easyFairs innovations in packaging pan-european … · Apple and Coca-Cola tied for top spot...

14

sponsored by easyFairs ® innovations in packaging pan-european survey 2012 an investigation into the drivers of change

-

Upload

phungthuan -

Category

Documents

-

view

213 -

download

0

Transcript of easyFairs innovations in packaging pan-european … · Apple and Coca-Cola tied for top spot...

sponsored by

easyFairs® innovations in packaging pan-european survey 2012an investigation into the drivers of change

About easyFairs®

easyFairs is the world’s leading organiser of time & cost-effective trade shows and is part of the Artexis Group.For more information visit us at www.easyFairs.com

easyFairs SA/NVRue Saint-Lambert 135 1200 Brussels Belgium Phone +32 (0)2 740 10 70 Fax +32 (0)2 740 10 75

innovations in packaging 2012 I 1

easyFairs® innovations in packaging pan-european survey 2012

It is a great honour to be listed as a “thought leader” on packaging. Whatever the list tells us, the survey is a signal that the packaging profession is maturing. And this in particular gives me a good feeling. Packaging design is much more than what you see on the outside. To create new packaging requires a lot of engineering and insight into many processes. Packaging is continuously on the move because it is being influenced by many other disciplines such as printing techniques, logistics, food

technology, engineering, process engineering, material innovations and machine developments, to mention a few. A designer or engineer cannot develop packaging in isolation any more. Many aspects have to be considered. Therefore, we need to view the world of packaging in a more structured way. This survey is already a good start to get more insight and is a next step towards maturity.

Having a chair at University Twente provides the opportunity to work on this and look at packaging from multiple perspectives. Students are very helpful in this, because they have an open mind and live in a dynamic world. Alongside this academic endeavour, it is good to be involved on many packaging design projects at the office of Plato product consultants. I hope this combination of lecturing and design consultancy will attract others to focus on this field of activity and become influencers on packaging as well.

Roland ten Klooster Professor at the University Twente – Packaging Design and Management www.utwente.nl Consultant and Designer at Plato product consultants www.platopc.nl

It’s hard to think of any business that combines technical wizardry, beauty and practicality in quite the same way as packaging. Whether it’s the latest easy-open lid, a fabulous new graphic design or an ingenious cost-saving material, there can be few businesses that have the innovative energy of packaging.

But understanding what is driving those changes, which factors are behind the packaging decisions of the technologists, designers, marketers and product developers, is crucial to everyone. For professionals working at brand owners and retailers, it helps understand where they stand compared to their competitors. For professionals working at packaging manufacturers, design agencies and materials firms, it is crucial to helping them understand what makes their customers tick.

That’s why Packaging News is delighted to be supporting this new pan-European study on packaging innovation, and the people making it happen, from easyFairs. We hope you will find it as enlightening as we have.

Josh Brooks Brand Director, Packaging News and packagingnews.co.uk

foreword

contentsExecutive Summary 2

Survey Demographics 3

Thought Leaders 11

Most Influential Brands 11

Frequency of Packaging Revamps 12

Likelihood that Budgets will Increase 14

The Spirit of Innovation 15

Plans to Innovate in the Coming 12 months 16

Most Important Drivers of Innovation 17

Packaging Materials: What’s Hot and What’s Not 18

Sources of Inspiration 21

Cost and the Environment Expected to Drive Future Innovation 22

Approach to Environmental Packaging 23

The Germans are Europe’s Sustainability Champions 24

Acknowledgements 25

innovations in packaging 2012 I 3

easyFairs® innovations in packaging pan-european survey 2012

2589 packaging professionals took part in the easyFairs Innovations in Packaging Survey 2012.

The survey was conducted in June 2012. Emails were sent to people who have attended or

exhibited at easyFairs packaging trade shows. The survey questionnaire was sent in six languages

(English, Dutch, German, Spanish, French and Swedish). Replies were received from packaging

professionals in 16 European countries. The distribution largely reflects easyFairs’ market presence

in these countries, with the Netherlands, Spain, Belgium, Germany, Switzerland, Sweden, the

United Kingdom and Austria accounting for 90% of completed questionnaires. Other countries

represented were Norway, Ireland, Denmark, France, Portugal, Poland, Finland and Italy.

