EARNINGS PRESSURE AND COMPETITIVE BEHAVIOR: EVIDENCE …

27

EARNINGS PRESSURE AND COMPETITIVE BEHAVIOR: EVIDENCE FROM THE U.S. ELECTRICITY INDUSTRY YU ZHANG University of California, Irvine JAVIER GIMENO INSEAD This study examines the effect of pressure felt by management to meet or beat analysts’ earnings forecasts on firms’ behavior in oligopolistic output competition. We argue that firms under such earnings pressure strive to increase current profits by exploiting market power opportunities and tightening output, even though these acts could encourage rival output expansion. Using data from the U.S. electricity generation industry, we found that firms facing earnings pressure tended to restrict output in markets in which market structure and competitor characteristics were favorable for the exercise of market power, but their competitors tended to increase output in those markets. Agency theorists have traditionally interpreted the performance expectations set by capital mar- kets as efficient mechanisms for shareholder mon- itoring (Jensen, 1986; Jensen & Meckling, 1976). Yet, dissenting work in strategy and finance has emerged, expressing concern about the likely ef- fects of such capital market pressures on long-term strategy (Jensen, 2005; Porter, 1992; Stein, 1989). Managers often complain that capital market ex- pectations shift their focus toward current earnings and away from long-term strategic commitments. For instance, Ted Turner, founder of CNN, com- mented: “When all companies are quarterly earn- ings– obsessed, the market starts punishing compa- nies that aren’t yielding an instant return. This not only creates a big incentive for bogus accounting, but also it inhibits the kind of investment that builds economic value” (Turner, 2005: 229). In a recent worldwide survey by McKinsey & Company (2006), 42 percent of respondents (managers and board members of publicly traded firms) strongly agreed that issuing earnings guidance and trying to meet earnings expectations from equity analysts led their firms to focus more on short-term earn- ings. Another survey, by Graham, Harvey, and Ra- jgopal (2005), indicated that 80 percent of respon- dents (chief financial officers [CFOs] and financial executives) would decrease discretionary spending on R&D, advertising, or maintenance to meet an earnings target, and 60 percent would avoid initi- ating a positive net present value (NPV) project if it meant falling short of analysts’ consensual earnings forecasts. This strong contrast between theory and practice highlights the importance of examining the impact of earnings pressure on firms’ behaviors and the types of actions firms choose to deal with such pressure. We define earnings pressure as the ten- sion felt by management about meeting or beating analysts’ earnings forecasts (Levitt, 1998). Graham et al.’s (2005) survey suggested that CFOs viewed earnings as the most important performance mea- sure reported to outsiders. Seventy-three percent of respondents considered analyst consensus fore- casts as an important benchmark, and over 80 per- cent believed that meeting earnings benchmarks helped to build credibility in the capital market and to maintain or increase their firm’s stock price. In general, a management can respond to earn- ings pressure in multiple ways, such as ignoring it (King, 2004), managing expectations (earnings guidance) by communicating more effectively with capital market agents (Bernhardt & Campello, We appreciate feedback from Raffi Amit, Mary Benner, Weiru Chen, James Constantini, Parthiban David, Gary Dushnitsky, Douglas Frank, Igal Hendel, Dawn Matsu- moto, Steven Monahan, Vicente Salas Fuma ´s, Peter Zem- sky, and seminar participants at the Academy of Man- agement 2007 annual meeting, Copenhagen Business School, HEC Paris, IESE, INSEAD, London Business School, National University of Singapore, Singapore Management University, Wharton School, University of California at Irvine, University of Michigan, University of North Carolina, and University of Zaragoza. We also ap- preciate the help given by Kenneth McClevey, Glenn McGrath, Robert Schnapp, Antoine Smith, Howard Stone, Sharon Sutton, and Channele Wirman at the En- ergy Information Administration, who provided access to and knowledge about the databases. Academy of Management Journal 2010, Vol. 53, No. 4, 743–768. 743 Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s express written permission. Users may print, download or email articles for individual use only.

Transcript of EARNINGS PRESSURE AND COMPETITIVE BEHAVIOR: EVIDENCE …

EARNINGS PRESSURE AND COMPETITIVE BEHAVIOR:EVIDENCE FROM THE U.S. ELECTRICITY INDUSTRY

YU ZHANGUniversity of California, Irvine

JAVIER GIMENOINSEAD

This study examines the effect of pressure felt by management to meet or beat analysts’earnings forecasts on firms’ behavior in oligopolistic output competition. We arguethat firms under such earnings pressure strive to increase current profits by exploitingmarket power opportunities and tightening output, even though these acts couldencourage rival output expansion. Using data from the U.S. electricity generationindustry, we found that firms facing earnings pressure tended to restrict output inmarkets in which market structure and competitor characteristics were favorable forthe exercise of market power, but their competitors tended to increase output inthose markets.

Agency theorists have traditionally interpretedthe performance expectations set by capital mar-kets as efficient mechanisms for shareholder mon-itoring (Jensen, 1986; Jensen & Meckling, 1976).Yet, dissenting work in strategy and finance hasemerged, expressing concern about the likely ef-fects of such capital market pressures on long-termstrategy (Jensen, 2005; Porter, 1992; Stein, 1989).Managers often complain that capital market ex-pectations shift their focus toward current earningsand away from long-term strategic commitments.For instance, Ted Turner, founder of CNN, com-mented: “When all companies are quarterly earn-ings–obsessed, the market starts punishing compa-nies that aren’t yielding an instant return. This notonly creates a big incentive for bogus accounting,but also it inhibits the kind of investment thatbuilds economic value” (Turner, 2005: 229). In a

recent worldwide survey by McKinsey & Company(2006), 42 percent of respondents (managers andboard members of publicly traded firms) stronglyagreed that issuing earnings guidance and trying tomeet earnings expectations from equity analystsled their firms to focus more on short-term earn-ings. Another survey, by Graham, Harvey, and Ra-jgopal (2005), indicated that 80 percent of respon-dents (chief financial officers [CFOs] and financialexecutives) would decrease discretionary spendingon R&D, advertising, or maintenance to meet anearnings target, and 60 percent would avoid initi-ating a positive net present value (NPV) project if itmeant falling short of analysts’ consensual earningsforecasts.

This strong contrast between theory and practicehighlights the importance of examining the impactof earnings pressure on firms’ behaviors and thetypes of actions firms choose to deal with suchpressure. We define earnings pressure as the ten-sion felt by management about meeting or beatinganalysts’ earnings forecasts (Levitt, 1998). Grahamet al.’s (2005) survey suggested that CFOs viewedearnings as the most important performance mea-sure reported to outsiders. Seventy-three percent ofrespondents considered analyst consensus fore-casts as an important benchmark, and over 80 per-cent believed that meeting earnings benchmarkshelped to build credibility in the capital marketand to maintain or increase their firm’s stock price.

In general, a management can respond to earn-ings pressure in multiple ways, such as ignoringit (King, 2004), managing expectations (earningsguidance) by communicating more effectively withcapital market agents (Bernhardt & Campello,

We appreciate feedback from Raffi Amit, Mary Benner,Weiru Chen, James Constantini, Parthiban David, GaryDushnitsky, Douglas Frank, Igal Hendel, Dawn Matsu-moto, Steven Monahan, Vicente Salas Fumas, Peter Zem-sky, and seminar participants at the Academy of Man-agement 2007 annual meeting, Copenhagen BusinessSchool, HEC Paris, IESE, INSEAD, London BusinessSchool, National University of Singapore, SingaporeManagement University, Wharton School, University ofCalifornia at Irvine, University of Michigan, University ofNorth Carolina, and University of Zaragoza. We also ap-preciate the help given by Kenneth McClevey, GlennMcGrath, Robert Schnapp, Antoine Smith, HowardStone, Sharon Sutton, and Channele Wirman at the En-ergy Information Administration, who provided access toand knowledge about the databases.

� Academy of Management Journal2010, Vol. 53, No. 4, 743–768.

743

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download or email articles for individual use only.

2007), engaging in “creative accounting” (such ascapitalizing rather than expensing some costs, ormanaging discretionary accruals) (Degeorge, Patel,& Zeckhauser, 1999), or making business decisionsto accommodate the pressure (Graham et al., 2005).Researchers in accounting and finance have ex-plored how earnings pressure may affect financialcommunications and accounting manipulations(Burgstahler & Eames, 2006) and have revealed dra-matic stock reactions when firms miss earningsforecasts (Skinner & Sloan, 2002). Yet an importantquestion for strategic management scholars andpractitioners is whether firms make substantivechanges in business actions (such as competitivebehaviors, tangible or intangible investments, entryor exit into markets) in response to earnings pres-sure, and if so, whether these changes are beneficialor detrimental for long-term competitiveness.

This study focuses on the impact of earningspressure on product-market competitive behaviorin oligopolistic markets. Competitive behavior inoligopolistic industries involves managing trade-offs between current earnings and future competi-tiveness, particularly in regulating the exercise ofmarket power when firms have powerful positions.In oligopolistic industries, firms have varying de-grees of market power, depending on the marketstructure in which they function, their extent ofdominance in the market, and the extent of theircompetitors’ motivation and ability to respond ag-gressively. In industries with differentiated prod-ucts, firms with market power may increase prices,with the expectation that demand will not reduceexcessively. In commodity industries, firms withmarket power may influence prices and currentearnings by restraining the output supplied to themarket (Jacquemin & Slade, 1989). However, exer-cising market power (by restricting output or in-creasing prices) may hinder future competitivenessby inciting competitive expansions by rivals or en-trants that could have been preempted by moreaggressive competitive behavior (Caves, Fortunato,& Ghemawat, 1984; Kamien & Schwartz, 1975). Sofirms with market power experience an intertem-poral trade-off between generating current earningsby exercising their potential market power, andmaintaining long-term competitiveness by pre-empting competitors’ expansions.

