e Dissertation

85

CHAPTER ONE 1.0 INTRODUCTION Nigeria is facing the twin problem of underdevelopment and stagnant growth rate despite its natural position as a green area with huge resource endowment. It manifests most of the attribut es of sub-Sa haran Africa which has about the large st absolute increase of 72 million people in the last decade. About 70 percent of Nigerians live on less than N100 / day (US$ 0.7/da y), while youth unemployment is close to 90 percent (EZE,2003 ). The country has a large informal sector in which a substantial number of the unemployed take up employment (CBN, 2000a). The poverty syndrome is a bit difficult to understand with Nigeria being the sixth world highest producer of crude oil and earning upwards of US$ 15 billion annually (CBN, 2000b). Regrettably in 2002 alone, 80 percent of the national earning accruing from oil exportation was spent on maintaining the government, leaving only 20 percent for economic development. This partly explains the nature of budgetary 1

Transcript of e Dissertation

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 1/84

CHAPTER ONE

1.0 INTRODUCTION

Nigeria is facing the twin problem of underdevelopment and stagnant growth rate despite

its natural position as a green area with huge resource endowment. It manifests most of

the attributes of sub-Saharan Africa which has about the largest absolute increase of 72

million people in the last decade. About 70 percent of Nigerians live on less than N100 /

day (US$ 0.7/day), while youth unemployment is close to 90 percent (EZE,2003 ). The

country has a large informal sector in which a substantial number of the unemployed take

up employment (CBN, 2000a). The poverty syndrome is a bit difficult to understand with

Nigeria being the sixth world highest producer of crude oil and earning upwards of US$

15 billion annually (CBN, 2000b). Regrettably in 2002 alone, 80 percent of the national

earning accruing from oil exportation was spent on maintaining the government, leaving

only 20 percent for economic development. This partly explains the nature of budgetary

1

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 2/84

problems facing the nation. The question then is, what intervention option besides the oil

sector, does the nation have for sustainable growth?

Nigeria’s overall economic performance since Independence in 1960 has been decidedly

unimpressive. According to World Bank data, the average annual growth rate of Gross

Domestic Product (GDP) between 1960 and 2000 was less than 4 percent. Thus, despite

the availability and expenditure of colossal amounts of foreign exchange obtained mainly

from its oil and gas resources, Nigeria’s economic growth has been weak and the

incidence of poverty has increased. It is estimated that Nigeria received over US$228

billion from oil export receipts between 1981 and 1999 (Udeh, 2000). Yet the number of

Nigerians living in abject poverty- that is, on less than US$1 a day – more than doubled

between 1970 and 2000, and the proportion of the population living in poverty rose from

36% in 1970 to 70% in 2000. Nigeria’s per capita income of US$260 in 2000 is much

less than, indeed it is only one-third of its level, US$780, in 1980, World Bank (2003).

Nigeria faces the challenge of meeting the macroeconomic targets of growth rate and

development. Nigeria is among the world’s 27 poorest countries, according to the United

Nations Development Programme (UNDP 2001). The country has had lost decades of

development due to negative and slow growth and has been one of the weakest growing

economy in the world on a per capita basis especially for the period between 1981- 2000.

In analysing the major macroeconomic targets of growth rate we will be looking at the

aggregate GDP, the manufacturing sector, agricultural sector, the service sector which are

basically the non-oil sector for this particular study. The level of economic development

and growth rate over the decades has been disappointing. The real sector is dominated by

the primary sectors of the economy which has always been the crude oil sector. The

agricultural sector is a predominating sector with a low and declining productivity. This

sector has stagnated and failed to keep pace with the needs of the rapidly growing

population in Nigeria. The crude oil sector is categorised to fall under the primary sector

for which the resources from this particular sector has not been diversified to other

sectors of the economy to enhance growth and development in other sectors. Using a

poverty frontier of US$2 per day, Collier and Dollar (1999:33) reports that 60% of

Nigeria’s population was below the poverty line in 1996. A recent report issued by the

2

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 3/84

Federal Government of Nigeria confirms that the problem of poverty is acute. According

to the report titled “Poverty alleviation policy”. With a per capita income of about

US$300 and a human development index of 0.4, Nigeria is a poor country despite the

abundance of human, material and natural resources. Recent studies show that at least

50% of the population is poor while another 30% may be regarded as moderately poor.

The majority of the poor, over 70%, are located in the rural areas where most of the

people and national resources are located. The paradox of this is that she is ranked the 6th

largest producer of petroleum in the world. Nigeria nevertheless has one of the lowest

GDP per capita incomes: $970 in purchasing power parity-adjusted U.S. dollars.

The secondary sector deals with the manufacturing sector, and the service sector. Themanufacturing sector is one sector of the economy that has classified Nigeria as the least

industrialized countries in Africa. This sector of the economy has been stale and entails

about 5 - 7% of GDP, according to NEEDS report (2004, p.20). In the industrial sector, it

is the role of the manufacturing sector that appears to be the strategic factor in modern

economic growth. ‘Solow stated that development cannot occur without growth (Hall,

1983:19). Thus, the objective of this paper is to analyse the impact of the major various

sectors contributions to economic growth and development, laying more emphasis on the

manufacturing sector, agricultural sector, and the service sector. The Global Research

Project, ‘Explaining Growth’ is an attempt to compile the most comprehensive

assessment of growth in developing and transition countries. Yuba and Suman (2002

p.1). This research work on growth consists of three phases. Phase one of the study

comprises the progression of growth. The current dilemma in understanding economic

development and growth is not just about understanding the process by which an

economy raises its savings rate and boosting the rate of physical capital accumulation, but

'something else’, which captures the differences in economic growth and economic

development, TFP is usually ascribed to as the 'something else', which contributes to the

differential growth rates.

1.1 JUSTIFICATION OF STUDY

3

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 4/84

By the time Nigeria became politically independent in October 1960, the agricultural

sector was known to be the dominant sector of the economy, contributing almost 70% of

the Gross Domestic Product (GDP). But today, the development of this sector tends to be

neglected. In as much as the government has been trying to provide stable growth rate in

the core sectors, the truth still remains that there are lack of distribution of resources for

the development of these non-oil sectors.The major sector contributions to economic

growth in Nigeria, for the purpose of this study will be the economic indicators which are

basically the Consumption expenditure, gross fixed capital formation (GFCF) this will

serve as the gross investments , government expenditure, net exports and lagged variables

of GDP. Over the years, too much attention has been allocated to indicators that do not

have significant impact on GDP in Nigeria. The country’s decade of development plans

has not led to increase growth rate in the non-oil sectors which consist of the

manufacturing industry, service sector and the agriculture industry in country. High

productivity in the non-oil sectors like the industrial, agricultural and the service sectors

are essential for rapid economic growth and development in Nigeria. Transformation in

the relative significance of agriculture, service and industry has been recognized as the

core sectors for the process of growth. In the industrial sector, it is the role of

manufacturing sector that seem to be the significant factor in modern economic growth.

Barro (1990) concludes that the role of public service (infrastructure) creates positive

linkage between government and growth. Barro's work established that there is a negative

correlation between growth in government expenditure and economic growth, as well as

savings rates for governments whose expenditures provide consumption services only.

The role of government in development is a controversial one. Datta-Chandhuri (1990)

notes "the success of Keynesian activism in fighting the great depressions in the western

countries, the success of the Marshall Plan in engineering the quick reconstruction of the

war-damaged economies of western Europe, and the achievements of the Soviet

industrialization drive in the 1930s had created a virtual intellectual consensus in the

world on the power of the "visible hand. There is no doubt that the state has a role to play

in the economic development of a country. The importance of the study therefore lies

4

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 5/84

with the fact that government should pay attention and devote economic resources to the

growth of non-oil sectors. The Nigerian economy should be concerned about policy

implementation that tends to hamper its efforts in development. If the implementation

problem is to be alleviated, it is of paramount significance that the nature of the existing

measures maybe taken.

