Doing Business in AZERBAIJAN Azerbaijan Export & Investment Promotion Foundation.

Doing Business

in Azerbaijan May 2011

GRATA Law Firm / Azerbaijan Office

13A, Koroglu Rahimov St., Abu Park

Baku, AZ1072, Republic of Azerbaijan

Telephone: +994 12 465 43 65

Facsimile: +994 12 465 43 66

www.gratanet.com

All of the information included in this brochure is for informational purposes only and may

not reflect the most current legal developments, judgments, or settlements. This information

is not offered as legal or any other advice on any particular matter. The Firm and the

contributing authors expressly disclaim all liability to any person in respect of anything, and

in respect of the consequences of anything, done or omitted to be done wholly or partly in

reliance upon the whole or any part of the contents of Grata Law Firm Doing Business in

Azerbaijan brochure. No client or other reader should act or refrain from acting on the basis

of any matter contained in this brochure without first seeking the appropriate legal or other

professional advice on the particular facts and circumstances.

3

Contents

5 Introduction

5 Starting a Business

5 Types of Business entities

5 Joint Stock Companies

8 Limited Liability Companies

9 Structural Subdivisions of Foreign Enterprises

9 Corporate Registration

10 Licensing

12 Banking and Finance

13 Licensing

13 Establishment of Banks

14 Participation of Foreign Capital

14 Management of Banks

14 Reorganization of Banks

15 Prohibited Types of Activities

15 Borrowing in Foreign Currency

15 Currency Transfer and Conversion

15 Employment Matters

15 Employment Contract

16 Work Time

17 Attraction and Use of Foreign Labour in Azerbaijan

18 Tax Regulation

18 Statutory Tax Regime

19 Corporate Tax

21 Personal Income Tax

22 Other State Taxes

23 Double Taxation Treaties

24 Transfer pricing

24 Judicial System and Dispute Resolution

24 Judicial System

24 Settlement of Disputes

25 Language Policy

4

CBA Central Bank of the Republic of Azerbaijan

CIS Commonwealth of Independent States

GMS General Meeting of Shareholders

GMP General Meeting of Participants

JSC Joint Stock Company

Law Law of the Republic of Azerbaijan

LLC Limited Liability Company

MA Ministry of Agriculture

MCIT Ministry of Communication and Informational Technologies

MCT Ministry of Culture and Tourism

ME Ministry of Education

MED Ministry of Economic Development

MENR Ministry of Ecology and Natural Resources

MES Ministry of Emergency Situations

MF Ministry of Finance

MH Ministry of Health

MLSPP Ministry of Labour and Social Protection of the Population

MIA Ministry of Internal Affairs

MIE Ministry of Industry and Energy

MNS Ministry of National Security

MT Ministry of Transportation

USD a dollar, national currency of the United States of America

AZN a manat, the national currency of the Republic of Azerbaijan

Abbreviations

5

Introduction

This pamphlet is the guide provided by the Grata Law Firm for foreign investors interested in

Azerbaijan. Doing Business in Azerbaijan is a brief and concise overview of the legislative and

administrative procedure that is necessary to be familiarized with when starting up a business. It

also provides information as to the different formalities needed to be fulfilled or considered for

successful business operation. This information is not exhaustive, but aims at summarizing the

key facts of legislation concerning foreign investment. These pamphlets will provide Doing

Business guidelines for the Central Asia and Caspian regions that have a Grata office.

Azerbaijan, officially the Republic of Azerbaijan, is the largest country in the Caucasus region of

the Eurasia. After regaining its independence in September 1991, Azerbaijan has been steadily

improving its investment environment and now has become one of the most attractive

destinations for foreign investment in the CIS. Legal and economic reforms undertaken during

these years coupled with stable political situation and abundance of natural resources create

welcoming atmosphere for foreign investment and entrepreneurship.

Starting a Business

In Azerbaijan a company may start its commercial activities after state registration at the Ministry

of Taxes. Registering a local entity is in general a prerequisite to open a bank account, apply for

licenses, certify goods, etc.

Azerbaijani law neither contains specific requirements regarding the size of share of a foreign

company in Azerbaijani entity nor does it establish legal limitations regarding foreign founders’

jurisdiction.

There are several forms of legal entities that a foreign company may choose from. Such forms

include a partnership (general and limited), joint-stock company (open and closed type) and

limited liability company. For general commercial activity the most recommendable and widely

used in practice form of a legal entity is an LLC. Another very popular corporate vehicle is a

branch office of a foreign company which although not deemed a legal entity has distinctive

advantages that make it appropriate for many types of activities that foreign investors carry out in

Azerbaijan. Additionally, foreign companies may set up a representative office in Azerbaijan

which commonly is not authorized to conduct business operations.

Types of Business entities

Joint Stock Companies

General

6

A JSC is a legal entity whose charter capital is divided into certain number of shares. Liability of

shareholders of the JSC for the obligations of the company is limited by the value of their

shareholding. The JSC is not responsible for obligations of its shareholders.

A JSC may be open or closed.

An open JSC may have a public subscription for issued shares and freely sell them, subject to

legislation requirements. The number of shareholders of open JSC is unlimited.

Shares in a closed JSC may only be distributed among its founders or another predetermined

group of persons. The number of shareholders in a closed JSC may not exceed 50. In case the

number of the shareholders exceeds the statutory limit set for closed JSC, the company must be

transformed into an open JSC within one year from the date of registration in the registry of

shareholders, the number of which exceeds the statutory limit. If the closed JSC fails to reregister

as an open JSC, such closed JSC shall be liquidated by the court decision. Open subscription or

otherwise offer of the issued shares to the public is not permitted. Shareholders of the closed

joint-stock company shall enjoy a pre-emptive right to purchase shares offered for sale by other

shareholders of the company at the price and terms and conditions offered to the third party and

in proportion to the amount of their shares.

