Don’t go in circles.

9

Build the right defense for modern crimes with Integrated Financial Crimes Management. Don’t go in circles. Whitepaper

Transcript of Don’t go in circles.

Build the right defense for modern crimes withIntegrated Financial Crimes Management.

Don’t goin circles.

Whitepaper

01Introduction

03Current Challenges in

Modernizing and

Integrating Financial

Crime

Key challenges

experienced by Financial

Crime functions in

technology areas

04The Way Ahead:

Modernizing and

Integrating Financial Crime

05Accelerating

Investigations with

Intelligent Automation

& Analytics

The Shift to Tech-enabled

"Fusion" model to defend

Financial Crimes

An Approach for

Consistent (Single Pane

of Glass) View

About the Authors

06How are we helping

other banks in this

transformation? 07Conclusion

Contents

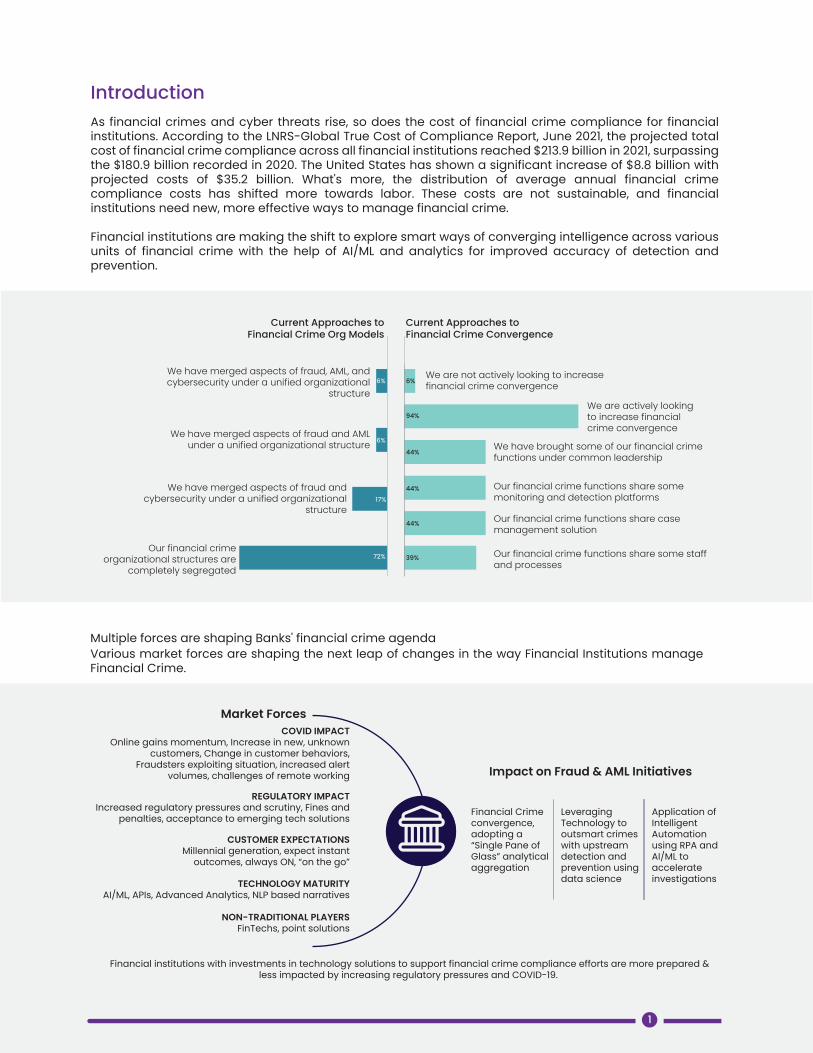

IntroductionAs financial crimes and cyber threats rise, so does the cost of financial crime compliance for financial institutions. According to the LNRS-Global True Cost of Compliance Report, June 2021, the projected total cost of financial crime compliance across all financial institutions reached $213.9 billion in 2021, surpassing the $180.9 billion recorded in 2020. The United States has shown a significant increase of $8.8 billion with projected costs of $35.2 billion. What's more, the distribution of average annual financial crime compliance costs has shifted more towards labor. These costs are not sustainable, and financial institutions need new, more effective ways to manage financial crime.

