Dr. Stefan Heng InternationalInternational Telecommunications Society, Berlin, September 6, 2004...

37

Dr. Stefan Heng International Telecommunications Society, Berlin, September 6, 2004 E-PAYMENT SYSTEMS: CHANCE ONLY IN THE MEDIUM TERM

-

date post

18-Dec-2015 -

Category

Documents

-

view

216 -

download

1

Transcript of Dr. Stefan Heng InternationalInternational Telecommunications Society, Berlin, September 6, 2004...

Dr. Stefan Heng

International Telecommunications Society,Berlin, September 6, 2004

E-PAYMENT SYSTEMS: CHANCE ONLY IN THE MEDIUM TERM

Page 2 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

11 Initial situation: Symbiosis developing in onlineInitial situation: Symbiosis developing in onlinecommercecommerce

22 Demands on payment systems

33 Comparison of current payment systems

44 Conclusion

Page 3 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Symbiosis developing in online trade (I)E-business: Hype and reality

During internet hype: forecasts of exorbitant e-business growth rates.

• Actually far more moderate growth.

• B2C in Germany: currently only 2% of retail turnover.

Thanks to enhanced technologies (3G, 4G) mobile telephony will emerge as important business area.

• 2001: worldwide turnover of EUR 600 m spent on mobile content.

• 2005: worldwide turnover of EUR 11 bn.

Page 4 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Symbiosis developing in online trade (II)Great hope on payment systems

E-commerce pioneers tended to see product range, marketing, and logistics as problem areas.

• Challenges of payment transactions in e-commerce underestimated at first.

Currently great hopes on payment systems.

• Cooperation of content providers and payment providers needed.

Page 5 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

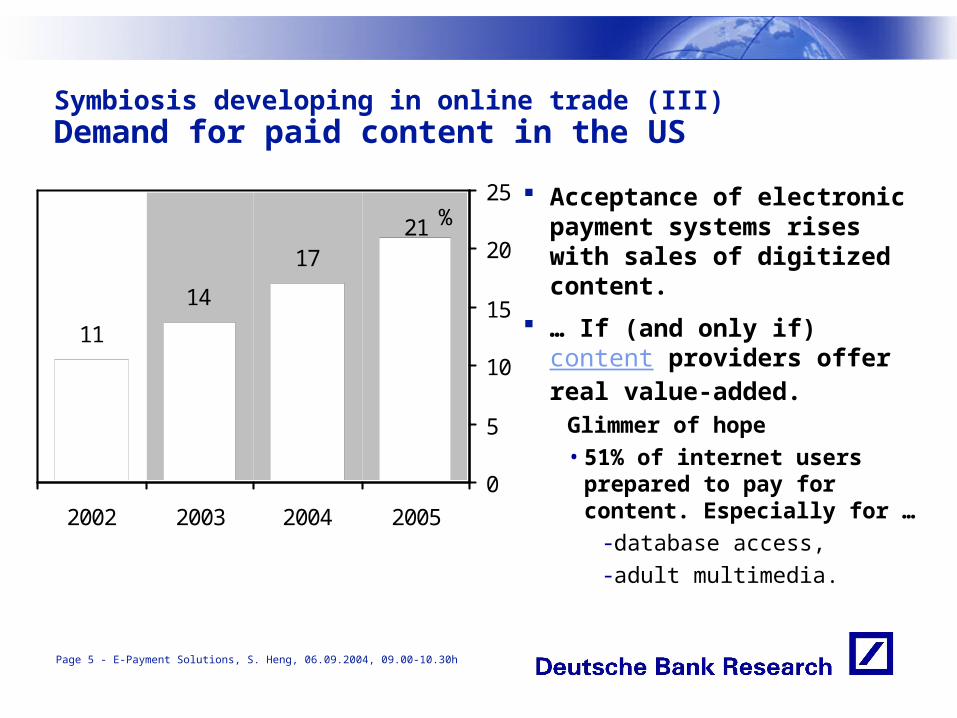

Symbiosis developing in online trade (III)Demand for paid content in the US

Acceptance of electronic payment systems rises with sales of digitized content.