1.2 AIMS AND OBJECTIVES OF THE STUDY

This dissertation examines Nigeria’s economic growth in three steps. First, it conducts a

straightforward examination of past economic growth trends by looking at the

contributions of the major economic sectors in Nigeria to the GDP which includes the

manufacturing sector, the agricultural sector and the service sector from 1970 to 2005.

Secondly it presents an in-depth literature on economic growth which explains the

determinants of growth. The review takes into consideration both theoretical and

empirical literature on growth which are considered as important determinants of growth.

Thirdly it also aims at identifying which components of growth is the most important

determinant of economic growth in Nigeria by regressing the GDP of Nigeria against the

following independent variables: Consumption expenditure, gross fixed capital formation

(GFCF) this will serve as the gross investments , government expenditure, net exports

and lagged variables of GDP. The statistical aggregate of GFCF is a measure of the net

investment by enterprises in the domestic economy. This usually comes in as fixed

capital assets during an accounting. Due to data availability GFCF is used in place of

gross investment, this is due to the fact that GFCF time series is often used to analyse the

trends in investment activity over time. These variables are considered because they are

readily available and form the core components in econometric studies of this kind. This

research therefore reveals how important the traditional determinants of growth

(consumption expenditure, gross fixed capital formation, government expenditure and net

exports) as used in the study and variables on how investments on the GDP dependent

variable will greatly influence or impact economic growth rate in Nigeria. The GDP of

Nigeria is used as a proxy for economic growth. This study is carried out econometrically

using both univariate and multivariate regression techniques. GDP (the dependent

5

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 6/84

variable) is regressed on all the independent variables indicated above for the period 1970

to 2005.

1.3 SIGNIFICANCE OF THE STUDY

This study is significant for various reasons; firstly the study provides an insight into the

determinants of economic growth and development which enriches the existing literature

on the topic by exploring some of the most recent literatures on economic growth and

applying it to the Nigerian economy. Secondly the study on the sectoral contribution to

economic growth in Nigeria will give an insight of which sectors of the Nigeria economy

will dominate in attracting economic growth and development. The results obtained from

this agenda can assist the Nigeria government in the country’s economic policy to

attracting growth and development and as well help in addressing what measures can be

taken in boosting economic growth and development.

1.4 ORGANISATION OF THE STUDY

Chapter two reviews the relevant literature on the subject under study. This chapter looks

at the determinants of growth, outlines and explains the factors that attract growth to a

country. Chapter three comprises the research methodology as well as the econometric

model to be used in the empirical analysis. Chapter four gives an overview of the overall

assessment of the Nigeria economy. This chapter outlines the economic performance of

the Nigeria economy. In chapter five the actual test is conducted and the results

discussed. Chapter six concludes the study and tenders some policy implication for

boosting growth in Nigeria.

6

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 7/84

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

The literature on the analysis and contributions of economic growth and development is

vast and inconclusive. Many economists and other social scientists would say that drives

to develop are present but are masked by current political structures and organisation

barriers. Many theories have been developed by economist over the years to explain

economic growth and development. These usually try to identify what the determining

factors that contribute to growth and development are. Nevertheless this literature

remains one of the most researched with respect to development and growth. The

importance of the economic growth and development can hardly be over-emphasized.

The likes of Hamilton (1995) were of the opinion that economic growth is unsustainable,

if the elasticity of substitution between exhaustible resources and reproducible capital is

7

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 8/84

less than unity. Growth can be regarded as one of the mainstays of a modern economy. It

is challenging for any researcher to point at a particular set of theory or determinants

which contributes to economic growth and development. In this chapter an extensive

review of the literature relating to the application of economic growth and development,

sources of economic growth by explaining the use of GDP in Nigeria as a proxy for

economic growth which accounts for national income in an open economy such as that of

Nigeria, sectoral contributions and their impacts to GDP is reviewed. This dissertation

empirically assesses conflicting views that retards various factors to economic growth.

The approach complements the growth literature, which examines the relationship

between the level of development and economic growth. This study adds to a large

policy-oriented literature on the relationship between economic development and growth.

This paper highlights some policy approach that will boost the Nigerian economic

performance.

2.1 DETERMINANTS OF ECONOMIC GROWTH

Understanding the growth process is central in the context of development economics;

while theory is useful to streamline guidance for identifying, analysing and interpreting

the determinants of growth. Most of the empirical literature is actually based on cross-

country growth regressions, which are seen as being useful in identifying those factors

that most consistently appear to be important determinants. The existing studies of

determinants of growth can be grouped into several categories, there are studies which

focused on the explanation of Output growth of an economy can be attributed to many

reasons. Technological progress, capital accumulation, employment growth and

institutional change are attributed to be driving forces of economic growth. Levine and

Renelt (1992) and Sala-i-Martin (1997) identify investment as a key determinant. High

investment ratios do not necessarily lead to rapid economic growth; the quality of

investment, its productivity, existence of appropriate policy, political, and social

8

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 9/84

infrastructure are all determinants of the effectiveness of investment (Hall and Jones,

1999; Fafchamps, 2000; Artadi and Sala-i-Martin, 2003). Investment in general is

often seen as the engine that drives a country’s economy; Investment can be classified

into public and private investment. Public investment provides the necessary

infrastructure that is need for the economy while private investment is the driving force

that spins the economy. Public investment can affect growth either directly, through

productivity, or indirectly through the effect on private investment. Public investment in

human capital, law and order, research and development, and social and economic

infrastructure leads to creation of positive externalities which in turn improve the

productivity of private investment. One of the principal determinants of growth necessary

for any takeoff is the mobilization of domestic and foreign saving in order to generate

sufficient investment to accelerate economic growth. The growth mechanism by which

more investment leads to more economic growth can be described in terms of the Harrod-

Domar growth model. Every economy should be able to save certain proportion of its

national income in order to be able to replace worn out or impaired capital goods.

However in order to grow, new investments representing net additions to the capital stock

are considered important. Every good economy’s growth rate should greatly depend on

the level of savings, the savings ratio and as well the productivity of investment. Thus,

one would expect a positive relationship between public investment and economic

growth (Barro, 1991, 1996, 2003; Artadi and Sala-i-Martin, 2003). Conventional

macroeconomic policies such as government investment can greatly affect the level of

per-capita income but they have no effect on the long run growth rate of the economy

Barro (1991), Mankiw et al. (1992) and Barro and Sala-i-Martin (1992).

Kaipornsak (1995) studied the source of economic growth and found that spending on

R&D, especially government expenditure, and the degree of openness with the emphasis

on FDI were major factors.

Another factor that is related to investment is foreign aid. In theory, foreign aid could

relax any or all of three constraints on investment (Bacha, 1990). The constraint on

savings give rises to low-income countries, domestic savings are not sufficient to meet

the requirements of the general investment as a whole. There are constraint which

9

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 10/84

captures the possibility that government reactions can affect private savings and public

investment and this can affect investment. Chenery and Strout (1966) also posit a

knowledge gap in developing countries and foreign aid in the form of technical assistance

can relax this constraint (and increase productivity). If foreign aid is used to relax these

constraints it is expected to be positively correlated with investment and growth

(Hjertholm et al, 2000). Elbadawi (1999) argues that the African foreign aid causes

exchange rate appreciation thereby dampening growth of exports and thus economic

growth. Foreign trade is one major variable that influences private investment and

ultimately economic growth.

