e-track - Punjab National Bank Institute of Information...

32

vol. V no. 2 quarterly journal april-june-2009 e-track business of future e-track e-CRM

Transcript of e-track - Punjab National Bank Institute of Information...

vol. V no. 2 quarterly journal april-june-2009

e-trackbusiness of futuree-track

e-CRM

e-track

April-June-2009

Editor

Pratima Trivedi

Editorial Team

Pramod Dikshit

Ambrish Mishra

Swapnil Srivastava

Sanjay Srivastava

Printed by

Swastik Printing Press

27, Mai Gi Ki Bagiya,

Kapoorthala Crossing,

Mahanagar, Lucknow

Mobile : 9415419300

punjab national bank institute of

information technology

Vibhuti Khand, Gomti Nagar,

Lucknow--226 010 (U.P.)

T : +91 522 2721442, 2721174

F : +91 522 2721201, 2721441

E-mail : [email protected]

URL : www.pnbiit.com

e-track

“Anyone who stops learning is old,

whether at twenty or eighty."

- Henry Ford

Thought for the quarter

From the editor

Dear Readers, As the internet is becoming more and more important in business life, many companies consider it as an opportunity to reduce customer-service costs, tighten customer relationships and most important, further personalize marketing messages and enable mass customization. Together with the creation of Sales Force Automation (SFA), where electronic methods were used to gather data and analyze customer information, the trend of the upcoming Internet can be seen as the foundation of what we know as e CRM today. E CRM comprises of activities which are required to manage customer relationships by using the Internet, web browsers or other electronic touch points. The challenge hereby is to offer communication and information on the right topic, in the right amount, and at the right time that fits the customer's specific needs. Since the company's performance depends upon the satisfaction of its customers which can be achieved through e CRM. Article on “e CRM” has been included in this issue to elaborate various intricacies attached to it. The Global Economy faced its biggest shock which was of such magnitude that many say that it is as worse as that of 1929 shock. Article “Slowdown in global economy and its effects on Indian banks” has been included in this issue to elaborate its impact on Indian Banks.One of the important indicators of financial health of a Bank is the proportion of NPAs in its books. Poor credit quality exposes the banks to vulnerability of further distress in its portfolio and adverse effect on profitability that leads to a vicious cycle. Though RBI has permitted sale of distressed loans to other banks and ARCs activities on the loan sales front are very tardy. The article on “Electronic Trading of Distressed Bank Loans” covers in detail various issues relating to it.Enterprise resource planning is a business tool, which seamlessly integrates the strategic initiatives and policies of the organization with the operations, thus providing an effective means of translating strategic business goals to real time planning and control. It is planned to facilitate information sharing, business planning and decision making on a broad business basis. Today various softwares are available in the market for SME segment depending on the size of the organization .Article “E.R.P trend towards SMEs” elaborates the topic.

Hope you find this issue of e track informative and interesting..

Happy Reading…………

Pratima Trivedie-mail : [email protected]

ContentsFrom Director's Desk Ajay Misra 3

E-CRM Sweety Dube 4

Slowdown in Global Economy and its Effect on Indian Banks Goutam Kumar Mukherji 10

Electronic Trading of Distressed Bank Loans M Ravindran 16

E.R.P TREND TOWARDS SMEs Research Scholar.......... Anchal Singh 22

Financial and Technical News 29

2

e-track

April-June-2009

It gives me immense pleasure to write this column once again, especially after completing 3 years of my taking the reign of the Institute. These years have been a great journey with this Institute in its evolution from a mere training establishment to an eminent organization ready to take a big leap towards educational activities. When I look back in retrospection I have a feeling of satisfaction in the sense that the Institute has slowly but steadily moved towards accomplishing its Mission. Training had remained the bread and butter for the Institute and there has been gradual broad basing in this dimension. With more than 15 Banking Organizations having used infrastructural and training resources of the institute the vision of the Institute to supplement training and infrastructure resources to the BFI sector stands justified. .The industry today looks at the Institute as a premier state of art organization in the information technology.

Banking and Financial sector has undergone a sea change during the last few years. It has witnessed deregulation, liberalization and migration from legacy system to Core Banking. The processes are getting increasingly IT oriented, handling very large volume of sensitive financial transactions online and managing critical financial data. The legacy workforce of the bank being less suitable for optimizing the technology all banks require fresh technical manpower. Most of the banks are on recruitment spree searching for techno bankers suitable to perform smooth and efficient banking operations using technology.

Taking a strong note of this requirement, PNBIIT had launched Advanced Diploma in Banking Technology (ADBT), which aims at creating a pool of responsible techno-bankers for banking and IT sector. This programme is unique blend of IT and its usage in the modern banking operations. It is designed to impart in depth knowledge and expertise to the students through innovative learning, supported by relevant high end technology.ADBT is aimed at creating professionals, who should be employable from the day one.

The launch of ADBT has been a march towards attaining the deemed university status for the institute as per the mission statement. The success of ADBT was an encouragement to explore more possibilities for educational endeavors. The immediate future course of action for the institute, should therefore be, brand imaging of ADBT and holding two programmes in a year thereafter graduating to long duration diploma/degree course in management and information technology for the students by the year 2010.In this context, I am thankful to Union bank of India for

considering ADBT of PNBIIT as an eligibility criteria for selection of Manager(Information Technology) in MMG-II. I am also thankful to Punjab National Bank, Dena Bank, United

bank of India, Hewlett Packard India and Nurture Technology for showing their interest in conducting campus recruitment at the Institute.

Another important area where the institute should make a foray with a rapid fire speed should be to broaden its organic linkage with the organization of national repute for the proposed sharing of resources and knowledge. This should be done by subsequent conduct of awareness seminar for the top executives of the BFSI, on the upcoming contemporary challenges in the area of IT.

Some of these areas could be Customer Relationship Management (CRM), Entreprise Wide Data Warehouse (EDW), Transaction Processing and Use of IT in financial inclusion.

The ultimate aim is to attain self sustenance both operationally and financially. At the moment when I relinquish the charge of this institute and pass on the baton to the new establishment, my message to the institute is very clear. The coming few years are crucial for consolidation of what has been achieved and focused efforts are needed to put on wheel the thoughts and actions emerged out of Governing Body and Academic Council of the Institute to accomplish its Mission. I congratulate the team of PNBIIT for all achievements and thank all learned members of Governing Body and Academic Council of PNBIIT and all eminent personalities of different premier organizations who associated with the institute and contributed for its development.

Ajay MisraDirector PNBIIT

Email – [email protected]

From Director's Desk

3

e-track

April-June-2009

e-CRM

Abstract:

CRM: A Changing Perspective

Conservative CRM Perspective

e-CRM is the latest buzzword in

the corporate sector and is CRM is THE business buzzword on the perceived as one of the most Internet these days. Customer Relationship effective tools in this direction for Management promises faster customer service at service companies. e-CRM lower costs, higher customer satisfaction and from provides a means to conduct this, better customer retention and ultimately interactive, personalized and customer loyalty. eCRM provides a more interactive relevant communication with customers across and personalized way of communicating with electronic channels. e-CRM is nothing but the customers. The advancement in the information and electronic counter part of CRM. It doesn't replace the communication technology has made the new traditional channels of communication, such as millennium “e-millennium”. Now, service phone or fax, but is just another extension for the organisations' activities are not confined to one customers to interact with companies on a one-to-single activity, but they provide a plethora of one basis. It's a more personalized and interactive services keeping in mind the requirement and form of communication and synchronizes convenience of customers. In the fast changing communications across both electronic as well as marketing environment worldwide, service traditional channels. Such a system has training companies in India not only need to learn the rules benefits too. A new salesperson, for instance, can use but also upgrade the skills as well as the tools of the CRM package to quickly learn about his modern marketing.customers or their past history.

