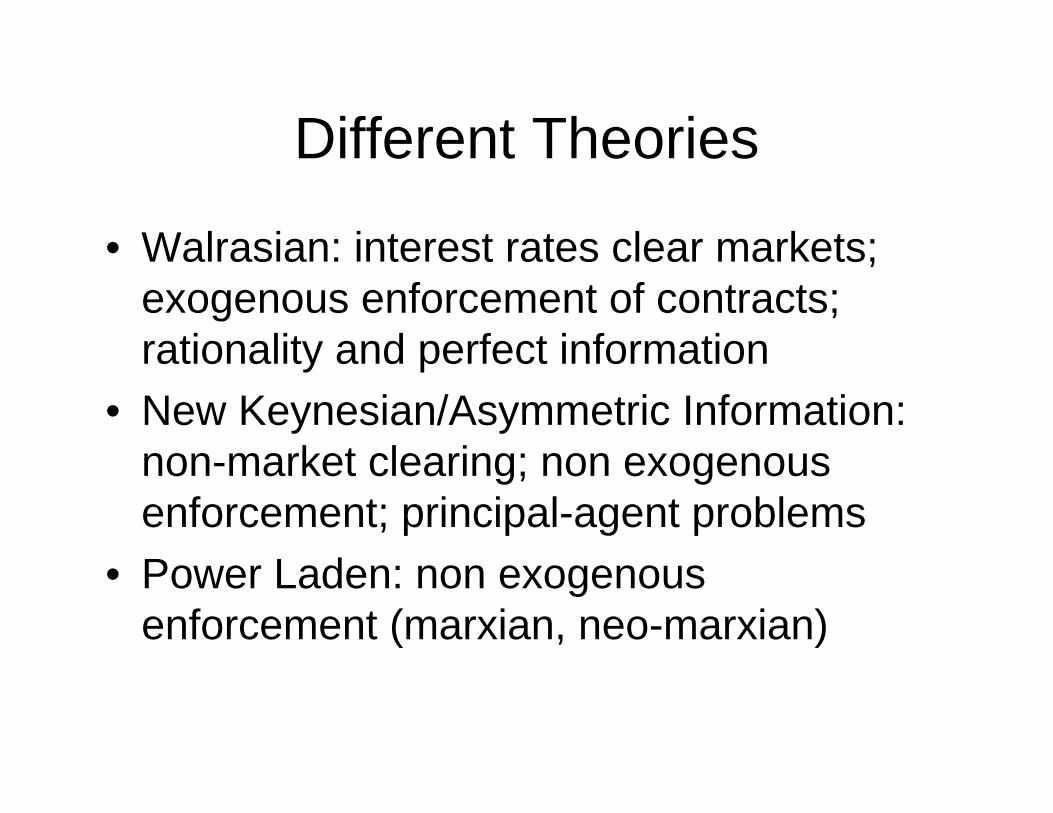

Different Theories

• Walrasian: interest rates clear markets; exogenous enforcement of contracts; rationality and perfect information

• New Keynesian/Asymmetric Information: non-market clearing; non exogenous enforcement; principal-agent problems

• Power Laden: non exogenous enforcement (marxian, neo-marxian)

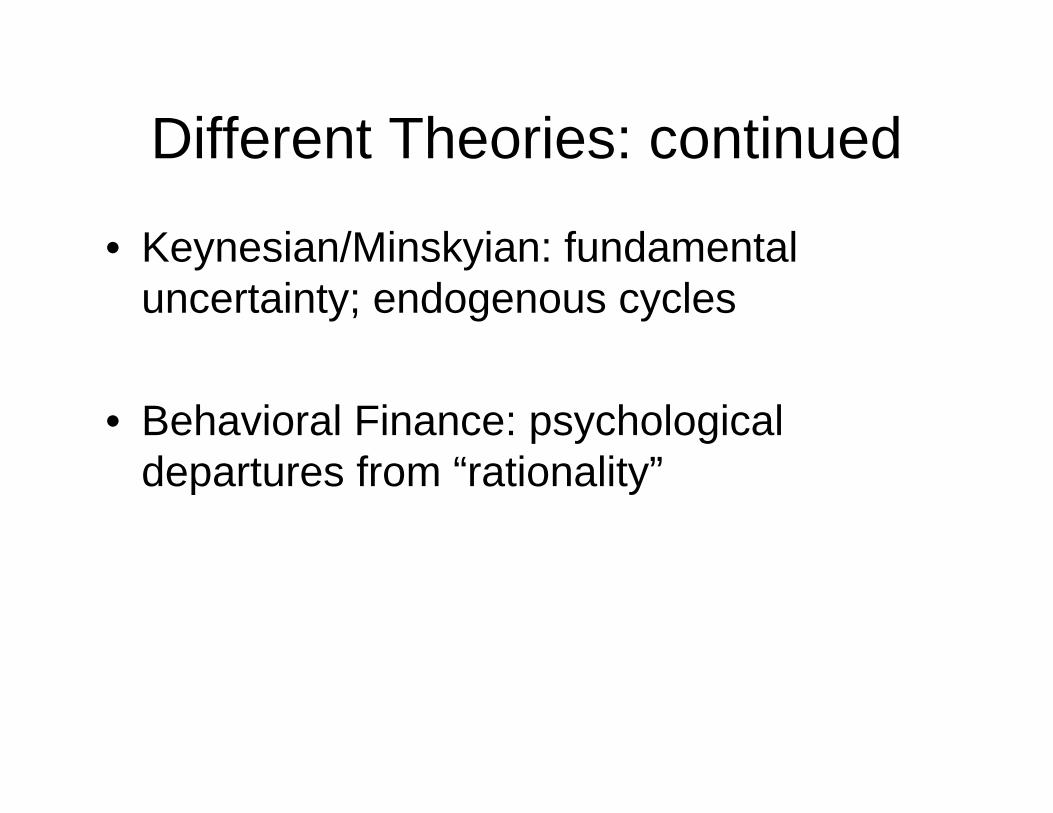

Different Theories: continued

• Keynesian/Minskyian: fundamental uncertainty; endogenous cycles

• Behavioral Finance: psychological departures from “rationality”

