Document of The World Bankdocuments.worldbank.org/curated/en/514671468300575864/...Document of The...

89

Document of The World Bank Report No: ICR00001801 IMPLEMENTATION COMPLETION AND RESULTS REPORT (IDA-32170, IDA-32171, IDA-3217A) ON A CREDIT IN THE AMOUNT OF SDR 15.5 MILLION (US$21.4 MILLION EQUIVALENT) TO THE REPUBLIC OF MADAGASCAR FOR A MICROFINANCE PROJECT IN SUPPORT OF THE FIRST PHASE OF THE MICROFINANCE PROGRAM September 30, 2011 Finance and Private Sector Development AFCS4 Africa Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Document of The World Bankdocuments.worldbank.org/curated/en/514671468300575864/...Document of The...

Document of The World Bank

Report No: ICR00001801

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IDA-32170, IDA-32171, IDA-3217A)

ON A

CREDIT

IN THE AMOUNT OF SDR 15.5 MILLION (US$21.4 MILLION EQUIVALENT)

TO THE

REPUBLIC OF MADAGASCAR

FOR A

MICROFINANCE PROJECT

IN SUPPORT OF THE FIRST PHASE OF

THE MICROFINANCE PROGRAM

September 30, 2011

Finance and Private Sector Development AFCS4 Africa Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

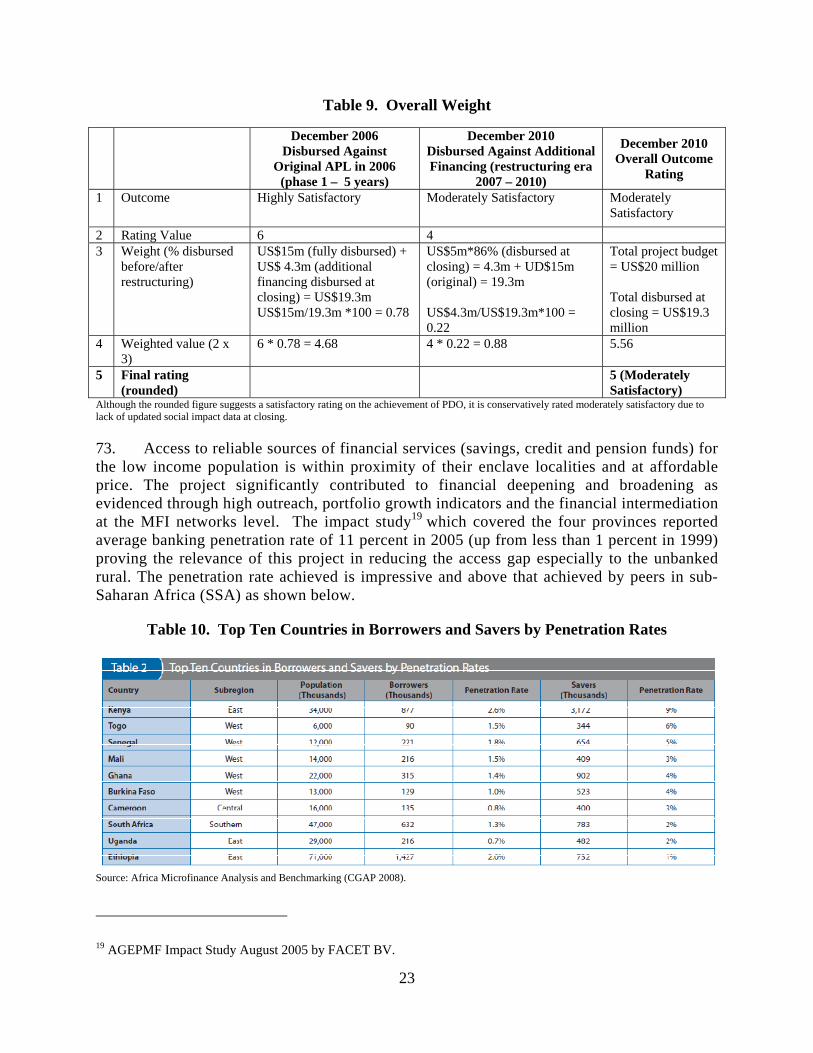

rized

ii

CURRENCY EQUIVALENTS

(Exchange Rate Effective December 31, 2010)

Currency Unit = Malagasy Ariary (MGA) MGA 2,000 = US$1

US$1.54 = SDR 1

FISCAL YEAR January 1 – December 31

ABBREVIATIONS AND ACRONYMS

AGEPMF Project Coordination Unit APIMF Apex Microfinance Professional Association APL Adaptable Program Loan APMF Microfinance Apex Association AROA Adjusted Return on Assets BCM Banque Centrale de Madagascar CAS Country Assistance Strategy CECAM Caisses d’Epargne et de Crédit Agricole Mutuels (Agricultural Savings and

Credit Cooperative) CEM Country Economic Memorandum CGAP Consultative Group to Assist the Poor CNAPS Social Security Administration CSBF Commission de Supervision Bancaire et Financière DCA Development Credit Agreement DID Développement International Des Jardins FM Financial Management FSAP Financial Sector Advisory Program FSS Financial Self Sufficiency GNI Gross National Income IBFI International Banking and Finance Institute IBRD International Bank for Reconstruction and Development ICR Implementation Completion and Results Report IDA International Development Association IMF International Monetary Fund IO Intermediary Outcome IRAM Institut de Recherches et d’Application des Méthodes de développement ISR Implementation Status and Results Report KPI Key Project Indicator M&E Monitoring and Evaluation MAP Madagascar Action Plan MEC Mutuelle d’Epargne et de Crédit MFI Microfinance Institution MGA Madagascar Ariary MTR Mid-Term Review

iii

NPL Non-Performing Loan OSS Operational Self Sufficiency PAD Project Appraisal Document PAR Portfolio at Risk PASEF Financial Services Project PCU Project Coordination Unit PDO Project Development Objective PIU Project Implementation Unit PP Project Paper PPF Project Preparation Facility RFTAP Rural Finance Technical Assistance Project ROA Return on Assets ROE Return on Equity SDI Subsidy Dependence Index SDR Special Drawing Rights SLA Savings and Loan Association SSA Sub-Saharan Africa TA Technical Assistance TOT Training of Trainers TTL Task Team Leader UNCDF United Nations Capital Development Fund WOCCU World Council of Credit Unions

Vice President: Obiageli Katryn Ezekwesili

Country Director: Haleh Z. Bridi

Sector Manager: Michael J. Fuchs (Acting)

Project Team Leader: Korotoumou Ouattara

ICR Team Leader: Zahia Lolila

iv

v

REPUBLIC OF MADAGASCAR Microfinance Project

CONTENTS

Data Sheet A. Basic Information B. Key Dates C. Ratings Summary D. Sector and Theme Codes E. Bank Staff F. Results Framework Analysis G. Ratings of Project Performance in ISRs H. Restructuring I. Disbursement Graph

1. Project Context, Development Objectives and Design ........................................................... 1

2. Key Factors Affecting Implementation and Outcomes ........................................................ 12

3. Assessment of Outcomes ...................................................................................................... 19

4. Assessment of Risk to Development Outcome ..................................................................... 35

5. Assessment of Bank and Borrower Performance ................................................................. 36

6. Lessons Learned .................................................................................................................... 41

7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners ....................... 42

Annex 1: Project Costs and Financing ......................................................................................... 43

Annex 2: Outputs by Component ................................................................................................ 45

Annex 3. Economic and Financial Analysis ................................................................................. 57

Annex 4. Bank Lending and Implementation Support/Supervision Processes ............................. 65

