ECON 464 Senior Project

14

CALIFORNIA POLYTECHNIC STATE UNIVERSITY, SAN LUIS OBISPO IPO Underpricing: The Case of Twitter Lars C. Johnson June 2015 -

-

Upload

lars-johnson -

Category

Documents

-

view

227 -

download

0

Transcript of ECON 464 Senior Project

CALIFORNIA POLYTECHNIC STATE UNIVERSITY, SAN LUIS OBISPO

IPO Underpricing: The Case of Twitter

Lars C. Johnson

June 2015

-

Introduction

2013 was a big year for initial public offerings (IPOs) with over 157 IPOs, with an

average first-day return of 21.1% - the highest it had been since the tech bubble in 2000, with an

average first-day return of 56.3% and 381 IPOs. Social media companies have largely

contributed to these higher returns, stimulating demand for ownership in familiar companies that

most people are hyped about when they go public. This “social media bubble” has been

addressed by many literatures in how startups since the tech bubble have gained mass media

attention from users and businesses alike. Businesses have such strong interest in these social

media companies because of their ability to advertise their products in an effective way on their

website, app, or platform where users can just “click” to research or even buy what they’re

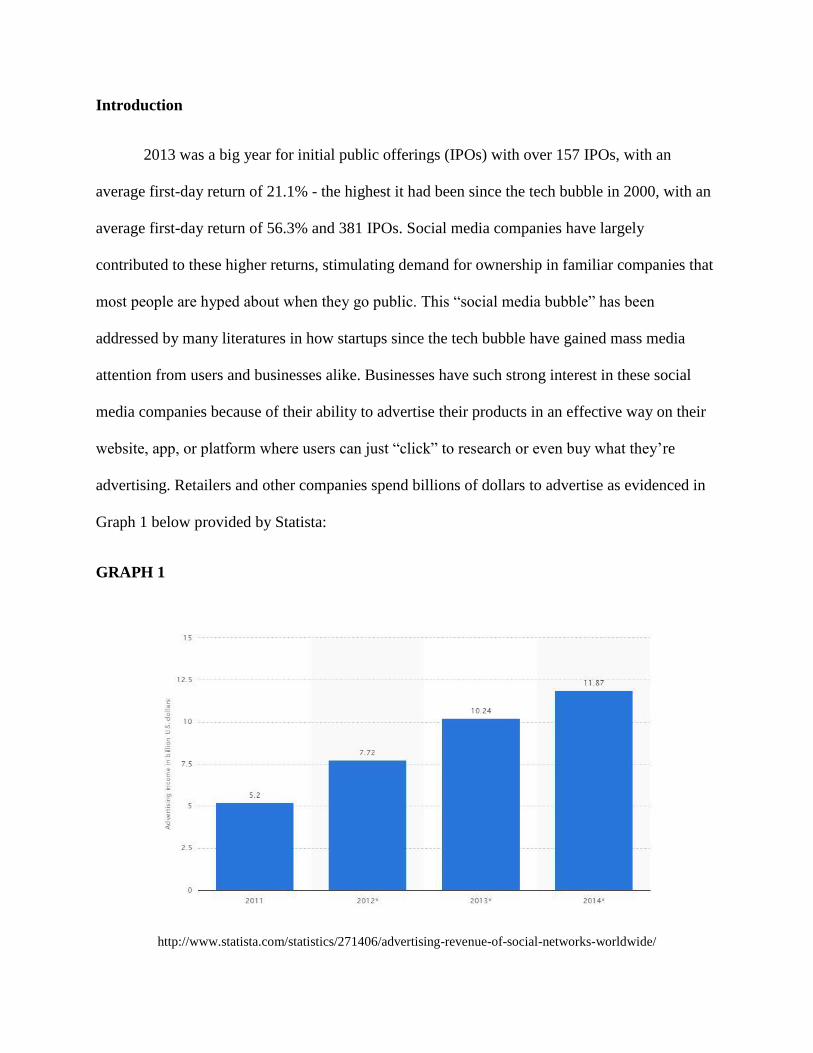

advertising. Retailers and other companies spend billions of dollars to advertise as evidenced in

Graph 1 below provided by Statista:

GRAPH 1

http://www.statista.com/statistics/271406/advertising-revenue-of-social-networks-worldwide/

With these social media companies bringing in so much revenue from just advertising,

when they choose to go public it is a big deal. This is because of not only their attractiveness, but

also how, historically, IPOs on their first day of trade experience such large returns – this

phenomenon is mostly due to underpricing their IPO.