Earnings pressure, we argue, affects how firmsregulate their competitive behavior and resolve thatcompetitive intertemporal trade-off. Here, we ex-amined the effect of earnings pressure on compet-itive behavior in the U.S. electricity generation in-dustry. This is a commodity industry in whichcompetition intensity is based on available outputrelative to demand. We argue that earnings pres-

sure encourages dominant firms to exercise marketpower by restricting output so as to increase pricesand current earnings, even though such behaviormay encourage output expansion by competitorsand undermine competitiveness. Consequently, weexplore contingencies that regulate the incentivesto exercise market power. We also examine howearnings pressure influences competitive interac-tion and the competitive behavior of rivals.

To our knowledge, this is the first study to exam-ine the effect of earnings pressure on competitivestrategy decisions. It contributes to a small butgrowing literature on how capital markets and fi-nancial conditions affect firms’ competitive deci-sions. Prior work in this stream has focused mainlyon the role of financial leverage on competitivedecisions (Chevalier, 1995a, 1995b; Phillips, 1995),whereby cash flow requirements to cover interestpayments impose a short-term constraint on com-petitive decisions. Our study shifts attention from“hard” constraints imposed by capital structure,such as debt covenants, to “soft” constraints asso-ciated with the management of capital market ex-pectations. In addition, though leverage representsa constraint on short-term cash flows, earningspressure influences the trade-off between currentand future earnings. Our study shows that pres-sures from capital markets may shift the emphasistoward current earnings generation, affecting thecompetitive behavior of firms and the competitiveinteractions in oligopolistic competitive environ-ments (Porter, 1992; Stein, 1989). It adds to emerg-ing understanding of the impact of investment an-alysts and capital markets on firm behavior andperformance (Benner, 2007; Moreton & Zenger,2005; Zuckerman, 1999, 2000).

THEORY AND HYPOTHESES

Earnings Pressure: Antecedents and Effects

Earnings pressure results from the complex dy-namic interactions between investors, investmentanalysts, and managers, in a context characterizedby uncertainty, asymmetric information, imperfectobservability of managerial actions, and potentialconflicts of interest. Given consistent operating andaccounting practices, managements develop inter-nal expectations about their firms’ future perfor-mance that are based on historical performance,comparisons with peer firms (Cyert & March, 1963;Greve, 2003), and estimates about internal and ex-ternal changes (Chen, 2008; Gavetti & Levinthal,2000). Managers experience attainment discrepancywhen, for a given future or ongoing period of activity(year or quarter), the consensus of external analysts’

744 AugustAcademy of Management Journal

earnings forecasts is above the internal expectationsof management about future company earnings(Wiseman & Bromiley, 1996). Earnings pressure mayresult from the confluence of two intertwined condi-tions: (1) divergence between analysts’ and manage-ment’s earnings expectations and (2) the large actualand perceived market penalties for a company miss-ing earnings forecast consensus.

The role of investment analysts is not to provideperformance targets for management, but to evalu-ate a number of stocks and provide buy, hold, orsell recommendations to investors. As part of thejustification for their recommendations, analystsforecast future company earnings in their reports.For their forecasts, analysts do not limit themselvesto using historical information or stock market in-formation, but also use information disclosed bymanagers about a company’s past performance andfuture prospects, external information about thecompany and its environment, and their own re-search and professional judgment (Schipper, 1991).There is evidence that analysts with greater forecastaccuracy benefit from improved reputation and bet-ter career promotions (Stickel, 1992). However, de-spite the overarching objective of accuracy, ana-lysts are exposed to diverse organizational andcareer incentives that may cause systematic biasesin their forecasts. First, there is substantial evi-dence of optimism bias in analysts’ forecasts andrecommendations (Chopra, 1998; Dreman & Berry,1995). This optimism bias has been associated withconflicts of interests, such as the incentives tomaintain underwriting relationships with a cov-ered firm (Dechow, Hutton, & Sloan, 1999a; Dugar& Nathan, 1995; Lin & McNichols, 1998; Michaely& Womack, 1999) or to generate sales and tradingcommissions for the employer brokerage house(Cowen, Groysberg, & Healy, 2006). Hong and Ku-bik (2003) found that, controlling for relative fore-cast accuracy, analysts with greater optimism biasexperienced superior career progressions. Second,analysts also exhibit a herding bias as a result ofcareer and reputation concerns. Inexperienced an-alysts who deviate from the consensus others havearrived at are more likely to be terminated (Hong,Kubik, & Solomon, 2000). Consequently, analyststend to release forecasts similar to those previouslyannounced by other analysts, even when their in-formation does not justify doing so (Trueman,1994). Therefore, although analysts provide richand informative individual forecasts, in aggregatethese forecasts may exhibit excessive consensustoward optimistic earnings projections.

Firms’ managements can influence the formationof analysts’ forecasts by the public disclosure ofinternal information and objectives, or “public

earnings guidance” (Cotter, Tuna, & Wysocki,2006). Because of the perceived penalties for miss-ing earnings forecasts, managements may use pub-lic guidance to “talk down” the analysts’ forecastsso that they are easier to meet or beat. Offeringguidance, however, is costly in terms of manage-ment attention, and risky for a firm’s reputation forcredibility. Chen (2004) showed that stock marketreactions to negative earnings surprises were moredrastic if a firm failed to meet its own guidance. Asa consequence, public guidance releases tend to beinfrequent and overly conservative, as firms seek to“under-promise and over-deliver” (Graham et al.,2005: 42). Cotter et al. (2006) found that firms is-sued guidance for only about 22 percent of reportedearnings and that guidance was disproportionallyused when analysts’ forecasts were perceived asoverly optimistic. Most management guidancetends to be pessimistic, not only relative to ana-lysts’ forecasts, but also relative to the earningsactually reported (Chen, 2004). In fact, CFOs tendto publicly announce targets that are below theirfirms’ internal expectations so as to maximizechances of a positive surprise (Graham et al., 2005:42). Although analysts adjust their forecasts to newguidance, most analysts anticipate a conservativebias in guidance and do not fully match it in theirforecasts (Cotter et al., 2006). In consequence, theinteractions between analysts and management inthe formation of earnings forecasts might be viewedas a negotiation process (with analysts taking anoptimistic stance and management taking a morepessimistic position in public guidance), whichmay explain the divergence between consensualforecasts and internal management expectations.

The second factor contributing to earnings pres-sure is the large perceived and actual stock pricedecline suffered by a company that fails to meet anearnings forecast consensus. For example, Skinnerand Sloan (2002) found that unexpectedly missingearnings forecasts by 1 percent could lead to anegative abnormal stock market return of 15 per-cent for growth stocks and 5 percent for valuestocks. This stock price reduction can have a largeimpact on managers’ stock options compensation(Hall & Liebman, 1998). Failing to meet analysts’earnings forecasts is also a strong predictor of CEOturnover (Puffer & Weintrop, 1991).

In principle, it is not obvious why management,rather than analysts, should be penalized whenreported earnings differ from analysts’ forecasts(Dechow & Skinner, 2000). One reason for the stockmarket penalty is that investors use analysts’ fore-casts to form their valuation of stocks and thereforeupdate their expectations of future earnings levelsand growth rates when those forecasts are not met.

2010 745Zhang and Gimeno

Because investors have limited cognitive capabilityto process available information, and informationsearch costs are high, they are willing to use ana-lysts’ forecasts to help them infer a firm’s perfor-mance (Degeorge et al., 1999). Recent research hasshown that although some (more sophisticated) in-vestors were aware of possible biases in certainanalysts’ forecasts and tried to correct for it (Mal-mendier & Shanthikumar, 2007; Mikhail, Walther,& Willis, 2007), the overall market was not able tofully correct for such biases (Hayes & Levine, 2000).When a negative earnings surprise happens, inves-tors must determine how much to update theirprior beliefs about future earnings. Two sources ofasymmetric information between investors andmanagement contribute to a large negative updat-ing of expectations. First, investors lack detailedinformation about the management actions andbusiness fundamentals that impact future earnings,and they therefore rely heavily on inferences fromcurrent earnings to assess long-term value (De-chow, Hutton, & Sloan, 1999b). An earnings sur-prise therefore leads to a quick update of expecta-tions about future earnings levels and growth rates(Skinner & Sloan, 2002). Second, investors lackinformation about the credibility of a firm’s re-ported earnings but are aware of management in-centives to meet earnings forecasts and understandthat management has some discretion to smooth ormanipulate reported earnings to meet forecasts (bymanaging accounting accruals, deferral or capitali-zation of expenses, delay of investments, or otherchanges in business decisions). Therefore, the in-ability to meet earnings forecasts is perceived as acue about more serious underlying problems(Stein, 1989). Both reasons lead investors to heavilydiscount a stock after a negative earnings surprise(Graham et al., 2005: 30). The intensity of the stockmarket response and the negative personal conse-quences for managers’ incomes and careers rein-force the strong incentive for managers to meetearnings expectations.

