Document of The World Bank FSTA... · Key performance indicators 2 ... THE KINGDOM OF NEPAL...

62

Document of The World Bank Report No: 23992 NEP PROJECT APPRAISAL DOCUMENT ONA PROPOSED CREDIT IN THE AMOUNT OF SDR12.4 MILLION (US$16.0 MILLION EQUIVALENT) TO THE KINGDOM OF NEPAL FOR A FINANCIAL SECTOR TECHNICAL ASSISTANCE PROJECT November 13, 2002 Finance and Private Sector Development South Asia Regional Office

Transcript of Document of The World Bank FSTA... · Key performance indicators 2 ... THE KINGDOM OF NEPAL...

Document of

The World Bank

Report No: 23992 NEP

PROJECT APPRAISAL DOCUMENT

ONA

PROPOSED CREDIT

IN THE AMOUNT OF SDR12.4 MILLION (US$16.0 MILLION EQUIVALENT)

TO

THE KINGDOM OF NEPAL

FOR A

FINANCIAL SECTOR TECHNICAL ASSISTANCE PROJECT

November 13, 2002

Finance and Private Sector DevelopmentSouth Asia Regional Office

CURRENCY EQUIVALENTS

(Exchange Rate Effective May 31, 2002)

Currency Unit = Nepalese rupeeI rupee = US$0.01284

US$1.00 = rupee 77.881

FISCAL YEARJuly 15 - July 14

ABBREVIATIONS AND ACRONYMS

Vice President: Mieko NishirnizuCountry Manager/Director: Kenichi Ohashi

Sector Manager/Director: Joseph Del Mar PerniaTask Team Leader/Task Manager: Simon C. Bell

NEPALFINANCIAL SECTOR TECHNICAL ASSISTANCE PROJECT

CONTENTS

A. Project Development Objective Page

1. Project development objective 22. Key performance indicators 2

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project 32. Main sector issues and Government strategy 43. Sector issues to be addressed by the project and strategic choices 8

C. Project Description Summary

1. Project components 102. Key policy and institutional reforms supported by the project 103. Benefits and target population 114. Institutional and implementation arrangements 11

D. Project Rationale

1. Project alternatives considered and reasons for rejection 112. Major related projects financed by the Bank and other development agencies 123. Lessons learned and reflected in the project design 144. Indications of borrower commitment and ownership 155. Value added of Bank support in this project 16

E. Summary Project Analysis

1. Economic 162. Financial 163. Technical 174. Institutional 175. Environmental 186. Social 187. Safeguard Policies 19

F. Sustainability and Risks

1. Sustainability 202. Critical risks 203. Possible controversial aspects 21

G. Main Conditions

1. Effectiveness Condition 212. Other 22

H. Readiness for lmplementation 22

I. Compliance with Bank Policies 22

Annexes

Annex 1: Project Design Summary 23Annex 2: Detailed Project Description 26

Annex 3: Estimated Project Costs 31Annex 4: Cost-Benefit Analysis Summary, or Cost-Effectiveness Analysis Summary 33Annex 5: Financial Summary for Revenue-Earning Project Entities, or Financial Summary 34Annex 6: Procurement and Disbursement Arrangements 35Annex 7: Project Processing Schedule 43Annex 8: Documents in the Project File 44

Annex 9: Statement of Loans and Credits 45Annex 10: Country at a Glance 46Annex 11: Financial Sector Strategy Statement 48

MAP(S)

NEPAL

Financial Sector Technical Assistance Project

Project Appraisal DocumentSouth Asia Regional Office

SASFP

Date: November 13, 2002 Team Leader: Simon C. BellSector Manager/Director: Joseph Del Mar Pernia Sector(s): Banking (100%)Country Manager/Director: Kenichi Ohashi Theme(s): State enterprise/bank restructuring andProject ID: P071291 privatization (P), Corporate governance (S), RegulationLending Instrument: Technical Assistance Loan (TAL) and competition policy (S), Standards and financial

reporting (S)

Project Financing Data[ Loan [X] Credit [ ] Grant [ ] Guarantee [ ] Other:

For Loans/Credits/Others:Amount (US$m): 16.0

Proposed Terms (IDA): Standard CreditGrace period (years): 10 Years to maturity: 40Commitment fee: 0.5 Service charge: 0.75%Financing Plan (US$m): Source Local Foreign TotalBORROWER 4.10 0.00 4.10IDA 0.00 16.00 16.00UK: BRITISH DEPARTMENT FOR INTERNATIONAL 0.00 10.00 10.00DEVELOPMENT (DFID)Total: 4.10 26.00 30.10

Borrower: THE KINGDOM OF NEPALResponsible agency: NEPAL RASTRA BANKAddress: Nepal Rastra Bank, Baluwatar, Kathmandu, NEPALContact Person: Governor, Nepal Ratsra BankTel: 977-1-410386 Fax: 977-1-410159 Email: bkprornotahtp.com.np - another email -

nrbgov(rnos.co.np

Other Agency(ies):Ministry of FinanceAddress: Ministry of Finance, Bag Dubar, Kathmandu, NEPALContact Person: Secretary, Ministry of FinanceTel: 977-1-259880 Fax: 977-1-259891 Email: [email protected]

Estimated Disbursements ( Bank FY/US$m):FY 2003 2004 2005 2006 2007

Annual 2.50 4.60 4.00 3.37 1.53Cumulative 2.50 7.10 11.10 14.47 16.00

Project implementation period: March 2003 to June 2007Expected effectiveness date: 03/31/2003 Expected closing date: 06/30/2007

OCS PAC Fe,, fl. .d R_fl 20

A. Project Development Objective

t. Project development objective: (see Annex 1)

The overarching objective of the Reform Program in the Financial Sector is to support the renewedefforts of His Majesty's Government of Nepal (HMGN) to improve the sector in order to bringmacroeconomic stability and promote private-sector-led economic growth. The proposed FinancialSector Technical Assistance Project is the first major step in this process and focuses on three broadobjectives (a) helping to restructure and re-engineer the Central Bank (Nepal Rastra Bank - NRB), so thatit can effectively perform its key central banking functions; (b) commencing commercial banking reformin the two large ailing commercial banks that dominate the sector (Rastriya Banijya Bank (RBB) andNepal Bank Limited (NBL)) -- by introducing stronger bank management that protects the financialintegrity of the two banks and would take on a conservator role to prepare the banks for the next steps ofrestructuring; and (c) supporting a better environment for financial sector reform in areas such asenhanced credit information, better financial news reporting, and better training for staff in financialinstitutions. These actions will help create a more prudently operated and commercially viablecommercial banking system that is overseen by a modem, effective, and technically competent centralbank. If sufficient progress is made during this first phase of reform, then subsequent IDA support wouldfocus on more longer term objectives. These include further deepening and broadening of the sector,supporting worker retrenchment in the banks, bank privatization and/or liquidation, and helping to coverthe financial losses in the large publically owned banks.

It is anticipated that IDA's support for the overall financial sector reform program will be in the form ofseveral, sequential projects. The first of these - the Financial Sector Technical Assistance Project - iscentered around the re-engineering of Nepal Rastra Bank (particularly in its core central bankingfunctions; supervision, monetary policy, banking legislation, accounting and auditing, informationtechnology; human resources, and training); reform of the two large commercial banks - RBB and NBL(through the recruitment of Management Teams to put these two banks in conservatorship on behalf ofthe central bank); and support for capacity building in the financial sector (through support for training,financial journalism, and a credit information bureau). This project will finance a range of activities thatare necessary to prepare for a major reform operation. This initial phase will also serve to demonstrateand confirm broad-based commitment to undertake difficult reforms. This sequential approach tofinancial sector reform has been endorsed by colleagues in the International Monetary Fund (IMF), theDepartment for International Development (DFID) U.K., and the Asian Development Bank (ADB).

The Financial Sector Reform Program is also important in terms of enhancing poverty alleviation. It isexpected to (a) support private-sector-led economic growth and job creation; and (b) reduce the numberof nonperforming loans made through the banking system to the politically powerful elite in Kathmandu.As the large non-recoverable losses in the banking system will have to ultimately be borne by theGovermment -- this represents a transfer of resources from the tax payer in Nepal to the urban rich (whorepresent some of the largest defaulting borrowers in the banking system). A more efficientintermediation of funds should also result in a better allocation of financial resources and hence strongereconomic growth.