… If (and only if) content providers offer real value-added.

Glimmer of hope

• 51% of internet users prepared to pay for content. Especially for …

-database access,

-adult multimedia.

11

14

1721

0

5

10

15

20

25

2002 2003 2004 2005

%

in % of internet usersSource: eMarketer, 2003

Page 6 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Symbiosis developing in online trade (IV) Cashless payment systems

35 m online purchases in Europe.

Payment methods with origin in offline business dominant. Only …• Proton (Belgium),

• Minicash (Luxembourg), and

• Chipknip (Netherlands) …

relevant as yet.0 70 140 210

EU 12

NL

LU

FR

ES

DE

BE

Bank transferDirect debitCredit/debit cardChequeCard-based e-money

Number of annual transactions per inhabitant, 2002Source: European Central Bank, 2003

Page 7 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

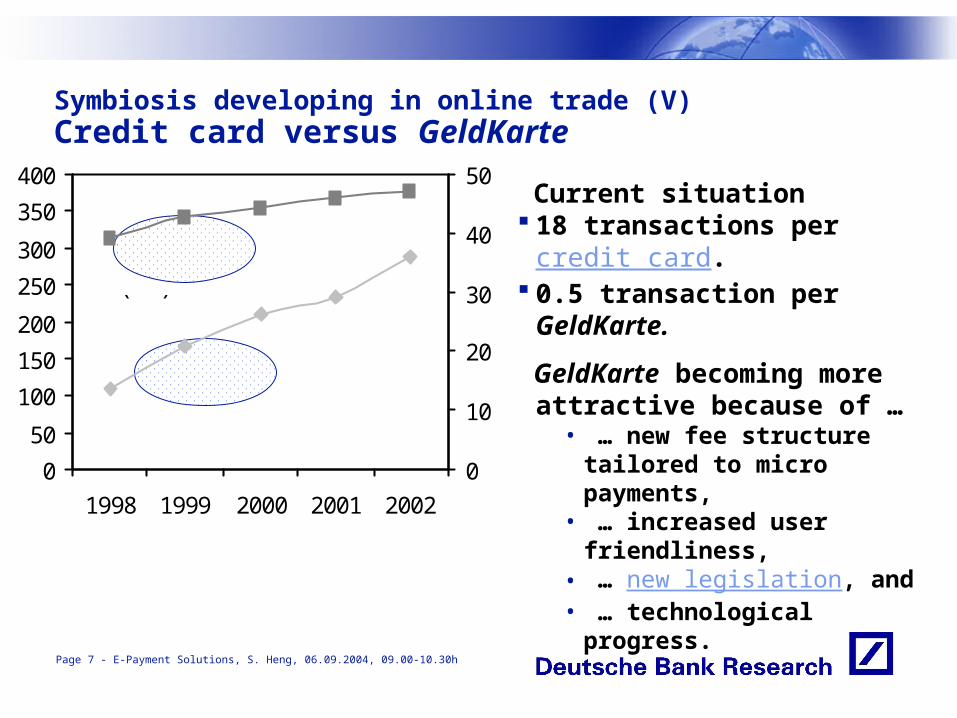

Symbiosis developing in online trade (V) Credit card versus GeldKarte

Current situation 18 transactions per credit card. 0.5 transaction per GeldKarte.

GeldKarte becoming more attractive because of …

• … new fee structure tailored to micro payments,

• … increased user friendliness,• … new legislation, and• … technological progress.

0

50

100

150

200

250

300

350

400

1998 1999 2000 2001 2002

0

10

20

30

40

50

GeldKarte(right)

Credit card(left)

Transactions in mSource: Association of German Banks, 2003

Page 8 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

11Initial situation: Symbiosis developing in onlinetrade

22 Demands on payment systems

33 Comparison of current payment systems

44 Conclusion

Page 9 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Demands on payment systems (I)Different players with different needs

General

(Perceived) security.

Consistency.

Totality.

Special demands of customers

Ease of use.

Portability.

Anonymity.