The survey covered all stakeholders in packaging. Suppliers of packaging, packaging materials,

packaging machinery and packaging services accounted for the largest single sector (23%). The

graphical industry accounted for 8% of the total and logistics suppliers for a further 3%. The food

& drink industry was the largest packaging consumer sector, accounting for 18% of respondents,

followed by industrial goods (7%), pharmaceutical & medical and chemicals (each 5%), cosmetics

& perfumery (3%) and retail and wholesale (3%).

survey demographics

survey respondents by country (total: 2589)

Figure 1: Survey Respondents by Country

20%

19%

15%11%

10%

9%

6%4% 1% NL

Spain

Belgium

Germany

CH

Sweden

UK

Austria

Norway

Other

Ireland

Denmark

France

executive summary

• Roland ten Klooster is Europe’s Packaging “Thought Leader”

• The most respected brands among packaging experts are Apple and Coca-Cola

• Two-thirds of packaging consumer companies currently revamp their packaging more often than once every two years; large companies rather more frequently; medium-sized companies change their packaging less frequently than the very large and the very small

• Household & non-food FMCG packaging consumers update most frequently

• Most packaging professionals (54%) believe their packaging budget will remain unchanged over the coming year. Of the remainder, more expect an increase than expect a decrease

• 57% of respondents regard their companies as radical or incremental innovators; the rest regard themselves as being in line with market norms

• Graphical changes to existing pack formats are the most common form of updates to packaging; the application of new materials is the second most common

• Cost reduction is the most important driver of innovation at the moment, followed by the desire to enhance a brand’s image

• The environment is expected to play a leading role as a driver of innovation over the next five to ten years

• Biodegradables are no longer seen as a fad; on the contrary, they are seen as the materials of the future

• Packaging professionals also regard paper and flexibles as the materials that will become increasingly important

• Mixed materials look to be stable; plastics and PET are mostly regarded as stable but sentiment is overall positive; glass, metal and wood will experience a more significant decline

• The two most significant sources of inspiration are suppliers of packaging and visiting trade shows (there is a strong correlation between the two)

• Sustainability is increasingly important Nearly half of the respondents (47%) regard environmental responsibility as a part of their brand identity

• Germany is Europe’s clear leader on the issue of sustainability in packaging

“Roland ten Klooster is Europe’s Packaging Thought Leader”

“Cost reduction is the most important driver of innovation”

“Environmental responsibility is increasingly important”

survey respondents by sector (total: 2481)

Figure 2: Survey Respondents by Sector

Packaging

Food & drink

Graphical industry and design

Industrial goods

Pharmaceuticals and medical

Chemicals

Logistics

Services and IT

Cosmetics & perfumery

Retail & wholesale

Household & non-food FMCG, toys

Construction

Agri-industry

Automotive

Mechanical engineering

Fashion, footwear & textiles

Electrical & electronic

Marketing services

Giftware

Toiletries

Other

18%

8%8%5%

5%4%3%3%

3%2%

2%

2%2%

1%1%5%

2%

23%

innovations in packaging 2012 I 5

easyFairs® innovations in packaging pan-european survey 2012

food & drink respondents by sub-sector (total: 457)

Figure 3: Food & Drink Survey Respondents by Sub-Sector

Food - dairy

Food - other

Food - chilled

Food - confectionery

Food - bakery

Drinks - alcoholic

Food - crisps & snacks

Food - frozen

Food - fast food

Food - luxury & gourmet

Drinks - non-alcoholic

Food - meat, fish and poultry

Food - pet food

Tobacco

14%

13%

12%

10%9%

8%

8%

6%

5%5%

5% 2% 2% 1%

innovations in packaging 2012 I 7

Within the food & drinks sector, dairy was the largest sub-sector, accounting for 14%, followed

by other foods (13%), chilled foods (12%), confectionery (10%) and bakery (9%). Alcoholic drinks

accounted for 8% of the food & drink total.

survey respondents by function (total: 2589)

The survey population was also representative of a broad spread of packaging stakeholders.

Operations, packaging & logistics accounted for the largest segment (26%) followed by general

management (this included managing directors and owners, financial controllers, HR managers

etc, 23%) and marketing & brand management (16%). Designers (10%), consultants (9%), sales

(6%), purchasing & procurement (3%) and R&D and innovation (3%) accounted for most other

functions.

