Do bank-affiliated P&C insurers perform better? An ... ANNUAL MEETINGS/2018-Milan... ·...

46

1 Do bank-affiliated P&C insurers perform better? An empirical investigation Suggested short title: Do bank-affiliated P&C insurers perform better?

Transcript of Do bank-affiliated P&C insurers perform better? An ... ANNUAL MEETINGS/2018-Milan... ·...

1

Do bank-affiliated P&C insurers perform better?

An empirical investigation

Suggested short title: Do bank-affiliated P&C insurers perform better?

2

Abstract

In the last years European banks have entered the high margin P&C insurance business by

means of selling agreements with insurers and through stock holdings in captive insurance

firms whose main distribution channel is their parent banks’ branch network. This article

sheds light on these insurance companies’ performance, by means a sample comprising all

Italian P&C insurers operating in the country during the 2005-2015 timeframe. Our data show

that bank-affiliated insurers pay higher distribution costs, presumably shifting profits to parent

banks through fees. They also have a higher underwriting profitability than other insurers.

However, our evidence seems to imply that this might be due more to their ability at

transferring costs to policyholders than to their selection expertise, as bank-affiliated insurers

exhibit a more intensive use of passive reinsurance, pointing at poorer risk management skills.

Overall, our results seem to indicate that bank affiliation per se is counterproductive.

3

JEL Classification

G21, G22, L25, M21.

Keywords

Non-life insurance performance; Bancassurance; Non-life policies. P&C insurers; P&C

insurers’ profitability;

4

1. Introduction:

The debate about the merits of combining the traditional banking with other financial

activities has a long story. Proponents of financial liberalization score an important point

when, in order to foster the creation of an integrated market for financial services in Europe,

the EU Second Banking Directive was enacted in 1989. The directive set the conditions for

the entrance of (mostly) specialized national financial players into foreign markets and for the

creation of full-fledged financial conglomerates combining banking, insurance and securities

related activities.

Bancassurance is the word used to refer to the cooperation between banks and insurers

aimed at profiting from cross - selling opportunities created after 1989. It is mostly due to

banks’ entrance in the insurance industry. European banks swiftly took advantage from the

new regulatory framework. Insurers were not as assertive, also due to their dedicated

distribution networks, which are less versatile, and mostly decided to stick to their usual

business.

Even though individual banks may pursue different strategies and the national context

has an impact on its spread, todays’ bancassurance relevance is undisputed in both developed

and emerging economies1. However, while the selling of life insurance products by banks is

an established fact, banks’ interest in P&C products is more recent.

Since the 1990s, in France and the UK only at first and later in other countries too,

European banks have sold payment protection insurance policies - a.k.a. PPI products - linked

1 Fiordelisi and Ricci 2012; Sreesha 2015; Liang and Ching 2015.

5

to loans granted to customers. PPI policies are designed by an instructed insurer to protect the

lender from the borrowers’ default. These products include both life policies covering the

borrower’s death risk and non-life policies addressing various risks related to the borrower’s

health and business or professional activity. Temporary or permanent disability insurance,

health insurance and unemployment insurance are typically part of the package. PPIs may

also include a protection on the value of the loan collateral – i.e. mortgage loans have often

property policies attached2.

While purely protective non-life insurance products sold independently from credit

products (a.k.a. stand-alone policies) commanded lower priority in the past, data on European

bank branches’ annual premium market share show that this is not the case anymore: banks

have entered new lines of business such as motor and travel insurance3. Lasting low interest

rates make both the traditional banking and the life insurance business less profitable and

banks seek to enhance their performances entering the higher margin P&C insurance industry.

The range of stand-alone policies offered through banks in part covers the same risks

covered by PPI policies, from health to property risks. However, the product design is not

ancillary to any financial product. The customer or her damaged counterparties are the only

beneficiaries of the claim repayment. The risks insured by stand-alone policies include the

following: Health, (Critical illness, Medical expenses, Personal accident, Permanent

disability), Unemployment (loss of income) but also Travel, Property and Motor.

As far as the insurance and the banking activities are concerned, financial

conglomerates do not usually carry out the full range of services as in-house departments. On

one hand, national laws may still require that a specialized player take care of the

underwriting part of the process - as it happens in Italy. On the other hand, even when

2 Artikis et al. 2008. 3 Insurance Europe, 2016.

6

allowed to operate in house the entire financial business, as in Germany, conglomerates

usually combine banking and insurance activities via a separately capitalized subsidiary of

either an insurer or a bank.

Three different types of insurers perform P&C policies underwriting. First, bank-

affiliated ones, i.e. insurance companies whose shares are held by one or more banks. Parent

banks exploit the controlled insurance companies’ underwriting powerhouse to design

products (mostly) targeted to their customers and mainly (but not exclusively) sold through

their branch networks. Second, non-bank-affiliated insurers (a.k.a traditional insurers) who

signed commercial agreements with banks but also operate their own distribution networks -

through which they mostly sell their products. Last, traditional P&C insurers who do not

cooperate with banks.

While the academic literature has examined the role and performance of banks and

bank-affiliated insurers in the life industry, the exploration of banks and bank-affiliated

insurers’ behaviour and performance in the P&C sector is very limited. We want to contribute

to this investigation, by analysing the performance and its determinants for bank-affiliated

and traditional P&C insurers.

In particular, this article intends to shed light on non-life bank-affiliated insurers’

performance. First, we want to ascertain whether their profitability is different from P&C

traditional insurers’ profitability. Second, we want to examine the determinants of bank-

affiliated P&C firms’ performance in order to explain it, comparing their competitive

positioning with respect to traditional insurers’.

Spotorno et al. 2016 found that during the period 2003-2012 Italian bank-affiliated life

insurers were able to capitalize on their parent banks’ extensive distribution networks to save

on acquisition costs and that their product portfolio composition was in part different from the

7

one featured by traditional insurers, possibly to better serve bank customers’ needs.

Moreover, the proprietary link with a parent bank benefited life insurers’ performance per se.

In this paper, we investigate if that is the case for P&C insurers too. In our sample

bank-affiliated insurers’ product mix focus on risk coverage products that are mostly suitable

to retail customers, which is consistent with sales to bank customers through bank networks.

Bank-affiliated insurers’ product mix composition is different from traditional insurers’,

whose portfolios include a fair share of policies that target corporate customers, whose needs

are more complex and risks more nuanced than in the retail case. Unexpectedly, though in

line with the anecdotal evidence coming from the UK regarding PPI policies selling practices,

we found that bank-affiliated P&C insurers are less efficient than traditional ones also due to

their higher selling costs. They are also on average more reliant on passive reinsurance, even

if that is detrimental to performance, suggesting average poorer risk management abilities

than traditional insurers. On the other hand, they are more profitable at the underwriting level

- even if we suspect that this result comes from their higher ability at shifting costs to

customers and not from superior selection skills. Moreover, our analysis suggest that bank

affiliation per se impairs performance.

