Domestic Credit Rating –Operation and Effectiveness in … 2015-17. Being a permanent member of...

37

CPD SEMINER PAPER ON Domestic Credit Rating – Operation and Effectiveness in Bangladesh At The Institute of Chartered Accountants of Bangladesh (ICAB) By N K A Mobin FCA, FCS, CFC Managing Director & CEO Emerging Credit Rating Ltd. On April 30, 2015

Transcript of Domestic Credit Rating –Operation and Effectiveness in … 2015-17. Being a permanent member of...

CPD SEMINER PAPER

ON

Domestic Credit Rating – Operation and Effectiveness in Bangladesh

At

The Institute of Chartered Accountants of Bangladesh (ICAB)

By

N K A Mobin FCA, FCS, CFC Managing Director & CEO

Emerging Credit Rating Ltd.

On

April 30, 2015

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 2

N K A Mobin FCA, FCS, CFC

Mr. Mobin is one of the sponsor Directors of the Emerging Credit Rating Ltd. (ECRL). Currently he is

the Managing Director and Chief Executive Officer of the company. Professionally a Chartered

Accountant and the fellow member of the Institute of Chartered Accountants of Bangladesh

(ICAB) since 1992 and was an Articled student of KPMG-Rahman Rahman Huq, Chartered

Accountants during 1982-1986. He is also the fellow member of the Institute of Chartered

Secretaries of Bangladesh (ICSB) and a member of the Institute of Financial Consultants

(IFC) of USA. He did completed his BBA and MBA in Finance from University of Dhakaduring

1977-1982.

Mr. Mobin has vast experience in the field of Finance, Accounting, Taxation, System design,

implementation of computerized Accounting and Management (ERP) system, Financial Planning,

Budgeting, Internal Controls, Investment Decision, and Company Secretarial Practices. He has

specifically worked for arrangement of huge financing from local and international Banks and World

agencies couple of times. He had quite some international training and management courses namely

in Stockholm Business School in Sweden, National University of Singapore, INSEAD in France and

also AOTS/HIDA in Japan.

He has an illustrious 23 years professional career (13 years in top management and Board position)

in 4 multinational companies. Prior to joining ECRL, he worked at the biggest multinational

telecommunication Co. named Grameenphone Ltd. for 10+ years in various capacities as Director

Finance, Director Administration, Director Projects and Company Secretary. Before joining

Grameenphone in 1998, he worked in the Swiss pharmaceuticals Co. named Novartis Bangladesh

Limited(Ex Ciba–Geigy) for 3 years as Director Finance and Company Secretary,in multinational

fertilizer company named Karnaphuli Fertilizer Co. Ltd. (KAFCO) for 5 years as Manager

Finance & IT, and in Swedish Match/STORA named Dhaka Match Industries Co. Ltd. for 5 years

as Chief Accountant.

Mr. Mobin is the Vice President of Bangladesh Society for Total Quality Management (BSTQM) and

Advisor to the Executive Committee of Bangladesh Association of AOTS Alumni Society (BAAS) for

2015-17. Being a permanent member of Kurmitola Golf Club (KGC), he is a regular Golf Player and

managed to bag couple of trophies. He is married and having 3 sons.

mobile : +880 1711 500387, +880 1833 330002

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 3

Table of Contents

Introduction: ........................................................................................................................................................ 5

What is Credit Rating? ........................................................................................................................................ 5

What Credit Rating is Not : ............................................................................................................................ 6

Substituting Ratings for Independent Analysis : ........................................................................................ 6

Who Can Perform Credit Rating : ................................................................................................................. 6

Who are the Regulators? ................................................................................................................................... 8

Bangladesh Securities and Exchange Commission (BSEC) : .................................................................... 8

Bangladesh Bank (BRPD) : ............................................................................................................................ 9

Insurance Development and Regulatory Authority (IDRA): ................................................................... 10

Types of Credit Rating Performed by DCRAs Operating in Bangladesh.................................................... 10

Corporate Debt .............................................................................................................................................. 11

Entity ............................................................................................................................................................... 11

Financial Institutions ..................................................................................................................................... 11

Insurance Rating ........................................................................................................................................... 11

Project Finance .............................................................................................................................................. 12

Small and Medium Enterprises (SME) ........................................................................................................ 12

Credit Rating Methodology .............................................................................................................................. 12

Credit Rating Evaluation Process .................................................................................................................... 13

Information Collection .................................................................................................................................. 13

Data Input, Analysis, Scoring & Review .................................................................................................... 14

Rating Score Sheet : ................................................................................................................................. 14

Score To Notch/Rating Symbol: .............................................................................................................. 15

Meaning of Rating Symbols: .................................................................................................................... 16

Rating Outlook:.......................................................................................................................................... 17

Rating Committee : ....................................................................................................................................... 17

Reporting : ..................................................................................................................................................... 17

Benefits of Credit Rating : ............................................................................................................................... 18

BASEL II and Credit Rating : ........................................................................................................................... 19

Basel II in Bangladesh : ................................................................................................................................... 19

PILLAR 1: ........................................................................................................................................................ 20

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 4

PILLAR 2: ........................................................................................................................................................ 20

PILLAR 3: ........................................................................................................................................................ 21

Rating Category Mapping : .............................................................................................................................. 22

Capital Adequacy Ratio (CAR): .................................................................................................................... 23

Risk Based Capital Adequacy: ..................................................................................................................... 23

Risk Weighted Assets (RWA): ..................................................................................................................... 24

Basel III : ........................................................................................................................................................... 24

Changes after implementation of Basel III :............................................................................................. 25

Economic Rationale of Credit Rating : ........................................................................................................... 25

Best Practices in Credit Rating Industry : ...................................................................................................... 27

Best Practices recommended by ADB : ...................................................................................................... 27

Best Practices advocated by ACRAA : ........................................................................................................ 28

Best Practices advocated by International Organization of Securities Commissions (IOSCO) : ....... 28

Performance of DCRA of Bangladesh regarding best practice of compliance : ................................... 29

Emergence of ACRAB : ................................................................................................................................. 29

Credit Rating vs. Auditing : .............................................................................................................................. 30

Criticisms of Credit Rating Agencies : ............................................................................................................ 32

Current Scenario in Bangladesh : ................................................................................................................... 33

Summary and Recommendations : ................................................................................................................ 34

Recommendations: ....................................................................................................................................... 34

Emerging Credit Rating Ltd. – A Brief Profile ................................................................................................ 36

References .......................................................................................................................................................... 37

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 5

Introduction:

This paper is written on the roles and functions of Domestic Credit Rating Agencies (DCRAs) in

Bangladesh. This paper addresses definition of credit rating and its benefits, methodology followed

by DCRAs, context of Basel II, current practices in Bangladesh and recommendation thereon. With

the implementation of Basel II (introduced in Bangladesh by BRPD Circular No- 09, published on

December 31st 2008), in the context of Pillar 1, regulatory capital requirements for credit risk is

calculated according to two alternative approaches: (i) the Standardized Approach; and (ii) the

Internal Ratings-Based Approach. The Standardized Approach is generally conducted worldwide by

independent Credit Rating Agency (CRA) who is licensed by domestic regulators (Bangladesh

Securities and Exchange Commission (BSEC) and Bangladesh Bank (BB) in Bangladesh). Recent

scandals and events has reinforced the need for strict framework and regulatory awareness to

various banks nationwide which furthermore extends the requirement and support of DCRAs to

operate and execute credit rating efficiently. BRPD Circular No- 18 (published on December 21,

2014) issues a roadmap for implementation of Basel-III in Bangladesh and also additional BRPD

Circular No- 01 (published on January 01, 2014) issues external DCRA‟s to perform credit rating of

Small and Medium Enterprise (SME). Therefore the need for DCRAs in a drive to develop the

financial system of Bangladesh is evermore growing.

