Driving Shareholder Value Managing for the New Millennium

29

Driving Shareholder Value Managing for the New Millennium Dr. Roger A. Morin Georgia State University, Distinguished Professor of Finance Chairman & CEO Utility Research International

-

Upload

octavia-noel -

Category

Documents

-

view

14 -

download

1

description

Driving Shareholder Value Managing for the New Millennium. Dr. Roger A. Morin Georgia State University, Distinguished Professor of Finance Chairman & CEO Utility Research International. FI 8360 Lecture #2 Roadmap. Why Value Value Value and Capital Markets The Value Manager - PowerPoint PPT Presentation

Transcript of Driving Shareholder Value Managing for the New Millennium

Driving Shareholder ValueManaging for the New Millennium

Dr. Roger A. MorinGeorgia State University, Distinguished Professor of Finance

Chairman & CEO Utility Research International

FI 8360Lecture #2 Roadmap

Why Value Value Value and Capital Markets The Value Manager Valuation Frameworks: DCF

NPV, FTE, FCF, APV, etc.

Why Value Value?

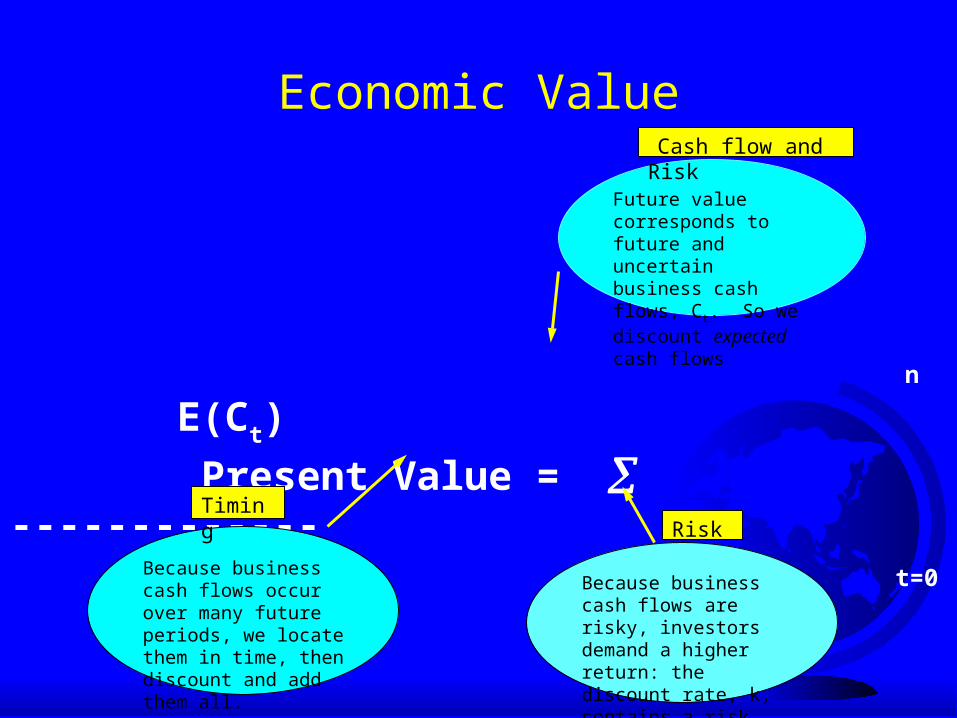

Economic Value

n E(Ct)

Present Value = ------------- t=0 (1 + k)t

Future value corresponds to future and uncertain business cash flows, Ct. So we discount expected cash flows

Cash flow and Risk

Because business cash flows occur over many future periods, we locate them in time, then discount and add them all.

Timing

Because business cash flows are risky, investors demand a higher return: the discount rate, k, contains a risk premium.

Risk

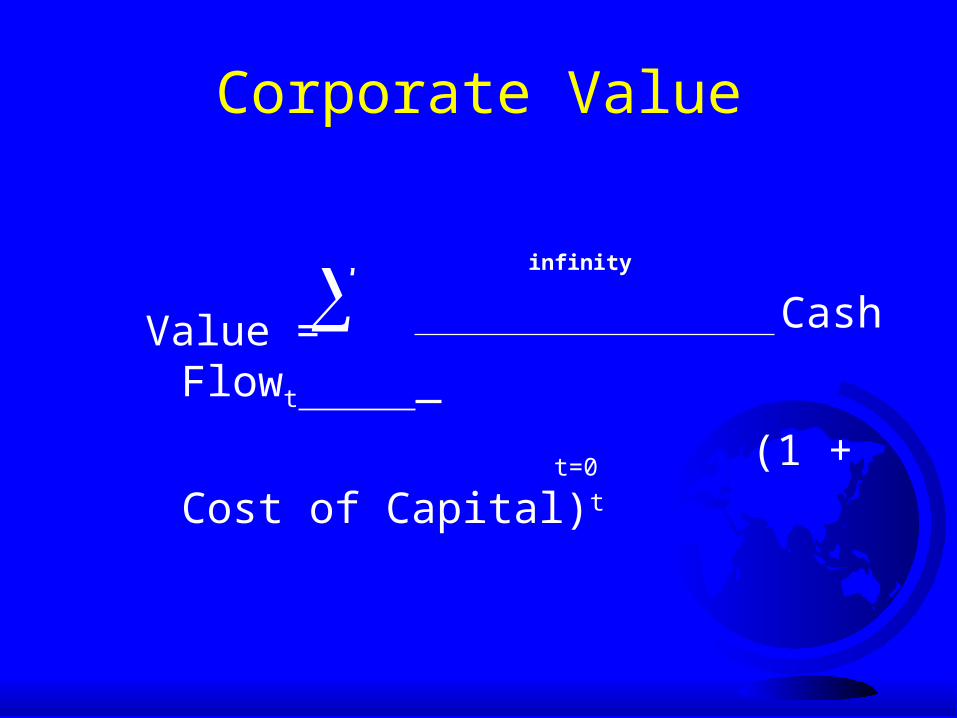

Corporate Value

infinity

Value = Cash Flowt

t=0 (1 + Cost of Capital)t

Shareholder value analysis focuses on the factors that investor use to

value companies:

Cash Flows Long-Term Expected Performance Risk

What is VBM?

