EBRD EastAgri Annual Meeting 2005 1 st March 2005.

30

EBRD EBRD EastAgri Annual Meeting 2005 EastAgri Annual Meeting 2005 1 1 st st March 2005 March 2005

-

Upload

gerard-goodman -

Category

Documents

-

view

214 -

download

0

Transcript of EBRD EastAgri Annual Meeting 2005 1 st March 2005.

EBRDEBRDEastAgri Annual Meeting 2005EastAgri Annual Meeting 2005

11stst March 2005 March 2005

EBRD’s Objective in MSE FinanceEBRD’s Objective in MSE Finance

Provide private micro and small enterprises, throughout our countries of operations, not catered to by the formal financial sector with sustainable access to financial services regardless of the industry sector.

Approach to MSE FinanceApproach to MSE Finance

Ensure fast and wide outreach including remote and depressed areas

Ensure commercial viability of MSE lending as building block for sustainability

Integration of MSE lending operations into formal financial system as standard

Efficient use of Technical Assistance funds with clear and measurable performance benchmarks

Donor Co-ordination & Harmonization - in On-lending, Project Management, and TA-Institution Building

PBs, MFIs and NGOsPBs, MFIs and NGOs

Where there are commercial banks that meet standards of integrity, commitment and financial stability, TA and loan funds are provided (40).

Where no suitable commercial banks are available, or where these banks are unwilling to adopt necessary procedures and client orientation, specialised MFIs are set up (12).

NGOs being explored – ‘best-practice’, track-record, and preferably ‘commercialising’ so that they can attract capital market funds rather than scarce donor resources for lending (1 NGO upgrade, 1 NGO loan and 1 NGO TC only).

Results & Successes Overall Results & Successes Overall (to end Dec 2004)(to end Dec 2004)

EBRD has been promoting MSE development throughout the region for 10 years. It is now operating in 19 countries with 55 partners, through 944 branches employing 3,671 loan officers

Results & Successes Overall Results & Successes Overall (to end Dec 2004)(to end Dec 2004)

to end Dec 03

to end Dec 04

%Change

Total No. of loans disbursed

454,651 785,855 75%

Total volume of loans disbursed

3,134,485,865 5,095,057,243 65%

Average loan amount 6,894 6,483 -6%

Outstanding portfolio – number

170,526 295,069 73%

Outstanding portfolio – volume

937,155,312 1,602,394,279 71%

Arrears > 30 days 0.60% 0.68% 13%

Results: Number of Loans DisbursedResults: Number of Loans Disbursed(to end Dec 2004)(to end Dec 2004)

Caucasus68,699

Balkans211,100

Russia225,082

Central Asia157,386

Ukraine + Belarus123,512

Results: Volume of Loans DisbursedResults: Volume of Loans Disbursed(to end Dec 2004)(to end Dec 2004)

RussiaUSD 1,914,683,190

CaucasusUSD 300,177,654

BalkansUSD 1,387,074,493

Central AsiaUSD 800,188,024

Ukraine + BelarusUSD 694,638,377

Agricultural Loans – Volume of Loans Agricultural Loans – Volume of Loans Outstanding Outstanding ( to end Dec '04)( to end Dec '04)