2. Key performance indicators: (see Annex i)

SECTORAL INDICATORS:Comprehensive financial sector reform that eliminates the need for additional (real or contingent)budgetary support for the financial system -- once the banks have been restructured and privatized orliquidated.

-2 -

OUTCOME/IMPACT INDICATORS:

1. Lay the basis for a modem legal framework for the financial sector;

2. A strengthening of Nepal Rastra Bank's supervisory function -- in particular, its ability to enforceprudential regulations and relevant banking legislation - based on internationally accepted norms;

3. An increase in the range and sophistication of financial instruments and services available atcompetitive prices;

4. Enhanced accounting and auditing standards within the banking sector; and

5. A more prudently operated financial sector with better trained staff, a better informed general public,and an enhanced system of credit information.

OUTPUT INDICATORS:

1. Producing quarterly off-site and annual on-site bank supervision reports (with accompanyinganalysis), on a timely basis, for each of the banks operating in Nepal;

2. Finalizing a new Central Banking Act (completed), a Banking and Financial Institutions Act (inprocess), and other ancillary financial sector legislation (Companies Act, Bankruptcy Law) withassociated regulations;

3. Producing audited financial data for RBB and NBL, which conforms with international accountingstandards, within four months of the end of the financial year;

4. Preparing a restructuring plan for privatization/liquidation of RBB and NBL;

5. Creating a leaner, more efficient, and professional Central Bank;

6. A strengthened Bankers' Training Center and more reliable and timely data from the CreditInformation Bureau; and

7. The production of increasingly better financial data and an enhanced financial performance withinthe two largest banks managed by the professional management teams.

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project: (see Annex I)Document number: IDA/R98-168 Date of latest CAS discussion: 12/15/98

The overarching theme of the 1998 Country Assistance Strategy (CAS) was to help improve public sectorgovemance. Poor management of financial resources at RBB and NBL has been one of the mostimportant ways by which the powerful elite has been able to abuse the public institutions. Theinefficiency of the financial sector, in part, occasioned by heavy-handed state involvement. This hasresulted in liquidity problems within the banks, growing nonperforming assets, problems of capitaladequacy, and an increased scope for systemic risk within the sector. The Government's commitment tostopping this will be a major departure from the past and serve to send a clear signal that the oldstandards of govemance are no longer acceptable. The CAS also emphasizes faster growth in Nepal insupport of sustained poverty alleviation. It notes that although the macroeconomy has been stable (eventhough budgets have been consistently unrealistic), growth has been slow and the pace of structuralreform "in areas such as privatization and banking hasfaltered, and growth hasfallenfrom 5.5% inFY91-94 and 4.4% in FY95-96 to an estimated 4.0% in FY97 and 1.9% in FY98. "Annex 1 of the CAS -- on sectoral strategies - identifies the need for the World Bank to focus on four

- 3 -

key areas:

1. the restructuring/privatization of the two largest commercial banks, RBB and NBL;2. the development of NRB's regulatory and supervisory capacity;3. the development of a simple uniforn legal framework for Nepal's financial system; and4. the establishment of additional private financial institutions, using the International FinanceCorporation (IFC).

Nepal's macroeconomic situation has deteriorated signiificantly since the last CAS was written -- withgrowing fiscal imbalances, lower levels of investment, and slower growth. Given these problems andincreased macroeconomic uncertainty, avoiding a banking crisis has become even more urgent.

The proposed Financial Sector Program will address these concerns and provide technical assistance toHMGN to implement the reform agenda.

2. Main sector issues and Government strategy:

Financial Sector Background. Nepal has 15 commercial banks -- RBB, NBL, 9 Joint Venture Banks(JVB's), which are mixed public/privately owned, and 4 local banks. In addition, the sector also includes2 large development banks (the Agricultural Development Bank of Nepal (ADB/N) and the NepalIndustrial Development Corporation (NIDC)), 48 finance companies, 13 insurance companies, numerousmicrofinance institutions, 7 Grameen Replicator Banks, 35 financial cooperatives, 25 financialNon-Government Organizations (NGO's), and a stock exchange. The two large banks - RBB and NBL --account for around 50 percent of total banking system assets, and are in a very precarious financialposition. Political intervention, weak management, disruptive unions, poor financial informationsystems, and a deeply entrenched culture of non-repayment of loans has resulted in a rapid deteriorationof their financial health.

RBB, which represents 27 percent of commercial banking system assets, is estimated to have a largenegative net worth and therefore a capital base that is well below the levels required by generallyaccepted international norms. Although in slightly better financial condition, NBL has similar problemsincluding a high negative net worth. This could have serious ramifications for the Government in termsof systemic risk and could prove to be a severe financial strain on an already delicate budget shouldeither of these two banks face a crisis of confidence with concomitant adverse macroeconomicimplications. A 2000 review of RBB and NBL indicated that these banks together had estimated losses,as of mid-1998, as much as $426 million - equivalent to around 46 percent of the Government budget orabout 8.6 percent of GDP. The situation in these two banks has inevitably deteriorated considerablysince this date.

In general, Nepal's financial system suffers from the following problems that are also recognized by theGovernment:

The Government's Role. His Majesty's Government of Nepal (HMGN) plays a large direct role in thefinancial sector. From ownership of key financial institutions such as RBB, ADBN, the Grameen banks,the insurance industry, and, until recently, the Nepal Bank Limited (where it is still the largest singleshareholder); to significant influence over the Joint Venture Banks; the Government's involvement isevident in almost every aspect of financial sector activity. This has resulted in strong politicalinterference in banking activities which, in turn, has resulted in non-repayment of loans, and poorfinancial health throughout the system.

-4 -

Nepal Rastra Bank - the Central Bank. Until January 2002, when a new NRB Act was approved, theNRB fell under the authority of the Ministry of Finance. This historical lack of autonomy has hinderedthe NRB's ability to supervise and regulate the banking system adequately. Political influence in theRBB and NBL - as well as their sheer dominance within the banking system - placed these banksoutside the influence and control of the central banking authorities. Although it may take time to becomefully operational, the new 2002 Act provides the NRB with sufficient autonomy and full authority overthe entire banking system. Recently approved banking regulations will also provide the regulatory basisfor NRB to move the system closer to international banking norms while permitting the bank supervisorsto deal expeditiously with errant banks. For the immediate future, the NRB's challenge will be to enforcethe rules that have now been established.

The Government and the NRB need to reorient their activities away from being active participants (asowners and operators) in the financial sector to increasingly focus on becoming more effective regulatorsand supervisors.

Rastriya Banijya Bank (RBB) is 100 percent Government owned. As the largest commercial bank,with more than 200 branches, RBB has an important role to play in the economy. However, burdened bypolitical demands, an active and disruptive union movement, management weaknesses, poor accountingand auditing functions, and high levels of non-performing assets, RBB has reached a particularly parlousfinancial state. A recent audit points to a high negative net worth, weak internal systems, poor internalfinancial management, and shabby operating methods. At the request of the government, a diagnosticreview of the RBB and NBL was carried out by KPMG/Barents in 1999/2000. This study's majorfindings confirm that (a) the banks' management is basically dysfunctional; (b) there are no reliable dataavailable on the loan portfolio; (c) financial accounting is primitive and not according to internationalstandards (accounts are virtually all manual and annual statements have not been produced for over sixyears); (d) business strategies are not in place; (e) human resource policy is weak and counterproductive;(f) management information systems and record keeping are very basic; and (g) governance andmanagement are highly politically driven and lacking a commercial focus. This work was financiallysupported under a Policy and Human Resources Development Fund (PHRD) grant (TF 025473) for bothRBB and NBL.

The Nepal Bank Limited (NBL). While in somewhat better financial condition, NBL is still a weakinstitution. Its dominant role in the financial sector creates scope for inefficiency and a low level ofbanking competition. Over the 1990s, the Government reduced its stake in NBL by selling parcels ofshares to the private sector. The Government has reduced its shareholding to a minority 41 percent,although it remains the single biggest shareholder in the bank. This disinvestment by HMGN was carriedout with the objective of reducing political interference in NBL's management and promoting privatesector participation in the bank so that it could operate in a more commercial and business-like manner.The Government's policy of successively selling shares to the general public has, however, left the bankwithout a single strategic partner with a strong background in commercial banking and internationallinkages with the global economy. Connected lending activities by the new private owners are thought tohave further compromised its operations. As such, it also has many of the same problems as RBB (seeabove) as identified in the KPMG diagnostic.

