EAST ASIA AND PACIFIC INFRASTRUCTURE...

46

EAST ASIA AND PACIFIC INFRASTRUCTURE STRATEGY

Transcript of EAST ASIA AND PACIFIC INFRASTRUCTURE...

EAST ASIA AND PACIFICINFRASTRUCTURE STRATEGY

PART A: THE EAST ASIA INFRASTRUCTURE CHALLENGE

1. Infrastructure, growth and poverty reduction: The East Asia story

2. Emerging infrastructure challenges: A new environment

3. Infrastructure needs and financing 4. A new framework for policy makers

PART B: THE EAP BUSINESS STRATEGY1. Overview2. Program characteristics, emerging trends and

implementation of the new analytical framework

PART A. THE EAST ASIA INFRASTRUCTURE CHALLENGE

• The East Asia development model – NICs led the way• Strong aggregate growth supporting impressive

poverty reduction• Virtuous cycle of savings, investment and

infrastructure expenditures, enhancing competitiveness

• But significant variation remains in service access

1. Infrastructure, Growth And Poverty Reduction: The East Asia Story

From infrastructure to poverty reduction, through growth and service access

Growth Service Access

Poverty Reduction

Infrastructure Growth Determinants

Access Determinants

Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

The East Asia development model

Hong Kong (China) Korea Taiwan (China)

Hong Kong

0

2,000

4,000

6,000

8,000

10,000

12,000

1960

1970

1980

1990

Korea

0

20,000

40,000

60,000

80,000

100,000

1960

1970

1980

1990

2000

Taiwan

0

10,000

20,000

30,000

40,000

1960

1970

1980

1990

2000

Singapore Japan Malaysia

Singapore

0

1,000

2,000

3,000

4,000

5,000

1960

1970

1980

1990

2000

Japan

0

50,000

100,000

150,000

200,000

250,000

1960

1970

1980

1990

2000

0.90.91.01.01.11.11.21.2

mil

Right Axis

Malaysia

0

2,000

4,000

6,000

8,000

10,000

12,000

1960

1970

1980

1990

2000

010203040506070

'000

Right Axis

5Total Road Length (km) � Electricity generating capacity (million kWh) < Main Telephone Lines (000s)

Growth in infrastructure stocks, East Asian NICs, 1960 - 2000

?

• Export led model supported by• Strong levels of investment and savings• Strong centralized vision and co-ordination by effective planning agencies• Directed savings through development banks • Infrastructure as integral part of the model

• High growth helped maintain policy consensus

• Much of the inner-workings hidden from public view

• Under increasing stress from the 1990s

NICs led the way…

Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

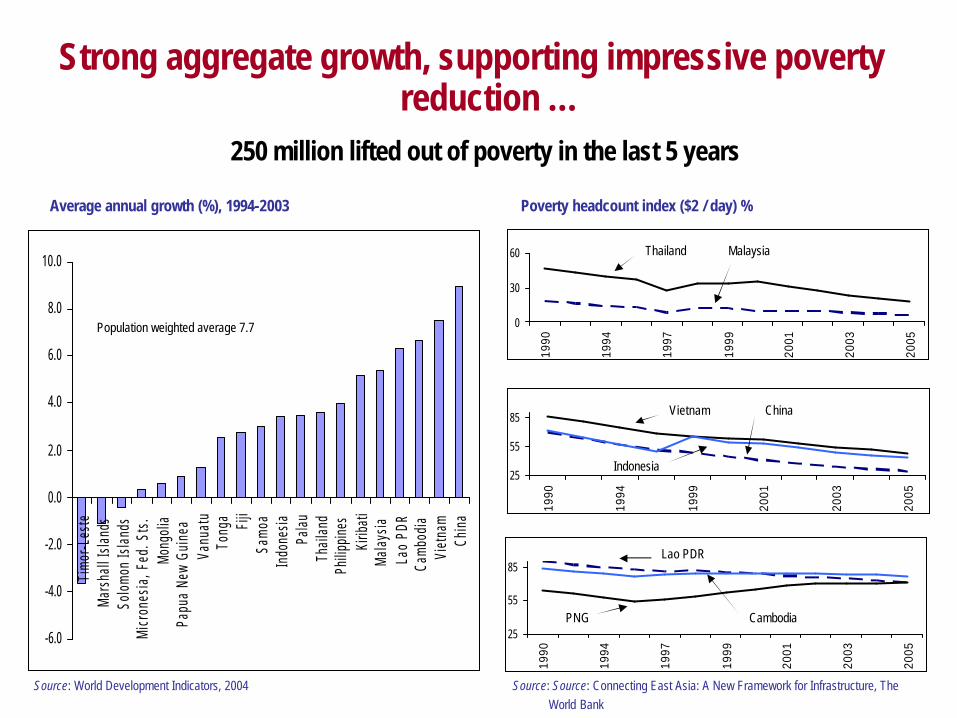

Average annual growth (%), 1994-2003 Poverty headcount index ($2 / day) %

25

55

85

1990

1994

1999

2001

2003

2005

0

30

60

1990

1994

1997

1999

2001

2003

2005

25

55

85

1990

1994

1997

1999

2001

2003

2005

Thailand

Vietnam China

Indonesia

Lao PDR

CambodiaPNG

Malaysia

Strong aggregate growth, supporting impressive poverty reduction …

250 million lifted out of poverty in the last 5 years

Source: World Development Indicators, 2004 Source: Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Tim

or-L

este

Mars

hall

Isla

nds

Solo

mon

Isla

nds

Mic

rone

sia,

Fed

. Sts

.Mo

ngol

iaPa

pua

New

Guin

eaVa

nuat

uTo

nga Fiji

Sam

oaIn

done

siaPa

lau

Thai

land

Philip

pine

sKi

ribat

iMa

lays

iaLa

o PD

RCa

mbod

iaVi

etna

mCh

ina

Population weighted average 7.7

Savings and investment (% GDP) 1993-2002

Infrastructure investment (% GDP)

0 20 40

SSA

LAC

SA

ECA

MENA

EAP

Cambodia

Vanuatu

Mongolia

Philippines

Vietnam

Indonesia

Thailand

China

Malaysia

Investment Savings

0-3% 4-7% Over 7%

Cambodia Lao PDR China

Indonesia Mongolia Thailand

Philippines Vietnam

0% 50% 100%

Thailand

Indonesia

Philippines

China

Lao PDR

Vietnam

0% 50% 100% 150%

Philippines

Lao PDR

Indonesia

Thailand

China

Vietnam

Expansion of infrastructure stocks, 1990 – 2000

Total road network Electricity generation capacity

… supported by a virtuous cycle of savings, investment and infrastructure expenditures

Source: World Development Indicators, 2004 Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

Infrastructure quality ranking, World Competitiveness Report, East Asia

Note: Rankings are shown for developing East Asian economies (darker bars), and advanced East Asian economies (lighter bars). Vertical line is the average for all 102 surveyed countries, both within and outside of East Asia.