Financial institutions are making the shift to explore smart ways of converging intelligence across various units of financial crime with the help of AI/ML and analytics for improved accuracy of detection and prevention.

Multiple forces are shaping Banks' financial crime agendaVarious market forces are shaping the next leap of changes in the way Financial Institutions manage Financial Crime.

6%6%

6%

17%

72%

94%

44%

44%

44%

39%

Current Approaches toFinancial Crime Org Models

We have merged aspects of fraud, AML, andcybersecurity under a unified organizational

structure

We are not actively looking to increasefinancial crime convergence

We have brought some of our financial crimefunctions under common leadership

Our financial crime functions share somemonitoring and detection platforms

Our financial crime functions share casemanagement solution

Our financial crime functions share some staffand processes

We are actively looking to increase financialcrime convergenceWe have merged aspects of fraud and AML

under a unified organizational structure

We have merged aspects of fraud andcybersecurity under a unified organizational

structure

Our financial crimeorganizational structures are

completely segregated

Current Approaches to Financial Crime Convergence

Market ForcesCOVID IMPACT

Online gains momentum, Increase in new, unknown customers, Change in customer behaviors,

Fraudsters exploiting situation, increased alert volumes, challenges of remote working

REGULATORY IMPACTIncreased regulatory pressures and scrutiny, Fines and

penalties, acceptance to emerging tech solutions

CUSTOMER EXPECTATIONSMillennial generation, expect instant

outcomes, always ON, “on the go”

Financial Crime convergence, adopting a “Single Pane of Glass” analytical aggregation

Leveraging Technology to outsmart crimes with upstream detection and prevention using data science

Application of Intelligent Automation using RPA and AI/ML to accelerate investigationsTECHNOLOGY MATURITY

AI/ML, APIs, Advanced Analytics, NLP based narratives

NON-TRADITIONAL PLAYERSFinTechs, point solutions

Impact on Fraud & AML Initiatives

Financial institutions with investments in technology solutions to support financial crime compliance efforts are more prepared &less impacted by increasing regulatory pressures and COVID-19.

1

Pandemic Influenced New Normal

The Unrelenting Regulatory Focus

Customer Expectations

The Technology Edge

Financial crime prevention and management is dealing with an unprecedented change, and financial institutions need flexible, efficient, more collaborative, and smarter ways to deal with it. Agile, automated, and proactive mitigation techniques will reduce labor costs and bring consistency and standardization to the process. However, you can't fix what you can't see. The fragmented and silo-ed systems provide little to no intelligence from the other side to help better prevention, detection and investigation of financial crime, be it fraud or AML. An integrated approach, with data and analytics at its core will provide vital insights and intelligence to connect the dots and identify crimes that would otherwise go undetected. This puts the financial institutions on a stronger footing to fulfil their regulatory obligations, protect the bank from risks and create a safer banking environment for their customers, thus adding business value. The time is ripe for banks to start converging intelligence across various units of financial crime, namely Fraud, AML, KYC, and Case Management, etc. for an improved financial crime risk management.

While the pandemic-related restrictions accelerated the digital transformation journeys, making it imperative for customers to get onto the digital bandwagon, it also made it easier for fraudsters to target individuals and financial institutions. The speed and sheer volumes of the Paycheck Protection Program (PPP) increased loan fraud as unprepared financial institution systems dealt with quickly rolling out the program. Changing customer behaviors and increased digital payments have added to the fraud potentials with social engineering, phishing, and identity threats.

The regulators are continuously pushing the envelope on the AML and customer protection laws. For example, the AML Act of 2020 became law on January 1, 2021. In addition, the US National AML/CFT Priorities were published in July 2021, requiring Financial Institutions to ensure their programs identify and update their risk assessments and customer risk scoring while ensuring that monitoring scenarios detect the activity.

There is also an increased regulatory focus and pressure on US institutions towards consumer protection as Consumer Finance Protection Board gears up to play an active role in overseeing and examining financial institutions.

While the pandemic-related restrictions accelerated the digital transformation journeys, making it imperative for customers to get onto the digital bandwagon, it also made it easier for fraudsters to target individuals and financial institutions. The speed and sheer volumes of the Paycheck Protection Program (PPP) increased loan fraud as unprepared financial institution systems dealt with quickly rolling out the program. Changing customer behaviors and increased digital payments have added to the fraud potentials with social engineering, phishing, and identity threats.