Because both analysts’ forecasts and potentialearnings are updated via additional informationand ongoing interactions between analysts andmanagement, earnings pressure is a dynamic phe-nomenon. In this article, we focus on the effects ofearnings pressure during a period of business ac-tivity. To avoid reverse causation, we examinedearnings pressure at the beginning of that period.Managers had various means to manage earningspressure during the period. One approach, as de-scribed above, is to disclose additional informationduring the period or prior to earnings announce-ments to guide analysts’ forecasts downward to-ward achievable levels (Bernhardt & Campello,

2007). Another approach, typically taken at thetime of earnings announcement (i.e., after the clos-ing of accounts), is to use “creative” accounting tomeet earnings expectations, such as capitalizingexpenditures and managing discretionary accruals(Degeorge et al., 1999), or to use symbolic languageto reduce the negative impact when reporting earn-ings below analysts’ consensual expectations(Pozner & Zajac, 2005). Finally, managers maychange real business decisions affecting revenuesor expenses during a period in order to increasecurrent earnings (Graham et al., 2005). Our studyfocuses on this third mechanism.

From a strategic management perspective, a ma-jor concern is whether earnings pressure leads tochanges in business decisions and whether thosechanges have a beneficial or detrimental effect onfuture performance. So far, the debate has mainlybuilt on anecdotal evidence (Abegglen & Stalk, 1985;Porter, 1992; Useem, 1996), interviews or surveyswith managers (Graham et al., 2005; McKinsey &Company, 2006), classroom experiments (Bhojraj &Libby, 2005), or indirect inference from financialstatements (Roychowdhury, 2006). There is no sys-tematic direct evidence of the consequences of earn-ings pressure for firms’ behavior and performance.

The effect of earnings pressure on long-term per-formance hinges on whether firms face a bindingintertemporal trade-off between current and futureearnings (i.e., whether increasing current earningswould reduce future earnings), and the nature ofthat trade-off. Previous research on myopic corpo-rate behavior has tended to focus on intertemporaltrade-offs due to long-term investments, particularlyif those investments involve current (i.e., noncapital-ized) expenses, such as discretionary R&D and mar-keting expenses, that reduce current earnings whilecreating future intangible assets that are difficult forinvestors to measure (Stein, 1989). In these situations,myopic firms can easily increase current earnings byreducing investment in intangible assets (e.g.,Bushee, 1998; David, Hitt, & Gimeno, 2001; Hoskis-son, Hitt, Johnson, & Grossman, 2002).

Another source of intertemporal trade-offs iscompetitive interactions. Firms’ current competi-tive decisions, such as pricing or output decisions,influence not only current earnings, but also futurecompetitive reactions and long-term competitive-ness. For example, firms with aggressive behaviorin output competition may discourage output ex-pansion by competitors and preempt future entry(Ghemawat, 1984; Lieberman, 1987). Firms that re-spond in an aggressive (rather than accommodat-ing) way to new entry or rival expansion may buildreputations for toughness that deter similar expan-sions in the future (Milgrom & Roberts, 1982).

746 AugustAcademy of Management Journal

Therefore, it is important to examine the impact ofearnings pressure on firms’ competitive behavior inoligopolistic contexts.

Competitive Behavior under Earnings Pressure

We define competitive behavior as decisions oractions that improve a firm’s market position rela-tive to its competitors (Grimm, Lee, & Smith, 2006:22). In a general context, competitive behavior mayinclude decisions that provide superior customervalue (either by increasing the customers’ willing-ness to pay for the firm’s products relative to rivalofferings, or by reducing the price), or that preemptmarket space from competitors. Two trade-offs typ-ically determine the intensity of competitive be-havior: a static trade-off between margins and vol-umes, which determines current earnings, and adynamic, or intertemporal, trade-off between cur-rent and future earnings. In the static trade-off,aggressive competitive behavior (decreasing price,increasing marketing expenses, expanding output)can reduce unit margins and will only be effectiveif it results in sufficient volume increase to com-pensate for the lower unit margins. In particular,firms with market power (firms with dominantmarket shares in concentrated markets and withrivals that are unwilling or unable to challengethem) can expand current profits by reducing theaggressiveness of their competitive behavior (in-creasing prices, tightening supply), since the in-crease of margins over a large volume will compen-sate for some moderate reduction in volumes.However, the short-term exercise of market powercan hamper future competitiveness and profitabil-ity, creating an intertemporal trade-off betweencurrent and future earnings (Caves et al., 1984).

In commodity industries, the main competitivedecisions firms make concern capacity invest-ments, which are difficult to adjust in the shortterm, and output decisions, which are limited bycapacity and determine market-clearing prices (theprice at which supply equals demand) and compet-itive intensity. Because earnings pressure takesplace over a short period (a quarter or a year), wefocus on its effect on determining output relative toavailable capacity, also known as capacity utiliza-tion. Output decisions in oligopolistic competitionare highly interactive, since firms’ output decisionsaffect market-clearing prices and competitors’ out-put decisions. This mutual adjustment of outputdecisions, and the equilibrium outcomes, are cap-tured in simplified form in the Cournot oligopolymodel (Cournot, 1838), whereby firms make simul-taneous interdependent output decisions that de-termine market-clearing prices and profits.

Capacity utilization is first determined by thestatic trade-off between volume and margin. Facingthis trade-off, firms acting as price takers (e.g., firmsin fragmented markets or with low market shares)generally seek capacity utilization that is as high aspossible (thereby spreading fixed costs over greatervolume), as they face technical and economic lim-itations, such as demand volatility and variation inthe relative cost efficiency of their different produc-tion units. However, when firms have marketpower and sufficient capacity and output share toinfluence market-clearing prices, they recognizethat increasing capacity utilization in marginalunits may decrease market-clearing prices and mar-gins for other units. Absent intertemporal trade-offs, the tension between reducing average costs byincreasing utilization versus increasing prices byrestricting output determines capacity utilization.1

Intertemporal trade-offs between current and fu-ture earnings may also influence capacity utiliza-tion. Research in industrial economics has sug-gested that both capacity and output levels affectthe development of attractive future competitivepositions. Capacity and output competition repre-sent competition in “strategic substitutes,” whereinone party’s competitive action level leads to a re-duction of the other party’s action level (Fudenberg& Tirole, 1984). Building and maintaining excesscapacity may provide a credible commitment todeter entry or rival expansion (Ghemawat, 1984;Lieberman, 1987; Spence, 1977). In addition, for agiven level of installed capacity, greater output lev-els (i.e., greater capacity utilization) reduce resid-ual demand for competitors, reduce market-clear-ing prices, and generally discourage outputexpansion by rivals and potential entrants. Thisbehavior, known as “limit pricing” in the econom-ics literature (Bain, 1949; Lieberman, 1987), sug-gests that higher output and capacity utilization byincumbents (and therefore lower prices) preventoutput and capacity expansion by rivals and poten-

1 In an oligopolistic competition market, the optimal static

output decision is determined by MC(qi) � MR(qi) � P�1 �

si

��� � P, where MC is marginal cost, MR is marginal reve-

nue, P is market price, si is firm i’s market share, � is thedemand elasticity, and � is a “competitive conduct pa-rameter” that measures how a firm’s decreased outputaffects total market output (including the output fromcompetitors) (Bresnahan, 1989). Therefore, output reduc-tion associated with exercising market power will begreater when market share is high and elasticity is low,and when competitor output expansions will not under-mine a firm’s output reduction.

2010 747Zhang and Gimeno

tial entrants and encourage the exit of marginal rivals.These mechanisms have been empirically supportedin several industries (Masson & Shaanan, 1986).Limit pricing represents a sacrifice of short-termprofits relative to the potential profits from fullexercise of pricing power, but a potential enhance-ment of future performance. For firms with marketpower, this tension constitutes an intertemporaltrade-off between maximizing current earnings andmaintaining strong competitive positions for thefuture (Caves et al., 1984).

We argue that earnings pressure shifts the bal-ance between short-term exercise of pricing powerand future competitive preemption. Companieswhose management is not facing earnings pressureare more likely to sacrifice some potential earningsto preempt entry and rival expansion. Given theirexisting capacity, their level of capacity utilizationshould be higher than the level that would maxi-mize current earnings by exploiting the availablemarket power (Kamien & Schwartz, 1975). In con-trast, firms whose managements face earnings pres-sure (abbreviated hereafter to “firms facing earn-ings pressure”) need to meet current earningsexpectations and are more likely to exercise theshort-term pricing power available to them, even ifthat encouraged rival expansion or entry (Caveset al., 1984). This logic suggests the following:

Hypothesis 1. Firms facing greater earningspressure have lower capacity utilization rela-tive to available capacity, other things beingconstant.

