Do IPO Firms Misclassify Expenses? Implications for IPO ... · Do IPO Firms Misclassify Expenses?...

53

Do IPO Firms Misclassify Expenses? Implications for IPO Price Formation and Post-IPO Stock Performance Xiaotao (Kelvin) Liu D’Amore-McKim School of Business Northeastern University [email protected] Biyu Wu School of Accountancy College of Business University of Nebraska-Lincoln [email protected] July 2018 Acknowledgments: We received very helpful comments from Jaehan Ahn, Scott Bauguess, Yun Fan, Andrew Trotman, Michael Willenborg, and Summer Xia. We also thank participants at the workshop at Division of Economic Risk and Analysis, Securities and Exchange Commission, Peking University, and Renmin University of China.

Transcript of Do IPO Firms Misclassify Expenses? Implications for IPO ... · Do IPO Firms Misclassify Expenses?...

Do IPO Firms Misclassify Expenses?

Implications for IPO Price Formation and Post-IPO Stock Performance

Xiaotao (Kelvin) Liu

D’Amore-McKim School of Business

Northeastern University

Biyu Wu

School of Accountancy

College of Business

University of Nebraska-Lincoln

July 2018

Acknowledgments: We received very helpful comments from Jaehan Ahn, Scott Bauguess, Yun Fan,

Andrew Trotman, Michael Willenborg, and Summer Xia. We also thank participants at the workshop at

Division of Economic Risk and Analysis, Securities and Exchange Commission, Peking University, and

Renmin University of China.

Do IPO Firms Misclassify Expenses?

Implications for IPO Price Formation and Post-IPO Stock Performance

Abstract

This study investigates whether IPO firms inflate “core” earnings through classification shifting (i.e.,

misclassifying core expenses as income-decreasing special items) immediately prior to IPOs. We provide

initial evidence that IPO firms engage in classification shifting in the pre-IPO period. Using hand-collect

price and share information from prospectuses, we find that pre-IPO classification shifting is positively

associated with the price revision from the mid-point of initial price range to the final offer price, suggesting

that pre-IPO classification shifting influences IPO price formation. Furthermore, we find that pre-IPO

classification shifting is followed by negative post-IPO stock returns, indicating that classification shifting

contributes to post-IPO underperformance. In addition, we find that IPO firms classification shift to a

greater degree when accruals management is constrained. Overall, our findings caution investors, auditors,

and regulators that classification shifting, a seemingly innocuous accounting maneuver, can mislead

investors in their IPO valuation and contribute to post-IPO underperformance.

Keywords: initial public offerings; classification shifting; special items; price formation; post-IPO stock

performance

1

Do IPO Firms Classification Shift?

Implications for IPO Price Formation and Post-IPO Stock Performance

1. Introduction

Initial public offering (IPO) firms often highlight in their prospectuses such “core” earnings

measures as earnings before interest, taxes, depreciation, and amortization (EBITDA) and adjusted

EBITDA. These earnings measures exclude transitory items (e.g., special items), and thus are often

considered to constitute “core” earnings. For example, SeaWorld Entertainment, Inc., in its prospectus,

asserts that “investors, lenders, financial analysts and rating agencies have historically used EBITDA

related measures … to estimate the value of a company and to make informed investment decisions.”1

Extant accounting studies have demonstrated that core earnings are more persistent than special items and

have a stronger association with market reactions (Lipe 1986, Francis et al. 1996, Barton et al. 2010). IPO

literature suggests that these “core” earnings measures are often used in valuing IPOs (e.g., Kim and Ritter

1999, Purnanandam and Swaminathan 2004).

To report higher “core” earnings, managers can misclassify persistent core expenses such as cost

of goods sold (COGS) and selling, general, and administrative expenses (SG&A) as part of income-

decreasing special items such as restructuring expenses, and merger and acquisitions (M&A), which are

typically considered to be transitory and non-recurring. This accounting manipulation is referred to as

classification shifting or expense misclassification (McVay 2006). Classification shifting allows firms to

report higher core earnings, where core earnings are defined as sales less core expenses, without altering

the bottom-line earnings (i.e., net income). Classification shifting research has attracted growing interest in

recent years. This research stream has thus far focused primarily on already-public companies and

concluded that they misclassify core expenses to achieve various earnings benchmarks (e.g., Fan and Liu

2017). We investigate in this study whether IPO firms engage in classification shifting prior to the IPO and,

if so, whether classification shifting is associated with IPO price formation and lower post-IPO returns.

1 See https://www.sec.gov/Archives/edgar/data/1564902/000119312513161702/d448022d424b4.htm.

2

These research questions are important for the following reasons. First, IPO price formation is

comprised of the price revision from the mid-point of initial price range to the final offer price and the

initial return from the final offer price to the first-trading-day closing price (i.e., underpricing). Accounting

information plays an important role in the book-building process (Brau and Fawcett 2006, Willenborg et al.

2015). Inflated “core earnings” through classification shifting will likely influence investor valuation, while

this association remains untapped. Second, prior IPO research shows that issuers experience relatively

lower returns in the post-IPO period (e.g., Teoh et al. 1998 a, b). If the implications of pre-IPO classification

shifting are unraveled (i.e., misclassified core expenses recur) in the post-IPO period, then post-IPO

underperformance is likely associated with pre-IPO classification shifting. This is consequential and we

investigate this possibility. Third, prior IPO literature has focused primarily on accruals management (e.g.,

Teoh et al. 1998 a, b, DuCharme et al. 2001, Ball and Shivakumar 2008, Venkataraman et al. 2008,

Armstrong et al. 2016). Little is known about classification shifting of IPO firms. The IPO context is

characterized by both heightened incentives and opportunities for earnings management, which provides a

unique setting to investigate classification shifting. Classification shifting differs from accrual manipulation

as it does not change either current or future net income. Hence, empirical evidence on accruals

management does not readily apply to classification shifting.

IPO firms’ valuation often involves the use of an issuer’s core earnings and comparable firms’

earnings-to-price ratios (e.g., Kim and Ritter 1999, Purnanandam and Swaminathan 2004). The use of “core”

earnings in pricing and valuing IPOs provides IPO firms significant incentives to misclassify core expenses

as special items. Countering this incentive, IPO firms are subject to heightened litigation risk and

monitoring scrutiny from the Securities and Exchange Commission (SEC), auditors, and other stakeholders

(Lowry and Shu 2002, DuCharme et al. 2004, Venkataraman et al. 2008). For example, Section 11 of the

Securities Act of 1933 holds an IPO firm and its managers liable for an untrue statement or an omission of

a material fact in the registration statement, whereas plaintiffs do not need to prove the issuer’s fraudulent

intent. For another example, Venkataraman et al. (2008) find that pre-IPO accruals are less than post-IPO

3

accruals and audit fees for IPO engagements are greater than those for post-IPO engagements. This

evidence is also consistent with higher litigation exposure for IPO firms mitigating their opportunistic

earnings management. Given the increased monitoring scrutiny in the pre-IPO period, issuers may refrain

from pursuing opportunistic classification shifting. In summary, it remains an empirical question whether

IPO firms will engage in classification shifting.

We argue that IPO firms are likely to engage in classification shifting despite heightened scrutiny

around IPOs. This is because external monitors (e.g., auditors) are more concerned with income-increasing

than non-income-increasing earnings management (Nelson et al. 2002, Pittman and Zhao 2017).

Classification shifting does not affect either current or future net income, and thus likely attracts less

monitoring scrutiny and is subject to lower litigation exposure. On balance, we hypothesize that IPO firms

will misclassify core expenses as income-decreasing special items prior to going public, which inflates their

pre-IPO core earnings.

During the book-building period, an issuer and its underwriters conduct road shows to receive

indications of investor interest before finalizing the offer price. If road-show investors are impressed by

“core” earnings, they will signal stronger interest in the issuer’s stock. This leads to a positive price revision

from the initial price range to the final offer price. Thus, we hypothesize that the degree of pre-IPO

classification shifting is positively associated with price revisions. Since the positive IPO price adjustment

is often incomplete (e.g., Hanley 1993), we predict that pre-IPO classification shifting is also positively

associated with initial returns. However, it is conceivable that issuers will negotiate aggressively over the

final offer price such that it compounds fully the implications of classification shifting. This possibility

would lead to a lack of association between pre-IPO classification shifting and initial returns. When

misclassified core expenses reappear following IPOs, it will become at last clear to investors that pre-IPO

core earnings have been overstated and investors will downward adjust the issuer’s valuation. Therefore,

we hypothesize that pre-IPO classification shifting is associated with lower post-IPO stock returns.

4

Using a sample of 805 firm-commitment U.S. IPOs from 2001 to 2016, we find that IPO firms’

pre-IPO unexpected core earnings increase with income-decreasing special items (coded as positive values),

which supports our hypothesis that IPO firms engage in classification shifting prior to their offerings. To

test the effect of classification shifting on price revisions, we hand-collect price and share information from

both the preliminary prospectus that first disclose the IPO offer price range and the final IPO prospectus.

Our findings also show that pre-IPO classification shifting is positively associated with the price revision

from the initial price range to the final offer price, suggesting that classification shifting activities influence

investor valuation. We do not find an association between pre-IPO classification shifting and IPO initial

returns. This result suggests that issuers manage to negotiate a final offer price that fully absorbs the investor

interest arising from inflated core earnings due to classification shifting, leaving little money on the table

on the issuing day. Finally, we find that pre-IPO classification shifting is negatively associated with post-

IPO stock returns. Taken together, our findings indicate that pre-IPO classification shifting inflates core

earnings and the final offering price but decreases stock returns in the subsequent year. Using three different

abnormal accruals proxies, we further find that pre-IPO classification shifting is negatively associated with

levels of abnormal accruals. These findings suggest that IPO firms utilize classification shifting to a greater

degree when accruals management is more constrained.2

Our study makes the following contributions to the accounting literature. First, this study

contributes to the IPO price formation literature by showing that issuers’ pre-IPO classification shifting is

associated with IPO price revisions in the book-building process. Our findings corroborate recent IPO

literature suggesting that “core earnings,” albeit not bottom-line earnings, constitute important signals that

issuers convey regarding their value (Brau and Fawcett 2006, Willenborg et al. 2015). By showing that the

final offer price capitalizes inflation of core earnings, this study enriches the IPO overvaluation literature

2 IPO firms can also use real activities manipulation (i.e., actions managers take that deviate from normal business

practices) to influence market valuation (e.g., Roychowdhury 2006, Cohen and Zarowin 2010, Wongsunwai 2013).

Unlike real activities manipulation, both accruals management and classification shifting rely only upon accounting

manipulation. A comprehensive investigation of trade-offs among classification shifting, accruals manipulation, real

activities manipulation in the IPO context is beyond the scope of this study.

5

(e.g., Teoh et al. 1998 a, b, Purnanandam and Swaminathan 2004). Second, our results add to the post-IPO

underperformance literature by offering an alternative cause (e.g., Teoh et al. 1998a, Ritter 1991). That is,

pre-IPO classification shifting is associated with lower post-IPO stock performance. Third, we provide

initial evidence that IPO firms engage in classification shifting, suggesting that IPO firms are not

necessarily fixated on bottom-line earnings. We also find that IPO firms classification shift to a greater

degree when they are constrained to manage accruals. Overall, our findings caution investors, auditors, and

regulators that the seemingly innocuous classification shifting, which does not alter current or future net

income, can mislead investors and contribute to post-IPO underperformance.

