du pont 2005 Annual Meeting Proxy Statement

82

1 New York November 7, 2005 Actions to Increase Shareholder Value Actions to Increase Shareholder Value

-

Upload

finance9 -

Category

Economy & Finance

-

view

334 -

download

1

Transcript of du pont 2005 Annual Meeting Proxy Statement

1

New YorkNovember 7, 2005

Actions to Increase Shareholder

Value

Actions to Increase Shareholder

Value

Investment Community Meeting

Investment Community Meeting

Carl Carl LukachLukachVice President, Investor RelationsVice President, Investor Relations

WelcomeWelcome

3

Agenda

9:00 AM Opening Remarks Chad HollidayProductivity Advancement Richard GoodmansonCapital Deployment Gary PfeifferGrowth Acceleration Tom ConnellyBio-Based Materials Expansion Tom Connelly

10:00 AM Q & A

10:30 AM Closing Remarks Chad Holliday

4

Emergency EXIT

Emergency EXIT

5

Regulation GThe attached charts include company information that does not conform to generally accepted accounting principles (GAAP). Management believes that an analysis of this data is meaningful to investors because it provides insight with respect to ongoing operating results of the company and allows investors to better evaluate the financial results of the company. These measures should not be viewed as an alternative to GAAP measures of performance. Furthermore, these measures may not be consistent with similar measures provided by other companies.

This data should be read in conjunction with previously published company reports on forms 10-K, 10-Q and 8-K. These reports along with reconciliations of non-GAAP measures to GAAP are available on the investor center of www.dupont.com.

6

During the course of this presentation, I would like to remind you that we may make forward-looking statements. All statements that address expectations or projections about the future are forward-looking statements. Some of these statements include words such as ‘expects,’ ‘anticipates,’‘plans,’ ‘intends,’ ‘projects’ and ‘indicates.’ Although they reflect our current expectations, these statements are not guarantees of future performance, but involve a number of risks, uncertainties, and assumptions. We urge you to review DuPont's SEC filings, particularly its latest annual report on Form 10-K and quarterly reports on Form 10-Q, for a discussion of some of the factors which could cause actual results to differ materially.

Forward-Looking Statement

Chad HollidayChad HollidayChairman & Chief Executive OfficerChairman & Chief Executive Officer

Actions to Increase Shareholder

Value

Actions to Increase Shareholder

Value

8

Put Science To Work

Go Where The Growth Is

One DuPont - Productivity

Dynamic Science Company

Richard GoodmansonExecutive Vice President & Chief Operating Officer

Productivity AdvancementProductivity Advancement

10

Productivity Advancement

Stake $1B cost improvement over 3 years $1B reduction in net working capital over 3 years

Scope All supply chainsAll support functions

Approach Significant down-payment in 2006Extensive re-engineering for simplification and standardization (streamlining)

Performance Quarterly Fixed Cost as % of Sales Metric

11

Discussion Structure

Fixed Cost Momentum

Tight CostControl

Support Processes

‘05Costs

Lean Supply Chain

2006 2007 2008

Support Processes

Streamline

12

Total Fixed Cost* ($B)2000 - 2004

$13.7

$12.860

0.9

0.31.1 (1.4)

(2.5)

2000 Portfolio CurrencyPension/OPEBS/Stock Opts

Volume Inflation Cost Reductions

2004

0.7

* Excludes Significant Items

13

Discussion Structure

Fixed Cost Momentum

Lean Supply Chain

2006 2007 2008Tight Cost

Control

Support Processes

Support Processes

‘05Costs

Streamline

14

’06 Fixed Cost Momentum ($MM YOY)

• Growth Investments: $ 220- China capacity: $70- Major programs (increases): $120- Other (e.g. regulatory, security): $30

• Wage/Salary Increases 180

• Other People Costs 70(e.g. health care, options expenses)

• Depreciation 30Prior year investments (e.g. SAP)

• Currency Translation ?