Technology, people and customers are the A typical CRM application integrates and co-three elements on which the success of service

ordinates multiple business functions such as sales, companies hinges in the e-millenium. Technology marketing, support/service, and the multiple has been an enabler in managing the pace and channels of communication with the customer, such quantum of changes. Skilled human resource as, face-to-face, call center, and Web. Thus the key management has brought about success in requirements for a CRM solution includes: technology, which is fundamental in generating Analytical capabilities, unified channel of customer these capabilities. However, ultimately the service interaction, Web-based functionality, centralized company's performance depends upon the database of customer data, integrated workflow, and satisfaction of its customers. integration with ERP applications.

e-CRM provides Business Solutions by

integrating Process, Vision and Technology.

= Customer Contact through

·Telephone

·in person

=Personal Selling

-Sweety Dube

Expenses

Sales

Improve Sales

Reduce

Expenses

4

e-track

April-June-2009

= Direct benefits of an e-CRM system include:

= Service level improvements –

=

=Revenue growth –

Productivity – Internet-based CRM Perspective

=Customer satisfaction –

=

=

=

=

=

=

What is the Customer Life Cycle?

Finding the Customer

Emphasis on after sales service

Complaint handling Using an integrated

database to deliver consistent and improved Responsive Customer Servicecustomer responses.

Finally satisfied customer Decreasing costs by focusing on

retaining customers and using interactive service

tools to sell additional products.

Consistent sales and service

procedures to create efficient work processes.Customer database management

Automatic customer Effective data mining

tracking and detection will ensure enquiries are met Leveraging technology and issues are managed. This will improve the

Electronic point of sale customer's overall experience in dealing with the

organisation.Call centres

Service customization

Volume be serviced by technology and value

be given personalized service

It takes ten times more effort and costs ten

times more money to attract a new customer than to

keep an existing customer. This “statistic” alone

should be enough for companies to invest in CRM.

Finding customers is the first step and the faster you

get through the sorting process of qualifying

prospects into customers, the faster will be the

returns. A web environment adds to this process in a

very positive way. You can provide the means for

people visiting your site to select whether they are CRM is a comprehensive sales and marketing indeed right to be customers. Good design and clear approach to build long-term customer relationships information will aid in this goal.and improve business performance. The above

elaboration states about the transition which

Customer Relationship Management is undergoing The process starts with finding customers. The and how technology has affected the modern Internet allows you to attract customers in two ways: relationship with the customers. (1) getting them to find you through search engines,

CRM and the Customer Life Cycle

5

e-track

April-June-2009

links, and alliances with other sites; and (2), by organisations also have multiple lines of business

proactively finding them and sending material that interact with the same customers.

electronically.

Now that you have found your customer, it is

important to find ways to add value to the

relationship. Keep in mind that value is in the mind

of the customer. Find out what they perceive to be

valuable by surveying them either online, by phone,

or by regular mail.

e-CRM systems enable customers to do

business with the organisation the way the customer As you gain more experience with online wants - any time, via any channel, in any language or services you might use more sophisticated ways to currency—and to make customers feel that they are build customer loyalty and strong relationships. dealing with a single, unified organisation that Building customized or personalized sites for your recognises them every step of the way.customers to use will provide both added services

and give customers a reason to return regularly to

your e-business.

The e-CRM system does this by creating a It is easy to get customers to visit your website central repository for customer records and for the first time. It is much more difficult to get them providing a portal on each employee's computer to return. You must create value for the return visitor. system allowing access to customer information by Ensuring you have good content can do this. Content any member of the organisation at any time. Through can be unique articles about the industry or simply this system, e-CRM gives you the ability to know links to other sources of information. Content can more about customers, products and performance also be tools that a visitor may find useful. Many real results using real time information across your estate sites have mortgage calculators or home business.buying checklists that aid customers in using the

service.

In today's world, customers interact with an

organisation via multiple communication

channels—the World Wide Web, call centres, field

salespeople, dealers and partner networks. Many

Building Value for the Customer

Establishing Long-Term Relationships

A hotel may know, immediately after

registering the customer, what he prefers in the

morning-tea or coffee.E-Loyalty

How does e-CRM work? Communicating the customer about flight

through SMS is always the least

expensive.

6

e-track

April-June-2009

Customer Focus in Banking Services

CRM in Punjab National Bank

*

*

*

*

customers. Today customers are offered ATM

services, access to internet banking and phone As the intense competition becomes a way of banking facilities and credit cards. These have doing business, it is the customer who calls the shot elevated banking beyond the barriers of time and in deciding the nature of products and services space.offered in the market. The customers are becoming

demanding, dominant and selective. In fact the

perceptions and the expectations of the customers PNB is implementing CRM to reach have undergone a sea change, with the availability of customers and to create banking services to the customers at their door steps a robust marketing and through the help of technology. sales structure in the

Marketing of customer services aims at two o rg a n i z a t i o n . T h e

important goals: prosperity to the bank and satisfied objective is to have a

customers. Banks offer tangible services like loan well-defined methodology for sales, marketing and

schemes, interest rates and kinds of account and the pre-sales activities. CRM implementation has been

intangible services like behavior and efficiency of positioned as 'Customer First'. As the name signifies,

staff, speed of transactions and the ambience. The the initiative is mainly to highlight the importance of

banks may need to include customer oriented the customer to the bank and in turn generate a sense

approach or customer focus in their five areas of of recognition and loyalty into the customers as well

businesses such as Cash accessibility, asset security, as prospects.

money transfer, deferred payment and financial

advices.

There are four strategies available to customer

relations' managers:

To win back or save customers

To attract new and potential customers

To create loyalty among existing customers

and

To up sell or offer cross services.

The future of banking business very much

depends upon the ability of the banks to develop

close relationship with the customers. In order to

develop close relationship with the customers the

banking industry has to focus on the technology

oriented innovations that offer convenience to the

Functions In CRM:

Business partner Management:

Contact Management:

Activity Management:

The following activities can be

performed with the help of CRM:

Capturing

customers' basic information with the aim to sell

different products of the bank.

Maintaining customer

information and contact histories of existing

customers.

Providing calendar and

scheduling of activities of individual sales people.

Lead Management: Capturing potential leads from

new/existing customers and converting leads into

actual business. Campaign Management: Targeting

customer with promotions/offers based on customer

segmentation/data analysis and also analyzing the

effectiveness of the campaign.

7

e-track

April-June-2009

Glolbalised Scenario

Innovation

Competition from Foreign Banks and New

Private Sector Banks

Technological Advancement

SMS Banking

vistas and in turn has brought new possibilities for

doing the same work differently and in a most cost-"Change" is a continuous process and banking effective manner. Technology helps to have 24 hours industry is no exception to this natural law. Change a day banking, all seven days in a week. Tele in the Indian banking industry is inevitable due to the banking, Internet banking and E-banking have implementation of the financial sector reforms and opened new business potentials and opportunities policies in the country. The main objective of which hither to remained unexplored. All these financial sector reforms is to promote an efficient, technological advancement may pave the way for competitive and diversified financial system in the home banking rather than branch banking.country. Indian banking industry has undergone

tremendous transformation after liberalization and

globalisation process initiated from 1991. These Another important force of change in the changes have forced the Indian banking industry to Indian banking sector is innovation. Banks are adjust the product mix to effect the rapid changes in innovative, pro-active now-a-days and offer top their process to remain competitive in the globalised class service to customers. They play a dynamic role environment. not only as a provider of finance but also as a

departmental store of finance. As a result of this, new

products like merchant banking, mutual funds,

leasing, factoring, forfeiting, corporate advisory The entry of more and more foreign banks and services and venture capital are emerging. These new private sector banks, with lean and nimble innovative services may augment revenue with cost footed structure, better technology, market effective measures.orientation and cost effective measures, have

intensified the competition in the Indian banking

industry. Financial Institutions have also started

entering into the domain of banks. In recent years,

the share of business of public sector banks has

declined considerably. So there is a compelling need

for the Indian banking industry to modify its

marketing strategy to attract the customers and to

withstand the stiff competition from foreign banks

and new private sector banks

The advent of technology both in terms of

computers and communications has drastically When people are hard pressed for time, the

altered the methodology of banking business. In the need for "anytime anywhere" banking gains utmost

banking sector, the technology has opened new importance. Bearing this in mind, banks provide a

8

e-track

April-June-2009

novel service which gives retail customers account prepare appropriate manpower plans and strategies.

information and real-time transaction capabilities e-CRM applications could enhance the delivery of a from their cell phones. With SMS banking the CRM strategy, such applications should be chosen following services can be obtained: carefully to fit in with organisational culture,

Get account balance details process and legacy IT systems. The financial and

human resource cost as well as the amount of time Request a cheque book required for implementation of a CRM application

Request last three transaction details should also be key factors in the selection of e-CRM

Pay bills for electricity, mobile, insurance etc.applications.