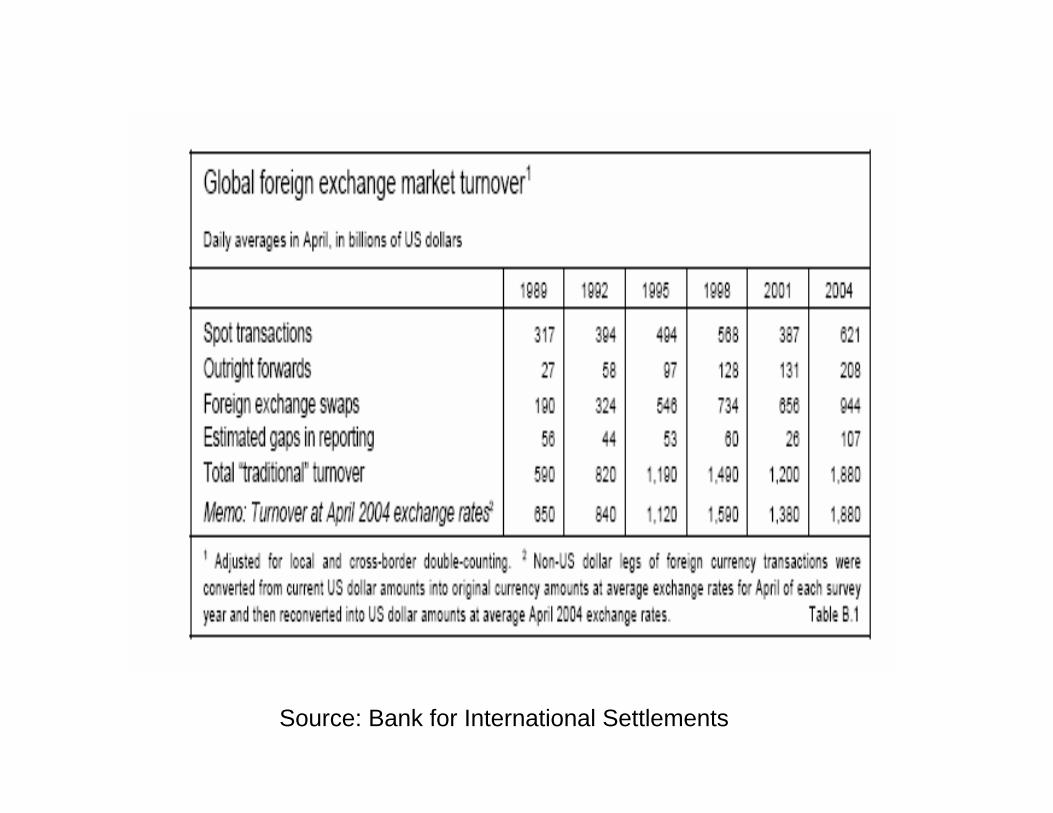

Survey of Some Current Financial Markets/Institutions

Current value of Daily Forex trading

• 1.9 trillion dollars daily

Source: Bank for International Settlements

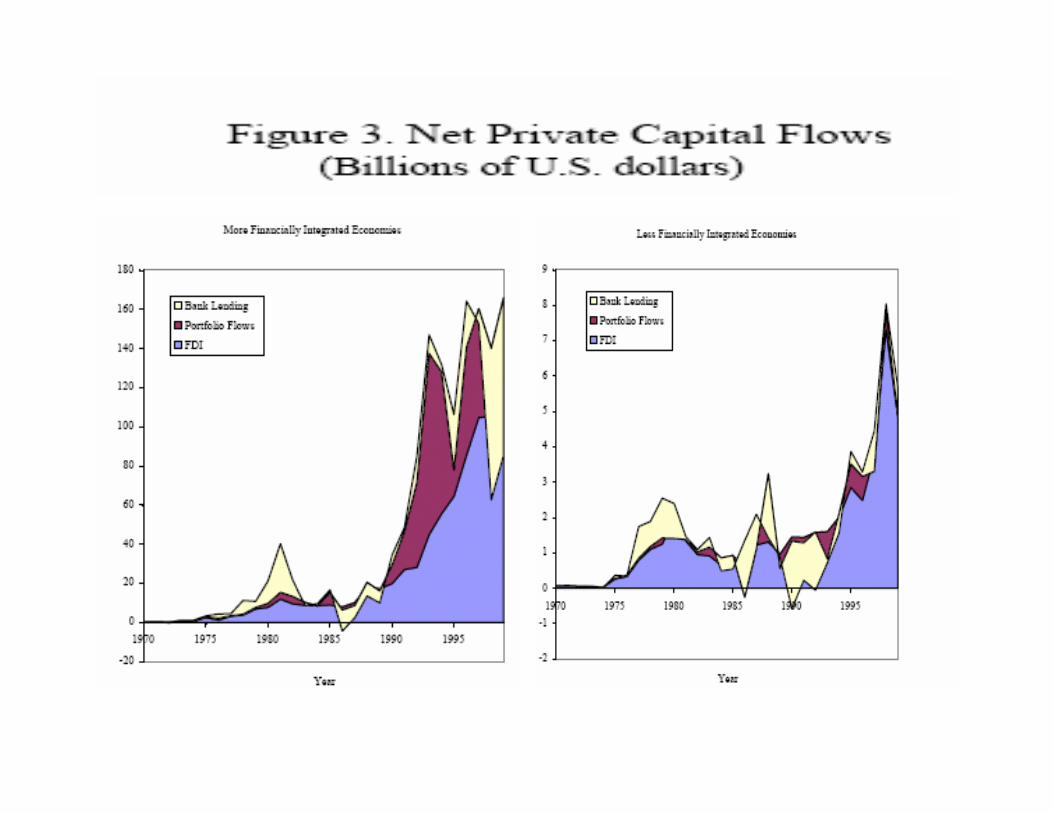

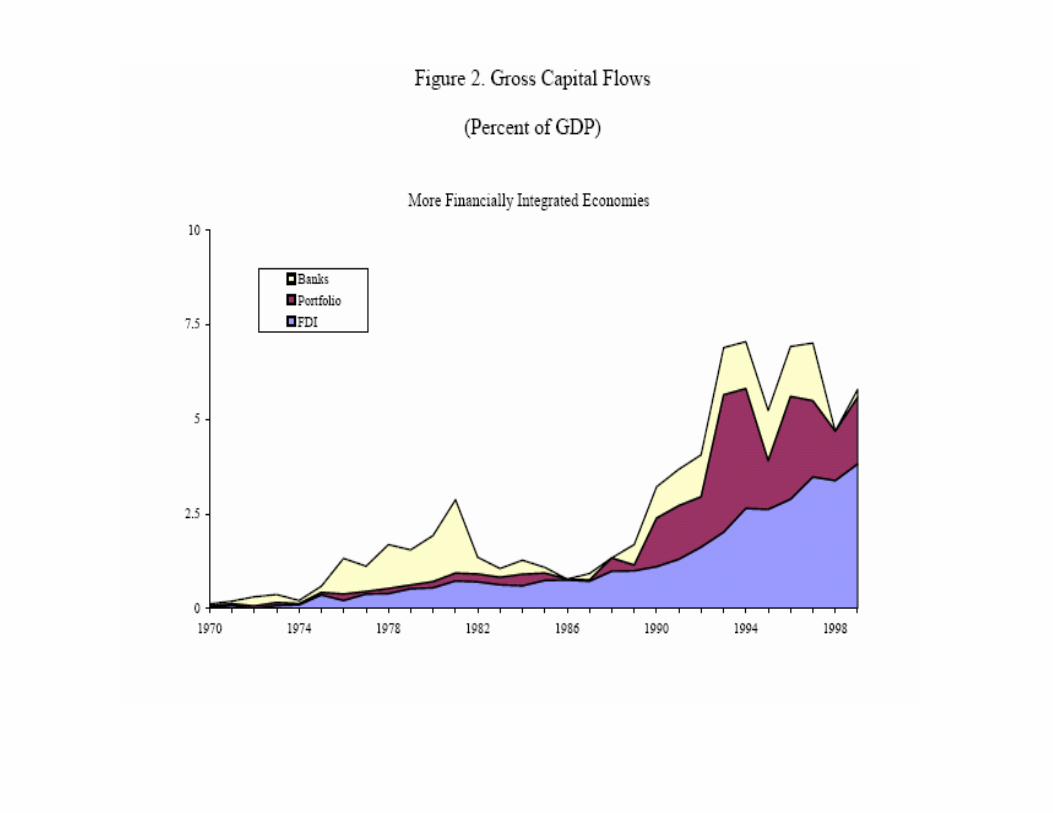

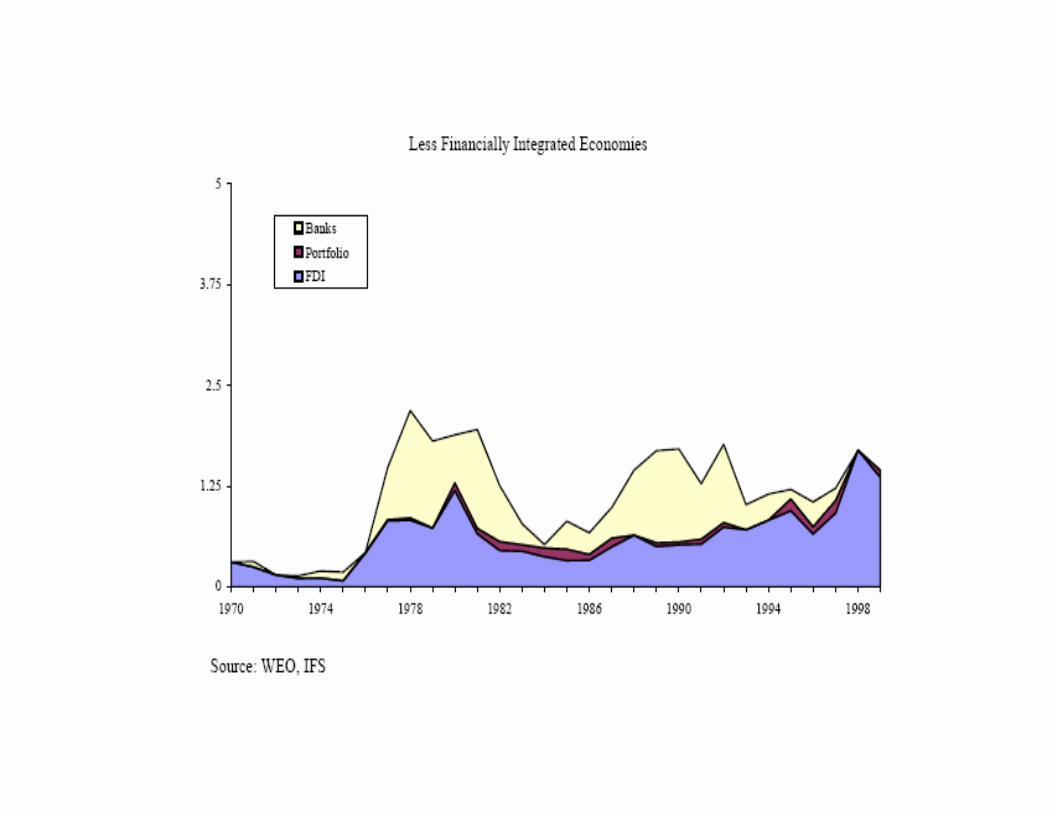

Types of financial flows:

• Debt-portfolio-banksEquity-portfolio-FDIDerivatives and other exotic transactions

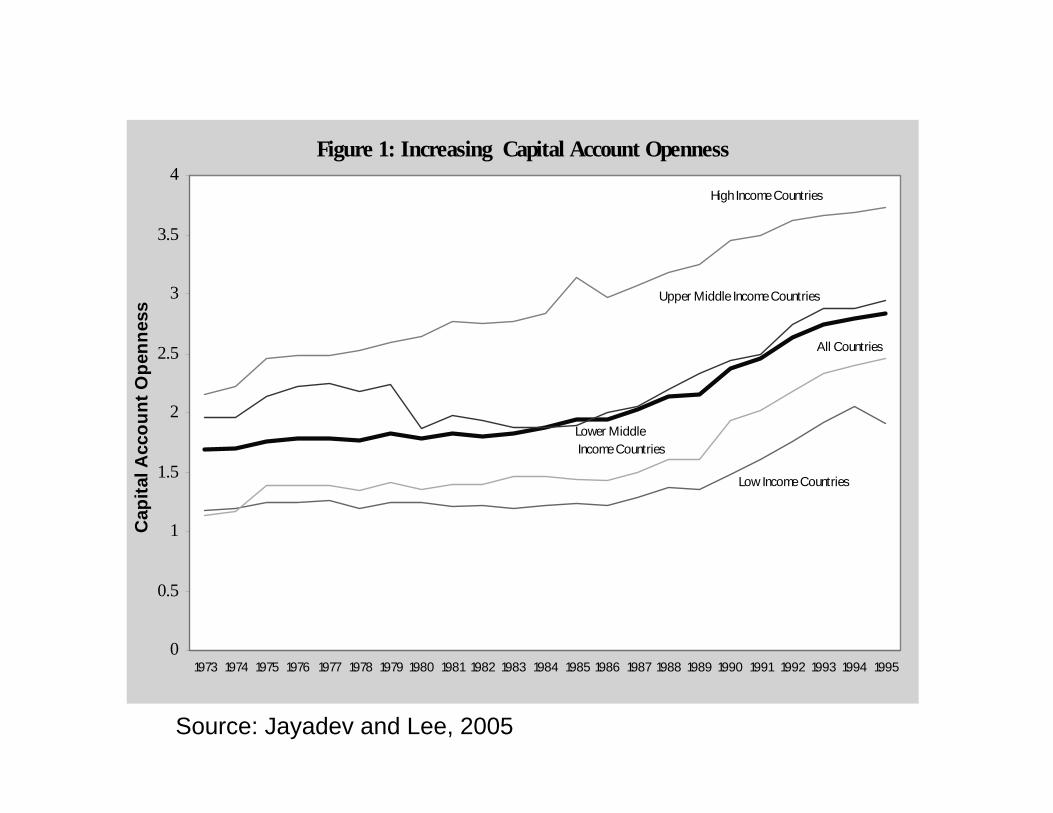

