Drake DRAKE UNIVERSITY Fin 288 Options Chapters 8, 9, and 10 Fin 288.

126

Drake DRAKE UNIVERSITY Fin 288 Options Chapters 8, 9, and 10 Fin 288

-

Upload

barrie-sims -

Category

Documents

-

view

222 -

download

3

Transcript of Drake DRAKE UNIVERSITY Fin 288 Options Chapters 8, 9, and 10 Fin 288.

DrakeDRAKE UNIVERSITY

Fin 288

Options Chapters 8, 9, and 10

Fin 288

DrakeDrake University

Fin 288Option Terminology

Call Option – the right to buy an asset at some point in the future for a designated price. Put Option – the right to sell an asset at some point in the future at a given price

DrakeDrake University

Fin 288

Review of Option Terminology

Expiration Date The last day the option can be exercised (American Option)

also called the strike date, maturity, and exercise date

Exercise Price The price specified in the contract

American Option Can be exercised at any time up to the expiration date

European Option Can be exercised only on the expiration date

DrakeDrake University

Fin 288

Review of Option Terminology

Long position: Buying an option Long Call: Bought the right to buy the asset Long Put: Bought the right to sell the asset

Short Position: Writing or Selling the optionShort Call Agreed to sell the other party the right to buy the underlying asset, if the other party exercises the option you deliver the asset. Short Put - Agreed to buy the underlying asset from the other party if they decide to exercise the option.

DrakeDrake University

Fin 288Review of Terminology

In - the - money optionswhen the spot price of the underlying asset for a call (put) is greater (less) than the exercise price

Out - of - the - money optionswhen the spot price of the underlying asset for a call (put) is less (greater) than the exercise price

At the money optionswhen the exercise price and spot price are equal.

DrakeDrake University

Fin 288Underlying Assets

Stock OptionsTraded on: CBOE, Philadelphia Stock Exchange, Pacific Exchange, American Stock Exchange, International Stock ExchangeTraded in 100 share blocks

Foreign Currency OptionsMainly over the counter and on Philadelphia Exchange

Index Options One contract is for 100 times the index (S&P for example)

DrakeDrake University

Fin 288Other underlying Assets

Interest Rate OptionsTraded on CBOE on treasury securities.Interest rate Options are traded on 13 Week, 5 year, 10 year and 30 year treasury securities

Futures OptionsTraded on the same exchange as the futures contract

DrakeDrake University

Fin 288Options on Futures

Options on futures are as popular or even more popular than on the actual asset.

Options on futures do not require payments for accrued interest.The likelihood of delivery squeezes is less.Current prices for futures are readily available, they are more difficult to find for bonds.

DrakeDrake University

Fin 288Futures Options

Call option holder will own a long futures position if the option is exercised.The writer of the call option accepts the corresponding short position at the exercise price.

DrakeDrake University

Fin 288

Mechanics of Options on Futures

Call Option Example Exercise price = $85 Current Futures price =

$95Upon exercise both the long position and the

short owned by the writer of the short option is set to $85.

When marked to market the holder of the long makes $10, the holder of the short looses $10.

The holders of the short and long position then face the same risks as any other holder of the futures contract.

DrakeDrake University

Fin 288

Buyer Margin Requirements on Futures Options

The buyer of the call option is not required to place any margin deposits. The most that could be lost is the cost of the option.

DrakeDrake University

Fin 288Margins on Stock Options

Stock purchases are allowed to be purchased on margin. An option on must be purchased with cash since they already leverage the underlying asset.When an option is written the writer must maintain a margin account to help prevent default.

DrakeDrake University

Fin 288Writing Naked Options

Naked Option- No offsetting position in the underlying stockWritten Naked Call Options – Margin is the greater of:

100% of the proceeds of the sale plus 20% of the underlying share price minus any amount by which it is out of the money100% of the option proceeds plus 10% of the underlying share price

DrakeDrake University

Fin 288Margin on Put Options

Written Naked Put Options100% of the proceeds of the sale plus 20% of the underlying share price minus any amount by which it is out of the money100% of the option proceeds plus 10% of the underlying exercise price

DrakeDrake University

Fin 288Covered Calls

Covered Calls – writing an option when you also own the underlying stock.No margin is required if the options is out of the money or in the moneyIf it is in the money the share price is reduced by the amount it is in the money for the purpose of calculating the equity position.

DrakeDrake University

Fin 288

Call Option on Futures Writer Margin Requirements

The writer of the call option accepts all of the risk since the buyer will not exercise if there would be a loss. The writer is required to deposit the original margin that would be required on the futures contract and the option price that is received for writing the option. The writer is also required to deposit variation margin as the contract is marked to market.

DrakeDrake University

Fin 288

Position Limits and Exercise Limits

CBOE and most other exchanges have a limit on the number of positions on the same side of the market. Long Calls and Short Puts would be considered to be on the same side of the market.Large cap stocks 75,000 contracts, small cap stocks 60,000, 31,500, 22,500 or 13,500 contracts Exercise limit is often equal to the position limit

DrakeDrake University

Fin 288Basic Call Option Profit

Call option – as the price of the asset increases the option is more profitable. Once the price is above the exercise price (strike price) the option will be exercisedIf the price of the underlying asset is below the exercise price it won’t be exercised – you only loose the cost of the option.The Profit earned is equal to the gain or loss on the option minus the initial cost.

DrakeDrake University

Fin 288

Profit Diagram Call Option(Long Call Position)

Profit

Spot Price Cost

S

S-X-C

X

DrakeDrake University

Fin 288 Call Option Intrinsic Value

The intrinsic value of a call option is equal to the current value of the underlying asset minus the exercise price if exercised or 0 if not exercised. In other words, it is the payoff to the investor at that point in time (ignoring the initial cost)

the intrinsic value is equal tomax(0, S-X)

DrakeDrake University

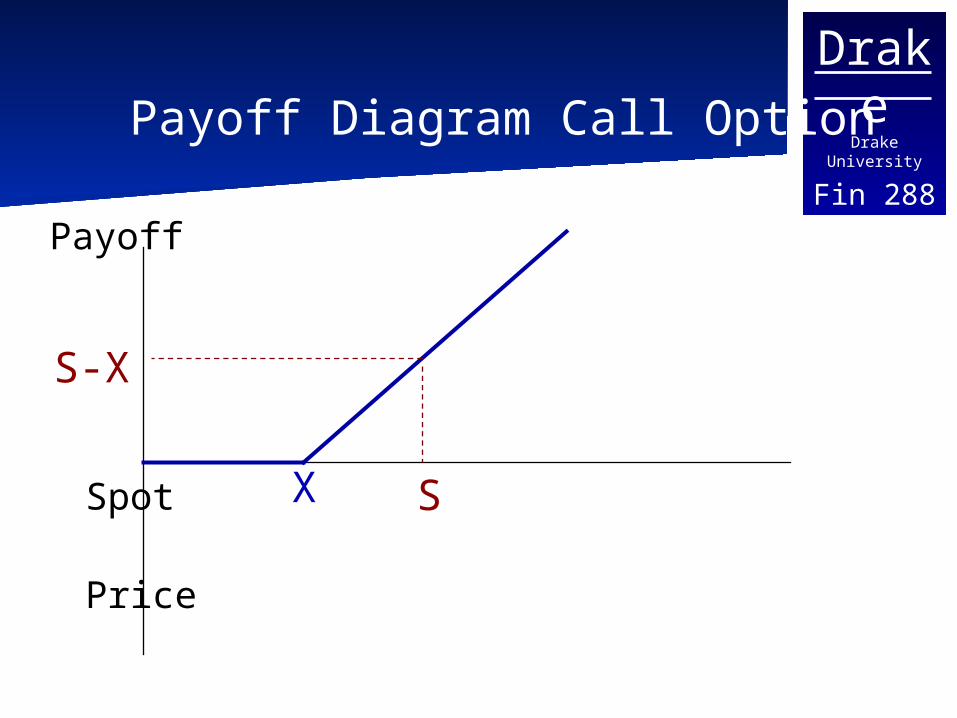

Fin 288Payoff Diagram Call Option

Payoff

Spot

PriceS

S-X

X

DrakeDrake University

Fin 288Example: Naked Call Option

Assume that you can purchase a call option on an 8% coupon bond with a par value of $100 and 20 years to maturity. The option expires in one month and has an exercise price of $100.Assume that the option is currently at the money (the bond is selling at par) and selling for $3.What are the possible payoffs if you bought the bond and held it until maturity of the option?