Widespread use among merchants.

Special demands of merchants

Indisputability.

Low transaction costs.

Widespread use among customers.

Page 10 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Demands on payment systems (II) E-payment systems as network goods

Attractiveness rises faster than the number of users.

Exceeding critical mass as a prerequisite for long-term potential.• Merchants hesitant about investing in a system that only a few

customers are interested in.

• Few customers opt for a system used by only a limited number of merchants.

Page 11 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

11Initial situation: Symbiosis developing in online trade

33 Demands on payment systems

44 Comparison of current payment systems

55 Conclusion

Page 12 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Comparison of current payment systems (I)Credit Card

In use all around the world.

Especially suitable for macro payments.

Consumers fear misuse of card data in the anonymity of the internet.

• Risk of fraud more on merchants and credit-card companies.

• Add-ons like “Verified by Visa” make credit-card use even safer.

Origin in offline business - Adaptation of traditional systemCost to the merchant: 3- 5% of sales Accepting outlets in Germany: 400,000Users in Germany: 21 m

Page 13 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

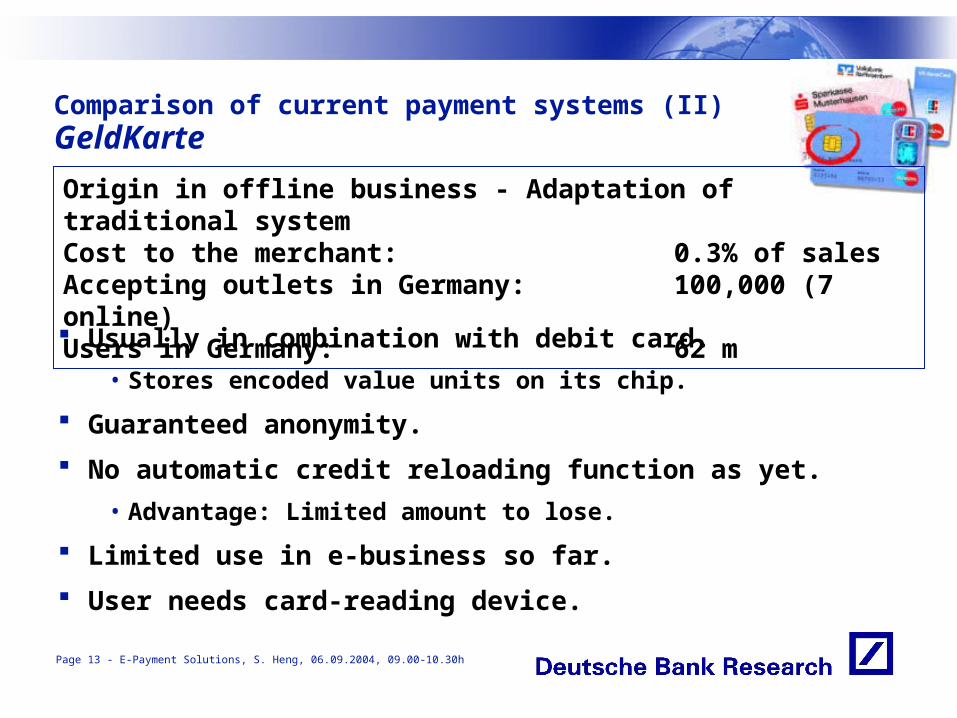

Comparison of current payment systems (II) GeldKarte

Usually in combination with debit card.

• Stores encoded value units on its chip.

Guaranteed anonymity.

No automatic credit reloading function as yet.

• Advantage: Limited amount to lose.

Limited use in e-business so far.

User needs card-reading device.

Origin in offline business - Adaptation of traditional system Cost to the merchant: 0.3% of salesAccepting outlets in Germany: 100,000 (7 online)Users in Germany: 62 m

Page 14 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Comparison of current payment systems (III) Firstgate click&buy

Aggregated micro-payments are debited from bank account.

Payment made by entering user name and password.

Guaranteed anonymity.