According to neoclassical thinking, openness to trade has many advantages such as

efficiency gains that come with specialisation and competition from international trade;

embodied technological transfer through imported inputs; scale economies arising from

expanded markets, and diffusion of ideas through global interaction (Piazolo, 1995;

Zhang and Zou, 1995; Harrison, 1996; Frankel and Romer, 1999). The literature on

trade and growth tends to mainly pay attention on exports, there are two justifications for

concentrating on imports – they represent imported technology, capital, and intermediate

goods and to some extent they can be used directly for investment. Michaely (1977)

tested the hypothesis "that a rapid growth of exports accelerates the economy's growth of

a country." Balassa (1985) concluded that "trade orientation has been an important factor

contributing to inter-country differences in the growth of output. Dornbusch and

Reynoso (1988) concluded that there was no evidence to attribute rapid development of a

country to financial liberalization alone. Tyler (1981) argues that the dramatic economic

success of some countries pursuing export oriented policies, along with the equally

dramatic failures of those countries pursuing autarkist policies, has provided examples

necessitating a reexamination of the role of international trade in the development of poor

countries. Thus, he concluded that countries which neglect their export sectors through

discriminatory economic policies are likely to have to settle for lower rates of economic

growth as a result.

2.2 A BRIEF HISTORY OF GROWTH THEORIES AND EMPIRICS

10

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 11/84

Studies conducted on growth theories draws back to Adam Smith’s (1776) An Inquiry

into the Nature and Causes of the Wealth of Nations may be seen as a suitable starting

point for economic growth theories. In Smith (1776), not only capital accumulation but

also technological progress and institutional and social factors play a crucial role in the

economic development process of a country (Kibritcioglu, 1997). Smith distinguished

between three different stages of economic growth. In his own view, some nations were

at “a low level equilibrium trap” because of “bad-governance” and an insufficiency in

maintaining common human rights and freedoms or “property rights” in modern

parlance. This, stated was due to cultural and institutional backwardness of these

countries.

Developed nations in his time were England and North America but they were only at the

second stage of development. They were still in a “natural freedom” environment, and

therefore, in an ongoing economic growth process. Smith believed that no country in the

18th century was rated at the third stage of economic growth. According to his view, the

natural environment limits economic growth beyond a certain level. Falling profit rates

along with the growth path of an economy gives way to changes in the relative factor

scarcity and decreases in profitable investment opportunities all play a role in

constraining economic growth. Thus, every developing economy had to slow down and

stop at an upper limit of development. The notion of an upper limit to growth is perhaps

related to the agrarian based economy of Smith’s age. As a corollary of the model,

government policies can affect the long-run growth rate of real output in an economy.

The standard neoclassical growth model implies that the steady state growth rate, aside

from exogenous technological progress, is zero.

In this case our focus is to find the statistically significant relationship between GDP and

some economic indicators in Nigeria. Theories of growth are highly aggregated usually

featuring only one or two types of output and a limited number of inputs. Exogenous

growth models that have focused primarily on the role of factor accumulation in the

growth process, as well as endogenous growth models given examples from Romer

1990, Grossman and Helpman 1991, and Aghion and Howitt 1992 have devoted their

11

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 12/84

attention to the role of endogenous technological progress in the process of development,

were designed to capture the main characteristics of the Modern Growth Regime. These

models are however not consistent with the pattern of development that had characterized

economies over most of human existence. Most endogenous and exogenous growth

models are not consistent with the changes in the demographic regime along the process

of development.

2.3 FACTORS THAT ATTRACTS GROWTH TO A COUNTRY

The kind of factors which attracts any form of growth and development to a country

differs. To disentangle the sources of economic growth one needs an analytical

framework to assess the contribution of various factors to growth. This involves the

formulation of theories, models and hypotheses on the role of accumulation, productivity

and technology. In the last decades this has been the concern of economists and economic

historians; however there is no consensus on what emphasis that should be given to the

key factors behind growth. The significance of economic growth involves as follows; the

role of investment as a form of foreign investment, technological progress and financial

development.

One of the factor economists anticipate is that financial integration will lead to more

investment with a progress on more efficient allocation of capital. Increase in investment

is expected because of financial integrated markets. Financial integration is not an end in

itself but rather a means to achieve higher economic growth. Greater investment and its

more efficient allocation are the two principal channels through which financial

integration will lead to growth. The prevailing view in economics is that financial

development contributes greatly to growth in various ways. Economists have found

empirical evidence that countries with developed financial systems tend to grow faster

and rapidly. King and Levine (1993) pointed out that early literature tried to explain that

growth is positively related to the level of financial development. Given evidence from

80 countries from 1960 to 1989, they show that the relative size of the financial sector in

1960 is positively correlated with economic growth over the period. However, positive

12

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 13/84

correlation may simply reflect the fact that faster and rapidly growing countries have

larger financial sectors because of the increase in the number of financial transactions

conducted. Subsequent work using statistical techniques to control for the endogenous

effect of economic growth on financial development as well as for country-specific

factors that are not explicitly considered, and using both time series and cross-sectional

data to extract more information from the data, has analyzed this information more

efficiently. In addition, once a project has started, they can better monitor its managers to

the effect of financial development is robust (Levine, Loayza, and Beck 2000,

Benhabib and Spiegel 2000).

2.4 EVIDENCE FROM SOME SELECTED EMPIRICAL STUDIES

Studies on the contribution to economic growth have been studied differently in past

research. These studies have been conducted at inter country level. Inter country studies

gives an insight on the pattern of growth varies across nations in terms of their different

characteristics. In this section we review briefly some of the findings conducted on

growth rate simply because this study is interested in estimating the determinants of

growth of which sectoral investment is likely to have a positive effect on GDP growth.

The benefit of these studies is that it helps developing countries to formulate good

policies which help to attract growth and development.

The pioneer work in this regard is the work of Lucas (1988) which explained that the

growth rate of human capital is also dependent on the amount of time, allocated by

individuals to acquire skills found out that time investment positively the growth rate of

human capital. Rebelo (1991) using the time investment as a proxy for growth rate

human capital yielded the same result but later extended the model by introducing

physical capital as an additional input in the human capital accumulation function.

However, the model of endogenous growth by Romer (1990) assumes that the creation

of new ideas is a direct function of human capital, which manifests in the form of

knowledge. As a result investment in human capital led to growth in physical capital

which in turn leads to economic growth. Other studies that supported the human capital

accumulation as a source of economic growth include (Barro and Lee, 1993; Romer,

13

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 14/84

1991; Benhabib and Spiegel, 1994). Some studies have examined different ways

through human capital can affect economic growth, however recent studies on growth

factors such as human growth accumulation influence the determinants of growth have

been diverse from one research to the other. Gupta and Chakraborty (2004) developed

an endogenous growth model of a dual economy where human capital accumulation is

the source of economic growth. Bratti et al (2004) estimated a model of economic

growth and human capital accumulation based on a sample of countries at a different

stage of development. Based on this identification of structural constraints to growth and

development, it is not surprising that a major part of colonial economic policies was

devoted to tackling some of these, even if in obviously inadequate terms. It was that need

to reduce the fragility of the economy and hasten structural change that informed early

post-independence development strategy (World Bank 1993). Although the techniques

employed in past studies seem to be accurate, one cannot concretely point at what

particular factors that determines economic growth and development in a country. At best

these studies give a general idea of what determines economic growth and development.

CHAPTER THREE

NIGERIAN ECONOMY: AN OVERALL ASSESSMENT

3.0 INTRODUCTION

This chapter is aimed at presenting an overview of the economic performance of the

Nigeria economy from 1970 to 2005. This chapter provides a brief overview of Nigeria’s

key development challenges in order to provide a basis for assessing contributions to the

nation’s development priorities during this period (1970-2005). Nigeria is a relatively

large nation of considerable wealth, it has a rich natural resource endowment and

relatively high levels of human and social capital. Notwithstanding its wealth and

considerable economic potential, Nigeria has not as yet succeeded in effectively

translating its potential into economic growth, human development and overall social

14

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 15/84

transformation. This chapter reviews the Nigerian economy by focusing on the

contributions of the major sectors to GDP.