The remainder of this paper is organized as follows. In the next section, we review the relevant

literature and develop our hypotheses. In section 3, we present sample selection procedure and descriptive

statistics, followed by a description of the methodology used to measure classification shifting in section 4.

Section 5 discusses the research design and results. Finally, we conclude with a discussion of our results

and implications in section 6.

2. Literature and Hypotheses Development

Classification Shifting

Investors attach different values to different line items in the income statement. A line item closer

to sales is more persistent (Lipe 1986, Elliott and Hanna 1996, Francis et al. 1996). Using a broad cross-

country sample, Barton et al. (2010, p. 786) find that performance measures toward the middle of the

income statement “generally tend to be more value relevant when they include core operating expenses and

exclude more transitory items like extraordinary items, gains and losses, and other comprehensive income.”

Managers are, therefore, incentivized to misclassify persistent core expenses (i.e., COGS and SG&A) as

transitory income-decreasing special items (e.g., merger and acquisition costs, and restructuring

expenditures), such that companies can report higher “core” earnings. This form of earnings management

(i.e., classification shifting), does not affect current or future bottom-line earnings (i.e., net income).

6

Classification shifting has received increasing attention in recent literature. McVay (2006) first

documents that unexpected core earnings increase with income-decreasing special items, concluding that

firms engage in classification shifting. Using quarterly data, Fan et al. (2010) provide results indicating that

firms employ classification shifting to achieve various earnings benchmarks. Collectively, these studies

suggest that firms engage in classification shifting to influence investor valuation. However, it remains an

empirical question whether IPO firms will engage in opportunistic classification shifting to window dress

“core” earnings.

Classification Shifting by IPO Firms

The IPO setting provides an excellent context to investigate classification shifting as it presents

both heightened incentives and constraints for opportunistic classification shifting. On one hand, prior IPO

studies have documented that accounting information will influence IPO valuations (Brau and Fawcett 2006,

Willenborg et al. 2015). As such, managers of IPO firms have strong financial incentives to manipulate

earnings to increase IPO valuations (Friedlan 1994, DuCharme et al. 2001). On the other hand, IPO firms

encounter heightened litigation risk (e.g., Billing and Lewis 2016). 3 Lawsuits and regulatory actions

following the detection of pre-IPO earnings manipulation impose significant costs on IPO firms and their

executives (Ball and Shivakumar 2008, Venkataraman et al. 2008, Wongsunwai 2013). For example,

DuCharme et al. (2004) find that the incidences of IPO lawsuits and settlement amounts are positively

related to the extent of discretionary accruals around IPOs. In addition, issuers’ registration statements,

which include financial statements, are also subject to scrutiny from auditors, regulators and other

stakeholders (Morsfield and Tan 2006, Ball and Shivakumar 2008).

3 While all public firms are subject to Rule 10b-5 of the Securities Exchange Act of 1934 for material misstatements,

IPO firms face additional litigation risks under Section 11 of the Securities Act of 1933. Compared to Rule 10b-5,

Section 11 does not require plaintiffs (e.g., investors) to prove that defendants (e.g., IPO firms’ managers) acted with

intent or reckless disregard (scienter) and thus relaxes the pleading requirements of plaintiffs.

7

IPO firms often highlight “core” earnings that exclude “unusual” or “non-recurring” items in their

prospectuses. They claim that these “core” earnings are more value relevant.4 Classification shifting allows

an IPO firm to misclassify recurring expenses as “unusual” or “non-recurring” expenses (i.e., income-

decreasing special items), and therefore, to inflate the “core” earnings. In addition, IPO firms often

experience special item events such as acquisitions or divestitures (e.g., Teoh et al. 1998a), providing

abundant opportunities for classification shifting. However, IPO firms are also subject to heightened

litigation risk and scrutiny (e.g., Ball and Shivakumar 2008, Morsfield and Tan 2006, Venkataraman et al.

2008). On one hand, the salient litigation risk and monitoring scrutiny may inhibit issuers from engaging

in classification shifting. On the other hand, auditors and other stakeholders likely focus primarily on

income-increasing as opposed to non-income-increasing attempts (e.g., Becker et al. 1998, Nelson et al.

2002, Pittman and Zhao 2017). Since classification shifting does not alter either current or future net income,

external monitors may acquiesce to classification shifting even if they can detect it.

On balance, we conjecture that IPO firms will classification shift core expenses as income-

decreasing special items to inflate their core earnings.

H1: IPO firms engage in classification shifting prior to the IPO.

Classification Shifting and Price Formation

An IPO firm must provide an initial price range within which it plans to sell its stocks when it files

to go public in its initial prospectus or an amended prospectus. Following this disclosure, the issuer’s senior

management and its underwriters conduct road shows and meet with select investors. Through these

meetings, the underwriters receive indications of interest from these investors and discuss the final offer

price with the issuer. This is commonly referred to as the book-building process, during which regular (or

roadshow) investors obtain access to an issuer’s financial statements and non-financial disclosures. The

4 For example, Axalta Coating Systems Ltd. reports in its prospectus adjusted EBITDA, and suggests that EBITDA

provides a clearer indicator for “core earnings.” For details, please see

https://www.sec.gov/Archives/edgar/data/1616862/000119312514411385/d764723d424b1.htm.

8

final offer price is determined the evening before the first day of trading, and then the shares begin to trade.

The initial return or underpricing (i.e., the difference between the first-day closing price and the offer price)

is on average positive (e.g., Benveniste and Spindt 1989, Hanley 1993).5 Although the positive initial

returns (i.e., “underpricing”) have been the primary focus in extant IPO pricing literature, recent accounting

studies are increasingly interested in the price revision from the midpoint of initial price range to the final

offer price (e.g., Willenborg et al. 2015, Bochkay et al. 2018). As Ritter and Welch (2002, p. 1803) point

out, price revision is key to understand initial returns and that “the solution to the underpricing puzzle has

to lie in focusing on the setting of the offer price.”

During roadshows, issuing companies present and discuss financial (e.g., core earnings) and non-

financial information contained in their prospectus. These disclosures inform investors of an issuer’s

prospect and risks and help to shape investor valuation and IPO pricing. In their survey of chief financial

officers (CFOs) (Brau and Fawcett 2006, p. 399), CFOs consider that the “most important positive signal

is the historical earnings” in the IPO valuation process. If pre-IPO classification shifting inflates core

earnings, it likely influences IPO price formation in the book-building process during which roadshow

investors express their interest in the issuer’s shares. Willenborg et al. (2015) find that financial

performance reported in the prospectus is positively associated with price revisions. Bochkay et al. (2018)

demonstrate that management’s voluntary disclosures of going-concerns are associated with downward

offer price revisions. When an issuer’s core earnings are inflated by classification shifting, investors will

likely consider its performance favorably and express stronger interest in the issuer’s stock. The positive

investor interest will likely lead to a positive price update from the initial range to the final price. Therefore,

we predict that the IPO price revision is positively associated with pre-IPO classification shifting.

H2a: IPO price revisions are positively associated with pre-IPO classification shifting.

5 For example, Kayak Software Corp. determined an initial offer price range of $22-$25. Following its road shows,

Kayak Corp. finalized its offer price at $26 and closed its first trading day at $33.18.

9

The effect of pre-IPO classification shifting on initial returns (“underpricing”) is likely contingent

on the completeness of the final offer price incorporating implications of pre-IPO classification shifting.

According to the book-building theory (Benveniste and Spindt 1989), the final offer price partially adjusts

to positive information during roadshows, but fully adjusts to negative information. This “partial”

adjustment of offer price allows issuing companies to compensate investors for truthfully revealing their

interest in the issuer’s stock. Hanley (1993) provides initial evidence that first-day returns are significantly

and positively associated with price revisions, which lends support to the “partial adjustment” theory. As

discussed above, pre-IPO classification shifting inflates core earnings, leading to positive price revisions.

Consistent with the “partial” adjustment literature, it is likely that the positive investor interest induced by

pre-IPO classification shifting is only partially incorporated in the final offer price. Consequently, initial

returns are likely to be positively associated with pre-IPO classification shifting.

On the other hand, an issuer experiences urgency of cashing out the benefits of pre-IPO

classification shifting. When an IPO firm inflates core earnings via classification shifting, road-show

investors are unlikely to be aware of this window-dressing maneuver. Nevertheless, investors will

ultimately unravel the implications of pre-IPO classification shifting in the following year, if not sooner,

when misclassified core expenses reappear. Understanding that they have one year or less to realize the pre-

IPO window-dressing benefits, issuers likely request the final offer price to completely capitalize the

inflated core earnings. Otherwise, they run the risk of forfeiting the financial benefits of classification

shifting. Hence, the issuer will negotiate aggressively with the underwriter for an increase of the final offer

price from the initial price range to the extent that it fully absorbs investor interest in the issuer’s stock

arising from pre-IPO classification shifting. If this is the case, then price revisions are complete and issuers

leave little money on the table on the issuing day. As a result, initial returns will not be associated with pre-

IPO classification shifting.

In summary, the relation between pre-IPO classification shifting and initial returns is an empirical

question. We provide a hypothesis in its alternative form as follows.

10

H2b: IPO initial returns are positively associated with pre-IPO classification shifting.

Classification Shifting and Post-IPO Stock Performance

Core expenses that were misclassified as income-decreasing special items in the pre-IPO period

will most likely reappear in the fiscal period following the IPO (McVay 2006). As discussed before,

investors will eventually realize that offering firms that are involved in pre-IPO classification shifting have

been previously overvalued, and thus downward adjust their valuations. This realization will likely occur

around the disclosure of the first annual income statement in the post-IPO period, if not sooner. Therefore,

we hypothesize that IPO firms, which misclassify core expenses as income-decreasing special items before

the IPOs, will likely experience lower stock returns in the following year when core expenses reappear.

H3: Post-IPO stock returns are negatively associated with pre-IPO classification shifting.

3. Sample and Descriptive Statistics

Sample

We obtain two samples: the full sample and the IPO sample. We use the full sample to estimate

expectation models for both levels and changes in core earnings, and we use the IPO sample to test our

hypotheses. For the full sample, we obtain all firm-years from Compustat from 1999 to 2015. 6 7 Consistent

with the classification shifting literature (e.g., McVay 2006, Barua et al. 2010), we use sales as scalar and

drop firm-years that have annual sales missing or less than $1 million,8 or have negative net operating assets.

To ensure that our data are comparable across years, we exclude firm-years that change fiscal-year-end

from t-1 to t or from t to t+1. We further eliminate firm-years that do not have sufficient data to estimate

the core earnings (both levels and changes) expectation models. We define industries based on Fama and

6 The sample period of the full sample is consistent with that of the IPO sample, which we discuss later. We require

one year of lagged data and one year of future data in our hypotheses tests. Therefore, to construct variables for

hypotheses testing during 1999-2015, we start with all firm-years from Compustat during 1998–2016. 7 Consistent with the classification shifting literature (e.g., McVay 2006, Fan et al. 2010), we replace missing values

of special items (SPI) and extraordinary items and discontinued operations (XIDOC) with zeroes. 8 To test the sensitivity of our results to this sampling requirement, we construct alternative testing samples with at

least $0.5 million annual sales. Results are inferentially the same.

11

French’s (1997) 48 industries and require a minimum of 15 observations per industry year to estimate

expected core earnings. Our final full sample consists of 84,630 firm-years.