The Role of Market Structure andCompetitive Environment

Hypothesis 1 is proposed as a main effect ofearnings pressure on capacity utilization levels.However, our theory suggests that the presence andintensity of this effect depend on structural contin-gencies, and particularly the extent to which a firmhas pricing power. If a firm has little or no pricingpower, a reduction of capacity utilization, as pro-posed above, could be self-defeating, since the firmwould sacrifice volume to spread fixed costs with-out gaining any additional margin per unit. There-fore, variables that reflect the extent of pricingpower should moderate the relationship betweenearnings pressure and capacity utilization. Marketpower implies that a firm has sufficient output andcapacity position to influence market-clearingprices and that its competitors are unwilling orunable to quickly expand output to make up for ashortage it creates as the dominant firm. In partic-ular, we focus on four general dimensions: the capac-

ity share dominance of a firm within a particularmarket, market concentration among the remainingincumbents, goal heterogeneity among incumbents,and competitors’ capacity constraints.2

Dominant capacity share. When a firm with adominant capacity share restricts output, it createsa price “umbrella” that benefits its remaining out-put in the market. Therefore, the loss of volume iscompensated for by the gain in margin over itsremaining output. Moreover, because this firm hasa dominant share of capacity, it can restrict enoughof its capacity to meaningfully influence prices. Incontrast, firms with lower shares of capacity haveneither the ability nor the motivation to act as pricemakers. Given their limited capacity, restrictingoutput may not be sufficient to generate the desiredincrease in market prices. Even if they can affectprices, the gain on margins will affect a smallerremaining output, and the benefit will be lower.Therefore, in general, firms with significant capac-ity share are more motivated to act as price makersand to restrain capacity utilization to maintainprices and margins (Chen & Hambrick, 1995; Jac-quemin & Slade, 1989), even though this may resultin future market share erosion (Caves et al., 1984;Ferrier, Smith, & Grimm, 1999). Firms with limitedcapacity share tend to act as price takers and tofree-ride on the price umbrella created by the dom-inant firms.

If earnings pressure puts an emphasis on currentearnings generation, we would expect its negativeeffect on capacity utilization to be particularlyprevalent among firms with dominant capacityshare rather than those with limited capacity share.For firms with limited share, decreasing capacityutilization will fail to increase prices and thereforewill not help the firms meet their current earningstargets (in fact, it will reduce earnings). For domi-nant firms, however, for a given available capacitythis restriction on capacity utilization will allowthem to increase current earnings, albeit at the riskof encouraging rival output expansion.

Hypothesis 2a. The effect of earnings pressureon capacity utilization level is more negativewhen firms have larger capacity shares.

Market concentration. A firm’s ability to act as aprice maker depends on the likely responses by

2 These dimensions are linked to the general formula

for marginal revenue �MR � P�1 �si

���� in footnote 1 as

well, since market share is a factor in the model (si), andmarket concentration, goal heterogeneity, and competi-tors’ capacity constraints are linked to the competitiveconduct parameter (�).

748 AugustAcademy of Management Journal

other incumbents. If the firm faces a fragmentedmarket structure with many competitors, this couldreduce the short-term benefit of restraining output,since these competitors are likely to expand outputaccordingly. On the other hand, if the rest of themarket is concentrated in a few incumbents withlarger shares, these incumbents will be aware oftheir oligopolistic interdependence and will recog-nize the collective benefits of exercising marketpower. Under these conditions, the expected returnfrom a short-term exercise of pricing power will begreater, since other incumbents are more likely toalso maintain output discipline to benefit fromhigher prices. Therefore, in general, we expect afirm to be more likely to restrict capacity utiliza-tion, for a given available capacity, if it is in aconcentrated market than if it is not in a concen-trated market (Stigler, 1964). Earnings pressure fur-ther enhances that effect, since it shifts the inter-temporal trade-off in favor of current earnings. Wetherefore propose that the restriction of capacityutilization by firms facing earnings pressure will bestronger if the firms are in concentrated markets.

Hypothesis 2b. The effect of earnings pressureon capacity utilization level is more negativewhen firms are in more concentrated markets.

Goal heterogeneity among competitors. In someindustries and markets, competitors have heteroge-neous governance and strategic objectives. For ex-ample, for-profit banks compete with credit unioncooperatives, for-profit insurance companies com-pete with mutuals, and private hospitals competewith public and not-for-profit hospitals. This het-erogeneity of objectives is believed to complicateoligopolistic coordination and therefore increasecompetition (Newman, 1978). In the electricity in-dustry, as in other deregulated industries, investorownership is often complemented by other forms ofasset ownership (e.g., federal or state governments,municipal authorities, cooperatives, etc.). The ob-jectives of these non-investor-owned generatorsdiffer markedly from those of investor-owned gen-erators, since their prime objective tends to be wel-fare maximization subject to a constraint of self-financing, rather than profit maximization. Inparticular, reducing output to increase prices isantithetical to the nature of these non-investor-owned generators. Therefore, they have vastly dif-ferent objectives that lead them to act in a way thatdisrupts investor-owned generators’ ability to exer-cise pricing power. Restricting capacity utilizationto increase market price is likely to be counterpro-ductive in markets in which non-investor-ownedgenerators hold a significant share. For companiesexperiencing earnings pressure, we expect to see

restrictions in capacity utilization, relative to avail-able capacity, in markets that are dominated by for-profit competitors (investor-owned generators), butwe expect to see less such restriction in markets withsignificant penetration by not-for-profit competitors.

Hypothesis 2c. The effect of earnings pressureon capacity utilization level is more negativewhen firms are in markets with more for-profitcompetitors.

Competitors’ capacity constraints. A firm’s abil-ity to exercise market power is limited if its com-petitors can easily and quickly expand capacityutilization to take advantage of the resulting resid-ual demand. A dominant firm’s restriction of ca-pacity utilization, given its available capacity, in-creases the residual demand available to rivals. Ifthese rivals have excess capacity in relatively effi-cient plants, they can meet the increased residualdemand while incurring only the marginal costs ofthe marginal plant in operation. In that situation, areduction of output by the focal firm simply shiftsoutput to its competitors, without necessarily in-creasing market prices. However, when competi-tors are capacity constrained, they are unable tomeet the increased residual demand. A reduction ofcapacity utilization by a focal firm will more likelyresult in increased prices and margins. Therefore,firms facing earnings pressure can exercise marketpower more effectively if competitors are capacityconstrained. Accordingly, we argue that:

Hypothesis 2d. The effect of earnings pressureon capacity utilization level is more negativewhen firms face competitors with tighter ca-pacity constraints.

Competitive Interactions by Firms FacingEarnings Pressure

The previous hypotheses suggest that dominantfirms facing earnings pressure seek to increase cur-rent earnings by restricting capacity utilization,given their available capacity. However, the perfor-mance consequences of earnings pressure criticallydepend on the nature of competitive interactionswith rivals. Since output decisions in oligopolisticcompetition are interdependent, we expect earn-ings pressure by dominant firms to affect not onlythe competitive behavior of these firms, but also thecompetitive behavior of their competitors. In par-ticular, we argue that firms intensify their compet-itive behavior when their dominant competitorsface earnings pressure. These cross-rival effectspartially undermine the intended performance ben-

2010 749Zhang and Gimeno

efits of output restrictions, since rivals benefit byexpanding their output.

Output and capacity utilization decisions arepart of the common repertoire of competitive ac-tions in output-based industries, and therefore thelikelihood of competitive interaction is high (Chen,Smith, & Grimm, 1992). As represented in theCournot model, output decisions by oligopolisticcompetitors are “strategic substitutes” (Fudenberg& Tirole, 1984): lower output by one competitormotivates higher output by its rivals, and viceversa. In our context, dominant competitors facingearnings pressure will lower capacity utilization(as stated in the previous hypotheses). Other thingsbeing constant, this output reduction causes an in-crease in market-clearing prices and encourageshigher capacity utilization by other firms in themarket. A higher price umbrella will allow firms toincrease utilization of marginal plants with lowerproductivity or higher unit costs.

Theoretically, the cross-rival effect of earningspressure may occur through two causal processes.The first, and most likely, is an indirect causalpath: dominant competitors facing earnings pres-sure reduce their capacity utilization, and this re-duction triggers greater capacity utilization by ri-vals. In that path, firms do not need to be aware ofthe earnings pressure on their rivals, but they reactto their rivals’ realized competitive behaviors. An-other possible, but far less likely, causal path is adirect one: firms recognize their dominant competi-tors are suffering from earnings pressure and act ag-gressively in anticipation of a soft, accommodatingresponse. However, this path would require commonknowledge about earnings pressure on rivals, whichmay be a limiting assumption in many contexts.

Empirically, capacity utilization decisions amongcompetitors in commodity industries do not occurdiscretely and in sequence but happen interactivelyover time. For example, electricity generators ad-just output for daily and hourly intervals of de-mand. In those cases, competitors’ capacity utiliza-tion levels are mutually interdependent, as each firmadapts its output to the actual or expected output ofcompetitors. When dominant firms in a market faceearnings pressure, the mutual adjustment would shifttoward lower capacity utilization by the dominantfirms and consequently greater capacity utilization bytheir competitors. Therefore, we propose:

Hypothesis 3. Firms have higher capacity uti-lization relative to available capacity whentheir dominant competitors face higher earn-ings pressure.

In summary, we propose that firms experiencingearnings pressure shift their focus toward generating

current earnings by exercising market power (tryingto increase prices by restricting output), the more sowhen structural conditions favor this effort. Yet earn-ings pressure may also affect competitive interac-tions, since it may encourage expansion by competi-tors. Our hypotheses provide a model of howearnings pressure interacts with competitive contextin determining competitive behavior.

