EBPAQC Audits of Employee Stock Ownership Plans Webinar Troubleshooting Tips Disable all pop-up...

91

EBPAQC Audits of Employee Stock Ownership Plans Webinar Troubleshooting Tips Disable all pop-up blockers on your computer You should be able to hear music, if not, you may need to do one of the following: Verify that the volume on your computer is not muted If you are in Windows Media Player, please logout and try Real Player If you are in Real Player, please logout and try Windows Media Player Most often any audio or video difficulties are at the local user office so you may need to check with your IT administrator If you are still having difficulties, please let us know by typing your problem in the question box on the left hand side, and a Genesys representative will assist you 1

-

Upload

henry-oliver -

Category

Documents

-

view

218 -

download

0

Transcript of EBPAQC Audits of Employee Stock Ownership Plans Webinar Troubleshooting Tips Disable all pop-up...

EBPAQC Audits of Employee Stock Ownership Plans

Webinar Troubleshooting Tips Disable all pop-up blockers on your computer You should be able to hear music, if not, you may need to do one of the

following: Verify that the volume on your computer is not muted If you are in Windows Media Player, please logout and try Real Player If you are in Real Player, please logout and try Windows Media Player

Most often any audio or video difficulties are at the local user office so you may need to check with your IT administrator

If you are still having difficulties, please let us know by typing your problem in the question box on the left hand side, and a Genesys representative will assist you

1

Employee Benefit Plan Audit Quality Center

Audits of Employee Stock

Ownership Plans

Live Forum

April 20, 2010

2

CPE Credit For Participating

• Must have registered for CPE credit prior to this live forum– CPE Credit Approval Form posted on webinar instruction site

• Listen for announcement of 4 CPE codes (7 digits: ALL_ _ _ _ ) and 4 polling questions during the live forum

• Record CPE Codes on CPE Credit Approval Form (no need to record polling questions)

• Return completed form (by fax or mail) to AICPA Service Center for record of attendance

• Keep a copy of completed CPE Credit Approval Form for your records

3

Presenters

Becky Miller, CPA

McGladrey & Pullen, LLP

Hal Hunt, CPAMayer Hoffman McCann P.C

.

David Bogus, ASAEllin and Tucker, Chartered

Mark Swanson, Esq.Crowe Horwath LLP

4

Audit and Accounting Issues

• Introduction to ESOPs• Common prohibited transactions • Leveraged ESOPs• Tax considerations• Stock valuation issues• Financial statement presentation

5

Introduction to ESOPs

Mark Swanson

Senior Manager

Crowe Horwath LLP

6

Introduction

• What is an ESOP?– Employee benefit plan that must satisfy all

requirements of a qualified plan (IRC and DOL)– Designed to invest primarily in employer

securities– May borrow money to purchase employer

securities

7

Introduction

• ESOPs – Provide an employee benefit– Technique of corporate finance– Business perpetuation– Provide market for privately held / thinly traded stock– Provide liquidity for estates of business owners– Business acquisition technique

8

Introduction

• Benefits to Employee-Participants– Employees not currently taxed on contributions

when contributed and allocated– Taxation of earnings and contributions deferred

until distributed.

9

Introduction

• Benefits to Plan Sponsor– Contributions are deductible– Potential deductions for dividends paid to ESOP– Possible elimination of federal income tax at corporate

and shareholder level– Provide employees with incentives to enhance

productivity and profitability.

10

Introduction

• Benefits to Selling Shareholder(s) – Provide market for shares

– Provide potential to realize higher value for shares

– Can control timing of transaction: Sell all at once or over time

– Selling shareholder may be able to retain effective control

– Ability to defer gain on sale under Sec. 1042.

11

Introduction

• Items to Note – Different provisions can apply to C Corp ESOPs

and S Corp ESOPs – For purposes of S Corp 100 shareholder rule,

the ESOP trust is treated as one shareholder.

12

Introduction

• Conclusion to Introduction: – ESOPs are a great tool when used in appropriate

situations– Provide a level of flexibility to meet needs to employee-

participants, plan sponsor and selling shareholder.

13

Prohibited Transactions

Becky Miller, CPA

McGladrey & Pullen LLP

14

15

Prohibited Transaction Implications for ESOPs

• Remember, AG Chapter 11 on party-in-interest transactions illustrates GAAS

• Potential ESOP issues– Purchase of stock– Sale of plan’s stock– Loan to acquire stock– Failure to follow plan or loan terms– Failure to follow prohibited transaction exemption

conditions on loan– Refinancing– Plan Termination– Application of dividends to debt service– Application of accumulated funds in ESOP to debt service

16

Commonly Encountered PTs

• Valuation not as of the transaction date– No roll forward to the actual date– Failure to recognize that purchase of stock by sponsor

out of the plan to fund distributions is subject to the transaction date valuation rule

– Creative approach see PTE 2003-32• Failure to properly release shares

– Principal only method when not eligible– Principal and interest method, incorrectly calculated– Some other disallowed method – e.g. fair market value

method

Commonly Encountered PTs

• ESOP loan not adequately documented• ESOP appraisal not sufficient• Special S corporation limitations not satisfied - §4975(f)