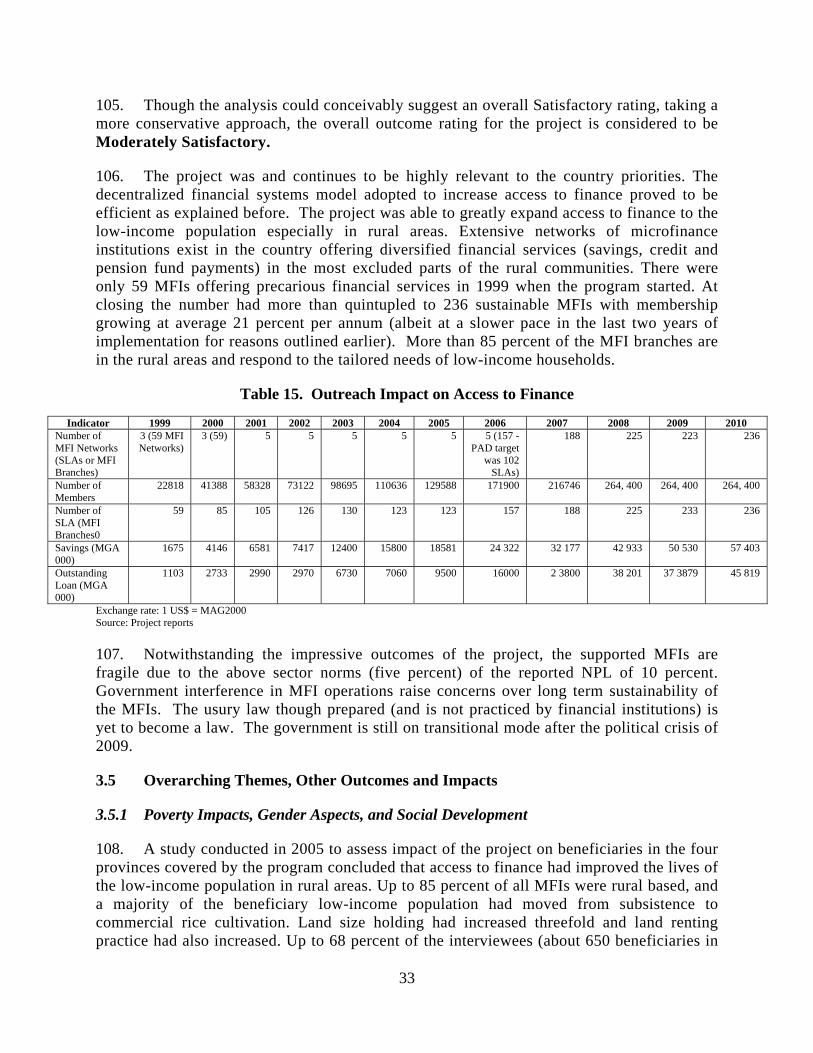

Annex 5. Beneficiary Survey Results ........................................................................................... 67

Annex 6. Stakeholder Workshop Report and Results ................................................................... 68

Annex 7. Summary of Borrower's ICR and/or Comments on Draft ICR ..................................... 69

Annex 8. Comments of Cofinanciers and Other Partners/Stakeholders ....................................... 70

Annex 9. List of Supporting Documents ...................................................................................... 71

Map ............................................................................................................................................... 73

vi

List of Tables Table 1. Grouping of PDO Indicators and Intermediate Indicators ............................................... 4 Table 2. Project Statements of Objectives ..................................................................................... 4 Table 3. List of Original and Revised Targets at Restructuring (2007) by PDOs ......................... 5 Table 4. List of Original & Revised Indicators at Restructuring (2007) - Project Outcome

Indicators .......................................................................................................................... 6 Table 5. Financing Breakdown by Component ........................................................................... 10 Table 6. Breakdown of sources of funds (US$) ........................................................................... 10 Table 7. Additional Financing Cost Breakdown & Disbursement Rate (December 2010) by

Component ..................................................................................................................... 11 Table 8. Achievement of Performance Indicators of MFI Networks (Pre and Additional

Financing Eras) ............................................................................................................... 22 Table 9. Overall Weight ............................................................................................................... 23 Table 10. Top Ten Countries in Borrowers and Savers by Penetration Rates ............................. 23 Table 11. Rating of Project Efficiency (Pre-Additional Financing and Additional financing eras)

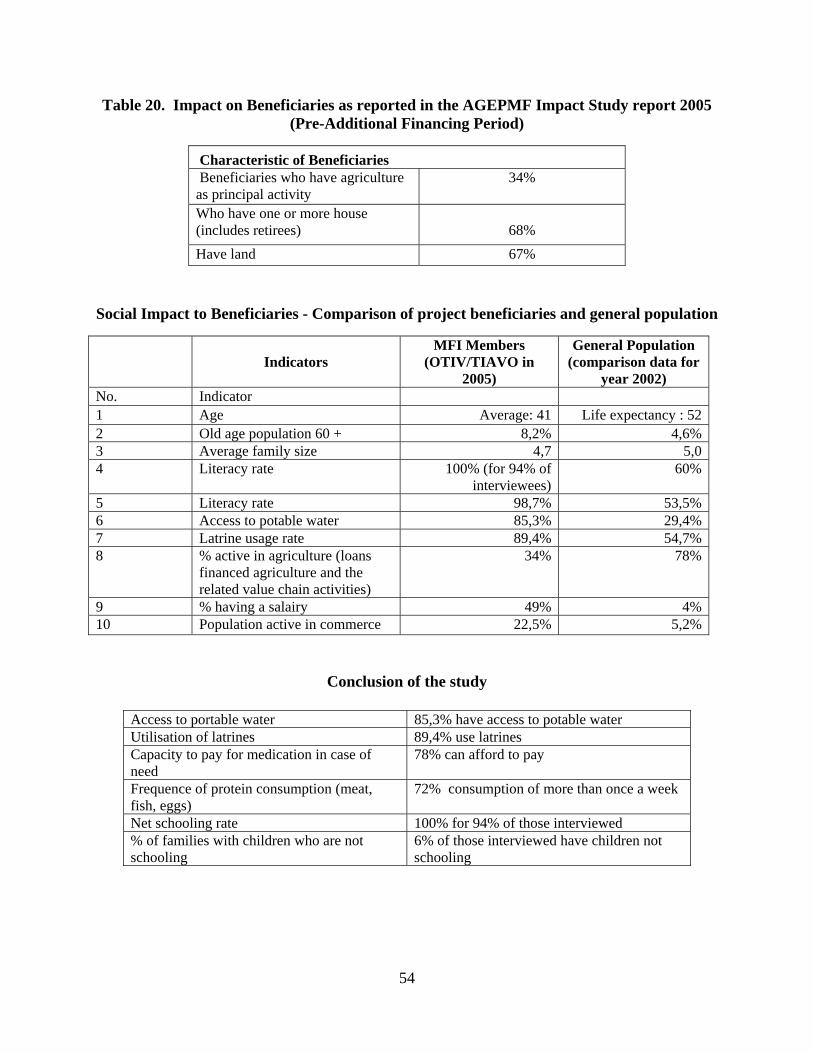

........................................................................................................................................ 28 Table 12. MFI Networks’ Profitability/Sustainability Index (December 31, 2010) .................... 30 Table 13. Operating Efficiency Trend of the Supported MFIs .................................................... 31 Table 14. Summary of Overall Outcome Ratings of PDOs ......................................................... 32 Table 15. Outreach Impact on Access to Finance ........................................................................ 33 Table 16. MFI Penetration Rate ................................................................................................... 34 Table 17. Results Framework - Outputs by Component - PDOs ................................................. 45 Table 18. Results Framework - Outputs by Component – IO Indicators .................................... 49 Table 19. Performance of Individual MFI networks (Additional financing era 2007 – 2010) .... 52 Table 20. Impact on Beneficiaries as reported in the AGEPMF Impact Study report 2005 (Pre-

Additional Financing Period) ......................................................................................... 54 Table 21. Consolidated Financial Analysis for the five MFI Networks in December 2010 ....... 57 Table 22. List of Legal Instruments prepared .............................................................................. 59 Table 23. Classification of MFIs (Level 1 – 3) including Capital Adequacy Requirements ....... 60 Table 24. List of new Licenses Issued and Classification of MFIs (2008 – 2010) to MFIs (from

level 1 to 2 & 3) .............................................................................................................. 61

vii

A. Basic Information

Country: Madagascar Project Name: MG-Microfinance

Project ID: P052186 L/C/TF Number(s): IDA-32170,IDA-32171,IDA-3217A

ICR Date: 06/30/2011 ICR Type: Core ICR

Lending Instrument: APL Borrower: GOVERNMENT OF MADAGASCAR

Original Total Commitment:

XDR 12.1 M Disbursed Amount: XDR 14.7M

Revised Amount: XDR 15.5 M Environmental Category: C Implementing Agencies: AGEPMF CSBF Cofinanciers and Other External Partners: The PAD anticipated contributions from other donors as explained below. These pledges were not channeled through the project, and there is no evidence to substantiate whether they were given to MFIs directly or not. Interviews with beneficiary MFIs indicated that UNCDF provided direct support to some of the MFI networks to support women’s credit programs. Contribution from the government was stopped at the time of project restructuring in 2007 at the request of the authorities who had difficulties to honor their commitments. Government: MGA1.8 million (US$913,860) Savings and Loan Association Networks: US$0.2 million UNCDF: US$0.7 EU: US$0.7 Developpement International Desjardins US$0.3 Total Financing including IDA US$20.4 million

B. Key Dates

Process Date Process Original Date Revised / Actual

Date(s)