Internet-based micro-payment systemCost to the merchant: 10- 35% of salesAccepting outlets in Germany: 2,500Users in Germany: 2 m

Page 15 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Comparison of current payment systems (IV) Infin-MicroPayment

Operates through fixed-rate telephone service lines.

Collects payment via telephone bill.

Seller appreciates payment guarantee provided by the system operator.

Guaranteed anonymity.

Additional telephone charges on top.

Only for micro-payments:

• Law puts limit on payments through service lines.

Micro-payment system charging by phone billCost to the merchant: 15- 35% of salesAccepting outlets in Germany: < 50Users in Germany: n.a.

Page 16 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Comparison of current payment systems (V) Moxmo

Mobile phone-based method

Transmission of payment separate from ordering process to guarantee anonymity. But

• … high security levels guaranteed by digital signature not reached.

Mobile phone-based payment methodCost to the merchant: 3% of salesAccepting outlets in Germany: 10Users in Germany: 1 m

Page 17 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

11Initial situation: Symbiosis developing in online trade

22 Demands on payment systems

33 Comparison of current payment systems

44 ConclusionConclusion

Page 18 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

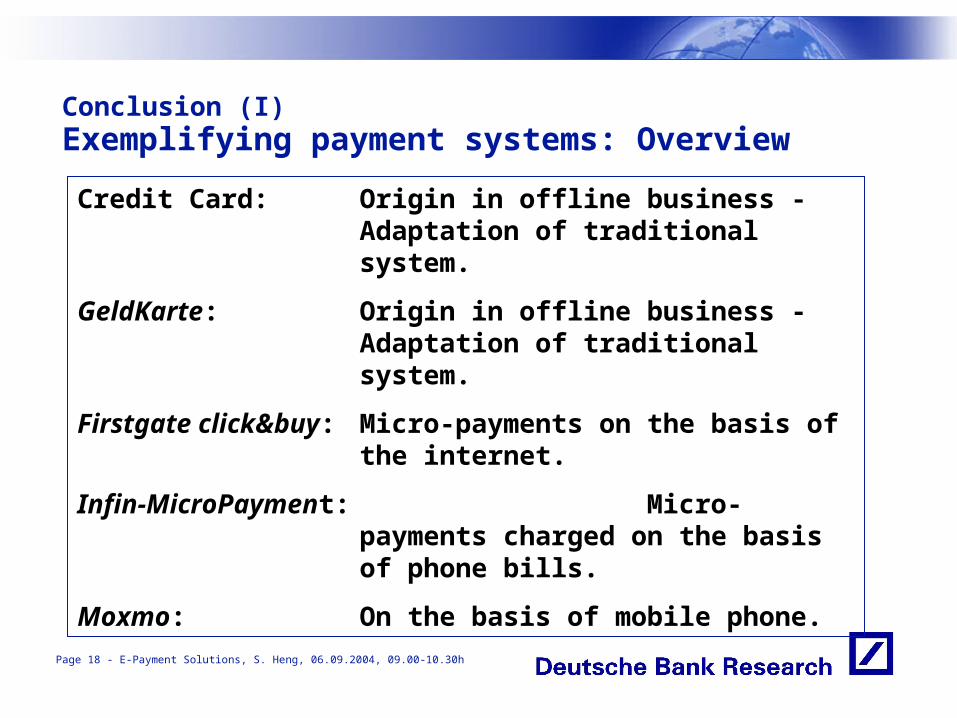

Credit Card: Origin in offline business - Adaptation of traditional system.

GeldKarte: Origin in offline business - Adaptation of traditional system.

Firstgate click&buy: Micro-payments on the basis of the internet.

Infin-MicroPayment: Micro-payments charged on the basis of phone bills.

Moxmo: On the basis of mobile phone.

Conclusion (I) Exemplifying payment systems: Overview

Page 19 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Conclusion (II) Prospects for innovative payment systems

Online business needs …

• secure,

• user-friendly, and

• low-priced …

innovative payment solutions.

Demands of consumers and merchants on payment solutions diverge widely.

Support from high-profile partners crucial to wider dissemination.

