Dynamics in Aquaculture - IntraFish...

28

Intrafish Summit 2016 , Jeroen Leffelaar Managing Director Large Corporates Food & Agri NYC 2016 Dynamics in Aquaculture

Transcript of Dynamics in Aquaculture - IntraFish...

Intrafish Summit 2016 ,

Jeroen Leffelaar

Managing Director Large Corporates Food & Agri

NYC 2016

Dynamics in Aquaculture

2

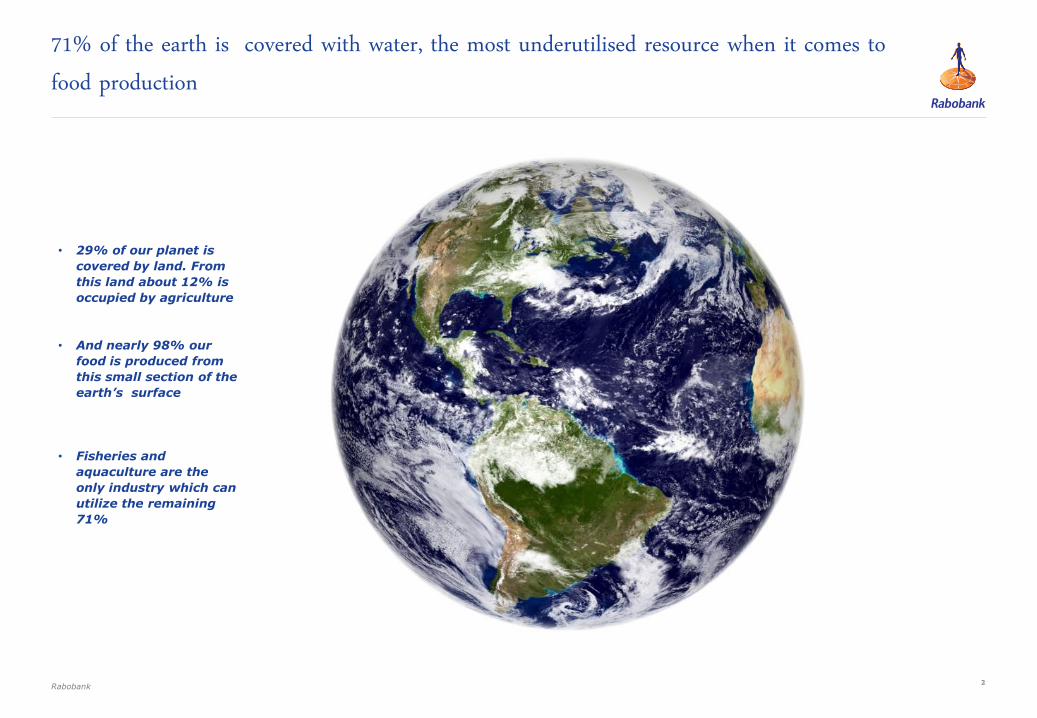

• 29% of our planet is

covered by land. From

this land about 12% is

occupied by agriculture

• And nearly 98% our

food is produced from

this small section of the

earth’s surface

• Fisheries and

aquaculture are the

only industry which can

utilize the remaining

71%

71% of the earth is covered with water, the most underutilised resource when it comes to food production

Rabobank

Demand – Seafood has the most unsatisfied demand function of any protein I

4

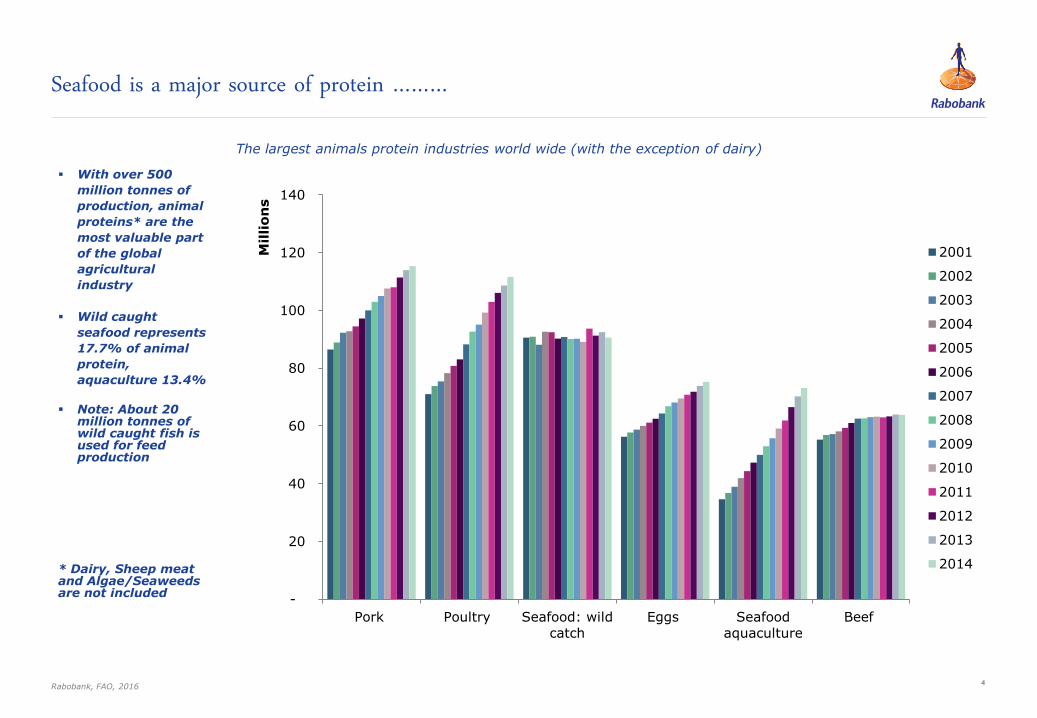

With over 500

million tonnes of

production, animal

proteins* are the

most valuable part

of the global

agricultural

industry

Wild caught

seafood represents

17.7% of animal

protein,

aquaculture 13.4%

Note: About 20 million tonnes of wild caught fish is used for feed production

* Dairy, Sheep meat and Algae/Seaweeds are not included

Seafood is a major source of protein ………

The largest animals protein industries world wide (with the exception of dairy)