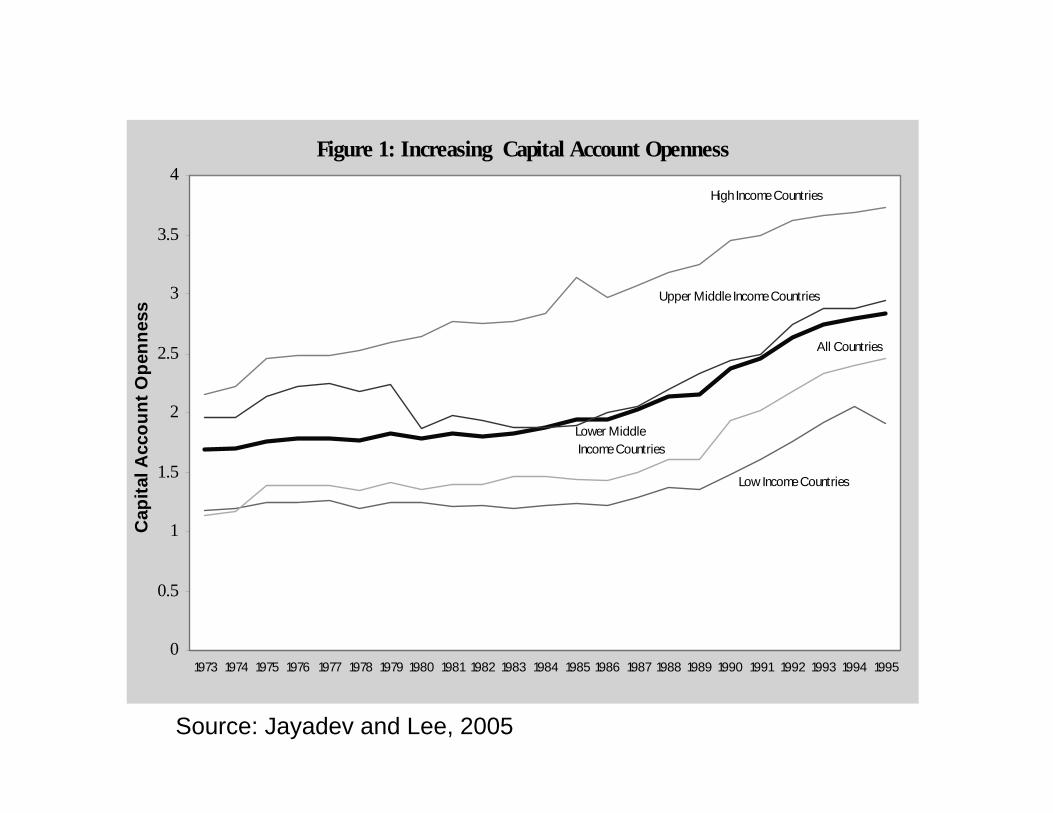

Figure 1: Increasing Capital Account Openness

0

0.5

1

1.5

2

2.5

3

3.5

4

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995

Cap

ital A

ccou

nt O

penn

ess

High Income Countries

Upper Middle Income Countries

All Countries

Lower Middle Income Countries

Low Income Countries

Source: Jayadev and Lee, 2005

This Surge in Trading and Flows

• Relatively new

• During 1930’s, WWII, and early post-war period, tight regulations over forex trading and capital flows.