(6)(B)(ii) only works on a sale to a plan, not a purchase from the plan

• Application of allocated dividends to debt service fails the “return for value” standard – IRC §§ 404(k) and 4975(f)(7)– This is the tax concept of “allocated” meaning dividends on

shares released from collateral and allocated into participant accounts

17

Auditor’s Duties on Party-in-Interest Transactions

• Gain an understanding of the transaction• Gain an understanding of the applicable ERISA

exemption• Compare the two for any inconsistencies

– Reconcile any inconsistencies• Document such effort in the file• Document the conclusions in the file• Report any PTs on the ERISA schedules• Material PTs will require discussion in the related party

footnote

18

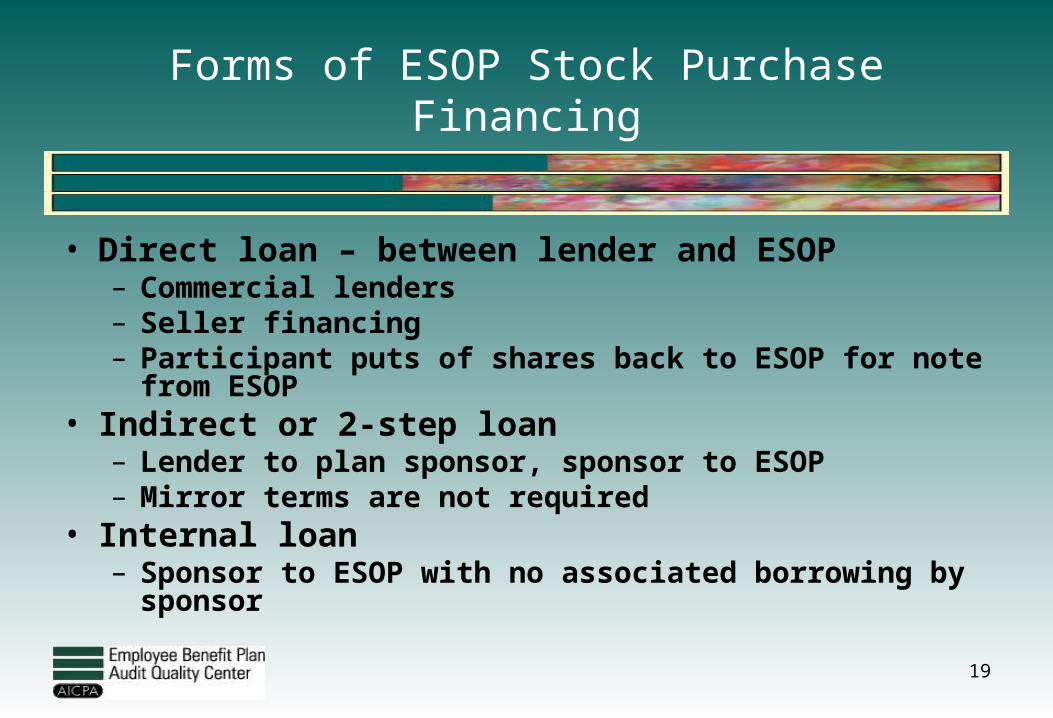

Forms of ESOP Stock Purchase Financing

• Direct loan – between lender and ESOP– Commercial lenders– Seller financing– Participant puts of shares back to ESOP for note from ESOP

• Indirect or 2-step loan– Lender to plan sponsor, sponsor to ESOP– Mirror terms are not required

• Internal loan– Sponsor to ESOP with no associated borrowing by sponsor

19

Indirect ESOP Structure

Chart

20

Direct Loan - Seller Financing ESOP Structure

Chart

21

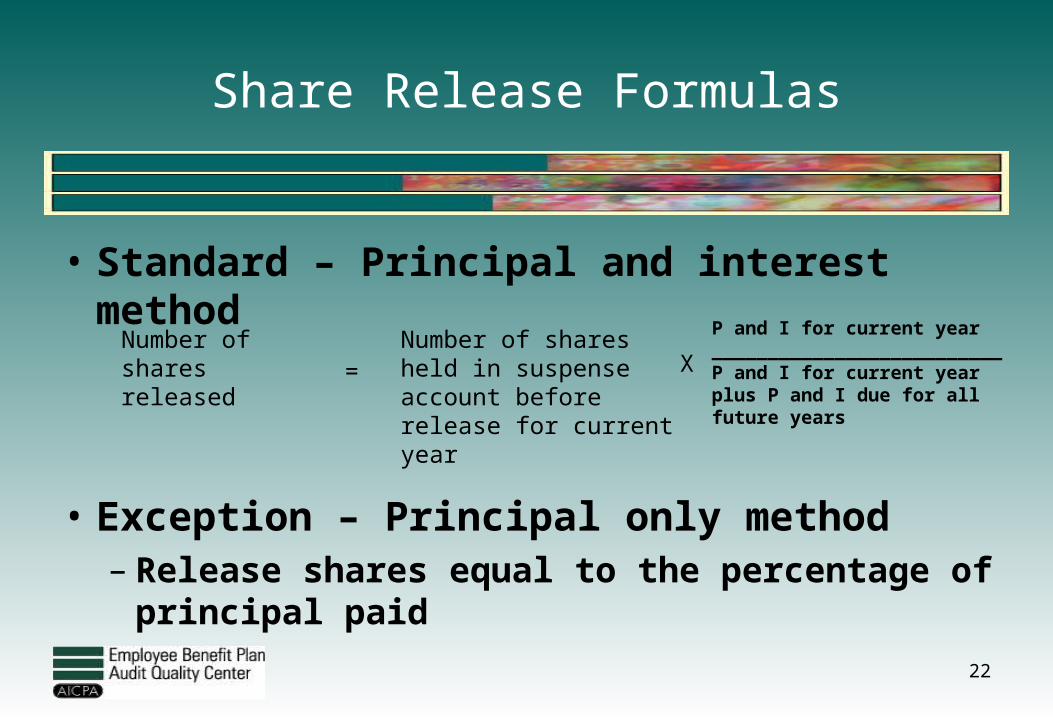

Share Release Formulas

• Standard – Principal and interest method

• Exception – Principal only method– Release shares equal to the percentage of

principal paid

22

Number of shares released

Number of shares held in suspense account before release for current year

P and I for current year__________________________P and I for current year plus P and I due for all future years

= X

Other Potential Non-Exempt Transaction Issues

• Purchase of stock from plan to fund distributions• Dividends applied to debt service• Prepayments of debt service• Use of accumulated funds for debt service• Refinancing ESOP debt• Terminating an ESOP

23

Purchase of Shares

• Most plans distribute cash, not stock• Distributions typically take place after annual

administration is completed – 3 to 9 months after year-end

• Purchases from plan by a PII must be for not less than FMV on the date of the transaction.