Rabobank, FAO, 2016

-

20

40

60

80

100

120

140

Pork Poultry Seafood: wild

catch

Eggs Seafood

aquaculture

Beef

Millio

ns

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

5

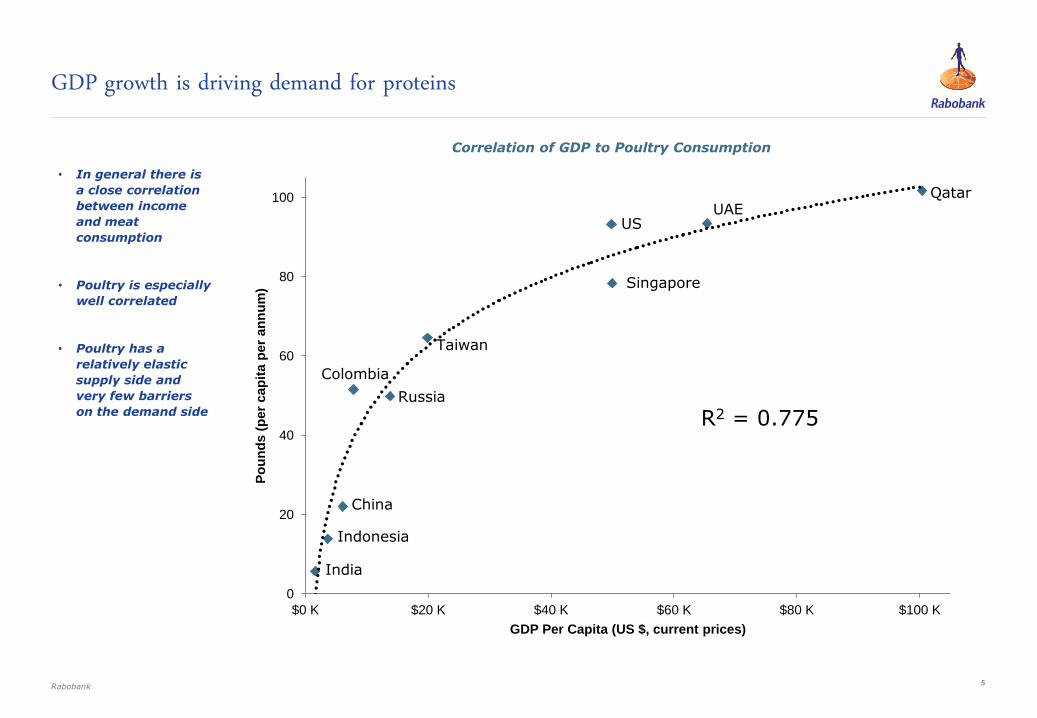

• In general there is

a close correlation

between income

and meat

consumption

• Poultry is especially

well correlated

• Poultry has a

relatively elastic

supply side and

very few barriers

on the demand side

GDP growth is driving demand for proteins

Correlation of GDP to Poultry Consumption

Rabobank

0

20

40

60

80

100

$0 K $20 K $40 K $60 K $80 K $100 K

Po

un

ds (

per

cap

ita p

er

an

nu

m)

GDP Per Capita (US $, current prices)

