e Philippine Sugarcane Industry: Challenges & Opportunities · Cane / Day No. of Operang Sugar...

27

Presenter: Presenter: Ma. Regina Bautista-Martin Ma. Regina Bautista-Martin Administrator, SRA Administrator, SRA Sugar Regulatory Administration Sugar Regulatory Administration Department of Agriculture Department of Agriculture Philippines Philippines Asia-Pacific Sugar Asia-Pacific Sugar Conference Conference 11-12 June 2012 11-12 June 2012 e Philippine Sugarcane Industry: Challenges & Opportunities

-

Upload

truongquynh -

Category

Documents

-

view

215 -

download

0

Transcript of e Philippine Sugarcane Industry: Challenges & Opportunities · Cane / Day No. of Operang Sugar...

Presenter:Presenter:Ma. Regina Bautista-MartinMa. Regina Bautista-MartinAdministrator, SRAAdministrator, SRA

Sugar Regulatory AdministrationSugar Regulatory AdministrationDepartment of AgricultureDepartment of AgriculturePhilippinesPhilippines

Asia-Pacific SugarAsia-Pacific SugarConferenceConference11-12 June 201211-12 June 2012

e Philippine Sugarcane Industry:Challenges & Opportunities

The Philippine Sugarcane Industry:Challenges and OpportunitiesChallenges and Opportunities

Order of Presentation:

1) Basic Information on PhilippineSugarcane Industry

2) Sugarcane Industry Roadmap3) Industry Challenges4) Opportunities Ahead

CropYear2011‐2012CropYear2011‐2012

IndustryContribu.ontoIndustryContribu.ontoPHLPHLeconomyeconomy

AreaPlantedAreaPlanted

P70BP70Bannuallyannually

424222,,5500Hectares00Hectares

No.FarmersNo.Farmers 62,00062,000

No.ofOpera.ngSugarMillsNo.ofOpera.ngSugarMills

‐TotalMillingCapacity‐TotalMillingCapacity

2929

185,000TonsCane/Day185,000TonsCane/Day

No.ofOpera.ngSugarRefineriesNo.ofOpera.ngSugarRefineries

‐TotalRefiningCapacity‐TotalRefiningCapacity

1414

8,000MT/Day8,000MT/Day

No.ofNo.ofBioethanolBioethanolDis.lleriesDis.lleries

‐TotalAnnualRatedCapacity‐TotalAnnualRatedCapacity

44

133millionliters133millionliters

VISAYAS(18 mills + 7 refineries

+ 3 distilleries)

MAP OF PHILIPPINE SUGAR MILLS & BIOETHANOL DISTILLERIESMAP OF PHILIPPINE SUGAR MILLS & BIOETHANOL DISTILLERIES

LUZON

(7 mills + 4 refineries + 1 distillery)

NEGROS

MINDANAO(4 mills + 3 refineries)

TARLAC

Batangas Sugar

CAMARINES SUR

PAMPANGA

CAGAYAN

ILOILO

CAPIZ

LEYTE

CEBU

BUKIDNON

DAVAO DEL SUR

Davao

NORTH COTABATO

NEG

ROS

OCC

IDEN

TAL

NEGROSORIENTAL

LopezSa

Tolong

AGUSANDEL NORTE

BOHOL

LANAO DEL NORTE

MASBATE

MISAMISOCCIDENTAL

MISAMISORIENTAL

SAMAR

SURIGAODEL NORTE

SURIGAODEL SUR

ZAMBOANGADEL NORTE

ZAMBOANGADEL SUR

SOUTHCOTABATO

PALAWAN

Legend

MANILA

Sugar millsMills with annexed refineryMajor sugar ports

SAN CARLOS

5,000 HECTARES

Green Future Innovations

CAGAYAN / ISABELA

11,000 HECTARES

Bioethanol production areasPampanga Bioenergy

7,000 HECTARES

PANAY

BATANGAS

Bioethanol target areas

Canlaon Alcogreen

5,000 HECTARES

Bioethanol Distilleries

CAVITE

Cavite Biofuels

7,000 HECTARES

N

S

EW

Luzon

Mindanao

Panay

EasternVisayas

Negros17,000 has.17,000 has.

Total Cane Area Total Cane Area –– 420,000 hectares 420,000 hectares

Farm Sizes, HectaresFarm Sizes, Hectares

24%24%

12 %12 %

15 %15 %

15 %15 %

16 %16 %

18 %18 %

PhilippineSugarcaneAreasforthePast10CropYears

350,000

360,000

370,000

380,000

390,000

400,000

410,000

420,000420,000

395,381

385,662

392,567398,872

388,003

377,182

391,552 391,451

383,745

Area,Hectares

CropYears

PhilippineCane&SugarProduc<onforthePast10CropYears

Million MT

Crop Years

PhilippineFarmProduc<vityforthePast10CropYears

PhilippineSugarProduc<on&TradeforthePast10CropYears

Crop Year Pesos Per 50-kilo bag

Peso-US $Exchange Rate

USCents/lb

2011-2012* 1,404 43.15 29.58

2010-2011 1,864 43.4638.99

2009-2010 1,664 46.21 32.74

2008-2009 945 47.93 17.92

2007-2008 1,057 43.1022.29

2006-2007 844 48.17 15.93

2005-2006 978 53.01 16.77

2004-2005 664 55.5010.88

2003-2004 710 55.68 11.59

2002-2003 843 53.46 14.34

HISTORICAL PHILIPPINE RAW SUGAR COMPOSITE PRICESHISTORICAL PHILIPPINE RAW SUGAR COMPOSITE PRICES

* As of April 2012

BioethanolBioethanolProduc<on,LitersProduc<on,Liters

YearTOTAL

Produc<on(MillionLiters)

MandatedBioethanol

Blend

MandatedVolume

(MillionLiters)

2008 0.368 Voluntary None

2009 23.11 5% 208

2010 9.89 5% 219

2011 4.14 10% 461

2012* 12.00(es<matesasof

May2012)

10% 486

In 2012, around 486 million liters bioethanol is required under the 10% mandatedblend, however, only 4 distilleries are operational with a combined annual ratedcapacity of 133 million liters.

2010 Power Generation by Plant Type, GWh

Gross Power = 67,743 GWh

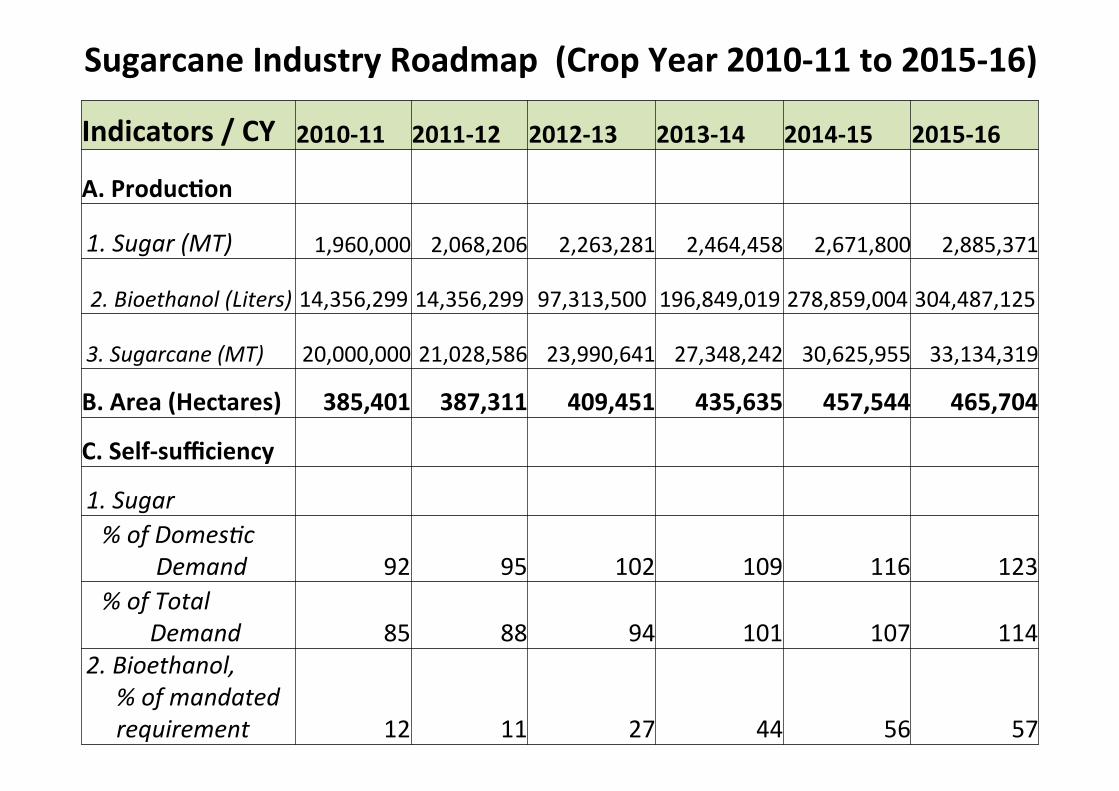

SugarcaneIndustryRoadmap(CropYear2010‐11to2015‐16)

Indicators/CY 2010‐11 2011‐12 2012‐13 2013‐14 2014‐15 2015‐16

A.Produc<on

1.Sugar(MT) 1,960,000 2,068,206 2,263,281 2,464,458 2,671,800 2,885,371

2.Bioethanol(Liters) 14,356,299 14,356,299 97,313,500 196,849,019 278,859,004 304,487,125

3.Sugarcane(MT) 20,000,000 21,028,586 23,990,641 27,348,242 30,625,955 33,134,319

B.Area(Hectares) 385,401 387,311 409,451 435,635 457,544 465,704

C.Self‐sufficiency

1.Sugar%ofDomes>cDemand 92 95 102 109 116 123%ofTotalDemand 85 88 94 101 107 114

2.Bioethanol,%ofmandatedrequirement 12 11 27 44 56 57

SugarcaneIndustryRoadmap(CropYear2010‐11to2015‐16)

1/Assumingthepriceofbioethanolisinfluencedbysugarprice2/Agriculturalworkersonly

D.Na<onalYield 2010‐11 2011‐12 2012‐13 2013‐14 2014‐15 2015‐16

1.MTSugarcane/Ha,Average 51.9 54.3 58.6 62.8 66.9 71.2MTSugarcane/Ha.,High 65.0 70.0 75.0 80.0 85.0 90.02.LKG/MTCane,Average 1.96 1.99 2.01 2.04 2.07 2.10LKG/MTCane,High 2.00 2.10 2.20 2.30 2.40 2.50

E.Farmers'Income(Pesos/Hectare/Year)‐@Planters'shareof65%;@P1,700/LKGSugar1/

1.'@Prod'nCost,P70,000/Ha.,average 42,383 49,381 60,131 71,519 83,115 95,1042.'@Prod'nCost,P100,000/Ha.,high 43,650 62,435 82,325 103,320 125,420 148,625

F.JobsGenerated

TotalNumberofworkers(1.5jobs/ha) 578,102 580,967 614,177 653,453 686,316 698,556No.ofjobsgenerated2/ ‐ 2,865 33,210 39,276 32,864 12,240

•SugarTariffSchedulesandImplica<ons

•MaintainingProfitabilityinthePhilippineSugarcaneIndustry

•PerformanceofPhilippineSugarMillsandDeterrentstoMillImprovements

•Implementa<onoftheBiofuelsandRenewableEnergyLaws

AFTA–CEPTTariff

Schedule:

2011‐38%

2012‐28%

2013‐18%

2014‐10%

2015‐5%

Implica<ons:

•Entryofimportedsugarwouldthreaten

thelivelihoodofthe62,000farmers

and600,000workersofthe

Philippinesugarcaneindustry

•Entryofimportedsugarwillpush

downwardsthemillsitepriceoflocally‐

producedsugar

Maintaining Profitability in the PhilippineSugarcane Industry

•FragmentedfarmsduetotheComprehensive

AgrarianReformLaw

•Smallfarmshavelowfarmproduc.vi.es

•Smallfarmershavenofinancialcapabilityin

procuringthenecessaryfarminputs

•Lacksinfrastructuresupportfromgovernment

Performance of Philippine Sugar Mills andDeterrents to Mill Improvements

•Lessefficientsugarmills,lowcapaci.es

•MajorityofPhilippinemillsneedtobe

rehabilitatedandupgraded

•Lackoffinancialpackagefromgovernment

financingins.tu.ons

Implementation of the Biofuelsand Renewable Energy Laws

•Uncertaintyinthebuyingpriceofbioethanol–

howsuccessfulistheimplementa.onoftheprice

indexoflocally‐producedbioethanol

•Feed‐in‐tariffrateforbiomasswasissuedatP6.63

perKWHbytheEnergyRegulatoryCommission

• Prospects for Cane Expansion Areas - Increasing Farm Productivity• Bioethanol Production• Power Cogeneration• Increased Farm Mechanization Due to LaborSupply Shortage• Sustaining Domestic Requirement andMaintaining World and US Quota Exports

Prospects for Cane Expansion AreasAnd Increase in Productivity

•MostPhilippinesugarmillsareunderu.lizedduetothelackofcanesupply

•Developmentofexpansionareasforsugarcanetosupplythefeedstocks

forbioethanolfuel

•Targetproduc.vity:70tons/hectare;2.1LKg/TCrecoveryatreducedcost

Bioethanol Production

•Thirteenmoredis.llerieswithanannualcapacityof

30millionlitersarerequiredtomeetthevolumerequirement

ofthe10%mandateofbioethanolblend

Power Cogeneration

•Exis.ngpowergenera.ngcapacityofallthesugarmillsinthe

Philippinesis200megawahs;

•Giventherightinvestmentenvironment,theboilersandpower

generatorsofsuchmillscanbeupgradedupto600megawahs

makingavailable400megawahsforpowercogenera.on

•ThePhilippinesiscurrentlyexperiencingpowershortagesand

thepowergeneratedbythesugarmillscouldhelpsolvethe

country’sproblemonpowerdeficit

Increased Farm Mechanization Due to LaborSupply Shortage

•FarmlaborersinthePhilippinesbecamescarceandthe

newgenera.onarenolongerinclinedinfarmingbut

preferredtoworkoverseas

•Theshortageoffarmlabortriggeredtheshiktofarm

mechaniza.oninthePhilippines

Sustaining Domestic Requirement andMaintaining World and US Quota Exports

•ThePhilippineshastobeanetexporterofsugarby2015in

ordertobeintheoffensivemoveratherthanbefloodedwith

importedsugar

•Moreopportuni.esforinvestmentinmill

moderniza.on,infrastructureandfarmandequipmentare

seentoflourishinthePhilippinesgiventheneedtobe

compe..veinworldsugarproduc.on