The Agricultural Development Bank of Nepal (ADB/N). The financial and operational situation of theADB/N, the third biggest bank in Nepal, is also poor. The ADB/N will require restructuring, systemdevelopment, changes in govemance arrangements, and a review of its ultimate role and ownershiparrangements. This bank is being dealt with by the Asian Development Bank. Close coordinationbetween IDA and the ADB mean that actions taken in RBB and NBL are likely to be applied to ADB/N

-5-

to ensure a consistency of approach.

A Weak and Fragmented Legal Financial Environment. Nepal has a proliferation of both laws andregulations that are institutionally rather than functionally focused. This has created a fragmented legalenvironment.

* The Nepal Rastra Bank Act, now superseded by a January 2002 Act, was seriously outdated anddeficient with respect to issues of central bank autonomy, accountability, and governance. Now thatnew legislation has been approved, the challenge will be to ensure that NRB can effectively enforcethe provisions of the new legal and regulatory environment.

* The 1974 Commercial Bank Act is also defective. Most importantly, the act does not cover alldeposit-taking institutions. Other nonbank deposit-taking institutions are governed by their own laws- the Development Bank Act of 1996, the Agricultural Development Bank Act of 1967, and so on.A proliferation of laws covering various classes of deposit-taking institutions has permitted legalarbitrage. NRB has recently completed drafting a new Banking and Financial Institutions Act thatcovers all major deposit-taking institutions. This Act is expected to become law in 2003.

* Ancillary Laws. Once the above two key pieces of legislation have been amended, it will beimportant to ensure that other ancillary laws are developed in support of a modem banking system.New legislation is required in such areas as collateral, credit activity, bankruptcy law, and so on.

A Weak and Fragmented Accounting and Auditing Environment. A weak accounting and auditingtradition has meant that the timeliness and reliability of financial data (particularly from the largestbanks) is extremely poor. Corporate sector accounting is also weak, making lending decisions difficultfor the banks. If Nepal's financial system is to operate in a prudentially sound and efficient manner,strengthening of accounting and auditing is essential.

Competition in the Banking Sector. Reform of the state-owned banking sector should be designed toreduce fragmentation and support the more efficient intermediation of funds within the banks andnonbanks. This would increase competitive pressures and thereby provide more efficient andcost-effective solutions to the banking public. Market-oriented approaches also need to be developed toenhance competitive pressures. These are preferable to mandated efforts such as those developed tocontrol interest rate spreads and priority and deprived sector lending.

Other Issues. In addition to the above, the financial sector environment needs to be strengthened inseveral fundamental ways. For example, credit information systems have not been effective tools againstnon-performing borrowers; capacity building in the sector remains very weak; and the general public'slow level of financial sophistication means that it does not serve as an effective check and balance withinthe system. These weaknesses also require attention.

These issues call for urgent reform and modernization. Nepal needs to create the preconditions for thedevelopment of an efficient banking system that is capable of developing new financing mechanisms andinstruments to meet private sector needs. Without such reforms, the prospects for faster growth andultimately poverty reduction will be constrained. However, financial sector development is a long andcomplex process that will take many years, particularly given the very low starting point in Nepal. Theproposed program will start this process and deal with only the most serious of these problems --specifically central banking, the two largest banks, and strengthening the financial environment.

- 6 -

Government Strategy. Over the past few years, the Government has undertaken general reformmeasures in the financial sector. These include interest rate deregulation, the phase out of StatutoryLiquidity Requirements (SLR), introduction of modem banking regulations, capital market reforms, andforeign exchange liberalization. However, much remains to be done, particularly with respect toinstitutional reform. To help establish a framework for the way forward, the Government has formulateda Financial Sector Strategy Statement (FSSS) that consolidates its thinking and develops acomprehensive and interlinked reform program. The FSSS has been discussed widely within Nepal -within the private sector and the financial sector - and it has been adopted as Government policy. TheFSSS was publicly released and published in the Nepali and English press at the end of 2000. The desirefor reform in the financial sector is further reflected by the fact that the Government has asked for WorldBank, IMF, and Department for International Development (DFID) assistance to proceed with the reformagenda. Initial support has been provided through a PHRD grant and a Project Preparation Facility(PPF).

The main elements of the HMGN's FSSS sector strategy include:

* Reduce the role of the Government in the financial sector as a direct owner of financial institutionswhile strengthening its role as a supervisor and regulator of banks and financial institutions;

* Require strong corporate governance by ensuring that banks (in particular the two largest commercialbanks) are owned and managed by "fit and proper" private investors;

* Strengthen the role of Nepal Rastra Bank in the overall financial system by drafting a new Act toprovide sufficient autonomy in the conduct of monetary policy, banking system regulation andsupervision, and the licensing of banks and nonbanks;

* Improve existing banking and financial legislation and judicial processes for enforcing financialcontracts;

* Improve auditing and accountancy standards within the banking sector; and

* Promote financial discipline through adequate disclosure and competition.

The reforms in the financial sector, particularly with respect to the state-owned banks, require strongpolitical commitment. As in many countries, bank restructuring issues are likely to be difficult for theGovernment when the time comes for action. For example, although liquidation of RBB is one of theoptions that will be considered, this may not be politically acceptable. Even privatizing the bank to goodforeign-banking interests or splitting its activities into several distinct components may prove difficult toimplement (given its poor financial health, its long public-sector association, and the weak state of theNepali economy). Nonetheless, fundamental reform is required and strong political commitment will benecessary if the reform measures are to be carried through to a point where they make a lasting andirreversible contribution to overall economic development. Government commitment to reform, to date,has been demonstrated by its contracting of KPMG to assess future options for RBB and NBL; theinstallation of a professional management team in NBL in July 2002 and a CEO in RBB in late 2002;development of a modern legal and regulatory environment for banking; and the issuance of anoverarching Government policy on financial sector reform. These activities provide the World Bankwith comfort that the Government is willing to transparently assess the condition of the banks and todevelop credible corrective action plans.

-7 -

3. Sector issues to be addressed by the project and strategic choices:

Sector Issues to be Addressed. To support HMGN's financial reform efforts, the World Bank proposesstarting with a strictly limited, but nonetheless ambitious, menu of actions. These focus on key conceptsof strengthening prudential oversight, enhancing the banking sector's financial integrity, and increasingtransparency and information.

To this end, the Credit will support an initial program of Central Bank strengthening in core areas,focusing initially on human resources, on-site and off-site banking supervision support, legal, research,accounting and auditing, and information technology. The project will also support professionalconservator arrangements (the management teams) in the two large banks (RBB and NBL) ultimatelypreparing them for restructuring and privatization. In addition, the Credit will assist in strengthening theoverall financial sector through technical and financial support for the Bankers' Training Center, CreditInformation Bureau, and financial journalism. See Annex 2 for a detailed description of projectcomponents.

The Goverunent's past performance record demonstrates that carrying out meaningful and far-reachingreform requires significant political capital. Hence, the reform program has specifically been designed tobe narrow and precise. In addition, the absorptive capacity of the Central Bank and the publicly-ownedcommercial banks is such that advances beyond the lirmited (but fundamental) reforms envisaged may notbe possible. Therefore, the program focuses on a limited set of actions within the Central Bankcombined with initial support for restructuring the two largest banks and capacity building for selectedinstitutions. Future support will need to address broader policy issues, including supporting the ultimateprivatization of RBB and the restructuring and reform of NBL.

In terms of sequencing and timing, the technical assistance program is already ongoing with support froma PHRD grant and a PPF used to begin initial consultancies. The PHRD grant supported an initial banksupervisory consultancy and a review of strategic options for RBB and NBL carried out byKPMG/Barents. Subsequent support has been provided by a PPF, which funded a second (longer term)phase of the bank supervision consultancy and the initial costs of the management team contract.

Strategic Choices. Given the politically difficult problems to be addressed and the ongoing politicalinstability within Nepal, it was considered strategic to commence with a focused Technical Assistance(TA) operation to support key, fundamental reform elements in the three identified areas. Support underfuture World Bank operations would provide the resources to deal with the financial problems in the statebanks and possible retrenchment in the two large banks prior to their privatization or liquidation.

COOPERATION/COLLABORATION. Given the strong political commitment required to carry out acomprehensive program of financial sector reform, the World Bank sought to develop this program inclose collaboration with the key donors involved in this sector (the IMF, DFID of UK, and the ADB) andthe Government of Nepal. Close cooperation between the main donors is designed to provide strategicleverage to help ensure that difficult political decisions are made when the occasion arises. Ensuringmutually consistent and reinforcing messages through the envisioned IMF Poverty Reduction and GrowthFacility (PRGF) and the ADB's proposed restructuring of the Agricultural Development Bank of Nepal isalso important.