Our work contributes to the existing literature on bancassurance in several ways.

First, we present evidence on the relationship between their shareholders’ nature and P&C

insurers’ performance. Second, we uncover the way banks operate in the P&C insurance

sector through controlled companies: our results show that the competitive levers that banks

employ in the non-life insurance industry are different from the ones they are able to exploit

when confronting life insurers. Third, our analysis highlights that, possibly due to the peculiar

nature of the non-life business P&C deserves an autonomous investigation. Research works

8

examining the link between banks and insurers that do not recognize P&C distinctiveness

might produce flawed conclusions.

The structure of the paper is the following. The next section contains the literature

review. The third one depicts our research questions and the methodology we use. The fourth

section presents and comments on the results of our descriptive analysis while the fifth one

contains our multivariate regression analysis and its results discussion. Conclusions follow.

2. Literature review

Very little research is devoted to bancassurance activity in the non-life insurance

sector even though the phenomenon is sizeable, at least in Europe. According to Insurance

Europe4, in most Western European countries the bancassurance share in the distribution of

non-life policies lies between 5% to 15%, with Portugal (16,6%), France (13%) and Spain

(10,5%) leading the pack in 2015.

A few articles focus on banks’ sale of P&C policies attached to loans (PPI products).

As mentioned above, these contracts are meant to protect the lending bank in case of certain

negative events affecting either the borrower’s ability to repay the loan or the value of the

loan collateral. However, this literature focuses on the effect on loan interest rates5 and on the

mis-selling of these products by banks6 due to both the limitations in coverage7 and to their

high complexity and opaqueness8. These articles limit their analysis to either the bank or the

borrower point of view and do not consider the impact of banks’ PPIs selling activity on the

insurance companies underwriting the products. 4 Insurance Europe (2016). 5 Ashton and Hudson (2014). 6 Ashton and Hudson (2017). 7 Burchardt and Hills (1998). 8 FSA (2012).

9

Some works tackle the general issue of banks’ profitability linked to the cross selling

of non-bank products. However, these papers do not specifically deal with P&C insurance.

Research works examine either financial conglomerates overall profitability and efficiency9

or, when explicitly considering insurance, investigate the impact of cross selling life insurance

products only10.

Other authors investigate if there is any positive consequence on risk and return for

stockholders coming from the diversification effect due to the combination of the banking

business with the insurance business. Apart from papers dealing with product-line

diversification opportunities impact on the insurance business as a whole11, some works

specifically deal with the benefits coming from integrating the traditional bank with the non-

life insurance activity. In theory, the low correlation between the above activities should

allow the combined entity to stabilize earnings, enjoying a lower risk exposure. However,

empirical results do not always confirm this intuition. While Santomero and Chung12 and also

Boyd13 find that banks operating in the non-life insurance underwriting enjoy some risk

reduction, opposite results are obtained by Lown14 and by Nurullah and Staikouras15.

According to the latter, evidence from Europe shows that entering the non-life insurance

business significantly increase return volatility and the probability of bankruptcy for the

controlling bank while not benefiting its profitability.

9 for example see Vander Vennet (2002). 10 for example Fiordelisi and Ricci (2011), Chang et al. (2011). 11 such as Yildirim et al. (2006) and Elyasiani et al. (2015). 12 Santomero and Chung (1992). 13 Boyd et al. (1993). 14 Lown et al. (2000). 15 Nurullah and Staikouras (2008).

10

3. Research question, data and methodology

3.1 Research question and relevance of the present study

Are bank-affiliated P&C insurers different from traditional ones? And how relevant is

being “bank-affiliated” for succeeding in the non-life insurance business?

In this article, we answer the above questions by analysing the performances of Italian

non-life insurers from 2005 to 2015. We perform a descriptive analysis that help us single out

the features of bank-affiliated insurers, contrasting them with the traditional insurers’ ones

and we examine the impact that bank affiliation, distribution costs, claims, diversification and

age had on P&C insurers’ financial performance.

Our empirical evidence offers some interesting results that can enrich different streams

of literature.

First, ours is one of the few studies dealing with bancassurance that considers the

insurers’ point of view.

Second, the sale of a broad array of products, aiming at completing the range offered

to customers, can be accomplished by various means. The literature has examined the impact

of contractual agreements that reward the sellers through fees paid by the underwriters16.

However, while selling agreements are flexible and imply a limited investment, the seller can

obtain a stronger foothold in the business by controlling the underwriter, exploiting its

production powerhouse and directing its distribution. To our knowledge, the consequences of

this strategy in the P&C insurance industry are yet to be investigated. Therefore, our research

complements the existing literature on bancassurance and contributes to the debate on banks’

diversification into the insurance sector by considering a new point of view.

16 see for example Fiordelisi and Ricci (2011).

11

Third, the results of this study complete previous empirical researches devoted to the

life insurance sector17. Besides offering a detailed analysis of the Italian non-life insurance

market, our investigation indicates that the specificity of the non-life insurance sector is

relevant in defining banks’ strategies and the competitive levers they exploit.

Fourth, our paper reconciles existing literature on bancassurance with studies in the

area of non-life insurance performance18, by exploring the determinants of non-life insurers’

profitability and by investigating the impact of bank branches as an alternative distribution

network on financial results.

3.2. Methodology

After providing a detailed description of the differences between bank-affiliated and

traditional insurers, we check if bank affiliation per se creates value for non-life insurers via a

multivariate fixed effect panel regression that also enables us to explore the correlation

between differences in diversification and cost structures with our sample insurers’

performance.

In order to check the reliability of our methodology, first we performed the Hausman

test to choose among random and fixed effect panel estimation. After that, in order to treat

endogeneity problems that might arise from the impact of performance on reinsurance

decisions - bad performing firms might choose to reinsure more to save equity capital - we

instrumented the variable that measures the reinsurance used during the year and performed a

2SLS fixed effect panel estimation. Then we tested both the quality of our instrument and the

endogeneity of our instrumented variable. As we could not reject that the variable we

17 Spotorno et al. (2016). 18 see Moro and Anderloni (2014) for example.

12

instrumented is exogenous while our instrument’s quality was high, we chose to revert to a

fixed effect panel estimation, controlling for within cluster error correlation.

3.2.1. Model and variables

Our multivariate model is depicted by the following equation:

Performance measurei,t = f (αi, Bank affiliation dummyi,t ,Control variablesi,t) + εi,t

As for the dependent variable, we use both ROS (operating results/sales) and ROE

(earnings/equity) as we take into consideration both operating and shareholders’ profitability.

We calculated both Return on Sales (ROS) and Return on Equity (ROE) using as numerator

for the ratios the “Intermediate operating result”, which in turn is the sum of non-life

“Technical account result” and non-life “Net investment income”. This way we avoid the

influence of one-time items on results19.