To meet the new challenges, banks have to www.techtarget.com, www.efuture.ca

devise novel ways of meeting the customer's www.eca.com, www.findarticles.com

demands. To help the banking staff to get sufficient palisade.plynt.com/issues/2005Sep/sms-bankingexposure to technology, suitable packages relating

to hardware and software applications in relation to www.netbanker.com, www.crmtrends.com,

their works are to be provided. Further, a separate www.customerservicepoint.commarketing wing may be created in every bank to

market their banking services. They must be trained CRM at the speed of light by Paul Greenberg

suitably to keep pace with the changing CRM concepts & cases by Alok Kr. Raienvironment. In order to meet the challenges, the

Human Resource Department in banks have to

·

·

·

·

Development of the Skills of Bank PersonnelWeb references:

Books referred :

Author is PS to Director PNBIIT

'Starfish'Author Unknown

A friend of ours was walking down a deserted Mexican beach at sunset.

As he walked along, he began to see another man in the distance. As he grew nearer, he noticed that the local native kept leaning down, picking something up, and throwing it out into the water. Time and again, he kept hurling something out into the ocean.

As our friend approached even closer, he noticed that the man was picking up starfish that had washed up on the beach and, one at a time, was throwing them back into the water.

Our friend was puzzled. He approached the man and said, "Good evening, friend. I was wondering what you are doing?"

"I'm throwing these starfish back into the ocean. You see, it is low tide right now, and all of these starfish have washed up onto the shore. If I don't throw them back into the sea, they'll die from lack of oxygen."

"I understand," my friend replied, "but there must be thousands of starfish on this beach! You can't possibly get to all of them. There are simply too many! And don't you realize this is probably happening on hundreds of beaches all up and down this coast? Can't you see that you can't possibly make a difference?"

The local native smiled, bent down, and picked up yet another starfish and, as he threw it back into the sea, replied:

"Made a difference to THAT one!"

9

e-track

April-June-2009

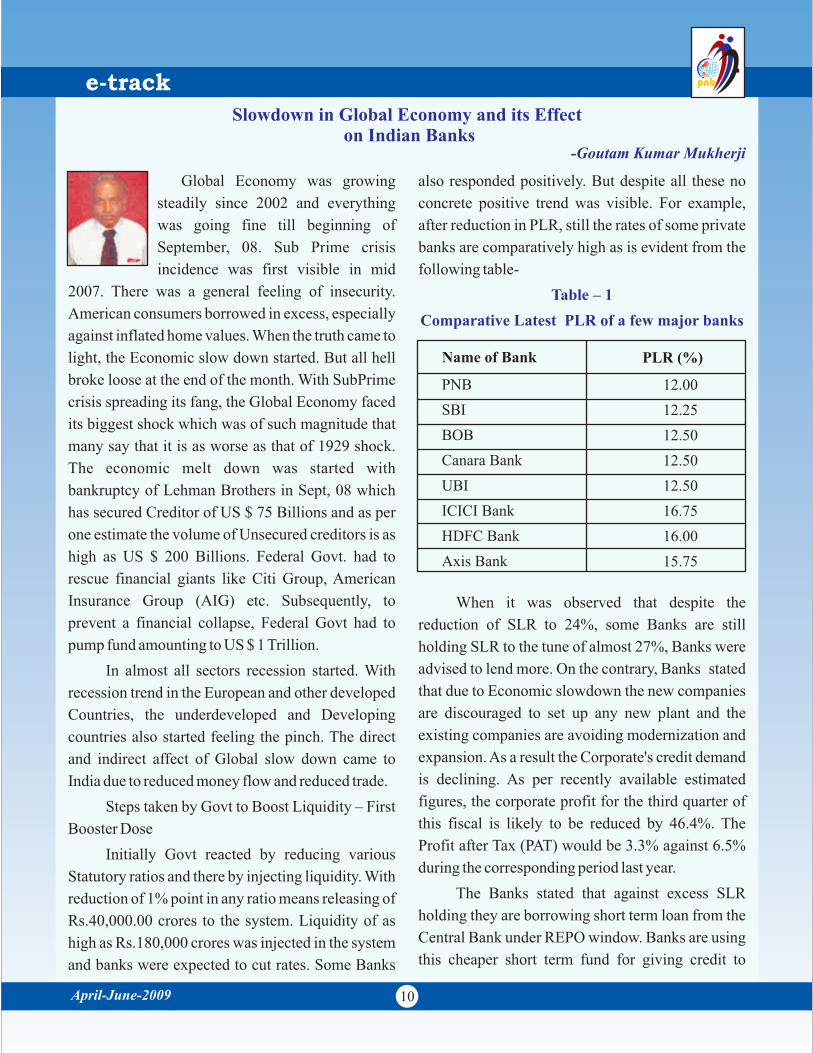

Global Economy was growing also responded positively. But despite all these no

steadily since 2002 and everything concrete positive trend was visible. For example,

was going fine till beginning of after reduction in PLR, still the rates of some private

September, 08. Sub Prime crisis banks are comparatively high as is evident from the

incidence was first visible in mid following table-

2007. There was a general feeling of insecurity.

American consumers borrowed in excess, especially

against inflated home values. When the truth came to

light, the Economic slow down started. But all hell

broke loose at the end of the month. With SubPrime

crisis spreading its fang, the Global Economy faced

its biggest shock which was of such magnitude that

many say that it is as worse as that of 1929 shock.

The economic melt down was started with

bankruptcy of Lehman Brothers in Sept, 08 which

has secured Creditor of US $ 75 Billions and as per

one estimate the volume of Unsecured creditors is as

high as US $ 200 Billions. Federal Govt. had to

rescue financial giants like Citi Group, American

Insurance Group (AIG) etc. Subsequently, to When it was observed that despite the

prevent a financial collapse, Federal Govt had to reduction of SLR to 24%, some Banks are still

pump fund amounting to US $ 1 Trillion. holding SLR to the tune of almost 27%, Banks were

advised to lend more. On the contrary, Banks stated In almost all sectors recession started. With

that due to Economic slowdown the new companies recession trend in the European and other developed

are discouraged to set up any new plant and the Countries, the underdeveloped and Developing

existing companies are avoiding modernization and countries also started feeling the pinch. The direct

expansion. As a result the Corporate's credit demand and indirect affect of Global slow down came to

is declining. As per recently available estimated India due to reduced money flow and reduced trade.

figures, the corporate profit for the third quarter of Steps taken by Govt to Boost Liquidity – First this fiscal is likely to be reduced by 46.4%. The Booster DoseProfit after Tax (PAT) would be 3.3% against 6.5%

Initially Govt reacted by reducing various during the corresponding period last year.