A Way of Thinking A Process for Planning and Execution A Set of Tools

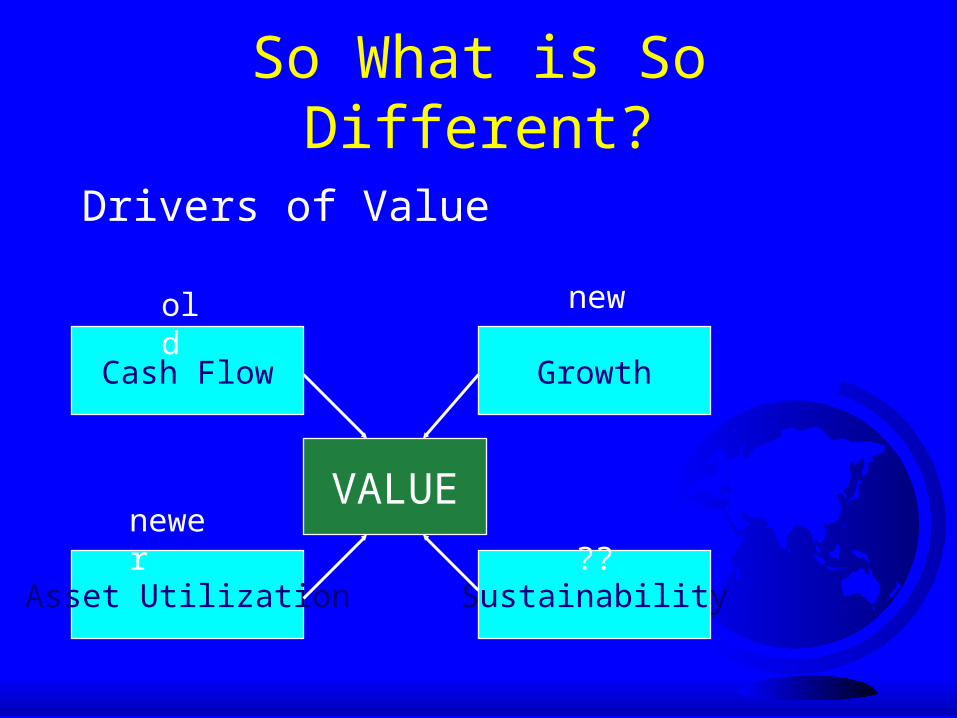

So What is So Different?