Credit rating is an independent opinion on ability of a business or a government to repay its debt

obligations. Hence CRAs act as corporate gatekeepers to bridge the gap of asymmetric information

between lenders, investors and issuers about the creditworthiness of companies or business.

What is Credit Rating?

Credit rating is the assessment of the credit worthiness of a particular borrower with reference to a

particular debt or financial obligations. Ability to pay debt is known as “creditworthiness”.1Credit

Rating usually appears in form of alphabetical letter grades such AAA, A+,BBB etc.2 Usually a credit

rating grade is inversely proportional to default risk which means higher the grade lower the risk. A

credit rating can be assigned to any institution that intends to borrow money; any individual,

government, proprietorship business, partnership business, company or a government institution

may opt for credit rating for the purpose of borrowing funds. These are known as entity ratings.

Credit Rating is also applicable for the issuance of commercial papers such bonds; however credit

rating is not applicable for issuance of common stock. Typically the entity who is applying for credit

rating is known as obligor.

An article of S&P states “From a slightly different perspective, credit ratings are a specialized type of

securities research, similar to what independent securities analysts and analysts at sell-side firms

produce. Like such research, credit ratings embody forward-looking opinions designed to contribute

to an investor's decision-making process. However, instead of providing opinions about the overall

1 Rating agencies (and other credit professionals) hold differing views of what constitutes "creditworthiness" or "credit

quality." In broad terms, each explains its view in the definitions of its rating symbols. For an explanation of how Emerging Credit Rating Limited defines creditworthiness, visit www.emergingrating.com 2 Different credit rating institution uses different credit rating scales.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 6

investment merit of specific securities or types of securities (which embodies many different

dimensions, including creditworthiness), a credit rating addresses creditworthiness only. Accordingly,

credit rating agencies operate only in the fixed-income arena, while securities analysts cover the

entire landscape of the capital markets.”3 In addition Peterson [2013] states that an ideal credit

rating should have three major attribute : (i) transparent, (ii) comparable and (iii) forward looking.

What Credit Rating is Not :

Credit Rating only takes financial risk into account and does not consider other risks. One should not

use credit rating as investment advice and should not hold it as recommendation to buy, sell or hold

securities. According to the president of Standard & Poor‟s Douglas L Peterson “Credit Rating

addresses only one aspect of a debt instrument-credit quality”.

Substituting Ratings for Independent Analysis :

US Securities and Exchange Commission advices in one of its publications that credit rating should

be used as supplement and not replacement of an investor‟s own research.4 Using credit rating as

an independent analysis may not give the full picture of an investment as credit worthiness is only

one of the factors which should be considered during making an investment decision. Depending on

the circumstances other factors may arise such as risk free rate, taxability of interest rate, market

technical, structural complexity etc.

Who Can Perform Credit Rating :

Credit Rating Agencies performs credit rating assignments of various entities and debt instruments.

In Bangladesh they are known as External Credit Assessment Institution (ECAI). Elkhoury [2008]

explains that rating agencies falls into two categories: (i) recognized; and (ii) non recognized. The

former are recognized by supervisors in each country for regulatory purposes. In Bangladesh there

are four regulatory authorities: (i) Bangladesh Securities and Exchange Commission; (ii) Bangladesh

Bank; (iii) Insurance Development and Regulatory Authority of Bangladesh; and (iv) Association of

Credit Rating Agencies in Bangladesh. First two regulatory authorities recognize the following eight

local credit rating agencies5:

I. Emerging Credit Rating Ltd (ECRL): ECRL was incorporated in March 2009, with the

view of providing Credit Rating Services in Bangladesh. ECRL obtained credit rating license

from BSEC in June 2010 as per Credit Rating Companies Rules 1996 and also received

Bangladesh Bank Recognition as an External Credit Rating Institution (ECAI) in October

2010. On March 2009 ECRL also established technical collaboration with Malaysian credit

rating company named Malaysian Rating Corporation Berhad (MARC). The company has its

head office in Dhaka and regional offices in Khulna and Chittagong (further details in page

36).

II. Credit Rating Association of Bangladesh Ltd (CRAB): CRAB was established in 2003

and received license from BSEC in 2004. The company has technical collaboration with ICRA,

India. Its head office is situated in Dhaka and the regional offices are in Bogra and

Chittagong.

3 “The Role of Credit Ratings in The Financial System”, May 2012.

4 “The ABCs of Credit Ratings”, SEC Pub. No. 161(10/13).

5 The ECAI descriptions are taken from their websites

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 7

III. Credit Rating Information and Services Ltd (CRISL):CRISL was formed in

1995 as a joint venture between RAM Holdings Malaysia Berhad (RAM), JCR-VIS Credit

Rating Company of Pakistan, few financial institutions and some professionals of Bangladesh.

CRISL‟s head office is situated in Dhaka and it also has two more regional office one in

Chittagong and the other one in Khulna.

IV. National Credit Rating Ltd. (NCRL): Incorporated as a public company, NCR started its

business in 2010 after obtaining license from BSEC. The company has technical collaboration

with Pakistan Credit Rating Agency (PACRA).

V. Alpha Credit Rating Ltd. (ALPHA):ALPHA was incorporated in February 2011. Istanbul

International Rating Services Inc. acts as the technical partner. It has one office in Dhaka.

VI. WASO Credit Rating Company (BD) Ltd. (WASO): WASO started its journey in

February, 2012 with acquiring license from Bangladesh Securities and Exchange Commission

(BSEC) and finally has been recognized by Bangladesh Bank as and ECAI in October 2012.

WASO also has the technical collaboration with Financial Intelligence Services Ltd. (FISL).

WASO has one office in Dhaka.

VII. Argus Credit Rating Services Ltd. (ARGUS): Argus started its journey in 2011 as a joint

venture between Singapore based credit rating company DP Information Group (“DP”) and

local sponsors. The company has one office in Dhaka.

VIII. The Bangladesh Rating Agency Ltd. (BDRAL)[1]: BDRAL is a subsidiary of Dun &

Bradstreet South Asia Middle East Ltd.It obtained license in 2012 and for only to do the SME

Rating. The company has one office in Dhaka.

Apart from these Credit Rating Agencies the Bangladeshi Regulatory Authorities also recognizes the

following international credit rating agencies mainly for sovereign rating.

I. Standard & Poor’s (S&P): S&P is considered one of the Big 3Credit Rating Agencies,

which also include Moody's Investor Service and The Fitch Ratings. It has 26 offices around

the world, and the head office is located on 55 Water Street in Lower Manhattan, New York

City. Standard & Poor's Ratings Services publishes more than a million credit ratings on debt

issued by sovereign, municipal, corporate and financial sector entities. In 2013, it rated $6.6

trillion worth of new debt.

II. The FitchRatings: The firm was founded by John Knowles Fitch on December 24, 1913 in

New York City as the Fitch Publishing Company. It merged with London-based IBCA Limited

in December 1997. In 2000 Fitch acquired both Chicago-based Duff & Phelps Credit Rating

Co. (April) and Thomson FinancialBankWatch (December). Fitch Ratings is the smallest of the

"big three" NRSROs, covering a more limited share of the market than S&P and Moody's,

though it has grown with acquisitions and frequently positions itself as a "tie-breaker" when

the other two agencies have ratings similar, but not equal, in scale.

III. Moody’s Investor Service (Moody’s): Moody's was founded by John Moody in 1909 to

produce manuals of statistics related to stocks and bonds and bond ratings. In 1975, the

company was identified as a Nationally Recognized Statistical Rating Organization (NRSRO)

by the U.S. Securities and Exchange Commission. Following several decades of ownership by

[1]

BDRAL only has license for performing SME rating. Others may perform all kinds of rating.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 8

Dun & Bradstreet, Moody's Investors Service became a separate company in 2000;

Moody's Corporation was established as a holding company.

Who are the Regulators?