Statutory ratios and there by injecting liquidity. With The Banks stated that against excess SLR reduction of 1% point in any ratio means releasing of

holding they are borrowing short term loan from the Rs.40,000.00 crores to the system. Liquidity of as Central Bank under REPO window. Banks are using high as Rs.180,000 crores was injected in the system this cheaper short term fund for giving credit to and banks were expected to cut rates. Some Banks

Table – 1

Comparative Latest PLR of a few major banks

Slowdown in Global Economy and its Effect on Indian Banks

-Goutam Kumar Mukherji

Name of Bank PLR (%)

PNB

SBI

BOB

Canara Bank

UBI

ICICI Bank

HDFC Bank

Axis Bank

12.00

12.25

12.50

12.50

12.50

16.75

16.00

15.75

10

e-track

April-June-2009

borrowers. But the Central Government is not observed that banks are lending more to this sector as

willing to buy this plea. is evident from the following figures

Recently, the Finance Secretary Shri Arun

Ramanathan has advised the State run banks to (Amount in Rs.crores)increase lending and also upwardly revise the Credit

Disbursement targets of banks for this fiscal by

Rs.56,000 crores.

The effect of economic slow down was

reflected in the decline in share prices of three Banks

which are included in BSE 30 Share Index till

31.12.08 which were very high and were as under Unsecured loan mainly comprises of

Corporate bill discounting & overdraft loan,

Personal loan products, education loan, credit card

receivables, loan against salaries, consumer

durables etc. Here the rate of return is high but risk is

also correspondingly higher. In case of economic

slow down, this portfolio is likely to suffer first and

most. The latest incidence is of M/S Satyam to whom

one of the Leading PSU Banks has advanced about

Rs.200 crores unsecured loan on the personal

guarantee and now is very worried about the fate of

the loan amount.

Central bank is giving more stress on giving As per latest available data Banks' credit loans to Corporate, Retail, Exports and SMEs. For growth on year to Year basis as on 21.11.08 in case of this they have come up with second booster dose Commercial and Non food credit sectors improved which has been given at the later part of the article. in comparison to the corresponding period last year

and were as under as on 21.11.08

Now Banks are increasingly turning to retail

lending as they did in 2001 after economic

slowdown. The main sectors are Housing, Auto,

Personal loans and Consumer durables. But with

recent scenario of job losses and reduction of salary

the repayment are likely to face problems. CRISIL in

its mid term review has already estimated that NPA

in Retail lending is likely to be increased from 2.7%

However if we take a closure look on the as on march, 07 to 4.0% as on march, 09.

Unsecured portfolio of the Banks' credit it may be

Table–4 Comparative position of Unsecured Loan

Table – 2

Share prices of 3 Banks included in BSE 30

Share Index

Banks Credit

Retail Lending

Table – 3

Comparative position of Year to Year (Y-O-Y)

growth in Bank's credit

Name of BankPrice as on 31.12.08

% Change

ICICI Bank

SBI

HDFC Bank

SENSEX

Rs.448.35 (-) 63.58

Rs.1288.25 (-) 42.76

Rs.997.60 (-) 42.37

(-) 52.0

Y-O-Y Growth % as on 21.11.08Name of Sector

Last Year This Year Commercial

23.1%

27.0%

Non Food

23.7%

26.9%

Unsecured loan

As on 31.03.07

As on 31.03.08

Growth %

PSU Banks 2692.95 3793.51 40.9 Private Banks 770.66 1076.87 39.7 Foreign Banks

577.07

851.22

47.5

11

e-track

April-June-2009

Export

Table - 5

Comparative Figures of Export and Import for

Nov, 07 Vis a Vis Nov, 08

SENSEX Variation

Table - 7

Variation in SENSEX data

Table - 6

Comparative Figures of Export and Import for

Apr- Nov, 07 Vis a Vis Apr- Nov, 08

From the above figures of October and

November, 08 it is clear that the present global India's export witnessed three-fold growth slowdown has caused reversal in the demands of during the boom period of Global economy during Indian merchandise and services from the 2002-03 to 2007-08. Despite this, the Country's Developed countries. As a fallout of the declining share in Global merchandise and Service market is export, the main affected sectors would be only about 1.5%. The country was trying to augment Traditional export items like textiles & apparels', the share by doing more export and the export clothing, metal & metal products and other performance was positive during the first half of this miscellaneous manufacturing units. Out of these fiscal.Textiles & apparels, Leather products, gem, jewelry But for the first time in last 5 years, India's & handicrafts. All these are great employment Export showed a negative growth of 12.1% during provider. The job cuts in these sectors are already the month of October, 08. The same trend continued being reported in various media. Many big Industrial in the month of November, 08 also as is evident from houses are reporting that they are short of order and the following figures :wef April, 09, they have to rethink their production

schedule.

Agriculture, the main employment provider in

India would also be adversely affected as many (Amount in Billion U S $) processed food units and other agriculture item

processing units will not require the raw materials

which otherwise would have been brought from the

market.

The negative Variation in SENSEX due to

various market forces as well as due to the Global However, the cumulative figure of Export till slowdown was as under :the month of November, 08 in this fiscal is showing

positive trend as is evident from the following

figures :

(Amount in U S $ billions)

However though the Index crossed 10000

marks later on but due to Stayam episode it has again

crashed. In all probabilities some time will be

required for necessary correction.

Particulars Nov ‘07 Nov‘08 Growth %

Exports 12.7 11.5 (-) 9.9%

Imports 20.3 21.5 6.1% Trade Deficit 7.6 10.0 31.6%

Particulars Apr -Nov ‘07

Apr– Nov ‘08

Growth %

Exports 99.9 119.30 19.4%

Imports 153.1 203.64 33.0%

Trade Deficit 53.19 84.34 58.6%

Date Index

10.01.08 21206.8

20.11.08 8451.0

26.12.08 9328.9

12

e-track

April-June-2009

Additional Steps taken by Govt to Boost direction several Silver Linings are clearly visible.

Liquidity – Second Booster Dose. Decline in Crude Oil Price & Finding new

Indian Government delivered the second domestic source.

booster dose on 02.01.09 by announcing various The crude oil price of late increased many measures to boost Indian economy. One major dose folds. Luckily for Indian and global economy, the was reduction in various rates of Interest and Ratio price of crude oil was drastically reduced in the as under: recent time which is evident from the following

figures has now declined as under;

(Price in US $ per barrel)

Due to this reduction in price of crude oil the

fertilizer subsidy is likely to be brought down from With the reduction in CRR by 0.5% Cash estimated Rs.119,000 crores to Rs.102,000 crores. amounting to Rs.20000 cr will be released in system In the next fiscal it is likely to be reduced by 50%. which will boost the Bank's lendable Fund. Similarly, the OIL & Gas subsidy will also be Various other measures have been announced substantially reduced. for Export. SME sectors, re-capitalisation of Banks

Recent development in India in the Fuel front etc. is a very good silver lining for the future fiscal Even Indian Railways have reduced the tariff management as is revealed by the following facts. by 6% for carrying Iron ore meant for export to any (i) Reliance Industries Krishna Godavari Gas Indian port. India's annual iron ore production is

Project has capacity to produce 550,000 barrels approximately 200 million tones out of which 50% per day of OIL EQUIVALENT. This production is exported. is equal to 40% of India's current output. But all these measures to boost exports may be

(ii) Cairn India's Barmer Oil Project can produce negated by importing countries as some countries 20% of the present domestic crude oil are contemplating imposition of anti Dumping or production. At present, 3 million barrels crude Countervailing duties to restrict imports and to oil is being processed in India per day out of increase demand for indigenous manufactured which only 0.8 million is domestic production goods. .and 2.2 millions is being imported.India has to search new opening for export as With expected additional domestic production well as conclude the Doha round of negotiations.

of such huge amount of crude oil and gas or oil

equivalent, the import bill will be substantially All attention is now focused to revive the

reduced and Current A/C deficit may be controlled to economy in 2009 and to put it back on rail. In this

some extent.