As for the ratios’ denominator, sales are gross premiums written while equity is the

average value of two subsequent year-ends - which explains the lower number of observations

for ROE.

As mentioned, insurers are considered bank-affiliated if one or more banks own at

least 20% of their ordinary shares. The variable named Bank Affiliated_Dummy equals 1 if

that is the case and 0 whenever it is not.

As our main concern is the impact of bank affiliation on non-life insurers’

performance, several controls are necessary to disentangle it from other effects. We also

19 Nissim (2010).

13

exploited the variables listed below to single out differences in operations linked to the

insurers’ affiliation at a descriptive level.

Specifically, we check for differences in underwriting profitability (Loss ratio),

operating costs (Operating costs ratio), financial revenues (Investments financial return),

diversification (Diversified_Dummy), size (Size_Assets), age (Startup_Dummy) leverage

(Leverage) and passive reinsurance (Reinsurance ratio_Premiums).

Insurers’ underwriting profitability is usually measured using the loss ratio, which also

proxies the insurer appraisal of the current risk environment.

Our Loss ratio variable is the sum of total paid cost and total reserved cost for all

claims incurred, divided by earned premiums. We calculated both the numerator and the

denominator of the ratio net from reinsurance transfers, as the loss ratio is a measure of the

underwriting profitability of the insurance business retained by the firm (Ellis, 1998).

We expect a negative impact of this variable on profitability.

As different lines of business have structurally different levels of claims costs (also

due to the specific features of the policies sold), the loss ratio of the whole portfolio depends

on the company’s business mix. However, the claims reserve provisioning policy and the

premiums charged have also an impact on it: A low loss ratio – which indicates a high

underwriting profitability for the company – may be reconciled with an insurance company

that is covering its risks too little or that it is charging too much its customers. Both factors do

not immediately affect the insurer performance, but might have implications in the future20. If

we speculate that bank-affiliated insurers sell their policies to clients tied to their parent

20 Barth and Eckles (2009).

14

company via other products, they might be able to shift a higher portion of their costs on

customers, ceteris paribus lowering their loss ratios. On the other hand, in order to protect

customer relationships, banks might be willing to liquidate higher claims to their customers,

even if this implies a higher loss ratio (and a lower profitability) for their captive insurers.

Therefore, we do not have ex ante definite expectations about the differences in loss ratios

between traditional and bank-affiliated insurers.

The Operative costs ratio considers both distribution and administrative costs and

divides them by gross premiums written. We expect a negative impact on profitability.

At a descriptive level, we want to check if bank-affiliated insurers are able to exploit

their parent company branch network in order to save on distribution costs. We name the

variable that measures insurers’ selling efficiency Distribution costs ratio. It is the ratio

between distribution costs and gross premiums. Distribution costs are calculated by summing

up acquisition costs (the fees paid to agents, brokers and bank branches for selling the

company’s products) and fees paid for premium collection activities. Distribution costs are

then divided by gross premiums written because they include costs for selling all policies,

reinsured ones included.

In the academic literature, we found little evidence on the relevance of different

distribution channels and of their cost differentials for non-life insurers. Etgar21 compares

costs arising from different distribution choices. Berger22 offers an explanation for the

coexistence of distribution channels featuring sizable differences in costs while Kim23

suggests that the choice of the distribution channel is linked to governance issues and it is

therefore not entirely dependent on efficiency reasons only.

21 Etgar (1977). 22 Berger et al. (1997). 23 Kim et al. (1996).

15

The evidence regarding life insurers is more extensive. Spotorno24 finds lower

acquisition cost for Italian bank-affiliated life insurers. This result is confirmed by Klotzi25

that also document a variation in the difference between various distribution channels costs

depending on the country analyzed. While in Germany the difference between broker, tied

agent and bank channel are menial, in the countries where distributing policies through bank

branches is the most popular way to market life products (Austria, Belgium, Greece, Italy,

Portugal and Spain), selling through bank branches is also much cheaper than selling life

policies through other means. On the other hand, Chang26 results, coming from the analysis of

a Taiwanese life insurers’ sample, suggest that in that country bancassurance is less efficient

than the traditional sales channels in the life business.

Anecdotal evidence coming from the analysis of Italian traditional insurers’ financial

statements shows that non-bank-affiliated insurance companies tend to use a broad range of

distribution channels whose relevance depends on targeted customers (individuals or

companies) and on the range and peculiarities of operated lines of business. Traditional

insurers take advantage of the selling services offered by tied agents but also by banks’

branches and direct sales channels when selling to individuals while for corporate customers,

brokers and insurance companies’ direct selling force are prevalent.

According to information coming from surveys27, reports prepared by consultants28

and banks’ press releases29, bank-affiliated insurers, on the contrary, focus on retail customers

and tend to operate the business lines that these customers. Some banks promote the policies

they sell claiming to transfer part of their profit to customers (usually by discounting the

24 Spotorno et al. (2016). 25 Klotzi et al. (2017). 26 Chang et al. (2011). 27 Cetif (2013). 28 Meroni and Schiavi )2017). 29 Bonafede Dell’Olio (2017).

16

premium of additional policies covering ancillary risks offered to the client). If profits are

generated through cost savings, as it happens in the life business, we would expect that bank-

affiliated companies’ distribution costs are lower than non-bank-affiliated insurers. If the sale

of policies is instrumental to generate fee income for the parent bank, as it seems to have been

the case in the UK for PPI products, the opposite is to be expected.

Also at a descriptive level, we check if traditional insurers are more efficient at

managing claims than bank affiliated ones. We name Administrative costs ratio the variable

we use to perform that test. We calculate the Administrative costs ratio by dividing each firm

administrative costs by its net premiums written. Administrative costs refer to administration

expenses mainly related to the technical management of the company and are generally much

lower than distribution costs. Reinsurers manage transferred risks and this is the reason we do

not consider ceded premiums in the ratio denominator. A low administrative costs ratio might

be due to economies of scale. If bank-affiliated insurers are on average smaller, as we might

expect due to their more recent entrance in the business, their higher administrative costs over

net premiums written might not be due to their lack of skills at managing claims but to their

size.

The results of insurers’ financial investment activity are also included in our

multivariate analysis by means of the Investments financial return variable. We calculated

Investments financial return by dividing net investment financial results by the average

investments value over the year - obtained by averaging the year-end accounting value of the

firm investments over two subsequent years.

Being crucial for life insurers, investment activity is important for P&C insurance

companies as well. We obviously expect a positive impact of our variable on profitability.

Through our descriptive investigation, we also want to ascertain if bank-affiliated insurers’

17

investment results are different from traditional insurers’ ones as being part of a financial

conglomerate might positively influence investment activity through economies of scope.

As for diversification influence on performance, we check for it by a dummy variable

named Diversified_Dummy.