China

Indonesia

India

Taiwan

Russia

Colombia

Singapore

US UAE

Qatar

R2 = 0.775

6 6

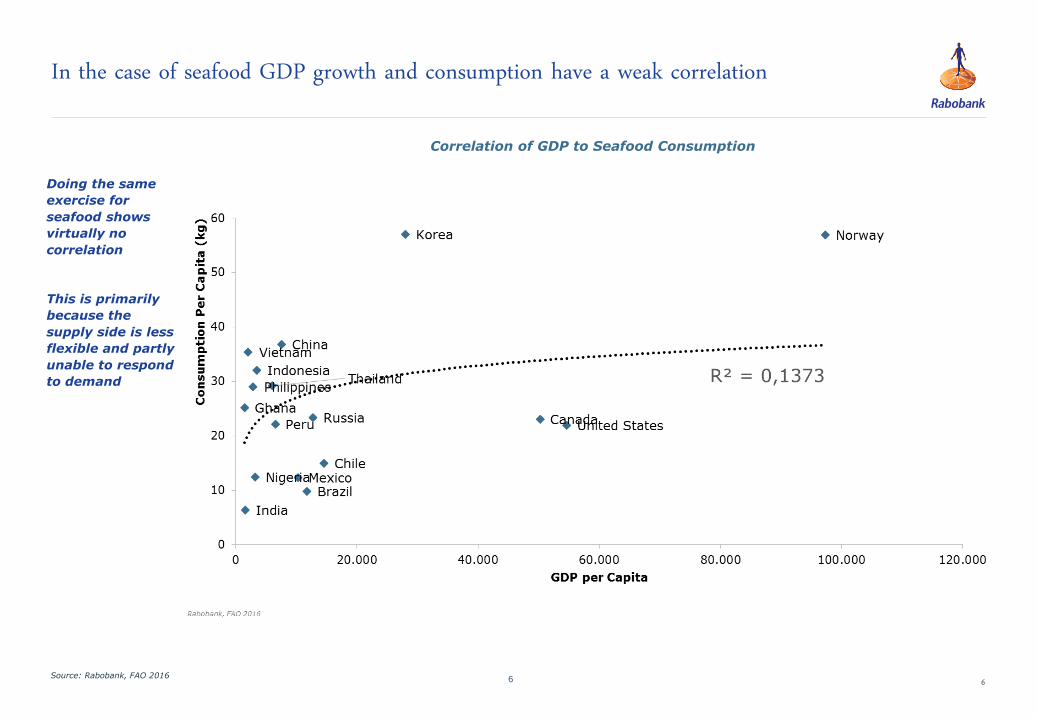

Doing the same

exercise for

seafood shows

virtually no

correlation

This is primarily

because the

supply side is less

flexible and partly

unable to respond

to demand

Source: Rabobank, FAO 2016

In the case of seafood GDP growth and consumption have a weak correlation

Correlation of GDP to Seafood Consumption

7

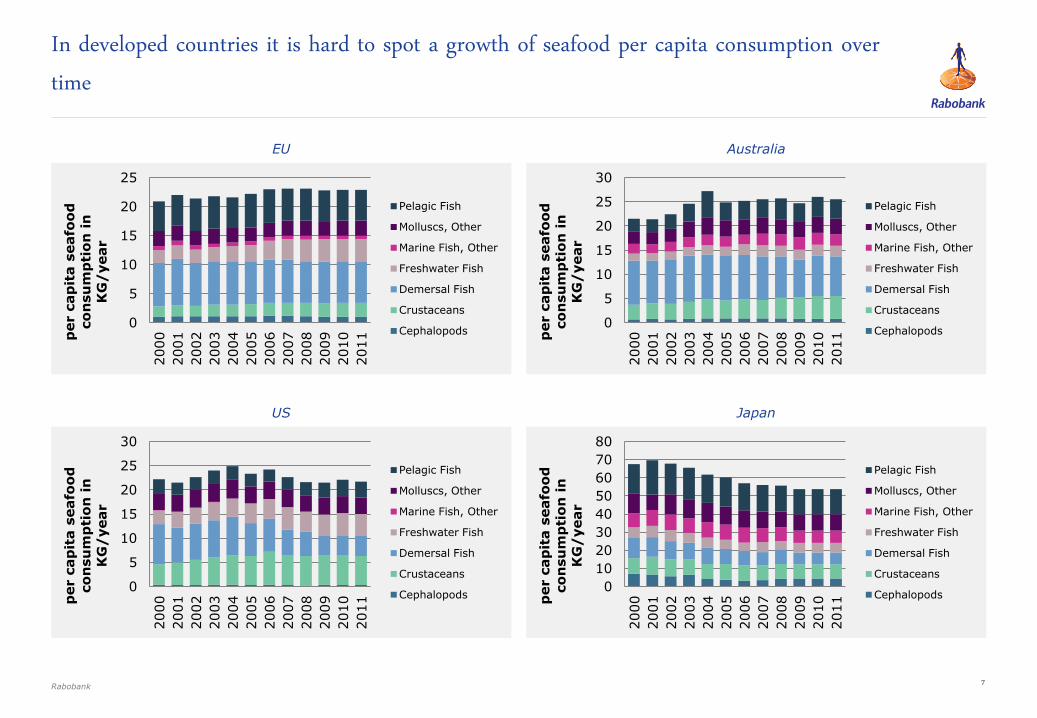

In developed countries it is hard to spot a growth of seafood per capita consumption over time

Australia

Japan

EU

US

Rabobank

0

10

20

30

40

50

60

70

80

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

per c

ap

ita s

eafo

od

co

nsu

mp

tio

n i

n

KG

/year

Pelagic Fish

Molluscs, Other

Marine Fish, Other

Freshwater Fish

Demersal Fish

Crustaceans

Cephalopods 0

5

10

15

20

25

30

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

per c

ap

ita s

eafo

od

co

nsu

mp

tio

n i

n

KG

/year

Pelagic Fish

Molluscs, Other

Marine Fish, Other

Freshwater Fish

Demersal Fish

Crustaceans

Cephalopods

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

per c

ap

ita s

eafo

od

co

nsu

mp

tio

n i

n

KG

/year

Pelagic Fish

Molluscs, Other

Marine Fish, Other

Freshwater Fish

Demersal Fish

Crustaceans

Cephalopods 0

5

10

15

20

25

30

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

per c

ap

ita s

eafo

od

co

nsu

mp

tio

n i

n

KG

/year

Pelagic Fish

Molluscs, Other

Marine Fish, Other

Freshwater Fish

Demersal Fish

Crustaceans

Cephalopods

8

China has a very high income elasticity of demand and supply elasticity (high share of aquaculture)

China Statistical Yearbook 2011 National Bureau of Statistics of China, Industry reports, 2014

Relative seafood and animal protein expenditure per income group Urbanization & disposable income growth China

Rabobank research

0%

10%

20%

30%

40%

50%

60%

0

5,000

10,000

15,000

20,000

25,000

30,000

Urbanization rate of China (rsa)

Annual disposal income of urban households

Annual net income of rural households

4%

5%

6%

7%

8%

12%

14%

16%

18%

20%

22%

24%

Lowest Low Lower Middle

Middle Upper Middle

High Highest

Seafo

od

exp

en

dit

ure s

hare

Meat

exp

en

dit

ure s

hare

Meat, Poultry and Processed Products (LHS)

Aquatic Products (RHS)

9

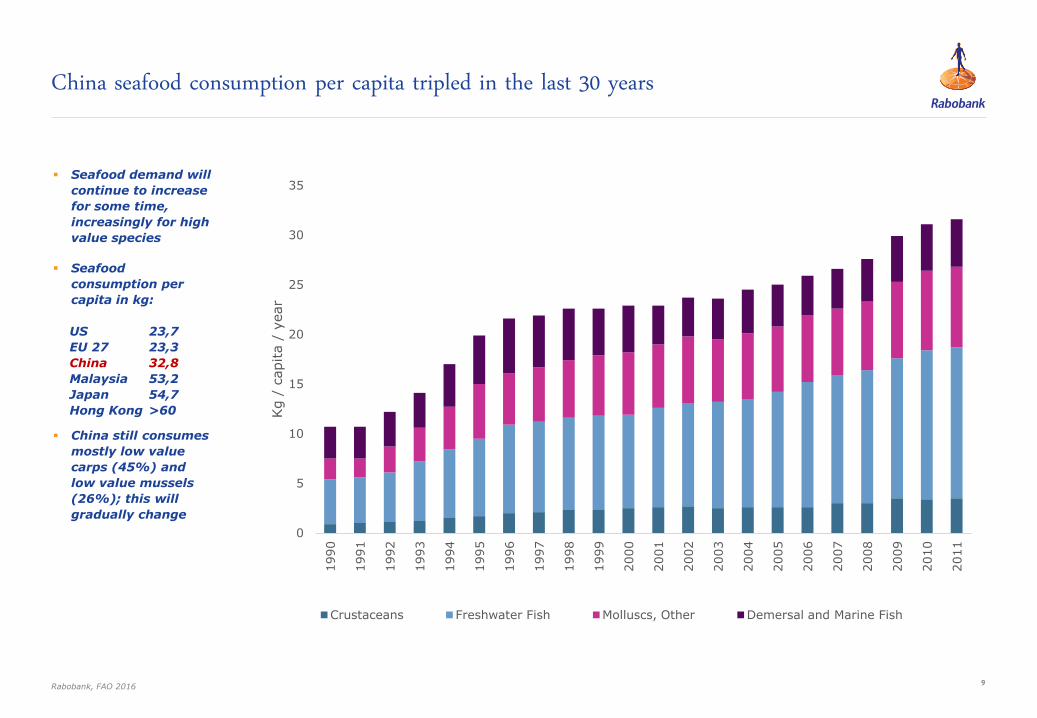

Seafood demand will

continue to increase

for some time,

increasingly for high

value species

Seafood

consumption per

capita in kg:

US 23,7

EU 27 23,3

China 32,8

Malaysia 53,2

Japan 54,7

Hong Kong >60

China still consumes

mostly low value

carps (45%) and

low value mussels

(26%); this will

gradually change

China seafood consumption per capita tripled in the last 30 years

Rabobank, FAO 2016

0

5

10

15

20

25

30

35

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Kg /

capita /

year

Crustaceans Freshwater Fish Molluscs, Other Demersal and Marine Fish

10

-

2

4

6

8

10

12

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Millions M

T

wild catch aquaculture

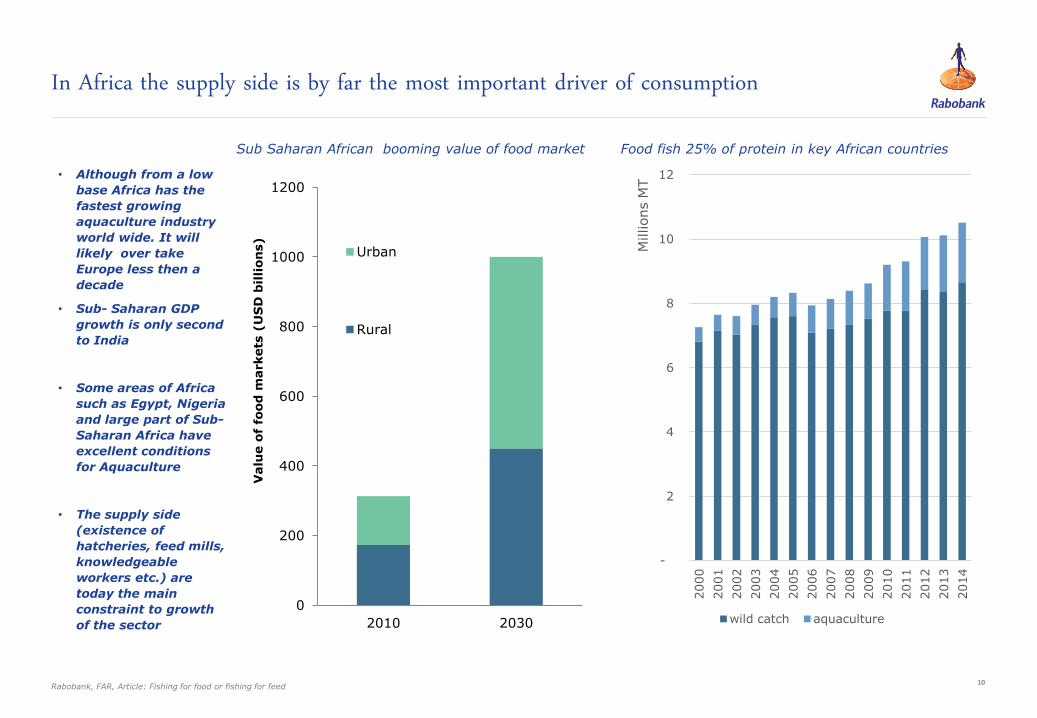

• Although from a low

base Africa has the

fastest growing

aquaculture industry

world wide. It will

likely over take

Europe less then a

decade

• Sub- Saharan GDP

growth is only second

to India

• Some areas of Africa

such as Egypt, Nigeria

and large part of Sub-

Saharan Africa have

excellent conditions

for Aquaculture

• The supply side

(existence of

hatcheries, feed mills,

knowledgeable

workers etc.) are

today the main

constraint to growth

of the sector

In Africa the supply side is by far the most important driver of consumption

Sub Saharan African booming value of food market Food fish 25% of protein in key African countries

Rabobank, FAR, Article: Fishing for food or fishing for feed

0

200

400

600

800

1000

1200

2010 2030

Valu

e o

f fo

od

markets

(U

SD

bil

lion

s)

Urban

Rural

11

• Based on historical

link of income and

seafood consumption

and future income

growth expectations it

is easy to see why

Asia is key to future

growth

• Asia and China

dominates fish

consumption and

growth world wide

• Europe has near zero

volume growth

• Growth of aquaculture

could eventually

increase seafood

consumption growth

in developed markets

OECD outlook: fish consumption and growth dominated by Asia and China

OECD outlook on the Fish consumption per region world wide (in MT)

OECD 2015

0

10000

20000

30000

40000

50000

60000

70000

80000

NORTH

AMERICA

EUROPE AFRICA LATIN

AMERICA AND CARIBBEAN

China Asia ex China

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Supply – All cards on Aquaculture II