One of the key directives the AML Act of 2020 provides to FinCEN is to modernize its software systems. The law also directs regulators to remove barriers impeding financial institution technology modernization. Improving technology Leveraging emerging technology will bring many benefits, such as allowing financial institutions to move financial crime compliance applications from on-premises to the cloud, data aggregation strategies, and exploring the application of AI/ML, visual analytics, API infrastructure to be more interoperable. Institutions can take diverse approaches of either implementing a single system or work on building a logical end-to-end Financial Crime Management system, taking the best solutions in each area and integrating them to construct a system best suited for them.

2

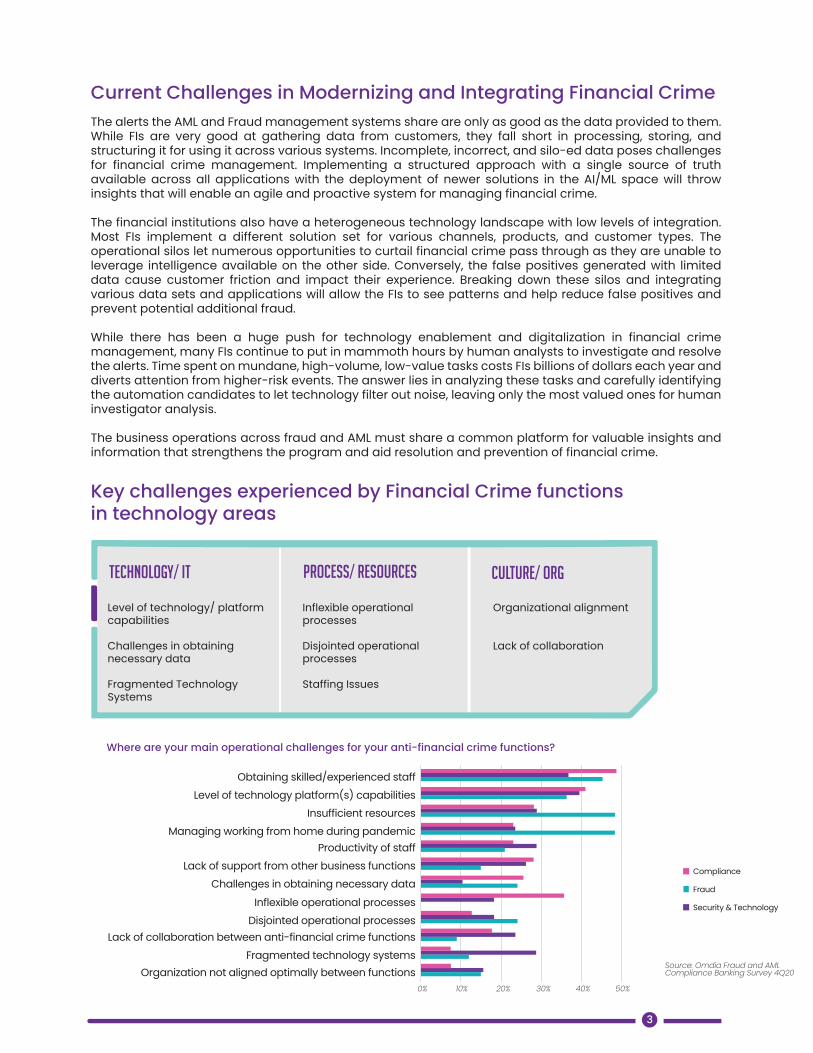

Current Challenges in Modernizing and Integrating Financial CrimeThe alerts the AML and Fraud management systems share are only as good as the data provided to them. While FIs are very good at gathering data from customers, they fall short in processing, storing, and structuring it for using it across various systems. Incomplete, incorrect, and silo-ed data poses challenges for financial crime management. Implementing a structured approach with a single source of truth available across all applications with the deployment of newer solutions in the AI/ML space will throw insights that will enable an agile and proactive system for managing financial crime. The financial institutions also have a heterogeneous technology landscape with low levels of integration. Most FIs implement a different solution set for various channels, products, and customer types. The operational silos let numerous opportunities to curtail financial crime pass through as they are unable to leverage intelligence available on the other side. Conversely, the false positives generated with limited data cause customer friction and impact their experience. Breaking down these silos and integrating various data sets and applications will allow the FIs to see patterns and help reduce false positives and prevent potential additional fraud. While there has been a huge push for technology enablement and digitalization in financial crime management, many FIs continue to put in mammoth hours by human analysts to investigate and resolve the alerts. Time spent on mundane, high-volume, low-value tasks costs FIs billions of dollars each year and diverts attention from higher-risk events. The answer lies in analyzing these tasks and carefully identifying the automation candidates to let technology filter out noise, leaving only the most valued ones for human investigator analysis. The business operations across fraud and AML must share a common platform for valuable insights and information that strengthens the program and aid resolution and prevention of financial crime.