DATA AND METHODS

Data and Sample

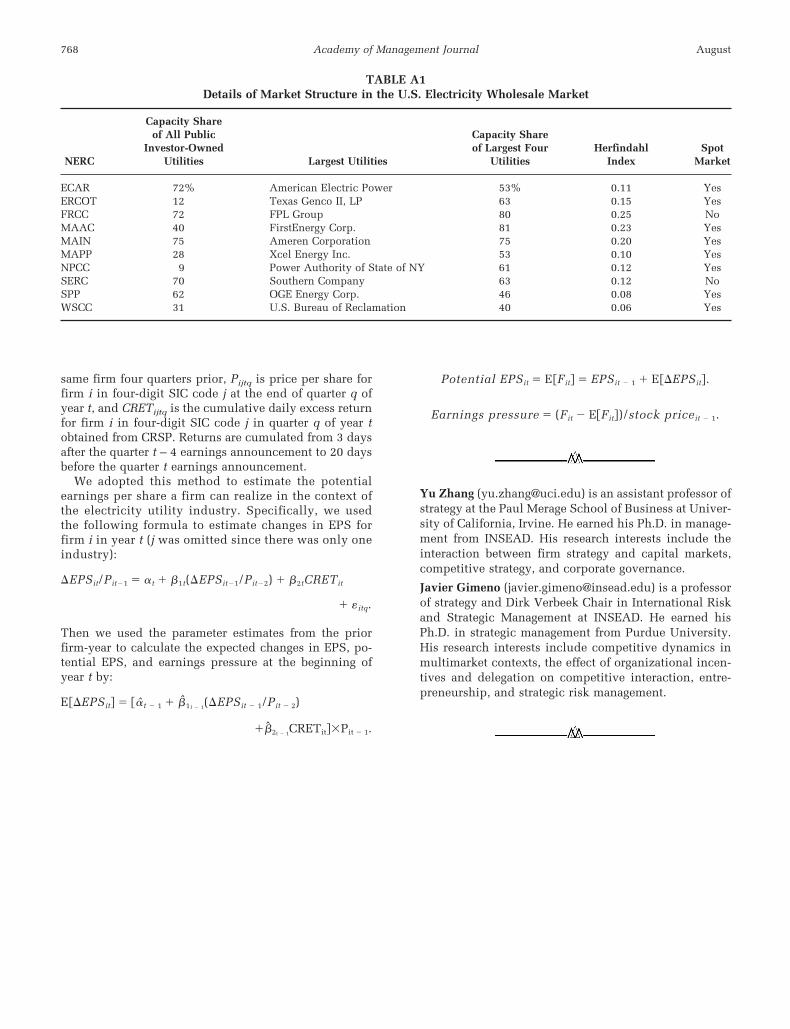

Since competitive interaction patterns vary acrossindustries, depending on economic and institu-tional conditions, it was helpful to focus on a singleindustry in hypothesis testing. After consideringseveral contexts, we selected the U.S. electricitygeneration industry, as its characteristics made it asuitable setting in which to test the effect of earn-ings pressure on competitive behavior in commod-ity markets. Electricity is the quintessential homo-geneous product: electricity produced by onegenerator is indistinguishable from that producedby another. Typically, generators supply output fordifferent daily and hourly periods, and the totaloutput supplied in the market and the demandduring those periods determine the price of thatelectricity. Economic researchers have found theCournot model of output competition to be a goodapproximation of the competitive interactions inthis industry (Borenstein & Bushnell, 1999). Thepassage of the Energy Policy Act in 1992 opened thewholesale electricity market (for transactions be-tween generators and distributors) to competition byeligible generators, even before the opening of theretail market. For the purposes of wholesale electric-ity competition, the United States was divided into12 wholesale markets, or North American ElectricReliability Council (NERC) regions, as described inAppendix A. This feature provided heterogeneity ofcompetitive structures in different markets.

Despite the deregulation of the wholesale market,there is concern as well as evidence that thesemarkets have developed oligopolistic structures inwhich a few large generators dominate. The aggre-gate demand for electricity is very inelastic, whichfurther enables incumbents to exercise pricingpower. Economic research on deregulated electricitymarkets has shown that dominant firms in concen-trated electricity markets perform “strategic with-holding” of output at periods of peak demand tomanipulate spot prices (Fabra & Toro, 2005; Joskow &Kahn, 2002; Sweeting, 2007). In particular, strategicoutput withholding was extensively studied and de-bated after the California electricity crisis in 2000.

750 AugustAcademy of Management Journal

During that period, it emerged that electricity gener-ators used artificial power plant outages to createsupply shortages in order to raise market prices andincrease their profit (McLean & Elkind, 2003).

The COMPUSTAT database listed about 124publicly traded firms for which electricity genera-tion and distribution was the principal business(under SIC codes 4911 and 4931), and analystsconstantly followed 70–80 of them (Besanko,D’Souza, & Thiagarajan, 2001). Consistently withour previous discussion, investors tended to reactsensitively to earnings forecasts and earnings sur-prises. For example, when American ElectricPower missed analysts’ consensus of $1.44 by onlya penny on October 23, 2001, its stock price fellfrom $44.19 to $42.24 within the following week(Dow Jones News Service, 2001).

Data were obtained from several sources. First,the U.S. Department of Energy’s Electricity Infor-mation Administration (EIA) provided the EIA-860database, a census of generating units (i.e., tur-bines) in power plants owned and operated by elec-tricity generators. From there, we obtained the totalcapacity that a firm held in operation or standby(still in operation but out of service for more thanthree months) in each wholesale region (market) ineach year, as well as the share of capacity in themarket. Second, the EIA-906 and EIA-920 data-bases provided annual data on electricity genera-tion at the power plant level. From there, we cal-culated the total output produced by the generatorin each market and year, as well as its averagecapacity utilization rate over the year. Finally,earnings forecasts and historical company earningswere obtained from the Institutional Broker Esti-mates System (I/B/E/S) database offered by Thom-son Financial/First Call. Our sample period wasfrom 1993, right after the deregulation, to 2005,when the latest data were published. For all firmswith more than 1 percent capacity share in anystudied market-year, we combined I/B/E/S earn-ings data and EIA capacity and output data bymatching the generator names and their I/B/E/S“tickers” and cross-checked this information by re-ferring to industry and company historical pro-files.3 We created a panel data set of 62 generation

companies,4 14 among them present in more thanone market, followed over 13 years. Despite thegeographical expansion of generators, multimarketcontact was negligible, with only 2 companiesmeeting in two or more markets.

Methods

We used panel data methods, with the unit ofanalysis being the firm-market-year. Our focus wason understanding the determinants of capacity uti-lization, given available capacity, which constrainsoutput. Moreover, because of the seasonality, cycli-cality, and volatility of electricity demand, genera-tors often maintain sufficient available capacity toserve peak demand, and average capacity utiliza-tion rates are generally low (about 52 percent in oursample). Increasing capacity utilization is not easy,however. Firms typically develop diverse portfo-lios of plants with different technologies and dif-ferent cost structures. Plants serving peak demandtend to have higher variable costs. Capacity utiliza-tion rates may not be easily comparable across gen-erators, since utilization depends on firms’ plantportfolio choices on such matters as scale and tech-nology. We constructed a model of capacity uti-lization (qimt/Kimt) that allowed it to be influ-enced by a firm’s available capacity (Kimt) in agiven market, other independent (Ximt) and con-

3 The EIA data are reported at the level of the “utilitycode” representing a single operational unit. We aggre-gated total capacity and output at the parent firm level,excluding those of “captive plants” held by verticallyintegrated industrial users (e.g., metal or chemical pro-ducers). We started with 738 utility codes with more than1 percent of capacity share in any market-year. Amongthose, 205 were privately held, 125 were public utilities

(either government-owned or cooperatives), and 356were associated with 89 publicly traded companies inCOMPUSTAT and matched to 76 I/B/E/S tickers. For theremaining 52 utility codes, we couldn’t identify owner-ship; we assumed them to be privately held, but theresults were robust to alternative classifications.

4 The NERC region excluded is Alaska, which hadonly one publicly traded electric utility in the market.For the regression analysis we excluded firm-market-years that had less than a 1 percent market share ina year, and we required firm-markets to have at least fiveyearly observations during the sample period. We alsodropped firm-years when fewer than three analysts pro-vided earnings forecasts. Our sample of publicly tradedutilities covered by analysts showed that these firmswere larger and had higher capacity utilization than theother, nonpublicly traded (not-for-profit, state, or pri-vate), utilities (p � .001 for Kolmogorov-Smirnov tests).The analyst-covered firms were also larger and hadhigher capacity utilization than other publicly tradedfirms listed in COMPUSTAT but not covered by analysts(p � .001). These results suggested that ownership typesand analyst coverage were not random. Since we definedour target population as publicly traded utilities withanalyst coverage, we did not interpret these differencesas representing a bias in our sample, but as reflectingdifferences between populations.

2010 751Zhang and Gimeno

trol variables (Zimt), and some unobserved hetero-geneity, as follows:

qimt/Kimt � � � log(Kimt) � � � Ximt � � Zimt

� im � �t � �imt.

The model included fixed effects for firm-marketcombinations (im), since firms’ positions and ca-pacity portfolios across markets are highly hetero-geneous.5 In addition, we included fixed effects foreach year (�t), as longitudinal trends in demand andinput costs (e.g., economic growth, oil prices) caninfluence capacity utilization. The results of aHausman test (p � .01) comparing the model to arandom-effects specification supported use of fixedeffects to model firm-market heterogeneity.

