East Africa/media/IE Singapore/Files...East Africa growth dominates the African regions – > 15% of...

32

Rahul Ghosh Divisional Director, Middle East & Africa Group [email protected] 21 July 2015 East Africa SUDAN ETHIOPIA DJIBOUTI KENYA TANZANIA RWANDA UGANDA BURUNDI

Transcript of East Africa/media/IE Singapore/Files...East Africa growth dominates the African regions – > 15% of...

Rahul Ghosh Divisional Director,

Middle East & Africa Group

21 July 2015

East Africa SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

Agenda • Overview of East Africa

• Singapore’s economic engagement with

East Africa

• Sectoral Opportunities

Overview

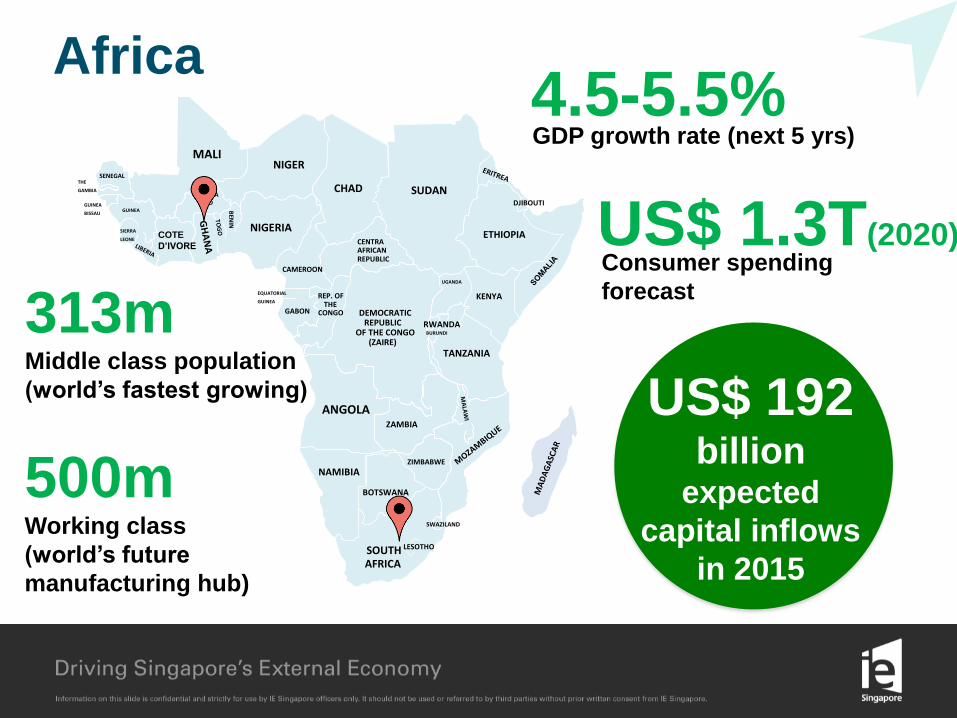

Africa

MALI NIGER

CHAD SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

DEMOCRATIC

(ZAIRE)

CENTRAL

RWANDA

GABON

EQUATORIAL

CONGO

NIGERIA

BEN

IN

SIERRA

SENEGAL THE

GUINEA

CAMEROON

ZAMBIA

ZIMBABWE

BOTSWANA

SWAZILAND

LESOTHO

NAMIBIA

ANGOLA

UGANDA

OF THE CONGO

REPUBLIC

BURUNDI

GUINEA REP. OF

BURKINA FASO

GUINEA

LEONE

GAMBIA

BISSAU

REPUBLIC

AFRICAN

THE

SOUTH AFRICA

COTE

D’IVORE

US$ 192 billion

expected

capital inflows

in 2015

1.1b(2014) 2.4b(2050)

People People

4.5-5.5% GDP growth rate (next 5 yrs)

313m Middle class population

(world’s fastest growing)

US$ 1.3T(2020) Consumer spending

forecast

500m Working class

(world’s future

manufacturing hub)

MALI NIGER

CHAD

SUDAN & SOUTH SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

DEMOCRATIC

(ZAIRE)

CENTRAL

RWANDA GABON

EQUATORIAL

CONGO

NIGERIA

BEN

IN

SIERRA

SENEGAL THE

GUINEA

CAMEROON

ZAMBIA

ZIMBABWE

BOTSWANA

SWAZILAND

LESOTHO

NAMIBIA

ANGOLA

UGANDA

OF THE CONGO

REPUBLIC

BURUNDI

GUINEA REP. OF

BURKINA FASO

GUINEA

LEONE

GAMBIA

BISSAU

REPUBLIC

AFRICAN

THE

SOUTH AFRICA

COTE

D’IVORE

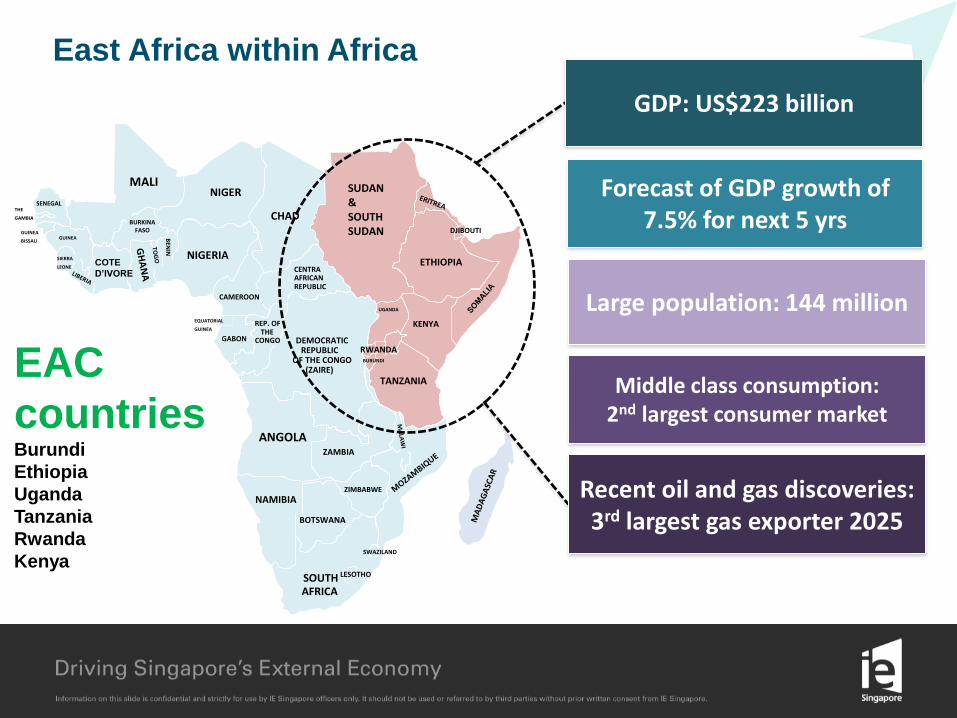

East Africa within Africa

GDP: US$223 billion

Large population: 144 million

Forecast of GDP growth of 7.5% for next 5 yrs

Recent oil and gas discoveries: 3rd largest gas exporter 2025

Middle class consumption: 2nd largest consumer market

EAC

countries Burundi

Ethiopia

Uganda

Tanzania

Rwanda

Kenya

East Africa growth dominates the African regions –

> 15% of continent’s GDP

7.1% GDP growth vs. 3.9% av. of SSA

Best performing region

Among the world’s fastest growing countries

Source: IMF, DB Research

Source: Standard Chartered Research

Potential Growth of East African Countries –

Kenya, Ethiopia & Tanzania lead the pack

USD bn, Results of growth simulation based on current GDP trends

South Africa Nigeria Angola Ghana Kenya Ethiopia Cameroon Côte

d’Ivoire

Tanzania Equatorial

Guinea

Growth to multiply by

3-4 times

Source: Standard Chartered Research

Improving Business Climate amongst East African Community (EAC) states – Rwanda tops the list

Source: Ease of Doing Business 2014

EAC Countries Filtered Ranking

Rwanda 3

Tanzania 13

Ethiopia 14

Kenya 15

Uganda 22

Most progressive towards creating common market and diversified economies

EAC ranks 2nd to SADC in EODB

Rwanda ranks 3rd after Mauritius, S Africa in EODB

Top 4 East Africa economies rank within top 15

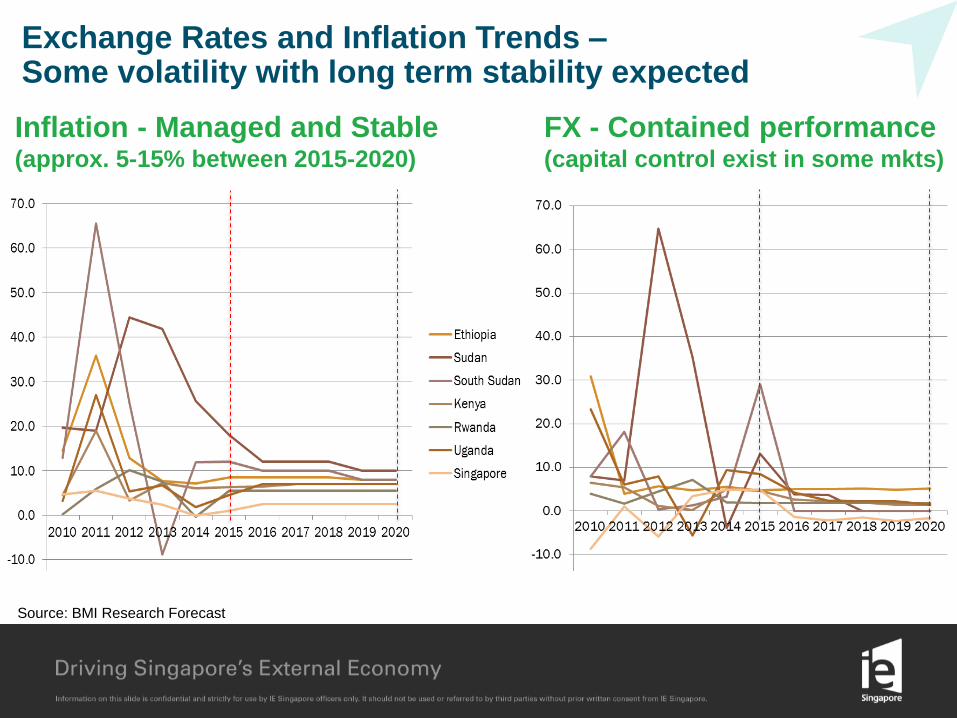

Exchange Rates and Inflation Trends – Some volatility with long term stability expected

Inflation - Managed and Stable (approx. 5-15% between 2015-2020)

FX - Contained performance (capital control exist in some mkts)

Source: BMI Research Forecast

Increasing FDI (Mostly from Asia) – Large pledges but fund utilization is slow

• US$ 3 billion Djibouti-Ethiopia Railway Line

• US$ 10 billion Tanzania Bagamoyo Port

• US$ 8 billion Uganda’s Power, Rail & Oil sector

• US$ 3 billion in Ethiopia SEZs (Light Mfg.)

• US$ 2 billion LAPPSET corridor

• US$ 300 million for Mombasa Port Development

• Tanzania’s central line railway, expansion of Port

of Dar es Salaam, agriculture, light mfg.

• US$ 550 million to create Tanzania’s first

commercial cotton plantation

• Numerous infrastructure projects driven by the

private sector

• Export - Import (EXIM) Bank of India partnership

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

Ethiopia

Ethiopia 94.1 million people - largest

in East Africa, 2nd in SSA

GDP of US$ 44.3 billion

10.3% GDP growth - fastest

growing in East Africa

S$ 28.2 million trade with

Singapore (2014)

Key industries: Agri-

business, Manufacturing

and Mining

Government spending is

main economic driver

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

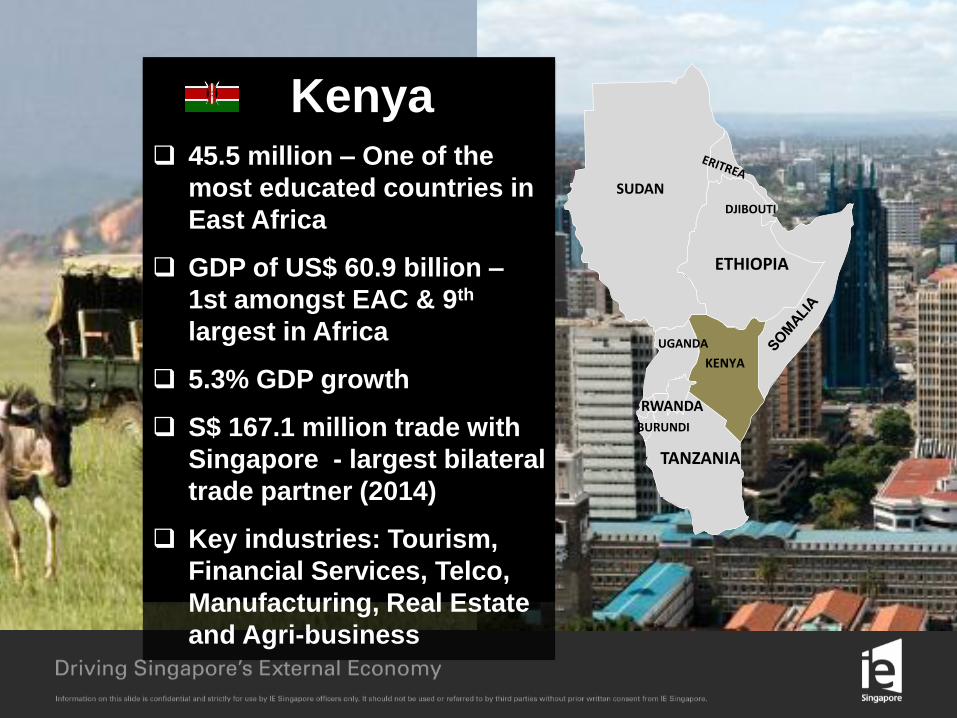

Kenya 45.5 million – One of the

most educated countries in

East Africa

GDP of US$ 60.9 billion –

1st amongst EAC & 9th

largest in Africa

5.3% GDP growth

S$ 167.1 million trade with

Singapore - largest bilateral

trade partner (2014)

Key industries: Tourism,

Financial Services, Telco,

Manufacturing, Real Estate

and Agri-business

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

Tanzania

Population of 51 million

GDP of US$ 49.2 billion

7.1% GDP growth – 2nd

fastest in East Africa

S$136.4 million trade with

Singapore (2014)

Key industries: Mining, Agri-

business, Retail and Oil & Gas

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

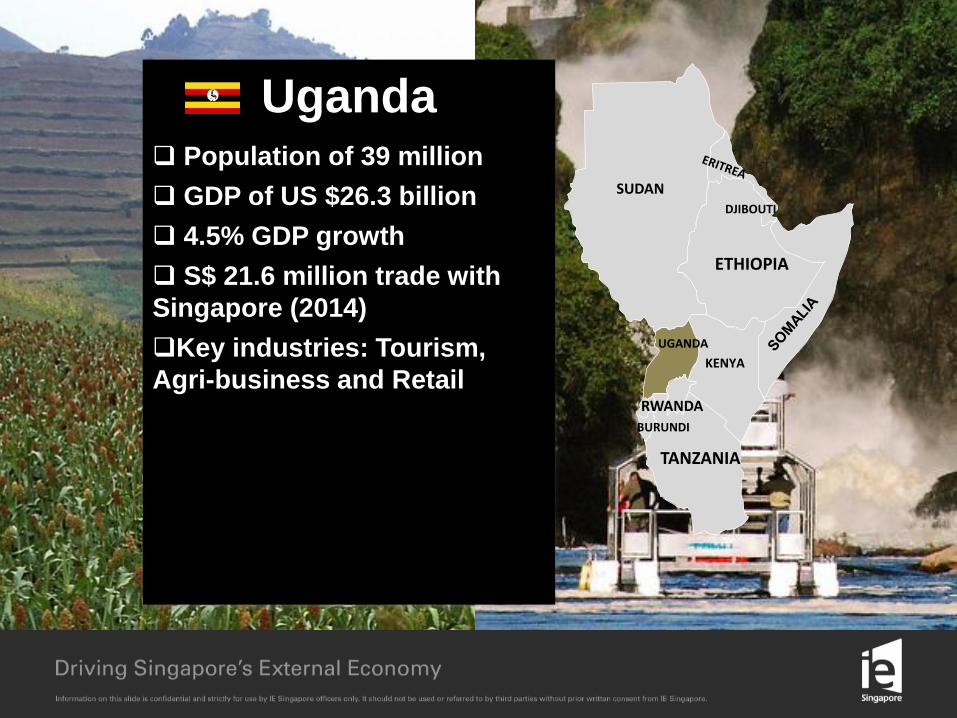

Uganda Population of 39 million

GDP of US $26.3 billion

4.5% GDP growth

S$ 21.6 million trade with

Singapore (2014)

Key industries: Tourism,

Agri-business and Retail

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

Trade and Investment with Singapore

Rank Country Total trade (in SGD m)

1 Kenya 167.1 m

2 Tanzania 136.4 m

3 Djibouti 34.1 m

4 Ethiopia 28.2 m

Trade flows between Singapore and East Africa is constant within a band and forecast is bright

Source: IE Statlink

2.7 % of total trade in SSA

Source: IE Statlink

Total trade with Africa (2014): S$15.4 billion

Top Traded Products

• Machineries and Machinery Parts

• Chemicals • Coffee, Tea and Spices • Seafood (Fish and

Mollusks)

Total trade with East Africa (2014):

S$ 409.7 million

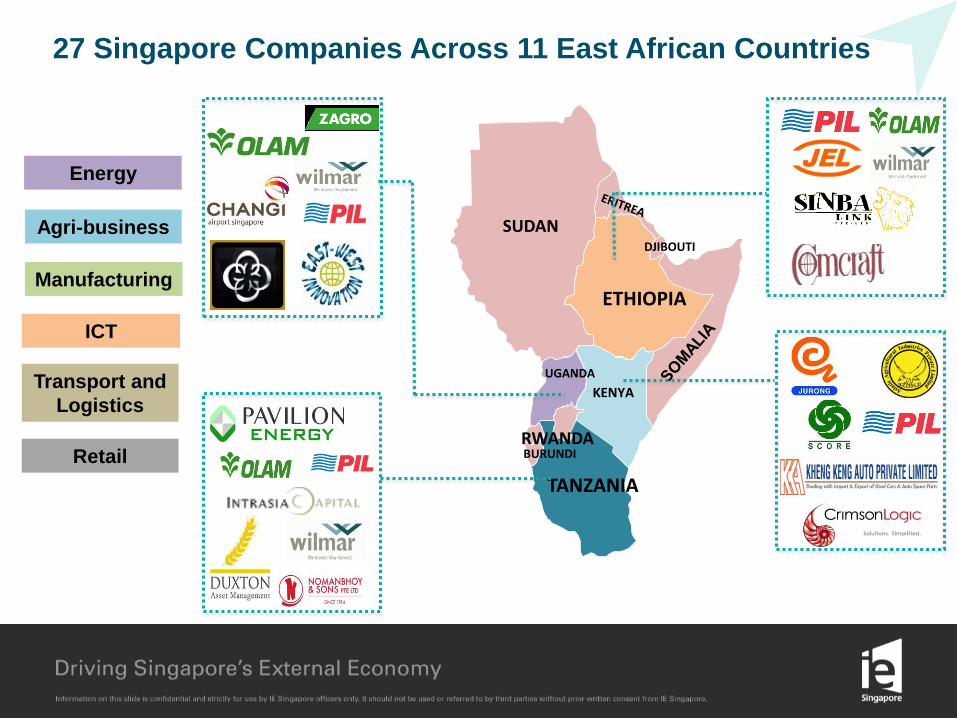

27 Singapore Companies Across 11 East African Countries

SUDAN

ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

Energy

Agri-business

Transport and

Logistics

Manufacturing

ICT

Retail

West Gate Attack - Kenya

South Sudan Conflict

Al Shabaab-Somalia

Garissa University Attack - Kenya

But the region has been in the news for the wrong reasons -

South Sudan Conflict Mpeketoni Attack-Kenya

Business as usual despite

the occasional instability

Sectoral Opportunities

Focus on sectors that mirror East Africa’s fundamental economic trends

Trend Sector of Focus

Growing middle class/

demographic shifts

FMCG

Technology/ICT

E-Government Services

Public sector capacity

building

Need for better

alternatives to public

sector services

Address infrastructure

constraints to benefit

business

Urban Infrastructure Solutions

Oil and Gas Services

Transportation and Logistics

Sustainable comparative

advantage

Agri-business

Manufacturing

Education

TVET

Increasingly educated

workforce & job skills

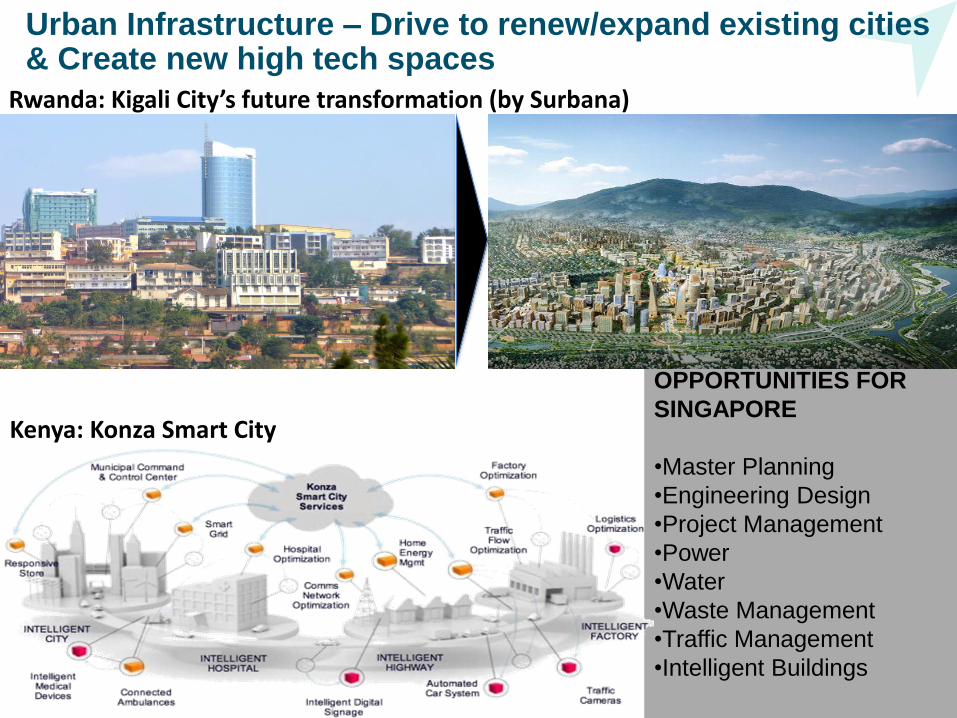

Urban Infrastructure – Drive to renew/expand existing cities & Create new high tech spaces

OPPORTUNITIES FOR

SINGAPORE

•Master Planning

•Engineering Design

•Project Management

•Power

•Water

•Waste Management

•Traffic Management

•Intelligent Buildings

Rwanda: Kigali City’s future transformation (by Surbana)

Kenya: Konza Smart City

Ogaden Basin

Southern

Rift Basin

Albertine Basin

Rift Valley Basin

Lamu Basin

Ruvu Basin

Rovuma Basin

Prospective Hotspots in East and

South Eastern Africa

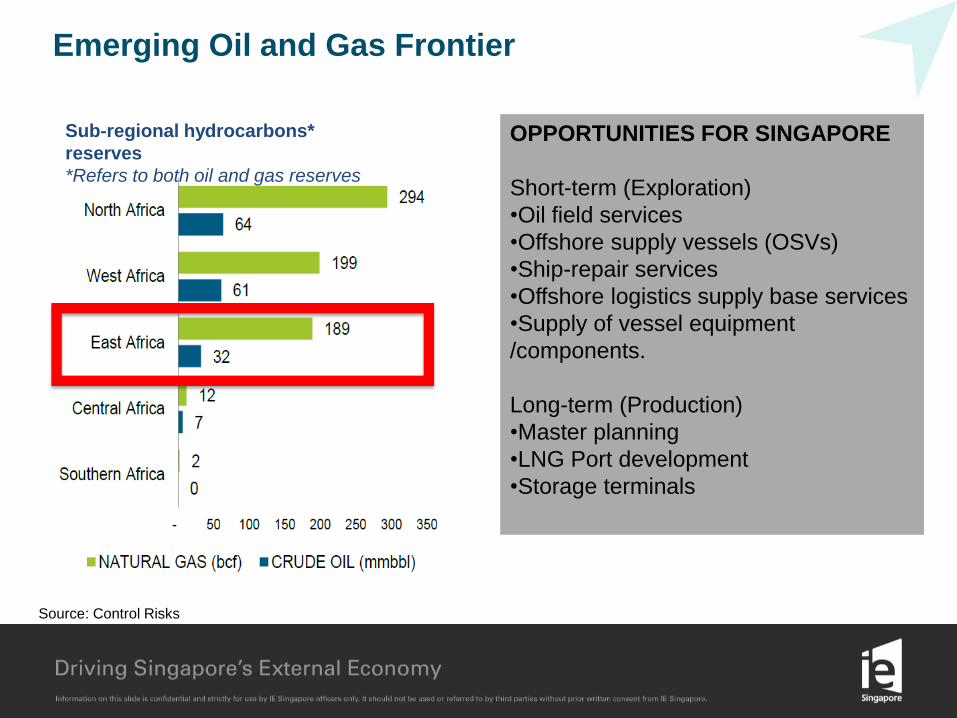

Emerging Oil and Gas Frontier

Source: Control Risks

3rd largest gas exporter by 2025

Emerging Oil and Gas Frontier

Sub-regional hydrocarbons*

reserves

*Refers to both oil and gas reserves

Source: Control Risks

OPPORTUNITIES FOR SINGAPORE

Short-term (Exploration)

•Oil field services

•Offshore supply vessels (OSVs)

•Ship-repair services

•Offshore logistics supply base services

•Supply of vessel equipment

/components.

Long-term (Production)

•Master planning

•LNG Port development

•Storage terminals

Transport and Logistics Sector –Sea and land-side opportunities

OPPORTUNITIES FOR

SINGAPORE

Proximity to Asia allows

East Africa to receive

growing volume of Asian

imports and exports

Opportunities:

•Logistics planning

•Port development and e-

customs systems

•Container freight stations

and warehousing

•Security and cargo tracking

systems

•Cold chain logistics

•Industrial zone planning

and development

Several new logistics corridors are being developed (e.g. Kenya Lappset Growth Area)

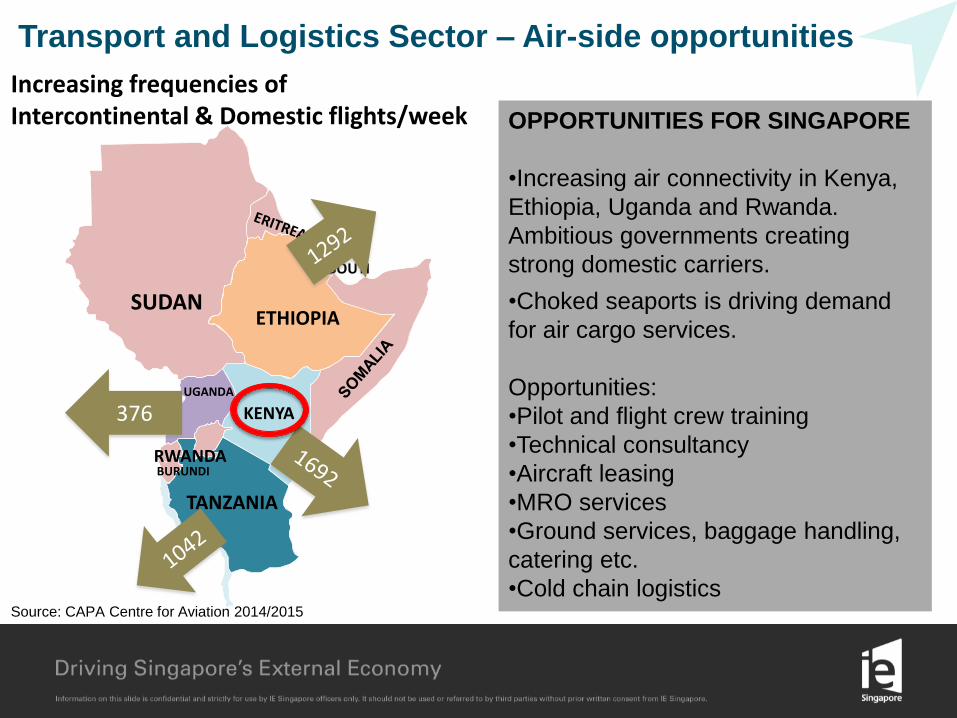

Transport and Logistics Sector – Air-side opportunities

OPPORTUNITIES FOR SINGAPORE

•Increasing air connectivity in Kenya,

Ethiopia, Uganda and Rwanda.

Ambitious governments creating

strong domestic carriers.

•Choked seaports is driving demand

for air cargo services.

Opportunities:

•Pilot and flight crew training

•Technical consultancy

•Aircraft leasing

•MRO services

•Ground services, baggage handling,

catering etc.

•Cold chain logistics

Increasing frequencies of Intercontinental & Domestic flights/week

SUDAN ETHIOPIA

DJIBOUTI

KENYA

TANZANIA

RWANDA

UGANDA

BURUNDI

376

Source: CAPA Centre for Aviation 2014/2015

Fierce competition for FDI motivates Public Capacity Building and development of e-Government Services

OPPORTUNITIES FOR SINGAPORE

Governments focusing on:

•Harmonizing business laws

•Improving EODB rankings

•Facilitating cross border trade

•Introducing and implementing

regulatory and legal policies

•Improving tax collection processes

Singapore has a rich experience in

public sector capacity building and e-

Government systems.

Improving E-government

Development in East Africa (2008-2014)

0 0.1 0.2 0.3 0.4 0.5 0.6

Middle Africa

North Africa

Southern Africa

Western Africa

East Africa

World

2014

2010

Source: UN 2014

One of the fastest growing middle classes in Africa - Demand for more consumer goods, manufacturing and tech-related services booming

OPPORTUNITIES FOR SINGAPORE

•FMCG goods (exports & in-mkt mfg)

•Technology-related products, services

and applications

•Luxury goods

•Cars and spare parts

•Food retail and service concepts

0 10 20 30 40 50

Kenya

Uganda

Ethiopia

Tanzania

Rwanda

% of Middle Class (2014)

Source: UN 2014

Middle class growth 3-5%, East Africa will

be 2nd largest consumer market by 2040

Technology-related service innovations will

become widespread (e.g. M-PESA)

Africa’s trapped agricultural potential can feed the world - Provides opportunity for Agri-business mfg. & services

OPPORTUNITIES FOR

SINGAPORE

Singapore can leverage on its

capable companies for:

oUpstream –

• High yield seed technology

• Crop protection chemicals,

fertilizers etc.

• Farm management

techniques

• Micro-financing schemes

oDownstream –

• Agro-processing units

• Cold chain logistics

• Warehousing and

transportation

• Technology apps for

farming communities etc.

46% of Africa’s arable land is unused, and less

than 30% of yield is achieved on used land

OPPORTUNITIES FOR SINGAPORE

•Pressing need to upskill youth and

provide jobs for the unemployed.

•Despite being on target to meet the

100% primary enrollment MDG,

education gap in various education

stages need to be met.

•Singapore is well positioned to enter:

•Pre-school

•Secondary

•Tertiary

•Technical and vocational

education training (TVET)

Need for education and vocational training as economy grows and diversifies

Source: Human Development Report Office, UNDP (Ernst and Young

2013)

IE’s East Africa Approach

Sector Engagement

Urban Solutions 1

3

E-Government

& ICT

Transport &

Logistics

4

Agri-

business 6

7 Education FMCG 5

Trade & Investment Infrastructure (Agreements)

Building & Leveraging Networks

Awareness Creation

Broad Strategy

2 Oil & Gas

Thank You www.iesingapore.com