BosniaUSD 11,787,796

Albania USD 5,727,964

UkraineUSD 560,654

BulgariaUSD 11,075,657

GeorgiaUSD 6,848,841Kosovo

USD 8,183,086Macedonia

USD 1,112,362

MoldovaUSD 516,937

RomaniaUSD 2,974,481

Serbia & MontenegroUSD 28,580,553

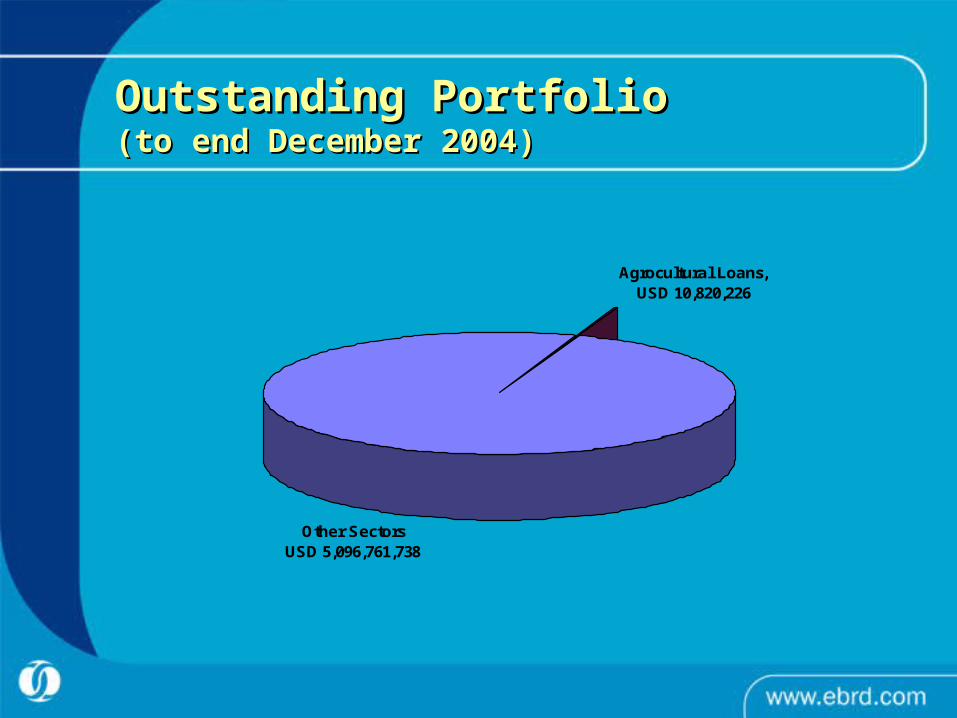

Outstanding Portfolio Outstanding Portfolio (to end December 2004)(to end December 2004)

Other SectorsUSD 5,096,761,738

Agrocultural Loans, USD 10,820,226

Main Lessons:Main Lessons:

Economic impact is substantial on regional/national basis, but only if large number of enterprises reached rather than “token” levels

Financial viability of Micro and Small lending for partner institutions requires “critical mass”, i.e. volume and efficiency needed for these transactions to make good business sense

Know-how to fill finance gap exists - there is a model that works

Factors that limit or unleash impact:

– TA availability for institution building– Consultant Quality– Legal regulatory environment: key impediments must be tackled– Cannot totally rely on existing banks (design innovation needed).

In some cases the creation of a “Greenfield” bank dedicated to MSE finance is required (for example, KMB in Russia)

Next Steps for MSE lending Next Steps for MSE lending programmesprogrammes

Increase rural lending and village outreach Farm Lending – specialised loan officers Push extremes –express micro loans and

longer term fixed asset loans as borrowers grow

Partner Banks: continue to include new banks as long as sufficient TA is available (a long-term proposition). Mature partners to continue business without consultants’ (80% of branches have ‘graduated’)

MSE banks - increase deposit mobilisation and gain independence from IFIs; diversify creditors; widen branch networks, increase financial services for the ‘poor’

“Loan officers in Kyrgyz Republic solve

transport problems in rural areas by using

bicycles”

ProCredit ProCredit Bank SerbiaBank Serbia

IntroductionIntroduction

ProCredit Bank Serbia (former MFB) started in March 2002

Now operating through 28 branches

Faculty of Agriculture, Novi Sad Great potentials in Vojvodina Novi Sad-training and database

centre Agriculture-long tradition in

Vojvodina Vojvodina-regions

AgricultureAgriculture

● 21% of GDP, second only to manufacturing (24%)

● 25% of GDP together with associated food and beverage products

● 44% of population lives in rural areas, a third of whom rely wholy, or in part, on agriculture for their livelihoods

AgricultureAgriculture

● 17% of total exports are agri products, processed food, beverages, and tobacco products.

● Agriculture producers: private farmers, Agro Kombinats (460) and co- operatives (400)

● Private farmers own 83% of the 3.35 mill. ha of arable land. The average farm is 2- 5 ha, usualy in several plots

● 3% of land is irrigated

Variety of Agricultural ProductionVariety of Agricultural Production

Vegetables/CropsFruits/CropsVegetables/HogsHogs/CropsHerbsCows/CropsCrops

Crop YearCrop Year

Revenues

Soybean,Sunflower,

Corn Sugar Beat

B BarleyW Wheat

Sep Oct Nov Dec Jan Feb Mar Apr Jun Jul

Wheat, Barley

Corn,Soybean,Sunflower,SugarBeat

Investment period

Agro Credit Agro Credit TechnologyTechnology

Technological Maps

Financial resume

Income statement

Cash flow

Agricultural analysis

Technological mapTechnological map

Lists all necessary operations

Gives the timing for these operations

Includes all expenses (seed, fertilizers, fuel…)