The U.S. Congress passed the Credit Rating Agency Reform Act of 2006, allowing the United States

Securities and Exchange Commission (SEC) to regulate the internal processes, record-keeping and

certain business practices of CRAs. The Dodd-Frank Wall Street Reform and Consumer Protection

Act of 2010 further grew the regulatory powers of the SEC, including requiring a disclosure of credit

rating methodologies. The European Union has never produced a specific or systematic legislation or

created a singular agency responsible for the regulation of CRAs. There are several EU directives,

such as the Capital Requirements Directive of 2006, that affect rating agencies, their business

practices and their disclosure requirements. Most directives and regulations are the responsibility of

the European Securities and Markets Authority. For Domestic CRA of Bangladesh‟s regulatory

agencies and their guidelines are listed below:

Bangladesh Securities and Exchange Commission(BSEC) :

Bangladesh Securities and Exchange Commission (BSEC) has been one of the prime regulators for

CRA, along with the authority to issue license and quarterly monitoring of CRA‟s, it also oversees the

compliance requirement and rules laid down by Credit Rating Companies Rules 1996.

Credit Rating Companies Rules 1996

Credit Rating Companies Rules 1996 has been in effect from July 2006 conferred by Securities and

Exchange Ordinance 1969 to regulate the business of Credit Rating Companies. This rules states

that no issue of debt at a premium shall be made by an issuer unless the issue is rated by a credit

rating company and declaration about such rating is given. Credit Rating Company has been defined

in the rules as an investment adviser company which intends to engage in or is so engaged primarily

in the business of evaluation of credit or investment risk through a recognized and formal process of

assigning rating to present or proposed loan obligations or equity of any business enterprise. The

rules give basic guidelines such as eligibility for registration and states that a company proposing to

commence business as a credit rating company shall be eligible for registration if: (a) such a

company is incorporated as a public limited company (b) such company have paid up capital of at

least 50 lakh taka (c) such company has technical collaboration arrangement with a reputed credit

rating company and others.

The rules further provides for registration procedure in Rule 5 and power of the Commission to

cancel or suspend registration in Rule 6. Through Rule 8, the Commission made it compulsory for all

credit rating companies to submit its quarterly reports in writing to the Commission. Rule 9 has been

inserted vide Notification No. SEC/CMRRCD/2001-27/01 dated November 17, 2009, which includes

operation procedures of credit rating companies to be adopted. It includes requirements for

improving quality of rating process, monitoring and updating operation of Credit Rating Company,

requirements for standard agreement, requirements for improving integrity of rating process,

independence of employees and defines conflict of interest, procedures and policy to be followed by

Credit Rating Company, transparency and timeliness of rating disclosure, on treating confidential

information, communicating with market participants about Credit Rating Company.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 9

The rules require Companies to establish rating methodologies and disclose to its website. All

analysts are required to use them duly and Rating Committee (consisting of 5 members) shall review

the rating criteria at least once every year and amend the rating methodology if necessary. The

review shall be made with the outcome of internal and external research, best practice and historical

experience. Not only those, companies are also required to prepare written procedures for obtaining

rating and disclose such procedures to its website. The rating companies shall ensure that it has

sufficient number of rating analysts having appropriate knowledge, skill, experience and access to

sufficient quality information. If any rating involves a type of financial product with limited historical

data, analyst shall disclose clearly the limitations in the rating report. Rating teams shall be

composed of at least two analysts in order to make objective assessment with different viewpoints.

Also, an Internal Review Committee (IRC) comprising of appropriate professionals shall double check

the documents and information on which the analysts make ratings. Further to this, rule 10 deals

with powers of the Commission to inspect and investigate Credit Rating Companies.

Limitations of Credit Rating Companies Rules 1996:

Rule 6 mentions that the Commission has power to cancel or suspend the registration of a credit

rating company if the company has contravened any provision or has otherwise failed to comply

with any requirement of the 1969 Ordinance or any rules given by the Commission if it considers

necessary in the public interest to do so. There are many rules in Credit Rating Companies Rules

1996 which have been made according to international standard practice but which need to be

revised or rephrased according to practical scenario of Bangladesh. Hence, it is not possible to fulfill

all the requirements of the rules and contravention of such rules may make it liable to have

registration cancelled. It may be proposed to the Commission to make an amendment to the rules to

incorporate more definite and concrete situations where credit rating companies can have their

registration cancelled or suspended.

No definition/description has been given of compliance report submission in rule 4(g). Compliance

issues have not been defined properly and work of a compliance officer needs to be addressed

more. Professional qualification has not been described in the rules such as analyst when

reviewing/analyzing or rating a certain company or an industry, their level of qualification has not

been described in details. This is a major issue which needs to be addressed in more details.

Bangladesh Bank (BRPD):

Credit Rating Companies (“Company”) are also being regulated by Bangladesh Bank through various

circulars, policy and guidelines. To perform credit assessment, credit rating companies must be

recognized as an External Credit Assessment Institution (ECAI) under the Risk Based Capital

Adequacy Framework (Basel II) issued by Bangladesh Bank. Through this recognition, companies

must comply with certain requirements. Those requirements are that credit worthiness rating

assessed should be independent, consistent and free from conflict of interest. Further to that, it is

suggested that rating methodology should cover at least analysis of the risk factors supported by

scoring as approved by Bangladesh Bank. The company should maintain an undisrupted and

continuous database management system using both solicited and unsolicited credit ratings. The

recognition given by Bangladesh Bank will be reviewed annually and it is expected that

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 10

methodologies and credit assessments remain appropriate over different periods of time

and in case of changes in market conditions. The company is also required to disclose credit rating

reports of related parties quarterly to the Bangladesh Bank after the assessment is final.

Other than the recognition, credit rating companies are also governed by the circulars and guidelines

issued by Bangladesh Bank from time to time. Banking Regulation and Policy Department (BRPD)

issued Circular No.05 dated May 29, 2004 which made it mandatory for the banks to have

themselves credit rated to raise capital from capital market through IPO. Further to that, from

January 2007, in BRPD Circular No. 07 dated July 05, 2006 it has been decided for all banks to have

themselves credit rated by a Credit Rating Company. Such credit rating reports of the banks will be

submitted to Bangladesh Bank and non-compliance of any provision of the circular will be a breach

of Banking Companies Act 1991.

Another circular issued by Bangladesh Bank is BRPD Circular No. 01 dated January 01, 2014

regarding Small and Medium Enterprises (SME). Bangladesh Bank has developed a “Credit Rating

Methodology for Small and Medium Enterprises” which will ensure uniformity, larger levels of

transparency of external credit assessment and thereby determine the relative creditworthiness of

entities belonging to this segment. The credit risk assessment in this segment requires a specific

approach, as the factors affecting the creditworthiness differ from those compared to large

corporate entities and other institutions.

Limitationsof Bangladesh Bank Regulations:

Although Bangladesh Bank states in its recognition that credit rating companies should perform their

rating assessment free from any conflict of interest, however, the term “conflict of interest” has not

been defined anywhere in circulars or policy or any guidelines. It is also not clear whether all the

credit rating reports should be sent to Bangladesh Bank or not. Since, in the recognition given by

Bangladesh Bank, it is mentioned that disclosure should be made of credit rating reports of “related

parties” quarterly to the Bangladesh Bank. In the recognition given, “related parties” is not given

any clarified meaning.

Insurance Development and Regulatory Authority (IDRA):

For credit rating assessment of insurance companies, the respective regulatory authority is

Insurance Development and Regulatory Authority Bangladesh (IDRA). To perform credit assessment,

credit rating companies can be recognized as a Credit Rating Institution by IDRA. Circular of Chief

Controller of Insurance No. 21/21/98-376 dated 27 March 2007 requires all general insurance

companies to get credit rating assessment once a year and all life insurance companies to get credit

rating assessment every two years. Further to that, a circular issued by Banking Regulation and

Policy Department (BRPD) No.06 dated March 13, 2011 also made it mandatory for general

insurance companies to get credit rating assessment.

