Download the guidelines and regulations for members in practice

66

AAT is a registered charity. No. 1050724 Member in practice regulations and guidance

Transcript of Download the guidelines and regulations for members in practice

AAT is a registered charity. No. 1050724

Member in practice regulations and guidance

2

Contents

Introduction........................................................................................................................................ 5

The member in practice regulations .............................................................................................. 5

The Interpretation Act .................................................................................................................... 5

Definitions...................................................................................................................................... 5

The guidance ................................................................................................................................ 6

Regulation 1 - Being in practice ........................................................................................................ 7

Guidance to regulation 1 ............................................................................................................... 7

Services covered by the scheme for members in practice ............................................................ 10

Accountancy ................................................................................................................................ 10

Bookkeeping (BK) ....................................................................................................................... 10

Financial Accounting and Accounts Preparation (FA and AP) .................................................... 10

Budgeting and Forecasting (B and F) ......................................................................................... 11

Management Accounting (MA) .................................................................................................... 11

Payroll (P) .................................................................................................................................... 11

Independent Examination (IE) ..................................................................................................... 11

Limited Assurance Engagement (LAE) ....................................................................................... 12

Forensic Accounting (FoA) .......................................................................................................... 12

Internal Audit (IA) ........................................................................................................................ 12

Taxation ...................................................................................................................................... 13

Value Added Tax (VAT) .............................................................................................................. 13

Personal Income Tax (PT) .......................................................................................................... 13

Business Income Tax (BT) .......................................................................................................... 13

Corporation Tax (CT) .................................................................................................................. 14

Capital Gains Tax (CGT) ............................................................................................................. 14

Inheritance Tax (IHT) .................................................................................................................. 14

Consultancy ................................................................................................................................ 14

Business Plans (BP).................................................................................................................... 14

Computerised Accountancy Systems (CAS) ............................................................................... 15

Company Secretarial Services (CSS) ......................................................................................... 15

Regulation 2- Restrictions on being in practice ............................................................................. 16

Regulation 3 - Exemptions .............................................................................................................. 17

Guidance to Regulation 3 – Exemptions ..................................................................................... 17

The scheme for members in practice framework ............................................................................ 18

Regulations applicable to members registered on the scheme ...................................................... 20

Regulation 4 - Registered members in practice .............................................................................. 20

3

Guidance to regulation 4 – application process for registered status ......................................... 20

Regulation 5 - Conditions of members registered on the scheme .................................................. 22

Guidance to regulation 5 – conditions of registration .................................................................. 22

Benefits for registered members in practice ............................................................................... 23

Regulations applicable to licensed members in practice ................................................................ 25

Regulation 6 - Licensed members in practice ................................................................................. 25

Guidance to regulation 6 – application process for licensed status ............................................ 25

Regulation 7 - Conditions of a practising licence ............................................................................ 28

Guidance to regulation 7 – conditions of a practising licence ..................................................... 28

Benefits for licensed members in practice .................................................................................. 28

Professional Indemnity Insurance (PII) ........................................................................................... 30

Continuity of Practice Agreement .................................................................................................... 31

Practice management ..................................................................................................................... 32

Anti money laundering and professional ethics diagnostic tests ..................................................... 33

Members in practice with gross fee income below £1,000.............................................................. 34

Regulation 8 - Conditions of members undertaking voluntary work ............................................... 35

Guidance to regulation 8 – members undertaking voluntary work ............................................. 35

Regulation 9 - Extension of approved services .............................................................................. 36

Guidance to regulation 9 – Extension of approved services ....................................................... 36

Regulation 10- Renewal of practising licences or registration on the scheme for members in practice

........................................................................................................................................................ 37

Guidance to regulation 10 – renewal of practising licences or registration ................................ 37

Regulation 11- Withdrawal or restriction of a practising licence or registration on the scheme ..... 39

Regulation 12 - Return of the licence ............................................................................................. 40

Regulation 13 - Restoration of a practising licence or registration and removal or modification of

restrictions ....................................................................................................................................... 41

Regulation 14 - Effects of declaration of ineligibility........................................................................ 42

Regulation 15 - Effect of non-payment of fees ................................................................................ 43

Regulation 16 - Powers to require the production of information and documents .......................... 44

Regulation 17 - Powers of review ................................................................................................... 45

Guidance to regulation 17 – Reviews ......................................................................................... 45

Regulation 18 – Continuing professional development (CPD) ....................................................... 47

Guidance to regulation 18 – Continuing professional development (CPD) ................................ 47

Regulation 19 - Anti money laundering ........................................................................................... 49

Guidance to regulation 19 - What it means to be supervised by AAT for Money Laundering

Compliance ................................................................................................................................. 49

Regulation 20 - Appeals .................................................................................................................. 50

Guidance to regulation 20 – Appeals .......................................................................................... 50

Regulation 21 - Publicity for members' services ............................................................................ 51

4

Regulation 22- Letters of Engagement ........................................................................................... 52

Guidance to regulation 22 – Letters of engagements ................................................................. 52

Regulation 23 - Members approved to carry out Limited Assurance Engagements ...................... 56

Guidance to regulation 23 – Members applying for or approved to carry out Limited Assurance

Engagements .............................................................................................................................. 56

Regulation 24 - Client monies ......................................................................................................... 57

Regulation 25 - Client Account ........................................................................................................ 58

Professional ethics .......................................................................................................................... 60

Forms of regulation not provided by AAT ....................................................................................... 61

a) Audit .................................................................................................................................... 61

b) Pensions or investment advice ........................................................................................... 61

c) Insolvency services ............................................................................................................. 61

Enquiries and contact details .......................................................................................................... 62

a) General enquiries .................................................................................................................. 62

b) Member in practice enquiries ................................................................................................ 62

c) Ethical enquiries .................................................................................................................... 62

d) CPD enquiries ....................................................................................................................... 62

e) Technical enquiries ............................................................................................................... 63

f) Tax enquiries ........................................................................................................................... 63

Schedule 1 ...................................................................................................................................... 64

Services ...................................................................................................................................... 64

Schedule 2 ....................................................................................................................................... 65

Professional Indemnity Insurance (PII) ...................................................................................... 65

Schedule 3 ...................................................................................................................................... 66

Gross Fee Income (GFI) ............................................................................................................. 66

5

Introduction

The member in practice regulations

AAT’s Council approved the member in practice regulations on 14 March 2013 under Article 51(2) of AAT's Articles of Association. The regulations take effect from 1 October 2013. These regulations supersede earlier member in practice regulations.

These regulations only apply to members who are in practice within the meaning of regulation 1:

(a) within the UK, Channel Islands or Isle of Man

(b) in any other jurisdiction but who, by agreement between the member and AAT, are bound by these regulations.

Breach of the provisions of these regulations shall constitute grounds for disciplinary action in accordance with AAT’s Disciplinary Regulations in force from time to time.

Explanatory guidance has been produced to accompany these, and members should refer to the guidance for further information on the provisions of the regulations.

The Interpretation Act

The Interpretation Act 1978 applies to these regulations in the same way as it applies to an enactment.