Table – 8

Reduction Announced on 02.01.09 Table– 9 Variation in Crude price

Positive aspects or Silver Lining for 2009

Price as on August, 08 Current price

148 40

Name of Ratio Previous Ratio

Present Ratio

Reverse Repo 6.5% 5.5%

Repo 5.0% 4.0% CRR 5.5% 5.0%

13

e-track

April-June-2009

Inflation

Table - 12

Inflow and Outflow of FIIs Fund in 2008

Table – 10 Variation in Inflation figureFood Sectors

Table – 13

Comparative Position of Required Buffer FOREX Reserve

stock vis a vis estimated stock

Table –11 Variation in Forex Reserve

Banks Profit from Treasury Operation

relevant figures are as under-

After a long gap of 16 years, the Inflation

figure registered its peak in the month of August, 08.

Luckily, the same started climbing down for straight th10 weeks and recently to a manageable level as

under

The position in the Food sector appears to be

comfortable which is evident from the under

mentioned figuresThis has enhanced the hope of further rate cut

by Banks.

Forex reserve including gold and SDR was (Quantity in million tones)

rising till September, 08 during this fiscal but after

that it started declining. For the first time as on

26.12.08, the declining trend was reversed as under

(Amount in Billion US $)

The additional stock will help to check the

prices and give more food security.

With the recent development in the Money The net increase of US $ 651 million in inflow

Market, one advantage has been accrued to the of FOREX during the week ended 26.12.08 was

Banks. The yield on 10 years Govt Bonds has fallen entirely due to increased inflow of US $ 652 millions

from 9.55% as on Sept, 08 to 5.43% as on last week by FIIs.

of Dec, 08. The net inflow of FIIs has become positive

Banks stand to earn 7 paise for change of every which has a wider ramification. For one of the main

basis point in the price of 10 year Govt. bonds. reason for crash in Share Prices was heavy

Therefore, there will be windfall profit for the Banks withdrawal by FIIs during later part of 2008 as is

from Treasury operation. However, the problem is evident from the following figures:

that the Banks can book profit only if they actually There was various reasons for the variation but

sell the above Govt. Security. Alternatively, if not one important point was withdrawal of funds by

sold, then the provision already been made by most Foreign Institutional Investors (FIIs) and the

of the Banks in the June, 08 quarter for rise in the

Expected StockCommodity Buffer stock Requirement

Quantity As on Quantity

Wheat

4.00

01.04.09

9.17

Rice

5.20

01.10.09

7.37

Inflow Outflow

US $ 17 Billions US $ 13 Billions

st1 week of August, 08 As on 26.12.08

12.91% 6.61%

As on Amount of Reserve

06.04.08 200.3 Sept, 08 278.0 19.12.08 253.9 26.12.08 254.6

14

e-track

April-June-2009

price of 10 year Govt. bond and marking them to credit. For this it has increased the Credit Guarantee

market, can be offset. Anyhow, whether the Banks Limit from Rs.50 lacs to Rs.100 lacs. Further, units

book profit through actual sale or offset the earlier employing 10 or more people are being brought

provision, the profit will be increased and the same under Social Security Measures. Various other

may be utilised to make more provision for NPA, measures have been declared.

which is any way going to rise across the Board for

all banks as on March, 09. One of the Sliver Lining is that despite the

general belief that international tourist inflow to the

(i) The most important factor for Rural economy country would be reduced due the economic slow

is that the Agriculture Production is likely to down and terror incidence and terror threats, actually

be positive for four years in succession i.e. the international tourist inflow increased as is

from 2004-05 to 2008-09 which is a rare evident from the following figures:

phenomenon.

(ii) Huge Fund has been released to the Rural area

under various Govt. schemes. Like under

National Rural Employment Guarantee

Scheme alone out of total allocation of

Rs,26000 crores already 70% has been

released. Under Pradhan Mantri Gram Sadak

Yojana, Swarna Jayanti Gram Swarojgar

General Election is scheduled in the country Yojana and Indira Awas Yojana - 50% of the

this year. New American President is to take over allocated amount have been released.

charge shortly. Therefore priority shift may be there (iii) Minimum Support Prices (MSP) of all the after installation of New Government. major cereals has been increased. The MSP of

Sugar cane has also been increased.

As per Dr. Montek Singh Ahluwalia 2009 is (iv) The most important factor is that rural India is

going to be very difficult year for Global Economy. not affected by the Global Slowdown.

However, India can grow over 7 % next fiscal. All Therefore, more focus is to be given to rural

the present indications are directing to improvement areas by all may be it is Banks or Private

in the situation in India if not immediately but in the companies dealing with auto, telecom or

second half of 2009 as the country is determined to FMCGs.

overcome all adversaries and to grow.However, some problems are being faced in

* * *case of sugar and edible oil etc.

(Data Sourcing has been done from Economic Times

for which the Author expresses his sincere gratitude)SME contributes 8 to 9 % of the Country's

GDP. Government is also trying to boost SME

International Tourist arrival

Focus on Rural Area

Table – 14

Comparative Positive of International tourist

arrival and FOREX income

Conclusion

More stress in SME Sector

Author is Circle Head, Punjab National BankCircle Office Midnapur

Particulars In 2007

In 2008

Growth (%)

Arrival (in millions) 5.08 5.30 6.0 FOREX Earning (In billion US $

10.07 11.50 8.0

15

e-track

April-June-2009

The proportion of NPAs in the entire banking system between 2005-06 and 2006-

bank loan books is an important 07 which is less than 1% of the total loan sales

indicator of financial health of the outstanding in the entire banking system.

bank and any adverse indicator shall

impact the bank's rating in the system

and its ability to raise capital for its business

efficiently. Poor credit quality exposes the banks to

vulnerability of further distress in its portfolio and

adverse effect on profitability that leads to a vicious

cycle.

Experience shows that any NPA account, if

unrecovered early, loses value over time. Over the

next few months, banks are likely to see a spurt in

their underperforming loans, thanks to the

economic downturn. Banks are also likely to face

more pressure from regulators and shareholders to

act decisively to eliminate problem loans—through The reasons are not far to seek. Currently, all

recovery or loan sales or both. For banks that attack loan sale deals are done off line. The entire loan

the problem aggressively through a regular program sales cycle take about 45 to 60 days on an average.

of distressed loan sales, the reward will be lower The number of players on the buy side is limited .As

NPAs, a stronger balance sheet and ultimately, a of now, there are only 11 RBI Approved Asset

higher share price. Reconstruction Companies and not all of them are

Though RBI has permitted sale of distressed very active in the loan sales market. Pricing is loans to other banks and ARCs (Asset another ticklish issue which is often arrived at after Reconstruction Companies), activities on the loan lengthy negotiation with the would be buyers and sales front is very tardy. there is no market mechanism for price discovery.

The entire loan sales cycle take about 45 to 60 The following are the credit facilities that are days on an average, as depicted below in Figure 1. normally traded between banks .

The table shows the total loan sales of the

Loan Sales

Amount in Rs.crores

Electronic Trading of Distressed Bank Loans-M Ravindran

Bank loan Products

0

5000

10000

15000

LoanSa le

s

2005-06

2006-07

2005-06 2006-07 Increase/Decrease

Loan Sales

13441.85 8041.82 -40.2%

As a % of total loan

0.89%

0.41%

Source: RBI

16

e-track

April-June-2009

RBI guidelines on sale of assets are summarized as 'without recourse' basis, i.e., the entire credit

under: risk associated with the non-performing

financial assets should be transferred to the The financial asset must be NPLs for at least purchasing bank. Selling bank shall ensure that 24 months.the effect of the sale of the financial assets Consideration for sale of NPLs, inter-se, should be such that the asset is taken off the within the banking system should be only in books of the bank and after the sale there the form of 'Cash'.should not be any known liability devolving on Post-acquisition, these NPLs cannot be sold the selling bank.before 15 months.Banks should ensure that subsequent to sale of NPLs will be treated as standard asset in the the non performing financial assets to other books of purchasing bank for 90 days, after banks, they do not have any involvement with which asset classification will depend on reference to assets sold and do not assume recovery with reference to cash flows operational, legal or any other type of risks estimated.relating to the financial assets sold.

