Draft decisions 2011-16 Access Arrangements for APT Allgas and Envestra (Qld) Warwick Anderson...

43

Draft decisions 2011-16 Access Arrangements for APT Allgas and Envestra (Qld) Warwick Anderson General Manager, Network Regulation 1 March 2011 Public forum

-

Upload

wilfred-mckenzie -

Category

Documents

-

view

214 -

download

1

Transcript of Draft decisions 2011-16 Access Arrangements for APT Allgas and Envestra (Qld) Warwick Anderson...

Draft decisions2011-16 Access Arrangements for

APT Allgas and Envestra (Qld)

Warwick AndersonGeneral Manager, Network Regulation

1 March 2011Public forum

Housekeeping matters

• Please sign the attendance sheet

• A record of this meeting will be made

2

Purpose of the forum

• Present the main features of the AER’s draft decision on the access arrangement proposals submitted by APT Allgas and Envestra

• Inform parties intending to make submissions on the AER’s draft decision

3

Submissions

• Submissions on the AER’s draft decision can be sent to [email protected], until 21 April

• The AER’s access arrangement guideline provides guidance on making submissions– available at www.AER.gov.au

• Timeframes under the NGL and NGR limit the AER’s ability to accept late submissions

4

Revenues & Prices - APT Allgas

• The AER has determined lower revenues & prices than those proposed by APT Allgas.

• The main reductions are to the proposed WACC, forecast opex and tax allowance.

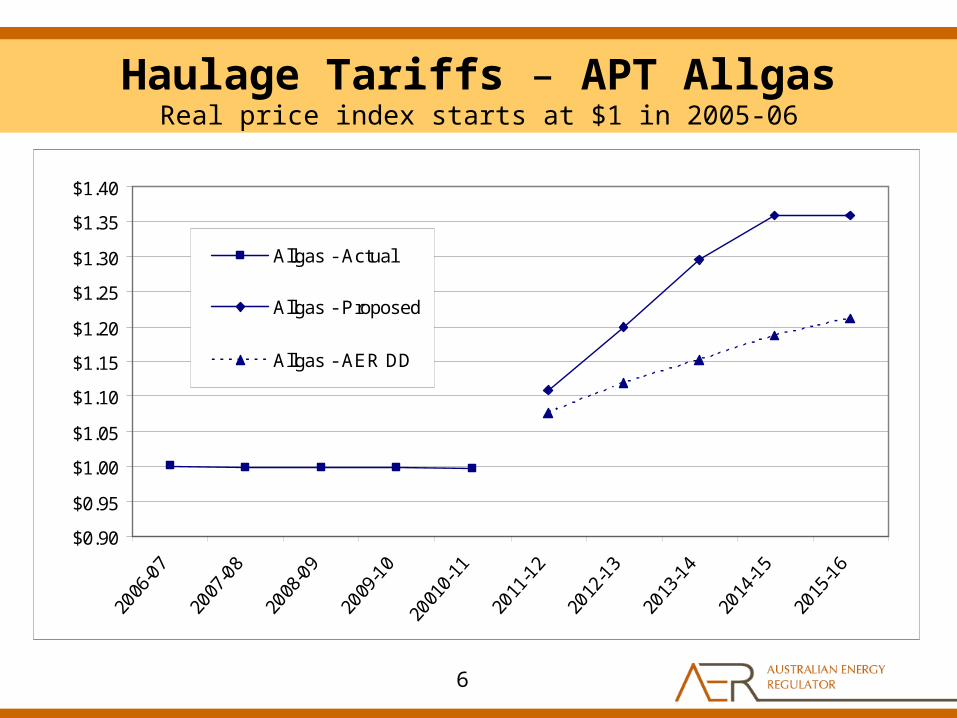

• Tariffs for haulage services are expected to rise in real terms by about 3.6 per cent per annum (on average) over the AA period.

• The tariffs for ancillary services were revised and will increase each year only by the rate of change in CPI.