Concept Review: 09/24/1997 Effectiveness: 10/28/1999 10/28/1999

Appraisal: 11/09/1998 Restructuring(s): 10/22/2002

Approval: 05/20/1999 Mid-term Review: 06/30/2006 02/19/2004

Restructuring(s): 02/23/2007

Closing: 12/31/2004 12/31/2010

C. Ratings Summary C.1 Performance Rating by ICR

Outcomes: Moderately Satisfactory

viii

Risk to Development Outcome: Moderate

Bank Performance: Moderately Satisfactory

Borrower Performance: Moderately Unsatisfactory C.2 Detailed Ratings of Bank and Borrower Performance (by ICR)

Bank Ratings Borrower Ratings

Quality at Entry: Satisfactory Government: Moderately Unsatisfactory

Quality of Supervision: Moderately Satisfactory Implementing Agency/Agencies:

Unsatisfactory

Overall Bank Performance:

Moderately Satisfactory Overall Borrower Performance:

Moderately Unsatisfactory

C.3 Quality at Entry and Implementation Performance Indicators

Implementation Performance

Indicators QAG Assessments (if

any) Rating

Potential Problem Project at any time (Yes/No):

Yes Quality at Entry (QEA):

None

Problem Project at any time (Yes/No):

Yes Quality of Supervision (QSA):

Moderately Satisfactory

DO rating before Closing/Inactive status:

Moderately Satisfactory

D. Sector and Theme Codes

Original Actual

Sector Code (as % of total Bank financing)

Central government administration 6 6

Micro- and SME finance 94 94

Theme Code (as % of total Bank financing)

Gender 13 13

Improving labor markets 13 13

Regulation and competition policy 25 25

Rural markets 24 24

Small and medium enterprise support 25 25 E. Bank Staff

Positions At ICR At Approval

Vice President: Obiageli Katryn Ezekwesili Callisto E. Madavo

Country Director: Haleh Bridi Michael N. Sarris

Sector Manager: Michael J. Fuchs Paul Murgatroyd (Acting)

ix

Project Team Leader: Korotoumou Ouattara Herminia Martinez

ICR Team Leader: Zahia Msuya Lolila-Ramin

ICR Primary Author: Zahia Msuya Lolila-Ramin F. Results Framework Analysis

Project Development Objectives (as stated in the Project Appraisal Document) The original Project Development Objective was to provide increased financial services to the low-income population not served by the traditional banking sector through (a) the formulation of regulations governing microfinance; improvement in business laws applicable to microfinance, notably on collateral, and the establishment of a supervision mechanism for microfinance institutions (MFIs); (b) the design and testing of a training system for microfinance; and (c) the establishment and expansion of MFIs, particularly the savings and loan associations (SLAs). This in long-term will contribute to improved standard of living and productivity. Revised Project Objectives as approved by original approving authority Project objectives were not revised. However they are written differently in the PAD, restructuring document and in the credit and financing agreements (see details under section 1.4, Table 1). Although the wording is different, the three elements of improving long term access, policy and capacity in the microfinance sector remained unchanged and relevant. In the Development Credit Agreement (DCA), the objective included three intermediate outcomes that would be achieved under each component of the project: (i) The establishment of legal and regulatory framework for microfinance operations; (ii) The expansion of microfinance skills (capacity); and (iii) The development of strong and sustainable microfinance institutions through inter alia establishment of a refinancing mechanism. (a) PDO Indicators Below is a summary of achievement of PDO indicators which is complemented by a detailed results framework in Annex 2.

Project Development

Objectives (PDO)

Baseline Value

Original Target Values

(from approval documents)

Formally revised Target Values

Actual Values Achieved at Completion or Target

Years

PDO Indicator 1:*

Enabling legal and regulatory environment for doing microfinance business in Madagascar exists

(Text) -Several legal impediments exist for MFIs operating in Madagascar (including lack of legal supervisory

-Microfinance laws and regulations that reflect international best practice are

-Microfinance laws are effective and regulations that reflect international best practice are adopted including

- Based on the banking law number 95-030 and law number 96-020 (1996) on mutualist financial institutions, prudential and operating rules for mutualist

x

Project Development

Objectives (PDO)

Baseline Value

Original Target Values

(from approval documents)

Formally revised Target Values

Actual Values Achieved at Completion or Target

Years

framework for microfinance institutions and prudential norms). -Usury law exists restricting growth of microfinance sector.

issued, adopted and implemented. -Liberalization of interest rates in microfinance and simplification of legal procedures for collateral seizure.

prudential norms to facilitate effective supervision of microfinance institutions. -Liberalization of interest rates is effective and microfinance collateral is recognized in legal procedures for collateral seizure

and non mutalist MFIs were issued including: 11 regulations; 2 decrees; 8 instructions and 1 legislation to improve microfinance sector. These were developed based on microfinance international best standards. - A law was passed giving the Central bank supervisory role of MFIs with clear mandate. - Microfinance collateral is legally recognized and procedures for collateral seizure were developed based on international best practice. - The usury law was prepared but has not yet been submitted to the Parliament for endorsement due to the transitional nature of the government.

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments

Target achieved. The introduction of simplified microfinance prudential norms on capital adequacy, credit risk, limitation on exposures (to staff/Board members) and clarity on regulatory roles and codes of conduct have improved operations of the microfinance sector. The regulator is satisfactorily enforcing the laws; MFIs are adequately trained and are effectively in compliance with the norms. A streamlined registration procedure and supervision mechanism of microfinance institutions is in place for the different types of MFIs (level 1 - 3). Microfinance database and credit bureau managed by the regulator (Central Bank) is operational and has been linked with the credit bureau for banks. This has reinforced regulator’s capacity to supervise and manage risk for the entire financial sector. Although the old usury law has not formally been abolished, MFIs and other financial institutions are not obliged to adhere to it and in fact they currently set competitive market interest rates. (See Annex 3, Table 22, Table 23 and Table 24 for the full list of laws and legal instruments prepared).

PDO Indicator 2:*

Increased access to financial services by low income populations

Value (Quantitative)

3 SLA (microfinance networks) with 59 branches and 22818 members

About 72,500 low income families access financial services provided by SLAs/MFIs - 102 SLAs in operation

Existing five viable SLA networks with 200 SLAs in operation reach about 300,000 members of which 50% are women and 25% from disadvantaged groups

Five SLA Networks (comprised of 236 decentralized MFI branches) exist and are reaching 391538 members with diversified products (savings, loans, pension transfer) of which 51 percent are women.

xi

Project Development

Objectives (PDO)

Baseline Value

Original Target Values

(from approval documents)

Formally revised Target Values

Actual Values Achieved at Completion or Target

Years

-Total savings reach US$2.9 million and -Total outstanding loans US$3.5 million.

Total savings reach US$25 million and Total outstanding loans US$23 million. All MFIs are operationally self-sufficient and profitable.

A total of US$ 29million in savings was mobilized Loan portfolio had outstanding loans valued at US$23 million. The five MFI networks are on average operational self sufficiency (106%) and on average are financially self sufficient (103%).

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments (incl. %

achievement)

Target achieved. Membership target was exceeded by 30 percent. About 51 percent of beneficiaries are women. Reported beneficiaries comprise all members (savers only, savings and credit, savings and pension receivers). The total beneficiaries reported comprised 48,022 active loan accounts at closing in December 2010. Savings is prerequisite to loans which in this case indicate that there were more savers than borrowers among the beneficiaries.

PDO Indicator 3:*

Greater efficiency in judicial system for microfinance Institutions (Results are reported under PDO #1)

(Text) Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments Results are reported under PDO #1

PDO Indicator 4:

Increased productivity and improved standards of living of MFI clients

Value (Text)

No baseline data Impact study to confirm improved standards of living

An impact study (2005) confirmed that standard of living of beneficiaries had improved and land productivity had increased. Sixteen intermittent studies including feasibility studies for expansion were prepared.

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010

Comments (incl. % achievement)

This impact study was conducted before the 2007 restructuring of the project. The study findings indicate that standards of living of beneficiaries had improved. The study confirmed that overall 57 percent of the interviewed beneficiaries reported that their standards of living had improved as a result of participating in the project. Rural farmers reported that they were able to increase their land surface holding and bought fertilizers and inputs which increased productivity. In Lac Alaotra about 54 percent of interviewed beneficiaries were able to buy improved agriculture equipment, and 48 percent increased their land holding (at appraisal Lac Alaotra was reported to have high incidence of land seizure by money lenders - loan sharks) who were the main source of credit1. In Fianarantsoa, 40 percent reported increased number of livestock holding. Overall 40 percent of the interviewed beneficiaries reported increased revenues, 39 percent had increased

1 Restructuring paper for Additional Financing 2007.

xii

Project Development

Objectives (PDO)

Baseline Value

Original Target Values

(from approval documents)

Formally revised Target Values

Actual Values Achieved at Completion or Target

Years

school enrolment for their children due to income from their businesses. Overall 33 percent reported improved daily diet and 29 percent improved health status of their families. Focus group discussion reported that some borrowers were able to make home improvements due to profits gained from their businesses. Some were able to buy consumer goods like radios, television and fridges. The instability during the additional financing phase (2007 – 2010) made it difficult to undertake another study towards the end which could have provided updated evidence of the improved productivity and beneficiaries’ standard of living.

