dndn cowen

39

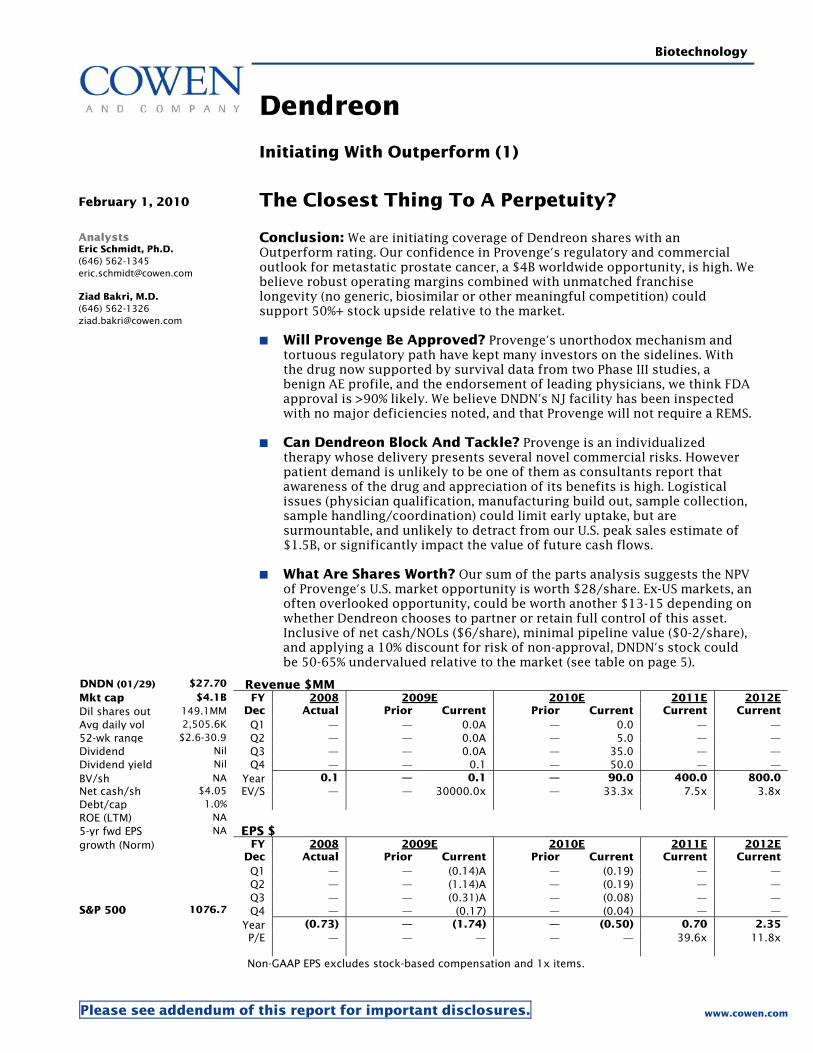

Biotechnology Dendreon Initiating With Outperform (1) February 1, 2010 The Closest Thing To A Perpetuity? Analysts Eric Schmidt, Ph.D. (646) 562-1345 [email protected] Ziad Bakri, M.D. (646) 562-1326 [email protected] Conclusion: We are initiating coverage of Dendreon shares with an Outperform rating. Our confidence in Provenge’s regulatory and commercial outlook for metastatic prostate cancer, a $4B worldwide opportunity, is high. We believe robust operating margins combined with unmatched franchise longevity (no generic, biosimilar or other meaningful competition) could support 50%+ stock upside relative to the market. ■ Will Provenge Be Approved? Provenge’s unorthodox mechanism and tortuous regulatory path have kept many investors on the sidelines. With the drug now supported by survival data from two Phase III studies, a benign AE profile, and the endorsement of leading physicians, we think FDA approval is >90% likely. We believe DNDN’s NJ facility has been inspected with no major deficiencies noted, and that Provenge will not require a REMS. ■ Can Dendreon Block And Tackle? Provenge is an individualized therapy whose delivery presents several novel commercial risks. However patient demand is unlikely to be one of them as consultants report that awareness of the drug and appreciation of its benefits is high. Logistical issues (physician qualification, manufacturing build out, sample collection, sample handling/coordination) could limit early uptake, but are surmountable, and unlikely to detract from our U.S. peak sales estimate of $1.5B, or significantly impact the value of future cash flows. ■ What Are Shares Worth? Our sum of the parts analysis suggests the NPV of Provenge’s U.S. market opportunity is worth $28/share. Ex-US markets, an often overlooked opportunity, could be worth another $13-15 depending on whether Dendreon chooses to partner or retain full control of this asset. Inclusive of net cash/NOLs ($6/share), minimal pipeline value ($0-2/share), and applying a 10% discount for risk of non-approval, DNDN’s stock could be 50-65% undervalued relative to the market (see table on page 5). DNDN (01/29) $27.70 Revenue $MM Mkt cap $4.1B FY 2008 2009E 2010E 2011E 2012E Dil shares out 149.1MM Dec Actual Prior Current Prior Current Current Current Avg daily vol 2,505.6K Q1 0.0A 0.0 52-wk range $2.6-30.9 Q2 0.0A 5.0 Dividend Nil Q3 0.0A 35.0 Dividend yield Nil Q4 0.1 50.0 BV/sh NA Year 0.1 0.1 90.0 400.0 800.0 Net cash/sh $4.05 EV/S 30000.0x 33.3x 7.5x 3.8x Debt/cap 1.0% ROE (LTM) NA 5-yr fwd EPS NA EPS $ FY 2008 2009E 2010E 2011E 2012E growth (Norm) Dec Actual Prior Current Prior Current Current Current Q1 (0.14)A (0.19) Q2 (1.14)A (0.19) Q3 (0.31)A (0.08) S&P 500 1076.7 Q4 (0.17) (0.04) Year (0.73) (1.74) (0.50) 0.70 2.35 P/E 39.6x 11.8x Non-GAAP EPS excludes stock-based compensation and 1x items. Please see addendum of this report for important disclosures. www.cowen.com

-

Upload

sgoldstein12 -

Category

Documents

-

view

5.458 -

download

3

Transcript of dndn cowen

Biotechnology

Dendreon

Initiating With Outperform (1)

February 1, 2010 The Closest Thing To A Perpetuity?

Analysts Eric Schmidt, Ph.D. (646) 562-1345 [email protected] Ziad Bakri, M.D. (646) 562-1326 [email protected]

Conclusion: We are initiating coverage of Dendreon shares with an Outperform rating. Our confidence in Provenge's regulatory and commercial outlook for metastatic prostate cancer, a $4B worldwide opportunity, is high. We believe robust operating margins combined with unmatched franchise longevity (no generic, biosimilar or other meaningful competition) could support 50%+ stock upside relative to the market.

■ Will Provenge Be Approved? Provenge's unorthodox mechanism and tortuous regulatory path have kept many investors on the sidelines. With the drug now supported by survival data from two Phase III studies, a benign AE profile, and the endorsement of leading physicians, we think FDA approval is >90% likely. We believe DNDN's NJ facility has been inspected with no major deficiencies noted, and that Provenge will not require a REMS.

■ Can Dendreon Block And Tackle? Provenge is an individualized therapy whose delivery presents several novel commercial risks. However patient demand is unlikely to be one of them as consultants report that awareness of the drug and appreciation of its benefits is high. Logistical issues (physician qualification, manufacturing build out, sample collection, sample handling/coordination) could limit early uptake, but are surmountable, and unlikely to detract from our U.S. peak sales estimate of $1.5B, or significantly impact the value of future cash flows.

■ What Are Shares Worth? Our sum of the parts analysis suggests the NPV of Provenge's U.S. market opportunity is worth $28/share. Ex-US markets, an often overlooked opportunity, could be worth another $13-15 depending on whether Dendreon chooses to partner or retain full control of this asset. Inclusive of net cash/NOLs ($6/share), minimal pipeline value ($0-2/share), and applying a 10% discount for risk of non-approval, DNDN's stock could be 50-65% undervalued relative to the market (see table on page 5).

DNDN (01/29) $27.70 Revenue $MMMkt cap $4.1B FY 2008 2009E 2010E 2011E 2012EDil shares out 149.1MM Dec Actual Prior Current Prior Current Current CurrentAvg daily vol 2,505.6K Q1 � � 0.0A � 0.0 � �52-wk range $2.6-30.9 Q2 � � 0.0A � 5.0 � �Dividend Nil Q3 � � 0.0A � 35.0 � �Dividend yield Nil Q4 � � 0.1 � 50.0 � �BV/sh NA Year 0.1 � 0.1 � 90.0 400.0 800.0Net cash/sh $4.05 EV/S � � 30000.0x � 33.3x 7.5x 3.8xDebt/cap 1.0% ROE (LTM) NA 5-yr fwd EPS NA EPS $

FY 2008 2009E 2010E 2011E 2012Egrowth (Norm) Dec Actual Prior Current Prior Current Current Current

Q1 � � (0.14)A � (0.19) � � Q2 � � (1.14)A � (0.19) � � Q3 � � (0.31)A � (0.08) � �S&P 500 1076.7 Q4 � � (0.17) � (0.04) � � Year (0.73) � (1.74) � (0.50) 0.70 2.35 P/E � � � � � 39.6x 11.8x Non-GAAP EPS excludes stock-based compensation and 1x items.

Please see addendum of this report for important disclosures. www.cowen.com

Dendreon

February 1, 2010 2

Provenge�s Revenge

Dendreon�s flagship product is Provenge, a personalized immunotherapy for late stage prostate cancer. Provenge has demonstrated the ability to prolong survival in two randomized controlled trials and is awaiting FDA approval in patients with metastatic castrate-resistant prostate cancer (CRPC), a potential $2B+ U.S. opportunity. The product has a PDUFA date of May 1, 2010.

Provenge�s trials and tribulations have provided a wild ride for investors. Despite marginal data from two initial Phase III studies, a March 2007 FDA advisory panel surprised the Street when it voted in favor of regulatory approval. Two months later, Provenge received a Complete Response letter from the FDA, essentially requesting confirmation of the drug�s survival benefit in a third ongoing (much larger, and prospectively designed) Phase III study, IMPACT. Provenge rapidly became the subject of a high profile public (and to some extent political) debate, when the FDA�s decision was criticized by patient advocacy groups and certain members of Congress. In April 2009, Provenge was back in the spotlight of the medical and investment communities when positive data from the 512-patient, SPA-sponsored IMPACT study were presented at the annual meeting of the American Urology Association. IMPACT demonstrated a 4-month improvement in median survival in patients treated with Provenge relative to placebo (p=0.032).

CRPC is the second-leading cause of cancer death in men, yet there remain few therapies to treat the condition. Taxotere chemotherapy has become the treatment choice for around 50% of patients with metastatic disease despite its harsh toxicity profile. Provenge has now succeeded in improving survival in men regardless of whether they are candidates for Taxotere. This survival advantage has come with a tolerability profile that could be better than that of any approved anticancer therapy. All signs suggest that Provenge is poised to transform the prostate cancer treatment paradigm.

Regulatory Risk Appears Low

Dendreon shares were among the best performers in biotech during 2009. Nonetheless, we believe Provenge�s tortuous development history and novel mechanism, and the reluctance of many investors to accept any FDA risk have kept many potential Dendreon shareholders on the sidelines pending approval. Based on our assessment of the evidence and discussions with many prostate cancer specialists, we conclude that Provenge is 90% or more likely to be approved in 2010. Factors that give us confidence around this catalyst include the positive survival data seen in two Phase III studies, Provenge�s benign safety profile relative to other cancer therapies, support from multiple thought-leading oncologists and the prior positive FDA panel vote. With Dendreon management gearing up its commercial efforts (district sales managers have been hired), it would appear that management�s confidence in FDA approval is also high. In this report, we also address specific aspects of investor concern, including: nuances around trial statistics and design; inconsistencies between the PFS and survival results; and the potential for CMC considerations to delay manufacturing approval. Importantly, we apply a 10% discount to our overall valuation of DNDN shares to reflect our 90% estimate for likelihood of FDA approval.

Dendreon

February 1, 2010 3

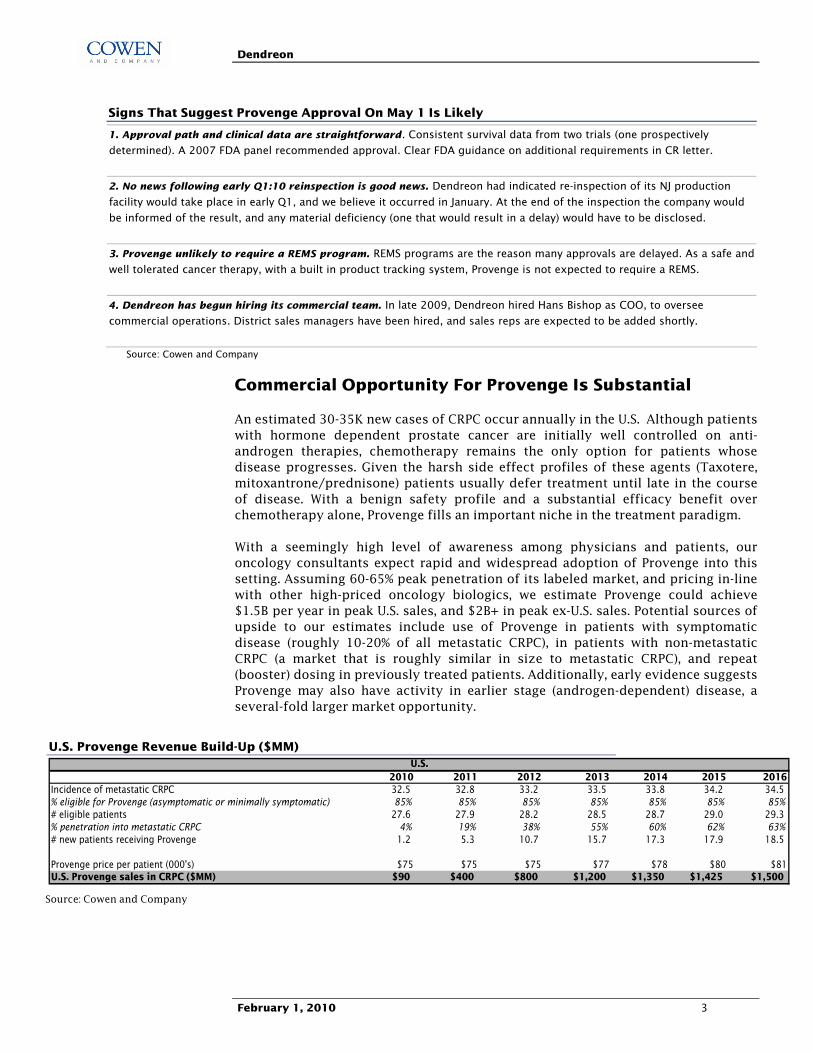

Signs That Suggest Provenge Approval On May 1 Is Likely

1. Approval path and clinical data are straightforward. Consistent survival data from two trials (one prospectively

determined). A 2007 FDA panel recommended approval. Clear FDA guidance on additional requirements in CR letter.

2. No news following early Q1:10 reinspection is good news. Dendreon had indicated re-inspection of its NJ production

facility would take place in early Q1, and we believe it occurred in January. At the end of the inspection the company would

be informed of the result, and any material deficiency (one that would result in a delay) would have to be disclosed.

3. Provenge unlikely to require a REMS program. REMS programs are the reason many approvals are delayed. As a safe and

well tolerated cancer therapy, with a built in product tracking system, Provenge is not expected to require a REMS.

4. Dendreon has begun hiring its commercial team. In late 2009, Dendreon hired Hans Bishop as COO, to oversee

commercial operations. District sales managers have been hired, and sales reps are expected to be added shortly.