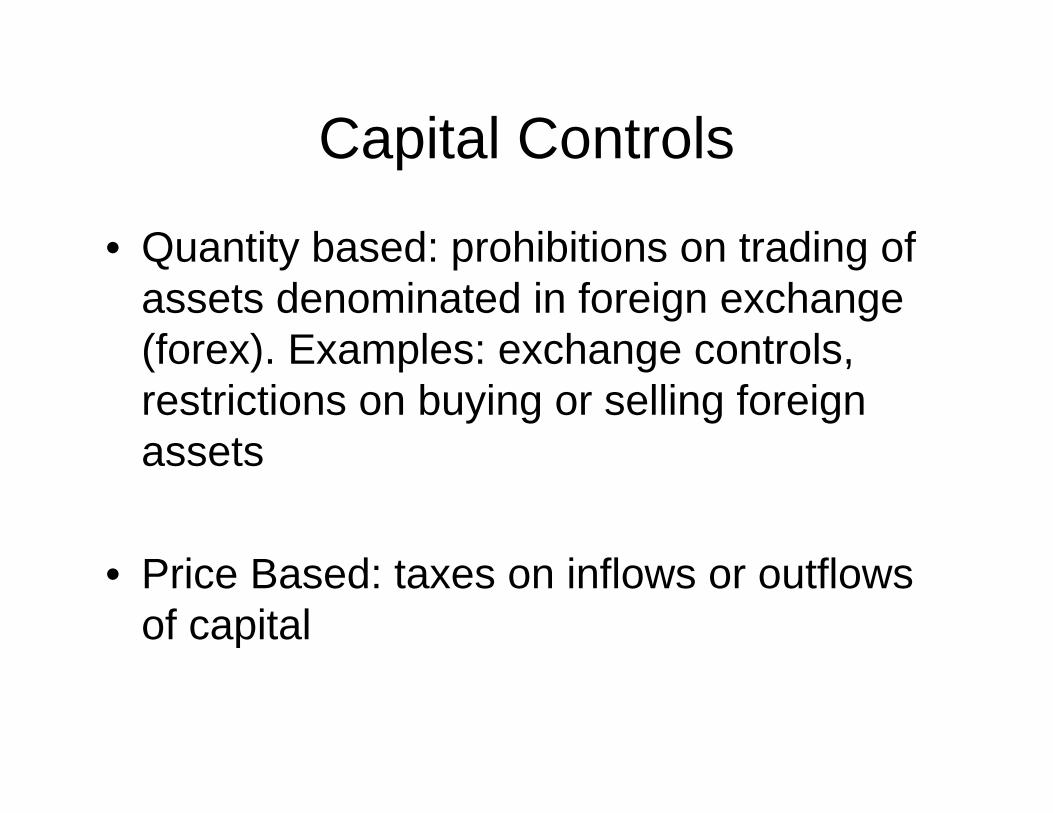

Capital Controls

• Quantity based: prohibitions on trading of assets denominated in foreign exchange (forex). Examples: exchange controls, restrictions on buying or selling foreign assets

• Price Based: taxes on inflows or outflows of capital

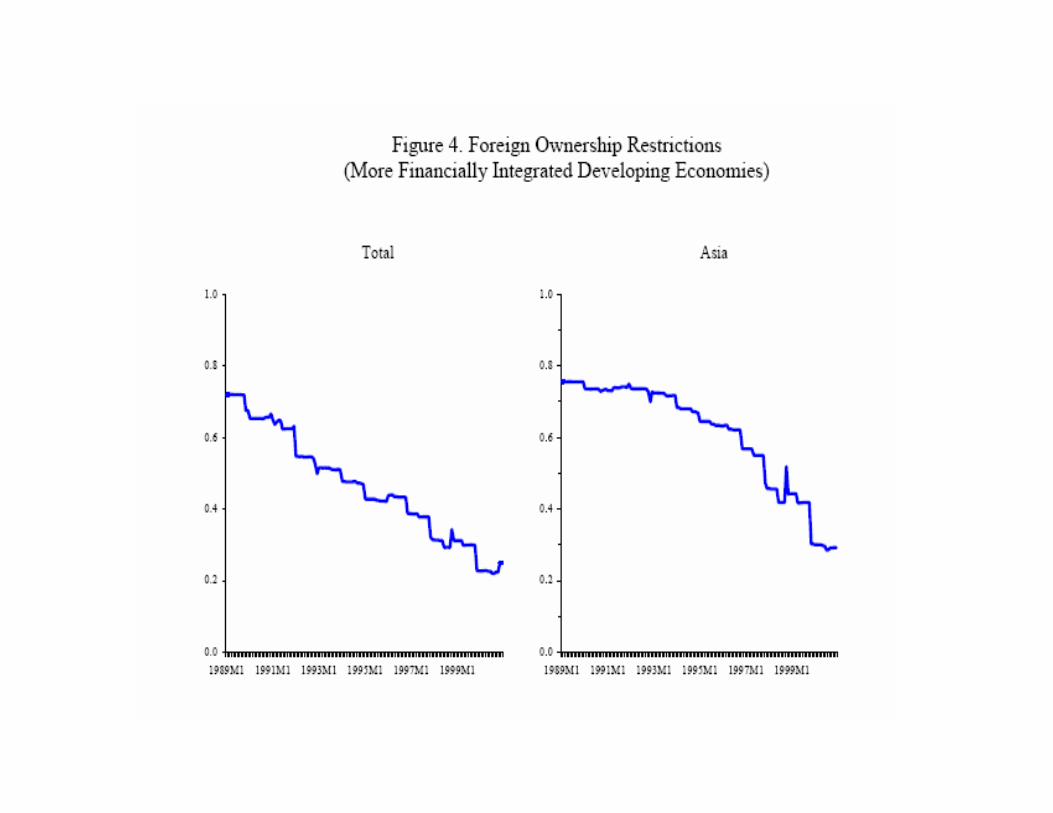

Distinction Between De-jure and De-facto financial liberalization

• De-jure: legal restrictions (or the absence there-of)