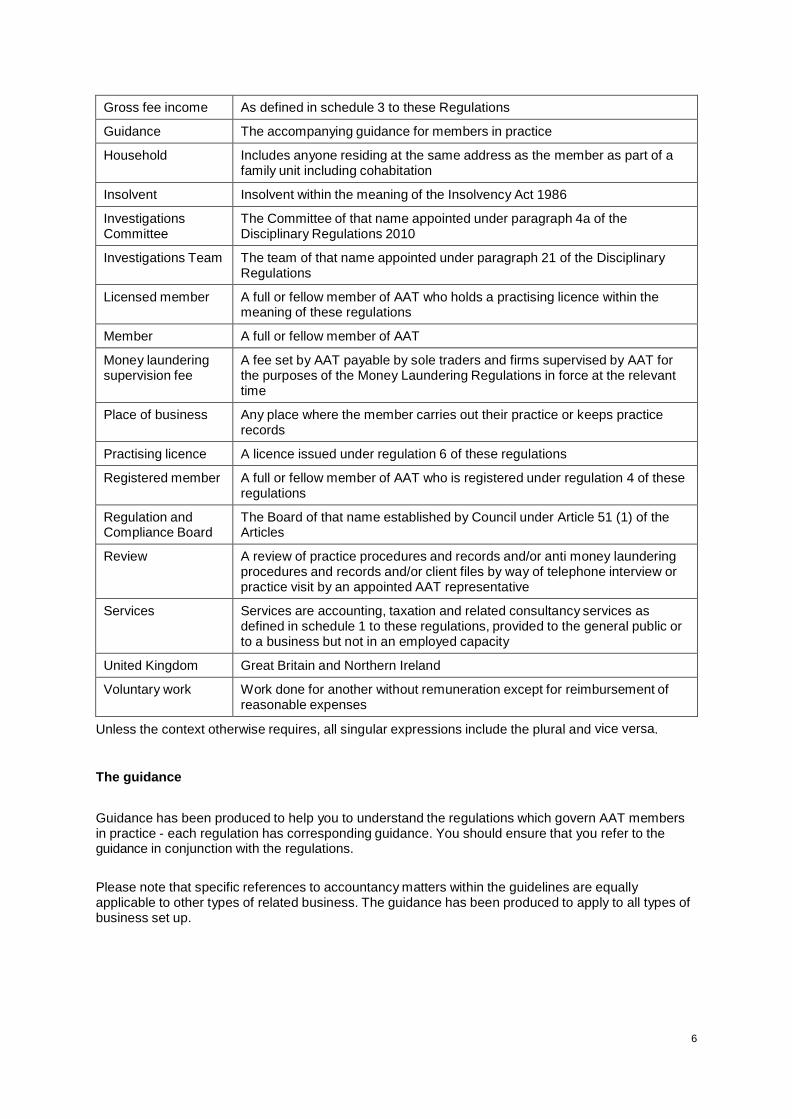

Definitions

Unless stated otherwise, in these regulations the following words and phrases mean:

AAT The Association of Accounting Technicians

Articles AAT’s Articles of Association 2011

Business stationery Letterheads, business cards, websites, advertisements, email signatures or similar electronic documentation.

Bankruptcy Bankruptcy within the meaning of the Insolvency Act 1986

CPD Continuing professional development as referenced in the guidance

Council The Council responsible for the overall management of the affairs of AAT

Disciplinary Committee

The Committee of that name established by Council under Article 19 of the Articles and appointed under paragraph 4(b) of the Disciplinary Regulations 2010

Disciplinary Tribunal A Tribunal appointed under paragraph 47 of the Disciplinary Regulations 2010

Family Parents, spouse, siblings, half-siblings and offspring

Fee(s) The fee or fees set from time to time by Council for any purpose under these regulations

Fellow member A fellow member of AAT as defined by AAT’s Articles

6

Gross fee income As defined in schedule 3 to these Regulations

Guidance The accompanying guidance for members in practice

Household Includes anyone residing at the same address as the member as part of a family unit including cohabitation

Insolvent Insolvent within the meaning of the Insolvency Act 1986

Investigations Committee

The Committee of that name appointed under paragraph 4a of the Disciplinary Regulations 2010

Investigations Team The team of that name appointed under paragraph 21 of the Disciplinary Regulations

Licensed member A full or fellow member of AAT who holds a practising licence within the meaning of these regulations

Member A full or fellow member of AAT

Money laundering supervision fee

A fee set by AAT payable by sole traders and firms supervised by AAT for the purposes of the Money Laundering Regulations in force at the relevant time

Place of business Any place where the member carries out their practice or keeps practice records

Practising licence A licence issued under regulation 6 of these regulations

Registered member A full or fellow member of AAT who is registered under regulation 4 of these regulations

Regulation and Compliance Board

The Board of that name established by Council under Article 51 (1) of the Articles

Review A review of practice procedures and records and/or anti money laundering procedures and records and/or client files by way of telephone interview or practice visit by an appointed AAT representative

Services Services are accounting, taxation and related consultancy services as defined in schedule 1 to these regulations, provided to the general public or to a business but not in an employed capacity

United Kingdom Great Britain and Northern Ireland

Voluntary work Work done for another without remuneration except for reimbursement of reasonable expenses

Unless the context otherwise requires, all singular expressions include the plural and vice versa.

The guidance

Guidance has been produced to help you to understand the regulations which govern AAT members in practice - each regulation has corresponding guidance. You should ensure that you refer to the guidance in conjunction with the regulations.

Please note that specific references to accountancy matters within the guidelines are equally applicable to other types of related business. The guidance has been produced to apply to all types of business set up.

7

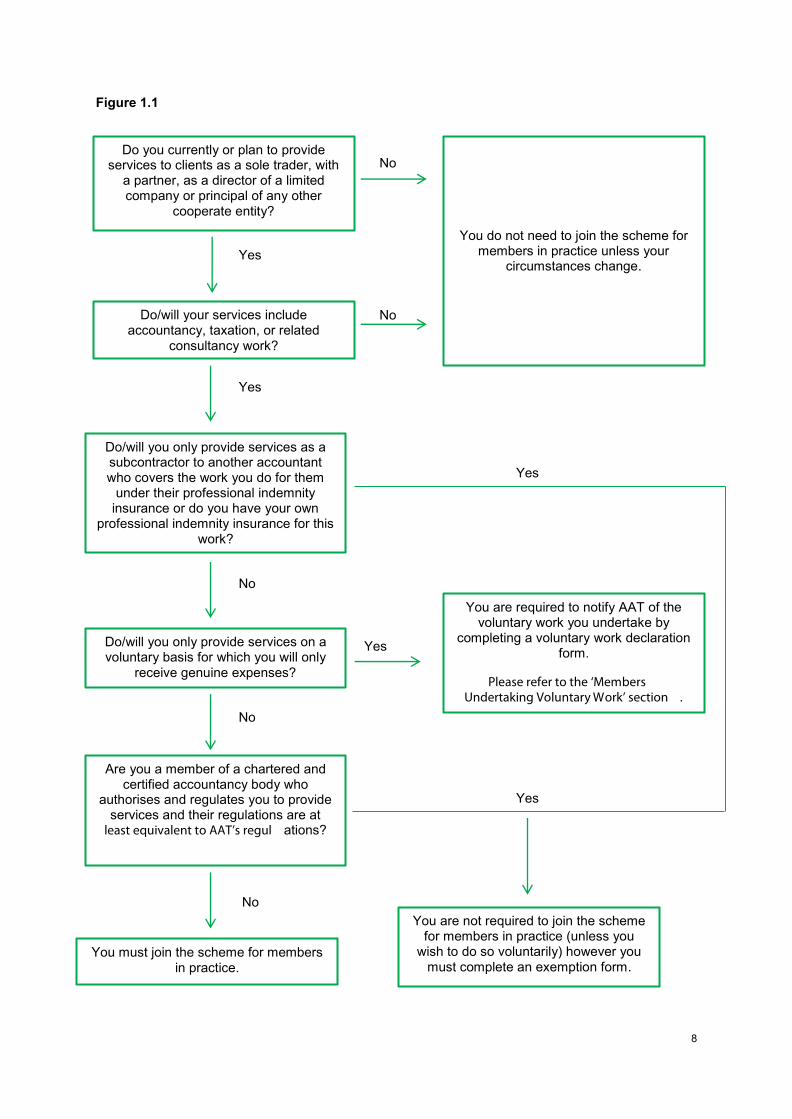

Regulation 1 - Being in practice

For the purpose of these regulations, a member is in practice if they provide services:

(a) as a sole trader

(b) as a partner (whether salaried or equity) in a partnership, including a limited liability partnership*

(c) as a Director, including a shadow Director, of a limited company* (d) as a principal in any other corporate entity*.

*and they hold at least 5% of the shares of that company or entity. Shares belonging to anyone in the member's household or family are treated as belonging to the member.

Guidance to regulation 1

If you are a full or fellow AAT member offering accountancy, taxation or related consultancy services to clients, as a sole trader, in a partnership (including limited liability partnership), as a director of a limited company or principal of any other corporate entity and you live and work in the UK, Channel Islands or Isle of Man, you must join AAT’s scheme for members in practice. If you provide any of the services listed in schedule 1 as a partner in a partnership (whether salaried or equity), a director of a limited company or a principal in any other corporate entity and hold at least 5% of the shares of that partnership, company or entity, then you must join the scheme for members in practice.

To find out which services are covered by the scheme, please refer to the section services covered by the scheme for members in practice and schedule 1 to the regulations. For the purposes of AAT, you are deemed to be in practice if you provide any of the services covered by the scheme regardless of the way you operate.

Joining AAT’s scheme for members in practice will add credibility to the services you offer. It will also demonstrate both to the general public and the accountancy profession, that you are competent, highly trained and committed to maintaining the highest standards of ethics and professionalism. It also enables us to confidently promote your services, credibility and professionalism.

The figure 1.1 will help you to establish whether you need to join the scheme for members in practice.

8

Figure 1.1

Do you currently or plan to provide services to clients as a sole trader, with

a partner, as a director of a limited company or principal of any other

cooperate entity?

Do/will your services include accountancy, taxation, or related

consultancy work?

Do/will you only provide services as a subcontractor to another accountant who covers the work you do for them

under their professional indemnity insurance or do you have your own

professional indemnity insurance for this work?

Do/will you only provide services on a voluntary basis for which you will only

receive genuine expenses?

Are you a member of a chartered and certified accountancy body who

authorises and regulates you to provide services and their regulations are at

least equivalent to AAT’s regul ations?

You must join the scheme for members in practice.

You do not need to join the scheme for members in practice unless your

circumstances change.

You are required to notify AAT of the voluntary work you undertake by

completing a voluntary work declaration form.

Please refer to the ‘Members Undertaking Voluntary Work’ section .

You are not required to join the scheme for members in practice (unless you

wish to do so voluntarily) however you must complete an exemption form.

Yes

Yes

No

No

No

No

No

Yes

Yes

Yes

9

There are member in practice fees which are payable on application and annually thereafter, these are in addition to the annual full or fellow membership subscription. . The fees charged will depend on the annual gross fee income you derive from your practice work (please refer to schedule 3 of the regulations for a definition of gross fee income and how you should calculate it). If AAT is your supervisory authority for the Money Laundering Regulations, a money laundering supervision fee will also be charged. For details of the current fees please refer to aat.org.uk/fees

10

Services covered by the scheme for members in practice

Each of the services are described, to give an indication of what is included in that service area rather than being a prescriptive and exhaustive description of each service. This is in order to assist members and for the purposes of AAT’s scheme for members in practice.

The services covered by the scheme are as follows:

Accountancy

Bookkeeping (BK)

Bookkeeping is that part of accounting which deals with the recording of actual transactions in monetary terms.

This classification only includes recording and not the calculation of actual transactions. For example, the calculations of depreciation, accruals/prepayments and work-in-progress are not included. Effectively, this means the preparation of accounts up to trial balance without any adjustments.

The scope of bookkeeping is limited. Therefore, it is expected that a member who is approved to offer bookkeeping will also be approved to offer Financial Accounting and Accounts Preparation or Management Accounting or both.

Financial Accounting and Accounts Preparation (FA and AP)

Financial Accounting is the preparation of the full and abbreviated accounts that are required for statutory purposes by the prevailing Companies Acts and prepared using the relevant Accounting Standard(s).

Financial Accounts are sometimes referred to as “published accounts” or “annual accounts”.

A member approved to offer Financial Accounting and Accounts Preparation but not approved to offer Limited Assurance Engagement, must not provide any additional assurance of the accuracy of the information included with the financial accounts over and above stating in the accountant’s report that: “these accounts have been prepared based on the information and explanations supplied by the principals/directors/trustees”, or in accordance with prevailing legislation where the accounts prepared are of a statutory nature.

A member approved to offer Financial Accounting and Accounts Preparation but not approved to offer Limited Assurance Engagement can provide information to banks and buildings societies in support of their client’s mortgage or loan application.

11

Note: there are risks when providing information on behalf of a client to a bank/building society and members are advised to take steps to manage these risks. For further assistance please refer to the document titled covering letter to a bank or building society (sample) which is available online from the online MIP Zone.

Budgeting and Forecasting (B and F)

Budgeting includes the preparation of financial reports prepared before the accounting period(s) usually showing planned income, expenditure, capital employed or cash flow.

Forecasting is the prediction of relevant future factors affecting a business and its environment and may be used as the basis for preparing budgets, for example a sales forecast or cash flow forecast.

Management Accounting (MA)

Management Accounting is the preparation of financial reports required by the owner or management team of a business, often on a more frequent basis (for example quarterly, monthly or weekly) than financial accounts.

Some examples of management accounting reports are:

monthly profit and loss statement

monthly sales analysed by product or division

standard costing reports.

Payroll (P)

Payroll includes the calculation (manually or by computer) of net pay of employees by deducting Income Tax, National Insurance and other deductions from the gross pay. In the UK this is often referred to as Pay As You Earn (PAYE).

Independent Examination (IE)

The Charities Act 1993 introduced the concept of an Independent Examination as an alternative to an audit for unincorporated charities whose gross income fell within a specified range. The concept is being extended to include incorporated charities and the specified range is changing (and may be subject to further changes), therefore please refer to the Charity Commission website to establish the accounting and external scrutiny requirements for your charity clients.

For the purposes of these guidelines and regulations and in respect of the Charities Act 1993 section 43(3) (a), reference to “a member of the Association of Accounting Technicians” in the Charities Act is defined as “a licensed member in practice (licensed to carry out Independent Examinations)”. Therefore, only licensed members in practice (licensed to carry out Independent Examinations) are permitted to undertake independent examinations for the larger charities permissible by virtue of AAT’s inclusion in the Charities Act 1993. AAT members who are registered on the scheme for members in practice or are exempt from it are only permitted to act as Independent Examiner for the smaller charities.

12

Limited Assurance Engagement (LAE)

In a Limited Assurance Engagement the accountant expresses an opinion regarding the organisation’s financial accounts which is intended to be relied upon by third parties (thereby creating a duty of care between the accountant and the third party).

AAT members may be able to undertake Limited Assurance Engagements on private sector organisation. However, at the moment AAT members are not allowed to undertake a Limited Assurance engagement on public sector organisations.

It is a mandatory requirement that licensed or registered members in practice undertaking a Limited Assurance Engagement use the following wording in the accountant’s report “... nothing has come to our attention to refute the principals’ confirmation that the financial statements give a true and fair view”. The member is allowed to add additional caveats as they deem necessary to further reduce the level of risk, for example by specifying which third parties can rely on the financial statements.

For the purposes of AAT’s guidelines and regulations, the area of Limited Assurance Engagement specifically excludes Independent Examinations, as it is a separate service area (even though an Independent Examination may be perceived to be a form of assurance engagement).

Forensic Accounting (FoA)

Forensic Accounting is the area of accountancy that results from actual or anticipated disputes, litigation or legal proceedings where the Forensic Accountant is engaged:

to investigate, examine or analyse financial information and relevant non-financial information and inform the client of their findings

where required, to give expert evidence in legal proceedings.

The services of a Forensic Accountant may be required in, for examples, personal injury claims, matrimonial disputes, criminal cases, commercial dispute, insurance claims, professional negligence claims and so on.

As a member in practice offering Forensic Accounting as a service you should ensure that:

you make your Professional Indemnity Insurance provider aware that you are offering this service

your Professional Indemnity Insurance policy covers your work in this area.

Internal Audit (IA)

An organisation (such as a business, charity or public sector organisation) may want to carry out an Internal Audit to assess the effectiveness of management, financial controls and governance processes with a view to improvement. The person(s) who undertakes the Internal Audit may be:

an employee of the organisation (larger organisations may have an Internal Audit department)

a suitably qualified external accountant engaged on a consultancy basis.

The results and report from the Internal Audit are generally used internally by management within the organisation, unlike a statutory audit where the audit report and accompanying financial statements are intended for external users (such as shareholders and investors).

13

Please note that members in practice must use the whole phrase “Internal Audit” and must not drop the word “internal” in order to suggest that they are qualified to undertake “audits”, as this can only be construed as misrepresentation.

Taxation

Value Added Tax (VAT)

VAT is the tax levied on goods and services at the standard rate, reduced rate or zero rate and does not include exempt goods and services.

This classification includes the preparation of VAT returns, dealing with HMRC on behalf of a client, advising what VAT rate should be applied to the goods or services of the business.

A member practising in this area of work can be expected to provide their client with:

an explanation of the principles of VAT

calculations of the VAT to be paid to, or receivable from, HMRC

advice on VAT planning.

Personal Income Tax (PT)

Personal Income Tax is the calculation of an individual’s personal Income tax liability taking into account relevant prevailing legislation and the taxpayer’s income arising from all sources including:

business

earned

savings and investments.

This classification includes the completion of all relevant HMRC returns and will include the calculation of tax credits unless otherwise specified in the letters of engagement.

A member practising in this area of work can be expected to provide their client with:

an explanation of the principles of Income Tax

calculations of their Income Tax due or repayable

advice on the mitigation of Income Tax.

Business Income Tax (BT)

Business Income Tax is the tax liability on the profits/losses of a business, operated either by a sole trader or by partners under Income Tax legislation, as distinct from Corporation Tax.

This classification includes the completion of all relevant HMRC returns.

A member practising in this area of work can be expected to provide their client with:

an explanation of the principles of Business Income Tax

calculations of the Business Income Tax due

advice on Business Tax planning.

14

Corporation Tax (CT)

Corporation Tax is the tax liability arising on the taxable profits of an incorporated business under the prevailing corporate tax legislation.

This classification includes the completion of all relevant HMRC returns.

A member practising in this area of work can be expected to provide their clients with:

an explanation of the principles of Corporation Tax

the calculations of the Corporation Tax due

advice on Corporation Tax planning.

Capital Gains Tax (CGT)

Capital Gains Tax is the tax liability arising on the chargeable gains made by a taxpayer, their business(s) or a corporate entity.

This classification includes the completion of all relevant HMRC returns.

A member practising in this area of work can be expected to provide their clients with:

an explanation of the principles of Capital Gains Tax

calculations of the Capital Gains Tax due

advice on Capital Gains Tax planning.

Inheritance Tax (IHT)

Inheritance Tax is the tax payable either on the advent of a person’s death, or at the time of making a chargeable lifetime transfer.

This classification includes the completion of all relevant HMRC returns.

A member practising in this area of work can expect to provide their client with:

an explanation of the principles of Inheritance Tax

calculations of the Inheritance Tax due

advice on Inheritance Tax planning.

Consultancy

Business Plans (BP)

A member in practice in this area of work might be expected to provide their client with a comprehensive business plan which may be used for the purposes of, for example, obtaining government grants or business finance.

A business plan is a comprehensive report that could contain:

the organisation’s mission statement

a written report summarising the business plan

market research

budgeted expenditure and sales forecasts

15

budgeted profit and loss account

cash flow or funds flow statement.

Computerised Accountancy Systems (CAS)

This area would include a consultant who demonstrates, installs or provides training of accountancy and accountancy related software.

A consultant’s activities could include the set-up, supply and maintenance of:

accountancy software to produce financial or management accounts

payroll software

software for the calculation of a client’s tax liability.

Company Secretarial Services (CSS)

In the context of a member in practice providing company secretarial services the duties may include some of the following examples:

filing Companies House forms and returns

maintaining the register of directors and secretary

issuing share certificates and recording transfers of shares

maintaining the register of members and debenture holders

arranging for charges to be registered and recorded in the register of charges

recording the minutes of board meetings.

16

Regulation 2- Restrictions on being in practice

A member must not provide services unless the member is:

(a) registered on the scheme and acting within the conditions of their registration

(b) a licensed member acting within the conditions of their licence

(c) exempt from the scheme under these regulations and appropriately supervised by a money laundering supervisory authority.

17

Regulation 3 - Exemptions

In exercising discretion, AAT may approve a member to provide services without being registered on the scheme or licensed, if they submit the appropriate application form and supporting evidence, which shows (subject to any dispensation granted by AAT) that:

(a) they provide such services only as a subcontractor to another accountant and hold written confirmation that they are covered by that accountant’s Professional Indemnity Insurance or have provided evidence of their own Professional Indemnity Insurance

(b) they only provide services that have been declared by the Regulation and Compliance Board (whether generally or in a special case) to be outside the scope of these regulations, or

(c) they are a member of a chartered and certified accounting body; and:

(i) that body authorises them to provide services and regulates them in the provision of the services

(ii) such regulation is at least equivalent to AAT’s regulations.

Guidance to Regulation 3 – Exemptions

There are certain circumstances where the scheme for members in practice may not apply to you:

if you are a subcontractor to another accountant and all of the work you do is covered either by your own Professional Indemnity Insurance or the accountant’s Professional Indemnity Insurance

if it has been agreed by the Regulation and Compliance Board that the services you provide are outside the scope of the scheme

If you are a member of chartered and certified accounting body who authorises and regulates you to provide services and their regulations are at least equivalent to AAT’s own scheme.

If you think you may be exempt from the scheme you will need to complete an exemption application form.

18

The scheme for members in practice framework

The scheme for members in practice operates on the basis that its members either have, or are working towards, attaining an AAT practising licence. If, on application, you are able to demonstrate that you meet the licence criteria you will be granted a practising licence straight away. If however, you meet some but not all of the elements of the licence criteria, you can register on the scheme until you are eligible for a licence*. Whilst you are registered on the scheme you will receive support and guidance to help you to attain your licence. All members of the scheme are referred to as AAT members in practice.

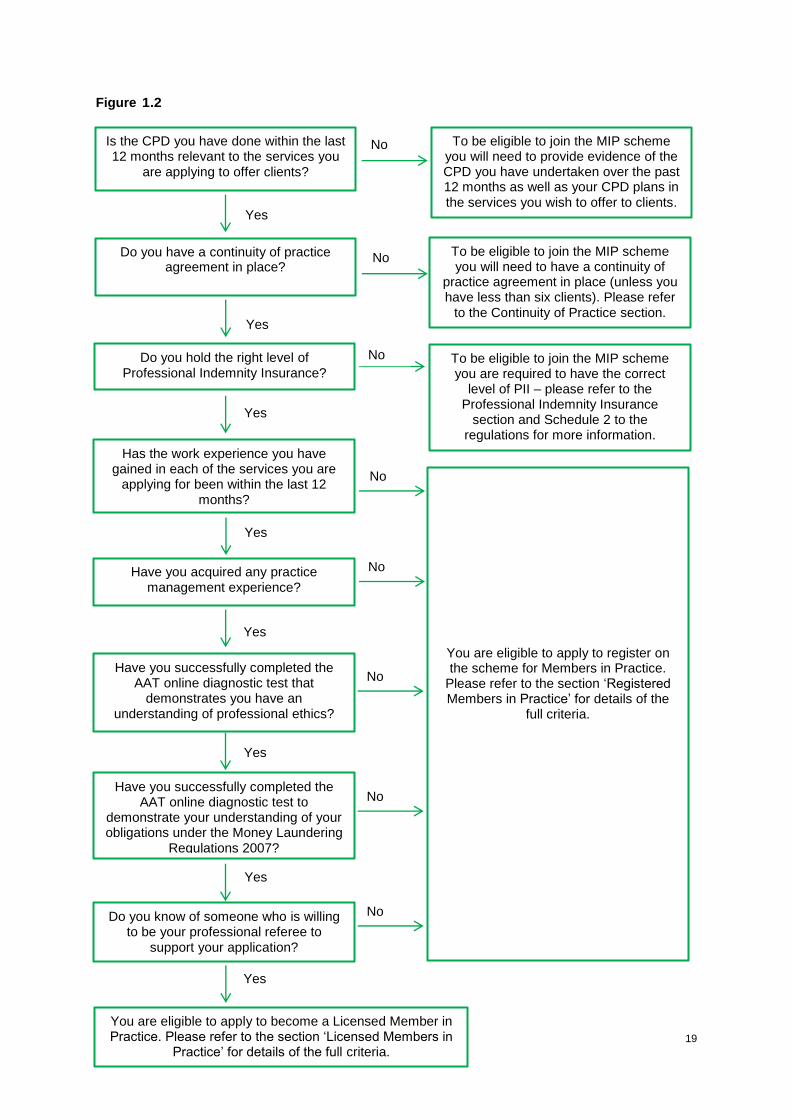

To help you to understand whether you are eligible for a licence or whether you initially need to register on the scheme please refer to the figure 1.2.

*you can be registered on the scheme for members in practice for a maximum of two years after which time you will be required to apply for a licence.

19

Figure 1.2

Is the CPD you have done within the last 12 months relevant to the services you

are applying to offer clients?

Do you have a continuity of practice agreement in place?

Do you hold the right level of Professional Indemnity Insurance?

Has the work experience you have gained in each of the services you are

applying for been within the last 12 months?

Have you acquired any practice management experience?

Have you successfully completed the AAT online diagnostic test that

demonstrates you have an understanding of professional ethics?

Yes

Yes

Yes

Have you successfully completed the AAT online diagnostic test to

demonstrate your understanding of your obligations under the Money Laundering

Regulations 2007?

Yes

Yes

Yes

Yes

Do you know of someone who is willing to be your professional referee to

support your application?

Yes

You are eligible to apply to become a Licensed Member in Practice. Please refer to the section ‘Licensed Members in

Practice’ for details of the full criteria.

To be eligible to join the MIP scheme you will need to provide evidence of the CPD you have undertaken over the past 12 months as well as your CPD plans in the services you wish to offer to clients.

To be eligible to join the MIP scheme you will need to have a continuity of

practice agreement in place (unless you have less than six clients). Please refer

to the Continuity of Practice section.

To be eligible to join the MIP scheme you are required to have the correct

level of PII – please refer to the Professional Indemnity Insurance

section and Schedule 2 to the regulations for more information.

You are eligible to apply to register on the scheme for Members in Practice.

Please refer to the section ‘Registered Members in Practice’ for details of the

full criteria.

No

No

No

No

No

No

No

No

20

Regulations applicable to members registered on the

scheme

Regulation 4 - Registered members in practice

1. AAT may register a member on the scheme for members in practice if the member:

(a) is not ineligible to be registered on the scheme as a result of a decision by the Investigations Team (or Conduct and Compliance acting under delegated powers) or the Disciplinary Tribunal

(b) has complied fully with any order imposed by the Disciplinary Tribunal, Investigations Team (or Conduct & Compliance under delegated powers) or the Appeals Tribunal

(c) is not insolvent (within the definitions detailed in the Insolvency policy) or subject to any unspent criminal conviction, civil sanction, or disciplinary finding of another professional body (within the definitions detailed in the Policy on convictions, civil sanctions and disciplinary findings of other professional bodies)

(d) is not the subject of any criminal investigation or investigation being undertaken by AAT, other regulatory organisation or professional body

(e) has submitted the appropriate application forms

(f) has paid the appropriate fee and is fully paid on the membership subscription account

(g) has paid the appropriate AAT money laundering supervision fee, if applicable

(h) has provided evidence of Professional Indemnity Insurance cover that meets with schedule 2 to these regulations

(i) has a Continuity of Practice Agreement in place in the event of illness or prolonged absence from work or is exempt from this requirement, as detailed in the guidance

(j) has satisfied the CPD requirements within the meaning of Regulation 18 within these Regulations in all the self- employed services that he wishes to offer

(k) has demonstrated that he has gained work experience in all the self-employed services that he wishes to offer.

2. In the exercise of its discretion under regulation 4(1) above and thereafter during the period of a member's registration AAT may:

(a) approve the member to offer some or all of the services listed in paragraph 1 of schedule 1 to these regulations, and/or

(b) impose any condition, requirement or restriction on the member’s practising licence or registration and/or

(c) revoke the member’s registration.

Guidance to regulation 4 – application process for registered status

(a) Application process

To apply to register on the scheme for members in practice you will need to:

complete an application form which will require you to give details about your business, for example the business name and address, the number and type of clients you have and the services you currently offer or wish to offer in the future. The application form includes a section on the Money Laundering Regulations 2007, the information in this section will be used to determine whether you are eligible for supervision by AAT for compliance with the

21

money laundering legislation (please refer to Regulation 19 to find out more about money laundering supervision)

provide details of relevant work experience and qualifications you have gained in the services you wish to offer (as detailed in schedule 1). This information will be assessed to determine whether you have adequate and appropriate knowledge and experience to offer the services to clients. To apply to offer Limited Assurance Engagements you will need to submit additional information, as outlined in the guidance to regulation 23 Limited Assurance Engagements

provide continuing professional development (CPD) records for the 12 month period prior to your application as well as your CPD plans for the forthcoming year. Your CPD records and plans should reflect the services you wish to offer. For further details please refer to the Regulation 18

provide a copy of your Professional Indemnity Insurance (PII) cover note. For further details about PII please refer to the Professional Indemnity Insurance section and schedule 2 to the regulations

provide details of the person(s) you have nominated in your Continuity of Practice Agreement. If you have six or fewer clients you can apply for exemption from this requirement. Please refer to the Continuity of Practice section for further details

pay the appropriate member in practice and money laundering fees, details of which can be found at aat.org.uk/fees These are payable in addition to your membership subscription. Your full membership subscription account must be in balance before your application can be approved

submit your completed application form, supporting documents and fees to the Members in practice team for processing. It usually takes between four and eight weeks to fully process an application; however this varies from case to case. It is quite usual for the Members in practice team to contact you if they need any clarification or further information in support of your application.

(b) What happens next?

Once your application has been approved and you have paid the appropriate fees you will receive a letter to confirm your registration on the scheme for members in practice. Your approval letter will outline all the services that you have been approved to offer. We will also confirm whether AAT will be your money laundering supervisory authority (if you are not eligible for AAT supervision we will refund the money laundering fee).

Your initial registration will be valid for between 11 and 12 months depending on when your application is approved. Your approval letter will include details of your registration expiry date.