13

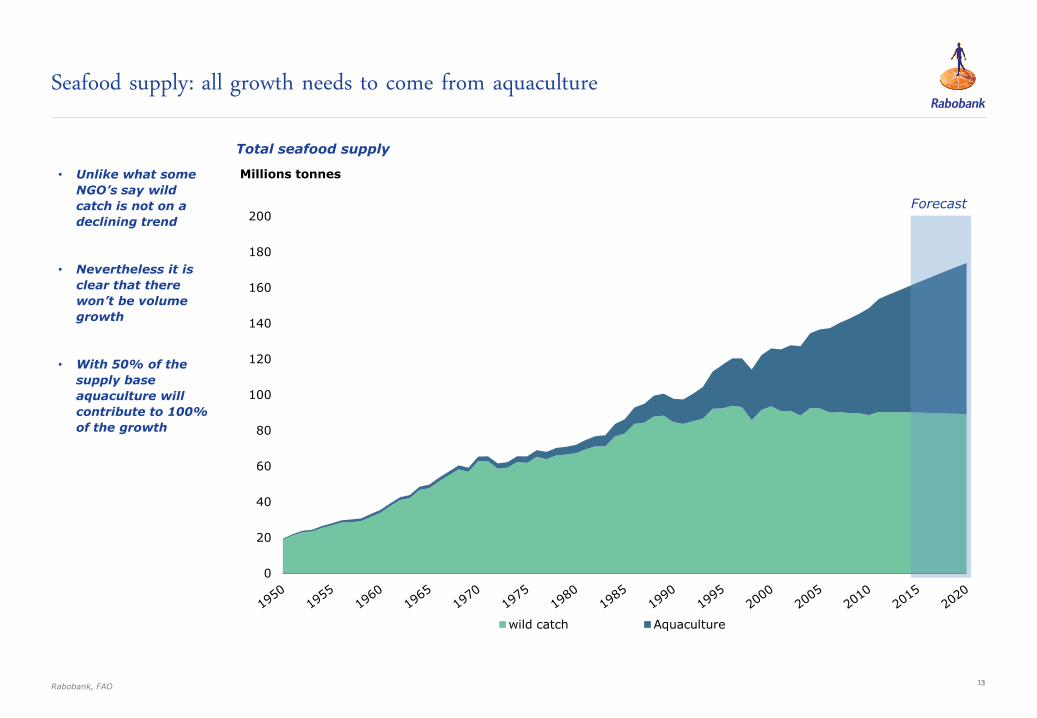

• Unlike what some

NGO’s say wild

catch is not on a

declining trend

• Nevertheless it is

clear that there

won’t be volume

growth

• With 50% of the

supply base

aquaculture will

contribute to 100%

of the growth

Seafood supply: all growth needs to come from aquaculture

Total seafood supply

Rabobank, FAO

0

20

40

60

80

100

120

140

160

180

200

Millions tonnes

wild catch Aquaculture

Forecast

14

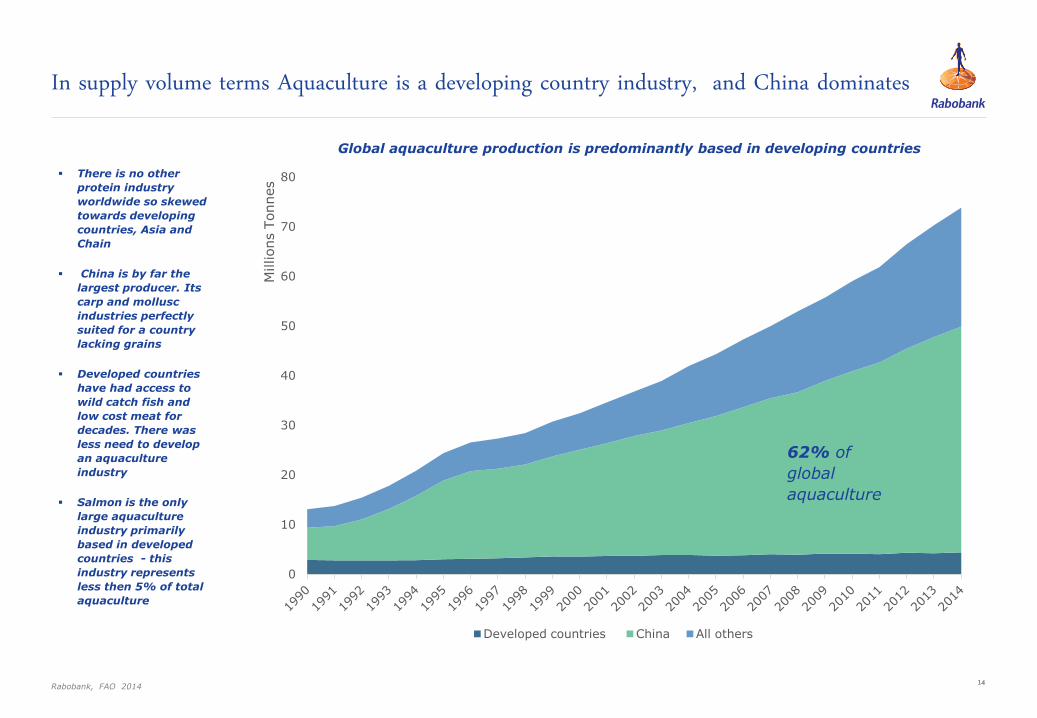

There is no other

protein industry

worldwide so skewed

towards developing

countries, Asia and

Chain

China is by far the

largest producer. Its

carp and mollusc

industries perfectly

suited for a country

lacking grains

Developed countries

have had access to

wild catch fish and

low cost meat for

decades. There was

less need to develop

an aquaculture

industry

Salmon is the only

large aquaculture

industry primarily

based in developed

countries - this

industry represents

less then 5% of total

aquaculture

In supply volume terms Aquaculture is a developing country industry, and China dominates

Global aquaculture production is predominantly based in developing countries

Rabobank, FAO 2014

0

10

20

30

40

50

60

70

80

Millions T

onnes

Developed countries China All others

62% of

global

aquaculture

15

• Nearly all Carp and

Mollusk farming is

based on extensive

faming technology

• In terms of inputs

and technology this

can be compared to

pasture farming on

land

• Intensive farming -

such as salmon,

shrimp, tilapia in

terms of land use

and exposure to the

environment

compare to FREE

RANGE Chicken of

Pork production

• As LAND is the key

input for extensive

farming, Intensive

aquaculture will the

future of the

industry

Moreover 2/3rd of aquaculture is based on extensive farming (loosely comparable to pasture farming on land)

Rabobank, FAO FIGIS

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

Molluscs Carps, barbels and other cyprinids Other fresh water

Crustaceans Salmons, trouts, smelts All other diadromous

Marine fishes

Extensive farming technology

Intensive farming

Global aquaculture production (excluding aquatic plants) 1990 – 2014 per key species group

16

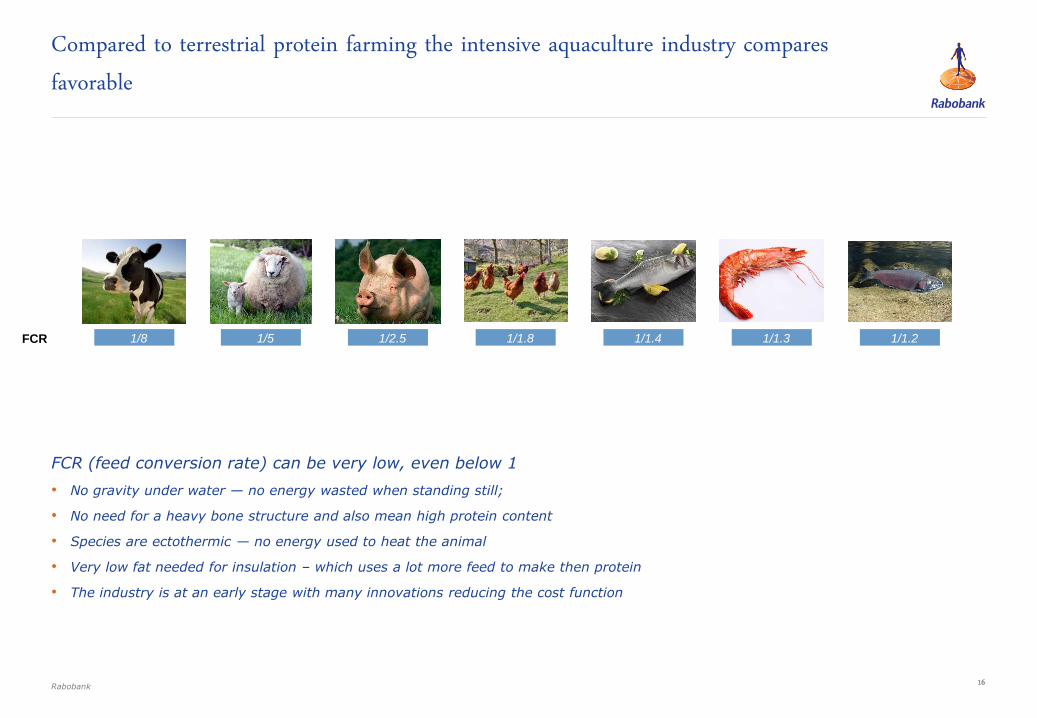

Compared to terrestrial protein farming the intensive aquaculture industry compares favorable

Rabobank

FCR (feed conversion rate) can be very low, even below 1

• No gravity under water — no energy wasted when standing still;

• No need for a heavy bone structure and also mean high protein content

• Species are ectothermic — no energy used to heat the animal

• Very low fat needed for insulation – which uses a lot more feed to make then protein

• The industry is at an early stage with many innovations reducing the cost function