PDO Indicator 5:

Appropriate supervisory methodologies for MFIs established (Results are reported under PDO #1)

(Text) Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments

Results are reported under PDO #1

(b) Intermediate Outcome Indicators

Intermediate Outcome Indicator

Baseline Value

Original Target Values

(from approval documents)

Revised Target Values

(as approved by original approving

authority)

Actual Values Achieved at Completion or Target Years

IO Indicator 1: Prudential rules are issued for all MFIs (Results are reported under PDO #1)

(Text) Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Results are reported under PDO #1

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments Results are reported under PDO #1

IO Indicator 2:* Two existing SLAs (Fianaransoa and Toamasina) are strengthened and two new networks are created in Tana and Antsiranana and perform well (Results are reported under PDO #2)

Value (Quantitative)

Results are reported under PDO #2

Results are reported under PDO #2

Results are reported under PDO #2

Results are reported under PDO #2

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments (incl. % achievement)

Results are reported under PDO #2

IO Indicator 3: Build Capacity of microfinance through training

Value (Text)

Only few Malagasy have had formal training and can properly manage an MFI

80 persons attend one or more microfinance courses

Training program delivers specially designed and adapted technical modules to practitioners from all MFIs in the country. Evaluation of program confirms increased knowledge

A total of 19 training sessions including Training of Trainers (TOT) were organized through an umbrella microfinance apex association (APMF) for more than 100 MFI staff and practitioners. CSBF trained about 50 staff/Board members of MFI networks on the

xiii

Intermediate Outcome Indicator

Baseline Value

Original Target Values

(from approval documents)

Revised Target Values

(as approved by original approving

authority)

Actual Values Achieved at Completion or Target Years

and skills for proper management of MFIs.

new laws, prudential norms and internal risk control. CSBF staff benefited from; Exchange visits to Indonesia, Sydec Dakar and Boulder. They benefited from seminars offered by the World Bank on financial management/procurement, seminar on Basel norms; IBFI - banking accounting; FIS/BIS managing supervisions /financial risk, Credit Risk management; internship in Swiss Mutualist banks (RAIFFEISEN), K-REP Kenya; Indonesia bank Rakiat and NGO BINA SWADYA etc. AGEPMF resident consultants (DID Canada) offered various in-house training to staff/Board of MFI networks on governance, internal control systems, credit risk management etc. Evaluations reports confirm improved capacity of MFI practitioners (see training reports attached).

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments

Targets achieved with positive impact at all levels (sector , Central bank, MFI networks staff & Board etc) as evidenced by solid capacity of MFI networks in credit risk and operations management and the effective regulation/supervision of MFIs by the regulator. There is evidence of increasing number of microfinance specialists in the country who provide consultancy services. MFI practitioners interviewed confirmed that there are sufficient courses in microfinance in Madagascar compared to 1999 where most of the trainings were conducted abroad.

IO Indicator 4:* Financial Self Sufficiency (FSS) (Core Indicator)

Value (Text)

N/A N/A FSS for all MFIs to be measured (< 100% for all MFI networks)

The five MFI networks achieved 103% average financial self sufficiency

Date achieved 20-May-1999 31-Dec-2004 31-Dec-2010 31-Dec-2010

Comments (incl. % achievement)

Target achieved satisfactorily. OSS & FSS were added as core mandatory indicators. Average OSS achieved was 106 percent (against 122 percent baseline (2006*) set at restructuring2 and against international best practice of 100 percent breakeven point. The OSS targets established at restructuring were based on a good trend performance of prior years (before additional financing) but they proved to be ambitious during the turbulent era of additional financing. Average FSS achieved of 103 percent is quite good3 as international best practices have proved that institutional development of rural MFIs can

2 There was no OSS target established for 2010 during restructuring as the project was to end in 2009. Also no FSS targets were established as this core indicator was added after restructuring was completed. 3 No targets were established for FSS.

xiv

Intermediate Outcome Indicator

Baseline Value

Original Target Values

(from approval documents)

Revised Target Values

(as approved by original approving

authority)

Actual Values Achieved at Completion or Target Years

take up to 15 years to become fully financially self sufficient (breakeven at 100% FSS) due to high start-up costs (fixed/operating) particularly in remote rural settings dealing mainly with agriculture loans as was the case in this project. The FSS is an excellent measure of efficiency and efficacy of MFIs as it takes into account costs of funds and inflationary effects as opposed to OSS which focus on coverage of operational costs. At closing the FSS achieved for two MFIs (Diana and Fianarantsoa) was far above the breakeven point. These two networks are the best performers with Diana being the main source of loans to other MFI networks at 12% interest rate which is slightly below average market rate of 15%. The FSS for three MFI Networks were slightly below the 100% breakeven point (OTIV Tana 94.5%; Alaotra Mangoro 99.14% and Toamasina 97.16%). OTIV Tana which covers semi urban settings had high incidence of borrowing from commercial banks which comes with high cost of funds. Also commercial borrowing shrunk in 2009/10 due to financial crisis. (See Annex 2 for a thorough performance assessment of OSS & FSS for the five MFI networks).

IO Indicator 5: Portfolio At Risk (PAR) (Core Indicator)

Value (Text)

N/A NPL to be measured

MFI networks have NPL of 10% against the industry norm of 5%..

Date achieved 20-May-1999 31-Dec-2010 31-Dec-2010

Comments

PAR (NPL) was core mandatory indicator added later to the project. NPL ratio decreased by 4% from 14% observed in 2009 during the financial and political crisis. This means an estimated overall average repayment rate of 90 percent (30 days past due loans) against 95 percent estimated target during restructuring in 2007. Loan underwriting was slowed down in 2009/2010 to focus on risk management and loan recovery. Overall MFIs made profits with 17 percent Return on Equity (ROE) in 2010 albeit the worries on portfolio at risk. The microfinance sector as a whole in sub-Saharan Africa (SSA) suffered losses and raising NPL in 2009 – 2010 (see sub-Saharan Africa (SSA) microfinance performance details under section 3.2 – 3.4)..

IO Indicator 6: Number of active loan accounts – Microfinance (Core Indicator) Value

4,027 70,212 48022

Date achieved 20-May-1999 31-Dec-2010 31-Dec-2010

Comments (incl. % achievement)

Target achieved at 68%. Loan underwriting which was steady prior to 2009 crisis was substantially decreased in 2010. Despite the decrease, the networks remained profitable and were on average operationally self sufficient (106%). This figure includes only loan accounts as opposed to overall beneficiaries’ number which include borrowers and savers (including pensioners).

IO Indicator 7: Active loan accounts for women) (Core Indicator)

Value 1562 4,505 18715

Date achieved 20-May-1999 31-Dec-2010 31-Dec-2010

Comments

Target achieved and exceeded. Loans to women groups were above 50%. Special associations were established to accommodate the needs of women from the low income groups. The women tailored program has been mainstreamed to core products of MFI networks.

xv

G. Ratings of Project Performance in ISRs

No. Date ISR Archived

DO IP Actual Disbursements

(USD millions) 1 06/30/1999 Satisfactory Satisfactory 0.00 2 11/22/1999 Satisfactory Satisfactory 1.88 3 05/15/2000 Satisfactory Satisfactory 2.35 4 10/16/2000 Satisfactory Satisfactory 3.12 5 05/29/2001 Satisfactory Satisfactory 4.12 6 11/29/2001 Satisfactory Satisfactory 5.73 7 05/15/2002 Satisfactory Unsatisfactory 6.32 8 09/26/2002 Satisfactory Unsatisfactory 6.74 9 04/28/2003 Satisfactory Satisfactory 7.69

10 11/06/2003 Unsatisfactory Satisfactory 9.46 11 03/02/2004 Unsatisfactory Satisfactory 9.56 12 05/11/2004 Unsatisfactory Satisfactory 10.12 13 11/18/2004 Satisfactory Satisfactory 10.66 14 06/13/2005 Satisfactory Satisfactory 12.98 15 12/13/2005 Highly Satisfactory Satisfactory 13.90 16 06/26/2006 Highly Satisfactory Satisfactory 15.34 17 12/29/2006 Highly Satisfactory Satisfactory 15.80 18 06/25/2007 Highly Satisfactory Satisfactory 16.22 19 10/31/2007 Satisfactory Satisfactory 16.35 20 06/12/2008 Satisfactory Satisfactory 17.80 21 12/19/2008 Satisfactory Moderately Satisfactory 19.23 22 06/19/2009 Moderately Satisfactory Moderately Satisfactory 19.29 23 12/29/2009 Moderately Satisfactory Moderately Satisfactory 19.29 24 05/31/2010 Moderately Satisfactory Moderately Satisfactory 19.29 25 03/27/2011 Moderately Satisfactory Moderately Satisfactory 20.98

H. Restructuring (if any)

Restructuring Date(s)

Board Approved PDO

Change

ISR Ratings at Restructuring

Amount Disbursed at

Restructuring in USD millions

Reason for Restructuring & Key Changes Made

DO IP

10/22/2002 U S 6.94

The political crisis made it necessary to restructure the project and enable the Bank finance all activities at 100% without government contribution to allow for effective implementation. Government contribution was not easily forthcoming and that affected implementation.

xvi

Restructuring Date(s)

Board Approved PDO

Change

ISR Ratings at Restructuring

Amount Disbursed at

Restructuring in USD millions

Reason for Restructuring & Key Changes Made

DO IP

2007 HS S 16.22

Additional financing was to bridge the gap required to prepare the Financial Services Project (PASEF) program through which the subsequent phases of the microfinance adaptable program loan (APL) were to be undertaken.