Figure 4: Survey Respondents by Job Function

Operations, production & logistics

General management

Marketing & brand management

Design

Consultant

Sales

Purchasing & procurement

R&D and innovation

Other general

Packaging management & technology

Other technical

Quality control

the survey was broadly representative

26%

23%

16%

10%

9%

6%

3%3% 2%

innovations in packaging 2012 I 9

1%1%

innovations in packaging 2012 I 11

easyFairs® innovations in packaging pan-european survey 2012

survey respondents by company size (total: 2459)

thought leaders

most influential brands

The survey population represents all sizes of company from single-trader consultancies to

multinational corporations with more than 1,000 employees. Medium-sized companies are

strongly represented.

We asked packaging professionals whom they considered the most influential people in their

sector in Europe. The most frequently named individual (by far, partly reflecting the large

number of participants in the Benelux) was Roland ten Klooster, Professor Packaging Design &

Management at the University of Twente. Ranked equal second were Lars Wallentin, author and

former packaging design guru at Nestlé and the late Steve Jobs, founder of Apple. The President

of the United Kingdom’s Packaging Federation, Dick Searle, and the designer and architect Philippe

Starck tied for fourth place.

• Roland ten Klooster• Lars G Wallentin• Steve Jobs• Dick Searle• Philippe Starck

We also asked the survey population which they considered to be the most influential brands in

the packaging industry in Europe. Apple and Coca-Cola tied for top spot followed by Nespresso.

Here are the top ten brands nominated by our respondents:1 to 10

11 to 25

26 to 50

51 to 100

101 to 250

251 to 500

501 to 1000

More than 1000 • Apple• Coca-Cola• Nespresso• Danone• Absolut

• Heineken• Tetra Pak• Nestlé• HAK• Unilever

Figure 5: Survey Respondents by Company Size

19%

11%

12%

11%16%

10%

6%

15%

innovations in packaging 2012 I 13

easyFairs® innovations in packaging pan-european survey 2012

frequency of packaging revamps

how often do you change your packaging? (total: 1325)

how often do you change your packaging? (largest companies, total: 206)

We received 1325 valid replies (mostly from packaging consumer companies) to the question,

“How often do you currently change or update your product packaging?” Nearly two-thirds of

respondents (66%) stated that they change their packaging at least once every two years, with

nearly a fifth (19%) stating that they change their packaging at least once every six months.

Smaller companies (up to 50 employees) change or update their packaging less frequently but

only marginally so, with 18% saying that they update at least once every six months. Only a third

of the respondents update their packaging less frequently than once every two years.

The largest companies (with more than 1000 employees) change their packaging more frequently

than the average, with 70% making updates at least once every two years, and 22% updating at

least once every six months.

At least once every 6 months

Every 6 to 12 months

Every 12 months to 2 years

Every 2 years or more

Figure 6: Frequency of Change, All Companies

Figure 7: Frequency of Change, Largest Companies

Figure 8: Frequency of Change, Smallest Companies

The survey suggests that the companies that are slowest to change and update their packaging

are mid-sized enterprises with between 51 and 1000 employees; more than two-thirds (67%)

of these change their packaging less than once a year, and well over a third (37%) change it less

frequently than every two years.

As one would expect, there are significant variations between sectors. In our survey, respondents

from the cosmetics & perfumery sector were most likely to make changes at least once every six

months – 26% of respondents. 80% make changes at least once every two years.

At the other end of the scale, only 53% of respondents from the industrial goods sector say their

companies revamp their packaging at least once every two years and only 8% make changes

more frequently than once every six months.

In the pharmaceuticals & medical sector, 23% of respondents reported that their companies make

changes to packaging at least once every six months. Food & drink companies make slightly less

frequent changes.

The sector that makes most frequent changes overall is household & non-food FMCG, with 47%

of companies making changes or updates at least once a year.

19%

16%

31%34%

22%

19%

29%30%

At least once every 6 months

Every 6 to 12 months

Every 12 months to 2 years

Every 2 years or more

how often do you change your packaging? (up to 50 employees, total: 495)

how often do you change your packaging? (medium sized companies, total: 624)

At least once every 6 months

Every 6 to 12 months

Every 12 months to 2 years

Every 2 years or more

18%17%

32%

33%

Figure 9: Frequency of Change, Medium Companies

At least once every 6 months

Every 6 to 12 months

Every 12 months to 2 years

Every 2 years or more

18%15%

30%

37%

innovations in packaging 2012 I 15

easyFairs® innovations in packaging pan-european survey 2012

Figure 10: Frequency of Change, Household & Non-Food

change frequency - household & non-food

do you expect your packaging budget to increase? (total: 1535)

25%

30%

22%

At least once every 6 months

Every 6 to 12 months

Every 12 months to 2 years

Every 2 years or more

23%

likelihood that budgets will increaseDespite the recession that is biting hard in many European domestic markets, investment in packaging

is holding up well. We asked respondents if, in the next 12 months, they expected their budget for

packaging innovation to increase, decrease, or stay the same. Only 12% forecast a decrease in budgets,

with 34% expecting an increase. A slight majority expects budgets to stay the same.