We had to come to terms with the fact that Italian non-life insurers are allowed to

operate eighteen different lines. In order to simplify insurers’ product portfolio composition,

we cut down to five sets by aggregating similar risks. Therefore, we considered Sickness and

Accidents as one single line that we named Health. Fire and Other property damages lines

were combined in an aggregate that we called Property. The aggregate we named Liability

contains Motor and other third-party liability lines, Transportation incorporates any kind of

vehicles and transported goods damage lines, while the Other set includes Legal expenses and

Assistance insurance, Financial losses, Credit, Suretyship.

If a company collects premiums in more than one single aggregate, we consider it to

be diversified and the dummy variable that checks for that (Diversified_Dummy) takes a value

of 1. If an insurer’s premium collection activity belongs to one aggregate only, we consider

the company to be specialized and the Diversified_Dummy variable value equals to zero.

The literature provides contrasting evidence on diversification impact on profitability:

while Cummins30 and Liebenberg and Sommer31 among others show that diversification

penalizes performance, Elango and Pope32 reaches the opposite conclusion. We want to

include diversification in our model in order to avoid misspecification problems, but we do

not have a definite expectation for its impact on our dependent variables.

30 Cummins et al. (2010). 31 Liebenberg and Sommer (2007). 32 Elango and Pope (2008)

18

As mentioned, we also included in the multivariate analysis model as additional

controls: the company size and age, its leverage and the weight of its passive reinsurance

activity. We also analyse these variables to compare their value in our two subsamples.

As for size we estimated it by using the Size_Assets variable i.e. the natural logarithm

of each firms’ total assets.

Past empirical analysis concludes that economies of scale are relevant in the P&C

insurance business33. If that is the case, we should find a positive coefficient for the size

variable. In the descriptive analysis, we also measured size with the Size_Premiums variable,

measured as the logarithm of gross written premiums. The Size_Assets variable can be

influenced by product mix as total assets of those insurers that cover big risks are increased by

technical reserves’ size and age while the Size_Premiums variable measures the company’s

size without considering its process of claims repayment. On the other hand, measuring size

by using premiums written might bias our regression results because size would correspond to

a log-transformation of the denominator of our dependent variable in the ROS case.

As for age, we single out recently created insurers by building a dummy variable

named Startup_Dummy which equals 1 if the insurer’s age is lower than 4 years. We expect a

negative coefficient sign as some time is needed for the company to establish itself in the

market.

We measured leverage (Leverage variable) by dividing the company total assets less

equity over total assets. The higher the company’s leverage the lower its capitalization. A

higher leverage benefits the company’s shareholders because, given a certain level of

operating performance, their investment in the company decreases. At the same time, a lower

33 see Praetz (1985) for a survey of the literature on the topic and also Cummins and Nini (2002), Liebenberg and Sommer (2008).

19

leverage increases the insurer’s financial strength and capability of absorbing losses. This in

turn might allow the insurer to charge higher premiums. Moreover, a lower leverage increases

the flexibility of the company investment activity because of solvency regulation and

consequently might increase profitability through this channel. The literature shows a

negative relationship between leverage and shareholders’ profitability34, and we do not have

reasons to expect a different sign in our case.

The influence of Leverage on ROS is more uncertain, because if the increased

profitability due to a lower leverage comes from the ability to charge higher premiums, this

effect influences both the numerator and the denominator of the ratio in the same direction.

Last, we include a measure of passive reinsurance activity among our controls

(Reinsurance ratio_Premiums). Reinsurance ratio_Premiums is calculated by dividing

premiums transferred to reinsurers over gross premiums written. Reinsurance is an efficient

risk management device for non-life insurers as it helps to reduce the risks portfolio

variability and to smooth losses. The level of reinsurance depends on business line

composition, as in certain risk classes risk transfer through reinsurance is highly used. For

Cummins35 reinsurance significantly increases insurers’ costs but significantly reduces loss

ratio volatility. According to Chen-Ying36 firm performance is positively related to

reinsurance utilization while Cummins37 finds a performance penalty for reinsurance

concentration. Therefore we do not have precise expectations for the coefficient sign of this

variable as passive reinsurance can be used by poor risk managers in order to compensate

inadequate selection skills and increase their profitability but, on the other hand, passive

34 Cummins and Nini (2002) and Chen-Ying (2014) among others. 35 Cummins et al. (2008). 36 Chen-Ying (2014). 37 Cummins et al. (2012).

20

reinsurance entails transaction costs due to information asymmetry that might be passed on

the transferring insurer, decreasing its performance.

We also note that reinsurance can have a tax planning purpose38. However, while

domestic tax avoidance within insurance groups comprising several P&C companies can be

obtained by exploiting the transfer of losses between taxable and non-taxable insurers, it is

impossible to attain when only one P&C firm operates within the group (as it is the case for

our bank-affiliated players).

Therefore, at a descriptive level, we do not have definite expectations. Bank affiliated

insurers might use passive insurance to avoid managing risks whose quality they might not be

sure about, but in bank affiliated insurers’ case reinsurance is not a tool to lower the

consolidated tax base, which might be the case for traditional insurers. Table 1 below

summarizes variables names, definitions and coefficients expected sign.

Table 1 Variables names, definitions and coefficients expected sign.

38 OECD (2001).

21

22

3.2.2. The sample

In order to perform our analysis, we collected data from a sample comprising all

Italian P&C insurance companies operating in the country during the 2005-2015 timeframe.

According to OECD numbers, Italy occupies the fourth place in Europe in 2015 for

non-life premiums written, making the Italian market deserving of an analysis of its own.

Distribution through banks of both life and non-life policies is an established reality and, even

if the non-life market penetration by banks is still limited – 7,2% of gross premiums written in

2015 excluding the motor third party liability business and 4% of total non-life gross

premiums written were sold through bank branches – banks’ market share is growing39. In

Italy, tied agents dominate the sale of non-life policies. However, the agents’ high fees make

the entrance in this industry attractive for players such as banks, which on paper should be

able to take advantage of current distribution inefficiencies.

Our starting sample included all non-life insurance companies headquartered in Italy,

associated to ANIA40, and operating during the 2005-2015, period, and whose financial

statements data are included in the ANIA database named Infobila.

Adopting Leech41’s threshold for identifying the minimum stake needed to influence

corporate policy, we consider an insurer to be bank-affiliated if one or more banks own at

least 20% of its equity. We label as traditional insurers the following entities: independent

companies, firms owned by other insurers, firms whose equity is participated by banks but

banks’ stake is lower than 20%.

39 Insurance Europe (2016). 40 Italian insurance association. 41 Leech (2002).

23

Information regarding insurers’ ownership structure comes from the database “Orbis”,

maintained by Bureau Van Dijk. When needed, the data were completed and integrated with

information coming from insurers’ web sites and original annual reports.