• Purchased Goods/Services Inflation ?________$ 500 MM+

15

Discussion Structure

Fixed Cost Momentum

Lean Supply Chain

2006 2007 2008Tight Cost

Control

Support Processes

Support Processes

‘05Costs

Streamline

16

Tight Cost ControlPlatforms

A&NFunctions Corporate SBU SBU TOTALS

Finance $ $ + $

HR

IT

Sourcing __________ _________

Totals $ $ + $ $

ILLUSTRATIVE

Set Non-NegotiableStretch Goals

Generate Options

Optimize Trade-offs

17

Generate Options

Staffing Optimization $ 60 – 100 MM

Other HR Opportunities 60 – 70

Functional Optimization 100 – 150

Strengthen Contract Mgt. 30 – 40

POTENTIAL $250 – 360 MM

18

Discussion Structure

Fixed Cost Momentum

Lean Supply Chain

2006 2007 2008Tight Cost

Control

Support Processes

Support Processes

‘05Costs

Streamline

19

The Bigger Opportunity –Streamline Core Processes

Manage the Corporation & Business Portfolio

Marketing Processes

Provide Solutions (Supply Chain)

Develop New Technologies, Products, Services

Sales Processes

Manage Physical ResourcesAccounting and Finance

Manage People ResourcesManage Information / Knowledge

20

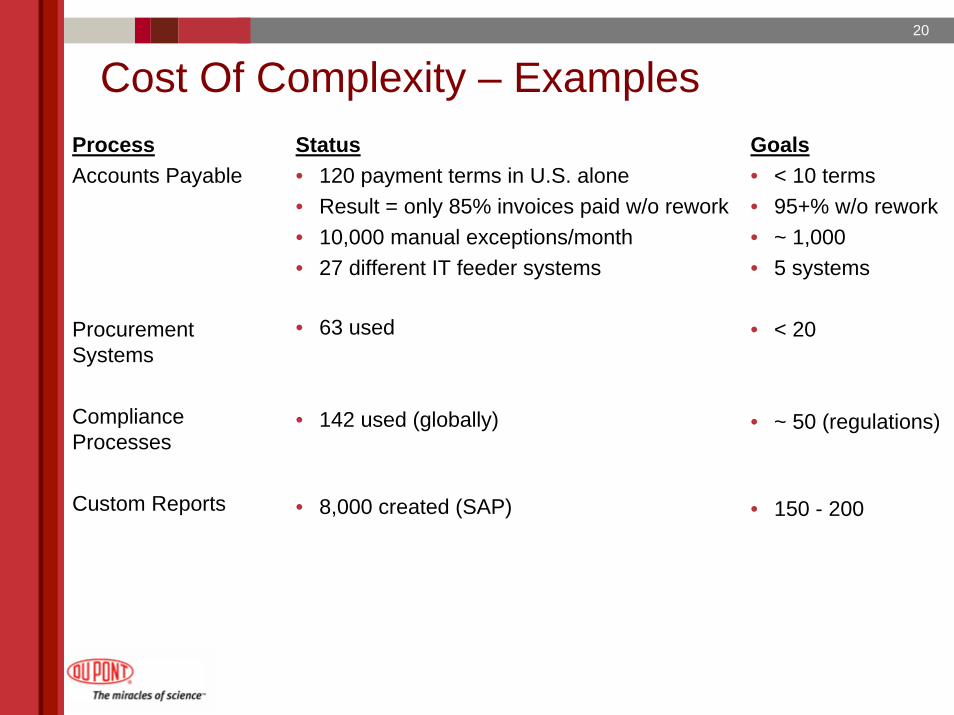

Cost Of Complexity – ExamplesProcessAccounts Payable

Procurement Systems

Compliance Processes

Custom Reports

Status• 120 payment terms in U.S. alone• Result = only 85% invoices paid w/o rework• 10,000 manual exceptions/month• 27 different IT feeder systems

• 63 used

• 142 used (globally)

• 8,000 created (SAP)

Goals• < 10 terms• 95+% w/o rework• ~ 1,000• 5 systems

• < 20

• ~ 50 (regulations)

• 150 - 200

21

Execution Through Six Sigma Project Teams

• Understand Current Processes• Identify Performance Gaps• Use Kaizen for Improvement

• Define Simplified “Best” Process• Assess Conformance & Benchmarks• Establish Standards & Metrics

• Agree Entitlement• Shift Process Capability• Drive Uniformity

QuickWins

StandardizedApproach

Transformation

Execution Through Six Sigma Project Teams

“Tried & True” Approach

22

Lean Supply ChainThe Destination:

Examples of Benefits:

• Waste elimination• Faster order lead times• More capacity• Less inventory/obsolescence• Quicker changeovers• More efficient warehousing• Transport optimization

Transform capability over 3-4 years:• Retain differentiation at lower cost• Improve service level and response time• Be flexible / adaptive