• Content providers, suppliers of telecom infrastructure and banks have an obligation to act.

Page 20 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

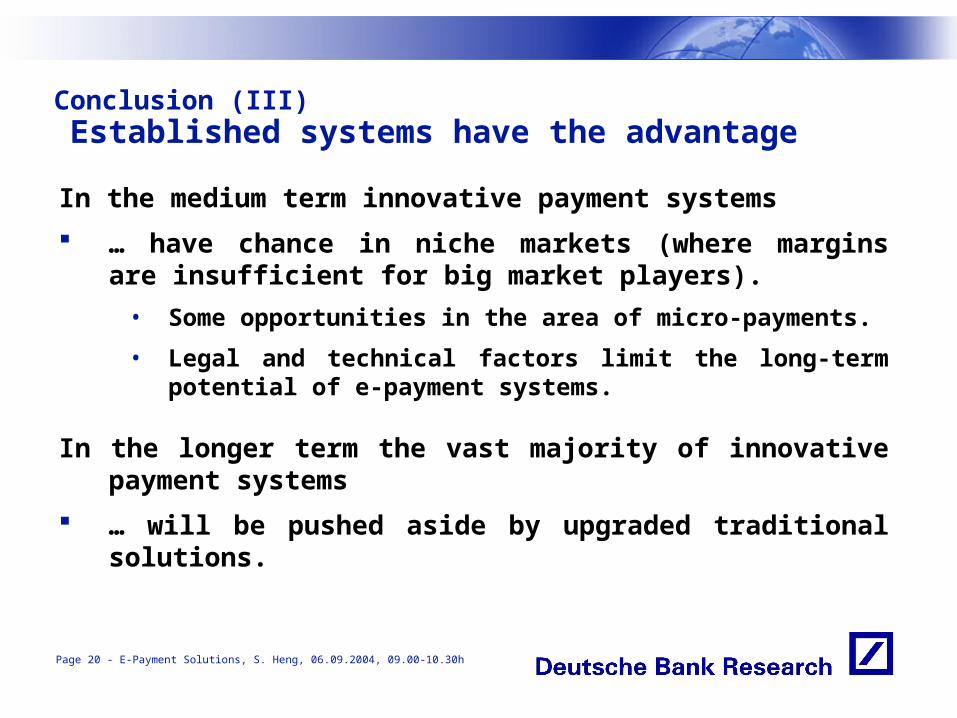

Conclusion (III) Established systems have the advantage

In the medium term innovative payment systems

… have chance in niche markets (where margins are insufficient for big market players).

• Some opportunities in the area of micro-payments.

• Legal and technical factors limit the long-term potential of e-payment systems.

In the longer term the vast majority of innovative payment systems

… will be pushed aside by upgraded traditional solutions.

Dr. Stefan Heng

International Telecommunications Society,Berlin, September 6, 2004

Visit our home page to download

“E-payments: modern complement to traditional payment systems”, E-Conomics No. 44