I. Disbursement Profile

1

1. Project Context, Development Objectives and Design

1.1 Project Description

1. The microfinance project was the first phase of a 15-year microfinance program aimed at fostering a sustainable microfinance system to address the lack of financial services for lower income population and contribute to the national objective of poverty reduction. A study on poverty changes4 in Madagascar revealed that poverty rose from an already high level of 70 percent in 1993, to 73.3 in 1997, before falling to 71.3 in 1999. This pattern of change, which corresponded to the evolution of macroeconomic policy during that period, was restricted primarily to urban areas. Populations in rural areas witnessed persistent increases in poverty despite market reforms, as structural constraints including remoteness and low land productivity affected their ability to escape poverty. Small scale agricultural households were hit particularly hard. Access to financial services was limited as all banks were state owned and failing. Attempts to develop credit operations to smallholder farmers had not been successful, as the banking sector, mainly the public banks which were to lend to low-income clients, had ill-adapted products, high costs, and poor recovery rates.

2. Rationale for Bank Assistance: The Microfinance program was designed to increase access to finance for low income population, and improve policy and capacity in the microfinance sector. This was to be achieved through the establishment of an appropriate legal, regulatory and supervisory framework for microfinance, the expansion of microfinance skills, and the development of strong and sustainable local institutions. The program built on successful experiences piloted under the World Bank-financed Rural Finance Technical Assistance Project (RFTAP) (Cr. 2459-MAG), designed in 1993, which developed a new approach of delivering savings-based credit through the creation of savings and loan associations (SLAs) also known as financial cooperatives. Recognizing that traditional approaches to rural finance were ineffective and paid little attention to savings, RFTAP aimed to promote a sustainable savings and loan movement at the grass-roots level that would provide sound financial services to its members and over time link up with formal institutions. Under RFTAP, between 1993 and 1997, a law was promulgated and three microfinance networks totaling 54 SLAs/financial cooperatives were created with about 175 members per SLA on average and average savings of US$15-US$20 per person. These SLAs were subsequently licensed as microfinance institutions (MFIs) under the new law. The experience brought to light the importance of capacity building in microfinance and the time needed for MFIs to break even and become sustainable. Experience had also proved that this type of intervention required sustained support over a long period of time to support policy development and implementation. Thus, an Adaptable Program Loan (APL) was chosen as the instrument to support the program over a 15-year period in three five-year tranches with the aim to ensure long-term viability of SLAs (or MFIs). Phase I would support the development of a legal/regulatory and supervisory framework for microfinance institutions (MFI); the design and testing of a national training program in microfinance; and the establishment of SLAs in four of Madagascar's six provinces. Phase II would support the

4 Stefano Paternostro et al, 2001, Cornell Food and Nutrition Policy Program Working Paper No. 120

2

consolidation of the SLAs by expanding coverage in the areas where they were established, and, if feasible, penetrate into other areas to reach a sustainable scale and cost structure. It would also implement a microfinance training program. Phase III would finally help strengthen the financial core of SLA networks and support its evolution into full-fledged self-sustainable financial institutions.

3. The Microfinance program supported the Government's objective of reducing widespread poverty, which was at the center of the Country Assistance Strategy (CAS, document number 16249-MAG, February 1997). Improving access to financial services—a frequently cited constraint to agricultural and entrepreneurial activity in Madagascar—was to support the CAS objectives of rural development as well as private sector development. Government’s aim was to improve financial intermediation to support investment and growth. Microfinance was seen as a vehicle for financial deepening and a means to compensate for the failure of the banking sector in providing financial services to people with limited resources. The project was to help alleviate poverty by making financial services (both credit and savings facilities) available to an increasing number of lower income populations, especially small-scale farmers, artisans, traders and women. This would help increase productivity, incomes, and living conditions. The program also supported the CAS objectives of sustainability, capacity building, stakeholder consultation, donor collaboration and continuous learning (building on the pilot RFTAP).

1.2 Context at Appraisal

4. At appraisal, the Malagasy financial system was embryonic, and represented a constraint to investment and economic activity. In 1998, the system comprised six commercial banks (two state-owned, being privatized), a savings bank, three insurance companies (two state-owned), four savings and loans associations (SLAs) also known as financial cooperative networks, and two small donor-supported microfinance institutions (MFIs). Madagascar’s financial sector reforms led to the closing of many rural bank branches and further widened the gap in access to financial services by the poor and people in the rural areas. The Government was aware of the financial sector constraints. It was committed to address them by pursuing macroeconomic policies that ensured price stability, which is a precondition for financial sector development. Equally, it was committed to further liberalize the sector. The Government's strategy for microfinance was spelled out in its Letter of Development Policy of April 1999: the objective of improving access to financial services was part of the financial sector strategy. Reflecting this commitment, the Government had encouraged private initiatives in support of MFI development and enacted legislation promoting and regulating MFIs under the Rural Finance Technical Assistance Project (RFTAP) upon which the microfinance project was built.

1.3 Original Project Development Objectives (PDO) and Key Indicators (as approved)

5. The original Project Development Objective was to provide increased financial services to the low-income population not served by the traditional banking sector. The project aimed to set up an appropriate policy framework for the development of microfinance and to help establish microfinance institutions. The Project development objective was to be measured through the following key outcome Indicators:

3

a) Enabling laws and regulations for MFIs

b) Greater efficiency in the judicial system (through improved legal texts and legal procedures)

c) Appropriate supervisory methodologies for MFIs established

d) Outreach to low-income families (about 72,500 low-income families accessing financial services provided by SLAs)

e) Increased productivity and improved standards of living of the beneficiary households

1.4 Revised PDO (as approved by original approving authority) and Key Indicators, and reasons/justification

6. The PDO remained unchanged throughout the project. However, it was expressed differently in the original PAD, the restructuring paper and DCA.

7. The Key Outcome Indicator for assessing the achievement of the PDO for this project is, therefore, indicator #2 which is “increased access to financial services by low income population.” More than 70 percent of the project budget and the level of effort were directed to support this objective.

8. Some of the targets were changed and new indicators introduced during project implementation (See Table 4). The results framework for this ICR is based on the revised indicators adopted in 2007 when the project was restructured as well as core indicators (Operational Self Sufficiency (OSS) & Portfolio at Risk (PAR) or Non Performing Loans - NPL) which were added later. All baseline values are as of June 1999 except for mandatory core indicators which did not have a baseline as they were added towards the end of the project. The analysis in section 3.2 has taken into account the targets for operational self-sufficiency (OSS) which were established in the restructuring paper (2007).

9. The justification of overall outcome rating under section 3.4 has been split for two periods of project implementation (before and after additional financing) and a weighted method has been adopted for this assessment. The same method has been used in sections 3.2 and 3.3 to rate achievement of PDOs and project Efficiency/Efficacy. Although the PDO of the project was never changed, the analysis has adopted the weighting method in order to effectively recognize the outcomes achieved during the two separate eras (Pre Additional Financing period and the Additional Financing period that started in 2007 when the project was restructured and lasted until 2010.

10. The results framework has several similar indicators (project development objectives - PDOs & intermediate outputs - IOs). Some adjustments were made for improved analysis and reporting. Two PDO indicators were, thus, combined and two intermediate outcome indicators were matched with relevant PDO indicators for analysis of results (see table below).

4

Table 1. Grouping of PDO Indicators and Intermediate Indicators

Grouping of indicators Comment on adjustments PDO Indicator #1 Enabling legal and regulatory environment for doing microfinance business in Madagascar exists

PDO Indicator #3: Greater Efficiency in judicial system for microfinance institutions

Results for PDO #3 are reported under PDO Indicator #1

PDO Indicator #5: Appropriate supervisory methodologies for MFIs established

Results for PDO #5 are reported under PDO Indicator #1

Intermediate Outcome Indicator #1: Prudential rules are issued for all MFIs

Results for IO#1 are reported under PDO Indicator #1.

