DLF Hyde Park Chandigarh, DLF Mullanpur Plots, DLF Mullanpur

Upload

aks-hay-kumarCategory

view

83download

1description

A

PROJECT REPORT

ON

‘A Market survey report on analysis of DLF group limited’

Submitted to Jaipur National University, Jaipur, school of business and Management in fulfillment of project of 3rdSemester for award of Master in business administration

Session (2013)

Submitted to:Prof. Rajesh MehrotraDirector of school of business managementSubmitted by:Dhananjay singhMBA (3rd sem)

JAIPUR NATIONAL UNIVERSITY, JAIPUR

Acknowledgement

The project study will be considered incomplete without acknowledging the persons who have helped

us a lot to complete it.

It was indeed a great opportunity for us to prepare this report of DLF LIMITED. It makes us aware of

the practical business environment. Here, the student gets an opportunity to learn the practical aspect of

business administration and can apply the theoretical knowledge in practice.

We would like to express our gratitude to Prof. Mr.Balraj who has given us an opportunity to prepare

market survey report and provided us the necessary guidelines and also guide us in preparing the t

report.

We are also very thankful to the other teaching & non-teaching staff of the institute for extended their

help; co-operation and support which have greatly ease our work and made our report unproblematic.

At Last but not least we would like to thank all those who helped directly or indirectly for

preparation of this financial report, their efforts have not gone unnoticed.

Thanks for being there.

EXECUTIVE SUMMARY

For any company analysis is very important because by analyzing company on financial basis you are

able to know its profit & loss that you can do analysis of their current & liquidity position, not only this

you are also able to know the financial position of the company & whether to invest in to or not. You

can also know that it is a good company or loss making company.

This project report is prepared on Analysis of DLF group Ltd. This report contains main theme of the

report that is Analysis of DLF group.

The initial part of this report is the general information of the DLF Ltd. It contains the introduction of

the company, History, General & Corporate Information, Formal Distribution of Employee.

.

REAL ESTATE SECTOR – AN OVERVIEW

The real estate sector plays a significant role in the Indian economy: it is second only to agriculture in terms of employment generation and substantially contributes to the gross domestic product of the country. Almost 5 per cent of GDP is contributed by the housing sector, and in the next few years it is expected to rise to 6%.

According to the report of the Technical Group on Estimation of Housing Shortage, an estimated shortage of 26.53 million houses was reported which gives a big investment opportunity for DLF. Market analysis expects returns from realty in India at an average of 14% annually with a tremendous upsurge in commercial real estate on account of the Indian BPO boom. Further, the housing sector has been growing at an average of 34% annually, while the hospitality industry witnessed a growth of 10-15%.

India leads the pack of top real estate investment markets in Asia for 2010, according to a study by PricewaterhouseCoopers (PwC) and Urban Land Institute, a global non-profit education and research institute, released in December 2009. The report, which provides an outlook on Asia-Pacific real estate investment and development trends, points out that India, in particular Mumbai and Delhi, are good real estate investment destinations. Residential properties are viewed as more promising than other sectors. While, Mumbai, Delhi and Bengaluru top the pack in the hotel 'buy' prospects as well.

According to the data released by the Department of Industrial Policy and Promotion (DIPP), housing and real estate sector including cineplex, multiplex, integrated townships and commercial complexes etc, attracted a cumulative foreign direct investment (FDI) worth US$ 8.4 billion from April 2000 to April 2010 wherein the sector witnessed FDI amounting US$ 2.8 billion in the fiscal year 2009-10.

At the time of depression Indian real estate sector was affected the most. But with the help of cumulative GDP rate and booming economy Indian Real Estate was able to stand again and has emerged at one of the topmost positions in real estate sector in Asia, after China.

The recovery in the Indian real estate sector is still in its early stages due to the lag effect. Within the sector, the homes segment has seen buoyancy in volumes and prices while the commercial segment lacks demand both for offices and retail malls. The industry has also seen developers in a significant credit crunch and hence accelerated access to the capital markets, renewed borrowings from the banking system and non-core asset sales have also been undertaken aggressively by the sector.

