Dwayne Crombie - BUPA Australia - Innovation & Collaboration Across the PHI Industry

12

COLLABORATION AND INNOVATION TO PRODUCE BETTER OUTCOMES FOR THE CONSUMER July 28 th 2015

-

Upload

informa-australia -

Category

Healthcare

-

view

195 -

download

0

Transcript of Dwayne Crombie - BUPA Australia - Innovation & Collaboration Across the PHI Industry

COLLABORATION AND INNOVATION TO PRODUCE BETTER OUTCOMES FOR THE CONSUMERJuly 28th 2015

Bupa

Competition versus CollaborationHealth Funds• 34 tribes… 2 with shareholders• 3 federations

• 1 industry• Health Insurer and Health Partner and Healthcare Provider

Old Relationships• The umbilical cord with private hospitals

• An uneasy relationship with public hospitals & states• Competition through portability and switching of funds (PHIAC)

New Relationships• A new world, e.g. GPs & PHNs, with a collection of new and old players

• Networks, relationships and trust

• Provider development in primary and community care areas

Bupa

Wish ListCollaboration and Innovation to Produce Better Outcomes• Competition versus Collaboration

• Value for Money and Transparency

o Affordability

o Appropriate and Effective Care

o Health Information Networks

o Access to Information & Informed Decision Making

o Shared Feedback on Care

Bupa

AffordabilityContext• Overall Spend of GDP is 9.5%, lower than OECD average

• Out of Pocket Spend faced by consumers is in top 2 in OECD, ergo government spending on health is NOT a crisis in absolute terms

• Impact of 6% average health insurance increases is more like 9% for anyone receiving a rebate (impact of scale-back of rebate increases to CPI only, and step reductions in rebate due to movement between fixed income bands)

• About half of the 6% annual increase is due to provider cost of living increases, remainder due to ageing which drives utilisation and technology

• Price comparators capturing significant market share of new joins, and take out 25-40% of an annual premium

• Switching and downgrading behaviour by consumers at industry highs

• Significant price variation between hospital providers for like for like

Bupa

Affordability – Opportunities to AddressProvision• Health insurers have ACCC issues over common pricing they pay although a

nationally efficient hospital pricing model does beg the question• Drive a lower rate of growth of provider cost of living, say 2% (6% to 5%)• Transparency over “out of pocket charges” by doctors although cartel behaviour is

difficult to eradicate unless regulators take an interest, e.g. cataract prices• Restricted hospital networks to drive down price (trading off access)• Change Commonwealth price setting method for prostheses by using actual RFPs

Insurers• Mergers to drive scale (34 funds, only 15 have > 100,000 members)• Regulated fees for price comparators• Regulated minimum cover hospital insurance products to prevent “junk” being sold

that only really prevents MLS and a race to the bottom

Bupa

More Effective CareThe spectre of “managed care” has set back progress in Australia on getting better value for money from the private health sector

Contracting• Activity based efficient pricing, bundled payments, e.g. joint surgery• Reduce non-cost effective care, e.g. back surgery, arthroscopies• Risk sharing or coverage by providers for “defective care”, incentives and disincentives

such as never events and pay for quality (Bupa and Healthscope/Genesis), “market power” stand-offs

Alliance Purchasing• Common care pathways in primary care and across primary/secondary using the GP as

the medical home, e.g. a private insurer wraps an additional programme around the underlying Medicare structure, e.g. Medibank & Sonic, HCF, Bupa

• With a provider to provide a continuum of care for an area such as mental health or rehabilitation for a defined group of members in an area, e.g. Bupa and Ramsay

• Between an insurer/s and a provider/s to put a significant part of their joint business into value-based clinical arrangements such as cardiac care that focus on the Triple Aim of better health, better care and lower costs by a certain date

Bupa

Health Information Exchanges

Myriads of disintegrated health systems• PCIER and Repositories…

• Health information exchanges

• Opportunities to carry out proof of concept pilots between key stakeholders such as public and private hospitals, PHNs and GPs, private health insurersØ E.g. CAHIE’s vision is to provide a California trust framework with pathways

that ensure that all providers can connect to and use the nationally-recognized Direct, Exchange and other vetted protocols that may emerge. CAHIE will assist member organizations with implementations of existing standards, promoting interoperability throughout the state, and will represent California HIOs in the national HIE planning and governance process