PDO Indicator #2 Increased access to financial services by low income populations

Intermediate Outcome Indicator #2: Two existing SLAs (Fianarantsoa and Toamasina) are strengthened and two new networks are created in Tana and Antrisanana and perform well

Results for IO #2 are reported under PDO Indicator #2

Table 2. Project Statements of Objectives

Objective as stated in the PAD

Objective as stated in the DCA

Objective as stated in the

Project Paper – Additional financing

Objectives as stated in Project

Agreement

To provide increased financial services to the low-income population not served by the traditional banking sector.

To assist the Borrower in a) Carrying out the first phase of its program to provide about 80,000 low-income families engaged in small-scale farming, livestock, fishing, commerce, and handicrafts production activities with long-term access to financial services thereby improving their productivity, income and living standards and conditions. b) The establishment of legal and regulatory framework for microfinance operations c) The expansion of microfinance skills and d) The development of strong and sustainable microfinance institutions through inter alia establishment of a refinancing mechanism.

To increase long-term access to financial services to low-income populations in Madagascar.

Providing increased financial services to the low-income population not served by the traditional banking sector.

5

11. Although the objective is expressed differently the three elements of improving long term access, policy and capacity in the microfinance sector which were core to the original PAD objective remained unchanged and relevant. These three elements were consistently used in the Implementation Status and Results (ISR) reports and have been used to judge the achievement of PDOs for this Implementation Completion and Results (ICR) Report. Improving “access” carries more weight than the other two elements since more than 70 percent of the budget and most of the level of effort was directed to support this objective than the other two. Some of the targets were changed and new indicators introduced during project implementation (see table below). The results framework for this ICR is based on the revised framework adopted in 2007 when the project was restructured as well as mandatory corporate indicators which were added later. The end-of project targets in the results framework are thus those in the project paper of 2007. All baseline values are as of June 1999 except for mandatory core indicators which did not have a baseline as they were added towards the end of the project. ICR reporting on the Outcomes at completion is based on revised targets where applicable.

12. Project outcome indicators as well as other key performance indicators (KPIs) and targets were revised during restructuring in 2007 as explained before and summarized in the table below.

Table 3. List of Original and Revised Targets at Restructuring (2007) by PDOs

PDO Indicators Original target at appraisal in

1999 Revised target in 2007

PDO 1: Enabling laws and regulations for MFIs

Microfinance law and regulations that reflect international best practice are issued, adopted and implemented

Microfinance law is effective and regulations that reflect international best practice are issued, adopted, and implemented

PDO 2: Increased access to financial services by low income populations

About 72,500 low income families access financial services provided by SLAs/MFIs

Existing five SLA networks are viable and able to offer services to 300,000 members

PDO 3: Greater efficiency in judicial system (through improved legal texts and procedures)

Liberalization of interest rates in microfinance and simplification of legal procedures for collateral seizure

Liberalization of interest rates is effective and microfinance collateral is recognized in legal procedures for collateral seizure

PDO 4: Increased productivity and improved standards of living of microfinance clients

Impact study to confirm improved standards of living

Impact study to confirm improved standards of living of SLA members

PDO 5: Appropriate supervisory methodologies for MFIs established

All licensed MFIs are adequately supervised by the authorities

N/A

6

Table 4. List of Original & Revised Indicators at Restructuring (2007) - Project Outcome Indicators

Intermediate Outcome (IO)

Indicators

Original target at appraisal in 1999

Revised target in 2007

IO indicator 1 Prudential rules are issued for all MFIs Appropriate laws and regulations are

passed and implemented for all MFIs.

Appropriate laws and regulations are passed and implemented for all MFIs.

IO Indicator 2* Two existing SLAs (Fianaransoa and Toamasina) are strengthened) and two new networks are created in Tana and Antsiranana and perform well.

149 SLAs exist in at least 4 provinces. Total membership; 72,469 members included 23,351 in disadvantaged groups. Total savings is US$3.5 and total loans is US$4.4 million. MFIs are profitable.

Five SLA networks with 200 SLAs in operation reach about 300,000 members of which 50% are women and 25% from disadvantaged groups Total savings reach US$25 million and Total outstanding loans US$23 million. All MFIs are operationally sustainable.

IO Indicator 3* Build Capacity of microfinance through training 80 people attended one or more

external courses. Training program tested and evaluated. 22 field agents and 46 professional staff are trained each year

Training program delivers specially designed and adapted technical modules to practitioners from all MFIs in the country*. Evaluation of program confirms increased knowledge and skills for proper management of MFIs.

IO Indicator 4** Core

N/A Financial Self Sufficiency (FSS)**

IO Indicator 5** Core

N/A Portfolio At Risk (PAR or NPL)**

IO Indicator 6** Core

N/A Outstanding Microfinance Loan Portfolio**

IO Indicator 8** Core

N/A Number of active loan accounts – Microfinance**

IO Indicator 9** Core

N/A Active loan accounts for women**

* Revised indicator at restructuring ** New mandatory Core World Bank Indicators were introduced after 2007

1.5 Main Beneficiaries

13. The main beneficiaries were the low income populations, particularly those in the rural areas. The project was supposed to help make financial services available in four out of six provinces in Madagascar to low-income households that lacked access to banking services, thereby expanding their incomes and reducing poverty. MFI networks were particularly targeted including women’s savings and credit groups to help them reach an estimated 72,500 low-income families (about 300,000 people) with adapted financial services. Another group of beneficiaries were the Central Bank of Madagascar (BCM) through the Banking Commission (CSBF) for supervision of microfinance, and the umbrella

7

microfinance Professional Association (APIMF) for the training program.

1.6 Original Components

The project had originally four technical components and one administrative component:

Component 1: Improve legal, judicial and regulatory framework (US$0.61 million)

14. Success in the development of microfinance in Madagascar was dependent on the ability of the government to improve the legal regulatory and judicial and supervisory framework. Project funds were made available to (i) support preparation and enactment of laws and regulations that supported development of an inclusive microfinance sector based on international best practices; and (ii) establish competencies at the Secretariat of the Banking Supervisory Commission for inspection of MFI networks rather than delegating this function to an outside entity. This involved preparation of laws and decrees, intensive training of supervisory authorities (courses, seminars, study tours and internships), MFI Board members and MFI staff on the new regulatory framework, including prudential norms, regulators roles, internal control, risk management and reporting.

Component 2: Develop MFIs (US$13.5 million)

15. This component was allocated 82 percent of the International Development Association (IDA) funding to support the development of five microfinance networks. The funding was primarily used to finance resident technical assistance from international microfinance capacity building providers (DID, WOCCU, IRAM) to strengthen the capacity of MFIs to become efficient and viable financial structures. Funding also supported operational expenses for the apex organization, vehicles and equipment, start-up costs for MFIs branches, including expenses associated with the construction of office buildings, staff salaries for the first year of operations, as well as training of staff and the Board.

Component 3: Build Capacity in microfinance (US$0.5 million)

16. This component aimed to address the long-term goal of increasing the microfinance capacity in the country through existing local training institutes and the umbrella association for microfinance institutions. The funding supported training needs assessment, design of the curriculum and training materials, study tours, internships, workshops and seminars for practitioners. The training program was to breed a cadre of trained trainers and trained staff managing the MFIs.

Component 4: Studies (US$0.92 million)

17. This component was to support a number of audits, impact studies and feasibility studies. Audits included financial and management audits of MFIs and the project coordination agency (AGEPMF).

Component 5: Project coordination (US$0.90 million)

18. Project coordination was undertaken by the Executive Secretariat of AGEPMF, an

8

independent agency created by Government decree. The Secretariat was made up of an Executive Secretary, technical and administrative staff with responsibility of coordinating overall project implementation. It is to be noted that a separate agreement was signed between the Central Bank and IDA to allow CSBF - the unit in charge of microfinance development at the Central Bank - to oversee implementation of component 1 (policy reforms) of the project.

1.7 Revised Components

19. Project components were not changed. As explained before (section 1.4 above) targets and some indicators were revised at restructuring in 2007 for the additional financing. Also additional core indicators were introduced (FSS & PAR or NPL).

20. Targets under component 1 were revised to: (i) support the implementation of the Microfinance law rather than a financial cooperative law passed previously as well as the adoption of prudential regulations that were in line with industry best practice, and (ii) strengthen the capacity of the Central Bank (CSBF) to properly supervise MFIs licensed under the new law. A 10 percent of the additional financing went to this component to help CSBF execute its mandate effectively. At closing, 32 percent of budget was utilized with outstanding commitments yet to be paid.