COFINANCING ARRANGEMENTS WITH DFID. DFID has fully endorsed the HMGN's financialsector reform agenda and will provide financial and technical support for this project. DFID hascommitted a US$ 10.0 million equivalent grant to supplement the IDA Credit. The project will be jointlyfinanced by DFID and IDA. The funds will be disbursed in agreed proportions, 62 percent IDA and 38

- 8 -

percent DFID) on all agreed expenditure items. DFID has agreed that their grant will be administered byIDA and expenditures will be made according to IDA's financial management, disbursement, andprocurement guidelines. A Memorandum of Understanding (MOU) between IDA and DFID has beenprepared which outlines more detailed administrative arrangements between the two donors.

INDEPENDENCE OF NEPAL RASTRA BANK. Although the NRB now has legal independence fromthe Government, it may take time before the Central Bank is willing or able to exercise real autonomy.This independence must also have strong political support, most importantly from the Minister and theMinistry of Finance. Therefore, the preparation team believes that it is strategically important to workwith the Ministry of Finance when seeking increased independence for NRB. The project also seeks toensure the development of a stronger and more professional Central Bank so that it can ultimatelybecome a stronger constituency for financial sector change (becoming a stronger and more credibleadvocate for its own enhanced independent status).

RASTRIYA BANLTYA BANK (RBB) AND NEPAL BANK LIMITED (NBL). In June 2000,KPMG/Barents provided HMGN with a diagnostic assessment of the financial and operational positionof the RBB and NBL as well as a list of options for their future operation. The report recommendedseveral immediate steps be taken to stem further hemorrhaging of the banks' financial resources. Theseincluded (a) issuing a statement of government commitment to depoliticize the banking system; (b)bringing in a management team to take over all aspects of banking operations; and (c) ultimatelyprivatizing the bank to a good name "fit and proper" buyer. The management team would be expected to(a) take complete control of the day-to-day running of the bank; (b) immediately help to stabilize theoperational and financial position of the bank; (c) bring in an accounting team to help strengthen theaccounts of the bank; (d) develop a human resources program for the bank which would determine, interalia, a training program, a retrenchment program, and a more appropriate remuneration package for bankstaff; and (e) prepare the bank for privatization/re-privatization. The government accepted theserecommendations and has taken action accordingly.

BUDGETARY PROVISIONS FOR DEALING WITH RBB AND NBL. The existing stock of loanlosses within these two banks is estimated to be between Rs25 to 29 billion (US$368 to US$426 million).This represents 7.5 to 8.6 percent of Nepal's GDP and between 40 - 46 percent of Nepal's budget.Considering the magnitude of these losses, this is a national issue. Losses associated with theprivatization of the banks will also need to be budgeted by the Government.

PROTECTION FOR DEPOSITORS. As the reform program proceeds, monitoring liquidity managementwithin the banking system will be important to make sure that depositors' funds are protected. The WorldBank has been working with the IMF and the bank supervisors in NRB to monitor this situation.

SOCIAL DIMENSIONS OF BANKING. The Government's strong emphasis on the social dimensions ofbanking will need to be addressed delicately and with some sensitivity. An appropriate balance will needto be struck between ensuring that there is a reasonable country-wide coverage of basic banking servicesand interventions that distort the operation of the banking system. Strategic, ongoing dialogue with theGovernment and with the restructuring/privatization agents will be essential in sensitizing both sides tothe concerns of all parties involved.

GOVERNANCE ISSUES. Additional work on governance issues will be pursued by the managementteams - particularly as they relate to action on non-performing borrowers and the production of auditedfinancial data from RBB and NBL.

-9-

C. Project Description Summary

1. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed costbreakdown):

The project has three main components (Table below). Based on its cofinancing agreement, DFID willprovide US$10.0 million equivalent in the form ofjoint financing for this project. The respective DFIDshares for the three components will be: US$1.56 million for re-engineering of NRB; US$8.10 millionfor restructuring of RBB and NBL; and US$0.34 million for capacity building in the financial sector.The balance of US$4.1 million will be provided by HMGN.

Indicative Bank- % ofComponent Costs % of financing Bank-

(US$M) Total (USSM) financingRe-engineering Nepal Rastra Bank 4.68 15.5 2.64 16.5Restructuring the Two Big Banks (RBB and NBL) 24.43 81.2 12.81 80.1

Capacity Building in the Financial Sector 0.99 3.3 0.55 3.4Total Project Costs 30.10 100.0 16.00 100.0

Total Financing Required 30.10 100.0 16.00 100.0Note: The amounts indicated above are inclusive of the PPF of US$ 1.15 Million. Details are in Annex 3.

2. Key policy and institutional reforms supported by the project:

The Financial Sector Technical Assistance Credit represents the first step in a long process of reformwhich will seek to reorient the role of the Government from active participant in the sector to a strongregulator and supervisor of the financial system. Efforts will be made to achieve this through reforms inthree key areas.

Re-engineering the Nepal Rastra Bank. The Central Bank of Nepal (Nepal Rastra Bank) is aparticularly weak institution. Failure to supervise and regulate banks, produce robust accountinginformation, and conduct appropriate monetary policy - are all exacerbated by a weak legal structure,politicization of the Central Bank, a lack of computerization, and weak human resource managementcapabilities, which has resulted in few appropriate incentives for good work. NRB's problems need to beaddressed on many fronts, although the FSTA project will focus initially on a smaller subset of the mostimportant issues. The ultimate aim is to develop a well-run, fully professional public-sector institutionwith adequate oversight of the financial system and monetary policy.

Restructuring RBB and NBL. This will involve commencing a process, with professional managementteams, which will ultimately permit a fundamental change in the existing ownership and governancearrangements within these two banks. After a period of intense restructuring, the Government's preferredoption is to privatize these two banks to "fit and proper" international bankers. The reality, however,may be that alternative options will have to be pursued. The ultimate objective is to ensure afundamental and sustainable change in these banks so that they no longer act as a drag on financial andreal sector development.

Capacity Building in the Financial Sector. In support of the above reforms, it will also be necessary toimprove human resource capacities in the financial sector and to ensure better checks and balanceswithin the system by developing greater public awareness of financial sector issues. Training for thefinancial sector will be provided through an upgrading of the Bankers' Training Center activities, and its

- 10-

conversion into a more independent Bankers' Institute. Improved public awareness will be achieved bysupporting better financial journalism in Nepal. Lastly, better credit information will be supported undera program of assistance for the Credit Information Bureau.

3. Benefits and target population:

The project will begin to create a financially sound, prudently-managed, and well-supervised financialsector, which will contribute to macroeconomic stability and growth. A secondary benefit of theprogram will be the emergence of a more dynamic, competitive, and customer-focused banking sector.These developments will benefit the banking public in particular and the total population in general bylending support to the establishment of a more dynamic, private-sector led and potentially faster growingeconomy.

4. Institutional and implementation arrangements:

A Coordination and Support Team (CST) has been formed within Nepal Rastra Bank under the BankingOperations Department to administer this project. The Executive Director of the Banking OperationsDepartment heads the CST and provides overall guidance and leadership on matters of projectimplementation. The CST is supported by a dedicated Financial Management Specialist who is aqualified professional accountant and by a dedicated Procurement Specialist. The CST is also supportedby adequate ancillary staff and facilities. The operating costs of the CST will be funded under theproject on a declining cost basis over the project implementation period. These operating costs includecommunications, office supplies and materials, incremental staff costs, and other expenses which will bejointly financed by the IDA Credit and the DFID Grant. Staff salaries are excluded.

Financial Management (also see Section E - Summary Project Analysis and Annex 6) A financialmanagement capacity assessment of the implementing agency, Nepal Rastra Bank, was carried out byWorld Bank financial management specialists during appraisal. The project has adequate financialmanagement arrangements in place to account for and report on project expenditures. To mitigatepotential financial management risks and to strengthen the financial management capabilities of NRB, afinancial management improvement component has been designed and built into the project to ensurethat noted deficiencies are appropriately addressed. Terms of reference for consultancy services to helpimprove the accounting capacity of NRB have been agreed and advertised in the local and internationalpress (including the UN Development Business). The proposed consultancy services are expected to becarried out in three phases. The first phase is a diagnostic and planning phase and will identify the areasthat need improvement resulting in the development of a time-bound action plan to address anyweaknesses. The second phase will implement the agreed actions. The third phase will include intensivetraining for NRB staff and a follow-up evaluation of the impact of the financial managementimprovement program. These steps will build on the good initiatives that are already underway withinNRB to ensure the establishment of a robust financial management system. Annual project financialstatements, SOE's, and special account statements will be audited by the Office of the Auditor Generaland submitted to IDA within six months after the end of the fiscal year. NRB entity financial statementswill be audited by a certified private auditor who will be appointed by the Auditor General and submittedto IDA within six months after the end of the fiscal year.