From Thomson Financials’ Securities Data Company (SDC) database, we obtain the IPO sample

by identifying firm-commitment domestic IPOs by nonfinancial registrants from January 1, 2001 to

December 31, 2016. Following prior IPO studies (e.g., Lowry and Shu 2002), we drop unit offerings (i.e.,

bundles of stocks and warrants) and American Depository Receipts (ADRs). We also exclude issuers whose

most current pre-IPO fiscal year financial data is not available on Compustat. Similar to the sampling

procedure of the full sample, we eliminate IPO firms that do not have the necessary data for classification

shifting analyses.9 Our final IPO sample for IPO firms’ classification shifting tests (H1) consist of 805 IPOs

with the most-recent pre-IPO fiscal years from 1999 to 2015. For our tests of IPO price formation (H2) and

post-IPO stock returns (H3), we also drop IPOs with the midpoint of initial price range less than five dollars

(e.g., Ljungqvist and Wilhelm 2003, Lowry and Schwert 2004), or missing required data. Our final IPO

sample for the analyses of price revision (H2) and post-IPO returns (H3) include 789 IPOs.

Descriptive Statistics

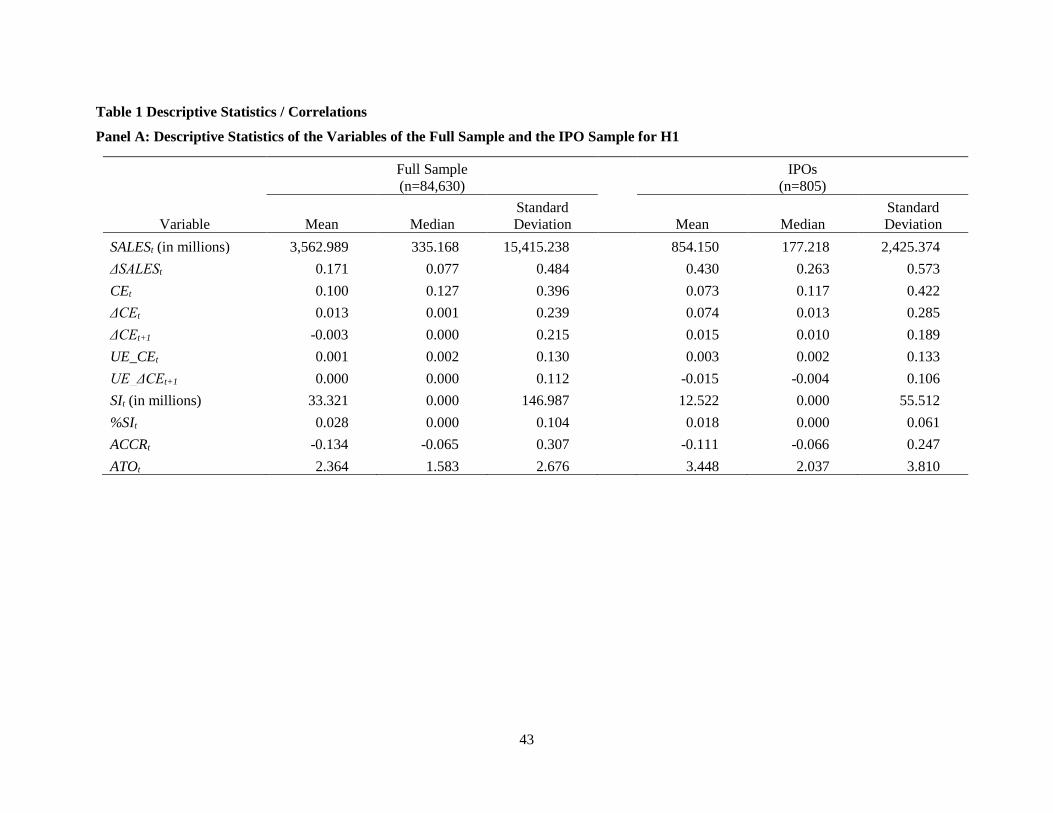

Panel A of Table 1 provides descriptive statistics for both the full sample and the IPO sample. For

the full sample, the mean (median) CEt (core earnings scaled by sales) is 0.100 (0.127). The mean (median)

ΔCEt (change in core earnings from fiscal year t-1 to t) is 0.013 (0.001). Following McVay (2006), we

replace income-increasing special items with zeroes and code income-decreasing special items as positive.10

Mean (median) %SIt (income-decreasing special items scaled by sales) is 0.028 (0.000). The mean (median)

UE_CEt (unexpected core earnings in year t) is 0.001 (0.002). The mean (median) UE_ΔCEt+1 (unexpected

9 The IPO sample comprises 39 of the 48 Fama-French industries with necessary data, and 21 of these industries

each constitutes more than one percent of the IPO sample, indicating a wide selection of industries (untabulated).

There is a concentration of IPOs (22.48%) in the business service industry, which is similar to that reported by

recent IPO studies (e.g., Venkataraman et al. 2008, Cecchini, et al. 2012). 10 We focus on income-decreasing (versus income-increasing) special items, which allows firms to absorb core

expenses to report higher core earnings. Nevertheless, our inferences and conclusions are unaffected when we do not

code income-increasing special items as zeros.

12

change in core earnings from year t to t+1) approximates zero. We discuss the computations of the

unexpected level of and change in core earnings in the following section.

[Insert Table 1 here.]

We test our hypotheses using the IPO sample and define year t as the fiscal year immediately prior

to the IPO. IPO prospectuses include financial statements for year t, which are provided to investors prior

to issuers’ road shows in the book-building process. Year t+1 is the year in which the IPO firm goes public

(i.e., the IPO year). The last three columns of Table 1, Panel A, provide the descriptive statistics of the IPO

sample. Whereas the mean (median) CEt is 0.073 (0.117), which is lower than 0.100 (0.127) of the full

sample, the mean (median) ΔCEt is 0.074 (0.013), which is much higher than 0.013 (0.001) of the full

sample. These comparisons are consistent with prior IPO literature suggesting that IPO firms, compared to

already-public firms, are less profitable and have high growth (e.g., Fama and French 2004). As a ratio of

sales, the average income-decreasing special items is 0.018 for IPO firms, which is lower than that of the

full sample (0.028). The relatively lower amount of income-decreasing special items will likely work

against us finding IPO firms using special items to misclassify core expenses.

Panels B and C of Table 1 present Pearson correlations of the main variables for the full sample

and the IPO sample used for testing H1, respectively. For both the full sample and the IPO sample, %SIt is

positively correlated with UE_CEt (0.032 and 0.141, respectively) and negatively correlated with

UE_ΔCEt+1 (-0.009 and -0.103, respectively). These preliminary statistics are largely consistent with the

classification shifting hypothesis for both the full sample and IPO sample. That is, IPO and non-IPO

companies misclassify core expenses as income-decreasing special items, leading to a positive correlation

between unexpected core earnings and income-decreasing special items; whereas core expenses recur in

the following year, resulting in a negative correlation between unexpected change in core earnings and

income-decreasing special items. Furthermore, the correlation between %SIt and UE_CEt or UE_ΔCEt+1

are notably larger in magnitude for the IPO sample than those for the full sample. These correlations suggest

that IPO firms’ expense misclassification is likely to be greater than those of non-IPO firms.

13

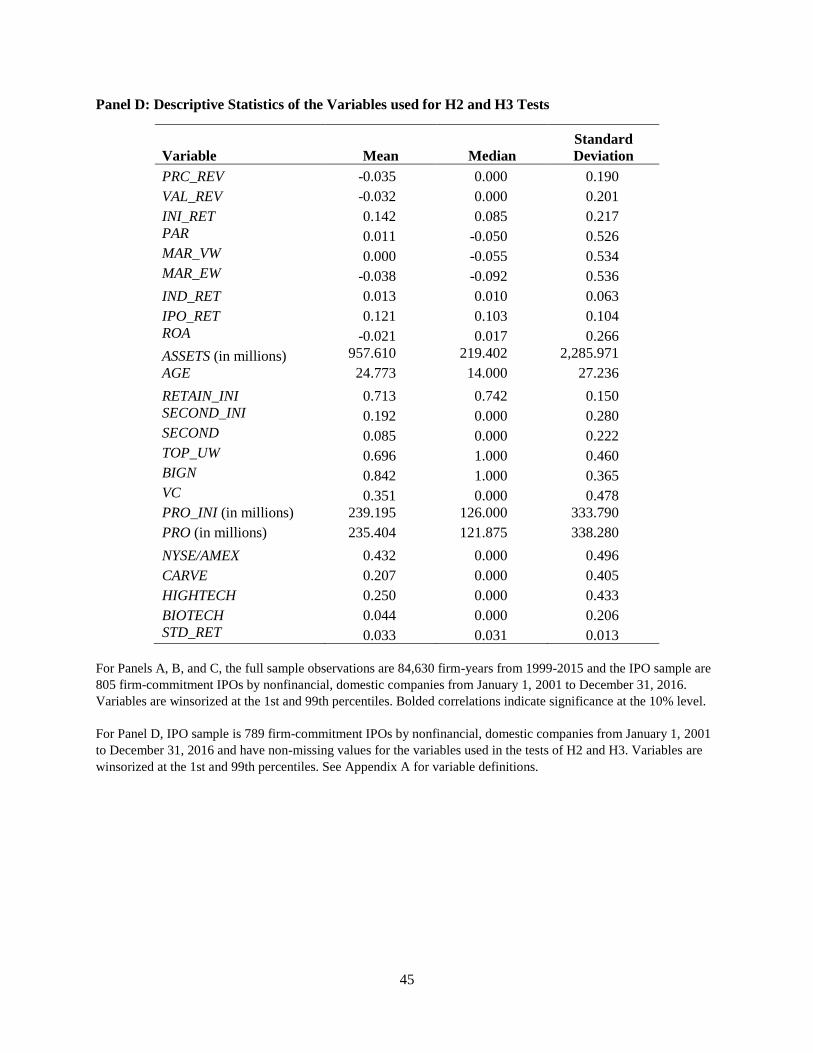

Panel D of Table 1 provides descriptive statistics for the IPO sample for testing both H2 and H3.

Given the data requirement for classification shifting analyses, our IPO sample will likely differ from those

used in previous IPO studies. We discuss descriptive statistics of the IPO sample in this study in comparison

to those from several prior IPO studies. We focus to a greater extent on a comparison with Willenborg et

al.’s (2015) sample because they focus on price formation and their sample period ranges from 2001 to

2013, which overlaps to a large degree with our sample period from 2001 to 2016.

Panel D shows that the mean (median) PRC_REV (percentage change from the midpoint of initial

price range to the offer price) is -3.5% (0.0%). The average PRC_REV is less negative than the -4.5% of

Willenborg et al.’s (2015) sample, and more negative than the -1.4% of Lowry and Schwert’s (2004) pre-

bubble period sample. The mean (median) INI_RET (percentage change from offer price to the first-day

closing price) is 14.2% (8.5%). This average value is similar in magnitude to Lowry and Schwert’s (2004)

12.3% and Willenborg et al.’s (2015) 14.7%. The average one-year post-IPO buy-hold-returns adjusted by

Fama-French 25 portfolio returns (PAR), CRSP value-weighted market portfolio returns (MAR_VW), and

CRSP equally-weighted market portfolio returns (MAR_EW) are 1.1%, 0.0%, and -3.8%, respectively.11 In

summary, the descriptive statistics of these key dependent variables are comparable to prior IPO studies.