Source: Cowen and Company

Commercial Opportunity For Provenge Is Substantial

An estimated 30-35K new cases of CRPC occur annually in the U.S. Although patients with hormone dependent prostate cancer are initially well controlled on anti-androgen therapies, chemotherapy remains the only option for patients whose disease progresses. Given the harsh side effect profiles of these agents (Taxotere, mitoxantrone/prednisone) patients usually defer treatment until late in the course of disease. With a benign safety profile and a substantial efficacy benefit over chemotherapy alone, Provenge fills an important niche in the treatment paradigm.

With a seemingly high level of awareness among physicians and patients, our oncology consultants expect rapid and widespread adoption of Provenge into this setting. Assuming 60-65% peak penetration of its labeled market, and pricing in-line with other high-priced oncology biologics, we estimate Provenge could achieve $1.5B per year in peak U.S. sales, and $2B+ in peak ex-U.S. sales. Potential sources of upside to our estimates include use of Provenge in patients with symptomatic disease (roughly 10-20% of all metastatic CRPC), in patients with non-metastatic CRPC (a market that is roughly similar in size to metastatic CRPC), and repeat (booster) dosing in previously treated patients. Additionally, early evidence suggests Provenge may also have activity in earlier stage (androgen-dependent) disease, a several-fold larger market opportunity.

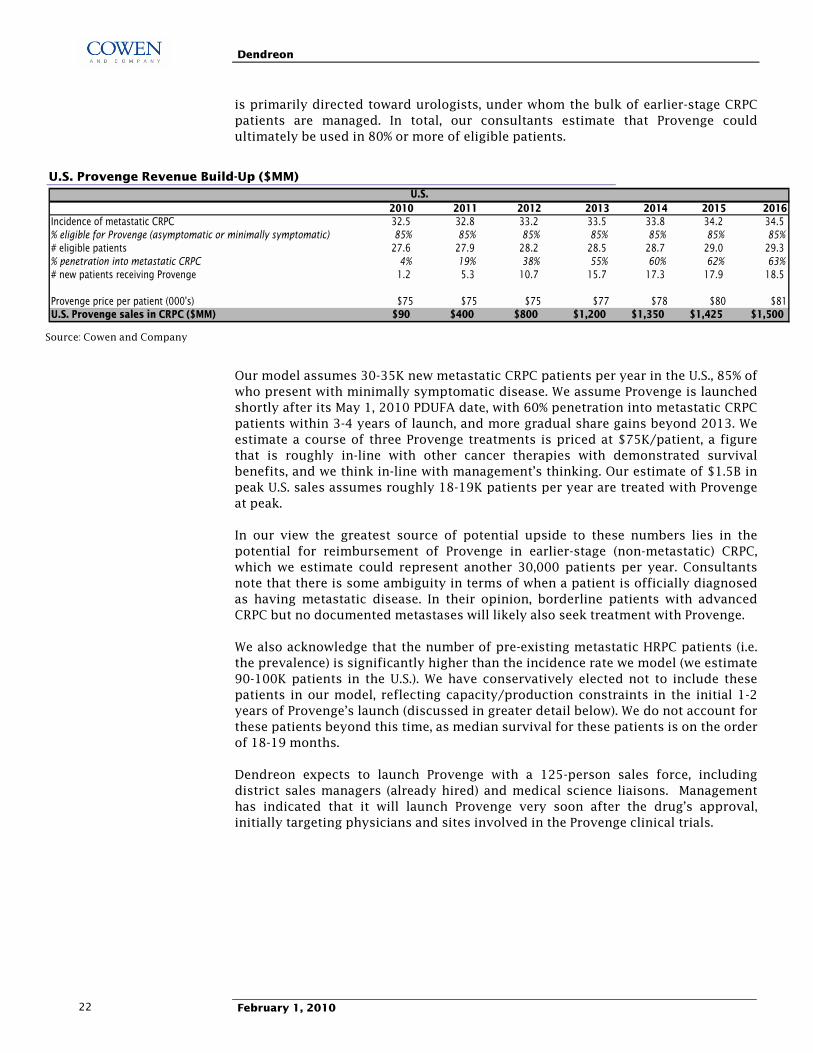

U.S. Provenge Revenue Build-Up ($MM)

2010 2011 2012 2013 2014 2015 2016Incidence of metastatic CRPC 32.5 32.8 33.2 33.5 33.8 34.2 34.5% eligible for Provenge (asymptomatic or minimally symptomatic) 85% 85% 85% 85% 85% 85% 85%# eligible patients 27.6 27.9 28.2 28.5 28.7 29.0 29.3% penetration into metastatic CRPC 4% 19% 38% 55% 60% 62% 63%# new patients receiving Provenge 1.2 5.3 10.7 15.7 17.3 17.9 18.5

Provenge price per patient (000's) $75 $75 $75 $77 $78 $80 $81U.S. Provenge sales in CRPC ($MM) $90 $400 $800 $1,200 $1,350 $1,425 $1,500

U.S.

Source: Cowen and Company

Dendreon

February 1, 2010 4

Execution Risk Is Real, But Unlikely To Detract From Peak Sales

Because Provenge is a personalized, cell-based therapy, its commercialization is considerably more challenging than that of a typical biotech product. While the process is relatively simple for patients (three initial blood collection procedures followed by three Provenge infusions over four weeks), a sequence of steps must be coordinated in advance of Provenge administration. First, the white blood cell sample must be collected at a leukapheresis center validated and contracted by Dendreon. This sample is then sent to a Provenge manufacturing facility, where the specific (dendritic) cells are separated, �activated�, and formulated into Provenge. Provenge must then undergo certain quality assurance measures before being reinfused to the patient. Using barcodes, the entire process will be trackable under a GPS-like system (�Intellivenge�).

In order to optimize Provenge�s sales potential, Dendreon will need to successfully navigate logistical issues such as physician and leukapheresis center qualification, sample collection, in-house manufacturing, and coordination by the different carriers. We are confident that all these hurdles are surmountable, as none of the individual steps in this process are particularly challenging, and the process has been navigated, albeit on a smaller scale, with high success rates in clinical trials. Dendreon will employ well-established service providers to perform key steps along the Provenge supply chain. As an example, Dendreon has contracted with the American Red Cross to provide leukapheresis services, and the company is working with couriers that are well-versed in transportation of medical products.

Lastly, Dendreon will need to complete build-out of its three manufacturing facilities to satisfy the likely very high level of demand for Provenge. Currently, Dendreon is operating with only 25% of its New Jersey facility, this portion of which Dendreon estimates is capable of producing between $125-250MM in yearly revenues. Clearly, in order to meet our sales estimates, Dendreon will need to successfully execute on the build-out, validation and inspection of its New Jersey (completion in H1:11), LA, and Atlanta facilities (providing additional capacity by mid-2011). The New Jersey facility has been successfully manufacturing clinical supply of Provenge since 2007. Management has indicated that the facility was to be reinspected early in Q1, and we believe the inspection likely took place in January. We expect that any material deficiency (one that could represent a delay to approval timelines) would have to be press released or published in an 8-K. Assuming NJ passes FDA muster, we see no reason why Dendreon cannot successfully scale up the process in this and other locations. Although manufacturing, logistical, training, or other access-related issues could always produce minor delays to expected timelines, such delays shouldn�t detract from the high level of patient-driven demand that drives our peak sales estimates, or substantially detract from our NPV-based estimates of Provenge�s value.

Sum-of-the-Parts Analysis Suggests DNDN Shares Have 50%+ Relative Upside

Provenge�s Longevity Is A Key Part Of The Equation

We employ a sum-of-the-parts methodology to value Dendreon, adding together the estimated NPV of each of Dendreon�s assets. In contrast to small molecule drugs, and even standard protein-based biologics, the barriers to creating a generic or

Dendreon

February 1, 2010 5

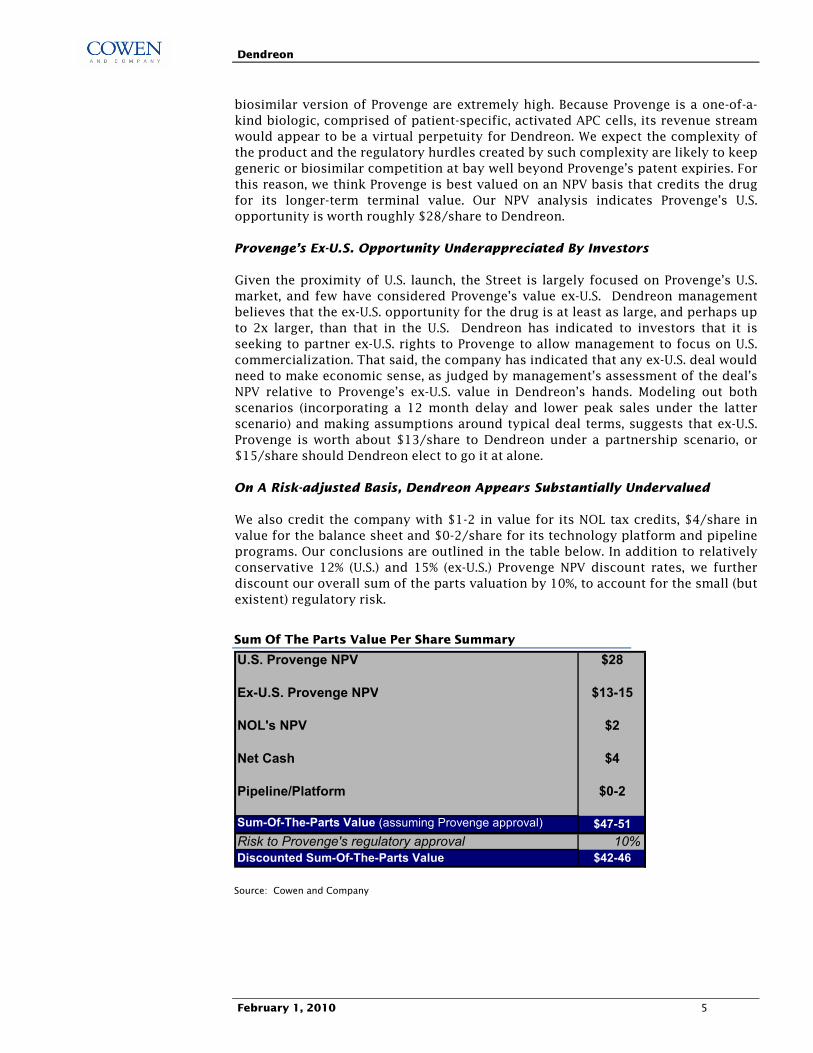

biosimilar version of Provenge are extremely high. Because Provenge is a one-of-a-kind biologic, comprised of patient-specific, activated APC cells, its revenue stream would appear to be a virtual perpetuity for Dendreon. We expect the complexity of the product and the regulatory hurdles created by such complexity are likely to keep generic or biosimilar competition at bay well beyond Provenge�s patent expiries. For this reason, we think Provenge is best valued on an NPV basis that credits the drug for its longer-term terminal value. Our NPV analysis indicates Provenge�s U.S. opportunity is worth roughly $28/share to Dendreon.

Provenge�s Ex-U.S. Opportunity Underappreciated By Investors

Given the proximity of U.S. launch, the Street is largely focused on Provenge�s U.S. market, and few have considered Provenge�s value ex-U.S. Dendreon management believes that the ex-U.S. opportunity for the drug is at least as large, and perhaps up to 2x larger, than that in the U.S. Dendreon has indicated to investors that it is seeking to partner ex-U.S. rights to Provenge to allow management to focus on U.S. commercialization. That said, the company has indicated that any ex-U.S. deal would need to make economic sense, as judged by management�s assessment of the deal�s NPV relative to Provenge�s ex-U.S. value in Dendreon�s hands. Modeling out both scenarios (incorporating a 12 month delay and lower peak sales under the latter scenario) and making assumptions around typical deal terms, suggests that ex-U.S. Provenge is worth about $13/share to Dendreon under a partnership scenario, or $15/share should Dendreon elect to go it at alone.

On A Risk-adjusted Basis, Dendreon Appears Substantially Undervalued

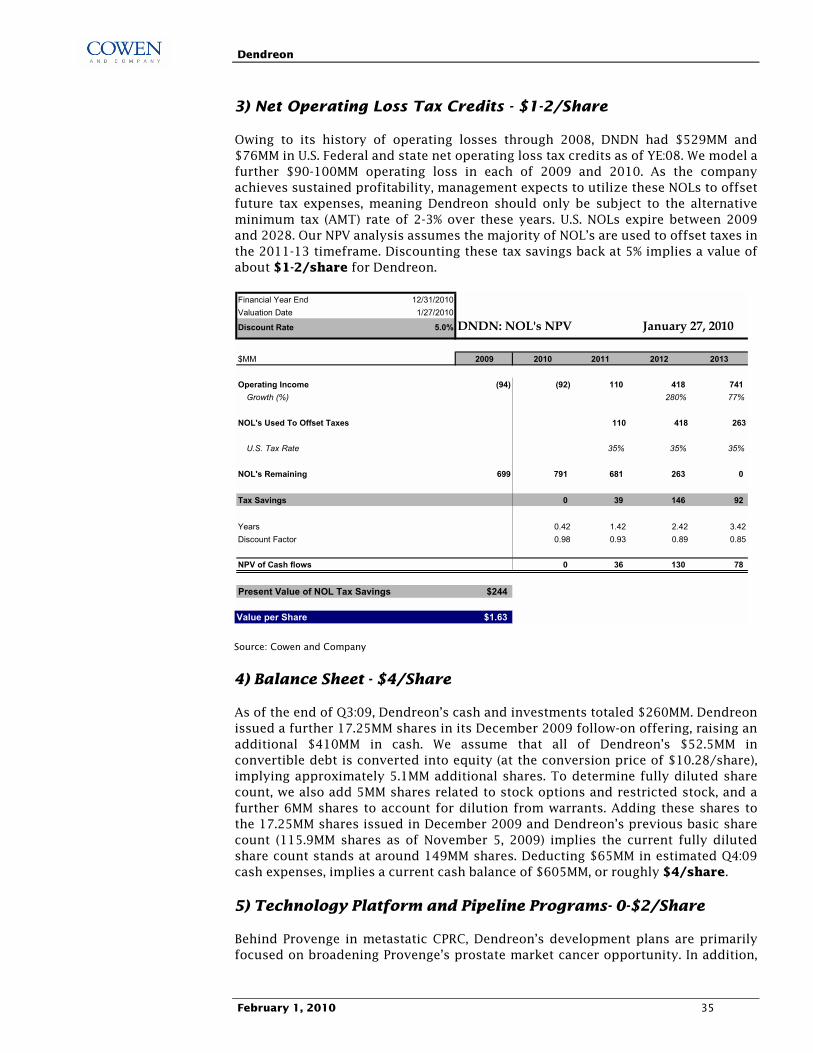

We also credit the company with $1-2 in value for its NOL tax credits, $4/share in value for the balance sheet and $0-2/share for its technology platform and pipeline programs. Our conclusions are outlined in the table below. In addition to relatively conservative 12% (U.S.) and 15% (ex-U.S.) Provenge NPV discount rates, we further discount our overall sum of the parts valuation by 10%, to account for the small (but existent) regulatory risk.

