Early Stage Venture Financings: Terms, Negotiations, and Closing

24

© 2015 Morgan, Lewis & Bockius LLP EARLY STAGE VENTURE FINANCINGS: TERMS, NEGOTIATIONS AND CLOSING John Park Eric Foster May 2016

Transcript of Early Stage Venture Financings: Terms, Negotiations, and Closing

© 2015 Morgan, Lewis & Bockius LLP

EARLY STAGEVENTURE FINANCINGS:TERMS, NEGOTIATIONSAND CLOSINGJohn ParkEric Foster

May 2016

OVERVIEW OF EARLY STAGEVENTURE FINANCINGS

Early Stage Investors

• Angels and smaller funds / family offices

• Venture capital investment professionals activelymanaging institutional investor money– Board seats and control issues are standard– Funds often focus by industry sector (e.g., communications,

software, biotech, etc.)– And by stage of development (e.g., start-up, mid-stage, late-

stage, cross-over)

• Friends and Family

• Accelerators / Incubators (Y-Combinator, 500 Start-Ups,Gateway, QB3)

• Crowdfunding

3

Investment Instruments

• Convertible Note

• Series A Preferred Stock

• Series Seed Preferred Stock

• SAFE

• KISS

• But it’s more than that . . .– Active, strategic business advisors

– Perspective born of experience

– Network of relationships– Key employees

– Customer connections

– Service providers

– External validation

4

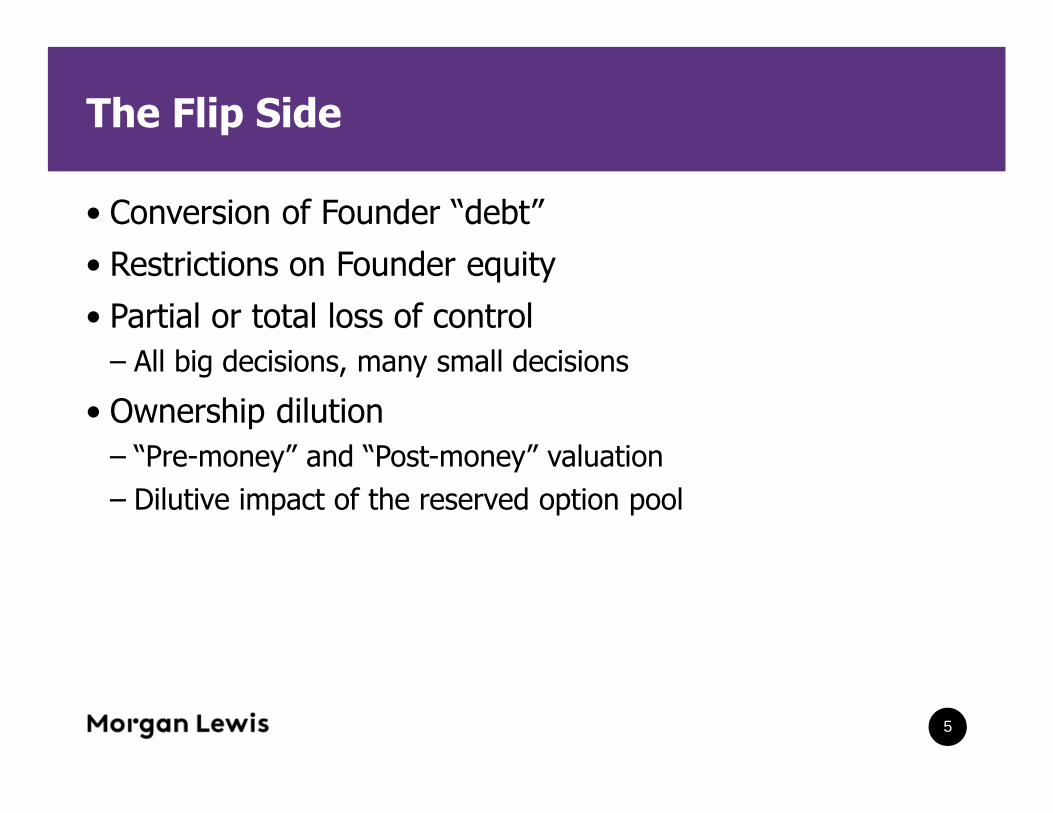

The Flip Side

• Conversion of Founder “debt”

