Doss Rebuttal Exhibit I Accounting Standard

29

Doss Rebuttal Exhibit 1 E-7, Sub 1214 Doss Rebuttal Exhibit I Accounting Standard Codification 410-20

Transcript of Doss Rebuttal Exhibit I Accounting Standard

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Doss Rebuttal Exhibit I

Accounting Standard Codification 410-20

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page I of28

Table of Contents

1. 410-20-00 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations > 00 Status 2 . 410-20-05 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations > 05 Overview and Background 3 410-20-15 41 0 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations > 15 Scope and Scope Exceptions 4 . 410-20-20 410 Asset Retirement and Environmental Obl1gat1ons > 20 Asset Retirement Obligations > 20 Glossary 5 410-20-25 41 0 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations > 25 Recognition 6 . 410-20-30 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obhgallons > 30 Initial Measurement 7. 410-20-35 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligallons > 35 Subsequent Measurement 8 410-20-40 410 Asset Retirement and Environmental Obhgat1ons > 20 Asset Retirement Obligations > 40 Derecognitron 9 410-20-45 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations> 45 Other Presentation Matters 10 410-20-50 410 Asset Retirement and Environmental Obhgatrons > 20 Asset Retirement Obligations > 50 Disclosure 11. 410-20-55 410 Asset Retirement and Environmental Obligations > 20 Asset Retirement Obligations > 55 Implementation Guidance and Illustrations 12 410-20-60 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations> 60 Relat1onsh1ps 13 410-20-75 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations> 75 XBRL Elements

410-20-00 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 00 Status

General Subsection revised 01-0ct-2012

Combine Subsections

00-1 The following table identifies the changes made to this Subtopic.

Paragraph Action Accounting Standards Update Date

Fair Value (3rd def.) Added Accounting Standards Update No 2012-04 10/01/2012

410-20-55-27 Amended Accounting Standards Update No 2012-04 10/01/2012

410-20-55-66 Amended Accounting Standards Update No 2012-04 10/01/2012

Table Of Contents

410-20-05 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 05 Overview and Background

General Subsection revised 01-Jul-2009

Combine Subsections

http://www.pwccomperio.com/JASDocViewer.aspx?Topicc-4) 0&SubTopic=20&docid=4 l ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 2 of28

05-1 This Subtopic establishes accounting standards for recognition and measurement of a liability for an asset retirement obligation and the associated asset retirement cost. This Subtopic also addresses the accounting for an environmental remediation liability that results from the normal operation of a long-lived asset.

05-2 Paragraph Not Used

Table Of Contents

410-20-15 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 15 Scope and Scope Exceptions

General Subsection revised 01.Jul-2009

Combine Subsections

> Entities

15-1 The guidance in this Subtopic applies to all entities, including rate-regulated entities that meet the criteria for application of Subtopic 980-10, as provided in paragraph 980, 10·15-2. Paragraphs 980-340•25·1 and 980--405-25-1 provide specific conditions that must be met to recognize a regulatory asset and a regulatory liability, respectively. (See paragraphs 410-20-55-1 through 55-12 and 410-20-55-21 through 55-22 for implementation guidance)

> Transactions

15-2 The guidance in this Subtopic applies to the following transactions and activities;

a. Legal obhgallons associated with the rehrementof a tangible long-lived asset that result from the acquisition, construction, or development and (or) the normal operation of a long-lived asset, including any legal obligations that require disposal of a replaced part that is a component of a tangible long-lived asset.

b. An environmental remediation liability that results from the normal operation of a long-lived asset and that is associated with the retirement of that asset. The fact that partial settlement of an obligation rs required or performed before full retirement of an asset does not remove that obligation from the scope of this Subtopic. If environmental contamination is incurred in the normal operation of a long-lived asset and is associated with the retirement of that asset, then this Subtopic will apply (and Subtopic 410-30 will not apply) if the entity is legally obligated to treat the contamination.

c. A conditional obligation to perform a retirement activity. Uncertainty about the timing of settlement of the asset retirement obhgat on does not remove that obligation from the scope of this Subtopic but will affect the measurement of a liability for that obligation (see paragraph 410-20-25-10).

d. Obligations of a lessor in connection with leased property that meet the provisions in (a). Paragraph 840-10-25-16 requires that lease classification tests performed in accordance with the requirements of Subtopic 840-10 incorporate the requirements of this Subtopic to the extent applicable.

e. The costs associated with the retirement of a specified asset that qualifies as historical waste equipment as defined by EU Directive 2002/96/EC. (See paragraphs 410-20-55-23 through 55-30 and Example 4 [paragraph 410-20-55-63) for illustration of this guidance.) Paragraph 410-20-55-24 explains how the Directive distinguishes between new and historical waste and provides related implementation guidance.

15-3 The guidance in thts Subtopic does not apply to the following transactions and activities:

a. Obligations that arise solely from a plan to sell or otherwise dispose of a long-lived asset covered by Subtopic 360-10.

b. An environmental remediation liability that results from the improper operation of a long-lived asset (see Subtopic 410-30). Obligations resulting from improper operations do not represent costs that are an integral part of the tangible long-lived asset and therefore should not be accounted for as part of the cost basis of the asset For example, a certain amount of spillage may be inherent in the normal operations of a fuel storage facility, but a

http://www.pwccomperio.com/JASDoc Viewer.aspx?Topic=41 0&SubTopic~20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 3 of28

catastrophic accident caused by noncompliance with an entity's safety procedures is not. The obligation to clean up the spillage resulting from the normal operation of the fuel storage facility is within the scope of this Subtopic. The obligation to clean up after the catastrophlc accident results from the improper use of the facility and is not within the scope of this Subtopic.

c Activittes necessary to prepare an asset for an alternative use as they are not associated with the retirement of the asset.

d . Historical waste held by private households. (The guidance in this paragraph does not pertain to an asset retirement obligation in the scope of thls Subtopic.) For guidance on accounting for historical electronic equipment waste held by private households for obligations associated with Directive 2002/96/EC on Waste Electrical and Electronic Equipment adopted by the European Union, see Subtopic 720-40.

e. Obligatrons of a lessee in connection with teased property, whether imposed by a lease agreement or by a party other than the lessor, that meet the definition of either minimum lease payments or contingent rentals in paragraphs 840-10-25-4 through 25-7. Those obligations shall be accounted for by the lessee in accordance with the requirements of Subtop[c 840-10. However, if obligations of a lessee in connection with leased property, whether imposed by a lease agreement or by a party other than the lessor, meet the provisions in paragraph 410-20-15-2 but do not meet the defin[tfon of either minfmum lease payments or contingent rentals in paragraphs 840-10-25-4 through 25-7, those obligations shall be accounted for by the lessee in accordance with the requirements of this Subtopic.

f . An obfigation for asbestos removal that results from the other-than-normal operation of an asset. Such an obligation may be subject to the provlslons of Subtopic 410-30.

g . Costs associated with complying with funding or assurance provisions. Paragraph 410-20-35-9 otherwise addresses the measurement effects of funding and assurance provisions.

h. Obligations associated with maintenance, rather than retirement, of a long-lived asset.

i The cost of a replacement part that is a component of a long-lived asset.

Table Of Contents

410-20-20 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 20 Glossary

Accretion Expense

An amount recognized as an expense classified as an operating item in the statement of income resulting from the increase in the carrying amount of the liability associated with the asset retirement obligation.

Asset Retirement Cost

The amount capitalized that increases the carrying amount of the long-lived asset when a liability for an asset retirement obligation is recognized.

Asset Retirement Obligation

An obligation associated with the retirement of a tangible long-lived asset.

Conditional Asset Retirement Obligation

A legal obligation to perform an asset retirement activity in wh[ch the timing and (or) method of settlement are conditional on a future event that may or may not be within the control of the entity.