REAL ESTATE SECTOR THREE SEGMENTS:-

1)Residential Segment

2)Commercial Segment

3)Retail Segment

Residential SegmentSubsequent to the economic crisis in 2008, there was a sudden and sharp fall in the demand of real estate products. Customers postponed their buying decisions on account of job uncertainties and concerns of regular income resulting from the economic slowdown.The increased uncertainty of business expansion led to companies slowing or completely freezing any new employee additions. This created a huge demand- supply gap, wherein supply exceeded demand leading to a significant correction in prices. With the fiscal stimuli announced by the Government and the growth recovery in the economy, this trend gradually reversed in the second half of FY’10 with prices stabilizing to moving up in certain micro markets. The credit crisis in 2008-09 also brought along with it a paradigm shift in consumer preferences from attaining luxury and high end products towards the more affordable and mid income products. Developers thus shifted focus from luxury and high end offerings towards offering a judicial portfolio of mid-income/affordable and luxury residential projects. While the demand drivers in the homes segment continue to drive longer term growth prospects, higher inflationary concerns and the Governments initiatives to control inflation through monetary & fiscal measures could result in an interest rate up cycle impacting affordability of customers. In the current environment, the steep price increase that has been witnessed in some micro markets, especially city centre locations, are seeing volumes tapering off as customers are holding back their purchase decisions in anticipation of a marginal price correction.

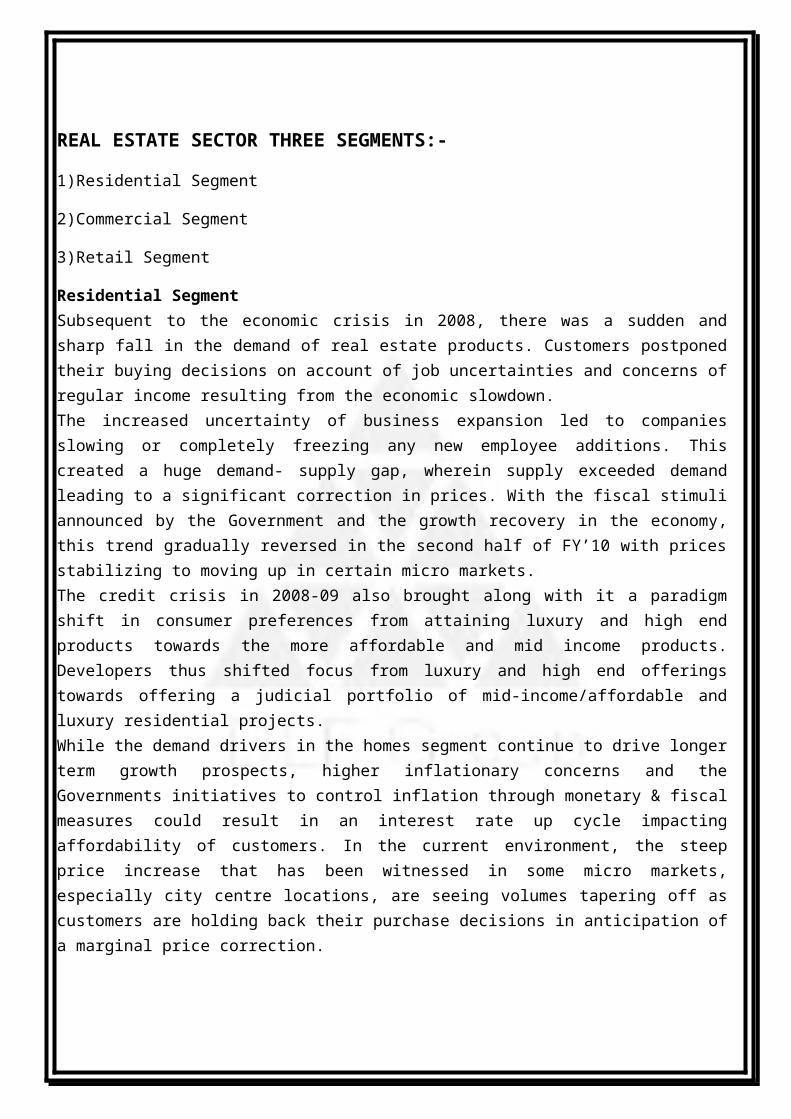

RESIDENTIAL DEMAND(2011-2015)