• Restrictions on Founder equity

• Partial or total loss of control

– All big decisions, many small decisions

• Ownership dilution

– “Pre-money” and “Post-money” valuation

– Dilutive impact of the reserved option pool

5

DOCUMENTATION &PROCESS

The Primary Deal Documents

• Term Sheet

• Stock Purchase Agreement

• Charter

• Investors’ Rights Agreement

• Voting Agreement

• RoRF & Co-Sale Agreement

7

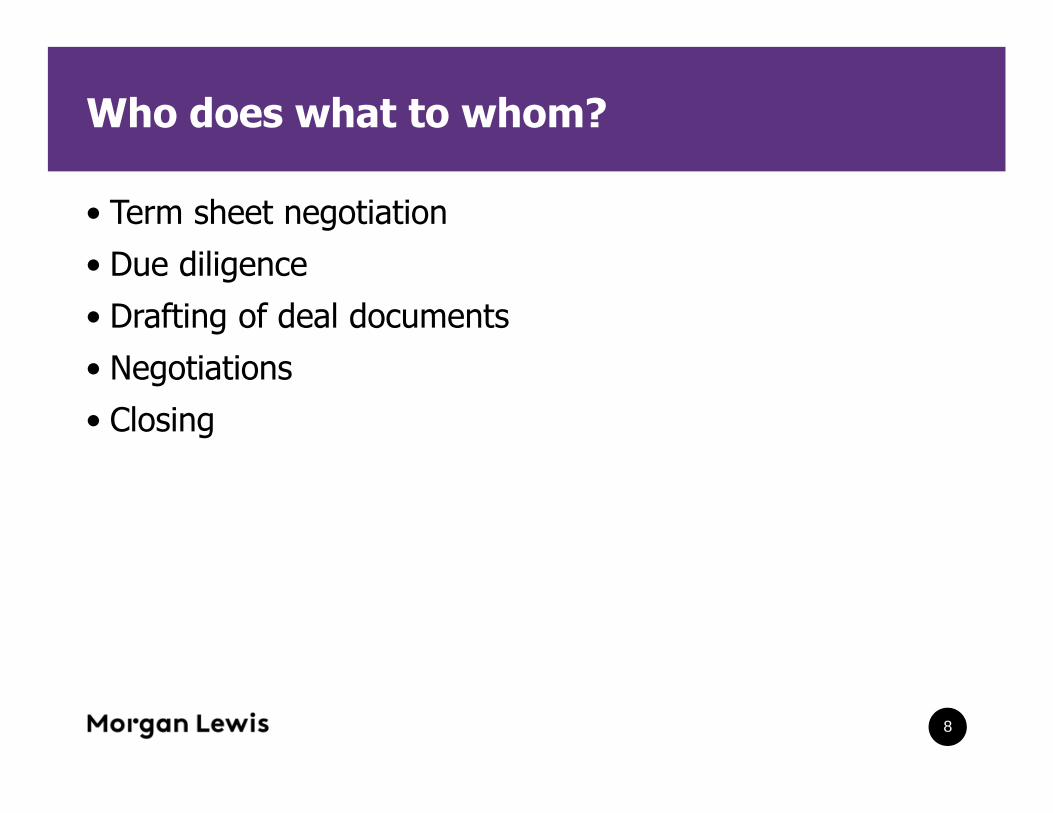

Who does what to whom?