Types of Credit Rating Performed by DCRAs Operating in Bangladesh

While carrying out a Credit Rating assignment, the process is guided by rating methodology which

sets the framework to execute credit rating analysis. Keeping in mind the various industry segment

and client requirements, the following types of credit rating is practiced.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 11

Corporate Debt

Corporate Debt Rating is an analysis of the issue structure and terms on the other hand would

evaluate the suitability of the instrument in the context of the Company‟s business model and

financial profile. Also evaluated are the competencies and track record of management and other

qualitative factors such as parent strength, formal support agreements and ownership. Industry

outlook is considered to evaluate the level of risk involved in participating in a particular business or

businesses. Some of the pertinent factors out of the many to be considered would be demand

growth, pricing flexibility, research and development requirements, barriers to entry and regulatory

framework where appropriate, and benefits of diversification. The ratee‟s sensitivity to economic

cycles will require more conservative financial profiles/ policies on the part of the ratee to offset its

inherent earnings variability. This form of rating assesses the probability of timely repayment of

principal and payment of interest over the term till the maturity of such debts.

Entity

The common methodology used to analyze Corporate Debt Rating can be similarly applied to Entity

Rating. This form of rating assesses the probability of timely repayment of principal and payment of

interest over the term till the maturity of all debt obligations that the entity hold at that date. Since

it not only analyzes the individual characteristics of a particular borrowing based on their specific

structure, and terms and conditions, therefore it does not comment on each individual borrowing;

instead entity rating gives a generalized opinion on all borrowings of the rated entity. This form of

rating also includes IPO (Initial Public Offering) rating.

Financial Institutions

Financial Institution Ratings are applied to assess the creditworthiness of financial institutions (FI).

The FI rating process works through sovereign and macro-economic issues; the financial sector

outlook and regulatory trends; the FI‟s business profile (including strategy); and eventually to the

CAMELS rating components. The CAMELS framework that is also employed by national bank

regulators is largely supported by both theoretical and empirical literature and comprises capital

adequacy, asset quality, management quality, earnings, liquidity and sensitivity to market risk.

Insurance Rating

This form of rating assesses the credit-worthiness of insurance companies, both general and life

insurance, i.e. the financial security characteristics of the insurance company and its ability to meet

its policy holder obligations.

1. General Insurance

It assesses the financial security characteristics of an insurance company with respect to its

ability to meet its obligations to policyholders in accordance with the terms of their insurance

contracts. When rating insurance companies, analyst‟s consider macroeconomic factors,

industry dynamics including regulatory issues, and individual company performance. The

analyst examines how economic factors affect the company‟s growth opportunities and

financial condition. In-depth analyses are then made of the insurer‟s business, management

and corporate strategy, operating and underwriting performance, investment, liquidity,

capitalization, reserves and reinsurance arrangements.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 12

2. Life Insurance

The common methodology used to analyze general insurers can be similarly applied to life

insurers. Life companies display inherently superior operating stability compared to general

insurers due to the high degree of predictability of claims outcome using mortality and

morbidity tables. The life industry has been experiencing softening demand for the more

traditional protection policies, with shifting consumer preference towards savings and

investment products. Also gaining popularity are products covering critical illness and medical

care, due to the concern over the rising cost of health care.

Project Finance

Generally, project finance involves raising of funds to finance a project (usually with limited

recourse) in which the investors or providers of the funds focuses on the future cash flows from the

project (usually secured through an off take agreement) which serve as the primary source of funds

to service and repay the loans taken to finance the project and/or provide the return on their equity

invested.

The ability to repay principal and interest in a timely manner, which is what analyst‟s rate, is

dependent on the success of a single specific project or a series of project facilities. The project

rating focuses on identifying specific project risks, understanding how they affect credit quality and

assessing the strength of mitigating measures.

Small and Medium Enterprises (SME)

The rating of Small and Medium Enterprises (SME) indicates relative level of creditworthiness of an

SME entity in relation to other SMEs. This form of rating considers these factors among others:

industry characteristics, operating efficiency, competitive position, management quality, financial risk

characteristics, relationship with lenders and capital structure to evaluate overall risk profile of the

SME entity.

Credit Rating Methodology

Credit Rating Methodology is the manual or set of guidelines which is used to rate a company. Based

on these guidelines a score sheet is developed and is used for credit rating purpose. At first the

ECAI prepares the credit rating methodology and score sheet then submits it to the Regulatory

Authorities for the purpose of gaining approval. After gaining approval the ECAI posts its rating

methodology in the website. Different credit rating methodologies are designed keeping different

objectives in mind; Bhatia [2002] explains that sovereign rating methodology of S&P‟s rating seeks

capture only the probability of the occurrence of default, not the severity of default and provides no

assessment of expected time in default, mode of default resolution, or recovery values more

generally. Moody‟s rating focus on expected loss, which is a function of both probability of default

and the expected recovery rate, after default has occurred. Fitch ratings are hybrid focusing on

probability of default until the point default has occurs, and differentiating on the basis of expected

recovery rates after default has occurred.

To avoid this specific problem sometimes the regulatory authority lays down guideline for designing

methodology. For example Bangladesh Bank Circular stated “Both quantitative and qualitative

factors should be considered in assessing the SME operation. The methodology is comprehensive

where assessment area concentrates five broad categories– Financial Risk, Business/Industry Risk,

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 13

Management Risk, Bank Relationship Risk, Financial Security Risk and others. Although, the

above concentration areas are in line with corporate rating methodology, the relative weightage for

different parameters may differ in between the two sectors. The financial position (i.e. Balance

Sheet and Income Statement) and Cash flow Statement may be collected as per accounting

Standard provided by concerned regulators that may either be audited or signed by the appropriate

authority. “6

Credit Rating Evaluation Process

Credit rating is an independent opinion on ability of a business or a government to repay its debt

obligations. Since the assignment itself entails a vast arena of information and analysis, data

collection and research forms the base of the evaluation process.

Information Collection

Information collection is in the form of both primary and secondary information. Once a legal

agreement is formed between the client and CRA, the CRA initiates the process of collecting

information. Since modernization and the use of accounting law and guidelines were neglected by

previous generation owners, the visibility of income and expense is blurred by various clients to

restrict disclosure of information. It is also observed in various times that many client also produces

several financial statements each to cater different purpose7. Moreover, it has also been witnessed

that many limited companies although are required to prepare audited financial statements are not

abiding by the rule set out by The Companies Act 19948. However, imposition of banking and

various association rules to some extend have tutored local businesses to maintain a certain set of

paperwork which needs to be further refined to help the flow of information and its visibility.

Contrasting this scenario to the practice followed internationally, many Asian countries face the

6 “Amendment of Guidelines of Risk Based Capital Adequacy (RBCA)”, January 2014

7 “Regulators Must Enforce Ethical Standard In the Business”, The Daily Star,2014

8Credit Rating Companies Rules 1996

Collect Information

Data Input, Analysis, Scoring &

Review

Approval from

Rating Committee

Draft Sent

Final Report Print, Delivery & Published to

Authority

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 14

same scenario, whereas most Western Countries face relative ease in collection of

authenticated information.

Data Input, Analysis, Scoring & Review

Subsequent to collection of valid and relevant information from every possible source, the CRA

incorporates it into the software or specially designed format which has been acquired from the

CRA‟s International Technical partner. Once incorporated, the formats generate various aspect of

analysis, however, physical verification, information obtained from industry, peers, banks,

government institutions, etc. are also incorporated to form an overall understanding of the business

in the current context in addition to understanding its future position. During this stage, CRA‟s make

use of various financial models; whichever fit in the context of Bangladesh, to present their

analytical findings.