Drivers of Value

Cash Flow

SustainabilityAsset Utilization

Growth

VALUE

old new

??newer

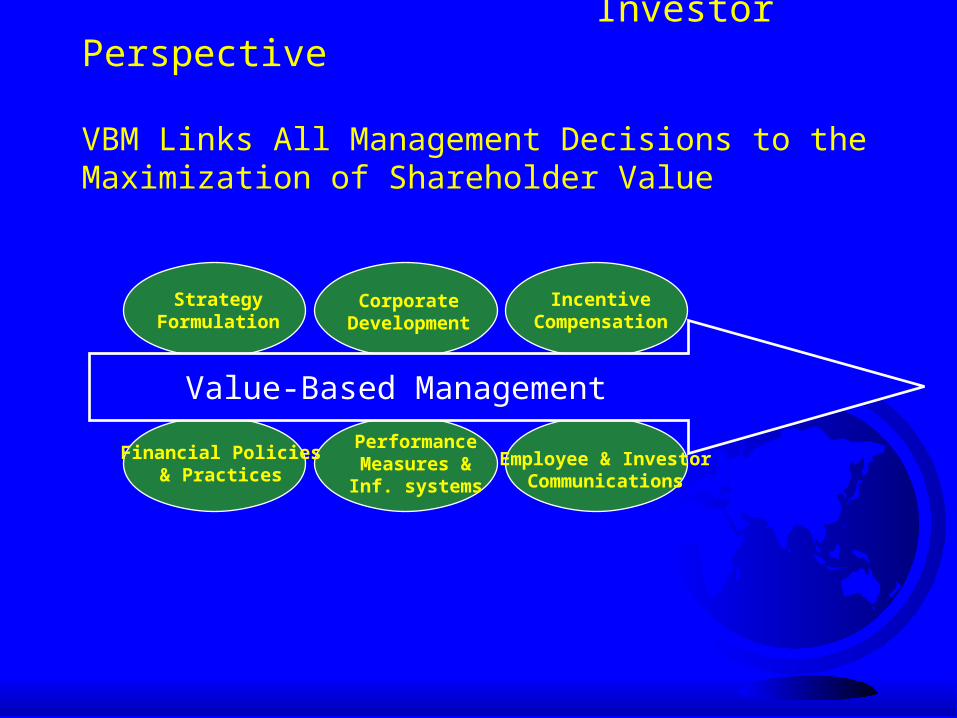

Investor Perspective

VBM Links All Management Decisions to the Maximization of Shareholder Value

Value-Based Management

StrategyFormulation

CorporateDevelopment

IncentiveCompensation

Financial Policies& Practices

PerformanceMeasures &Inf. systems

Employee & InvestorCommunications

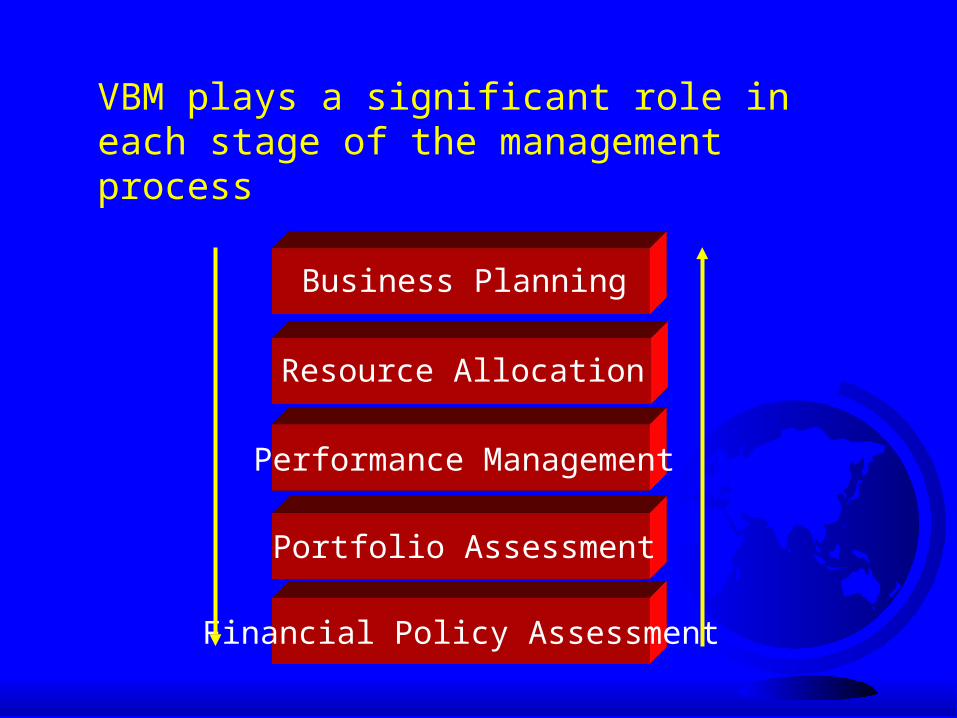

VBM plays a significant role in each stage of the management process

Financial Policy Assessment

Business Planning

Resource Allocation

Performance Management

Portfolio Assessment

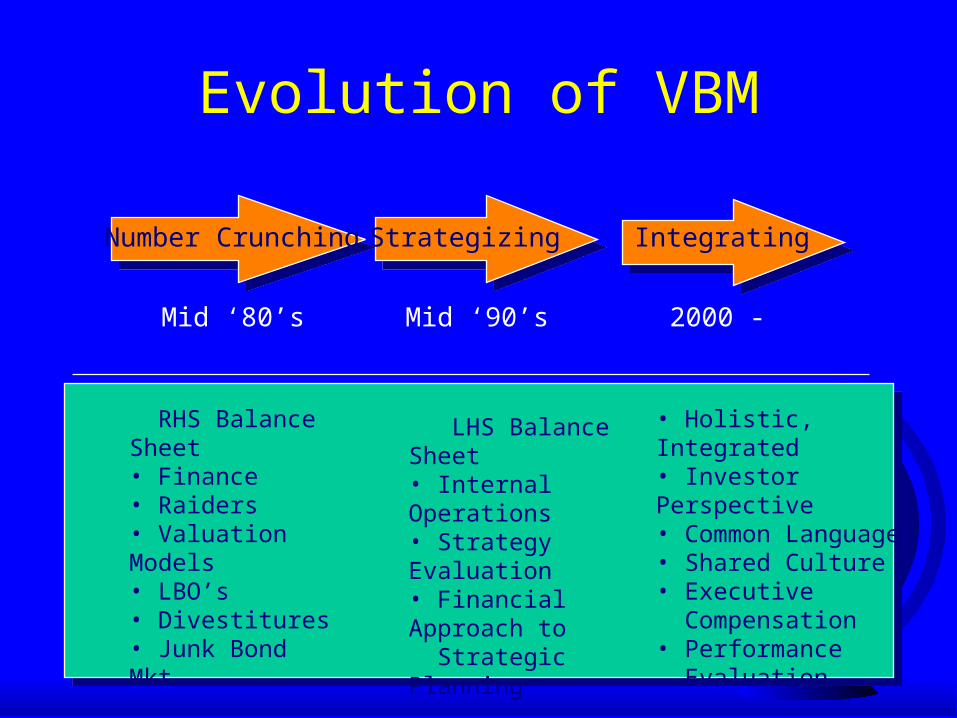

Evolution of VBM

Number Crunching Strategizing Integrating

Mid ‘80’s Mid ‘90’s 2000 -

RHS Balance Sheet• Finance• Raiders• Valuation Models• LBO’s• Divestitures• Junk Bond Mkt

LHS Balance Sheet • Internal Operations• Strategy Evaluation• Financial Approach to Strategic Planning

• Holistic, Integrated• Investor Perspective• Common Language• Shared Culture• Executive Compensation• Performance Evaluation

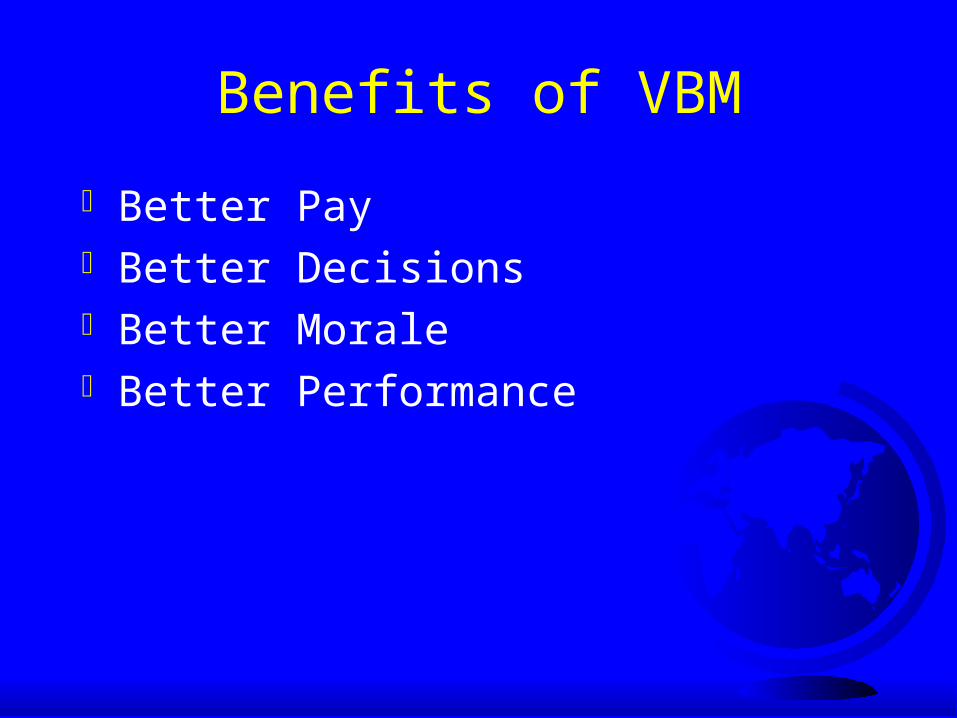

Benefits of VBM

Better Pay Better Decisions Better Morale Better Performance

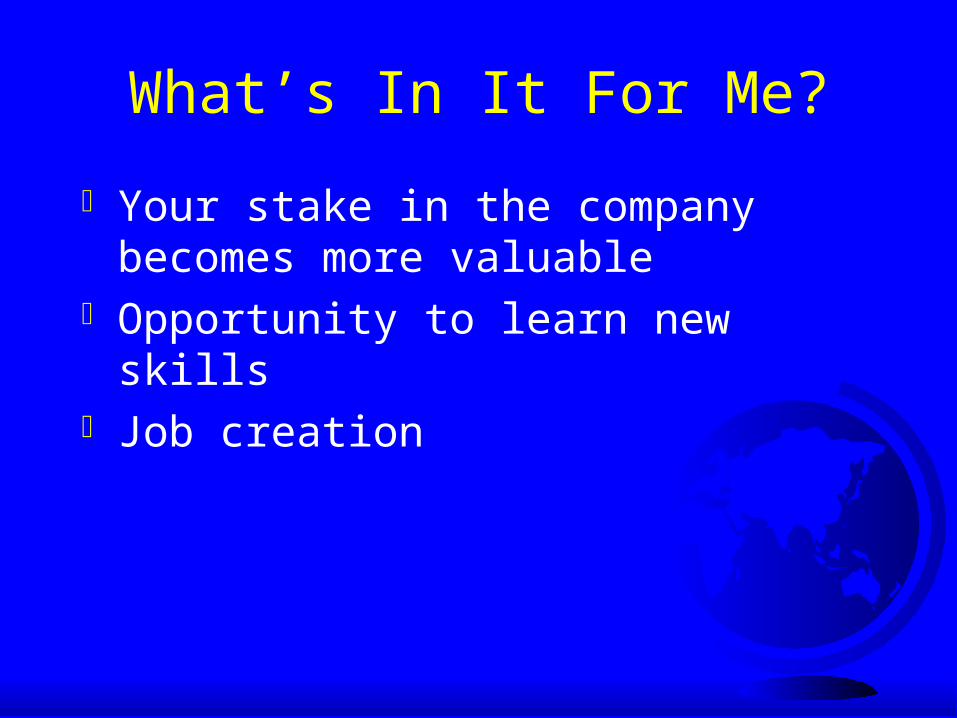

What’s In It For Me?