Map has two sections

Comment

We have about 40 maps

Maps for cattle breeding

Financial resumeFinancial resume

A continuation of the technological map

Its role is to sum up the expenses listed in the technological map

The financial resume does not include yields eaten by animals

Serbian Chamber of Commerce

Stock exchange

Risk in AgricultureRisk in Agriculture

Risk Measures taken for Risk Mitigation

Long production process

Farmers with a minimum of one year’s experience

Weather Meteorological posts, Farmers with a minimum of three crops

Diseases Veterinary institutes

Land Map with six types of soil

Agriculture perspectiveAgriculture perspective

Privatisation and restructuring of AK and agro-processors

Land restitution and strengthen land markets

Rejuvanate food marketing chain

Rehabiltate drainage canals

Regional development

Rural finance

Business Loans Outstanding – numberBusiness Loans Outstanding – number

31%

36%

9%

21%3%

Agriculture

Trade

Production

Services

Other

Business Loans Outstanding – volumeBusiness Loans Outstanding – volume

19%

38%20%

19%4%

AgricultureTradeProductionServicesOther

NumberNumber of of AgrAgrii Loans Loans Disbursed By Disbursed By BranchesBranches

0

100

200

300

400

500

600

700

800

900

Novi Sad Subotica uključujući Sombor Čačak Šabac

Novi Pazar Beograd 1 Beograd 2 Beograd 4

Beograd 6 Niš Užice Kragujevac

Krusevac Kraljevo Vranje Becej

Kikinda

VolumeVolume of of AgrAgrii Loans Loans Disbursed By Disbursed By BranchesBranches

EUREUR

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Novi Sad Subotica uključujući Sombor Čačak Šabac

Novi Pazar Beograd 1 Beograd 2 Beograd 4

Beograd 6 Niš Užice Kragujevac

Krusevac Kraljevo Vranje Becej

Kikinda

Agri Loans Agri Loans OutstandingOutstanding - in volume- in volume

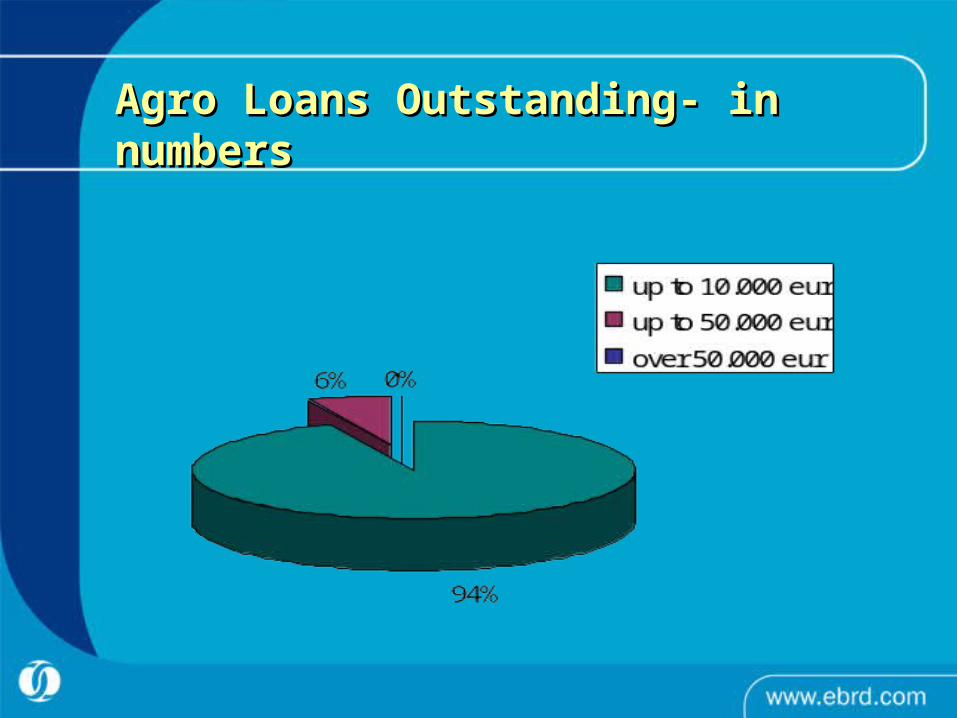

Agro Loans Agro Loans OutstandingOutstanding- in numbers- in numbers

Agro Loans Agro Loans OutstandingOutstanding-By Maturity-By Maturity (Volume)(Volume)

19%

39%

21%

21%

up to 12 mth

up to 24 mth

up to 36 mth

over 36 mth