We will contact you prior to your registration expiry date with details about how to renew your registration or apply for a licence. Please refer to the Regulation 10 for further details about the renewal process.

22

Regulation 5 - Conditions of members registered on the scheme

1. A member registered on the scheme for members in practice must comply with the following conditions. The member must:

(a) only provide the services endorsed on their confirmation of registration letter or such other areas as AAT may decide

(b) apply for a member in practice licence within two calendar years of being approved as a registered member in practice starting from the date endorsed on his confirmation of registration letter

(c) have complied fully with any order imposed by the Disciplinary Tribunal, Investigations Team (or Conduct & Compliance under delegated powers) or the Appeals Tribunal

(d) not be insolvent (within the definitions detailed in the Insolvency policy) or subject to any unspent criminal conviction, civil sanction, or disciplinary finding of another professional body (within the definitions detailed in the Policy on convictions, civil sanctions and disciplinary findings of other professional bodies)

(e) not be the subject of any criminal investigation or investigation being undertaken by AAT, other regulatory organisation or professional body

(f) not represent themselves as a licensed member in practice

(g) not use AAT logo or crest on their business stationery or at all, but he may use specific wording which has been approved by AAT

(h) comply with any condition, requirement or restriction imposed on their registration on the scheme by AAT, including any conditions to be met in order to apply for a licence

(i) maintain adequate and appropriate knowledge and experience in the services they provide

(j) not use AAT designatory letters after or in conjunction with the name of their business

(k) comply with AAT policy on CPD for members in practice from time to time in force

(l) maintain Professional Indemnity Insurance cover that meets with schedule 2 of these regulations

(m) have adequate and appropriate Continuity of Practice Agreement in place in the event of illness or prolonged absence from work or must be exempt from this requirement, as detailed in the guidance

(n) comply with the money laundering legislation, AAT guidance on money laundering and procedures in force at the relevant time;

(o) comply with the provisions of AAT’s Code of Professional Ethics; and

(p) cooperate fully with AAT practice assurance activity including, but not limited to submission of practice information, telephone reviews, and/or on site visits

(q) during the period of registration, immediately disclose to AAT any matter which could lead to a breach of any condition of Regulation 5(1).

Guidance to regulation 5 – conditions of registration

You can remain registered on the scheme for members in practice for a maximum of two years, after which time you will be required to apply for a licence. If you do not meet the licence criteria within two years of registering on the scheme you will not be permitted to continue to practice under AAT’s scheme. If you continue to practice you may face disciplinary action for practising without a licence. There are other conditions which you must adhere to whilst registered on the scheme, outlined within the regulation above. Please refer to the continuing professional development, Professional Indemnity Insurance, continuity of practice, money laundering and Powers of review sections for further information.

Members registered on the scheme for members in practice are permitted to refer to their registered

23

status for advertising purposes; this does not include use of AAT logo. For details of the wording please refer to the online MIP zone.

Applying for a licence

You can apply for a practising licence at any time; you do not have to wait until your registration is due for renewal. To check that you meet the criteria to be eligible for a licence please refer to the flow chart, anti money laundering and professional ethics diagnostic tests and practice management sections. To apply for a practising licence you will need to:

complete an application form which will require you to confirm you have met all the elements of the licence criteria

submit evidence of your relevant work experience in any areas you did not have 12 months of work experience in when you initially joined the scheme

submit your CPD records for the previous six months (you do not need to submit CPD records if your initial application to join the scheme was less than six months ago however we reserve the right to request your CPD records at any time)

submit a copy of your Professional Indemnity Insurance policy if your policy expired since your initial application to join the scheme.

Once your application has been approved we will send you an approval pack which includes a licence certificate detailing the services you are licensed to offer. You will keep the same renewal date as when you first joined the scheme as a registered member. We will contact you prior to your licence expiry date with details about how to renew your licence.

Benefits for registered members in practice

In addition to the general full and fellow membership services and benefits, when you register on the scheme you will have additional recognition and access to the following services and support.

Support and benefits

Free unlimited access to CCH Online – an online resource covering a wide range of topics including accountancy, taxation and companies legislation.

Access to the CCH business support helpline giving advice in taxation, VAT, payroll, employment and personnel, health and safety and Commercial Law. A voucher code must be purchased to access the helpline, for details visit aat.org.uk/technicalhelp

Access to the AAT Practice Management Toolkit for resources tailored to running a practice including sample letters and contracts

A monthly e-newsletter The Professional containing useful updates and information for members in practice.

An online forum, designed to further support networking and the sharing of advice and experience throughout the community of members in practice, visit forums.

CPD events arranged exclusively for AAT members in practice.

A list of PII providers, special PII rates and a fixed premium policy for members who undertake a small amount of work for clients, please refer to aat.org.uk/pii for further details.

Use of wording agreed by AAT to refer to your registration on the scheme, visit the online MIP Zone for details.

An online directory of members in practice designed to support networking and business opportunities. Inclusion in the directory is optional.

Recognition

Increased publicity by AAT to raise the profile of AAT members in practice. For

example successful publicity campaigns with articles focusing on the value accounting

24

technicians can bring to small business success.

AAT enhances the reputation of members in practice through its responding to consultation documents and, in doing so, promoting the suitability of AAT members in practice to provide a wide range of accountancy related services.

Over 106 mortgage lenders currently recognise accounts prepared by AAT members in practice to support intended borrowers’ mortgage loan applications (some lenders only recognise licensed members in practice). An up to date list of the current lenders can be found in the online MIP zone.

AAT further enhances the reputation of members in practice through its active involvement with the HM Revenue and Customs forum, known as Working Together, whose purpose is to establish a better working tax system within the UK at an operational level.

25

Regulations applicable to licensed members in practice

Regulation 6 - Licensed members in practice

1. AAT may licence a member on the scheme for members in practice if the member:

(a) is not ineligible to hold a practicing licence a result of a decision by the Investigations Team (or Conduct and Compliance acting under delegated powers) or the Disciplinary Tribunal

(b) has complied fully with any order imposed by the Disciplinary Tribunal, Investigations Team (or Conduct & Compliance under delegated powers) or the Appeals Tribunal

(c) is not insolvent (within the definitions detailed in the Insolvency policy) or subject to any unspent criminal conviction, civil sanction, or disciplinary finding of another professional body (within the definitions detailed in the Policy on convictions, civil sanctions and disciplinary findings of other professional bodies)

(d) is not the subject of any criminal investigation or investigation being undertaken by AAT, other regulatory organisation or professional body

(e) has submitted the appropriate application forms

(f) has paid the appropriate fee and is fully paid on their membership subscription account

(g) has paid the appropriate AAT money laundering supervision fee, if applicable

(h) has provided evidence of professional indemnity insurance cover that meets schedule 2 to these regulations

(i) has a Continuity of Practice Agreement in place in the event of illness or prolonged absence from work or is exempt from this requirement, as detailed in the guidance

(j) has demonstrated that they have gained work experience within the last 12 months covering the services they wish to be licensed in

(k) has demonstrated evidence of practice management skills as detailed in the guidance

(l) has demonstrated to the satisfaction of AAT, evidence of their understanding of professional ethics and anti money laundering. This includes being required to undertake an assessment of their understanding of both areas as outlined in the accompanying guidance

(m) has demonstrated adequate and appropriate CPD in all the self-employed services that they wish to offer.

2. In the exercise of its discretion under regulation 6 (1) above and thereafter during the period of a member's licence, AAT may:

(a) approve the member to offer some or all of the services listed in paragraph 1 of schedule 1 to these regulations, and/or

(b) impose any condition, requirement or restriction on the member’s practising licence or registration and/or

(c) revert a member's practising licence to registration on the scheme in accordance with regulation 11(3) and/or

(d) revoke the member’s practicing licence.