Following prior studies, we include macro-economic, firm-level and deal-specific control variables

for testing IPO price formation (H2). We control for marketwide public information (i.e., IND_RET and

IPO_RET) during the book-building phase (Ljungqvist and Wilhelm 2003). IND_RET is the average return

on all firms in CRSP in the issuer’s Fama-French 48 industry, and IPO_RET is the average initial return for

all IPOs. We also include IND_RET_POS to allow for the differential effect of positive and negative market

news on IPO price formation (e.g., Loughran and Ritter 2002, Lowry and Schwert 2004). The average

IND_RET (1.3%) and IPO_RET (12.1%) are both comparable to Willenborg et al.’s (2015) 1.57% and

12.82%, respectively.

11 The average raw one-year post-IPO buy-and-hold-return of the IPO sample is 7.2% (untabulated), which is close

to that of Jay Ritter’s sample of IPOs during 1980-2015, 7.4% (see Table 20-1 of Initial Public Offerings: Updated

Statistics, available on Jay Ritter’s IPO Data website.)

14

The mean (median) ROA of our IPO sample is -2.1% (1.7%), which is much higher than Willenborg

et al.’s (2015) -22.24% (0.16%) and lower than Fedyk et al.’s (2017) 3.86% (2.04%). The mean (median)

ASSETS of 957.61 (219.40) for our IPO sample is greater than Willenborg et al.’s (2015) 701.77 (100.00).

Our IPO firms are older on average than Willenborg et al.’s (2015) sample firms (the average of AGE:

24.77 versus 19.94). The percentage of IPO firms from high-technology industries (25%) approximates

Willenborg et al.’s (2015) 28%, whereas biotechnology firms account for a smaller percentage of our

sample (4.4% versus 15.25%). Combined, these differences indicate that our sample firms are larger, older,

more profitable, and less likely from biotechnology industries than Willenborg et al.’s (2015) sample

firms.12

In terms of IPO characteristics, management equity retainment (RETAIN_INI) and the number of

shares to be sold by current shareholders (SECOND_INI) have an average of 71.3% and 19.2%, respectively.

They are comparable to Willenborg et al.’s (2015) 72.24% and 16.17%. The percentage of IPO firms backed

by venture capitalists in our IPO sample (35.1%) is close to Lowry and Schwert’s (2004) 35.50% and lower

than Willenborg et al.’s (2015) 53%. IPO issuers with Big N auditors account for an average of 84.2% of

our sample, which is close to the 87% of Willenborg et al.’s (2015) sample. Compared to Willenborg et

al.’s (2015) sample, our IPO firms on average raise more offering proceeds (PRO_INI: 239.20 versus

201.66) and are more likely to be listed on NYSE or AMEX (the average of NYSE/AMEX = 43.2% versus

32%). The carve-out IPOs account for a greater percentage of our sample firms (20.7%) than those of Lowry

and Schwert’s (2004) sample (12.3%). Given these differences in descriptive statistics, caution must be

taken when generalizing our inferences of our results to the entire IPO population.

4. Measuring Classification Shifting

12 As we focus on expense misclassification, we require IPO firms to have revenue (greater than one million dollars)

such that a sample firm can have economically meaningful core expenses for classification shifting purposes. Some

issuers, especially biotechnology companies, may have negligible revenue and core expenses (e.g., COGS and selling

expenses) in the pre-IPO period and, therefore, are excluded from our IPO sample. For example, Aegerion

Pharmaceuticals, Inc., a biotechnology company, went public in 2010 and did not recognize revenue until 2013. It is

not meaningful for this issuer to engage in expense misclassification and thus it is excluded from our IPO sample.

15

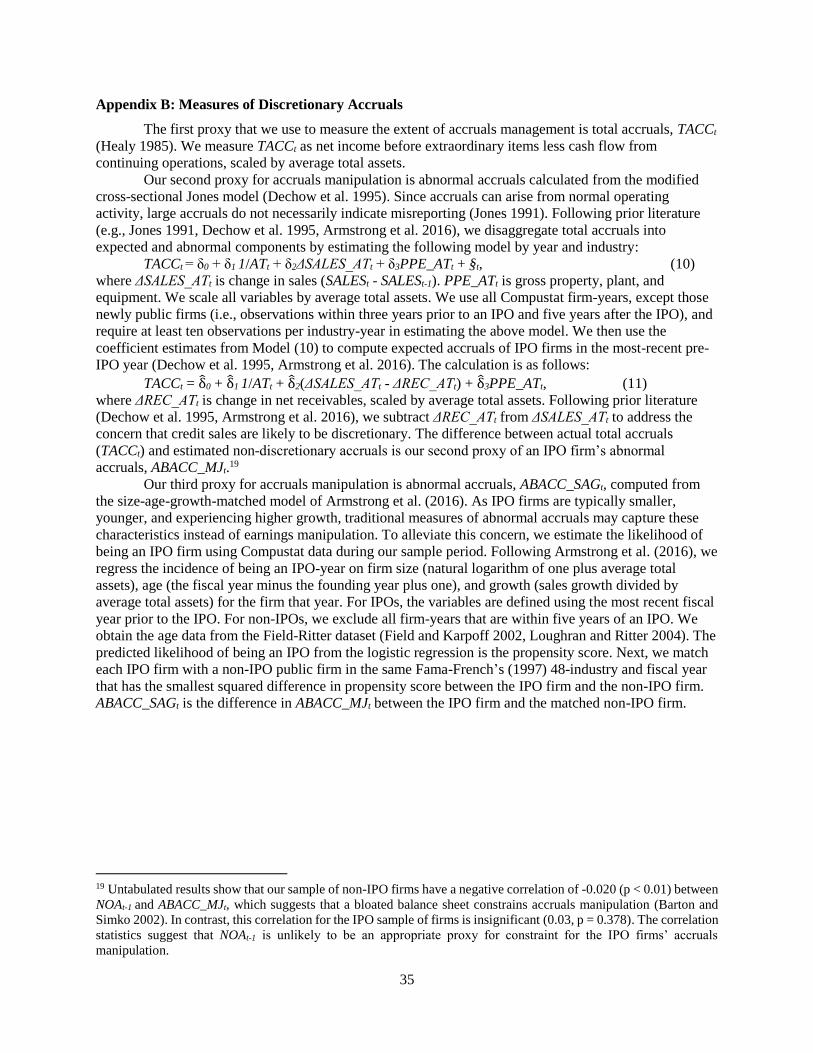

Following the classification shifting literature, we model expected level of and changes in core

earnings using all Compustat firm-years with available data.13 We predict that unexpected core earnings are

positively associated with the amount of income-decreasing special items. However, this positive

association can also result from the enhanced operating efficiency (i.e., “efficiency improvement”

hypothesis). That is, firms can increase efficiency and in turn “core” earnings by removing unproductive

assets or restructuring unprofitable business lines. To distinguish classification shifting hypothesis from

efficiency improvement hypothesis, we follow McVay (2006) and employ “reversal” analyses. Specifically,

we model expected changes in core earnings and examine the association between unexpected change in

core earnings from year t to t+1 and income-decreasing special items in year t. If this association is positive,

indicating that firms are able to sustain higher levels of core earnings following special item events, then

the efficiency improvement hypothesis is likely to hold. Otherwise, if unexpected changes in core earnings

from year t to year t+1 are negatively associated with special items in year t, then it suggests that at least a

portion of previously misclassified core expenses reappears a year later. This scenario would be consistent

with the classification shifting hypothesis.

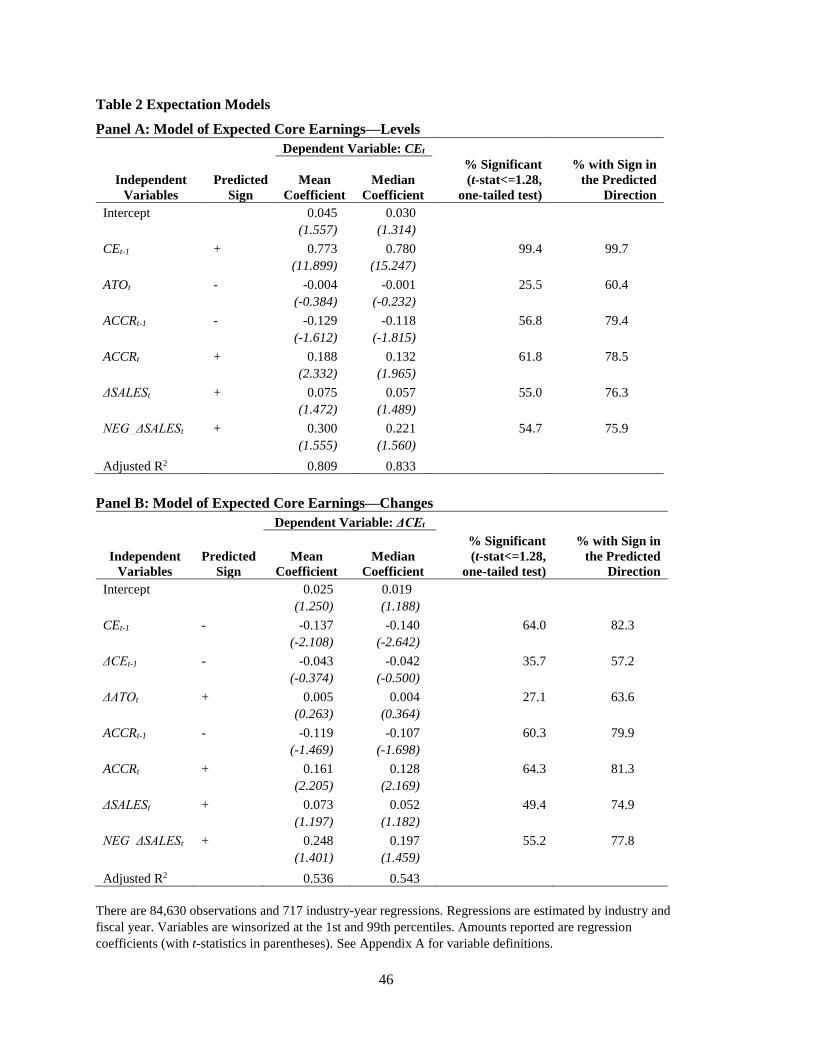

Models of expected core earnings and expected change in core earnings

Following McVay (2006), we use the following expectation models for the level of (Model 1) and

change in (Model 2) core earnings, respectively:

CEt = α0 + α1CEt-1 + α2ATOt + α3ACCR t−1 + α4ACCRt + α5ΔSALEt + α6NEG_ΔSALEt + μt, (1)

ΔCEt = α0’ + α1’CEt-1 + α2’ΔCEt-1 + α3’ΔATOt + α4’ACCRt-1 + α5’ACCRt + α6’ΔSALEt +

α7’NEG_ΔSALEt + μt’, (2)

Appendix A provides variable definitions. We calculate core earnings (CEt) as sales less COGS

and SG&A, scaled by sales. As core earnings tend to be persistent over time, we include lagged core

earnings (CEt-1) in Model (1). We control for average asset turnover as it is inversely correlated with profit

13 We use annual data instead of quarterly observations because some quarterly data (e.g., data items ATQ, RECTQ,

OANCFY, etc.) required to estimate classification shifting are missing in Compustat for significant number of pre-

IPO firm-quarters, thus limiting our ability to examine pre-IPO quarterly classification shifting.