Sum Of The Parts Value Per Share Summary

U.S. Provenge NPV $28

Ex-U.S. Provenge NPV $13-15

NOL's NPV $2

Net Cash $4

Pipeline/Platform $0-2

Sum-Of-The-Parts Value (assuming Provenge approval) $47-51Risk to Provenge's regulatory approval 10%Discounted Sum-Of-The-Parts Value $42-46

Source: Cowen and Company

Dendreon

February 1, 2010 6

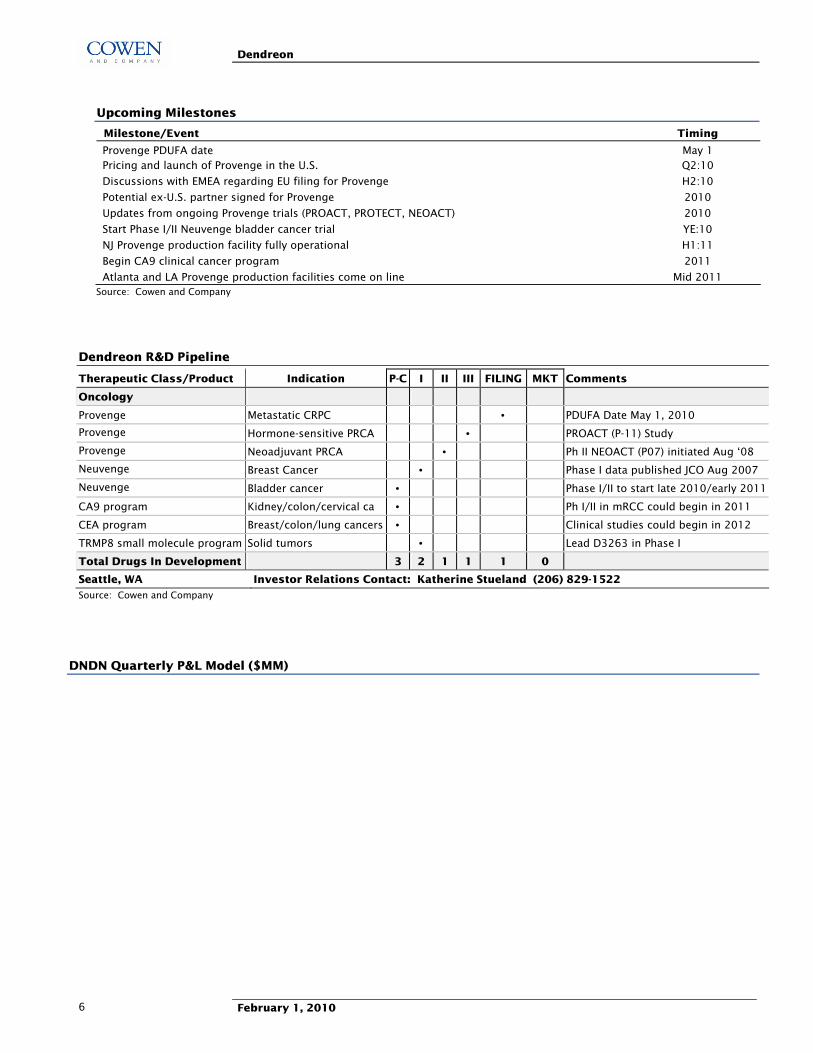

Upcoming Milestones

Milestone/Event Timing

Provenge PDUFA date May 1 Pricing and launch of Provenge in the U.S. Q2:10

Discussions with EMEA regarding EU filing for Provenge H2:10

Potential ex-U.S. partner signed for Provenge 2010

Updates from ongoing Provenge trials (PROACT, PROTECT, NEOACT) 2010

Start Phase I/II Neuvenge bladder cancer trial YE:10

NJ Provenge production facility fully operational H1:11

Begin CA9 clinical cancer program 2011

Atlanta and LA Provenge production facilities come on line Mid 2011 Source: Cowen and Company

Dendreon R&D Pipeline

Therapeutic Class/Product Indication P-C I II III FILING MKT Comments

Oncology

Provenge Metastatic CRPC • PDUFA Date May 1, 2010

Provenge Hormone-sensitive PRCA • PROACT (P-11) Study

Provenge Neoadjuvant PRCA • Ph II NEOACT (P07) initiated Aug �08

Neuvenge Breast Cancer • Phase I data published JCO Aug 2007

Neuvenge Bladder cancer • Phase I/II to start late 2010/early 2011

CA9 program Kidney/colon/cervical ca • Ph I/II in mRCC could begin in 2011

CEA program Breast/colon/lung cancers • Clinical studies could begin in 2012

TRMP8 small molecule program Solid tumors • Lead D3263 in Phase I

Total Drugs In Development 3 2 1 1 1 0

Seattle, WA Investor Relations Contact: Katherine Stueland (206) 829-1522

Source: Cowen and Company

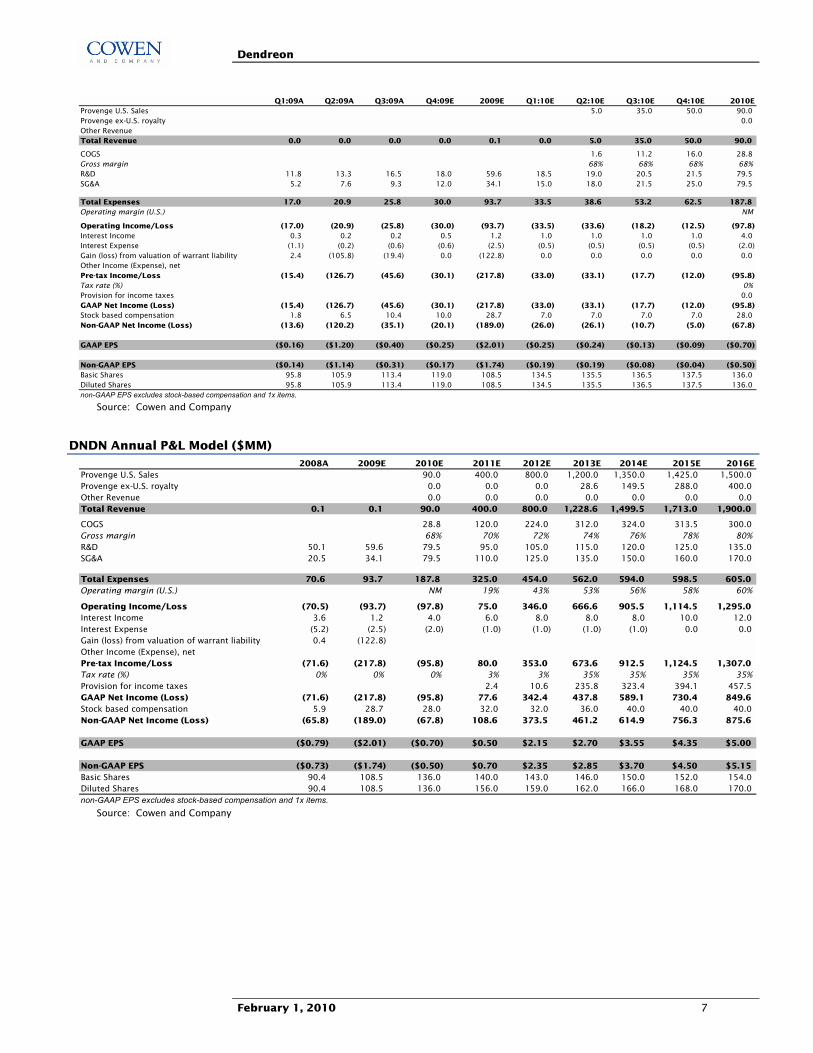

DNDN Quarterly P&L Model ($MM)

Dendreon

February 1, 2010 7

Q1:09A Q2:09A Q3:09A Q4:09E 2009E Q1:10E Q2:10E Q3:10E Q4:10E 2010EProvenge U.S. Sales 5.0 35.0 50.0 90.0Provenge ex-U.S. royalty 0.0Other RevenueTotal Revenue 0.0 0.0 0.0 0.0 0.1 0.0 5.0 35.0 50.0 90.0

COGS 1.6 11.2 16.0 28.8Gross margin 68% 68% 68% 68%R&D 11.8 13.3 16.5 18.0 59.6 18.5 19.0 20.5 21.5 79.5SG&A 5.2 7.6 9.3 12.0 34.1 15.0 18.0 21.5 25.0 79.5

Total Expenses 17.0 20.9 25.8 30.0 93.7 33.5 38.6 53.2 62.5 187.8Operating margin (U.S.) NM

Operating Income/Loss (17.0) (20.9) (25.8) (30.0) (93.7) (33.5) (33.6) (18.2) (12.5) (97.8)Interest Income 0.3 0.2 0.2 0.5 1.2 1.0 1.0 1.0 1.0 4.0Interest Expense (1.1) (0.2) (0.6) (0.6) (2.5) (0.5) (0.5) (0.5) (0.5) (2.0)Gain (loss) from valuation of warrant liability 2.4 (105.8) (19.4) 0.0 (122.8) 0.0 0.0 0.0 0.0 0.0Other Income (Expense), netPre-tax Income/Loss (15.4) (126.7) (45.6) (30.1) (217.8) (33.0) (33.1) (17.7) (12.0) (95.8)Tax rate (%) 0%Provision for income taxes 0.0GAAP Net Income (Loss) (15.4) (126.7) (45.6) (30.1) (217.8) (33.0) (33.1) (17.7) (12.0) (95.8)Stock based compensation 1.8 6.5 10.4 10.0 28.7 7.0 7.0 7.0 7.0 28.0Non-GAAP Net Income (Loss) (13.6) (120.2) (35.1) (20.1) (189.0) (26.0) (26.1) (10.7) (5.0) (67.8)

GAAP EPS ($0.16) ($1.20) ($0.40) ($0.25) ($2.01) ($0.25) ($0.24) ($0.13) ($0.09) ($0.70)

Non-GAAP EPS ($0.14) ($1.14) ($0.31) ($0.17) ($1.74) ($0.19) ($0.19) ($0.08) ($0.04) ($0.50)Basic Shares 95.8 105.9 113.4 119.0 108.5 134.5 135.5 136.5 137.5 136.0Diluted Shares 95.8 105.9 113.4 119.0 108.5 134.5 135.5 136.5 137.5 136.0non-GAAP EPS excludes stock-based compensation and 1x items.

Source: Cowen and Company

DNDN Annual P&L Model ($MM) 2008A 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E

Provenge U.S. Sales 90.0 400.0 800.0 1,200.0 1,350.0 1,425.0 1,500.0Provenge ex-U.S. royalty 0.0 0.0 0.0 28.6 149.5 288.0 400.0Other Revenue 0.0 0.0 0.0 0.0 0.0 0.0 0.0Total Revenue 0.1 0.1 90.0 400.0 800.0 1,228.6 1,499.5 1,713.0 1,900.0

COGS 28.8 120.0 224.0 312.0 324.0 313.5 300.0Gross margin 68% 70% 72% 74% 76% 78% 80%R&D 50.1 59.6 79.5 95.0 105.0 115.0 120.0 125.0 135.0SG&A 20.5 34.1 79.5 110.0 125.0 135.0 150.0 160.0 170.0

Total Expenses 70.6 93.7 187.8 325.0 454.0 562.0 594.0 598.5 605.0Operating margin (U.S.) NM 19% 43% 53% 56% 58% 60%

Operating Income/Loss (70.5) (93.7) (97.8) 75.0 346.0 666.6 905.5 1,114.5 1,295.0Interest Income 3.6 1.2 4.0 6.0 8.0 8.0 8.0 10.0 12.0Interest Expense (5.2) (2.5) (2.0) (1.0) (1.0) (1.0) (1.0) 0.0 0.0Gain (loss) from valuation of warrant liability 0.4 (122.8)Other Income (Expense), netPre-tax Income/Loss (71.6) (217.8) (95.8) 80.0 353.0 673.6 912.5 1,124.5 1,307.0Tax rate (%) 0% 0% 0% 3% 3% 35% 35% 35% 35%Provision for income taxes 2.4 10.6 235.8 323.4 394.1 457.5GAAP Net Income (Loss) (71.6) (217.8) (95.8) 77.6 342.4 437.8 589.1 730.4 849.6Stock based compensation 5.9 28.7 28.0 32.0 32.0 36.0 40.0 40.0 40.0Non-GAAP Net Income (Loss) (65.8) (189.0) (67.8) 108.6 373.5 461.2 614.9 756.3 875.6

GAAP EPS ($0.79) ($2.01) ($0.70) $0.50 $2.15 $2.70 $3.55 $4.35 $5.00

Non-GAAP EPS ($0.73) ($1.74) ($0.50) $0.70 $2.35 $2.85 $3.70 $4.50 $5.15Basic Shares 90.4 108.5 136.0 140.0 143.0 146.0 150.0 152.0 154.0Diluted Shares 90.4 108.5 136.0 156.0 159.0 162.0 166.0 168.0 170.0non-GAAP EPS excludes stock-based compensation and 1x items.

Source: Cowen and Company

Dendreon

February 1, 2010 8

How Much Risk Is There To FDA Approval Of Provenge?

Provenge has had a tortuous regulatory history: despite an overwhelmingly positive vote by an FDA advisory committee in March 2007, the Agency went on to issue a Complete Response letter in May 2007, requesting additional prospective survival data from the then ongoing Phase III IMPACT study. Based on a statistically significant survival benefit in IMPACT, Dendreon refiled the BLA, which was accepted by the FDA and granted a PDUFA date of May 1, 2010.

Provenge�s tortuous history and the reluctance to take on regulatory risk have kept many potential DNDN investors on the sidelines, providing the possibility of significant stock price performance upon approval. While approval is not assured, DNDN bulls point to the positive survival data from two Phase III studies, the consistency of the data across trials, and most importantly the fact that Dendreon has satisfied the requirements of the FDA�s 2007 Complete Response letter. Investor concerns include the inconsistency between primary and secondary endpoints (survival and PFS), the potential for outstanding manufacturing issues to impact or delay approval, and a lack of confidence in the FDA�s willingness to approve a therapy with such a novel (and to some extent, undetermined) mode of action.

Based on our discussions with leading prostate cancer experts and statisticians, we conclude that Provenge is 90% or more likely to be approved in 2010. A summary of Provenge�s regulatory history and reasons for our confidence are outlined below. Most importantly, we acknowledge that handicapping any FDA decision is fraught with hazard, and reflect this by discounting our fair value estimate for DNDN stock by 10%.

Dendreon

February 1, 2010 9

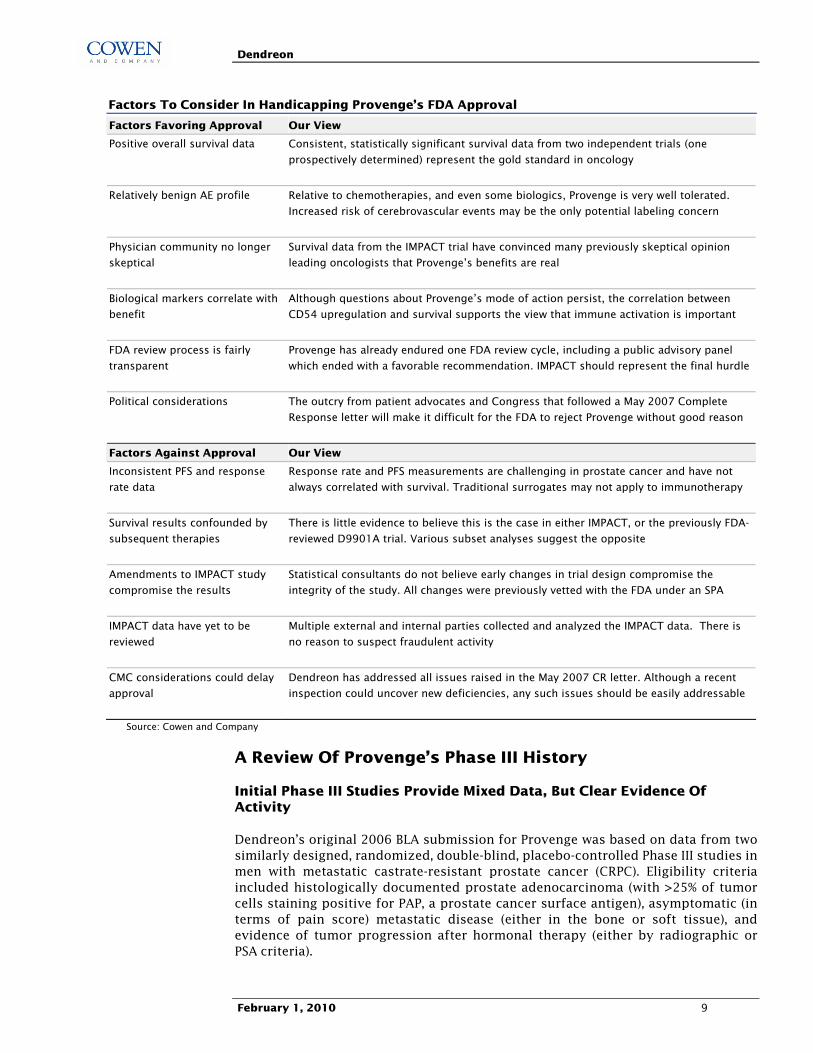

Factors To Consider In Handicapping Provenge�s FDA Approval

Factors Favoring Approval Our View

Positive overall survival data Consistent, statistically significant survival data from two independent trials (one

prospectively determined) represent the gold standard in oncology

Relatively benign AE profile Relative to chemotherapies, and even some biologics, Provenge is very well tolerated.