The foundation of the JSC presumes holding of a foundation meeting and entering into

agreement or adopting decision on establishment of JSC (in case if the JSC is established by

one person), distribution of shares between the founders and preparation (adoption) of the

charter of the JSC..

Charter Capital

The charter capital of a JSC is comprised of the nominal value of the company’s shares acquired

by the shareholders. The company can distribute common and preferred shares, where the

nominal value of preferred shares may not exceed 25% of the company’s charter capital.

The minimum charter capital of a closed JSC may not be less than AZN 2,000 (an amount

equivalent to USD 2,560) and for an open JSC twice that amount.

The charter capital may be increased by raising the nominal value of shares or by issuing

additional shares, or decreased by reducing either the nominal value of shares or the total

number of shares issued. Once the decision on decreasing of charter capital is made, the

company must within 15 days notify its creditors in writing.

Shares

Shares of a JSC must be registered at the SSC. The shares can be either preferred or common.

Preferred shares give their holders the priority right to receive dividends and other rights as

stipulated in the Civil Code of the Azerbaijan Republic, as effective of 1 September 2000.

7

Common share is the voting share giving the right for dividends, participation in General Meeting

and managing of the company.

The forms and terms of distribution of shares are specified in the company Charter. Shares must

be paid for at their fair market value, while the founders pay only nominal value when founding

the JSC.

Information on the amount of the charter fund, amount of shares issued, their nominal value, and

the category of registered securities belonging to shareholders shall be kept with the Register of

Shareholders (the “Register”). JSC may keep the Register within the company, however, when

number of holders of registered shares exceeds 20 (twenty) persons, JSC must hire special

depositary services to keep the register of shareholder.

Management

The JSC is managed by the GMS, Supervisory Board and Executive Body.

GMS

The GMS is the supreme management body of the JSC, convened not less than once a year,

which decides upon the issues of high priority, such as the company’s management,

administration, business policy, corporate structure, financial aspects and certain other issues.

A meeting of shareholders other than the annual meeting is considered to be an extraordinary

meeting. No decision within the exclusive competence of the GMS may be delegated for

resolution to an executive body.

For most decisions, a simple majority vote shares is sufficient. A qualified majority vote (2/3) is

required for certain matters, such as approval of amendments and addendums to the company

charter, reorganization and liquidation of the company. The GMS is valid if shareholders holding

in aggregate over 60% of the voting shares attend such meeting.

Supervisory Board

If the JSC has more than 50 shareholders, the Supervisory Board must be created. The

Supervisory Board exercises overall management of the JSC within its competence, commonly

covering matters related to determination of business priorities, overseeing the activities of the

executive body and carrying out other issues assigned to the Board by the GMS. The charter of

the JSC defines matters that fall into exclusive competence of the Supervisory Board and which

cannot be transferred to the executive body.

Executive Body

8

The competence of Executive Body includes the management of the day-to-day activities of the

company and arrangement of execution of GMS and Supervisory Board’s decisions through

Director (CEO) or a Directorate (collective executive body).

The Director or Directorate acts in the name and on behalf of the JSC within the capacity of

authority delegated by the GMS or Supervisory Board or as provided for in the company charter.

Upon the decision of GMS the power of the Executive Body can be referred to commercial

organization (management company) or individual entrepreneur (manager) under the contract.

Limited Liability Companies

General

LLC is a company established by one or more individuals or legal entities – participants – who

are not liable for its obligations while bearing the risk of losses related to company’s activity within

the limits of their personal contributions value. Participants in the company are jointly liable for its

obligations prior to its establishment and related in connection therewith. The liability of the

company is limited to the extent of its assets.

Charter Capital

The charter capital of the LLC is divided into shares of size specified in the foundation documents

(the Charter and the Resolution on establishment of LLC). Under the Civil Code the LLC cannot

be established in Azerbaijan solely by a legal entity which has only one shareholder.

Azerbaijani Civil Code stipulates neither minimum nor maximum limit for the LLC’s charter

capital. Prior to registration of the company, each participant must pay the charter capital

contributions.

Management

The LLC is managed by the GMS, Executive Body, and by if provided by the Charter,

Supervisory Board.

GMP, which held not less than once a year, is a supreme management body of the LLC.

According to the Civil Code the following matters lay within the exclusive competence of the

GMP:

making changes to the charter and the charter capital of the company;

establishment of the executive bodies of the company and early termination of their authorities;

approval of the company’s annual statements and accounting balance sheets, and distribution of

its profits and losses;

9

decision onto reorganization or liquidation of the company;

election of the inspection commission (inspector) of the company, board of directors of the

Company (or supervisory board).

An executive body, Supervisory Board, inspection committee and participants holding together no

less than 10% of votes can request an extraordinary GMP at any time for any reason.

Day-to-day management of the LLC’s operations is carried out: by its sole executive body –

Director (Manager); or by collegial executive body – Managing Board. Depending on scope of

business and necessity of control, GMP can establish the Supervisory Board and/or inspection

committee (auditor) which oversee activities of the executive body.

Structural Subdivisions of Foreign Enterprises

Representative Offices and Branches

A representative office or a branch of a foreign legal entity represents the interests of a foreign

company in Azerbaijan.