D. Project Rationale

1. Project alternatives considered and reasons for rejection:

An alternative approach to dealing with Nepal's financial sector problems could be to pursue a broaderfinancial sector reform agenda providing support on a wide range of fronts to a large array of institutions

-1 1-

- particularly some of the other weak (but significantly smaller) privately-owned commercial banks andthe two development finance institutions. However, given the primacy of the problems in the CentralBank and the two largest commercial banks, in combination with the Government's own limitedimplementation capacity, the project team decided to focus on a narrower agenda of issues.Re-engineering the Central Bank and strengthening its core functions while simultaneously dealing withthe problems in the largest state-owned banks -- are initial steps in the overall reform program that arelikely to have the biggest impact. Going beyond this initial agenda is not considered plausible at thisstage given the limited capacity of the Government.

Another option could be to have an even more limited agenda - only focusing on the largest bank (RBB)and the Central Bank - while omitting fundamental policy change in NBL (which is, in theory, a privatebank). However, this option was strongly rejected by our donor partners, the IMF and DFID, as well asby ourselves, as representing an "unduly limited" reform agenda, which may not have the desireddemonstration effects for the next phase of reform. The design team therefore ruled out the omission ofNBL (which represents over 20 percent of banking system assets), from this initial phase of reform.

2. Major related projects financed by the Bank and/or other development agencies (completed,ongoing and planned).

Latest SupervisionSector Issue Project (PSR) Ratings

(Bank-financed projects only)Implementation Development

Bank-financed Progress (IP) Objective (DO)

Financial sector reform -- including Structural Adjustment Credit S SCBPASS under which RBB and NBL (SAL) II (June 1989)were both recapitalizedSecond Structural Adjustment Credit(Cr. No. 2046-NEP) - was approved inJune 1989 and was closed in July1992. The ImplementationCompletion Report (Report No. 12871)was prepared in March 1994.

Financial Sector Adjustment Operation Banking Sector Adjustment(planned for FY05) to cover the cost of Operationretrenchments in RBB and NBL (toprepare them for privatization) andNRB (to assist in the Central Bank'sre-engineering process).

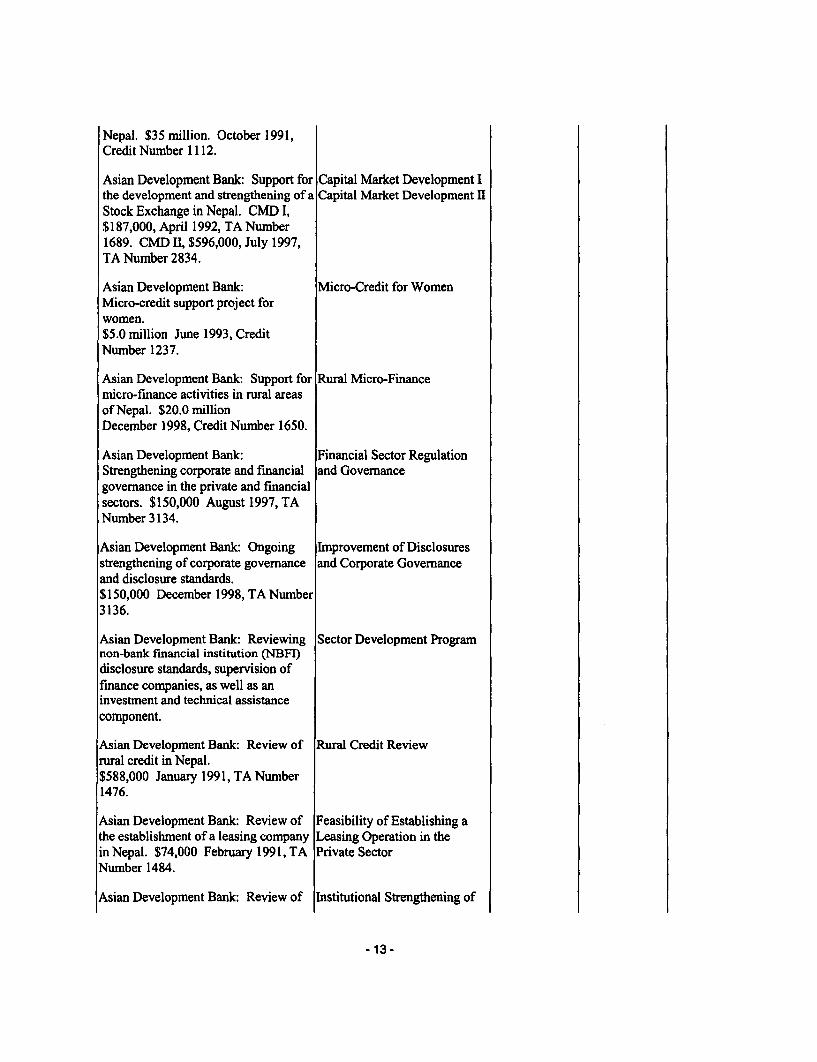

Other development agenciesAsian Development Bank (ADB): Third Small Farmers'Support for small farmers' Developmentdevelopment. $30 million. October1990, Credit Number 1037.

Asian Development Bank: Credit lines Sixth Agricultural Creditin support of rural credit through theAgricultural Development Bank of

- 12 -

Nepal. $35 million. October 1991,Credit Number 1112.

Asian Development Bank: Support for Capital Market Development Ithe development and strengthening of a Capital Market Development HStock Exchange in Nepal. CMD I,$187,000, April 1992, TA Number1689. CMD II, $596,000, July 1997,TA Number 2834.

Asian Development Bank: Micro-Credit for WomenMicro-credit support project forwomen.$5.0 million June 1993, CreditNumber 1237.

Asian Development Bank: Support for Rural Micro-Financemicro-finance activities in rural areasof Nepal. $20.0 millionDecember 1998, Credit Number 1650.

Asian Development Bank: Financial Sector RegulationStrengthening corporate and financial and Governancegovernance in the private and financialsectors. $150,000 August 1997, TANumber 3134.

Asian Development Bank: Ongoing Improvement of Disclosuresstrengthening of corporate governance and Corporate Governanceand disclosure standards.$150,000 December 1998, TA Number3136.

Asian Development Bank: Reviewing Sector Development Programnon-bank financial institution (NBFI)disclosure standards, supervision offinance companies, as well as aninvestment and technical assistancecomponent.

Asian Development Bank: Review of Rural Credit Reviewrural credit in Nepal.$588,000 January 1991, TANumber1476.

Asian Development Bank: Review of Feasibility of Establishing athe establishment of a leasing company Leasing Operation in thein Nepal. $74,000 February 1991, TA Private SectorNumber 1484.

Asian Development Bank: Review of Institutional Strengthening of

- 13 -

ways to strengthen the operations of the ADB/NAgricultural Development Bank ofNepal. $690,000 April 1993, TANumber 1871.

Asian Development Bank: Review of Rural Financerural finance in Nepal. $500,000August 1997, TA Numnber 2836.

International Monetary Fund: General PRGF Program - withProgram Support. Preparatory Mission emphasis on financial sectorin December 2000. reform, fiscal reform, etc.

KFW: Funding of the Nepal Industrial Industrial Finance IIDevelopment Corporation (NIDC). DM2.0 million (1996)

Industrial Finance mDM3.0 million (1974)Industrial Finance IVDM5.0 million (1982)Industrial Finance VDM5.0 million (1989)

DEG, Germany. Equity Participation DMI.0million (1991)

GTZ, Germany. Small Farmers' DevelopmentProgram SFDP (TA). Phase IDM3.7 million (1987-92)SFDP (TA) Phase IIDM2.0 millionSFDP (TA) Phase HIDM2.6 million

IP/DO Ratings: HS (Highly Satisfactory), S (Satisfactory), U (Unsatisfactory), HU (Highly Unsatisfactory)

3. Lessons learned and renected in the project design:

The OED Performance Audit Report for the Second Structural Adjustment Credit (Credit 2046-NEP),May 17, 1995, concluded that: "The basic cause of the weakness of the financial sector design [in thatproject] was:

(i) Lack of commitment by the Government to change its basic attitude towards the state-ownedbanks, including a much stronger emphasis on commercial orientation and on preparation for eventualprivatization;

(ii) Absence of an Action Program did not require the Govemment to introduce drastic changes inthe managerial culture to ensure that managers were professionals with autonomy and accountability; and

(iii) Lack of specific fundamental reforms needed to achieve a major improvement in financial andoperational performance of the banks."