Increased risk of cerebrovascular events may be the only potential labeling concern

Physician community no longer

skeptical

Survival data from the IMPACT trial have convinced many previously skeptical opinion

leading oncologists that Provenge�s benefits are real

Biological markers correlate with

benefit

Although questions about Provenge�s mode of action persist, the correlation between

CD54 upregulation and survival supports the view that immune activation is important

FDA review process is fairly

transparent

Provenge has already endured one FDA review cycle, including a public advisory panel

which ended with a favorable recommendation. IMPACT should represent the final hurdle

Political considerations The outcry from patient advocates and Congress that followed a May 2007 Complete

Response letter will make it difficult for the FDA to reject Provenge without good reason

Factors Against Approval Our View Inconsistent PFS and response

rate data

Response rate and PFS measurements are challenging in prostate cancer and have not

always correlated with survival. Traditional surrogates may not apply to immunotherapy

Survival results confounded by

subsequent therapies

There is little evidence to believe this is the case in either IMPACT, or the previously FDA-

reviewed D9901A trial. Various subset analyses suggest the opposite

Amendments to IMPACT study

compromise the results

Statistical consultants do not believe early changes in trial design compromise the

integrity of the study. All changes were previously vetted with the FDA under an SPA

IMPACT data have yet to be

reviewed

Multiple external and internal parties collected and analyzed the IMPACT data. There is

no reason to suspect fraudulent activity

CMC considerations could delay

approval

Dendreon has addressed all issues raised in the May 2007 CR letter. Although a recent

inspection could uncover new deficiencies, any such issues should be easily addressable

Source: Cowen and Company

A Review Of Provenge�s Phase III History

Initial Phase III Studies Provide Mixed Data, But Clear Evidence Of Activity

Dendreon�s original 2006 BLA submission for Provenge was based on data from two similarly designed, randomized, double-blind, placebo-controlled Phase III studies in men with metastatic castrate-resistant prostate cancer (CRPC). Eligibility criteria included histologically documented prostate adenocarcinoma (with >25% of tumor cells staining positive for PAP, a prostate cancer surface antigen), asymptomatic (in terms of pain score) metastatic disease (either in the bone or soft tissue), and evidence of tumor progression after hormonal therapy (either by radiographic or PSA criteria).

Dendreon

February 1, 2010 10

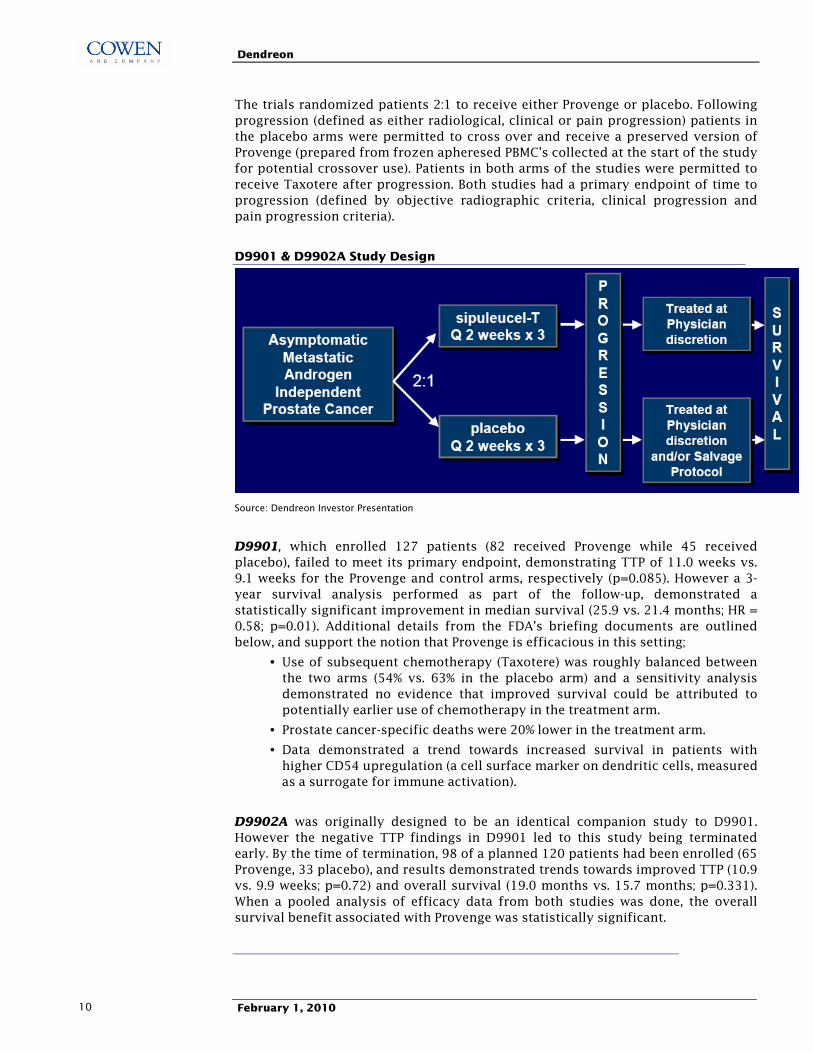

The trials randomized patients 2:1 to receive either Provenge or placebo. Following progression (defined as either radiological, clinical or pain progression) patients in the placebo arms were permitted to cross over and receive a preserved version of Provenge (prepared from frozen apheresed PBMC�s collected at the start of the study for potential crossover use). Patients in both arms of the studies were permitted to receive Taxotere after progression. Both studies had a primary endpoint of time to progression (defined by objective radiographic criteria, clinical progression and pain progression criteria).

D9901 & D9902A Study Design

Source: Dendreon Investor Presentation

D9901, which enrolled 127 patients (82 received Provenge while 45 received placebo), failed to meet its primary endpoint, demonstrating TTP of 11.0 weeks vs. 9.1 weeks for the Provenge and control arms, respectively (p=0.085). However a 3-year survival analysis performed as part of the follow-up, demonstrated a statistically significant improvement in median survival (25.9 vs. 21.4 months; HR = 0.58; p=0.01). Additional details from the FDA�s briefing documents are outlined below, and support the notion that Provenge is efficacious in this setting;

• Use of subsequent chemotherapy (Taxotere) was roughly balanced between the two arms (54% vs. 63% in the placebo arm) and a sensitivity analysis demonstrated no evidence that improved survival could be attributed to potentially earlier use of chemotherapy in the treatment arm.

• Prostate cancer-specific deaths were 20% lower in the treatment arm.

• Data demonstrated a trend towards increased survival in patients with higher CD54 upregulation (a cell surface marker on dendritic cells, measured as a surrogate for immune activation).

D9902A was originally designed to be an identical companion study to D9901. However the negative TTP findings in D9901 led to this study being terminated early. By the time of termination, 98 of a planned 120 patients had been enrolled (65 Provenge, 33 placebo), and results demonstrated trends towards improved TTP (10.9 vs. 9.9 weeks; p=0.72) and overall survival (19.0 months vs. 15.7 months; p=0.331). When a pooled analysis of efficacy data from both studies was done, the overall survival benefit associated with Provenge was statistically significant.

Dendreon

February 1, 2010 11

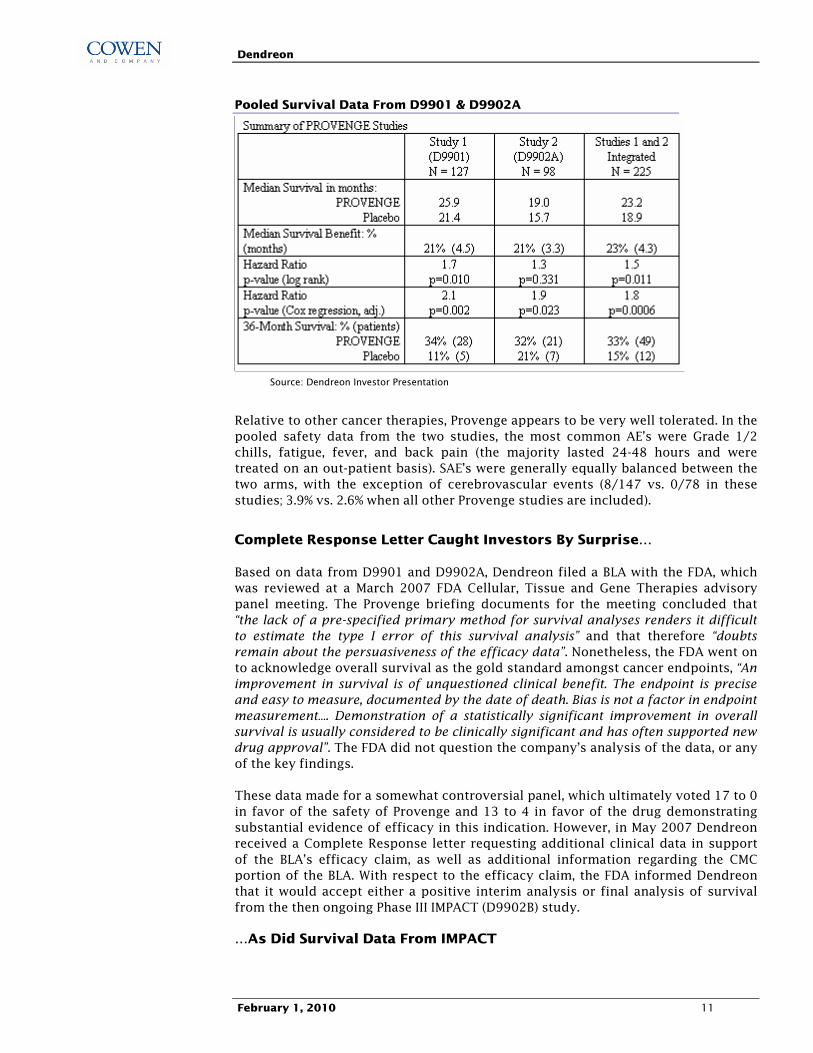

Pooled Survival Data From D9901 & D9902A

Source: Dendreon Investor Presentation

Relative to other cancer therapies, Provenge appears to be very well tolerated. In the pooled safety data from the two studies, the most common AE�s were Grade 1/2 chills, fatigue, fever, and back pain (the majority lasted 24-48 hours and were treated on an out-patient basis). SAE�s were generally equally balanced between the two arms, with the exception of cerebrovascular events (8/147 vs. 0/78 in these studies; 3.9% vs. 2.6% when all other Provenge studies are included).

Complete Response Letter Caught Investors By Surprise�

Based on data from D9901 and D9902A, Dendreon filed a BLA with the FDA, which was reviewed at a March 2007 FDA Cellular, Tissue and Gene Therapies advisory panel meeting. The Provenge briefing documents for the meeting concluded that �the lack of a pre-specified primary method for survival analyses renders it difficult to estimate the type I error of this survival analysis� and that therefore �doubts remain about the persuasiveness of the efficacy data�. Nonetheless, the FDA went on to acknowledge overall survival as the gold standard amongst cancer endpoints, �An improvement in survival is of unquestioned clinical benefit. The endpoint is precise and easy to measure, documented by the date of death. Bias is not a factor in endpoint measurement�. Demonstration of a statistically significant improvement in overall survival is usually considered to be clinically significant and has often supported new drug approval�. The FDA did not question the company�s analysis of the data, or any of the key findings.

These data made for a somewhat controversial panel, which ultimately voted 17 to 0 in favor of the safety of Provenge and 13 to 4 in favor of the drug demonstrating substantial evidence of efficacy in this indication. However, in May 2007 Dendreon received a Complete Response letter requesting additional clinical data in support of the BLA�s efficacy claim, as well as additional information regarding the CMC portion of the BLA. With respect to the efficacy claim, the FDA informed Dendreon that it would accept either a positive interim analysis or final analysis of survival from the then ongoing Phase III IMPACT (D9902B) study.

�As Did Survival Data From IMPACT

Dendreon

February 1, 2010 12

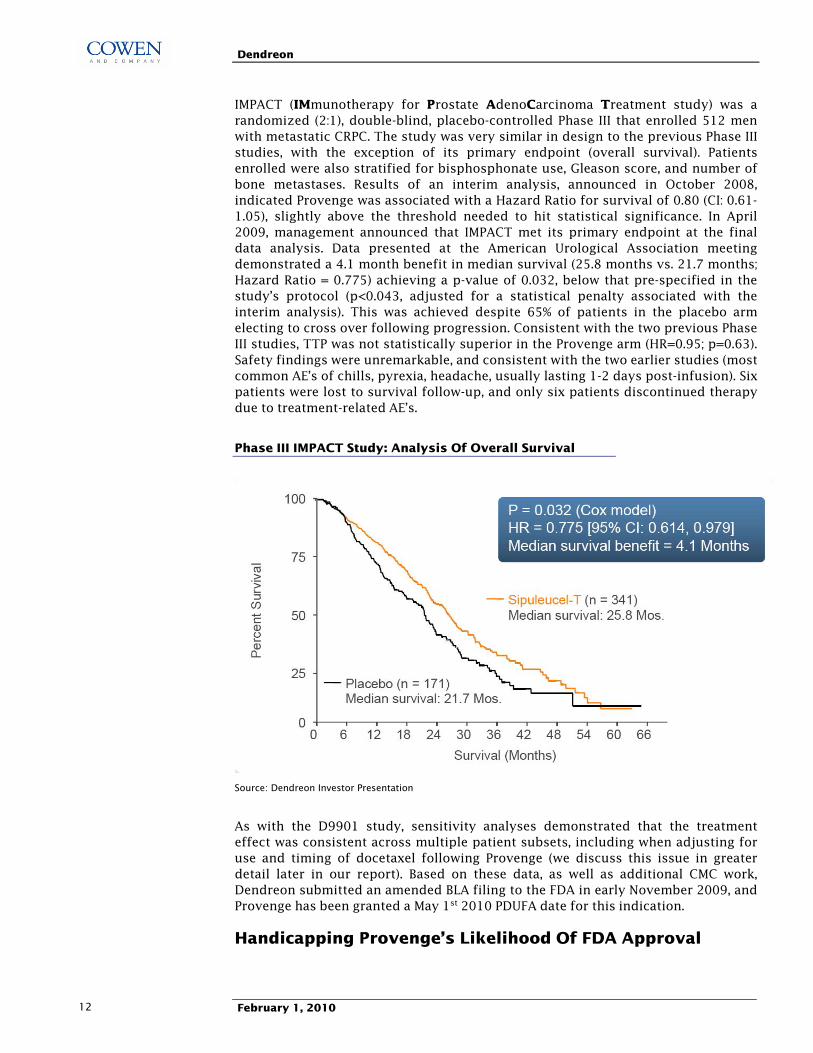

IMPACT (IMmunotherapy for Prostate AdenoCarcinoma Treatment study) was a randomized (2:1), double-blind, placebo-controlled Phase III that enrolled 512 men with metastatic CRPC. The study was very similar in design to the previous Phase III studies, with the exception of its primary endpoint (overall survival). Patients enrolled were also stratified for bisphosphonate use, Gleason score, and number of bone metastases. Results of an interim analysis, announced in October 2008, indicated Provenge was associated with a Hazard Ratio for survival of 0.80 (CI: 0.61-1.05), slightly above the threshold needed to hit statistical significance. In April 2009, management announced that IMPACT met its primary endpoint at the final data analysis. Data presented at the American Urological Association meeting demonstrated a 4.1 month benefit in median survival (25.8 months vs. 21.7 months; Hazard Ratio = 0.775) achieving a p-value of 0.032, below that pre-specified in the study�s protocol (p<0.043, adjusted for a statistical penalty associated with the interim analysis). This was achieved despite 65% of patients in the placebo arm electing to cross over following progression. Consistent with the two previous Phase III studies, TTP was not statistically superior in the Provenge arm (HR=0.95; p=0.63). Safety findings were unremarkable, and consistent with the two earlier studies (most common AE�s of chills, pyrexia, headache, usually lasting 1-2 days post-infusion). Six patients were lost to survival follow-up, and only six patients discontinued therapy due to treatment-related AE�s.