Lean Supply Chain Expectations

0

200

400

600

800

1000

1200

2006 2007 2008

$MM Earnings

NWCImprovement

Lean Supply Chain Expectations

23

Lean Example – One Business Unit

Pre-Lean Situation

• Inventory: 103 days

• Service level outliers: 18.3%

• 2nd Quality sales: 5%

• Distribution expenses: $145 MM

To Date

• 17% improved…$81MM cash freed

• 24% improved

• 29% reduced

• Saved $15MM YTD

24

Discussion Structure

Fixed Cost Momentum

Lean Supply Chain

2006 2007 2008

Streamline

Tight CostControl

Support Processes

Support Processes

‘05Costs

25

HR ExampleObjectives

• Outsource transaction activities

• Implement global SAP platform

• Strengthen HR role to create more business impact

Timing

11/04 - RFP6/05 - Due Diligence

10/05 - Agreement6/06 - Global blueprint

12/07 - Complete

Impact

• Costs down 20-30% over contract life

• Costs variabilized

• Stronger people processes

26

High

Low

IT B

usin

ess I

mpa

ct

(Effe

ctive

ness

)Hackett IT Value Grid

Key Efficiency Drivers+ On-time project delivery+ Number of help desk calls+ Number of programming languages,

database platforms+ Number of network protocols and

data centers- Business standardization and

adherence- Technology infrastructure cost per

end user- On-budget project delivery

Key Effectiveness Drivers+ Member of executive committee+ Orders, payments remittances,

expense reports transmitted electronically

+ Help desk call resolution+ Number of hardware suppliers- Internal SLAs met- Project adhered to standard

methodology- Planning and strategy staff and

costsHighIT Efficiency

Companies in database= SBU

World Class

G&A BenchmarkingOne SBU

27

High Level Benchmarks

20%

30%

25%

0%Cost/$SpendSourcing

Cost/$RevenueFinance

Cost/UserIT

HR Staff/1000 EmployeesHR

DuPont vs. Median

World ClassMedianDuPont

28

Streamlining Opportunity $MM PTOI

Supply Chain Work Plan (over 3 years):

- NWC improvement $1,000

- Annual earnings 600

Other Functions: Gap to Median

- HR $ 60

- IT 200

- Finance 90

- Sourcing 0

29

Broad-Based Severance Not Required

Annual attrition* ~2,000

Displacing variable staff ~1,000

Business growth & improvement projects ~1,000

Redeployment potential ~4,000

Headcount

* e.g. U.S. – 2,500 fully pension eligible

Expected Staffing Needs

30

Productivity Advancement

Lead: Goodmanson

Tight Cost Control

HodgsonBorelGiblin

Streamline Projects

Supply Chain: JohnsonSourcing: CoeFacilities: PorterFinance: PfeifferHR: BorelIT: Ridout

“Best Quartile”Benchmarking

LinsenmannHackett Group

2006 OperationalPlanning

Operating Team

CapitalDeployment

Pfeiffer

InnovationChoices

Connelly

31

TimelineG&A Benchmarking Oct Nov Dec 1Q06 2Q06 3Q06 4Q06Pilot (Hackett)

Execute Pilot

Conduct Co-wideProgram

Execute Co-wideProjects

Streamline

Design

Conduct PilotsExecute PilotsExtendProcesses/Projects

‘05 ‘06

32

Transparency – Metrics ReportedFixed Cost* as a percent of Segment Sales

1 Qtr 2 Qtr

43.1%40.5

38.6

43.240.7

38.9

50.746.7 47.0 48.7

47.0

3 Qtr 4 Qtr2003

2004

2005 * Excludes T&I segment and significant items

33

Productivity Advancement

Stake $1B cost improvement over 3 years $1B reduction in net working capital over 3 years

Scope All supply chainsAll support functions

Approach Significant down-payment in 2006Extensive re-engineering for simplification and standardization (streamlining)

Performance Quarterly Fixed Cost as % of Sales Metric

Gary PfeifferSenior Vice President & Chief Financial Officer

Capital DeploymentCapital Deployment

35

Capital Deployment

Stake Additional 3 point increase in ROIC

Scope All businesses with RONA < 12%

Approach Reallocation of resources (cost and capital) aligned with shifts in strategy, business model, mission. 18 month action plan.