Key challenges experienced by Financial Crime functions in technology areas

Where are your main operational challenges for your anti-financial crime functions?

Process/ Resources Culture/ OrgTechnology/ IT

Level of technology/ platform capabilities

Challenges in obtaining necessary data

Fragmented Technology Systems

Inflexible operational processes

Disjointed operational processes

Staffing Issues

Organizational alignment

Lack of collaboration

Obtaining skilled/experienced staffLevel of technology platform(s) capabilities

Insufficient resourcesManaging working from home during pandemic

Productivity of staffLack of support from other business functions

Challenges in obtaining necessary dataInflexible operational processes

Disjointed operational processesLack of collaboration between anti-financial crime functions

Fragmented technology systemsOrganization not aligned optimally between functions

Compliance

Fraud

Security & Technology

Source: Omdia Fraud and AML Compliance Banking Survey 4Q20

0% 10% 20% 30% 40% 50%

3

The Way Ahead: Modernizing and Integrating Financial CrimeMany Financial Institutions are exploring the unification of their Anti-Fraud and Anti Money Laundering efforts and establishing more formal mechanisms for collaboration between the two operations, technology infrastructure, and intelligence & data sharing. However, the collaboration must be achieved at multiple levels to yield true cost and effectiveness benefits to the organization.

The most important activity is the Organization & Process Alignment for Centralized "Fusion Center" model for better collaboration & coordination. This can be achieved through multiple ways – either a hard-wired "fusion" of the functions under a single head or a more flexible and collaborative approach of virtual teams. Either way, for culture and mindset to change, alignment of organization, the right technology application, and connected data sets form the basic blocks of success.

At the foundation level, the initiatives need to be supported with centralized and consistent data sourcing across domains, channels, and products to enable combined intelligence. The "Single source of truth" data foundation can then be instrumental in the creation of an integrated eco-system with a 3600 customer view across domains offering a "Single Pane of Glass" view to the applications and investigators alike.

Advanced analytics and AI/ML-enabled automation provide levers to accelerate investigations through automation and move a proactive and more accurate system.

An Approach for Consistent (Single Pane of Glass) ViewFinancial Institutions aiming at converging fraud and AML initiatives must start by setting a vision for integrated financial crime management. They must then assess their existing maturity and start small on the path while continuing to build on their success in a phased approach. SLK supports assessments with their *Integrated Financial Crime Maturity Matrix along with the banks teams to come up with the current and desired state and chart a roadmap to reach there.

Organization & Process Alignment for Centralized “Fusion Center” model for better collaboration & co-ordination

Analytics to shift to preventive measures

Automation to accelerate the investigations

Single Pane of Glass - Integrated eco-system with a 3600 customer view across domains

Centralized, consistent data sourcing across domains to enable combined Intelligence

The Shift to Tech-enabled "Fusion" model to defend Financial Crimes

Bringing teams together and enabling them with an integrated view of intelligence to solve and prevent financial crimes