Being a subdivision of a foreign legal entity, representative office generally is not entitled to

conduct business activity. A representative office and a branch acts on the basis of a

“Regulation”, and is managed by an individual authorized by the parent company under a power

of attorney.

A branch, however, may fulfil all or part of the functions of its parent company, including income

generating business activity. Structural subdivisions are formed in essentially the same manner

as a legal entity and are subject to the same formation procedures that are applicable to a legal

entity with foreign ownership.

Corporate Registration

Commercial legal entities and subdivisions of legal entities are registered at the Ministry of

Taxes. Incorporation of a corporate vehicle in Azerbaijan depends on the type of legal entity or

subdivision and commonly consists of the following steps:

adoption of a decision on establishment of an entity;

drafting and adopting statutory documents (charter, foundation agreement, if applicable, or

regulation);

establishment of management and supervisory bodies;

carrying out registration with the Ministry of Taxes.

All documents required for the purposes of establishment of the corporate presence of foreign

legal entity in Azerbaijan and adopted/passed/executed abroad, require notarization and

10

legalization in the country of its origin (apostil) and notary-certified translation into Azerbaijani

language. Letters and applications necessary for submission to the mentioned authorities can be

signed by duly authorized representatives of a foreign company.

The process of state registration of the commercial legal entities and their subdivisions with

relevant state registration authority takes 3 (three) business days from the submission of all

required documents.

The state duty for registration of legal entities and subdivisions of the foreign legal entities ranges

from AZN 11 to AZN 220 (equivalent of USD 14 to USD 280), respectively.

Licensing

Presidential Decree No. 782, “On Improving the License Issuance Rules for Some Types of

Activity,” dated 2 September 2002 constitutes the principal legislation in this field.

Decree No. 782 stipulates the activities that are subject to licensing, authorities that are entitled

to issue licenses and the state fee to obtain a respective license.

License is the official document which grants a right to carry out certain types of business

activities to all legal entities, including with foreign investment and individuals carrying out

entrepreneurial activities without establishing a legal entity.

Each type of activity requires a separate license. The license can only be used by a licensee and

cannot be transferred.

In general the term of a license is five years, except for a license for the production (three years)

and import (one year) of ethanol (alcohol) and alcoholic drinks.

Carrying out the licensable activity without a license may lead to significant penalties under the

Administrative Offences Code and Criminal Code.

Current list of activities due to licensing is as follows:

Activities Subject to Licensing Licensing Authority

Private security activity to ensure the safety of legal entities created in Azerbaijan by foreign legal entities or foreigners or stateless persons, including legal entities, established with direct or indirect participation of the foreign capital; Design and production of data protection devices

MNS

Private security activity (other than above-mentioned); Production of seals and stamps.

MIA

Cartographic activities Committee on Land

and Cartography

Utilization and neutralization of toxic production waste; Collection of raw wild medicinal plant materials

MENR

Purchase, processing and sale of non-ferrous metals waste and indus-trial waste containing precious metals and stones; Commodity exchange

MED

11

Sale of oil and gas products MIE Medical and pharmaceutical activities; Production, import, export and transit transportation of precursors

MH

Production and import of ethanol (alcohol) and alcoholic drinks; Production and import of tobacco products; Production and sale of veterinary medications; private veterinary ser-vices.

MA

Sale of ethanol (alcohol) and alcoholic drinks; sale of tobacco products City and district execu-tive bodies (except city

districts)

Carriage of passengers and cargo by air State Civil Aviation Ad-

ministration Carriage of passengers and cargo by sea; Carriage of cargo (within the country and abroad) and of passengers (intercity, city, international and by taxi) by motor transport

MT

Communication services: telephone (fixed line), mobile, radio trunk and wireless, arrangement of internal telecommunication channels, ar-rangement of international telecommunication channels, IP-telephony, express postal service, data communications; Mobile communication service of 3rd generation (3G); Creation and servicing of biometric technologies Establishment of databases and information systems for private data; maintenance services

MCIT

Educational activities: preschool institutions, general education schools, vocational schools and professional lyceums, colleges, higher education institutions, secondary special and higher religious educa-tion institutions

ME

Intermediary services related to job placement of citizens of Azerbaijan abroad

MLSPP

Banking activities (banks and non-bank credit institutions) National operator of post communication

CBA

Activities of non-state pension funds; Activities in insurance sector: insurance, reinsurance, insurance bro-kers and agents’ activities; Manufacturing of financial reporting documents; Production of precious metals and gemstones (extraction of precious metals from ore and concentrate); Processing and use of precious metals and gemstones (manufacturing and repair of products, including jewellery and other personal items, from precious metals and stones) Turnover (retail and wholesale, purchase of precious metals and gem-stones from the population as well as products, including jewellery and other personal items made from them)

MF

Auditing activities Chamber of Auditors

Stock exchange and investment funds activities; Activities of professional participants of securities market (brokers, dealers, securities management, clearing, depository, register of hold-ers of securities, organization of trade on securities market; Preparation and sale of securities

State Securities Com-mittee

Tourism and hotel activities MCT TV and radio broadcasting, addition information broadcasting, cable network broadcasting, satellite broadcasting, re-broadcasting of foreign TV and radio channels via satellite using coding devices

National Council on Television and Radio

Broadcasting

12

Banking and Finance

Banking and finance sector is primarily regulated by the Civil Code, Law of the Azerbaijan

Republic “On banks” dated 16 January 2004 (“Banking Law”), Law of the Azerbaijan Republic

“On Central Bank” dated 10 December 2004 (“CBA Law”), Law of the Azerbaijan Republic “On

non-banking credit institutions”, dated 25 December 2009 (“Credit Institutions Law”) and other

regulations of the CBA.

