DEMOGRAPHIC DIVIDEND DEMOGRAPHIC DIVIDEND DEMOGRAPHIC DIVIDEND

Dutch Dividend Tax Act 1965

Jeroen van der LindenMarch 17, 2011

Contents

• Who are subject?• What is subject?• Tariff and exemptions• Dividendstripping

Who are subject

- Who are subject to Dutch dividend tax?

• Those who are entitled to the return of shares in, profit certificates or hybrid loans from Dutch resident:- NV’s, - BV’s, - Open CV’s and - other entities whose capital is divided into shares.

1/3

Who are subject

• Dutch cooperatives are not mentioned in the Dutch dividend tax act, however…

• It should by all means be avoided that cooperatives are compared with “other entities whose capital is divided into shares” on the basis of case law.

2/3

Who are subject

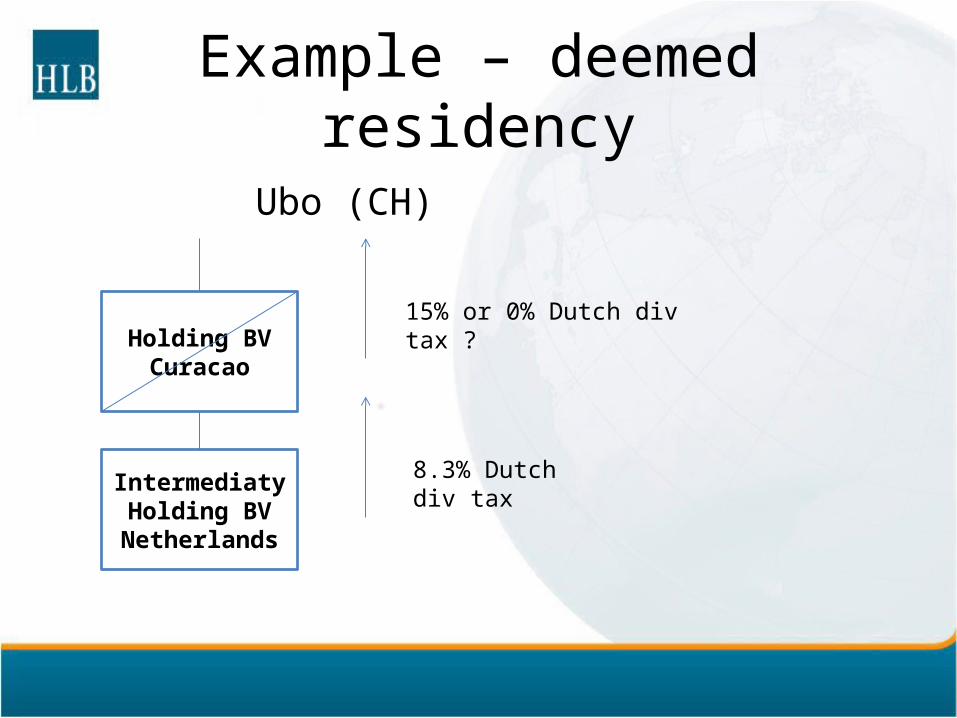

• If the entity was incorporated under Dutch law, it is deemed to be Dutch resident for Dividend tax purposes.

• As a result, Dutch dividend tax claim can remain even if Dutch company was moved abroad.

3/3

Example – deemed residency

Ubo (CH)

Holding BV Curacao

Intermediaty Holding BV

Netherlands

8.3% Dutch div tax

15% or 0% Dutch div tax ?