http://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000079835.pdf

Page 22 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

Appendix I: ContentAppendix I: Content

Page 23 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

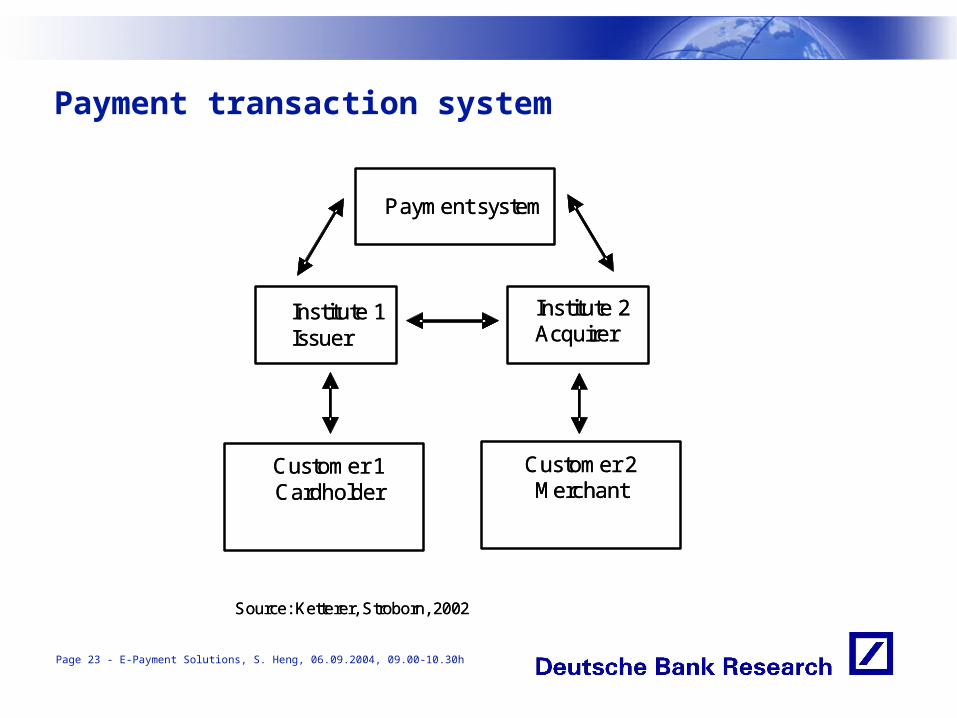

Payment transaction system

Payment system

Institute 1Issuer

Institute 2Acquirer

Customer 1Cardholder

Customer 2Merchant

Source: Ketterer, Stroborn, 2002

Payment system

Institute 1Issuer

Institute 2Acquirer

Customer 1Cardholder

Customer 2Merchant

Source: Ketterer, Stroborn, 2002

Page 24 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Sales of paid content in Germany

Sales of paid content rise.

Tenfold increase between 2002 and 2005.

But starting from a low level.

14

45

86

127

0

20

40

60

80

100

120

140

2002 2003 2004 2005Source: Sapient, 2003

EUR m

Page 25 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Interest gainDate dueInterest loss