Legal Obligation

An obligation that a party is required to settle as a result of an existing or enacted law, statute, ordinance, or written or oral contract or by legal construction of a contract under the doctrine of promissory estoppel.

http://www.pwccomperio.com/ J AS Doc Viewer .aspx?Topic::41 O&S ub Topic=20&doc id=4 l . .. 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 4 of28

Promissory Estoppel

"The principle that a promise made without consideration may nonetheless be enforced to prevent injustice if the promisor should have reasonably expected the promisee to rely on the promise and if the promisee did actually rely on the promise to his or her detriment." (See Black's Law Dictionary, seventh edition.)

Retirement

The other-than-temporary removal of a long-lived asset from service. That term encompasses sale, abandonment. recycling, or disposal in some other manner. However, it does not encompass the temporary idling of a long-lived asset. After an entity retires an asset, that asset is no longer under the control of that entity, no longer in existence, or no longer capable of being used in the manner for which the asset was originally acquired, constructed, or developed.

Closure

Related to the Resource Conservation and Recovery Act of 1976· the process in which the owner-operator of a hazardous waste management unit discontinues active operation of the unit by treating, removing from the site, or disposing of on site all hazardous wastes in accordance will\ an Environmental Protection Agency or state-approved plan. Included, for example, are the process of emptying, cleaning, and removing or filling underground storage tanks and the capping of a landfill. Closure entails specific financial guarantees and technical tasks that are included in a closure plan and must be implemented.

Disposal

Related to the Comprehensive Environmental Response, Compensation, and Liability Act of 1980 and the Resource Conservation and Recovery Act of 1976: under the Resource Conservation and Recovery Act of 1976, the discharge, deposit, injection, dumping. spilling, leaking, or placing of any solid waste or hazardous waste into or on any land or water so that such solid waste or hazardous waste or any constituent thereof may enter the environment or be emitted into the air or discharged into any waters, including groundwaters. Similarly under the Comprehensive Environmental Response. Compensation, and Liability Act of 1980 with regard to hazardous substances.

Hazardous Waste

Related to Resource Conservation and Recovery Act of 1976 a waste, or combination of wastes, that because of its quantity, concentration, toxicity, corrosiveness, mutagenicity or inflammability, or physical, chemical, or infectious characteristics may cause, or significantly contribute to, an increase in mortality or an increase in serious irreversible, or incapacitating reversible illness or pose a substantial present or potential hazard to human health or the environment when improperly treated, stored, transported, or disposed of, or otherwise managed. Technically, those wastes that are regulated under the Resource Conservation and Recovery Act of 1976 40 CFR Part 261 are considered to be hazardous wastes.

Natural Resources

Under the Comprehensive Environmental Response, Compensation, and Liability Act of 1980, natural resources are defined as land, fish, wildlife, biota, air, water, groundwater, drinking water supplies, and other such resources belonging to, managed or held in trust by, or otherwise controlled by the United States, state or local governments, foreign governments, or Indian tribes.

Discount Rate Adjustment Technique

A present value technique that uses a risk-adjusted discount rate and contractual, promised, or most likely cash flows.

Fair Value

The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement dale.

Table Of Contents

410-20-25 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 25 Recognition

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 5 of28

General Subsection revised 01-Jul-2009

Combine Subsections

> Background for Recognition

25-1 Paragraph 35 of FASB Concepts Statement No. 6, Elements of Financial Statements, defines a liability as follows (Note: The indented text below is reproduced from FASB Concepts Statement No. 6 and includes editorial changes for intemal consistency within the Codification}.

Liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.

25-2 Probable is used with its usual general meaning, rather than in a specific accounting or technical sense (such as that in paragraph 450-20-25-1 ), and refers to that which can reasonably be expected or believed on the basis of available evidence or logic but is neither certain nor proved (Webster's New World Dictionary). Its inclusion in the definition is intended to acknowledge that business and other economic activities occur in an environment characterized by uncertainty in which few outcomes are certain (see paragraphs 44 through 48 of FASB Concepts Statement No. 6).

25-3 As stated in the preceding paragraph, the definition of a liability in Concepts Statement 6 uses the term probable in a different sense than it is used in paragraph 450-20-25-1 . As used in Topic 450, probable requires a high degree of expectation. The term probable in the definition of a liability, however, is intended to acknowledge that business and other economic activi.ties occur in an environment in which few outcomes are certain .

25-3A Paragraph 410-20-40-3 states that providing assurance that an entity will be able to satisfy its asset retirement obligation does not satisfy or extinguish the related liability.

> Fair Value Is Reasonably Estimated

25-4 An entity shall recognize the fair value of a liability for an asset retirement obligation in the period in which it is incurred if a reasonable estimate of fafr value can be made. If a reasonable estimate of fair value cannot be made in the period the asset retirement obligation is incurred, the liability shall be recognized when a reasonable estimate of fair value can be made. If a tangible long. lived asset with an existfng asset retirement obligation is acquired, a liability for that obligation shall be recognized at the asset's acquisition date as if that obligation were incurred on that date.

25-5 Upon initial recognition of a liability for an asset retirement obligation, an entity shall capitalize an asset retirement cost by increasing the carrying amount of the related fang-lived asset by the same amount as the liability. Paragraph 835-20-30-5 explains that capitalized asset retirement costs do not qualify as expenditures for purposes of applying Subtopic 835-20.

25-6 An entity shall identify all its asset retirement obligations. An entity has sufficient information to reasonably estimate the fair value of an asset retirement obligation i f any of the following conditions exist:

a. It is evident that the fair value of the obligation is embodied in the acquisition price of the asset

b. An active market exists for the transfer of the obligation.

c. Sufficient information exists to apply an expected present value technique .

> Obligations with Uncertainty in Timing or Method of Settlement

25-7 The obligation to perform the asset retirement activity is unconditional even though uncertainty exists about the timing and (or) method of settlement. Thus, the timing and (or) method of settlement may be conditional on a future event. Accordingly, an entity shall recognize a liability for the fair value of a cond11ional asset retirement obligation if the fair value of the liability can be reasonably estimated. In some cases, sufficient inforrnatron about the timing and (or) method of settlement may not be available to reasonably estimate fair value. An expected present value technique incorporates uncertainty about the timing and method of settlement into the fair value measurement. Uncertainty is factored into the measurement of the fair value of the liability through assignment of probabilities to cash flows.

25-8 An entity would have sufficient information to apply an expected present value technique and therefore an asset retirement obl[Qation would be reasonably estimable if either of the following conditions exists;

a. The settlement date and method of settlement for the obligation have been specified by others. For example, the law, regulation, or contract that gives rise to the legal obligation speci fies the settlement date and method of settlement In this situation, the settlement date and method of settlement are known and therefore the only

http://www.pwccomperio.com/JASDoc Viewer.aspx?Topic=4 l 0&SubTopic=20&docid=4 I... 4/29/20 I 4

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 6 of28

uncertainty is whether the obligation will be enforced (that is, whether performance will be required). In certain cases, determining the settlement date for the obligation that has been specified by others is a matter of judgment that depends on the relevant facts and circumstances. For example, a contract that provides the entity with an ability to extend its term through renewal should be evaluated to determine whether the settlement date should take into consideration renewal periods. Uncertainty about whether performance will be required does not defer the recognition of an asset retirement obligation because a legal obligation to stand ready to perform the retirement activities still exists, and it does not prevent the determination of a reasonable estimate of fair value because the only uncertainty is whether performance will be required.

b. The information is available to reasonably estimate all of the following:

1. The settlement date or the range of potential settlement dates

2. The method of settlement or potential methods of settlement (The term potential methods of settlement refers to methods of settling the obligation that are currently available to the entity. Therefore, uncertainty about future methods yet to be developed would not prevent the entity from estimating the fair value of the asset retirement obligation.)

3. The probabilities associated with the potential settlement dates and potential methods of settlement. (The entity should have a reasonable basis for assigning probabilities to the potential settlement dates and potential methods of settlement to reasonably estimate the fair value of the asset retirement obligation. If the entity does not have a reasonable basis of assigning probabilities, it is expected that the entity would still be able to reasonably estimate fair value when the range of time over which the entity may settle the obligation is so narrow and (or) the cash flows associated with each potential method of settlement are so similar that assigning probabilities without having a reasonable basis for doing so would not have a material impact on the fair value of the asset retirement obligation.)