It is expected that the demand for residential segment is going to increase by cumulative 9.3 million units by 2015. The affordable and mid segment category is likely to constitute 85% of the total demand. 43% of the total demand is likely to be generated in the cities of Bangalore, Mumbai & NCR

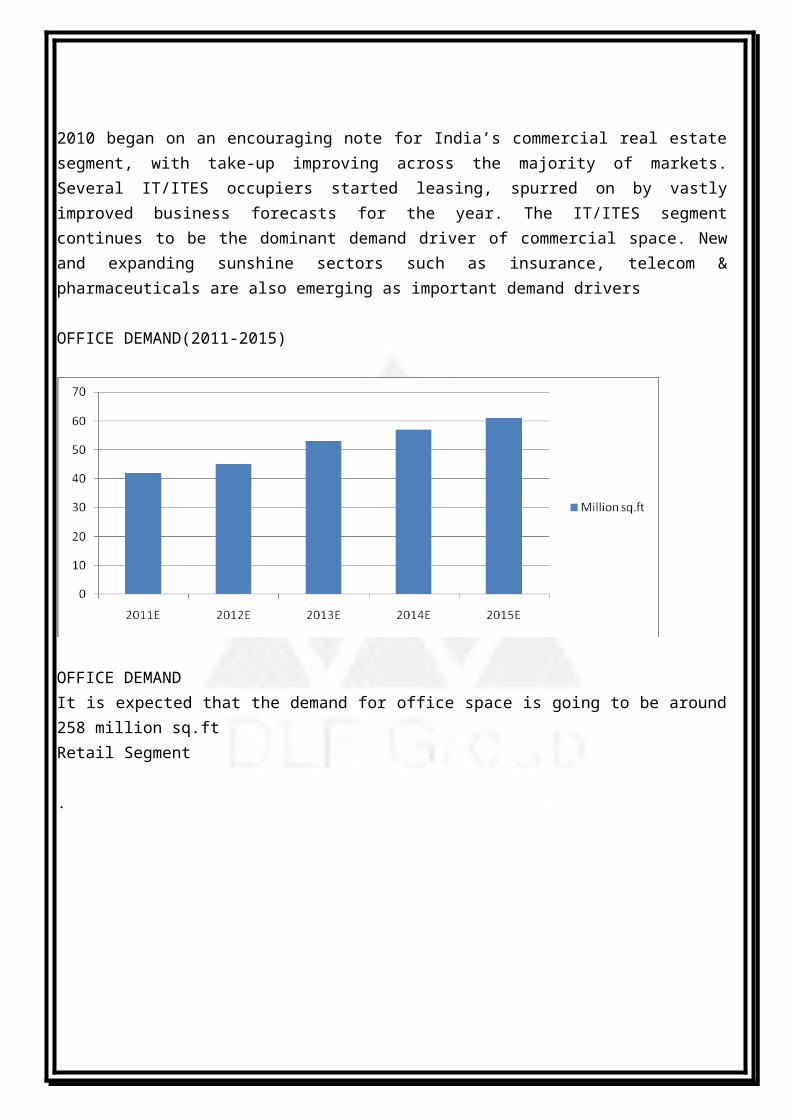

Commercial SegmentThe Indian office market did not remain insulated from the global upheavals in 2008-09 and consequently real estate activities in the segment witnessed a significant slowdown as compared to previous years. The majority impact of the slowdown was observed in the first-half of FY’10, when several projects were pulled back due to the liquidity crisis. Lack of business confidence and deferment of expansion plans by companies also led to a drastic fall in leasing activity. Various developers shelved their commercial projects which resulted in the reduced supply of commercial office space across major cities. SEZ projects were also under pressure during the year due to the STPI extension of one year. As a result, various SEZ projects were deferred, with some developers even de-notifying their SEZs. Almost all micro markets experienced rental corrections over the previous year. The rate of correction, however, eased out by the second half of FY’10, with many locations beginning to stabilize. 2010 began on an encouraging note for India’s commercial real estate segment, with take-up improving across the majority of markets. Several IT/ITES occupiers started leasing, spurred on by vastly improved business forecasts for the year. The IT/ITES segment continues to be the dominant demand driver of commercial space. New and expanding sunshine sectors such as insurance, telecom & pharmaceuticals are also emerging as important demand drivers

OFFICE DEMAND(2011-2015)

OFFICE DEMANDIt is expected that the demand for office space is going to be around 258 million sq.ftRetail Segment

.