There are wide divergences in expectations between sectors. Nearly half (42%) of food & drink

companies expect to see an increase in investment in packaging over the next 12 months,

compared with just 30% in cosmetics & perfumery. Pharmaceutical & medical companies are more

likely to expect their budgets to stay the same (55%) or decrease (18%).

Increase

Decrease

Stay the same

Figure 11: Expectations of Budget of food & drink companies expect to see an increase in investment in packaging over the next 12 months42%

Figure 12: Radical and Incremental Innovators and Followers

the spirit of innovation

The spirit of innovation is alive in European packaging. We asked the survey population if they

considered their companies to be radical innovators, incremental innovators or just the same

as the competition. A clear majority (57%) consider themselves to be innovators with nearly a

quarter (24%) seeing themselves as radical innovators.

level of innovation (total: 1666)

The food & drink sector sees itself as marginally less innovative than average. By contrast, a

majority of cosmetics & perfumery companies are conservative in their approach, with only 17%

seeing themselves as radical innovators.

Perceptions change by country. In Germany, a very high proportion of companies (45%) see

themselves as incremental innovators while only 38% are happy to change at the same pace as

the competition. In Switzerland, 48% of companies see themselves as incremental innovators and

36% as the same as competitors.

By contrast, in the Nordic countries (Sweden, Norway, Denmark and Finland) there are more

radical innovators (25%) yet the majority (52%) simply aim to match the competition.

Nearly a third of UK-based respondents (32%) regard their companies as radical innovators.

Benelux-based respondents see themselves as slightly more innovative than the average, with 41%

regarding their companies as in line with the competition.

Radical innovator

Incremental innovator

Same as competitors

24%

43% 33%

consider themselves to be innovators57%

34%

12%

54%

innovations in packaging 2012 I 17

easyFairs® innovations in packaging pan-european survey 2012

plans to innovate in the coming 12 months most important drivers of innovation

We asked the survey population about its plans to make changes over the next 12 months.

This confirmed the finding that change is mostly of an incremental nature. Graphical changes to

existing pack formats are the most common, mentioned by 709 respondents, and a substantial

number of companies (580 respondents) plan changes in materials. 261 respondents said they

planned to renew their entire packaging.

Unsurprisingly in the year of the Diamond Jubilee and the London Olympics, UK-based

respondents are more likely to be introducing designs related to events. 23% said they would do

so, compared to 18% in Germany and just 7% in Benelux countries.

We asked packaging professionals, “Which of the following considerations are currently driving your

packaging decisions?” They could choose the three most important of nine drivers.

Cost reduction is the most important driver of change according to our survey population, closely

followed by brand image. Despite claims of “greenwashing” by critics of packaging, a very high

proportion of respondents named environmental considerations as an important driver, almost as

important as brand image.

Legislation and regulations are less important than one might imagine (these are often cited as burdens

on the packaging community). Perhaps most surprising of all is the weak influence of demographic

factors such as the ageing population or the increasing number of single-person households. These

developments clearly have very little impact on the packaging community’s business strategies and it

may be that companies will have to adjust in future.

Figure 14: Innovation Drivers

Cost reduction

Enhanced brand image

Environmental impact

Improved product performance

Improved shelf standout

Tamper evidence/product security

Faster plant throughput

Regulatory/legislation

Demographics

0 100 200 300 400 500 600 700 800 900

Figure 13: Planned Changes

Make graphical changes to pack formats

Introduce new materials

Make structural changes to pack formats

Introduce new technology e.g. RFID

Renew your entire packaging

Introduce new inks or coatings

Introduce designs related to events

0 100 200 300 400 500 600 700 800

innovations in packaging 2012 I 19

easyFairs® innovations in packaging pan-european survey 2012

packaging materials: what’s hot and what’s not

biodegradables (total:1218)

paper (total: 1434)

We asked packaging professionals to give their opinion on which materials are increasing in

importance, which are in decline and which are stable.