• Term sheet negotiation

• Due diligence

• Drafting of deal documents

• Negotiations

• Closing

8

KEY DEAL TERMS

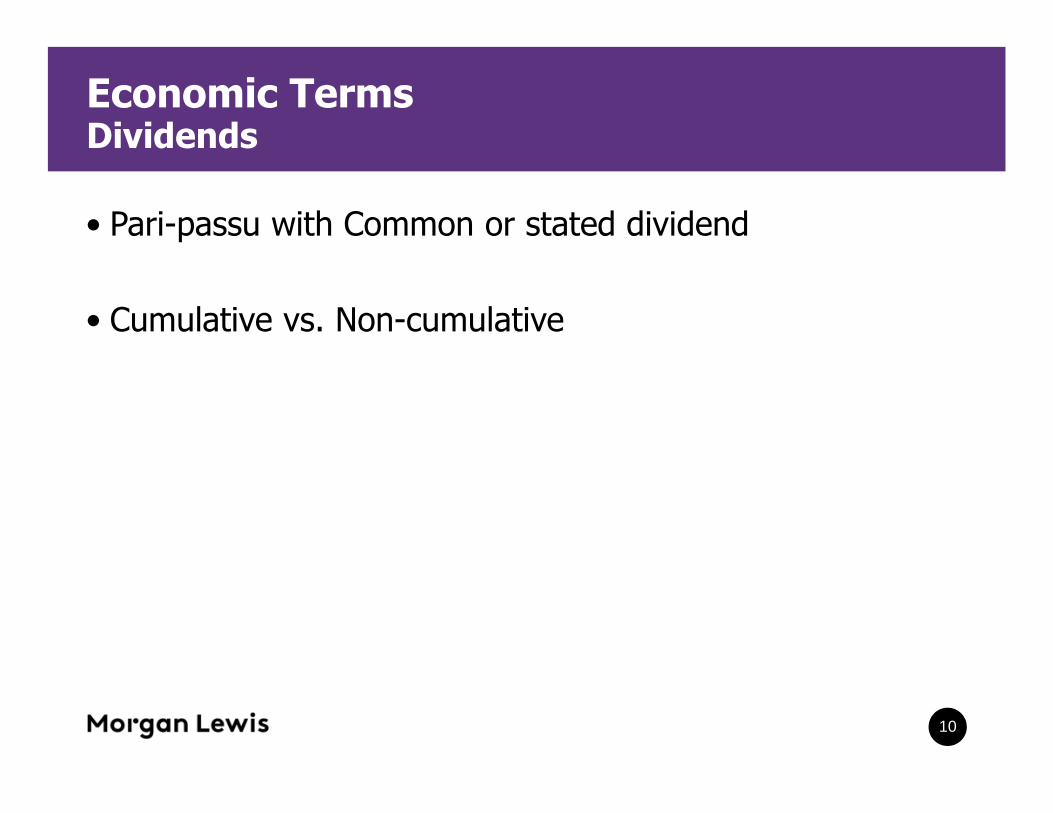

Economic TermsDividends

• Pari-passu with Common or stated dividend

• Cumulative vs. Non-cumulative

10

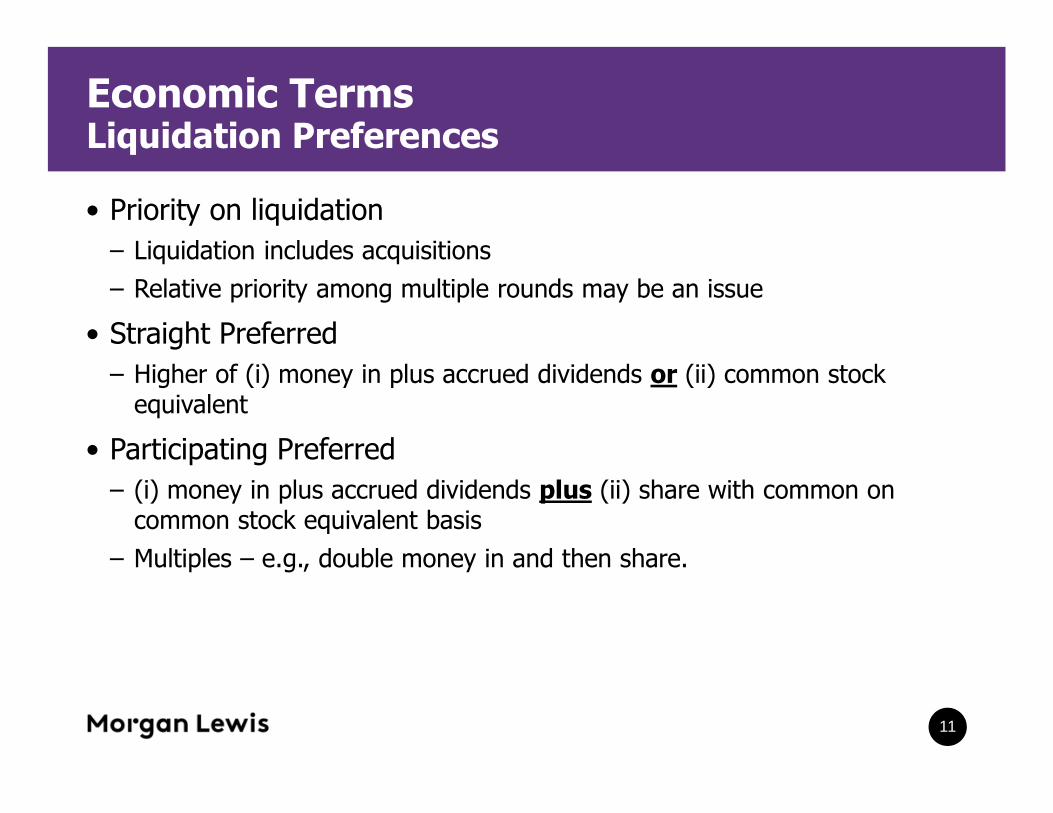

Economic TermsLiquidation Preferences

• Priority on liquidation

– Liquidation includes acquisitions

– Relative priority among multiple rounds may be an issue

• Straight Preferred

– Higher of (i) money in plus accrued dividends or (ii) common stockequivalent

• Participating Preferred

– (i) money in plus accrued dividends plus (ii) share with common oncommon stock equivalent basis

– Multiples – e.g., double money in and then share.