21. Targets under component 2 were revised to help MFIs (i) increase their membership to 300,000 clients of which 50 percent would be women and 25 percent from disadvantaged groups, (ii) increase savings to US$25 million, and credit outstanding to US$23 million, and (iii) achieve operational self-sufficiency (OSS) for all partner MFI networks. Most of the additional financing (74 percent) was allocated to this component and 95 percent of these funds were utilized by the closing date in December 2010.

22. Targets for component 3 were revised to include training of trainers (TOT) curriculum and modules which was done with help from CGAP.5 Only 1.8 percent of the additional budget was allocated to this component of which 88 percent was spent at closing.

23. New targets for Operational Self Sufficiency (OSS) were established in 2007 during restructuring for additional financing. Additional core indicators (FSS & PAR or NPL) were introduced later.

1.8 Other significant changes (in design, scope and scale, implementation arrangements and schedule, and funding allocations)

24. The political crises and implementation of FSAP recommendations which were all unforeseen at the design stage changed the scope of the project and directly contributed to the lengthy implementation period of eleven years. The microfinance project was initially planned to close on December 31, 2004. The project closing date was extended five times with the final closing date being December 31, 2010. The project was restructured in 2002

5 CGAP = Consultative Group to Assist the Poor is a leading microfinance think-tank involved in setting standards and providing training in microfinance.

9

due to unsatisfactory performance on implementation resulting from the first political crisis and again in 2007 to implement FSAP recommendations as explained below. Restructuring and preparation of the additional financing also contributed to the lengthy implementation period.

25. The first two closing date extensions were for one year each from December 31, 2004 to December 31, 2005 and then to December 31, 2006. These extensions were justified by consequences of the December 2001 Presidential elections crisis that led to a slowdown in project activities and disbursement; hence the need for reallocation of project funds including increasing the amount of the authorized allocation for the project coordination unit (AGEPMF).

26. The third extension was from December 31, 2006 to June 30, 2009. The scope of the project changed when FSAP (2005) recommended that microfinance project be part of the larger financial sector project (PASEF). In 2005, the World Bank/IMF Financial Sector Assessment (FSAP) Report had identified persistent lack of access to finance for micro, small and medium enterprises (MSMEs) and the need to design a broader financial sector program that would support banks and non bank financial institutions including microfinance. When the Government of Madagascar was ready to implement these recommendations in 2006 through a sector wide Financial Service Project (PASEF), an agreement was reached with the Bank to consolidate operations and have Phases 2 and 3 of the microfinance APL folded into the PASEF. The microfinance project had achieved overwhelming results at this stage (end 2006) and MFIs had proved to be making very good progress towards sustainability.

27. This third extension to June 2009 (at the request of the Government of Madagascar) allowed the project to complete some key activities and to continue to provide support to the microfinance sector in the absence of a phase 2 APL due to IDA constraints. The microfinance project was, thus, restructured in 2007 when additional financing of US$5 million was approved as bridge finance to facilitate smooth transition of microfinance project to PASEF which was still in preparation as a Specific Investment Loan (SIL). This ensured continued financial support and technical assistance to avoid a serious risk of systemic failure of the microfinance sector if assistance was to be stopped abruptly (the networks supported under the project accounted for over 70 percent of all microfinance savings in the country).6 The supplemental credit was approved by the Board of Executive Directors on April 10, 2007 and was ratified by the Parliament of Madagascar end-June 2007. Tables below show project financing provided during the life of the project including sources of funds.

6 Refer to ISR #18 of the microfinance project for more details.

10

Table 5. Financing Breakdown by Component

1.9 Original

Financing (SDR)

Additional Financing

(SDR)

Total Financing

(SDR)

Total Financing

(US$) A. Improve legal, judicial, and regulatory framework

416,300 340,000 756,300 1,164,702

B. Develop MFIs 8,005,938 2,520,000 10,525,938 16,209,945

C. Build Capabilities in Microfinance

725,193 60,000 785,193 1,209,197

D. Conduct Studies 610,337 110,000 720,337 1,109,319

E. Coordinate Project 982,328 360,000 1,342,328 2,067,185

Equipment 70,000 10,000 80,000 123,200

PPF 0

Totals 10,810,096 3,400,000 14,210,096 21,883,548

Project burn rate at closing 100% (in 2006)

86% December

2010 & 94% April 30, 2011

Exchange rate used: SDR 1 = US$ 1.54 Slight variations are observed on the total budget due to the exchange rate effects. Extension to spend beyond closing date was approved up to April 2011 which resulted to 94 percent burn rate when the credit closed.

Table 6. Breakdown of sources of funds (US$)

From 1999 to

2004 2005 2006 2007 2008 2009 2010 Cumulative %

IDA (US$) 8,321,835 2947917 1265815 5041595 2281996 82031 1628848 17,032,603 93

Government (US$)

913,890 20,081 5078 34676 22117 995,842 5

Other Sources (Short Term Debt)

796,152 1,300 -386860 14038 -235911 143328 332,046 2

TOTAL 10,031,877 2,971,303 886,040 554,881 2,070,211 227,368 1,630,858 18,360,491 100

Source: Project documents (AGEPMF progress report – April 2011) Notes: Conversion rate US$1 = MGA 2000. Totals are slightly different from project documents due to exchange rate fluctuations. It is not clear in the report what the source of the short term (ST) debt was. Also Government contribution quoted beyond the APL phase (may include the office space and salary of project coordinator who was government employee)

28. The fourth closing date extension period was from July 1, 2009 to June 30, 2010, which was followed by the fifth and last extension of six months to December 31, 2010. These two extensions were due to the political crisis that hit Madagascar following a coup in March 2009 and were to allow the project to remain open through the crisis period. The crisis led to the country operating under World Bank Operational Policy OP 7.30 which caused interruption in project activities due to lack of funds in the designated/special accounts.

29. Finally when the OP 7.30 was waived (for a select group of projects including this project), it was crucial to have a six months extension to facilitate payment of all the arrears that were due to diverse entities, including partner microfinance institutions as well as

11

project staff. The disbursement ratio reached 94 percent at end of April 2011 after the four-month grace period given to the project for disbursement.

Table 7. Additional Financing Cost Breakdown & Disbursement Rate (December 2010) by Component

1.10 Additional Credit

(Restructuring Stage 2007)

Actual Expenditures (Additional Financing)

December 31, 2010

Burn Rate on

Additional Financing (December 31, 2010)

Percentage of

Additional Financing to

Each Component

A - Improve legal, judicial, and regulatory framework

0. 2 0.07 32% 10%

B – Development of MFIs

1.6 1.55 95% 74%

C - Equipment 0.01 0.01 90% 0.30%

D - Build Capabilities in Microfinance

0.04 0.03 88% 1.80%

E - Conduct Studies 0.07 0.05 75% 3.20%

F - Coordinate Project 0.23 0.16 68% 11%

TOTAL FINANCING 2 2 86% Exchange rate used: US$ 1 = SDR 1.54 Slight variations are observed on the total budget due to the exchange rate effects.

30. The Development Credit Agreement (APL phase 1) was amended once during implementation on January 23, 2003 to update the disbursement table and provide, inter alia, for a temporary 12-month increase in the disbursement percentages of certain categories of expenditures, increased the amount of the authorized allocation for the project implementation unit (AGEPMF) special account, and provide for the regular preparation and transmission of financial monitoring reports.

31. A major change on project management took place in 2007 during the restructuring for additional financing7 when the Government was allowed to nominate one of its staff to become the Executive Secretary of the PIU.

7 See Project Paper on Proposed Additional Financing (Report # 38892). This decision was made to support Governments’ agenda on implementation of Paris Declaration on “Harmonization and Alignment for Development Results”

12

2. Key Factors Affecting Implementation and Outcomes

2.1 Project Preparation, Design and Quality at Entry

32. The Microfinance program was prepared at a time when Madagascar was in need of alternative instruments to complement macro reforms and spur equitable growth. In the 1990s when the economic reforms supported by the World Bank were shaping the macroeconomic future of the country, financial sector reforms left the majority of the population, particularly the poor and rural areas, without access to financial services.

33. The project design supported the financial sector CAS (document number 16249 of February 1997) goal which was to improve savings and support economic expansion, and raise the low level of financial services, especially outside key urban centers. Project preparation took into account the Bank's financial sector reviews and worldwide experience that identified reasons for insufficient and ineffective provision of financial services in Madagascar to lower income clients.

34. The design was intended to mitigate key constraints to financial access; particularly the access gap for the poor in rural areas. The design was cognizant that: (i) private commercial banks were lending only to well-established clients because of limited competition in the sector, their business philosophy and negative perception of country risk; (ii) transaction costs of microfinance programs were high; (iii) low-income clients generally lacked collateral and were unknown to the banks, which made it difficult to assess their ability and willingness to repay; and (iv) the legal and judicial systems were not developed and contract enforcement was difficult.

