Doing Business in India

42

1 Doing Business in India Contractor, Nayak & Kishnadwala Chartered Accountants, Mumbai, India Tel. +91-22-6623 0600 Fax. + 91 -22- 2261 5814 e mail [email protected]

-

Upload

galvin-randolph -

Category

Documents

-

view

55 -

download

1

description

Doing Business in India. Contractor, Nayak & Kishnadwala Chartered Accountants, Mumbai, India Tel. +91-22-6623 0600 Fax. + 91 -22- 2261 5814 e mail [email protected]. Reasons for Doing Business in India. Large & Fast Growing Market Global Outsourcing of Services Political Stability - PowerPoint PPT Presentation

Transcript of Doing Business in India

1

Doing Business in India

Contractor, Nayak & KishnadwalaChartered Accountants, Mumbai, India

Tel. +91-22-6623 0600Fax. + 91 -22- 2261 5814

e mail [email protected]

2

Reasons for Doing Business in India Large & Fast Growing Market Global Outsourcing of Services Political Stability IPR Protection Large Educated Workforce Lower Costs Business & Policy Environment Tax Breaks & Subsidies

3

FDI Equity Inflows – Top Investing CountriesRank

Country Cumulative Inflows (April 2000 to Nov

2010) USD Million

% of total value

1 Mauritius 52,398 42%

2 Singapore 11,557 9%

3 U.S.A. 9,204 7%

4 U.K. 6,269 5%

5 Netherlands 5,289 4%

6 Japan 4,631 4%

7 Germany 2,903 2%

4

FDI Equity Inflows – Top SectorsRank Sector Cumulative Inflows (April

2000 to November 2010)USD Million

% of total value

1 Services (Fin & Non-Fin) 26,197 21%

2 Computer Software & Hardware

10,446 8%

3 Telecommunications 10,023 8%

4 Housing & Real Estate 9,356 8%

5 Construction activities 8,887 7%

6 Power 5,611 5%

7 Automobile 5,129 4%

8 Metallurgical industry 4,090 3%

9 Petroleum & Natural Gas 3,195 3%

10 Chemicals 2,767 2%

5

Establishment of Business Applicable Laws governing

Establishment of Business Options for foreign companies/citizens Applicable taxes

6

Applicable Laws Industrial Policy of Government of India Foreign Exchange Management Act,

1999 (FEMA) Companies Act, 1956

7

Options for foreign companies/citizens Liaison Office Branch Investment in Subsidiary company/joint

venture/other company

8

Applicable taxes Central

Income Tax [including Tax Deduction at Source (TDS, i.e. withholding tax), dividend distribution tax & fringe benefit tax] & Wealth Tax

Excise Duty Service Tax Customs Duty

State VAT Profession Tax

9

Industrial Policy GoI New Industrial Policy of 1991 Industrial Licensing, Foreign Investment,

Foreign Technology Agreements, Public Sector Policy

Prohibited sectors, Sectors permitted under Automatic Route, Sectoral caps

Governed by Department of Industrial Policy & Promotion, Ministry of Commerce & Industry, Government of India (website: www.dipp.nic.in )

Secretariat of Industrial Approvals (SIA)/ Foreign Investment Promotion Board (FIPB) for cases not covered by Automatic Route

10

Foreign Exchange Management Act (FEMA) Exchange Control Regulations Administered by Reserve Bank of India (RBI) –

website www.rbi.org.in Current Account convertibility with few

restrictions Capital Account controls with few permitted

types of transactions Liaison offices & branches of foreign companies,

foreign direct investment in Indian companies Foreign citizens (other than persons of Indian

origin) not permitted to acquire shares on Indian stock exchanges

11

Setting up a Company Incorporation process takes 20-30 days Cost of incorporation of a company

About Rs.50,000 for authorised capital of Rs.100,000

About Rs.75,000 for authorised capital of Rs.1,000,000

Public limited company or private limited company

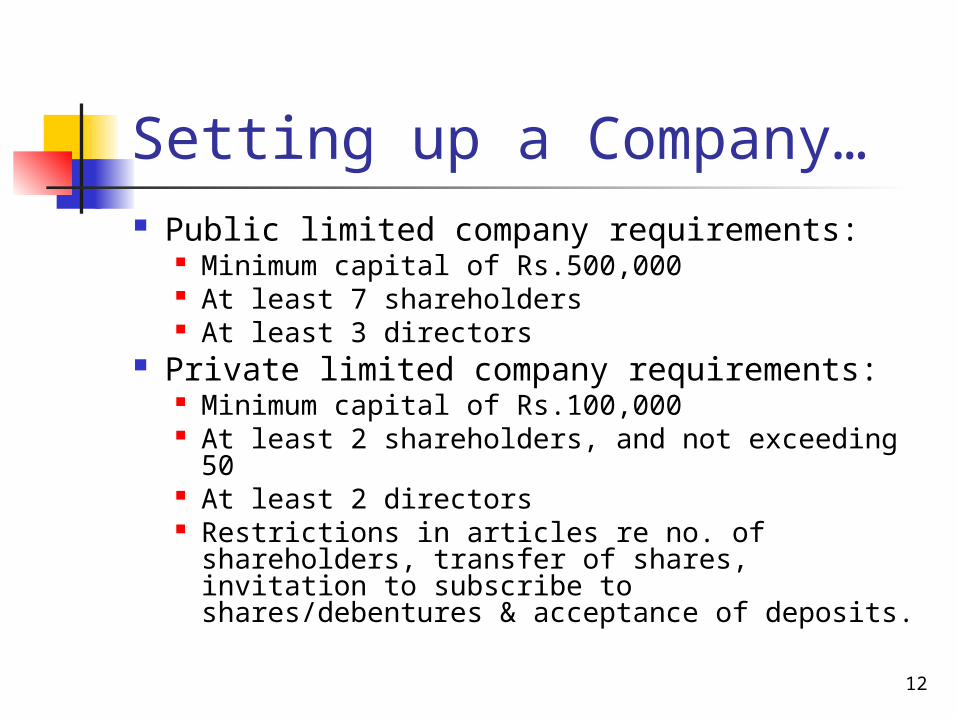

12

Setting up a Company… Public limited company requirements:

Minimum capital of Rs.500,000 At least 7 shareholders At least 3 directors

Private limited company requirements: Minimum capital of Rs.100,000 At least 2 shareholders, and not exceeding

50 At least 2 directors Restrictions in articles re no. of shareholders,

transfer of shares, invitation to subscribe to shares/debentures & acceptance of deposits.

13

Companies Act Requirements All companies liable to get accounts audited To file annual return and audited accounts

electronically To maintain minutes of shareholders and

directors meetings To have whole time company secretary if

capital exceeds Rs. 50,000,000 Secretarial audit if capital between Rs.

2,000,000 & Rs. 50,000,000 Restrictions for public limited companies

regarding managerial remuneration, inter corporate loans and investments

14

Liaison Office Governed by FEMA and Companies Act Prior Approval of RBI under FEMA Subsequent registration with Registrar of

Companies (RoC) Not permitted to carry on any income earning

activity in India Only deposits by way of inward remittance

permitted in bank account To file annual audited accounts of liaison office

with RBI & RoC Not liable to income tax (except TDS)

15

Liaison Office…. Permitted activities –

Representing parent company/group companies in India

Promoting export/import from/to India Promoting technical/financial collaborations

between parent/group companies and companies in India

Acting as communication channel between the parent company and Indian companies

16

Branch Office Governed by FEMA and Companies Act Prior Approval of RBI under FEMA Subsequent registration with Registrar of

Companies (RoC) Can earn income in India To file annual audited accounts of office

with RBI & RoC Liable to all taxes in India Income tax at 40% plus surcharge

(effectively 42.23%) Transfer pricing provisions applicable

17

Branch Office – Permitted Activities Export/import of goods Rendering professional or consultancy services Carrying out research, in which parent co engaged Promoting technical/financial collaborations

between parent/group companies and companies in India

Representing parent company in India and acting as buying/selling agent in India

Rendering services in Information Technology and development of software in India

Rendering technical support to products supplied by parent/group companies

Foreign airline/shipping company

18

Investment in Indian Company Investment in shares of an Indian

company Either by direct subscription or by

purchase of existing shares Either under Automatic Route or with

prior permission of FIPB Subject to sectoral caps and prohibited

sectors

19

Investment in Indian Companies- Prohibited sectors Retail Trading (except single brand) Atomic Energy Lottery Business Gambling & Betting Real estate business or construction Business of Chit Fund Nidhi Company Trading in TDRs Agriculture (excluding floriculture, horticulture, seed

development, animal husbandry, pisciculture, cultivation of vegetables & mushrooms under controlled conditions, services related to agro and allied sectors) and Plantations (other than tea plantations)

20

Investment in Indian Companies - Sectoral Caps Scheduled Air Transport – 49% (100% for NRIs) Non-Scheduled Air Transport – 74% (100% for

NRIs) Ground Handling – 74% (100% for NRIs) Banking – 74% (FDI + FII and within this FII

cannot exceed 49%) Insurance - 26% Telecommunications – 49% NBFC activities – permitted list of 18 with

minimum capitalization norms

21

Some Sectors for which Automatic Route not available Petroleum sector (except refining), LNG/Gas pipelines Commodity Exchange Infrastructure Companies in Securities Market Credit Information companies Investment companies in infrastructure & services Defence & Strategic Industries Atomic Minerals Print Media Broadcasting Satellite Postal Services Courier Services Establishment & Operation of Satellite Development of Integrated Township Tea Sector Asset Reconstruction Companies

22

Sectors under Automatic Route with no sectoral caps All others, including

Software BPO/KPO Drugs & Pharmaceuticals Advertising Roads, Highways, Ports, Harbours Shipping Power

23

Certain Restrictions under Different Statutes/Policies Professional Services – Statutes governing

each profession Print Media – Information & Broadcasting

Ministry Guidelines Investment in SEZ and Free Trade

Warehousing – subject to Special Economic Zones Act, 2005 and Foreign Trade Policy

Satellite – Department of Space/ISRO Petroleum & Natural Gas – Ministry of

Petroleum & Natural Gas

24

Some Sector Specific Issues - Trading Single Brand Retail Trading permitted

under FIPB route Test Marketing permitted under FIPB

route Franchise?

25

Some Sector Specific Issues - Real Estate Development Subject to

minimum development area – 10 hectares for serviced housing plots, 50,000 sq.mtrs. for construction

minimum capitalization norms – US $ 5 million for JVs, US $ 10 million for WOS – funds to be brought in within six months of commencement of Company’s business

time period for completion – 50% within 5 years from receipt of statutory approvals

lock-in period for funds – 3 years from completion of minimum capitalisation

26

Taxation – Income Tax

Scope of Taxation For residents & domestic companies,

worldwide income For non-residents – income accruing,

arising or received in India, or deemed to accrue or arise or be received in India

27

Income Tax – Rates of Tax Domestic Companies – 30% plus

surcharge (effectively 33.2175%) Foreign Companies – 40% plus

surcharge (effectively 42.23%) Dividend Distribution tax – 15% plus

surcharge (effectively 16.995%)

28

Withholding Tax Rates for Payments to Foreign Companies

Nature of Payment Rate

Interest on Foreign Currency Loan

21.115%

Royalties & Fees for Technical Services

10.5575%

Dividends Nil

Short Term Capital Gains 15.83625%

Long Term Capital Gains 21.115%

Other Income 42.23%

29

Other tax provisions No provisions for group consolidated returns No controlled foreign corporation rules No thin capitalization rules Deemed Dividend in respect of loans to

shareholders Rates of Depreciation prescribed on written

down value basis No carry backward of losses Carry forward of losses for 8 years Minimum Alternate Tax at 18% of book profits Authority for Advance Rulings for non-

residents

30

Some Tax Holidays New Software Technology Park Units & Export

Oriented Units – 100% of export profits till 31st March 2012

New Units in Special Economic Zones – 100% of profits for first 5 years, 50% of profits for next 5 asst. years – for the next 5 year, up to 50% of the amount transferred to SEZ Reinvestment Reserve account.

Infrastructure Companies – 100% of profits for any 10 consecutive years out of first 20 years

Power Generation, Transmission & Distribution units - 100% of profits for any 10 consecutive years out of first 15 years

31

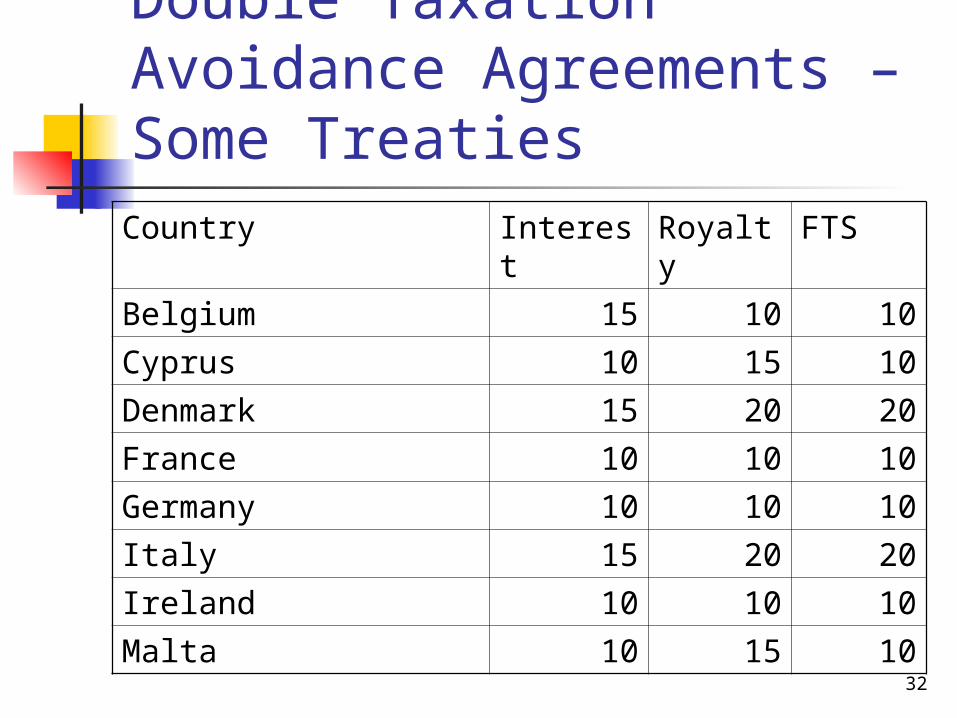

Double Taxation Avoidance Agreements Override domestic tax law, to the extent

that treaty more beneficial to taxpayer Comprehensive Treaties with 79

countries

32

Double Taxation Avoidance Agreements – Some TreatiesCountry Interest Royalty FTS

Belgium 15 10 10

Cyprus 10 15 10

Denmark 15 20 20

France 10 10 10

Germany 10 10 10

Italy 15 20 20

Ireland 10 10 10

Malta 10 15 10

33

Double Taxation Avoidance Agreements – Some Treaties

Country Interest Royalty FTS

Netherlands 10 10 10

Norway 15 10 10

Portugal 10 10 10

Spain 15 10/20 20

Sweden 10 10 10

Switzerland 10 10 10

United Kingdom 15 10/15 15

34

Transfer Pricing Applicable to transactions between related

entities, at least one of which is a non-resident 5 recognised methods for ALP determination

Comparable Uncontrolled Price Resale Price Method Cost Plus Method Profit Split Method Transactional Net Margin Method

No safe harbour rules Transfer Pricing Audit Scrutiny of transactions exceeding

Rs.150,000,000 in a year

35

Income Tax Procedures Payment of advance tax Filing of tax returns Assessment by Assessing Officer Appeals to Commissioner (Appeals) Appeals to Income Tax Appellate Tribunal Appeals to High Court Reference to Supreme Court Website www.incometaxindia.gov.in

36

Excise Duty Duty payable by manufacturer on

manufacture of goods To be paid at time of removal from factory Normally payable on selling price –

generally recovered from customer Normal rate of 10% plus education cess

(effectively 10.30%) Cenvat Credit available for excise duty

paid on inputs & service tax paid on input services

Website www.cbec.gov.in

37

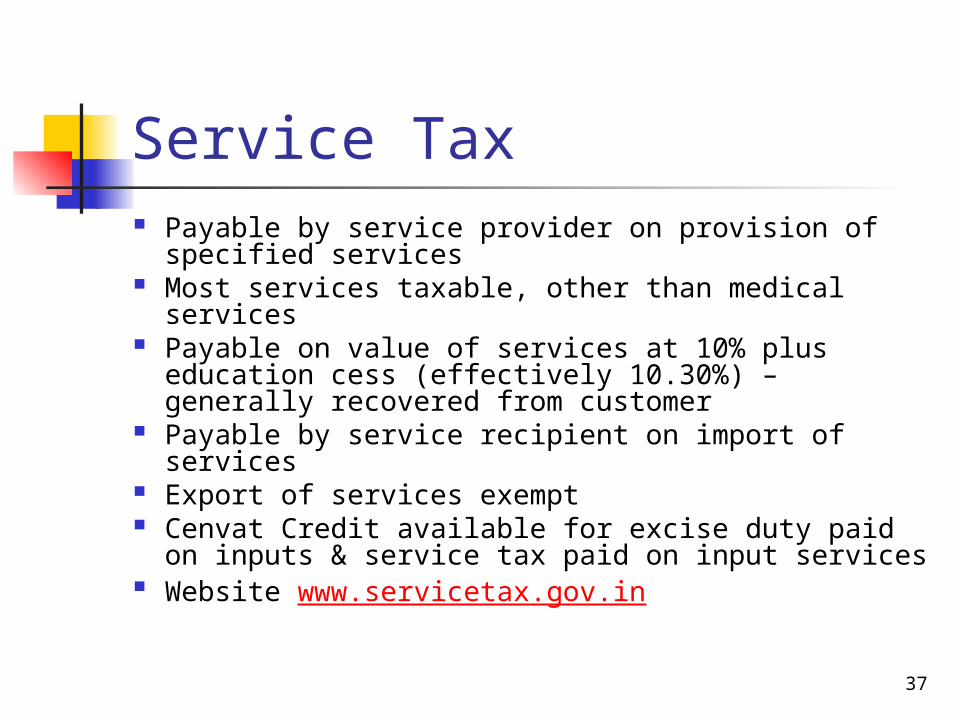

Service Tax Payable by service provider on provision of

specified services Most services taxable, other than medical

services Payable on value of services at 10% plus

education cess (effectively 10.30%) – generally recovered from customer

Payable by service recipient on import of services

Export of services exempt Cenvat Credit available for excise duty paid on

inputs & service tax paid on input services Website www.servicetax.gov.in

38

Customs Duty Payable on import of goods into India Payable on clearance of goods from

port/airport Normal Customs Duty rate of 10% plus

education cess (effectively 10.30%) Additional Duty to match Excise Duty

rates Special Additional Duty at 4% of value Website www.cbec.gov.in

39

VAT Payable on sale of goods Payable on sale price, including excise

duty Lease and works contracts deemed to be

sales Normal rate of 12.5% Set off available for VAT paid on purchases Central Sales Tax on inter-state transfers No VAT on purchases during course of

import or on exports

40

Cultural Aspects of Doing Business in India Land of different cultures – people from North

India more aggressive, from South India more conservative, from West India more businesslike

Both strongly held traditional values and emerging modern business practices prevalent

Greet with a handshake or namaste Always use formal titles (Mr., Dr., Sir, Madam )

when greeting for first time Punctuality – be prepared for delays in

appointments, particularly in Government offices

41

Cultural Aspects of Doing Business in India …. Most Indians are reluctant to say no directly -

try and understand the message behind the words

Get to know your counterpart as a person and gain his trust

Be willing to share a cup of tea/coffee and indulge in small talk before getting down to the main business

Do not be offended at personal questions Do not be too aggressive or forceful or

confrontationist – try and use reasoned logic after understanding the other person’s problem

42

Thank You!