11

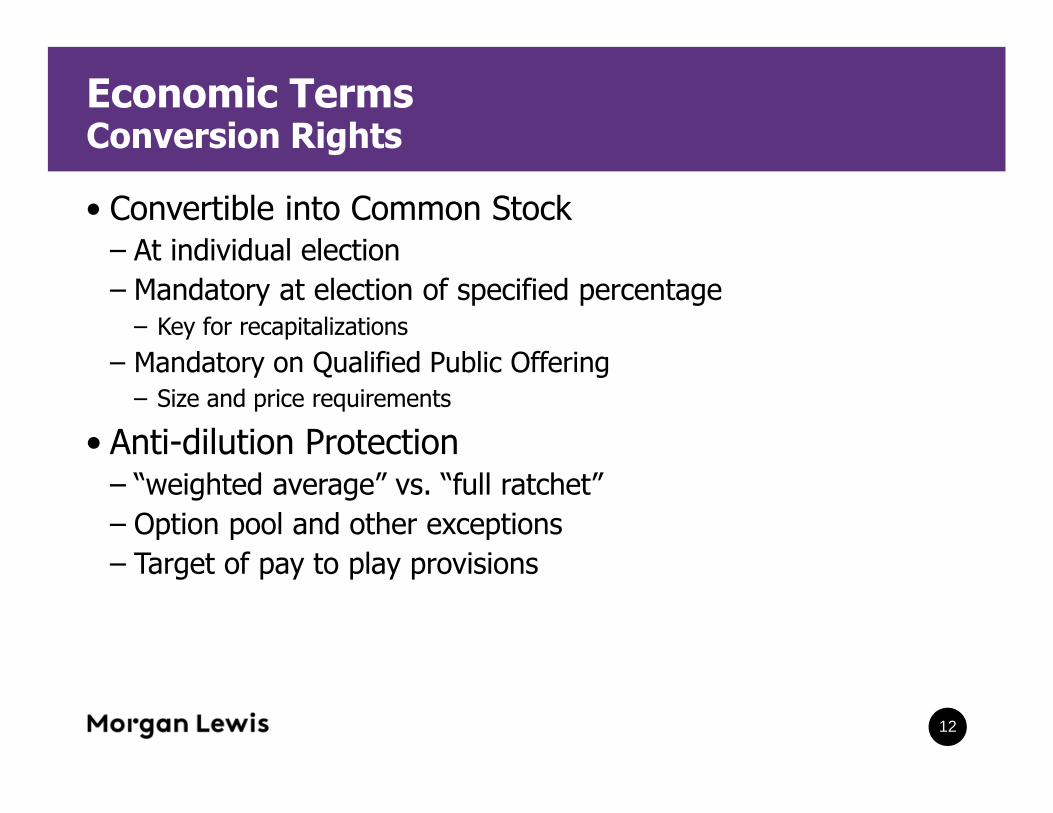

Economic TermsConversion Rights

• Convertible into Common Stock– At individual election

– Mandatory at election of specified percentage– Key for recapitalizations

– Mandatory on Qualified Public Offering– Size and price requirements

• Anti-dilution Protection– “weighted average” vs. “full ratchet”

– Option pool and other exceptions

– Target of pay to play provisions

12

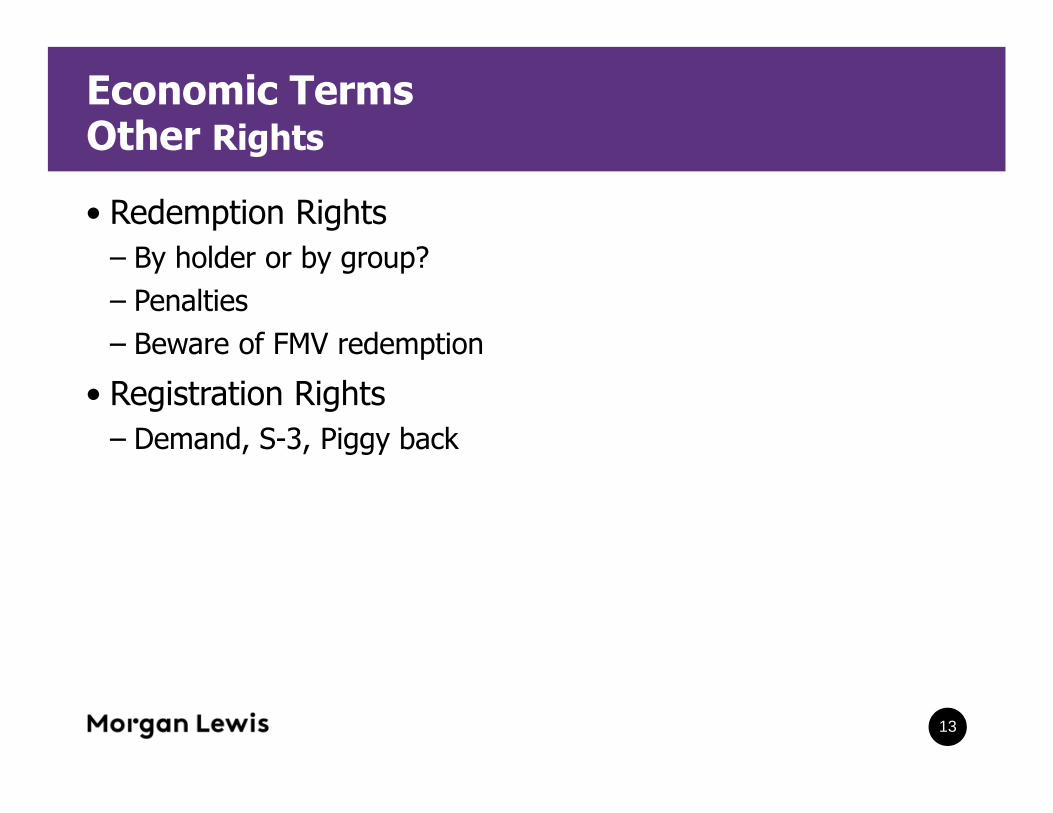

Economic TermsOther Rights

• Redemption Rights

– By holder or by group?