3.1 THE STRUCTURE OF THE ECONOMY

An analysis of the structure of the Nigerian economy is fundamental for comprehending

the predominance of poor economic growth and development in the country. During the

period of independence in 1960, the backbone of the national economy relied primarily

on agricultural sector. The agricultural sector accounted for more than half of its national

output between 1950 and 1960. The attraction drawn to the agricultural sector was later

diverted to the oil sector, which became a major source of revenue. The oil boom

transformed the economy drastically. The economy became absolutely dependent on the

oil sector, which accounted for more than 98 per cent of export earnings. From table 3.1

below, the manufacturing sector has experienced rather sluggish growth since around

1970, while the services sector appears to have had persistent growth interrupted only by

the economic recession of the 1980s. The agricultural sector has experienced a general

improvement in a portion of GDP since 1985, over the incessant increase from 26.6 to

about 40.8 in 1990. Over the same period, oil and mining fell to about 14 per cent of

GDP, while infrastructure and services appear to stabilize at lower levels of about 9 per

cent and 28 per cent, respectively, between 1987 and 1990.

Table 3.1 Distribution of gross domestic product in Nigeria for selected years (%)

(1960-1990)

Sector 1960 1965 1970 1975 1980 1985 1987* 1990

Agriculture 64.1 55.4 44.7 26.5 21.1 26.6 40.2 40.8

Mining 1.2 4.7 11.9 23.9 24.1 19.8 13.4 13.8

Manufacturing 4.8 7.0 7.5 4.5 8.9 9.3 9.7 8.5

Infrastructure 8.9 10.4 9.1 15.4 17.6 12.8 8.0 8.6

Services 21.0 22.5 26.8 29.7 28.3 31.5 28.7 28.3

Total 100 100 100 100 100 100 100 100

Value (Nm) 2 493.4 3 146.8 4 219.0 26 283.3 30 808.3 26 159.0 79 270.0 89 100.0

15

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 16/84

Source: Central Bank of Nigeria. Annual Report and Statement of Accounts,

Various Issues

Analysing one the recent work of the Central Bank of Nigeria (CBN, 2000) highlights

most of the structural issues in perspective, with supporting data as evidence. Agriculture

dominates the Gross Domestic Product (GDP), but its contribution has reduced gradually

over the years since the accomplishment of political independence in 1960. This ratio

drastically dropped from 64.1% in 1960 to 28.35% in 2002, this is detailed in the table

above. An economy that experiences rapid and sustained growth that is not less than 6–

10% per annum at the end of the present Administration’s tenure, the creation of a

national economy that is highly competitive, responsive to incentives, private sector–led,

broad-based, diversified, and market-oriented and open, but based on internal momentumfor its growth is the aim. (Nigeria, Ministry of Finance 2000c, pp. 8–9)

3.2 GENERAL PERFORMANCE OF THE ECONOMY

The Nigerian economy has had a truncated history. Between the period of 1960 and 1970,

the Gross Domestic Product (GDP) recorded was 3.1 per cent growth annually. During

the oil boom era, which was in the period of 1970 to 1978, GDP grew positively by 6.2

per cent annually; this signified a remarkable growth. In the period of 1980s, the growth

rate of GDP dropped negatively. Between the periods of 1988 to 1997, the GDP

responded positively at a rate of 4.0, this period was a period there was economic

adjustment policy which is known as the structural adjustment and economic

liberalization. After independence, the industry and manufacturing sector had a slowly

positive growth rate given exception for the period of 1980 to 1988, during this time

frame of the two periods, the industry and manufacturing sector grew negatively by 3.2

per cent and 2.9 per cent respectively. The growth rate for the agricultural sector for the

periods 1960 to 1970 and 1970 to 1978 was unsatisfactory. In the early 1960s, the

agricultural sector declined in low commodity prices while the oil boom contributed to

the negative growth of agricultural sector in the 1970s. The services sector includes

wholesale and retail trade, real estate, government services, transportation, financial,

16

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 17/84

communication, hotels and restaurant services. According to Nigeria Bureau of Public

Enterprise (BPE 2000) the three highest contributors to Nigeria’s GDP are agriculture

(34.62%), oil (33.44%) and Service (12.45%).

3.3 AN OVERVIEW OF THE AGRICULTURAL SECTOR

Agriculture is the backbone of the rural economy, generating more than 30 percent of

gross domestic product (GDP) and so far has provided the largest source of rural

employment. Before the outbreak of the Second World War, the Nigerian economy was

still largely dominated by peasant agriculture (Helleiner, 1966) albeit with a small and

active export enclave. It was an open economy (Kilby, 1969); exporting agricultural

products and importing manufactured ones.

The empirical work will attempt to improve on the recent results on the sources of

economic growth in Nigeria reported by Iyoha (2000b).

Growth in Nigeria’s agricultural sector, seen as attaining better than the growth achieved

in many other African countries, has fallen short of expectations. Value added per capita

in agriculture has accelerated by less than 1 percent per year for the past 20 years, from

analysis states in past years, food production supply have not kept pace with population

growth, this is as a result in increase of food imports and a decline rate of national food

self-sufficiency. Blessed with abundant land, natural resources and water resources,

Nigeria’s agricultural sector has a high potential for growth, but this potential is not been

actualized. Productivity is very low and basically stagnant. Most of the agricultural

policies that have established have been ineffective, either because they have been

misguided, or for a reason that their impacts have been swamped by macro policies

affecting inflation, exchange rates, and the cost of capital. The rapid expansion of the oil

sector has also played so much eroding the competitiveness of agriculture, due to the fact

that successive governments have chosen the easy path of depending heavily on earnings

from oil exports rather than making the investments needed to diversify the economy by

maintaining productivity growth in agriculture and other non-oil sectors. The largely

subsistence agricultural sector has not kept up with the rapid population growth in recent

times. Nigeria once a big net exporter of food has now become an importer of food.

17

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 18/84

Agriculture was the backbone of the economy at the time of independence in 1960s.

Nevertheless, due to over-dependence on oil, its contribution to national revenue declined

from 64.1 per cent in 1960 from table 4.1 to 28.35 per cent in 2002 from table 4.2 below.

This was known to be the economy’s booming sector and people’s main source of

livelihood along with its contribution to GDP. Agriculture, if given direct attention and

improved on will remain the major contributor to GDP.

There are several major reasons which are defined for the declines in production of

agricultural products in the agricultural sector are noted as follows:

• Deterioration in rural infrastructure.

• Lack of working capital for agricultural boost.

• Low rate of adoption of high technology.

• Poor post-harvest technology.

• Environmental degradation.

• Premature liberalisation and deregulation.

• Lack of proactive pro-farmer food pricing.

• High cost of farm inputs.

• Poor distribution of fertilizer.

• High population growth.

3.3.1 CONSTRAINTS TO INADEQUATE AGRICULTURAL PRODUCTION IN

NIGERIA

There is inadequate empirical analysis of the real problems situations facing agricultural

production in Nigeria. Problem identification will be beneficial to agricultural policy

makers, the extension agents, the researchers and the peasant farmers. Basic

understanding of these problems and the ability to plan in advance will help immensely to

accelerate agricultural production and pave the way for effective management of both

agricultural inputs and outputs in Nigeria.