DrakeDrake University

Fin 288Five possible results

The price of the bond at maturity of the option is $100. The buyer looses the entire purchase price, no reason to exercise.The price of the bond at maturity is less than $100 (the YTM is > 8%). The buyer looses the $3 option price and does not exercise the option.

DrakeDrake University

Fin 288

Five Possible Results continued

The price of the bond at maturity is greater than $100, but less than $103. The buyer will exercise the option and recover a portion of the option cost.The price of the bond is equal to $103. The buyer will exercise the option and recover the cost of the option.The price of the bond is greater than $103. The buyer will make a profit of S-$100-$3.

DrakeDrake University

Fin 288

Profit Diagram Call Option(Long Call Position)

Profit

Spot Price -3

S

S-100-3

100

103

DrakeDrake University

Fin 288Price vs. Rate

Note buying a call on the price of the bond is equivalent to buying a put on the interest rate paid by the bond.As the rate decreases, the price increases because of the time value of money.

DrakeDrake University

Fin 288

Profit Diagram Call Option(Short Call Position)

Profit

Spot Price S

C+X-S

X

DrakeDrake University

Fin 288Put option payoffs

The writer of the put option will profit if the option is not exercised or if it is exercised and the spot price is less than the exercise price plus cost of the option.In the previous example the writer will profit as long as the spot price is less than $103.What if the spot price is equal to $103?

DrakeDrake University

Fin 288Put Option Profits

Put option – as the price of the asset decreases the option is more profitable. Once the price is below the exercise price (strike price) the option will be exercisedIf the price of the underlying asset is above the exercise price it won’t be exercised – you only loose the cost of the option.

DrakeDrake University

Fin 288Profit Diagram Put Option

Profit

Spot Price

Cost X

S

X-S-C

DrakeDrake University

Fin 288 Put Option Intrinsic Value

The intrinsic value of a put option is equal to exercise price minus the current value of the underlying asset if exercised or 0 if not exercised. In other words, it is the payoff to the investor at that point in time (ignoring the initial cost)

the intrinsic value is equal tomax(X-S, 0)

DrakeDrake University

Fin 288Payoff Diagram Put Option

Profit

Spot Price

Cost

XS

X-S

DrakeDrake University

Fin 288

Profit Diagram Put OptionShort Put

Profit

Spot PriceX

S

S-X+C

DrakeDrake University

Fin 288Pricing an Option

Arbitrage argumentsBlack Scholes Binomial Tree Models

DrakeDrake University

Fin 288

PV and FV in continuous time

e = 2.71828 y = lnx x = ey

FV = PV (1+k)n for yearly compoundingFV = PV(1+k/m)nm for m compounding

periods per yearAs m increases this becomesFV = PVern =PVert let t =n rearranging for PV PV = FVe-rt

DrakeDrake University

Fin 288

Lower Bound of Call Option Price

Assume that you have an asset that does not pay a cash income (A non dividend paying stock for example)Consider the case of an option as it expires. In this case, regardless of whether it is an American or European option it will be worth its intrinsic value (max(S-X,0)). Assuming a positive value the lower bound is given by:

S - X

DrakeDrake University

Fin 288Formal Argument

Consider two portfolios A: One European call option on the stock of Widget Inc. plus cash equal to Xe-rT

B: One share of stock in Widget Inc.

Note: If the cash in portfolio A is invested at r, it will grow to be worth X at time T.

DrakeDrake University

Fin 288Portfolio A

There are two possible outcomes at time T depending upon the value of S at time T

ST > X Exercise the option and purchase the asset with a current value of ST (The value of portfolio A at time T is ST ).

ST < X Do not exercise the option, The portfolio is then worth the value of the cash, X.

Therefore the portfolio is worth: max(ST,X)

DrakeDrake University

Fin 288Portfolio B

The value of portfolio B is simply the value of the stock at time T, ST.

DrakeDrake University

Fin 288Comparing A to B

Combining the two results it is easy to see that portfolio A (the option and the cash) is always worth at least as much as portfolio B (owning the stock), and sometimes it is worth more than B.

Without arbitrage, the same relationship should be true today as well as at time T in the future.

DrakeDrake University

Fin 288

Equal value of the portfolios today

Let c be the call price (value of option) today.Then the value of portfolio A is: c + Xe-rT

The value of portfolio B is: S

Since the value of A is always worth as much as B and sometimes it is worth more:

c + Xe-rT >S or rearranging

c > S - Xe-rT

DrakeDrake University

Fin 288Final result

The worst outcome to buying a call option is that it expires worthless, so the option is worth either nothing or S-Xe-rT

Therefore:

c > max(S - Xe-rT,0)

DrakeDrake University

Fin 288Put Option

Similar to a call option the put option should always have a positive value. Considering the case of an option as it expires (either an American or European Option), the value of the option should be equal to its intrinsic value. The lower bound is therefore:

X - S

DrakeDrake University

Fin 288European Put Option

Again, in the case of a European option prior to maturity this equation will not hold and it is necessary to account for the time value of money. In this case the lower bound for the option is given by:

Xe-rT - S

DrakeDrake University

Fin 288Formal Argument:

Consider two Portfolios C: One European put option plus one

shareand

D: An amount of cash equal to Xe-rT

DrakeDrake University

Fin 288Portfolio C:

There are two possibilities:ST < X Exercise the option at time T and the portfolio is worth X. ST > X The option expires and the portfolio is worth ST

Portfolio C is therefore worth max(ST,X)

DrakeDrake University

Fin 288Portfolio D

Investing the amount at a rate equal to r, the portfolio will be worth X at Time T.

Combining the two arguments it is easy to see that portfolio C is always worth at least the same amount as portfolio D and sometimes it is worth more.

DrakeDrake University

Fin 288Comparing the two

Let p = the value (price) of the put optionWithout arbitrage opportunities:

p + S > Xe-rT or rearranging

p > Xe-rT - S

the value of the put option is then given as

p > max(Xe-rT-S,0)

DrakeDrake University

Fin 288Put Call Parity

Consider portfolio A and C above A: One European call option plus an amount of cash equal to Xe-rT

C: One European put option plus one share

Both portfolios are have a value of max(X,ST) at the expiration of the options. If no arbitrage opportunities exist, they should also have the same value today which implies:

c + Xe-rT = p + S

DrakeDrake University

Fin 288Put Call Parity

In other words, the value of a European call with a given exercise date can be deduced from the value of a European put with the same exercise date and exercise price.

DrakeDrake University

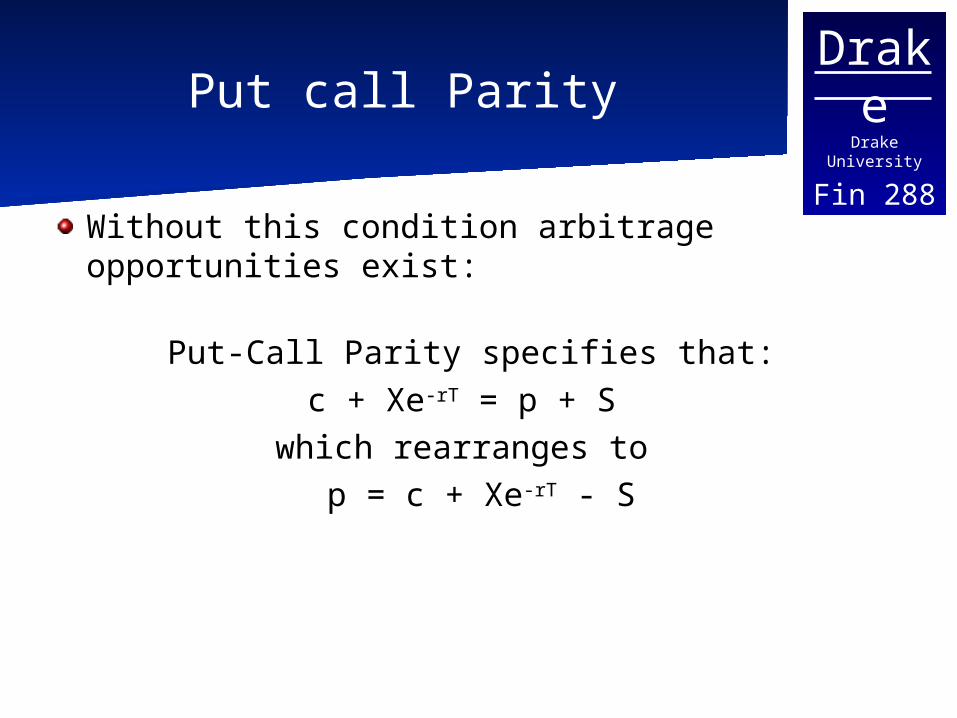

Fin 288Put call Parity

Without this condition arbitrage opportunities exist:

Put-Call Parity specifies that: c + Xe-rT = p + S

which rearranges to p = c + Xe-rT - S

DrakeDrake University

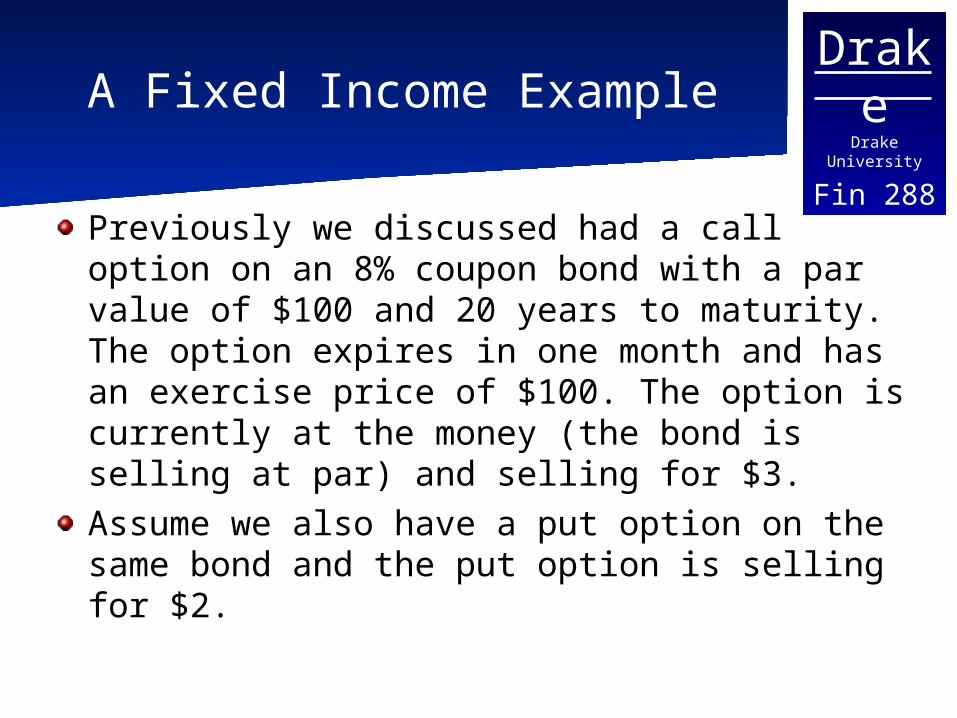

Fin 288A Fixed Income Example

Previously we discussed had a call option on an 8% coupon bond with a par value of $100 and 20 years to maturity. The option expires in one month and has an exercise price of $100. The option is currently at the money (the bond is selling at par) and selling for $3.Assume we also have a put option on the same bond and the put option is selling for $2.

DrakeDrake University

Fin 288A Fixed Income Example

For now, ignore the coupon payments on the bond. Consider three possible strategies simultaneously

Buy the bond in the spot market for $100Enter into a short call position (sell the call) for $3Buy a put at a price of $2

DrakeDrake University

Fin 288

Possible Outcomes at expiration

Bond Price > $100The call option is exercised so you are forced to sell the bond at a price equal to $100. The put option expires. You make $1 profit from the difference in the call and put prices

Bond Price <$100You exercise the Put option and sell the Bond for $100, which is the same price you paid. The Call expires worthless . You make a $1 from the difference in the price.

DrakeDrake University

Fin 288Arbitrage

Regardless of the price of the bond at expiration, there was a $1 profit. Three possible things would eliminate arbitrage.

An increase in the price of the bond today.A decrease in the call option price.An increase in the put option price.

DrakeDrake University

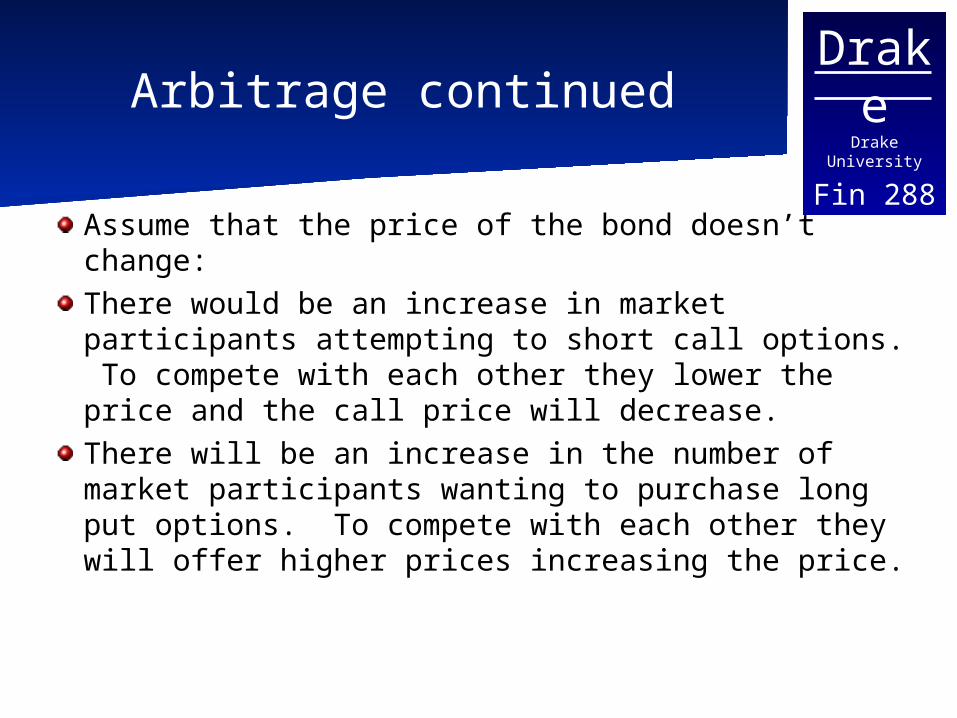

Fin 288Arbitrage continued

Assume that the price of the bond doesn’t change:There would be an increase in market participants attempting to short call options. To compete with each other they lower the price and the call price will decrease.There will be an increase in the number of market participants wanting to purchase long put options. To compete with each other they will offer higher prices increasing the price.