16

margin (Nissim and Penman 2001). Since extreme performance is highly correlated with changes in

accruals (DeAngelo et al. 1994), we control for current accruals (ACCRt) and expect it to increase with core

earnings. Accruals have lower persistence than do the cash flow component of earnings, and current

accruals are negatively related to future earnings (Sloan 1996). Thus, we include accruals in year t-1

(ACCRt−1) in Model (1) and expect it to be negatively related to current core earnings. Core earnings as a

ratio of sales (CEt) is unlikely to be constant since fixed costs do not change when sales change; we hence

include sales growth (∆SALEt). We also include sales decrease (NEG_∆SALESt) because expenses increase

more when activity rises than they decrease when activity falls by an equivalent amount (Anderson et al.

2003). We then calculate unexpected core earnings (UE_CEt) as the residual from Model (1).14

Equation (2) models expected changes in core earnings. We include both core earnings one year

ago (CEt−1) and the change in core earnings from year t-2 to t-1 (∆CEt−1) to control for mean reversion.

Other variables are also similarly defined as in McVay (2006). We obtain the unexpected change in core

earnings (UE_∆CEt) by taking the difference between reported and predicted change in core earnings

estimated from Model (2).

Results of Estimating Expected Levels of and Changes in Core Earnings

We estimate Models (1) and (2) by industry and year to control for macroeconomic and industry

shocks. Panels A and B of Table 2 provide the mean and median estimation results for Models (1) and (2),

respectively. Consistent with prior classification shifting studies (e.g., McVay 2006), the mean and median

adjusted R2s for these models are relatively high. The mean (median) R2 for the levels model (Model 1) is

14 We obtain unexpected core earnings for both IPO firms and already-public firms. This approach is consistent with

accruals estimation in prior IPO literature (e.g., Teoh et al. 1998 a, b, Armstrong et al. 2016) and classification shifting

studies (McVay 2006, Fan et al. 2010). However, IPO firms differ from already-public firms along various economic

dimensions such as size and growth, and therefore, it is important to control for these economic determinants. Our

expectation models explicitly control for size by scaling non-accruals variables by sales and include a control variable

of sales growth (∆SALEt), which helps to more accurately identify unexpected component of core earnings. Moreover,

classification shifting is not measured by unexpected core earnings per se; instead, it is captured by the association

between unexpected core earnings and special items. To the extent that unexpected levels of core earnings are

measured with errors for IPO firms, it likely works against us detecting classification shifting.

17

80.9 (83.3) percent, and that for the changes model (Model 2) is 53.6 (54.3) percent. Furthermore, the mean

and median coefficients of the levels and changes models reported in Table 2 are as predicted.

[Insert Table 2 here.]

5. Research Design and Test Results

The Relation between Unexpected Core Expenses and Income-Decreasing Special Items

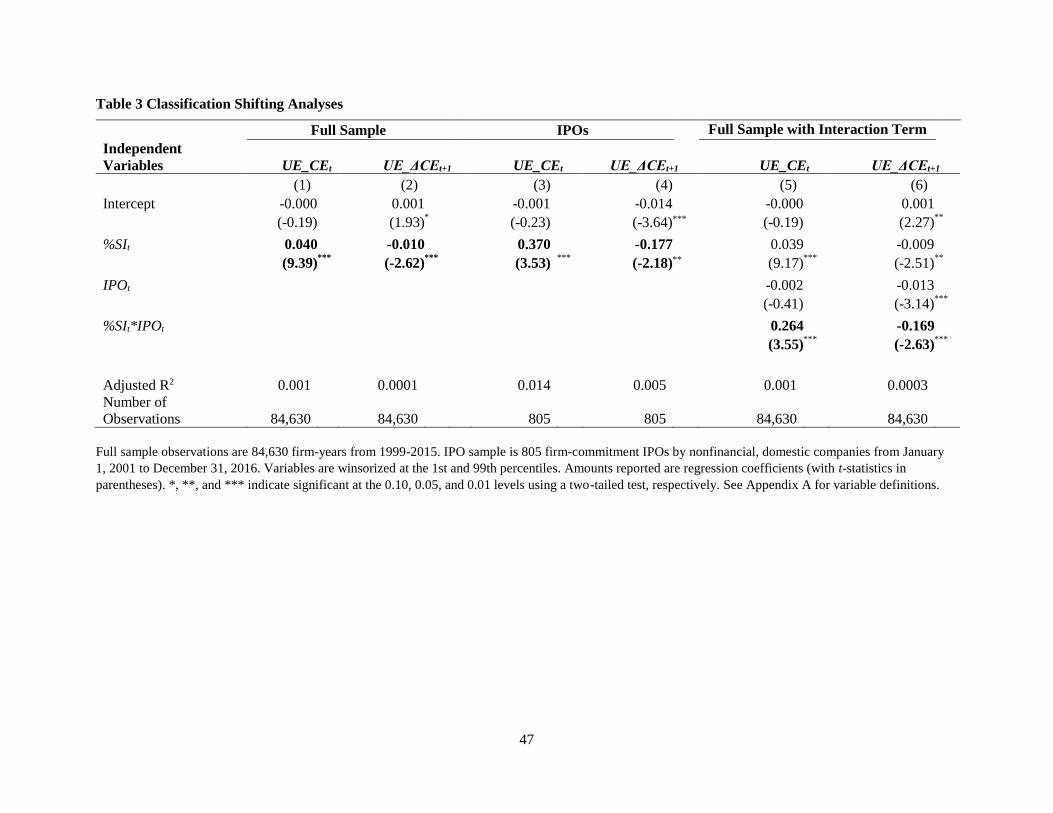

We adopt the following regression model to test the classification shifting hypothesis:

UE_CEt (UE_∆CEt+1) = β0 + β1%SIt + εt, (3)

The dependent variable is either unexpected core earnings (UE_CEt) or unexpected change in core

earnings one year later (UE_ΔCEt+1). %SIt is income-decreasing special items multiplied by −1 and scaled

by sales in year t. According to the classification shifting hypothesis, we expect %SIt to be positively

associated with UE_CEt and negatively associated with UE_∆CEt+1.

Table 3 shows the regression results for Model (3). Columns (1) and (2) present results for the full

sample, whereas columns (3) and (4) provide results for IPO firms. Column (1) of Table 3 indicates

that %SIt is positively associated with UE_CEt (β1 = 0.040; t = 9.39) for the full sample. Economically, a

one standard deviation increase in income-decreasing special items is expected to increase unexpected core

earnings (scaled by sales) by 41.6 basis points, calculated as 0.040 (β1, the coefficient on %SIt from column

(1) of Table 3) multiplied by 0.104 (the standard deviation of %SIt for the full sample from Table 1, Panel

A). Results in column (2) show that %SIt is negatively associated with UE_∆CEt+1 (β1 = -0.010; t = -2.62),

suggesting that understated core expenses in year t reappear in the following year. Overall, these results

support the classification shifting hypothesis that, on average, already-public firms misclassify core expense

as income-decreasing special items but are inconsistent with the efficiency improvement argument.

[Insert Table 3 here.]

H1 predicts that IPO firms engage in classification shifting. To test this hypothesis, we estimate

Model (3) for the IPO sample. Table 3 columns (3) and (4) present the results. Column (3) shows that, for

18

the IPO sample, %SIt is positively associated with UE_CEt (β1 = 0.370; t = 3.53). A one standard deviation

increase in income-decreasing special items for IPOs increases unexpected core earnings (scaled by sales)

by 225.7 basis points (0.370 × 0.061) in the most-recent pre-IPO fiscal year. Column (4) reports that %SIt

is negatively associated with UE_∆CEt+1 (β1 = -0.177; t = -2.18), suggesting that understated core expenses

in the most recent pre-IPO year (year t) reappear in the IPO year (year t+1).15 This result is inconsistent

with the efficiency improvement hypothesis. Combined, these results suggest that issuers misclassify core

expenses as income-decreasing special items immediately prior to the IPO, thus supporting H1.

The coefficient estimates on %SIt for the full sample (columns 1 and 2) are comparable to those

from McVay (2006, Table 6). Notably, the corresponding coefficients for the IPO sample (columns 3 and

4) are much larger in magnitude. Hence, we explore whether IPO firms misclassify core expenses as special

to a greater degree than already-public firms. Specifically, we include IPOt and an interaction term

(%SIt×IPOt) in Model (3), where IPOt equals one for the most recent pre-IPO fiscal year of an IPO firm,

and zero otherwise. Table 3 columns (5) and (6) provide results. The coefficient on %SIt×IPOt for the

unexpected core earnings regression is positive (0.264; t = 3.55) and for the unexpected change in core

earnings regression is negative (-0.169; t = -2.63). These results suggest that IPO firms, compared to

average already-public firms, misclassify an even greater proportion of core expenses as special items to

inflate core earnings.

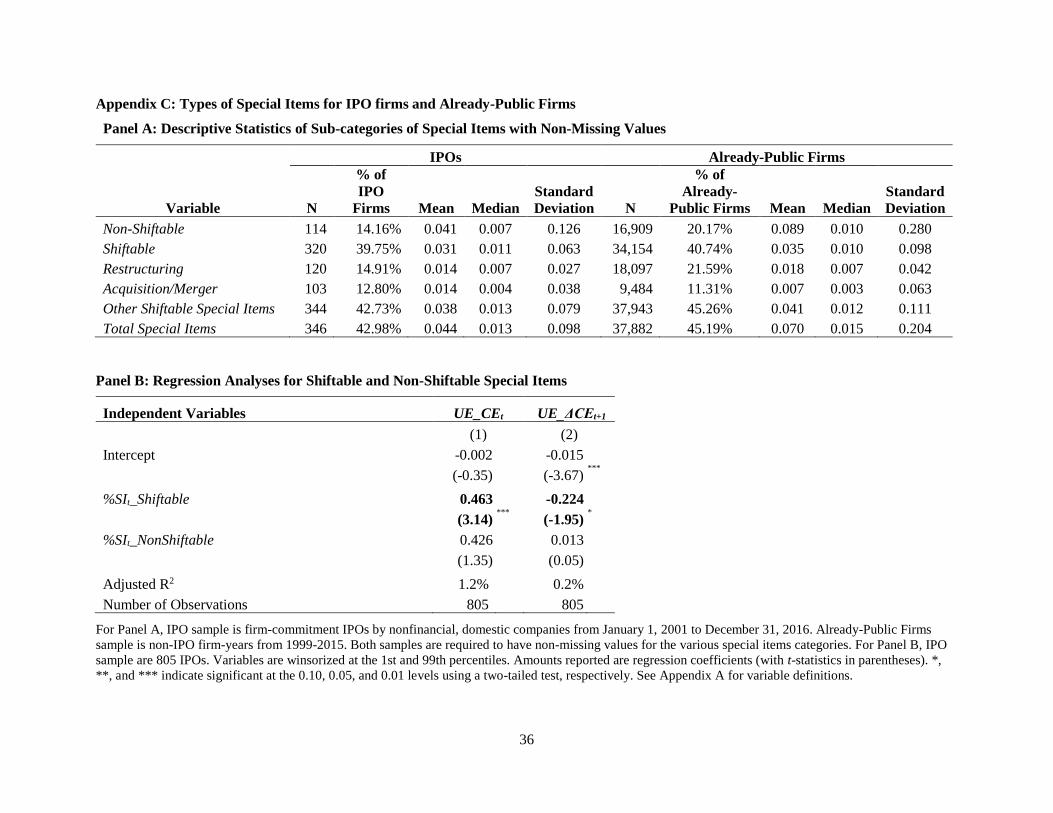

The greater degree of classification shifting of IPO firms is likely due to different special items

events experienced by IPO firms in comparison to already-public firms. To investigate this possibility, we

provide descriptive statistics for sub-categories of special items for IPO firms and already-public firms in

Appendix C Panel A. We focus on shiftable special items: restructuring, acquisition/merger, and other

special items (McVay 2006). As shown, IPO firms have lower restructuring frequency (14.91% versus

15 IPO firms may experience special items events in the post-IPO years, which enables them to sustain an inflated core

earnings through repeated classification shifting. If this is the case, it would be less likely to find a negative association

between %SIt and UE_∆CEt+1. To the extent that we find a negative coefficient (β1 < 0), we infer that offering firms

have most likely engaged in pre-IPO classification shifting.