25-9 In many cases, the determination as to whether the entity has the information to reasonably estimate the fair value of the asset retirement obligation is a matter of judgment that depends on the relevant facts and circumstances. II is expected that the narrower the range of time over which the entity may settle the obligation and the fewer potential methods of settlement the entity has available to it, the more likely it is that the entity will have the information to reasonably estimate the fair value of an asset retirement obligation. For an illustration of this guidance, see Example 3 (paragraph 410-20-55-47).

25-10 Instances may occur in which insufficient information to estimate the fair value of an asset retirement obligation is available. For example, if an asset has an indeterminate useful life, sufficient information to estimate a range of potential settlement dates for the obligation might not be available. In such cases, the liability would be initially recognized in the period in which sufficient information exists to estimate a range of potential settlement dates that is needed lo employ a present value technique to estimate fair value.

25-11 Examples of information that is expected to provide a basis for estimating the potential settlement dates. potential methods of settlement, and the associated probabilities include, but are not limited to, information that is derived from the entity's past practice, industry practice, management's intent, or the asset's estimated economic life. The estimated economic life of the asset might indicate a potential settlement date for the asset retirement obligation. However, the original estimated economic life of the asset may not, in and of itself, establish that date because the entity may intend to make improvements to the asset that could extend the life of the asset or the entity could defer settlement of the obligation beyond the economic life of the asset. In those situations, the entity would look beyond the economic life of the asset in determining the settlement date or range of potential settlement dates to use when estimating the fair value of the asset retirement obligation.

25-12 An asset retirement obligation may result from the acquisition, construction, or development and (or) normal operation of a long-lived asset that has an indeterminate useful life and thereby an indeterminate settlement date for the asset retirement obligation.

25-13 If a current law, regulation, or contract requires an entity to perform an asset retirement activity when an asset is dismantled or demolished, there is an unambiguous requirement to perform the retirement activity even if that activity can be indefinitely deferred. At some time deferral will no longer be possible, because no tangible asset will last forever (except land). Therefore, the obligation to perform the asset retirement activity is unconditional even though uncertainty exists about the timing and (or) method of settlement

> Uncertainty in Performance Obligations

25-14 This Subtopic requires recognition of a conditional asset retirement obligation before the event that either requires or waives performance occurs. Uncertainty surrounding conditional performance of the retirement obligation is factored into its measurement by assessing the likelihood that performance will be required. In situations in which the conditional aspect has only 2 outcomes and there is no information about which outcome is more probable, a 50 percent likelihood for each outcome shall be used until additional information is available.

http://www.pwccomperio.com/ J AS Doc Viewer .aspx ?Topic=41 O&Sub Topic=20&doc idc4 J ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 7 of28

25-15 An unambiguous requirement that gives rise to an asset retirement obligation coupled with a low likelihood of required performance still requires recognition of a liability. Uncertainty about the conditional outcome of the obligation is incorporated into the measurement of the fair value of that liability, not the recognition decision. Uncertainty about performance of conditional obligations shall not prevent the determination of a reasonable estimate of fair value. A past history of nonenforcement of an unambiguous obligation does not defer recognrtion of a liability, but its measurement is affected by the uncertainty over the requirement to perform retirement activities.

> Acquired Asset Retirement Obligations

25-16 If a tangible long-lived asset with an existing asset retirement obligation is acquired, a liability for that obligation shall be recognized at the asset's acquisition date as if that obligation were incurred on that date.

Table Of Contents

410-20-30 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 30 Initial Measurement

General Subsection revised 01.Jul-2009

Combine Subsections

> Determination of a Reasonable Estimate of Fair Value

30-1 An expected present value technique will usually be the only appropriate technique with which to estimate the fair value of a liability for an asset retirement obligation. An entity, when using that technique, shall discount the expected cash flows using a credit-adjusted risk-free rate. Thus, the effect of an entity's credit standing is reflected in the discount rate rather than in the expected cash flows. Proper application of a discount rate ad1ustment technique entails analysis of at least two liabilities-the liability that exists in the marketplace and has an observable interest rate and the liabUity being measured. The appropriate rate of interest for the cash flows being measured shall be inferred from the observable rate of interest of some other liability, and to draw that inference the characteristics of the cash flows shall be similar to those of the liability being measured. Rarely, if ever, would there be an observable rate of interest for a liability that has cash flows similar to an asset retirement obligation being measured. In addition, an asset retirement obligation usually w i11 have uncertainties in both timing and amount. In that circumstance, employing a discount rate adjustment technique, where uncertainty is incorporated into the rate, will be d ifficult, if not impossible. See paragraphs 410-20-55-13 lhrough 55-17 and Example 2 (paragraph 410-20-55-35). For further information on present value techniques, see the guidance beginning in paragraph 820-10-55-4.

Table Of Contents

410-20-35 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 35 Subsequent Measurement

General Subsection revised 01.Jul-2009

Combine Subsections

> Allocation of Asset Retirement Cost

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 8 of28

35-1 A liability for an asset retirement obligation may be incurred over more than one reporting period if the events that create the obl1gation occur over more than one reporting period. Any incremental liability incurred in a subsequent reporting period shall be considered to be an additional layer of the original liability. Each layer shall be initially measured at fair value. For example, the liability for decommissioning a nuc!ear power plant is incurred as contamination occurs. Each period, as contamination increases, a separate layer shall be measured and recognized. Paragraph 410-20-30-1 provides guidance on using that technique.

35-2 An entity shall subsequently altocate that asset retirement cost to expense using a systematic and rational method over its useful life. Application of a systematic and rational allocation method does not preclude an entity from capitalizing an amount of asset retirement cost and allocating an equal amount to expense In the same accounting period. For example, assume an entity acquires a long-lived asset with an estimated life of 10 years. As that asset is operated, the entity incurs one-tenth of the liability for an asset retirement obligation each year. Application of a systematic and rational allocation method would not preclude that entity from capitalizing and then expensrng one-tenth of the asset retirement costs each year.

35-3 In periods subsequent to initial measurement, an entity shall recognize period-to-period changes in the liabil ity for an asset retirement obligation resulting from the following:

a. The passage of time

b. Revisions to either the timing or the amount of the orig[nal estimate of undiscounted cash flows.

35-4 An entity shall measure and incorporate changes due to the passage of time into the carrying amount of the liability before measuring changes resulting from a revision to either the timing or the amount of estimated cash flows.

35-5 An entity shall measure changes in the liability for an asset retirement obligation due to passage of time by applying an interest method of allocation to the amount of the liability at the beginning of the period. The interest rate used to measure that change shall be the credit-adjusted risk-free rate that existed when the liability, or portion thereof, was initially measured. That amount shall be recognized as an increase in the carrying amount of the liability and as an expense classified as accretion expense. Paragraph 835-20-15-7 states that accretion expense related to exit costs and asset retirement obligations shall not be considered to be interest cost for purposes of applying Subtopic 835-20.

35-6 The subsequent measurement provisions require an entity to identify undiscounted estimated cash flows associated with the initial measurement of a liability. Therefore, an entity that obtains an initial measurement of fair value from a market price or from a technique other than an expected present value technfque must determine the undiscounted cash flows and estimated timing of those cash flows that are embodied in that fair value amount for purposes of applying the subsequent measurement provisions. Example 1 (see paragraph 410-20-55-31 ) provides an illustration of the subsequent measurement of a liability that is initially obtained from a market price. (See paragraph 410-20-25-14 for a discussion on conditional outcomes.)

35-7 Paragraph 410-20-25-14 explains how uncertainty surrounding conditional performance of a retirement obligation is factored into its measurement by assessing the likelihood that performance will be required. As the time for notification approaches, more information and a better perspective about the ultimate outcome will likely be obtained. Consequently, reassessment of the timing, amount, and probabilities associated with the expected cash flows may change the amount of the liability recognized. See paragraphs 410-20-55-18 through 55-19.