Rating Score Sheet :

Risk Variables Weighting Initial Total Remarks

1.0 Industry Analysis

Industry Outlook 10.00% 2.5

0.25

Stock Market Review 5.00% 1.75 0.09

2.0 Business Risk Analysis

Market Outlook 10.00% 1.75

0.18

Competitive / Industry position 10.00% 1.00

0.10

Operating Risk 15.00% 1.25

0.19 3.0 Financial Risk

Profitability

15.00% 1.25

0.19

Liquidity & Financial Flexibility 10.00% 1.25

0.13

Capital Structure 5.00% 1.75

0.09

Cashflow Coverage 10.00% 1.25

0.13

4.0Management and Other Qualitative Factors 10.00% 1.50

0.15

Weighted Score 100.00% 15.25

1.48

RATING AAA

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 15

Score To Notch/Rating Symbol:

Score Definition Rating Weighted Score

AAA 1.00 - 1.50

1.00 Well Below Average Risk

AA + 1.51 - 1.75

1.25

AA 1.76 - 2.00

1.50

AA- 2.01 - 2.25

1.75

Below Average Risk A+ 2.26 - 2.50

2.00

A 2.51 - 2.75

2.25

A- 2.76 - 3.00

2.50

Average Risk

BBB+ 3.01 - 3.20

2.75

BBB 3.21 - 3.40

3.00

BBB- 3.41 - 3.60

3.25

BB+ 3.61 - 3.80

3.50

BB 3.81 - 4.00

3.75 Above Average Risk

BB- 4.01 - 4.20

4.00

B+ 4.21 - 4.40

4.25

B 4.41 - 4.60

4.50

Well Above Average Risk B- 4.61 - 4.80

4.75

C 4.81 & Above

5.00

D Not Classified

The meaning of the each rating symbol or notch is enumerated in two tables in the next page.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 16

Meaning of Rating Symbols:

AAA - Ability to repay principal and pay interest on a timely basis is extremely high

AA - Very strong ability to repay principal and pay interest on a timely basis

A - Ability to repay principal and pay interest is strong

BBB - The lowest investment grade category; indicates an adequate capacity to repay principal and pay interest

BB - While not investment grade, this rating suggests that likelihood of default is considerably less than for lower-rated issues.

B - Indicates a higher degree of uncertainty, and therefore, greater likelihood of default.

C - High likelihood of default, with little capacity to address further adverse changes in financial circumstances.

D - Payment in default.

High

Low

AAA Extremely Strong

AA Very Strong

A Strong

BBB Adequate

BB Less Vulnerable

B More Vulnerable

CCC Currently Vulnerable

CC Currently Highly Vulnerable

D Default

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 17

Rating Outlook:

Rating Outlook

DCRA‟s Rating Outlook assesses the potential direction of a particular Rating over the intermediate

term (typically over one to two-year period). The Rating Outlook may either be :

POSITIVE which indicates thata rating may be raised;

NEGATIVE which indicates that a rating may be lowered;

STABLE which indicates that a rating is likely to remain unchanged; or

DEVELOPING which indicates that a rating may be raised, lowered or remain unchanged.

Rating Committee :

Once all the findings and analysis is concluded, it is presented to a selected board of members in

Rating Committee9. It comprises of appropriate professionals who shall double check the documents

and information on which the analysis was made. The credit rating report is scrutinized along with

sources of information, physical verification, analysis method, business perspective, etc. Once the

board is convinced on the due diligence during analysis of the client, the board approves a

designated Credit Rating Grade, which justifies the client‟s creditworthiness.

Reporting :

As the rating process concludes and the board has approved a Credit Rating Grade, the report is

sent to the client by means of electronic mail. Once the report reaches the client, they mostly place

meeting to discuss the reasons for the assigned grade. In case of various big clients, such as group

of industries, banks, insurance, etc., several meetings are conducted between different segments of

management to discuss various issues. Many such issues are the source of information and their

authenticity and reliability, any misunderstanding of operating process that may have happened,

eagerness to provide various documents which were not provided to CRA initially when requested.

Once all the issues are addressed by both parties, the report is confirmed by the client to proceed to

the next step.

Before proceeding to the next step, it is necessary to address the fact that worldwide every

professional firm faces the threat of self-interest. Since the client is the one who pays to the

professional firm or in this case CRA, and the CRA is analyzing the same client, clients may often try

to induce the CRA in occasions. And to safeguard this threat, international associations and national

regulators and associations are designed to obstruct such event. Moreover, the Domestic CRA‟s are

required to appoint a Compliance Officer10 to oversee these issues within the CRA.

9Credit Rating Companies Rules 1996

10 Credit Rating Companies Rules 1996

NegativDeveloping

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 18

The report is then discussed with client and finalized. Once the report is printed, CRA

publishes the credit rating and incorporates the grades in all necessary reporting made to various

regulatory body. However, the responsibility of the CRA still remains after completion of the credit

rating assignment. The CRA needs to be at continuous watch as to whether the assigned grade is

still applicable to the designated client. If any occasion occurs when the grade is no longer

applicable to the client, the CRA has to follow certain step to revoke the assigned grade. Apart from

continuous watch, the CRA is also liable to carry out surveillance review (next consecutive 3 years as

per BSEC Law) every year of rating.

Benefits of Credit Rating :

Credit Rating provides various benefits such as it gives insight of financial health of a company.

Since financial risk analysis is a major component of a credit rating report, reading this particular

section will give the user an idea how sound the financial health of the obligor is.11 Another benefit

of credit rating is that its comparable, if two obligor operating in the same industry is rated and the

grades are presented to an investor; simply by taking the grades into account the investor shall

understand which obligor has higher risk. This is why credit rating particularly helpful for an issuer

with little or no credit history (new company or a company which never borrowed before), as less

well-known issuers gains market access by having information and analysis of their credit widely

available on a comparable basis [Peterson, 2013].

Reduction of information asymmetry is another primary benefit of credit rating which was farther

explained by Adelson [2012] with an example “Posit that every car is either good (a "creampuff") or

bad (a "lemon"). The buyer of a new car doesn't know before his purchase whether the car is a

creampuff or a lemon. Rather, he gains that knowledge after owning the car for a sufficient period

of time (say, a year).

Now suppose that the owner of a creampuff wants to sell his car, and that a used creampuff is really

worth $10,000, while a used lemon is worth only $2,000. The owner knows that his car is a

creampuff, but potential buyers do not. As such, potential buyers, concerned that the car could be a

lemon, will be unwilling to pay $10,000 for it. If there is a chance that the car could be either a

creampuff or a lemon, buyers might be willing to pay some price between $2,000 and $10,000.

However, buyers will also figure out that sellers will be reluctant to sell creampuffs if they can't

realize what the cars are worth, which means that most or all of the used cars offered for sale will

be lemons. Accordingly, buyers will likely refuse to pay more than $2,000 for a used car. Thus, the

seller of a used creampuff would likely be unable to get a buyer to pay the fair price. The whole

problem boils down to information asymmetry between the seller and the buyer: The seller knows

whether the car is a lemon or a creampuff, while the buyer lacks that knowledge.

A simple theoretical application of the lemons principle in credit markets might go as follows:

Lenders, in the role of potential used-car buyers, would be unable to distinguish high-risk borrowers

(lemons) from low-risk borrowers (creampuffs). Therefore, a lender would charge all borrowers the

same rate of interest: the one necessary to cover the risk of lending to a high-risk borrower. Just

11

It should be noted that different credit rating companies use different credit rating methodology so the level of financial insight will differ from company to company.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 19

like the seller of a creampuff could expect to sell his car only for the price of a lemon, a low-

risk borrower would have to pay the same interest rate as a high-risk one. In such a situation, the

volume of borrowing by low-risk borrowers would suffer, and lenders would misallocate productive

resources away from low-risk borrowers. This suggests that economic output would be suboptimal.”

Credit Rating helps to avoid this problems as it distinguishes between low risk borrowers and high

risk borrowers through assigning them appropriate grades so the lenders gets an idea of proper

allocation of funds.

BASEL II and Credit Rating :

Roy [2005] states that “In May 2003, the Basel Committee on Banking Supervision released its third

- and final – consultative paper on the New Basel Capital Accord, which is meant to replace the 1988

capital adequacy framework by a more risk-sensitive approach. One year later, on June 26, 2004,

central bank governors and the head of bank supervisory authorities from the G-10 countries

endorsed the new framework commonly known as Basel II”12. The Basel Committee has developed

two approaches for calculating regulatory capital for credit risk, the so-called “standardized

approach” and “internal ratings based approach” (hereafter IRB). The standardized approach uses

external ratings such as those provided by ECAI to determine risk-weights for capital charges,

whereas the IRB allows banks to develop their own internal ratings for risk-weighting purposes

subject to the meeting of specific criteria and supervisory approval. Large International Financial

Institution usually opts for IRB however the small and medium financial institution does not have

necessary funds to adapt IRB so it usually chooses standardized approach to calculate regulatory

capital risk.

Basel II in Bangladesh :

Bangladesh Bank (BB) is the central bank of Bangladesh and governs all the active performing

commercial banks in the country. Considering the persistent complexity and diversity in the banking

industry and to make the bank‟s capital more risk sensitive and shock absorbent, Bangladesh Bank

has introduced Risk Based Capital Adequacy guideline relating to the Basel II Accord. In compliance

to international standards Bangladesh Bank has made the guidelines statutory for all scheduled

banks in Bangladesh from January 01, 2010. Basel II attempts to integrate Basel capital standards

with national regulations, by setting the lowest capital requirements of financial institutions with the

goal of ensuring organization or Institution liquidity.

These guidelines are structured on following three aspects or PILLARS

12

Details of BASEL II in Bangladesh will be explained in a later chapter

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 20

PILLAR 1:

Minimum capital requirements to be maintained by a bank against credit, market, and operational

risks.

Regulatory Capital as calculated for three major components including:

I. Credit Risk ,as calculated by one of three approaches, including:

a) Standard Approach for Internal Rating Based Approaches (IRB)

b) Foundation Approaches IRB

c) Advanced Approach IRB

II. Operational Risk consists of three components, which are:

a) Basic Indicator Approach (BIA),

b) Standardized Approach (SA), and

c) Internal Measurement Approach

III. Market Risk is calculated by Value at Risk

PILLAR 2:

Process for assessing the overall capital adequacy aligned with risk profile of a bank as well as

capital growth plan. It deals with the regulatory responses to the first pillar. It also provides a frame

work for dealing with all the other risks a bank may face. Such as system risk, pension risk,

BASEL II CAPITAL ACCORD

Pillar 1.

MINIMUM CAPITAL REQUIREMENTS

•Sets minimum acceptable Capital Level

•Enhanced approach for - - credit risk -Public rating -Internal Ratings -Mitigation

•Explicit Treatment of Operational Risk

•Market risk framework, capital definition/ratios are unchanged.

Pillar 2. SUPERVISORY REVIEW OF CAPITAL ADEQUACY

•Banks must assess solvency vs. risk profile

•Supervisory review of bank's calculations & capital strategies

•Banks should hold in excess of minimum level of capital

•Regulators will intervene at an early stage if capital levels deteriorate

Pillar 3.

MARKET DISCIPLINE

•Improved disclosure of capital structure

•Improved disclosure of risk measurement and management practices

•Improved disclosure of risk profile

•Improved disclosure of capital adequacy

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 21

concentration risk, strategic risk, reputational risk, liquidity risk and legal risk, which the

accord combines under the title of residual risk. It gives banks a power to review their risk

management system.

PILLAR 3:

This guides the framework of public disclosure on the position of a bank's risk profiles, capital

adequacy, and risk management system. Market discipline is based on enhanced disclosure of risk.

This may be an important pillar due to the complexity of Basel. Under Basel II, banks may use their

own internal models but the price of this is transparency. Information to be disclosed includes:

I. Available capital in the group, capital structure, detailed capital requirements for credit risk;

II. Breakdown of asset classification and provisioning

III. Breakdown of portfolios according to risk buckets and risk components

IV. Credit risk mitigation (CRM) methods and exposure covered by CRM

V. Operational risk

Assessment of Capital Adequacy is carried out in conjunction with the capital Adequacy reporting to

the Bangladesh Bank and following approaches were pursued to calculate Minimum Capital

Requirement:

I. Credit Risk- Standardized Approach (SA) :

Credit Risk is the possibility that the borrower or counterparty will fail to meet its obligations

in accordance with agreed terms. Bank‟s claim will include loans and advances to and

deposits in local and foreign currency to other banks, central bank and other local and

international institution which include International Monetary Fund (IMF), World Bank, Asian

Development Bank (ADB), and etc. Assets in non-bank financial institutions (NBFIs),

corporate, retail and SME will also have to be counted.

II. Operational Risk- Basic Indicator Approach (BIA) :

It is defined as the risk of loss resulting from inadequate or failed internal processes, people

and systems or from external events. This definition includes legal risk but excludes strategic

and reputational risk (BB, 2010, pp45). For calculating operational risk capital charges there

are two types of approaches- The basic indicator Approach, The Standardized Approach.

III. Market Risk- Standardized Approach (SA) :

Market risk is defined as the risk of losses in on and off-balance sheet positions arising from

movements in market prices. The market risk positions subject to this requirement are:

a) The risks pertaining to interest rate related instruments and equities in the trading

book; and

b) Foreign exchange risk and commodities risk throughout the bank (both in the banking

and in the trading book) (BB, 2010, pp 15).

In Standardized Approach, the capital requirement for various market risks (interest rate risk, equity

price risk, commodity price risk, and foreign exchange risk) is determined separately. The total

capital requirement in respect of market risk is the sum of capital requirement calculated for each of

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 22

the market risk sub-categories such as interest rate movements, adverse price movements

of securities, foreign exchange, repo reverse, repo transactions, interest rate derivatives, Forward

Rate Agreements and SWAPS (BB, 2010, pp16).

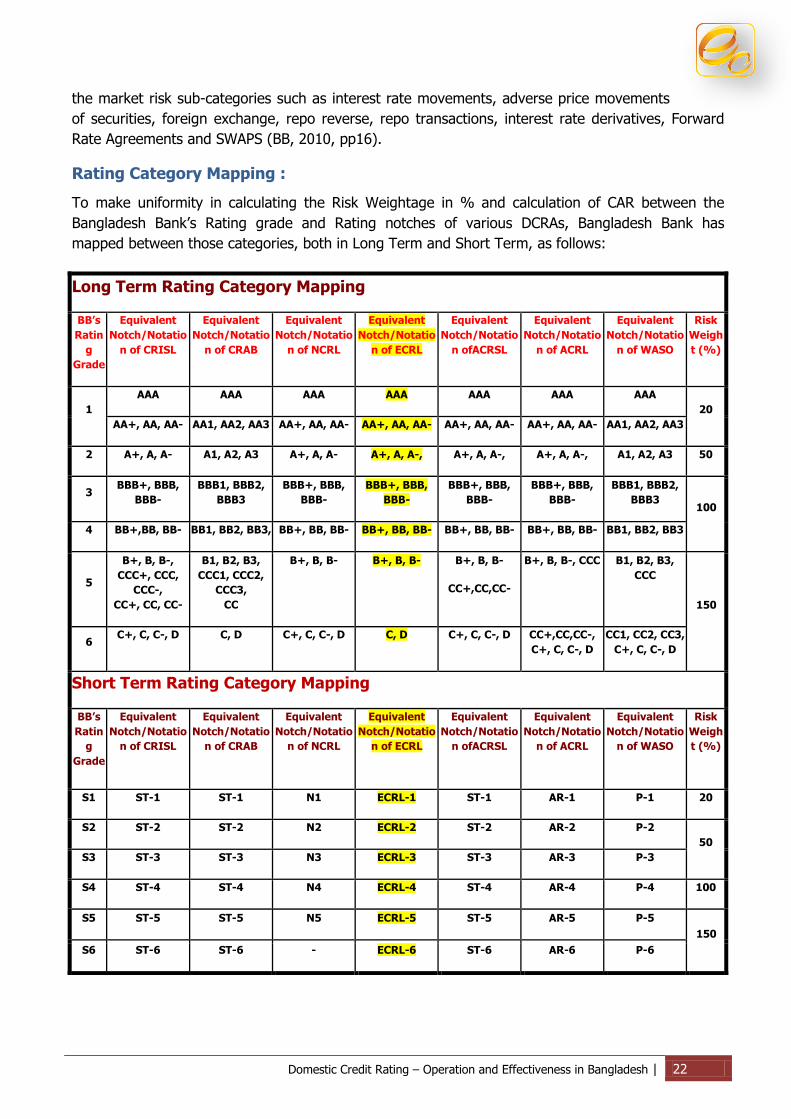

Rating Category Mapping :

To make uniformity in calculating the Risk Weightage in % and calculation of CAR between the

Bangladesh Bank‟s Rating grade and Rating notches of various DCRAs, Bangladesh Bank has

mapped between those categories, both in Long Term and Short Term, as follows:

Long Term Rating Category Mapping

BB’s

Ratin

g

Grade

Equivalent

Notch/Notatio

n of CRISL

Equivalent

Notch/Notatio

n of CRAB

Equivalent

Notch/Notatio

n of NCRL

Equivalent

Notch/Notatio

n of ECRL

Equivalent

Notch/Notatio

n ofACRSL

Equivalent

Notch/Notatio

n of ACRL

Equivalent

Notch/Notatio

n of WASO

Risk

Weigh

t (%)

1

AAA AAA AAA AAA AAA AAA AAA

20

AA+, AA, AA- AA1, AA2, AA3 AA+, AA, AA- AA+, AA, AA- AA+, AA, AA- AA+, AA, AA- AA1, AA2, AA3

2 A+, A, A- A1, A2, A3 A+, A, A- A+, A, A-, A+, A, A-, A+, A, A-, A1, A2, A3 50

3 BBB+, BBB,

BBB-

BBB1, BBB2,

BBB3

BBB+, BBB,

BBB-

BBB+, BBB,

BBB-

BBB+, BBB,

BBB-

BBB+, BBB,

BBB-

BBB1, BBB2,

BBB3 100

4 BB+,BB, BB- BB1, BB2, BB3, BB+, BB, BB- BB+, BB, BB- BB+, BB, BB- BB+, BB, BB- BB1, BB2, BB3

5

B+, B, B-,

CCC+, CCC,

CCC-,

CC+, CC, CC-

B1, B2, B3,

CCC1, CCC2,

CCC3,

CC

B+, B, B- B+, B, B- B+, B, B-

CC+,CC,CC-

B+, B, B-, CCC B1, B2, B3,

CCC

150

6 C+, C, C-, D C, D C+, C, C-, D C, D C+, C, C-, D CC+,CC,CC-,

C+, C, C-, D

CC1, CC2, CC3,

C+, C, C-, D

Short Term Rating Category Mapping

BB’s

Ratin

g

Grade

Equivalent

Notch/Notatio

n of CRISL

Equivalent

Notch/Notatio

n of CRAB

Equivalent

Notch/Notatio

n of NCRL

Equivalent

Notch/Notatio

n of ECRL

Equivalent

Notch/Notatio

n ofACRSL

Equivalent

Notch/Notatio

n of ACRL

Equivalent

Notch/Notatio

n of WASO

Risk

Weigh

t (%)

S1 ST-1 ST-1 N1 ECRL-1 ST-1 AR-1 P-1 20

S2 ST-2 ST-2 N2 ECRL-2 ST-2 AR-2 P-2

50

S3 ST-3 ST-3 N3 ECRL-3 ST-3 AR-3 P-3

S4 ST-4 ST-4 N4 ECRL-4 ST-4 AR-4 P-4 100

S5 ST-5 ST-5 N5 ECRL-5 ST-5 AR-5 P-5

150

S6 ST-6 ST-6 - ECRL-6 ST-6 AR-6 P-6

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 23

Score & Weight Mapping of BB rating grade with SME Rating

Exposure Type BB Rating Grade Risk Weight

(%)

SME 1 20

SME 2 40

SME 3 60

SME 4 80

SME 5 120

SME 6 150

Unrated (small enterprise &<BDT 3.00m) 75

Unrated (small enterprise having ≥ BDT

3.00m & Medium enterprise) 100

Capital Adequacy Ratio (CAR):

To be more risk sensitive and shock resilient against credit, market and operational risk, the

depository institutions are asked by the Bangladesh Bank to maintain some minimum Capital against

its assets. Bangladesh Bank put on guidelines on how to calculate the banks‟ Capital Adequacy Ratio

(CAR).

In order to calculate CAR, banks are required to calculate their Risk Weighted Assets (RWA) on the

basis of credit, market, and operational risks. Total RWA will be determined by multiplying the

amount of capital charge for market risk and operational risk by the reciprocal of the minimum CAR

and adding the resulting figures to the sum of risk weighted assets for credit risk. The CAR is then

calculated by taking eligible regulatory capital as numerator and total RWA as denominator (BB,

2012, pp 12). The Minimum Capital Requirement (MCR) is 10% of the total RWA. Thus The Capital

Adequacy Ratio is calculated by the following formula:

Risk Based Capital Adequacy:

Bangladesh Bank did not make any certain amount of Capital target. A bank should weight its assets

according to its risk exposure and thus maintain sufficient capital to protect itself through any shock.

The assets should be weighted with risk factors and calculate Total Risk Weighted Asset (RWA).

Banks are to calculate Risk Weighted Asset (RWA) on the basis of risk weight mapping circulated by

BB against the credit rating assessment made by listed External Credit Rating Agencies (ECAI)

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 24

Risk Weighted Assets (RWA):

Risk must be taken into consideration while calculating the capital needed to meet BB requirements.

BB provides a list of assets and necessary weights based on their respective risk. The basic RWA

calculation (BBL, 2011) is as below:

Example: If a Bank finance a company BDT 35.00 million which is secured by the company‟s fixed

assets, and obtains a credit rating grade of A will have a RWA of BDT 17.50 million

Basel III :

Bangladesh Bank through BRPD circular no. 7 dated March 31, 2014 introduced Basel III in

Bangladesh. The circular stated that Basel III reforms strengthen the Bank level i.e. micro-prudential

regulation, with the intention to raise the resilience of individual Banking Institutions in period of

stress. Besides the reform have macro prudential focus also, addressing system wide risks, which

can build up across the banking sector. These new global regulatory and supervisory standards

mainly addressed thefollowing areas:

I. Raise the quality and level of capital to ensure banks are better able to absorb losses on both

as going concern and as gone concern basis II. Increase the risk coverage of the capital framework

III. Introduce leverage ratio to serve as a backstop to the risk-based capital measure IV. Raise the standards for the supervisory review process (pillar 2) and V. Public disclosures (pillar 3) etc.

Bangladesh Bank published a roadmap that will be followed by all the financial institutions from

2015 and Basel III will be fully implemented in 2020.

Calculation of RWA for Rated Company:

BDT 35.00 million x RW mapping against A= BDT ? million

BDT 35.00 million x 50% = BDT 17.50 million

Therefore, the Provisioning of Capital is 10% of RWA = RWA x 10%

= BDT 17.50 million x 10%

= BDT 1.75 million

Calculation of RWA for Un-Rated Company:

BDT 35.00 million x RW = BDT ? million

BDT 35.00 million x 125% = BDT 43.75 million

Therefore, the Provisioning of Capital is 10% of RWA

= RWA x 10%

= BDT 43.75 million x 10%

= BDT 4.37 million

Additional capital that can be lend by BANK is BDT 2.63 million (4.37-1.75) million

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 25

Roadmap for Basel III prescribed by Banking Regulation & Policy Department

Action Deadline

Issuance of Guidelines on Risk Based Capital Adequacy December 2014

Commencement of Basel III Implementation process January 2015

Capacity Building of bank and BB officials January 2015- December 2019

Initiation of Full Implementation of Basel III Deadline January 2020Action

Changes after implementation of Basel III :

Previously Capital Adequacy Ratio in Basel II will be termed as Capital to Risk-weighted Asset

Ratio(CRAR), and be calculated as shown below as guidelines of Basel III:

To calculate Capital to Risk-weighted Asset Ratio (CRAR), banks are required to calculate their Risk

Weighted Assets (RWA) on the basis of credit, market, and operational risks. Total RWA will be

determined by multiplying the amount of capital charge for market risk and operational risk by the

reciprocal of the minimum CRAR and adding the resulting figures to the sum of risk weighted assets

for credit risk. This guideline is applicable to all scheduled banks either on Solo or Consolidated13

basis.

Economic Rationale of Credit Rating :

Credit ratings, while they can be a potentially positive part of the financial industry, can also have a

negative effect on the economic policy of countries. Along with rating of different corporate houses,

both government and non-government organizations, country credit ratings is also carried out,

which have had its share of impact.

For countries that take out loans or to buy sovereign bonds,a rating downgrade has negative effects

on their access to credit and the cost of their borrowing. This could potentially force a government

to have to borrow money at a higher interest rate and thus scale down its plans for economic

developmentEkhoury[2008].

While rating agencies can have an effect on individual countries, they can also affect the global

economic system at large as can be seen by their actions in the current global financial crisis.

13

‘Solo Basis’ - refers to all position of the bank and its local and overseas branches/offices

‘Consolidated Basis’ - refers to all position of the bank (including its local and overseas branches/offices) and its subsidiary company/companies engaged in financial (excluding insurance)activities like merchant banks, brokerage firms, discount houses, etc (if any)

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 26

On a macro level, while rating a financial institution, both banking and NBFI, it‟s credit

rating grade impacts not only the bank itself but also several thousand stakeholders who are

associated. Similarly credit rating grade provided to an institutional business also ripples the effect

far wider into the economy than that witnessed a decade ago. The following table denotes the

economic rationale of credit rating to various stakeholders.

Factors Bank

Financial

Institutions Insurance Client

Foreign

Investors

Country

As a

Whole

Safeguards against bankruptcy √ √ √ √

Recognition of risk √ √ √ √ √ √

Wider access of Loan for

Borrowers

√ √ √ √

Lower cost of borrowing √ √ √ √ √ √

Improved confidence of

Lenders

√ √ √ √ √

Improved loan sanctioning

capacity of lenders

√ √ √ √

Reflection of institutional image √ √ √ √ √

Job creation and skill

enhancement

√

International demand √

Export and International

Financing

√ √ √

BASEL II Compliance √ √

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 27

Best Practices in Credit Rating Industry :

Best Practices recommended by ADB :

In December 2008 ADB published “Handbook on International Best Practices in Credit Rating”. In

that book ADB differentiated best practices in two parts: (i) Essential Best Practices and (ii)

Desirable Best Practices. These are explained below

Essential Best Practice

1. Pre rating requirements. Before commencing the rating process the DCRA must sign a

written agreement with the obligor requisitioning a credit rating assignment and under no

circumstances shall promise implicitly or explicitly rating outcome. The organizational

structure and rating process should ensure that rating decisions are not influenced by rating

fees received by the DCRAs.

2. Rating definitions and recognition of Default. A missed payment on a debt obligation on due

date or after pre-specified grace period should constitute as default. Filing for bankruptcy

and involuntary loan rescheduling should also construe as default.

3. Policies and processes for ratings. A DCRAs should have well-defined and updated credit

rating criteria, which are publicly available and consistently applied. Formal rating

committees should have the sole authority to assign ratings. All rating actions should be

announced promptly, and a list of all outstanding ratings should be freely availableon the

DCRA‟s Web site. Every rating should be kept under surveillanceuntil it is withdrawn.

4. Confidentiality requirements. All information submitted by a rated entity or an issuer in

connection with a credit rating assignment is presumed confidential and should be kept so at

all times. Members of the Boardof Directors should not have access to such confidential

informationsubmitted by the rated entity, unless as a part of the rating committee.

5. Independence and avoidance of conflicts of interest. A DCRAs should not refrain from taking

a rating action because of the potential effect of the action on the DCRAs, issuer, investor, or

other market participant. Rules regarding avoidance of conflicts of interest, maintaining

neutrality of analysts, and preventing employees from making gains by misuse of confidential

information are also included.

6. Private ratings. Issuers may seek private credit assessments of their businesses, and a

DCRAs should, in such cases, maintain complete confidentiality of its ratings.

7. Unsolicited ratings. A DCRAs should publicly state its stance on assigning unsolicited ratings.

Where it chooses to assign unsolicited ratings, a DCRAs should distinguish unsolicited ratings

from mandated ratings using a notation in the rating symbol.

8. Unaccepted ratings. A DCRAs should have a published policy regarding disclosures on

unaccepted ratings, where the rated entity has not accepted the initial rating assigned to its

debt issuance.

9. Process audit. A DCRAs should set up audit checkpoints to ensure that the adopted best

practices, policies, and procedures in acquiring, executing, communicating, and surveillance

of ratings are implemented.

Desirable Best Practice

1. Computation of default statistics. Every rating agency should publish, at least annually, a

default and transition study, along with the methodology used for calculating default rates.

Domestic Credit Rating – Operation and Effectiveness in Bangladesh | 28

2. Dedicated advanced functional group.It is recommended that a DCRA have

dedicated functional groups for industry focus, quality assurance, and library and data

management.

3. Use of rating enhancers and early warning indicators.It isrecommended that a DCRA provide

some indication, such as a ratingoutlook, of the possible movement of the assigned rating.

4. Market feedback before major changes.A DCRA should seek feedback from market

participants whenever it contemplates major changes in its rating criteria or key rating

policies, and apprise market participants of these changes.

Best Practices advocated by ACRAA :

Association of Credit Rating Agencies in Asia (ACRAA) was formed on 14th September 2001 at the

Asian Development Bank Headquarters Metro Manila, by 15 Asian credit rating agencies from 10

countries. It was formed with the following objectives14

To develop and maintain cooperative efforts that promote interaction and exchange of ideas,

experiences, information, knowledge and skills among credit rating agencies in Asia and that

would enhance their capabilities and their role of providing reliable market information.

To undertake activities aimed at promoting the adoption of best practices and common

standards that ensure high quality and comparability of credit ratings throughout the region,

following the highest norms of ethics and professional conduct.

To undertake activities aimed at promoting the development of Asia's bond markets and

cross-border investment throughout the region.

Keeping these objectives in mind ACRAA has designed a detailed checklist which member credit

rating agencies can full fill in order to understand what are the best practices of credit rating

companies in Asia and how far behind are they from that practice. ACRAA now has around 31 Rating

agencies in 14Countries in Asia as member. ACRAA is also in the process of attaching with other

similar association in the World like Europe and Latin America.

Best Practices advocated by International Organization of Securities Commissions

(IOSCO) :

Published in September 2003, International Organization of Securities Commissions, IOSCO‟s

Technical Committee issued a statement of principles regarding the Activity of CRA‟s. These Codes