24

Dividends for Debt Service

• Only dividends on shares acquired with debt• Dividends on allocated shares may only be used

where the FMV of the stock returned in exchange for the use of such dividends is not less than the dollar value of the dividends so applied– Can use shares released from dividends paid

on unallocated shares to make up any difference.

25

Prepayments of Debt Service

• Technically a refinancing unless loan agreement permits such action

• Watch loan terms – Typically apply to interest then principal

• Collateral release– If principal only – no problem– If principal and interest – changes denominator

• Watch for Excel© failures

26

Use of Accumulated Funds for Debt Service

• Debt service limited to:– Collateral– Employer contributions for Debt Service and

earnings thereon– Dividends on shares acquired with the debt and

earnings thereon

27

Refinancing of ESOP Debt

• Exclusive Benefit requirement

• Field Assistance Bulletin 2004-1

28

ESOP Terminations

• Sale of stock

• Cancellation of debt

• Holdbacks on purchase price– Can’t take a receivable from the new plan

sponsor– Typically holdback is deposited in cash in an

escrow account

29

Tax Considerations

Mark Swanson, Esq.

Senior Manager

Crowe Horwath LLP

30

Tax Considerations

• Topics:– Deduction Limits

• C Corp• S Corp

– Section 415– S Corp ESOPs: Section 409(p)– Diversification: Section 401(a)(28)

31

Tax Considerations

• Deduction Limits– Note differences for C and S Corporations– C Corp

• Contributions used to pay principal can be as high as 25% of participant compensation

• No limit on deduction for loan interest• Separate deduction limit for ESOP contributions to

pay principal and deduction for contribution to other qualified plans

32

Tax Considerations

• Deduction Limits (continued)• Dividends paid on stock held in ESOP deductible if:

– Reasonable: What’s reasonable? General rule is amount of dividend Sponsor can reasonably expect to pay on a recurring basis

– Paid in cash directly to or through ESOP to participants– Reinvested in employer securities (if participants have been

given election to receive dividend in cash); or – Used to repay ESOP loan on shares (allocated and

unallocated) aquired with the loan being repaid. Dividends on allocated shares subject to ‘fair market value’ test.

33

Tax Considerations

• Deduction Limits (continued)– Fair Market Value Test: If dividends on shares allocated to

participant accounts are used to make loan repayments, shares with a fair market value at least equal to the dividends must be allocated to participant accounts.

• Example: Fair Market Value = $16 / share– $200,000 loan repayment. $100,000 is a dividend. 10,000 shares released

from suspense account of which 5,000 are attributable to dividends. – Fair market value of shares released with dividends = $80,000 – Allocation would be based on 6,250 shares allocated on basis of dividends

and remaining 3,750 shares allocated based on employer contribution. Check plan document to determine how shares are allocated based on dividends and employer contribution.

34

Tax Considerations

• Deduction Limits (continued)– S Corp

• Contributions used to pay principal and interest limited to 25% of participant compensation

• No separate deduction limit for ESOP contributions and contributions to other plans

• While not a deduction issue per se, S Corp distributions may be used to repay the ESOP loan. Distributions on shares allocated to participant accounts that are used for loan repayments are subject to the fair market value test.

35

Tax Considerations

• Deduction Limits (conclusion)– Both C and S Corp

• Contributions exceeding 415 limits are not deductible

• Nondeductible contributions subject to 10% excise tax under IRC Sec. 4972.

36

Tax Considerations

• Section 415 – Limits annual additions to participant accounts in all plans

sponsored by the employer to the lesser of 1) 100% of the participant’s compensation or 2) 49,000 (2010).

– Includes 401(k) deferrals (but not catch up contributions).– If plan permits, shares released from suspense account can be

valued at lesser of fair market value or contribution. – Special Rule for C Corps: If no more than 1/3 of the employer

contribution applied to principal and interest is allocated to highly compensated employees, the contribution attributable to loan interest and reallocation of forfeitures of leveraged shares aren’t treated as annual additions.

37

Tax Considerations

• S Corp ESOPs: Section 409(p) Anti-Abuse Rules.

– Simple result of a complex test: Disqualified Persons (DP’s) cannot own more than 50% of the S-Corp ESOP shares, non-ESOP shares and Synthetic Equity.

– Consequences of a violation have been termed “draconian.”• Corporation pays 50% excise tax on prohibited allocations and 50% excise tax

on fair market value of synthetic equity held by a DP• Prohibited allocations treated as distributions to individual and subject to taxes

and penalties.• Prohibited allocations include:

– Stock and stock related allocations made to DPs during year of failure – Stock and stock related balances in DP accounts at the beginning of the

year

38

Tax Considerations

• Section 409(p) (continued)– Defining the Key Terms: DP and Deemed-Owned Shares

• Disqualified Person (DP)– Individual who owns 10% of all Deemed-Owned shares– Member of family owning 20% of all Deemed-Owned shares

• Deemed-Owned shares include:– ESOP shares: actual and pro-rata share of suspense shares– Synthetic Equity:

» Determined by reference to shares» Determined by reference to deferred compensation» Determined by reference to rights to acquire interests in certain related

entities – Deemed -Owned shares do not include stock directly owned by the individual or

family

39

Tax Considerations

• Section 409(p) (continued)– Defining the Key Terms: Synthetic Equity

• Synthetic Equity that is determined by reference to shares– Warrants– Options– Restricted Stock– Deferred issuance stock right– Payments based on share value or appreciation such as phantom stock and SARs. – Person entitled to the Synthetic Equity is treated as owning the corresponding

number of shares of stock • Synthetic Equity that is determined by deferred compensation

– Includes right to receive property in a future year or transfer of property still subject to vesting at the end of the plan year of transfer

– Remuneration under and arrangement deferring compensation to a date more than 2 ½ months following the entity’s taxable year.