We excluded from our initial sample companies that either did not write premiums or

started their writing activity during the year. We also excluded observations pertaining to the

non-life insurance company controlled by the Italian Postal Service because of the

heterogeneous nature of its owner. Our final sample includes pure non-life companies and

companies also operating in the life business. - before 1979 operating in both life and non-life

insurance was possible and companies created before that year that were allowed to do so kept

the privilege. However, as for the latter, we only consider their non-life business in the

analysis.

In our final sample there are 25 bank-affiliated insurers and 90 traditional insurance

companies. Over time, some insurers change their “status” becoming bank-affiliated from

being traditional ones due to the establishment of joint ventures with banks or due to

acquisitions performed by banks. On the other hand, some bank-affiliated insurers become

traditional companies following a reduction or a cut of the equity links between the

participated insurer and its banking stockholders.

Our final sample includes 949 company-year level observations, of which 208 pertain

to the bank-affiliated subsample and 741 to the traditional insurers subsample.

From a descriptive point of view, our sample provides a good picture of the Italian

non-life insurance industry. Comparing the total amount of gross premiums written by

companies included in our sample with the Italian insurance regulator (IVASS) aggregate data

that covering the entire market, we reckon that companies included in our analysis collected

on average 90% of gross premiums written in Italy.

24

4. Descriptive analysis

In this paragraph we show the results of a descriptive analysis that compares bank-

affiliated insurers to traditional ones to single out differences (if any) in performance and

operations.

We divide our sample into two subsamples, according to the insurer’s affiliation, summarize

our variables for each subsample and test for differences.

In general, the number of bank-affiliated insurers and their market share, calculated as

the percentage of total gross premium written in our sample, did not change during our

timeframe. On the other hand, as one can notice from Figure 1, traditional insurers face a

gradual consolidation over time, their number steadily decreasing.

Figure 1 Percentage of premiums written and number of insurers (subsamples)

25

Figure 2 shows the product mix of the two subsamples, calculated by averaging the

percentage of gross premium written in each risk aggregate over total gross premiums in each

subsample during the period of time we analyse different customers/risk classes targeted by

bank-affiliated and traditional insurers is mirrored in the subsamples product mix

composition. Bank-affiliated companies are more active in the Health lines of business (24%

of gross premium written vs 14% for traditional insurers) and in the Other risks (13% vs 5%

for traditional insurers). The latter result is possibly linked to the fact that a fair share of the

policies included in the Other aggregate are attached to loans and bank-affiliated insurers have

a competitive advantage over traditional ones in this arena. The percentage of premiums

collected in the Property business is similar to traditional insurers (16% vs 14%) while bank-

affiliated companies show a lower involvement in the Liability business (41% vs 58%) and in

the Transportation business (6% vs 10%).

Figure 2 Product mix: bank-affiliated and traditional insurers

26

Product mix choice depends on targeted customers but has an impact on costs and

claims ratios. Therefore, the specific features of the lines probably influence positioning

decisions as well, especially for new entrants. As shown in Figure 3, risk lines featuring a

higher average loss ratio show a higher efficiency as well. On average, the table shows a

negative correlation between the average loss ratio and the average cost ratio, with bank-

affiliated insurers positioning their products where costs are higher and loss ratios are lower

(and claims possibly less difficult to manage). The most profitable risk classes (the ones

showing the lower “combined ratio”, which is the sum of the loss and cost ratios) on average

are Health, Property and Other risk lines. The share of these business lines in the bank-

affiliated insurers product mix is higher than their weight in traditional insurers product mix.

Figure 3 Average Loss ratio, Cost ratio and Combined ratio for various business lines (whole

sample)

27

If we analyse the average cost ratio and the average loss ratio over different business

lines for the two subsamples separately, we find that bank-affiliated insurers’ loss ratio is on

average markedly lower than traditional insurers’ where bank-affiliated insurers’ product mix

is concentrated. However, average loss ratios in the Transportation and Liability business

lines are higher than average loss ratios for traditional insurers covering the same risks

(Figure 4).

Figure 4 Average Loss ratio for various business lines (subsamples)

Two contrasting stories might explain that. On one hand, bank- affiliated insurers

might be able to exploit a competitive advantage in selecting and managing risks in the

business lines they mainly target - possibly profiting from information on the policy holders

coming from their controlling bank. Except for motor insurance, Transportation and Liability

business lines policies are mainly sold to corporate customers and professionals and brokers

representing customers are one of the main distribution channel: profiting from economies of

scope might be more difficult (even though banks also lend money to corporate customers).

28

On the other hand, bank-affiliated insurers might either enact a claims repayment

strategy that is more penalizing for the policy beneficiary than the one traditional insurers

apply given the amount of premium charged. According to FSA42 this case seems to have

applied to PPI policies in the UK. In 2014 the Italian supervisor conducted a survey that

examined the PPI market in Italy43. The analysis compared PPIs with stand-alone policies

belonging to the same business line. While on average P&C policies costs differentials for

policyholders are not statistically different from zero when the analysis breaks down costs by

distributors, the findings suggest that PPI policies sold by banks are more expensive than

analogous stand-alone ones.44 Unfortunately, we do not have direct information on the

amount of PPI premiums collected by insurers in our sample. However, employing data from

the cited survey (limited to 2014), a conservative back of the envelope calculation allows us

to reckon that in our sample, in 2014, 2% of total P&C premiums collected belonged to PPIs

and that 15,4% of the premiums collected in the Other business lines were PPI policies

premiums. As mentioned above, bank affiliate insurers disproportionately collect premiums in

this business line. In 2014 theirs were 5,5% of the total P&C premiums of our sample and

16,2% of the Other business lines premiums.

The analysis of the cost ratio might shed some light on this. If bank-affiliated insurers

are less efficient than traditional insurers and are able to transfer their higher costs to

policyholders through higher prices we could partly explain their lower loss ratio. The data

show that bank-affiliated insurers are less efficient than traditional ones in the very business

lines they favour – and where they thrive (Figure 4 and Figure 5). This might be due to higher

selection costs that allow banks to cherry pick and avoid risky customers (which is consistent

42 FSA (2012). 43 IVASS (2016). 44 This finding might be due to PPI life policies sold by banks having higher costs than similar stand-alone products and not to P&C products sold by banks. IVASS (2016) do not provide evidence that allow us to disentangle this effect from the distribution channel one.

29

with a low loss ratio). However, we wonder why this selection cost story works for some

business lines but not for others.

Figure 5 Average Cost ratio for various business lines (subsamples)

Figure 6 Average Combined ratio for various business lines (subsamples)

30

Higher costs could be due to bank-affiliated insurers’ average size. If on average bank-

affiliated insurers are smaller than traditional insurers - which is what we found in the data -

bank-affiliated insurers might be prevented from exploiting economies of scale. However, a

smaller size should impair these companies’ ability at selecting risks as well, which is not

what data regarding the average loss ratio suggest. On the other hand, banks asking higher

fees than the ones paid by traditional insurers to distribute their policies through other means

could give a reason for the relative average inefficiency we see in the data. This explanation is

consistent with a low loss ratio (due to higher premiums charged) and with the fact that bank-

affiliated insurers’ lower average efficiency is limited to the risk lines where distribution

through banks is relatively more popular45 and banks presumably have a higher bargaining

power.