– Penalties

– Beware of FMV redemption

• Registration Rights

– Demand, S-3, Piggy back

13

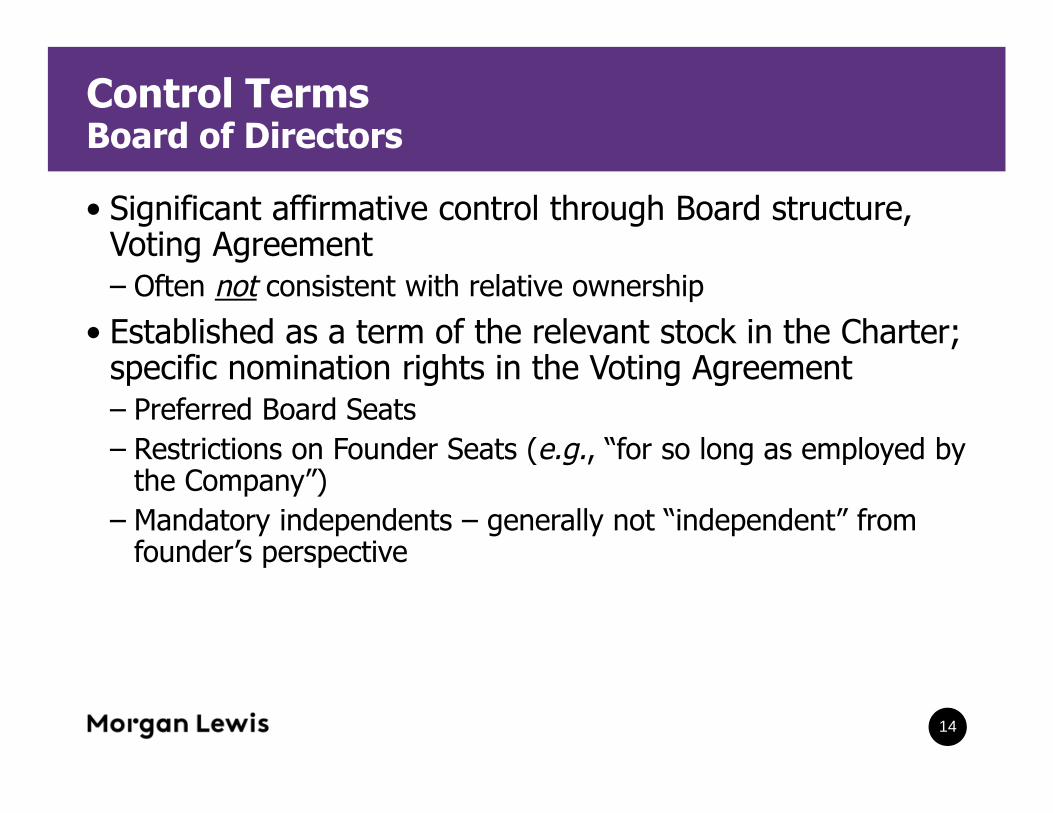

Control TermsBoard of Directors

• Significant affirmative control through Board structure,Voting Agreement– Often not consistent with relative ownership

• Established as a term of the relevant stock in the Charter;specific nomination rights in the Voting Agreement– Preferred Board Seats

– Restrictions on Founder Seats (e.g., “for so long as employed bythe Company”)