Guidance to regulation 6 – application process for licensed status

(a) Application process

To apply to be licensed on the scheme for members in practice you will need to:

complete an application form which will require you to give details about your business, for example the business name and address, the number and type of clients you have and the services you currently offer or wish to offer in the future. The application form includes a

26

section on the Money Laundering Regulations 2007, the information in this section will be used to determine whether you are eligible for supervision by AAT for compliance with the money laundering legislation (please refer to Regulation 19 to find out more about money laundering supervision)

provide details of relevant work experience and qualifications you have gained in the services you wish to offer (as detailed in schedule 1). This information will be assessed to determine whether you have adequate and appropriate knowledge and experience to offer the services to clients. To apply to offer Limited Assurance Engagements you will need to submit additional information, as outlined in the guidance to regulation 23 Limited Assurance Engagements.

provide continuing professional development (CPD) records for the 12 month period prior to your application as well as your CPD plans for the forthcoming year. Your CPD records and plans should reflect the services you wish to offer. For further details please refer to the Regulation 18.

provide a copy of your Professional Indemnity Insurance (PII) cover note. For further details about PII please refer to the Professional Indemnity Insurance section and schedule 2 to the regulations

provide details of the person(s) you have nominated in your Continuity of Practice Agreement. If you have six or fewer clients you can apply for exemption from this requirement. Please refer to the Continuity of Practice section

provide a statement of suitability from a professional referee

provide evidence of practical experience and/or CPD in practice management.

Please refer to the Practice Management section for further information

provide evidence that you have successfully completed the AAT anti money laundering diagnostic test

provide evidence that you have successfully completed the AAT Professional Ethics diagnostic test

pay the appropriate members in practice and money laundering fees. These are payable in addition to your membership subscription. Your full membership subscription account must be in balance before your application can be approved

submit your completed application form, supporting documents and fees to the Members in practice team for processing. It usually takes four to eight weeks to fully process an application; however this varies from case to case. It is quite normal for the Members in practice team to contact you if they need any clarification or further information in support of your application.

(b) Professional referee

As part of the licence application process you are required to provide details of a professional referee who has first-hand knowledge of your work (either in an employed or self-employed capacity) and is able to vouch for your professional conduct. Your professional referee will be required to provide a statement on your professional attributes which in his/her view makes you suitable for a practicing licence with AAT.

Your professional referee:

will need to have known you in a professional capacity for at least six months and within the last six months

cannot be a family member (unless they are an AAT member in practice or member of one of the chartered and certified accountancy bodies)

can be the same person who provides continuity cover

can be a mentor

can be a client.

(c) What happens next?

Once your application has been approved and you have paid the appropriate fees we will send you an approval pack which includes a licence certificate detailing the services you are licensed to offer. We

27

will also confirm whether AAT will be your money laundering supervisory authority (if you are not eligible for AAT supervision we will refund the money laundering fee). Your initial licence will be valid for between 11 and 12 months depending on when your application is approved. Your approval letter will include details of your licence expiry date. We will contact you prior to your licence expiry date with details about how to renew. Please refer to the Regulation 10 for further details about the renewal process.

28

Regulation 7 - Conditions of a practising licence

1. A member licensed on the scheme for members in practice must comply with the following conditions. The member must:

(a) only provide the services endorsed on their practising licence or such other areas as AAT may decide

(b) maintain adequate and appropriate knowledge and experience in the services they provide

(c) have complied fully with any order imposed by the Disciplinary Tribunal, Investigations Team (or Conduct & Compliance under delegated powers) or the Appeals Tribunal

(d) not be insolvent (within the definitions detailed in the Insolvency policy) or subject to any unspent criminal conviction, civil sanction, or disciplinary finding of another professional body (within the definitions detailed in the Policy on convictions, civil sanctions and disciplinary findings of other professional bodies)

(e) not be the subject of any criminal investigation or investigation being undertaken by AAT, other regulatory organisation or professional body

(f) not use AAT crest on their business stationery or at all, but may use AAT logo with specific wording following AAT brand guidelines for licensed members in practice

(g) use specific wording if the member's business stationery refers to their practising licence. Details of the wording can be found in the online MIP Zone

(h) not use AAT designatory letters after or in conjunction with the name of their business

(i) comply with AAT policy on CPD for members in practice from time to time in force

(j) maintain Professional Indemnity Insurance cover that meets the requirements of schedule 2 to these regulations

(k) have an adequate and appropriate Continuity of Practice Agreement in place in the event of illness or prolonged absence from work or must be exempt from this requirement, as detailed in the guidance

(l) comply with the money laundering legislation, AAT guidance on money laundering and procedures in force at the relevant time

(m) comply with the provisions of AAT Code of Professional Ethics

(n) cooperate fully with any AAT practice review

(o) comply with any condition, requirement, modification or restriction imposed on their practicing licence by AAT

(p) during the course of a period of a practising licence, immediately disclose to AAT any matter which could lead to a breach of any condition of Regulation 7(1).

Guidance to regulation 7 – conditions of a practising licence

There are other conditions which you must adhere to whilst registered on the scheme, outlined within the regulation above. Please refer to the continuing professional development, Professional Indemnity Insurance, continuity of practice, money laundering and Powers of review sections for further information.

Licensed members are permitted to use the AAT logo and specific wording for advertising and promotional purposes. For details of the wording you must use and the format of the logo please refer to the online MIP zone.

Benefits for licensed members in practice

In addition to the full and fellow membership services and benefits, as a licensed member in practice you will have additional recognition and access to the following services and support.

29

Support and benefits

*A licence certificate to display at your business address.

*Use of the AAT logo and wording on your business stationery.

Free unlimited access to CCH Online – an online resource covering a wide range of topics including accountancy, taxation and companies legislation.

Access to the AAT Practice Management Toolkit with resources tailored to running a practice including sample letters and contracts.

A monthly e-newsletter The Professional containing useful updates and information for members in practice.

Access to the CCH business support helpline giving advice in taxation, VAT, payroll, employment and personnel, health and safety and Commercial Law. A voucher code must be purchased to access the helpline, for details visit aat.org.uk/technicalhelp

An online directory of members in practice designed to support networking and business opportunities. Inclusion in the directory is optional.

An online forum, designed to further support networking and the sharing of advice and experience throughout the community of members in practice, visit forums forums.aat.org.uk

CPD events arranged exclusively for AAT members in practice.

A list of PII providers, special PII rates and a fixed premium policy for members who undertake a small amount of work for clients, for more information visit aat.org.uk/pii

*Benefits for licensed members only, those registered on the scheme cannot take advantage of these.

Recognition

Over 106 mortgage lenders currently recognise accounts prepared by AAT licensed members in practice to support intended borrowers mortgage loan applications. An up to date list of the current lenders can be found in the online MIP zone.

The Department for Transport has agreed AAT licensed members in practice are authorised to sign off the Bus Service Operators Grants (previously known as the Fuel Duty Rebate Claims)

Increased publicity by AAT to raise the profile of AAT members in practice. For example successful publicity campaigns with articles focussing on the value accounting technicians can bring to small business success.

AAT enhances the reputation of members in practice through its responding to consultation documents and, in doing so, promoting the suitability of AAT members in practice to provide a wide range of accountancy related services.

AAT further enhances the reputation of members in practice through its active involvement with the HM Revenue and Customs forum, known as Working Together, whose purpose is to establish a better working tax system within the UK at an operational level.