Post-paidPre-paid

t

Source: DB Research, 2004

• Credit card

• Pre-paid e-moneyunits on smart card

• Network money

Debit dates of various payment methods

Page 26 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

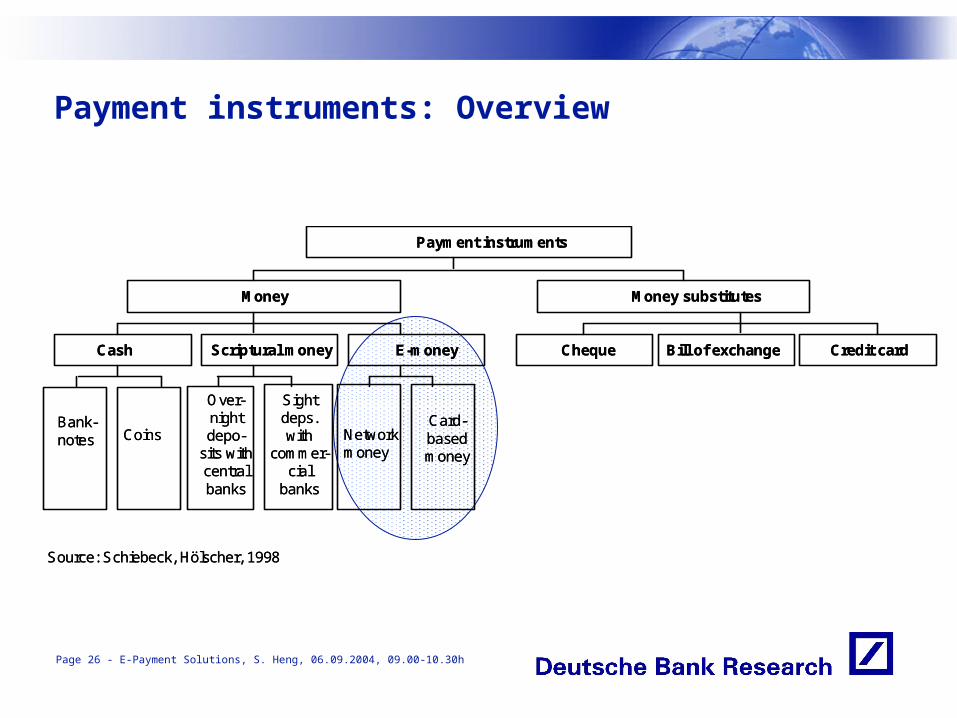

Payment instruments: Overview

Bank-notes Coins

Payment instruments

Source: Schiebeck, Hölscher, 1998

Money Money substitutes

Cash Scriptural money E-money Cheque Bill of exchange Credit card

Networkmoney

Card-basedmoney

Over-nightdepo-

sits withcentralbanks

Sightdeps. with

commer-cial

banks

Bank-notes Coins

Payment instruments

Source: Schiebeck, Hölscher, 1998

Money Money substitutes

Cash Scriptural money E-money Cheque Bill of exchange Credit card

Networkmoney

Card-basedmoney

Over-nightdepo-

sits withcentralbanks

Sightdeps. with

commer-cial

banks

Page 27 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

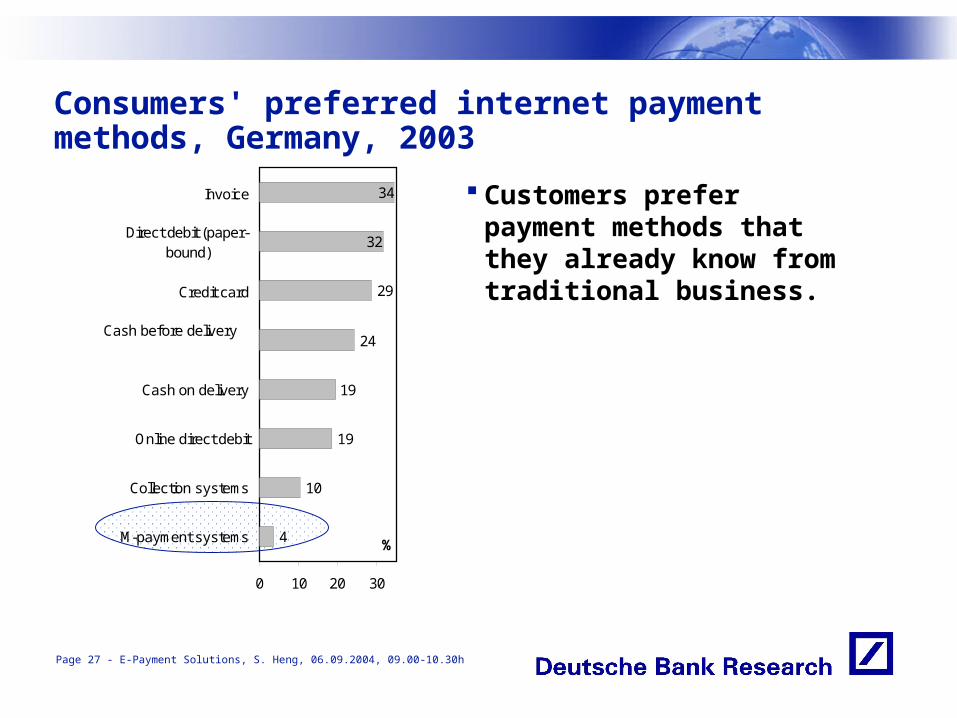

Consumers' preferred internet payment methods, Germany, 2003

Customers prefer payment methods that they already know from traditional business.29

24

19

10

4

19

32

34

0 10 20 30

Invoice

Direct debit (paper-bound)

Credit card

Cash before delivery

Cash on delivery

Online direct debit

Collection systems

M-payment systems %

in %, multiple answ ers possibleSource: Institute for Economic Policy and Economic Research, Karlsruhe University, 2003

Page 28 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Core criteria of preferred payment methods

User-friendly, …

widely available, and …

low-priced innovative payment solutions must be established very soon.40

27

16

56

66

0 20 40 60

User-friendly

Widelyavailable

Low effort

Low cost

Simple tocancel

transactions

in %, multiple answ ers possibleSource: Institute for Economic Policy and Economic Research, 2003

%

Page 29 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

(Perceived) security a crucial factor (Perceived) security derived from the level of security

provided by technology and its marketing.