19

21.59%) and amounts (0.014 versus 0.018) than already-public firms. This is understandable since IPO

firms tend to be younger firms and less likely in need of restructuring than already-public firms. As to

merger and acquisitions (M&A), although its occurrence is similar between IPO firms and already-public

firms (12.80% versus 11.31%), IPO firms incur on average twice the amount of M&A expenses incurred

by already-public firms (0.014 versus 0.007). As to “Other Shiftable Special Items,” we find that both its

occurrence (42.73% versus 45.26%) and magnitude (0.038 versus 0.041) are similar between IPO and

already-public firms. When we sum up the three categories of shiftable special items, we find that IPO and

already-public firms have similar frequency (39.75% versus 40.74%) and magnitude (0.031 versus 0.035)

of shiftable special items. For non-shiftable special items, the frequency (14.16% versus 20.17%) and

magnitude (0.041 versus 0.089) are both lower for IPO firms than non-IPO firms.

Appendix C Panel B presents regression analyses for IPO firms by decomposing special items into

shiftable and non-shiftable types. Consistent with McVay (2006), we find that only shiftable special items

allow issuers to classification shift and improve core earnings (0.463; t = 3.14), whereas non-shiftable

special items do not (0.426; t = 1.35). Our results tabulated in Table 3 for IPO firms are thus attributable to

shiftable as opposed to non-shiftable special items.

Combined, Appendix C results provide more details about IPO special items relative to already-

public companies. Although the total shiftable amounts are similar between IPO firms and non-IPO firms,

we find the composition of special items are structurally different. That is, IPO firms have lower frequency

of restructuring events, but higher magnitude of M&A expenses. The different composition of special items

offers a plausible account for the greater degree of classification shifting for IPO firms than already-public

firms.

Classification Shifting and Price Formation

We conjecture that the primary motivation for IPO firms to pursue pre-IPO classification shifting

is to influence investors’ valuation. We, therefore, investigate whether IPO price formation is associated

with pre-IPO classification shifting (H2). We use two empirical proxies that capture IPO price formation.

20

The first proxy is the percentage change in offer price (PRC_REV) from the midpoint of initial price range

in the preliminary prospectus to the final offer price in the final prospectus (e.g., Ljungqvist and Wilhelm

2003). The second empirical measure is the initial IPO return (INI_RET) (e.g., Lowry and Schwert 2004).

Using these two proxies, we test whether pre-IPO classification shifting is associated with price revisions

(H2a) and initial returns (H2b). In addition to price revisions, IPO issuers may change the number of shares

offered from the initial prospectus to the final prospectus, which affects the IPO proceeds. Thus, we

complement the test of price revisions (i.e., H2a) using an alternative measure, value revisions (VAL_REV).

We define VAL_REV as the percentage change of offering value from the initial value, which is determined

by the price and share information in the preliminary prospectus, to a comparable measure that is

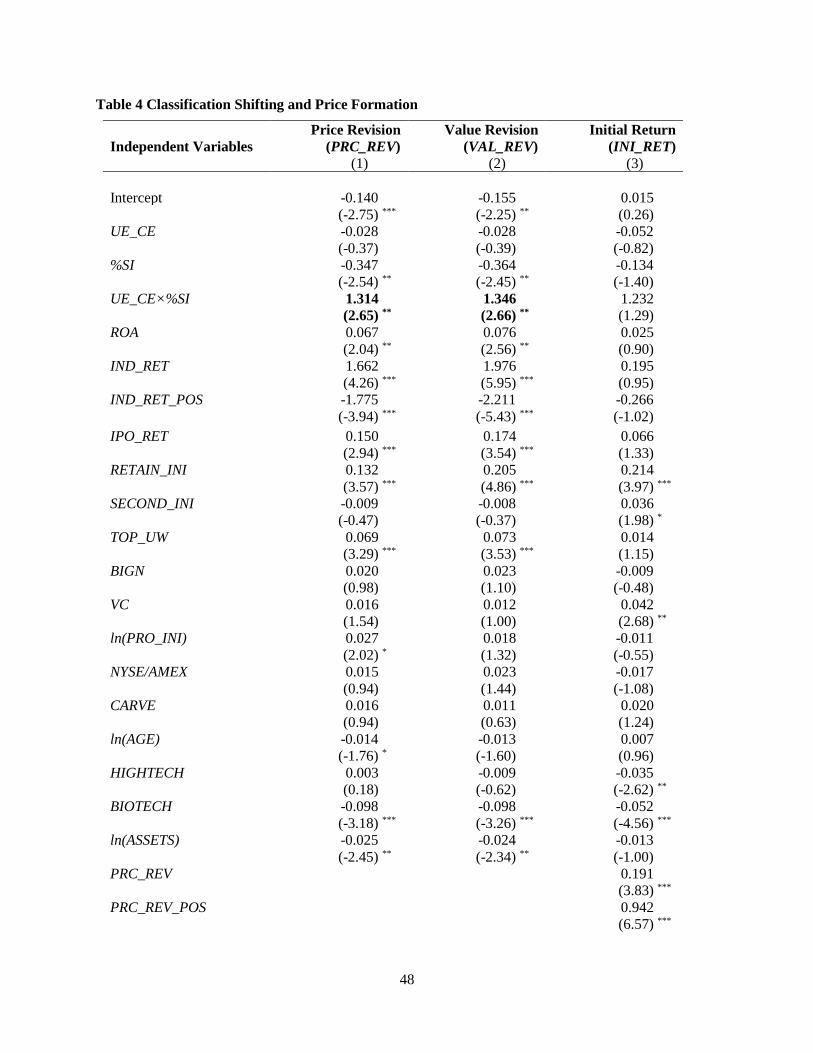

determined by the price and share information in the final prospectus. To test H2, we adapt Willenborg et

al. (2015)’s models as below.

PRC_REV (or VAL_REV) = γ0 + γ1 UE_CEt + γ2 %SIt + γ3 UE_CEt×%SIt + γ4 ROA + γ5 IND_RET

+ γ6 IND_RET_POS + γ7 IPO_RET + γ8 RETAIN_INI + γ9 SECOND_INI + γ10 TOP_UW +

γ11 VC + γ12 BIGN + γ13 ln(PRO_INI) + γ14 NYSE/AMEX + γ15 CARVE + γ16 ln(AGE) + γ17

HIGHTECH + γ18 BIOTECH + γ19 ln(ASSETS) + YEAR_DUMMY + νt, (4)

INI_RET = γ0 + γ1 UE_CEt + γ2 %SIt + γ3 UE_CEt×%SIt + γ4 ROA + γ5 IND_RET + γ6

IND_RET_POS + γ7 IPO_RET + γ8 RETAIN + γ9 SECOND + γ10 TOP_UW + γ11 VC + γ12

BIGN + γ13 ln(PRO) + γ14 NYSE/AMEX + γ15 CARVE + γ16 ln(AGE) + γ17 HIGHTECH +

γ18 BIOTECH + γ19 ln(ASSETS) + γ20 PRC_REV + γ21 PRC_REV_POS +

YEAR_DUMMY + νt, (5)

Consistent with McVay (2006, p. 523), we focus on UE_CE×%SI as our proxy for the extent of

pre-IPO classification shifting. This measure of the extent of classification shifting increases with both

levels of unexpected core earnings and special items. If classification shifting influences price revisions

(H2a) and initial returns (H2b), then we would expect that coefficient for UE_CE×%SI to be positive

(γ3 >0).16 The estimation results are provided in Table 4. Column (1) reports the results for price revision

16 When %SIt is zero, it is not feasible for a firm to misclassify core expenses as special items. Similarly, if the

interaction term is negative (UE_CEt×%SIt < 0), a firm is less likely to engage in classification shifting. However, the

likelihood of classification shifting for a firm with negative value of UE_CEt×%SIt may not be lower than a firm

21

(PRC_REV). As shown, the coefficient estimate on UE_CE×%SI is positive and significant (1.314; t =

2.65). This finding suggests that inflated core earnings through classification shifting induce strong investor

interest in an IPO firm’s share. It supports that IPO price revisions increase with the degree of pre-IPO

classification shifting, and therefore, lends support to H2a. The coefficient on %SI is negative (-0.347; t =

-2.54), indicating that investors consider income-decreasing special items events per se unfavorably and,

as a response, issuers revise their offer price downward in the absence of classification shifting.

[Insert Table 4 here.]

Results on the covariates are generally consistent with prior studies. PRC_REV is positively

associated with ROA, suggesting that accounting earnings influence investors’ valuation of IPO firms

(Willenborg et al. 2015). The price revision is also positively related to secondary-market industry returns

(IND_RET) and contemporary IPO returns (IPO_RET), indicating that the final offer price reflects public

information revealed during the book-building phase (Ljungqvist and Wilhelm 2003). A negative

coefficient on IND_RET_POS suggests that price revisions to favorable market news are less complete than

they are to negative news (Lowry and Schwert 2004). Price revisions are positively associated with

management equity retainment (RETAIN_INI), higher values of which are positive signals of an IPO firm’s

value (Leland and Pyle 1977). Consistent with Ljungqvist and Wilhelm (2003), top-ranked underwriters

(TOP_UW) are better able to extract information during the book-building phase and incorporate it into the

final offer price. Firms in the biotech industry (BIOTECH) and larger firms (ln(ASSETS)) have more

negative price revisions (Willenborg et al. 2015).

Column (2) tabulates estimation results for VAL_REV. The untabulated correlation between

PRC_REV and VAL_REV is quite high (Pearson correlation is 0.968). Like PRC_REV, VAL_REV is

positively and significantly associated with UE_CE×%SI (γ3 = 1.346; t = 2.66), suggesting that offering

value revision in the book-building process is increasing with the extent of pre-IPO classification shifting.

without special items (UE_CEt×%SIt = 0). Therefore, we conduct a robustness test by setting the UE_CEt×%SIt as

zero when it is negative. Our results remain inferentially the same.

22

This result again supports H2a. Other estimation results are generally consistent with those reported for

PRC_REV in column (1).