At this stage we do not have enough evidence to discard any of the above explanations

as insurance firms accounting data on single business lines are not as detailed as the available

information on the aggregate P&C activity that we will present in the following paragraphs.

However, we intend to explore the issue in our future research.

Table 2 contains the descriptive statistics referred to our sample companies’ activity

for the whole P&C industry, broken down to single subsamples. Table 2 includes the results

of differences in means testing. As a robustness check, we also tested the difference in means

after standardizing our variables in order to discard outliers. The results these checks are

depicted in Table 3.

Table 2 Descriptive statistics, subsamples

45 see ANIA (2017)

31

The definitions of the variables can be found in Table 1.

*Significant at 0.10 level; **significant at 0.05 level; *** significant at 0.01 level

Table 3 Descriptive statistics, difference in means test after variable standardization,

subsamples

32

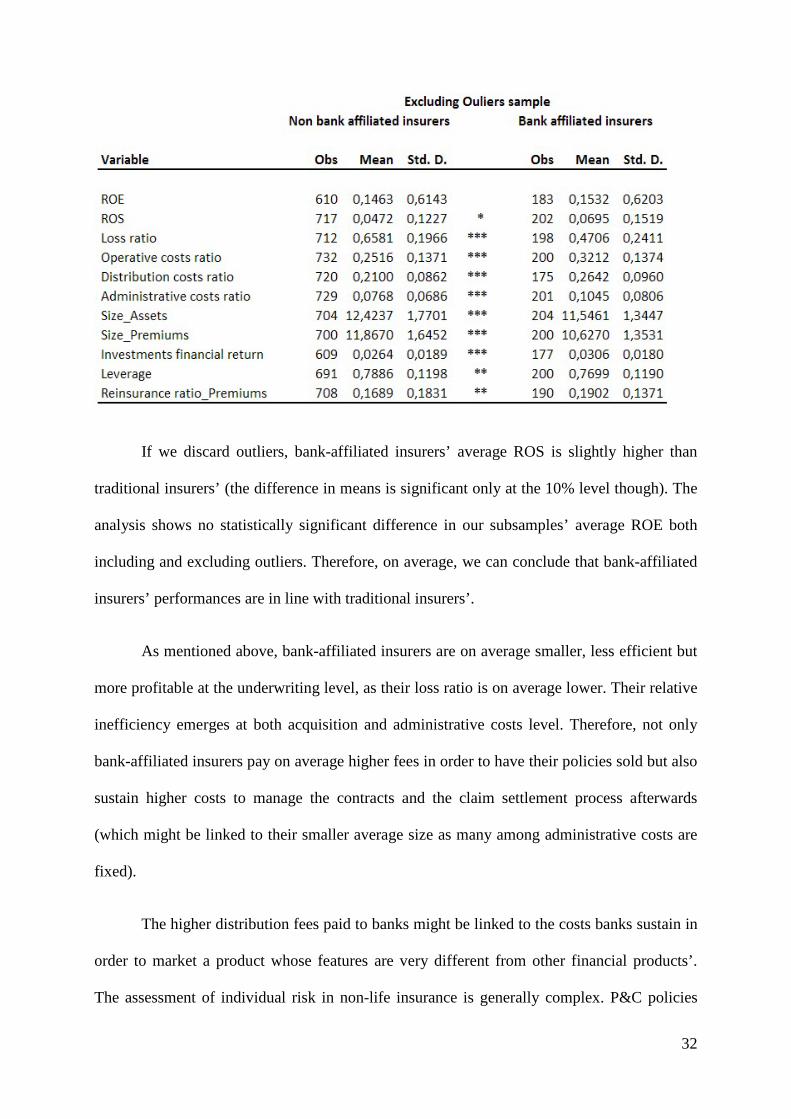

If we discard outliers, bank-affiliated insurers’ average ROS is slightly higher than

traditional insurers’ (the difference in means is significant only at the 10% level though). The

analysis shows no statistically significant difference in our subsamples’ average ROE both

including and excluding outliers. Therefore, on average, we can conclude that bank-affiliated

insurers’ performances are in line with traditional insurers’.

As mentioned above, bank-affiliated insurers are on average smaller, less efficient but

more profitable at the underwriting level, as their loss ratio is on average lower. Their relative

inefficiency emerges at both acquisition and administrative costs level. Therefore, not only

bank-affiliated insurers pay on average higher fees in order to have their policies sold but also

sustain higher costs to manage the contracts and the claim settlement process afterwards

(which might be linked to their smaller average size as many among administrative costs are

fixed).

The higher distribution fees paid to banks might be linked to the costs banks sustain in

order to market a product whose features are very different from other financial products’.

The assessment of individual risk in non-life insurance is generally complex. P&C policies

33

usually include multiple provisions to prevent policyholders’ moral hazard and bundle several

indemnities and defence coverages in a single contract, making products more difficult to

both understand and sell.

Returns from investments are on average higher for bank-affiliated insurers, possibly

due to their lower average leverage - the difference in means is significant only if we discard

outliers though- that partly free them from reserve coverage regulation. They might also

benefit from being part of a financial conglomerate. However, given that P&C policies

involve great uncertainty, non-life insurers tend to invest in assets subject to lower risk. Since

the timing of P&C claim payments is less predictable, insurance companies also tend to invest

in more liquid assets, featuring shorter maturity, in order to minimize interest rate sensitivity.

Therefore, the superior asset management ability a bank-affiliated insurer might have access

to thanks to its links with the bank might not express its benefits due to the limited range of

investible asset classes.

Bank-affiliated insurers also show a more intensive use of passive reinsurance. The

above result partly contradicts the reasoning that a higher selection ability might explain

lower loss ratios unless we assume that on average bank-affiliated insurers are systematically

able to transfer the worse part of their portfolios to reinsurers.

34

4. Regression Analysis

After performing the above descriptive analysis, we test our model over the entire

timeframe on our sample using three different specifications to include age and portfolio

diversification separately as we want to single out their influence on the insurers’

performance. We obtain our results running a fixed effect panel regression where time effects

are isolated using year dummies. As mentioned, we perform a Hausman test (not reported for

brevity) to choose between a fixed and a random effect panel regression.

Table 4 contains the descriptive statistics for the variables we included in our model.

Slightly more than a fifth of our observations belong to bank-affiliated insurers while the

rest pertain to traditional companies. A few (4%) among our observations belong to

companies whose age is less than four years, which we consider the minimum time needed to

establish their name in the market. Most firms in our sample (87%) operate in different risk

lines.