– Mandatory independents – generally not “independent” fromfounder’s perspective

14

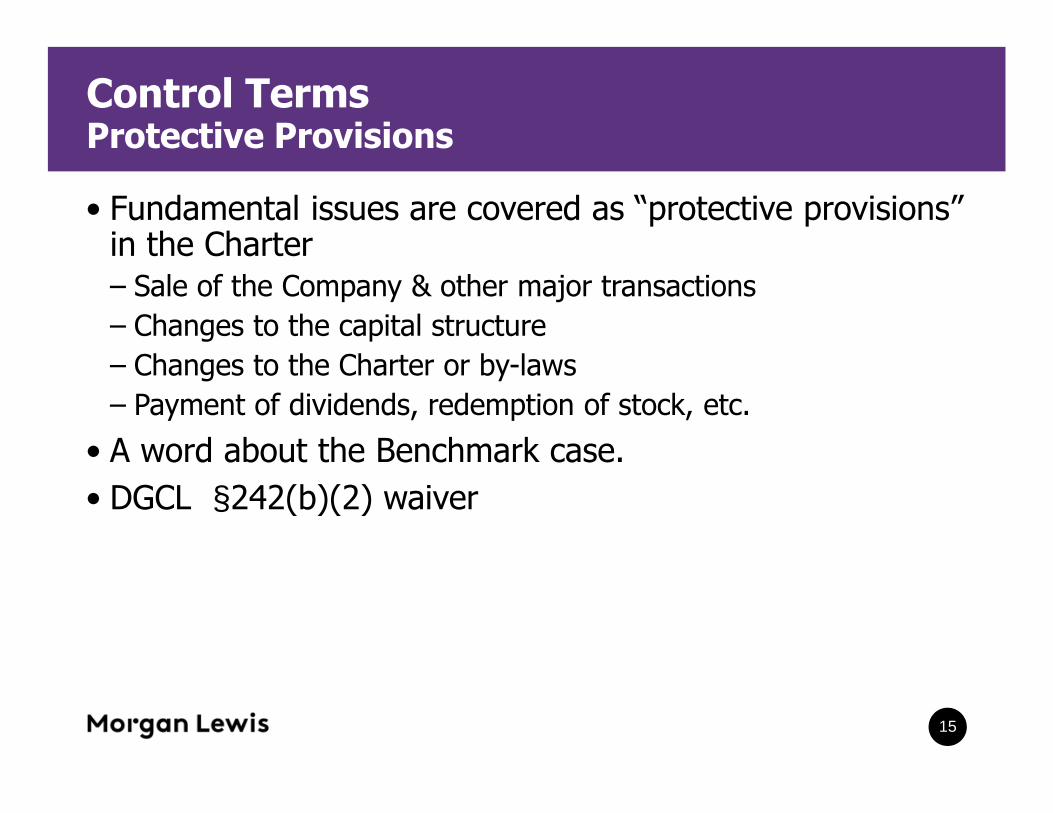

Control TermsProtective Provisions

• Fundamental issues are covered as “protective provisions”in the Charter– Sale of the Company & other major transactions

– Changes to the capital structure

– Changes to the Charter or by-laws

– Payment of dividends, redemption of stock, etc.

• A word about the Benchmark case.

• DGCL §242(b)(2) waiver

15

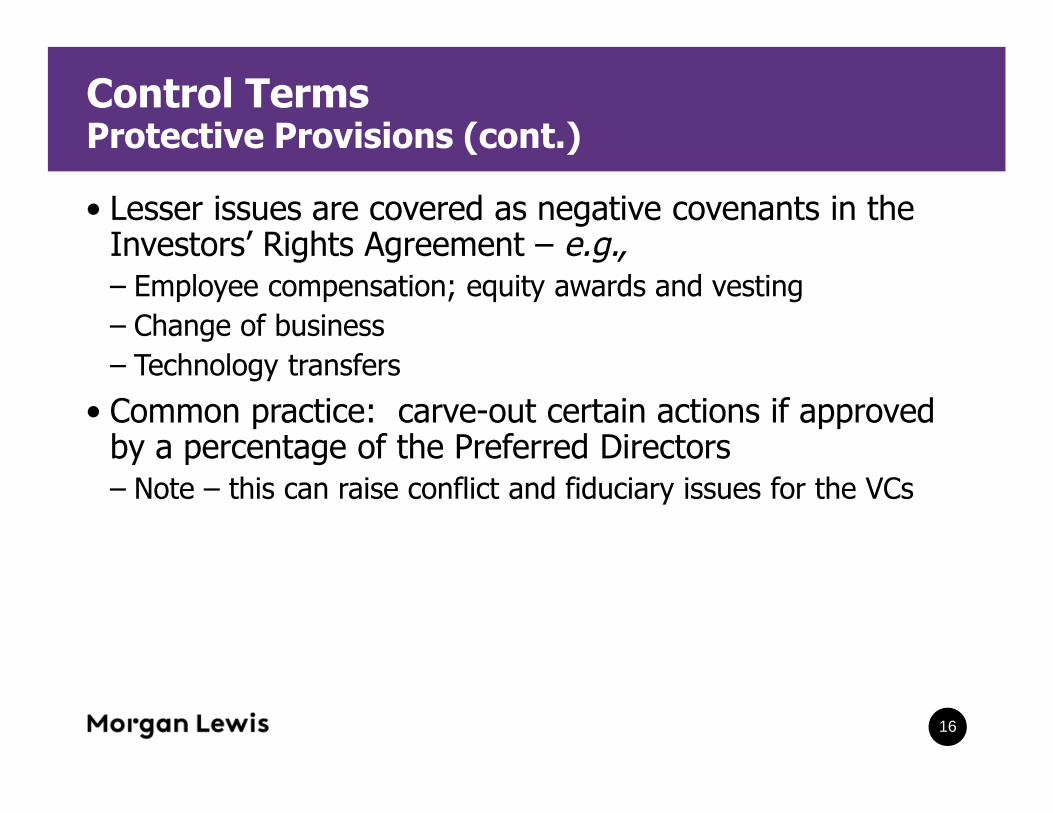

Control TermsProtective Provisions (cont.)