Column (3) provides estimation results for initial returns (INI_RET). We do not find a significant

coefficient on UE_CE×%SI (γ3 = 1.232; t = 1.29), and thus do not find support for H2b. This result is

consistent with IPO firms, under time pressure to cash out benefits rendered by pre-IPO classification

shifting, insisting that the final offer price fully capitalize the favorable signals, which allows IPO firms to

achieve greater proceeds. Combined with the results from columns (1) and (2), this finding suggests that

although underwriters tend to underprice all issues (Benveniste and Spindt 1989), issuers involved in pre-

IPO classification shifting negotiate harder to maximize the final offer price than those that have not

engaged in expense misclassification. This is conceivable because when misclassified core expenses

reappear in the post-IPO period, which decreases core earnings, pre-IPO inflation of core earnings will

become apparent. Therefore, issuers will run the risk of forfeiting their entire economic benefit from

engaging in this pre-IPO accounting manipulation if they acquiesce to underwriters’ lowballing the final

offer price.17

Estimation results for other control variables are generally consistent with prior studies (Lungqvist

and Wilhelm 2003, Willenborg et al. 2015). The coefficient estimates on PRC_REV and PRC_REV_POS

are both positive and significant, with the latter being larger than the former, which supports the “partial”

adjustment theory (Benveniste and Spindt 1989). A positive coefficient on VC indicates that an IPO backed

by venture capitalists experiences higher first-day returns (Lee and Wahal 2004). The coefficient on

17 Misclassified core expenses will reappear in the fiscal year following the classification shifting. This reversal feature

of classification shifting suggests that not all issuers have identical incentives to engage in pre-IPO classification

shifting. Issuers that sell more shares through the initial offering (i.e., less equity retention) will benefit more from

inflated core earnings through pre-IPO classification shifting as they are likely to obtain greater offering proceeds.

IPO firms that sell less shares during the initial offering (i.e., retain more shares) are less likely to engage in pre-IPO

classification shifting because the reversal of misclassified core expenses will undercut long-term proceeds from

selling additional shares following the IPO. Therefore, we conjecture that IPO firms with lower (higher) equity

retention are more (less) likely to engage in pre-IPO classification shifting. To test this conjecture, we partition IPO

sample into two subsamples based on the median equity retention (RETAIN) and estimate Model (3) for both

subsamples. Untabulated results show that IPO firms engage in opportunistic pre-IPO classification shifting only when

equity retention is low (β1 = 0.468; t = 3.59) but not when equity retention is high (β1 = 0.236; t = 1.39).

23

RETAIN_INI is positive and significant. This result is analogous to the corresponding result of price

revisions (PRC_REV), suggesting that management equity retainment conveys positive signals about an

IPO firm’s value.

Pre-IPO Classification Shifting, Initial Value and Price Revision

We predict and find that pre-IPO classification shifting increases investor valuation and thus the

price revision (H2a). However, this result is also consistent with an alternative explanation – IPO firms

that are (not) involved in classification shifting negotiate less (more) aggressively in their initial price range.

Underwriters and issuers jointly determine the initial price range in the initial prospectus without the

significant involvement of investors. It is conceivable that issuers involved in classification shifting are

aware of their accounting manipulation and are willing to concede to a greater degree over the initial price

range. During the book-building process, investors are road showed an issuer’s initial prospectus including

core earnings and initial price range. Road show investors tend to have greater interest in issuers with

stronger core earnings (Willenborg et al. 2015), whereas they have little knowledge whether the strong core

earnings are inflated by classification shifting. With inflated core earnings attracting greater interest from

roadshow investors, issuers involved in classification shifting are more likely to enjoy a greater increase in

the price revision. This argument based on the initial bargaining position of issuers also suggests a positive

association between the price revision and pre-IPO classification shifting.

The above conjecture suggests analyzing the initial offer price range in relation to pre-IPO

classification shifting. An analysis focusing on the initial price range is likely to be problematic because

IPO firms often target a standard price range and adjust their issuing shares accordingly to arrive at their

initial valuations. As a result, the initial price range does not vary greatly across IPOs (Willenborg et al.

2015). The standard deviation of the midpoint of initial price range for our sample is $6, which is

approximately 38% of its average of $16. These descriptive statistics are comparable to those of Willenborg

et al.’s (2015). Therefore, we use the initial value (INI_VAL) to test the relationship between pre-IPO

classification shifting and IPO firms’ initial valuation. Following Willenborg et al. (2015), we define

24

INI_VAL as the midpoint of initial price range multiplied by post-IPO shares outstanding from the

prospectus disclosing the initial price range divided by total assets. We specify the following model:

INI_VAL = γ0 + γ1 UE_CEt + γ2 %SIt + γ3 UE_CEt×%SIt + γ4 ROA + γ5 RETAIN_INI + γ6

SECOND_INI + γ7 TOP_UW + γ8 BIGN + γ9 VC + γ10 ln(PRO_INI) + γ11 NYSE/AMEX +

γ12 CARVE + γ13 ln(AGE) + γ14 HIGHTECH + γ15 BIOTECH + γ16 SALES_AT+ γ17

ΔSALES + YEAR_DUMMY + νt, (6)

Appendix E column (1) provides the estimation results for Model (6). As shown, the coefficient

estimate on UE_CEt×%SIt is significantly negative (-31.979; t = -3.45). It suggests that issuing firms

involved in pre-IPO classification shifting concede more over their initial price range. This result indicates

that the previously documented relation between pre-IPO classification shifting and price revisions (H2a)

is likely to be explained by the association between pre-IPO classification shifting and IPO firms’ initial

negotiation position. To test this possibility, we adapt Model (4) by including INI_VAL as an additional

explanatory variable as below:

PRC_REV (or VAL_REV) = γ0 + γ1 UE_CEt + γ2 %SIt + γ3 UE_CEt×%SIt + γ’ INI_VAL + γ4 ROA +

γ5 IND_RET + γ6 IND_RET_POS + γ7 IPO_RET + γ8 RETAIN_INI + γ9 SECOND_INI + γ10

TOP_UW + γ11 VC + γ12 BIGN + γ13 ln(PRO_INI) + γ14 NYSE/AMEX + γ15 CARVE + γ16

ln(AGE) + γ17 HIGHTECH + γ18 BIOTECH + γ19 ln(ASSETS) + YEAR_DUMMY + νt,

(4’)

Columns (2) and (3) of Appendix E provide the estimation results for price revisions and value

revisions, respectively. As shown in column (2), the coefficient estimate on UE_CEt×%SIt is positive and

significant (1.409; t = 2.67) even after including the IPO firms’ initial negotiation position (INI_VAL).

Similarly, column (3) shows that the value revision (VAL_REV) is positively associated with pre-IPO

classification shifting (1.435; t = 2.69). The results of columns (2) and (3) together suggest that pre-IPO

classification shifting is associated with price revisions even after controlling for IPO firms’ initial

negotiation position. These results provide consistent support to H2a. In summary, our results demonstrate

that while issuers involved in classification shifting concede more on their initial price ranges, they are

more aggressive in negotiating the final offer price by leveraging roadshow investors’ interest in their shares.

25

Classification Shifting and Post-IPO Stock Performance

Our findings above suggest that pre-IPO classification shifting is indeed associated with investor

valuation around IPOs. We next examine the relationship between pre-IPO classification shifting and post-

IPO underperformance (H3). When the misclassified core expenses reappear in the subsequent year,

investors are likely to unravel the implications of pre-IPO classification shifting. H3 predicts that pre-IPO

expense misclassification is associated with lower post-IPO returns. Building on Ritter (1991) and Carter

et al. (1998), we specify the following model.

POST_RET = γ0 + γ1 UE_CEt + γ2 %SIt + γ3 UE_CEt×%SIt + γ4 ROA + γ5 TOP_UW + γ6 VC + γ7

ln(AGE) + γ8 HIGHTECH + γ9 BIOTECH + γ10 ln(ASSETS) + γ11 ln(PRO) + γ12 STD_RET

+ γ13 SECOND + γ14 INI_RET + YEAR_DUMMY + νt, (7)

where POST_RET is one of the three post-IPO annual stock return measures as discussed below. The first

proxy for post-IPO stock return measure is Fama-French 25 portfolio-adjusted returns (PAR). Following

Lowry et al. (2017), we calculate PAR as an IPO firm’s raw buy-and-hold return less the size and book-to-

market matched Fama-French 25 portfolio return, where the holding period is from the offer date plus six

trading days through the earlier of offer date plus 253 trading days or the delisting date. Size is measured

as the market value of equity at the end of the first December after the IPO. Book-to-market is calculated

as the ratio of book value of equity to the market value, where book value of equity is measured at the first

fiscal year end after the IPO. Next, we match an IPO firm to a Fama-French 25 portfolio based on size and

book-to-market. We obtain the value-weighted returns for portfolios formed on size and book-to-market

from Kenneth French’s website. The second empirical proxy that we use to measure the post-IPO stock

performance is market-adjusted returns (MAR_VW). We calculate MAR_VW as an IPO firm’s one-year raw

buy-and-hold return less the CRSP value-weighted market portfolio return (e.g., Carter et al. 1998). We

define the third proxy, market-adjusted returns (MAR_EW), similarly to MAR_VW except that the

benchmark is the CRSP equally-weighted market portfolio return.

Following prior IPO literature focusing on annual stock performance (Ritter 1991, Carter et al.

1998), we include additional control variables. Specifically, we control for IPO gross proceeds (ln(PRO)),

26

firm age (ln(AGE)), post-IPO stock volatility (STD_RET), underwriter quality (TOP_UW), venture capital-

backing (VC), percentage of secondary shares sold (SECOND), and initial returns (INI_RET). We also

include year fixed effects. As previously, our variable of interest is UE_CEt×%SIt. H3 predicts a negative

coefficient on γ3, indicating that post-IPO stock return is decreasing with pre-IPO classification shifting.

Table 5 presents H3 testing results. Column (1) shows a negative coefficient on UE_CEt ×%SIt (γ3

= -2.505; t = -2.30) from the regression of Fama-French 25 portfolio-adjusted one-year returns. Column (2)

uses post-IPO returns adjusted by market value-weighted returns and reports a negative coefficient on

UE_CEt ×%SIt (γ3 = -2.116; t = -1.81). Column (3) provides results using market equally-weighted index

adjusted one-year post-IPO returns. Again, we find the coefficient significantly negative (γ3 = -2.379, t = -

2.03). Combined, these findings provide consistent support for H3 that pre-IPO classification shifting is

negatively associated with post-IPO stock returns.

[Insert Table 5 here.]

The coefficient estimates on the control variables are consistent with prior literature (Brav and

Gompers 1997, Carter et al. 1998, Krishnan et al. 2011). For example, post-IPO stock returns are positively

associated with investors’ pre-offer demand of an IPO, which is reflected in the fraction of shares offered

by current shareholders (SECOND), and firm size (ln(ASSETS)), and negatively associated with the

uncertainty of firm value around an IPO (STD_RET) and offer size (ln(PRO)). The positive coefficient on

VC is consistent with VC-backed IPOs perform better than non-VC-backed IPOs (e.g., Krishnan et al. 2011).