– Converted into shares by taking present value of deferred compensation / FMV of stock

40

Tax Considerations

• Section 409(p) (continued)– Defining the Key Terms: Synthetic Equity

• Synthetic Equity that is determined by reference to rights to acquire interests in certain related entities

– Includes right to acquire stock or similar interest in a related entity where:

» The related entity is the only significant assets of the S Corp; and

» The S Corp is the only significant owner of that related entity

41

Tax Considerations

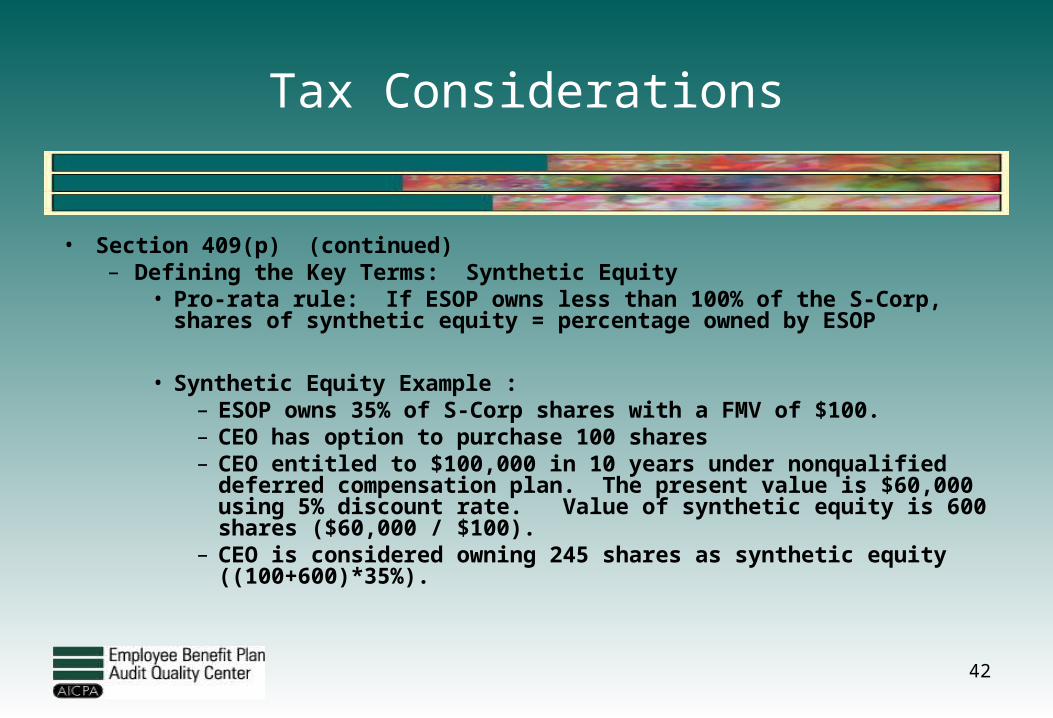

• Section 409(p) (continued)– Defining the Key Terms: Synthetic Equity

• Pro-rata rule: If ESOP owns less than 100% of the S-Corp, shares of synthetic equity = percentage owned by ESOP

• Synthetic Equity Example : – ESOP owns 35% of S-Corp shares with a FMV of $100.– CEO has option to purchase 100 shares – CEO entitled to $100,000 in 10 years under nonqualified deferred

compensation plan. The present value is $60,000 using 5% discount rate. Value of synthetic equity is 600 shares ($60,000 / $100).

– CEO is considered owning 245 shares as synthetic equity ((100+600)*35%).

42

Tax Considerations

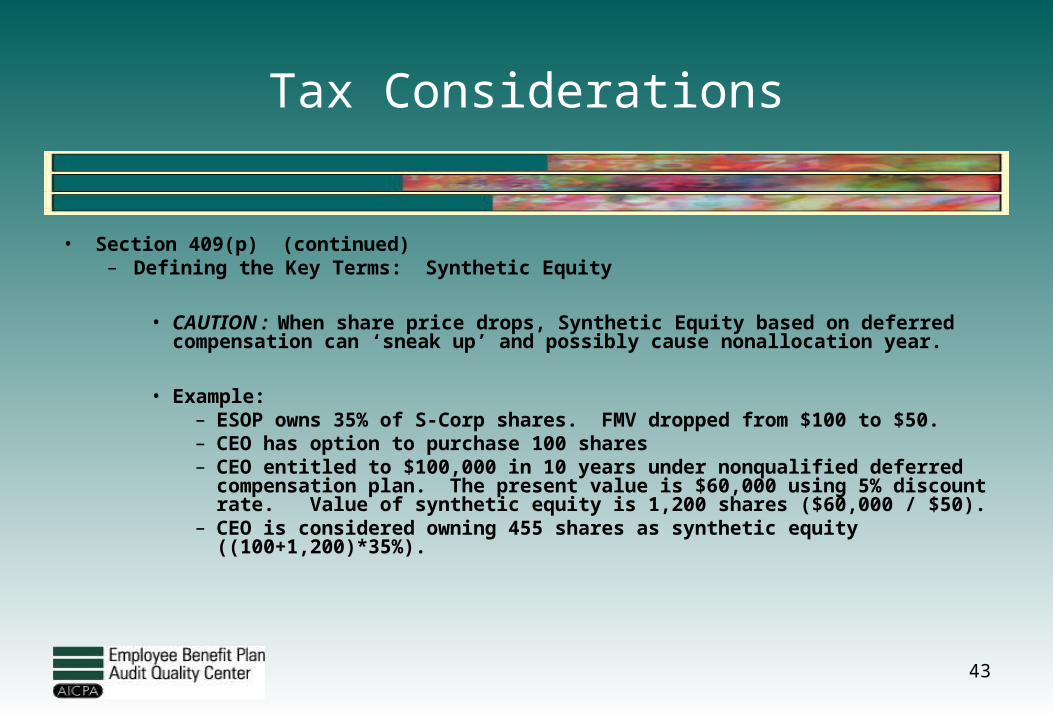

• Section 409(p) (continued)– Defining the Key Terms: Synthetic Equity

• CAUTION : When share price drops, Synthetic Equity based on deferred compensation can ‘sneak up’ and possibly cause nonallocation year.