The current operation has dealt with these lessons by not proceeding with IDA financing until there hasbeen upfront commnitment and action by the Government to carry out fundamental reforms in bankingsupervision generally and in the governance arrangements within the state owned bank RBB and in NBL,

- 14 -

in particular - starting with the placement of external management teams in the two banks. Thedevelopment of an overarching framework for financial sector reform - as encapsulated in the FinancialSector Strategy Statement -- will also help ensure consistency and commitment.

In addition, generic lessons learned from previous projects in the financial sector include:

(a) Sustainable banking sector reforms require that the autonomy and technical skills of the regulatorbe enhanced. This project aims to enhance the bank supervisory technical skill of NRB so that it canbecome increasingly more professional and autonomous;

(b) Legal framework reforms are critical to ensure successful implementation. This project hassupported the revision and modernization of key banking legislation. A new NRB Act, providing theCentral Bank with significantly more autonomy, was approved in January 2002. A new Banking andFinancial Institutions Act is currently under discussion within the banking community. Further legalreforms, including measures for debt recovery, and registration and prioritization of liens, are alsoenvisaged in the immediate future;

(c) Sequencing is important for successful financial sector reform. Strengthening the Central Bank,as anticipated under this project, is a high priority and should be carried out with a program of initialcommercial banking reform;

(d) Reforms should include rationalization of processes and procedures and should be backed byvigorous enforcement. The project will deal with procedures in the Central Bank and will provideassistance to ensure strict enforcement of prudential regulations and legal requirements;

(e) Reforms should focus on a limited number of key activities. This project will support apurposely limited agenda of focused activities;

(f) Forcing reforms from outside is not sustainable. Strong borrower commitment will produce thegreatest chance of success. This commitment appears to be in place as evidenced by the development ofthe Financial Sector Strategy Statement, the appointment of a professional management team in NBLand a professional CEO in RBB, and the ongoing close liaison between NRB and the Ministry ofFinance on all aspects of the financial reform process; and

(g) Re-capitalizing commercial banks without fundamental reforms in the ownership and governancestructures of the banks is not likely to be successful. Any injection of capital into RBB and NBL willonly be supported at the point of privatization/liquidation or some other acceptable change ingovernance arrangements within these banks.

4. Indications of borrower commitment and ownership:

HMGN has requested World Bank support for financial sector reform. The Government recognizes theproblems caused by RBB and the fact that its unhealthy financial position poses a serious problem for thesector and, potentially, for macroeconomic stability. There is also recognition that the process ofprivatizing NBL (without a strategic banking partner) has not been particularly successful.

Further demonstrations of the Government's commitment to the reform include: adding RBB to a list ofstate-owned companies to be privatized; contracting TA under a PHRD grant to reconstruct the accountsof RBB (for 1996 to 1998); contracting a consulting company to review options for the future of RBBand NBL; and appointing an external bank supervisor to help strengthen the bank supervisory capacitiesof NRB. It has agreed to the options laid out in the consultant's study, including recruiting twomanagement teams to take over RBB and NBL and completing the FSSS and adopting it as officialGovernment policy. To maintain the momentum of these preparatory activities, the Government

- 15 -

requested a Project Preparation Facility advance. The PPF (No. Q183-0-NEP), in an amount ofUS$550,000, was approved in September 1999, for the financing of required consultancies and trainingactivities. It was supplemented with another PPF of US$600,000 (No. Ql83-l-NEP) in 2002 for partialpayment for the NBL Management Contract and consultancies of RBB. These actions indicate that theGovernment recognizes the problems it faces in the financial sector and that it wishes to pursue atransparent process of clarifying and quantifying the true extent of the problem, reaching agreement onthe most workable options for dealing with these issues, and acting in a decisive manner. TheGovernment of Nepal has also kept a close dialogue with DFID on various development issues includingfinancial sector reform.

The FSSS outlines and clarifies for both the Government and the World Bank the issues within the sectorthat the Government has prioritized. Equally important has been the Central Bank's action to remove theold board of NBL, as the private sector members were particularly disruptive in moving towards theplacement of the professional management team within Nepal Bank Limited.

5. Value added of Bank support in this project:

The Bank has a growing background in the area of financial sector reform operations which will beuseful in the implementation of the proposed Nepal program. The Bank is also a significant source ofdevelopment assistance in Nepal and - in concert with the IMF, DFID, and the ADB - will be able topresent a strong case for making the appropriate decisions and tough choices.

In this regard, project preparation and appraisal has coincided with IMF and DFID missions which hasprovided an opportunity for close collaboration. Financial sector reform (along with fiscal reform) arealso central tenets of the IMF's support program for Nepal.

DFID's contribution of US$ 10 million equivalent for this joint project will reinforce IDA's efforts andwill establish a track record of cooperation between our two agencies in the area of financial sectorreform -- for the next phase of the reform effort.

E. Summary Project Analysis (Detailed assessments are in the project file, see Annex 8)

l. Economic (see Annex 4):C Cost benefit NPV=USS millioi; ERR = % (see Annex 4)

CL Cost effectiveness* Other (specify)As a Technical Assistance project there is no Economic Evaluation Methodology.Nevertheless, as indicated in numerous World Bank and IMF reports, a deepening of RBB and NBL'sfinancial difficulties would have serious systemic consequences with a clear adverse impact on overallmacroeconomic stability.

2. Financial (see Annex 4 and Annex 5):NPV=US$ million; FRR = % (see Annex 4)The financial cost of systemic failure within the banking system -- or even an isolated failure within RBBor NBL -- would create serious financial/fiscal constraints on the Government as the largest owner ofthese banks. There are losses in RBB and NBL of as much as $450 million and these losses need to berecognized and dealt with as part of a privatization and/or liquidation exercise. This will need to bebudgeted by HMGN.

- 16 -

Fiscal Impact:

The proposed project will assist the Government in reducing its involvement in the financial sector andthereby in reducing its exposure to losses within the banking system. While strengthening the CentralBank and restructuring of RBB and NBL will require considerable government financing in the short- tomedium-term, the long-term fiscal impact is likely to be positive if the expected results flow from theproject. The obligation to repay the IDA loan will also be over 40 years during which time thegovernment's control and involvement in the financial sector will be minimized. At the same time, astronger financial sector is expected to support more rapid private-sector-led economic growth.

3. Technical:The proposed project, and in particular the restructuring of RBB and NBL, are complex and require highquality advice and expertise. The proposed IDA Credit will fund expert managers to provide this supportover a three-year period. Within the Central Bank reform component, technical assistance will also beprovided to support high quality central banking technical support.

4. Institutional:This project focuses largely on issues of institutional reform. The most relevant of these pertains toNRB. The re-engineering of NRB is considered crucial to the establishment of better macro-monetaryand financial system management. This institutional strengthening program will, nonetheless, take time.Dealing with the state-owned banking institutions, their restructuring and eventualprivatization/liquidation, and staffing retrenchment issues will also be difficult and delicate tasks.

4.1 Executing agencies:

The program will be overseen by the three key Government economic policy-making bodies - theMinistry of Finance, NRB and the National Planning Commission (NPC). The primary implementationresponsibility, however, will rest with NRB and the Coordination Support Team (CST) within theBanking Operations Department. The establishment of a capable CST and the delegation of full projectadministration responsibilities to this team have been important prerequisites in ensuring smoothimplementation.

4.2 Project management:

The CST has established an efficient management information system and has finalized the Borrower'sProject Implementation Plan (PIP) with clear guidelines, procedures, and terms of reference for key staff.In addition, the CST has been housed in the Banking Operations Department, which has the biggest roleunder the project in overseeing the work of the management teams within the two commercial banks.