> Change in Estimate

35-8 Changes resulting from revisions to the timing or the amount of the original estimate of undiscounted cash flows shall be recognized as an increase or a decrease in the carrying amount of the liability for an asset retirement obligation and the related asset retirement cost capitalized as part of the carrying amount of the related long-lived asset Upward revisions in the amount of undiscounted estimated cash flows shall be discounted using the current credit-adjusted risk-free rate. Downward revisions in the amount of undiscounted estimated cash flows shall be discounted using the credit-adjusted riskfree rate that existed when the original liability was recognized. If an entity cannot identify the prior period to which the downward revision relates, it may use a weighted-average credit-adjusted risk-free rate to discount the downward revision to estimated future cash flows. When asset retirement costs change as a result of a revision to estimated cash flows, an entity shall adjust the amount of asset retirement cost allocated to expense in the period of change if the change affects that period only or in the period of change and future periods if the change affects more than one period as required by paragraphs 250-10-45-17 through 45-20 for a change in estimate.

> Effects of Funding and Assurance Provisions

35-9 Methods of providing assurance include surety bonds, insurance policies, letters of credit, guarantees by other entities, and establishment of trust funds or identification of other assets dedicated to satisfy the asset retirement obligation. The existence of funding and assurance provisions may affect the determination of the credit-adjusted risk-free rate. For a previously recognized asset retirement obligation, changes in funding and assurance provisions have no effect on the initial measurement or accretion of that liability, but may affect the credit-adjusted risk-free rate used to discount upward revisions in undiscounted cash flows for that obligation.

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=41... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 9 of28

Table Of Contents

410-20-40 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 40 Derecognition

General Subsection revised 01-Jul-2009

Combine Subsections

> Settlement of an Asset Retirement Obligation

40-1 Typically, settlement of an asset retirement obligation is not required untu the associated asset is retired. However, certain circumstances may exist in which partial settlement of an asset retirement obligation is required or performed before the asset is fully retired. The nature of asset retirement obligations In various industries is such that the obligations are not necessarily satisfied when the current operation or use of the asset ceases. These obligations can be settled during operation of the asset or after the operations cease. The liming of the ultimate settlement of a liability is unrelated to and should not affect its initial recognition in the financial statements provided the obligation is associated with the retirement of a tangible long-lived asset.

40-2 Paragraph 410-20-25-14 explains how uncertainty surrounding conditional performance of a retirement obligation is factored into its measurement by assessing the likelihood that performance will be required. If, as time progresses, it becomes apparent that retirement activities will not be required, the liability and the remaining unamortized asset retirement cost shall be reduced to zero.

40-3 Providing assurance that an entity will be able to satisfy its asset retirement obligation does not satisfy or extinguish the related liability. The effect of surety bonds. letters of credit, and guarantees is to provide assurance that third parties wil provide amounts to satisfy the asset retirement obligations if the entity that has primary responsibility (the obtigor) to do so cannot or does not fulfill its obligations. The possibility that a third party will satisfy the asset retirement obligations does not relieve the obliger from its primary responsibmty for those obligattons If a third party is required to satisfy asset retirement obligations due to the failure or tnabflity of the obliger to do so directly, the obliger would then have a liability to the third party.

Table Of Contents

410-20-45 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 45 Other Presentation Matters

General Subsection revised 01-Jul-2009

Combme Subsections

> Classification of Accretion Expense

45-1 Accretion expense shall be classified as an operating item in the statement of Income. An entity may use any descriptor for accretion expense so long as it conveys the underlying nature of the expense.

45-2 See paragraph 230-10-45-17 for additional information about the classification of cash payments for asset retirement obligations as operating items on the statement of cash flows.

http://www. pwccomperio .com/ J AS Doc Viewer.aspx?Topic=4 I O& Sub Topic=20&doc id=4 I ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page IO of28

> Statement of Cash Flows

45-3 Paragraph 230-10-45-17(e) states that a cash payment made to settle an asset retirement obligation is a cash outflow for operating activities,

Table Of Contents

410-20-50 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 50 Disclosure

General Subsection revised 01.Jul-2009

Combine Subsections

50-1 An entity shall disclose all of the following information about its asset retirement obligations:

a. A general description of the asset retirement obligations and the associated long-lived assets

b. The fair value of assets that are legally restricted for purposes of settling asset retirement obligations

c. A reconciliation of the beginning and ending aggregate carrying amount of asset retirement obligations showing separately the changes attributable to the following components, whenever there is a significant change in any of these components during the reporting period:

1. Liabilities incurred in the current period

2. Liabilities settled in the current period

3. Accretion expense

4. Revisions in estimated cash flows.

50-2 If the fair value of an asset retirement obligation cannot be reasonably estimated, that fact and the reasons therefor shall be disclosed.

Tab'e Of Contents

410-20-55 410 Asset Retirement and Environmental Obligations> 20 Asset Retirement Obligations > 55 Implementation Guidance and Illustrations

General Subsection revised 01-0ct-2012

Combine Subsections

> Implementation Guidance

> > Determination of Whether a Legal Obligation Exists

55-1 This implementation guidance illustrates Section 410-20-15, In most cases involving an asset retirement obligation, the determination of whether a legal obligation exists should be unambiguous. However, in situations in which no law,

http://www.pwccomperio.com/JASDoc Viewer.aspx?Topic=41 O&SubTopice::;2Q&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 11 of 28

statute, ordinance, or contract exists but an entity makes a promise to a third party (which may include the public at large) about its intention to perform retirement activities, facts and circumstances need to be considered carefully in determining whether that promise has imposed a legal obligation upon the promisor under the doctrine of promissory estoppel. A legal obligation may exist even though no party has taken any formal action. In assessing whether a legal obligation exists, an entity is not permitted to forecast changes in the law or changes in the interpretation of existing laws and regulations. Preparers and their legal advisors are required to evaluate current circumstances to determine whether a legal obligation exists.

55-2 For example, assume an entity operates a manufacturing facility and has plans to retire it within five years. Members of the local press have begun to publicize the fact that when the entity ceases operations at the plant, ii plans to abandon the site without demolishing the building and restoring the underlying land. Due to the significant negative publicity and demands by the public that the entity commit to dismantling the plant upon retirement, the entity's chief executive officer holds a press conference at city hall to announce that the entity will demolish the building and restore the underlying land when the entity ceases operations at the plant. Although no law, statute, ordinance, or written contract exists requiring the entity to perform any demolition or restoration activities, the promise made by the entity's chief executive officer may have created a legal obligation under the doctrine of promissory estoppal. In that circumstance, the entity's management (and legal counsel, if necessary) would have to evaluate the particular facts and circumstances to determine whether a legal obligation exists.

55-3 Once an entity determines that a duty or responsibility exists, it will then need to assess whether an obligating event has occurred that leaves it little or no discretion to avoid the future transfer or use of assets. If such an obligating event has occurred, an asset retirement obligation meets the definition of a liability and qualifies for recognition in the financial statements. However, if an obligating event that leaves an entity little or no discretion to avoid the future transfer or use of assets has not occurred, an asset retirement obligation does not meet the definition of a liability and, therefore, should not be recognized in the financial statements.

55-4 Identifying the obligating event is often difficult, especially in situations that involve the occurrence of a series of transactions or other events or circumstances affecting the entity. For example, in the case of an asset retirement obligation, a law or an entity's promise may create a duty or responsibility, but that law or promise in and of itself may not be the obligating event that results in an entity's having little or no discretion to avoid a future transfer or use of assets. An entity must look to the nature of the duty or responsibility to assess whether the obligating event has occurred. For example, in the case of a nuclear power facility, an entity assumes responsibility for decontamination of that facility upon receipt of the license to operate it. However, no obligation to decontaminate exists until the facility is operated and contamination occurs. Therefore, the contamination, not the receipt of the license, constitutes the obligating event.