• Example: – ESOP owns 35% of S-Corp shares. FMV dropped from $100 to $50.– CEO has option to purchase 100 shares – CEO entitled to $100,000 in 10 years under nonqualified deferred

compensation plan. The present value is $60,000 using 5% discount rate. Value of synthetic equity is 1,200 shares ($60,000 / $50).

– CEO is considered owning 455 shares as synthetic equity ((100+1,200)*35%).

43

Tax Considerations

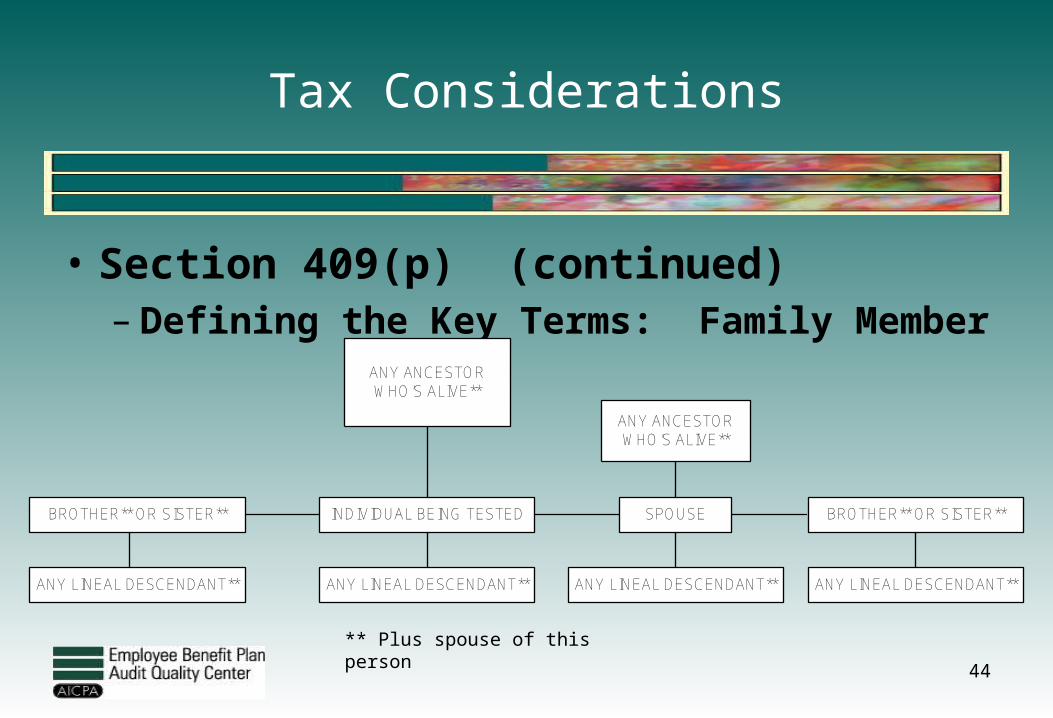

• Section 409(p) (continued)– Defining the Key Terms: Family Member

ANY ANCESTORWHO’S ALIVE**

ANY ANCESTORWHO’S ALIVE**

INDIVIDUAL BEING TESTED SPOUSEBROTHER** OR SISTER**

ANY LINEAL DESCENDANT**ANY LINEAL DESCENDANT** ANY LINEAL DESCENDANT**ANY LINEAL DESCENDANT**

BROTHER** OR SISTER**

** Plus spouse of this person

44

Section 409(p) Example

ESOP Shares DP % DP ?

Synthetic Equity

Synthetic Equity

(Pro-rata)

DP % w/ Synthetic

Equity

DP with Synthetic Equity?

Total ESOP & Deemed Owned

Shares for DP

A 18,000 18.00% Yes 0 0 18.00% Yes 18,000

B 12,500 12.50% Yes 0 0 12.50% Yes 12,500

C 10,000 10.00% Yes 0 0 10.00% Yes 10,000

D 7,500 7.5% No 52,500 21,000 23.55% Yes 28,500

Others 52,000 - - 0 0 52.00% -

E 0 0.00% No 125,000 50,000 33.33% Yes 50,000

Total DP

48,000 71,000 119,000Total 100,000 177,000 277,500

Total DP% 42.88% (119,000 / 277,500)

40% ESOP

45

Tax Considerations

• Section 409(p) (conclusion)– Correction/Preventive Measures

• Plan document includes procedure for transferring stock to a non-ESOP account within an ESOP to prevent a violation.

• Shares transferred results in UBTI but can be paid by redeeming shares out of the non-ESOP account.

• Exchange, reallocate or recharacterize assets if there is reasonable possibility nonallocation year will occur without taking action. This usually involves exchanging shares in DPs accounts for assets other than company stock held in non DP accounts.

• Eliminate or change the Synthetic Equity

46

Tax Considerations

• Diversification (IRC Sec. 401(a)(28))– Allows participants to reduce risk of having too much

allocated to employer stock • A Qualified Participant must be permitted, during the

Qualified Election Period, to diversify a certain percentage of their employer stock.

• Applies only to shares acquired after 1986 if plan so provides.

47

Tax Considerations

• Diversification (continued)– Qualified Participant

• Age 55 and 10 years of participation in the ESOP.– Definition of “Years of Participation” can be elusive. Does it

include years after termination of employment or just years which eligible for contribution? Absent specific definition in plan, most conservative approach is to count service while an inactive participant.

• Recent request for technical assistance issued by the IRS National office to the “ESOP Cadre” indicates that unless the plan contains an acceptable definition, a year of participation includes all years (or parts thereof) in which the participant had an account balance.

48

Tax Considerations

• Diversification (continued)– Qualified Election Period

• 6 Years • Starts with plan year after becoming a qualified participant • Election made in 90 day period following end of plan year and

can be revoked or modified during the 90 day period.• Participant’s election must then be implemented within 90 days

after the close of the election period. • Example:

– Calendar year plan. Participant becomes qualified participant in 2009. Initial election period is January 1 – March 31, 2010. Participant’s election implemented April 1 – June 30, 2010.

49

Tax Considerations

• Diversification (continued)– Shares eligible to diversify

• First 5 election periods: 25% of the shares ever allocated to the participant’s account less previously diversified shares.

• 6th election period: 25% is increased to 50%. • No diversification required if amount subject to

diversification is less than $500. Note: This really means that the shares ever allocated and subject to diversification are less that $500.

50

Tax Considerations

• Diversification (continued)– Implementing election

• Transfer within ESOP:– Must contain 3 investment options “not inconsistent with regulations

prescribed by the Secretary.” Interpreted to mean 3 diverse investment options within the meaning of 404(c).

– Not ‘recommended’ option due to participant directed investment requirements and fiduciary liability regarding monitoring investment options.

• Transfer to another plan sponsored by Employer– 3 investment options required– Best to track as separate source– Usually viable alternative when Sponsor has 401(k) plan.

• Permit distribution to participant – Can be rolled to IRA– Subject to 10% penalty if participant not 59 ½.

51

Tax Considerations

• Diversification (continued)– Practical Considerations

• Election period: 90 days following end of plan year. Election applies to shares allocated as of end of plan year preceding election period. Balances may not be available.

• Implementation period: 90 days following end of election period. Share value may not be known.

• Shares eligible for diversification: 25% (50%) of shares ever allocated less shares previously …. Shares ever allocated would include shares previously distributed, reallocated to other accounts or otherwise transferred.

• Less shares previously …. Notice 88-56 states “***; less the number of shares previously distributed, transferred, or diversified pursuant to a diversification election. Does this mean shares previously distributed or transferred for any reason or just shares that were distributed or transferred pursuant to a diversification election? Conservative approach would be to reduce shares that were previously diversified.

52

Valuation

53

David Bogus, ASA

Principal

Ellin and Tucker, Chartered

Standard of Value for Valuation Purposes

• The ESOP may not pay more than “adequate consideration” for employer company stock.

• ERISA defines adequate consideration as the “fair market value” of the asset (company stock) as determined in good faith by the trustee.

• DOL proposed regulations define fair market value as “the price at which an asset would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, and both parties are able, as well as willing, to trade and are informed about the asset and the market for such asset.”

• The IRS sets forth a similar definition for fair market value as “the price at which property would change hands between a willing buyer and a willing seller when neither is acting under compulsion and when both have reasonable knowledge of relevant facts.”

54

Standard of Value for GAAP Purposes

• ASC 820 (formerly SFAS 157) establishes “fair value” as the standard of value.

• Provides a single authoritative definition of fair value for financial reporting.

• Establishes a framework for making fair value measurements.

• Fair value is defined as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

• Market participants are independent of the reporting entity, knowledgeable, able to transact and willing to transact.

55

Entry Price Versus Exit Price

• ASC 820 describes fair value from the perspective of an exit (sale) price rather than an entry (purchase) price.

• Exit price is to be considered from the perspective of market participants in the principal (or most advantageous) market for the asset or liability.

• The principal market trumps the most advantageous market.

56

Highest and Best Use of an Asset

• A fair value measurement also assumes the highest and best use of an asset from the perspective of market participants, regardless of intended use.

• It also requires considering that the use of the asset is: (i) physically possible; (ii) legally permissible; and (iii) financially feasible.

• Highest and best use is based on the use of the asset and generally results in maximizing the value. As such, the valuation premise may be either “In-Use” or “In-Exchange.”

57

Fair Value Hierarchy

• ASC 820 specifies a hierarchy approach to determining fair value based on Level I, Level II or Level III inputs.

• Level 1 – Inputs are observable market inputs that reflect quoted prices for identical assets or liabilities.

• Level 2 – Inputs are observable market inputs other than quoted prices for identical assets or liabilities (i.e. quoted prices for similar assets, quoted prices for identical assets in markets that are not active).

• Level 3 – Inputs are unobservable market inputs.

58

Valuation Approaches

• Cost (or Asset) Approach

• Income Approach

• Market Approach

59

Cost Approach

• A general way of determining a value indication of a business, business ownership interest, or security by using one or more methods based on the value of the assets of that business net of liabilities.

• Based on the economic principle of substitution.• Least commonly applied approach for valuing ESOP

shares.

60

Income Approach

• A general way of determining a value indication of a business, business ownership interest, security, or intangible asset using one or more methods that convert anticipated benefits into a present single amount.

• Based on the economic principle of anticipation (expectation).• Direct capitalization method – the capitalization (i.e. the division by an

appropriate rate of return) of a constant or a constantly changing stream of economic income.

• Yield capitalization – the present value of a non-constant stream of projected economic income.

61

Market Approach

• A general way of determining a value indication of a business, business ownership interest, security, or intangible asset by using one or more methods that compare the subject to similar businesses, business ownership interests, securities, or intangible assets that have been sold.

• Based upon the related economic principals of competition and equilibrium. That is, in a free and unrestricted market, supply and demand factors will drive the price to a point of equilibrium.