5

Haulage Tariffs – APT AllgasReal price index starts at $1 in 2005-06

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

$1.20

$1.25

$1.30

$1.35

$1.40

Allgas - Actual

Allgas - Proposed

Allgas - AER DD

6

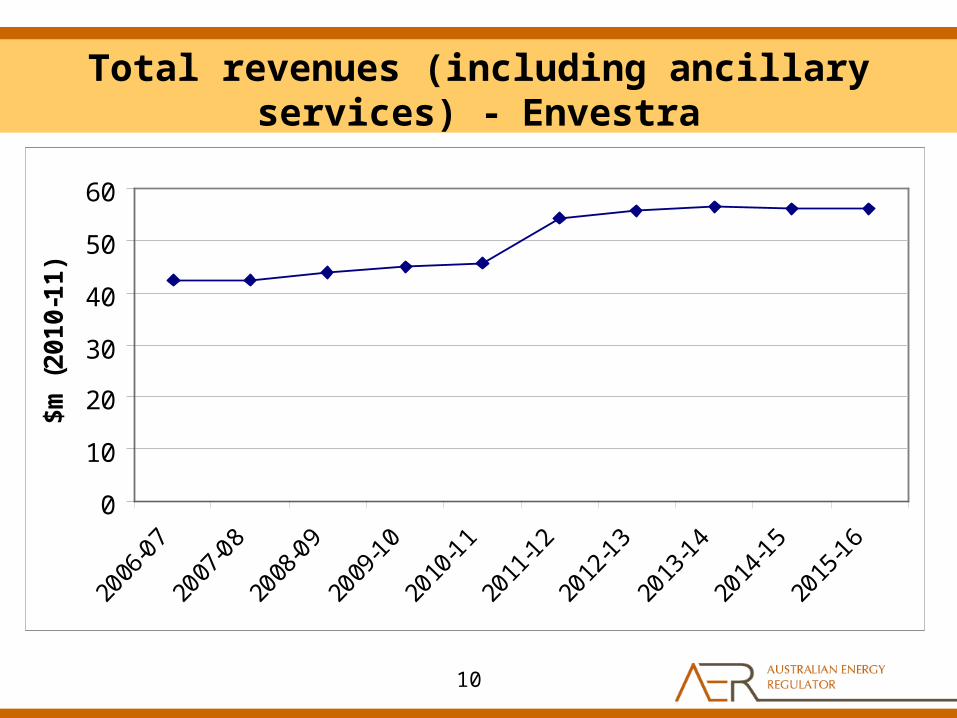

Total revenues (including ancillary services)

- APT Allgas

7

0

10

20

30

40

50

60

70

80

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

$m

(2

01

0-1

1)

Revenues & Prices - Envestra

• The AER has determined lower revenues & prices than those proposed by Envestra.

• The main reductions are to Envestra’s proposed WACC, forecast capex and forecast opex.

• Tariffs for haulage services are expected to rise in real terms by about 2.6 per cent per annum (on average) over the AA period.

• The tariffs for ancillary services were revised and will increase each year only by the rate of change in CPI.

8

Haulage Tariffs - Envestra Real price index starts at $1 in 2005-06

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

Envestra Qld - Actual

Envestra Qld - Proposed

Envestra Qld - AER DD

9

Total revenues (including ancillary services) - Envestra

10

0

10

20

30

40

50

60

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

$m

(2

01

0-1

1)

Key drivers of results

• Key drivers:– Return on capital (asset base * cost of capital) – Return of capital (depreciation)– Capital expenditure forecasts – Operating expenditure forecasts– Demand forecasts - for converting revenues

to prices.

11

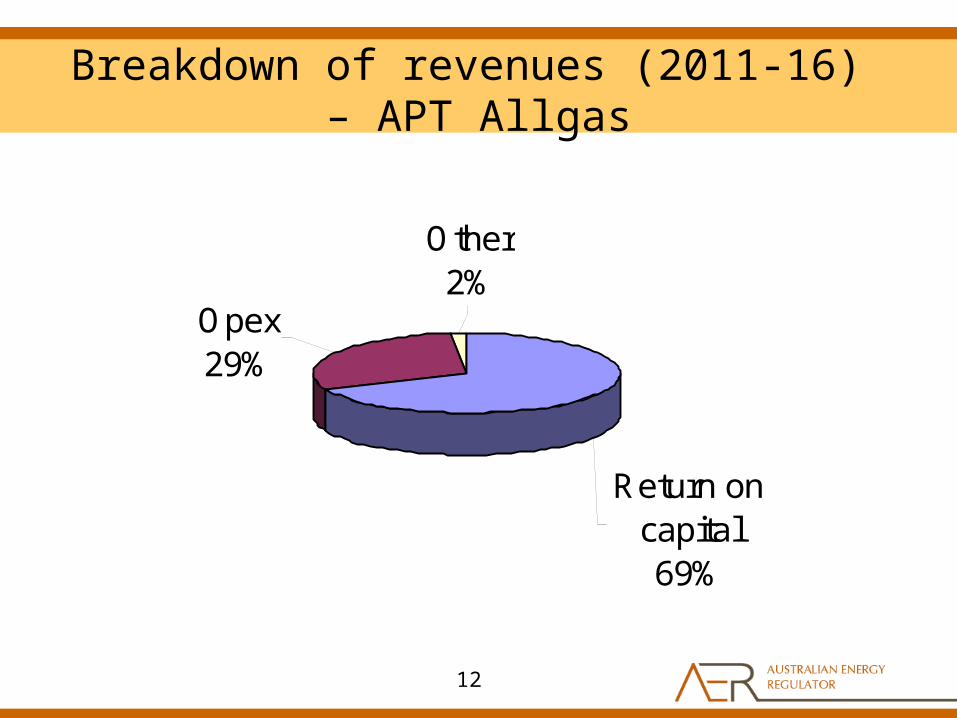

Breakdown of revenues (2011-16) – APT Allgas

12

Return on capital69%

Other2%

Opex29%

Breakdown of revenues (2011-16) – Envestra

13

Opex31%

Other9%

Return on capital60%

Cost of capital (WACC)

• The nominal cost of capital has increased significantly (see following table)

• Debt risk premium, more than tripled since the earlier AA period.

• The cost of equity has decreased, due mostly to a reduction in the equity beta.

• The AER has set the market risk premium to its pre-GFC level of 6%.

14

WACC parameters

15

Parameters (%)Earlier AA

periodAPT Allgas proposal

Envestra proposal

AER draft decision

Nominal risk free rate 5.3 5.1 5.3 5.7

Inflation forecast 2.8 2.5 2.6 2.5

Cost of equity 11.3 12.2 13.0 10.5

Equity beta 1.1 1.1 0.8-1.1 0.8

Market risk premium 6 6.5 6.5-8.0 6

Cost of debt 6.6 8.9 8.7 9.6

Debt risk premium 1.3 3.9 3.4 3.9

Gearing (D/(D+E)) 60 60 55 60

Nominal cost of capital 8.7 10.2 10.6 10.0

Revenues under different WACCs – APT Allgas

16

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2011-12 2012-13 2013-14 2014-15 2015-16

$m (

no

min

al)

Allgas - Proposed

Allgas - AER DD

Allgas - Earlier AA

Revenues under different WACCs – Envestra

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2011-12 2012-13 2013-14 2014-15 2015-16

$m

(n

om

ina

l)

Envestra Qld - Proposed

Envestra Qld - AER DD

Envestra Qld - Earlier AA

17

Regulatory asset base – APT Allgas

0

100

200

300

400

500

600

As a

t 30 J

un

e (

$m

, n

om

inal)

Proposed

AER approved

18

Capital expenditure – APT Allgas

• AER accepted APT Allgas’s proposed capex.

• AER identified a few issues with APT Allgas’s capex proposal. But the impact was not material.

19

Total capex – APT Allgas

0

5

10

15

20

25

30

35

40

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Rea

l $'

m 2

010-

11

Actual Estimate QCA allowance

Allgas forecast AER allowance

20

Capex by purpose – APT Allgas

Customer Requested

57%

Network augmentation

5%

Network renewal29%

Non-system9%

Customer Requested

63%Network

augmentation8%

Network renewal23%

Non-system6%

Earlier AA period

(actual)

Next AA period

(as proposed/accepted)

21

Regulatory asset base – Envestra

0

100

200

300

400

500

600

As a

t 30 J

un

e (

$m

, n

om

inal)

Proposed

AER approved

22

Capital expenditure - Envestra

• Envestra proposed a 71% real increase in capex compared to the earlier AA period– due largely to Envestra’s proposed expansion of its

mains replacement program.

• The AER accepted most of the proposed capex. Adjustments for– contingency amounts– overhead costs– real cost escalation and – mains replacement in Brisbane.