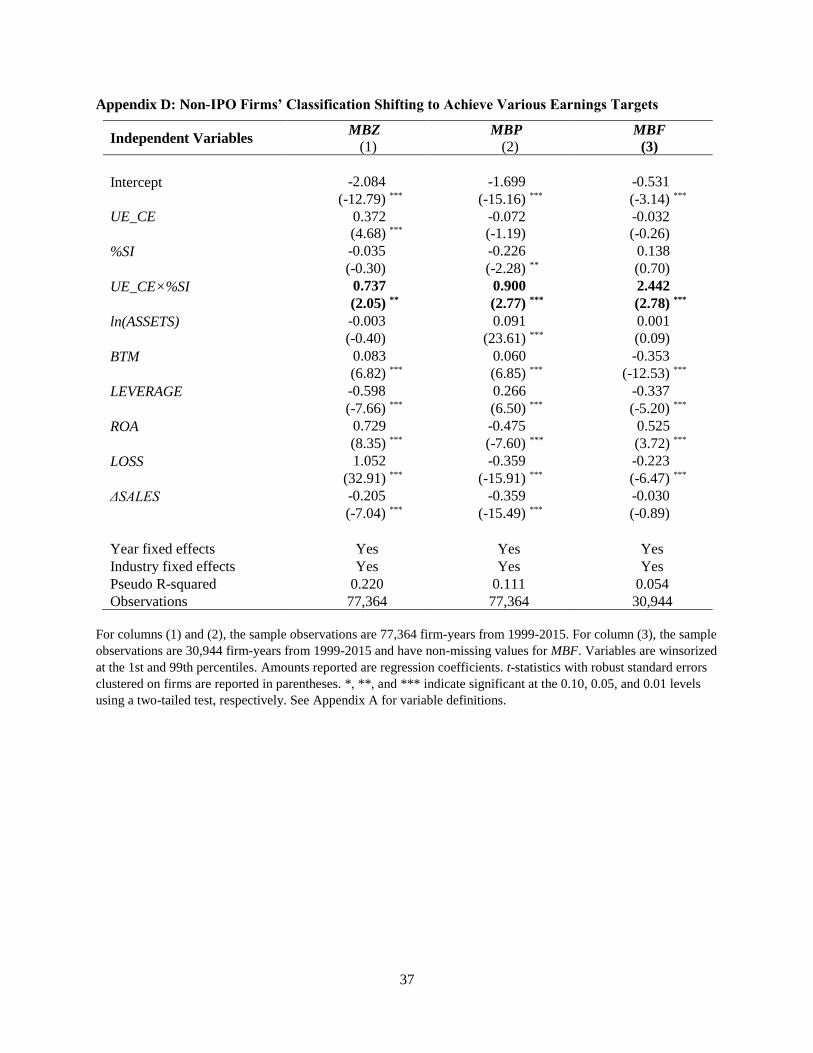

Classification Shifting and Non-IPO Firms’ Meeting or Beating Earnings Benchmarks

Consistent with McVay (2006, p. 523), we use UE_CEt ×%SIt to proxy for the degree of

classification shifting to test H2 and H3. However, this measure has received little validation from the

classification shifting research regarding its predictive validity. We conduct additional validity checks to

test whether this measure captures opportunistic expense misclassification as it is intended. Specifically,

we investigate whether classification shifting, as proxied by UE_CEt ×%SIt, allows public firms to better

27

able to achieve various earnings benchmarks. For this validation test, we use all public firm-years from

1999 to 2015 with necessary data. Following extant benchmark research (e.g., McVay et al. 2006, Shon

and Veliotis 2013), we specify the following logistic model:

MBE = θ0 + θ1UE_CEt + θ2%SIt + θ3 UE_CEt×%SIt + θ4 ln(ASSETSt) + θ5 BTMt + θ6 LEVERAGEt

+ θ7 ROAt + θ8 LOSSt + θ9 ΔSALES t + ηt, (8)

We measure MBE using three different measures and use each in separate tests. First, MBE = MBZ,

where MBZ equals one when core earnings (CEt) scaled by total assets (AT) at the beginning of the year

falls in between 0 and 0.02, and zero otherwise. Second, MBE = MBP, where MBP equals one when the

difference in core earnings (CEt - CEt-1) scaled by total assets at the beginning of the year is between 0 and

0.01, and zero otherwise. Third, MBE = MBF, where MBF is an indicator variable that equals one if the

difference between I/B/E/S actual earnings and the most recent consensus analyst forecasts is between $0.00

and $0.01, and zero otherwise. The definitions of explanatory variables are included in Appendix A.

Consistent with previous classification shifting studies (e.g., Fan and Liu 2017), we expect that

opportunistic classification shifting will allow public firms to better able to achieve various earnings

benchmarks (θ3 > 0).

Appendix D columns (1) – (3) present the estimation results when reported core earnings just meet

or beat the zero, prior year, and analyst forecast benchmarks, respectively. For the first two benchmarks,

the sample is comprised of 77,364 firm-years from 1999 to 2015. The sample for analyst forecast

benchmark is reduced to 30,944 observations because of missing I/B/E/S data for analyst earnings forecasts.

Column (1) reports a positive coefficient estimate on UE_CEt×%SIt (0.737; t = 2.05), suggesting that firms

misclassify core earnings as special items to meet zero core earnings expectation (MBZ). Column (2) shows

that the likelihood of achieving positive core earnings change (MBP) increases with UE_CEt×%SIt (0.900;

t = 2.77). This result indicates that firms misclassify core expenses as income-decreasing special items to

beat prior period core earnings benchmark. As shown in column (3), for firm-years that just meet or beat

the consensus analyst forecasts of earnings (MBF), managers misclassify a greater amount of core expenses

28

as income-decreasing special items (2.442; t = 2.78). Combined, these results support the validity of our

empirical proxy used in H2 and H3 tests for classification shifting (UE_CEt×%SIt).

IPO Classification Shifting versus Accruals Manipulation

IPO firms can employ a portfolio of earnings management tools such as classification shifting and

accruals management. Existing IPO literature has focused almost exclusively on accruals management (e.g.,

DuCharme et al. 2001, Venkataraman et al. 2008). Classification shifting may complement or supplement

accruals management for IPO issuers. On one hand, IPO firms may use both classification shifting and

accruals management to influence investor valuation. In such case, classification shifting will be positively

related to accruals management.

On the other hand, classification shifting may also be negatively associated with accruals

management. When managers’ discretion is more constrained for one earnings management tool, they often

make more use of the other tools (Zang 2012). Consistent with this argument, Fan et al. (2010) find that

when accruals management is constrained, classification shifting becomes more prevalent. In the pre-IPO

context, accruals management is likely to be more limited due to heightened litigation risk and monitoring

scrutiny around IPOs (Ball and Shivakumar 2008). Aggressive accruals on the IPO prospectuses are likely

to attract attention from disgruntled investors, who are looking to file offer-related lawsuits against the

issuers to recover their damage, and also from auditors who are required to exercise due diligence in the

IPO process (DuCharme et al. 2004, Venkataraman et al. 2008).18 Venkataraman et al. (2008) find that pre-

IPO audited accruals are negative, and that auditors charge higher fees for IPO engagements than post-IPO

engagements. To the extent that pre-IPO accruals management is more scrutinized, issuers are more likely

to engage in classification shifting instead. If this is the case, accruals management will be negatively

associated with classification shifting in the pre-IPO period.

18 Indeed, prior studies document that pre-IPO abnormal accruals is associated with increased litigation risk and

subsequent settlement amount (e.g., DuCharme et al. 2004, Billings and Lewis 2016).

29

To examine whether classification shifting is positively or negatively associated with accruals

management, we employ the following model:

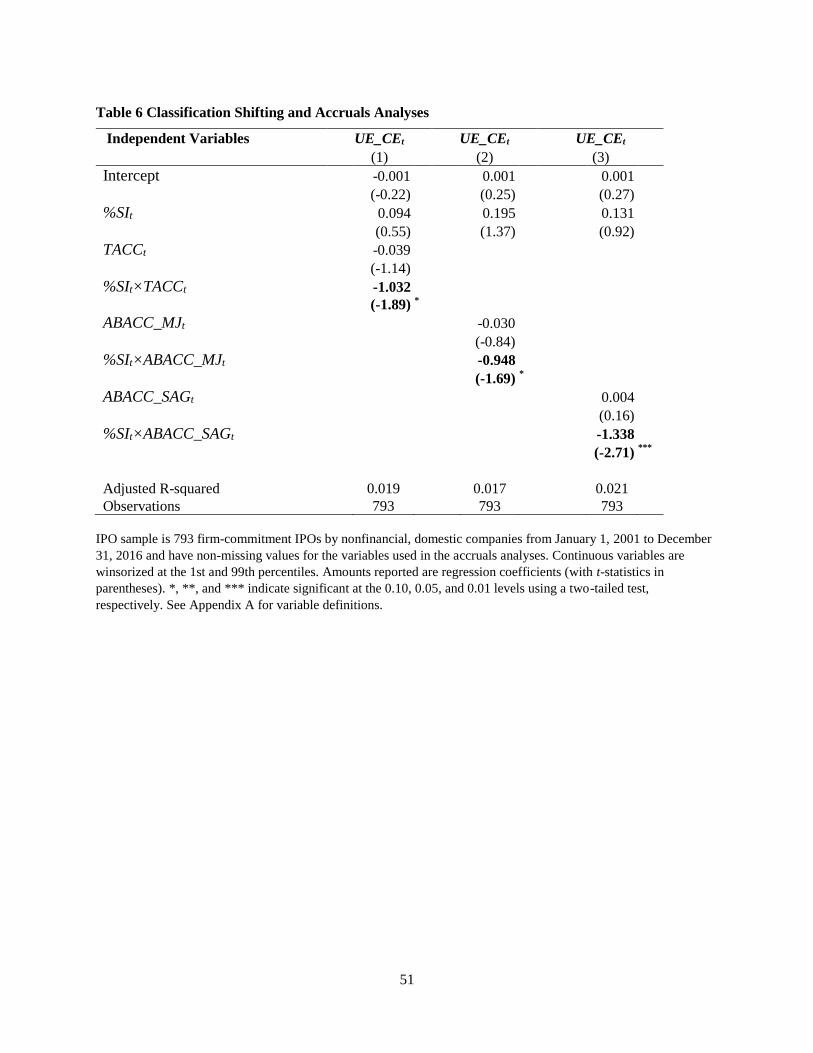

UE_CEt (UE_∆CEt+1) = λ0 + λ1%SIt + λ2ACCRUALSt + λ3%SIt×ACCRUALSt + ηt, (9)

where ACCRUALSt is one of the following three accruals measures – total accruals (TACC), abnormal

accruals estimated from the modified Jones model (ABACC_MJ) (Jones 1991, Dechow et al. 1995), and

abnormal accruals estimated based on Armstrong et al. (2016)’s size-age-growth-matched model

(ABACC_SAG). The definitions of the three accruals measures are provided in Appendix B. Our variable

of interest is the interaction between %SIt and the accruals proxy. A positive (negative) coefficient on λ3

suggests that classification shifting is increasing (decreasing) with accruals management. Table 6 columns

(1), (2), and (3) present the unexpected core earnings regression results with TACCt, ABACC_MJt, and

ABACC_SAGt as the accrual proxy, respectively. In each of the three models, the coefficient

on %SIt×ACCRUALSt is both negative and significant. In summary, these findings show that pre-IPO

classification shifting is negatively associated with pre-IPO accruals manipulation and suggest that IPO

firms misclassify more core expenses as income-decreasing special items when accruals manipulation is

constrained.

[Insert Table 6 here.]

6. Conclusion

Do IPO firms classification shift to influence IPO pricing? We address this question in this study.

We provide initial evidence that IPO firms engage in expense misclassification to inflate core earnings prior

to the IPO. In addition, we find that IPO firms classification shift to a greater degree than already-public

firms. More importantly, we find that pre-IPO classification shifting is positively associated with IPO price

revision from the initial price range to the final offer price, even though it is not associated with the first-

day market return. Furthermore, when misclassified core expenses reappear following IPOs, issuers

30

experience lower stock returns. Finally, we find that pre-IPO classification shifting is more prevalent when

accruals management is more limited.

This study contributes to the IPO literature in several important ways. First, this study extends the

growing literature of IPO price formation by demonstrating that pre-IPO classification shifting is positively

associated with an issuer’s price revision. We provide initial evidence that pre-IPO classification shifting,