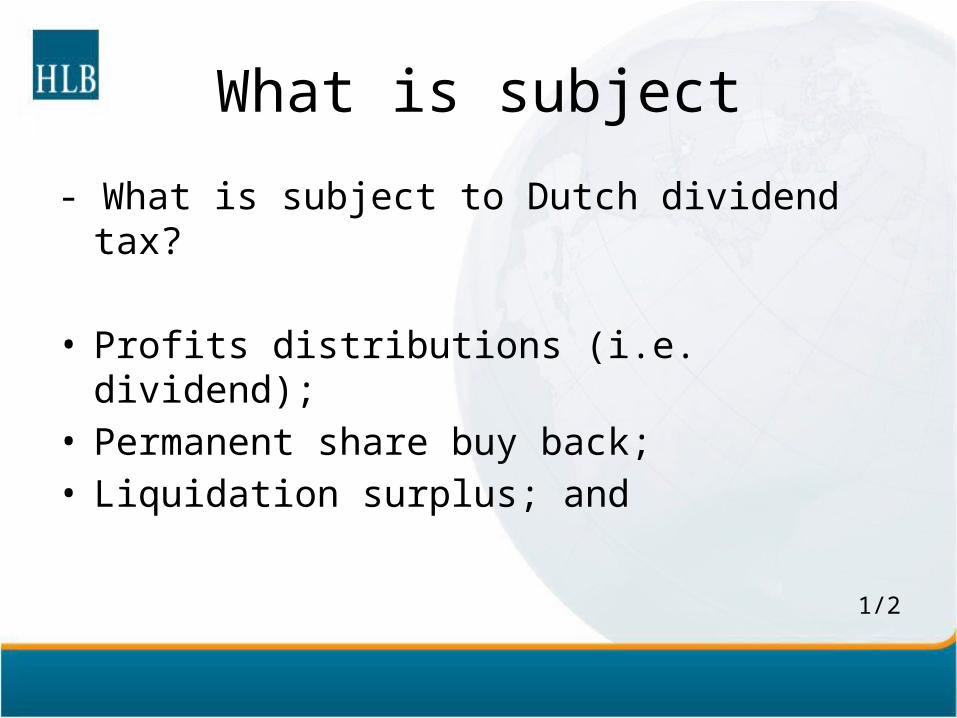

What is subject

- What is subject to Dutch dividend tax?

• Profits distributions (i.e. dividend);• Permanent share buy back;• Liquidation surplus; and

1/2

What is subject

- What is subject to Dutch dividend tax (Cont’d)?

• Bonus shares;• Repayment of sharepremium in case of profit;• “Interest” paid on hybrid loans.