Intra-regional exports

Emerging East Asia (China, ASEAN, newly industrializing economies, Mongolia), share of world exports (%)

0.0

5.0

10.0

15.0

20.0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Intra-regional exports increase from 32percent to 41 % of EAP

trade

East Asia infrastructure compares well with the rest of the world and accounts for a growing share of world exports …

Source: IMF, Direction of Trade Statistics

T e l e p h o n e s

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ippines

Vietnam

Indonesia

China

Thailand

Ma lays ia

O v e r a l l i n f r a s t r u c t u r e

q u a l i t y

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ipp ines

Vietnam

Indonesia

China

Thai land

Ma lays ia

E l e c t r i c i t y s u p p l y

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ipp ines

Vietnam

Indonesia

China

Thailand

Malays ia

P o r t s

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ipp ines

Vietnam

Indonesia

China

Thai land

Ma lays ia

R a i l r o a d s

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ipp ines

Vietnam

Indonesia

China

Thai land

Ma lays ia

A i r T r a n s p o r t

0 . 0 2 . 0 4 . 0 6 . 0 8 . 0

Japan

Taiwan

Korea

Hong Kong

Singapore

Phi l ipp ines

Vietnam

Indonesia

China

Thailand

Malays ia

0

25

50

75

100

PNG

Cam

bodi

a

Viet

nam

Lao

PDR

Mon

golia

Solo

mon

Mya

nmar

Chin

a

Indo

nesia

Pala

u

Philip

pine

s

Vanu

atu

Mal

aysia

Thai

land

Sam

oa

Tong

a

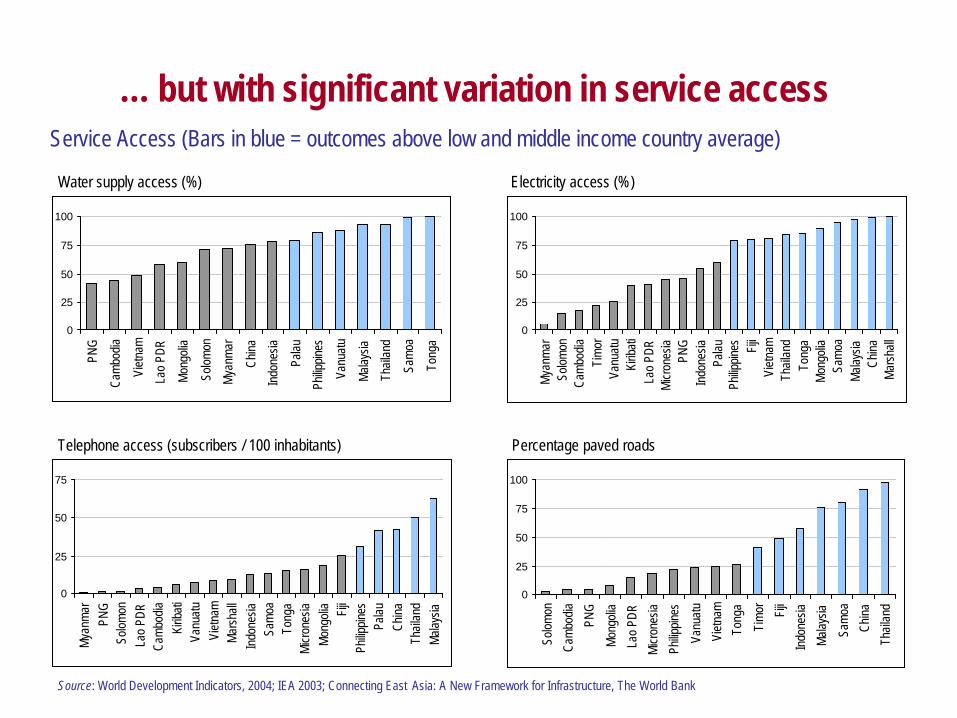

Service Access (Bars in blue = outcomes above low and middle income country average)

Water supply access (%) Electricity access (%)

0

25

50

75

100

Mya

nmar

Solo

mon

Cam

bodi

aTi

mor

Vanu

atu

Kirib

ati

Lao

PDR

Micr

ones

iaPN

GIn

done

siaPa

lau

Philip

pine

s Fiji

Viet

nam

Thai

land

Tong

aM

ongo

liaSa

moa

Mal

aysia

Chin

aM

arsh

all

Telephone access (subscribers / 100 inhabitants) Percentage paved roads

0

25

50

75

Mya

nmar

PNG

Solo

mon

Lao

PDR

Cam

bodi

aKi

ribat

iVa

nuat

uVi

etna

mM

arsh

all

Indo

nesia

Sam

oaTo

nga

Micr

ones

iaM

ongo

lia Fiji

Philip

pine

sPa

lau

Chin

aTh

aila

ndM

alay

sia

0

25

50

75

100

Solo

mon

Cam

bodi

a

PNG

Mon

golia

Lao

PDR

Micr

ones

ia

Philip

pine

s

Vanu

atu

Viet

nam

Tong

a

Tim

or Fiji

Indo

nesia

Mal

aysia

Sam

oa

Chin

a

Thai

land

… but with significant variation in service access

Source: World Development Indicators, 2004; IEA 2003; Connecting East Asia: A New Framework for Infrastructure, The World Bank

2. EMERGING CHALLENGES: A NEW ENVIRONMENT

• Rapid urbanization • Growing inequalities and disparities in

access• Changing governance model • Increased regional integration • Growing environmental concerns

1960

2025

2000

1980

0

25

50

75

100

SSA SA MENA LAC OECD EAP

Urbanization is the new driver for productivity and infrastructure

Urban population (% total population) Growth in number of cities over one million inhabitants

500 million more people move into Asian cities

0

20

40

60

80

100

120

140

160

180

2000 2005 2010 2015

… in 20 years, East Asia will be an urban region

Source: World Development Indicators, 2004; United Nations World Urbanization Prospects, 2003

Source: United Nations World Urbanization Prospects, 2003

Inequality – A contrasted picture

Poor provinces in the hinterland, but concentration of the poor along the coast …

Percentage population living below $2 / day (each dot = 50 000 people)Percentage population living below $2 / day (by region)

% of population living below PPP$2/day in 2002

20% 40% 60% 80%

Source: Poverty Reduction and Economic Management Unit, The World Bank, 2004 Source: Poverty Reduction and Economic Management Unit, The World Bank, 2004

Access to improved sanitation (2002)

0

20

40

60

80

100

120

China

Indone

siaKiri

bati

Marshal

l Island

s

Micrones

ia, Fed.