In this paper, I will analyze the Twitter IPO that occurred back in 2013, which was

considered to be one of the most hyped up, biggest IPOs that had one of the largest first-day

returns in history. In doing so, I will explain the general IPO process and the various entities

involved in bringing a company public, their roles, as well as their incentives. From there I will

utilize previous literature to explain why Twitter’s IPO was underpriced via economic theories.

Finally, I will explain how investing in IPOs are essentially a gamble in how there is a large

amount of uncertainty about their intrinsic value when they go public, and the risk that comes

with it.

Literature Review

Businesses choose to go public because they can expand their business or pay off debt via

issuing equity, or ownership, of the company. The company interested in going public will hire

an underwriter (i.e. an investment bank) who helps sell the initial shares to institutional investors

or entities who can sufficiently distribute these shares to the public market. The primary job of

the underwriter is to not only find the “right” clients/investors to sell these initial shares to, but to

also meet the market demand they predict when the company reaches its IPO. Based on what

clients they pick and how market demand looks from their perspective, they work with the

issuing firm (the company going public) to negotiate an initial price, called the bid price, for the

initial shares to be sold to the underwriter. This bid price is the value the issuing firm receives for

each share sold to the underwriter and their clients prior to the first day of trade to the public. In

exchange for the underwriter’s services, the issuing firm pays the underwriter a set fee, like a

commission, which tends to be a percentage of the offer made, which can be very hefty.

The majority of underwriters for IPOs are investment banks who typically buy 100% of

the issuing firm’s shares at a determined bid price. The return for the investment banker in

bearing underwriting risk – the risk that investors will demand less than 100% of the issue when

it is reoffered for sale to the market – is the spread between the public offer price and the bid

price. Therefore, investment bankers have the incentive to underprice an IPO to increase both (1)

the spread between the offering price and the bid price to maximize their investment banking

return, and (2) the probability of selling the whole issue to outside investors to minimize

underwriting risk. The underpricing effects of an IPO can be defined as when if shares are sold

too cheaply, issuing firms will have raised less capital than was warranted by the intrinsic value

of their assets. What this implies is that there is a considerable amount of “money left on the

table” by the issuing firm and causes more difficulty for them to raise capital than if its price had

been at its intrinsic value. So the controversy here is why the issuing firm would agree to such a

deal with an underwriter (Saunders 1990).

Studies conducted in the past have concluded that there are large informational

asymmetries present when IPOs occur in the stock market. In other words, there are entities that

have more information about the issuing firm than others do when bringing a company public

through the IPO process. The more informed parties tend to be the underwriters who have access

to information that all other entities in the IPO process aren’t knowledgeable of. It is theorized

that both information asymmetry and the incentives of the underwriters are causations to the

underpricing of IPOs.

Conflicts of interest occur between the underwriter and the issuing firm when the public

offering price is being decided. The underwriter has information regarding what the potential

market’s demand is for the issuing company’s shares and the overall state of the market when

they reach an IPO, and has the incentive to underprice it to reduce the costs of distributing the

shares and making the investment look attractive. What the issuing firm wants is to maximize

revenues from the IPO which is hindered by underpricing due to lost revenues from not being

priced at the fair value. The issuing firm also does not have access to the underwriter’s

information listed above. This conflict of interest between these two entities is what is known as

the principal-agency problem. An optimal contract that would satisfy both entities’ “wants”

would be to allow the issuing firm a choice of an offering price that the underwriter will agree to.

For the underwriter to comply with this agreement of providing valuable information to the

issuing firm, the underwriter would have to be compensated. After the underwriter is sufficiently

compensated, the principal-agent problem should be greatly reduced as long as the underwriter is

meeting the market’s demand for the issuing shares at its IPO (Baron 1982).

Informed investors will only purchase new shares of the company at its IPO if the

offering price is less than the fair price of that company. When these informed investors believe

that the firm is overpriced at its IPO, then the less informed investors will end up purchasing the

majority of shares – this results in a “winner’s curse” for the less informed investors. To keep

these uninformed investors in the IPO market, so that their capital is not lost due to the fear of a

“winner’s curse” and trust in the market, the underwriter will underprice IPOs. By doing this,

uninformed investors will realize positive gains on either unattractive investments since if the

offer price is too high they will not be able obtain all the shares of a firm. Same goes for

attractive investments because usually informed investors cannot obtain all the shares so they

will underprice so that uninformed investors can provide capital to attractive investments. This

also motivates informed investors to buy shares of an unattractive investment since they know

that it is underpriced (Rock 1986).

