Does Rising Student Debt Affect the Home Purchases of ... loan frbny - upjohn.pdf · Does Rising...

30

Upjohn Institute, October 26, 2013 Meta Brown, Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw Does Rising Student Debt Affect the Home Purchases of Young Borrowers? The views presented here are those of the author and do not necessarily reflect those of the Federal Reserve Bank of New York, or the Federal Reserve System

Transcript of Does Rising Student Debt Affect the Home Purchases of ... loan frbny - upjohn.pdf · Does Rising...

Upjohn Institute, October 26, 2013 Meta Brown, Andrew Haughwout, Donghoon Lee, Joelle Scally, Wilbert van der Klaauw

Does Rising Student Debt Affect the

Home Purchases of Young Borrowers?

The views presented here are those of the author and do not necessarily reflect those of the

Federal Reserve Bank of New York, or the Federal Reserve System

2

Higher education is crucial to improving the skill level of American

workers, especially in the face of a rising income and employment gap

across workers with varying education levels.

Due to increasing enrollment and the rising cost of higher education,

student loans play an increasingly important role in financing higher

education.

However, the rapidly increasing burden of student debt is now over $1

trillion, and is attracting special attention from policymakers, the

media, and the public.

We present our analysis on the historical and current situation of

student debt and discuss its implications for the borrowers and the

economy.

Higher Education and Student Debt

3

Data

Accounting for aggregate balance growth

Student loan payment and delinquency

Student loan and Housing and other debt.

Outline

4

The findings discussed here are based on the FRBNY Consumer

Credit Panel (CCP) – a representative sample of consumer credit data

that the New York Fed acquired from Equifax.

FRBNY CCP contains borrower level information on student loan

balance, payment status together with other types of household debt

such as mortgages, credit cards and auto loans – but no information

on federal loans vs. private loans.

This is a source data for “FRBNY Quarterly report on Household debt

and credit” which updates information on student loan borrowers and

related household debt.

www.newyorkfed.org/householdcredit

About the Data

5

Panel of loans, individuals and households based on individual credit reports Ability to track individual borrowers over time: follow individuals with and without student loans (entry and exit), and can link over consolidations, rehabilitations, account transfers due to defaults Ability to link multiple loans for same person at any point in time: multiple student loan accounts, federal and private loans Ability to link individuals in the same household: credit/loan situation of all family members – total exposure and distribution within household, Parents plus loans and parents cosigning for their children

Data. The FRBNY Consumer Credit Panel

6

Representative Panel and Household

Matching

Unique sample design generating a longitudinal quarterly panel of individuals and households from 1999-2013.

Universe: entire US Population with credit files (240 million

individuals per quarter, aged 18 and older.)

Sample selection: random 5% using last 4 digits of SSN + All household members

Household matching: based on home address

Representative sample of US individuals and households (about 40 million individuals per quarter)

Sample Design

7

Longitudinal information on all individual student loans and mortgages Individual account variables: opening date, origination amount,

current balance, origination balance, delinquency status, individual/joint account, term/monthly payment, narrative codes detailing credit events such as default

Borrower level information on auto loans, credit cards Consumer-level auto loan, credit card data: Total

Balance/Number of accounts by Delinquency Status, origination amount and credit limit

Public record information Public record information on bankruptcies, collections, tax liens

Individual characteristics Borrower characteristics: birth year, geographic location (state,

zipcode, census block)

Main Features of FRBNY CCP

for internal use only

Part 1: Growth of Student Loans

8

9

Total student loan balances by age group increasing across all age groups

0

100

200

300

400

500

600

700

800

900

1,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

under 30 30-39 40-49 50-59 60+

33%

Billions of Dollars

17%

12%

5%

33%

Source: FRBNY Consumer Credit Panel / Equifax

10

Non-mortgage balances

Student debt is the only kind of household debt that continued

to rise through the Great Recession and has now the second

largest balance after mortgage debt.

Source: FRBNY Consumer Credit Panel / Equifax

0

100

200

300

400

500

600

700

800

900

1000

0

100

200

300

400

500

600

700

800

900

1000

HELOC Auto Loan Student Loan Credit Card

Billions of Dollars Billions of Dollars

11

Distribution of student loan balance, 2012:Q4

40% of borrowers have balances less than $10,000

3.7% of borrowers have balances greater than $100,000

39.9%

29.8%

17.7%

9.0%

2.2% 0.9% 0.6%

$1-10,000

$10,000-25,000

$25,000-50,000

$50,000-100,000

$100,000-150,000

$150,000-200,000

$200,000+

Balance

Source: FRBNY Consumer Credit Panel / Equifax

12

Number of borrowers and average balance per person

0

10

20

30

40

Mil

lio

ns

Number of borrowers

Each increased by 70% between 2004 and 2012 (7% per year)

Source: FRBNY Consumer Credit Panel / Equifax

0

5

10

15

20

25

Th

ou

sa

nd

s o

f D

oll

ars

Average balance per borrower

13

Student borrowing increasingly prevalent

Source: FRBNY Consumer Credit Panel / Equifax

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2004:Q4 2005:Q4 2006:Q4 2007:Q4 2008:Q4 2009:Q4 2010:Q4 2011:Q4 2012:Q4

Share of 25 year olds with student debt

14

Student debt almost tripled between 2004 and 2012 and stands at $966B as of 2012:Q4

70% increase in the number of borrowers

70% increase average balance per person

High inflow:

▫ Increasing number of new borrowers

▫ Taking more years to complete education

Low outflow:

▫ Low repayment rates

▫ High delinquency

Two-thirds of the outstanding balance is held by borrowers under 40 years old

Student loans are now the second-largest form of household debt, after mortgages

Summary 1: Growth of Student Debt

for internal use only

Part 2: Student Debt Delinquency

15

16

6.7 million borrowers, or 17%, are 90+ days delinquent.

30-49 year olds have higher delinquency rates.

Source: FRBNY Consumer Credit Panel / Equifax

0%

5%

10%

15%

20%

25%

30%

35%

40%

age<30 age 30-49 age 50+ all

2004 2008 2012

Share of borrowers 90+ days delinquent (incl. default)

17

not in repayment: balance the

same 14%

not in repayment: balance up

30%

Borrower repayment status, 2012:Q4

About 44% of borrowers

are not yet in active

repayment due to

deferments and

forbearances.

Another way to look at the

delinquency rate is to

consider only those in

active repayment and

remove those who are not

in repayment from the

denominator…

in repayment:

balance delinquent

17%

in repayment: balance not delinquent

39%

Source: FRBNY Consumer Credit Panel / Equifax * Repayment status is defined using the quarterly

change in balance and the current payment status.

18

Delinquency rates higher among borrowers in repayment

Source: FRBNY Consumer Credit Panel / Equifax

0%

5%

10%

15%

20%

25%

30%

35%

40%

age<30 age 30-49 age 50+ all ages

Share of borrowers in repayment 90+ days delinquent

2004 2008 2012

0%

5%

10%

15%

20%

25%

30%

35%

40%

age<30 age 30-49 age 50+ all ages

Share of borrowers 90+ days delinquent

2004 2008 2012

19

Quarterly transition rate of borrowers in repayment from non-delinquent to delinquent

Source: FRBNY Consumer Credit Panel / Equifax

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2005 2006 2007 2008 2009 2010 2011 2012

20

About 17% of borrowers are past due on their student debt

more than 90 days in 2012, a large increase from under 10% in

2004

44% of borrowers are not yet in active repayment, and

excluding those, the effective 90+ delinquency rate rises to

more than 30%.

The transition rate among borrowers in active repayment from

current to delinquent has been rising since 2008 from about 7%

to nearly 9%.

Summary 2: Student Debt Delinquency

for internal use only

Part 3: Student debt and other debts

21

22

Non-student debt declined for all borrowers age 25-30 Decline particularly pronounced for borrowers with larger student debt

Source: FRBNY Consumer Credit Panel / Equifax

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$0

$1

-10

K

$1

0K

-25

K

$25K

-50K

$5

0K

-75

K

$7

5K

-10

0K

$100K

+

$0

$1

-10

K

$1

0K

-25

K

$2

5K

-50

K

$5

0K

-75

K

$7

5K

-10

0K

$1

00

K+

2005 Student Debt Balance 2012 Student Debt Balance

Average non-student loan balances, age 25-30

auto credit card mortgage HELOC other

2005 Student Debt Balance 2012 Student Debt Balance

23

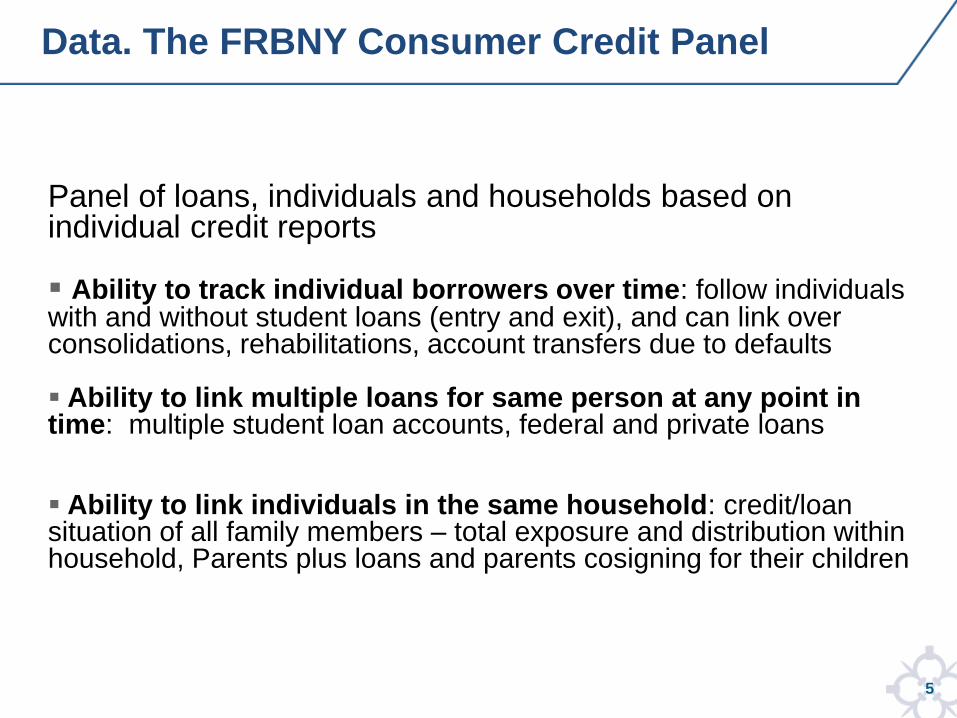

Deleveraging of Household Debt

0

3

6

9

12

15

0

3

6

9

12

15Mortgage HE Revolving Auto Loan Credit Card Student Loan Other

Trillions of Dollars Trillions of Dollars

Source: FRBNY Consumer Credit Panel/Equifax

2013Q1 Total: $11.23 Trillion

2013Q2 Total: $11.15 Trillion

(3%)

(9%)

(6%)

(7%)

(5%)

(71%)

24

Mortgages among student loan borrowers age 25-30 Originations by student loan balance and delinquency status

With delinquent student debt, mortgage origination is very difficult.

The mortgage origination gap across the size of student debt has declined

between 2005 and 2012.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2005:Q4 2006:Q4 2007:Q4 2008:Q4 2009:Q4 2010:Q4 2011:Q4 2012:Q4

no student debt with current student debt

with current 100K+ student debt with 90+ delinquent student debt

Source: FRBNY Consumer Credit Panel / Equifax; Note: delinquency is as of Q4 of previous year

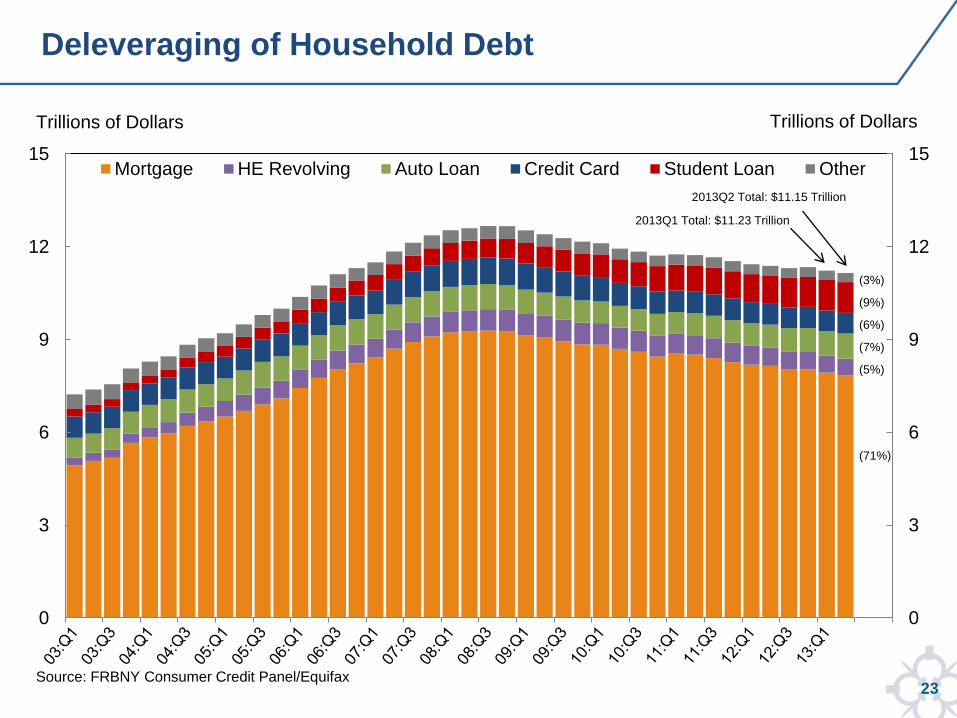

25

Non-student debt 90+ days delinquent, age 25-30, 12:Q4

Delinquent student loan borrowers are very likely to be delinquent on other

debt as well.

Source: FRBNY Consumer Credit Panel / Equifax

0%

5%

10%

15%

20%

25%

30%

35%

40%

no student debt current student debt 90+ delinquent student debt

auto loans credit card mortgage

26

Young people borrowed less in 2012 compared to 2005, but the

differences were more pronounced among borrowers with high

student loan balances, likely reflecting declines in demand and

access to credit.

Student debt delinquency reduces a young borrower’s ability to

secure other types of credit.

Student loan delinquency is also associated with higher

delinquency rates on other types of debt.

Summary 3: Student Debt and Other Debt

27

Higher education is an important investment among young

workers for better jobs and higher income, but it is

accompanied with a growing student debt burden.

Aggregate student loan balances almost tripled between 2004

and 2012 due to an increasing number of borrowers and higher

balances per borrower.

About 17% of borrowers are delinquent on student debt.

Adjusting for repayment causes the delinquency rate to rise to

over 30%.

The larger burden of student loans and higher delinquencies

may affect borrowers’ access to other types of credit and the

performance of other debt.

Conclusion

for internal use only

APPENDIX

28

29

Appendix A: Why borrow for education?

College graduates have lower unemployment rates, fare

better during recessions, and enjoy wages roughly double

those of high school graduates.

0

200

400

600

800

1000

1200

high schoolgraduates

bachelor's degreeor higher

Me

dia

n D

oll

ars

pe

r W

ee

k

Median Weekly Earnings, 2012:Q4

Dec-2007

Dec-2007

Jun-2009

Jun-2009

Jan-2013

Jan-2013

0

1

2

3

4

5

6

7

8

9

10

High SchoolGraduate

Bachelor's degree

Pe

rce

nt

Unemployment Rate

Source: Bureau of Labor Statistics

30

On our website, we provide:

Updates of our Quarterly Report on Household Debt &

Credit

▫ Balances for Mortgages, Credit Card, Auto, & Student Debt

▫ Delinquency rates

Spreadsheets:

▫ All data featured in the Quarterly Report on Household Debt &

Credit (1999-2013:q1, quarterly)

▫ Student loan

– # borrowers, delinquency rates, average balance

– By state (2004-2012, annual)

– By age group (2012 only)

Appendix B: www.newyorkfed.org/householdcredit