Sts.

Myanmar Pala

u

Philipp

ines

Vietnam

of p

opul

atio

n w

ith a

cces

s to

impr

oved

san

itatio

n

Rural Urban

Inequality – The rural-urban challenge

Access to electricity

0

20

40

60

80

100

120

Indonesia 1997 Philippines 1998 Vietnam 2004

% o

f hou

seho

lds

with

acc

ess

to e

lect

ricity

Rural Urban

0

20

40

60

80

100

China

Indone

siaKiriba

ti

Mongolia

Myanmar Pala

u

Philipp

inesTha

iland

% o

f pop

ulat

ion

with

acc

ess

to im

prov

es w

ater

sou

rce

Rural Urban

Access to improved water source (2002)

Disparities between rural and urban access are large and growingAccess to telecommunications (2003)

0

5

10

15

20

25

30

35

China Mongolia Myanmar Tonga Thailand

Mai

nlin

es p

er 1

00 p

eopl

e

Rural Urban

Source: World Development Indicators, 2004; Demographic and Health Surveys 1990-2001

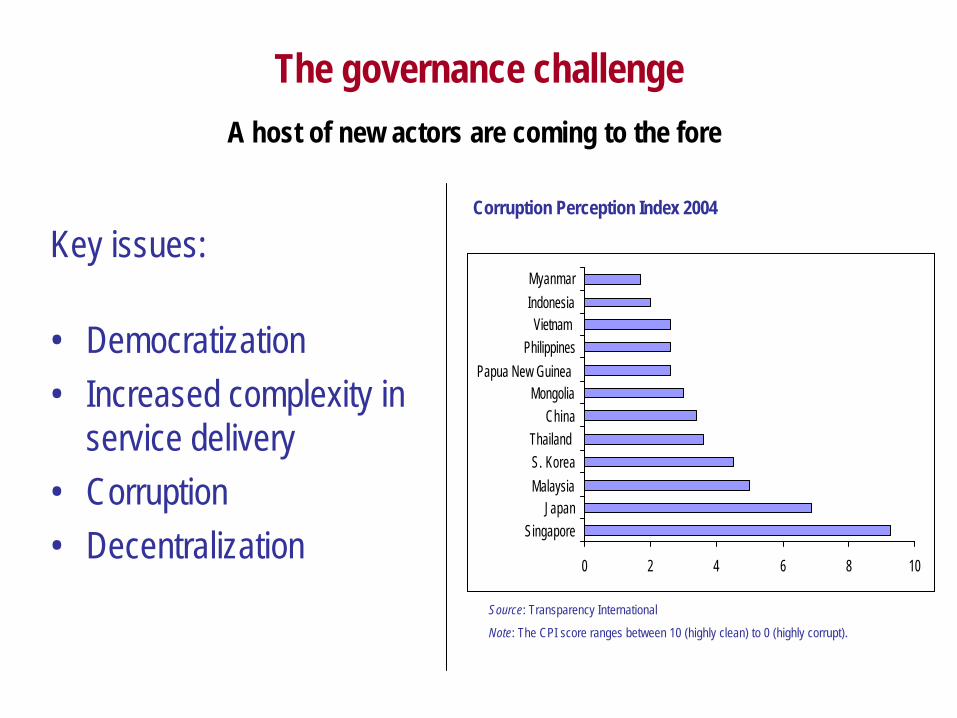

The governance challenge

Key issues:

• Democratization• Increased complexity in

service delivery• Corruption• Decentralization

Corruption Perception Index 2004

Source: Transparency International

Note: The CPI score ranges between 10 (highly clean) to 0 (highly corrupt).

A host of new actors are coming to the fore

0 2 4 6 8 10

SingaporeJapan

MalaysiaS. KoreaThailand

ChinaMongolia

Papua New Guinea Philippines

Vietnam IndonesiaMyanmar

Decentralization

Key challenges:

• Managing spillovers in service provision

• Fragmentation• The missing middle• Implementation of

integrated vision

Expenditure decentralization – sub-national expenditure (% total national expenditure)

0 10 20 30 40 50 60 70

Germany (1990s)

USA (1990s)

Japan (1990s)

OECD countries (1990s)

Pakistan (1990s)

Russia (1990s)

India (1990s)

Thailand (2001)

Philippines (2002)

Indonesia (2002)

Vietnam (2002)

China (2002)

All transition countries (1990s)

All developing countries (1990s)

Adapting the role of the state to a new reality

Source: East Asia Decentralizes—Making Local Government Work, The World Bank

Increased regional interdependence

Interdependence of auto-manufacturing in ASEAN

Philippines

Philippines Mindanao

Mongolia

Indonesia Sulawesi

Laos

Hong Kong

TaiwanSingapore

KoreaJapan

Thailand NE

Malaysia

ChinaThailand

China Inland

Vietnam Inland

-1.00

PNG

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

-15.00 -10.00 -5.00 0.00 5.00 10.00 15.00

Accessibility

Trade Openness

Cambodi

a

Indices of trade openness and accessibility in East Asia

East Asia’s growing intra-regional trade places increasing demand on regional access

Source: Nomura Research Institute, Reprinted in Connecting East Asia: A New Framework for Infrastructure, The World Bank

Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

Infrastructure and the environment

Exponential increases in the demand for energy and its uses will have major environmental consequences

Actual and projected growth in energy demand in EAP, by fuel type, 1990-2030

Source: World Bank RAINS - Asia Database

Projected no. of automobiles, China 2000 - 2020

0

10

20

30

40

50

60

70

80

90

2000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Proj

ecte

d no

. of a

utom

obile

s (in

mill

ions

) 13 million

77 million

Source: International Energy Agency, 2005; World Bank Staff Estimates

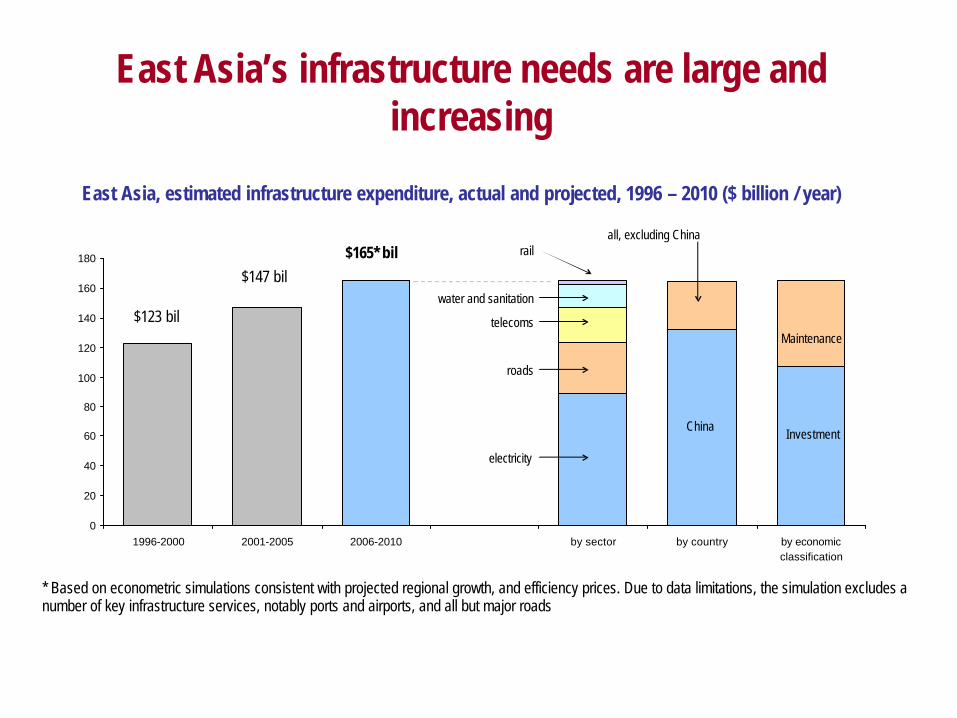

3: INFRASTRUCTURE NEEDS AND FINANCING

• East Asia needs are large and increasing • At the macro level, financing is not a constraint • But infrastructure needs vary significantly across

countries• Finance mobilization

– Private sector – the bubble has burst, but sentiment remains positive

– Public Sector – there is a need to create fiscal space – International donors – play a small role in most of the

region • Getting the priorities right: financial engineering is no

substitute for sound project design (tax payers and users must pay)

0

20

40

60

80

100

120

140

160

180

1996-2000 2001-2005 2006-2010 by sector by country by economicclassification

* Based on econometric simulations consistent with projected regional growth, and efficiency prices. Due to data limitations, the simulation excludes a number of key infrastructure services, notably ports and airports, and all but major roads

East Asia’s infrastructure needs are large and increasing

East Asia, estimated infrastructure expenditure, actual and projected, 1996 – 2010 ($ billion / year)

$123 bil

$147 bil$165* bil

electricity

roads

telecoms

water and sanitation

rail

China

all, excluding China

Investment

Maintenance

At the macro level, financing is not a constraint in East Asia …

Selected macroeconomic indicators 2004 (US$ billion)

4913*67Malaysia

193*28199S. Korea

1100*172845Japan

75746*623China

Gross domestic savings

Current a/c surplus

Foreign exchange reserves

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

China Low income Middle income

6.9 %6.3 %

3.6 %

… but, infrastructure needs vary significantly across countries

East Asia, estimated infrastructure expenditure, 2006-2010, % GDP

Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

Source: World Development Indicators 2004, 2003

* Numbers for 2003

Finance mobilization – The private sector

The private sector bubble has burst… … but sentiment is positive

0

5

10

15

20

25

30

35

40

45

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

0

20

40

60

80

100

120

140

24%

10%

88%

8%4%

67%

increase sustain decrease

Global firms East Asian firms

Does your company expect to increase, sustain, or decrease your total sector investment in the region in the next two years?

Private sector investment in infrastructure ($ billion)

To EAP (left axis)

To all developing countries (right axis)

… with new regional actors emerging

Source: World Bank PPI Database, 2005 Source: East Asia and Pacific Private Investors in Infrastructure Perception Survey 2004

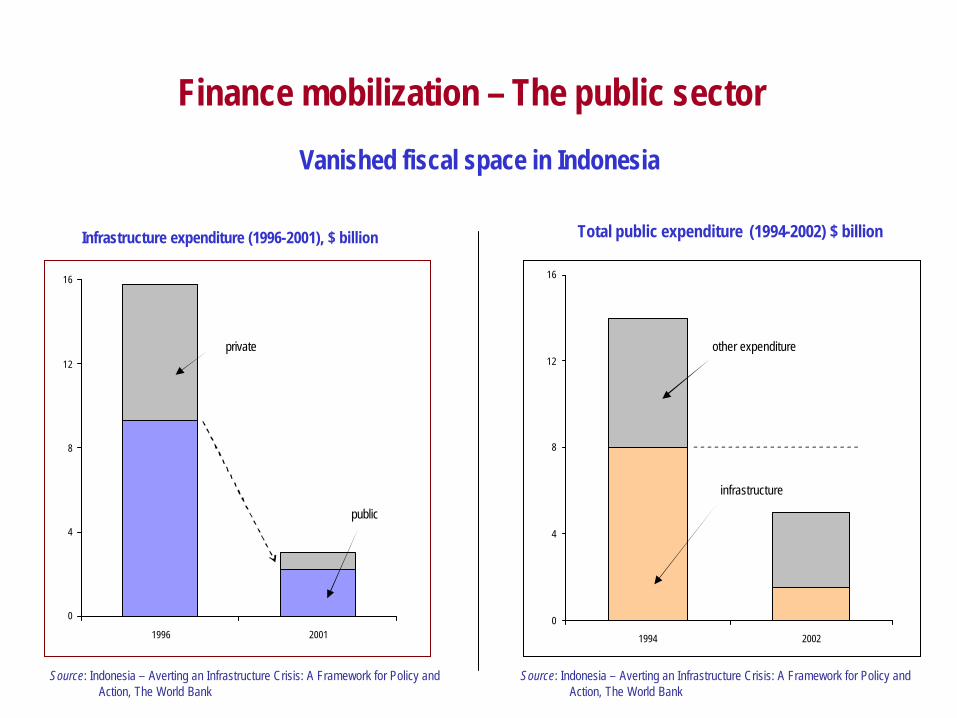

Finance mobilization – The public sector

0

4

8

12

16

1996 20010

4

8

12

16

1994 2002

Vanished fiscal space in Indonesia

Total public expenditure (1994-2002) $ billionInfrastructure expenditure (1996-2001), $ billion

private

public

infrastructure

other expenditure

Source: Indonesia – Averting an Infrastructure Crisis: A Framework for Policy and Action, The World Bank

Source: Indonesia – Averting an Infrastructure Crisis: A Framework for Policy and Action, The World Bank

Finance mobilization – The international community

-10 0 10 20 30 40 50 60

Thailand

China

Malaysia

East Asia & Pacific

Indonesia

Philippines

Vietnam

Cambodia

Mongolia

Aid (% of GDP and % of investment, 2003)

Donors are small players in most of the region

Aid (% of investment)

Aid (% of GDP)

Estimated regional infrastructure needs (percentage of GDP) – 6.2 %

For the region as a whole, aid is only a small portion

of infrastructure needs

Source: World Development Indicators, 2004

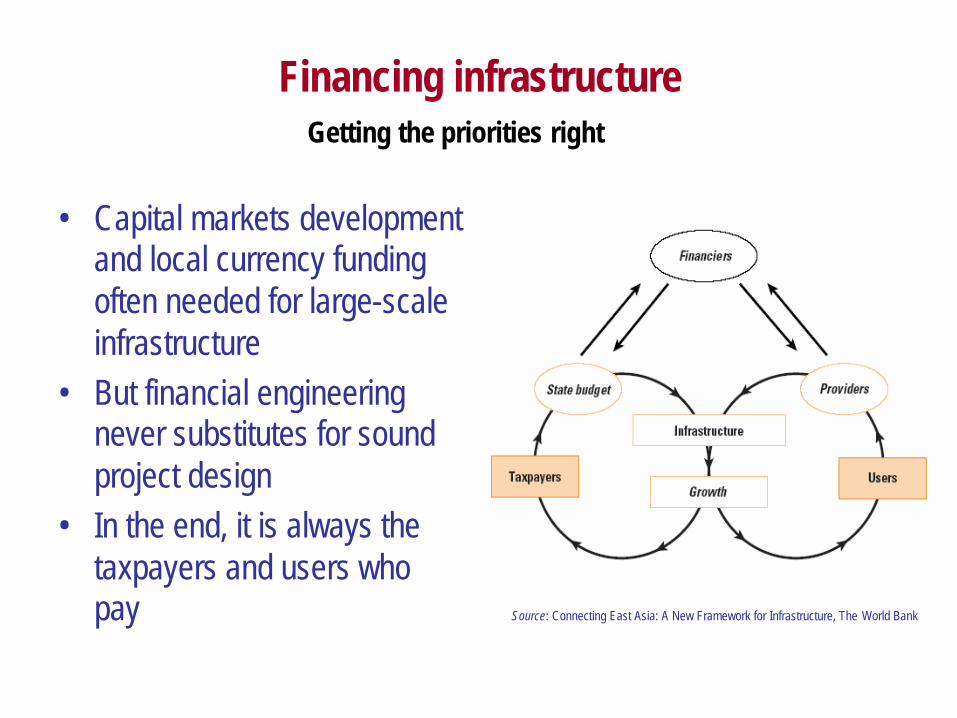

Financing infrastructure

• Capital markets development and local currency funding often needed for large-scale infrastructure

• But financial engineering never substitutes for sound project design

• In the end, it is always the taxpayers and users who pay

Getting the priorities right

Source: Connecting East Asia: A New Framework for Infrastructure, The World Bank

4: A NEW FRAMEWORK FOR POLICY MAKERS

• Inclusive development

– Coordination– Accountability– Risk management

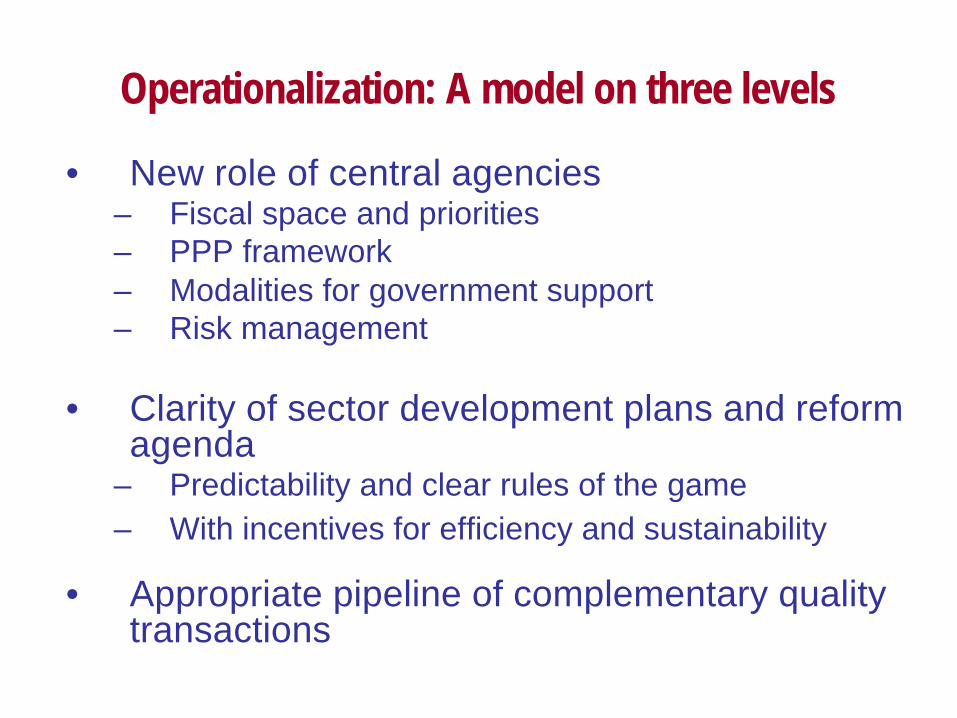

• Operationalization: A model on three levels

A new analytical framework for policy makers

Accountabilityand

Risk Management

Coordination

InclusiveDevelopment

Reconciling need for central vision with decentralization and market forces; getting expenditures right;

managing fiscal space

Clarifying rules of the game and social objectives; improving competition, regulation, and

oversight mechanisms

Economic growth, plus sharing the benefits of

growth to reduce poverty

Establishing public-private partnership frameworks; sharing risks and managing contingent liabilities

Inclusive development: A stool with three legs – coordination, accountability and risk management

Operationalization: A model on three levels

• New role of central agencies – Fiscal space and priorities– PPP framework – Modalities for government support – Risk management

• Clarity of sector development plans and reform agenda

– Predictability and clear rules of the game – With incentives for efficiency and sustainability

• Appropriate pipeline of complementary quality transactions

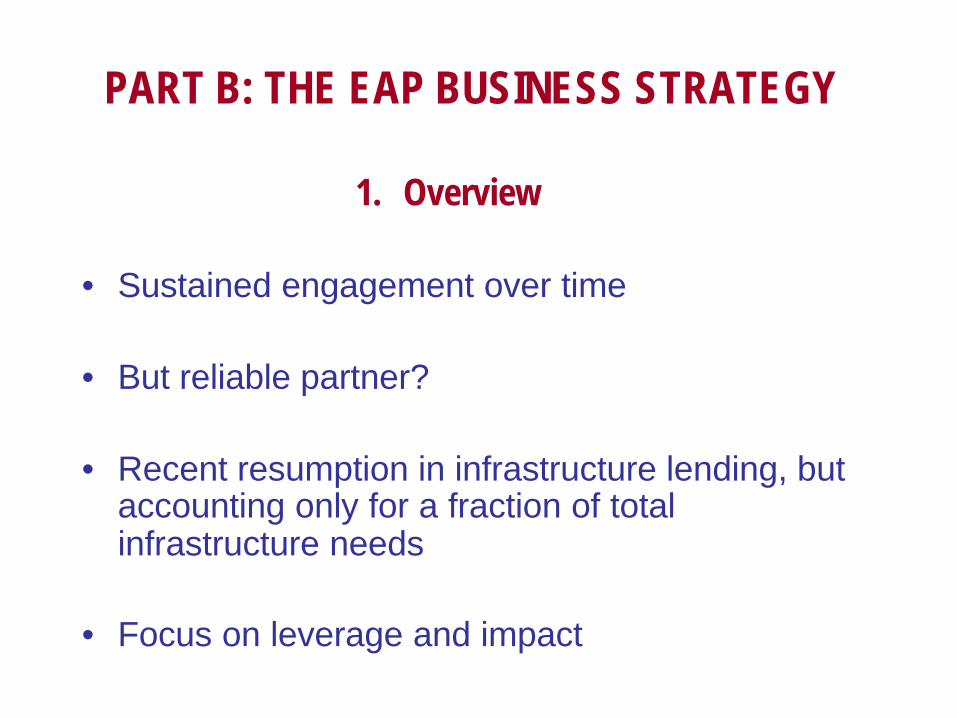

PART B: THE EAP BUSINESS STRATEGY

• Sustained engagement over time

• But reliable partner?

• Recent resumption in infrastructure lending, but accounting only for a fraction of total infrastructure needs

• Focus on leverage and impact

1. Overview

World Bank lending for infrastructure in East Asia & Pacific region 1951-2005

0

5

10

15

20

25

30

35

40

45

50

51 54 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

# Proj

IBRD+IDA+Grant

Total lending for Infrastructure in East Asia & Pacific (1951-2005): Over $60 billion

Sustained engagement over time

World Bank Group lending, EAP Region, 1995 to 2005 ($ million)

Note: No projects for 1994-2004 = PE+GEF+SF; FY05 includes also two operations postponed to FY06

But reliable partner?

EAP infrastructure: New projects and commitments: 1995-2005

18 1917 18

13 13

9

13

18 1719

3,3603,555

2,930

2,2991,843

1,152970

1,356

1,8491,700

1,841

0

5

10

15

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 20050

500

1000

1500

2000

2500

3000

3500

4000

No. Projects

IBRD + IDA + Grant Amt

EASIN PORTFOLIO

• 105 projects with netcommitments of $12.0 billion

• Lending doubled over three years to $1.7 billion

• Sustainable pipeline of around 18 projects, approximating $2 billion / year

• 60 percent of EAP net commitments

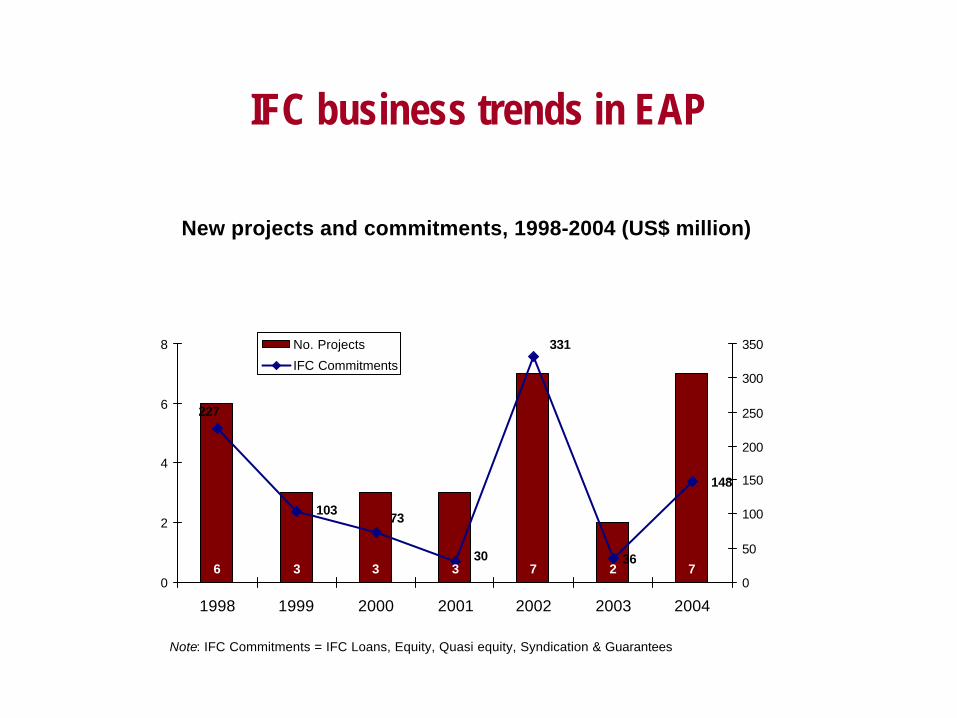

IFC business trends in EAP

New projects and commitments, 1998-2004 (US$ million)

Note: IFC Commitments = IFC Loans, Equity, Quasi equity, Syndication & Guarantees

6 3 3 3 7 2 736

227

10373

30

331

148

0

2

4

6

8

1998 1999 2000 2001 2002 2003 20040

50

100

150

200

250

300

350No. Projects

IFC Commitments

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

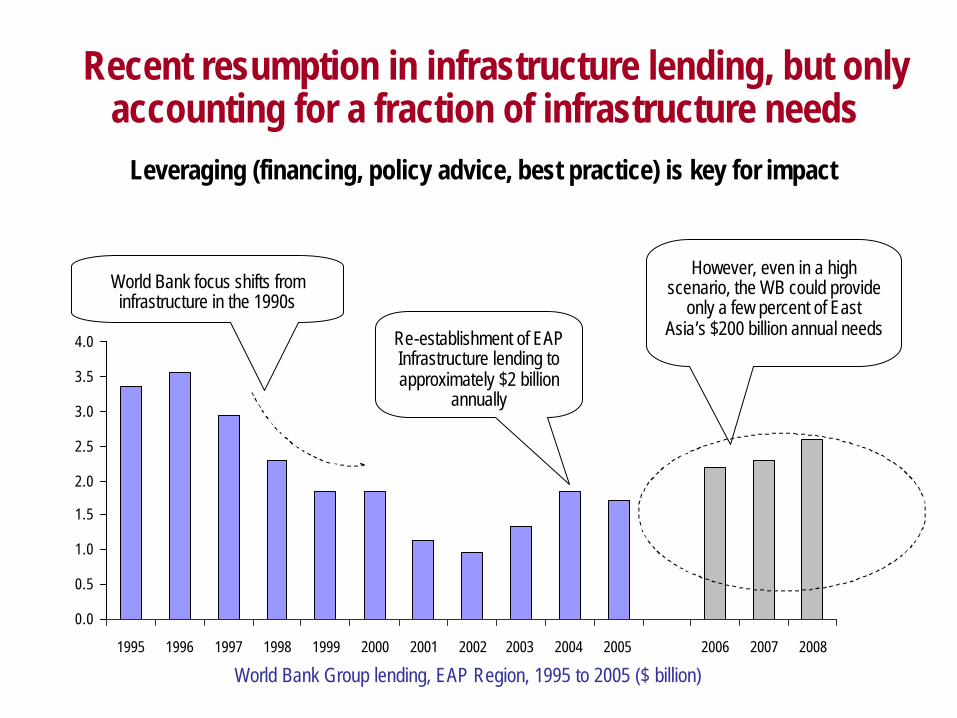

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

World Bank Group lending, EAP Region, 1995 to 2005 ($ billion)

World Bank focus shifts from infrastructure in the 1990s

Re-establishment of EAP Infrastructure lending to approximately $2 billion

annually

However, even in a high scenario, the WB could provide

only a few percent of East Asia’s $200 billion annual needs

Recent resumption in infrastructure lending, but only accounting for a fraction of infrastructure needs

Leveraging (financing, policy advice, best practice) is key for impact

Leveraging large volumes of private flowsExample: Nam Theun 2, Laos

• $1.45 billion hydro project (incl. contingent financing) exporting energy to Thailand

• Leveraged private sector financing of $1.2 billion through IDA grant of $20 million and combination of IDA and MIGA guarantees up to $100 million, matched by ADB.

• Entailed partnership with other donors and consortium of international and Thai Banks.

Phu My 3 PowerPhu My 2-2 Power

• Private sector with IDA guarantee

• 715 MW gas-fired power plant• Total project cost: US$ 400

million• Bank Group Support - IDA:

– US$ 75 M Partial Risk Guarantee

• Fully private supported by MIGA guarantee

• 716 MW combined cycle gas-fired power plant

• Total project cost: US$412 million

• Bank Group Support - MIGA:– US$ 48 M Equity– US$ 90 M Debt (P&I)

20032002

The evolving role of Bank Group enhancement Example: Phu My 1, 2, 3, Vietnam

Phu My 2-1 Power

1996

• Public financed project• 336 MW gas-fired power plant

(with subsequent expansions)• Bank Group supported the

development of first phase – IDA:– US$ 180 M equivalent

Credit

2. PROGRAM CHARACTERISTICS, EMERGING TRENDS & IMPLEMENTATION OF NEW

ANALYTIC FRAMEWORK

• 5 platforms of engagement

• EAP infrastructure business: by country, by sector, and by instrument

• Emerging trends

• Implementation of the new analytical framework

Five platforms of engagement

EAP BUSINESS STRATEGY

Global

Regional

National / Sovereign

Sub-sovereign

Community

• NT2

• Infrastructure regulator’s Forum

• Marine Electronic Highway (Singapore-Indonesia-Malaysia)

• GMS partnership - transport and energy

• East Asia Flagship

• Pacific Island Infrastructure strategy (REDI)

• Shanghai Urban Environment Program

• Laos Provincial Infrastructure

• Small town development in China (AAA)

• GEF and carbon financing: Xiaogushan Hydro; Mongolia District Heating

• GEF land pollution and air quality programs

• International Privatization experience (AAA for Malaysia)

• Bulk of EAP lending

• Indonesia, Philippines, Vietnam Infrastructure strategies (REDIs)

• Kabubatan Development Project

• Vietnam rural roads

Existing active portfolio by country (no. of operations)

China (54)Vietnam (15)

Indonesia (9)

Philippines (8)Cambodia (4)PNG(4)Samoa & Mongolia (3 each)Lao PDR & Timor Leste (2

each)Thailand & Tonga (1 each)

EAP infrastructure business by country …

• In savings-rich fast-growing countries, focus on introducing best practice, or scaling up and supporting existing policies and programs (Vietnam, China)

• In countries faced with fiscal constraints, focus on leveraging private sector finance (Philippines, Indonesia)

• In IDA countries, focus on meeting financing needs for basic infrastructure and on partnerships (Laos, Mongolia, Pacific Islands)

China (8739)

Vietnam (1973)

Indonesia (1096)

Philippines (475)

Cambodia (131)

Thailand, PNG, Mongolia, Lao PDR, Samoa, Tonga, Timor Leste (300)

Existing active portfolio by country (net commitments $ million)

• Strong transport portfolio across countries

• Fast growing portfolio in urban infrastructure

• Fluctuations in energy following sharp reductions in 1990s

• Growing multisectoralapproaches

… by sector

Existing active portfolio by sector (net commitments $ million)

Urban, water and sanitation (3798)

Transport (5733)

Energy and mining (3208)

I CT (4.5)

ICT (1)

Energy and mining (26)

Urban, water and

sanitation (35)

Transport (44)

Existing active portfolio by sector (no. of operations)

… and by instrument

Existing active portfolio by product line• Covering access and growth requirements

• Major focus on capacity expansion (Category A projects)

• Environmental management (water & sanitation) and renewable energy

• Growing GEF and PCF programs

IBRD (72)

IDA (28)

GEF (4)

Carbon Finance (3)

Special Financing (2)

Guarantees (1)