• Lesser issues are covered as negative covenants in theInvestors’ Rights Agreement – e.g.,– Employee compensation; equity awards and vesting

– Change of business

– Technology transfers

• Common practice: carve-out certain actions if approvedby a percentage of the Preferred Directors– Note – this can raise conflict and fiduciary issues for the VCs

16

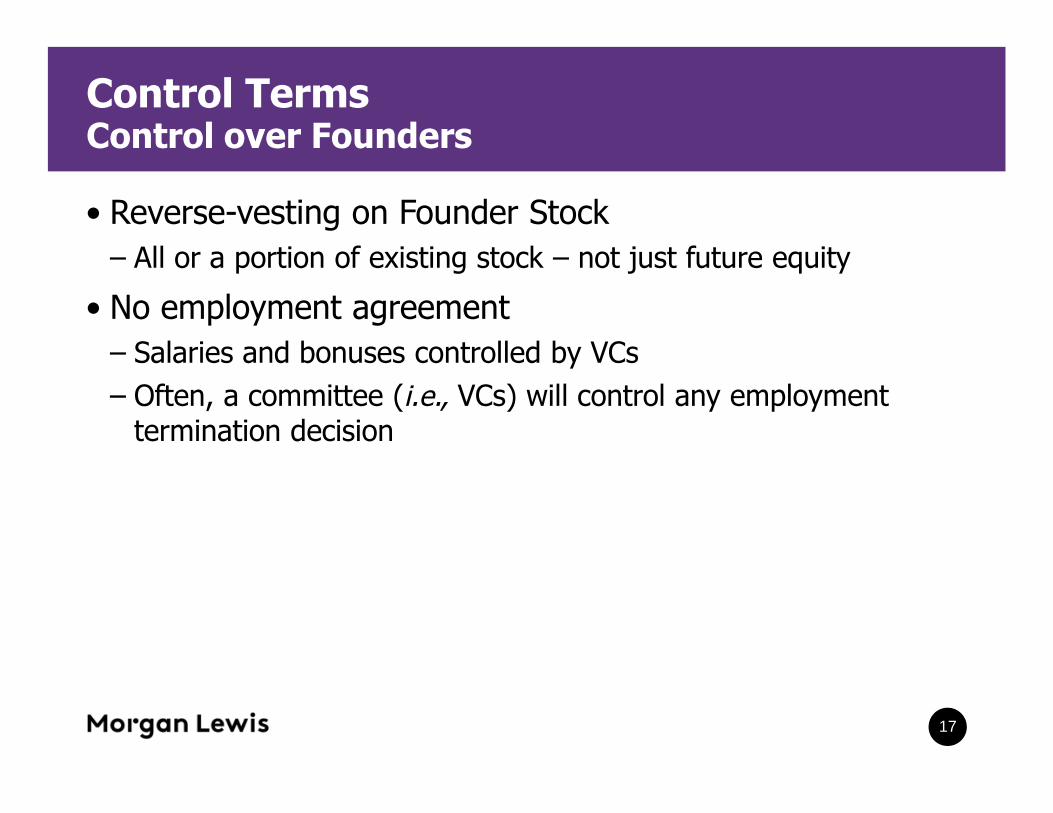

Control TermsControl over Founders

• Reverse-vesting on Founder Stock

– All or a portion of existing stock – not just future equity

• No employment agreement

– Salaries and bonuses controlled by VCs

– Often, a committee (i.e., VCs) will control any employmenttermination decision

17

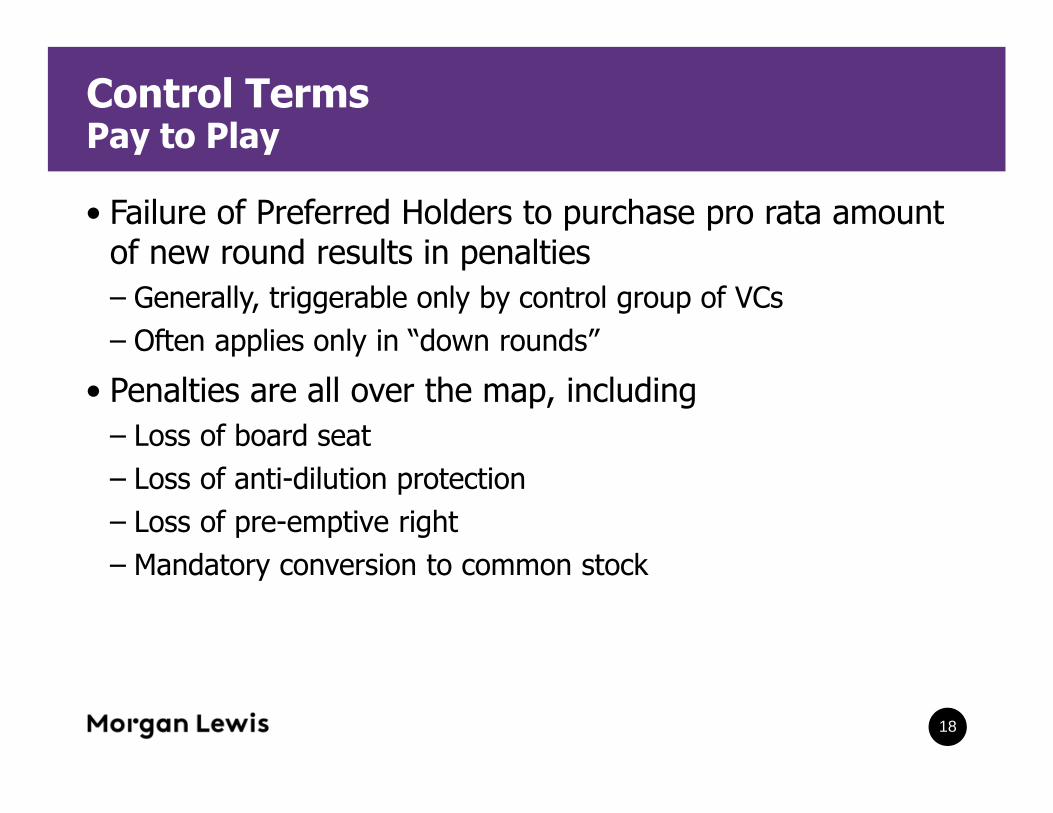

Control TermsPay to Play

• Failure of Preferred Holders to purchase pro rata amountof new round results in penalties

– Generally, triggerable only by control group of VCs

– Often applies only in “down rounds”

• Penalties are all over the map, including

– Loss of board seat

– Loss of anti-dilution protection

– Loss of pre-emptive right

– Mandatory conversion to common stock

18

Control TermsControl over Equity

• Preemptive Rights

– Maintain percentage . . . or more

– May not apply to all investors

• Stock transfer restrictions

– Right of First Refusal & Co-Sale Rights

– Typically this only restricts non-VC shares (i.e., Founders andKey holders)

• Drag Along rights

– Details vary widely

19

Other Issues

• Down rounds and recaps

• Milestone Investing

• Management Incentives & Carve-out Plans

20

Biography

E. John ParkSilicon Valley

T +1.650.843.7595

E. John Park focuses his practice on debt and equity offerings, publicsecurities offerings, recapitalizations, and mergers and acquisitions (M&A).He assists clients at every stage of the business cycle, from initial companyformation, venture capital financings, and M&A, to initial public offerings(IPOs), public company reporting, and general corporate counseling. Inaddition, John represents acquirers and targets in public-private and private-private business combination transactions.