The CBA, under the CBA Law, is described as a state authority the goal of which is to ensure

price stability within its authorities. The CBA is to also ensure stability and development of

banking and payment systems of Azerbaijan.

In order to fulfil its goals the CBA is authorized to provide foreign currency regulation and control,

manage foreign exchange reserves, issue licenses for banking activity, issue normative acts

regulating banking and payments operations, etc.

The CBA issues licenses for banking activity in Azerbaijan, establishes minimum charter capital

limits for banking activity, stipulates prudential requirements and establishes management

standards for the banks, etc.

Engineering research, construction and engineering works of Class One and Class Two buildings and structures (except for residential buildings and suburban houses of up to 12 meters in height); Fire protection of the companies and settlements on the basis of agreement; Production, purchase and testing of the fire fighting equipment; Installation, repair and maintenance of fire protection systems and fa-cilities; Repair and servicing of fire fighting equipment and primary fire fighting appliances, restoration of fire fighting appliances performance; Construction, reconstruction and repair of fire protection buildings, con-structions and premises; Storage and disposal of radioactive and ion-emitting substances; Transportation of dangerous goods; Installation and operation of facilities for liquid and natural gas infra-structure; Mining and drilling work; Installation and repair of elevators; Installation and operation of attractions; Installation, set-up and repair of power plants, equipment and facilities; Production, installation and repair of lifting facilities, metallurgical equipment, boilers and vessels, operating under pressure; Diagnostics and other checkups of equipment and technical equipment operated at potentially dangerous work places.

MES

Projection of Class One and Class Two buildings and structures State City-Building and Architecture Committee

Customs broker activity; Establishment of bonded warehouses, short term, storehouses and free warehouses

State Customs Commit-tee

13

Banking Law entitles banks to attract deposits, extend loans and carry out other money transfer

activities while under the Credit Institutions Law non-banking credit institutions are regarded as

specialized credit institutions dealing with lending and other limited functions relating to creation

of security instruments to secure extended loans.

The Banking Law stipulates that banks are permitted to engage in securities trading activities in

the stock exchange provided that respective activity is included into banking license.

Licensing

Banks and non-bank credit organizations may implement banking activities on the territory of the

Azerbaijan Republic on the basis of special permit (license), issued by the CBA.

Foreign citizens and foreign legal entities, registered in offshore zones, the list of which is

determined by the CBA, including also foreign banks and foreign bank holding companies,

cannot be the founders or shareholders of local banks and establish local subsidiary banks, open

local branches and representations.

The CBA has exclusive rights to issue and cancel banking licenses as well as issuance of

permits to banks for opening of branches, departments and representations and cancellation of

issued permits.

Banking licenses and permits shall be issued in writing for unlimited period of time. Banking

licenses and permits may be used only by persons they have been issued to, and cannot be

transferred to third parties. Banking licenses and permits enter into force from the date of

issuance by the CBA.

Where the applicant does not have sufficient technical base or qualifications, the CBA may

establish certain limitations of activities in licenses and permits.

In order to apply for bank license and permit, founder of the bank or their representatives

authorized in accordance with legislation shall submit written application to the CBA and provide

documents and information required under the Banking Law.

Branch offices of foreign banks can function in Azerbaijan only based on special permit of the

CBA. The Banking Law stipulates list of documents and requirements for such application.

While in accordance with the Banking Law branch offices of banks have the right to carry out

banking activity in Azerbaijan, the scope of activity of representative offices of banks is limited to

representation and protection of the banks’ interests only. The Banking Law does not permit

representative offices of banks to engage in banking activity.

Establishment of Banks

Banks can be established by at least three legal entities and/or individuals in the form of a public

joint-stock company.

14

Political parties, public associations, funds and other non-commercial organizations can not be

the shareholders of the bank.

A bank may issue a nominal share only. Owners of preferred shares shall not have the voting

rights.

Owners which are the founders of the bank shall not have any additional privileges or additional

obligations compared to future bank shareholders.

Participation of Foreign Capital

A foreign bank can be represented in Azerbaijan through a branch office, representative office or

a fully owned subsidiary.

According to the law, banks with foreign participation shall be subject to the same legal treatment

as those established with 100% local capital. However, the law provides that in subsidiary banks

of foreign banks and foreign bank holding companies no less than one member of the Board, and

in local branches of foreign bank no less than one of the administrators shall be a citizen of the

Azerbaijan Republic.

Management of Banks

Each bank is managed by the general meeting of shareholders, a supreme management

authority, supervisory board, an authority performing control over its management and

operations, auditing committee which performs the auditing activities in the bank and managing

board, an executive authority.

Reorganisation of Banks

Reorganisation (merger, association, division, separation or reformation) of the bank including

the bank the license of which is cancelled shall be allowed in accordance with procedures

established by the CBA, and with its prior written consent.

However, the bank is not entitled to purchase the share of the bank in other legal entities if such

purchasing will result in one of the following:

balance amount of participation exceeds 10 percent of the cumulative bank capital;

accumulated balance amount of all such shares of the bank exceeds 40 percent of the

accumulated bank capital.

15

Prohibited Types of Activities

With exception of activities for which the permit is issued in accordance with the law, no bank can

engage in wholesale or retail trade, production, transportation, agriculture, development of

mineral resources, construction and insurance, or with exception of insurance companies,

participate in such activities as partner, companion or shareholder.

Borrowing in Foreign Currency

The law allows local banks to attract foreign capital in a variety of ways. The most widely used

form of foreign financing is through borrowing from foreign debt markets or participation of the

foreign banks in the equity capital of Azerbaijani banks. Under the law, ownership interest

contributions to bank’s share capital are exempt from taxation.

Azerbaijani banks can make borrowings in hard currency. Principal loan amount is exempt from

taxation. The law stipulates 10% withholding tax on interest to be paid to non-resident banks

without a permanent establishment in Azerbaijan.

Currency Transfer and Conversion

The law provides that currency conversions within Azerbaijan can be carried out through licensed

banks of the Azerbaijan Republic only. The law does not stipulate any restrictions for foreign

currency cash flows on cross-jurisdictional basis except for a requirement to provide local banks

with underlying documents supporting the transfer

However, the law provides that foreign currency transfers within Azerbaijan can be carried out

based on CBA’s permit only.

Employment Matters

Employment Contract

Employment agreement (contract) is the written agreement between employee and employer

concluded on an individual basis and describing basic conditions of employment relations and the

rights and obligations of the parties. Employment contract is concluded for either uncertain term,

term not exceeding five years, or for the period of fulfillment of work, and specifies the workplace

(enterprise or its branch), functions of an employee (specialization, qualification, and

appointment), the commencement of work, period of employment contract (if concluded for a

fixed period), amount of remuneration and other labor conditions.

16

In accordance with the Labour Code remuneration of labour cannot be lower than Minimum

Wage adjusted by the Legislation. The minimum wage has been set up for computation of taxes,

dues, compulsory payments and social protection of population.

The person applying for work must present the following documents:

Workbook

Personal identification document

State social insurance certificate (except the cases of the first employment)

Diploma of higher or specialized secondary education

Medical certificate (when applicable)

Persons can be employed from 15 years old upon the written permission of one of the parents or

guardian.

Work Time

Normal duration of work time cannot exceed 8 hours a day, 40 hours per week. In a six-day work

week, the duration of daily work cannot exceed 7 hours, whereas in a five-day work week a

maximum of 8 hours a day is allowed.

In general, the Labor Code establishes a five-day work-week with two days off.

Duration of the work-time on the day before the election day, holidays considered as non-

business days, referred to in the Labor Code and the day of National Mourning shall be reduced

by one hour regardless of the number of working days in the week.

Day off holidays are as follows:

January 1 and 2 – New Year

March 8 – Women’s Day

May 9 – Victory Day over Fascism

May 28 – Republic Day

June 15 – Salvation Day

June 26 – Armed Forces Day

October 18 – State Independence Day

17

November 9 – State Flag Day

November 12 – Constitution Day

November 17 – National Renaissance Day

December 31 – Azerbaijan World Solidarity Day

Novruz – five days

Gurban – two days

Ramadan – two days

Employees are entitled for annual leave, which cannot be less than 21 calendar days.

Attraction and Use of Foreign Labour in Azerbaijan

Azerbaijani law does not directly set any local content or personnel quotas. However, there is a

sometimes cumbersome permit system in place if an employer attracts foreign citizens for work in

Azerbaijan.

There is not a notion of work visa under Azerbaijani law. Instead there is a special permit for

carrying out labour activity - work permit. Consequently, if a foreigner intends to be engaged in

labour activity in Azerbaijani the multiple-entry visa cannot replace the work permit.

The “Rules on issuing work permits for foreigners intending to carry out labour activity in

Azerbaijan” approved by Decree No. 214 of the Cabinet of Ministers provide that work permit

shall not be required for foreigners working in Azerbaijan on a business trip for a period of up to 3

months. The law does not provide whether the 3 month period shall be regarded as a cumulative

period of 3 months during a year or simply a consecutive period of 3 sequential months per

calendar year. This uncertainty creates risks of various interpretations.

According to the Law of the Azerbaijan Republic “On entering in the country and leaving the

country and passport regime” dated 14 June 1994, foreigners intending to leave in the territory of

the Azerbaijan Republic for the period of more than 1 month shall apply for police registration

with district police department.

Foreigners living in Azerbaijan based on work permit can obtain residence permit which is tied to

the period of work permit (usually 1 year) and entitles foreigners to live, enter and leave the

country for multiple times within its period of validity. This residence permit replaces visa and

police registration applications. The position of the State Migration Service is that a foreigner

applying for work permit shall file simultaneous residence permit application regardless of the

period of their actual residence in Azerbaijan. The assumption is that the work permit application

in fact implies that the foreigners will live and work in Azerbaijan for more than 3 months and

therefore shall file residence permit application.

18

Penalties for non-compliance with work permit requirements are substantial and vary from USD

36,000 to USD 42,000.

Tax Regulation

Currently, three separate and distinct tax regimes are applicable in Azerbaijan: the statutory

regime, tax regime applicable to oil and gas companies operating under Production Sharing

Agreements (PSAs) and Main Export Pipeline (MEP) regimes. In general statutory tax regime is

applicable to all entities operating in Azerbaijan outside the scope of the PSAs regime and the

Main Export Pipeline regimes. The PSAs regime is a description of the rules which covers a

number of PSAs that have been ratified by the Milli Majlis so far. The Main Export Pipeline

regimes apply to enterprises operating on the Baku-Tbilisi-Ceyhan oil export pipeline and on

South Caucasus Pipeline gas export pipeline.

Statutory Tax Regime

The tax regime outlined below is based on the Tax Code that was enacted on 1 January 2001

with consideration of subsequent amendments. The Tax Code has replaced most of the

individual tax acts adopted prior to it.

In compliance with provisions of the Constitution, the Tax Code stipulates three–level tax system,

which consists of the following:

State taxes (established by the Code);

Taxes of the Autonomous Republic (established by the legislation of the Nakhichivan

Autonomous Republic);

Local (municipal) taxes (established by decrees of the municipalities).

State Taxes:

Profit tax on legal entities (excluding enterprises and organizations in the ownership of

municipalities);

Personal income tax;

Value added tax;

Excise taxes;

Property tax on legal entities;

Tax on land on legal entities;

19

Road tax;

Mining tax;

Tax on simplified system.

Local (Municipal) Taxes:

Tax on land on individuals;

Property tax on individuals;

Mining tax on construction materials of local significance;

Property tax of enterprises and organisations in the ownership of municipalities.

Corporate Tax

Tax payers

All entities engaged in business activity in Azerbaijan (including non-residents who carry out their

activities through PE) are subject to taxes, unless a specific exemption is provided in the law.

The following entities are generally subject to profit tax in Azerbaijan:

Legal entities incorporated under the Azerbaijani laws , with or without foreign participation – i.e.

Azerbaijani residents;

Foreign legal entities with the Azerbaijan based place of management, which are regarded as

Azerbaijani residents;

Branches of foreign legal entities duly registered under Azerbaijani laws, i.e. permanent

establishments of non-residents in Azerbaijan;

Representative offices of foreign enterprises undertaking commercial activities in Azerbaijan, i.e.

permanent establishments of non-residents in Azerbaijan.

Taxable Base

Taxable profits are generally determined on the basis of gross revenue (excluding VAT, excise

tax) less business expenses except for those specifically disallowed by the Tax Code.

Taxable profits include trading profit, capital gains, profits from financial activities and other profit

items. Residents, including Azeri entities with foreign investment, are taxable on worldwide

income. Non-residents are taxable only on income from activities performed in Azerbaijan. The

20

gross income of a foreign enterprise received from Azeri sources not connected with the

permanent establishment is to be taxed at the source of payment without expenses being

deducted (see respective section below on withholding tax).

The most significant items of non-deductible expenditures for tax purposes are:

interest on loans received from abroad or from a related party in excess of 1.25 times refinancing

(discount) rate;

repair expenses in excess of established limits (excess amounts to be capitalized and expensed

through depreciation);

entertainment, accommodation and meal expenses;

business travel expenses in excess of statutory limits;

financial sanctions.

Losses may be carried forward to the next five years and offset against profits of the future years

without limitation.

Tax Rates

The general rate of corporate profit tax is 20%.

Companies which are not required to register for VAT purposes (with exception of credit and

insurance organizations; investment funds; companies producing excisable goods; securities’

market participants and certain other ones) may be subject to the simplified tax regime. Tax is

levied at 2% (4% for Baku city) on gross amount of the total revenue of a taxpayer during an

accounting period for realized goods (work, services) and property, and for non-sale operations.

It should be noted that in addition to profit tax, a branch of foreign legal entities is subject to a

10% tax for transmitting the branch profit abroad.

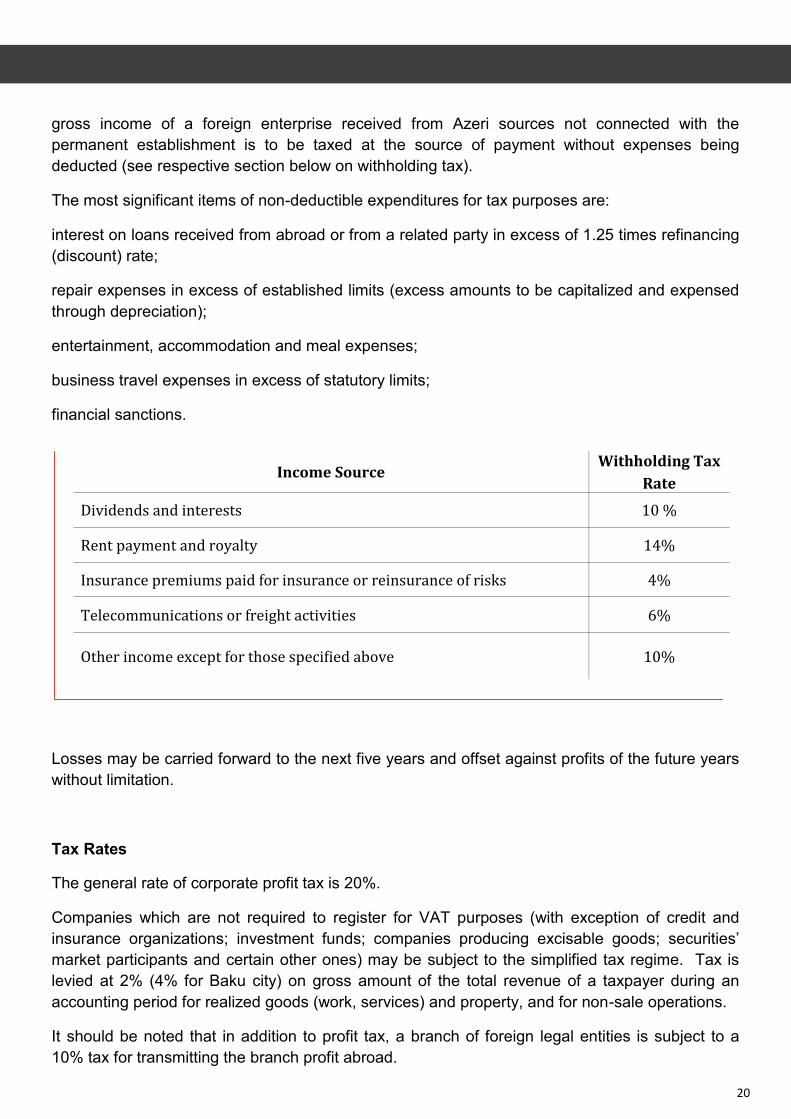

Income Source Withholding Tax

Rate

Dividends and interests 10 %

Rent payment and royalty 14%

Insurance premiums paid for insurance or reinsurance of risks 4%

Telecommunications or freight activities 6%

Other income except for those specified above 10%

21

Withholding Taxes

Income gained by non-resident from the source of payment in Azerbaijan not related to

permanent establishment, is subject to withholding tax at the source of payment on aggregate

income with no deductions at the following rates (which can be reduced by international treaties):

Personal Income Tax

Tax payers

Individuals who are present in Azerbaijan for 183 days or more in any calendar year are deemed

to be residents of Azerbaijan for tax purposes. Resident taxpayers are subject to tax on income

gained from sources of their activity both within Azerbaijan and abroad. Non-residents, however,

are taxed only on their income from sources within Azerbaijan.

Tax on Azerbaijani source income is normally paid by deduction of tax at source, at progressive

rates. Income from overseas source is assessed on a current year basis for residents.

Azerbaijani source income is defined as any income from commercial activities and sources in

Azerbaijan, and specifically includes any income from employment in Azerbaijan. Place of

payment in determining the source of income is irrelevant.

Virtually all income and benefits-in-kind are taxable in Azerbaijan, unless they are specifically

exempt. Taxable income specifically includes hardship, living and vacation allowances. The list of

specifically exempt income includes alimony, severance pay, gifts (within statutory limits), state

pension and other social allowances (excluding illness payments). Compensation of business

expenses also is not taxable.

Rates

Personal income tax rates applicable to annual non-commercial activity taxable income of

individuals are as follows:

Monthly (annual) amount of taxable in-

come

Tax rates (%)

Up to AZN 2,000 (24,000) 14 %

Above AZN 2,000 (24,000) AZN 280 (3,360) plus 30% of the amount above of AZN 2,000 (24,000)

22

Social security/national insurance payments

Azeri nationals and expatriates employed in Azerbaijan must contribute 3 percent of gross salary

to the state pension fund. Contributions are deducted at source and paid and reported by the

employer.

All employers must make social insurance contributions at the rate of 22 percent based on gross

payroll. Reports should be filed quarterly by the 20th of the month following the reporting quarter.

Social insurance contributions shall be remitted monthly at the date of salary payment but not

later than 15th of the following month. Contributions are deductible for profits tax purposes.

All entities are required to account for contributions on most remuneration paid to local and

foreign employees.

Other State Taxes

Value Added Tax

Value added tax (“VAT”) is a tax on the value added in the course of the production, sale, and

import of goods, work, and services. VAT is payable on turnover related to the sale, export, and

import of goods, work, and services. The VAT rate is 18%.

Excise Tax

Legal entities and individuals engaged in the production of excise goods in the Azerbaijan

Republic, or importation of such goods into the Azerbaijan Republic shall pay excise tax. Rates of

excise on imported goods and on production of hydrocarbon goods are separately to be

determined by the Cabinet of Ministers. Rates of excise on production of alcoholic beverages,

beer and tobacco products and rates of excise on importation of passenger vehicles are

determined in the Tax Code. Exports of these goods are subject to zero-rated excise tax.

Mining tax

Legal entities and individuals engaged in the extraction of mineral resources are subject to a

mining tax at the appropriate rate in addition to any land tax due. The tax is applied to the

wholesale price of the mineral resources at the rates, depending on the type of the mineral

resource: 3 percent (for all kinds of metals), 20 percent for natural gas and 26 percent for crude

oil. For other types of mineral resources, tax is based on fixed amounts ranging from 0.02 AZN

up to 6 AZN for each cubic meter. The corresponding tax rates and the list of minerals are given

in the Tax Code. Mining tax is deductible for profits tax purposes.

23

Property Tax

Property tax is levied at the rate of 1 percent on the average annual residual value of fixed assets

including buildings, machinery and equipment. The taxable base is calculated as the average

value at the beginning and the end of the year. Property tax is deductible for profit tax purposes.

From the 1st January 2010 in case the insurance of enterprise property exceeds the remaining

cost, the tax on property is counted up with the use of level of tax on property on the price

determined in accordance with the market value. In case the cost of insured property is

determined by taking into account the market value, calculation of the average of the above

mentioned value is not applied.

The following are specifically exempt from property tax:

education, health, cultural and sport facilities of the enterprises engaged in such fields;

environmental protection and security assets;

transportation, communication and power transmission networks.

Taxpayers shall submit their declarations not later than 31 March of the following year. The tax

due is payable in quarterly instalments by the 15th of the second month of the calendar quarter in

the amount of 20 percent of the property tax due for the previous year (companies which were

not payer of property tax during preceding year should pay quarterly instalments by the 15th of

the second month of the calendar quarter after obtaining taxable property in the amount of 20

percent of the annual property tax due on such property for the current year).

The difference between the amounts of quarterly instalments and final property tax should be

made before the deadline of submission of tax returns.

Land Tax

Companies owning and using land are subject to a land tax (for Baku, tax in the amount of 10

AZN for each 100 quadratic meters of industrial and etc. lands). Taxpayers shall submit their

declarations annually by May 15th. The tax due is payable in equal amounts twice a year, not

later than August 15th and November 15th of the year.

Double Taxation Treaties

As of 1 January 2011, Azerbaijan is a signatory to double taxation treaties with 40 countries, with

36 of them being in effect: Austria, Belarus, Belgium, Bulgaria, China, Czech Republic, Estonia,

Finland, France, Georgia, Germany, Greece, Hungary, Islamic Republic of Iran, Islamic Republic

24

of Pakistan, Italy, Japan, Canada, Kazakhstan, Korea, Kuwait, Latvia, Lithuania, Luxemburg,

Moldova, Netherlands, Norway, Poland, Qatar, Romania, Russian Federation, Serbia,

Switzerland, Tajikistan, The Hashemite Kingdom of Jordan, Turkey, Ukraine, United Arab

Emirates, United Kingdom, Uzbekistan. Treaties with Jordan, Kuwait, Pakistan and Serbia are

yet to come into force.

Transfer pricing

For taxation purposes transfer pricing rules are provided for use in cases of import and export

operations, barter transactions, transactions between related parties and transactions where

price varies from market prices by more than 30% within 30 days. Since neither the Ministry of

Taxes nor the Ministry of Finance has issued comprehensive guidelines, there is considerable

uncertainty about the application of the transfer pricing rules at the time of writing this guide.

From the 1st January 2010 transfer pricing rules have been applied in case if insurance of

enterprise property exceeds its remaining cost.

Judicial System and Dispute Resolution

Judicial System

Judicial system of Azerbaijan consists of three-tier judiciary: (i) first-instance courts, (ii) appeal

courts, and (iii) cassation courts.

The courts of first instance include the city (district) courts, military and local economic courts that

operate subject to territorial jurisdiction. There is also a court on grave crimes, a military court on

grave crime cases and a court on grave crime cases of Nakhchivan Autonomous Republic.

Court of appeal serves as a court of appellate instance. The court of appeal tries appeals lodged

against decisions of the first instance courts on civil, criminal, administrative and military matters.

The Supreme Court of Nakhchivan Autonomous Republic is regarded as an appellate court.

The Supreme Court of the Republic of Azerbaijan is a cassation instance court and consists of 4

collegiums: on civil cases, on criminal cases, on military courts’ cases and on administrative-

economic dispute cases. The Supreme Court hears cassation appeals to the decisions of the

appellate courts.

Settlement of Disputes

In accordance with the Civil Procedure Code a foreign investor may resolve the dispute at

Azerbaijani courts or choose foreign jurisdiction court, including arbitration court. Azerbaijani

25

courts have exclusive jurisdiction over disputes regarding immovable property in Azerbaijan, rent

or pledge of such property; recognition of validity or invalidity of the Azerbaijani legal entity, and

its decisions; patent rights.

The Civil Procedure Code stipulates that Azerbaijani courts shall recognize and enforce foreign

jurisdiction court judgments provided that such an enforcement is envisaged either in laws of the

Azerbaijan Republic, in international conventions or bilateral intergovernmental agreements.

The Azerbaijan Republic has concluded several bilateral treaties but is not party to any

multilateral or bilateral treaties with most of the Western countries for the mutual enforcement of

court judgements. Azerbaijan, however, is a party to the CIS Convention on Mutual Legal

Assistance in Civil, Family and Criminal Cases of 2004 as well as to the Convention on solving

disputes in connection with conducting business activity dated March 20, 1992 (the Kiev

Convention).

The Azerbaijan Republic also is a party to the 1958 New York Convention on the Recognition

and Enforcement of Foreign Arbitral Awards. Accordingly, a foreign arbitral award obtained in a

state which is a party to that Convention should be recognised and enforced by an Azerbaijani

court, subject to the qualifications in the Convention, compliance with Azerbaijani civil procedure,

public order rules and the procedures established by Azerbaijani legislation on commercial

arbitration for the enforcement of arbitration decisions. In addition Azerbaijan has signed and

ratified the 1965 Washington Convention on the Settlement of the Investment Disputes between

States and Nationals of Other States, which provides a possibility for arbitration of certain

investment disputes under the auspices at the International Centre for Settlement of Investment

Disputes. Azerbaijan has also ratified the European Convention on Foreign Commercial

Arbitration dated April 21, 1961.

Language Policy

In accordance with the Constitution Azerbaijani language is the state official language of the

Azerbaijan Republic. Azerbaijani alphabet is based on the Latin script.

Law of the Azerbaijan Republic “On state language”, as effective of 04 January 2003, requires

Azerbaijani legal entities to conduct their paperwork filing and other documentation in the

Azerbaijani language. In compliance with the provisions of this law, courts and state authorities

of the Azerbaijan Republic carry out the official interactions, produce and accept documentation

in Azerbaijani language only.

In order to comply with the legal requirements any official foreign document to be officially used in

Azerbaijan should be duly translated into Azerbaijani with subsequent notarization. Due to legal

requirements in practice many contracts with foreign parties are executed in two languages:

Azerbaijani and any other language acceptable to the parties.

Doing Business

in Azerbaijan May 2011

All of the information included in this brochure is for informational purposes only and may not

reflect the most current legal developments, judgments, or settlements. This information is not

offered as legal or any other advice on any particular matter.