23

Total capex - Envestra

0

5

10

15

20

25

30

35

40

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Rea

l $'

m 2

010-

11

Actual spend Estimate QCA allowanceEnvestra forecast AER allowance

24

Capex by purpose - Envestra

0

2

4

6

8

10

12

14

16

18

2006-07 2007-08 2008-09 2009-10(estimate)

2010-11(estimate)

2011-12 2012-13 2013-14 2014-15 2015-16

Mains replacement Grow th Assets Other capital expenditure

25

Mains replacement capex - Envestra

0

10

20

30

40

50

60

70

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Actual Approved Forecast

Mai

ns

rep

lace

d (

km)

26

Return of capital

• Both Envestra & APT Allgas proposed shorter asset lives than used previously.

• The AER has accepted these asset lives– increased the rate of depreciation.

• Return of capital has increased significantly.

• The following graph shows the trend in regulatory depreciation.

27

Regulatory depreciation – APT Allgas

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.520

06-0

7

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

$m (

2010

-11)

28

Regulatory depreciation - Envestra

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.020

06-0

7

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16$m

(20

10-1

1)

29

Operating expenditure – APT Allgas

• APT Allgas proposed a 23% real increase in opex compared to the earlier AA period, principally due to:– increased input costs – increased UAG costs, and– the need for various types of non-base year costs.

• The AER amendments, including– input cost escalators– a reduction in the price assumptions for UAG– various proposed step changes.

• The AER’s draft decision results in a 12% real increase in opex compared the earlier AA period.

30

Total opex – APT Allgas

APT Allgas opex

0

5

10

15

20

25

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Real

$'m

201

0-11

Actual Estimate QCA allowance AER allowance Allgas's forecast

31

Operating expenditure - Envestra

• Envestra proposed a 16% real increase in opex compared to the earlier AA period, principally due to:– increasing input costs– increasing UAG costs– increased network development, and – the need for various non-base year costs.

• The AER required a number of amendments, including:– input cost escalation– network development– UAG expenditure and– several of the proposed non base year costs.

• The AER’s draft decision results in an 11% real reduction in opex compared to the earlier AA period.

32

Base year costs - Envestra

33

Opex/km

0100020003000400050006000700080009000

$(2

00

9-1

0)/

km

Total opex - Envestra

Envestra opex

0

5

10

15

20

25

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Rea

l $'m

201

0-11

Actual Estimate QCA allowance Envestra's forecast AER allowance

34

Demand forecast - APT Allgas

• For the most part, the proposed demand forecasts are reasonable.

• AER adjustments:– average gas usage for residential customers– lower growth in business customer numbers

35

APT Allgas residential customer numbers forecast

Residential customer numbers

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Actual AER draft decision

36

APT Allgas average residential consumption forecast

Average residential consumption

0

2

4

6

8

10

12

14

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

GJ

Actual APT Allgas proposal AER draft decision

37

Demand forecast - Envestra

• For the most part, the proposed demand forecasts are reasonable.

• AER adjustments:– average gas usage for residential customers

38

Envestra residential customer numbers forecast

Residential customer numbers

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Actual AER draft decision

39

Envestra average residential consumption

Average residential consumption

0

2

4

6

8

10

12

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

GJ

Actual AER draft decision Envestra proposal

+

40

Terms and conditions

• Submissions:– overall terms and conditions were weighted

too much in favour of the service providers.

• The AER accepts most of the proposed terms and conditions for both service providers.

• However, changes are required to provide a better balance between the service providers and customers

41

Consultant advice

• Cost of capital: Professor Kevin Davis

• Opex and capex forecasts: Wilson Cook

• Labour cost growth: Access Economics

• Demand forecasts: ACIL Tasman

42

Timeline

Release of draft decisions 17 February 2011

Public forum on draft decisions 1 March 2011

Revised proposals to be submitted 23 March 2011

Submissions on draft decisions due 21 April 2011

Release of final decisions Late May 2011

43

![[XLS] · Web view2011 1/3/2011 1/3/2011 1/5/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/7/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011 1/11/2011](https://static.fdocuments.in/doc/165x107/5b3f90027f8b9aff118c4b4e/xls-web-view2011-132011-132011-152011-172011-172011-172011-172011.jpg)