NPLs, post-acquisition, must be realized Consequently, the specific financial asset

within 3 years and at least 5% must be realized should not enjoy the support of credit

in each half-year.enhancements / liquidity facilities in any form

or manner.A bank which is purchasing/ selling non-

Each bank will make its own assessment of the performing financial assets should ensure that

value offered by the purchasing bank for the the purchase/ sale is conducted in accordance

financial asset and decide whether to accept or with a policy approved by the Board.

reject the offer.While laying down the policy, the Board shall

Under no circumstances can a sale to other satisfy itself that the bank has adequate skills

banks be made at a contingent price whereby to purchase non performing financial assets

in the event of shortfall in the realization by the and deal with them in an efficient manner

purchasing banks, the selling banks would which will result in value addition to the bank.

have to bear a part of the shortfall.The Board should also ensure that appropriate

A non-performing asset in the books of a bank systems and procedures are in place to

shall be eligible for sale to other banks only if effectively address the risks that a purchasing

it has remained a non-performing asset for at bank would assume while engaging in this

least two years in the books of the selling bank.activity.

Banks shall sell non-performing financial The estimated cash flows are normally

assets to other banks only on cash basis. The expected to be realised within a period of three

entire sale consideration should be received years and not less than 5% of the estimated

upfront and the asset can be taken out of the cash flows should be realized in each half year.

books of the selling bank only on receipt of the A bank may purchase/sell non-performing

entire sale consideration.financial assets from/to other banks only on

·

·

·

··

·

Procedure for Sale of Non Performing Loans:

·

··

·

··

·

17

e-track

April-June-2009

· ·

·

·

· Books of selling bank

·

·

Asset classification norms

·

·

Books of purchasing bank

·

·

A non-performing financial asset should be Where the purchase/sale does not satisfy any

held by the purchasing bank in its books at of the prudential requirements prescribed in

least for a period of 15 months before it is sold these guidelines the asset classification status

to other banks. Banks should not sell such of the financial asset in the books of the

assets back to the bank, which had sold the purchasing bank at the time of purchase shall

NPFA. be the same as in the books of the selling bank.

Thereafter, the asset classification status will Banks are also permitted to sell/buy continue to be determined with reference to homogeneous pool within retail non-the date of NPA in the selling bank.performing financial assets, on a portfolio

basis provided each of the non-performing Any restructure/reschedule/rephrase of the

financial assets of the pool has remained as repayment schedule or the estimated cash

non-performing financial asset for at least 2 flow of the non-performing financial asset by

years in the books of the selling bank. The pool the purchasing bank shall render the account

of assets would be treated as a single asset in as a non-performing asset.

the books of the purchasing bank.

The selling bank shall pursue the staff

accountability aspects as per the existing When a bank sells its non-performing instructions in respect of the non-performing financial assets to other banks, the same will assets sold to other banks. be removed from its books on transfer.

If the sale is at a price below the net book value

(NBV) (i.e., book value less provisions held),

the shortfall should be debited to the profit and

The non-performing financial asset loss account of that year.

purchased, may be classified as 'standard' in If the sale is for a value higher than the NBV, the books of the purchasing bank for a period the excess provision shall not be reversed but of 90 days from the date of purchase. will be utilised to meet the shortfall/ loss on Thereafter, the asset classification status of account of sale of other non performing the financial asset purchased, shall be financial assets.determined by the record of recovery in the

books of the purchasing bank with reference The asset shall attract provisioning to cash flows estimated while purchasing the requirement appropriate to its asset asset classification status in the books of the The asset classification status of an existing purchasing bank.exposure (other than purchased financial (Source: RBI Circular DBOD 16/2005-06 dt 13/7/2005asset) to the same obligor in the books of the

This article outlines the benefits that banks purchasing bank will continue to be governed

and financial institutions can realize by using the by the record of recovery of that exposure and

electronic trading platform for distressed loan sales. hence may be different.

Provisioning norms

Prudential norms for banks for the purchase/ sale

transactions

18

e-track

April-June-2009

From Offline Sale to Online Sale

Standardization of Documents

Simplified Process for Sellers Leads to Greater

Liquidity

Streamlining the Process for Buyers Creates

More Bidding

Smaller loan amounts would greatly expand the

universe of buyers. Reduced offering sizes would Although all banks still choose an offline enable investors with limited resources to enter the transaction to sell distressed debt, an online loan market, make bids and consequently increase sale would yield higher proceeds and a host of other liquidity. advantages. For example, in an off line sale, the

complexity of selling a, say, Rs.150 crore distressed

portfolio to multiple buyers can be too complex and The standardization of documents at an online time consuming. In a transaction of that magnitude, marketplace allows a lender to sell a single loan or conducting due diligence simultaneously with a pools of loans as easily to dozens of buyers as to one. large number of parties is asking for unnecessary When investors have the flexibility to purchase only complications. . what they want and nothing more, more bids are

generated, and that leads to higher proceeds for the

selling bank. In essence, the aggregate of many

smaller bids becomes greater than if a single bidder An online marketplace provides the greatest purchases the entire amount.number of options for sellers and buyers of

distressed loans because of its efficiency and The purchase and sale documents can be

simplicity. At an online marketplace, the loan sale standardized to be the same for each online sale. A

process is easier. Each time a loan sale is completed condition of participating at an online marketplace

at an online marketplace, it becomes part of the is the agreement to use standardized transfer

collective knowledge base. The parties working documents, which eliminates the time and expense

with an online marketplace can readily access this of individually negotiated loan documents. The

information to help set the seller's expectations transfer documents, which can be posted online, can

about the eventual sale price. be accessed by legal teams for review in advance of

the bidding. Standardized documents minimize the At an online marketplace, current market possibility of legal complications, while giving values are easy to obtain from multiple interested investors the confidence that there will be no parties and can provide a lender with a more surprises at the end of the transaction. Equally accurate measure of a loan's resale value. Once a important is the simplification of the closing lender decides to sell a loan/loan portfolio, more process. options are possible at an online marketplace. For

example, a lender can divide a large loan or pool of

loans into smaller pieces. Breaking up a loan into

tranches gives investors with limited capital an For buyers, an online marketplace makes it opportunity to bid. Instead of having to purchase the easier to purchase debts because the entire process entire amount, an investor can afford to bid on a has been streamlined, from identification of loans to smaller portion. Separating loan into individual due diligence to bidding and closing. Online components is also a better alternative for investors marketplaces make it easy to identify buying than offline sales where the highest bidder is sold the opportunities. Greater efficiency in prospecting for entire loan piece. loans reduces loan acquisition costs.

In off line transactions, investors are forced to Similarly, due diligence is more convenient buy the entire loan portfolio including unwanted and less expensive at an online marketplace than in pieces of debt to get the piece they really want. an offline sale. All the loan documents can be

19

e-track

April-June-2009

digitized and uploaded to the online platform and institutions identify the types of loans that can be

investors can review that information right at their sold/purchased, in setting the initial loan price and

desk. That reduces dead deal costs if the investor is in smoothly managing the process for both sellers

outbid or if the investor declines to bid. In addition, and buyers. In setting the loan pricing in off line

because due diligence documents have been sales, selling banks rely on their experience, but

standardized, investors don't waste time looking for electronic trading can significantly improve the art

information because it is in the same place every of loan pricing through the introduction of objective

time. Being able to calculate the numbers quickly data.

permits buyers to look at more deals in less time, Typically, an on line loan sale process will which leads to more liquidity. involve the following steps.

By contrast, the negotiation of separately

drafted legal documents is one of the key reasons

that closings for offline transactions can take weeks.

Electronic trading enables dynamic loan

pricing and allows small pieces of debt to be

purchased cost effectively. Because the fixed costs

of the loan sales are dramatically lower, it becomes

possible to sell loans in small pieces. Another

important factor is that investors can now buy

exactly what they want—and no more. Currently,

investors often end up with loans they didn't want Once the selling bank decides to proceed with but were forced to buy because loans were bundled

a loan sale after a review, the next step is to prepare together. With electronic trading, investors can an offer document summarizing all critical purchase loans with greater precision, which further information. The synopsis is intended to give buyers lowers costs and improves the deployment of enough information to quickly ascertain the asset's capital.value and decide if they should bid. Typically, the

document will not include the price but will give Of all the benefits of electronic trading,

details of book outstanding and value of co laterals. superior trade execution may rank as the most

The price discovery is through the process of significant. Secondy, with more buyers and more

bidding in the open market. The offer letter may be bids per transaction, assets will fetch higher prices

standardized into readily identifiable sections that for sellers.

allow buyers to find the same information in the Electronic trading can dramatically shorten same places for each transaction. The

the time from offer to closing from 45/60 days to standardization of offer documents is necessary for about less than a week and closings can be quicker decision making on the part of the buyers.expedited.

Once the offer document is uploaded on line, While electronic trading can bring new the selling bank can kick off the marketing

efficiencies to the loan sale process, human campaign in right earnest. To attract the greatest judgment is still indispensable. Experienced loan number of buyers, prospective investors may be professionals play the central role in helping contacted by e mail and regular mail. Using

On line offer document

Superior Trade Execution

Marketing campaignThe Critical Importance of Human Judgment

20

e-track

April-June-2009

technology, the selling bank can reach prospective and aren't allowed to increase it. In an open, e-cry

buyers very efficiently because they can provide auction, bidders can increase their bid in response to

timely updates by e-mail and target investors with other offers they are seeing in real time on their

specific interest in individual kinds of loans. When computer screen.

investors register online to participate in a sale, they

will indicate the exact types of loans in which they The price to be quoted on the screen takes into

are interested. Highly efficient marketing creates a account a wide range of quantitative and qualitative

larger pool of qualified investors.factors, such as book outstanding, the dependability

of the financial stream, quality of collateral, loan-to-

It is necessary that all relevant loan-related value ratio and debt-service coverage ratio, among

documents are converted into digital files. These others. It also includes financial factors such as

documents, in various electronic formats, may external/internal credit rating ,if any, whether the

include original loan documents, collateral account falls under suit filed category, interest rate

appraisals, operating statements, court proceedings trends in the market, yield, whether interest is fixed

or other information that supports the original offer or floating ,the term to maturity ,the age of the loans

document of sale. Online access eliminates the time etc . The pricing process can take as little as a day for

and expense of physically inspecting the loan files. simpler loans, such as a pool of personal loans or it

can take even a week for more complicated loans,

such as a high value term loan.Provision is to be made on line for answering

queries from prospective buyers and the more

questions that can be answered, the smoother the Successful buyers can be selected at the end of

transaction process. the bidding period. In most instances, a loan will be

sold to the highest bidder, but in rare cases, the

selling bank may choose another buyer if there the To streamline the loan sale process, the selling

buyer is unable to close the transaction. With a live bank can use a standard purchase and sale

e-cry format, bidders see for themselves who has agreement. Once the selling bank has agreed to

won at the conclusion of the session. In a sealed bid, conduct a sale, transfer documents may be posted

the buyer is notified by the selling bank shortly after online to allow buyers to review the document ahead

the bid deadline.of time. By making documents accessible in

Closing As soon as the seller accepts the advance, buyers and sellers minimize the possibility winning bids, the buyer must deposit the bid amount of ambiguity and help ensure that the transaction and the closing can occur within two business days. proceeds in a fair and straightforward manner.

The streamlined on line loan sale process can

accelerate liquidity in the marketplace. These Bids can be submitted by investors through an

process improvements can witness a surge in online sealed bid or an electronic “e-cry” format.

volume of loan sales. In uncertain times, this can be The bid may be kept open for a specific period say

very comforting both to the buy side and sell side.48 hours. The auctions can be executed by a sealed

bid, which can be done online, or by a live online

auction fixed for a particular day and time. In the

sealed bid, buyers generally give their best bid first

Pricing

Online due diligence

Handling investor inquiries

Bid award

Preparation of transfer documents

Competitive bidding

Author is working at : Training & Consultancy, Financial Technologies Knowledge Management

Company Ltd, Exchange Square, First Floor, Gundavali, Suren Road ,Andheri , Mumbai

21

e-track

April-June-2009

Abstract

Introduction

Origin of the phrase

Purchase and Inventory or other

combinations. It generally comes in Enterprise Resource Planning (ERP) is often different suites Manufacturing suite, considered synonymous with enterprise Nonmanufacturing Suite. CRM computerization, which significantly dilutes the (Customer Relationship Management) concept. It is really a business tool, which are the extended forms of Enterprises Resource seamlessly integrates the strategic initiatives and Planning. policies of the organization with the operations, thus

providing an effective means of translating strategic E.R.P. standardizes manufacturing process

business goals to real time planning and control. and HR information, as well as integrating financial

data, so that sales and accounts have the same Small and medium enterprises (SMEs) have figures.been receiving less focus from the software vendors

as compared to Large Enterprises (LEs).Research Today various soft wares are available in the

on the implementation of ERP in certain European market for SME segment depending on the size of

countries shows that the job of implementing an the organization. E.R.P. software should be flexible,

Enterprise Resource Planning package (ERP) is a secure, and should easily integrate with the present

riskier business for SMEs than for LEs. business applications. The single data base is the

simple core concept which enables different However, in the present paper an attempt has divisions and departments to easily share been made to highlight the significance of ERP for information and communicate with one another. It economy boosters Indian SMEs and shown the also allows the automation of previously paper evolution of the ERP concept, their working based process leading to various processing procedures through the help of various secondary efficiencies. For example, a workflow system within datas and research papers.an integrated ERP system can eliminate the time to

place an order. An E.R.P. system can also “control” E.R.P is an integrated software package process such as an order placed by an employee. It

which integrates nearly all the facets of the business , knows who the employee is, and the sign-off level; it including planning, manufacturing, sales inventory , can pass this information on to the supervisor as a HRIS(Human Resource Information System) part of work flow process , so that the order can be finance and marketing .E.R.P. denotes Enterprise authorized , before being sent on electronically to Resource Planning which is a technique of using the supplier. computer machinery to connect various functions

like accounting , inventory control and human Its evolution started in 1960 and until now the resources of any company as a whole. It is planned

evolution continues. The phrase ERP formerly to facilitate information sharing, business planning obscure systems intended to plan the use of and decision making on a broad business basis. enterprise-wide resources. Though the acronym Basically it is a multimodal application that ERP is derived from the manufacturing integrates cross functional department centrally. environment, but in this competitive era it has The three modules should be present Sales,

E.R.P TREND TOWARDS SMEs

Research Scholar Faculty of Commerce, B.H.U., Varanasi - Anchal Singh

22

e-track

April-June-2009

greater relevance and much broader scope. ERP due to which earlier lacunas were removed. It

systems usually try to meet entire fundamental tasks standardized and reduced the number of software

of an organization, despite the organization's business specialties needed within bigger business groups.

or charter. There is hardly any organization, be it

Corporate, non-profit firms, non-governmental Typically in an organization, every

organizations, governments, and other large entities department may be finance, human resources or

which has been untouched by this panacea.warehouse has its own computer system and E.R.P.