C U L T U R E | O R G A N I Z A T I O N | T E C H N O L O G Y | D A T A

4

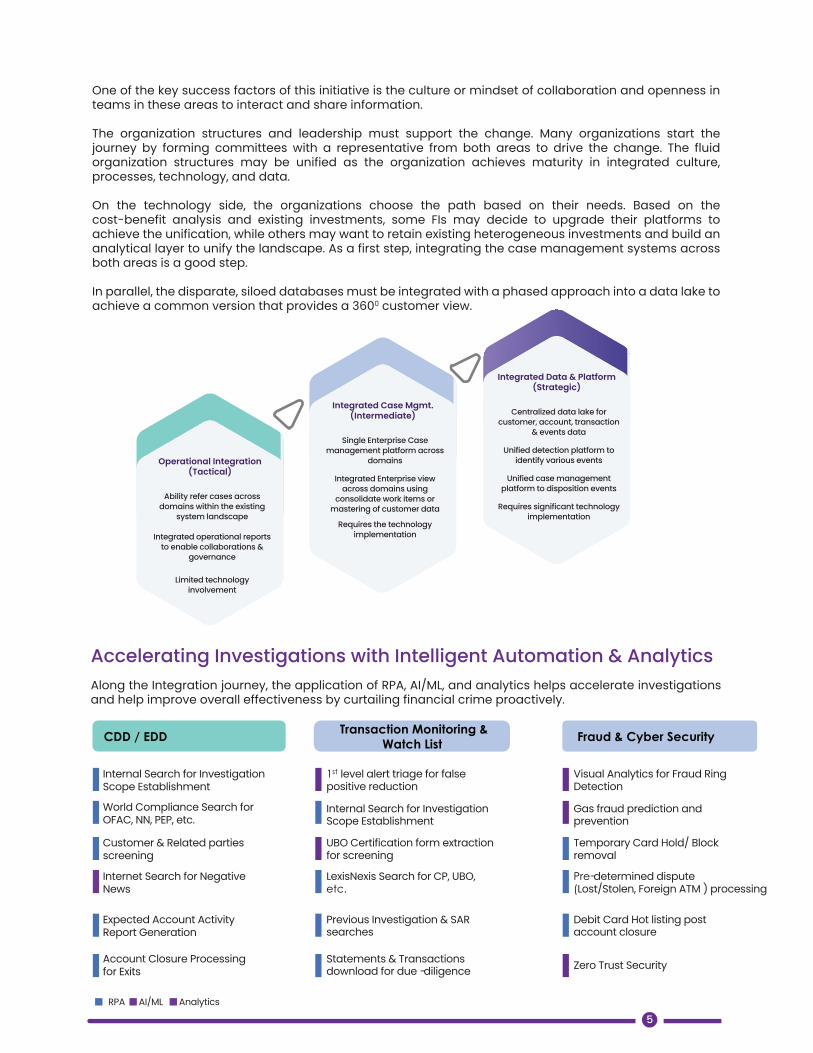

One of the key success factors of this initiative is the culture or mindset of collaboration and openness in teams in these areas to interact and share information.

The organization structures and leadership must support the change. Many organizations start the journey by forming committees with a representative from both areas to drive the change. The fluid organization structures may be unified as the organization achieves maturity in integrated culture, processes, technology, and data.

On the technology side, the organizations choose the path based on their needs. Based on the cost-benefit analysis and existing investments, some FIs may decide to upgrade their platforms to achieve the unification, while others may want to retain existing heterogeneous investments and build an analytical layer to unify the landscape. As a first step, integrating the case management systems across both areas is a good step.

In parallel, the disparate, siloed databases must be integrated with a phased approach into a data lake to achieve a common version that provides a 3600 customer view.

Operational Integration(Tactical)

Ability refer cases across domains within the existing

system landscape

Integrated operational reports to enable collaborations &

governance

Limited technology involvement

Integrated Case Mgmt.(Intermediate)

Single Enterprise Case management platform across

domains

Integrated Enterprise view across domains using

consolidate work items or mastering of customer data

Requires the technology implementation

Integrated Data & Platform(Strategic)

Centralized data lake for customer, account, transaction

& events data

Unified detection platform to identify various events

Unified case management platform to disposition events

Requires significant technology implementation

Accelerating Investigations with Intelligent Automation & AnalyticsAlong the Integration journey, the application of RPA, AI/ML, and analytics helps accelerate investigations and help improve overall effectiveness by curtailing financial crime proactively.

CDD / EDD

Expected Account ActivityReport Generation

Customer & Related partiesscreening

World Compliance Search forOFAC, NN, PEP, etc.

Internal Search for InvestigationScope Establishment

Transaction Monitoring &Watch List

1st level alert triage for false positive reduction

Internal Search for Investigation Scope Establishment

UBO Certification form extraction for screening

LexisNexis Search for CP, UBO, etc.