As a result of underpricing an IPO, investors buying on the first day of trading pay, on

average, more than the offering price when the market is open. This “premium” is unfair to many

investors because institutional investors, or clients of the investment bank that is underwriting

the IPO, are able to purchase shares at preferred pricing which can be much lower than the

offering price to the public market. Essentially, the shares of the issuing company are sold to

these large institutions, while all other investors have to wait until the market is open when

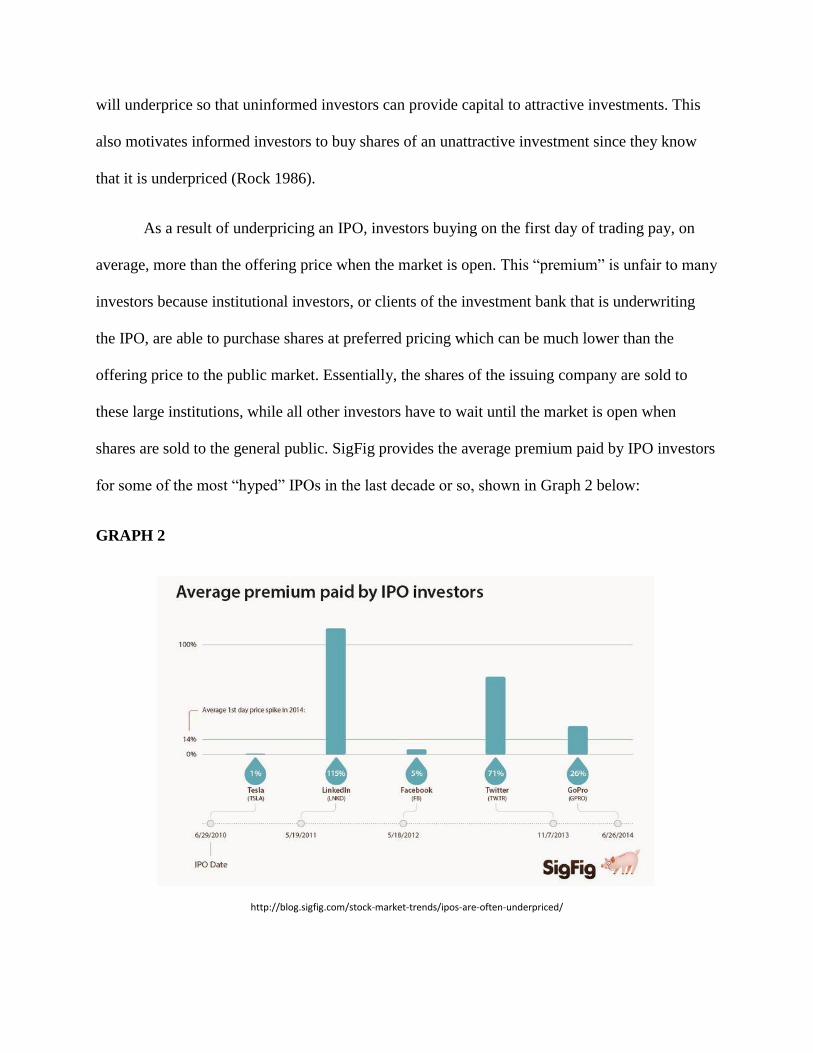

shares are sold to the general public. SigFig provides the average premium paid by IPO investors

for some of the most “hyped” IPOs in the last decade or so, shown in Graph 2 below:

GRAPH 2

http://blog.sigfig.com/stock-market-trends/ipos-are-often-underpriced/

The results evidence how there is potential for “hyped up” IPOs to be priced much lower

for institutional investors that get the privilege of preferred pricing, and how large of a premium

everyday investors have to pay – this “premium” essentially eliminates the personal gains that

could’ve been realized if the IPO had not been underpriced. In the case of Twitter, investors had

to pay a 71% premium to buy their shares when the bell rang on its first day of trade. These early

investors, including underwriters and their clients, can buy shares before anyone else at the offer

price negotiated and sell them when the price is higher – this is the price, including the premium,

that everyday investors will purchase their shares when made publicly available. There are,

however, contractual restrictions that can be made between the underwriter and the issuing firm

called a “lock-up period” that prevents insiders who are holding the majority of the shares of the

company, before it goes public, from selling stock for a period usually lasting 90-180 days after

the company goes public (Investopedia). This is unfair to the insiders of the company holding

significant shares in the company if this contractual restriction were to be made because the

underwriters and their clients can achieve huge gains on investment while the big stakeholders in

the company cannot. But this lock-up period can also be attractive to the original stakeholders of

the company because it prevents the market from being flooded with a large number of shares,

which would depress the stock’s price – a result no investor or shareholder wants to see happen

(SigFig).