PerformanceMetric Return on Net Assets =

After-Tax Operating IncomeSegment Net Assets

36

Return on Invested Capital*

0%

5%

10%

15%

20%

2001 2002 2003 2004

DuPont Proxy Frame of Reference

*Before Significant Items

GOAL

37

Current StateSegment Net Assets*

% with RONATotal >12% <12%

Agriculture & Nutrition $ 7.2 74% 26%

Coatings & Color Technologies $ 3.8 66% 34%

Electronic & Communication Technologies $ 2.2 49% 51%

Performance Materials $ 3.9 43% 57%

Safety & Protection $ 2.6 72% 28%

$19.7 64% 36%• 12 month average ending 9/30/05;

excludes significant items.

38

Current StateReturn on Net Assets (RONA)

Net Assets (1) RONA (2)

Above (Below)

$ % Total Average CoC

Growth Platforms $19.7 100% 15% 3 pts

(1) 12 month average ending 9/30/05(2) 12 months ending 9/30/05;

excludes significant items.

39

Net Assets (1) RONA (2)

Above (Below)

$ % Total Average CoC

Growth Platforms $19.7 100% 15% 3 pts

> 12% $12.5 64% 23% 11 pts

(1) 12 month average ending 9/30/05(2) 12 months ending 9/30/05;

excludes significant items.

Current StateReturn on Net Assets (RONA)

40

Net Assets (1) RONA (2)

Above (Below)

$ % Total Average CoC

Growth Platforms $19.7 100% 15% 3 pts

> 12% $12.5 64% 23% 11 pts

0 - 12% 5.0 25% 5% (7 pts)

(1) 12 month average ending 9/30/05(2) 12 months ending 9/30/05;

excludes significant items.

Current StateReturn on Net Assets (RONA)

41

Current StateReturn on Net Assets (RONA)

Net Assets (1) RONA (2)

Above (Below)

$ % Total Average CoC

Growth Platforms $19.7 100% 15% 3 pts

> 12% $12.5 64% 23% 11 pts

0 - 12% 5.0 25% 5% (7 pts)

< 0% 2.2 11% (6%) (18 pts)

(1) 12 month average ending 9/30/05(2) 12 months ending 9/30/05;

excludes significant items.

42

Current StateReturn on Net Assets (RONA)

Net Assets (1) RONA (2)

Above (Below) $ % Total Average CoC

Growth Platforms $19.7 100% 15% 3 pts> 12% $12.5 64% 23% 11 pts0 - 12% 5.0 25% 5% (7 pts)< 0% 2.2 11% (6%) (18 pts)

RONA < 12% Commonalities:- Dependence on U.S. Natural Gas- “Distressed” Market Space- Strong Commoditization Trend

or- Embryonic

(1) 12 month average ending 9/30/05(2) 12 months ending 9/30/05;

excludes significant items.

43

Range of Possible Actions

1. Adjust business strategy, business model and/or resource levels to earn RONA >12% across a business cycle

or2. Reduce resource levels – cost and capital – to

support only “operate and maintain safely” (cash mission)

or3. Monetize

44

Capital Deployment

Lead: Pfeiffer

Execution Plans Execution Progress TrackingSWAT Teams (6) Donnelly BeryBusiness Leaders Fyrwald

KeeferKullmanNaylor

2006 Operational PlanningOperating Team

45

Tracking ProgressKey Metric: RONA

Timeline

• Finalize ’06 Execution Plans 12/14/05- Set Compensation Metrics

• Report Progress on RONA Improvement 1/24/064/25/067/25/06

10/24/06

46

Capital DeploymentProgress Report

0 – 12 % <0%<0%

Segment Net Assets Average Segment Net Assets Average

$B % Total RONA $B % Total RONA

09/30/05 5.0 25% 5% 2.2 11% (6%)

12/31/05

03/31/06

06/30/06

09/30/06

12/31/06

Note: 12 months ending;excludes significant items.

47

Capital Deployment

Stake Additional 3 point increase in ROIC

Scope All businesses with RONA < 12%

Approach Reallocation of resources (cost and capital) aligned with shifts in strategy, business model, mission. 18 month action plan.