• De-facto: quantity of flows

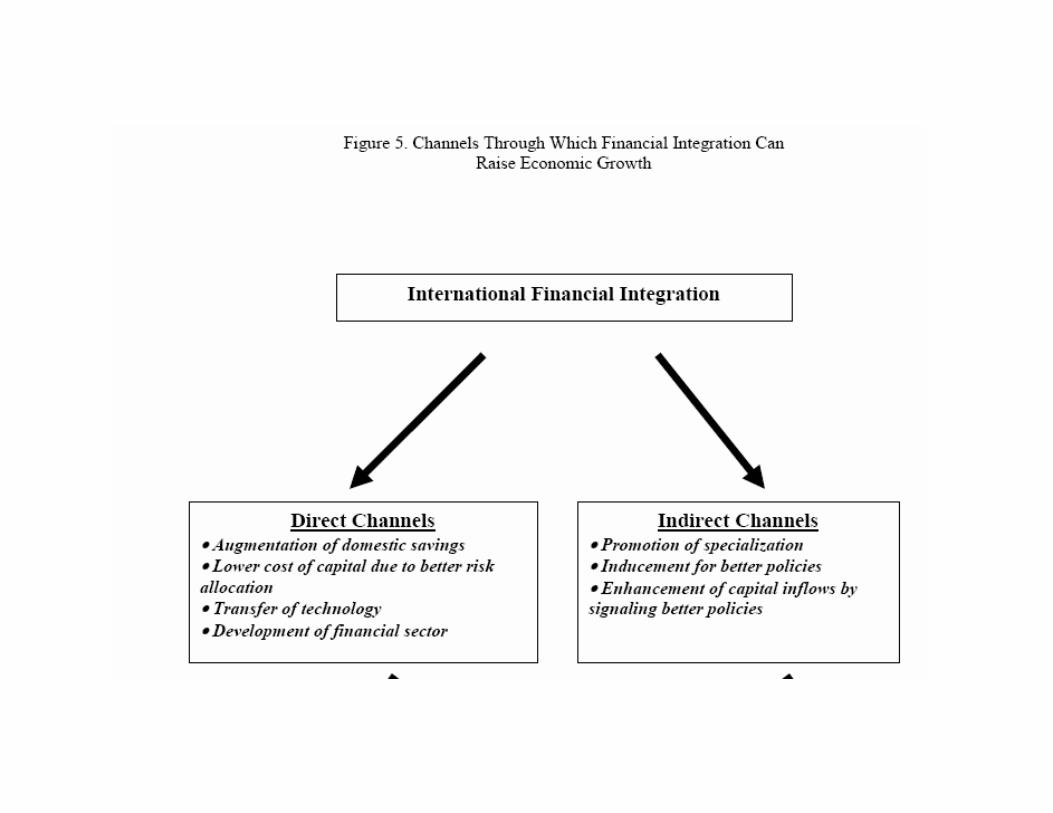

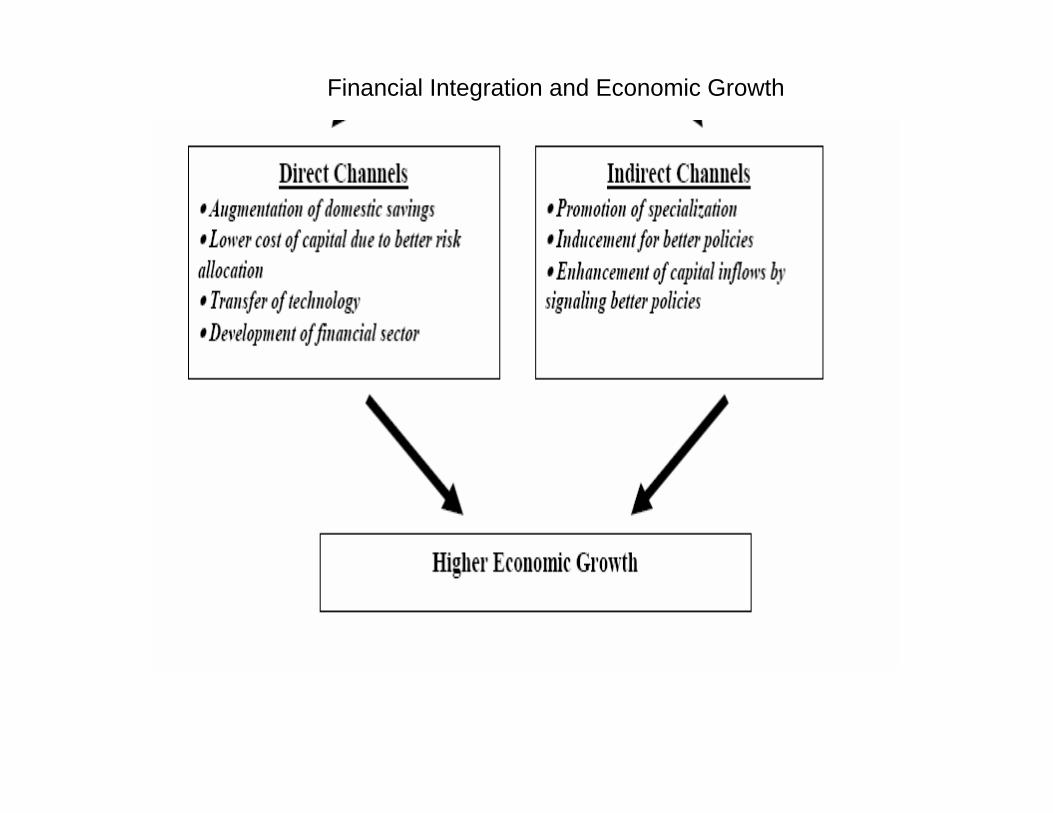

Financial Integration and Economic Growth

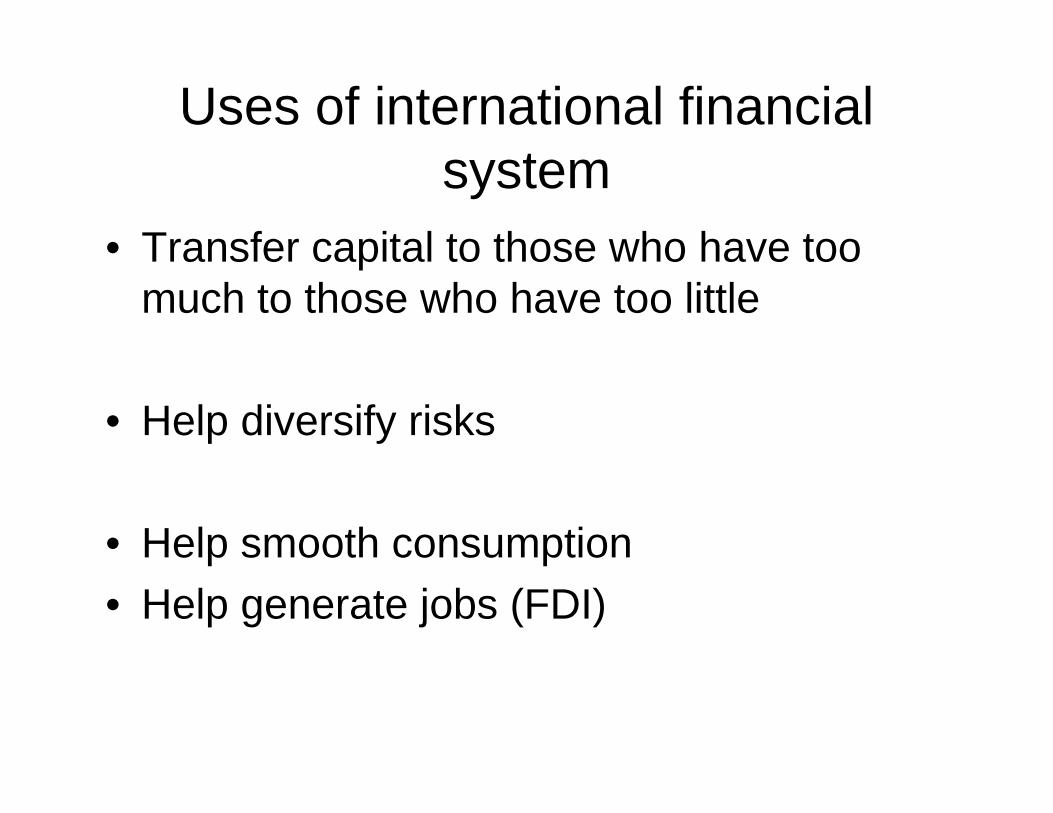

Uses of international financial system

• Transfer capital to those who have too much to those who have too little

• Help diversify risks

• Help smooth consumption• Help generate jobs (FDI)