Fraud & Cyber Security

Visual Analytics for Fraud Ring Detection

Gas fraud prediction and prevention

Temporary Card Hold/ Block removal

Internet Search for NegativeNews

Previous Investigation & SAR searches

Pre-determined dispute (Lost/Stolen, Foreign ATM ) processing

Debit Card Hot listing post account closure

Account Closure Processing for Exits

RPA AI/ML Analytics

Statements & Transactions download for due -diligence Zero Trust Security

5

How are we helping other banks in this transformation?SLK is well equipped to support banks in their journey with data aggregation strategies, analytics, and automation initiatives, specifically curated for them to provide the first-mover advantage in "Digital Transformation" and a "Fusion" approach to Financial Crime Risk Management.

Built a "Single pane of glass" view for analytical aggregation of data from various sources. We helped a leading bank leverage AI/ML and analytics for proactive and smart decisioning leading to improved accuracy of detection and prevention. By applying Intelligent Automation, the bank was able to accelerate investigations and reduce labor costs.

Automated Enhanced Due Diligence for a leading bank in the US

A leading bank spent significant time gathering and assembling information on high-risk customers as part of the EDD investigation. The lengthy process involved analysts identifying the customer, performing manual external and internal system queries, and then create a narrative and dossier that is manually uploaded.

Automated EDD processes have cognitive capabilities to reduce analyst research time to drive up operational efficiency, create better quality and consistency in the cases, and increase employee satisfaction. We helped our client minimize human intervention and reduced processing time from 3 days to 3-5 hours per case.

Conclusion In an evolving threat landscape, traditional approaches to financial crimes are no longer relevant. Banks and financial institutions need to quickly adopt robust data management, RPA, and AI/ML capabilities and move to the tech-enabled fusion model to defend against financial crimes.

For more information on Integrated Financial Crime Management and to assess your vulnerability with SLK’s proprietary *Integrated Financial Crime Maturity Matrix, please write to [email protected]

KYC, CDD & EDD

Watchlist Monitoring,

Sanctions, PEP

Suspicious Activity

Monitoring

Regulatory Response & Remediation Analytics &

ReportingCTR Processing & Automation

Case Management

Risk Data Sourcing & Integration

12+ Years ofexperience ofexecuting AML &Fraud managementprojects withmultiple RegionalBanks in US

80+ AML and Fraud Management Professionals across the spectrum of implementation

Platform agnostic approach with an ability to take on from anywhere in the life cycle

Strong domain expertise in Financial Crime Risk Management

Robust Data management, RPA and AI/ML capabilities

6

Abbreviations & Full-FormAML: Anti Money LaunderingBSA : Bank Secrecy ActCDD : Customer Due DiligenceCISO : Chief Information Security OfficerCTR : Currency Transaction ReportingCRO : Chief Risk OfficerCRR : Customer Risk RatingEDD : Enhanced Due DiligenceKYC : Know Your CustomerOFAC : Office of Foreign Assets & ControlPEP : Politically Exposed PersonsSAM : Suspicious Activity MonitoringSAR : Suspicious Activity ReportingWLM : Watch List Monitoring

References

LNRS-Global True Cost of Compliance Report, June 2021 FICO OMDIA Fraud and AML compliance platform strategies, March 2021Aite Financial Crime Convergence: Think Collaboration, Not Consolidation, April 2021Accenture Winning at the Point of Attack with Integrated Financial Crime OperationsDeloitte Global Framework for Fighting Financial Crime

About the AuthorsGururaj Karanth, Principal Consultant

Throughout his successful career Guru has been Technology consultant, strategist, thought leader and strong advocate to SLK’s customers in the Financial services industry. Guru has advised clients and led major engagements for super regional banks on their technology strategy, enterprise architecture, solution evaluations and systems development in the area of financial crime risk management

Kulpreet Kaur, Principal Consultant

Kulpreet spearheads SLKs research projects on Banking, Risk and regulatory compliance topics including AML, Fraud, intelligent automation, artificial intelligence among others. Her team conducts research on various topics leveraging industry events and prominent research reports focused on banks, fintechs and other financial institutions. Her focus is on building holistic perspectives through market view supported by SLK’s real experience working with their customers.

SLK takes an Intelligent automation first approach to achieving an enterprise’s central goals. Being a go-to technology & consulting firm for some of the Fortune 500 companies, we recognize the pace at which technology is transforming & its impact. With SLK’s deep understanding of the BFSI domain with serving our 20+ clients & giving them 32% CAGR over 5-years makes us the best partner in the sector.

slksoftware.com