According to Nwosu (1980:143), Ogunfiditime (1996), the major constraints on

agricultural production in Nigeria include:

18

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 19/84

A. Shortage of capital which includes shortage of credit facilities, farm

infrastructure, transport services, and high cost of production etc;

B. Shortage of qualified manpower in key areas

C. Inadequate supplies of agricultural inputs

D. Inadequate or lack of effective supporting services such as farm credit

to genuine farmers, marketing facilities, etc

E. The poor condition of feeder roads and other transport facilities

F. Management oriented problems such as the problem of land ownership, land and

water management, crop management, energy management problem, inadequate

farming systems, etc. Our land tenure system inhibits investment, expansion,

effective utilization and increased food production. There is need to allow small

farmers to have more access to land in order to boast their output;

G. The problem posed by increasing labour shortage in the rural areas in

consequence of rural urban migration;

H. The problem of diseases and pest control

I. Nature oriented problems like drought, desert encroachment, as lack of

dependable water resources constitutes an obstacle to agricultural productivity.

J. Problem of Technology. There is need to develop and encourage appropriate

technology for rapid development of the agricultural sector.

K. Inappropriate policies by government. There is need for sustainable policy

towards favourable conditions for farmers.

L. Neglect of irrigated agriculture

M. The instability in the price of agricultural products discourages farmers.

At the micro-economic level, Nigerian agricultural policy in the 1970s can be criticized

for its deficiencies in three key areas: (i) failure to encourage private price-setting and

marketing channels, (ii) failure to ensure a workable agricultural credit system, and (iii)

failure to provide necessary infrastructure and thus an enabling economic environment to

support provision of key services like machinery maintenance, repair and spare parts to

farmers.

Iyoha and Oriakhi (2002)

19

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 20/84

3.4 OIL SECTOR

The Nigerian oil sector can be categorized into three main sub-sectors, namely, upstream,

downstream and gas. The most uncertain over the years has been the downstream sector,

which demonstrates the distribution arm and association with final consumers of refined

petroleum products in the domestic economy.

According to Vincent Nwanma and Norval Scott Dow Jones Newswires (2004).

Nigeria is raking in the cash from the high prices of its crude-oil exports. But the country

is in a bind: Because of inadequate refining capacity, it has to import gasoline which it

sells at subsidized prices. Now, it faces rising bills to cover the costs. Although it is the

fifth-largest supplier of crude oil to the U.S. and the 12th largest world-wide, Nigeria is

saddled with a dilapidated infrastructure and little economic development outside the oil

sector. Its four refineries, with a total capacity of 438,750 barrels a day, have lasted for

the past 30 years old. Because of their age and poor maintenance, it operates at around

100,000 barrels a day. This embraces less than half of Nigeria's gasoline requirement of

around 250,000 barrels a day meaning it has to rely on imports. According to a journal

by Bureau of Public Enterprises Oil and Gas Investments in Nigeria Conference

(2002 p 4-7). Oil accounts for 40% of GDP, 70% of Government revenue and 95% of

foreign exchange earnings. Production level is about 2.2million bpd and 2 billion cubic

feet per day

TABLE 3.2 NIGERIA GAS SECTOR AND GDP

OPPORTUNITIES AND BARRIERS

THE POTENTIAL

● World’s 7th largest gas reserves=

184 TCF

● Significant gas reserves upside

5 BARRIERS

● Pricing

● Fiscal Terms

20

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 21/84

● No dedicated gas exploration to

date

● High grade gas quality – 0%

Sulphur; rich in liquids

● Institutional/Infrastructural

Arrangements

● Legal and Regulatory Framework

● Financing

Source: Nigeria National Petroleum Corporation, (NNPC) 2006

3.5 SERVICE SECTOR

The Service sector is a wide sector and can be classified as part of the Nigerian economy

which embrace most informal and many formal enterprises. In analysing the Nigerian

various sectors, services account for 24 percent of the GDP. The informal service sector

consists of small-scale enterprises that rely on family labour, including traders,

hairdressers, entertainers, porters, tailors, auto mechanics, restaurants, hotels, retail trade

and wholesales. Other services are provided by formal-sector entrepreneurs that include,

law offices, banks, and travel agencies, financial intermediaries, real estate, renting and

business activities, transport, storage, communication, government and other services.

High productivity in industrial, agricultural, oil and the service sectors are essential for

rapid economic growth and development in Nigeria. Transformation in the relative

significance of agriculture, service and industry has been recognized as the core of the

process of growth.

3.6 INDUSTRIAL SECTOR

The increased revenue from oil aided to speed up the rate of industrial development, but

the fall in the global price of oil in the mid-1980s created a shortage of the foreign

exchange needed to acquire raw materials. The industrial sector has performed dismally

in the last century. In the industrial sector, it is the role of manufacturing sector that seem

to be the significant factor in modern economic growth. The manufacturing sector

21

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 22/84

compose a range of goods that included milled grain, vegetable oil, meat products, dairy

products, sugar refined, soft drinks, beer, cigarettes, textiles, footwear, wood, paper

products, soap, paint, pharmaceutical goods, ceramics, chemical products, tires, tubes,

plastics, cement, glass, bricks, tiles, metal goods, agricultural machinery, household

electrical appliances, radios, motor vehicles, and jewelleries.

Between 1982 and 1986, Nigeria's value added in manufacturing fell 25 percent, this is

due to the effect of inefficient resource allocation caused by distorted prices most

importantly for exports and import substitutes and prohibitive import restrictions. Often,

the manufacturing sector is characterized by increasing returns to scale and positive

externalities. A decrease of the manufacturing sector further decreases the productivity

and profitability of investments, accelerating the decrease in investments (Sachs and

Warner 1995, 1999a, Gillis et.al 1996, Gylfason 2000, 2001a). Other reasons for the

poor performance of manufacturing enterprises include poor investment phase

preparation, (inadequate feasibility), lack of adequate techno managerial skills for

investments production and maintenance, misuses of monopoly powers, poor

capitalization resulting in inadequate working capital, defective capital structures

resulting in heavy dependence on government for the operation, bureaucracy in their

relations with supervising ministries, mismanagement, corruption and nepotism.

(Oyelaran-Oyeyinka et al, 1997). The following reasons account for the fall in the

performance of the manufacturing sector:

• Low capacity utilisation.

• A collapse in the world market price of oil, creating shortages of the foreign

currency required for importing raw materials and capital goods.

• Obsolete equipment and machinery.

• Inadequate infrastructure.

• Implementation of inappropriate economic policies, such as high interest-rate regimes and inflationary financing.

• Liberalisation and deregulation of the economy.

3.6.1 PERFORMANCE OF THE MANUFACTURING SECTOR

22

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 23/84

The performance of the manufacturing sector was unprepossessing, even appalling,

within the sub-period, exclusively between 1995 and 2000. This weak performance was

perhaps has not expectedly given the unclear macroeconomic and policy environment in

Nigeria. During the 1996-2000 periods, overall growth of real gross domestic product

(GDP) was unimpressive, ranging between 2.4% and 3.8%. See Table 3.2 below for

selected macroeconomic indicators. The early period of independence till the mid-1970s

brought about a rapid growth of industrial capacity along side with output, as this denotes

the contribution of the manufacturing sector to GDP which rose from 4.8% to 8.2%. This

structure was altered when crude oil suddenly became imperative and important to the

world economy through its supply-price nexus, as shown in the table below

Table 3.3 NIGERIA: SECTORAL CONTRIBUTION TO GROSS DOMESTIC

PRODUCT (GDP)

SECTOR 1960 1970 1980 1990 2000 2002

Agriculture 64.1% 47.6% 30.8% 39.0% 35.7% 28.35%

Manufacturing 4.8% 8.2% 8.1% 8.2% 3.4% 5.5%

Crude Oil 0.3% 7.1% 22.0% 12.8% 47.5% 40.6%

Others 30.8% 37.1% 39.1% 40.0% 13.4% 25.55%

Source: Central Bank of Nigeria, Changing Structure of the Nigerian Economy (2000)

and Annual Report & Statement of Accounts (2002).