DrakeDrake University

Fin 288

Put Call Parity Revisited p = c + Xe-rT - S

We have ignored the Time value of money so the relationship becomes:

p=c+X-SIn our example X=S which implies that p should equal c.If both the put and call price equaled each other there would be no arbitrage profits regardless of what happened to the bond price at maturity.

DrakeDrake University

Fin 288Put Call Extensions

We ignored the time value of money and the coupon payments paid by the bond.The coupon payment can be treated similar to the price. If you own the bond you will receive the cash payment in the future.The put call parity relationship for a coupon bond is simply:

p=c+Xe-rT+CPe-rT-Swhere CP is the coupon payment received at

time T

DrakeDrake University

Fin 288

Put Call Parity and American Options

Put-Call Parity holds only for European Options but it is possible to use the relationship to specify some generalizations concerning the relationship between American Puts and Calls.

DrakeDrake University

Fin 288

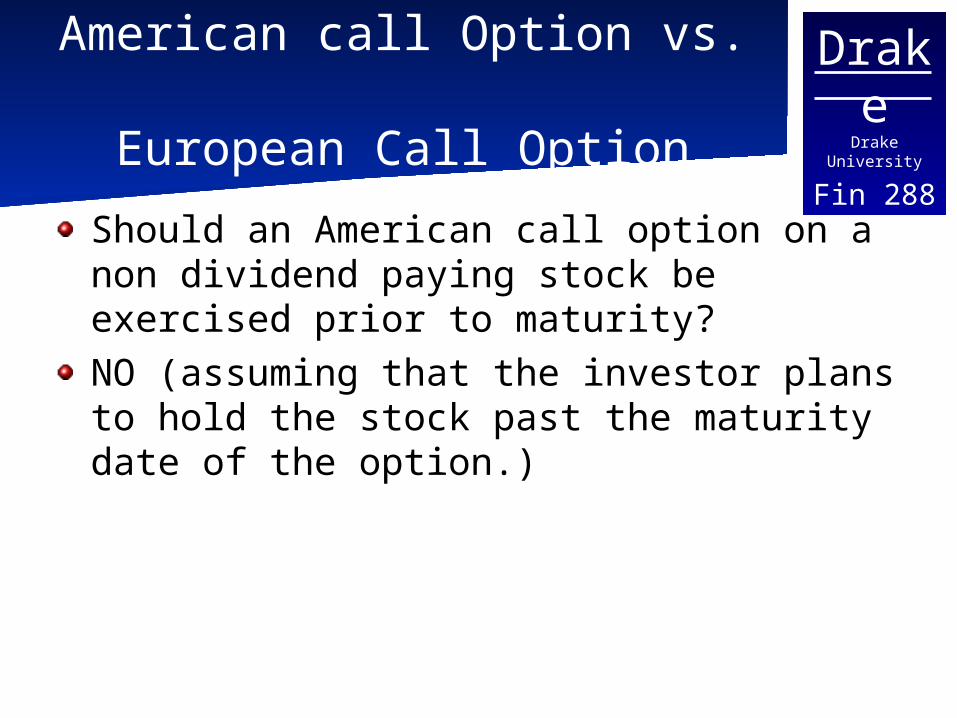

American call Option vs. European Call Option

Should an American call option on a non dividend paying stock be exercised prior to maturity? NO (assuming that the investor plans to hold the stock past the maturity date of the option.)

DrakeDrake University

Fin 288

Should an American call Option

be Exercised Early?

Assume that the option currently is deep in the money, The following possibilities exist1) S > X The investor can earn interest amount of cash equal to X and then still pay X for the stock upon expiration of the option.2) S < X The investor can then purchase the stock at the spot price and let the option expire.3) S=X Again there is no reason to exercise the option, and the investor will let the option expire.

DrakeDrake University

Fin 288Exercising Call Options

Since it is never optimal to exercise the call early, the value of the American Call (C) should be equal to the value of the European Call (c).

DrakeDrake University

Fin 288Exercising Put Options

Should an American put option on a non dividend paying stock be exercised prior to maturity?Yes (if it is sufficiently in the money)The general argument is that the Put option serves as insurance and that early exercise is a good idea if the investor realizes a significant gain from the exercise of the option

DrakeDrake University

Fin 288Exercising Put Options

The price of an American put option should be above that of an Equivalent European option (P>p)The value of an American Call should equal the value of an European Call. Using the put call parity relationship and substituting generalizations can be made about American Options:

DrakeDrake University

Fin 288

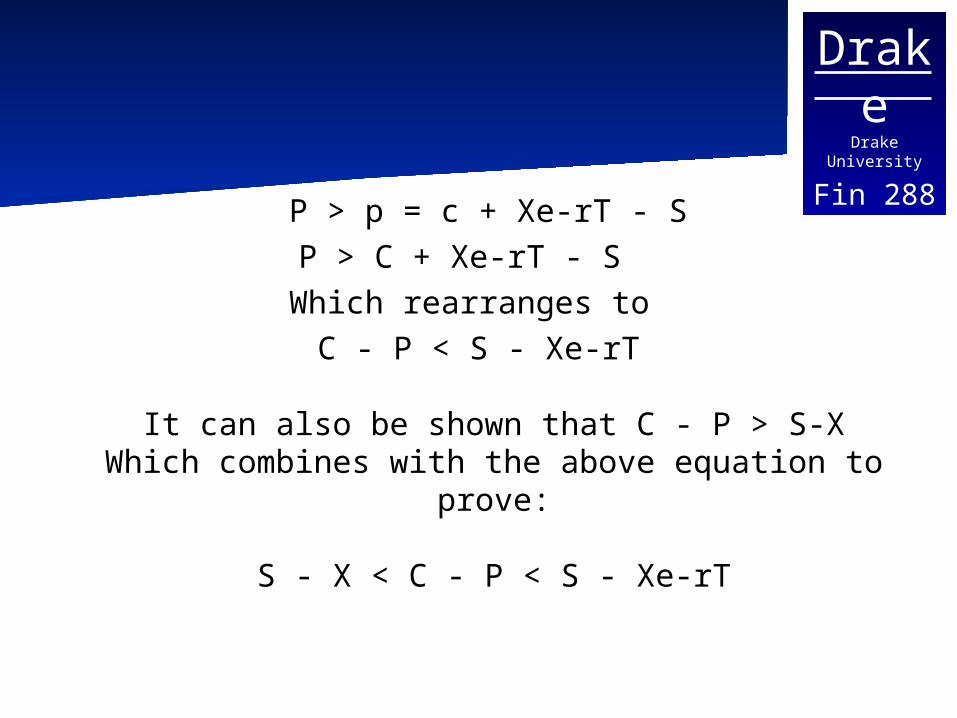

P > p = c + Xe-rT - SP > C + Xe-rT - S

Which rearranges to C - P < S - Xe-rT

It can also be shown that C - P > S-XWhich combines with the above equation to

prove:

S - X < C - P < S - Xe-rT

DrakeDrake University

Fin 288Black Scholes

The basic starting point for the actual pricing of an European option is the model developed by Fisher Black, Myron Scholes, and Robert Merton.