Information asymmetry ties back into this lock-up period because, in some scenarios,

without this contractual restriction, insiders may have valuable information about their

company’s future performance. Information such as an earnings report they have access to before

it is publicly available, they can decide to flip their shares, by either selling or buying, giving

them an unfair advantage over all other investors – this is what is called insider trading. In the

months following the IPO when the lock-up period is over, the early investors and insiders are

able to flip their shares which involves a lot of uncertainty in terms of where the stock’s value is

going to go in the long-run, however in the short-run IPOs can be a rather attractive investment.

Even though investors pay a premium on these IPOs in the cases shown in Graph 2, there

is an upside to investing in them because significant first-day gains can be made. Ritter

conducted an analysis on the performance of IPOs on their first day of trade which provided a

few takeaways. First, there is a price “pop” in which the stock price will, on average, close above

the offer price. Second, when the offer price is set too low, original shareholders leave money on

the table because they give up more of the company to new investors than is necessary in so far

as raising new funds. As a result of this, the big price pop can increase wealth of investors but

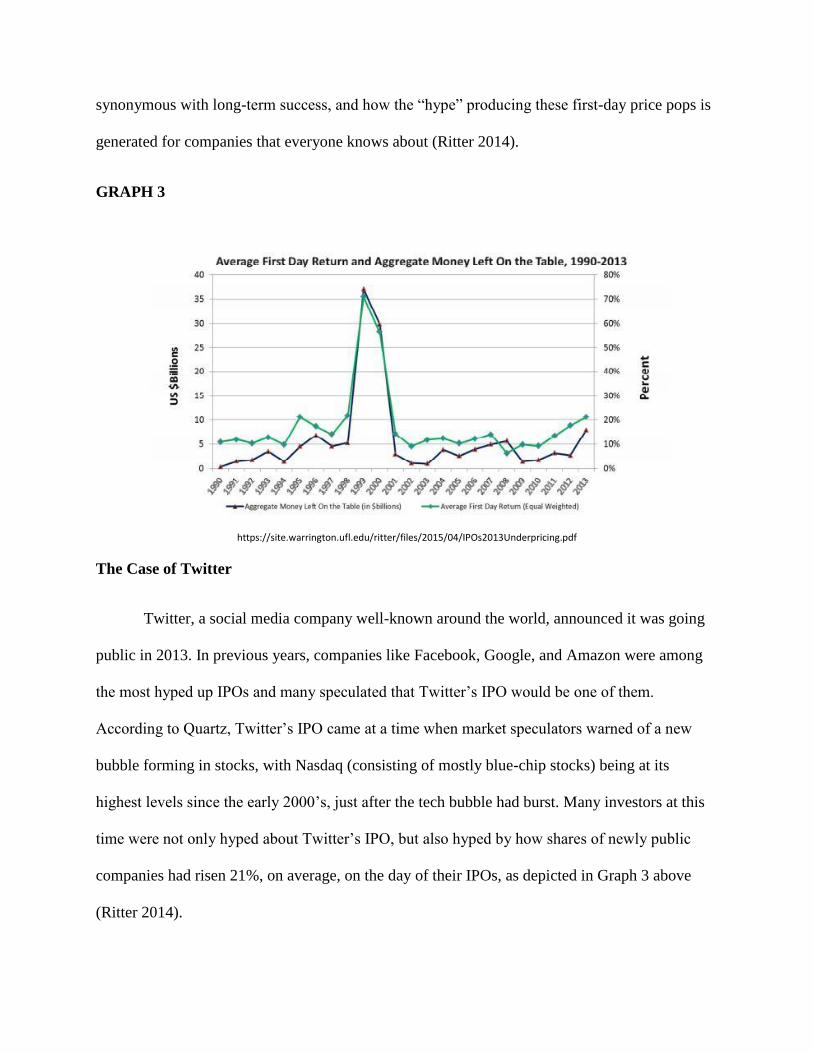

not the amount that it should have. Graph 3, on the next page, displays the relationship between

the average first-day returns and the aggregate money left on the table – as you can see, there is

somewhat strong, positive linear relationship between the two variables. This indicates the more

an IPO is underpriced, the more money there is left on the table, and the higher the return will be

on the first day of trade (Ritter 2014).