> > Expectation of Nonenforcement

55-5 This implementation guidance illustrates Section 410-20-15.Contracts between entities may contain an option or a provision that requires one party to the contract to perform retirement activities when an asset is retired. The other party may decide in the future not to exercise the option or to waive the provision to perform retirement activities, or that party may have a history of waiving similar provisions in other contracts. Even if there is an expectation of a waiver or nonenforcement, the contract still imposes a legal obligation. That obligation is included in the scope of this Subtopic. The likelihood of a waiver or nonenforcement will affect the measurement of the liability. For example, consider an entity that owns and operates a landfill. Regulations require that that entity perform capping, closure, and postclosure activities. Capping activities involve covering the land with topsoil and planting vegetation. Closure activities include drainage, engineering, and demolition and must be performed prior to commencing the postclosure activities. Postclosure activities, the final retirement activities, include maintaining the landfill once final certificati.on of closure has been received and monitoring the ground and surface water, gas emissions, and air quality. Closure and postclosure activities are performed after the entire landfill ceases receiving waste (that is, after the landfill is retired). However, capping activities are performed as sections of the landfill become full and are effectively retired. The fact that some of the capping activities are performed while the landfill continues to accept waste does not remove the obligation to perform those intermedi•ate capping activities from the scope of this Subtopic

>>Acquisition, Construction, or Development of a Long-Lived Asset

55-6 This implementation guidance illustrates Sectron 410-20-15. Whether an obligation results from the acquisition, construction, or development of a long-lived asset should, in most circumstances, be clear. For example, if an entity acquires a landfill that is already in operation, an obligation to perform capping, closure, and postclosure acUvities results from the acquisition and assumption of obligations related to past normal operations of the landfill. Additional obligations w ill be incurred as a result of future operations of the landfill.

> > Normal Operations

55-7 This implementation guidance illustrates Section 410-20-15. Whether an obligation results from the normal operation of a long-lived asset may require judgment. Obtigalions that result from the normal operation of an asset should be predictable and likely of occurring. For example, consider an entity that owns and operates a nuclear power plant. That entity has a legal obligation to perform decontamination activities when the plant ceases operations. Contamination, which

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 12of28

gives rise to the obligation, is predictable and likely of occurring and is unavoidable as a result of operating the plant. Therefore, the obligation to perform decontamination activities at that plant results from the normal operation of the plant.

55-8 For example, a certain amount of spillage may be inherent in the normal operations of a fuel storage facility, but a catastrophic accident caused by noncompliance with an entity's safety procedures is not. The obligation to clean up after the catastrophic accident does not result from the normal operation of the facility and is not within the scope of this Subtopic.

> > Components of a Larger System

55-9 An asset retirement obligation may exist for component parts of a larger system, In some circumstances, the retirement of the component parts may be required before the retirement of the larger system to which the component parts belong.

55-10 For example, consider an aluminum smeller that owns and operates several kilns lined with a special type of brick. The kilns have a long useful life, but the bricks wear out after approximately five years of use and are replaced on a periodic basis to maintain optimal efficiency of the kilns. Because the bricks become contaminated with hazardous chemicals while in the kiln, a state law requires that when the bricks are removed, they must be disposed of at a special hazardous waste site. The obligation to dispose of those bricks is within the scope of this Subtopic The cost of the replacement bricks and their installation are not part of that obligation. This implementation guidance Illustrates Section 41 O -20-15.

55-11 If assets with asset retirement obligations are components of a larger group of assets (for exampte. a number of oil wells that make up an entire oil field operation), aggregation techniques may be necessary to derive a co~ective asset retirement obligation. This Subtopic does not preclude the use of estimates and computational shortcuts that are conslstent with the fair value measurement objective when computing an aggregate asset retirement obligation for assets that are components of a larger group of assets. This implementation guidance illustrates paragraph 410-20-30· 1.

> > Obligations with Uncertainty About Government Enforcement

55-12 This implementation guidance illustrates Section 410-20-15. If, for example, a governmental unit retains the right (an option) to decide whether to require a retirement activity, there is some uncertainty about whether those retirement acUvities will be required or waived. Regardless of the uncertainty attributable to the option, a legal obligation to stand ready to perform retirement activities still exists, and the governmental unit might require them to be performed. Although the timing and method of settlement of the retirement obligation may depend on Mure events that may or may not be within the control of the entity, a legal obligation to stand ready to perform retirement activities still exists. The entity should consider the uncertainty about the t iming and method of setttement in the measurement of the liability, consistent with a fair value measurement objective. regardless of whether the event that will trigger the settlement is partially or wholly under the control of the entity.

> > Expected Present Value Technique

55-13 This implementation guidance illustrates paragraph 410-20-30-1 . In estimating the fair value of a liability for an asset retirement obligation using an expected present value technique, an entity shall begin by estimating the expected cash flows that reflect. to the extent possible, a marketplace assessment of the cost and timing of performing the required retirement activitles. Considerations in estimating those expected cash flows include developing and incorporating explicit assumptions, to the extent possible, about all of the following:

a. The costs that a third party would incur in performing the tasks necessary to retire the asset

b, Other amounts that a third party would inctude in determining the price of the transfer, including, for example, inflation, overhead, equipment charges, profit margin, and advances in technology

c The extent to which the amount of a third party's costs or the timing of its costs would vary under different future scenarios and the relative probabilities of those scenarios

d . The price that a third party would demand and could expect to receive for bearing the uncertainties and unforeseeable circumstances inherent in the obligation, sometimes referred to as a market-risk premium.

55-14 It is expected that uncertainties about the amount and timing of future cash flows can be accommodated by using the expected present value technique and therefore will not prevent the determination of a reasonable estimate of fair value.

> > Credit-Adjusted Risk-Free Rate

55-15 This implementation guidance illustrates paragraph 410·20-30-1 . An entity shall discount expected cash flows using an interest rate that equates to a risk-free interest rate adjusted for the effect of its credit standing (a credit-adjusted riskfree rate). In determining the adjustment for the effect of its credit standing, an entity should consider the effects of all terms, collateral, and existing guarantees on the fair value of the liability.

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 13 of 28

55-16 Adjustments for default risk can be reflected in either the discount rate or the expected cash flows. Jn most si tuations, an entity will know the adjustment required to the risk-free interest rate to reflect its credit standing. Consequently, ii would be easier and less complex to reflect that adjustment in the discount rate.

55-17 In addition, because of the requirements in paragraph 410-20-35-8 relating to upward and downward adjustments in expected cash flows, it is essential to the operationality of this Subtopic that the credit standing of the entity be reflected in the discount rate. For those reasons, the risk-free rate shall be adjusted for the credit standing of the entity lo determine the discount rate.

> > Calculation of Accretion Expense

55-18 This implementation guidance illustrates paragraphs 410-20-35-1 through 35-6. In periods subsequent to initial measurement, an entity recognizes the effect of the passage of time on the amount of a liability for an asset retirement obligation. A period-to-period increase in the carrying amount of the liability shall be recognized as an operating item (accretion expense) in the statement of income. An equivalent amount is added to the carrying amount of the liability. To calculate accretion expense, an entity shall multiply the beginning of the period liability balance by the credit-adjusted riskfree rate that existed when the liability was initially measured. The liability shall be adjusted for accretion prior to adjusting for revisions in estimated cash flows.

>>Changes in Assumptions and Legal Requirements

55-19 This implementation guidance illustrates paragraph 410-20-35-8. Revisions to a previously recorded asset retirement obligation will result from changes in the assumptions used to estimate the expected cash flows required to settle the asset retirement obligation, including changes in estimated probabilities, amounts, and liming of the settlement of the asset retirement obligation, as well as changes in the legal requirements of an obligation. Any changes that result in upward revisions to the expected cash flows shall be treated as a new liability and discounted at the current rate. Any downward revisions to the expected cash flows will result in a reduction of the asset retirement obligation, For downward revisions, the amount of the liability to be removed from the existing accrual shall be discounted at the credit-adjusted risk-free rate that was used at the time the obligation to which the downward revision relates was originally recorded (or the hlstorical weighted-average rate if the year[s} to which the downward revision applies cannot be determined).