35. Project design was anchored upon lessons emanating from the financial sector reform process and from a tested rural finance approach through the RFTAP pilot project and what other donors were doing in the country. As already mentioned, the lending instrument, a 15-year APL was quite appropriate as the project’s aim was to address the long term institutional and policy constraints that hindered access, which needed time to bear results. For a program that aimed at supporting microfinance institutions (MFIs) to become sustainable, international experience has proved that long time is required to achieve such a goal.

36. The project was kept relatively simple by focusing on microfinance issues rather than expanding its mandate to other sectors of the financial system such as banking and insurance. The project was designed to allow for gradual expansion to the rest of the country based on feasibility studies and the pre-identified triggers (see PAD April 1999)

37. Assessment of risk by project team was adequate at project preparation. The team properly identified risks related to the appropriateness of reforms, adequacy of training being offered, and interest of populations to become microfinance clients. For example the design of the microfinance reform agenda focused on improving the existing banking laws to fit the needs of the microfinance sector instead of pushing for a new and parallel reform agenda, which could have taken long time with risk of laws not being passed expeditiously (as was the case with a new law on usury which is yet to be passed after eleven years of project

13

implementation). Expansion to new provinces and sites was to be preceded by feasibility studies to appraise economic potential, clients demand and supply capacity required for effective interventions.

38. The design was cognizant of the risks associated with poor institutional and absorption capacity of key stakeholders to implement reforms and to develop a sustainable microfinance program that targeted the low-income segments. The design embedded intensive technical assistance and capacity building in the core components of the project to mitigate these risks. One of the outstanding design features was the emphasis on institutional and capacity development, legal and regulatory reforms as a foundation for building a sound and sustainable microfinance practice in the country. This resulted for most of the project indicators being qualitative with just a few on quantitative mainly focusing on the microfinance outreach and portfolio quality.

39. However, the design failed to assess the risks of the other phases of the APL not materializing as well as political instability in the country. Although the microfinance program took off from a stable political environment in 1999, the PAD did not foresee the political unrests that twice hit the country and hampered the speed of program implementation. Nevertheless, during the two political crises of 2001/2002 and 2009, MFIs remained resilient and continued to operate, albeit under difficult conditions and increased risk to their loan portfolio. This resilience is attributed to the design of the project which put core functions of MFIs’ management in the hands of their member-shareholders.

40. The design of the additional financing also failed to see the risks associated with allowing8 the Government to nominate a public servant to lead a team of experts paid by the project on terms that were not similar to those of the government. The design did not spell out a strict selection criteria for such a nominee which could have also ensured that the nominee had competencies required to lead a complex financial sector project.

2.2 Implementation

41. Project implementation started on a good footing. However, after relatively good progress made during the first two years, implementation progress was downgraded to unsatisfactory. The implementation period between 2001 – 2009 experienced significant grueling events (political crisis and restructuring in 2002, MTR in 2004 leading to the an extension of the closing date, the death of the project coordinator and recruitment of replacement, restructuring for additional financing and the second political crisis and financial crisis in 2009) that triggered ad-hoc changes which impacted the speed and relatively the quality of project implementation.

42. The political crisis in December 2001 affected the speed of implementation and posed certain institutional risk to MFIs. Several microfinance networks experienced liquidity constraints due to the freezing of their reserves by the monetary authorities that were unable to redeem the treasury bonds on schedule. MFIs also suffered from a high proportion of non-

8 See Project Paper on a Proposed Additional Financing ( Report #38892 MG)

14

performing loans resulting from exogenous factors in the borrowers’ business environment. In addition, one of the MFI (Toamasina) temporarily lost its technical support when the contract for the technical assistance agency (provided by DID Canada) expired in the middle of the crisis and could not be renewed. The project coordinator also died. Project activities slowed down until another qualified coordinator was hired. The project was restructured as well as some of the MFIs, and the closing date was extended. The mid-term review in February 2004 thoroughly appraised the request by members to split the Toamasina microfinance networks into two (Tamatave and Lac Alaotra) to ease implementation. The technical assistance program was also redesigned to accommodate these changes.

43. The political crisis of 2009 negatively affected the profitability and sustainability levels of MFIs. It also resulted in delays in implementation that led to two extensions of closing dates. Some of the MFIs that were operationally self sufficient experienced losses. The overall ratio of Non Performing Loans (NPL) reached peak levels (14 percent in 2009 against the sector norm of five percent). This reduced both the operational and financial self sufficiency ratios of the MFIs. The project which was rated highly satisfactory (2005 – June 2007) and satisfactory (December 2007-December 2008) was subsequently downgraded to moderately satisfactory. Risk mitigation strategies (curtailing loan underwriting, intensive savings mobilization, revised/tight loan appraisal/client risk assessment etc.) applied by MFIs reversed the performance in 2010 to an overall positive profitability (overall) and sustainability indices. The NPL ratio was reduced to 10 percent (4 percent positive leap in just one year). This was an indication that technical assistance provided to MFI networks by international technical assistance providers was well assimilated and had increased risk management capacity of local MFI staff.

44. Government’s commitment for the microfinance project remained generally strong during the life of the project especially through positive policies and strategies for the microfinance sector. However, some factors subject to government control affected project implementation. Government counterpart funds were often disbursed late due to bureaucracy and liquidity problems at the treasury resulting mainly from the political crisis. On government’s request the counterpart funds were waived during the 2007 restructuring to speed implementation.

45. The transition government in power after the 2009 political crisis has not been an effective partner in project implementation. Recommendations made by several supervision missions and audit reports were neither effectively followed upon nor implemented as per the signed agreements between IDA and the government. This contributed to the deterioration of project management and coordination (in the last three years) under the leadership of the PIU coordinator who is a government employee.

46. Poor leadership at the PIU also affected the quality and speed of project implementation after 2007. Project reports were often submitted late and auditors’ recommendations were not implemented. Auditor’s recommendations (2009) had reiterated the need to hire an internal auditor and procurement specialist to fill the vacant position left by the previous staff who had left the project. This was not implemented despite several recommendations made by World Bank supervision missions. Inefficiencies were noticed in internal control systems (undocumented equipment transfers and weak procurement capacity).

15

Poor staff morale was evident during the ICR mission. 9 The ICR mission observed unsecured project documents in unlocked offices in the office building which is shared with non project staff. There are also allegations of improper conduct by the Project Coordinator (Anonymous email communications were sent to the World Bank and were shared with INT- the Integrity Unit).

47. Despite the deteriorating leadership at the PIU, implementation of key project activities continued and most of the targets were achieved, even exceeded in certain cases. Fortunately, the policy component (component 1) which was directly implemented by the Central Bank was smoothly implemented and contributed to the impressive results achieved under that component. Also, the MFI Networks whose technical capacity had improved over the years, and their financial resources (owners’ equity) had significantly grown (savings and retained earnings) used their own funds and human capital to implement project activities under the “improved access component” (component 2) and produced outstanding results. As explained in other sections, the reason for the final closing date extension (June 30, 2010 to December 30, 2010) was to facilitate reimbursements of outstanding contracts to consultants as well as MFI Networks who had used their own funds during the crisis to implement activities (earmarked for funding by IDA’s additional financing). Most of the credit for the project results achieved since 2007 when the project was restructured for additional financing goes to the Central Bank and the MFI Networks who were resilient and consistent with implementation amidst the deteriorating leadership at AGEPMF.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization

48. The M&E design of the project was generally adequate and had sufficient indicators to monitor progress towards achieving outcome and impact of the PDO. Quantitative and qualitative indicators were defined to be tracked by the different key stakeholders (MFI networks, Central bank and APIMF for training). For example, the resident technical assistance (TA) providers were given contracts based on the performance of the MFI networks. The indicators for these performance-based contracts went beyond those indicated in the PAD to include for example measuring knowledge transmitted from the TA providers to local personnel. This encouraged speedy transfer of knowledge to Malagasy staff who today is instrumental in managing these viable MFI networks. The nature of the project which had significant level of effort on institutional and capacity building, legal and regulatory made it necessary to have many qualitative indicators and few quantitative ones to monitor outreach and portfolio quality (one component out of four of the project).

49. The design, however, failed to define specific units of measure meant for the “increased productivity and improved standards of living of the beneficiary households”, which would have helped objective tracking of social impact in these two areas. The impact study10 for the project could have benefited from such a framework to better inform and influence improvements of the project design during the second restructuring in 2007. The

9 Staff claimed of delayed approvals for resources required to effectively implement project activities (e.g. computers, vehicles and office space etc.). 10 AGEPMF Impact Study – FACET BV, Supporting Small Enterprises: Rapport de l’étude d’Impact de la micro finance a Madagascar

16