As manufacturers are required to invest huge capital funds to provide alternative

infrastructural facilities for their operations, domestic industries carry high cost/price

structure which results in loss of competitiveness for their products in both the domestic

and foreign markets. Hence, manufacturing capacity utilization rate has fallen from an

23

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 24/84

average of over 70.0 percent for the period 1975-80 to about 30.0 percent during 1996-

1998, owing to infrastructural failures and other

endemic problems of the economy, CBN (2000, p. 46).

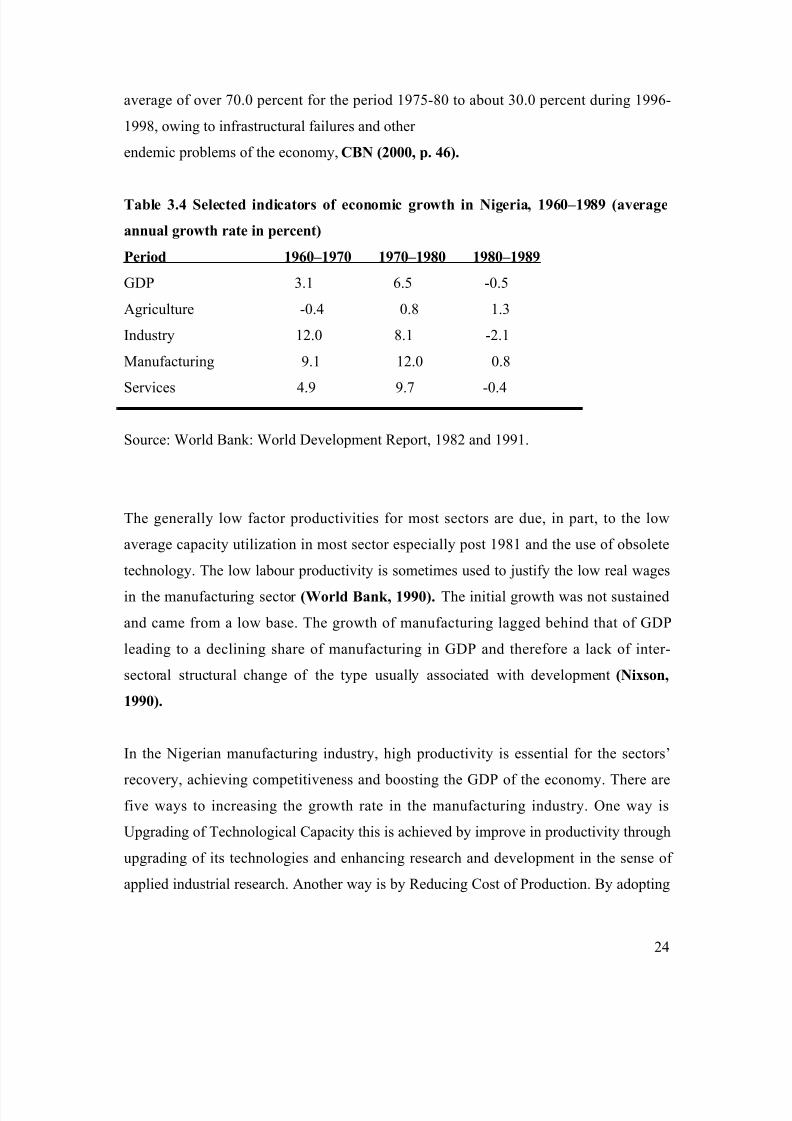

Table 3.4 Selected indicators of economic growth in Nigeria, 1960–1989 (average

annual growth rate in percent)

Period 1960–1970 1970–1980 1980–1989

GDP 3.1 6.5 -0.5

Agriculture -0.4 0.8 1.3

Industry 12.0 8.1 -2.1

Manufacturing 9.1 12.0 0.8

Services 4.9 9.7 -0.4

Source: World Bank: World Development Report, 1982 and 1991.

The generally low factor productivities for most sectors are due, in part, to the low

average capacity utilization in most sector especially post 1981 and the use of obsolete

technology. The low labour productivity is sometimes used to justify the low real wages

in the manufacturing sector (World Bank, 1990). The initial growth was not sustained

and came from a low base. The growth of manufacturing lagged behind that of GDP

leading to a declining share of manufacturing in GDP and therefore a lack of inter-

sectoral structural change of the type usually associated with development (Nixson,

1990).

In the Nigerian manufacturing industry, high productivity is essential for the sectors’

recovery, achieving competitiveness and boosting the GDP of the economy. There are

five ways to increasing the growth rate in the manufacturing industry. One way is

Upgrading of Technological Capacity this is achieved by improve in productivity through

upgrading of its technologies and enhancing research and development in the sense of

applied industrial research. Another way is by Reducing Cost of Production. By adopting

24

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 25/84

strategic planning is one way of minimising costs and boosting productivity in the

manufacturing sector. The third way is by Increasing Investments. Increase in

investments will yield a high growth rate and high productivity in the manufacturing

sector. The fourth method is by Reducing Dependence on Imports. Reducing dependence

on imports for industrial goods will contribute a lot in reducing cost in the long-run and

boosting productivity in the manufacturing sector. Finally there should be Rehabilitation

and Development of Infrastructural Facilities. The Government should give priority

facilities that will contribute or facilitate industrial operations, such as

telecommunication, transportation services, Power supply and water supply. Good

working framework increases productivity in the manufacturing sector and reduces

production costs.

3.6.2 PRODUCTIVITY IN THE NIGERIAN MANUFACTURING INDUSTRY

Perhaps owing to the complexities involved in constructing productivity index, there is

little or no data on productivity levels in the Nigerian economy in general and the

manufacturing sector in particular. Ad hoc studies conducted during 1989 indicated that,

on the average, there was little rise in productivity (Enisan and Akinlo, 1996). Oshoba

(1989) study on food and basic metal industries, only 30 per cent of respondents

indicated they had rising productivity. About 11 per cent recorded no growth, while more

than half, 57 per cent, recorded declining productivity levels. The Manufacturers

Association of Nigeria (MAN) acknowledged the general trend in productivity in the

industrial sector was proved negative in 1989. Since then it’s been indicated that the

situation has been worsened ever since then. Growth rate in the Industrial was relatively

high in the period 1960-70 at an annual average of 12.0 per cent. This demonstrated the

significance at which the government attributed to manufacturing activities and the

adoption of import substitution industralisation strategy from independence which was as

a result in the establishment of many consumer goods industries, including soft drinks,

cement, paints, soap and detergents. However, the manufacturing output growth cut down

drastically to an annual average of about -2.1 per cent during the period 1980-89. This

negative trend in the performance of manufacturing production indicates falling

productivity in the sub-sector.

25

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 26/84

3.6.3 INCESSANT PROBLEMS IN THE MANUFACTURING SECTOR

High productivity in the Nigerian manufacturing sector has been accountable to many

factors which include the following:

(a) Low Level of Technology: This is considered to be the greatest impediment

constraining productivity in the sub-sector as advancement in technology and innovations

are the fundamental forces propelling industrialization in recent times. Technology has

brought about easy processes and procedures of carrying out jobs and automation have

revolutionalised the manufacturing industry. Industries in Nigeria cannot secure the use

of modern machines in order to reduce processes. Most machineries used especially for

textiles, cement, bakery, leather, paper production and many others are all being

produced with machineries procured in the 1960s and 1970s, giving rise to frequent

breakdown and reduction in capacity utilization rates. Low technology is accountable for

the inadequacy for local industry to be able to produce capital goods such as raw

materials, spare parts and machinery, the bulk of which are imported.