2/2

Tariff and exemptions

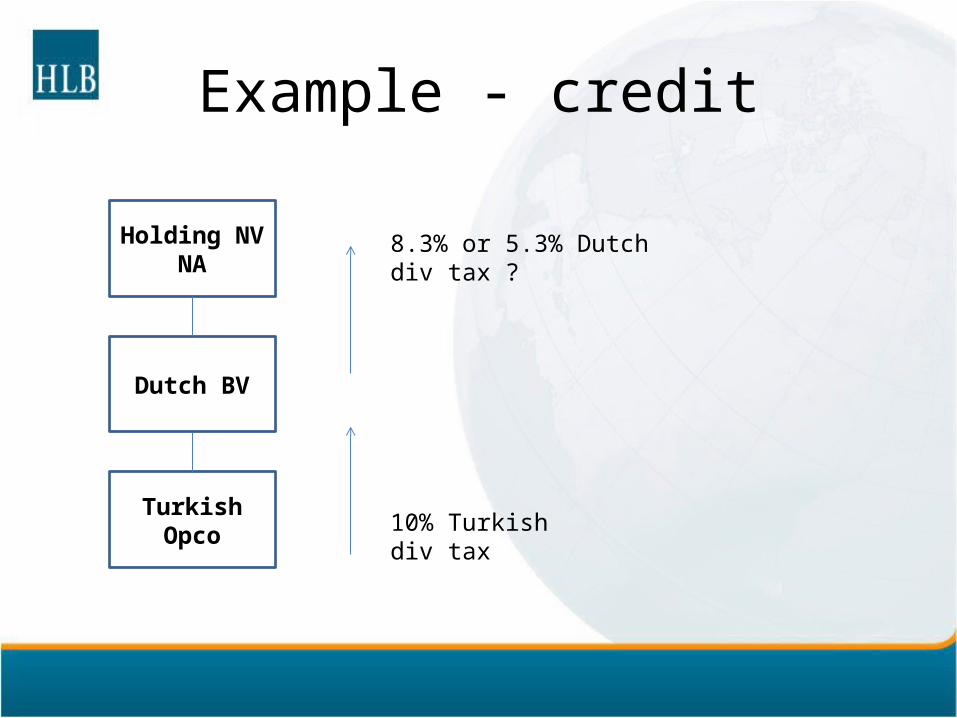

• The Domestic rate is 15% to be withheld by the Dutch company;

• Credit of 3% is available for foreign dividend tax imposed by qualifying subsidiaries.

Example - credit

Holding NV

NA

Dutch BV

Turkish Opco 10% Turkish div tax

8.3% or 5.3% Dutch div tax ?

Tariff and exemptions

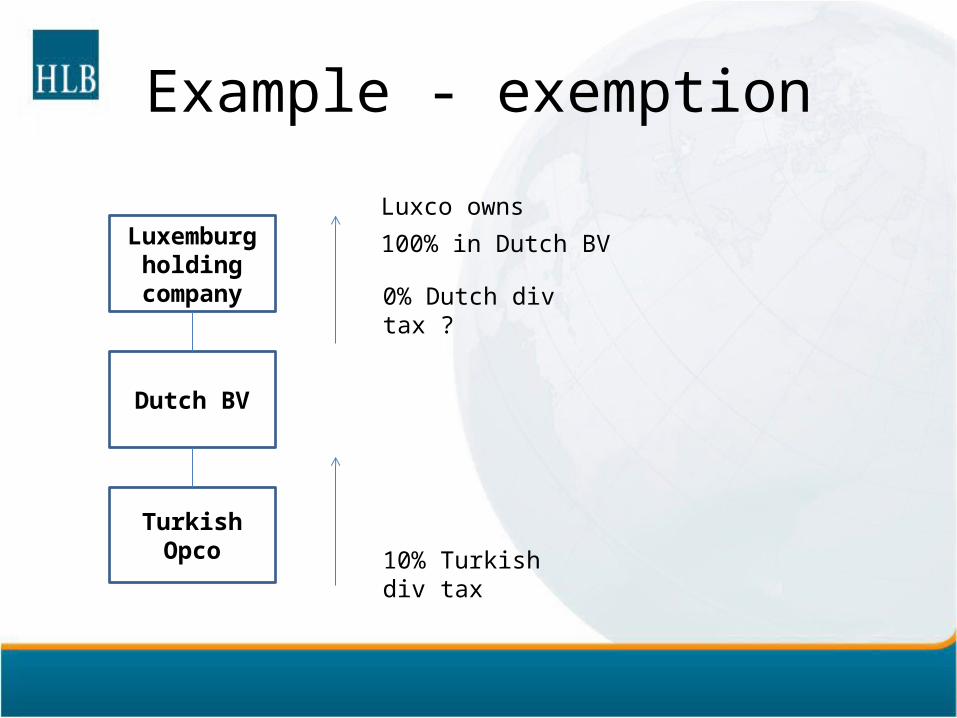

- Exemptions apply:

• If recipient can apply the Dutch participation exemption

• If EU recipient could apply the Dutch participation exemption as if he would be residing in the Netherlands

Example - exemption

Luxco owns

100% in Dutch BVLuxemburg holding

company

Dutch BV

Turkish Opco10% Turkish div tax

0% Dutch div tax ?

Tariff and exemptions

- Exemptions apply (Cont’d):

• If paying entity and recipient form fiscal unity;• If recipient is a qualifying investment company or

(green) fund that promotes certain sustainable projects.