Our sample firms’ Loss ratio is on average less than one and the average combined ratio,

calculated by adding the Loss ratio and the Operative costs ratio is 0,91 implying that, on

average, firms belonging to our sample are profitable from an underwriting point of view. The

latter variables show a high variance though. As for the Loss ratio, the minimum value is

negative, due to a positive impact of the change in the claims reserve. The minimum value of

the Operative costs ratio is also negative, due to fees coming from reinsurers.

35

The Reinsurance ratio_Premiums variable shows a very high variance too. Its median

value (0,11) is lower than the average, and the probability mass is concentrated in the tails of

the distribution (kurtosis 3,62), implying that most of our sample insurers either take strong

advantage of passive reinsurance or tend not to use it. The correlation of the variable with its

lagged value shows that the use of passive reinsurance tend to be systematic (correlation is

positive and close to 1, 0,9137)

Table 4

Sample descriptive statistics

Tables 5 contains the coefficients of our model variables regressed on ROE while Table 6

depicts the impact of our variables on ROS.

36

We present results for both ROE and ROS instead of ROA. We consider ROS a better

measure of operating performance due to the features of our sample.

Yearly premium writing activity is not necessarily linked to equity or asset size. The

company equity depends on both its history – its past earnings, dividend distribution policy

and equity issuance activity - and the rules that set minimum capitalization requirements.

Asset size is also dependent on the company history, because even if the length of P&C

policies is short, in Italy some of them last up to five years. Moreover, policies belonging to

some business lines include loss occurrence clauses that entitle policyholders to ask for

refunds after maturity, provided that the event covered had happened while the policy was in

place. Therefore, even after maturity the insurer has an obligation to provision that increases

its assets. As a result, small firms from an equity/asset point of view might still be able to

collect a sizable amount of premiums.

Our results show that, irrespective of the performance measure we employ, the bank

affiliation variable coefficient has always a negative sign and it is always significant.

37

Table 5:

Regression results: Return on sales

38

Table 6:

Regression results: Return on equity

39

Therefore, being bank-affiliated places a negative weight on the insurer performance.

Other variables’ coefficients have the expected signs and most of them are highly significant.

As expected, the loss ratio has a significant and strong impact both on shareholders’

return and on operative returns. Its coefficient sign is negative as it was expected. Given the

premiums level, the higher the claims that the insurer has paid during the year and the claims

the company is expecting to pay in the future, the lower the underwriting activity profitability.

The investments financial return variable coefficient shows the expected positive sign

and is highly significant as well. Even if the P&C insurers’ investing activity is constrained by

the short-term maturity of their liabilities – and therefore we expected a low variance in the

returns which was not found in our data - the economic impact of the results coming from it

are strong as the size of the coefficient in both regression shows.

To ascertain costs impact on insurers performance, in our specifications we used the

comprehensive variable operative costs ratio, which considers both distribution and

administrative costs. It has the expected signs in both models, but its significance is stronger

in the ROS model, in all specifications, than in the ROE model – where the variable

coefficients are not statistically different from zero. If inefficient insurers are able to transfer

at least in part their costs to policyholders via increased premiums, the negative effect of their

higher expenses on earnings (and consequently on ROE) is softened as a result. On the other

hand, cost transfer activity influences the return on sales performance measure anyway,

because the value of premiums that the insurers need to collect in order to generate 1

monetary unit of earnings becomes higher.

In the regressions, we measured size as the natural logarithm of total assets. We discarded

the premiums measure of size because of its mathematical link with the denominator of the

40

ROS measure, which could bias our results. Size shows a positive and significant coefficient,

highlighting the presence of economies of scale.

The leverage variable coefficient is negative in both models. It is highly significant for

ROE, as it directly influences shareholders’ profitability. The investment of free capital,

which might increase final profits, seems to prevail in influencing ROE levels. As said before,

the impact of leverage on ROS might be more nuanced if leverage affects premiums as well

as economic results: safer - i.e. less levered - insurers might command higher premiums.

However, when we single out younger firms – which are less levered because of binding

minimum capital requirements - by adding the d_startup variable to the analysis, the impact

of leverage becomes highly significant even for ROS.

The Reinsurance ratio_Premiums is negative in both regressions, independent of the

model specifications. However, its coefficient is never statistically different from zero and we

cannot conclude that a higher use of passive reinsurance is per se detrimental to performance.

Being a startup is a disadvantage for performance in both models while diversification

shows no influence on operative returns. However, our measure of diversification might not

be able to fully capture its influence on results. A more detailed analysis of this topic will be

the object of future research.

6. Conclusions

41

While investigating the P&C insurers’ point of view, our results are consistent with some

of the few previous studies attesting little or absent advantages for banks’ entrance in non-life

business such as Lown46 and Nurullah and Staikouras47.

Opposite to what academic literature found in the life insurance business, where bank-

affiliated players are among the biggest and most profitable, bank-affiliated P&C insurers’

operations seem, for the moment, constrained on a limited portion of the market, in terms of

both line of business and customers.

Our results suggest that bank affiliation per se seem to be counterproductive.

Even though in theory having access to banks’ customers could help these insurers’

growth and profitability, this potential is still to become effective also due to some hurdles

that it will be difficult to overcome even in the future. Cross selling non-life policies is more

difficult for banks than selling life products. Conflicts arising from claims repayment in the

short term can have an impact on customer’ relations, which might entail negative

consequences on the sale of other core financial products. Lacking appropriate incentives,

bank sales representatives might not be willing to put their reputation (and bonus) at risk.

Our data show that bank-affiliated insurers pay higher distribution costs, presumably

shifting profits to banks through fees. They also have a higher underwriting profitability than

traditional insurers. Our evidence suggest that this might be linked more to costs transfers to

policyholders than to selection ability, as bank-affiliated insurers show a more intensive use

of passive reinsurance, which suggests poorer risk management skills.

Our analysis has some limitations that we hope to address in future research. Our sample

is restricted to Italy. A more detailed investigation of insurers’ riskiness could help enhance

46 Lown et al. (2000). 47 Nurullah and Staikouras (2008).

42

the explanatory power of our model - especially when return on shareholders’ investments is

concerned. Moreover, bank-affiliated insurers’ position need further analysis at single

business line level in order to corroborate our results.

References

ANIA (2017) Premi trimestrali danni, Trends, various issues

Artikis P.G., Mutenga S. and Staikouras S.K. (2008) ‘A practical approach to blend insurance

in the banking network’. The Journal of Risk Finance, 9(2): 106-124.

Ashton J. K., Hudson R. S. (2017) ‘The price, quality and distribution of mortgage payment

protection insurance: a hedonic pricing approach’ British Accounting Review, 49(2):

242-255.

Ashton J. K., Hudson R. S. (2014) ‘Do lenders cross-subsidise loans by selling payment

protection insurance?’ International Journal of the Economics of Business, 21(1): 121-

138.

Barth M.M. and D.L. Eckles (2009), ‘An empirical investigation of the effect of growth on

short-term changes in loss ratios’, Journal of Risk and Insurance, 76(4): 867-885.