1/8

1/5

1/2.5

1/1.8

1/1.4

1/1.2

1/1.3

FCR

Constraints in aquaculture: Biology versus Demand III

18

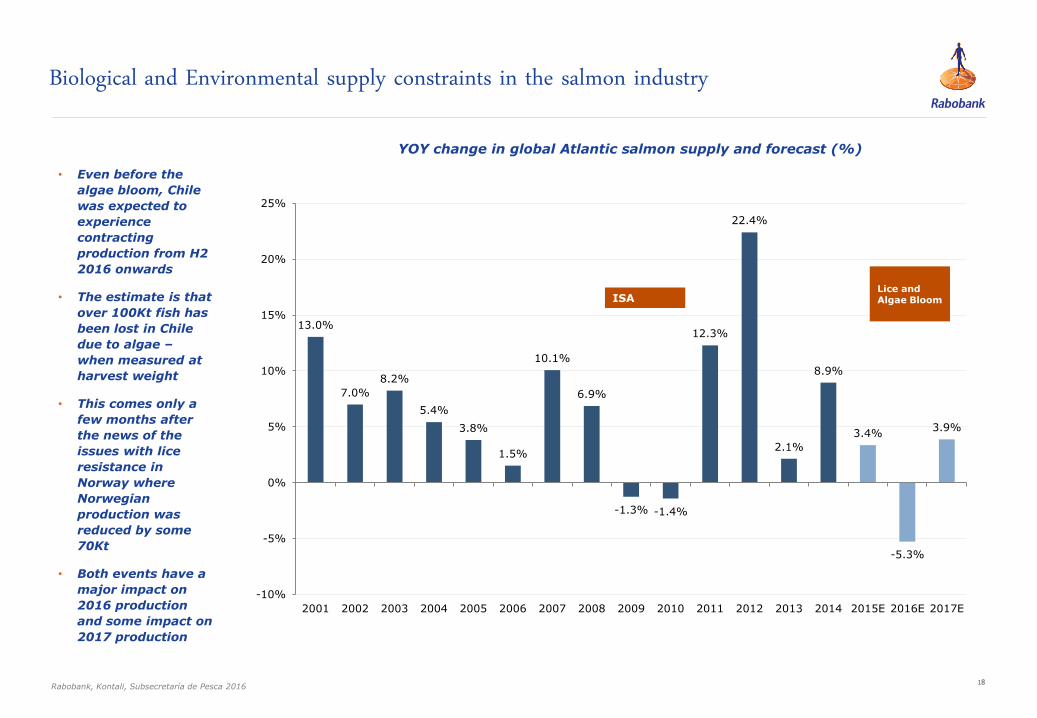

• Even before the

algae bloom, Chile

was expected to

experience

contracting

production from H2

2016 onwards

• The estimate is that

over 100Kt fish has

been lost in Chile

due to algae –

when measured at

harvest weight

• This comes only a

few months after

the news of the

issues with lice

resistance in

Norway where

Norwegian

production was

reduced by some

70Kt

• Both events have a

major impact on

2016 production

and some impact on

2017 production

Biological and Environmental supply constraints in the salmon industry

YOY change in global Atlantic salmon supply and forecast (%)

Rabobank, Kontali, Subsecretaría de Pesca 2016

13.0%

7.0%

8.2%

5.4%

3.8%

1.5%

10.1%

6.9%

-1.3% -1.4%

12.3%

22.4%

2.1%

8.9%

3.4%

-5.3%

3.9%

-10%

-5%

0%

5%

10%

15%

20%

25%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

ISA Lice and Algae Bloom

19

-

1

2

3

4

Mil

lion

s M

T

Asia LAM

3

4

5

6

7

8

9

10

usd

/lb

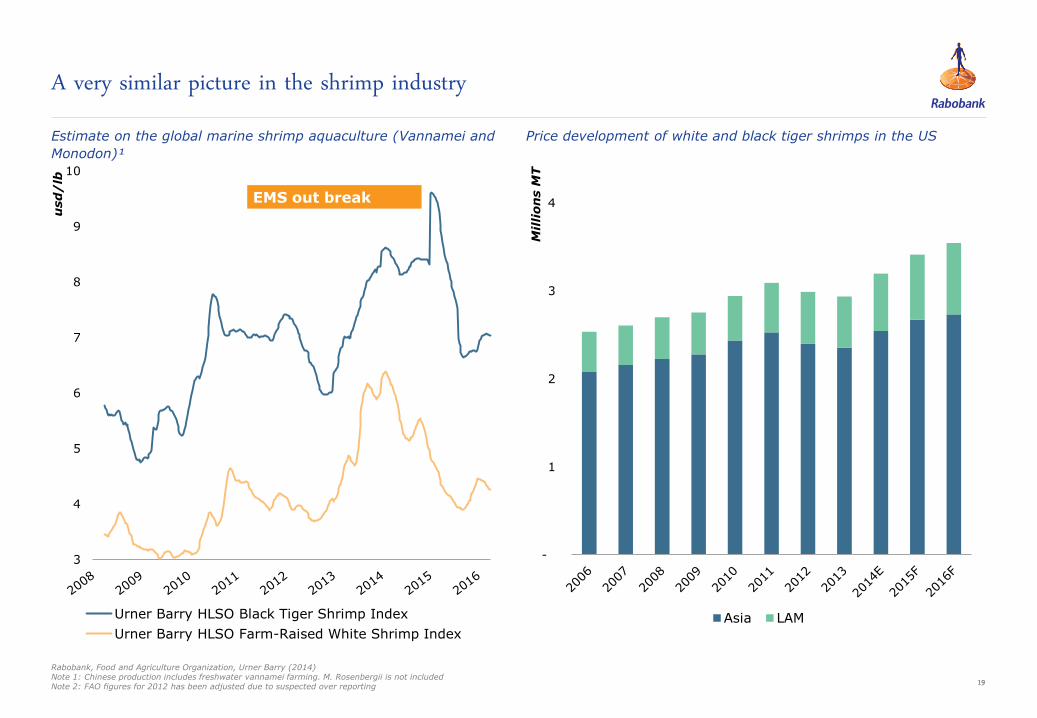

Urner Barry HLSO Black Tiger Shrimp Index

Urner Barry HLSO Farm-Raised White Shrimp Index

A very similar picture in the shrimp industry Price development of white and black tiger shrimps in the US Estimate on the global marine shrimp aquaculture (Vannamei and

Monodon)¹

Rabobank, Food and Agriculture Organization, Urner Barry (2014) Note 1: Chinese production includes freshwater vannamei farming. M. Rosenbergii is not included Note 2: FAO figures for 2012 has been adjusted due to suspected over reporting

EMS out break

20

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2008 2009 2010 2011 2012 2013 2014 2015 2016