62

SAS No. 73 – Using the Work of a Specialist

• SAS No. 73 provides guidance to the auditor who uses the work of a specialist in performing an audit in accordance with GAAP.

• The auditor should consider various factors when evaluating the professional qualifications of the specialist.

• The auditor should obtain an understanding of the nature of the work performed or to be performed by the specialist.

• What if the auditor believes the findings of the valuation specialist are unreasonable?

• What if the valuation specialist currently engaged by the ESOP was engaged by either the company and/or the selling shareholder to perform similar (valuation) services prior to the formation of the ESOP?

63

SAS No. 101 – Auditing Fair Value Measurements and Disclosures

• The auditor should obtain an understanding of the entity’s process for determining fair value measurements and disclosures.

• The auditor should evaluate whether the fair value measurements and disclosures are in conformity with GAAP.

• What if auditor requests a copy of the valuation report? Should it be provided? Who should provide it?

• See “White Paper on Recommended Procedure for ESOP Companies in Response to Auditors Request for ESOP Valuation Report.” Prepared by a Task Force of The ESOP Association’s Interdisciplinary Advisory Committee on Fiduciary Issues for members of The ESOP Association.

64

ERISA Requirements

• IRC 401(a) requires annual valuation of ESOP shares. • Form 5500 questions include: (i) whether any non-cash contributions

(i.e. closely-held stock) were made to the plan, the value of which was set without an appraisal by an independent third party; and (ii) whether the plan holds any non-publicly traded securities that were not appraised by an independent third-party.

• A problem may exist if “YES” is the answer to any of the above.

65

Guidance for Determining Value

• Revenue Ruling 59-60 provides methods for valuing shares of stock of closely-held corporations for estate and gift tax purposes. However, the factors may be used to determine values of assets in qualified plans.

• Examination steps of determined value.• When appropriate, stock values should be discounted due to a lack of

marketability and, if appropriate, a control premium should be added to the stock value.

66

Typical Valuation Questions

• Determination of multiples from guideline public company method

• Reliance/use of management forecasts

• Application of premiums and/or discounts

• Terminal value calculation in discounted cash flow analysis

67

Timing of Valuation

• DOL regulations require that fair market value be determined as of the date of the ESOP transaction.

• Typical annual valuations for ESOP administration purposes are typically done the last day of the plan year.

• What if the ESOP purchases, or sells, shares of company stock during the following year?

68

ESOP Plan Accounting and Financial Reporting

Hal J. Hunt, CPAPartner

Mayer Hoffman McCann P.C.

69

ESOP Plan Accounting and Financial Reporting Topics for Discussion

• GAAP for ESOP Plans• Leveraged ESOP Plan Financial Statement

Presentations• Reconciliation to Participant Accounts• ESOP Plan Footnotes• Other ESOP Accounting and Financial Reporting

Matters• Resources

70

GAAP For ESOP Plans

• A&A Guide Chapter 3 GAAP for defined contribution plans (FASB ASC 962, Plan Accounting–Defined Contribution Pension Plans)

• Topic 962 prescribes the general form and content of financial statements of these plans

• A&A Guide Appendix E.Ill, Illustrations of Financial Statements: Employee Stock Ownership Plans (See Exhibits E-7, E-8 and E-9)

71

GAAP For ESOP Plans

• Other GAAP may also apply to defined contribution plans (ESOPs) as described on the following slides

72

GAAP for ESOP Plans

FASB ASC 820, Fair Value Measurements and Disclosures

FASB ASC 825, Financial Instruments (as it relates to ESOP debt obligations) may require additional disclosures about financial instruments such as fair value, concentrations of credit risk and market risk

73

GAAP for ESOP Plans

However, Topic 825 applies to all entities but is optional (FASB ASC 825-10-50-3) for an entity that meets all of the following criteria: the entity is a nonpublic entity and the entity's total assets are less than $100 million on

the date of the financial statements and the entity has no instrument that, in whole or in part, is

accounted for as a derivative instrument under Topic 815

74

Leveraged ESOP Plan Financial Statement Presentation

A&A Guide Appendix E.III, Illustrations of Financial Statements: Employee Stock Ownership Plan, Exhibit E-7 • Unallocated - Shares and other assets

available as collateral on loan• Allocated - Shares and other assets released

from collateral

75

Leveraged ESOP Plan Financial Statement Presentation

A&A Guide Appendix E.III, Illustrations of Financial Statements: Employee Stock Ownership Plan, Exhibit E-7 footnote 1:

• The columns reflected in the example are appropriate for the presentation of a leveraged ESOP. For a nonleveraged ESOP, the presentation would reflect only the total column without the segregation between allocate and unallocated.

• Allocated and unallocated designations distinguish between assets that belong to plan participants and those that are still available as collateral for the ESOP loan. Under the Employee Retirement Income Security Act of 1974 (ERISA), the lender has access to the securities held by the plan, that represent unallocated employer contributions to service the debt, and any earnings on those amounts. Earnings on temporary cash investments also are available to the lender.

• An accrued employer contribution for current or future debt service is, therefore, reflected on the Statement of Net Assets Available for Benefits and the Statement of Changes in Net Assets Available for Benefits in the Unallocated column. In contrast, an employer contribution accrued to fund distributions to terminated participants is reflected in the Allocated column.

• This distinction is not reflected in the participant account balances when reporting to the participant under ERISA. Contributions accrued for future debt service are allocated to the accounts of plan participants.