PerformanceMetric Return on Net Assets =

After-Tax Operating IncomeSegment Net Assets

Tom ConnellyTom ConnellySenior Vice President & Chief Science and Technology Officer Senior Vice President & Chief Science and Technology Officer

Growth Acceleration Growth Acceleration

49

Growth Acceleration

Stake $850MM growth revenue in ’06 from new productsFurther 30% increase in innovation productivity by 2010

Scope All growth technology and marketing investments

Approach Reprioritize for current realities:- Increase resourcing of critical projects- Shut down marginal projects

Performance Percent of revenue from new productsMetrics Growth revenue from new product sales

50

Innovation Choices: Examples

Accelerated Growth Investments• Molecular Breeding• GLY/SU Input Traits• CPP Late Pipeline• New Nonwovens• Asia Resourcing

Restricted Growth Investments• Commodity Polymers• Commodity Coatings• Others

Fewer, Better-Resourced Growth Projects• All SBUs

• Bio-Materials/Fuels• BioSurfaces• BioMedical• I/C Materials/Packaging• PV Materials

51

Clear Momentum

4000

5000

6000

7000

8000

2000 2001 2002 2003 2004

$630 MM Top Line Growth Revenuefrom New Products Commercialized in 2004

30% of Total Sales

Sales From New Products New Products Commercialized

774

902

2004 Total

3Q 2005 YTD

$ M

illio

ns

52

Rich Innovation Pipeline Selected Examples

Ag Herculex® ECB + CRW

GLY/SU TraitsGN2 Insecticides E2Y Insecticide

Broad Spec Fung.

Herculex® XTRA Stacks

Stalk Rot Resist.Yield Traits

Drought ToleranceNutrium® Low–Lin SB

Improved Feed+Fuel

SU BlendsSteward ®/Avaunt®

Proof of Concept & Early Development Adv. Development Launched

Herculex® XTRA + GLY/SU StacksEnhanced Soy Texture/Flavor

53

Rich Innovation PipelineSelected Examples

Elect.Hydrogen FC

FED Materials

Next Gen Refrig

Embedded Passives

PV Enhancements

DMFC

OLED Materials

Thermal Color Filters

Cyrel® FAST/Digital

PV MaterialsFodel® for PDP

Pyralux®Refrig Blends

Early Development Adv. Development Launched

Safety Magellan M5 HighStrength Fiber

TYV 202Tyvek® RoofingTyvek® Flashing

Kevlar® Adv. BallisticOn-Site SAR Units

Medical Fabrics

High performance sheet structures and

filtration media

Chem/Bio Protection

Biofilm treatment / elimination

C-cable Resins

Clean & DisinfectPower Systems

54

Perf. Mat.

Nanocomposites Green Hytrel®

Sorona® EP

Zytel® HTNBlow Molded EP

SentryGlas® Plus

Early Development Adv. Development Launched

Coat. Global Waterborne Technology

New Ink Jet Dispersions and

ColorantsRadiation Cure

Powder

Super High Solids

Artistri™ Digital

HyperCure™ ClearsLaminate Grade TiO2

Super Durable TiO2

Rich Innovation PipelineSelected Examples

55

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2003A 2004A 2005 2006 2007

Cum

ulat

ive

Top

Line

Gro

wth

(Exc

lude

s re

plac

emen

t)$B

Business Identified Opportunity

Risk Adjusted (Traction Index)

Ag & Nutrition

Electronics

Safety & Protect

Perf MaterialsCoatings & Color

“Top 75” Revenue Projections

56

Growth Acceleration: Tracking Progress

• Total revenue from 5 year products

• Top line growth ($MM)from new products*

33%

700

2005 2006

34%

850

Targets

30%

630

2004Actual

2010

35%(4 yrs)

1,250

• Twice per year Pipeline updates

* Net of cannibalization

57

Growth Acceleration

Stake $850MM growth revenue in ’06 from new productsFurther 30% increase in innovation productivity by 2010

Scope All growth technology and marketing investments

Approach Reprioritize for current realities:- Increase resourcing of critical projects- Shut down marginal projects

Performance Percent of revenue from new productsMetrics Growth revenue from new product sales

Tom ConnellyTom ConnellySenior Vice President & Chief Science and Technology Officer Senior Vice President & Chief Science and Technology Officer