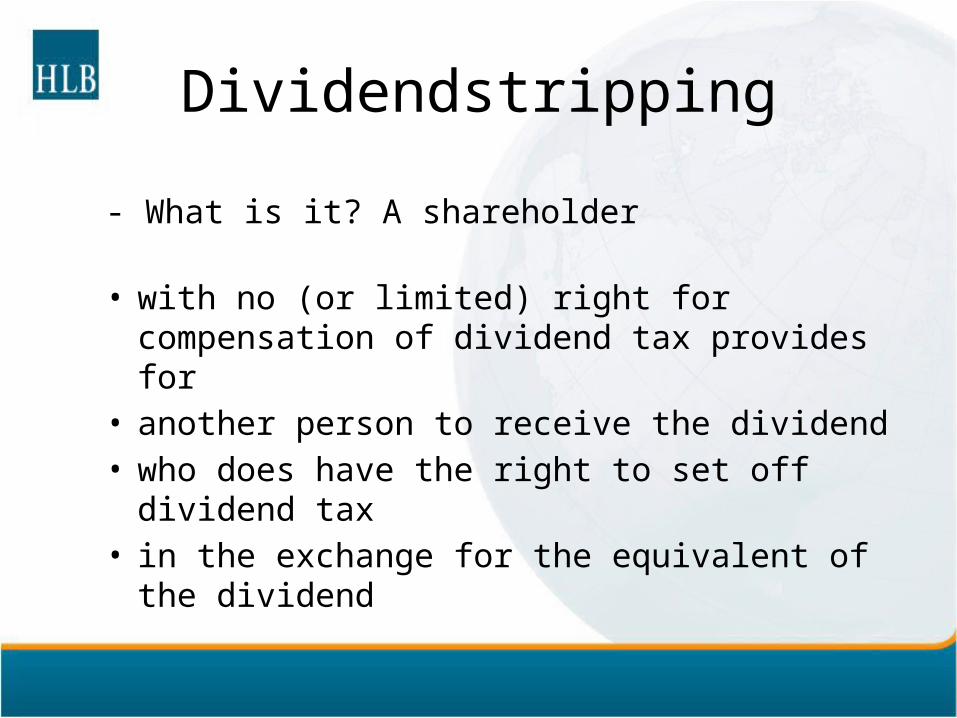

Dividendstripping

- What is it? A shareholder

• with no (or limited) right for compensation of dividend tax provides for

• another person to receive the dividend• who does have the right to set off dividend tax• in the exchange for the equivalent of the dividend