Bupa

Access to InformationHealth Content• “The world of digital” and vast amounts of information

• (Stop) Making sense of it…. e.g. FoodSwitch

• Personalised advice by using the individual’s health information

• New settings such as the workplace

Informed Decision Making• Arose out of unwarranted clinical variation research

• Evidence shows more informed consumers typically make decisions that are more evidence based and often less interventionist e.g. osteoarthritis

Transparency around Out of Pocket Costs• “The invoice is in the mail” versus publishing $ range and likelihood data

Bupa

Shared FeedbackContext• NIB and “White coat” on ancillary providers

• Web comparators and forums on providers and health funds

• UK/US style patient feedback platforms, current examples such as Hospital Consumer Assessment of healthcare Providers and Systems (HCAHPS) which is used by HCF and many hospitals and ACSQHC

Opportunity for Industry Wide Feedback Platform• Systemic feedback loop with learning

• Independence and oversight

• Who and what gets judged?

• Time for a broader industry approach and discussions are happening

Questions

Bupa

Bupa

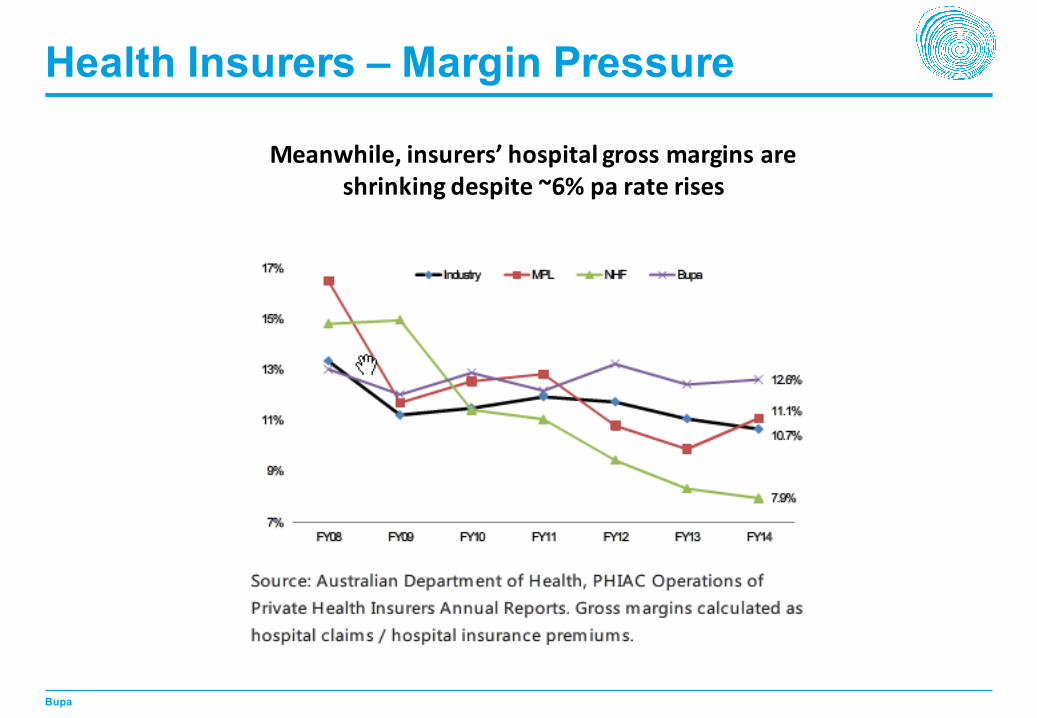

Health Insurers – Margin Pressure

Meanwhile, insurers’ hospital gross margins are shrinking despite ~6% pa rate rises

Bupa

Private Hospitals – Margin Growth

Private hospitals’ EBITDA margins continue expanding