Bio-Based MaterialsExpansion

Bio-Based MaterialsExpansion

59

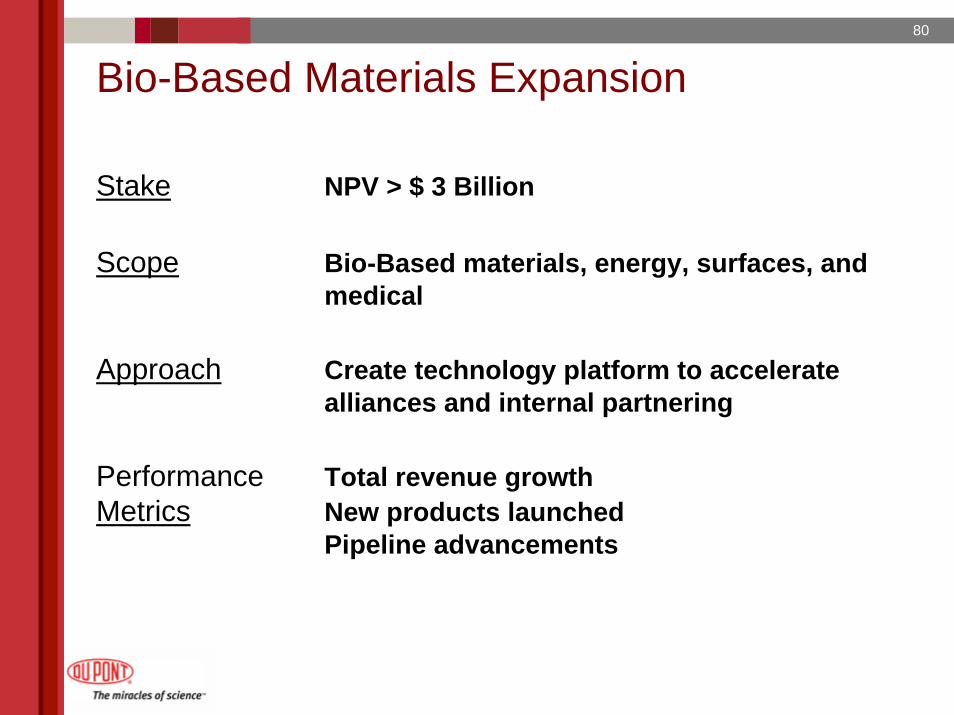

Bio-Based Materials Expansion

Stake NPV > $ 3 Billion

Scope Bio-Based materials, energy, surfaces, and medical

Approach Create technology platform to accelerate alliances and internal partnering

Performance Total revenue growthMetrics New products launched

Pipeline advancements

60

• Materials & Energy• Polymers • Fuels• Chemicals

• BioSurfaces• Personal Care• Fabric and Home Care

• BioMedical• Sealants & Adhesives• Interventional• Dental

Bio-Based Materials

61

0%100%200%300%400%500%600%700%800%

U S N a t . Ga s Oi l ( WTI )P r opy l e ne Gl y c ol C or n

1995 2000 2005

DuPont Bio-Based Materials “The right science at the right time”

62

Bio-Based Materials Strategy

Focus on transformative opportunities:

• Target areas of unique advantage

• Shape the industry with integrated knowledge base

• Establish partnerships to maximize value capture

63

Bio-PDO™

Sorona®

Polymer

Apparel

Elastomers

Fibers

Coatings

EngineeredResins

Flooring

PolyolsNew since

2004

Bio-PDO™ Strategy

Bio-PDO™New since

2004

Direct Applications

Cell software has been re-programmed to increase propanediol production by

500 fold

64

Loudon SiteLoudon SiteSept. 2005 Sept. 2005

DuPont Tate & Lyle BioProducts LLC&TATE LYLE

65

Materials PipelineNPV > $150 Million

Source of Uniqueness• High performance market applications

• Biocatalyst development know-how

• Renewable and sustainable feedstocks

• Sorona® Polymer• Bio-PDO™

• Polyols• Aromatics

• Bio-PDO™Extensions

• Sorona® PolymerExtensions

2006 2007 2008 2010

66

Fuels,Materials,Chemicals

Bio-Based Economy

• Environmental sustainability - energy security

• Biomass - the only renewable source of carbon

MetabolicEngineering

BiomassFeedstock

67

Sustainable Energy

DOE Vision of Oil Savings

Grain

Cellulose

0

5

10

15

20

25

30

35

2000 2005 2010 2015 2020 2025

Year

Eth

an

ol

(Bil

lio

ns

of

gal/

yr)