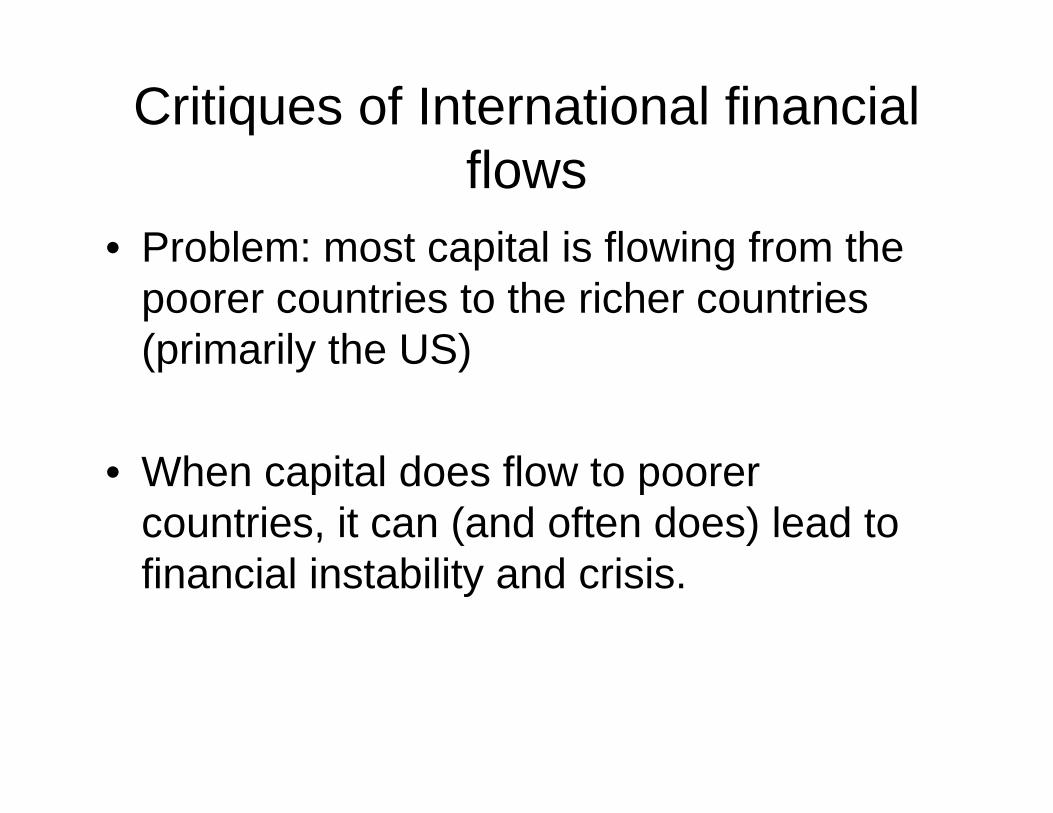

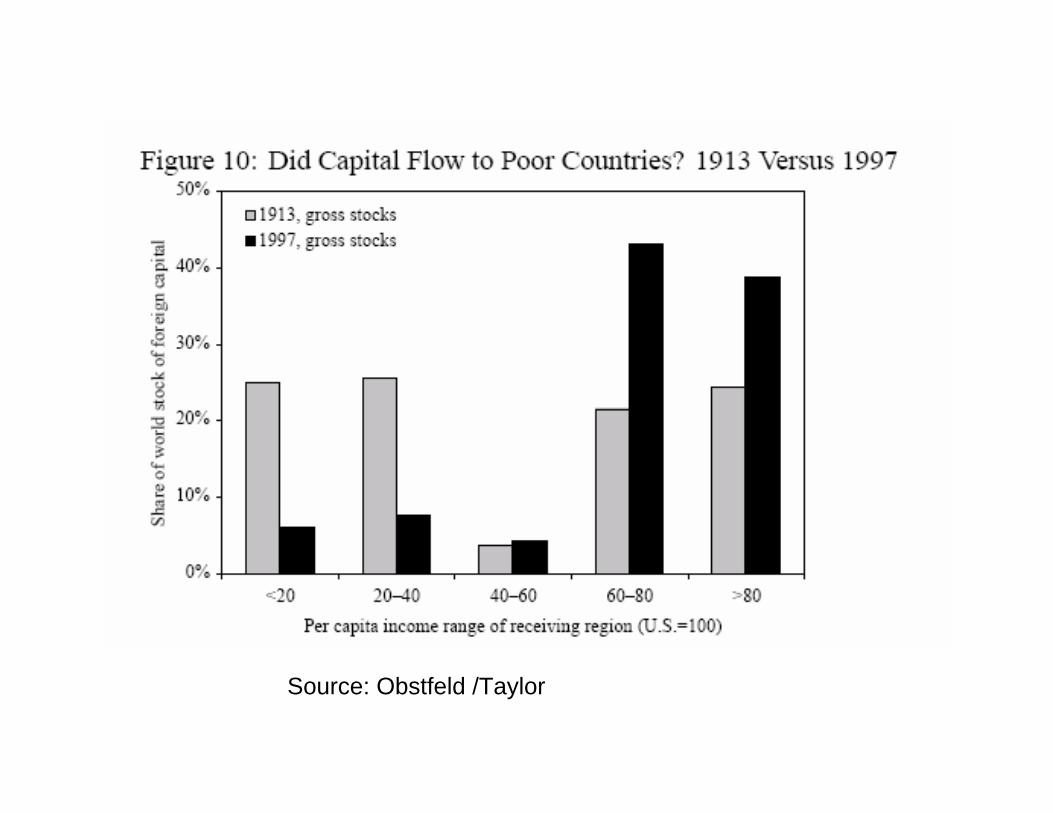

Critiques of International financial flows

• Problem: most capital is flowing from the poorer countries to the richer countries (primarily the US)

• When capital does flow to poorer countries, it can (and often does) lead to financial instability and crisis.

Source: Obstfeld /Taylor

Bretton Woods Institutions (BWI’s)

• IMF• World Bank

• Formed in 1944, Bretton Woods Conference

Original Functions

• IMF, to help stabilize the international financial system and to help avoid the “deflationary bias” of the world Economy in the 1930’s

World Bank

• Medium to longer term lending for reconstruction after war and for developing countries

IMF

• Became more and more involved in longer term lending

• “structural adjustment”

• Interfering in operations of domestic economies

Pushed International financial Liberalization

Internal: free up domestic financial markets

External: reduce capital controls

“Washington Consensus”

• Financial Liberalization• Privatization• Trade Liberalization• Cut Budget Deficits

Washington Consensus

• Export led growth and free markets• Making countries attractive for

international investment

• These are the keys to economic growth

Prabhat Patnaik

• Illusionism of Finance

3 defining moments

• Third World Debt Crisis, 1982

• Asian Financial Crisis, 1997

• 9/11 – Iraq and the Election of “progressive” leaders in Latin America, opposed to Washington consensus

Figure 1: Increasing Capital Account Openness

0

0.5

1

1.5

2

2.5

3

3.5

4

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995

Cap

ital A

ccou

nt O

penn

ess

High Income Countries

Upper Middle Income Countries

All Countries

Lower Middle Income Countries

Low Income Countries

Source: Jayadev and Lee, 2005

International Financial Crises

• Third World Debt Crisis of 1982; defining moment in world economy

Third World Debt Crisis

• Background• Impacts• Led to neo-liberal globalization• Increasing role of IMF and structural

adjustment• Neo-liberalism and Washington

Consensus

Asian Financial Crisis

• 2nd defining moment

• What went wrong with neo-liberalism?

International Financial Crises

• Third World Debt Crisis of 1982; defining moment in world economy

• Asian Financial Crisis of the 1990’s

Third World Debt Crisis

• Background• Impacts• Led to neo-liberal globalization• Increasing role of IMF and structural

adjustment• Neo-liberalism and Washington

Consensus

Are capital flows volatile

• Pro-cyclical• Sudden stops

What happens when capital flows and then sudden stops

• Individuals, companies and governments build up debts

• Debts denominated in foreign currencies• Rely on future flows to service past flows

Debt Service

• Debt Service =interest payments plus amortization (repaying debt)

If debts in foreign currency

• When forex stops flowing in, creates problem

• If raise interest rates, problem worse• If exchange rate falls, problem becomes

worse –debts denominated in foreign currency becomes greater in domestic currency

Effect of depreciation on value of debt

• Exchange rate: 1 peso = 1dollar

• 100 dollars debt = 100 pesos debt• Exchange rate devalues (depreciates): 2

pesos = 1 dollar

• Now the country has 200 pesos worth of debt!!