55-20 Revisions to the asset retirement obligation result in adjustments of capitalized asset retirement costs and will affect subsequent depreciation of the related asset. Such adjustments are depreciated on a prospective basis.

> > Interim Property Retirements

55-21 This implementation gutdance illustrates Section 410-20-15. There is no conceptual difference between interim property retirements and replacements and those retirements that occur in circumstances in which the retired asset is not replaced. Therefore, any asset retirement obligation associated with the retirement of or the retirement and replacement of a component part of a larger system qualifies for recognition provided that the obligation meets the definition of a liability, The cost of replacement components is excluded.

55-22 Examples of interim property retirements and repl'acements for component parts of larger systems are components of transmission and distribution systems (utmty poles), railroad ties, a single oil well that is part of a larger oil field, and aircraft engines. The assets in those examples may or may not have associated retirement obligations.

> > Historical Waste on Electrical and Electronic Equipment Associated with EU Directive 2002/96/EC

55-23 EU Directive 2002/96/EC was adopted on February 13, 2003, and directs EU-member countries to adopt legislation to regulate the col!ectfon, treatment. recovery, and environmentally sound disposal of electrical and electronic waste equipment. The actual legislation adopted by individual EU-member countries can have different requirements. An entity should apply the guidance herein, adjusted as needed for the specific requirements of the applicable EU-member country.

55-24 The Directive distinguishes between new and historical waste. All products put on the market on or before August 131

2005, are deemed to be historical waste equipment for the purposes of the Directive. Example 4 (see paragraph 410-20-55-63 ) does not address the accounting for new waste because there should be little diversity in practice in the accounting for such waste. Costs relating to waste of new equipment are to be borne solely by the producers of the new equipment. This implementation guidance illustrates Section 410-20-15.

55-25 Under the Directive, the waste management obligation remains with the commercial user until the historical waste equipment is replaced, at which time the waste management obligation for that equipment may be transferred to the producer of the replacement equipment depending on the law adopted by the appticable EU-member country. If the commercial user does not replace the equipment, the obligation remains with that user until it disposes of the equipment. The Directive provides each EU-member country with the option to obligate commercial users to pay part or all of the costs associated with the historical waste even if the equipment is replaced. In this situation, the obligation would remain (partly or wholly) with the commercial user until the user disposes of the equipment.

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic-=20&docid=41... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 14of28

55-26 The accounting for the initial recognition and measurement of the liability and asset retirement cost should be consistent with paragraphs 410-20-25-1 through 25-4. The ability or intent of the commercial user to replace the asset and transfer the obligation does not relieve the user of its present duty or responsibillty to settle the obligation. The replacement of the asset may, depending on EU-member country law, transfer the obligation to the replacement producer, and, if so, that transfer would affect the purchase price of the replacement asset Upon initial recognition of a liability, an entity shall capitalize an asset retirement cost by increasing the carrying amount of the related asset by the same amount as the liability. The accounting subsequent to the initial recognition of the asset and liability should be consistent with the guidance in paragraphs 410-20-35-3 through 35-8

55-27 If the asset is subsequently replaced, with the obligation being transferred to the producer of the replacement equipment, the commercial user should determine the portion of the total amount paid to the producer that relates to the replacement equipment (the new asset) and the portion that relates to the transfer of the asset retirement obligation. That determination should be based on the fair value of the asset retirement obligation, without the sale of the new asset The price paid by the commercial user would not Include any costs associated with the transfer of the obligation in situations in which the law in the EU-member country obligates commercial users to pay all of the costs associated with the hfstorical waste even if the equipment is replaced. In those situations, the commercial user would not derecognize the liability from its balance sheet upon replacement. but rather when the obligation is ultimately settled.

55-28 The new asset should be measured as the residual amount (the excess of the price paid over the fair value of the asset retirement obligation transferred). That amount should be used in determining the new asset's cost basis. The commercial user should derecognize the liability from its balance sheet and recognize a gain or loss based on the difference between the carrying amount of the liability at the date of the sale and the portion of the sales price that relates to the obligation. The producer of the new asset should recognize revenue for the total amount received reduced by the fair value of the obligation upon the transfer of the obligation from the commercial user (that is, on a net basis). The requirements for the producer to measure the revenue from the sale of the new asset as the residual amount and recognize revenue only for the sale of the new asset are applicable for those producers for which the recycling of electronic waste equipment is not a revenue-generating business activity. In situations in which the recycling of equipment is a revenuegenerating business activity for the producer, that producer should measure the revenue from the sale of the new asset and the assumption of the obligation in accordance with the provisions of Subtopfc 605-25.

55-29 The producer of the new asset should derecognize that liability when the obtigation is settled.

55-30 See Example 4 (paragraph 410-20-55-63), which describes accounting for obligations associated with Directive 2002/96/EC on Waste Electrical and Electronic Equipment adopted by the European Union. That Example refers to and paraphrases various provisions of the Directive. Nothing in that Example shall be considered a definitive interpretation of any provision of the Directive for any purpose.

> Illustrations

> > Example 1: Subsequent Measurement of a Liability Obtained from a Market Price

55-31 This Example illustrates the guidance in paragraphs 410-20-35-5 through 35-6. After initial measurement, an entity is required to recognize period-to-period changes in an asset retirement obligation liability resulting from the passage of time (accretion expense) and revisions in cash flow estimates. To apply the subsequent measurement provisions of this Subtopic, an entity must identify undiscounted cash flows related to an asset retirement obligation liability irrespective of how the liability was initially measured. Therefore, if an entity obtains the initial fair value from a market price, it must impute undiscounted cash flows from that price.

55-32 This Example illustrates the subsequent measurement of a liability in situations where the initial liability is based on a market price. Assume that the liability is initially recognized at the end of period O when the market price is $300,000 and the entity's credit-adjusted risk-free rate is 8 percent. As required by this Subtoplc. revisions in the timing or the amount of estimated cash flows are assumed to occur at the end of the period after accretion on the beginning balance of the liability is calculated. At the end of each period, the following procedure is used to impute cash flows from the end-of-period market price, compute the change in that price attributable to revisions in estimated cash flows, and calculate accretion expense:

a. The market price and the credit-adjusted risk-free interest rate are used to impute the undiscounted cash flows embedded in the market price.

b. The undiscounted cash flows from (a) are discounted at the initial credit-adjusted risk-free rate of 8 percent to arrive at the ending balance of the asset retirement obligation liability per the provisions of this Subtopic.

c. The beginning balance of the asset retirement obfigation liability is multiplied by the initial credit-adjusted riskfree rate of 8 percent to arrive at the amount of accretion expense per the provisions of this Subtopic.

d. The difference between the undiscounted cash flows at the beginning of the period and the undiscounted cash flows at the end of the period represents the reviston in cash flow estimates that occurred during the period If that change is an upward revision to the undiscounted estimated cash flows, it is discounted at the current credit-

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=4 I 0&SubTopic~20&docid=41... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 15 of28

adjusted risk-free rate. If that change is a downward revision, it is discounted at the historical weighted-average rate because it is not practicable to separately identify the period to which the downward revision relates.

55-33 The following table illustrates the subsequent measurement of an asset retirement obligation liability obtained from a market price.

Subsequent Measurement of an Asset Retirement Obllgallon Liability Obtained from a Market Price

End of Period 0 1 2

Market assumptlons: Market price ~ncludes market risk premium) $ 300,000 $ 400,000 $ 350,000 Current risk-free rate adjusted for entity's credit standing 8.00% 7.00% 7.50%

Tlme period remaining 3 2 1

Imputed undlscounted cash !lows (market price discounted at market rate) $ 3TT,914 $ 457,960 $ 376,250

Change In undlscounted cash nows 3TT,914 80,046 (81 ,710) Discount rate:

Current credit-adjusted risk-free rate (for upward revisions) 8.00% 7.00%

Historical weighted-average credit-adjusted risk-free rate (for downward revisions) 7.83%

Change In undlscounted cash nows discounted at credit-adjusted risk-free rate (current rate for upward revisions and historical rate for downward revis\Ons) $ 300,000 $ 69,916 s (75,777)

55-34 The following table illustrates the measurement of liability under the provisions of the asset retirement obligation statement.