DrakeDrake University

Fin 288Black Scholes Assumptions

1) Stock prices follow a lognormal distribution with and constant.

2) There are no transaction costs or taxes and all securities are perfectly divisible

3) There are no dividend on the asset during the life of the option

4) There are no riskless arbitrage opportunities5) Security trading is continuous6) Investors can borrow and lend at the same

risk free rate7) The short term risk free rate is constant

DrakeDrake University

Fin 288Inputs you will need

S = Current value of underlying assetX = Exercise pricet = life until expiration of optionr = riskless rate2 = variance

DrakeDrake University

Fin 288Black Scholes

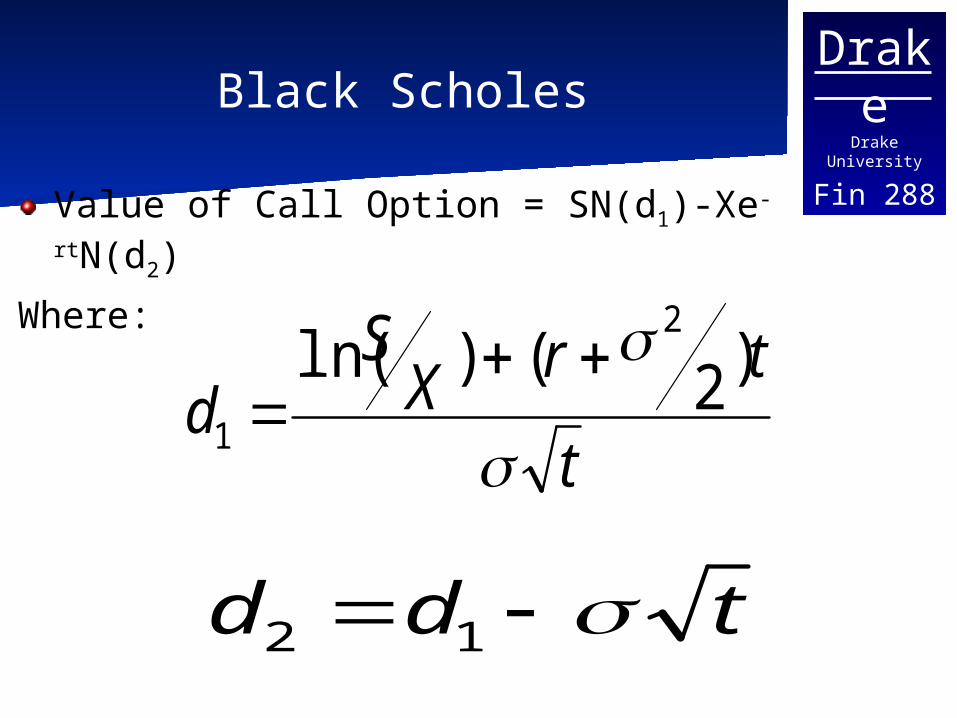

Value of Call Option = SN(d1)-Xe-

rtN(d2) S = Current value of underlying asset

X = Exercise pricet = life until expiration of optionr = riskless rate2 = varianceN(d ) = the cumulative normal

distribution (the probability that a variable with a standard normal distribution will be less than d)

DrakeDrake University

Fin 288Black Scholes (Intuition)

Value of Call Option

SN(d1) - Xe-rt N(d2)The expected PV of cost Risk NeutralValue of S of investment Probability

ofif S > X S > X

DrakeDrake University

Fin 288Black Scholes

Value of Call Option = SN(d1)-Xe-rtN(d2)

Where:

t

trXS

d

)2()ln(2

1

tdd 12

DrakeDrake University

Fin 288

Extending Black Scholes to Futures Options

Black extended the original model to price options on futures.

TddT

TXF

d

dNFdXNe

dXNdNFecrt

rt

12

20

1

102

210

2/ln

))()((p

))()((

DrakeDrake University

Fin 288Time Value of an Option

The time value of an option is the difference in the theoretical price of the option and the intrinsic value.It represents the the possibility that the value of the option will increase over the time it is owned.

DrakeDrake University

Fin 288Time Value of Call Option

S

S-X

X

Time value ofCall option

DrakeDrake University

Fin 288

Changes in the Value of the Option

The value of the option is dependent upon changes in any of the inputs in the Black Scholes model.The impact of a change in one of the inputs on into the Black Scholes Equations to the value of the option is measured by a group of variables known as “the Greeks” We will introduce them now and explore the relationship between changes in each input and the option value in depth later.

DrakeDrake University

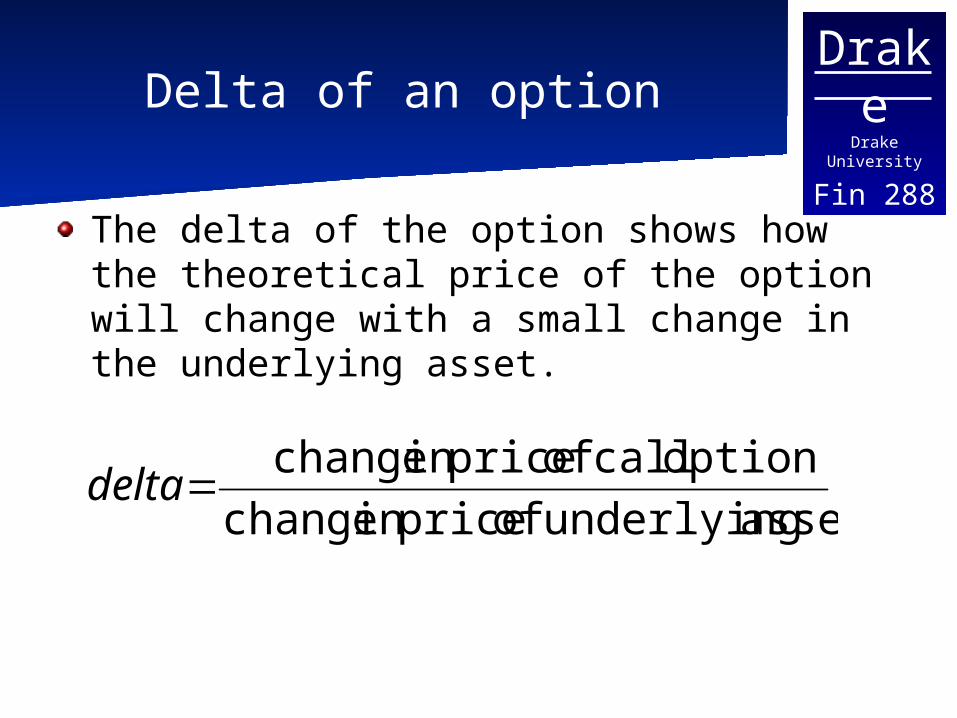

Fin 288Delta of an option

The delta of the option shows how the theoretical price of the option will change with a small change in the underlying asset.

asset underlying of pricein change

option call of pricein changedelta

DrakeDrake University

Fin 288

Delta and the Time Value of Call Option

S

S-X

X

Time value ofCall option

Delta is the slope of the tangent line at the given stock price

DrakeDrake University

Fin 288Delta of an option

Intuitively a higher stock price should lead to a higher call price. The relationship between the call price and the stock price is expressed by a single variable, delta. The delta is the change in the call price for a very small change it the price of the underlying asset.

DrakeDrake University

Fin 288Delta

Delta can be found from the call price equation as:

Using delta hedging for a short position in a European call option would require keeping a long position of N(d1) shares at any given time. (and vice versa).

)( 1dNS

c

DrakeDrake University

Fin 288Delta explanation

Delta will be between 0 and 1.

A 1 cent change in the price of the underlying asset leads to a change of delta cents in the price of the option.

DrakeDrake University

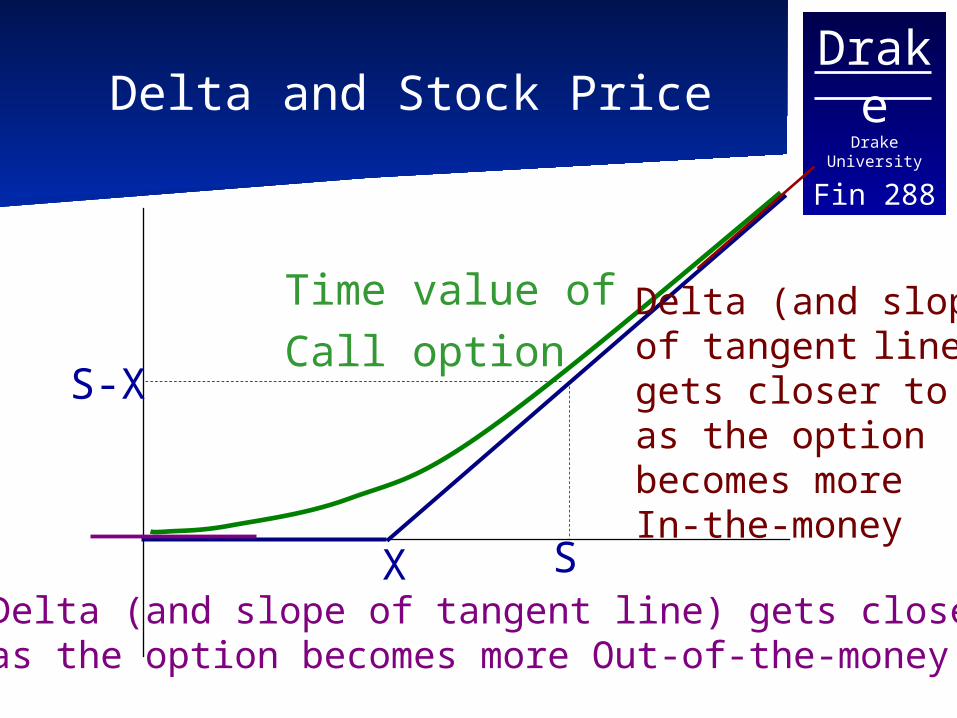

Fin 288Delta and Stock Price

S

S-X

X

Time value ofCall option

Delta (and slope of tangent line) gets closer to 1as the option becomes more In-the-money

Delta (and slope of tangent line) gets closer to 0 as the option becomes more Out-of-the-money

DrakeDrake University

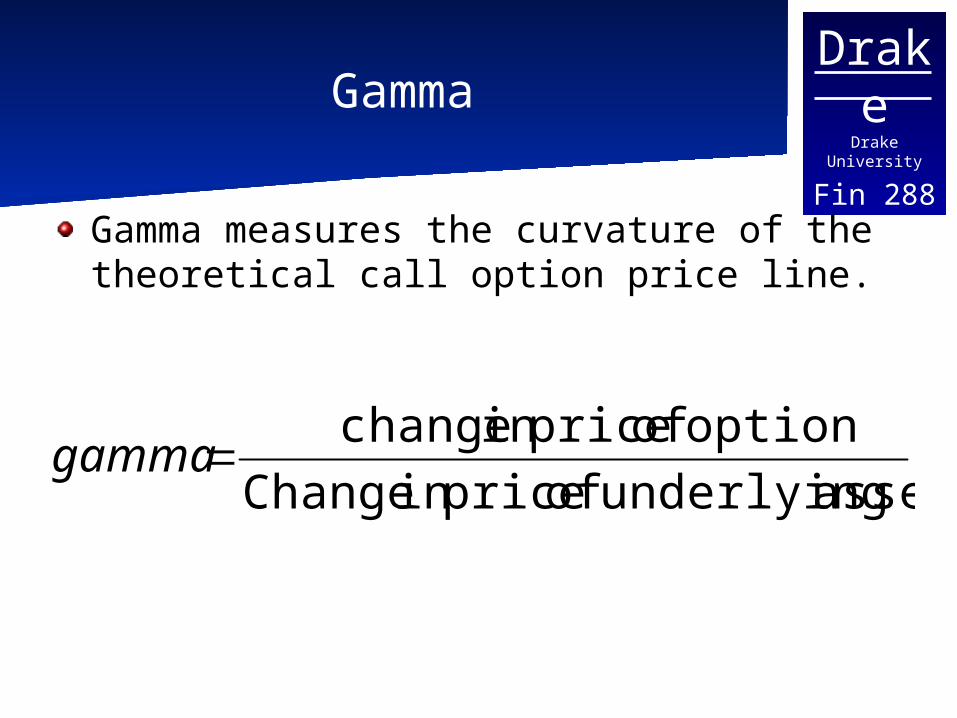

Fin 288Gamma

Gamma measures the curvature of the theoretical call option price line.

asset underlying of pricein Change

option of pricein changegamma

DrakeDrake University

Fin 288Gamma of an Option

The change in delta for a small change in the stock price is called the options gamma:

Call gamma = TS

e d

2

2/21

DrakeDrake University

Fin 288Other Measures

expiration toin time decrease

option of price ein th changetheta

expectedin Change

Priceoption in Changekappa

DrakeDrake University

Fin 288Hedging

If a firm is worried about an increase in borrowing costs it could buy a call option on the relevant interest rate. Any gains on the call options will offset the increased borrowing.Similarly if the firm is worried about a decline in rates decreasing income it could buy a put option on the interest rate. Any decline in income would be offset by the change in rates.

DrakeDrake University

Fin 288Hedging with options

Assume that you can purchase a put option on the futures contract with a strike price of $93 (7%) and a cost of .40If interest rates rates increase to 8% the put guarantees that the worst case would be a rte of 7% +1% +.4% = 8.4% which implies a total interest cost of $210,000If rates decrease to 7% you only have the added cost of the option resulting in a total interest expense of 7.4% or $185,000

DrakeDrake University

Fin 288Hedging Interest Rate Risk

Previously we purchased a put option on a eurodollars futures contract to hedge against a change in interest rates.The result was that it limited the upper rate that might be paid and allowed a decrease in rates to decease the actual rate paid (the option wasn’t exercised).There is a (sometimes substantial) cost to entering into the option contracts to accomplish this.

DrakeDrake University

Fin 288Option position

In the example the option profited as the level of interest rates increased (the price of bonds decreased)

DrakeDrake University

Fin 288Profit Diagram Put Option

Profit

Spot Price

Cost X

S

X-S-C

DrakeDrake University

Fin 288Spot Position

The investor was attempting to hedge against an increase in the level of interest rates, in other words, they paid a higher borrowing cost as rates increased. This is the same idea as saying the they lost money as the price of the bonds declined.This was offset by the profit from the option, but you incur the cost of the option.

DrakeDrake University

Fin 288Diagramming the spot

The spot position could be represented by a straight line that represents the corresponding savings in interest rates. The line will also slope up to the right. As the price increases (rate decreases) there is a relative improvement since the rate decrease saves the investor money.

DrakeDrake University

Fin 288Profit Diagram Spot

Profit

Spot Price

Cost

DrakeDrake University

Fin 288

Assume that the current interest rate is just below the rate implied by the strike price.The two positions could be represented on a single graph which explains the results of the hedge. At rates above the strike price the profit on the option cancels out the loss from the increased rates. At rates below the strike price you gain, but the gain is reduced by the cost of the option.

DrakeDrake University

Fin 288Profit Diagram Put Option

XCombinedPosition

DrakeDrake University

Fin 288“Selling off” benefits

It is possible to decrease the impact of the option’s costOne approach would be buying a cap as before, but also selling at cap at a higher rate (lower price). The money received from selling the option offsets the initial cost of the other option position.

The downside is that if rates increased above the second level, you are exposed to the interest rate change.

DrakeDrake University

Fin 288

Selling off benefits – options position

However if the level of interest rates increased too high the option that was sold would experience a loss offsetting the gains from the original position.Therefore the original position is no longer hedged.Assume that the two options are for the same expiration date and are both European

DrakeDrake University

Fin 288

Profit Diagram Put Options

Long Put

Short Put

Spot Price

DrakeDrake University

Fin 288

Profit Diagram Bear Spread

Bear Spread

Spot price

DrakeDrake University

Fin 288Bear Spread

The previous example was essentially buying an interest rate cap (buying put on price of bonds) and selling an interest rate cap (selling a put on the price of bonds). The position could also be thought of as buying and selling call options on the level of interest rates.Below the lower price (above the higher yield) the two options cancel each other out so the increased cost associated with the spot position is unhedged.

DrakeDrake University

Fin 288Adding the spot position

Again assume that the current level of interest rates is slightly below the lower of the two strike prices.

DrakeDrake University

Fin 288

Profit Diagram Bear Spread

Bear Spread

Spot priceHedgedPosition

DrakeDrake University

Fin 288Another Strategy

To avoid the downside of the previous example you could buy the same interest rate cap, but sell an interest rate floor at a higher price (lower yield).

DrakeDrake University

Fin 288Interest Rate Floor

A call option on the price of the bond can be represented as a floor on the level of interest rates. The option will be profitable if the price of the bond increases above the strike price (the interest rate decreases below the strike).This would offset a loss on an asset that is rate sensitive and effectively limit the loss.

DrakeDrake University

Fin 288

Profit Diagram Call Option(Long Call Position)

Profit

Spot Price Cost

S

S-X-C

X

DrakeDrake University

Fin 288Spot position

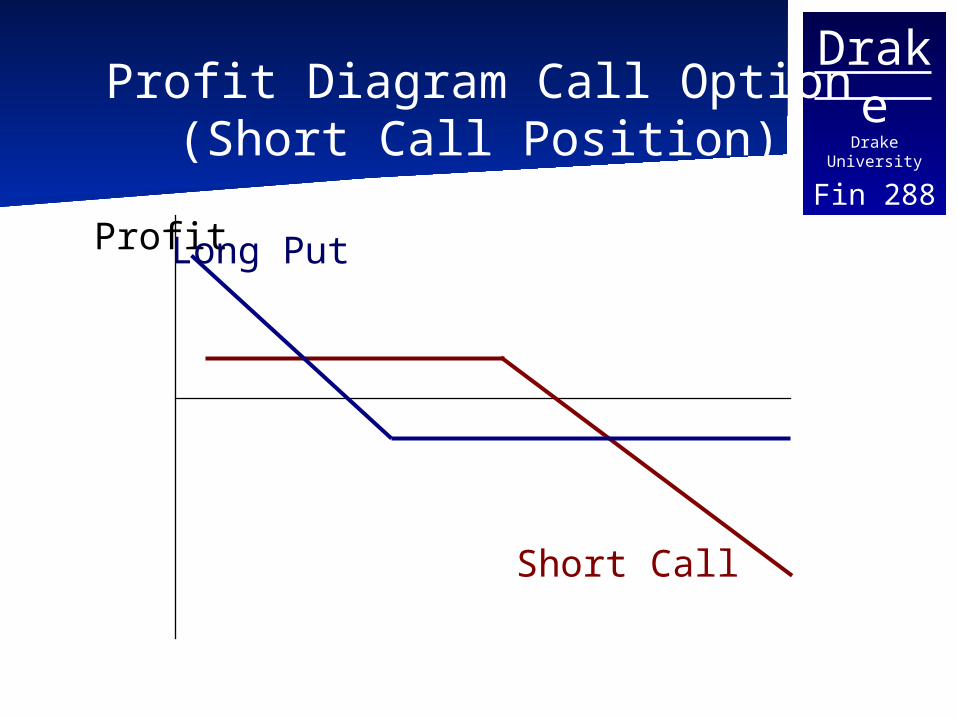

Since the option profits as the rates decrease (the price of a bond increases) this would offset lost income on an asset that is rate sensitive.In our new position we want to sell the option.

DrakeDrake University

Fin 288

Profit Diagram Call Option(Short Call Position)

Profit

Spot Price S

C+X-S

X

DrakeDrake University

Fin 288Another Strategy

The new strategy is to avoid the downside of the previous example you could buy the same interest rate cap, while selling an interest rate floor at a higher price (lower yield).

DrakeDrake University

Fin 288Profit Diagram Call Option

(Short Call Position)

Profit

Short Call

Long Put

DrakeDrake University

Fin 288Profit DiagramCostless Collar

Profit

Short Call

Long Put

Combined Profit

DrakeDrake University

Fin 288Combined with Spot

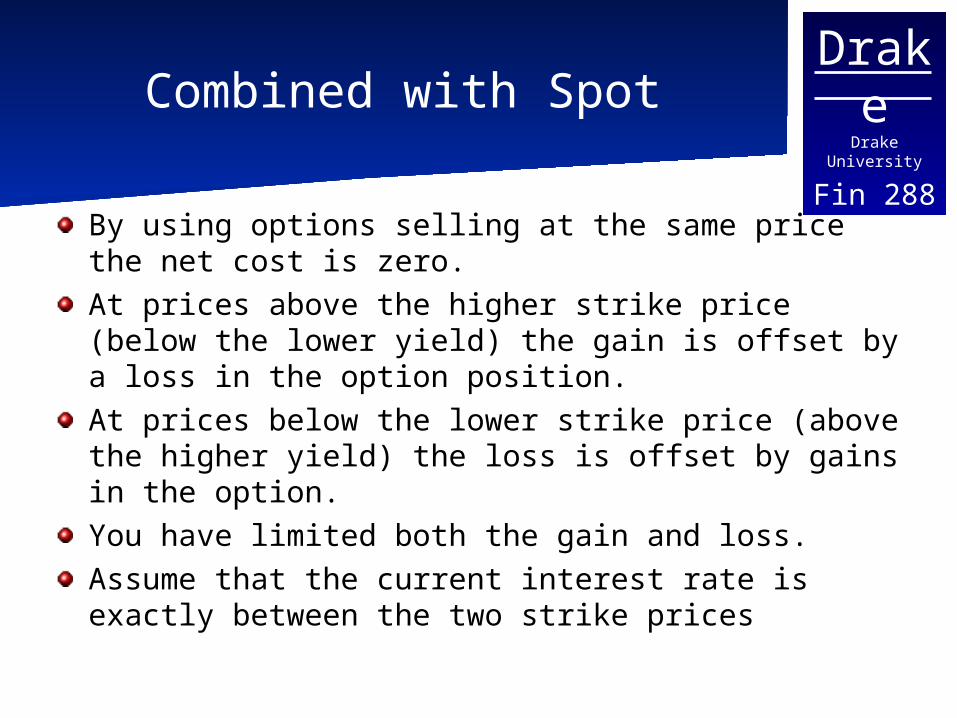

By using options selling at the same price the net cost is zero.At prices above the higher strike price (below the lower yield) the gain is offset by a loss in the option position.At prices below the lower strike price (above the higher yield) the loss is offset by gains in the option. You have limited both the gain and loss.Assume that the current interest rate is exactly between the two strike prices