John helps venture capital and corporate venture capital clients structureand implement early and late stage investments. He also represents privateand public companies providing general corporate and strategic advice onfinancings, partnerships, joint ventures and M&A transactions, as well asinbound, outbound, and cross-border transactions. In many of thesetransactions, he draws upon his experience in intellectual propertyprotection, technology licensing, environmental law, corporate governance,executive compensation, labor and employment, and international tax law.

21

Biography

Eric Q. Foster

Silicon Valley

T +1.650.843.7296

With an emphasis on investing in emerging companies, Eric Q. Fosteradvises clients on venture capital financing, private equity transactions,mergers and acquisitions, and securities. Eric also guides clientsthrough general corporate and securities matters. Before attending lawschool, he worked as a corporate paralegal at a large Silicon Valley–based law firm.

While attending Santa Clara School of Law, Eric was an editor on theSanta Clara Computer and High Technology Law Journal, a participantin multiple moot court competitions, and the recipient of multipleawards and honors.

22

ASIA

Almaty

Astana

Beijing

Singapore

Tokyo

EUROPE

Brussels

Frankfurt

London

Moscow

Paris

MIDDLE EAST

Dubai

NORTH AMERICA

Boston

Chicago

Dallas

Harrisburg

Hartford

Houston

Los Angeles

Miami

New York

Orange County

Philadelphia

Pittsburgh

Princeton

San Francisco

Santa Monica

Silicon Valley

Washington, DC

Wilmington

23

This material is provided as a general informational service to clients and friends of Morgan, Lewis & Bockius LLP. It does not constitute, and should not beconstrued as, legal advice on any specific matter, nor does it create an attorney-client relationship. You should not act or refrain from acting on the basis of thisinformation. This material may be considered Attorney Advertising in some states. Any prior results discussed in the material do not guarantee similar outcomes.Links provided from outside sources are subject to expiration or change.

© 2015 Morgan, Lewis & Bockius LLP. All Rights Reserved.

24