76

Reconciliation to Participant Accounts

• Non-leveraged ESOPs--net assets available to pay plan benefits should reconcile to the sum of the participant accounts

• Leveraged ESOPs--a reconciliation from participant accounts to allocated column on ESOP financial statements may be necessary and common reconciling items include:– Share release– Accrued contribution for debt service– Accrued dividends for debt service– Interest expense

77

Reconciliation to Participant Accounts

• Shares “Released” versus Shares “Allocated”:– Shares are released when the contribution is made and applied to

debt service.– Shares may be allocated at this same time or earlier, upon accrual

of contribution– Contribution for current year debt service is allocated to

participants in the plan’s records• Contribution revenue remains in “unallocated” column as it is

available to make payments on the loan– Dividends on unallocated shares can be used for debt service

• Dividends on allocated shares also can be used for debt service, but remain in the allocated column

78

Reconciliation to Participant Accounts (Exhibit E-8 of the Guide)

79

a Total Allocated at year end per F/S $ 35,616,000b Accrued Employer contribution for debt service 8,607,000c Accrued Dividends on collateral 459,000d Accrued interest expense -1,396,000e Total allocated per participant accounts 43,286,000f Total ESOP $ 27,609,000

FMV of Stock and Cash Held as Collateral 58,293,000Debt -73,970,000

g Difference – net fair value of collateral -15,677,000 -15,677,000h Reconciliation ( e - f + g ) 0

ESOP Plan Footnotes

• Plan Description and/or Summary of Significant Accounting Policies Footnote to include:– Voting rights– Participant accounts—allocated and unallocated– Release of shares--principal and interest versus principal only– Put Option--Put to sponsor is not a plan transaction– Diversification– Valuation of company stock– Tax Status

80

ESOP Plan Footnotes

• Investment in Company Stock Footnote to include:– Number of shares—allocated and unallocated– Cost of shares—allocated and unallocated– Estimated Fair Value—allocated and

unallocated

81

ESOP Plan Footnotes

• Fair Value Measurements (Topic 820) Footnote to include:– Valuation methodologies– Identification of plan assets and related Fair

Value Hierarchy Levels– Reconciliation of Fair Value Level III assets for

the period(s)

82

ESOP Plan Footnotes

A&A Guide Exhibit E-9, Note F entitled Fair Value Measurements:

The fair value of the XYZ company common stock held by the plan is valued at estimated fair value based upon an independent appraisal. This appraisal was based upon a combination of the market and income valuation techniques consistent with prior years. The appraiser took into account historical and projected cash flow and net income, return on assets, return on equity, market comparables and estimated fair value of company assets and liabilities. The preceding methods described may produce a fair value calculation that may not be indicative of net realizable value or reflective of future fair values. Furthermore, although the plan believes its valuation methods are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of certain financial instruments could result in a different fair value measurement at the reporting date.

83

ESOP Plan Footnotes

A&A Guide Exhibit E-9, Note G entitled Loan Payable:

In 20XX, the plan entered into an $80 million term loan agreement with a bank. The proceeds of the loan were used to purchase company's common stock. Unallocated shares are collateral for the loan. The agreement provides for the loan to be repaid over ten years. The estimated fair market value of the note payable as of December 31, 20X2 and 20X1 was approximately $77 million and $82 million, respectively, determined by using interest rates currently available for issuance of debt with similar terms, maturity dates and nonperformance risk. The scheduled amortization of the loan for the next five years and thereafter is as follows: 20X3—$6.5 million; 20X4—$7 million; 20X5—$7.5 million; 20X6—$8 million; 20X7—$8.5 million; and thereafter—$36.5 million. The loan bears interest at the prime rate of the lender. For 20X2 and 20X1 the loan interest rate averaged 7.34 percent and 5.12 percent, respectively.

84

ESOP Plan Footnotes

A&A Guide Exhibit E-9, Note H entitled Employer Contributions:

The company is obligated to make contributions in cash to the plan which, when aggregated with the plan's dividends and interest earnings, equal the amount necessary to enable the plan to make its regularly scheduled payments of principal and interest due on its term loan.

85

ESOP Plan Footnotes

A receivable from the employer must meet requirements of FASB ASC 960-310-25-2:

Employer’s contribution receivables are amounts due as of the report date. Amounts due include those pursuant to formal commitments and legal obligations. Evidence of a formal commitment may include (a) a resolution by the employer’s governing body approving a specific contribution, (b) a consistent pattern of making payments after the plan’s year-end pursuant to an established funding policy that attributes such subsequent payments to the preceding plan year, (c) a deduction of a contribution for federal tax purposes for periods ending on or before the reporting date, or (d) the employer’s recognition as of the report date of a contribution payable to the plan.

86

Other ESOP Accounting and Financial Reporting Matters

• Other Regulatory Issues:– SEC/PCAOB related to S-8 Registration of

ESOP shares and Form 11-K Filings– An ESOP is required to register, and be

regulated, as a bank holding company before acquiring control of 25 percent or more of any class of voting securities of a bank or bank holding company

87

ESOP Accounting and Financial Reporting Resources

• 2010 AICPA Audit & Accounting Guide, Employee Benefit Plans – to be available in May 2010

• 2010 Audit Risk Alert for Employee Benefit Plans – to be available in May 2010

• EBPAQC Authoritative Accounting and Reporting Standards For Employee Benefit Plans: FASB Accounting Standards Codification™

88

Question & Answer Session

Submit questions in the box on the left-hand side of the screen

89

Upcoming Events

• AICPA Annual Webcast on Employee Benefit Plans Strategic Briefing, April 28, 2010, 2:00 – 4:00 pm ET

• AICPA National Conference on Employee Benefit Plans, Las Vegas, NV, May 11 – 13, 2010

• AICPA Employee Benefit Plan Audit Workshop for Defined Benefit and Defined Contribution Plans, March 29 – 30, 2010, Chicago, Illinois; July 26 – 27, 2010, New York, New York

• AICPA Annual Employee Benefit Plans Accounting, Auditing and Regulatory Update Conference, Washington, DC, December 13 – 14, 2010

90

Employee Benefit Plan Audit Quality Center

Thanks for Participating!

91