DrakeDrake University

Fin 288Profit Diagram

Costless Collar (Fence)

Profit

Costless Collar

DrakeDrake University

Fin 288Complications

In the previous examples we ignored many real world complications.This is especially true if you are buying options on futures (treasury bond futures for example).Many of these complications arise from the ideas of basis risk presented earlier.

DrakeDrake University

Fin 288

New Example: Protective Put(From Fabozzi)

Assume that you own a corporate bond and you are afraid that an increase in interest rates will decrease the value of the bond.It would be possible to use futures or futures options to lock in a future sale price for the bonds.Assume that the coupon on the bond is 11.75% and they mature on April 19, 2023. Today is April 19, 1985 and you plan to sell the bond in June 1985.

DrakeDrake University

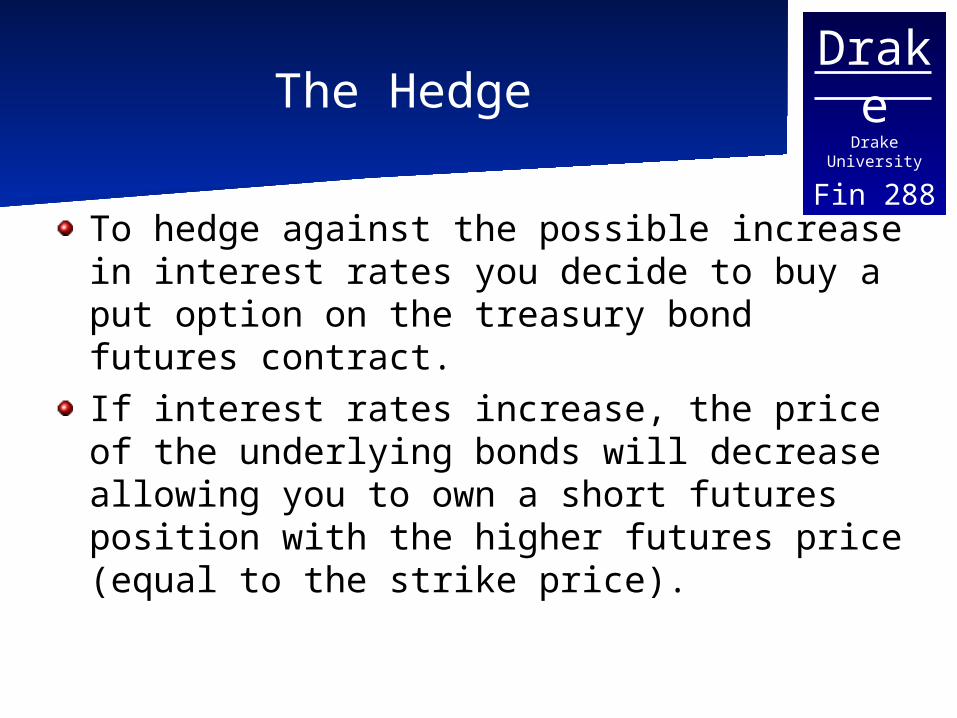

Fin 288The Hedge

To hedge against the possible increase in interest rates you decide to buy a put option on the treasury bond futures contract.If interest rates increase, the price of the underlying bonds will decrease allowing you to own a short futures position with the higher futures price (equal to the strike price).

DrakeDrake University

Fin 288Determining the Strike Price

The strike price will effectively set a cap on the level of interest rates since it rates increase above the rate corresponding to the strike price you profit from the option offsetting the loss in bond value. Assume that you do not want the price of the bond to drop below $87.668.

DrakeDrake University

Fin 288Target Strike Price = 87.668

The problem is that the futures option is not for the bond which you own, it is for a treasury bond. You need to set a strike price for the Treasury bond that corresponds with a price of 87.688 for the corporate bond.

DrakeDrake University

Fin 288Price Vs. Yield

Choosing the minimum price is equivalent to selecting the maximum yield on the corporate bond.A price of 87.668 implies that the corporate bond will be paying a yield of 13.41% (since it is selling at a large discount the yield will be above the coupon rate)

DrakeDrake University

Fin 288Yield on CTD treasury

The futures contract underlying the option has a large set of acceptable treasuries that can be delivered. You can find the cheapest to deliver at the current date.Assume that after finding the cheapest to deliver bond, you find that is has a current yield 90 basis points less than current yield on the corporate. Assume that the yield spread stays fixed.

DrakeDrake University

Fin 288Price of CTD Treasury

Given that the yield spread stays fixed at 90 basis points and that the maximum acceptable yield on the corporate bond is 13.41% it implies a yield of 12.51% on the treasury.This implies a price of $63.756 for the treasury that is currently CTD.The price used in the futures option will not be this price, it must be found using the conversion factor

DrakeDrake University

Fin 288Finding the Strike Price

Given the treasuries price of $63.756 and the conversion factor for the treasury of .9660, a futures price is then found to be:

63.756/.9660 = 66

Therefore a strike price of 66 on the treasury futures option contract would be used.

DrakeDrake University

Fin 288Hedge ratio

Hedging the position with just futures contract would have required finding the hedge ratio, this still applies.Assuming that you found the hedge ratio to be 1.24, you will need 1.24 put futures options for each spot position.

DrakeDrake University

Fin 288

Another approach:A Covered Call

The assumption is that the change in interest rates will be small. To hedge against a possible decline in rates, the holder of a bond (or portfolio) sells out of the money calls. The income from the sale of the option provides income to offset a possible increase in rates that lowers the bond value.

DrakeDrake University

Fin 288

The Maximum Effective Call Price

Assume that the maximum effective call price you set is 102.66 plus the premium from the call option. The price of 102.66 corresponds to a yield of 11.436% on the corporate bonds.Keeping the 90 basis point spread the yield on the CTD treasury should be 10.536% which implies a 75.348 price for the treasury

DrakeDrake University

Fin 288The strike price

Using the conversion factor, this implies a futures price of 75.348/.9960 = 78 which is also the strike price on the call option you sell.

DrakeDrake University

Fin 288Comparing Strategies

Comparing a basic futures position to the covered call and protective put in the previous examples shows that each has its own advantages and disadvantages.The basic futures position sets the price (and yield) regardless of what happens to the level of interest rates in the economy. However the other two provide scenarios where you are better off than this ( and scenarios where you would have been worse off)

DrakeDrake University

Fin 288Comparing Strategies

The protective put does better if rates decrease and the call option in the covered call option is exercised. The protective put also outperforms the basic futures option if as rates decline, but it is outperformed by the covered call.For extreme rate increases, the option strategies are both outperformed by the basic futures position.