Your stake in the company becomes more valuable

Opportunity to learn new skills Job creation

Challenge to Create Value

Curse of competition Curse of beating market expectations

Potential Rewards

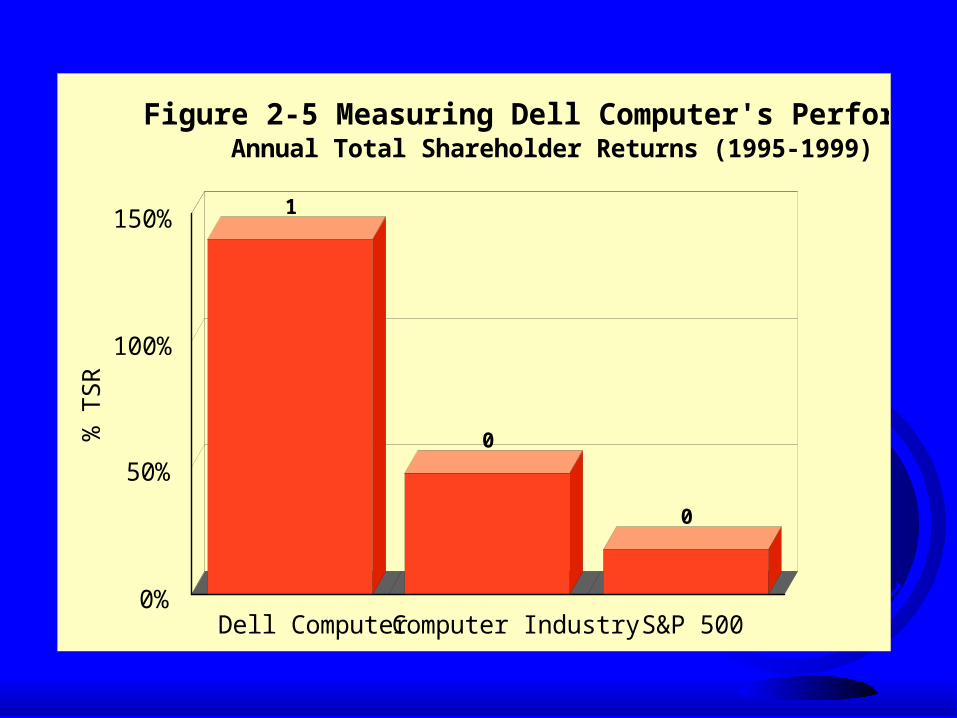

1

0

0

Dell Computer Computer Industry S&P 5000%

50%

100%

150%

% T

SR

Figure 2-5 Measuring Dell Computer's PerformanceAnnual Total Shareholder Returns (1995-1999)

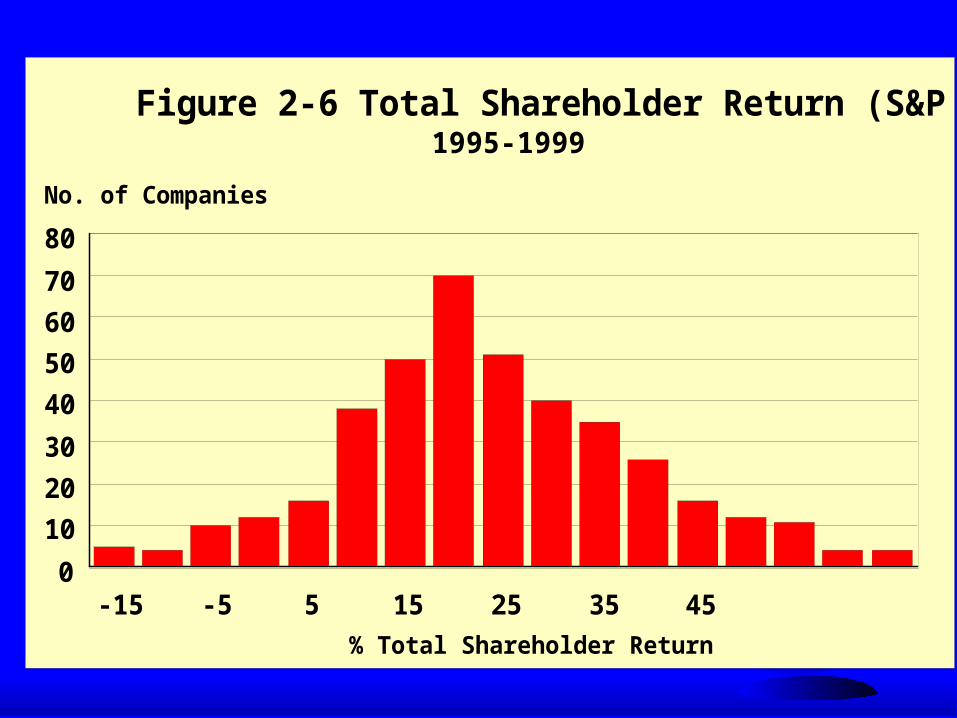

-15 -5 5 15 25 35 45

% Total Shareholder Return

0

10

20

30

40

50

60

70

80

No. of Companies

Figure 2-6 Total Shareholder Return (S&P 500)1995-1999

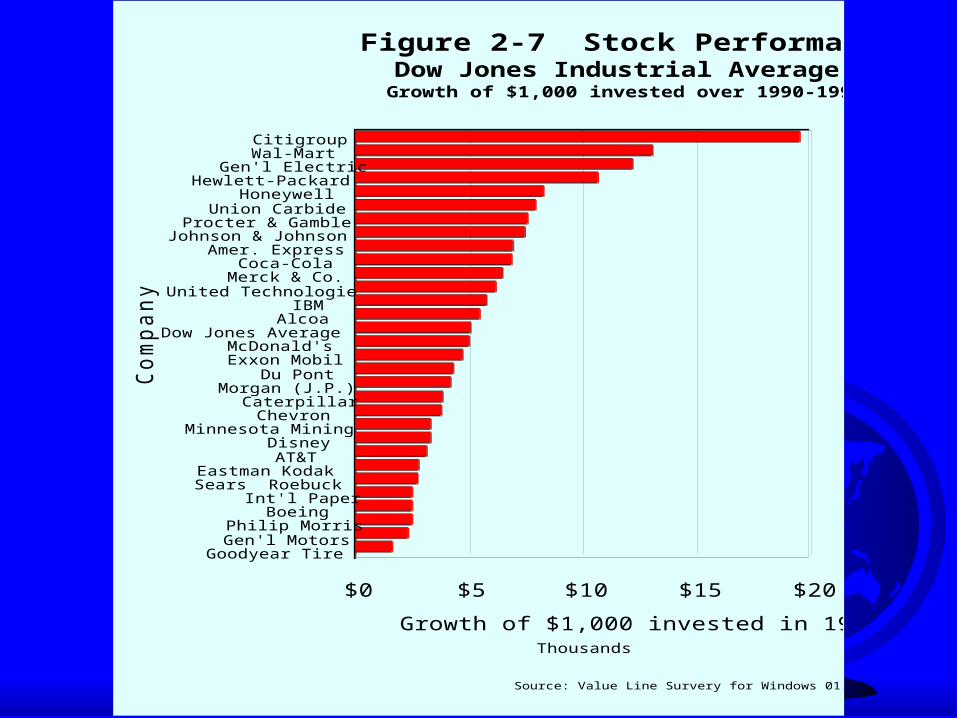

CitigroupWal-Mart

Gen'l ElectricHewlett-Packard

HoneywellUnion Carbide

Procter & GambleJohnson & Johnson

Amer. ExpressCoca-Cola

Merck & Co.United Technologie

IBMAlcoa

Dow Jones AverageMcDonald'sExxon Mobil

Du PontMorgan (J.P.)

CaterpillarChevron

Minnesota MiningDisneyAT&T

Eastman KodakSears Roebuck

Int'l PaperBoeing

Philip MorrisGen'l Motors

Goodyear Tire

Co

mp

any

$0 $5 $10 $15 $20

Thousands

Growth of $1,000 invested in 1990

Source: Value Line Survery for Windows 01/2000

Figure 2-7 Stock PerformanceDow Jones Industrial Average

Growth of $1,000 invested over 1990-1999

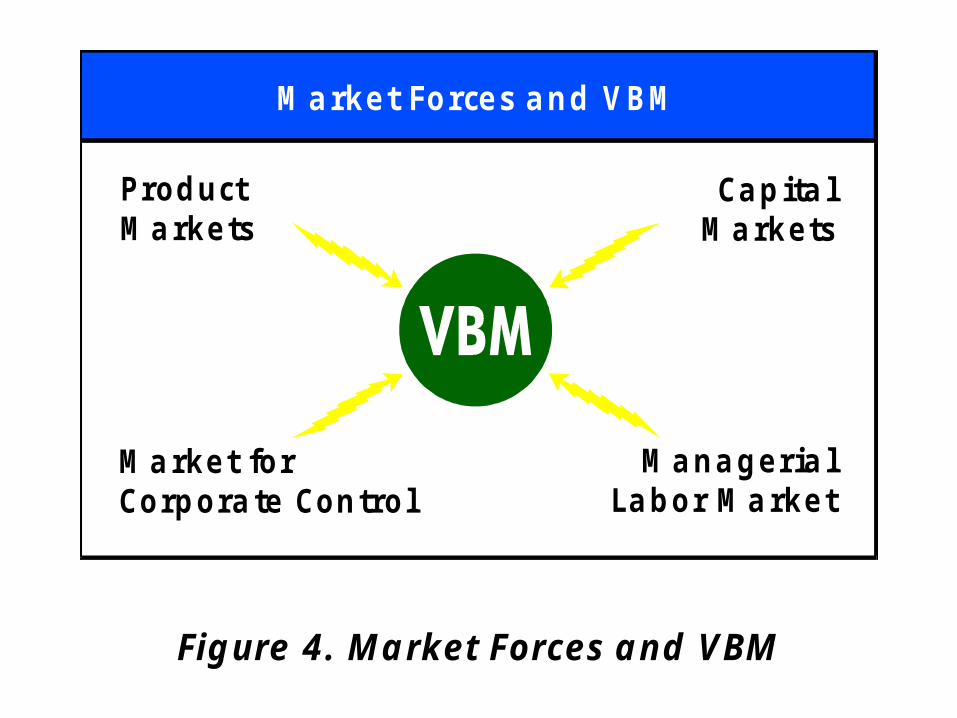

M a rket Forces a nd VBM

ProductM arkets

M arket forCorpora te Control

M anageria lLabor M a rket

Capita lM arkets

Fig ure 4. M a rket Forces a nd VBM

Growing Pressures From Sources Of Discipline

Product market– Globalization, technology, deregulation, digital

economy,

Market for corporate control– Threat of takeovers

Capital markets– Creditors, shareholders

Market for skilled managers

EMBA Finance II 21

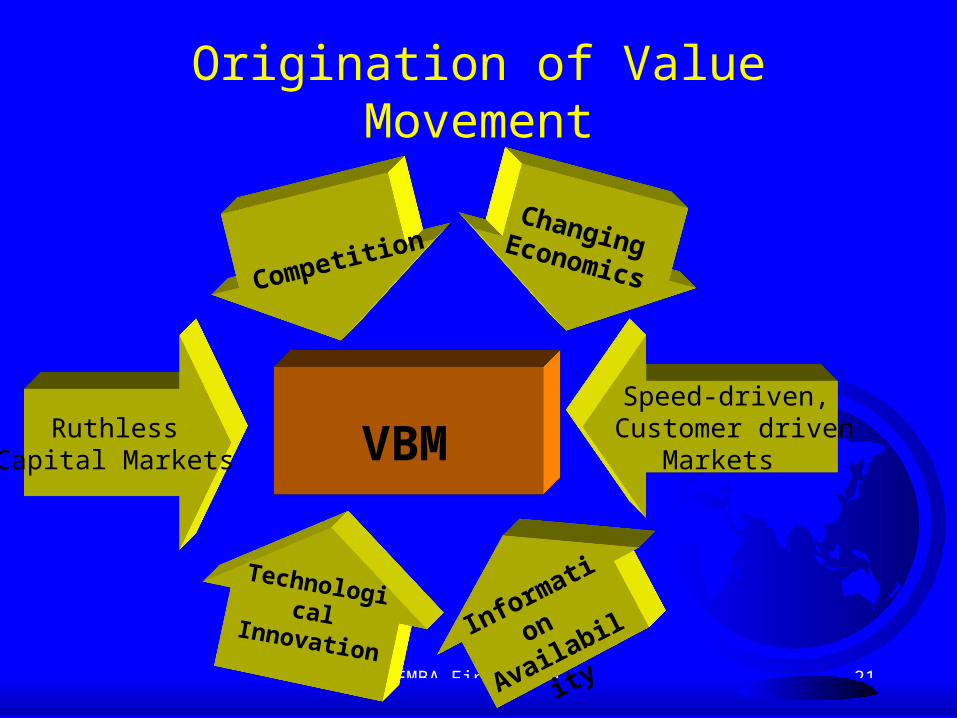

Origination of Value Movement

VBM

Changing EconomicsCompetition

Technological Innovation Information

Availability

RuthlessCapital Markets

Speed-driven,

Customer drivenMarkets

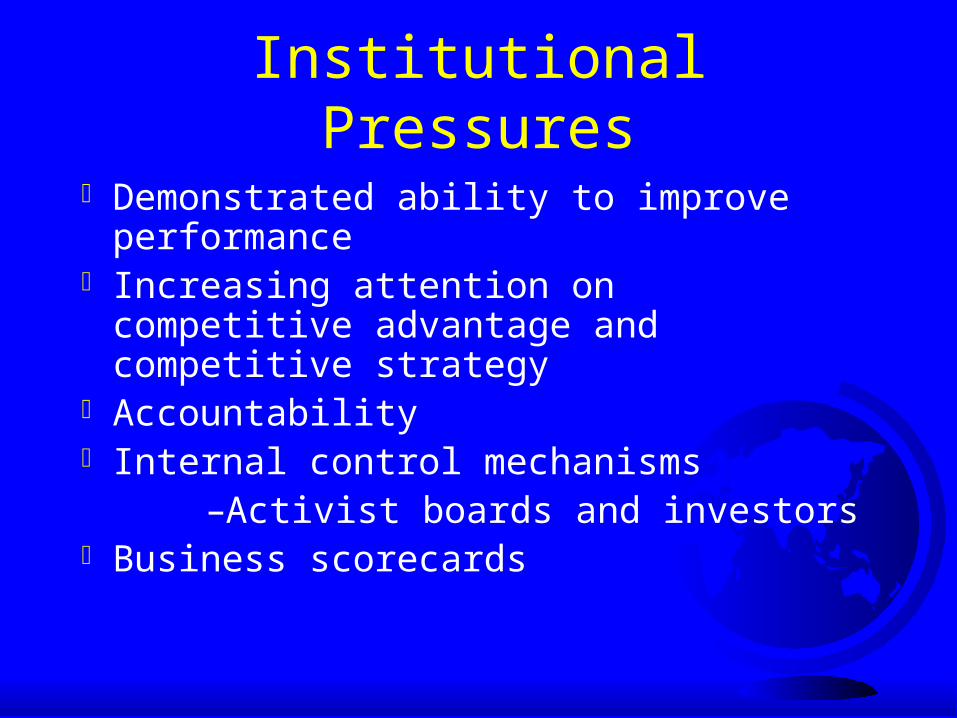

Institutional Pressures

Demonstrated ability to improve performance

Increasing attention on competitive advantage and competitive strategy

Accountability Internal control mechanisms

–Activist boards and investors Business scorecards

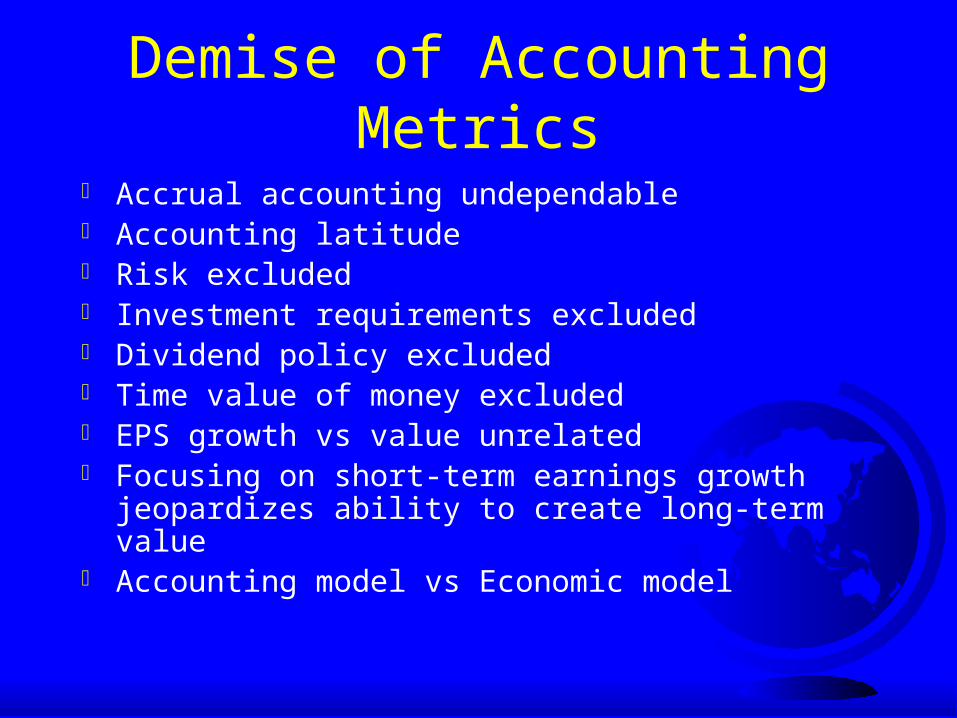

Demise of Accounting Metrics

Accrual accounting undependable Accounting latitude Risk excluded Investment requirements excluded Dividend policy excluded Time value of money excluded EPS growth vs value unrelated Focusing on short-term earnings growth jeopardizes ability

to create long-term value Accounting model vs Economic model

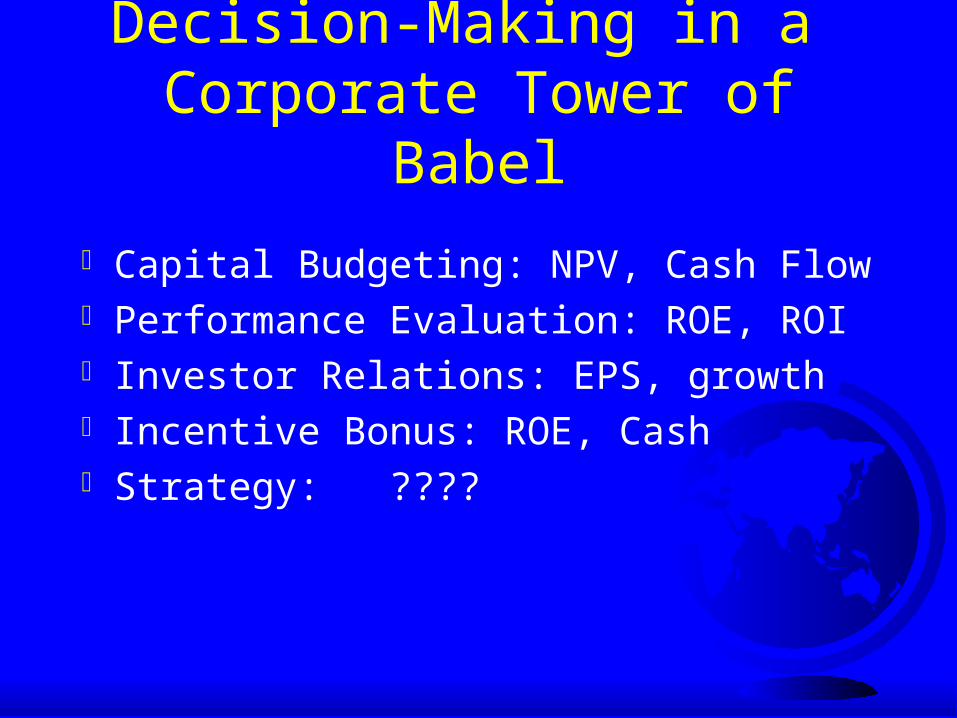

Decision-Making in a Corporate Tower of Babel

Capital Budgeting: NPV, Cash Flow Performance Evaluation: ROE, ROI Investor Relations: EPS, growth Incentive Bonus: ROE, Cash Strategy: ????

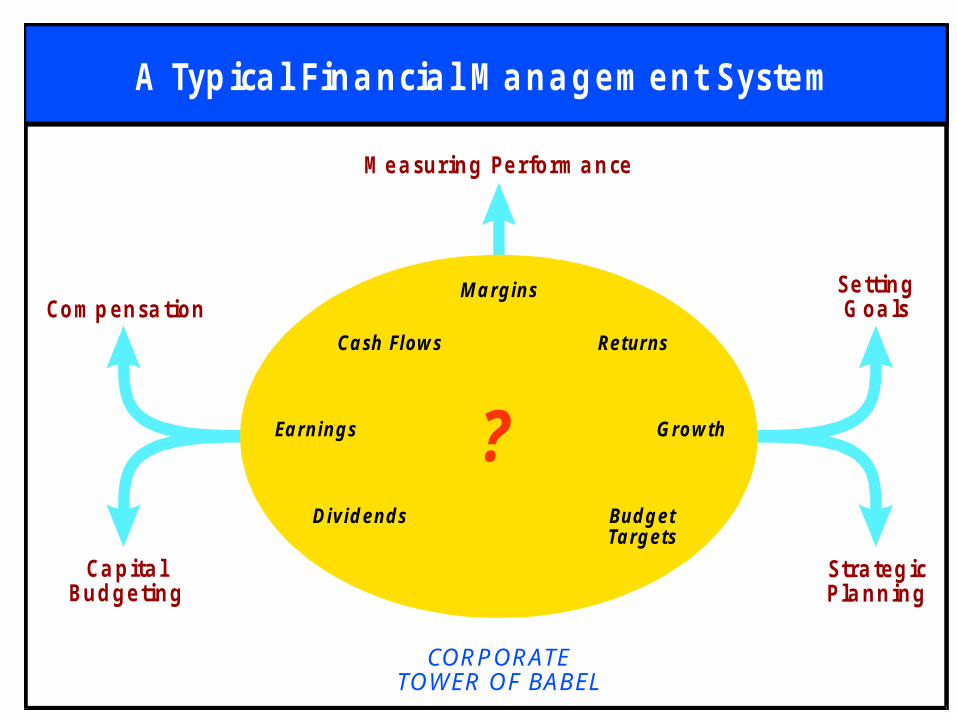

A Typ ica l Fina ncia l M a na gem ent System

Com pensa tion

Ca pita lBudgeting

SettingG oa ls

Stra teg icPla nning

M easuring Perform a nce

?

M a rg ins

Ca sh Flow s Returns

G row th

Bud g etTa rg ets

Ea rn ing s

D ivid end s

CO R P O R ATETO W ER O F BABEL

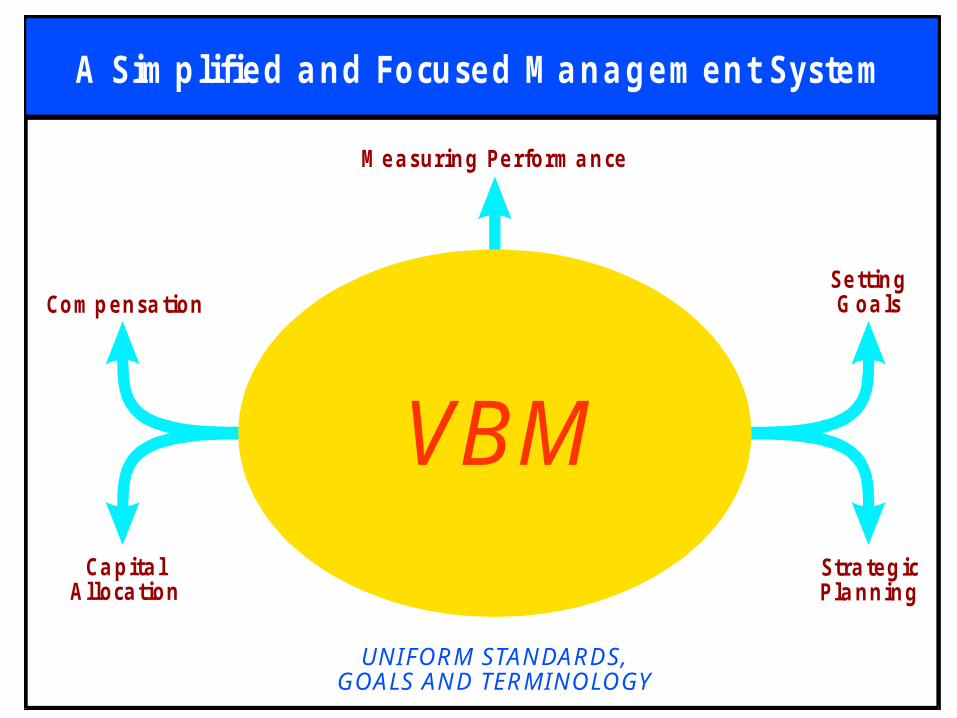

A Sim plified a nd Focused M a na gem ent System

Com pensa tion

Ca pita lA lloca tion

SettingG oa ls

Stra tegicPla nning

M easuring Perform a nce

UN I FO R M STAN DARDS,GO ALS AN D TER M I N O LO GY

VBM

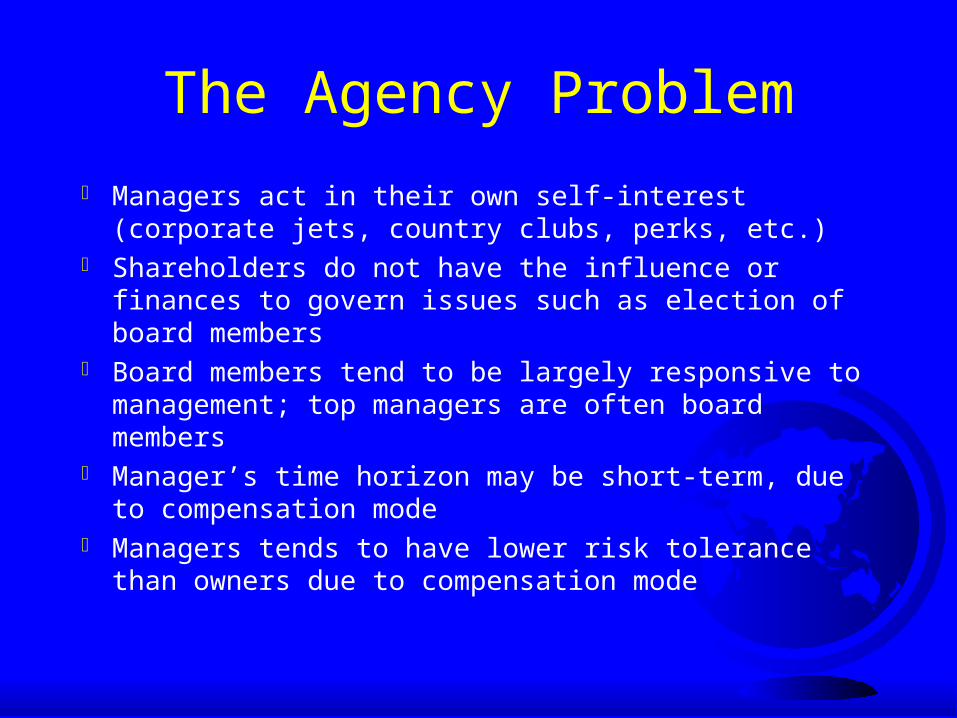

The Agency Problem

Managers act in their own self-interest (corporate jets, country clubs, perks, etc.)

Shareholders do not have the influence or finances to govern issues such as election of board members

Board members tend to be largely responsive to management; top managers are often board members

Manager’s time horizon may be short-term, due to compensation mode

Managers tends to have lower risk tolerance than owners due to compensation mode

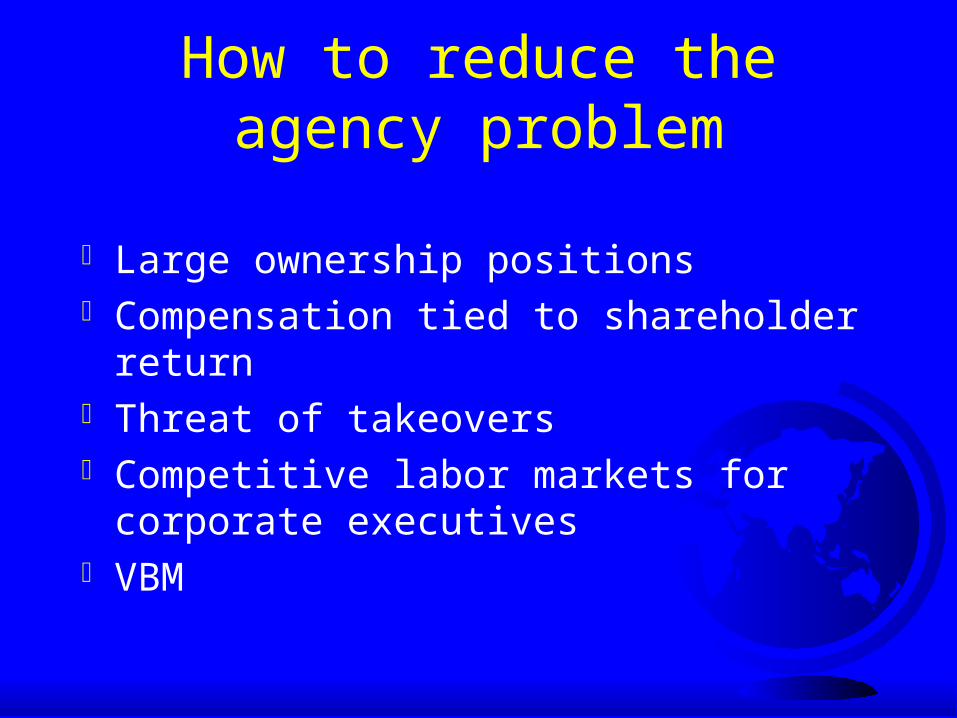

How to reduce the agency problem

Large ownership positions Compensation tied to shareholder return Threat of takeovers Competitive labor markets for corporate

executives VBM

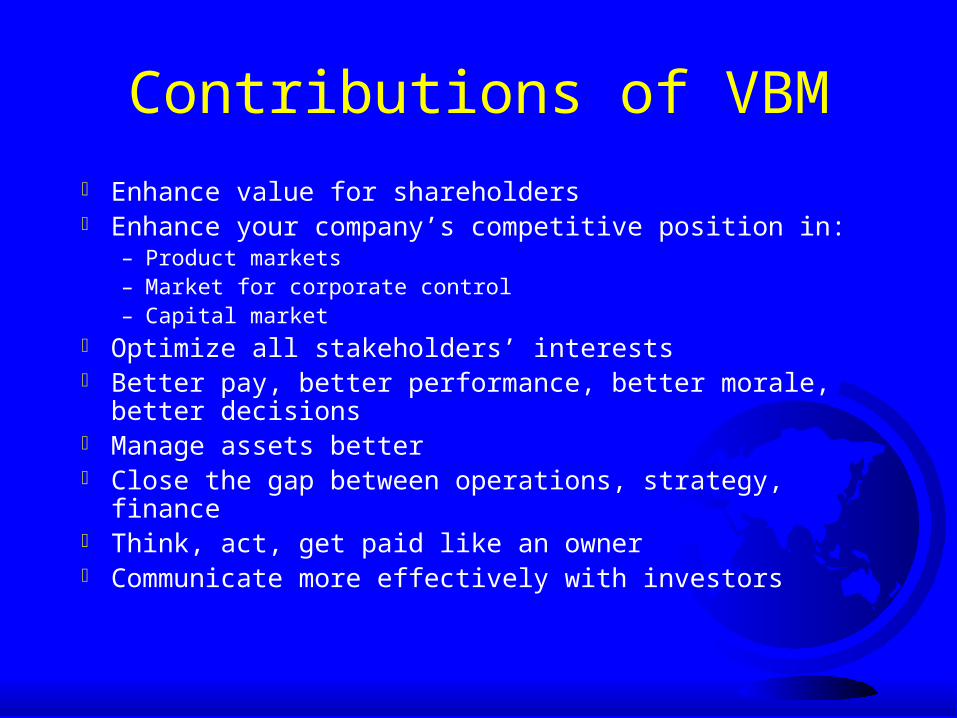

Contributions of VBM

Enhance value for shareholders Enhance your company’s competitive position in:

– Product markets– Market for corporate control– Capital market

Optimize all stakeholders’ interests Better pay, better performance, better morale, better decisions Manage assets better Close the gap between operations, strategy, finance Think, act, get paid like an owner Communicate more effectively with investors