(b) Low Level of Investments: The level of inadequacy of funds makes it difficult for

firms to invest in modern machines, information technology and human resources

development which are vital for reducing production costs, raising productivity and

improving competitiveness. The level of low investments has been traced immensely to

the financial sector mainly the indisposition to make credits available to manufacturers.

Nevertheless, banks acknowledge manufacturing as a high risk venture in the Nigerian

environment, hence banks prefer to lend to low-risk ventures, such as commerce, that

have high returns.

(c) High Cost of Production: Since the introduction of Structural Adjustment

Programme SAP (of which its major objectives were, to; restructure and diversify the

productive base of the economy so as to reduce dependency on the oil sector and imports;

achieve fiscal and balance of payments viability over the medium term; and to promote

non-inflationary economic growth), high and increasing cost of production has been

recorded by most firms as a main constraint on their operations. High cost are traced

largely to poor performing infrastructural facilities, high interest and exchange rates and

diseconomies of scale, which has developed into increased unit price of manufactures,

26

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 27/84

low effective demand for goods, liquidity squeeze and fallen capacity utilization rates.

(d) Inflation: This can be described as persistent increase in the general price level. It

creates a disincentive to for future saving use and also retards investments and growth. It

also encourages speculative activities thereby diverting resources from productive

ventures.

(e) Poor Performing Infrastructure: Poor performance of infrastructural facilities, are

characterized by frequent interruption in power supply, water supplies and inconsistency

in telecommunication systems and transportation systems. These poor performances have

a negative effect on productivity.

3.7 WHY THE PAST FAILURES?

According to Professor Kilby, who suggested great majority of underdeveloped countries

will have to place major emphasis upon import replacement if they wish to increase the

extent of their industrialization, Bauer (1991, p.133). The government used the old

development models of import substitution industrialization and this postulated the

government as the dictator, producer and controller in the economy which had affected

abnormal incentives, inefficiencies and waste. There was an inappropriate development

framework, poor and frequently changing policies and programmes, lack of clear

development vision and commitment to the Nigerian project. Nigeria's vast oil wealth,

was bankrupt by corrupt rulers in the past, is now unable to payoff foreign debts and

rebuilds the country. According to Gordon (1992), Nigeria has a national debt of $32

billion, compared with a Gross Domestic Product of $21 billion. The Nigerian debt came

when the price of oil crashed in the 1980's. Nigeria is depended on oil exports for 95% of

its foreign exchange. The price of oil escalated in the 1970's where the economy boomed

and afterwards the price of oil fell. There was a neglect of the agricultural sector by mid

1980s and this contributed to the origin of our economic problem. Bauer(1991, p.122)

analysed that industrialization in the sense of state support for manufacturing activity has

been a major plank of development policy and planning in many less developed

countries’ Manufacturing is a subset within the industrialization matrix and the

manufacturing sector in Nigeria has been facing many problems over the years. All these

contributed to the major causes of Nigeria’s failed past. In Nigeria the history of

27

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 28/84

industrial and manufacturing development is a classic illustration of how a country could

neglect a vital sector through policy inconsistencies. The neglect of the agricultural sector

has further denied manufacturers and industries their basic source of raw material and

this has to a shortage in locally sourced inputs which attributes to low industrialization.

There are certain constraints that drawn in this sector which include, Low patronage,

dumping of cheap products, unfair tariff regime, inadequate infrastructure, ineffective

regulatory agencies, high interest rates, unpredictable government policies, non-

implementation of existing policies. It is now accepted in the development conformity

that good policies matters and can bring about development. Nigeria has practised poor

policies and there have been policy inconsistencies.

3.8 SOUND ECONOMIC POLICIES

Economic growth is an integrated concept which includes increasing income and

productivity, generation of employment, and economic diversification. The type of

policies that drive economic growth include those on service, agricultural, and industrial

sector; in many poor countries agriculture is especially important. Growth generates

resources which are potentially available for development. A convenient way to approach

the complex is issues of appropriate trade policies for development is to set specific

policies in the context of a broader LDC strategy of looking inward. According to

Todaro (2000), Inward-looking development strategy stresses the need for LDCs to

evolve their own styles of development and control their own destiny. This means

policies to encourage indigenous “learning by doing” in manufacturing and the

development of indigenous technologies appropriate to a country’s resource endowments.

The last two centuries, countries rich in natural resources, e.g. Russia, Nigeria and

Venezuela, experienced growth of comparatively low or mediocre magnitude, Sachs and

Warner (1995) claim that this is a historically common pattern. According to the Fourth

National Development Plan, the overriding aim of development effort in Nigeria was to

bring about an improvement in the living conditions of the people. In addition to the three

policy objectives inherited from the Third National Development Plan namely; economic

growth and development and development, price stability and social equity, the fiscal

28

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 29/84

policy in the Fourth National Development Plan was specifically directed at raising

additional revenue (Mbanefoh 1992).

Herrick and Kindleberger (1988) stated that countries that aspire to economic

development must face international issues squarely if they are to be successful. In order

to rekindle economic growth, the authorities need to formulate and implement sound

macroeconomic policies that promote growth through;

• Sustenance of high but broad –based non-oil GDP growth rate consistent with poverty

reduction and employment generation.

• Diversification of the production structure away from oil/mineral resources.

• Ensuring international competitiveness.

• Systematic reduction of the role of government in direct production of goods and

strengthening its facilitation and regulatory roles

• Pursuit of private sector/export led growth

• Empowering the people through gainful employment and creating safety nets for

vulnerable groups.

3.8.1 EXPLAINING NIGERIA’S SLOW GROWTH

In the development orthodoxy it is accepted that good policies matters and can bring

about development. Nevertheless, Nigeria has been on the track of poor policies and this

brings about policy inconsistencies, policy reversals and often a lack of policy coherence.

In providing solution to the question of why Nigeria has failed to develop, adopting a

recently approach used by Taiwo (2001; 30-32) in attempting to explain Nigeria’s

economic stagnation. According to him, there are remote (long-term) and immediate

causes for this economic stagnation. The remote causes are based on weak production

base arising largely from a poor technological base. Taiwo(2001; 31-32) adds that these

remote causes are manifested in many immediate causes such as: (i) the high cost of

doing business arising mainly from inadequate infrastructure; (ii) the non-

competitiveness of the domestic producers; (iii) a falling investment-GDP ratio (which

had reached 6% during the 1995- 99 period), leading to continued de-industrialization;

(iv) a poor planning and data base, and incomprehensible delays in capital releases for

29

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 30/84

public sector projects coupled with inadequate capacity for executing large-scale projects;

and (v) political instability, insecurity of life and property, and social and ethnic

disharmony.

3.8.2 POLICIES TO REKINDLE ECONOMIC GROWTH IN NIGERIA

Between 1960 and 2000, the annual ratio of investment to income averaged 16.75%. This

is low compared with the standards of both developing and industrialized countries.

Following the presentation drawn on the discussion from Iyoha (1999b), the following

were identified as the major macroeconomic issues in the attempt to rekindle investment

and sustain it in Nigeria: “the macroeconomic policy environment; appropriate

macroeconomic policies; strategies, policies and measures to deal with uncertainty; the

debt overhang problem; achieving a deregulated financial environment; increasing

economic and financial openness; promotion of foreign private investment; and improved

political stability.” Macroeconomic policy instruments fall within the realm of major

macroeconomics policy. These economic policies should refer to the actions in which

government controls the economic field.