Tilapia Pangasius

-

1

2

3

4

5

6

7

8

9

10

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Mil

lio

ns

Tilapias Panga Catfish

In the case of Tilapia and Pangasius market development is the bottle neck

Rabobank, Food and Agriculture Organization, Urner Barry (2014) Note 1: Chinese production includes freshwater vannamei farming. M. Rosenbergii is not included Note 2: FAO figures for 2012 has been adjusted due to suspected over reporting

Aquaculture of selected fresh water species

Price development of Tilapia and Pangasius in the US

21

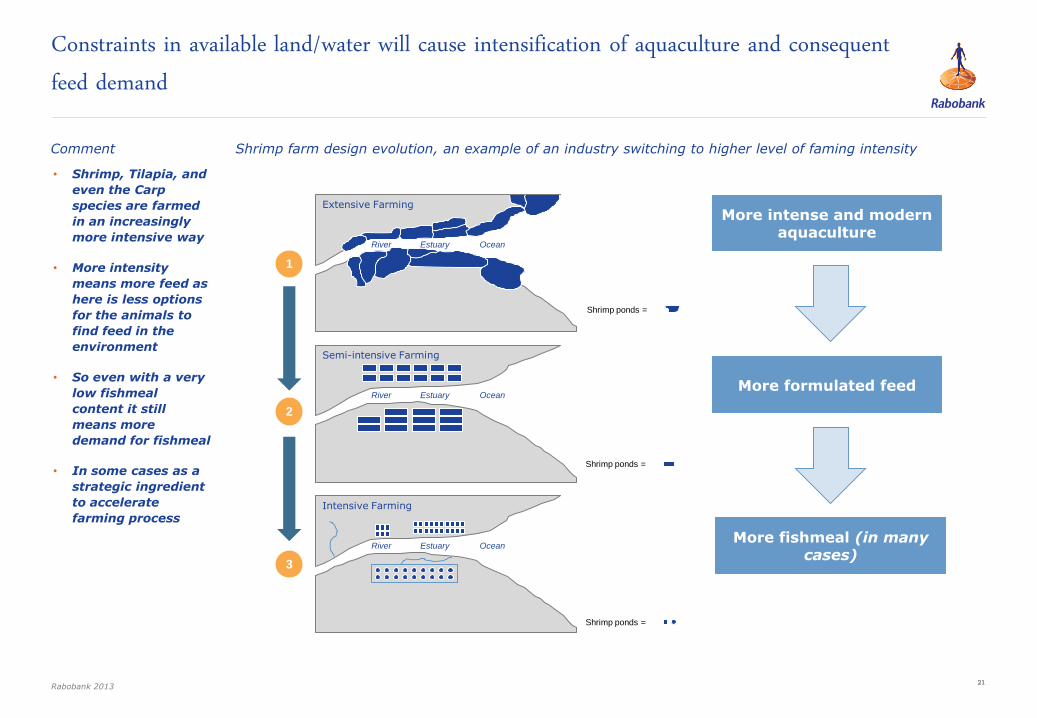

• Shrimp, Tilapia, and

even the Carp

species are farmed

in an increasingly

more intensive way

• More intensity

means more feed as

here is less options

for the animals to

find feed in the

environment

• So even with a very

low fishmeal

content it still

means more

demand for fishmeal

• In some cases as a

strategic ingredient

to accelerate

farming process

Constraints in available land/water will cause intensification of aquaculture and consequent feed demand

Shrimp farm design evolution, an example of an industry switching to higher level of faming intensity

Rabobank 2013

Intensive Farming

River Estuary Ocean

Shrimp ponds =

Semi-intensive Farming

River Estuary Ocean

Shrimp ponds =

Extensive Farming

River Estuary Ocean

Shrimp ponds =

2

1

3

More intense and modern aquaculture

More formulated feed

More fishmeal (in many cases)

Comment

22

Global supply of fish meal

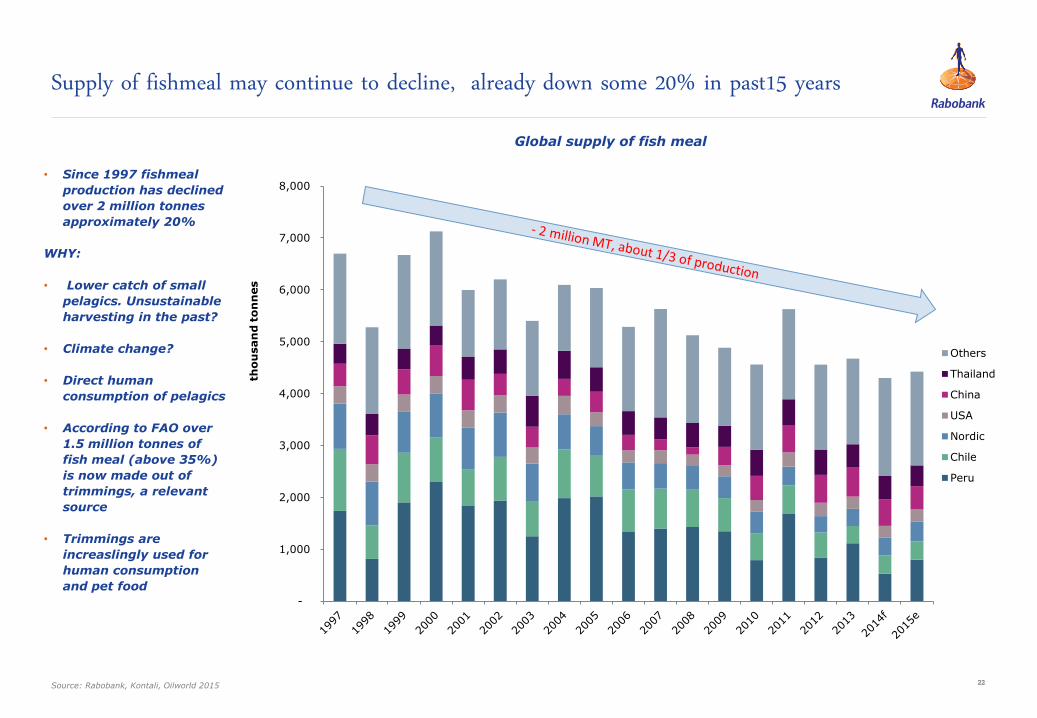

Supply of fishmeal may continue to decline, already down some 20% in past15 years

• Since 1997 fishmeal

production has declined

over 2 million tonnes

approximately 20%

WHY:

• Lower catch of small

pelagics. Unsustainable

harvesting in the past?

• Climate change?