Systems need answers on issues of …

Authorization: Only legitimate users have access to the system.Authentication: Partners to the transaction really are who they

claim to be.Privacy: Only participants are allowed to observe

transaction.Integrity: Protecting the information from being

manipulated dealing with theft of carrier medium upon which value units have been stored.

Totality: Dealing with accidental data corruption (technical defect).

Page 30 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

79

78

65

109

110

118

29

26

76

2

58

40

20

28

127

55

0 20 40 60 80 100 120 140

EU 12

NL

GB

FR

FI

ES

DE

BE

Credit cardDebit card

per 100 inhabitantsSource: European Central Bank, 2000

Credit versus debit card, 2000

Systems already successful in offline business have excellent prospects.

• Internationally established credit card .

• Especially in Germany the widely used debit card.

Page 31 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Germany’s Signature Law

Response to demands of e-business. The Signature Law …

• … equates digital signature with handwritten signature .

• Digital signature stored on smart card, used with the aid of card-reading device.

• Specific security mechanisms protect the identities of both partners to a contract.

Signature alliances (banks, businesses, government bodies) drive forward this project, which is crucial to electronic commerce.

Page 32 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Principle of M-payment systems

Buyer gives phone number (or dummy number) to seller

Seller forwards the instruction to payment system provider

Payment system provider calls buyer, verifies information…

• and collects amount through direct debit

Buyer Merchant

M-paymentsystem4 PIN,

€

€

1

2

35

€

: Order

: Delivery of goods

: Payment

1 – 5: process sequence

: Inquiry by mobile phone

PIN: Personal identification number

Source: DBResearch, 2004

Buyer Merchant

M-paymentsystem4 PIN,

€

€

1

2

35

€

: Order

: Delivery of goods

: Payment

1 – 5: process sequence

: Inquiry by mobile phone

PIN: Personal identification number

Source: DBResearch, 2004

Page 33 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

E-payment systems: Chance only in the medium term

Appendix II: DB ResearchAppendix II: DB Research

Page 34 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Deutsche Bank Research: Vision and mandate

Think tank of Deutsche Bank Group

Contribution to Deutsche Bank’s brand equity

Centre for independent assessment of risks and opportunities

In-house research for

• Board of Managing Directors

• Group Executive Committee

Bridge to politics via representatives

Bridge to academia

Page 35 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

Selective publications of Deutsche Bank Research

EU Monitor

• European integration

Current Issues

• Demography

• China

• Energy: the world without oil

• Global growth centres

• Banks 2015

Sector reports

Research Notes

E-Conomics

Publications available for free!

Visit our homepage: www.dbresearch.com

Page 36 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

DB Research: Organisation

• Identification and analysis of macroeconomic trends of relevance to Deutsche Bank

• Analysis of growth, interest rates and exchange rates

• Country and sovereign risk analysis and stress testing of developed and emerging markets•Country, event and event risk ratings•Industry risk modelling and stress testing

• Internet-driven structural change in financial services, e.g. e-banking, e-brokerage, ECNs, mobile banking

• Trends in e- and m-commerce• Technology and structural change in bank markets• A new regulatory framework for the internet society?• New economy in Europe

• Economic policy (regulation, taxes etc.)• Old-age provision and pension funds• Issues affecting small and medium-sized enterprises• European integration (EU enlargement, EMU, institutional issues etc.)

• Medium-term sector trends• Analysis of cross-sector technologies•Real-estate market research

Economic and European Policy Issues

Sector Research

Banking, Financial Markets, Regulation• Supervision and regulation• European capital market integration• Structure of banking systems

ManagementNorbert Walter

eResearch

Macro Trends

Risk Analysis

Page 37 - E-Payment Solutions, S. Heng, 06.09.2004, 09.00-10.30h

www.dbresearch.com