Example - dividendstripping

The Netherlands

Abroad

15% dividend

tax

Dividend distribution 100 Dividend tax 15Net 85

Private individual

BV

1/3

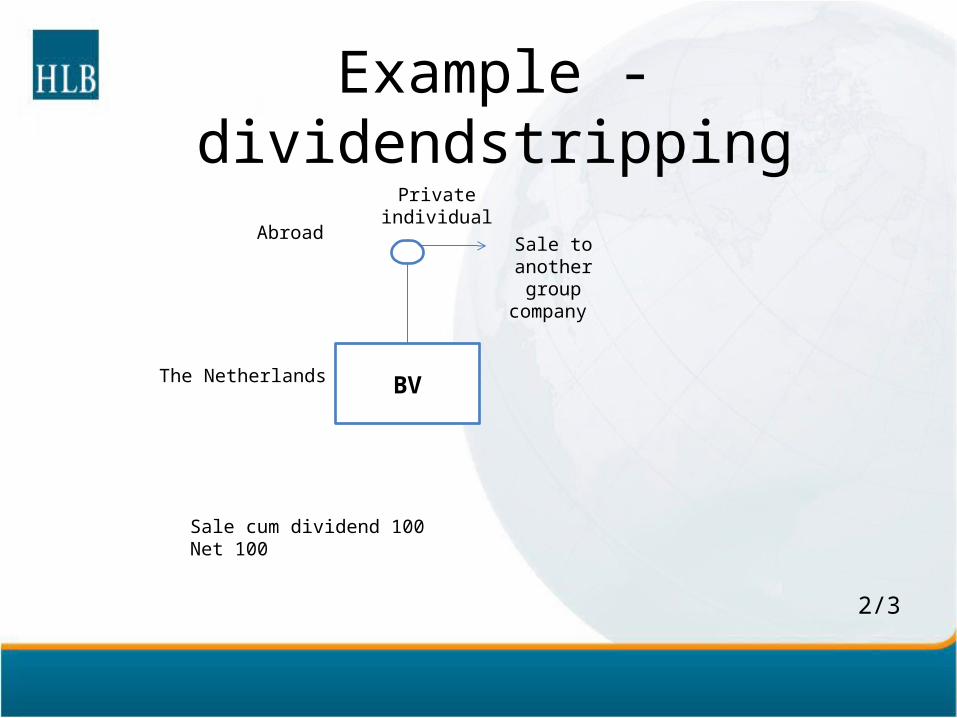

Example - dividendstripping

Sale cum dividend 100Net 100

BVThe Netherlands

AbroadSale to

another group

company

Private individual

2/3

Example - dividendstripping

0% dividendtax

The Netherlands

Abroad

100%

Private individual

BV

SRL

3/3

0% dividendtax

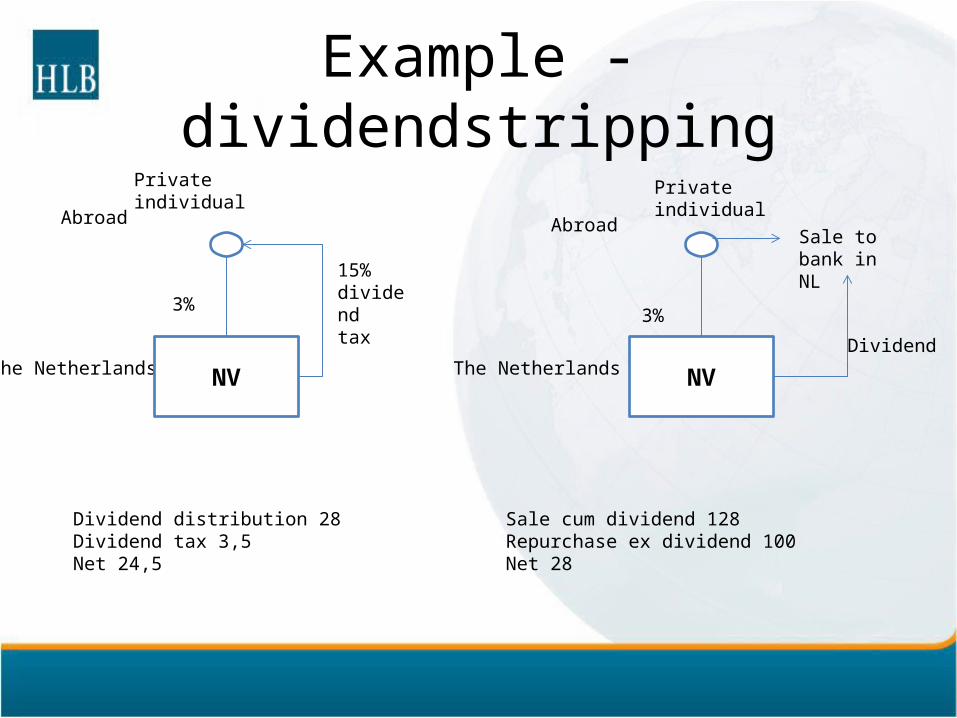

Example - dividendstripping

The Netherlands

Abroad

3%

15% dividendtax

Dividend distribution 28 Dividend tax 3,5 Net 24,5

Sale cum dividend 128Repurchase ex dividend 100Net 28

NVThe Netherlands

Abroad

3%

Sale to bank in NL

Dividend

Private individualPrivate individual

NV

Dividendstripping

- Examples of situations whereby dividendstripping can be recognised:

• Sale shares in Dutch listed companies to bank• Lending of shares• Sale and repurchase (call- and putoptions)• Hanging within concern• Intermediate holding company

Example - intermediate holding

NL BV

Canada Ltd

10% dividend taxCyprus Ltd

0% dividend tax

0% dividend tax

NL BV

B CH

15% dividend tax

Example - intermediate holding

Cyprus Ltd

0% dividend tax

0% dividend tax

Dividendstripping

- Measures against dividendstripping:

• Introduction definition beneficial owner• Sanction: reversing reduction or exemption to

domestic tariff of 15%

Dividendstripping

- When is a person not considered to be a beneficial owner?

• Recipient performs a service which is a part of several transactions

• In exchange for the income• Which income will actually be received by the holder

of the restricted right and• This holder keeps its position in the company

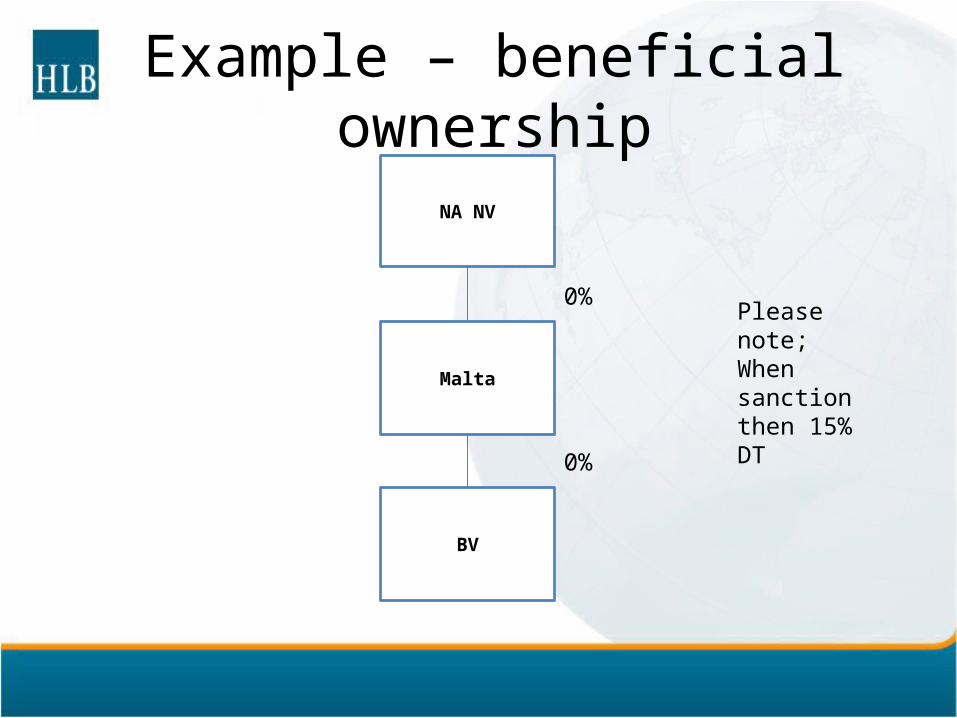

Example – beneficial ownership

NA NV

BV

8,3%Malta

0%

0%

Please note;When sanction then 15% DT

NV1

COÖPNV2

NV2 looses it’s current position, consequently no sanction

BVsale

Example – beneficial ownership

Dividendstripping

- Bonafide cases

• Bonafide purchaser on the stock exchange• Bonafide withholding agent (based on declaration

recipient of dividend)• Durable reorganisation combined with an ordinary

dividend distribution

Dividendstripping- Durable reorganisation

• Time between reorganisation and dividend distribution

• Type of dividend distribution• Durableness reorganisation

Safe Harbour: In case of durable reorganisation in combination with an ordinary dividend distribution irrespective of the time between reorganisation and dividend distribution

The End