• Direct human

consumption of pelagics

• According to FAO over

1.5 million tonnes of

fish meal (above 35%)

is now made out of

trimmings, a relevant

source

• Trimmings are

increaslingly used for

human consumption

and pet food

Source: Rabobank, Kontali, Oilworld 2015

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

tho

usan

d t

on

nes

Others

Thailand

China

USA

Nordic

Chile

Peru

23

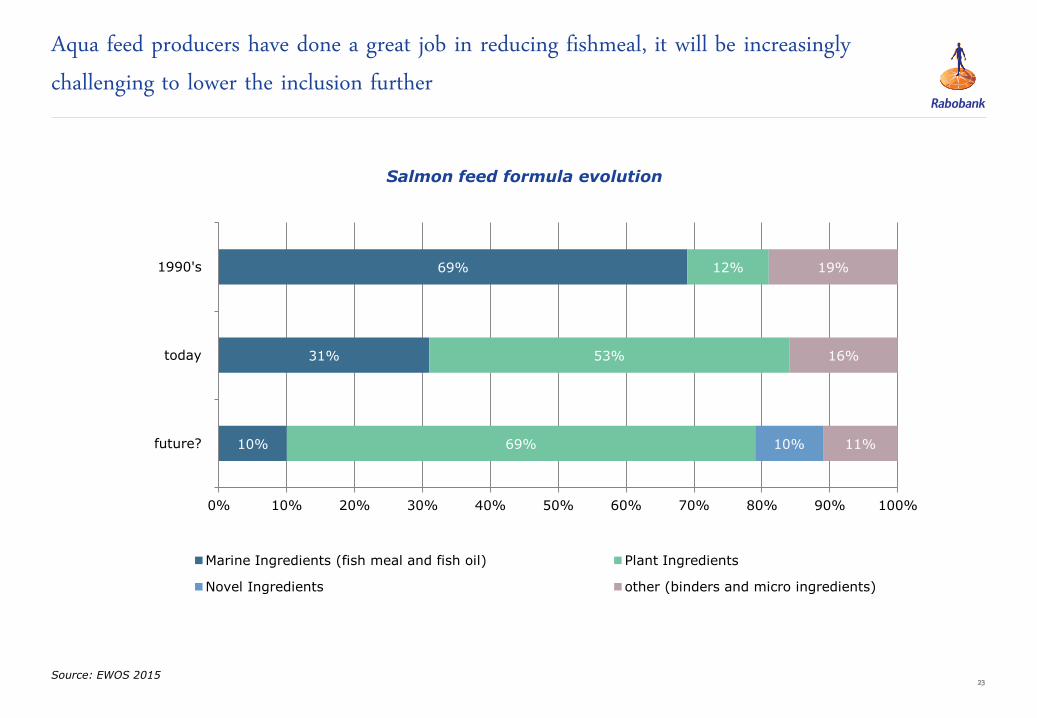

Aqua feed producers have done a great job in reducing fishmeal, it will be increasingly challenging to lower the inclusion further

Salmon feed formula evolution

Source: EWOS 2015

10%

31%

69%

69%

53%

12%

10% 11%

16%

19%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

future?

today

1990's

Marine Ingredients (fish meal and fish oil) Plant Ingredients

Novel Ingredients other (binders and micro ingredients)

24

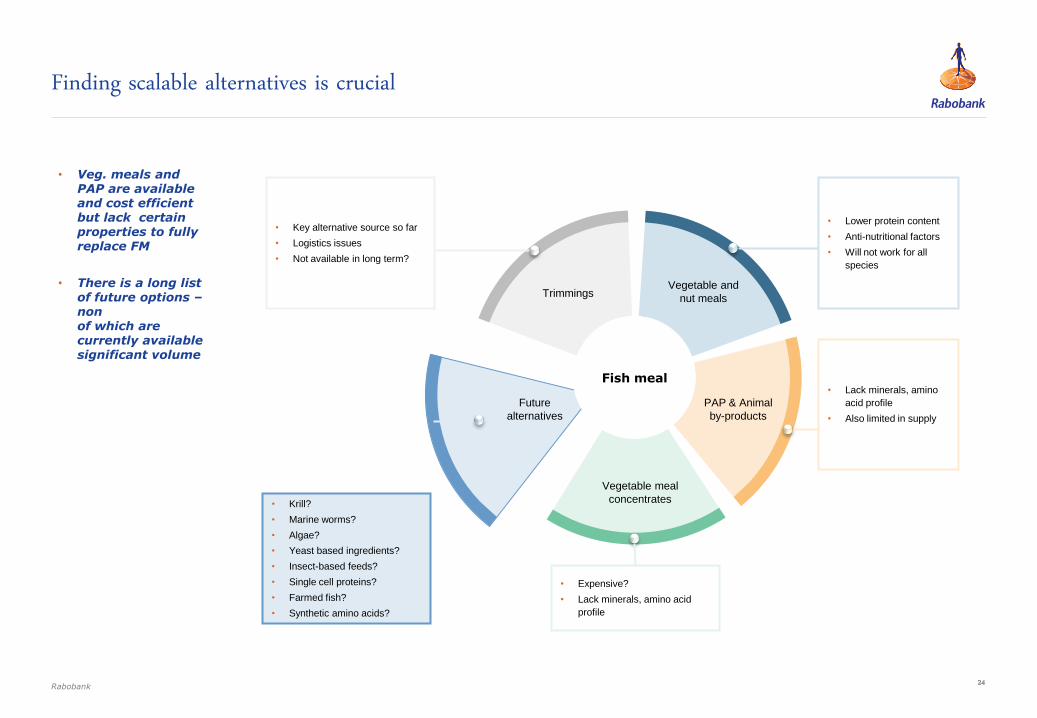

• Veg. meals and PAP are available and cost efficient but lack certain properties to fully replace FM

• There is a long list of future options – non of which are currently available significant volume

Finding scalable alternatives is crucial

Rabobank

Fish meal

Vegetable and

nut meals

PAP & Animal

by-products

Vegetable meal

concentrates

Future

alternatives

Trimmings

• Krill?

• Marine worms?

• Algae?

• Yeast based ingredients?

• Insect-based feeds?

• Single cell proteins?

• Farmed fish?

• Synthetic amino acids?

• Key alternative source so far

• Logistics issues

• Not available in long term?

• Expensive?

• Lack minerals, amino acid

profile

• Lack minerals, amino

acid profile

• Also limited in supply

• Lower protein content

• Anti-nutritional factors

• Will not work for all

species

Our view: growth in aquaculture will be enabled by unrivalled innovation IV

26

Seafood has a more complex demand function then the other proteins and is highly influenced by local availability

27

1. Global seafood demand growth depends on Asia and particularly China The most rapidly expanding middle class in the world also has the highest preference for seafood consumption 2. Value growth will be key Assuming change in species and higher level of processed products the value of seafood consumption is likely to grow much faster then volume

Global seafood consumption going forward: two expectations

Rabobank

28

Key driver for growth: innovation by the entire value chain - from genetics up to new farming technologies

Farming of new species New Feed formulas New Genetics

Farmed insects as raw material source New farming technologies Single cell organisms as a feed source