The ERP that earlier used stand-alone attempts to integrate all departments and functions applications include: Manufacturing, Supply Chain, across a company with a single unified software Financials, Customer Relationship Management program. For instance, if we have to track a customer (CRM), Human Resources , Warehouse order, then in a typical organization, the paper order Management and Decision Support System. system moves from department to department

ERP packages evolved into their present which causes delays and errors. But now days, a

form from the accounting tools that the large single software program removes this lacuna

corporations implemented for payroll processing in whereby, E.R.P. takes a customer order and provides

the 50's. Their functionality expanded into tracking a software roadmap for automating the process

stock levels, at the first for the purpose of financial involved in fulfilling the order. They can track down

controlling and later covering the entire process of the order at any point by logging onto the E.R.P.

good management. Material Requirement Planning system, which in turn reduces cost and time

(MRP) in the 70's automated the production overruns, brings in overall efficiency by minimizing

process, by scheduling operations and material errors and help in serving the customers faster. It can

purchasing based on the forecasted and current thus be used for other business process to optimize

requirements of finished goods and the constraints resources.

of the production facility. Manufacturing Resource E.R.P. in India is gaining popularity among Planning (MRP-II) systems in the 80's coordinated corporate. For effective implementation ,it should be the entire process, from planning the purchase of done on a modular basis, should be grounded in material and parts, requirement based production reality and should be a complete package in its capacity, planning, to distribution .The term E.R.P. coverage.was fist used by Gartner Group in the early 90's and

Most MSMEs in the manufacturing sector included multiple applications that automated parts

due to lack of awareness, technical know–how and of business (MRP –II, CAD, CAM, CAE, financial

low monetary resources continue to use inflexible module).

stand alone application and are not able to utilize the

benefits being reaped by the adoption of E.R.P.

MSMEs should try to streamline and upgrade their

operations for facilitating integration with supply

chain systems for gaining competitive advantage.

E.R.P. should be viewed not as an expense but an

investment that will reap in terms of higher sales, After emerging the ERP software the trends

profitability, hardware ensuring connectivity become differently changed. In this software ERP

through Electronic Data Interchange, Bar Code combined the data of formerly separate applications

How an E.R.P. works

The Gartner Group View.

After that

MRP

1980s 1990s 2000s

ERP eERP

23

e-track

April-June-2009

System, ERP , Intranet and Extranet as follows. decisions.

Operation cost reductions, as evident by the

metrics used for measuring the success of the

implementation

There are five major reasons why companies

undertake E.R.P.

Integrating financial information

Increased customer responsiveness in

operations

Standardize and speed up manufacturing

process.

Reduce inventory

Successful E.R.P. implementation would Improved strategic decision makinginvolve following factors.

Sensitization process in the organization, so as SME stands for small and medium enterprises to change mindset of employees who are which have become a globally accepted acronym for generally unwilling to accept it. discussion on issues relating to this sector. Small and Transformation in the business activities for medium-scale enterprises (SMEs) have come to having judicious uses of resources. play a predominant role in the domestic economies

of most countries around the worldSelection of suitable software in conformity

with the needs of the organization. This segment has developed in parallel with

large scale and MNC corporations. A continuous Imparting training to personnel for acquiring growth and development of the companies in this new sets of processes and new software segment ensures a balanced growth of the economy interface. and acts as a facilitator towards entrepreneurial Selecting across functional team for development, business ownership and related overseeing the implementation process.wealth creation, employment generation etc.

Implementing E.R.P. requires major changes ERP has changed the way of businesses in in the organizational, cultural and business process.

India and at present, more and more organizations

and industries are implementing it. The most contributory factors towards the

The best practices of its implementation are to implementation of E.R.P. are:

involve all users in the planning stages, at the time of Need for a common platform for replacing data entry, process mapping testing and training. innumerable legacy systems. Companies should involve all users during Improvement in overall process expected implementation. from its implementation There are few well known ERP vendors Data visibility for improving operating available in India. SAP, Oracle, Apps, Microsoft

Enterprise Resource Planning (ERP) ·

·

·

·

Primers for E.R.P. Implementers ·

·

SME (Small Scale Enterprises)Ø

Ø

Ø

Ø

Ø

Implementation of E.R.P.Market Scenario

Reasons for implementation:

·

·

·

24

e-track

April-June-2009

Dynamics (Navision Axapta), SSA Global desirable tool for most organizations, in the medium

Technologies, Infor Global, QAD and Exact a nd scale sectors.

Software are offering ERP software for big Generally the need for this catalytic

organizations. SAP and Oracle have launched their component arises when a business organization

ERP for SME segment. encounters problems in their working operations

that are usually related with the flow of information.

Entrepreneurs now seriously consider ERP as ERP Software is very competitive and

panacea for all their present day ills and as an growing and almost every company wants to grow

imperative to retain their competitive edge for rapidly by adopting it apart from also opting new

improving efficiency. Some of the factors that have technologies .Today India has emerged as a lucrative

catalyzed this process are globalization, market place for ERP Companies. In India, lots of

competition, need for faster response to the market small and medium size companies are growing very

place and the pressure to contain costs and improve fast and they need a software package for managing

efficiencies It is usually observed that much of the their growth .So, ERP companies are targeting small

time is wasted in order to collect and compile and medium size company. Nowadays, every top

relevant information, which in turn results into educational institute, consultancy and company is

inadequate management decisions and ERP constantly working towards promoting itself.

removes these obstacles. If we consider SMEs, then According to Frost and Sullivan research

most often the decision to purchase Commercial Off conducted in India, it has been found that due to

the Shelf (COTS) products is made for reducing cost rising competitive pressure most of the Indian

and finished implementation as quickly as possible. companies are looking forward to equip themselves

with modern technologies and business process like

ERP solutions that can further provide unlimited Today there are many open source and COTS

access to information and enable them to compete solutions covering almost any area of

effectively. Higher ROI, Rapid industrialization and business. Due to economies of scale, these

ease of integration with legacy systems are solution costs less than developing a custom

influencing the growth of ERP software market in solution from the very beginning. The benefit

India. In mid 90s, ERP was dream for small and is to cover most functionality required in a

medium size company, but now it is implemented by short time, with a tested solution. There are

many small and medium sized companies. disadvantages such as less control over the

code, less certainty of how a component will

behave in an integrated environment or A few years back, ERP was a distant concept,

dependence on different types of vendors. perceived as applicable for the most elite of

companies, with deep pockets, who are ready to

experiment with new ideas. Today, the scene has The software selection process has been

significantly changed and it is considered as a formalized on different levels, depending on

ERP Software in SME Segment

·Build or Buy

The Need for ERP in SMEs

·Software acquisition

25

e-track

April-June-2009

the objectives, and the complexity of the motivating management for defining

application selected. Most of the methods company's strategy that can be put into action

have been developed for large organizations, t h r o u g h r e o r g a n i z a t i o n a n d E R P

and the ones with high risks involved, namely implementation.

military or government. Large Enterprises Define new organization using the right

plan the software implementation keeping the amount of formalism because of the “adhoc”

long term goals in mind whereas SMEs, on the nature of SMEs compared to large companies

other hand decide to buy software for solving a a complex procedure of reorganization

particular problem at hand. involving lots of administrative and executive

changes which may discourage the

management, who might see these activities as Implementation of any complex software

wasting time.solution is associated with various risks. If we

make a comparison between SMEs and LEs

we can say that SMEs prefer slow – phased The typical risk of hiring a consultant is that he

implementation, as compared to Larger or she may not be acquainted with the

Enterprises that prefer implementation in a specifics of a particular company. There may

pilot project phase. be not be enough experience in one or more

of the fields that need to be covered by only