Third, investors who buy stock in a company that was already traded publicly and hold

onto for, say, a period of more than 6 months, will tend to outperform investors who bought

stock in a similar company (i.e. similar market cap and/or financial ratios) on its first trading day

and held onto it for the same amount of time. Ritter calls this phenomenon “long-term

underperformance”, which ties back to the amount of uncertainty of an IPO’s value in the long-

run, making it a riskier investment than that of a company that’s been traded publicly for an

adequate amount of time, where early investors and insiders are less likely to flip their shares. In

short, Ritter explains there is a psychological illusion that these first-day price pops are

synonymous with long-term success, and how the “hype” producing these first-day price pops is

generated for companies that everyone knows about (Ritter 2014).

GRAPH 3

https://site.warrington.ufl.edu/ritter/files/2015/04/IPOs2013Underpricing.pdf

The Case of Twitter

Twitter, a social media company well-known around the world, announced it was going

public in 2013. In previous years, companies like Facebook, Google, and Amazon were among

the most hyped up IPOs and many speculated that Twitter’s IPO would be one of them.

According to Quartz, Twitter’s IPO came at a time when market speculators warned of a new

bubble forming in stocks, with Nasdaq (consisting of mostly blue-chip stocks) being at its

highest levels since the early 2000’s, just after the tech bubble had burst. Many investors at this

time were not only hyped about Twitter’s IPO, but also hyped by how shares of newly public

companies had risen 21%, on average, on the day of their IPOs, as depicted in Graph 3 above

(Ritter 2014).

The underwriters of Twitter’s IPO were Goldman Sachs, Morgan Stanley, and JPMorgan

Chase, who negotiated an offer price of $26 – this was done with the traditional Wall Street

approach with the underwriters purchasing 100% of the shares from Twitter. Shares at this price

were being offered exclusively to clients of these investment banks, not Twitter, prior to the day

shares were being sold to the public. The morning the bell rang when Twitter’s shares were

available to purchase by the public, the opening stock price was $45.10, and closed at $44.90.

This 73% increase in price was the big price “pop”, which was a clear indication of underpricing.

The IPO price of $26 gave Twitter a market capitalization of over $14 billion, which increased to

more than $25 billion via the price pop – roughly 50 times the amount of revenue Twitter made

that year. The full underwriter option put Twitter’s IPO at $2.1 billion, the 2nd

largest tech IPO in

history behind Facebook and ahead of Google, and the 3rd

largest deal of 2013 (Forbes).

Twitter’s IPO was considered a huge success through the eyes of the underwriters and

their clients because of the 73% price pop (the 6th

largest first-day price pop on record), in which

they flipped their shares to almost make a quick double on their money. This surge was

“reminiscent of the dot com mania days when investor psychology allowed companies yet to

show a profit to trade at high prices on unrealistic hopes”, according to Forbes. Along with this

high first-day return, the underwriters also received 3.25% for their services in bringing Twitter

public. Overall, this IPO was a big win for those who were able to attain preferred pricing before

the stock’s value increased.

For Twitter, it was also a success in that their market cap had grown exponentially and

raised a significant amount of capital to expand their operations and overall business, and was

happy with the investment banks that were able to meet the demand for shares when it hit the

public market, as they were required to do. However, because of Twitter’s IPO was underpriced,

there were consequences in which Twitter itself lost out, while the underwriters and early

investors gained. The underpricing caused: a considerable amount of money to be left out on the

table, the lock-out period prevented original stakeholders to lose out on the price pop benefits,

and a loss in faith from everyday investors who bought shares the first day of trade and lost

money with the expectation of a first-day gain.