Phase III IMPACT Study: Analysis Of Overall Survival

Source: Dendreon Investor Presentation

As with the D9901 study, sensitivity analyses demonstrated that the treatment effect was consistent across multiple patient subsets, including when adjusting for use and timing of docetaxel following Provenge (we discuss this issue in greater detail later in our report). Based on these data, as well as additional CMC work, Dendreon submitted an amended BLA filing to the FDA in early November 2009, and Provenge has been granted a May 1st 2010 PDUFA date for this indication.

Handicapping Provenge�s Likelihood Of FDA Approval

Dendreon

February 1, 2010 13

Based on our analysis of Provenge�s Phase III data sets, checks with multiple physicians and statistician consultants and a review of FDA documents related to Provenge, we handicap the likelihood of FDA approval at 90% or more. Below we provide a discussion of what we believe to be the most significant factors favoring regulatory approval, and address the concerns raised by Provenge skeptics.

Factors Favoring FDA Approval Of Provenge

1) Provenge Has Demonstrated A Statistically Significant Survival Benefit In Two Phase III Studies

Much of the focus at the March 2007 FDA panel centered around the fact that survival was not the prospectively defined primary endpoint in D9901 or D9902A. This ultimately formed the basis of the FDA�s Complete Response letter, in which the agency requested supportive survival data from IMPACT, an SPA-backed Phase III in which survival was defined as the primary endpoint early on in the study. With Provenge now having met the �clear and unambiguous� efficacy hurdle outlined in the FDA�s Complete Response letter, consultants believe the Agency�s concerns around Provenge�s efficacy have now been all but satisfied by IMPACT.

2) Provenge�s Safety Profile Is Benign, Relative To Other Cancer Therapies

The most common adverse events in Provenge�s three Phase III trials were Grade 1/2 chills, fatigue, fever, and back pain. Adverse events were mostly transient and resolved within 24-48 hours. At the March 2007 FDA panel, questions were raised around Provenge�s propensity to cause cerebrovascular events, with 8/147 patients in the first two Phase III studies suffering a CVA, versus zero patients in the control arm. However, when data from all Provenge studies were included (i.e. including P-11 and IMPACT data) the CVA rate was 3.9% for Provenge vs. 2.6% in control patients. Meanwhile, Provenge�s safety profile in IMPACT (summarized below) demonstrated no difference the rate of CVA�s. Ultimately the FDA panel voted 17-0 in favor of Provenge�s safety profile.

Safety Data From Phase III IMPACT Study

Source: Dendreon investor presentation

Dendreon

February 1, 2010 14

Provenge appears to be better tolerated than any major oncology product that we are aware of. As such, the overall risk/benefit profile (on which the FDA judges all new drug applications) for Provenge appears to be highly favorable.

3) Provenge Has The Support Of Physicians, Data Viewed As Robust

Prior to Dendreon�s April 2009 announcement that the IMPACT study met its primary endpoint, our oncology consultants had been skeptical of Provenge, and its likelihood of demonstrating a significant survival advantage in a much larger Phase III study. Physicians cited Provenge�s unvalidated mechanism as a dendritic cell vaccine, its single antigen target (in what they consider a biologically heterogeneous disease), and a clinical dataset with conclusions predicated largely on retrospective analyses from small studies.

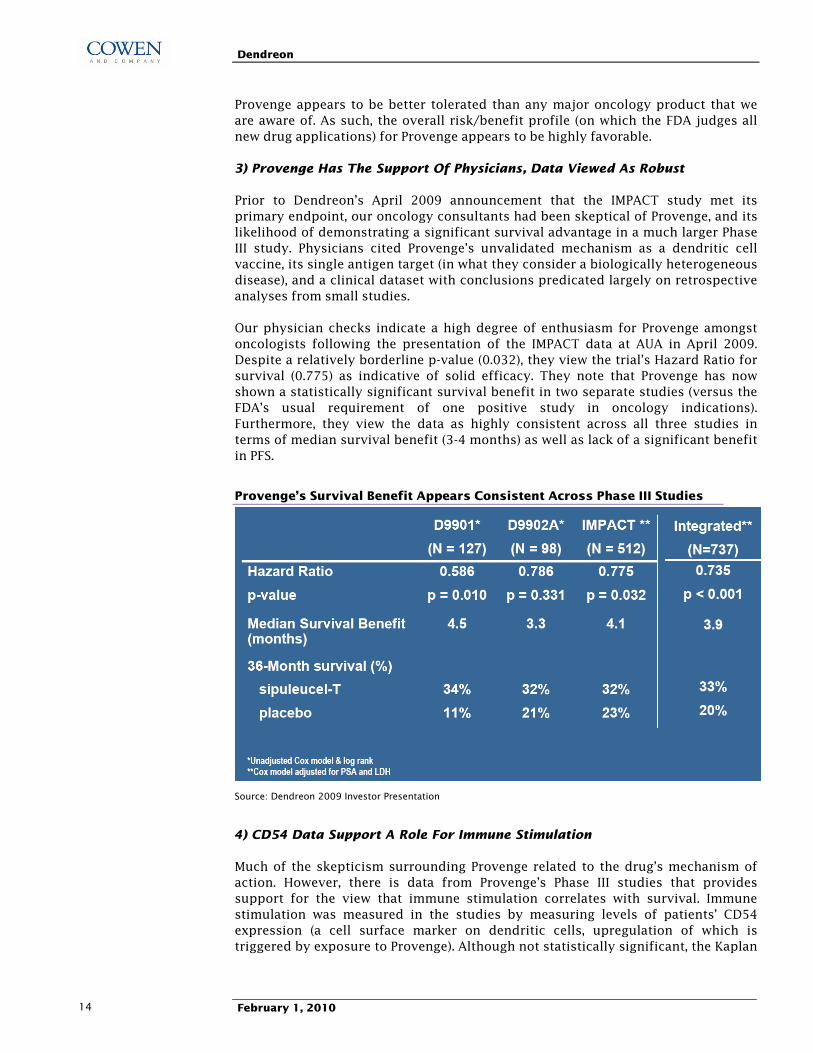

Our physician checks indicate a high degree of enthusiasm for Provenge amongst oncologists following the presentation of the IMPACT data at AUA in April 2009. Despite a relatively borderline p-value (0.032), they view the trial�s Hazard Ratio for survival (0.775) as indicative of solid efficacy. They note that Provenge has now shown a statistically significant survival benefit in two separate studies (versus the FDA�s usual requirement of one positive study in oncology indications). Furthermore, they view the data as highly consistent across all three studies in terms of median survival benefit (3-4 months) as well as lack of a significant benefit in PFS.

Provenge�s Survival Benefit Appears Consistent Across Phase III Studies

Source: Dendreon 2009 Investor Presentation

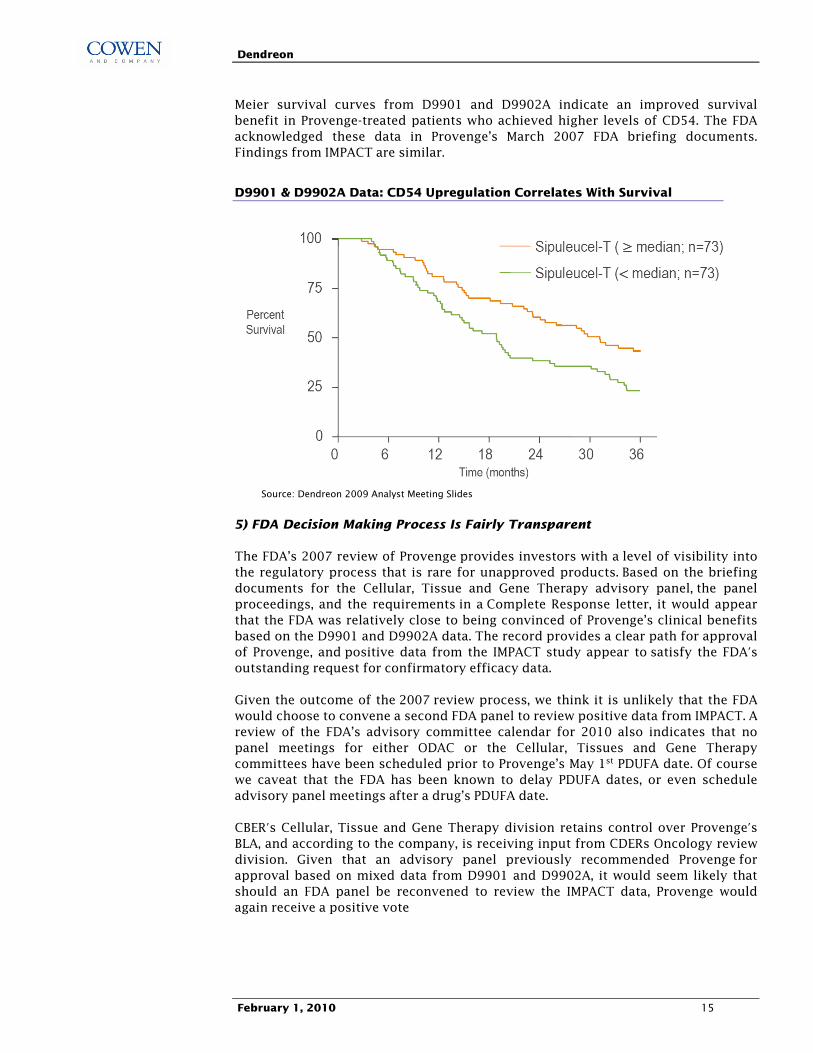

4) CD54 Data Support A Role For Immune Stimulation

Much of the skepticism surrounding Provenge related to the drug�s mechanism of action. However, there is data from Provenge�s Phase III studies that provides support for the view that immune stimulation correlates with survival. Immune stimulation was measured in the studies by measuring levels of patients� CD54 expression (a cell surface marker on dendritic cells, upregulation of which is triggered by exposure to Provenge). Although not statistically significant, the Kaplan

Dendreon

February 1, 2010 15

Meier survival curves from D9901 and D9902A indicate an improved survival benefit in Provenge-treated patients who achieved higher levels of CD54. The FDA acknowledged these data in Provenge�s March 2007 FDA briefing documents. Findings from IMPACT are similar.

D9901 & D9902A Data: CD54 Upregulation Correlates With Survival

Source: Dendreon 2009 Analyst Meeting Slides

5) FDA Decision Making Process Is Fairly Transparent

The FDA�s 2007 review of Provenge provides investors with a level of visibility into the regulatory process that is rare for unapproved products. Based on the briefing documents for the Cellular, Tissue and Gene Therapy advisory panel, the panel proceedings, and the requirements in a Complete Response letter, it would appear that the FDA was relatively close to being convinced of Provenge�s clinical benefits based on the D9901 and D9902A data. The record provides a clear path for approval of Provenge, and positive data from the IMPACT study appear to satisfy the FDA's outstanding request for confirmatory efficacy data.

Given the outcome of the 2007 review process, we think it is unlikely that the FDA would choose to convene a second FDA panel to review positive data from IMPACT. A review of the FDA�s advisory committee calendar for 2010 also indicates that no panel meetings for either ODAC or the Cellular, Tissues and Gene Therapy committees have been scheduled prior to Provenge�s May 1st PDUFA date. Of course we caveat that the FDA has been known to delay PDUFA dates, or even schedule advisory panel meetings after a drug�s PDUFA date.

CBER's Cellular, Tissue and Gene Therapy division retains control over Provenge's BLA, and according to the company, is receiving input from CDERs Oncology review division. Given that an advisory panel previously recommended Provenge for approval based on mixed data from D9901 and D9902A, it would seem likely that should an FDA panel be reconvened to review the IMPACT data, Provenge would again receive a positive vote

Dendreon

February 1, 2010 16

6) Public FDA Scrutiny May Weigh In Dendreon�s Favor

The failure of the FDA to approve Provenge in 2007 became a subject of intense scrutiny by non-profit groups and later by Congress. After the favorable panel vote, a prominent oncologist and researcher at Memorial Sloan Kettering Cancer Center (and also a panel member who voted against approval), wrote a letter to the FDA outlining reasons against approving Provenge�s BLA. This letter later leaked to an influential newsletter (The Cancer Letter) leading to angry protests (on blogs and websites) from patients and patient advocate groups.

In September 2007, in response to pressure from prostate cancer activists, three Congressmen requested a hearing into the FDA�s decision, and an investigation into possible conflicts of interest and ethical violations concerning two FDA advisory panel members who voted against approval of Provenge.

These events have led to a high level of public awareness around Provenge�s regulatory review, and would seem to raise an already high bar for an FDA rejection decision.

Potential Risks To FDA Approval Of Provenge

While we believe Provenge�s Phase III dataset to be compelling, there is a camp of investors that remain cautious toward Provenge�s regulatory prospects. Concerns range from the design and statistical integrity of the IMPACT study, to issues around the Chemistry, Manufacturing and Controls portion of the BLA. Our discussions with management, physicians, and statistical consultants suggest there is little merit to these arguments. Below, we address what we believe to be the key investor concerns regarding FDA approval.

Regulatory Concern #1: Provenge Is Not Associated With A PFS Or Response Rate Benefit

Much of the discussion at the March 2007 FDA panel was focused on Provenge�s failure to demonstrate a statistically significant improvement on D9901 and D9902A�s primary endpoint, PFS. Many theories have been put forth to explain the disconcordance in the data sets between PFS/response rates and survival (some of which are outlined below). Nonetheless, our read of the evidence and our discussions with prostate cancer experts suggest this is unlikely to have any bearing on the FDA�s final evaluation. Our reasons are set forth below.

First, a review of the prostate cancer literature confirms the view that there are no validated surrogate endpoints for assessing benefit in metastatic CRPC. This is because of difficulty in objectively quantifying changes in tumors that have metastasized to the bone (RECIST criteria are not applicable). A study published by Scher, et al in 2005 demonstrated that when RECIST criteria are applied to men with CRPC, less than half of patients have measurable target lesions greater than 2cm in size. Another study by Scher, et al published in 2007, demonstrated that the overall association between PFS and survival was weak to moderate (0.4 for radiographic PFS), and again concluded that current measure of PFS in CRPC are not strong surrogates for survival. Factors thought to contribute to this lack of correlation include interval censoring of progression data, and the discontinuation of therapy early in follow-up because of imaging changes that may not reflect true failure of the treatment. The FDA appears to be on board with this thinking, given that it is

Dendreon

February 1, 2010 17

increasingly encouraging companies operating in the prostate cancer space to focus on improvements in overall survival.

Second, our consultants think the lack of PFS benefit in all three Phase III studies is in-line with what might be expected from a slow acting immunotherapy, and is consistent with data seen from other cancer vaccine studies. In fact, a recently issued FDA guidance document titled �Clinical considerations for therapeutic cancer vaccines� appears to support our consultants� views, stating that: �Because cancer vaccines need time to elicit an immune response that could manifest as biological activity (i.e. a tumor specific immune response), a delayed effect can be expected in the subjects who have received the vaccine. Subjects may experience disease progression prior to the onset of biological activities or effects from the vaccine�.