30

Professional Indemnity Insurance (PII)

PII is a mandatory requirement for all members in practice. The level of cover you need depends on the total gross fee income (net of VAT) of your business and your business type. For details of the level of cover you must have please see schedule 2 to the regulations. Whilst AAT specifies a minimum level of cover you are required to have, you are strongly advised to undertake a risk assessment to determine a level of PII which is adequate for your practice. A risk assessment should take into account the type of clients you have and the type of work you undertake. For further information on carrying out a risk assessment and calculating an appropriate level of PII please refer to aat.org.uk/pii

It is your responsibility to arrange your own PII cover. For a list of some companies that provide PII please see our providers list at aat.org.uk/pii

If you carry out a small amount of work for clients you may be eligible to apply for the low turnover policy which will give you the minimum amount of PII cover required by AAT’s regulations. Details of the low turnover policy will be sent to you with your members in practice application form. Alternatively visit aat.org.uk/pii or contact the Members in practice team.

If you cease working in practice it is strongly recommended that you maintain your PII for a minimum period of six years after you have ceased your business. It should be noted that PII policies are usually provided on a claims-made basis which means you may not be covered where a claim is made against you after your PII has expired for work you have undertaken before your PII lapsed.

31

Continuity of Practice Agreement

As a registered or licensed member in practice you have a professional obligation to your clients to ensure that your practice operates effectively and can continue to operate if you are absent from your work for any length of time, such as in the case of serious illness. It is for this reason that a Continuity of Practice Agreement is a mandatory requirement for all AAT members in practice with more than six clients.

If you are in practice with a fellow director or partner, they may provide the continuity of cover, as could a suitably qualified existing employee engaged within your business. However, where you work alone you will need to arrange for an appropriately experienced individual to provide continuity of cover to ensure your practice continues to operate effectively in your absence. The individual providing cover will need to have sufficient experience and expertise. In addition, their procedures, fee structure and type of services provided will need to be compatible.

It is important that the person you nominate is in full agreement to this arrangement and understands their obligations in the event of their being called upon to undertake some or all of the work for which you are approved, on your behalf. It is vital that your alternate is independent of your clients and capable of operating without conflict of interest.

If you are a sole trader with six or fewer clients it may not be necessary for you to have a Continuity of Practice Agreement in place. However, you should ensure that:

your clients are aware, understand and agree to this

this agreement and decision is documented by both parties in a letter of engagement or other appropriate communication.

if you have six or fewer clients and do not have a Continuity of Practice Agreement in place you must complete a declaration form.

If you need help finding an appropriate individual to take on this role, you may wish to:

search our directory of members in practice

post a note on the members in practice discussion forum.

32

Practice management

As a licensed or registered member in practice you are required to ensure that you assess your CPD needs in practice management. If you are a registered member in practice you will be required to submit evidence of your practical experience in practice management and/or evidence of any CPD you have undertaken in this area as this will be required when you apply for a licence (CPD in practice management will also be required to renew your registration). If you are a licensed member in practice you will need to demonstrate that you have assessed your CPD needs in practice management when asked to submit your records as part of the CPD monitoring process (this is in addition to assessing your needs in your approved licence services).

AAT has developed a Practice Management Toolkit covering some of the areas we consider to be important to running a practice, whether this is on a small or large scale. Some elements of practice management are also covered regulations 22, 24 and 25. Whilst the toolkit is not an exhaustive list of all aspects of practice management and not all aspects may be relevant to you we strongly recommend that you refer to it for guidance. There are eight aspects of practice management covered by the toolkit, some of the content is listed below.

Legal and regulation - Data Protection Act 1998, Provision of Services Regulations 2009, Money Laundering Regulations 2007 and POCA 2002, health and safety, Equality Act 2010

Staff appraisal and development – managing staff recruitment process, identifying learning and development needs for staff, conducting employee appraisals, employee relations

Client money - handling client monies, operating a client’s bank account.

Quality assurance - helping you prepare for AAT review visits, complaints management, Professional Indemnity Insurance.

Practice promotion and marketing – guidance on how to promote and market your practice ethically.

Conduct of work - client engagement and disengagement procedures, letters of engagement, fees and commission, quality control of client work (covering file management, file review, supervision), managing workload, ownership of books and records.

Strategic planning - business plans, self-employed guide, corporate social responsibility.

IT risks - IT procedures and security, data retention and destruction.

33

Anti money laundering and professional ethics diagnostic tests

AAT has developed two online diagnostic tests which all members in practice can use to help them gain an understanding of the Money Laundering Legislation and professional ethics. The tests are tools that aid in the understanding of these areas, and identify any gaps in knowledge. They are not formal assessments. To be eligible for a practising licence you will be required to submit evidence with your licence application that you have successfully completed both tests (an email confirmation and certificate will be available to print). To be successful you will need to achieve the pass rate of 71%. We encourage all members in practice to use the tests as learning tools to form part of your CPD.

34

Members in practice with gross fee income below £1,000

If you earn below £1,000 from the services you offer to clients you are required to join the scheme for members in practice. However, in recognition of the amount of work you undertake AAT will be your supervisory authority for compliance with the Money Laundering Regulations free of charge. Please refer to the guidance for regulation 4 and regulation 6 for details on how to apply to join the scheme.

35

Regulations applicable to members undertaking voluntary work

Regulation 8 - Conditions of members undertaking voluntary work

A member undertaking voluntary work must comply with the following conditions. The member must:

(a) notify AAT that they are undertaking voluntary work, along with the details of the services being provided, by completing the appropriate forms

(b) submit updated information on the appropriate forms before the expiry of one calendar year after the provision of the information detailed in sub-paragraph (a) of this regulation. The member shall continue to provide that information on the appropriate forms annually, such information being provided before the expiry of one calendar year from the date of the last occasion, upon which they provided such information, until such time as they inform AAT in writing that they are no longer conducting voluntary work

(c) only provide the services that they have appropriate knowledge and experience of

(d) maintain adequate and appropriate knowledge and experience in the services they provide

(e) only provide services on a voluntary unpaid basis and must not earn any remuneration from their work except reimbursement of reasonable expenses. The member must not represent themselves as a licensed or registered member in practice

(f) comply with AAT policy on CPD for members from time to time in force

(g) advise clients whether they hold Professional Indemnity Insurance cover at the outset of any engagement..

(h) comply by the provisions of AAT Code of Professional Ethics.

Guidance to regulation 8 – members undertaking voluntary work

If you are undertaking work for clients on a voluntary basis and are only reimbursed genuine out of pocket expenses you are required to notify AAT. You are required to complete a voluntary work declaration form giving details of the service/s you provide on a voluntary basis, the number of clients you volunteer services to and the number of hours of voluntary work you undertake each month. You will be asked to renew this information every year to confirm that you are still undertaking work on this basis.

As a member undertaking voluntary work you are required to abide by regulation 8, please refer to this section to ensure that you are compliant. You should also ensure your CPD records reflect the voluntary work you undertake, please refer to Regulation 18 for further details about CPD. As you are not required to join the scheme you will not be given access to the benefits package that registered and licensed members enjoy however if you do wish to have access to the benefits package you can apply to join the scheme.

36

Regulations applicable to all members in practice

Regulation 9 - Extension of approved services

A registered or licensed member may apply in writing at any time to vary or extend the services he is approved to offer. AAT may grant the application if the member:

(a) has demonstrated adequate and appropriate knowledge and experience in relation to such variation or extension

(b) in the opinion of AAT, there is no other reason for such a variation or extension not to be granted.

Guidance to regulation 9 – Extension of approved services

If you would like to apply to add a service area to your licence or registration you may do so at any time, you do not need to wait until your renewal is due. To add a service you will need to submit details of the CPD and work experience you have gained in the service/s you wish to add and send this to the Members in practice team. Once this has been approved we will issue you with a new licence or letter of registration with the additional service/s added.

37

Regulation 10- Renewal of practising licences or

registration on the scheme for members in practice

1. A practising licence or registration on the scheme will start on the day it is issued or endorsed on