Theories Applied to the Case of Twitter

There are several theories that explain why Twitter’s IPO was underpriced when it hit the

market, which were discussed previously in my literature review. Saunders’ theory revolves

around how the underwriters of an IPO have the incentive to underprice in order to maximize

their investment banking return, as well as minimizing their underwriting risk. The underwriters

in Twitter’s case did underprice the IPO as evidenced in the section above. The investment banks

underwriting Twitter’s IPO left an aggregate amount of $1.6 billion on the table. This means that

Twitter essentially “lost” $1.6 billion in how this amount was unraised capital that could’ve been

achieved if Twitter was valued at its intrinsic value. While investment banks like Goldman Sachs

more than satisfied their clients whom they sold shares to at preferred pricing who realized a

73% ROI on the first day of trade, Twitter greatly suffered from more than a billion dollar loss in

unearned capital that exceeded their total revenues since they first became a company.

Baron’s theory behind underpricing discussed how there is a conflict of interest between

the issuing firm and the underwriter, called the principal-agency problem. The underwriters, or

investment banks in this case, had valuable information concerning what the market’s demand

was for Twitter when they were about to issue their IPO, while Twitter does not have this

information – also known as information asymmetry. The investment banks underwriting the

IPO wanted to make it look as an attractive of an investment as possible, so they had the

incentive to underprice it because if Twitter’s price was too high to the average investor, demand

for Twitter’s shares would not have been as high. If Twitter’s shares had not been fully sold on

the first day of trade due to insufficient demand, the investment banks underwriting would have

looked bad in that they did not perform well and would lose their reputation as a company and,

most likely, lose future business.

Rock adds on to Baron’s theory about how information asymmetry plays a large part in

why companies can be underpriced at their IPO. He explains the phenomenon known as winner’s

curse – which occurs to less informed investors when they purchase shares of an overpriced IPO,

while the informed investors know it is overpriced. In order to keep the less informed investors

in the market, the informed investors, or the investment banks underwriting the IPO and their

respected clients, will underprice the IPO. This may have been one of many reasons that gave the

investment banks underwriting Twitter’s IPO to underprice it – especially given the fact that

Twitter’s IPO was the biggest, most hyped up IPOs of 2013. If there was any indication to less

informed investors that Twitter’s IPO had been overpriced, Twitter would’ve not been able to

raise the capital it had hoped to by going public. The underwriters were most likely aware of this,

so by underpricing they were able eliminate that issue without the knowledge of the issuing firm,

Twitter.

Ritter’s studies on IPOs focused mostly on the premium paid by investors for hyped up

IPOs. He discussed more about the psychological illusion of how hyped up IPOs, like Twitter’s,

have these price pops where investors realize big first-day gains on investing in such companies.

The psychological illusion is that investors believe that these price pops and long-term

performance are synonymous, so they will blindly purchase shares of hyped up IPOs like

Twitter, where investors paid a premium of 71%. This premium ultimately serves as evidence of

underpricing and Ritter’s studies point to how there is a ton of uncertainty behind whether a

company is priced at its intrinsic value.

Conclusion

Historically, underpricing is a very common occurrence when companies choose to go

public. Investment banks have incentives to underprice IPOs to maximize their profits and

minimize risks, utilizing information that they and their clients have. This gives them an unfair

advantage over everyday investors who choose to invest in IPOs who do not realize the type of

gains that informed investors do. The issuing firm, such as Twitter, suffers greatly from

underpricing because they lose billions of dollars of capital had it not been underpriced. This

truly makes IPOs a gamble investment because the amount of uncertainty and risk involved with

investing in them, mostly due in part to the amount of information asymmetry existing between

the underwriter(s), the issuing firm, and all other types of investors.

References

Baron, David. A model of the demand of investment banking advising and distribution

services for new issues. Journal of Finance, 1982.

Ritter, Jay. "Initial Public Offerings: Updated Statistics." May 9, 2014. Accessed June 9, 2015.

https://site.warrington.ufl.edu/ritter/files/2015/04/IPOs2013Underpricing.pdf.

Rock, Kevin. Why New Issues are Underpriced. Journal of Financial Economics, 1986.

Saunders, Anthony. Why Are So Many Stock Issues Underpriced. Business Review, 1990.

"Advertising Revenue of Social Networks Worldwide 2011-2014 | Forecast." Statista. Accessed

June 9, 2015.

"What Is an IPO Lock-up Period and How Long Is It?" Investopedia. October 9, 2012. Accessed

June 9, 2015.

"With IPOs, the Cheap Shares Are Not for Us." The SigFig Blog. Accessed June 9, 2015.

![[Shinobi] Bleach 464](https://static.fdocuments.in/doc/165x107/568c53571a28ab4916ba6201/shinobi-bleach-464.jpg)