Lastly, we take heed of Provenge�s March 2007 FDA briefing documents detailing the FDA�s stance towards survival endpoints in oncology studies: �Survival is the most reliable cancer endpoint, and when studies can be conducted to adequately assess it, it is usually the preferred endpoint. An improvement in survival is of unquestioned clinical benefit. The endpoint is precise and easy to measure� Bias is not a factor in endpoint measurement�. With respect to D9901, the FDA goes on to state that �the survival analyses were post hoc, and it is difficult to estimate the true type I error rate for the survival effect with Provenge treatment observed in D9901�. Hence we think that Dendreon�s prospective demonstration of improved survival in IMPACT will be deemed sufficient evidence of Provenge�s efficacy to warrant FDA approval.

Regulatory Concern #2: Survival analysis confounded by post-progression chemotherapy treatment and/or �Frovenge� Control

The design of Provenge�s Phase III studies allowed for patients in the placebo arm to cross over and receive Provenge upon progression. Patients in both arms of the studies were also permitted to receive Taxotere during the study. Some investors have rightly speculated that crossover might have translated into a difference in timing of subsequent chemotherapy treatment between the two arms. In theory, the survival benefit in the studies could have resulted from earlier administration of Taxotere chemotherapy to patients in the Provenge arm.

While we believe this is a legitimate question raised, according to the IMPACT data presentation, use of Taxotere was well balanced between the two arms, with 50% of patients in the Provenge arm, and 52% of patients in the placebo arm receiving Taxotere treatment. Dendreon also performed a sensitivity analysis to assess the issue of chemotherapy timing, using a time-dependent covariate analysis. Dendreon confirmed that Provenge�s hazard ratio remain statistically significant when adjusted for use and timing of Taxotere (HR=0.763; p=0.036). Furthermore, in the D9901A study, FDA briefing documents state that �the analysis did not suggest that increased survival in the treatment group could be attributable to earlier use of chemotherapy in general or taxanes specifically�.

Dendreon

February 1, 2010 18

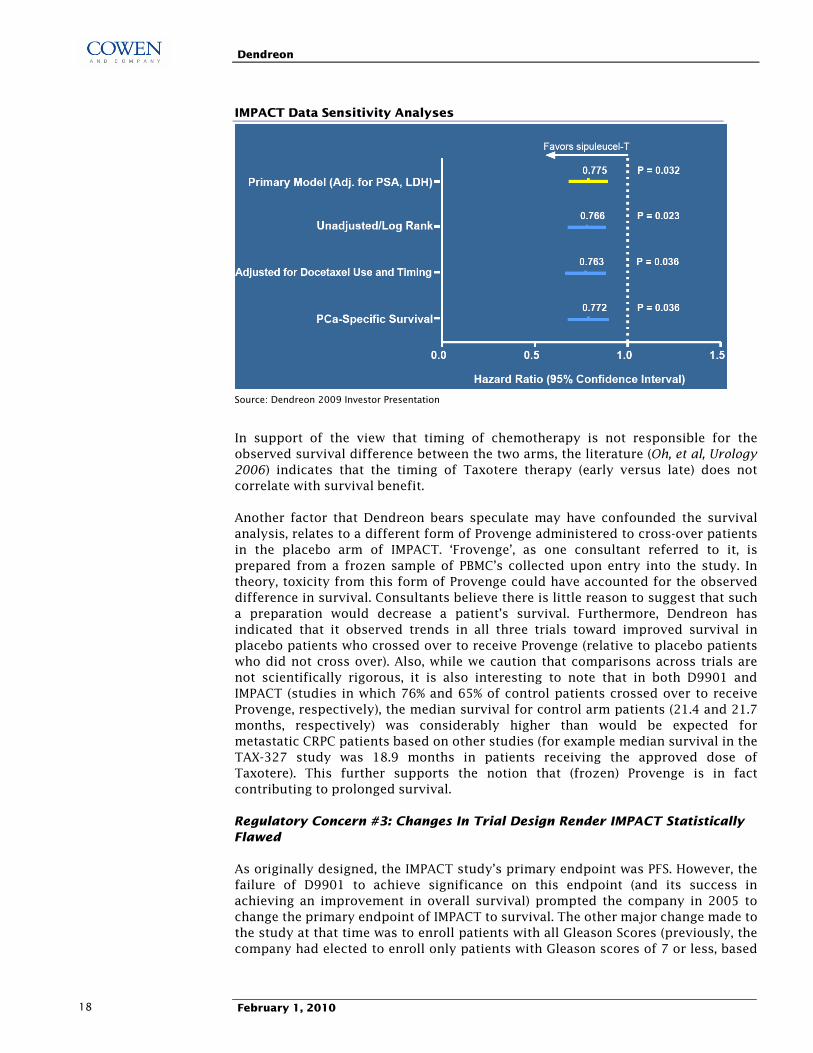

IMPACT Data Sensitivity Analyses

Source: Dendreon 2009 Investor Presentation

In support of the view that timing of chemotherapy is not responsible for the observed survival difference between the two arms, the literature (Oh, et al, Urology 2006) indicates that the timing of Taxotere therapy (early versus late) does not correlate with survival benefit.

Another factor that Dendreon bears speculate may have confounded the survival analysis, relates to a different form of Provenge administered to cross-over patients in the placebo arm of IMPACT. �Frovenge�, as one consultant referred to it, is prepared from a frozen sample of PBMC�s collected upon entry into the study. In theory, toxicity from this form of Provenge could have accounted for the observed difference in survival. Consultants believe there is little reason to suggest that such a preparation would decrease a patient�s survival. Furthermore, Dendreon has indicated that it observed trends in all three trials toward improved survival in placebo patients who crossed over to receive Provenge (relative to placebo patients who did not cross over). Also, while we caution that comparisons across trials are not scientifically rigorous, it is also interesting to note that in both D9901 and IMPACT (studies in which 76% and 65% of control patients crossed over to receive Provenge, respectively), the median survival for control arm patients (21.4 and 21.7 months, respectively) was considerably higher than would be expected for metastatic CRPC patients based on other studies (for example median survival in the TAX-327 study was 18.9 months in patients receiving the approved dose of Taxotere). This further supports the notion that (frozen) Provenge is in fact contributing to prolonged survival.

Regulatory Concern #3: Changes In Trial Design Render IMPACT Statistically Flawed

As originally designed, the IMPACT study�s primary endpoint was PFS. However, the failure of D9901 to achieve significance on this endpoint (and its success in achieving an improvement in overall survival) prompted the company in 2005 to change the primary endpoint of IMPACT to survival. The other major change made to the study at that time was to enroll patients with all Gleason Scores (previously, the company had elected to enroll only patients with Gleason scores of 7 or less, based

Dendreon

February 1, 2010 19

on post-hoc subset analyses from earlier studies). All changes were discussed and agreed to by the FDA.

Our statistical consultants do not expect this change to compromise the statistical integrity of the study, nor to bear negatively in any way on the FDA�s review process. This reflects that fact that changes were made early on in the study, were agreed to by the FDA, and the view that that survival is viewed as the more definitive and robust of the two endpoints.

One additional point worth noting relates the October 2008 interim analysis of the IMPACT data. Some investors have postulated that DNDN�s decision to publicly release data related to the study�s hazard ratio at that time point could have biased future follow-up, and somehow increased the rate of Type I error in the final data analysis. Our statistical consultant believes there is little relevance for such an argument in a survival-based study. Furthermore, Dendreon�s management team discussed and signed off on the final press release with the FDA prior to its publication.

Regulatory Concern #4: IMPACT Data Have Yet To Pass Scrutiny

Some investors are concerned that the IMPACT trial has not yet been reviewed by the FDA or published in a peer reviewed medical journal. As a result, they are fearful that key conclusions, such as the improvement in overall survival, may be altered upon further review. Indeed the p-value on survival (p=0.032) is not particularly robust, and only modestly lower than what was pre-specified in the trial�s protocol (p=0.043).

Biotechnology investors are keenly aware that blatant scientific fraud can be a risk factor (e.g. Sequenom, TKT). However, several reasons lead us to believe the quality of the IMPACT data are as advertised.

1. Data have been presented at the late breaking session of an important medical meeting (AUA) by a prestigious clinician (Dr. David Penson of USC).

2. The protocol for statistical analysis was followed according to Dendreon�s agreed upon SPA.

3. Overall survival is an objective endpoint that is easily verifiable by death certificate, which were collected externally and reviewed internally and externally.

4. The results from Provenge�s D9901 and D9902A trials did not change after review by the FDA in 2007.

5. Several members of management have sold DNDN shares in the months since the IMPACT data were presented. Given the consequences that could be associated with fraudulent selling, we believe senior management isn�t aware of any corporate malfeasance.

Regulatory Concern #5: Visibility Is Lacking Into Whether Dendreon Can Satisfy The CMC Issues Raised In The FDA�s Complete Response Letter

In addition to requesting more evidence regarding Provenge�s efficacy, the FDA�s May 2007 Complete Response letter asked Dendreon to supply additional

Dendreon

February 1, 2010 20

information on the chemistry, manufacturing, and controls (CMC) section of the BLA. At the time, the company indicated that it could satisfy the FDA with the information requested in a timely manner. A redacted copy of the CR letter indicates the FDAs requests were fairly mundane and related to things such as:

• Inadequate labeling and handling flow of samples (quality control steps for maintaining the identity of the samples)

• Concerns about aseptic processes

• Personnel without proper training

• Request for more data on handling of multiple samples in the same room

The company has since implemented additional controls and procedures, including a Laboratory Information Management System (LIMS) that includes bar coded sample tracking, to enhance quality control. Prior to the resubmission of the BLA in November 2009, Dendreon discussed each of the CMC items in the Complete Response letter with the FDA.

Our confidence that Dendreon has taken the appropriate measures to satisfy the FDA�s 2007 concerns is high. Nonetheless, we cannot rule out CMC risk as a barrier to timely FDA approval. Provenge�s manufacturing process is unique amongst therapeutics, and includes multiple steps that need to be completed in a timely and competent manner. The company indicated FDA re-inspection of its New Jersey manufacturing facility would occur in early 2010, and while we believe the inspection went off with out a hitch, there is always some risk that the FDA could dig up novel issues that could delay approval. While it is possible that CMC issues could prevent timely approval of Provenge, we don�t believe any such issues are insurmountable. The Provenge manufacturing process is not rocket science, but rather composed of discrete processes (recombinant antigen production, leukapheresis, centrifugation/purification of APCs, incubation, activity and sterility testing) that have been performed in medical centers and diagnostic/research labs for decades. Dendreon adequately performed these tasks for hundreds of patients enrolled in Phase III trials, and all that is required for FDA approval is adequate scale up.

Dendreon

February 1, 2010 21

How Big A Drug Could Provenge Be In The U.S.?

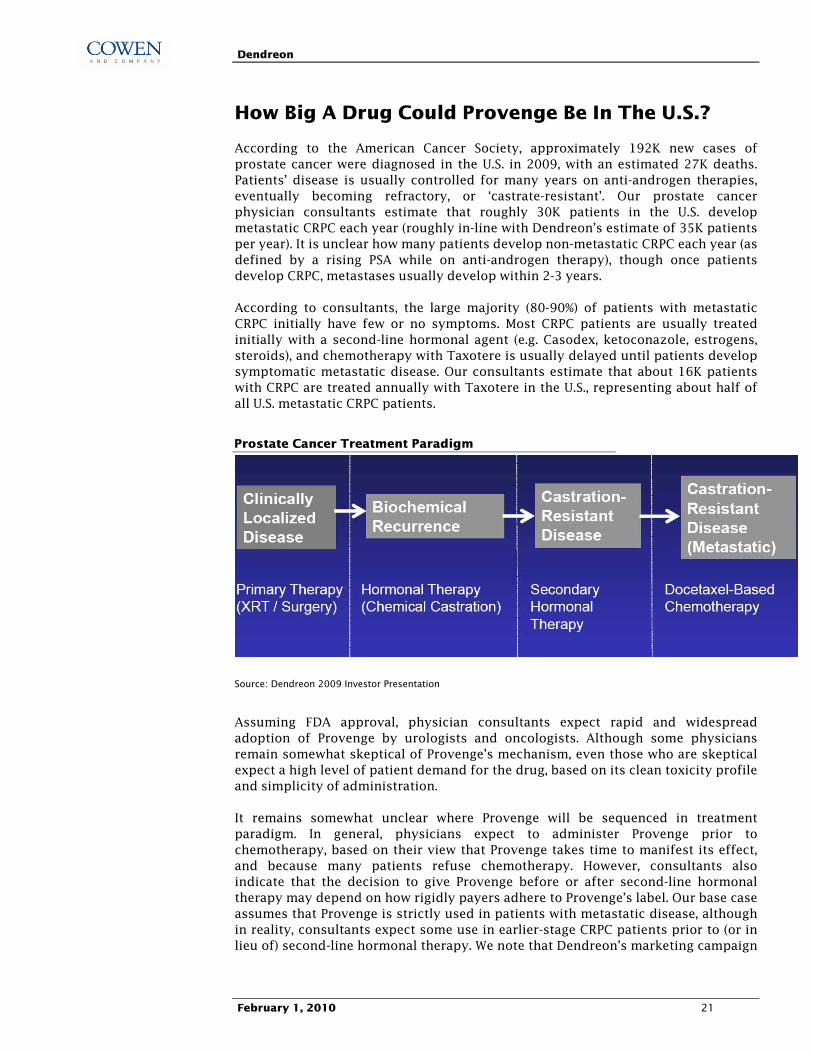

According to the American Cancer Society, approximately 192K new cases of prostate cancer were diagnosed in the U.S. in 2009, with an estimated 27K deaths. Patients� disease is usually controlled for many years on anti-androgen therapies, eventually becoming refractory, or �castrate-resistant�. Our prostate cancer physician consultants estimate that roughly 30K patients in the U.S. develop metastatic CRPC each year (roughly in-line with Dendreon�s estimate of 35K patients per year). It is unclear how many patients develop non-metastatic CRPC each year (as defined by a rising PSA while on anti-androgen therapy), though once patients develop CRPC, metastases usually develop within 2-3 years.

According to consultants, the large majority (80-90%) of patients with metastatic CRPC initially have few or no symptoms. Most CRPC patients are usually treated initially with a second-line hormonal agent (e.g. Casodex, ketoconazole, estrogens, steroids), and chemotherapy with Taxotere is usually delayed until patients develop symptomatic metastatic disease. Our consultants estimate that about 16K patients with CRPC are treated annually with Taxotere in the U.S., representing about half of all U.S. metastatic CRPC patients.

Prostate Cancer Treatment Paradigm

Source: Dendreon 2009 Investor Presentation

Assuming FDA approval, physician consultants expect rapid and widespread adoption of Provenge by urologists and oncologists. Although some physicians remain somewhat skeptical of Provenge�s mechanism, even those who are skeptical expect a high level of patient demand for the drug, based on its clean toxicity profile and simplicity of administration.

It remains somewhat unclear where Provenge will be sequenced in treatment paradigm. In general, physicians expect to administer Provenge prior to chemotherapy, based on their view that Provenge takes time to manifest its effect, and because many patients refuse chemotherapy. However, consultants also indicate that the decision to give Provenge before or after second-line hormonal therapy may depend on how rigidly payers adhere to Provenge�s label. Our base case assumes that Provenge is strictly used in patients with metastatic disease, although in reality, consultants expect some use in earlier-stage CRPC patients prior to (or in lieu of) second-line hormonal therapy. We note that Dendreon�s marketing campaign

Dendreon

February 1, 2010 22

is primarily directed toward urologists, under whom the bulk of earlier-stage CRPC patients are managed. In total, our consultants estimate that Provenge could ultimately be used in 80% or more of eligible patients.