Since the hypotheses involve the evaluation ofinteraction effects between earnings pressure andmarket structure variables, we centered the compo-nents of these interactions around their samplemeans prior to calculating the interactions (Aiken,West, & Reno, 1991). These changes allow the in-terpretation of main effects as the effects of a vari-able at the mean level of the moderator variable. Weestimated models using Stata 10.

Dependent Variable

Capacity utilization. The capacity utilizationrate of a firm in a certain market and year wascalculated as the ratio of its net annual output inthe market (in megawatt hours [MWh]), divided bythe number of hours per year (365 � 24 � 8,760)and the total summer capacity (in megawatts). Netgeneration output equaled gross output minus in-ternal electricity use and pumping energy. Thismeasure represents average capacity utilizationover the year, although output decisions are madecontinuously.

Independent Variables

Earnings pressure. The key independent vari-able was earnings pressure. Because we were inter-ested in its effect on competitive decisions, wemeasured earnings pressure at the beginning ofeach period of activity, before the competitive de-cisions took place. Theoretically, earnings pressurerepresents the gap between the consensus of ana-

lysts’ earnings forecasts and management expecta-tions about potential company earnings understeady management and accounting practices.

Despite the popularity of the term “earnings pres-sure” in the news media, few studies have at-tempted to operationally define this construct. Thislack of a measure is partly a consequence of thedifficulty of developing an independent estimate ofmanagement expectations of potential companyearnings.6 Management public guidance is not fea-sible because of its low frequency and pessimisticbias, as discussed in the theory section. Forecasts ofpotential earnings based on historical time series ofearnings have some predictive power (Lobo & Nair,1991), but they do not take into account new infor-mation available to management that may affect fu-ture earnings. Management expectations are likely tobe shaped by past performance, but also by new in-formation and by the performance of industry peers.

In this study, we adopted a method developed byMatsumoto (2002) to measure “estimated fore-casts,” or the earnings that a firm can realize, ametric now well accepted in the accounting litera-ture (e.g., Burgstahler & Eames, 2006) as a way tocalculate a firm’s potential earnings. Since the cal-culation is technical, we present additional detailsin Appendix B. The method combines informationabout the trends in a firm’s historical performancewith information about recent stock market returns(which convey information about earnings-relevantnews that would not be reflected in historical earn-ings, such as industry changes and social perfor-mance expectations). We calibrated the predic-tive effect of these two performance indicators onpotential earnings using regression parametersfrom a sample of other industry peers, excludingthe focal firm.

5 The use of fixed effects implies modeling longitudi-nal covariation (over years) between levels of indepen-dent and dependent variables for a given firm-marketcombination. The model controlled cross-sectional het-erogeneity in firm-market combinations.

6 Previous research in finance and accounting hadused the gap between earnings forecast consensus andthe premanaged earnings—where premanaged earningswere calculated as the reported earnings minus discre-tionary accruals—to measure the pressure to meet earn-ings forecast consensus (Jones, 1991; Payne & Robb,2000). Although this measure may be appropriate toidentify accounting manipulations to meet earnings con-sensus, it was not appropriate for our application. Ourfocus was to measure earnings pressure at the beginningof a period of activity (i.e., ex ante), but this measurecould only be calculated after earnings were announced(i.e., ex post). Moreover, since exercise of market powerand managing accounting accruals are alternative waysto meet earnings pressure, and these mechanisms takeplace at different points in the period, the Jones measurewould capture earnings pressure that could not be metthrough changes in competitive actions.

752 AugustAcademy of Management Journal

Specifically, the earnings pressure experiencedby firm i during year t was defined as the differencebetween the analysts’ earnings per share (EPS) fore-cast consensus for year t, measured at the beginningof the year, minus the potential EPS (the Matsumo-to’s measure at the beginning of the year), standard-ized by the firm’s stock price at the beginning ofyear t (e.g., Skinner & Sloan, 2002):7

Earnings pressureit

� (analyst forecast consensus

� potential EPS)/share price.

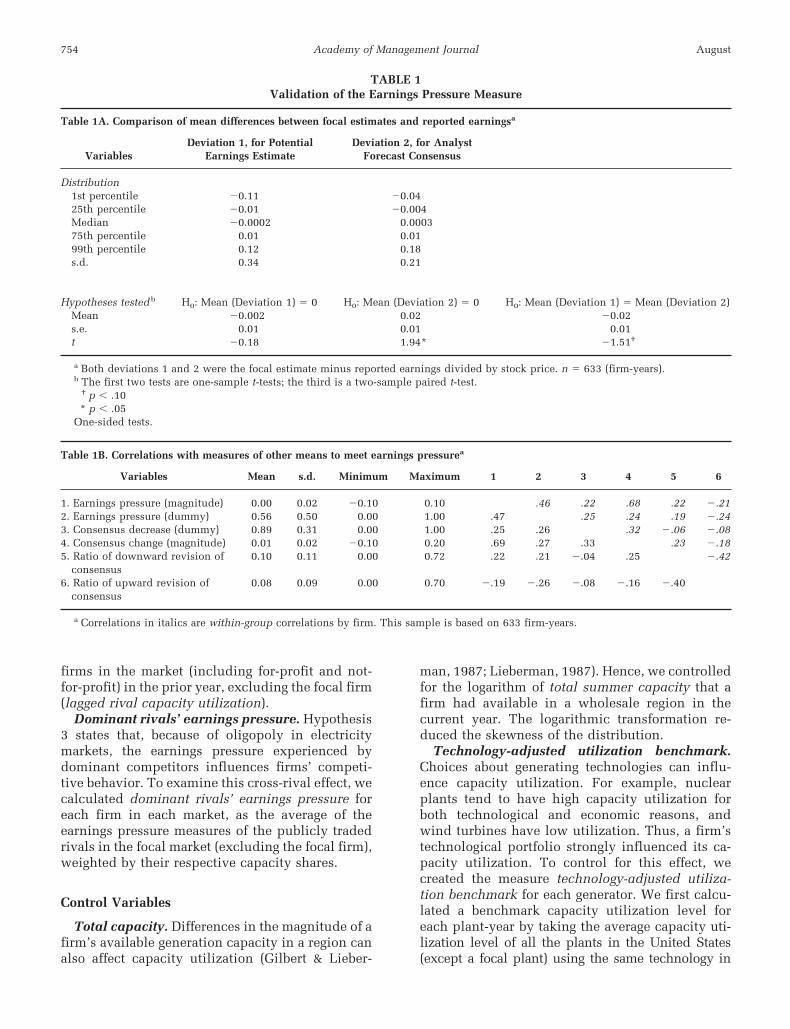

To avoid excessive reliance on a single analyst’sforecast, we selected firms that received forecastsfrom at least three different analysts. However, theresults didn’t change if we included consensus pro-vided by at least one analyst or by at least fiveanalysts. Because this measure was novel, wechecked its validity in two ways. First, we com-pared the accuracy of the potential earnings mea-sure with that of the analyst forecast consensus inpredicting reported earnings for a given year. AsTable 1A shows, the mean difference between theMatsumoto potential earnings estimate and re-ported earnings was significantly smaller than themean difference between analyst forecast consen-sus and reported earnings (paired t-test: p � 0.1).The distribution of analyst forecast consensus atthe beginning of the year was skewed toward over-estimating reported earnings (with a mean differ-ence significantly above 0), as is consistent withprior findings that analysts’ forecasts are optimisti-cally biased. In comparison, the mean differencebetween Matsumoto’s potential earnings estimatesand reported earnings was not significantly differ-ent from 0 (i.e., the measure is unbiased). On theother hand, the difference between analyst forecastconsensus and reported earnings had a lower stan-dard deviation, suggesting that the rich informationused by analysts allowed them to avoid large fore-cast errors. Thus, analyst forecasts are valuable,even if they appear to be biased.

Second, we also tested whether the earningspressure measure at the beginning of a year wasassociated with other means that managers may useto meet earnings pressure during the year. Bern-

hardt and Campello (2007) found that managersfacing earnings pressure tried to “talk down” ana-lysts’ forecasts so that they would be easier to meet.Although we could not find consistent informationabout public earnings guidance (which tends to beinfrequent), we could trace the evolution of ana-lysts’ earnings forecasts during a year for firms withpositive earnings pressure at the beginning of theyear, which can be viewed as partly the result ofmanagers’ talking down analyst forecasts. Results,presented in Table 1B, showed that positive earn-ings pressure was positively correlated with boththe incidence and magnitude of downward revi-sion of analysts’ forecast consensus. At the individ-ual analyst level, positive earnings pressure wasalso positively correlated with the frequency ofdownward revisions of analysts’ forecasts, and neg-atively correlated with the ratio of upward todownward revisions. All these results suggestedthat the Matsumoto’s (2002) method was a promis-ing means for estimating management expectationsof potential earnings based on historical and socialperformance references as well as estimates of fu-ture changes, and it therefore provided an objectivebenchmark to compare with analysts’ forecasts.