$ ~

$ ~

$

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=41 ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 16 of28

Measurement of Liability under Provisions of Asset ReUrement Obligation Statement

Beginning Accretion Change In Ending Period Balance ~8.0%~ Cash Flows Balance

0 $ 300,000 $300,000 1 $ 300,000 $ 24,000 324,000 2 324,000 25,920 349,920 3 349,920 27,994 3TT,914

Beginning Accretion Change In Ending Period Balance {!.0%~ CUh flows Balance

0 1 $ 69,916 $ 69,91 6 2 $ 69,916 $ 4,894 74,81 0 3 74,810 5,236 60,046

Beginning Accretion Change In Ending Period Balance (7.83%~ Cash Rows Balance

0 1 2 $ (75,7n) $ {75,7TT) 3 $ (75,777) $ (5,933) (81,71 0)

Beginning Change In Ending Period Balance Accretion Cash Rows Balance

0 1 2 3 $ 3,750 $ 3,750

Total

Beginning Accretion Change In Ending Period Balance EX!?!OS8 Cash Rows Balance

0 $ 300,000 $300,000 1 S 300,000 $ 24,000 69,916 393,916 2 393,916 30,814 (75,7n) 348,953 3 348,953 27,297 3,750 360,000

> > Example 2: Recognition and Measurement

55-35 The following Cases illustrate the recognition and measurement provisions of this Subtopic

a . Initial measurement of a liability for an asset retirement obligation using an expected present value technique, subsequent measurement assuming that there are no changes in expected cash flows, and settlement of the asset retirement obligation Habitity at the end of its term (Case A)

b. Subsequent measurement of an asset retirement obligation liability after a change in expected cash flows (Case B)

c Recognition and measurement of an asset retirement obligation liability that is incurred over more than one reporting period (Case C)

d . Accounting for asset retirement obligations that are conditional and that have a low likelihood of enforcement (Case D).

55-36 Cases A , B, C, and D incorporate simplified assumptions to provide guidance in implementing this Subtopic. For instance, Cases A and B relate to the asset retirement obligation associated with an offshore production platform that also

http://www.pwccomperio.com/JASDoc Viewer.aspx?Topic=4 I 0&SubTopicc::20&docid=4 l ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 17 of28

would likely have individual wells and production facilities that would have separate asset retirement obligations. Those Cases also assume straight-line depreciation, even though, in practice, depreciation would likely be applied using a units-of -production method. Other simplifying assumptions are used throughout the Cases.

> > > Case A: Initial Measurement Using a Present Value Technique, Subsequent Measurement with No Change in Expected Cash Flows

55-37 This Case depicts an entity that completes construction of and places into service an offshore oil platform on January 1, 2003. The entity is legally required to dismantle and remove the platform at the end of its useful life, which is estimated to be 10 years. Based on the requirements of this Subtopic, on January 1, 2003, the entity recognizes a liability for an asset retirement obligation and capitalizes an amount for an asset retirement cost. The entity estimates the initial fair value of the liability using an expected present value technique. The significant assumptions used in that estimate of fair value are as follows:

a. Labor costs are based on current marketplace wages required lo hire contractors to dismantle and remove offshore oil platforms. The entity assigns probability assessments to a range of cash flow estimates as follows.

Cash Flow Probablllty Expected Estimate Assessment cash Flows

S 100,000 25% $ 25,000 125,000 50 62,500 175,000 25 43.750

$ 131.250

b. The entity estimates allocated overhead and equipment charges using the rate it applies to labor costs for transfer pricing (80 percent). The entity has no reason to believe that its overhead rate differs from those used by contractors in the industry.

c. A contractor typically adds a markup on labor and allocated internal costs to provide a profit margin on the job. The rate used (20 percent) represents the entity's understanding of the profit that contractors in the industry generally earn to dismantle and remove offshore oil platforms.

d. A contractor would typically demand and receive a premium (market risk premium) for bearing the uncertainty and unforeseeable circumstances inherent in locking in today's price for a project that will not occur for 10 years The entity estimates the amount of that premium to be 5 percent of the expected cash flows adjusted for inflation.

e. The risk-free rate of interest on January 1. 2003, is 5 percent The entity adjusts that rate by 3.5 percent to reflect the effect of its credit standing. Therefore, the credit-adjusted risk-free rate used to compute expected present value is 8.5 percent.

f. The entity assumes a rate of inflation of 4 percent over the 10-year period.

55-38 On December 31, 2012, the entity settles its asset retirement obligation by using its internal workforce at a cost of $351,000. Assuming no changes during the 10-year period in the expected cash flows used to estimate the obligation, the entity would recognize a gain of $89,619 on settlement of the obligation. The entity would account for the asset retirement obligation as follows.

Labor Allocated overhead and equipment charges (80% of labor)

Total costs incurred Asset retirement obligation liability

Gain on settlement of obligation

$ 195,000

156.000

351,000 440.619

$ 89,619

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docidc 4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Initial Measurement of the Asset Retirement Obligation Llablllty at January 1, 2003

Expected labor costs Allocated overhead and equipment charges (.80 x $131,250) Contractor's mar1<up [.20 x ($131,250 + $105,000)] Expected cash flows before Inflation adjustment Inflation factor assuming 4 percenl rate for 10 years Expected cash nows adjusted for Inflation Market-risk premium (.05 x $419,637) Expected cash flows adjusted for mar1<et risk

Expected present value using credit-adjusted rtsk-tree rate Of 8.5 percent for 10 years

Interest Method of Allocation

Liability Liability Balance Balance

Year 1/1 Accretion 12131

2003 $ 194,879 s 16,565 $ 211,444 2004 211,444 17,973 229,417 2005 229,417 19,500 248,917 2006 248,917 21,158 270,075 2007 270,075 22,956 293,031 2008 293,031 24,908 317,939 2009 317,939 27,025 344,964 2010 344,964 29,322 374,286 2011 374,286 31,814 406,100 2012 406,100 34,519 440,619

Schedule of Expenses

Accretion Depreciation Total Year-End Expense Expense Expense

2003 $ 16,565 s 19,488 $36,053 2004 17,973 19,488 37,461 2005 19,500 19,488 38,988 2006 21,158 19,488 40,646 2007 22,956 19,488 42,444 2008 24,908 19,488 44,396 2009 27,025 19,488 46,513 2010 29,322 19,488 48,810 2011 31,814 19,488 51,302 2012 34,519 19,488 54,007

Expected Cash Rows

1/1/03

$ 131,250 105,000

47,250 283,500

1.4802 419,637

20,982 $ 440,619

$ 194,879

Page 18 of28

http://www.pwccomperio.com/ J AS Doc Viewer.aspx?Topic=41 O&S ub Topic=20&doc id=4 I . . . 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Journal Entries

January 1, 2003: Long-lived asset (asset retirement cost)

Asset retirement obligation liability To record the initial fair value of the asset retirement obligation llablllty

December 31, 2003-2012: Depreciation expense (asset retirement cost)

Accumulated depreciation To record straight-line depreciation on the asset retirement cost

Accretion expense Asset retirement obligation liability

To record accretion expense on the asset retirement obligation liability

December 31, 2012: Asset retlrement obligation liability

Wages payable Allocated overhead and equipment charges (.80 x $195,000)

Gain on settlement of asset retirement obligation liability To record settlement of the asset retirement obligation liability