U.S. Provenge Revenue Build-Up ($MM)

2010 2011 2012 2013 2014 2015 2016Incidence of metastatic CRPC 32.5 32.8 33.2 33.5 33.8 34.2 34.5% eligible for Provenge (asymptomatic or minimally symptomatic) 85% 85% 85% 85% 85% 85% 85%# eligible patients 27.6 27.9 28.2 28.5 28.7 29.0 29.3% penetration into metastatic CRPC 4% 19% 38% 55% 60% 62% 63%# new patients receiving Provenge 1.2 5.3 10.7 15.7 17.3 17.9 18.5

Provenge price per patient (000's) $75 $75 $75 $77 $78 $80 $81U.S. Provenge sales in CRPC ($MM) $90 $400 $800 $1,200 $1,350 $1,425 $1,500

U.S.

Source: Cowen and Company

Our model assumes 30-35K new metastatic CRPC patients per year in the U.S., 85% of who present with minimally symptomatic disease. We assume Provenge is launched shortly after its May 1, 2010 PDUFA date, with 60% penetration into metastatic CRPC patients within 3-4 years of launch, and more gradual share gains beyond 2013. We estimate a course of three Provenge treatments is priced at $75K/patient, a figure that is roughly in-line with other cancer therapies with demonstrated survival benefits, and we think in-line with management�s thinking. Our estimate of $1.5B in peak U.S. sales assumes roughly 18-19K patients per year are treated with Provenge at peak.

In our view the greatest source of potential upside to these numbers lies in the potential for reimbursement of Provenge in earlier-stage (non-metastatic) CRPC, which we estimate could represent another 30,000 patients per year. Consultants note that there is some ambiguity in terms of when a patient is officially diagnosed as having metastatic disease. In their opinion, borderline patients with advanced CRPC but no documented metastases will likely also seek treatment with Provenge.

We also acknowledge that the number of pre-existing metastatic HRPC patients (i.e. the prevalence) is significantly higher than the incidence rate we model (we estimate 90-100K patients in the U.S.). We have conservatively elected not to include these patients in our model, reflecting capacity/production constraints in the initial 1-2 years of Provenge�s launch (discussed in greater detail below). We do not account for these patients beyond this time, as median survival for these patients is on the order of 18-19 months.

Dendreon expects to launch Provenge with a 125-person sales force, including district sales managers (already hired) and medical science liaisons. Management has indicated that it will launch Provenge very soon after the drug�s approval, initially targeting physicians and sites involved in the Provenge clinical trials.

Dendreon

February 1, 2010 23

Can Dendreon Block And Tackle In The U.S. ?

Because Provenge is a personalized, cell-based therapy, its commercialization is considerably more challenging than a typical pharmaceutical or biotech product. Dendreon will need to successfully navigate several logistical issues related to the Provenge supply chain in order to maximize Provenge�s sales potential.

A Look At The Steps Involved In The Provenge Process

From a patient�s perspective, the process of receiving Provenge treatment is relatively simple. After a patient is prescribed Provenge, his/her physician contacts the Provenge call center, which coordinates the process providing the patient with six appointments: three appointments (2 or more weeks apart) for blood sample collection at a local apheresis center, and three follow-up appointments for Provenge infusion at the physician�s office or infusion center. Each infusion takes place a few days after each blood sample is collected, however the preparation and administration of each infusion involves a sequence of steps that must be coordinated during this time (described below). We are confident that Dendreon is capable of successful execution, as none of the individual steps in this process are particularly challenging, and the entire process has been navigated, albeit on a smaller scale, with high success rates in clinical trials.

Steps Involved In Provenge�s Preparation And Administration

Source: Dendreon 2009 Analyst Day Presentation

Sample Preparation And Transportation

The patient�s blood sample must first undergo leukapheresis (a procedure in which white blood cells are separated from the blood sample). This takes place at an apheresis center. Each of these centers must be validated and contracted by Dendreon. Dendreon estimates there are approximately 600 apheresis centers in the U.S. Approximately 75 of these sites were used in the Phase III IMPACT study, and management estimates 150-200 sites will be utilized at peak. Dendreon has contracted directly with many leading apheresis service providers (for example, The American Red Cross, the New York blood center), and will incentivize centers by reimbursing at higher rates than would be typical for a leukapheresis procedure (typically in the $700-800 range). Management and consultants are confident that multiple centers can be validated before Provenge�s approval providing sufficient capacity at apheresis centers to meet potential demand.

Dendreon

February 1, 2010 24

The white cell sample is then shipped by courier to one of Dendreon�s three manufacturing facilities (New Jersey, and eventually L.A. or Atlanta). Dendreon is working with established couriers that specialize in the time sensitive delivery of materials including medical products. Each individual sample is labeled with a bar code that should ensure patient samples are not mixed, and allow each sample to be trackable by a GPS-like computer system.

Manufacture Of Provenge

This is the only step in the process that is managed entirely by Dendreon. The process of making Provenge is depicted below. Specific cells known as Antigen Presenting Cells (or APC�s) are first separated out for a patient�s white blood sample. The cells are then incubated with an Antigen-Delivery-Cassette (GM-CSF combined with Prostatic Acid Phosphatase, an antigen that is widely expressed on the surface of prostate cancer cells) for a period of up to two days. This set of �activated� APC�s then undergo quality assurance testing including evaluation of surrogate markers for immune stimulation (such as CD54). The sample is then formulated with a buffer to create the final Provenge infusion, which is shipped back to the physician and administered to the patient as a simple one hour infusion in the physician�s office (no pre-medication is needed). The entire cycle is repeated three times, at two-weekly intervals, following which Dendreon collects payment from the physician.

A Look At The Science Behind Provenge

Source: Dendreon 2009 Analyst Day Presentation

Manufacturing Capacity Is The Rate-Limiting Step To Provenge�s Early Launch

At full capacity, Dendreon will operate three manufacturing sites: one each in New Jersey, L.A., and Atlanta. Dendreon built out 25% its NJ facility in 2006, and this has been used for the manufacture of Provenge since 2007. The company also intends to launch Provenge from this existing facility. Build-out of the remaining 75% of capacity is underway and is on track to complete in H1:11, while L.A. and Atlanta are expected to provide additional capacity by mid-2011. Because the three facilities have a modular construct with the same design and equipment for the GMP manufacturing core, this should dramatically reduce the engineering time required

Dendreon

February 1, 2010 25

to build the facilities. We estimate it will take 12-14 months to build each facility, and perhaps 4-6 months for validation and inspection.

Dendreon has provided an indication of the potential revenue that each facility will be capable of providing when complete. New Jersey (48 workstations at full capacity) will be capable of providing $500MM-$1B in yearly revenues, while LA and Atlanta (36 workstations each) will be capable of generating $375-$750MM each in yearly revenues.

Based on these figures, Dendreon has guided to a �step-wise� launch for Provenge, estimating that the initial manufacturing capacity (25% of NJ facility) is capable of producing $60-125MM in 2010 revenues (assuming Provenge is approved on its May 1st PDUFA date). 2011 (and to some extent 2012) should be a transition year, as build-out of the remaining workstations in NJ, and the LA an Atlanta facilities is completed.

We are confident that Dendreon can execute on the timely build-out, validation and inspection of its three facilities. The New Jersey facility has been successfully manufacturing clinical supply of Provenge since 2007, and assuming it is approved for commercial use, we see no reason why Dendreon cannot successfully scale up the process in this and other locations. Although manufacturing, logistical, training or other access-related issues could always produce minor delays to expected timelines, such delays shouldn�t detract from the high level of patient-driven demand that drives our peak sales estimates, and ultimately our valuation estimates.

Dendreon

February 1, 2010 26

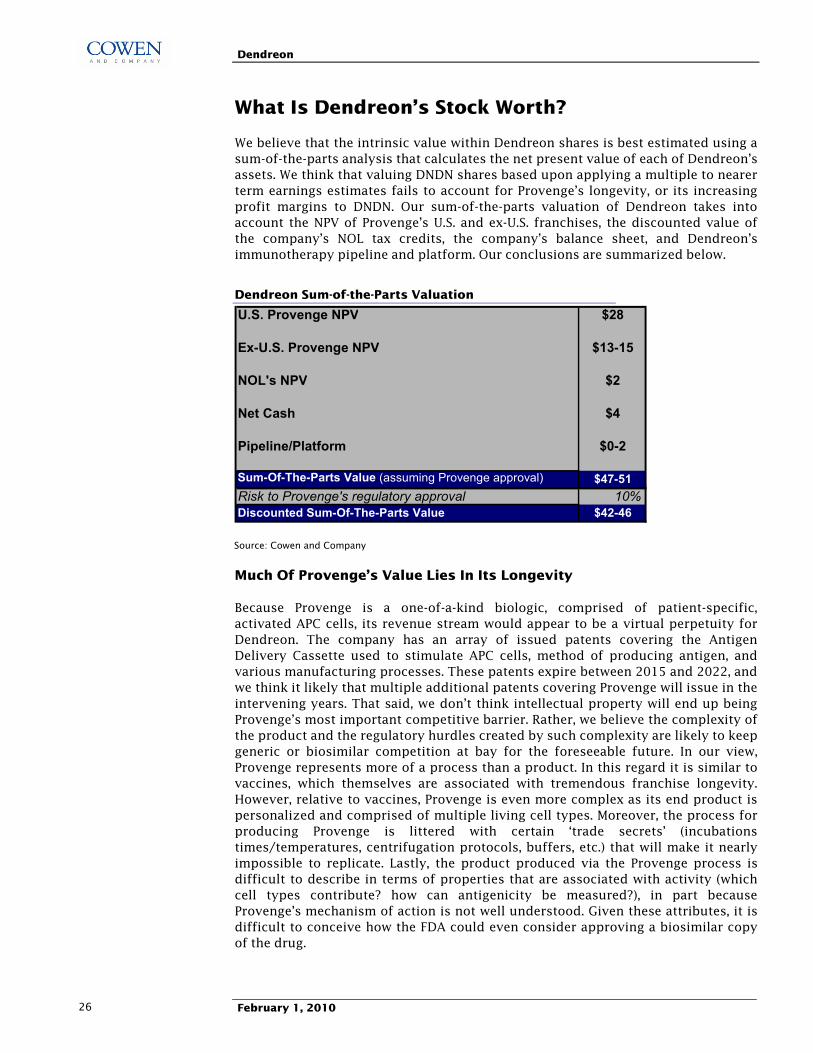

What Is Dendreon�s Stock Worth?

We believe that the intrinsic value within Dendreon shares is best estimated using a sum-of-the-parts analysis that calculates the net present value of each of Dendreon�s assets. We think that valuing DNDN shares based upon applying a multiple to nearer term earnings estimates fails to account for Provenge�s longevity, or its increasing profit margins to DNDN. Our sum-of-the-parts valuation of Dendreon takes into account the NPV of Provenge�s U.S. and ex-U.S. franchises, the discounted value of the company�s NOL tax credits, the company�s balance sheet, and Dendreon�s immunotherapy pipeline and platform. Our conclusions are summarized below.

Dendreon Sum-of-the-Parts Valuation

U.S. Provenge NPV $28

Ex-U.S. Provenge NPV $13-15

NOL's NPV $2

Net Cash $4

Pipeline/Platform $0-2

Sum-Of-The-Parts Value (assuming Provenge approval) $47-51Risk to Provenge's regulatory approval 10%Discounted Sum-Of-The-Parts Value $42-46

Source: Cowen and Company

Much Of Provenge�s Value Lies In Its Longevity

Because Provenge is a one-of-a-kind biologic, comprised of patient-specific, activated APC cells, its revenue stream would appear to be a virtual perpetuity for Dendreon. The company has an array of issued patents covering the Antigen Delivery Cassette used to stimulate APC cells, method of producing antigen, and various manufacturing processes. These patents expire between 2015 and 2022, and we think it likely that multiple additional patents covering Provenge will issue in the intervening years. That said, we don�t think intellectual property will end up being Provenge�s most important competitive barrier. Rather, we believe the complexity of the product and the regulatory hurdles created by such complexity are likely to keep generic or biosimilar competition at bay for the foreseeable future. In our view, Provenge represents more of a process than a product. In this regard it is similar to vaccines, which themselves are associated with tremendous franchise longevity. However, relative to vaccines, Provenge is even more complex as its end product is personalized and comprised of multiple living cell types. Moreover, the process for producing Provenge is littered with certain �trade secrets� (incubations times/temperatures, centrifugation protocols, buffers, etc.) that will make it nearly impossible to replicate. Lastly, the product produced via the Provenge process is difficult to describe in terms of properties that are associated with activity (which cell types contribute? how can antigenicity be measured?), in part because Provenge�s mechanism of action is not well understood. Given these attributes, it is difficult to conceive how the FDA could even consider approving a biosimilar copy of the drug.

Dendreon

February 1, 2010 27

Given the absence of meaningful biosimilar or generic competition, superior branded competition may represent about the only threat to Provenge�s longevity. In order to displace Provenge, a competitor would need to demonstrate better efficacy in a head to head study, or far superior results in a side by side comparison. We think either is unlikely. In fact, in the history of biotechnology, we are no aware of a single biologic with entrenched, blockbuster status ($500MM+ in sales) that has witnessed a decline in sales due to the arrival of new competition.

Most drugs in late stage development for prostate cancer would be used in conjunction with Provenge, either just before or just after therapy. These include JNJ�s abiraterone, Medivation�s MDV3100, and Roche�s Avastin. The only potential head on threat to Provenge on our radar screen comes from Bavarian Nordic�s PROSTVAC. PROSTVAC is an off the shelf vaccine comprised of seven monthly injections of two different poxyviruses that overexpress PSA and three immune enhancing co-stimulatory molecules. A 125-patient Phase II trial conducted in a prostate cancer population similar to that of Provenge trials demonstrated PROSTVAC improved survival relative to placebo control (HR=0.559, p=0.006). Bavarian Nordic intends to initiate Phase III testing in late 2010. We think data might be available in the 2014 timeframe

A Detailed Look At Our Sum-Of-The-Parts Analysis

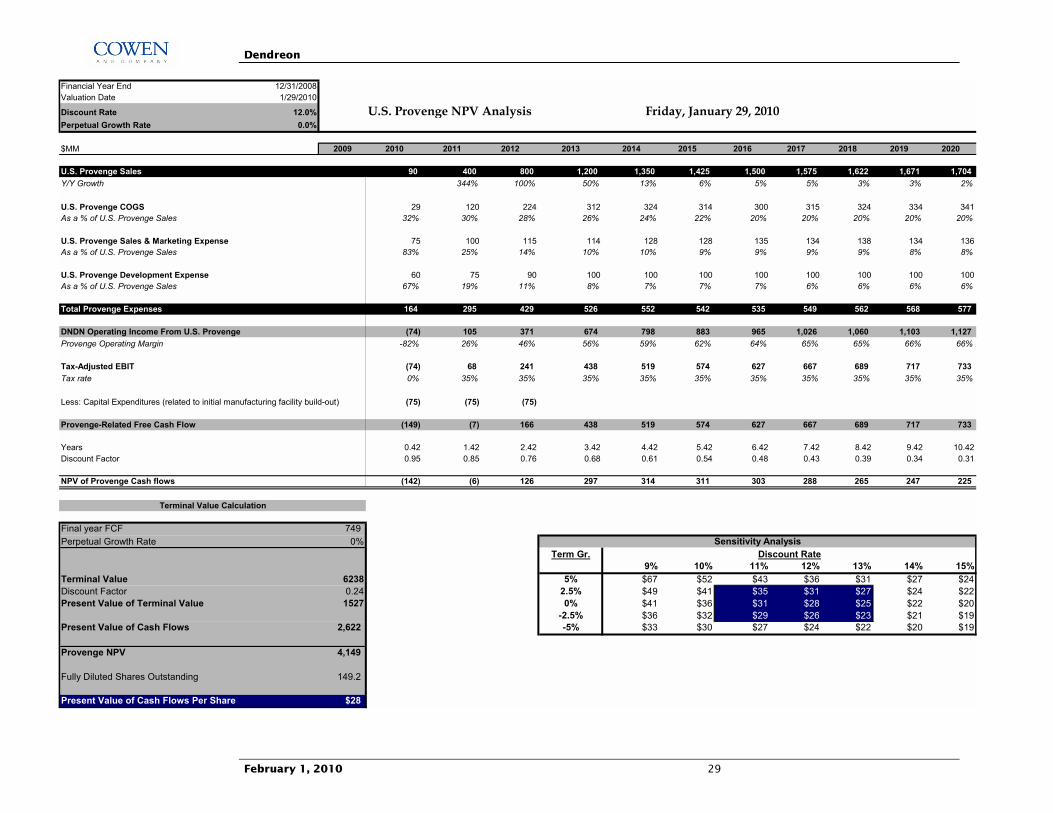

1) U.S. Provenge NPV - $28/share

Revenue Assumptions: Our U.S. Provenge NPV analysis is outlined below. Our revenue assumptions for the first six years of launch are outlined on page 22. Beyond 2016, we model medium-term (2016-22) Provenge sales growth of 3% per year in the U.S., achieved predominantly by patient population growth. Beyond 2022, we apply a 0% terminal growth rate (acknowledging that Provenge�s significant longevity could be offset by competition from newer therapies and unanticipated treatment paradigm changes). These assumptions imply U.S. sales of $1.5B by 2016 and $1.8B at peak in 2022.

Expenses: Dendreon management has guided to a gross margin for Provenge starting at 70%, rising to 80% as Provenge sales ramp, reflecting price breaks on raw materials and efficiency improvements. We model a gross margin of 70% in 2011, rising to 80% by 2016. To estimate selling costs related to Provenge, we assume Dendreon hires a sales force comprising 100-150 members at a cost of $250K per rep. We add in $50-100MM in additional marketing costs for Provenge. These figures would suggest total SG&A costs related to Provenge of $75-$150MM. To determine Free Cash Flow related to U.S. Provenge, we deduct Dendreon�s U.S. R&D expense related to Provenge, to account for costs related to additional post-marketing studies of Provenge (either those required by the FDA, or studies initiated by Dendreon to expand Provenge�s market opportunity). We estimate $60MM rising to $100MM annually in U.S. Provenge development expenses. In 2005-2007 (years during which the company was carrying out Phase III studies of Provenge), Dendreon spent $66-77MM in yearly R&D expense, suggesting our estimates are at least in the right ballpark.

Taxes: Dendreon has accumulated $529MM in U.S. Federal NOL tax credits and $76MM in State NOL�s as of year-end 2008. Therefore, the company�s tax expense should benefit for at least 1-2 years after profitability (we model Dendreon breaking even in mid to late 2011). For valuation purposes we have elected to tax Provenge

Dendreon

February 1, 2010 28

profits at 35% beginning at launch, and add back the value of NOL�s separately within our sum-of-the-parts analysis.

CapEx: We also incorporate an initial CapEx cost into Provenge�s NPV, to reflect the fact that Dendreon has yet to build out full manufacturing capacity for Provenge (only 10% of anticipated capacity has been built out to date). Management has guided that Provenge�s three U.S. manufacturing facilities are expected to cost $50-80MM each. This is consistent with a recently filed 8-K that outlines the company�s Atlanta facility construction contract (the agreement specifies a maximum price for this work of $40MM). We conservatively model $75MM in U.S. CapEx costs per year from 2010-2012.

Discount Rate: As applied to a DCF or NPV analysis, a discount rate represents the return an investor should demand for assuming a level of risk associated with the investment. Determining an appropriate discount rate for any pre-commercial biotech company is clearly fraught with hazard. In the case of Provenge, the main potential risks are regulatory and commercial. On the regulatory side, Provenge has established an overall survival benefit in two Phase III studies, with consultants unanimously predicting FDA approval. That said, Provenge�s novel first-in-class therapeutic approach to cancer represents relatively unchartered territory at the FDA. Overall, we view FDA approval as 90% likely. We account for this risk not in adjusting the discount rate, but instead in discounting our overall sum-of-the-parts value by 10%. We apply a 12% discount rate to our U.S. Provenge NPV estimates, to account for the remaining commercial and execution risk. These assumptions yield a fair value for the U.S. Provenge franchise of $28/share.

Risks To Our Valuation of U.S. Provenge: 1) Failure of the FDA to approve Provenge in CRPC; 2) competitive threats from other cancer immunotherapy programs; and 3) a disappointing commercial launch of Provenge due lower than expected demand or logistical factors (manufacturing capacity constraints). On the other hand, success in any of Provenge�s ongoing prostate cancer studies (neoadjuvant therapy, or use in androgen-dependent prostate cancer) would provide considerable upside to our longer term estimates.

Dendreon

February 1, 2010 29

Financial Year End 12/31/2008Valuation Date 1/29/2010

Discount Rate 12.0% U.S. Provenge NPV Analysis Friday, January 29, 2010Perpetual Growth Rate 0.0%

$MM 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

U.S. Provenge Sales 90 400 800 1,200 1,350 1,425 1,500 1,575 1,622 1,671 1,704Y/Y Growth 344% 100% 50% 13% 6% 5% 5% 3% 3% 2%

U.S. Provenge COGS 29 120 224 312 324 314 300 315 324 334 341As a % of U.S. Provenge Sales 32% 30% 28% 26% 24% 22% 20% 20% 20% 20% 20%

U.S. Provenge Sales & Marketing Expense 75 100 115 114 128 128 135 134 138 134 136As a % of U.S. Provenge Sales 83% 25% 14% 10% 10% 9% 9% 9% 9% 8% 8%

U.S. Provenge Development Expense 60 75 90 100 100 100 100 100 100 100 100As a % of U.S. Provenge Sales 67% 19% 11% 8% 7% 7% 7% 6% 6% 6% 6%

Total Provenge Expenses 164 295 429 526 552 542 535 549 562 568 577

DNDN Operating Income From U.S. Provenge (74) 105 371 674 798 883 965 1,026 1,060 1,103 1,127Provenge Operating Margin -82% 26% 46% 56% 59% 62% 64% 65% 65% 66% 66%

Tax-Adjusted EBIT (74) 68 241 438 519 574 627 667 689 717 733Tax rate 0% 35% 35% 35% 35% 35% 35% 35% 35% 35% 35%

Less: Capital Expenditures (related to initial manufacturing facility build-out) (75) (75) (75)

Provenge-Related Free Cash Flow (149) (7) 166 438 519 574 627 667 689 717 733

Years 0.42 1.42 2.42 3.42 4.42 5.42 6.42 7.42 8.42 9.42 10.42Discount Factor 0.95 0.85 0.76 0.68 0.61 0.54 0.48 0.43 0.39 0.34 0.31

NPV of Provenge Cash flows (142) (6) 126 297 314 311 303 288 265 247 225

Final year FCF 749Perpetual Growth Rate 0%

Term Gr.27.8 9% 10% 11% 12% 13% 14% 15%

Terminal Value 6238 5% $67 $52 $43 $36 $31 $27 $24Discount Factor 0.24 2.5% $49 $41 $35 $31 $27 $24 $22Present Value of Terminal Value 1527 0% $41 $36 $31 $28 $25 $22 $20

-2.5% $36 $32 $29 $26 $23 $21 $19Present Value of Cash Flows 2,622 -5% $33 $30 $27 $24 $22 $20 $19

Provenge NPV 4,149

Fully Diluted Shares Outstanding 149.2

Present Value of Cash Flows Per Share $28

Discount Rate

Terminal Value Calculation

Sensitivity Analysis

Dendreon

February 1, 2010 30

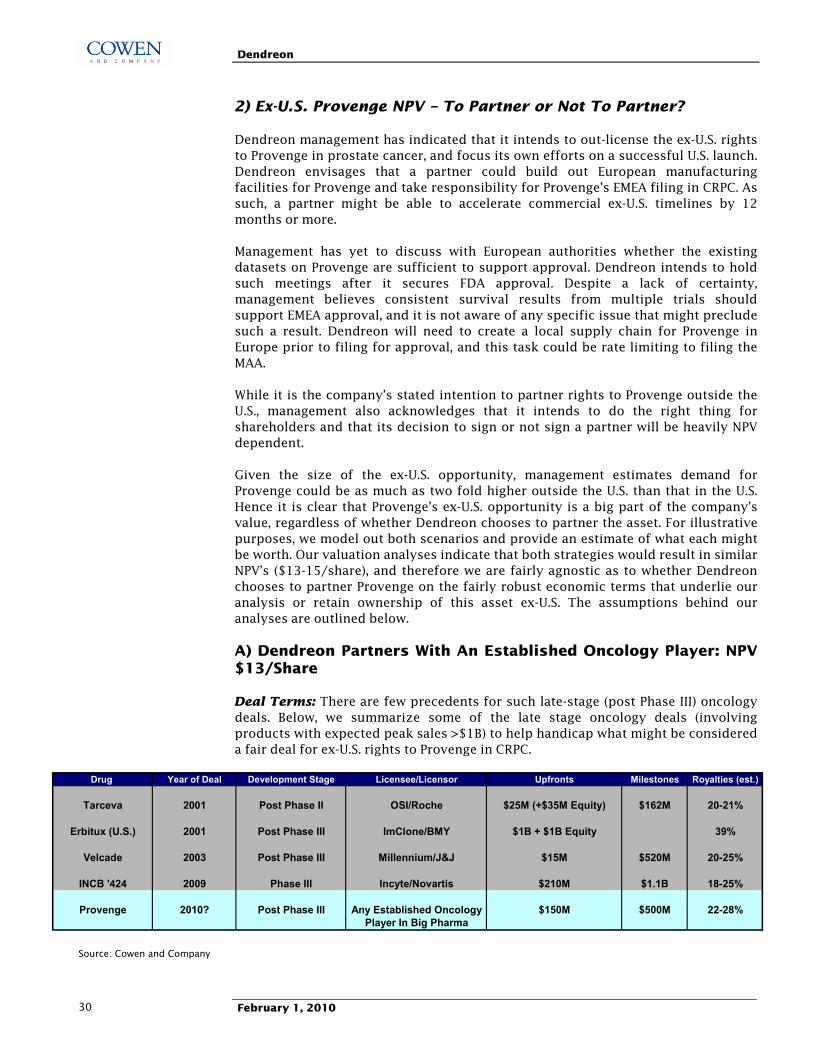

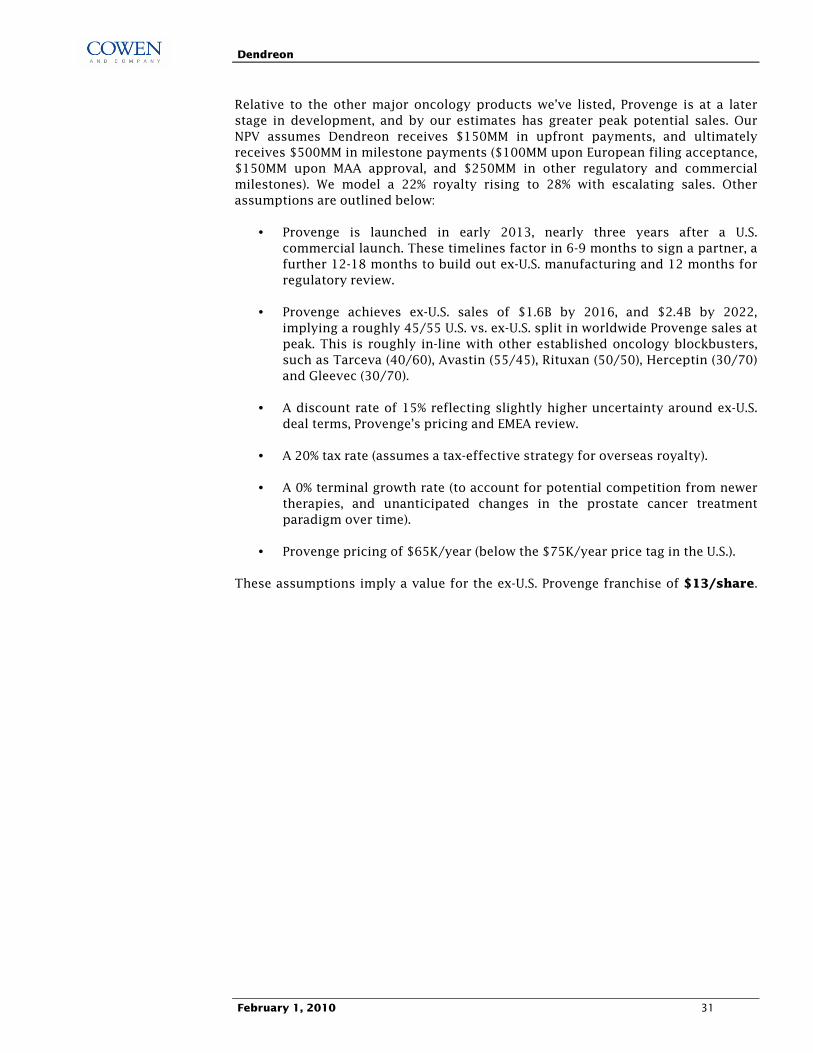

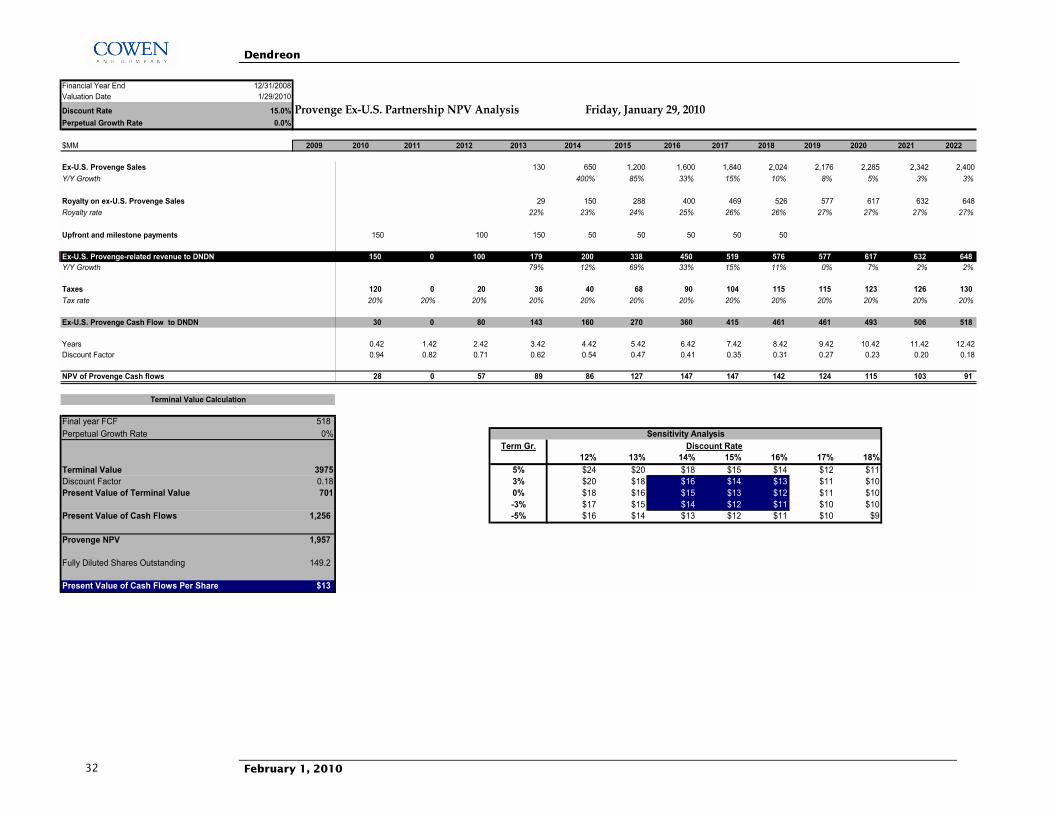

2) Ex-U.S. Provenge NPV � To Partner or Not To Partner?