Other Independent Variables

Market structure and competitive environmentvariables. To reduce concerns about endogeneityand reverse causality, we calculated the marketstructure variables on the basis of capacity levelsrather than output levels, and lagged rather thancurrent levels. To test Hypothesis 2a, we definedlagged capacity share as a generator’s share, in itsNERC regional market, of summer capacity in aprior year. To test Hypothesis 2b, we created aHerfindahl market concentration index based onthe summer capacity of all other rivals (for-profitand not-for-profit utilities) in the wholesale marketin the prior year (lagged rival Herfindahl), exclud-ing a focal firm. Excluding the focal firm reducedthe collinearity between its dominant share andmarket concentration and was helpful for distin-guishing firm-specific from structural marketpower (Cool, Dierickx, & Jemison, 1989). However,the results using the common Herfindahl index,including the focal firm’s share, were not qualita-tively different. For Hypothesis 2c, we measuredthe market presence of for-profit competitors by thetotal capacity share in the market of all other for-profit firms (publicly traded or privately owned) inthe prior year, excluding the focal firm (lagged for-profit rival share). Finally, to test Hypothesis 2d,we measured competitors’ capacity constraints bythe average capacity utilization level of all other

7 To limit the impact of observations with extremevalues, we capped earnings pressure to be positive ornegative 0.1 if the difference between the analysts’ EPSforecast consensus and the potential EPS estimate wasmore than 10 percent of the stock price. The resultsremained qualitatively the same if we excluded those 14observations from the analyses.

2010 753Zhang and Gimeno

firms in the market (including for-profit and not-for-profit) in the prior year, excluding the focal firm(lagged rival capacity utilization).

Dominant rivals’ earnings pressure. Hypothesis3 states that, because of oligopoly in electricitymarkets, the earnings pressure experienced bydominant competitors influences firms’ competi-tive behavior. To examine this cross-rival effect, wecalculated dominant rivals’ earnings pressure foreach firm in each market, as the average of theearnings pressure measures of the publicly tradedrivals in the focal market (excluding the focal firm),weighted by their respective capacity shares.

Control Variables

Total capacity. Differences in the magnitude of afirm’s available generation capacity in a region canalso affect capacity utilization (Gilbert & Lieber-

man, 1987; Lieberman, 1987). Hence, we controlledfor the logarithm of total summer capacity that afirm had available in a wholesale region in thecurrent year. The logarithmic transformation re-duced the skewness of the distribution.

Technology-adjusted utilization benchmark.Choices about generating technologies can influ-ence capacity utilization. For example, nuclearplants tend to have high capacity utilization forboth technological and economic reasons, andwind turbines have low utilization. Thus, a firm’stechnological portfolio strongly influenced its ca-pacity utilization. To control for this effect, wecreated the measure technology-adjusted utiliza-tion benchmark for each generator. We first calcu-lated a benchmark capacity utilization level foreach plant-year by taking the average capacity uti-lization level of all the plants in the United States(except a focal plant) using the same technology in

TABLE 1Validation of the Earnings Pressure Measure

Table 1A. Comparison of mean differences between focal estimates and reported earningsa

VariablesDeviation 1, for Potential

Earnings EstimateDeviation 2, for Analyst

Forecast Consensus

Distribution1st percentile �0.11 �0.0425th percentile �0.01 �0.004Median �0.0002 0.000375th percentile 0.01 0.0199th percentile 0.12 0.18s.d. 0.34 0.21

Hypotheses tested b H0: Mean (Deviation 1) � 0 H0: Mean (Deviation 2) � 0 H0: Mean (Deviation 1) � Mean (Deviation 2)Mean �0.002 0.02 �0.02s.e. 0.01 0.01 0.01t �0.18 1.94* �1.51†

a Both deviations 1 and 2 were the focal estimate minus reported earnings divided by stock price. n � 633 (firm-years).b The first two tests are one-sample t-tests; the third is a two-sample paired t-test.

† p � .10* p � .05

One-sided tests.

Table 1B. Correlations with measures of other means to meet earnings pressurea

Variables Mean s.d. Minimum Maximum 1 2 3 4 5 6

1. Earnings pressure (magnitude) 0.00 0.02 �0.10 0.10 .46 .22 .68 .22 �.212. Earnings pressure (dummy) 0.56 0.50 0.00 1.00 .47 .25 .24 .19 �.243. Consensus decrease (dummy) 0.89 0.31 0.00 1.00 .25 .26 .32 �.06 �.084. Consensus change (magnitude) 0.01 0.02 �0.10 0.20 .69 .27 .33 .23 �.185. Ratio of downward revision of

consensus0.10 0.11 0.00 0.72 .22 .21 �.04 .25 �.42

6. Ratio of upward revision ofconsensus

0.08 0.09 0.00 0.70 �.19 �.26 �.08 �.16 �.40

a Correlations in italics are within-group correlations by firm. This sample is based on 633 firm-years.

754 AugustAcademy of Management Journal

that year. We then calculated the technology-adjustedutilization benchmark for each firm-market-year asthe capacity-weighted average of benchmark capacityutilization levels for the firm’s plants in that marketand year. This variable is strongly correlated withcapacity utilization, suggesting that the compositionof the portfolio of power plants is a strong but exog-enous determinant of capacity utilization.

We also controlled for factors that have beenfound in previous research to influence capacityutilization (e.g., Lieberman, 1989).

Growth of demand. Demand for electricity isclosely related to the economic activities in a region.We used gross domestic product (GDP) growth rate inthe states composing a focal wholesale region as ourproxy for demand growth. Data on regional GDP wereobtained from the U.S. Bureau of Economic Analysis.

Lumpiness. Lumpiness in capacity has beenshown to affect capacity utilization negatively,since firms cannot easily match capacity increases tosmooth changes in demand (Lieberman, 1989). Fol-lowing Lieberman (1987), we used the inverse of thenumber of generating units that a firm had in a marketin a prior year as our proxy (lagged lumpiness).

Financial constraint and profitability. Finan-cial conditions, such as financial constraints or lowhistorical performance, might also affect competi-tive behavior (Borenstein & Rose, 1995; Busse,2002; Chevalier, 1995a, 1995b; Phillips, 1995). Wecontrolled for a firm’s financial ability to coverinterest payments with the measure lagged interestcoverage, defined as operating income before depre-ciation and amortization divided by the interest ex-pense. To empirically distinguish earnings pressurefrom low historical performance, we controlled forpast performance, measuring it as a company’s returnon total assets in a prior year (lagged ROA).

RESULTS

Descriptive Statistics

The final sample included 814 observations repre-senting 62 electric generators in 11 wholesale markets(NERC regions), 81 firm-market combinations in total,over 13 years from 1993 to 2005. Overall, electricitygeneration accounted for an average 74 percent ofrevenue for the sample firms. The total capacity of thefirms for which earnings pressure could be measuredaccounted for 92 percent of total capacity of the for-profit electric generators (publicly traded or privatelyheld), and 69 percent of the capacity of all the electricgenerators during the period.

Table 2 presents descriptive statistics and corre-lations. The mean capacity utilization in the sam-ple was about 52 percent. Capacity utilization had

a strong correlation with the technology-adjustedutilization benchmark (r � .77), highlighting theimportance of controlling for differences in firms’generation technologies. Capacity utilization wasweakly, negatively correlated to earnings pressure(r � �.05) and weakly, positively correlated todominant rivals’ earnings pressure (r � .06). Earn-ings pressure was also negatively correlated withboth interest coverage (r � �.30) and past perfor-mance (r � �.46), highlighting the importance ofcontrolling for these financial conditions. How-ever, the correlations between earnings pressureand the market structure and competitive environ-ment variables were weak (all below .11), whichfacilitated the independent identification of effectsfor these variables and their interactions.

Regression Analysis Results

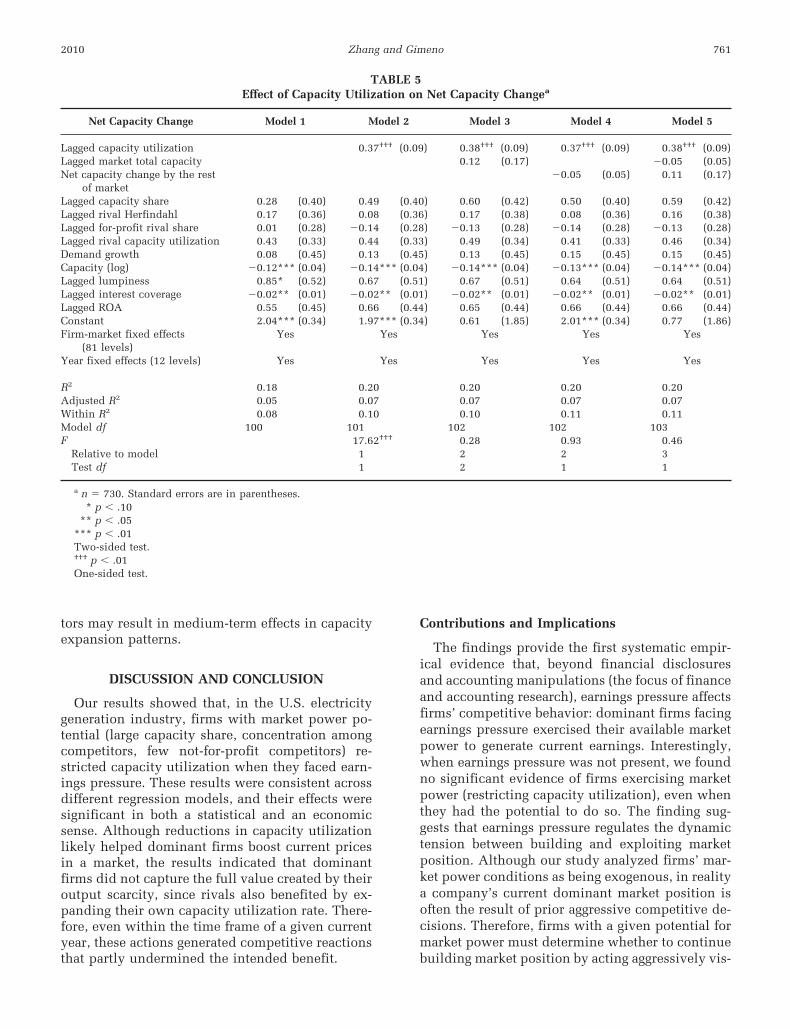

The results for the main hypotheses are pre-sented hierarchically in Table 3. Model 1 reportsthe results of the regression with the control vari-ables only, which showed that the addition of thetechnology-adjusted utilization benchmark had apositive and significant effect on both capacity uti-lization level and the goodness of fit of the model(with R2, adjusted R2, and within R2 increased by.06, .08, and .29, respectively). The inclusion of thiscontrol variable substantially reduced the coeffi-cient magnitude and significance of other controlvariables, suggesting that this was a critical controlvariable. The results were robust to an alternativespecification, wherein the dependent variable wasmeasured as capacity utilization relative to thetechnology-adjusted benchmark.