Unsurprisingly biodegradable materials are very much in the ascendancy, with 75% of respondents

stating that they are increasing in importance and only 5% stating that they are in decline.

Plastics and PET are viewed as mainly stable, but with those who say they are increasing in

importance outnumbering those who say they are in decline.

The other big winner in the survey is paper, with 47% stating that its importance is increasing

and only 8% that it is in decline.

The sentiment about flexibles and film materials is highly positive.

Respondents are divided over the future of mixed materials.

The future for glass, wood and metal appears to be less assured.

Increase

Decline

Stable

Increase

Decline

Stable

Figure 15: Biodegradables

Figure 16: Paper

plastic (total: 1352)

wood (total: 1144)

flexi & film (total: 1268)

mixed materials(total: 1108)

Increase

Decline

Stable

Increase

Decline

Stable

Increase

Decline

Stable

Increase

Decline

Stable

pet (total: 1220)

metal (total: 1122)

Increase

Decline

Stable

Increase

Decline

Stable

glass (total: 1152)

Increase

Decline

Stable

26%

15%

47%

35%29%

43%

9%

17%

45%

42%

26%

22%

52%

44%

48%

45%

53%

13%

42%

40%45%

47%

8%

Figure 17: Plastic

Figure 19: Flexi & Film

Figure 21: Wood

Figure 23: Mixed Materials

Figure 18 : PET

Figure 20 : Glass

Figure 22 : Metal

75%

5%

20%

7%

innovations in packaging 2012 I 21

easyFairs® innovations in packaging pan-european survey 2012

Other

0 200 400 600 800 1000Figure 24: Sources of Inspiration

Suppliers of packaging

Visiting trade shows

Competitors

Internal marketing staff

Internal production staff

Media, off & online

Branding and design agencies

Attending seminars & conferences

sources of inspirationWe asked packaging professionals where or whom they turn to for inspiration, again giving them

the opportunity to choose up to three from nine options.

Suppliers of packaging are the most frequently named source of inspiration, followed closely by

visiting trade shows. Many companies watch and analyse the competition as a source of insight.

Of those who named unprompted sources of inspiration (“Other”) a significant proportion

mentioned customer feedback, consumer research and personal insight and experience.