EXISTING

AdvancedCornMills

EMERGING

SugarPlatform-New Enzymes-Pretreatment-Fermentation

ADVANCED

FundamentalAdvances inLignocelluloseProcessingand fermentation

Re: J.D. McMillan, NREL

68

EnergyNPV >$1.5 Billion

Source of Uniqueness• Proprietary and economical biofuels

• Sustainable biofeedstocks with full value chain integration

• Novel bioprocesses as primary sources of innovation

• BioFuels II

• BioRefinery• Oil Recovery

• Biomass• BioFuels III

Present - 2007 2011 2009 - 2013 2015

• BioFuels I

69

Application• Uniquely specific to surfaces • Water-borne – no solvents• Non-toxic • Programmable placement

– On/off when desired• Novel functionality

BioSurfaces

Combining DuPont’s Biotech & Coatings Know-How

Anchor

Peptides/Proteins

DesiredAttribute

70

BioSurfaces Opportunity / Strategy

• Target high value-in-use– Personal care - hair, nails, oral, skin– Home & fabric care

• Driven by unique technology

• Maximize value capture– Partnerships

71

Source of Uniqueness• Transformational delivery systems that capture significant market value

• Peptides/proteins improve product safety and effectiveness

• Products leverage DuPont’s biology, materials and particle science know-how

BioSurfacesNPV > $300 Million

• Skin Care• Hair Care

• Skin Care Extensions• Hair Care Extensions• Oral Care

• Skin Care Extensions• Hair Care Extensions

• Home & Personal Care

2008 2009 20112010

72

BioMedical

• Sealants & Adhesives

• Dental Monomers

• Interventional Products

73

Tissuesurface

Sealants & Adhesives

Simple, Tunable, IP Protected

DuPont ActaMax™ Surgical Sealants

74

Incumbent ActaMax™***

ProductsSurgeon Needs

Prep time 30 minutes 30 secSet time 10 minutes 15 secBlood derived ingredients Viral carrier* Synthetic**

Patient BenefitsPerformance 3 days 14 + daysInflammatory responses Severe Non-detectableSlow resorption Uncontrolled – variable Tunable 1 - 60 days

* Risk of Hep C, HIV, or BSE** No risk of viral contamination*** Based on pre-clinical studies

ActaMax™ Performance

75

Monomer Formulation Production Distribution Marketing

Dental

DuPont Ultramer

DuPont monomer advantage> 33% less shrinkage

Dental composite manufacturers formulate

Enabling proprietary technology for differentiation

Composite Manufacturers

76

BioMedicalNPV > $1.5 Billion

Source of Uniqueness• Integrated science and engineering in very high value sectors

• DuPont inventions & DuPont/MIT Alliance

• Dental I

• Adhesives• Dental II• Interventional II

• Sealants• Interventional

• BioMedical II

2009 2011 20132007

77

Bio-Based MaterialsRich Innovation Pipeline

Biomass

BioMedical II

BioRefinery

BioFuels IIIBioFuels II

BioFuels I

BioMedical - Sealant

BioMedical – Dental

BioSurfaces – PC I

BioMedical – Interventional

Bio-Aromatics

BioSurfaces – PC III

Bio-PDO™ II

BioSurfaces – PC II

BioMedical – Dental II

BioSurfaces – PC IV

Early Development2010+

Adv. Development2007-2009

Launch2005-2006

Bio-PDO™Polyols

Sorona®EngineeredPolymers

GreenHytrel®

Bio-PDO™Derivatives

Sorona®Apparel

Sorona®Flooring

Bio-PDO™Coatings

Oil Recovery

78

Bio-Based Materials SummaryNPV > $3 Billion

Sorona®Bio-PDO™

Source of Uniqueness• Integrated science and engineering in very high value sectors

• IP and partnerships

Sorona® extBio-PDO™ extPolyolsDental IIBiofuels I & IISkin, Hair & Oral CareSealantInterventional I

Sorona® extBio-PDO™ extPolyolsDental IBiofuels ISkin & Hair Care

Sorona® extBio-PDO™ extPolyolsBioFuels IIIBioRefineryOil RecoverySealantInterventional IIAdhesivesHome & Personal Care

2008 2010 20122006

79

Bio-Based Materials: Tracking Progress

• Total revenue growth

• New products launched

• Pipeline advancements

NPV >$3B from Materials, Energy, BioSurfaces and BioMedical

80

Bio-Based Materials Expansion

Stake NPV > $ 3 Billion

Scope Bio-Based materials, energy, surfaces, and medical

Approach Create technology platform to accelerate alliances and internal partnering

Performance Total revenue growthMetrics New products launched

Pipeline advancements

81

Put Science To Work

Go Where The Growth Is

One DuPont - Productivity

Dynamic Science Company

82