Such depreciations can lead to bankruptcies

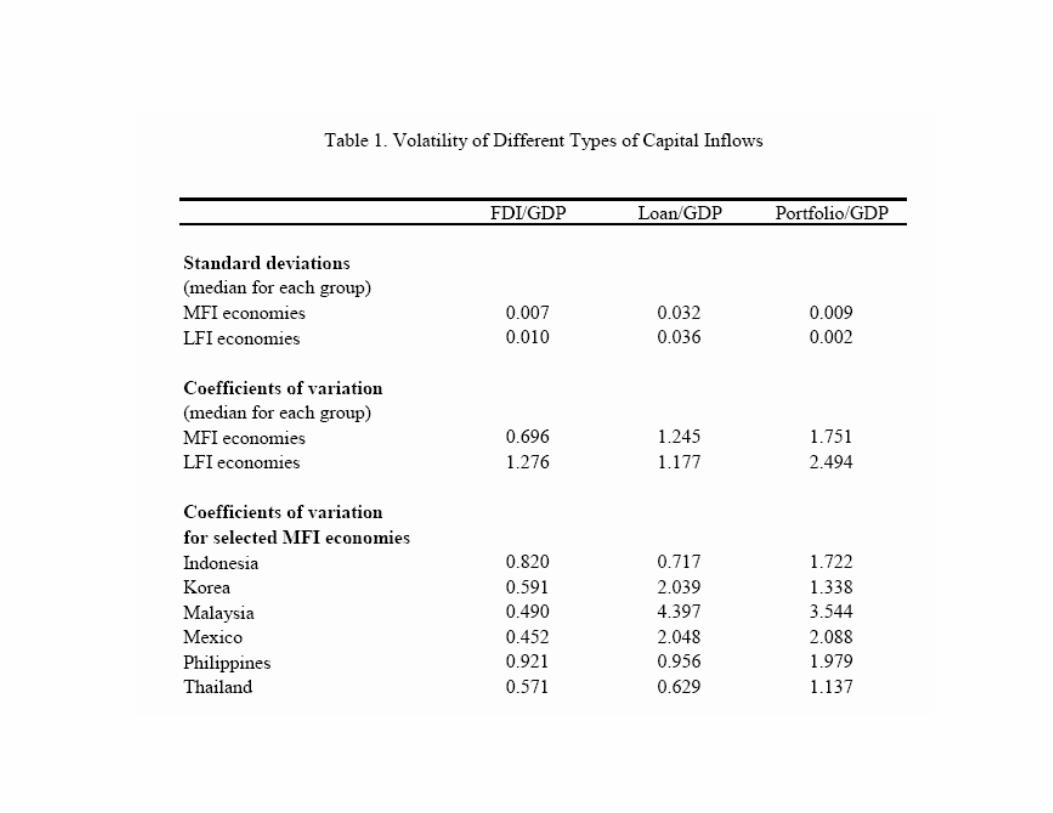

Volatility of Different Capital Flows

FDI, Investment of Choice?

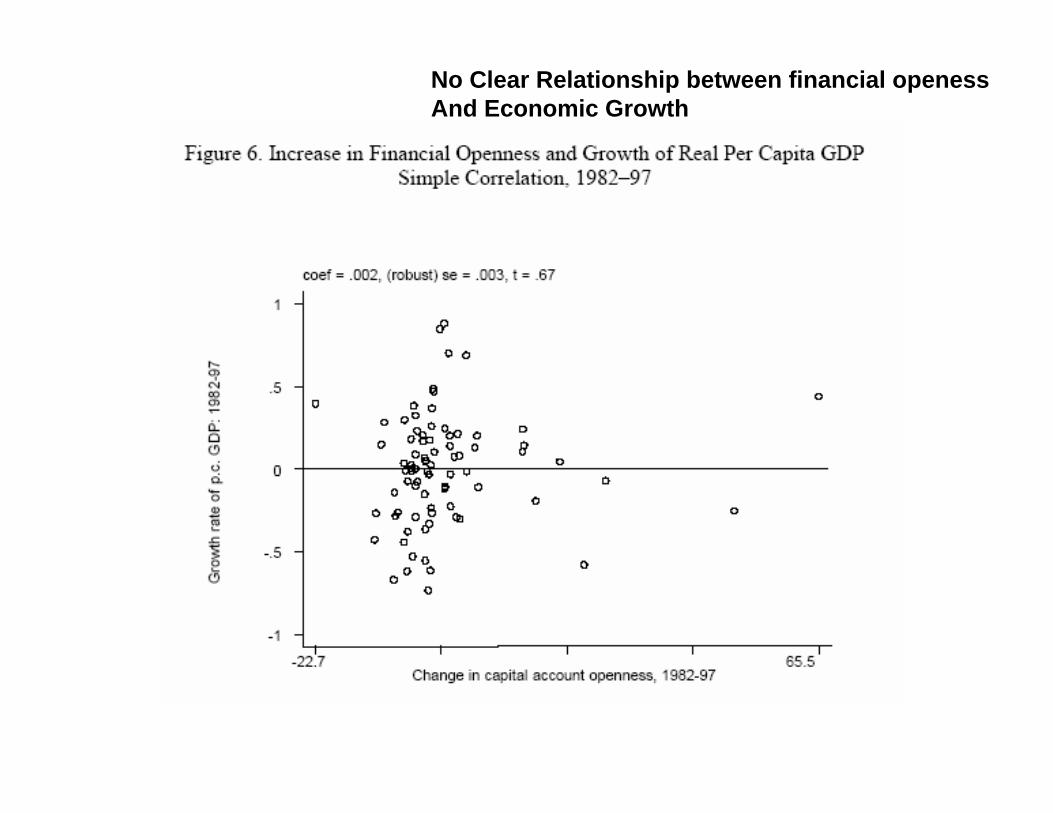

Does more capital flows increase economic growth?