S 194,879

19,488

Per schedule

440,619

Page 19 of 28

S 194,879

19,488

Per sche<lule

195,000

156,000 89,619

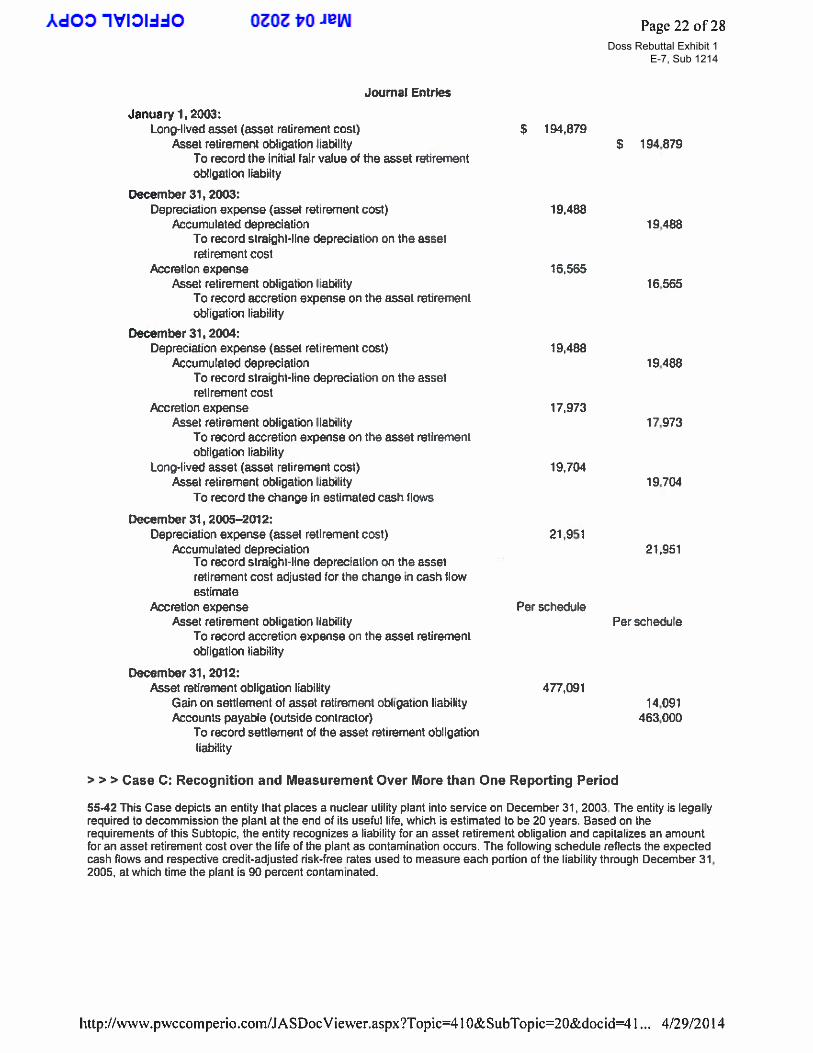

> > > Case B: Initial Measurement Using a Present Value Technique, Subsequent Measurement with Changes in Expected Cash Flows

55-39 This Case is the same as Case A with respect to initial measurement of the asset retirement obligation liability. In this Case, the entity's credit standing improves over time, causing the credit-adjusted risk•free rate to decrease by 0.5 percent to 8 percent at December 31, 2004.

55-40 On December 31, 2004, the entity revises its estimate of labor costs to reflect an increase of 10 percent in the marketplace. In addition, it revises the probability assessments related to those labor costs. The change in labor costs results in an upward revision to the expected cash flows; consequently, the incremental expected cash flows are discounted at the current credit-adjusted risk-free rate of 8 percent All other assumptions remain unchanged. The revised estimate of expected cash flows for labor costs is as follows.

Cash Flow Probability Expected Estimate Assessment cash Flows

$ 110,000 30% $ 33,000 137,500 45 61,875 192,500 25 48,125

$ 143,000

55-41 On December 31, 2012, the entity settles its asset retirement obligation by using an outside contractor. It incurs costs of $463,000, resulting in the recognition of a $14,091 gain on settlement of the obligation. The entity wou!d account for the asset retirement obligation as follows.

Asset retlrement obligation liability Outside contractor Gain on settlement of obligatfon

$4n,091 463,000

$ 14,091

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=41 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 20 of28

Initial Measurement of the Asset Retirement Obflgation Ltablltty at January 1, 2003

Expected cash Flows 1/1103

Expected labor costs Allocated ovemead and equipment charges (.80 x $131 ,250) Contractor's markup [ 20 x ($131 ,250 + $105.000)] Expected cash nows before inflation adjustment Inflation factor assuming 4 percent rate for 10 years Expected cash flows adjusted for inflation Market-risk premium ( 05 x $419,637) Expected cash flows adjusted for market risk

Present value using credit-adjusted risk~free rate cf 8.5 percent for 10 years

$

$

s

131 ,250 105,000 47.250

283,500 1.4802

419,637 20.982

440 619

194.879

Subsequent Measurement of the Asset Retirement Obligation Liability Reflecting a Change In Labor Coat Estimate as of December 31, 2004

Incremental expected labor costs (S 143,000 - $131,250) Allocated overhead and equipment charges (. 80 x S 11 ,750) Contractor's markup (-20 x (S 11 . 750 + $9.400)) Expected cash flews before inflation adjustment Inflation factor assuming 4 percent rate for 8 years Expected cash flows ad1usted for inflation Market-risk premium (.05 x $34,735) Expected cash flows adjusted for market risk Expected present value of Incremental liability using credit-adjusted riskfree rate or 8 percent for 8 years

Incremental Expected Cash Flows 12/31/04

s

$

$

11.750 9.,400 4,230

25,380 1.3686 34,735

1,737 36,472

19,704

http://www.pwccomperio.com/JASDocViewer.aspx?Topic=410&SubTopic=20&docid=41 ... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Page 21 of28

Interest Method or Allocation

Llablllty Change In Cash Liability Year Balance 1/1 Accretion Flow Estimate Balance 12/31

2003 $ 194,879 $ 16,565 $ 211,444

2004 211.444 17,973 $ 19,704 249,121 (~) 2005 249.121 21 ,078 270,199 2006 270,199 22.862 293,061 2007 293,061 24,796 317,857 2008 317,857 26,894 344,751 2009 344,751 29,170 373,921 2010 373,921 31,638 405,559 2011 405,559 34,315 439,874 2012 439,874 37,217 477,091

Schedule or Expenses

Accretion Depreciation Year-End Expense Expense Total Expense

2003 $ 16,565 s 19,488 s 36,053 2004 17,973 19,488 37,461 2005 21,078 21,951 43,029 2006 22,862 21,951 44,813 2007 24,796 21 ,951 46,747 2008 26,894 21,951 48,845 2009 29,170 21,951 51,121 2010 31,638 21 ,951 53,589 2011 34,315 21,951 56,266 2012 37,217 21 ,951 59,168

(a) The remainder of this table is an aggregation of two layers: the original liability, which is accreted at a rate of 8.5%, and the new incremental liability, which is accreted at a rate of 8.0%.

http://www.pwccomperio.com/JASDoc Viewer.aspx?Topic=4 I 0&SubTopic=20&docid=4 I... 4/29/2014

Doss Rebuttal Exhibit 1 E-7, Sub 1214

Journal Entries

January 1, 2003: Long-lived asset (asset retirement cost)

Asset retirement obligation liability To record the Initial fair value of the asset retirement obllgatloo liabilty

December 31, 2003: Depreciation expense (asset retirement cost)

Accumulated depreciation To record straight-line depreciation on the asset retirement cost

Accretion expense Asset retirement obligation liability

To record accretion expense on the asset retirement obligation liability

December 31, 2004: Depreciation expense (asset retirement cost)

Accumulated depreciation To record straight-line depreciation on the asset retirement cost

Accretion expense Asset retirement obligation llabtl lty

To record accretion expense on the asset retirement obligation liability

Long-lived asset (asset retirement cost) Asset retirement obligation liabt1ity