CHAPTER FOUR

METHODOLOGY

4.0 Introduction

This section discusses the methodology used in conducting our empirical studies. As

discussed briefly we employed most of the traditional variables that are considered as the

determinants for economic growth. These variables include private consumption,

government expenditure, gross fixed capital formation as a proxy for gross investment,

net exports which is the difference between exports and imports and lagged variables of

GDP. GDP which is set as the dependent variable in our empirical study is also used as a

proxy for economic growth. This chapter begins by explaining how these variables are

measured. Hence in section 4.1, we explain the variables used, in section 4.2 we specify

our model. Subsequently, section 4.3 expatiates on how the estimations are conducted

this includes how to test for the existence of a unit root, the generation of residuals and

30

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 31/84

the application of an Error correction model in conducting our regression for the

determinants of economic growth.

4.1 VARIABLES USED AND THEIR MEASUREMENT

The literature on the determinants of growth is replete in economic literature. Although

there exist a large volume of text on the subject of economic growth most of the literature

relies on the use of a cobb-douglas function which involves two variables such as labour

and capital which owning to data problems are not employed in this study. Economic

growth can be achieved at least theoretically through a high inflow of both domestic and

foreign capital, in a politically stable economy and in a country in which the rule of law is

enforced. However for the purposes of this study we only limit our study to the use of the

variables discussed in the introduction of this chapter.

4.1.1 GROSS DOMESTIC PRODUCT

This is one of the major ways of measuring the size of the economy. This is the actual

monetary value of all finished goods and services produced in a country within a specific

period of time. It is also the sum of value which is added up at every stage of production

of all final goods and services produced within a country in a specific period of time

(McGuckin, Van Ark and Barrington, 2000). As an economy grows it is expected that

the growth rate in GDP increases. Thus changes in the economic growth are captured by

changes in GDP. As a result we use the GDP in Nigeria as a proxy for economic growth.

Going by the expenditure approach in accounting for national income in an open

economy such as that of Nigeria. This will be based on the Keynesian model, aggregate

demand (AD) equals C + I + G + NX. Macroeconomic equilibrium in the short-run

Keynesian model occurs when aggregate output equals aggregate demand. This is

represented below by the following equation;

GDP = C + G + I + NX

Where

GDP = is a measure of economic growth from year to year

31

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 32/84

C – Equal to all private consumption, or consumer spending in a nation’s

economy.

G – is the sum of government spending

I – the sum of all the country’s businesses spending on capital

NX – the nation’s total net exports, calculated as total exports minus total imports.(NX =

Exports – Imports)

We therefore modify the above equation to ascertain the effectiveness of each of the

variables serve as the most important determinants of economic growth in Nigeria.

Due to the difficulty associated in obtaining annual data for gross investment in the

economy we use gross fixed capital formation as a proxy for gross investment in the

economy, variables such as gross fixed capital formation

net export, government expenditure and lagged variables of GDP are used.

4.2 MODEL SPECIFICATION

Given time and resource constraints this study relied mostly on secondary data. Data was

collected on those variables originating from the appendix review as being relevant to the

indicators of economic growth. Methods require form to be developed in order to find

statistically significant relationship between the traditional determinants of growth

(consumption expenditure, gross fixed capital formation, government expenditure and net

exports) and GDP. To allow for sustained growth GDP equation is employed. Gross

investment is assumed to be a fraction of GDP. Genuine saving is intended to indicate the

difference between sustainable net national product and consumption, where sustainable

net national product means the maximum amount that could be consumed without

reducing the present value of national welfare along the optimum path (Hamilton, 2001).

The main idea behind this assumption is that the higher the output or national income, the

more the economy can afford to invest. In this growth model, the larger the fraction of

GDP devoted to investment at the expense of consumption, the higher the rate of capital

32

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 33/84

formation and hence the higher the rate of GDP growth. The model of national income

determination in the short run is based on the forces of aggregate demand. By way of the

national income identity, national output can be decomposed into expenditure by the

consumers C, on investment I, by government G, and on net exports NX (exports minus

imports) and this is represented by

Y = C + I + G + NX……………………………………………………………..(1)

The modelling approach controls and measures variables we employ which are chosen to

be consistent with the prior high quality of national economic growth by economists

(Barro, 1991). We use ordinary least squares (OLS) regression to model economic

growth. Economic growth studied for about 35 years is employed for this research work.

This lag allows sufficient time for independent variables such as investment, private

consumption, net exports, and government expenditure to have an impact on national

economic performance.

We specify the econometric model used in the study as;

GDPt = αt + Σ β1Ct + Σ β2 It + Σ β3Gt + Σ β4NXt + Σ β5GDPt-1 + εt ...………………..

(2)

WHERE; OUR DEPENDENT VARIABLE

GDP=Gross domestic product

EXPLANATORY VARIABLES ARE

α = Constant factor

Σ = Summation of a variable from t=year 1 to 35 (i.e. 1970-2005)

C = Consumption

G = Government Expenditures

I= Gross fixed capital formation

NX = Net Exports = (X- M)

GDPt-1=lagged variables of GDP

33

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 34/84

Where

X = Exports

M = Imports

ε = the random error term to compensate for errors in data

4.3 ECONOMETRIC METHODOLOGIES: BASIC REGRESSION

SPECIFICATIONS

Recent developments in econometric studies suggests that caution is necessary in

applying the ordinary least square (OLS) method in time series analysis of this nature.

The reason is because most times series data are usually non- stationary. Non-stationarity

in the level of a time series can always be tested in an applied econometric research.

Stationarity results as the mean and variance of a time series data remains constant

overtime, whilst the value of the covariance between two specified periods depends only

on the gap between the periods and not the actual time at which the covariance is

considered and any violation in the conditions above results in the non-stationarity of the

process (Tsikata et al, 2000:49).

When a time series is non-stationary it is most likely for one to obtain regression results

with promising diagnostic test statistics given the when the reason of estimation isspurious Charemza & Deadman (1992),. In order to then avoid having a spurious result

we employ the Dickey – Fuller (DF) and Augmented Dickey – Fuller (ADF) test using

Microfit4.1 software package to test for the stationarity of the time series data. A time

series data is stationary when it is integrated to order zero I (0) and non-stationary when it

is integrated to a higher order I (n) where n is a higher order. When the ADF test statistic

(t-ratio) is greater than the DF critical value in absolute terms as reported by Microfit, we

reject the null hypothesis of a unit root and conclude that the variables are stationary

(Koop, 2005:154).

In order to test for the existence of stationarity or non stationarity among the variables,

we set the following hypothesis:

Ho: ρ =1 variables are non stationary and has a unit root

Hı: / ρ / <1 variables are stationary and has a deterministic trend.

34

8/8/2019 e Dissertation

http://slidepdf.com/reader/full/e-dissertation 35/84

Yt = β0 + ρYt-1+ et (3) by subtract Yt-1 from both sides of….… (3),

we obtain equation (4) below,

Yt -Yt-1 = β0 + ρYt-1 - Yt-1 + et………………………………… (4),

Re-arranging (4) we express the equation above as

Yt -Yt-1 = β0 + (ρ – 1)Yt-1+ et ………………………………….(5),

but ∆ Yt = Yt -Yt-1 hence

∆ Yt = β0 + (ρ – 1)Yt-1+

et…………………………………………………………………. (6),

when ρ=1, then the time series data is stationary and has a unit root. Let λ = (ρ – 1)

this simply implies that

∆ Yt = β0 + λYt-1+ et………………………………………………(7),

hence if ρ=1, then λ =0 and this gives the general condition for non-stationarity

or unit root for a time series data (i.e. -1< ρ <1 which is equivalent to -2< λ < 0). Thus

when ρ=1 the times series data is non-stationary.

In (time series) econometrics, a time series that has a unit root is known as a random walk

(time series). And a random walk is an example of a non-stationarity time series. When