Main effect of earnings pressure. Hypothesis 1proposes that earnings pressure on a focal firm hasa negative impact on capacity utilization. Model 2in Table 3 does not support this hypothesis: theeffect of earnings pressure at the beginning of a yearon the capacity utilization level during the yearwas not significantly different from zero. However,this finding reflected the average effect among thediverse firm-markets in the sample, many of whichlacked the ability to exercise market power. Weexplored contingent effects next.

Market structure and competitive environmentcontingencies. Hypotheses 2a–2d state that the ef-fect of earnings pressure on capacity utilization ismore negative for firms with more dominant capacityshares in their market, higher market concentration,larger for-profit rivals’ shares, and larger capacityconstraints by competitors. Despite the lack ofsignificance of the main effect of earnings pressure,the results of models 3–5 in Table 3 showed signif-icant, negative coefficients for three of the interac-

2010 755Zhang and Gimeno

TA

BL

E2

Des

crip

tive

Sta

tist

ics

and

Cor

rela

tion

sa

Var

iabl

esM

ean

s.d

.M

inim

um

Max

imu

m1

23

45

67

89

1011

1213

1.C

apac

ity

uti

liza

tion

b0.

520.

160.

080.

98.6

5�

.004

.06

�.2

4.0

5.2

0.1

1.0

4�

.36

.08

.09

.06

2.T

ech

nol

ogy-

adju

sted

uti

liza

tion

ben

chm

ark

0.52

0.14

0.19

0.91

.77

�.0

02.0

4�

.16

.04

.13

.07

.03

�.2

3.0

5.0

6.0

43.

Ear

nin

gsp

ress

ure

0.00

30.

02�

0.10

0.10

�.0

5�

.03

�.0

1.0

4�

.01

�.1

3.0

5�

.07

.06

�.0

2�

.29

�.4

44.

Dom

inan

tri

vals

’ea

rnin

gsp

ress

ure

0.00

20.

01�

0.03

0.04

.06

.04

�.0

5.0

8.1

4�

.08

.17

�.1

5.0

1.0

4.0

2.0

75.

Lag

ged

cap

acit

ysh

are

0.10

0.09

0.01

0.45

.01

.04

�.0

5�

.01

.17

�.4

4.1

6.1

4.6

0�

.22

.12

.09

6.L

agge

dri

val

Her

fin

dah

l0.

100.

060.

030.

34.0

1.0

3�

.04

.10

.01

.40

.00

.28

�.1

2.1

1.2

7.2

37.

Lag

ged

for-

pro

fit

riva

lsh

are

0.68

0.17

0.12

0.95

�.0

5.1

2.0

4.0

7�

.34

.15

�.1

6.1

7�

.43

.16

.17

.21

8.L

agge

dri

val

cap

acit

yu

tili

zati

on0.

510.

050.

400.

62.1

7.3

2.0

2.1

1�

.09

.08

.17

.03

�.0

5.0

2.1

3.0

99.

Dem

and

grow

th0.

030.

02�

0.02

0.09

.06

.01

�.0

8�

.18

.08

.14

�.1

6.0

2�

.05

.08

.26

.12

10.

Tot

alsu

mm

erca

pac

ity

7,10

16,

737

4742

,152

.12

.18

�.0

6�

.05

.71

�.0

9�

.27

.16

.05

�.1

5.0

3�

.03

11.

Lag

ged

lum

pin

ess

0.04

0.06

0.00

1.1

0.0

1�

.02

.06

�.3

1.0

5.0

0�

.13

.00

�.3

3�

.01

.03

12.

Lag

ged

inte

rest

cove

rage

4.10

1.49

�7.

448.

83.1

0.1

5�

.30

.03

.19

.13

.03

.07

.22

.12

�.1

0.6

813

.L

agge

dR

OA

0.03

0.02

�0.

190.

11.0

8.1

2�

.46

.06

.11

.13

.07

.08

.14

.07

�.0

6.7

1

aC

orre

lati

ons

init

alic

sar

ew

ith

in-g

rou

pco

rrel

atio

ns

byfi

rm.

Th

issa

mp

leis

base

don

814

firm

-mar

ket-

year

s.b

Cap

acit

yis

inM

Ws.

TA

BL

E3

Res

ult

sof

Fix

ed-E

ffec

tsR

egre

ssio

nA

nal

ysis

for

Cap

acit

yU

tili

zati

ona

Var

iabl

esM

odel

1M

odel

2M

odel

3M

odel

4M

odel

5M

odel

6M

odel

7M

odel

8M

odel

9

Ear

nin

gsp

ress

ure

�0.

04(0

.15)

�0.

29†

†(0

.17)

�0.

28†

(0.1

7)�

0.04

(0.1

5)�

0.05

(0.1

6)�

0.31

†(0

.19)

0.03

(0.1

6)E

arn

ings

pre

ssu

re�

lagg

edca

pac

ity

shar

e�

7.15

††

†(2

.41)

�4.

62††

(2.4

8)

Ear

nin

gsp

ress

ure

�la

gged

riva

lH

erfi

nd

ahl

�9.

44†

††

(3.2

5)�

7.15

††

(3.3

9)

Ear

nin

gsp

ress

ure

�la

gged

for-

pro

fit

riva

lsh

are

�3.

61†

††

(0.8

9)�

3.25

††

†(0

.92)

Ear

nin

gsp

ress

ure

�la

gged

riva

lca

pac

ity

uti

liza

tion

�0.

45(3

.02)

3.79

(3.1

0)

Dom

inan

tri

vals

’ea

rnin

gsp

ress

ure

0.72

††

(0.4

3)0.

74†

†(0

.44)

Tec

hn

olog

y-ad

just

edu

tili

zati

onbe

nch

mar

k0.

82**

*(0

.04)

0.82

***

(0.0

4)0.

81**

*(0

.04)

0.82

***

(0.0

4)0.

82**

*(0

.04)

0.82

***

(0.0

4)0.

82**

*(0

.04)

0.82

***

(0.0

4)0.

82**

*(0

.04)

Lag

ged

cap

acit

ysh

are

0.06

(0.1

4)0.

06(0

.14)

0.07

(0.1

4)0.

07(0

.14)

0.08

(0.1

4)0.

06(0

.14)

0.08

(0.1

4)0.

03(0

.14)

0.03

(0.1

4)L

agge

dri

val

Her

fin

dah

l0.

19(0

.13)

0.20

(0.1

3)0.

20(0

.13)

0.17

(0.1

3)0.

19(0

.13)

0.20

(0.1

3)0.

18(0

.13)

0.15

(0.1

3)0.

15(0

.14)

Lag

ged

for-

pro

fit

riva

lsh

are

0.36

***

(0.1

0)0.

36**

*(0

.10)

0.36

***

(0.1

0)0.

36**

*(0

.10)

0.38

***

(0.1

0)0.

36**

*(0

.10)

0.37

***

(0.1

0)0.

38**

*(0

.10)

0.38

***

(0.1

0)L

agge

dri

val

cap

acit

yu

tili

zati

on0.

07(0

.12)

0.07

(0.1

2)0.

07(0

.12)

0.02

(0.1

2)0.

07(0

.12)

0.07

(0.1

2)0.

04(0

.12)

0.11

(0.1

2)0.

11(0

.12)

Dem

and

grow

th0.

04(0

.17)

0.04

(0.1

7)0.

05(0

.17)

0.03

(0.1

7)0.

04(0

.17)

0.04

(0.1

7)0.

04(0

.17)

0.06

(0.1

7)0.

06(0

.17)

Tot

alsu

mm

erca

pac

ity

(log

)�

0.02

(0.0

1)�

0.02

(0.0

1)�

0.02

(0.0

1)�

0.02

(0.0

1)�

0.02

(0.0

1)�

0.02

(0.0

1)�

0.02

*(0

.01)

�0.

02(0

.01)

�0.

02(0

.01)

Lag

ged

lum

pin

ess

�0.

01(0

.07)

�0.

01(0

.07)

�0.

01(0

.07)

�0.

02(0

.07)

�0.

004

(0.0

7)�

0.01

(0.0

7)�

0.00

2(0

.07)

�0.

01(0

.07)

�0.

01(0

.07)

Lag

ged

inte

rest

cove

rage

0.00

0(0

.00)

0.00

0(0

.00)

�0.

001