4.3 Procurement issues:

Most of the funding under this IDA credit will be used to engage the services of several long-termconsulting companies -- most importantly, the management teams in the two commercial banks.Procurement of goods and selection of consultants under the project has been and will continue to beaccording to the World Bank Guidelines (Standard Bidding Documents: Procurement of Goods - January1995, Revised March 2000 and Standard Request for Proposals: Selection of consultants - July 1997,Revised April 1998 and July 1999). These documents have been made available to the borrower.

Given problems with procurement in the past, the CST has recruited an experienced procurement expertto help streamline procedures.

4.4 Financial management issues:

Financial Management Risks and Risk Mitigation Measures. The financial management risk at theproject level is low with the integration of the CST with the Banking Operations Department of NRB and

- 17 -

the recruitment of a qualified professional accountant as the financial management specialist and aqualified procurement specialist. However, there are some potential risks at the project level which willbe mitigated through the following actions: (a) deploying full staff in the CST, including support staff;(b) delegating authority to the CST by NRB to execute procurement activity and disbursement processesas per IDA's procurement guidelines and disbursement procedures; (c) instituting a mechanism tominimize layers of bureaucracy in procurement decisions inherent in NRB; and (d) assuring that the coreCST staff will be deployed for the duration of the project.

At the entity level, financial management risks are moderate. The NRB has failed to comply with its ownlegal requirement to submit audited Financial Statements within four months of the end of the financialyear. Currently, the average delay in auditing the financial statements is about ten months. Through thecapacity building component this issue will be addressed by assisting NRB to upgrade its capacity tomeet its own fiduciary requirements of completing the annual audited financial statements within fourmonths and improve the quality of financial statements in a timely manner. These changes also meet theWorld Bank's minimum requirements.

The new NRB Act has given a high priority to improved financial management within NRB and requiresit to (a) upgrade accounting to international accounting standards; (b) ensure that at least one of theBoard members has professional expertise in finance or accounting or banking; (c) constitute an AuditComnmtittee headed by one of the Board members; and (d) strengthen the internal audit capacity andcommission an internal auditor either through allotting staff or by recruiting professional audit finrnsfrom the market, and conduct the internal audit as per international audit standards.

5. Environmental: Environmental Category: C (Not Required)5.1 Summarize the steps undertaken for environmental assessment and EMP preparation (includingconsultationi and disclosure) and the significant issues and their treatnent emerging from this analysis.

5.2 What are the main features of the EMP and are they adequate?

5.3 For Category A and B projects, timeline and status of EA:Date of receipt of final draft:

5.4 How have stakeholders been consulted at the stage of (a) environmental screeninig and (b) draft EAreport on the environmental impacts and proposed environmient management plan? Describemechanisms of consultation that were used and which groups were consulted?

5.5 What mechanisms have been established to monitor and evaluate the impact of the project on theenvironment? Do the indicators reflect the objectives and results of the EMP?

6. Social:6.1 Summarize key social issues relevant to the project objectives, and specify the project's socialdevelopment outcomes.

The proposed project will have positive social impacts of protecting the small depositors who are likelyto be hurt if a banking crisis develop. There is a potential social impact from the suggested reforms interms of their impact on banking services in rural areas. There are also possible social imnplications fromlarge scale redundancies following restructuring and privatization of RBB and NBL. Given theperceived delicacy and political sensitivity of the proposed reform and the understanding that this is

- 18 -

likely to be an extended process over a number of years, these issues will need to be properly studied andsensitively administered. An analysis of various stakeholder perceptions of the reform agenda couldprovide a clearer picture of where advances might be possible, as well as where the barriers to progressand the potential points for leveraging support lie. The deployment of human resource professionals willassist in dealing with redundancies within the banks. This will only be carried out on a voluntary basisand not until a later stage in the restructuring process. In addition, work with other financial sectorinstitutions (development banks and microfinance institutions in particular) will be undertaken to ensurethat issues related to the 'social dimensions of banking' are dealt with sensitively and with a view to thesocial, economic, and political dimensions of providing a range of banking services across Nepal.

6.2 Participatory Approach: How are key stakeholders participating in the project?

NRB, the Ministry of Finance, and the National Planning Commission are the key implementinginstitutions. A participatory approach to working closely with the Ministry of Finance, NRB and NPCthrough a Working Group -- was established in mid-1999. This has extended to full consultation with theIMF, the ADB, and DFID, which has taken place at every step of program development and has involved(a) informnation sharing; (b) consultation; (c) collaboration; and (d) joint missions.

Within Nepal, key stakeholder meetings have also been held with the bankers and members of the privatesector to review the draft central banking and banking acts, as well as the associated regulationssupporting these acts.

6.3 Hlow does the project involve consultations or collaboration with NGOs or other civil societyorganizations?

Given the macro-banking focus of this project, it has not involved consultations or collaboration withNGOs. However, key consultations have taken place with the banks through the Bankers' Associationand with the wider donor community. In addition, the need for financial sector reform have beenvigorously debated at the Public Accounts Committee on several occasion, and that forthrightpresentations by MOF/NRB have broadened the understanding of the issues and support for the reformefforts.

6.4 What institutional arrangements have been provided to ensure the project achieves its socialdevelopment outcomes?

The project will employ human resource professionals in all three main institutions covered by thisproject to deal sensitively and compassionately with the issue of re-engineering of human resourceswithin these banks.

6.5 How will the project monitor perfonnance in tenns of social development outcomes?

7. Safeguard Policies:7.1 Do any of the following safeguard policies apply to the project?

Policy ApplicabilityEnvironmental Assessment (OP 4.01, BP 4.01, GP 4.01) ( Yes 0 NoNatural Habitats (OP 4.04, BP 4.04, GP 4.04) 9 Yes 0 No

Forestry (OP 4.36, GP 4.36) (9 Yes * NoPest Management (OP 4.09) _ Yes No

Cultural Property (OPN 11.03) (9 Yes * No

Indigenous Peoples (OD 4.20) (9 Yes 0 NoInvoluntary Resettlement (OPIBP 4.12) (_ Yes * No

-19 -

Safety of Dams (OP 4.37, BP 4.37) (.) Ycs NoProjects in International Waters (OP 7.50, BP 7.50, GP 7.50) (. Yes * NoProjects in Disputed Areas (OP 7.60, BP 7.60, GP 7.60)* K Yes No

7.2 Describe provisions made by the project to ensure compliance with applicable safeguard policies.

Not applicable.

F. Sustainability and Risks

1. Sustainability:

The sustainability of the financial reform program will depend upon the commitment of the Govenmmentto take hard political decisions on govemance issues in the two large banks. Given the politicization ofthese institutions, it may prove difficult to ensure the proper commitment to lasting restructuring (andultimately privatization or liquidation) that is required. Nonetheless, some actions demonstratinggovemment commnitment have already been taken upfront, and the project team feels that the program hasa significantly enhanced chance of success as a result. The Financial Sector Strategy Statement isthorough and sound in its approach to fundamental financial sector reform, and it reflects an appropriateset of policies. An expert management team has also taken over the management of NBL and a ChiefExecutive Officer has been selected to take over RBB -- in all their key functions. Overcoming thepolitical resistance to the introduction of extemal management teams already demonstrates considerableresolve on the part of the government and increases the likelihood of sustainability of the reform process.

Sustainability could be adversely impacted by political uncertainly within Nepal. Weak coalitions andfrequent changes in Governments, which seek to curry political favor with their electorate, may result ina policy reversal. Close cooperation with the IMF, the ADB, DFID and the rest of the donor communitywill also be important to ensure that adequate pressure is brought to bear against any perceived reversalin policy gains.

2. Critical Risks (reflecting the failure of critical assumptions found in the fourth column of Annex I):

Risk Risk Rating Risk Mitigation MeasureFrom Outputs to ObjectiveNRB is dominated by the Ministry of M The government has approved a new centralFinance and is not in a position to banking act which confers full autonomy onconduct its activities in an autonomous NRB. Continued close cooperation andand independent manner. monitoring with the IMF and DFID will also

ensure maximum leverage.

NRB does not take swift and decisive H Management teams/CEOs (conservatoraction (including taking curatorship) arrangements) have been put into place in thewhen a bank is found to be in two worst offending banks prior to projectnoncompliance with Central Bank approval. Close cooperation with the IMF andrequirements, even when the bank is a DFID will also help ensure maximum leverage.publicly-owned institution. Insistence on other upfront actions, wherever

possible, is necessary.

From Components to OutputsLack of adequate cooperation between M Ongoing dialogue and intensive use of the

- 20-

the World Bank and the MOF and NRB. World Bank Kathmandu Field Office.