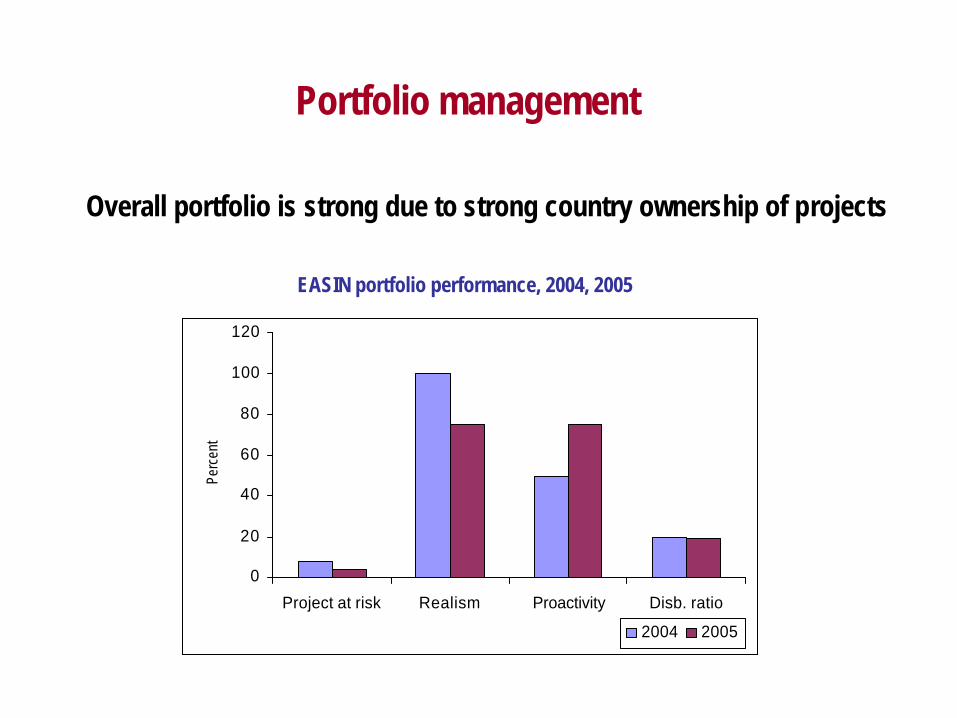

Portfolio management

EASIN portfolio performance, 2004, 2005

Overall portfolio is strong due to strong country ownership of projects

0

20

40

60

80

100

120

Project at risk Realism Proactivity Disb. ratio

Perc

ent

2004 2005

Analytical work

• Strong AAA and R&D crucial to support value added, relevant policy advice, sharing of experiences, and operational impact

– 12% of BB budget and 3-4 times leverage of Bank’s BB with trust funds over last 3 years

• Increasing focus on integrated cross-sectoral work – Infrastructure strategies (Indonesia, Philippines,

Vietnam, Pacific Islands, Mongolia) – PPP frameworks – Infrastructure finance

Analytical work (Cont..)

• Increasing focus on partnerships and regional engagement

– ADB/JBIC/WB flagship study– Engagement with GMS, ASEAN, APEC– East Asia & Pacific Infrastructure Regulatory Forum

(EAPIRF)– Infrastructure database

• Analytical work on three levels– Research, analytical pieces– Just-in-time policy notes– Advice and dialogue on on-going basis

Majority country-based, and closely linked to on-going projects

Emerging trends

• The infrastructure program is not constrained by demand, but by country borrowing requests, creditworthiness issues and IDA constraints.

• New priorities – Public-private partnerships agenda (cross-sectoral)– Subnational and infrastructure finance– Regional: GMS and regional GEFs– GEF and PCF– Renewed demand for energy (and hydro) generation– Cross-sectoral reform agenda.

Emerging trends (Cont..)

• Instruments– Majority will remain investment lending – Increased integration of policy agenda in

DPLs, & PRSCs– Emerging SWAPs, cross-sectoral urban

projects– Combination of WBG investments to

support PPP agenda– Subnational window?

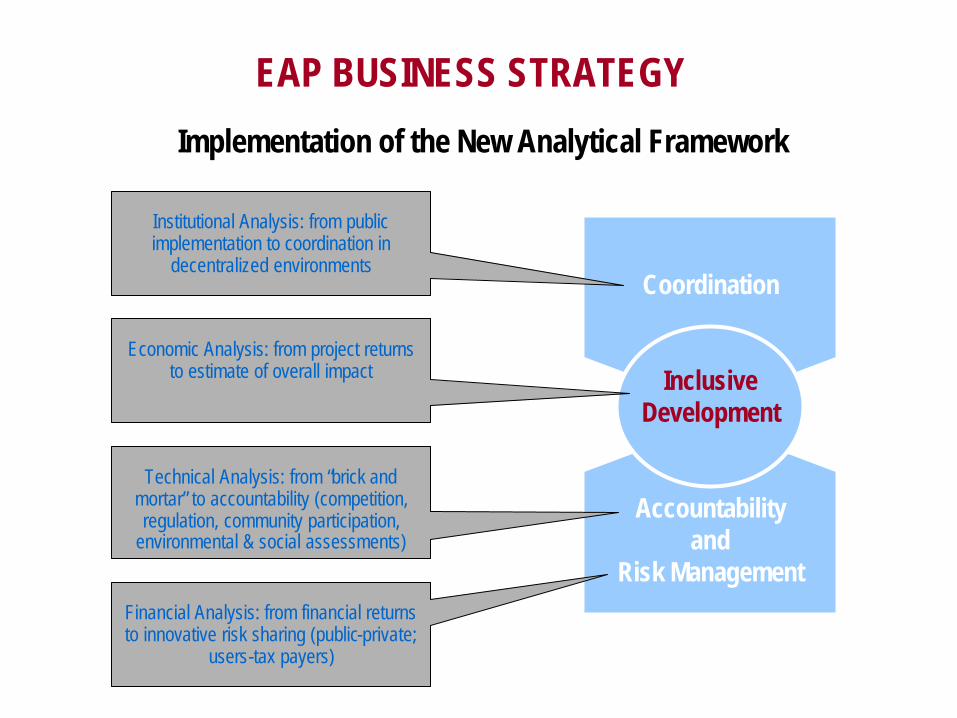

EAP BUSINESS STRATEGY

Accountabilityand

Risk Management

Coordination

InclusiveDevelopment

Implementation of the New Analytical Framework

Institutional Analysis: from public implementation to coordination in

decentralized environments

Economic Analysis: from project returns to estimate of overall impact

Technical Analysis: from “brick and mortar” to accountability (competition, regulation, community participation,

environmental & social assessments)

Financial Analysis: from financial returns to innovative risk sharing (public-private;

users-tax payers)