Berger, A.N., J.D. Cummins and M. Weiss (1997) ‘The Coexistence of Multiple distribution

systems for financial services: the case of property liability insurance’, Journal of

Business, 70(4): 515-546.

43

Bonafede A. and L. Dell’Olio (2017) ‘Sorpresa: Intesa è già adesso la prima assicurazione

italiana’, La Repubblica, 2nd of October

Boyd, J.H., S.L. Graham and R.S. Hewitt (1993) ‘Bank holding company mergers with non-

bank financial firms: Effects on the risk of failure’, Journal of Banking and Finance,

17(1): 43-63

Burchardt T., Hill J. (1998) ‘From public to private: the case of mortgage payment insurance

in Great Britain.’ Housing Studies”, 3(3): 311-323.

Cetif Università Cattolica di Milano (2013) Rapporto di Ricerca su Innovazione nella

distribuzione di polizze vita e danni per casse di risparmio, banche popolari e banche

piccole: fra servizio al cliente e redditività, from http://www.cetif.it

Chang P. R., Peng J. L. and Fan C.K. (2011) ‘A comparison of Bancassurance and traditional

insurer sales channels’, The Geneva Papers, 36:.76-93.

Chen-Ying L. (2014) ‘The Effects of Firm Specific Factors and Macroeconomics on

Profitability of Property-liability Insurance Industry in Taiwan’, Asian Economic and

Financial Review, 4(5): 681-691

Cummins, J. D., Nini G. (2002) ‘Optimal capital utilization by financial firms: evidence from

the property-liability insurance industry’, Journal of Financial Services Research, 21:

15-53.

Cummins J. D., Dionne G., Gagné R., Nouira A. (2008) The Costs and Benefits of

Reinsurance. working paper, HEC, Montreal (Canada).

44

Cummins J.D., M. Weiss, X. Xie, H. Zi (2010) ‘Economies of Scope in financial services: A

DEA efficiency analysis of the US insurance industry’, Journal of Banking and

Finance, 34(7): 1525-1539.

Cummins J.D., Feng Z., Weiss M.A. (2012) Reinsurance Counterparty Relationships and

Firm Performance in the U.S. Property-Liability Insurance Industry, working paper

from http://ssrn.com/abstract=1997444

Elango B., Ma Y.L. and Pope N. (2008), ‘An investigation into the diversification–

performance relationship in the U.S. property–liability insurance industry’, The

Journal of Risk and Insurance, 75(3): 567-591.

Ellis P.M. (1998), ‘The nature of the loss ratio in property-casualty insurance’, Journal of

insurance issues, 21(1): 46-62.

Elyasiani E., S.K. Stailouras, P. Dontis-Charitos (2015) ‘Cross-industry prpoduct

diversification and contagion in risk and return: the case of Bank Insurance and

insurance bank takeovers’, The Journal of Risk and Insurance, 83(3): 681-718.

Etgar M. (1977) ‘Cost Effectiveness in Insurance Distribution’, The Journal of Risk and

Insurance, 44(2): 211-222.

Fiordelisi F., Ricci O. (2011) ‘Bancassurance efficiency gains: evidence from the Italian

banking and insurance industries’ The European Journal of Finance, 17(9-10): 789-810

Fiordelisi F., Ricci O. (2012) Bancassurance in Europe, past, present and future. Palgrave

Macmillan Studies in Banking and Financial Institutions, London.

FSA Financial Services Authority (2012) Parliamentary Commission on Banking Standards.

Written evidence from the Financial Services Authority, available at

45

https://publications.parliament.uk/pa/jt201314/jtselect/jtpcbs/27/27ix_we_j12.htmKlot

zki U., N. Gatzert and B. Muestermann (2017) ‘The cost of life distribution in Europe’

The Geneva Paper, 42(2): 296-322

Insurance Europe (2016) European Insurance – Key Facts, available at

www.insuranceeurope.eu

IVASS (2016) PPI Payment protection insurance. Indagine sulle polizze abbinate ai

finanziamenti: premi, caricamenti e provvigioni, available at

https://www.ivass.it/pubblicazioni-e-statistiche/pubblicazioni/altre-

pubblicazioni/2016/report-ppi/index.html

Leech D. (2002) ‘Shareholders’ Voting Power and Ownership Control of Companies’ Homo

Oeconomicus, 19(3): 345-373.

Liang H.Y., Ching Y.P. (2015) ‘Suggestions for Bancassurance Markets in China:

Implications from European Countries’, The Geneva Papers, 40: 279-294.

Liebenberg A. P., Sommer D. W. (2008), ‘Effects of corporate diversification: evidence from

the property–liability insurance industry’, The Journal of Risk and Insurance, 75(4):

893-919.

Lown, C. S., C.L. Osler, A. Sufi and P.E. Strahan (2000). ‘The Changing Landscape of the

Financial Services Industry: What Lies Ahead’, FRB of New York Economic Policy

Review, 6(4): 9-55.

Meroni G. and D. Schiavi (2017) ‘Banche e mercato assicurativo, in Italia tre opzioni

strategiche’, Il Sole 24 ore, 5th July

46

Moro, O. and L. Anderloni (2014) ‘Non-life insurance economic performances – An

empirical investigation’, Journal of Economics and Management, 18: 159-177.

Nissim D. (2010) ‘Analysis and Valuation of Insurance Companies’. Columbia Business

School, Columbia University, CE|ASA (Center for Excellence in Accounting and

Security Analysis), Industry Study No. 2, November 30th, New York.

Nurullah M., Staikouras, S.K. (2008) ‘The separation of banking from insurance: evidence

from Europe’, Multinational Finance Journal, 12(3-4): 157-184.

Praetz P.D. (1985) ‘A Note on Economies of Scale in the United Kingdom Property Liability

Insurance Industry’, Journal of Risk and Insurance, 52(2)315-320,

Santomero, A. and E. Chung (1992) Evidence in support of broader bank powers, Cambridge

MA: Blackwell Publishers, pp 1-69

Spotorno L., Moro O. and Anderloni L. (2016) ‘Bank affiliation influence on life insurers’

performance before and after the financial crisis’, Journal of Economics and

Management, 26(4): 5-33.

Sreesha C. (2015) ‘Efficency of bancassurance channels - An evaluation of the performance

of public sector banks in India’, International Journal of Multidisciplinary Research

and Development; 2(2): 495-498.

Vander Vennet R. (2002) ‘Cost and profit efficiency of financial conglomerates and universal

banks in Europe’, Journal of Money, Credit and Banking, .34: 254-282.

Yildirim, H.S., S. Kwag, C.M. Collins (2006) ‘An examination of the equity market response

to the Gramm-Leach-Bliley Act across commercial banking, investment banking and

insurance firms’, Journal of Business, Finance and Accounting, 33(9-10): 1629-1649.