Inability to access accountancy skills of N Sufficient skills are available in the localsufficient quality or in sufficient market.quantities.

Government's resistance to restructure H Imnpact on World Bank lending and IMFthe state-owned banks and ultimately support for Nepal.give up control over them (as stated inofficial policy).

Institution building is made impossible S With support from this project through whichdue to a lack of commitment to skills' technical and financial assistance will beupgrading by financial sector provided for capacity building, andparticipants. determination of NRB to make changes in the

financial sector, it is expected that this risk willbe mitigated to a large extend.

Late provision of counterpart funds as H NRB and Ministry of Finance are required toagreed in the project plan. indicate the availability of upfront counterpart

funding from the budget.

Overall Risk Rating H High Risk High Reward Project

Risk Rating - H (High Risk), S (Substantial Risk), M (Modest Risk), N(Negligible or Low Risk)

3. Possible Controversial Aspects:

(a) Having foreign managers take over the two largest state dominated banks;(b) Need for significant staff retrenchments in the three banks (RBB, NBL, and NRB);(c) Possible bank branch rationalization as a result of the restructuring in RBB and NBL; and(d) Defaulting borrowers will be taken to court to reclaim on their outstanding borrowings.

G. Main Loan Conditions

l. Effectiveness Condition

There are no conditions of Effectiveness. However, the following were conditions of negotiations.

(a) The Financial Sector Strategy Statement (FSSS) has been discussed and publiclydisseminated;

(b) Contracts have been signed with the management teams coming into NBL and RBB(As mentioned in Annex 2, the management team for RBB pulled out right after theproject was negotiated. NRB and the Bank agreed an alternative arrangement forRBB management - - i.e., to hire a CEO and a team of experts. The selectionprocess is near completion, and a CEO will be appointed shortly.);

(c) The Nepal Rastra Bank Act has been approved and has come into effect;(d) The Banking and Financial Institutions Act has been drafted;(e) Banking Regulations have been issued as directives to the banks;(f) All main technical assistance positions within NRB have been advertized;

- 21 -

(g) The Banking Operations Department has purchased 30 computers;(h) The Borrowers' Project Implementation Plan is in final form;(i) The Coordination Support Team has been created and all staff have been appointed;

and(j) The Ministry of Finance has provided the World Bank with a letter (dated August 8,

2001) either exempting all foreign consultant contracts from taxation or alternativelyundertaking to make the requisite budget allocation in the upcoming budget. Inaddition, the Ministry of Finance also commits in a letter that any other counterpartfunding will be provisioned in the Government budget.

2. Other (classify according to covenant types used in the Legal Agreements.]

H. Readiness for Implementation

Li 1. a) The engineering design documents for the first year's activities are complete and ready for thestart of project implementation.

_ 1. b) Not applicable.

K 2. The procurement documents for the first year's activities are complete and ready for the start ofproject implementation.

L3. The Project Implementation Plan has been appraised and found to be realistic and of satisfactoryquality.

L. J4. The following items are lacking and are discussed under loan conditions (Section G):

1. Compliance with Bank Policies

L I 1. This project complies with all applicable Bank policies.n 2. The following exceptions to Bank policies are recommended for approval. The project complies

with all other applicable Bank policies.

J& ,- Simon C. Bell I Mar Pernia \ ic i OhashiTeam Leader Sector Manager/Director Country Manager/Director

- 22 -

Annex 1: Project Design Summary

NEPAL: Financial Sector Technical Assistance Project

Key Performance Data Collection StrategyHierarchy of Objectives Indicators Critical Assumptions

Sector-related CAS Goal: Sector Indicators: Sector/ country reports: (from Goal to Bank Mission)

Improve the efficiency and Comprehensive financial Periodic review of national Stability in the financial sectorstability of the financial sector sector reform that eliminates accounts, NRB's monetary and will help set the stage forto facilitate private-sector led the need for (real or financial data, and commercial longer term growth and moregrowth and ongoing contingent) budgetary support bank audited financial rapid poverty alleviation inmacroeconomic stability. for the financial system. statements. Nepal.

Reorient the role of the state in Periodic Economic and Sector A lower level of Governmentthe financial sector from that Work, including a Financial involvement within theof an owner of financial Sector Study (completed). financial sector will also freeinstitutions to that of a up budgetary resources forregulator and supervisor of the increased social sectorentire financial system. expenditures.

A deeper and broader financialsector will also ultimately,have a positive impact uponrural banking in Nepal.

Project Development Outcome / Impact Project reports: (from Objective to Goal)Objective: Indicators:NRB operates independently A record of timely, effective, Annual Report of NRB and Sufficient political stability toand effectively regulates the and independent supervision and achieve the overall goals ofbanking sector to ensure that implementation of central implementation reports. the program.commercial banks operate on banking policies.a prudent and commercialbasis.

Timely and effective Periodic supervision and Positive response by theintervention by NRB to evaluation reporting. private sector to bankingenforce prudential regulations sector reforms leading toand relevant banking higher levels of both domesticlegislation. and foreign investment and

consequent higher growth.Increased share of financial Commercial bank financialsystem owned and operated by statements, NRB reports, andprivate-sector players. supervision missions.

Increase in range and Annual reports of commercialsophistication of financial banks and supervisioninstruments and services missions.available at competitiveprices.

- 23 -

Key Performance Data Collection StrategyHierarchy of Objectives Indicators Critical Assumptions

Output from each Output Indicators: Project reports: (from Outputs to Objective)Component:I . Capacity of banking Production of timely quarterly NRB reports, supervision The Ministry of Finance issupervision department within off-site and annual on-site missions, midterm project willing to allow NRB toNRB strengthened to conduct banking supervision reports reviews. enforce the bank supervisoryexaminations of financial for each of the banks operating regulations unfettered byinstitutions competently and in Nepal with accompanying political considerations.undertake appropriate relevant analysis.remedial action. Review of the audited NRB is prepared to take swift

financial statements of all and decisive action (evencommercial banks. taking curatorship) when a

bank is found to be innoncompliance with CentralBank requirements even whenthe bank is a publicly-ownedinstitution.

2. Timely and reliable Production of good quality (to Review of draft legislation andbanking information published intemational standards) regulations.for general use, improved audited financial data for thecentral and commercial banks within four months of Supervision missions andbanking legislation (and the end of the financial year. midterm project reviews.accompanying regulations)drafted and ready for Finalization of a new Centraladoption. Banking Act (done) and a

Banking and FinancialInstitutions Act and associatedregulations.

3. Progress made on Gradually improved financial Review of annual financialrestructuring of RBB and health of RBB and NBL. statements.NBL.

4. Final decisions made on Progress made on:liquidation, privatization,splitting, or other options for (a) The promulgation of aRBB and NBL. new central banking and

commercial banking act.(b) Issuance of newregulations to cover the abovelegislation.(c) Revocation of existingrestrictions on foreignaccountancy companies fromoperating in Nepal.(d) Changed rules onmajority banking ownership inNepal.(e) Cessation of directedlending to priority sectors.

- 24 -

Key Performance Data Collection StrategyHierarchy of Objectives Indicators Critical Assumptions

Project Components / Inputs: (budget for each Project reports: (from Components toSub-components: component) Outputs)

1. Re-engineering NRB. US$4.68 million, of which: Quarterly disbursement Close cooperation between theIDA will finance US$2.64 reports; quarterly progress World Bank, MOF and NRB.million, and reports and supervision Close cooperation between theDFID will finance US$1.56 reports. World Bank, the IMF, DFID,million. and the ADB.

Accountancy skills can bedeveloped or imported to meetthe increased needs.

2. Restructuring the two US$24.43 million of which: HMGN is willing to privatizelargest commercial banks, IDA will finance US$12.81 and/or liquidate theRBB and NBL. million, and DFID will finance state-owned banks and lose

US$8. 10 million. control over them as stated inofficial policy.

Timely provision ofcounterpart funds as agreed inthe project plan.

3. Capacity building in the US$0.99 million, of which: Institution building will befinancial sector IDA will finance US$0.55 possible through a

million, and commitment to skills'DFID will finance US$0.34 upgrading by financial sectormillion. participants.

TOTAL Project Cost US$30.10 millionIDA financing of US$16.00million,DFID financing of US$10.00million.HMGN will flance thebalance of US54.10 million.

- 25-

Annex 2: Detailed Project Description

NEPAL: Financial Sector Technical Assistance Project

The proposed project includes three main components.

By Component: