Drake DRAKE UNIVERSITY Fin 288 Swaps Finance 288 Futures Options and Swaps.

132

Drake DRAKE UNIVERSITY Fin 288 Swaps Finance 288 Futures Options and Swaps

-

date post

20-Dec-2015 -

Category

Documents

-

view

232 -

download

2

Transcript of Drake DRAKE UNIVERSITY Fin 288 Swaps Finance 288 Futures Options and Swaps.

DrakeDRAKE UNIVERSITY

Fin 288

Swaps

Finance 288Futures Options and Swaps

DrakeDrake University

Fin 288Introduction

An agreement between two parties to exchange cash flows in the future.The agreement specifies the dates that the cash flows are to be paid and the way that they are to be calculated. A forward contract is an example of a simple swap. With a forward contract, the result is an exchange of cash flows at a single given date in the future. In the case of a swap the cash flows occur at several dates in the future. In other words, you can think of a swap as a portfolio of forward contracts.

DrakeDrake University

Fin 288Mechanics of Swaps

The most common used interest rate swap agreement is an exchange of cash flows based upon a fixed and floating rate. Often referred to a “plain vanilla” swap, the agreement consists of one party paying a fixed interest rate on a notional principal amount in exchange for the other party paying a floating rate on the same notional principal amount for a set period of time. In this case the currency of the agreement is the same for both parties.

DrakeDrake University

Fin 288Notional Principal

The term notional principal implies that the principal itself is not exchanged. If it was exchanged at the end of the swap, the exact same cash flows would result.

DrakeDrake University

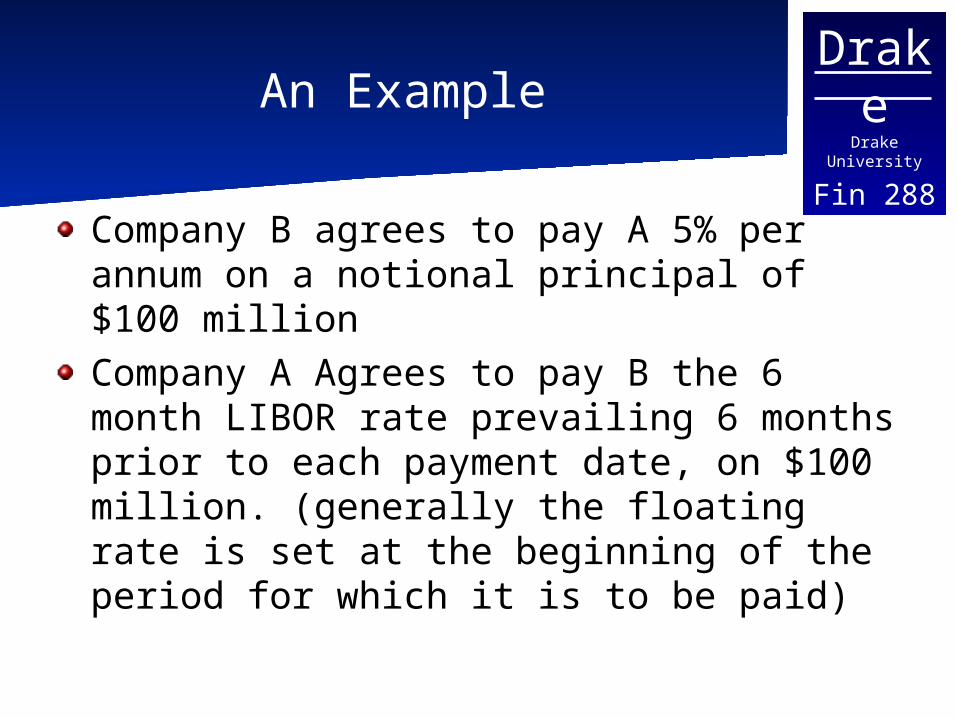

Fin 288An Example

Company B agrees to pay A 5% per annum on a notional principal of $100 millionCompany A Agrees to pay B the 6 month LIBOR rate prevailing 6 months prior to each payment date, on $100 million. (generally the floating rate is set at the beginning of the period for which it is to be paid)

DrakeDrake University

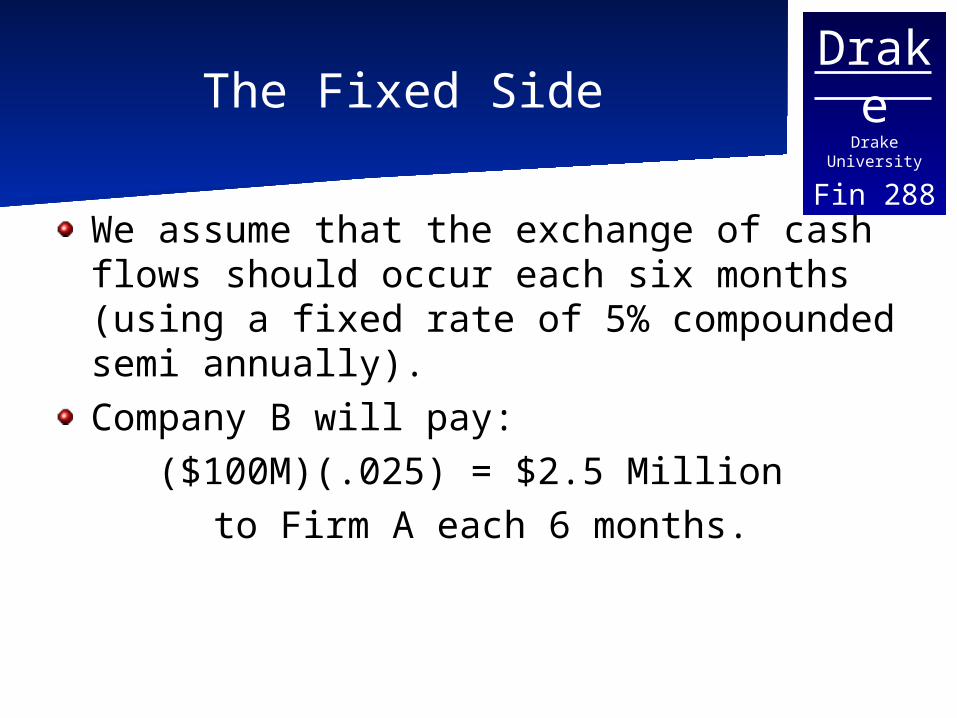

Fin 288The Fixed Side

We assume that the exchange of cash flows should occur each six months (using a fixed rate of 5% compounded semi annually). Company B will pay:

($100M)(.025) = $2.5 Million to Firm A each 6 months.

DrakeDrake University

Fin 288

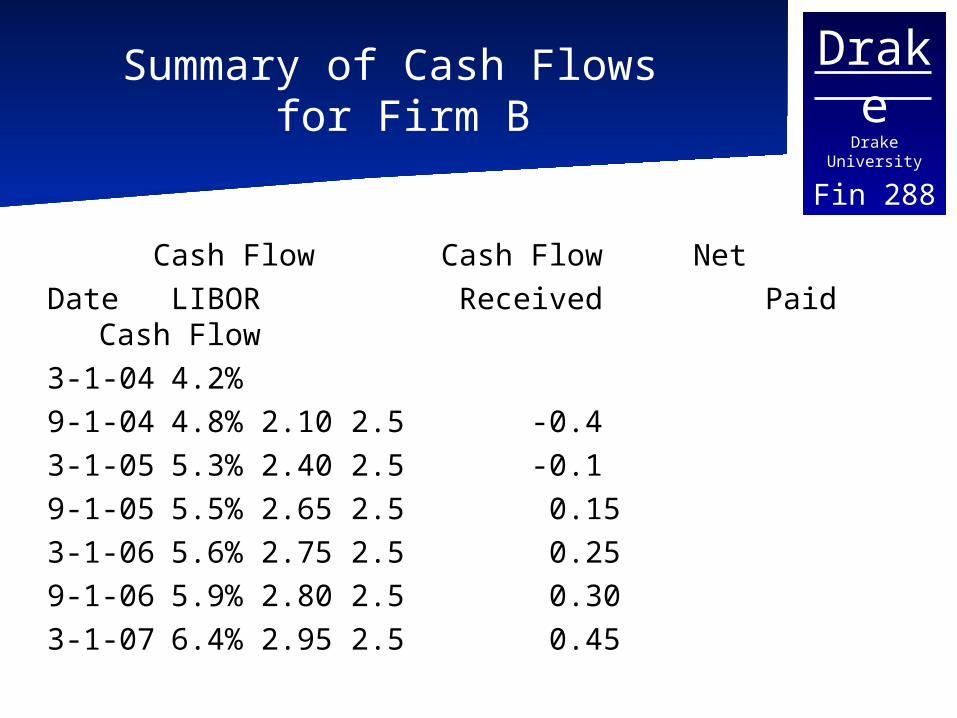

Summary of Cash Flows for Firm B

Cash Flow Cash Flow NetDate LIBOR Received Paid

Cash Flow3-1-04 4.2%9-1-04 4.8% 2.10 2.5 -0.43-1-05 5.3% 2.40 2.5 -0.19-1-05 5.5% 2.65 2.5 0.153-1-06 5.6% 2.75 2.5 0.259-1-06 5.9% 2.80 2.5 0.303-1-07 6.4% 2.95 2.5 0.45

DrakeDrake University

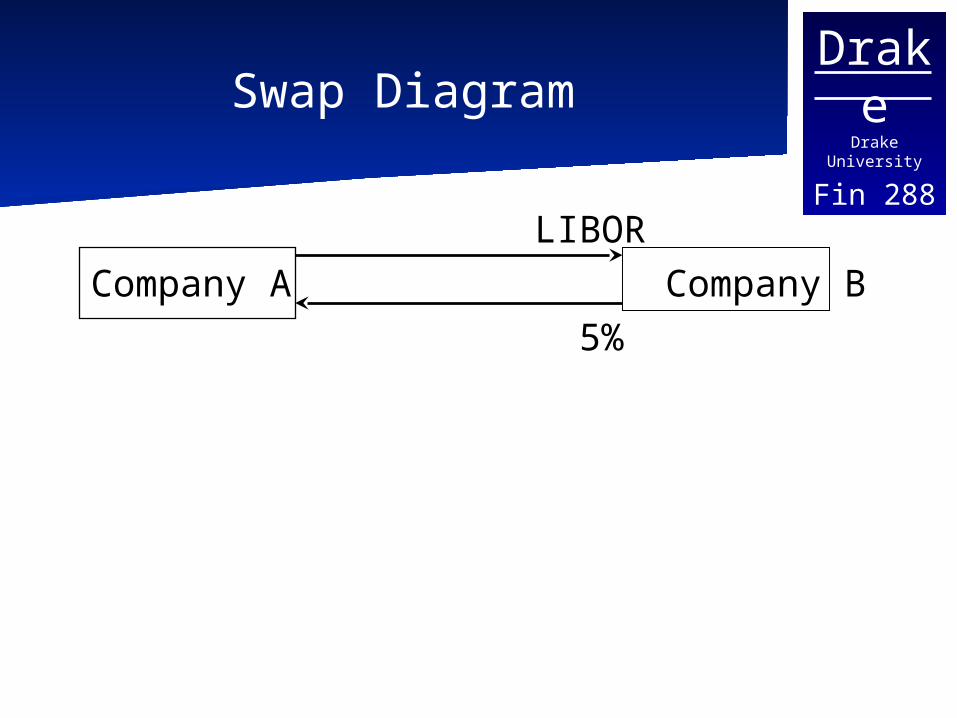

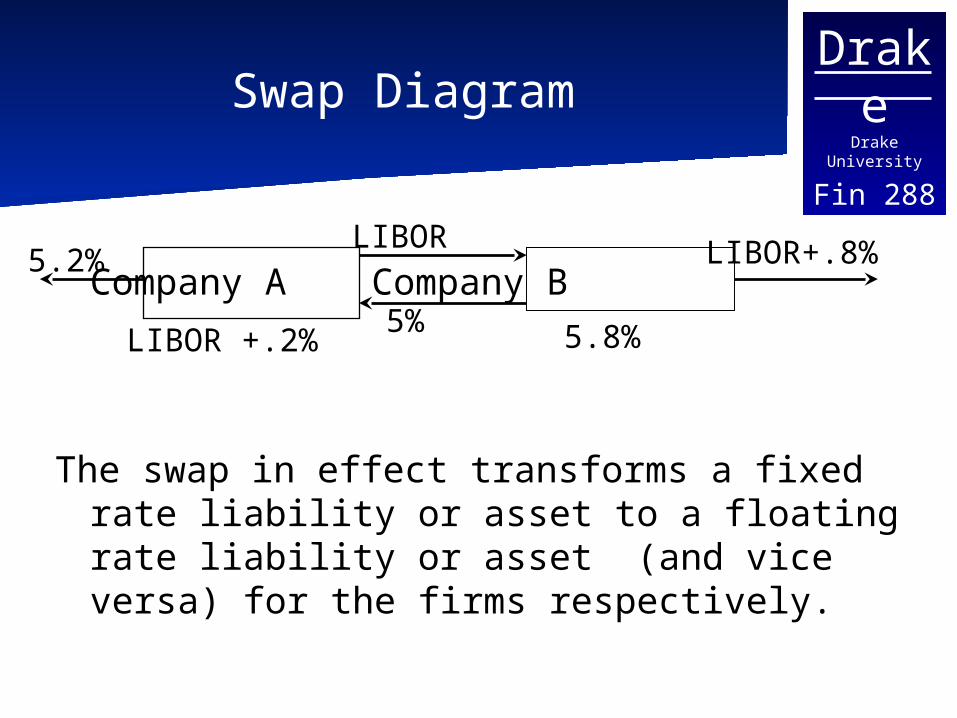

Fin 288Swap Diagram

LIBORCompany A Company B

5%

DrakeDrake University

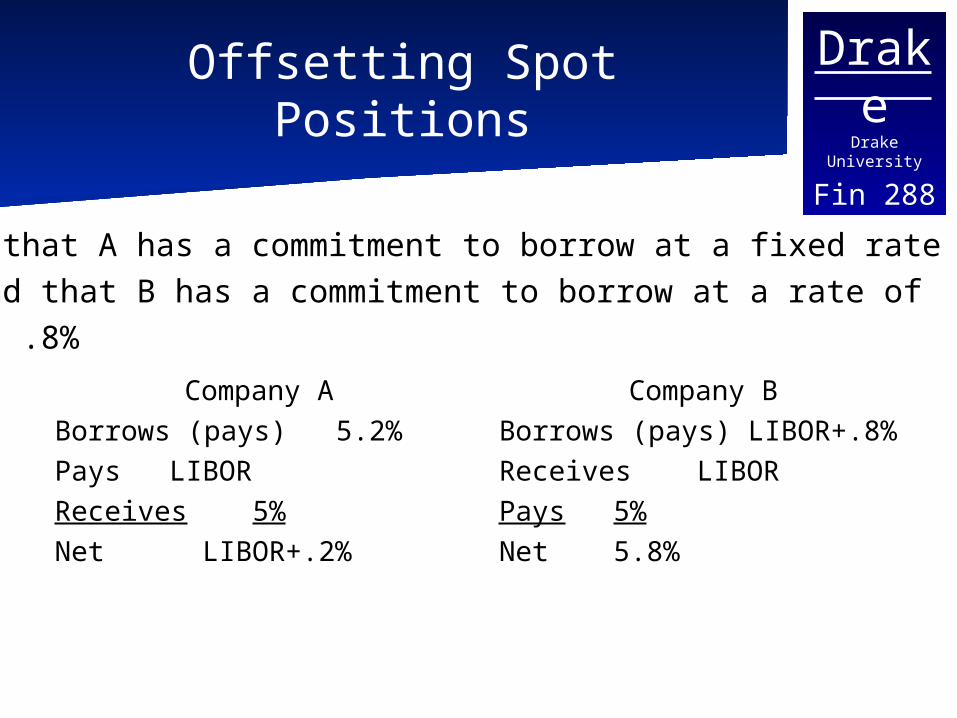

Fin 288Offsetting Spot Positions

Company ABorrows (pays) 5.2%Pays LIBORReceives 5%Net LIBOR+.2%

Company BBorrows (pays) LIBOR+.8%Receives LIBORPays 5%Net 5.8%

Assume that A has a commitment to borrow at a fixed rate of 5.2% and that B has a commitment to borrow at a rate of LIBOR + .8%

DrakeDrake University

Fin 288Swap Diagram

Company A Company B

The swap in effect transforms a fixed rate liability or asset to a floating rate liability or asset (and vice versa) for the firms respectively.

5.2% LIBOR+.8%

LIBOR +.2%5%

LIBOR

5.8%

DrakeDrake University

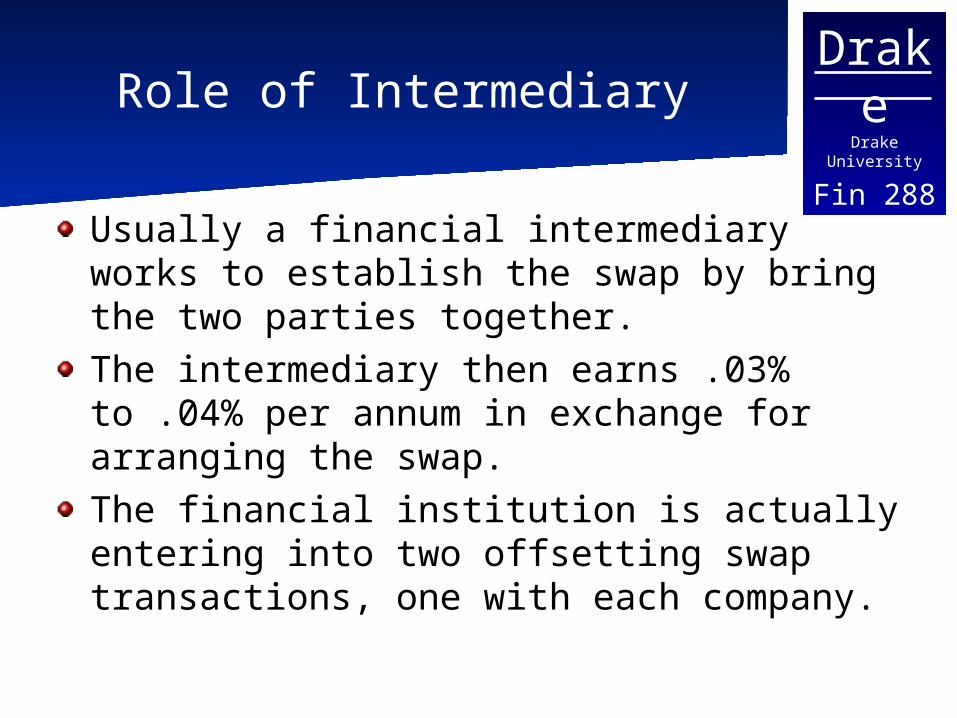

Fin 288Role of Intermediary

Usually a financial intermediary works to establish the swap by bring the two parties together. The intermediary then earns .03% to .04% per annum in exchange for arranging the swap. The financial institution is actually entering into two offsetting swap transactions, one with each company.

DrakeDrake University

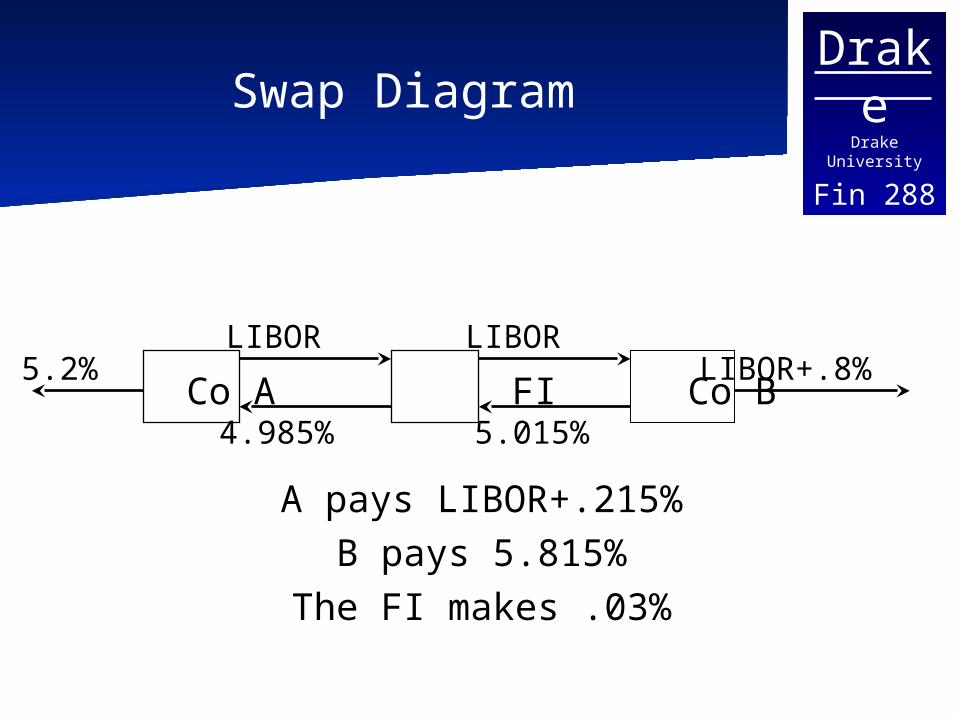

Fin 288Swap Diagram

Co A FI Co B

A pays LIBOR+.215%B pays 5.815%

The FI makes .03%

5.2% LIBOR+.8%

5.015%

LIBOR

4.985%

LIBOR

DrakeDrake University

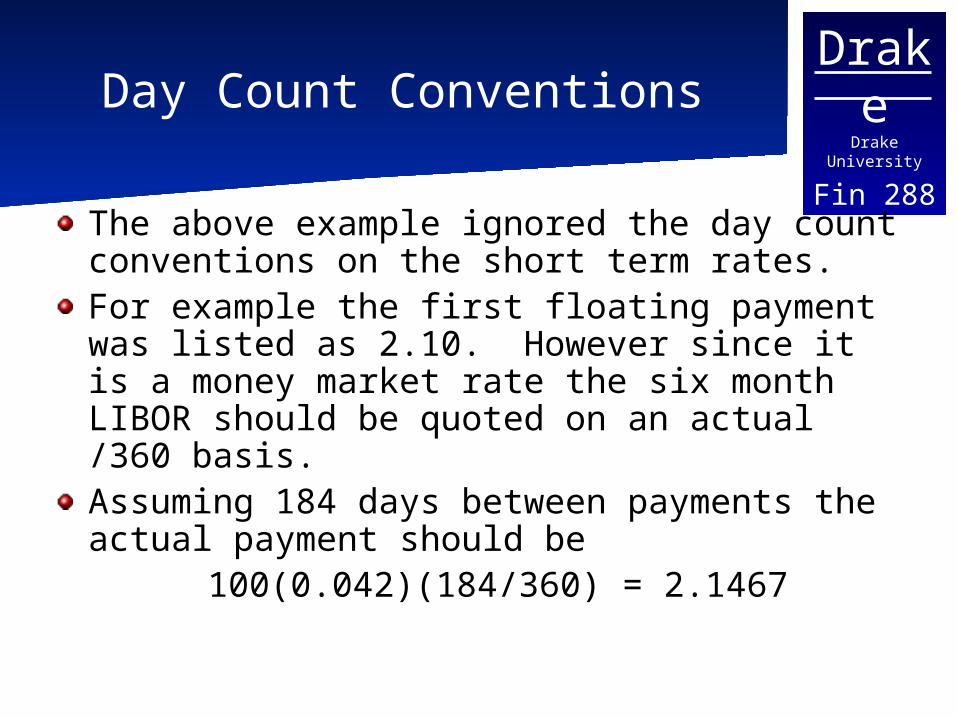

Fin 288Day Count Conventions

The above example ignored the day count conventions on the short term rates.For example the first floating payment was listed as 2.10. However since it is a money market rate the six month LIBOR should be quoted on an actual /360 basis. Assuming 184 days between payments the actual payment should be

100(0.042)(184/360) = 2.1467

DrakeDrake University

Fin 288Day Count Conventions II

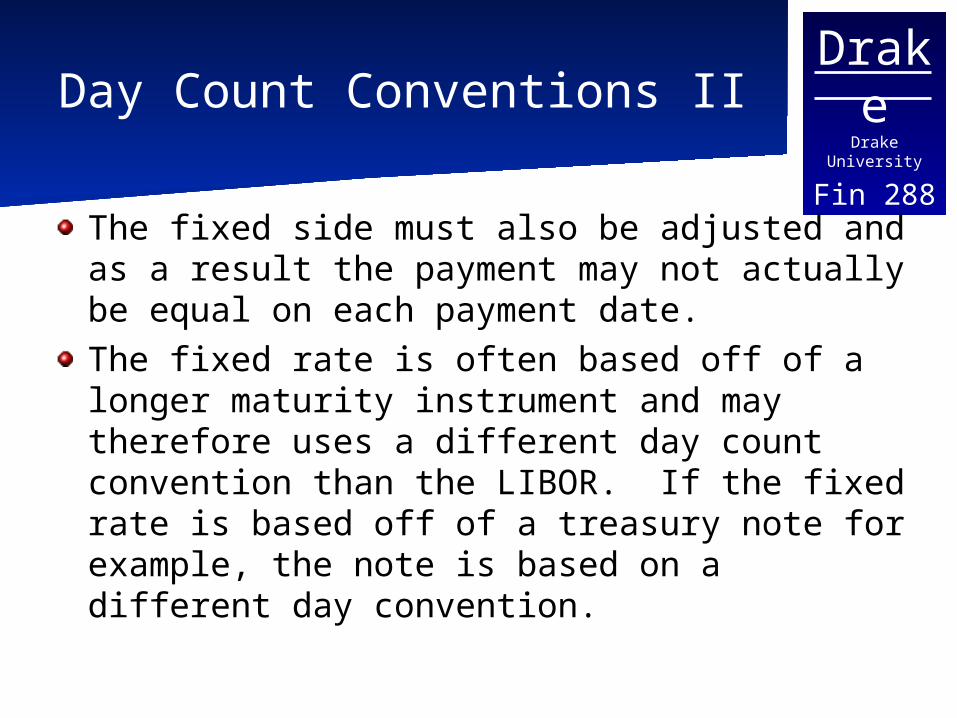

The fixed side must also be adjusted and as a result the payment may not actually be equal on each payment date. The fixed rate is often based off of a longer maturity instrument and may therefore uses a different day count convention than the LIBOR. If the fixed rate is based off of a treasury note for example, the note is based on a different day convention.

DrakeDrake University

Fin 288Role of the Intermediary

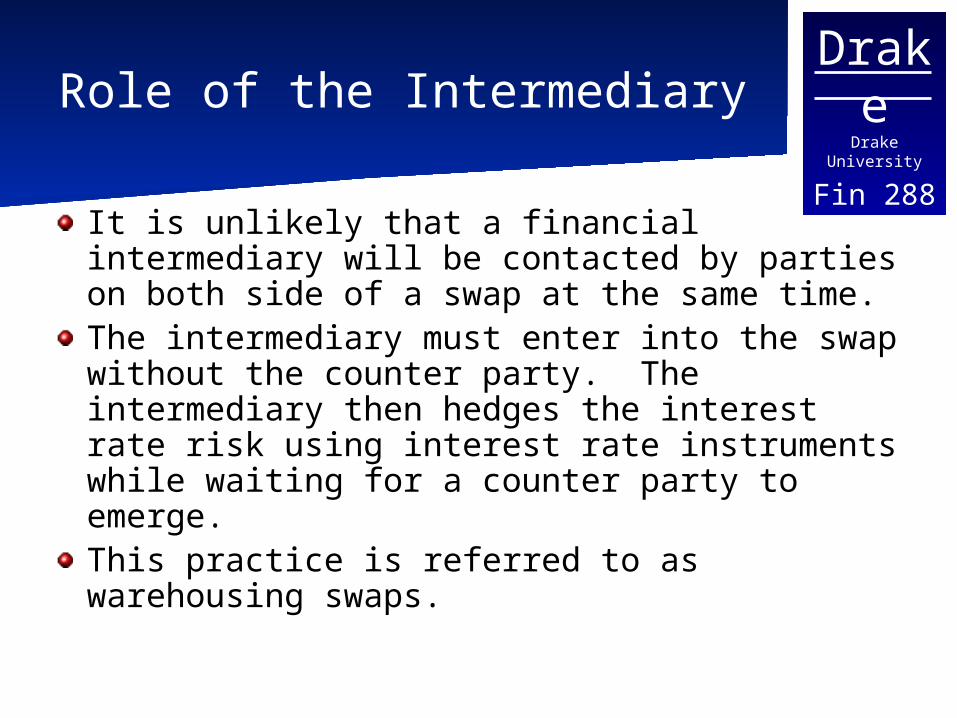

It is unlikely that a financial intermediary will be contacted by parties on both side of a swap at the same time.The intermediary must enter into the swap without the counter party. The intermediary then hedges the interest rate risk using interest rate instruments while waiting for a counter party to emerge. This practice is referred to as warehousing swaps.

DrakeDrake University

Fin 288Why enter into a swap?

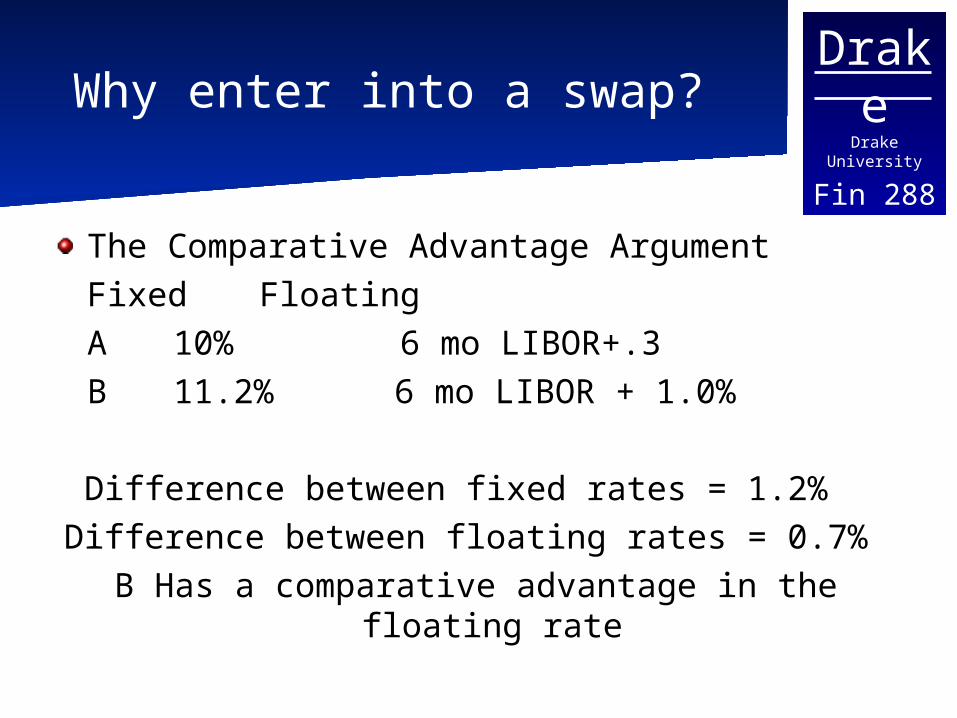

The Comparative Advantage ArgumentFixed Floating

A 10% 6 mo LIBOR+.3B 11.2% 6 mo LIBOR + 1.0%

Difference between fixed rates = 1.2% Difference between floating rates = 0.7%

B Has a comparative advantage in the floating rate

DrakeDrake University

Fin 288

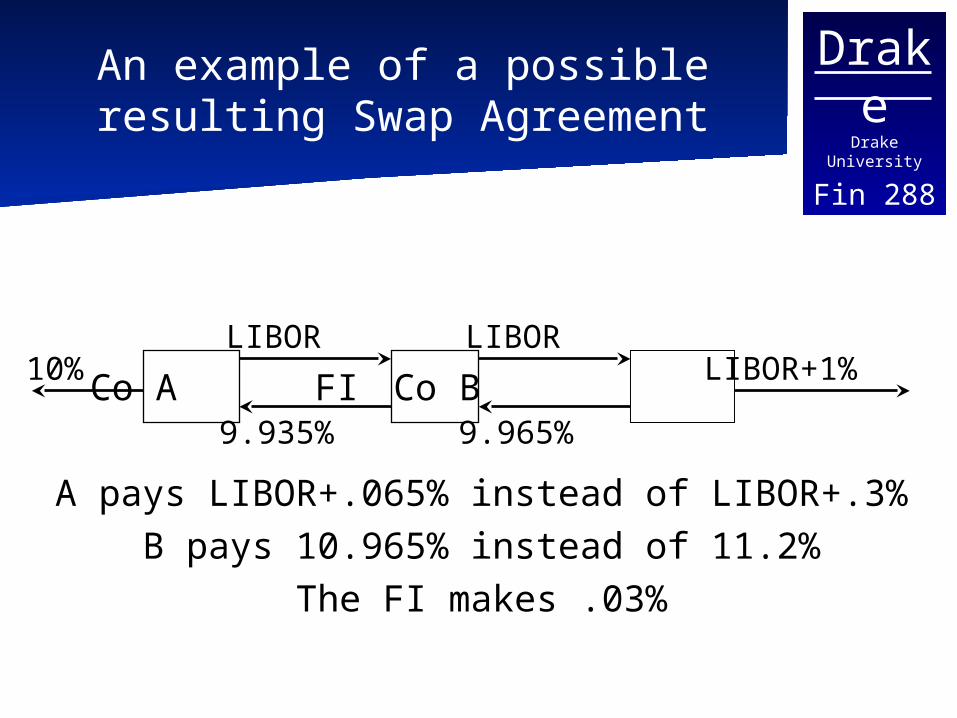

An example of a possible resulting Swap Agreement

Co A FI Co B

A pays LIBOR+.065% instead of LIBOR+.3%B pays 10.965% instead of 11.2%

The FI makes .03%

10% LIBOR+1%

9.965%

LIBOR

9.935%

LIBOR

DrakeDrake University

Fin 288Spread Differentials

Why do spread differentials exist?Differences in business lines, credit history, asset and liabilities, etc…

DrakeDrake University

Fin 288

Why Enter Into A Swap?Managing Cash Flows

Assume that an insurance firm sold an annuity lasting 5 years and paying $5 Million each year.To offset the cash outflows they invest in a 10 year security that pays $6 million each year.The firm runs a reinvestment risk when they stop paying the cash outflows on the annuity – a combination of swaps could eliminate this risk (on board in class)

DrakeDrake University

Fin 288

Valuation of Interest Rate Swaps

After the swap is entered into it can be valued as either:

A long position in one bond combined with a short position in another bond or A portfolio of forward rate agreements.

DrakeDrake University

Fin 288Relationship of Swaps to Bonds

In the examples above the same relationship could have been written asCompany B lent company A $100 million at the six month LIBOR rateCompany A lent company B $100 million at a fixed 5% per annum

DrakeDrake University

Fin 288Bond Valuation

Given the same floating rates as before the cash flow would be the same as in the swap example. The value of the swap would then be the difference between the value of the fixed rate bond and the floating rate bond.

DrakeDrake University

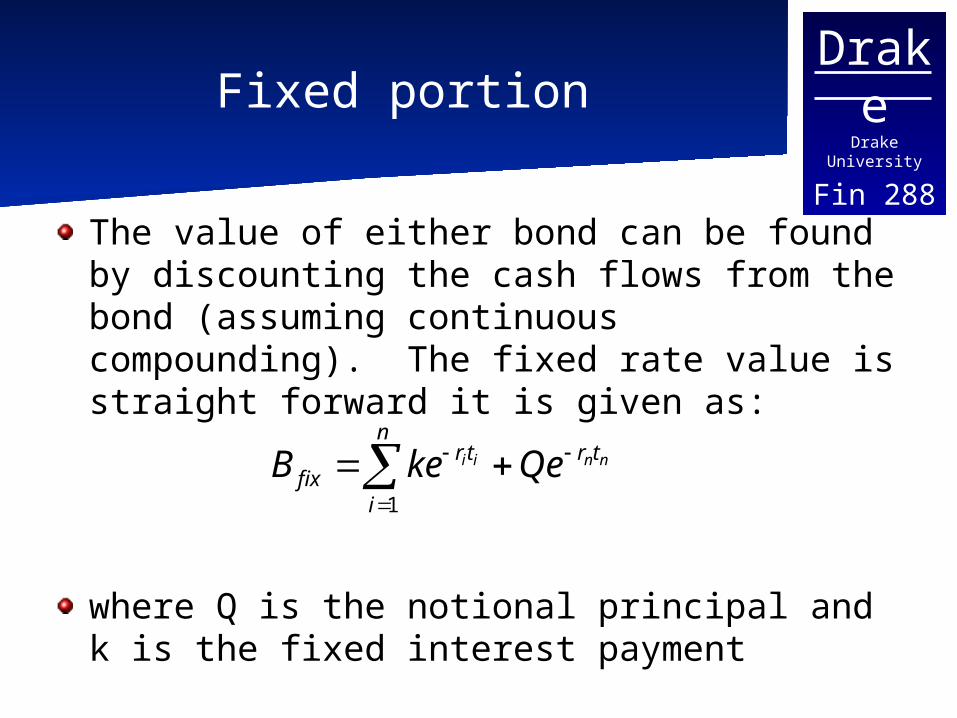

Fin 288Fixed portion

The value of either bond can be found by discounting the cash flows from the bond (assuming continuous compounding). The fixed rate value is straight forward it is given as:

where Q is the notional principal and k is the fixed interest payment

nnii trn

i

trfix QekeB

1

DrakeDrake University

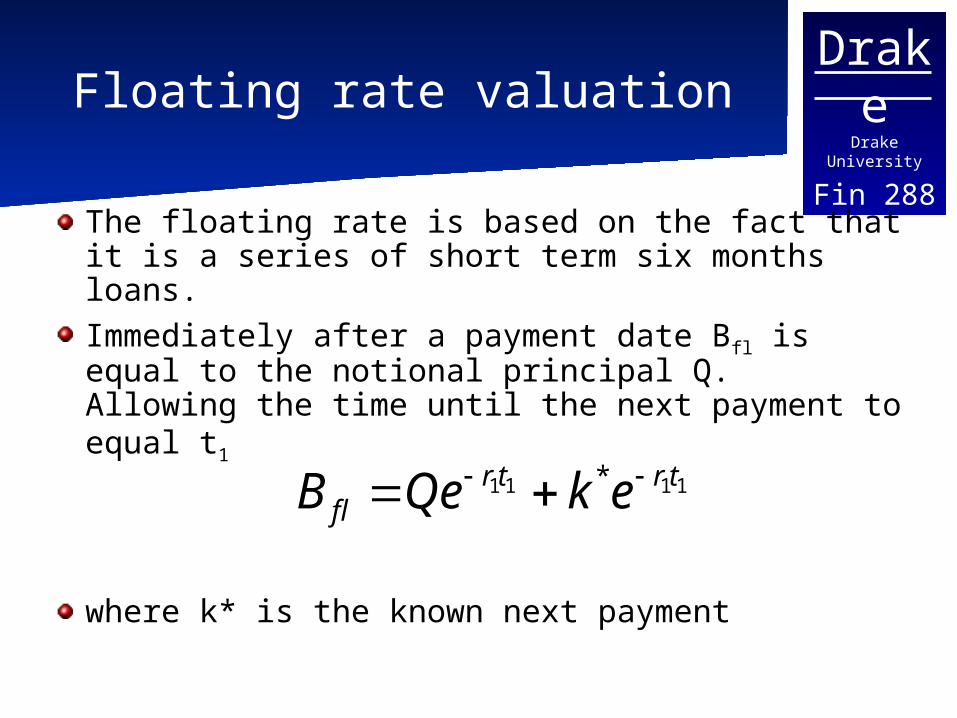

Fin 288Floating rate valuation

The floating rate is based on the fact that it is a series of short term six months loans.Immediately after a payment date Bfl is equal to the notional principal Q. Allowing the time until the next payment to equal t1

where k* is the known next payment

1111 * trtrfl ekQeB

DrakeDrake University

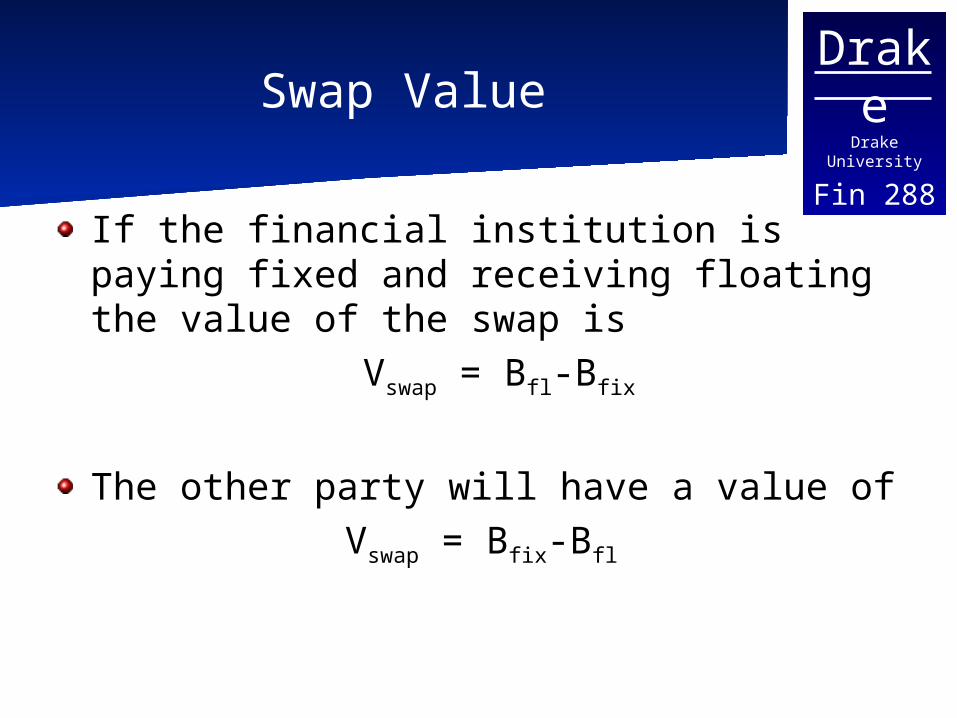

Fin 288Swap Value

If the financial institution is paying fixed and receiving floating the value of the swap is

Vswap = Bfl-Bfix

The other party will have a value of Vswap = Bfix-Bfl

DrakeDrake University

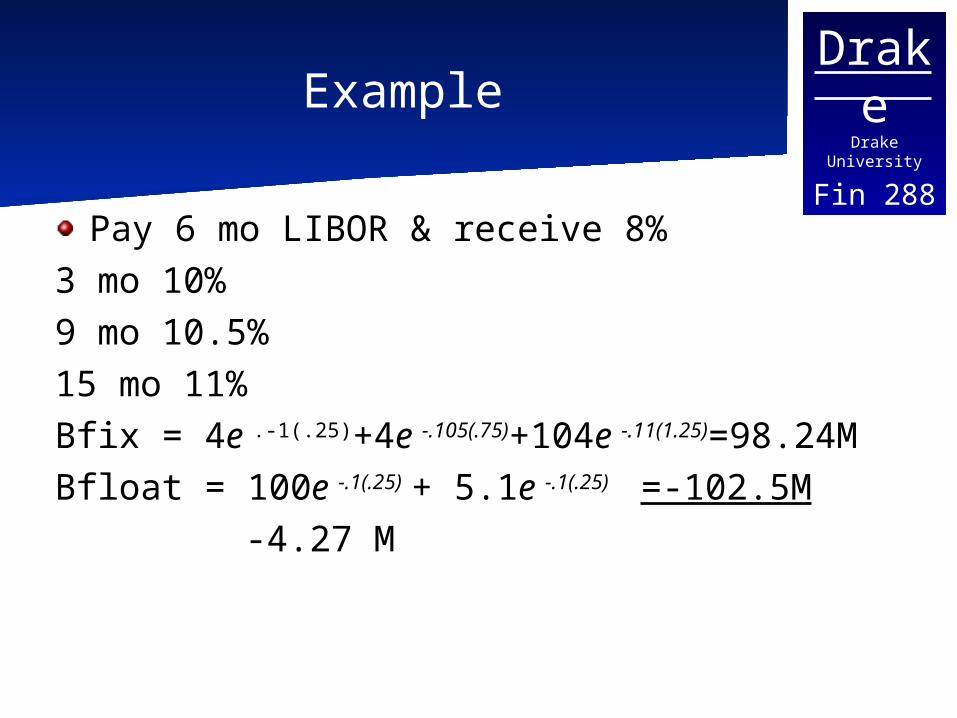

Fin 288Example

Pay 6 mo LIBOR & receive 8%3 mo 10%9 mo 10.5% 15 mo 11%Bfix = 4e .-1(.25)+4e -.105(.75)+104e -.11(1.25)=98.24MBfloat = 100e -.1(.25) + 5.1e -.1(.25) =-102.5M

-4.27 M

DrakeDrake University

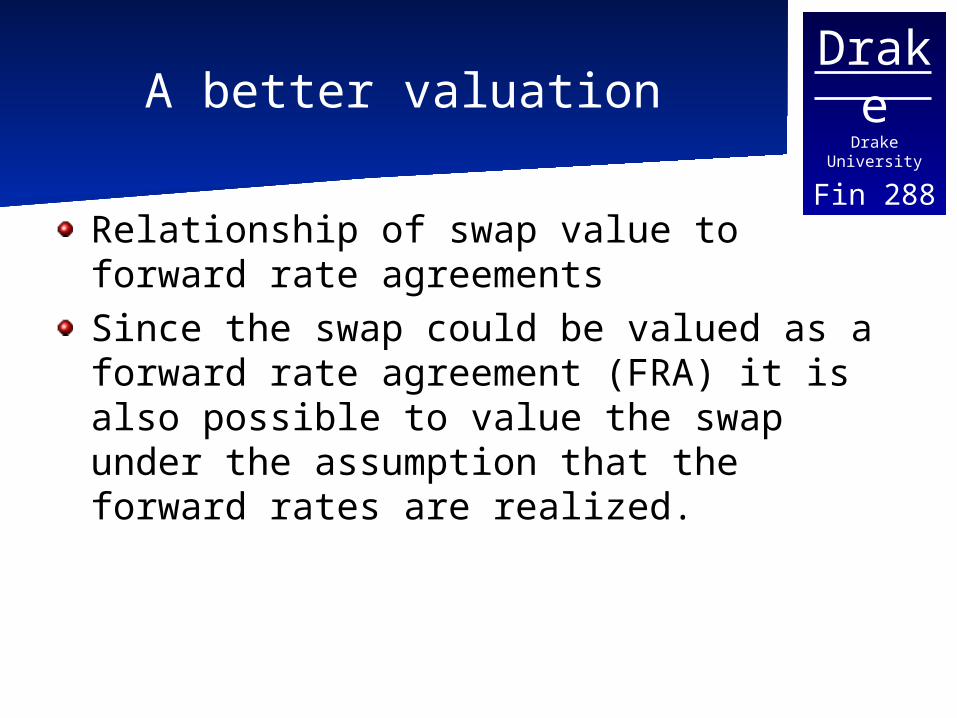

Fin 288A better valuation

Relationship of swap value to forward rate agreementsSince the swap could be valued as a forward rate agreement (FRA) it is also possible to value the swap under the assumption that the forward rates are realized.

DrakeDrake University

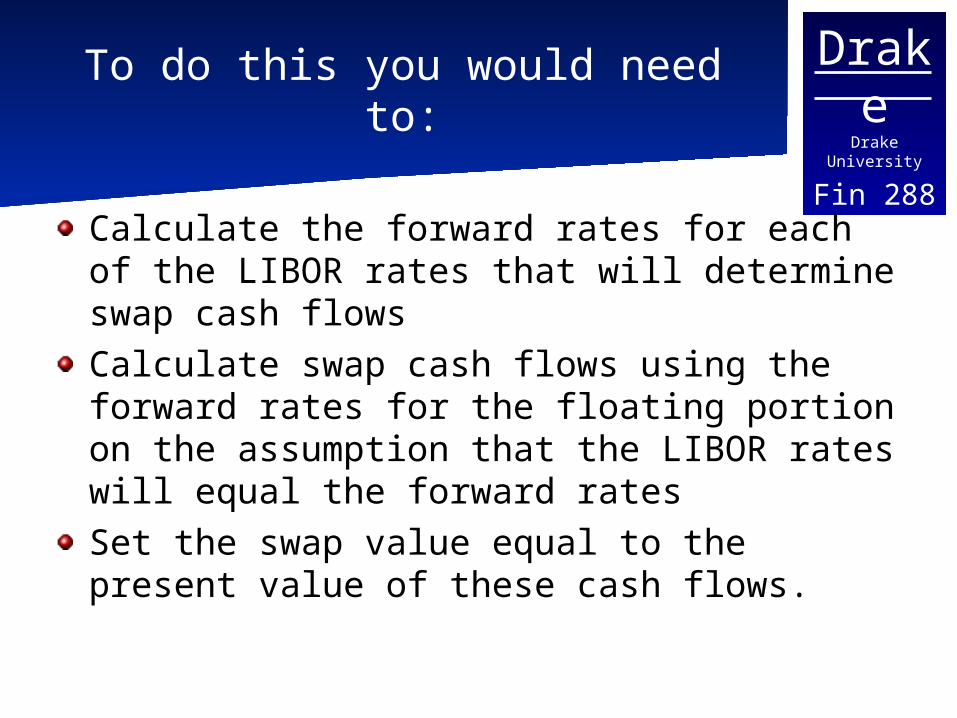

Fin 288To do this you would need to:

Calculate the forward rates for each of the LIBOR rates that will determine swap cash flowsCalculate swap cash flows using the forward rates for the floating portion on the assumption that the LIBOR rates will equal the forward ratesSet the swap value equal to the present value of these cash flows.

DrakeDrake University

Fin 288Swap Rate

This works after you know the fixed rate.When entering into the swap the value of the swap should be 0.This implies that the PV of each of the two series of cash flows is equal. Each party is then willing to exchange the cash flows since they have the same value.The rate that makes the PV equal when used for the fixed payments is the swap rate.

DrakeDrake University

Fin 288Example

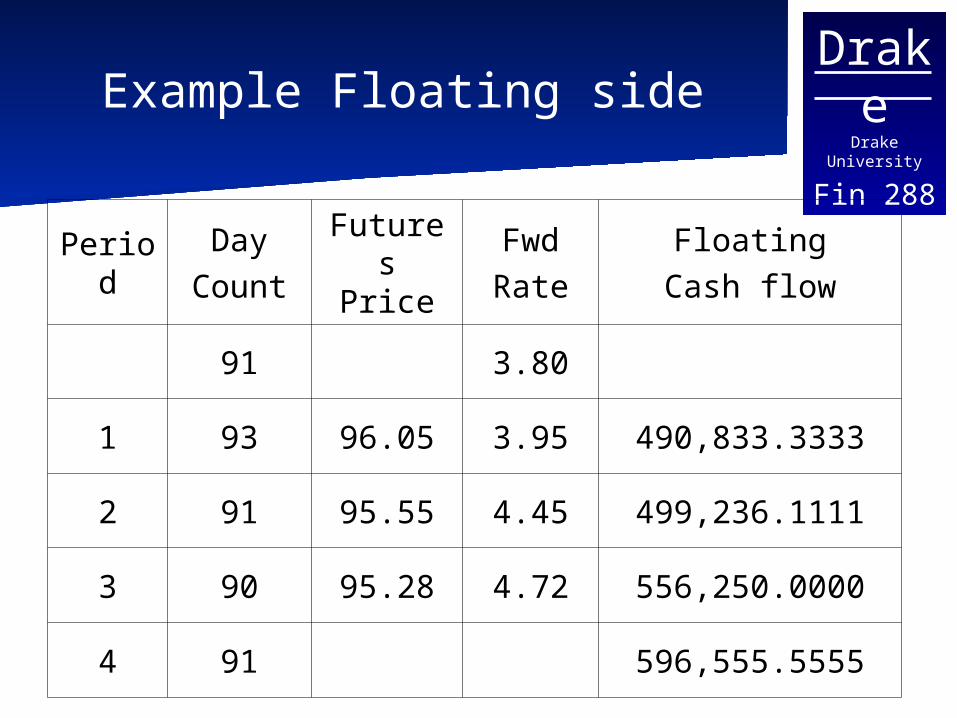

Assume that you are considering a swap where the party with the floating rate will pay the three month LIBOR on the $50 Million in principal.The parties will swap quarterly payments each quarter for the next year.Both the fixed and floating rates are to be paid on an actual/360 day basis.

DrakeDrake University

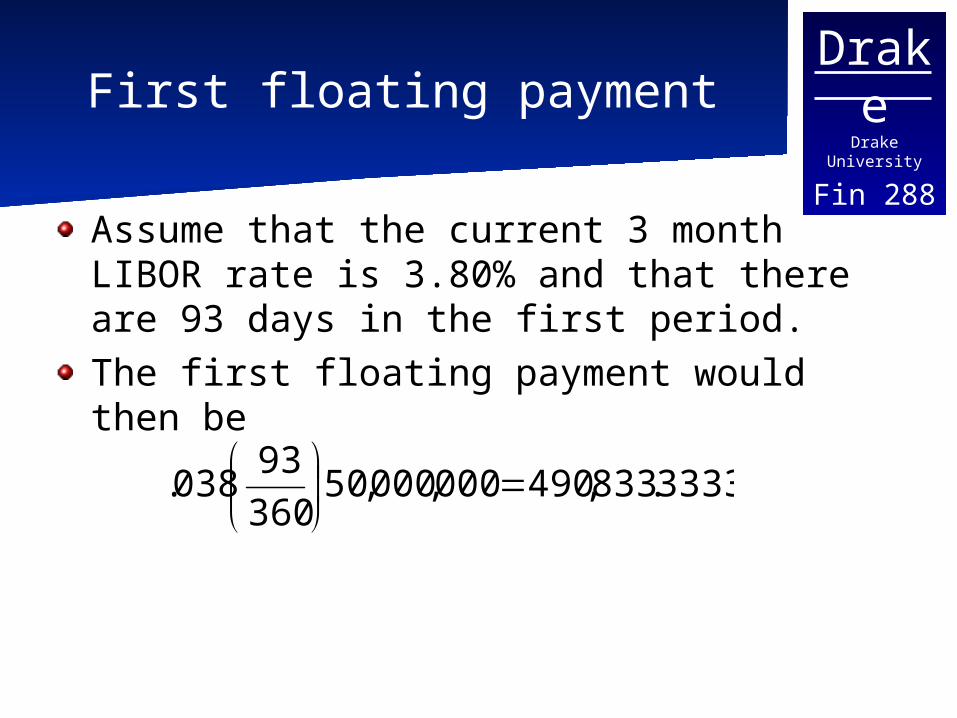

Fin 288First floating payment

Assume that the current 3 month LIBOR rate is 3.80% and that there are 93 days in the first period.The first floating payment would then be

3333.833,490000,000,50360

93038.

DrakeDrake University

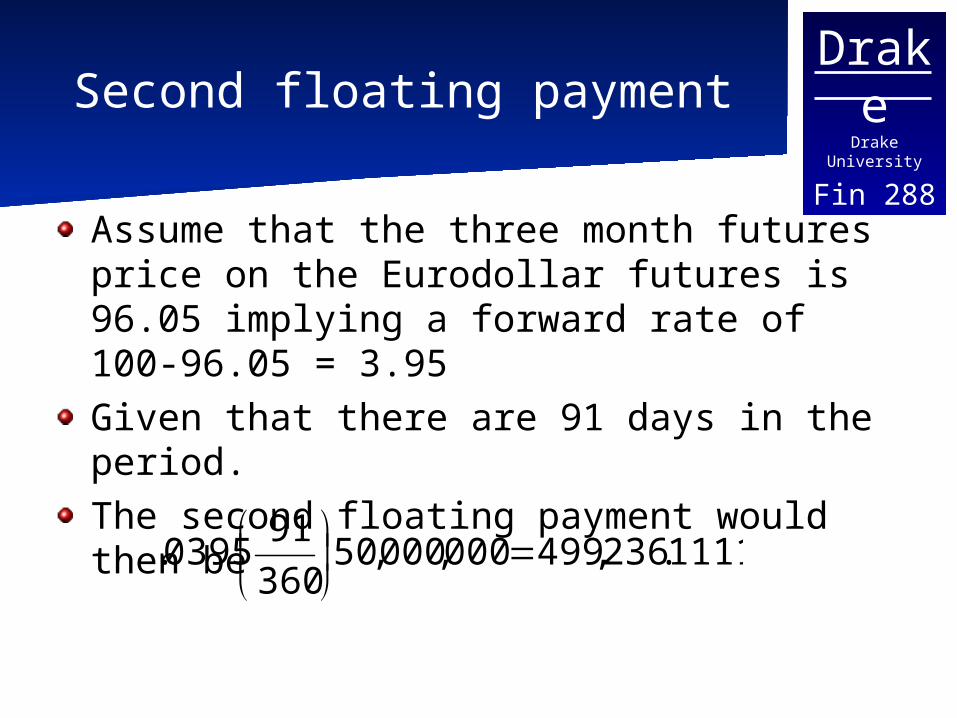

Fin 288Second floating payment

Assume that the three month futures price on the Eurodollar futures is 96.05 implying a forward rate of 100-96.05 = 3.95Given that there are 91 days in the period.The second floating payment would then be

1111.236,499000,000,50360

910395.

DrakeDrake University

Fin 288Example Floating side

PeriodDay

CountFutures

PriceFwdRate

FloatingCash flow

91 3.80

1 93 96.05 3.95 490,833.3333

2 91 95.55 4.45 499,236.1111

3 90 95.28 4.72 556,250.0000

4 91 596,555.5555

DrakeDrake University

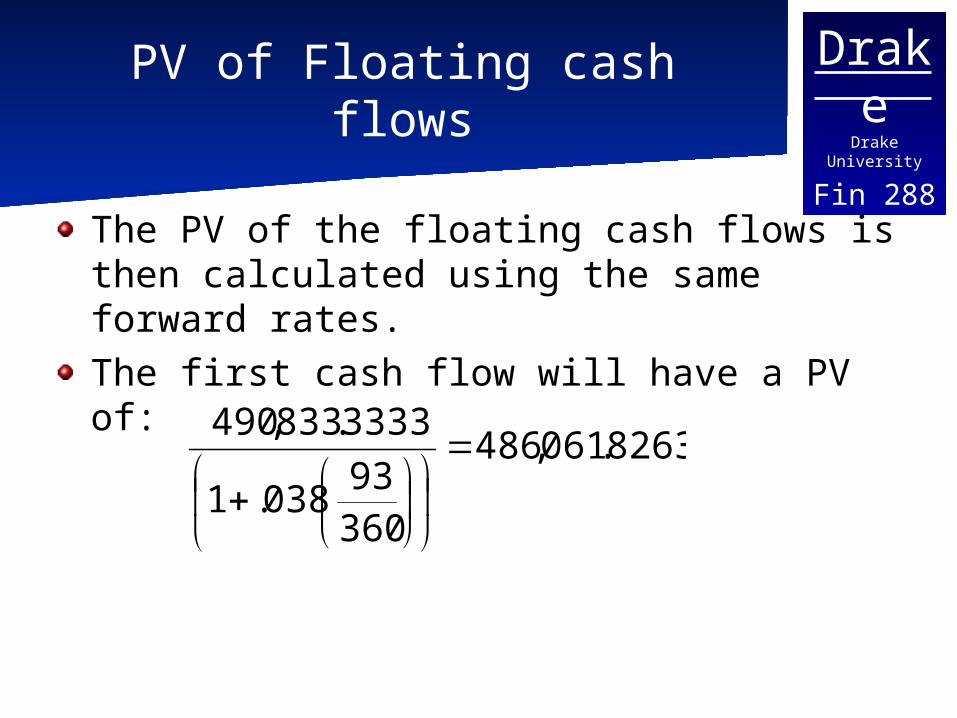

Fin 288PV of Floating cash flows

The PV of the floating cash flows is then calculated using the same forward rates.The first cash flow will have a PV of:

8263.061,486

36093

038.1

3333.833,490

DrakeDrake University

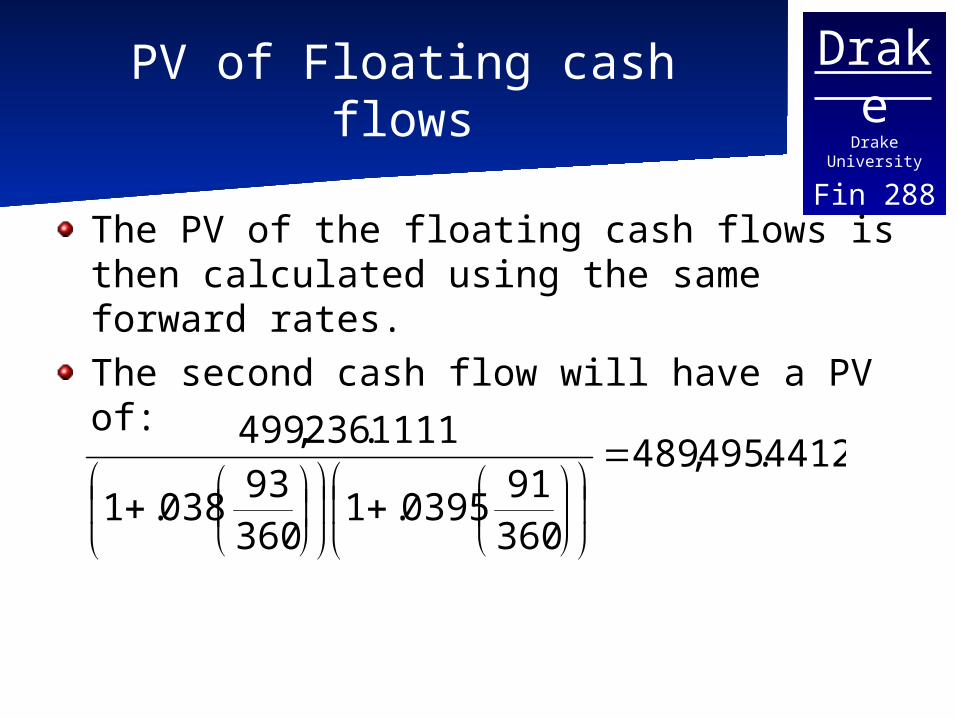

Fin 288PV of Floating cash flows

The PV of the floating cash flows is then calculated using the same forward rates.The second cash flow will have a PV of:

4412.495,489

36091

0395.136093

038.1

1111.236,499

DrakeDrake University

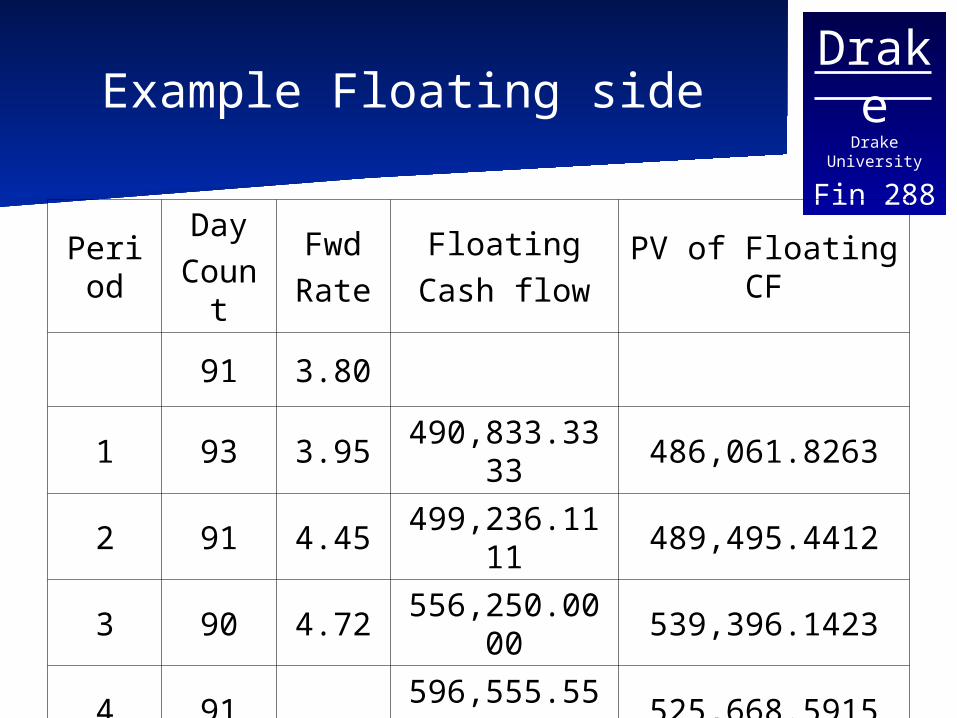

Fin 288Example Floating side

Period

DayCount

FwdRate

FloatingCash flow

PV of Floating CF

91 3.80

1 93 3.95490,833.333

3486,061.8263

2 91 4.45499,236.111

1489,495.4412

3 90 4.72556,250.000

0539,396.1423

4 91596,555.555

5525,668.5915

DrakeDrake University

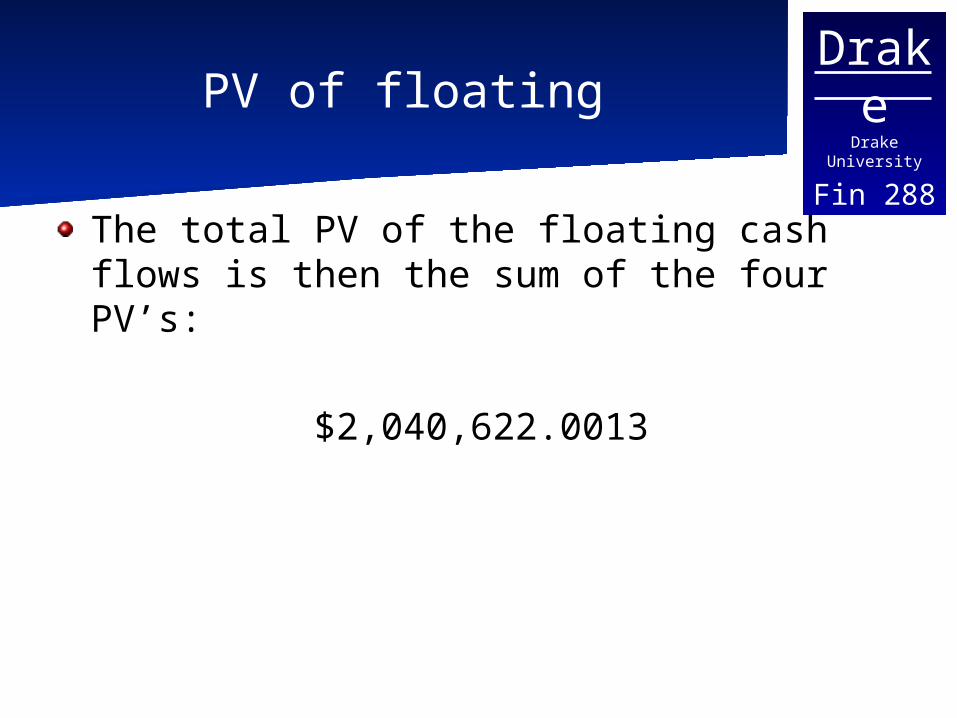

Fin 288PV of floating

The total PV of the floating cash flows is then the sum of the four PV’s:

$2,040,622.0013

DrakeDrake University

Fin 288Swap rate

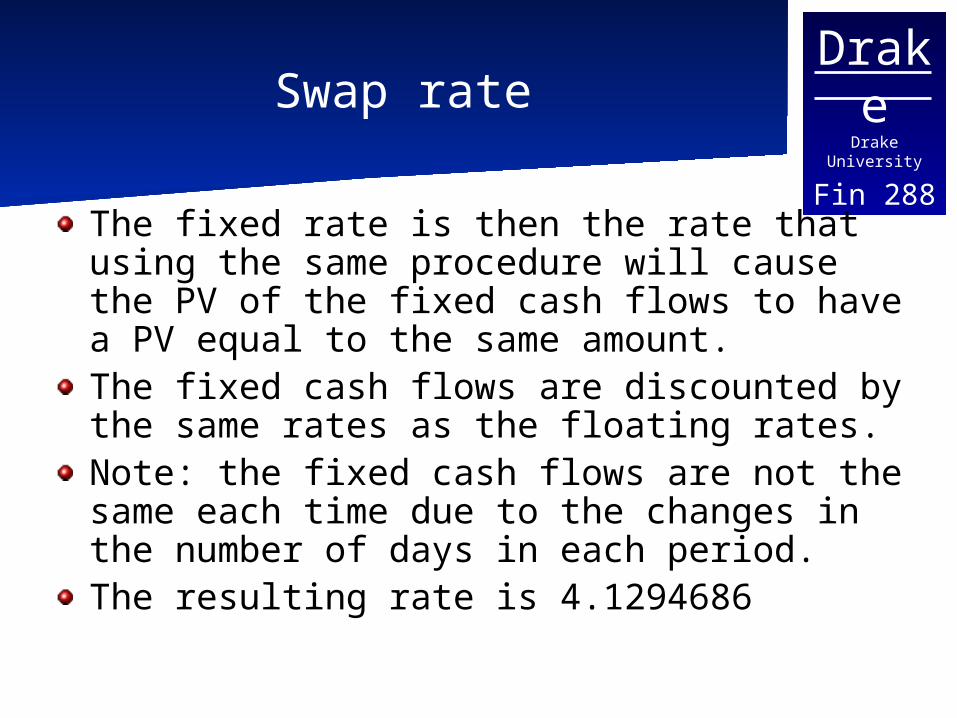

The fixed rate is then the rate that using the same procedure will cause the PV of the fixed cash flows to have a PV equal to the same amount.The fixed cash flows are discounted by the same rates as the floating rates.Note: the fixed cash flows are not the same each time due to the changes in the number of days in each period.The resulting rate is 4.1294686

DrakeDrake University

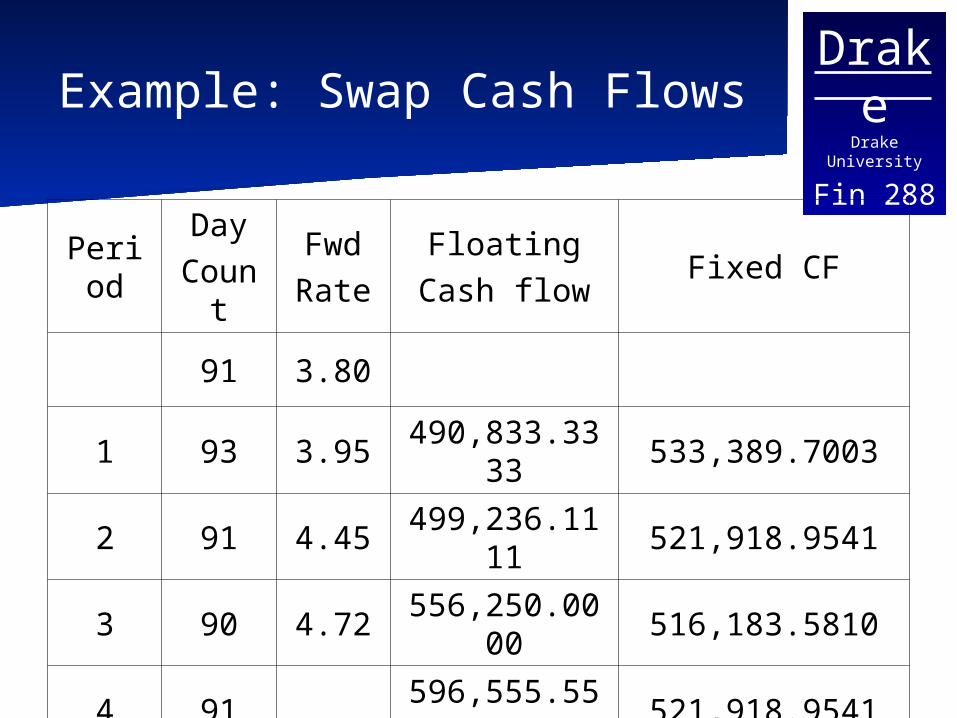

Fin 288Example: Swap Cash Flows

Period

DayCount

FwdRate

FloatingCash flow

Fixed CF

91 3.80

1 93 3.95490,833.333

3533,389.7003

2 91 4.45499,236.111

1521,918.9541

3 90 4.72556,250.000

0516,183.5810

4 91596,555.555

5521,918.9541

DrakeDrake University

Fin 288Swap Spread

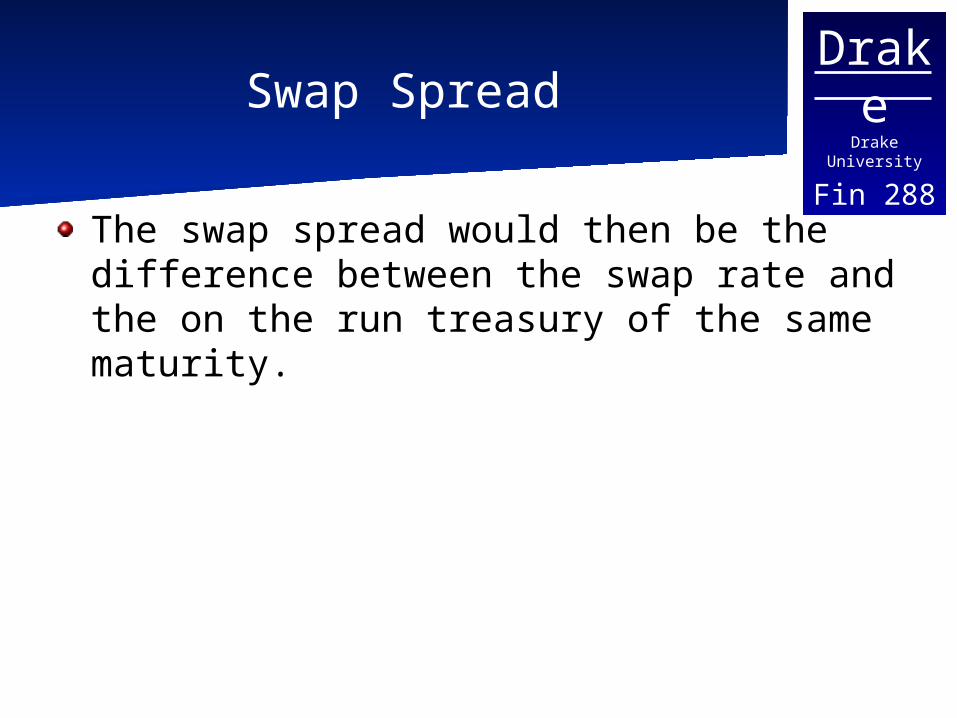

The swap spread would then be the difference between the swap rate and the on the run treasury of the same maturity.

DrakeDrake University

Fin 288Swap valuation revisited

The value of the swap will change over time.After the first payments are made, the futures prices and corresponding interest rates have likely changed. The actual second payment will be based upon the 3 month LIBOR at the end of the first period.Therefore the value of the swap is recalculated.

DrakeDrake University

Fin 288Swap Curve

The Eurodollar futures contract provides a set of 3 month forward LIBOR rates for the next 10 years.This could be used to construct a set of swap rates at different maturities or the swap curve.

DrakeDrake University

Fin 288Currency Swaps

The primary purpose of a currency swap is to transform a loan denominated in one currency into a loan denominated in another currency. In a currency swap, a principal must be specified in each currency and the principal amounts are exchanged at the beginning and end of the life of the swap. The principal amounts are approximately equal given the exchange rate at the beginning of the swap.

DrakeDrake University

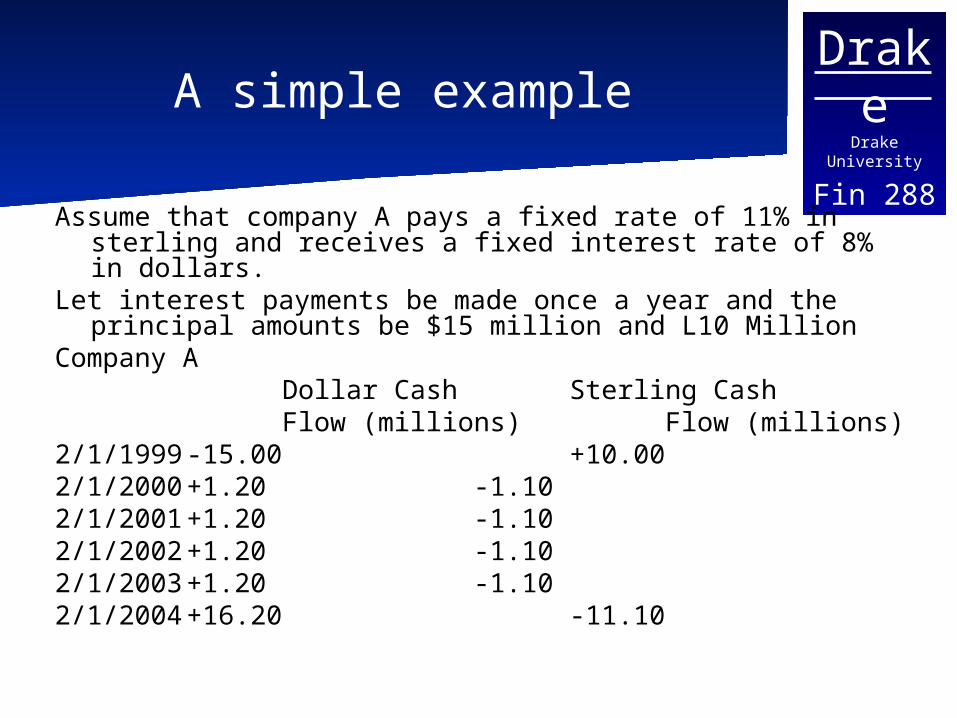

Fin 288A simple example

Assume that company A pays a fixed rate of 11% in sterling and receives a fixed interest rate of 8% in dollars.

Let interest payments be made once a year and the principal amounts be $15 million and L10 Million

Company ADollar Cash Sterling CashFlow (millions) Flow (millions)

2/1/1999 -15.00 +10.002/1/2000 +1.20 -1.102/1/2001 +1.20 -1.102/1/2002 +1.20 -1.102/1/2003 +1.20 -1.102/1/2004 +16.20 -11.10

DrakeDrake University

Fin 288Intuition

Suppose A could issue bonds in the US for 8% interest, the swap allows it to use the 15 million to actually borrow 10 million sterling at 11% (A can invest L 10M @ 11% but is afraid that $ will strength it wants US denominated investment)

DrakeDrake University

Fin 288Comparative Advantage Again

The argument for this is very similar to the comparative advantage argument presented earlier for interest rate swaps.It is likely that the domestic firm has an advantage in borrowing in its home country.

DrakeDrake University

Fin 288

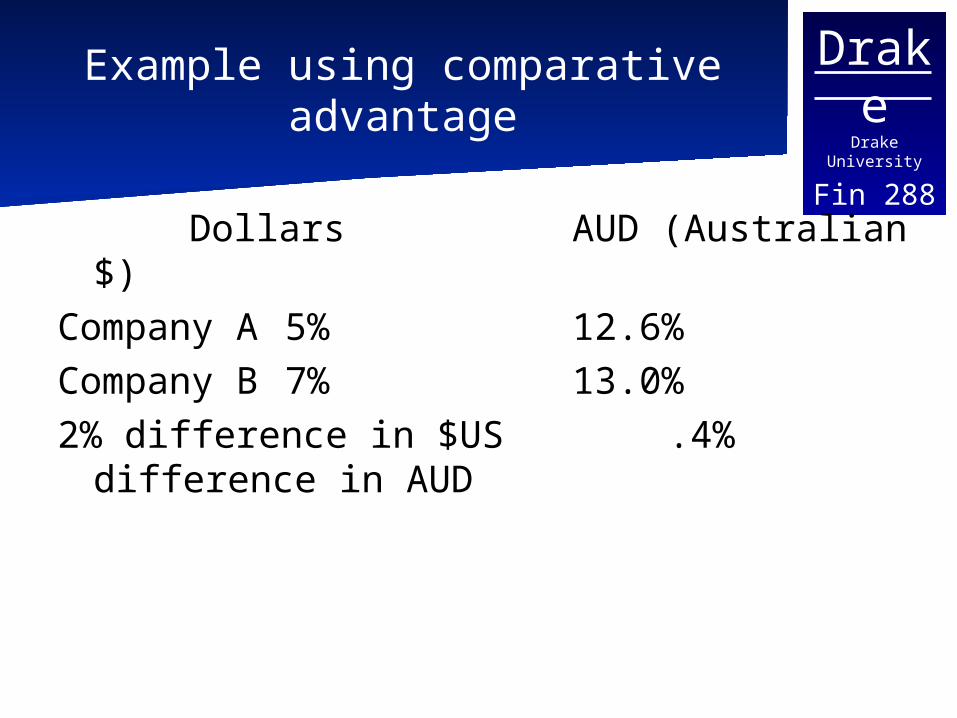

Example using comparative advantage

Dollars AUD (Australian $)

Company A 5% 12.6%Company B 7% 13.0%2% difference in $US .4% difference in

AUD

DrakeDrake University

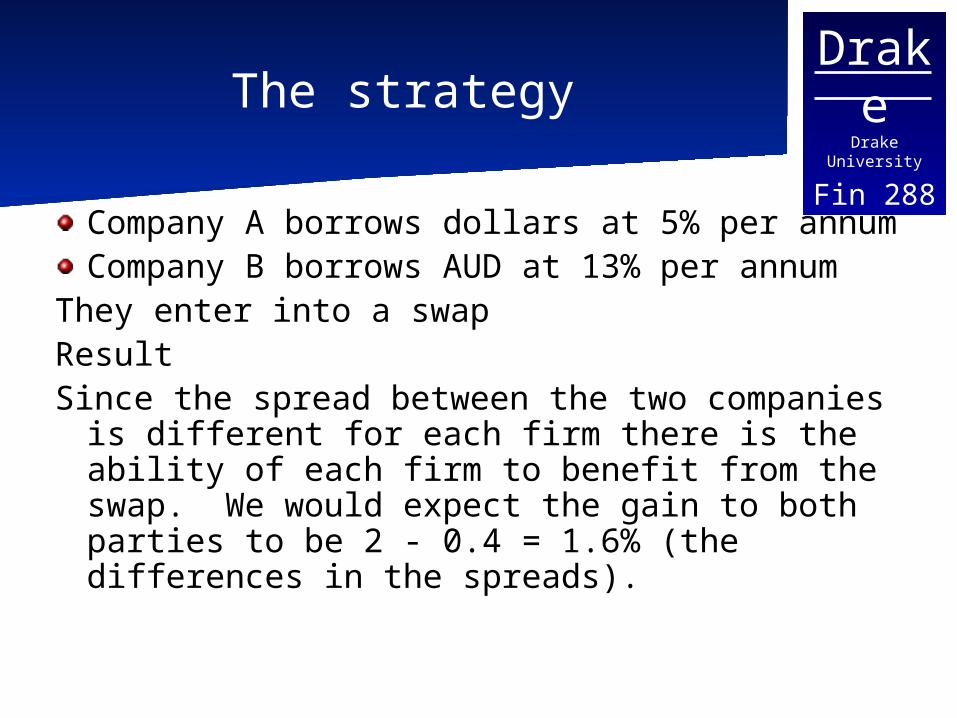

Fin 288The strategy

Company A borrows dollars at 5% per annumCompany B borrows AUD at 13% per annum

They enter into a swapResult Since the spread between the two companies is

different for each firm there is the ability of each firm to benefit from the swap. We would expect the gain to both parties to be 2 - 0.4 = 1.6% (the differences in the spreads).

DrakeDrake University

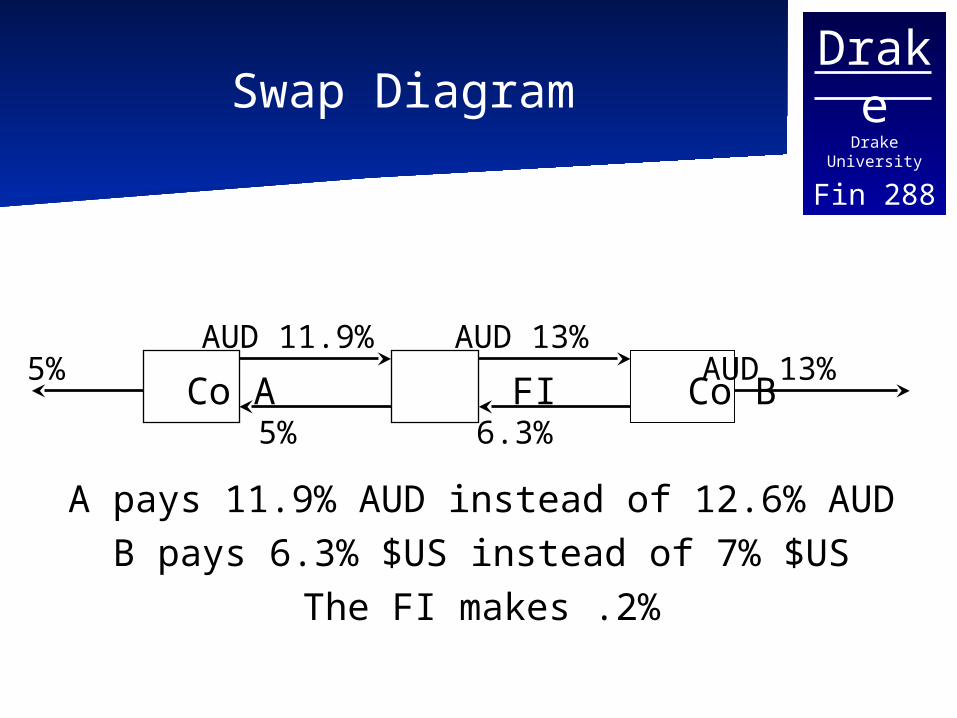

Fin 288Swap Diagram

Co A FI Co B

A pays 11.9% AUD instead of 12.6% AUDB pays 6.3% $US instead of 7% $US

The FI makes .2%

5% AUD 13%

6.3%

AUD 11.9%

5%

AUD 13%

DrakeDrake University

Fin 288Valuation of Currency Swaps

Using Bond TechniquesAssuming there is no default risk the currency swap can be decomposed into a position in two bonds, just like an interest rate swap.In the example above the company is long a sterling bond and short a dollar bond. The value of the swap would then be the value of the two bonds adjusted for the spot exchange rate.

DrakeDrake University

Fin 288Swap valuation

Let S = the spot exchange rate at the beginning of the swap, BF is the present value of the foreign denominated bond and BD is the present value of the domestic bond. Then the value is given as

Vswap = SBF – BD

The correct discount rate would then depend upon the term structure of interest rates in

each country

DrakeDrake University

Fin 288Other swaps

Swaps can be constructed from a large number of underlying assets. Instead of the above examples swaps for floating rates on both sides of the transaction. The principal can vary through out the life of the swap.They can also include options such as the ability to extend the swap or put (cancel the swap). The cash flows could even extend from another asset such as exchanging the dividends and capital gains realized on an equity index for a fixed or floating rate.

The Discussion of Commodity Swaps follows the material in Derivative Markets by McDonald

DrakeDrake University

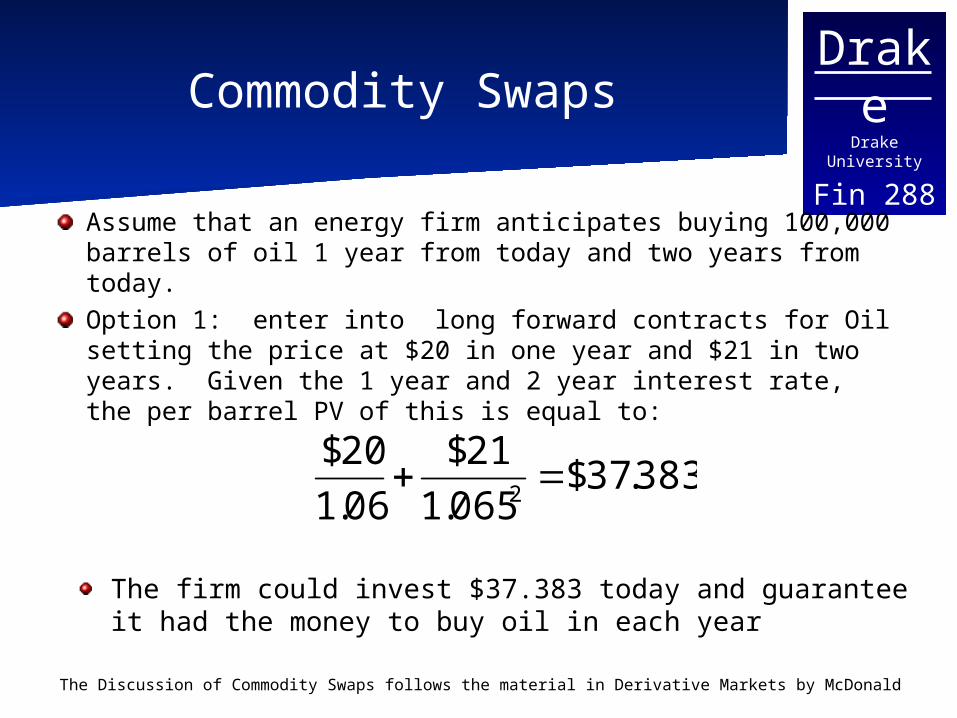

Fin 288Commodity Swaps

Assume that an energy firm anticipates buying 100,000 barrels of oil 1 year from today and two years from today.Option 1: enter into long forward contracts for Oil setting the price at $20 in one year and $21 in two years. Given the 1 year and 2 year interest rate, the per barrel PV of this is equal to:

383.37$065.1

21$

06.1

20$2

The firm could invest $37.383 today and guarantee it had the money to buy oil in each year

DrakeDrake University

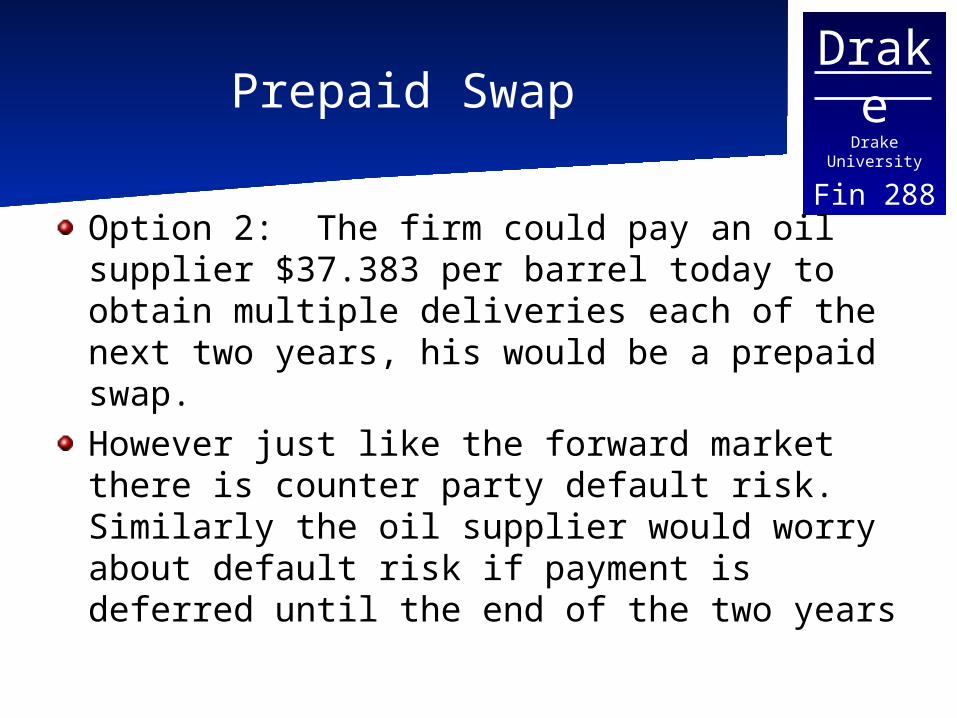

Fin 288Prepaid Swap

Option 2: The firm could pay an oil supplier $37.383 per barrel today to obtain multiple deliveries each of the next two years, his would be a prepaid swap.However just like the forward market there is counter party default risk. Similarly the oil supplier would worry about default risk if payment is deferred until the end of the two years

DrakeDrake University

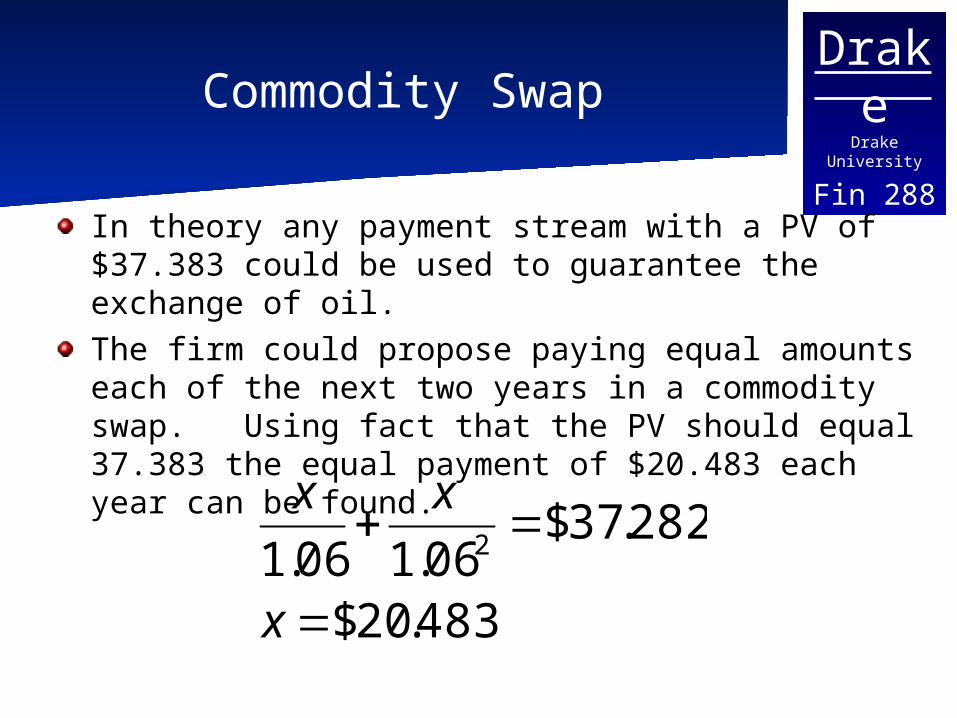

Fin 288Commodity Swap

In theory any payment stream with a PV of $37.383 could be used to guarantee the exchange of oil. The firm could propose paying equal amounts each of the next two years in a commodity swap. Using fact that the PV should equal 37.383 the equal payment of $20.483 each year can be found.

483.20$

282.37$06.106.1 2

x

xx

DrakeDrake University

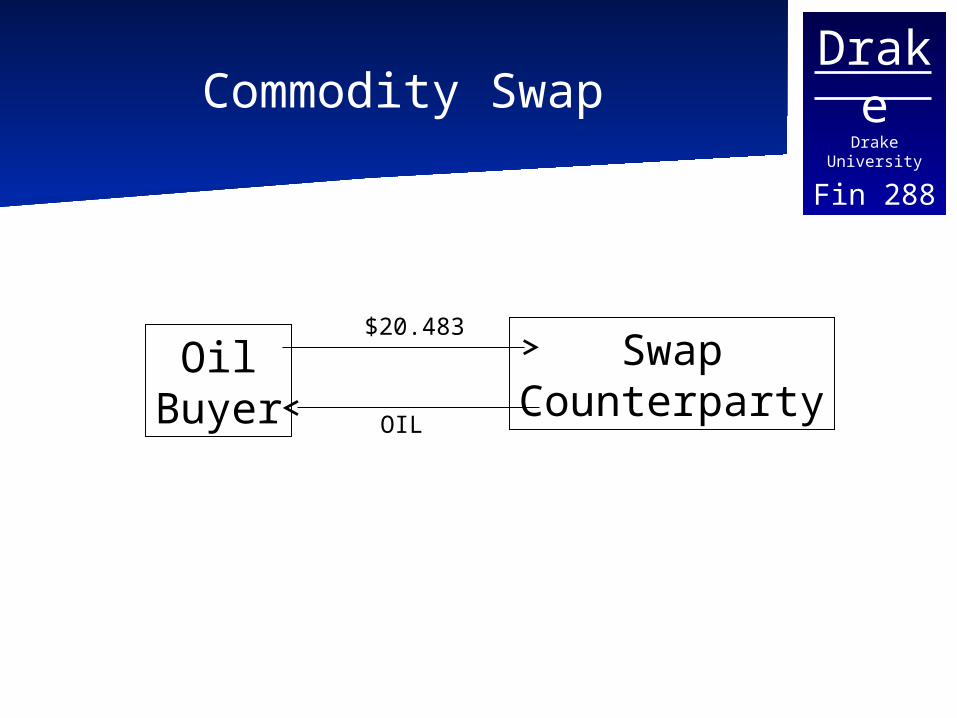

Fin 288Commodity Swap

OilBuyer

SwapCounterparty

$20.483

OIL

DrakeDrake University

Fin 288Financial Settlement

The firm could also enter into a financially settled swap based on the price of oil and purchase oil in the spot market.Assume the firm agrees to pay the swap counterparty $20.483 each period and the swap counterparty agrees to pay the firm the spot price of oil (per barrel).The net cash flow would only need be exchanged,

if the price of oil is above $20.483 the firm receives cash from the counterparty, if the price is below $20.483 the firm pays the counterparty.

DrakeDrake University

Fin 288

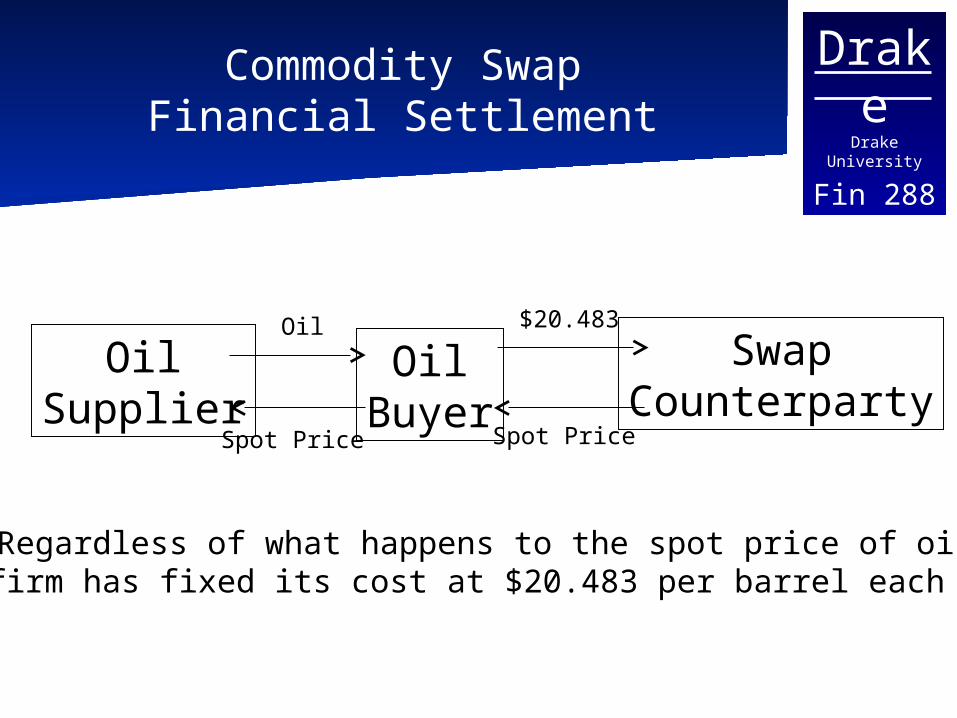

Commodity SwapFinancial Settlement

OilBuyer

SwapCounterparty

$20.483

Spot Price

OilSupplier

Spot Price

Oil

Regardless of what happens to the spot price of oil,the firm has fixed its cost at $20.483 per barrel each period

DrakeDrake University

Fin 288

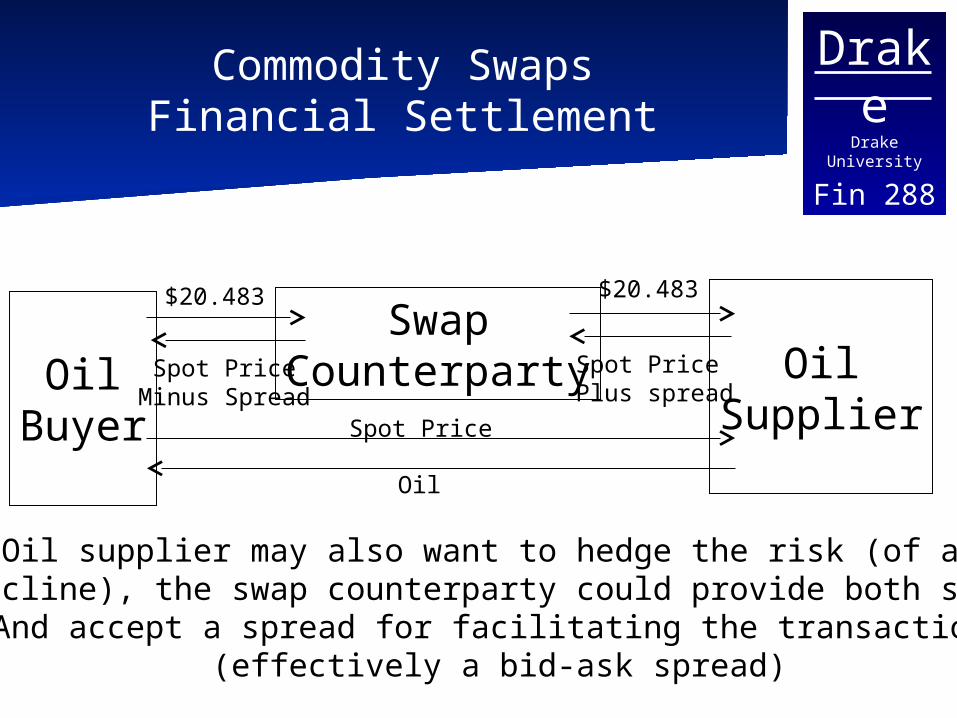

Commodity SwapsFinancial Settlement

OilBuyer

SwapCounterparty

$20.483

Spot PriceMinus Spread

OilSupplierSpot Price

Oil

The Oil supplier may also want to hedge the risk (of a pricedecline), the swap counterparty could provide both swaps

And accept a spread for facilitating the transaction (effectively a bid-ask spread)

$20.483

Spot PricePlus spread

DrakeDrake University

Fin 288

Hedging in the Forward Market

The swap counterparty might hedge risk in the forward market instead of serving as counterparty to both the buyer and supplier.Originally the swap counterparty is receiving $20.483 and paying the spot price.The swap counterparty could enter into a long forward or futures contract for oil to offset this position.

DrakeDrake University

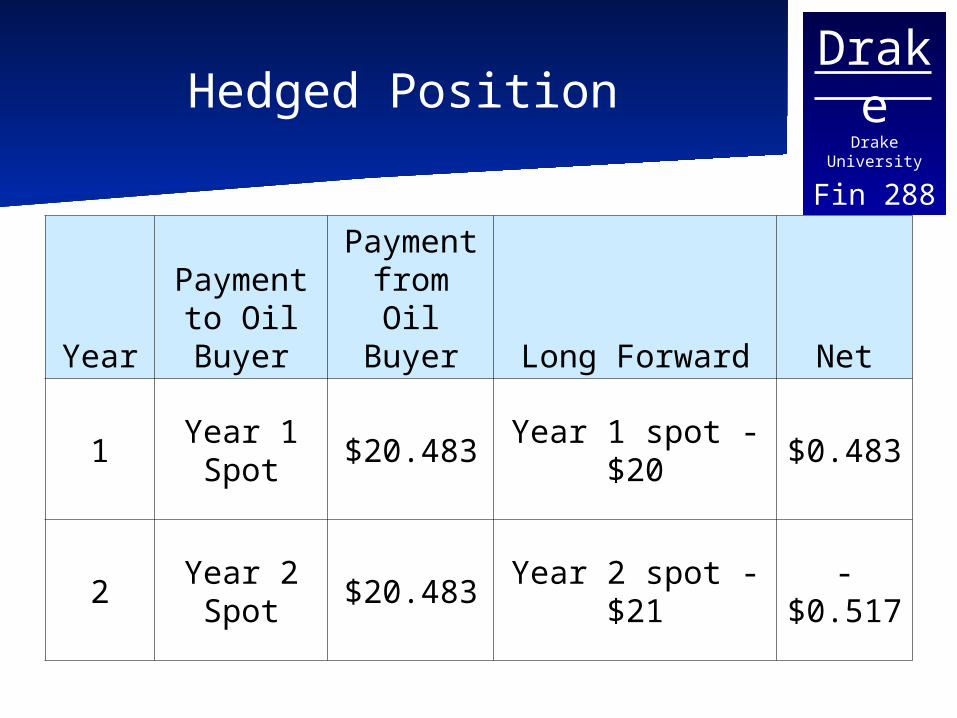

Fin 288Hedged Position

Year

Payment to Oil Buyer

Payment from Oil Buyer Long Forward Net

1Year 1 Spot

$20.483Year 1 spot -

$20$0.483

2Year 2 Spot

$20.483Year 2 spot -

$21-

$0.517

DrakeDrake University

Fin 288Hedged Position

The counterparty is effectively getting a loan by receiving $0.483 in the first year and repaying $0.517 in the second year.This works if the firm can invest the first year cash flow at a rate that allows it to make the payment in the second year. If rates drop the firm may have a loss – there is an interest rate exposure that is unhedged.

DrakeDrake University

Fin 288“Beyond Plain Vanilla”

Most of the examples so far have been fairly straight forward with the cash flows based on a relatively simple formula (the fixed for floating interest rate swap is often referred to as a “plain vanilla swap”).However the cash flows can be tied to more complex formulas and notional principal can change through time.

*From Derivative Markets by McDonald

DrakeDrake University

Fin 288

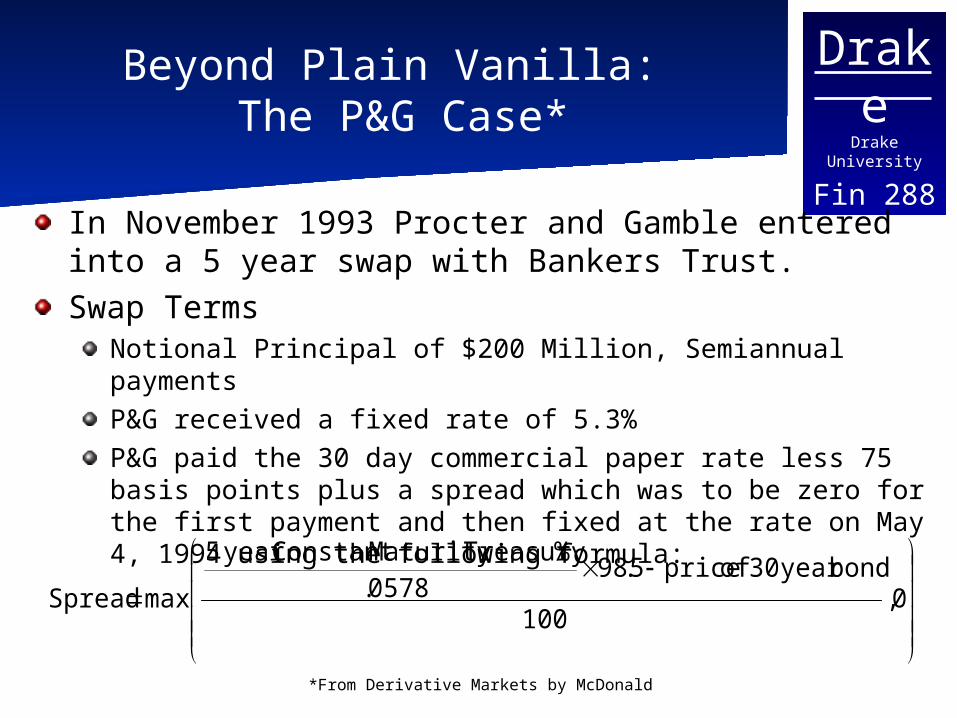

Beyond Plain Vanilla: The P&G Case*

In November 1993 Procter and Gamble entered into a 5 year swap with Bankers Trust.Swap Terms

Notional Principal of $200 Million, Semiannual paymentsP&G received a fixed rate of 5.3%P&G paid the 30 day commercial paper rate less 75 basis points plus a spread which was to be zero for the first payment and then fixed at the rate on May 4, 1994 using the following formula:

0,

100

bondyear 30 of price5.980578.

%TreasuryMaturity Constant year 5

max Spread

DrakeDrake University

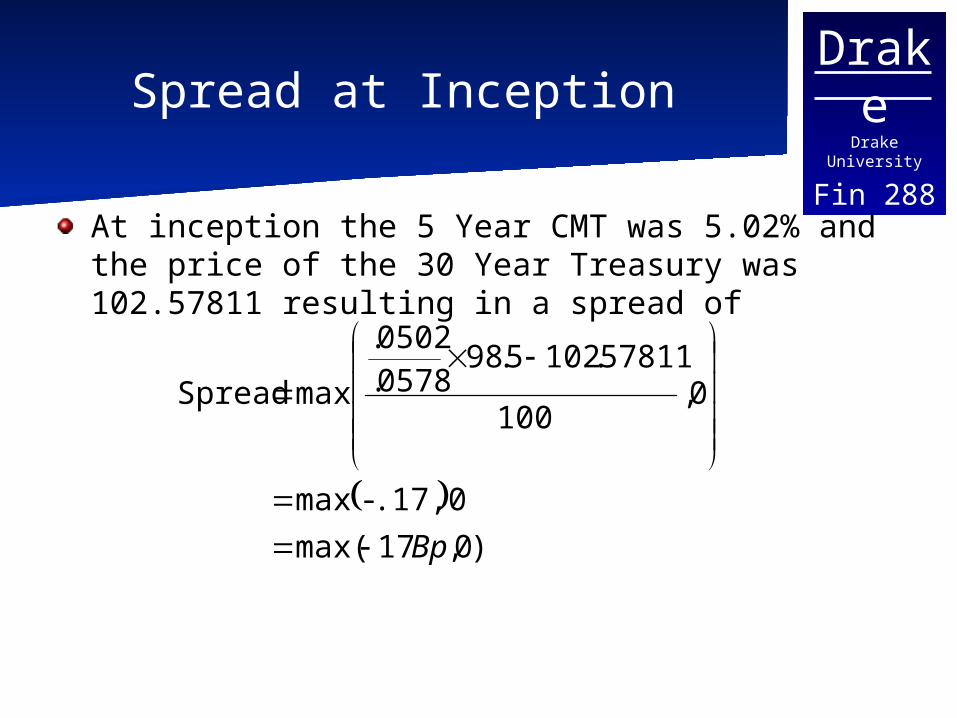

Fin 288Spread at Inception

At inception the 5 Year CMT was 5.02% and the price of the 30 Year Treasury was 102.57811 resulting in a spread of

)0,17max(

.17,0-max

0,100

57811.1025.980578.0502.

max Spread

Bp

DrakeDrake University

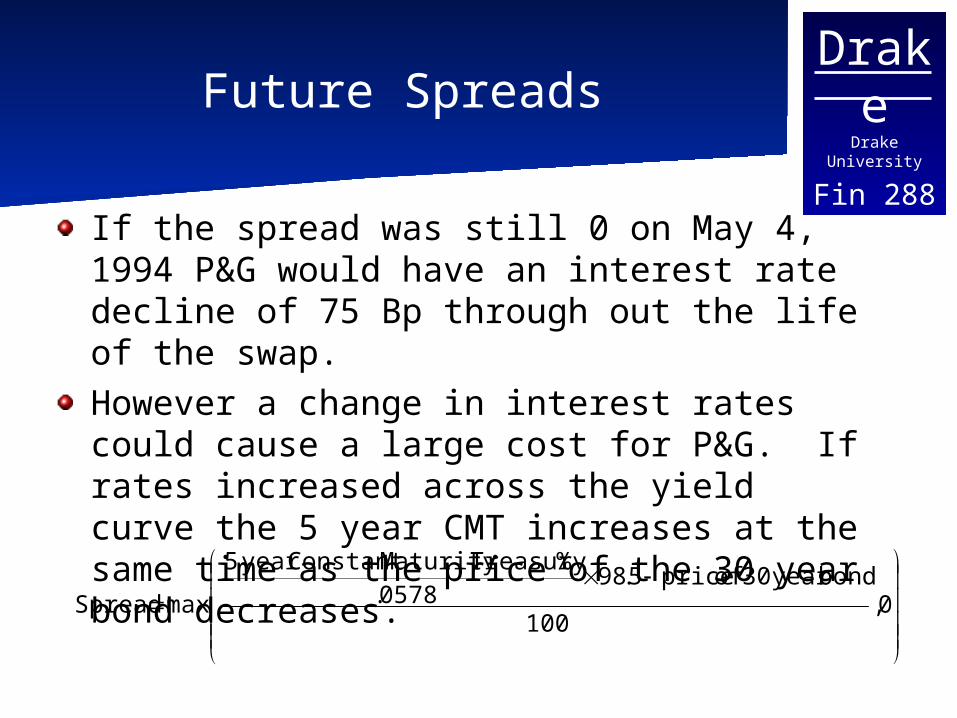

Fin 288Future Spreads

If the spread was still 0 on May 4, 1994 P&G would have an interest rate decline of 75 Bp through out the life of the swap.However a change in interest rates could cause a large cost for P&G. If rates increased across the yield curve the 5 year CMT increases at the same time as the price of the 30 year bond decreases.

0,

100

bondyear 30 of price5.980578.

%TreasuryMaturity Constant year 5

max Spread

DrakeDrake University

Fin 288P&G’s Problem

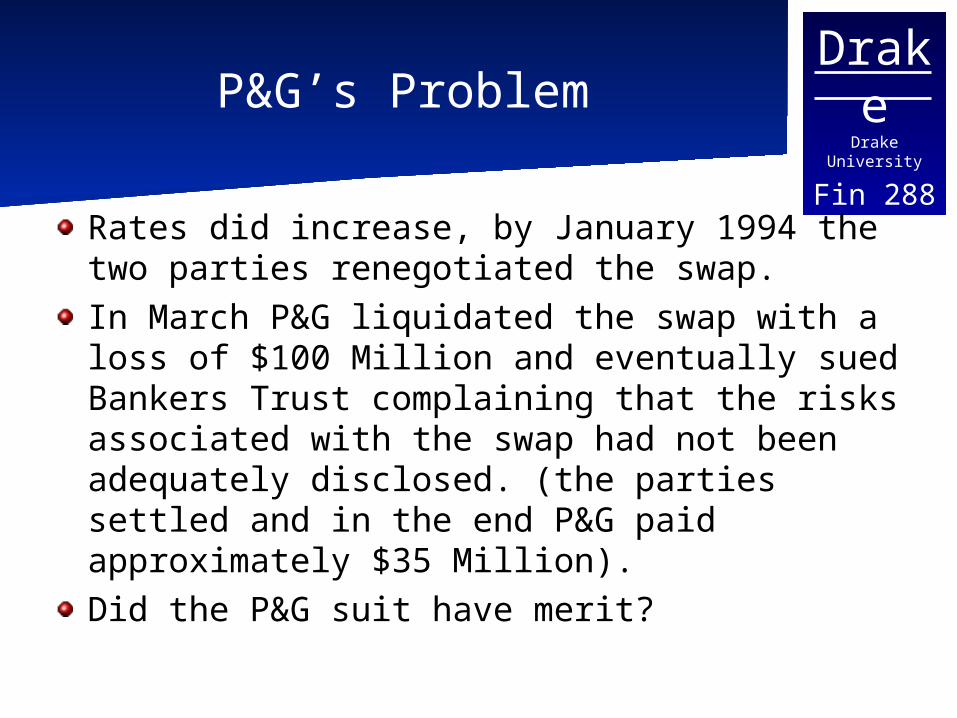

Rates did increase, by January 1994 the two parties renegotiated the swap.In March P&G liquidated the swap with a loss of $100 Million and eventually sued Bankers Trust complaining that the risks associated with the swap had not been adequately disclosed. (the parties settled and in the end P&G paid approximately $35 Million).Did the P&G suit have merit?

DrakeDrake University

Fin 288

Beyond Plain Vanilla Swaps other examples

Amortizing Swap -- The notional principal is reduced over time. This decreases the fixed payment. Useful for managing mortgage portfolios and mortgage backed securities.Accreting Swap – The notional principal increases over the life of the swap. Useful in construction finances. For example is the builder draws down an amount of financing each period for a number of periods.

DrakeDrake University

Fin 288Beyond Plain Vanilla

You can combine amortizing and accreting swaps to allow the notional principal to both increase and decrease.

Seasonal Swap -- Increase and decrease of notional principal based of f of designated plan

Roller Coaster Swap -- notional principal first increases the amortizes to zero.

DrakeDrake University

Fin 288Off Market Swap

The interest rate is set at a rate above market value.For example the fixed rate may pay 9% when the yield curve implies it should pay 8%.The PV of the extra payments is transferred as a one time fee at the beginning of the swap (thus keeping the initial value equal to zero)

DrakeDrake University

Fin 288

Forward and Extension Swaps

Forward swap – the payments are agreed to begin at some point in time in the futureIf the rates are based on the current forward rate there should not be any exchange of principal when the payments begin. Other wise it is an off market swap and some form of compensation is neededExtension Swap – an agreement to extend the current swap (a form of forward swap)

DrakeDrake University

Fin 288Basis Swaps

Both parties pay floating rates based upon different indexes. For example one party may pay the three month LIBOR while the other pays the three month T- Bill.The impact is that while the rates generally move together the spread actually widens and narrows, Therefore the return on the swap is based upon the spread.

DrakeDrake University

Fin 288Yield Curve Swaps

Both parties pay floating but based off of different maturities. Is similar to a basis swap since the effective result is based on the spread between the two rates. A steepening curve thus benefits the payer of the shorter maturity rate. This is utilized by firms with a mismatch of maturities in assets and liabilities (banks for example). It can hedge against changes in the yield curve via the swap.

DrakeDrake University

Fin 288Rate differential (diff) swap

Payments tied to rate indexes in different currencies, but payments are made in only one currency.

DrakeDrake University

Fin 288Corridor Swap

Payments obligation only occur in a given range of rates. For example if the LIBOR rate is between 5 and 7%.The swap is basically a tool based on the uncertainty of rates.

DrakeDrake University

Fin 288Flavored Currency Swaps

The basic currency swap can be modified similar to many of the modifications just discussed.Swaps may also be combined to produce desired outcomes. CIRCUS Swap (Combined interest rate and currency swap). Combines two basic swaps

DrakeDrake University

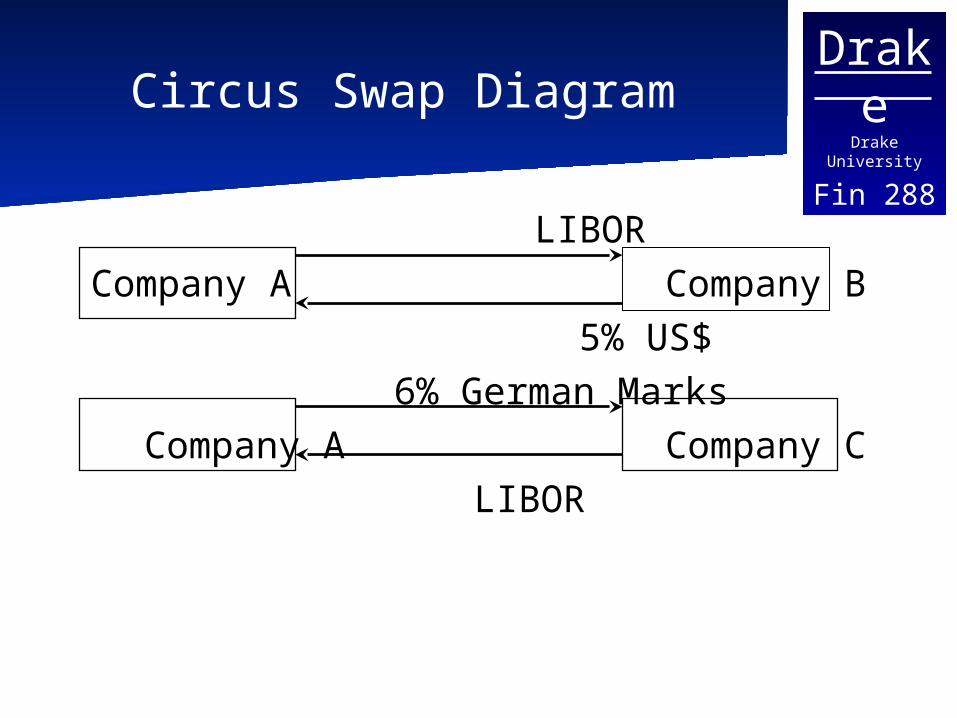

Fin 288Circus Swap Diagram

LIBORCompany A Company B

5% US$ 6% German Marks

Company A Company CLIBOR

DrakeDrake University

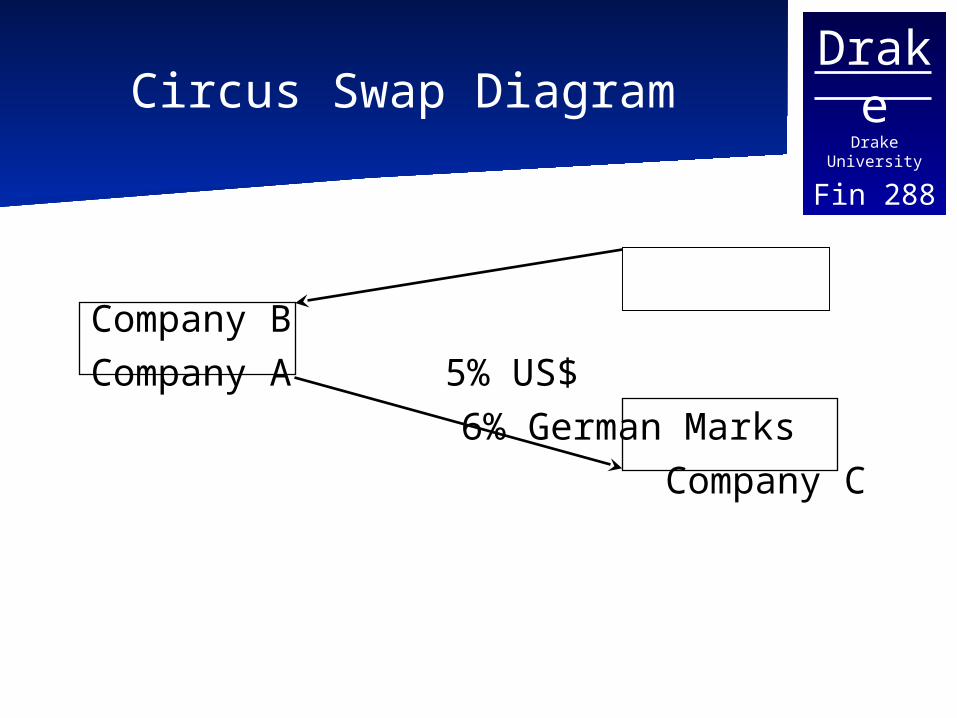

Fin 288Circus Swap Diagram

Company B

Company A 5% US$ 6% German Marks

Company C

DrakeDrake University

Fin 288Swapation

An option on a swap that specifies the tenor, notional principal fixed rate and floating ratePrice is usually set a a % of notional principal Receiver Swapation

The holder has the right to enter into a swap as the fixed – rate receiver

Payer SwapationThe holder has the right to enter into a particular swap as the fixed rate payer.

DrakeDrake University

Fin 288

Swapation as call (or put) Options

Receiver swapation – similar to a call option on a bond. The owner receives a fixed payment (like a coupon payment) and pays a floating rate (the exercise price)Payer swapation – if exercised the owner is paying a stream similar to the issue of a bond.

DrakeDrake University

Fin 288In-the-Money Swapations

A receiver swapation is in the money if interest rates fall. The owner is paying a lower fixed rate in exchange for the fixed rate specified in the contract. Similarly a payer swapation is generally in the money if interest rates increase since the owner will receive a higher floating rate.

DrakeDrake University

Fin 288When to Exercise

The owner of the receiver swapation should exercise if the fixed rate on the swap underlying the swapation is greater than the market fixed rate on a similar swap. In this case the swap is paying a higher rate than that which is available in the market.

DrakeDrake University

Fin 288

A fixed income swapation example

Consider a firm that has issued a corporate bond with a call option at a given date in the future. The firm has paid for the call option by being forced to pay a higher coupon on the bond than on a similar noncallable bond.Assume that the firm has determined that it does not want to call the bond at its first call date at some point in the future.The call option is worthless to the firm, but it should theoretically have value.

DrakeDrake University

Fin 288

Capturing the value of the call

The firm can sell a receiver swapation with terms that match the call feature of the bond.The firm would receive for this a premium that is equal to the value of the call option.

DrakeDrake University

Fin 288Example

Assume the firm has previously issued a 9% coupon bond that makes semiannual payments and matures in 7 years with a face value of $150 Million.The bond has a call option for one year from today.

DrakeDrake University

Fin 288Example continued

The firm can sell a European Receiver Swapation with an expiration in one year. The Swapation terms are for semiannual payments at a fixed rate of 9% in exchange for floating payments at LIBOR.The firm receives a premium for the swapation equal to a fixed percentage of the $150 Million notional value (equal to the value of the call option). The firm can keep the premium but has a potential obligation in one year if the counter party exercises the swap.

DrakeDrake University

Fin 288Example Continued

In one year the fixed rate for this swap is 11% The option will expire worthless since the owner can earn a fixed 11% on a similar swap. The firm gets to keep the premium.

DrakeDrake University

Fin 288Example Continued

If in one year the fixed rate of interest on a similar swap is 7% the owner will exercise the swap since it calls for a 9% fixed rate. The firm can call the bond since rates have decreased. It can finance the call by issuing a floating rate note at LIBOR for the term of the swap. The floating rate side of the swap pays for the note and the firm is still paying the original 9% fixed, but it has also received the premium on the swapation

DrakeDrake University

Fin 288

Extendible and Cancelable swaps

Similar to extension swaps except extension swaps represent a firm commitment to extend the swap. An extendible swap has the option to extend the agreement.Arranged via a plain vanilla swap an a swapation.

DrakeDrake University

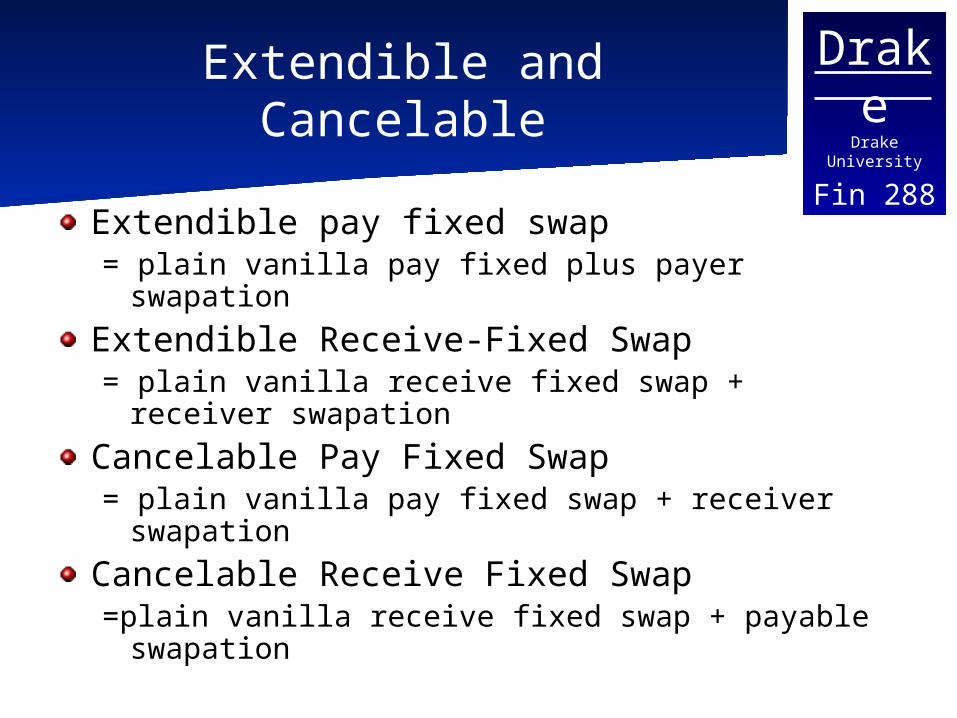

Fin 288Extendible and Cancelable

Extendible pay fixed swap= plain vanilla pay fixed plus payer swapation

Extendible Receive-Fixed Swap= plain vanilla receive fixed swap + receiver

swapation

Cancelable Pay Fixed Swap= plain vanilla pay fixed swap + receiver

swapation

Cancelable Receive Fixed Swap=plain vanilla receive fixed swap + payable

swapation

DrakeDrake University

Fin 288

Creating synthetic securities using swaps

The origins of the swap market are based in the debt market.Previously there had been restrictions on the flow of currency.A parallel loan market developed to get around restrictions on the flow of currency from one country to another, Especially restrictions imposed by the Bank of England.

DrakeDrake University

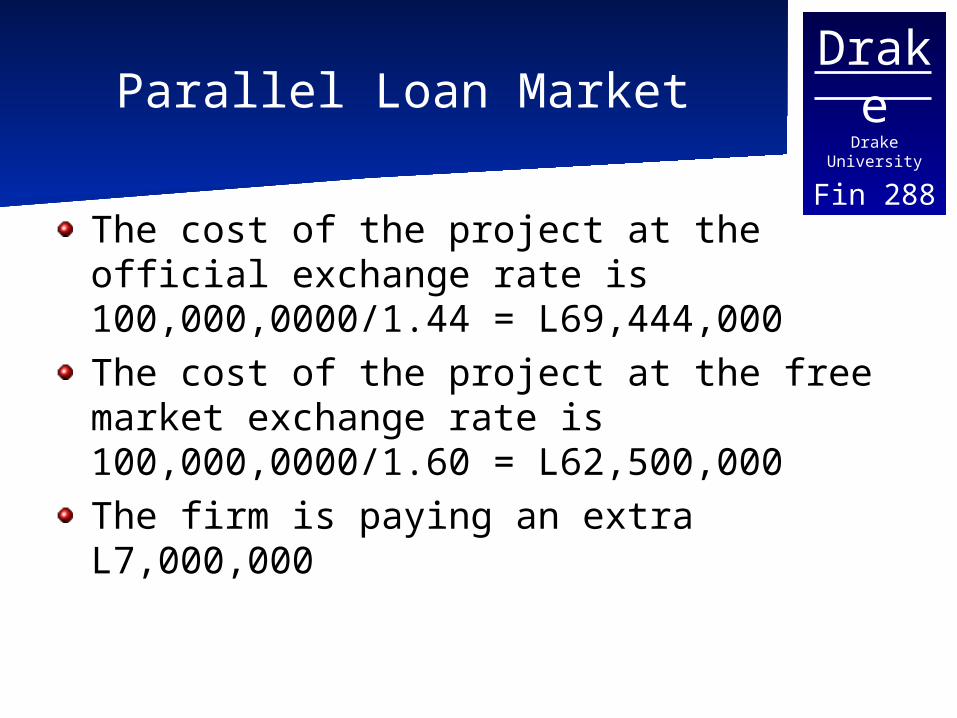

Fin 288The Parallel Loan Market

Consider two firms, one British and one American, each with subsidiaries in both countries.Assume that the free-market value of the pound is L1=$1.60 and the officially required exchange rate is L1=$1.44.Assume the British Firm wants to undertake a project in the US requiring an outlay of $100,000,000.

DrakeDrake University

Fin 288Parallel Loan Market

The cost of the project at the official exchange rate is 100,000,0000/1.44 = L69,444,000The cost of the project at the free market exchange rate is 100,000,0000/1.60 = L62,500,000The firm is paying an extra L7,000,000

DrakeDrake University

Fin 288Parallel Loan Market

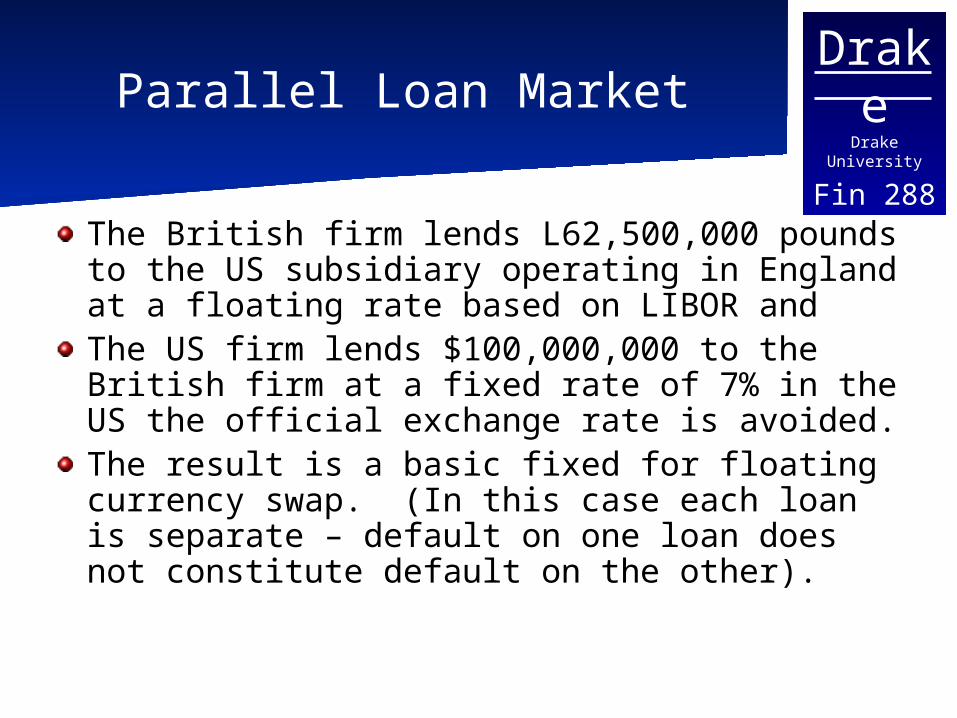

The British firm lends L62,500,000 pounds to the US subsidiary operating in England at a floating rate based on LIBOR and The US firm lends $100,000,000 to the British firm at a fixed rate of 7% in the US the official exchange rate is avoided.The result is a basic fixed for floating currency swap. (In this case each loan is separate – default on one loan does not constitute default on the other).

DrakeDrake University

Fin 288Synthetic Fixed Rate Debt

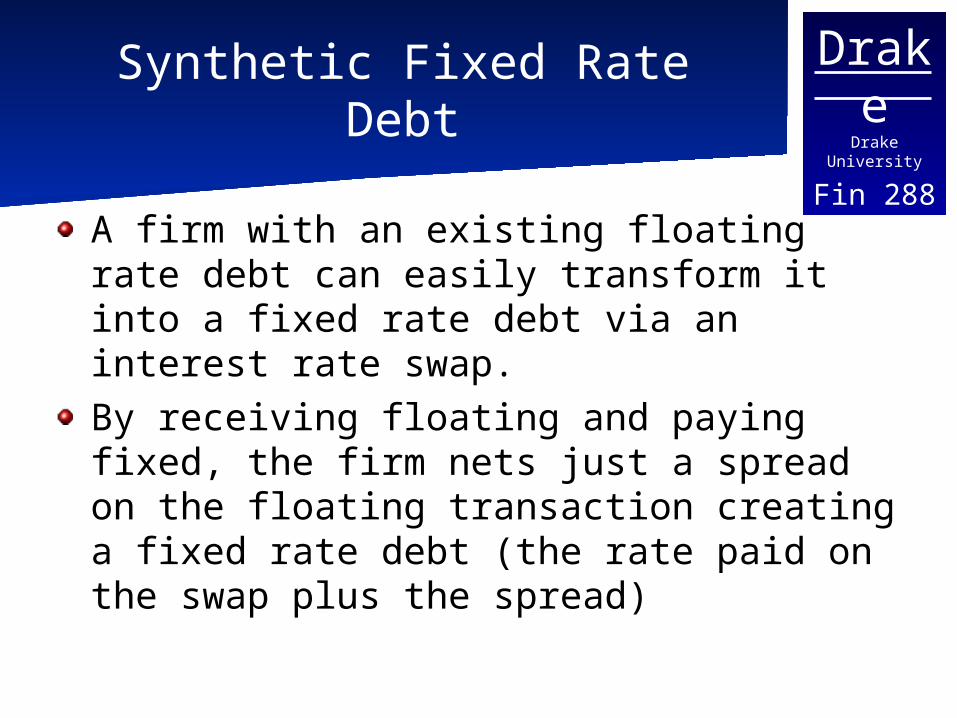

A firm with an existing floating rate debt can easily transform it into a fixed rate debt via an interest rate swap.By receiving floating and paying fixed, the firm nets just a spread on the floating transaction creating a fixed rate debt (the rate paid on the swap plus the spread)

DrakeDrake University

Fin 288Synthetic Floating Rate Debt

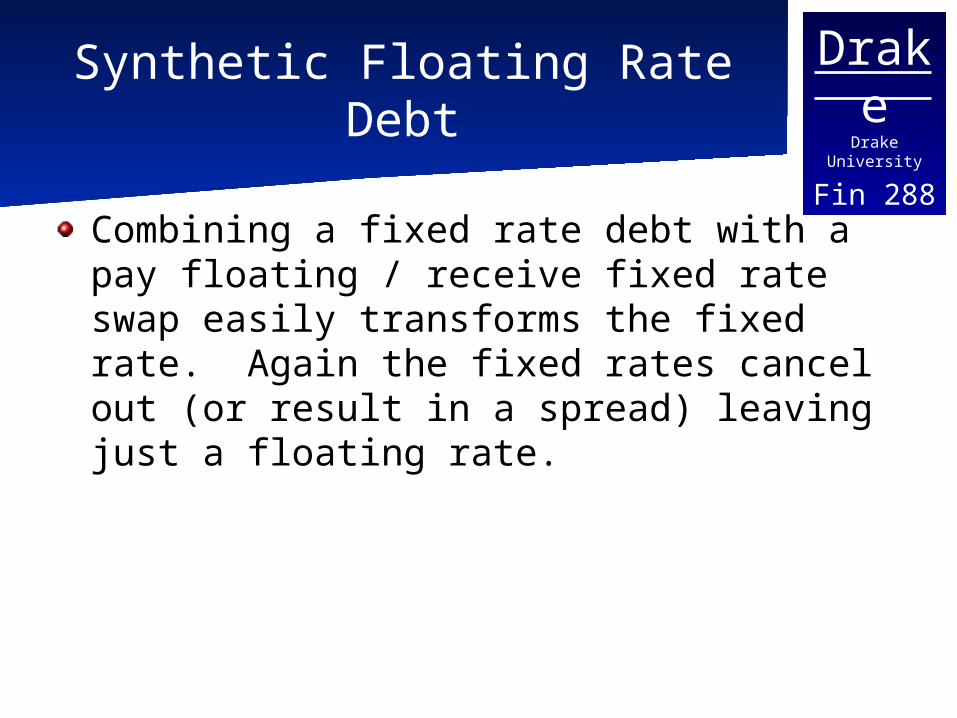

Combining a fixed rate debt with a pay floating / receive fixed rate swap easily transforms the fixed rate. Again the fixed rates cancel out (or result in a spread) leaving just a floating rate.

DrakeDrake University

Fin 288Synthetic Callable Debt

Consider a firm with an outstanding fixed rate debt without any call option.It can create a call option. If it had a call option in place it would retire the debt if called. Look at this as creating a new financing need (you need to finance the retirement of the debt.)You want the ability to call the bond but not the obligation to do so.

DrakeDrake University

Fin 288Synthetic Callable Debt

Buying a receiver swapation allows the firm to receive a fixed rate, canceling out its current fixed rate obligation. It will pay a new floating rate as part of the swap (similar to financing the call with new floating rate debt).

DrakeDrake University

Fin 288Synthetic non callable Debt

Basically the earlier example swapations.

DrakeDrake University

Fin 288

Synthetic Dual Currency Debt

Dual Currency bond – principal payments are denominated in one currency and coupon payments denominated in another currency.Assume you own a bond that makes its payments in US dollars, but you would prefer the coupon payments to be in another currency with the principal repayment in dollars. A fixed for fixed currency swap would allow this to happen

DrakeDrake University

Fin 288

Synthetic Dual Currency Debt

Combine a receive fixed German marks and pay US dollars swap with the bond. The dollars received from the bond are used to pay the dollar commitment on the swap. You then just receive the German Marks.

DrakeDrake University

Fin 288All in Cost

The IRR for a given financing alternative, it includes all costs including administration, flotation , and actual cash flows.The cost is simply the rate that makes the PV of the cash flows equal to the current value of the borrowing.

DrakeDrake University

Fin 288

Compare two alternative proposals

A 10 year semiannual 7% coupon bond with a principal of $40 million priced at parA loan of $40 million for 10 years at a floating rate of LIBOR + 30 Bps reset every six months with the current LIBOR rate of 6.5%. Plus a swap transforming the loan to a fixed rate commitment. The swap will require the firm to pay 6.5% fixed and receive floating.

DrakeDrake University

Fin 288All in cost

The bond has a all in cost equal to its yield to maturity, 7%Assuming the firm must pay $400,000 to enter into the swap so it only nest $39,600,000. Today. The net interest rate it pays is 6.8% implying semiannual payments of (.068/2)(40,000,000) = $1,360,000 plus a final payment of 40,000,000. This implies a rate of .034703 every six months or .069406 every year.

DrakeDrake University

Fin 288

BF Goodrich and RabobankAn early swap example*

In the early 1980’s BF Goodrich needed to raise new funds, but its credit rating had been downgraded to BBB-. The firm needed $50,000,000 to fund continuing operations.They wanted long term debt in the range of 8 to 10 years and a fixed rate. Treasury rates were at 10.1 % and BF Goodrich anticipated paying approximately 12 to 12.5%

* taken from Kolb - Futures Options and Swaps

DrakeDrake University

Fin 288Rabobank

Rabobank was a large Dutch banking organization consisting of more than 1,000 small agricultural banks. The bank was interested in securing floating rate financing on approximately $50,000,000 in the Eurobond market. With a AAA rating Rabobank could issue fixed rate in the Eurobond market for approximately 11% and for a floating rate of LIBOR plus .25%

DrakeDrake University

Fin 288The Intermediary

Salomon Brothers suggested a swap agreement to each party.This would require BF Goodrich to issue the first public debt tied to LIBOR in the United States. Salomon Brothers felt that there would be a market for the debt because of the increase in deposits paying a floating rate due to deregulation.

DrakeDrake University

Fin 288Problems

Rabobank was interested in the deal, but fearful of credit risk. A direct swap would expose it to credit risk. Without an active swap market it was common for swaps to be arranged between the two counter parties.The two finally reached an agreement to use Morgan Guaranty as an intermediary.

DrakeDrake University

Fin 288The agreement

BF Goodrich issued a noncallable 8 year floating rate note with a principal value of $50,000,000 paying the 3 month LIBOR rate plus .5% semiannually. The bond was underwritten by Salomon.Rabobank issued a $50,000,000 non callable 8 year Eurobond with annual payments of 11%Both entered into a swap with Morgan Guaranty

DrakeDrake University

Fin 288The swaps

BF Goodrich promised to pay Morgan Guaranty 5,500,000 each year for eight years (matching the coupon on the Rabobanks debt). Morgan agreed to pay BF Goodrich a semi annual rate tied to the 3 month LIBOR equal to: .5(50,000,000)(3 mo LIBOR-x) x represents an undisclosed discountRabobank received $5,500,000 each year for 8 years and paid semi annul payments of LIBOR-x

DrakeDrake University

Fin 288The intermediary role

The two swap agreements were independent of each other eliminating the credit risk concerns of Rabobank.Morgan received a one time fee of $125,000 paid by BF Goodrich plus an annual fee of 8 to 37 Bp ($40,000 to $185,000) also paid by BF Goodrich.

DrakeDrake University

Fin 288BF Goodrich

Assuming that the discount from LIBOR was 50 Bp and that the service fee was 22.5 BP (the midpoint of the range). BF Goodrich paid an all in cost of 11.9488 % annually compared to 12 to 12.5% if they had issued the debt on their own.

DrakeDrake University

Fin 288Rabobank’s Position

At the time of financing it would have paid LIBOR plus 25 to 50 Bp. Given that it paid no fees and the fixed rate canceled out it ended up paying LIBOR - x.

DrakeDrake University

Fin 288Securing financing

BF Goodrich was able to secure financing via its use of the swaps market, this is a common use of the market.The example provides a good illustration of the idea of the comparative advantage arguments we discussed earlier.

DrakeDrake University

Fin 288

A Second Example of securing financing*

It is possible for swaps to increases accessibility two the debt marketMexcobre (Mexicana de Corbre) is the copper exporting subsidiary of Grupo Mexico. In the late 1980’s it would have had a difficult time borrowing in international credit markets due to concerns or default riskHowever it was able to borrow $210 million for 38 months from a group of banks led by Paribas

* from Managing Financial Risk by Smithson, Smith and Wilford

DrakeDrake University

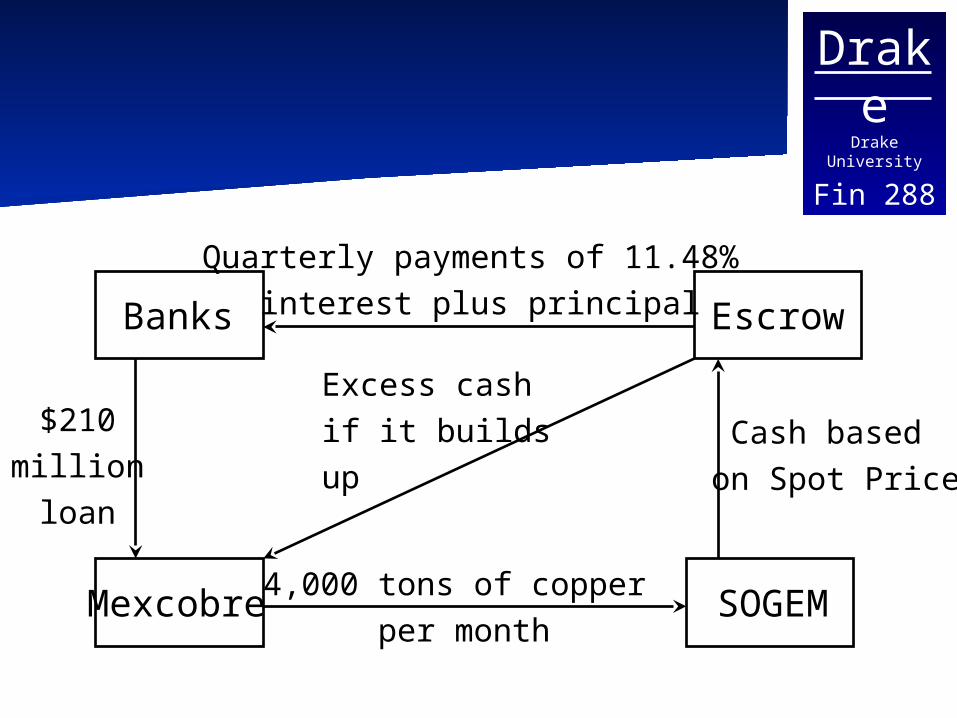

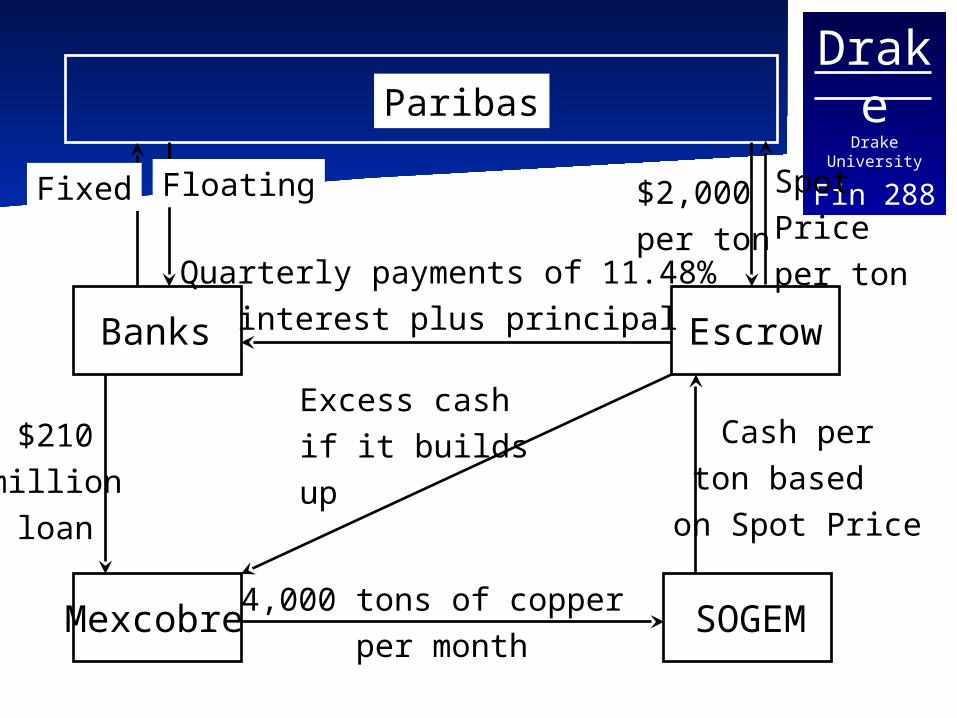

Fin 288The original loan

The banks lent the firm $210 Million at a fixed rate of 11.48%. The debt replaced borrowing from the Mexican government which had cost the firm 23%.A Belgian company Sogem agreed to buy 4,000 tons of copper per month at the prevailing spot rate from Mexcobre making payments into an escrow account in New York that was used to service the debt with any extra funds returned to Mexcobre.

DrakeDrake University

Fin 288

Banks Escrow

Mexcobre SOGEM4,000 tons of copper per month

Cash based on Spot Price

Quarterly payments of 11.48% interest plus principal

$210millionloan

Excess cashif it buildsup

DrakeDrake University

Fin 288Swaps

Swaps were added between Paribas and the escrow account to hedge the price risk of copper and between Paribas and the banks to change the banks position to a floating rate

DrakeDrake University

Fin 288

Banks Escrow

Mexcobre SOGEM4,000 tons of copper per month

Cash perton based

on Spot Price

Quarterly payments of 11.48% interest plus principal

$210millionloan

Excess cashif it buildsup

Paribas

SpotPrice per ton

FloatingFixed $2,000 per ton

DrakeDrake University

Fin 288

Duration of Interest Rate Swaps*

A plain vanilla swap can be valued as a portfolio of two bonds, therefore the duration of the swap should equal the duration of the bond portfolio.The duration can be either positive or negative depending on the side of the swap

* Kolb, Futures Options and Swaps

DrakeDrake University

Fin 288Duration of Swaps

Duration of Receive Fixed Swap = Duration of Underlying coupon bond - Duration of underlying floating Rate Bond >0

Duration of Pay Fixed Swap = Duration of underlying floating Rate Bond- Duration of Underlying coupon bond <0

DrakeDrake University

Fin 288Example

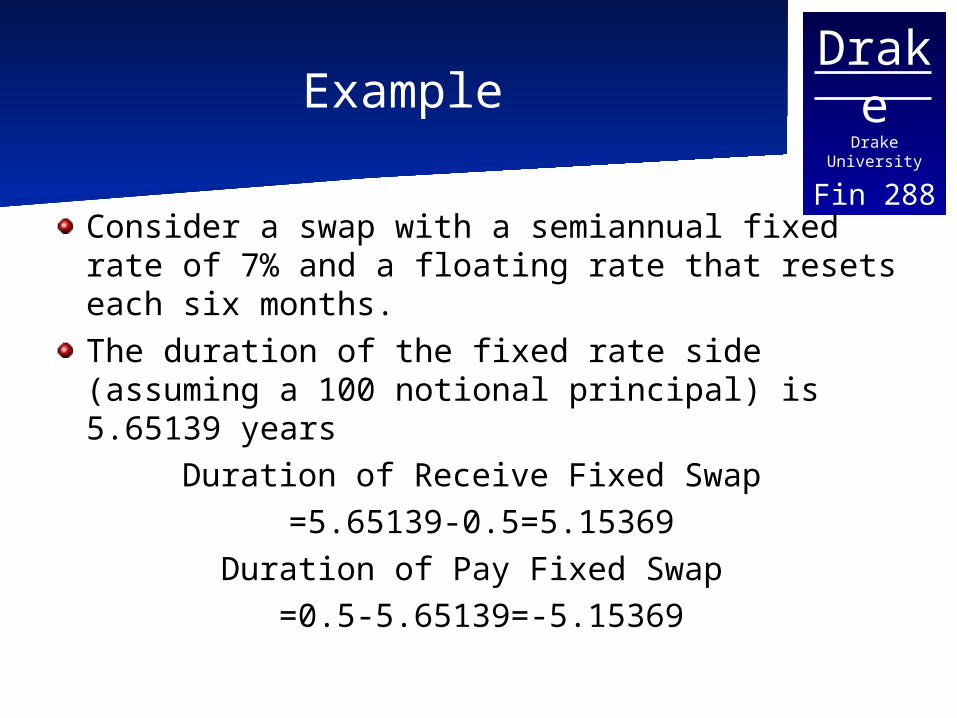

Consider a swap with a semiannual fixed rate of 7% and a floating rate that resets each six months.The duration of the fixed rate side (assuming a 100 notional principal) is 5.65139 years

Duration of Receive Fixed Swap =5.65139-0.5=5.15369

Duration of Pay Fixed Swap =0.5-5.65139=-5.15369

DrakeDrake University

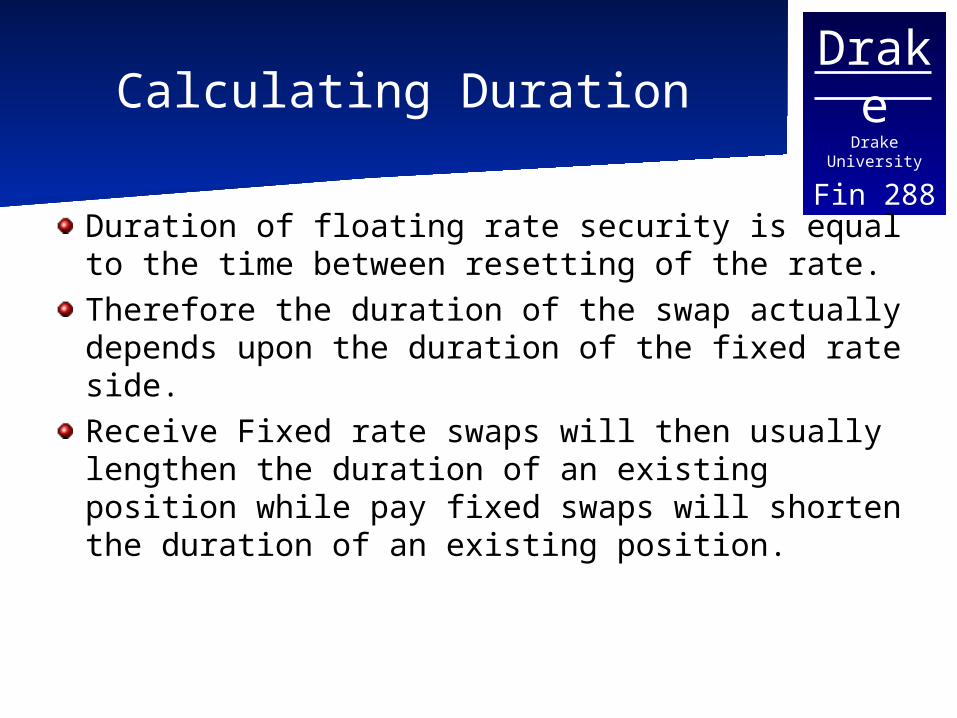

Fin 288Calculating Duration

Duration of floating rate security is equal to the time between resetting of the rate.Therefore the duration of the swap actually depends upon the duration of the fixed rate side.Receive Fixed rate swaps will then usually lengthen the duration of an existing position while pay fixed swaps will shorten the duration of an existing position.

DrakeDrake University

Fin 288Immunization with Swaps

Swaps can be used to hedge interest rate risk by impacting the duration of the assets and liabilities on the balance sheet.Going to look at a fictional financial services firm FSF

DrakeDrake University

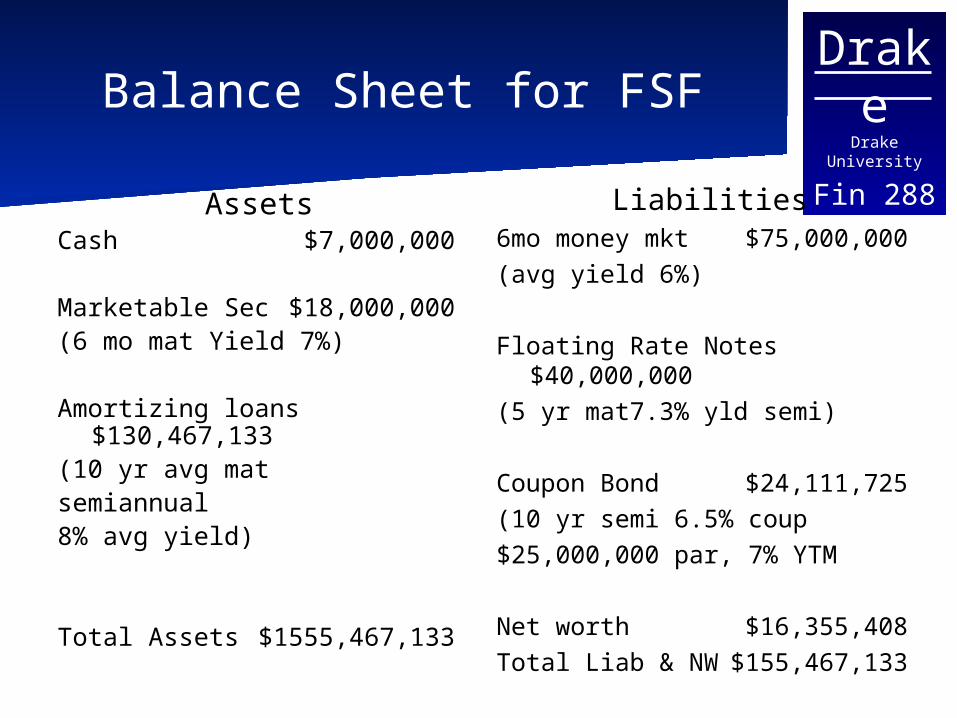

Fin 288Balance Sheet for FSF

AssetsCash $7,000,000

Marketable Sec $18,000,000(6 mo mat Yield 7%)

Amortizing loans $130,467,133(10 yr avg matsemiannual8% avg yield)

Total Assets $1555,467,133

Liabilities6mo money mkt $75,000,000(avg yield 6%)

Floating Rate Notes $40,000,000(5 yr mat7.3% yld semi)

Coupon Bond $24,111,725(10 yr semi 6.5% coup$25,000,000 par, 7% YTM

Net worth $16,355,408Total Liab & NW $155,467,133

DrakeDrake University

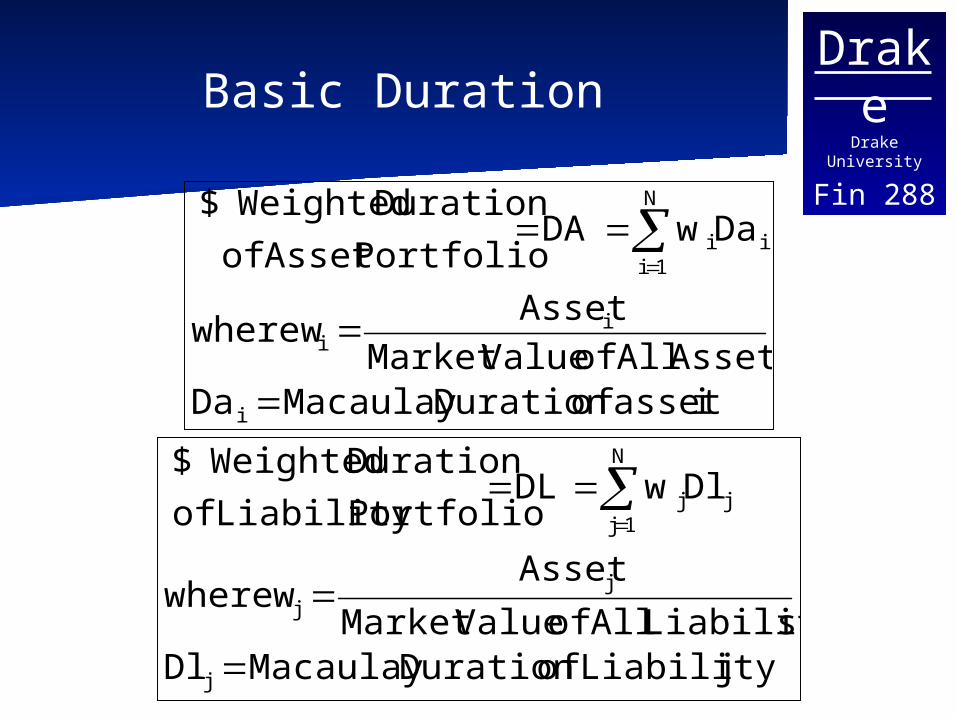

Fin 288Basic Duration

iasset ofDuration Macaulay DaAssets All of ValueMarket

Asset wwhere

DawDAPortfolioAsset of

Duration Weighted$

i

ii

i

N

1ii

jLiability ofDuration Macaulay DlsLiabilitie All of ValueMarket

Asset wwhere

DlwDLPortfolioLiability of

Duration Weighted$

j

jj

j

N

1jj

DrakeDrake University

Fin 288Duration

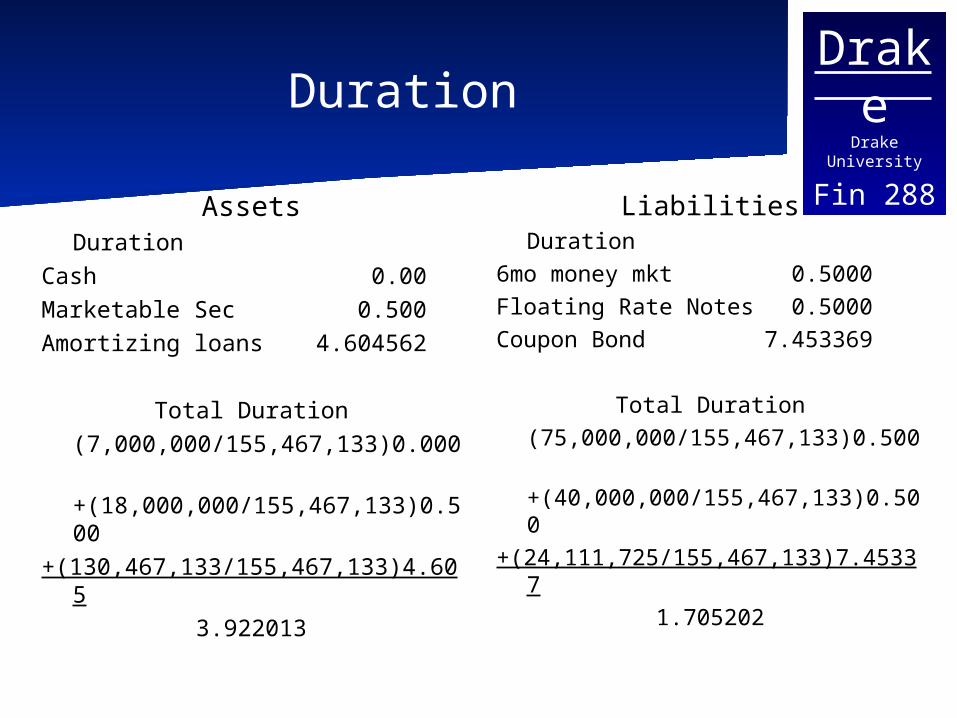

AssetsDuration

Cash 0.00Marketable Sec 0.500Amortizing loans 4.604562

Total Duration(7,000,000/155,467,133)0.000

+(18,000,000/155,467,133)0.500

+(130,467,133/155,467,133)4.605

3.922013

LiabilitiesDuration

6mo money mkt 0.5000Floating Rate Notes 0.5000Coupon Bond 7.453369

Total Duration(75,000,000/155,467,133)0.500

+(40,000,000/155,467,133)0.500+(24,111,725/155,467,133)7.4533

71.705202

DrakeDrake University

Fin 288

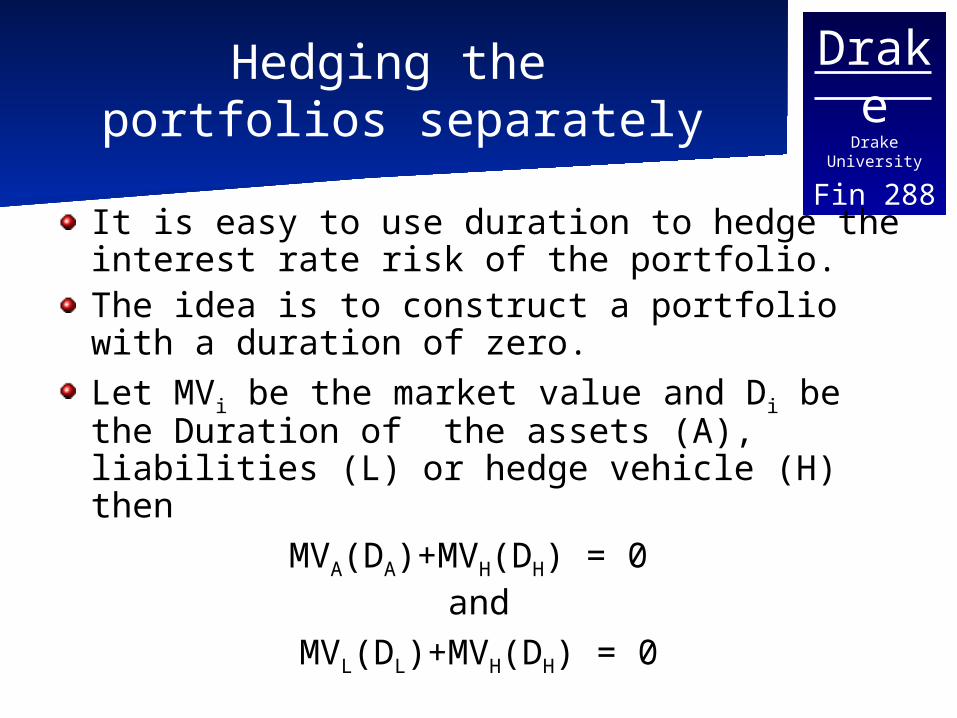

Hedging the portfolios separately

It is easy to use duration to hedge the interest rate risk of the portfolio.The idea is to construct a portfolio with a duration of zero.Let MVi be the market value and Di be the Duration of the assets (A), liabilities (L) or hedge vehicle (H) then

MVA(DA)+MVH(DH) = 0 and

MVL(DL)+MVH(DH) = 0

DrakeDrake University

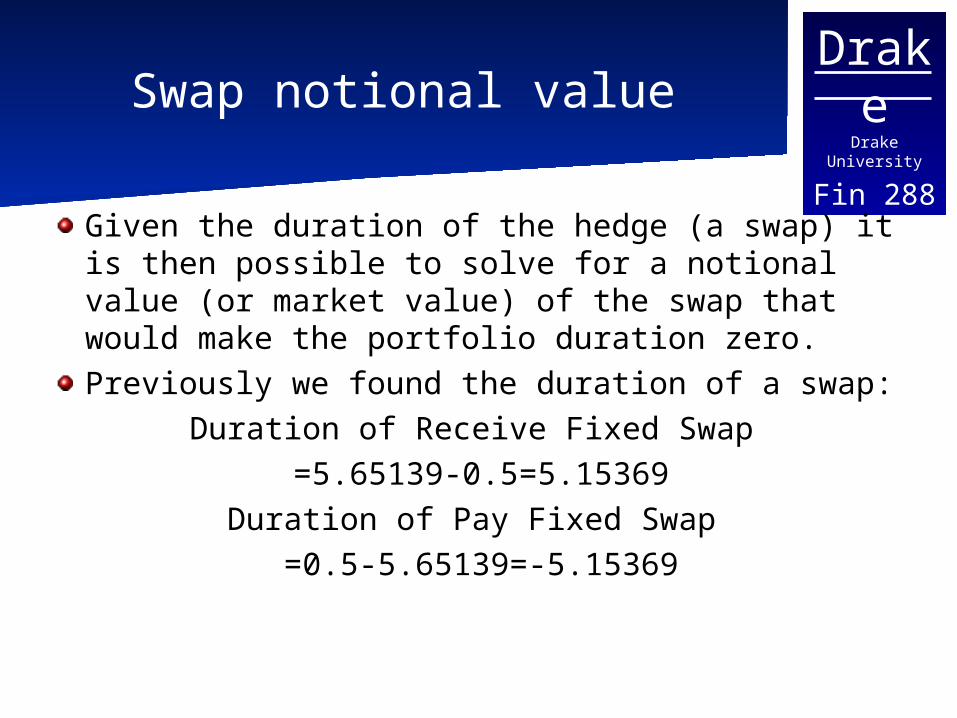

Fin 288Swap notional value

Given the duration of the hedge (a swap) it is then possible to solve for a notional value (or market value) of the swap that would make the portfolio duration zero. Previously we found the duration of a swap:

Duration of Receive Fixed Swap =5.65139-0.5=5.15369

Duration of Pay Fixed Swap =0.5-5.65139=-5.15369

DrakeDrake University

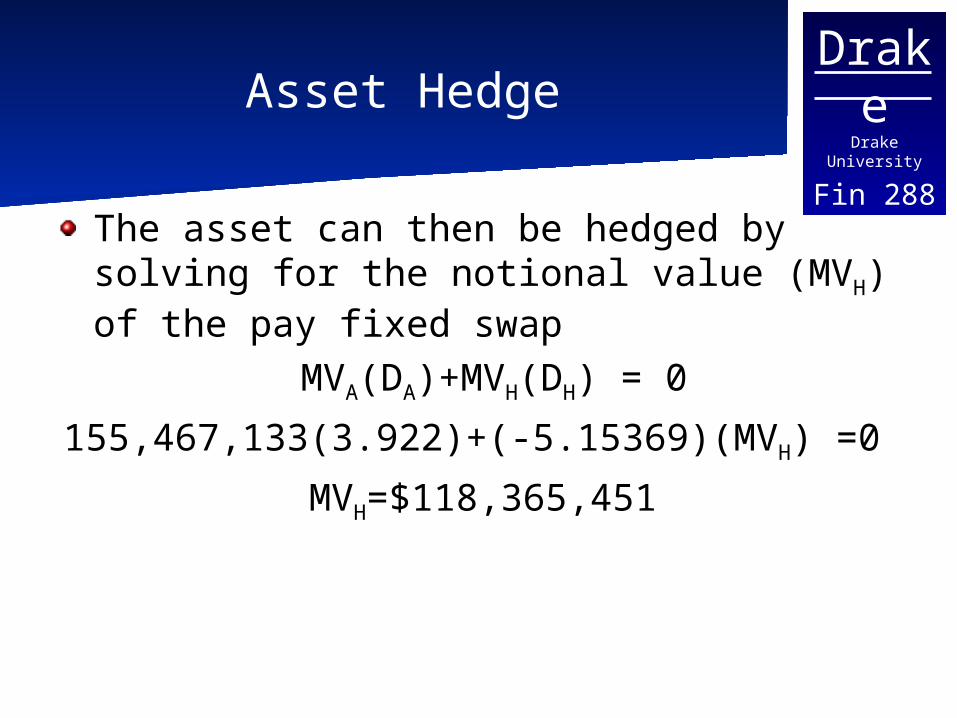

Fin 288Asset Hedge

The asset can then be hedged by solving for the notional value (MVH) of the pay fixed swap

MVA(DA)+MVH(DH) = 0

155,467,133(3.922)+(-5.15369)(MVH) =0

MVH=$118,365,451

DrakeDrake University

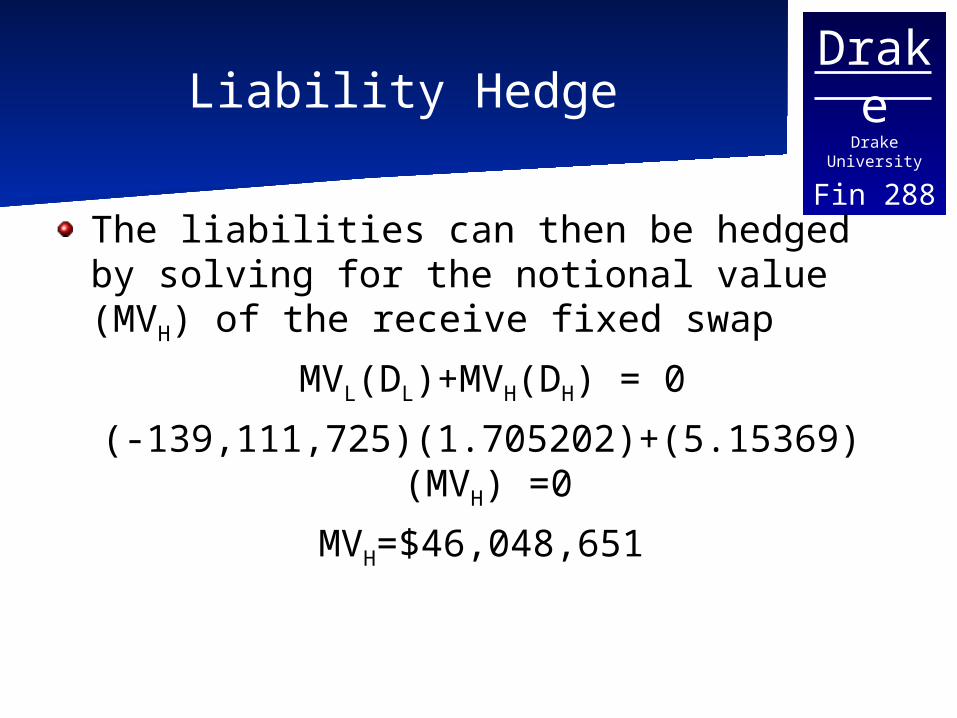

Fin 288Liability Hedge

The liabilities can then be hedged by solving for the notional value (MVH) of the receive fixed swap

MVL(DL)+MVH(DH) = 0

(-139,111,725)(1.705202)+(5.15369)(MVH) =0

MVH=$46,048,651

DrakeDrake University

Fin 288

Hedging Assets and Liabilities together

The entire balance sheet can be hedged with one interest rate swap by using GAP analysis.