many companies visit trade shows as a source of inspiration and insight

innovations in packaging 2012 I 23

easyFairs® innovations in packaging pan-european survey 2012

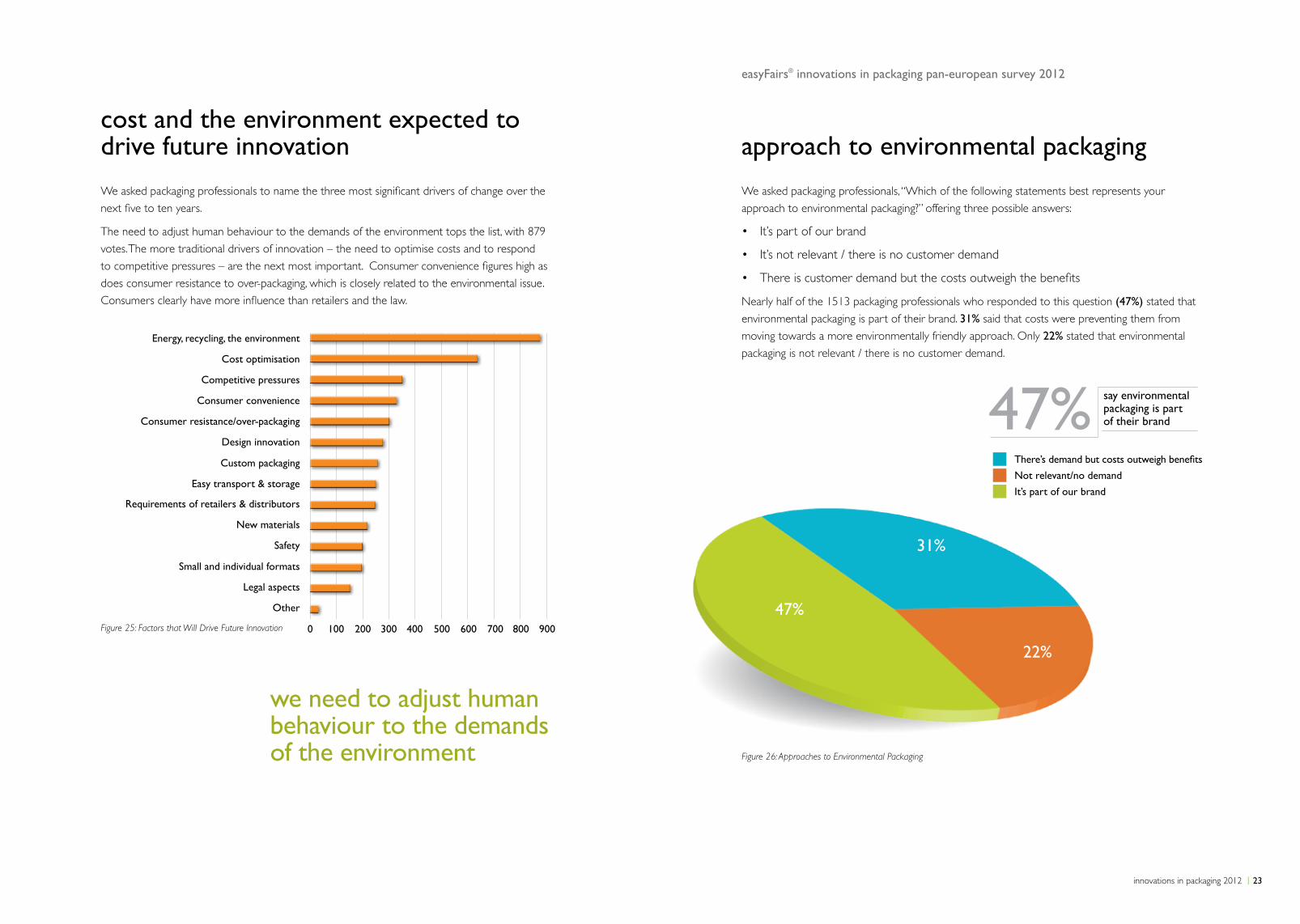

cost and the environment expected to drive future innovation approach to environmental packaging

we need to adjust human behaviour to the demands of the environment

We asked packaging professionals to name the three most significant drivers of change over the

next five to ten years.

The need to adjust human behaviour to the demands of the environment tops the list, with 879

votes. The more traditional drivers of innovation – the need to optimise costs and to respond

to competitive pressures – are the next most important. Consumer convenience figures high as

does consumer resistance to over-packaging, which is closely related to the environmental issue.

Consumers clearly have more influence than retailers and the law.

We asked packaging professionals, “Which of the following statements best represents your

approach to environmental packaging?” offering three possible answers:

• It’s part of our brand

• It’s not relevant / there is no customer demand

• There is customer demand but the costs outweigh the benefits

Nearly half of the 1513 packaging professionals who responded to this question (47%) stated that

environmental packaging is part of their brand. 31% said that costs were preventing them from

moving towards a more environmentally friendly approach. Only 22% stated that environmental

packaging is not relevant / there is no customer demand.Energy, recycling, the environment

Cost optimisation

Competitive pressures

Consumer convenience

Requirements of retailers & distributors

Consumer resistance/over-packaging

New materials

Custom packaging

Small and individual formats

Legal aspects

Design innovation

Safety

Easy transport & storage

Other

0 100 200 300 400 500 600 700 800 900Figure 25: Factors that Will Drive Future Innovation

Figure 26: Approaches to Environmental Packaging

say environmental packaging is part of their brand47%

There’s demand but costs outweigh benefits

Not relevant/no demand

It’s part of our brand

31%

22%

47%

the germans are europe’s sustainability champions

Finally, we asked packaging professionals “Which European country (apart from your own) do you

think takes sustainability in packaging most seriously?” We received 1512 valid responses.

While not all respondents respected the rule against voting for their own country, the outcome

was not in question: it was overwhelming endorsement of Germany’s efforts to embrace a

sustainable approach to packaging. Other northern European countries regarded by respondents

as doing relatively well are the Nordics, Switzerland and the United Kingdom.

Acknowledgements

Thanks to Ed Walker of Ed Walker Communications and Emeline Zagaroli for their help in compiling this report.Design by MSX Design Associates.

0 100 200 300 400 500 600

Germany

Sweden

Switzerland

Denmark

United Kingdom

Finland

Norway

France

Other

Italy

Spain

Netherlands

Belgium

Ireland

Austria

Figure 27: Which Countries Take Sustainability Most Seriously?