No Clear Relationship between financial openessAnd Economic Growth

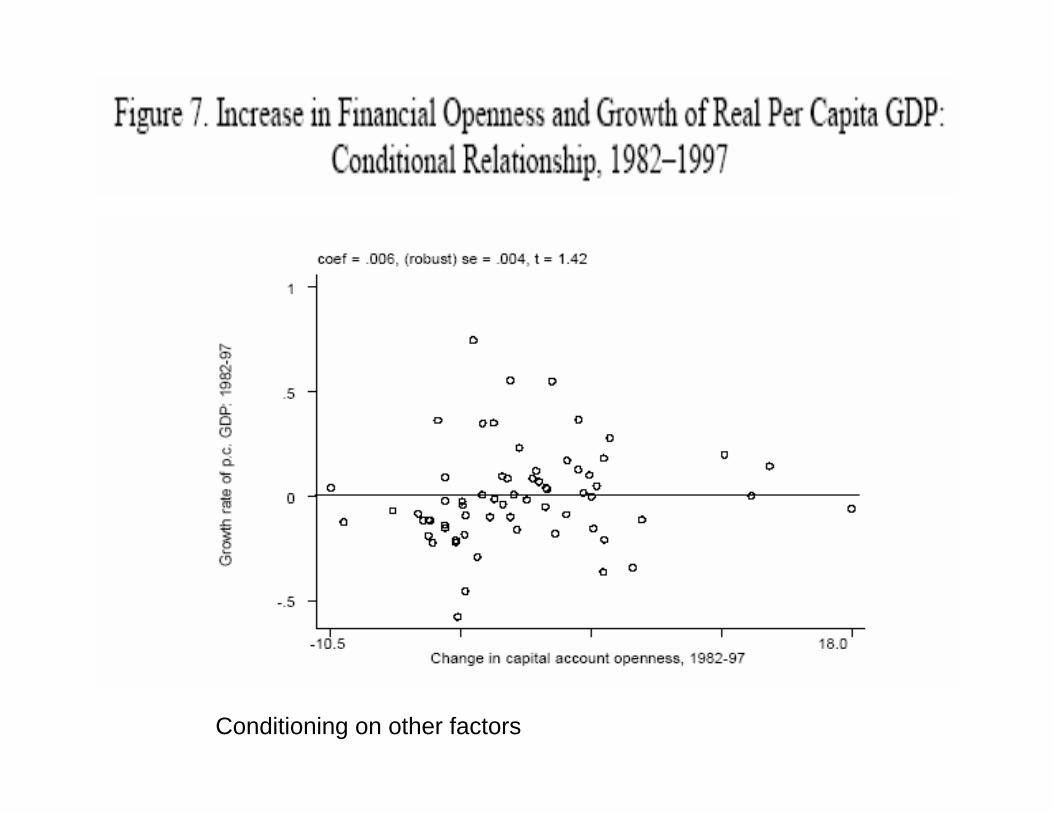

Conditioning on other factors

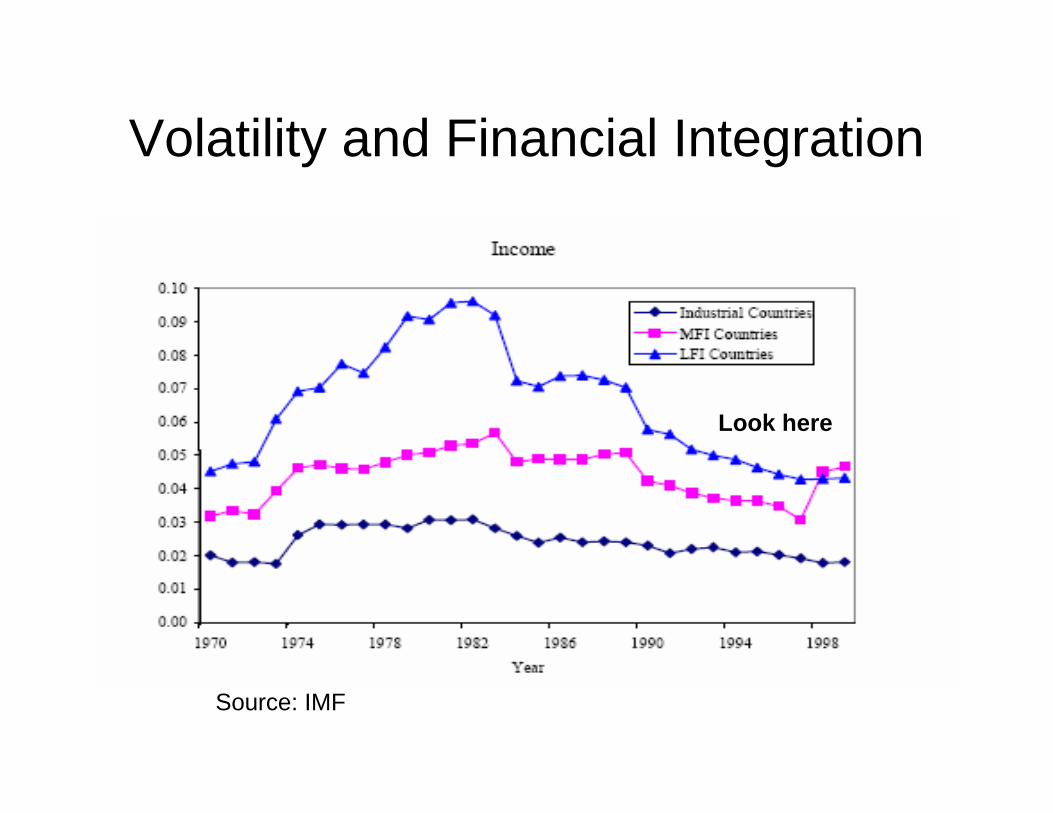

Volatility and Financial Integration

Source: IMF

Look here

Source: IMF

Differences between trade in Goods and in Financial Assets

• Financial Assets are bets on the future; trade is production in the present

• Trade is based on newly produced goods—generates jobs.

• Finance ---already produced assets.• Creation of a financial asset necessarily

creates a debt.

A trade-off between Finance and Trade?

Scepticism about Washington Consensus

• Post-Washington Consensus• More Policy space• Not all one size fits all• Capital controls?

Scepticism about Washington Consensus

• Post-Washington Consensus• More Policy space• Not all one size fits all• Capital controls?

Increasing Concern Even Among Neo-liberal institutions like IMF

Raghuram G. Rajan

• Economic Counselor and Director of Research

• “Has Financial Development Made the World Riskier?”

Financial Landscape Altered

• Technical Change• De-regulation• Institutional Change

Risk: Spreading and Concentration: role of banks

• Securitization: selling assets (“plain vanilla” assets: financial commodities)

• Banks holding onto less liquid assets.

Implications for Systemic Risk?

• Incentives facing bank managers and investors – increasing systemic risk?

• Banks and other investment institutions have more incentive to take on risk:

Incentives to take on Risk

• Compensation: asymmetric: upside is compensated more than downside is penalized

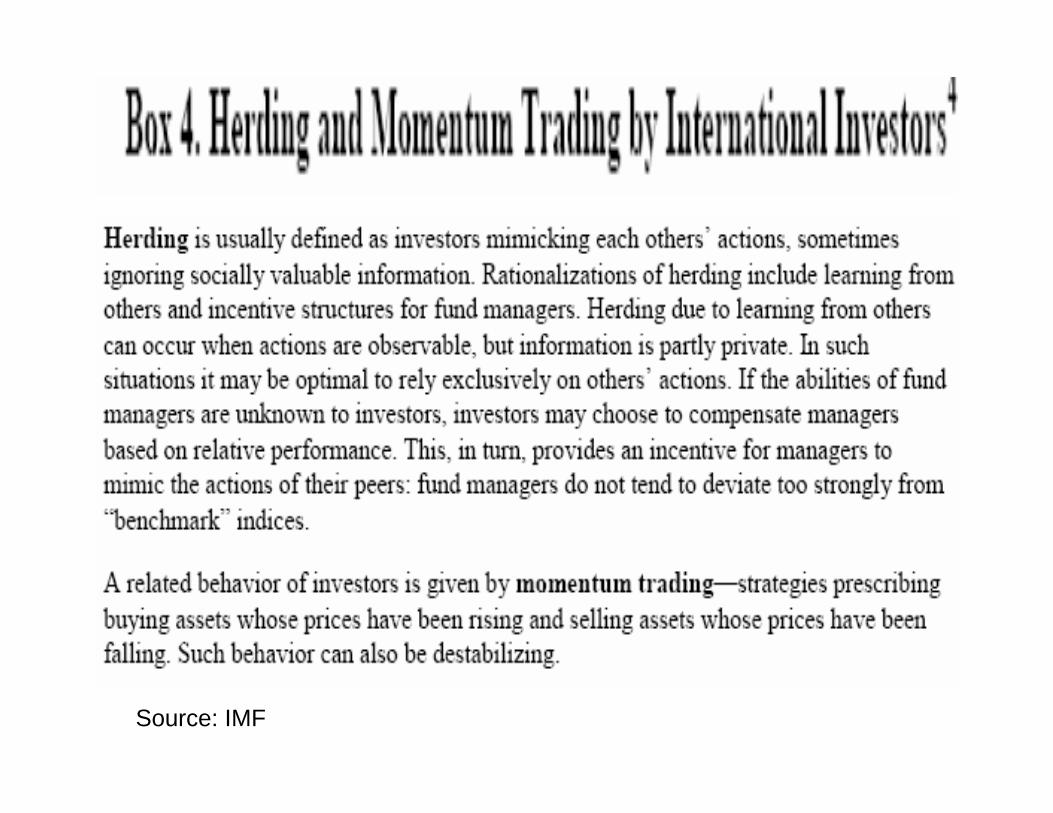

• Performance judged relative to peers-incentive to take hidden risk-incentive to herd (ass covering)

Reinforce each other in boom-willing to bear low probablity TAIL RISK

“Tail Risk”

• Non-normal probability distributions

Biggest Concern

• Will Banks be able to provide liquidity in the case of “tail risk” materializes

• In the past banks played that roleBased on their sound balance sheets

allowing them to attract liquidity in a crisis that they could on-lend

Illiquidity Risk?

• Banks today require liquid markets to hedge their bets, making them less able to provide the liquidity assurance they have provided in the past

Conclusion

• “Even though there are far more participants today able to absorb risk, the financial risks that are being created by the system are greater.

• More pro-cyclicality• Increased probablility of catastrophic

meltdown.