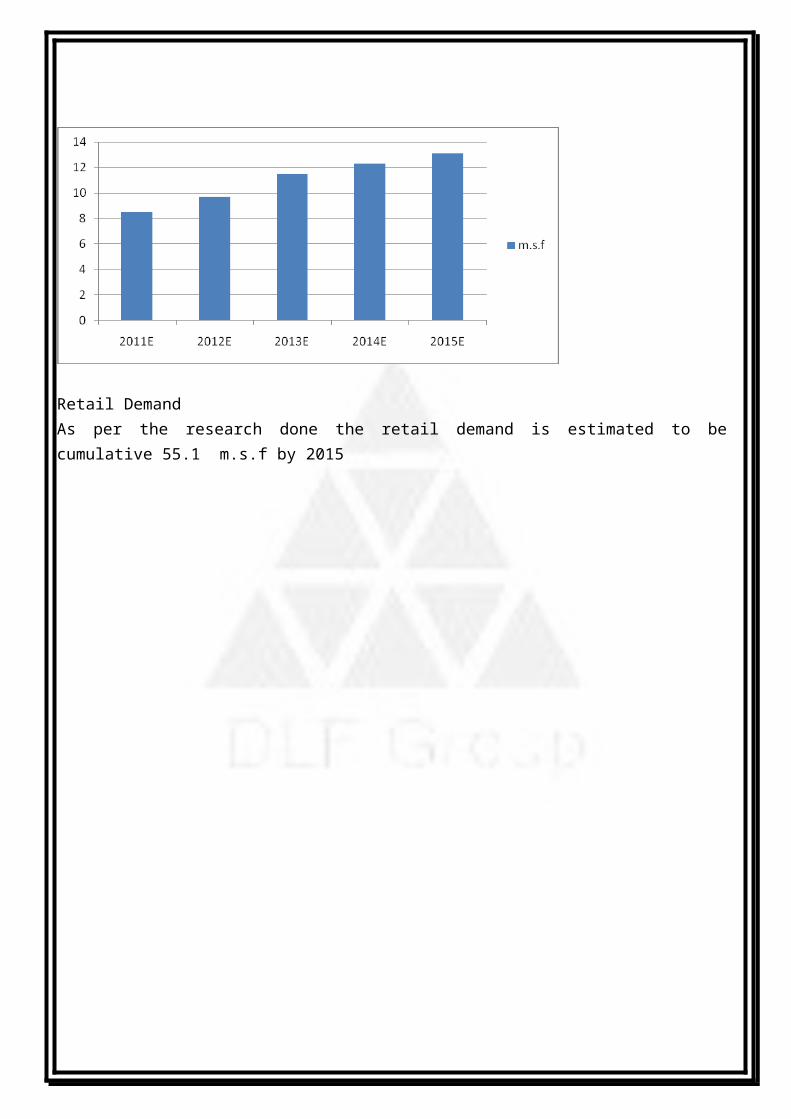

Retail Demand As per the research done the retail demand is estimated to be cumulative 55.1 m.s.f by 2015

CHAPTER 1

Company Profile

DELHI LAND AND FINANCE (DLF)

DLF Group is India’s one of the most famous and successful builders’ group. It is impossible to discuss the real state sector in India without giving a special reference to DLF group. It started as ‘Delhi Lease and Finance’ in 1946 aimed at revolutionizing the Real Estate industry in the country. Led by the visionary K. P. Singh in 1946, DLF began its journey from developing some of the initial Residential Colonies in the city. After the Delhi Government banned the private Real Estate and Residential

Colony Development in Delhi, the DLF group is completely involved in the development of the city of Gurgaon and other areas in NCR. The Company’s internal business includes development business and rental business.

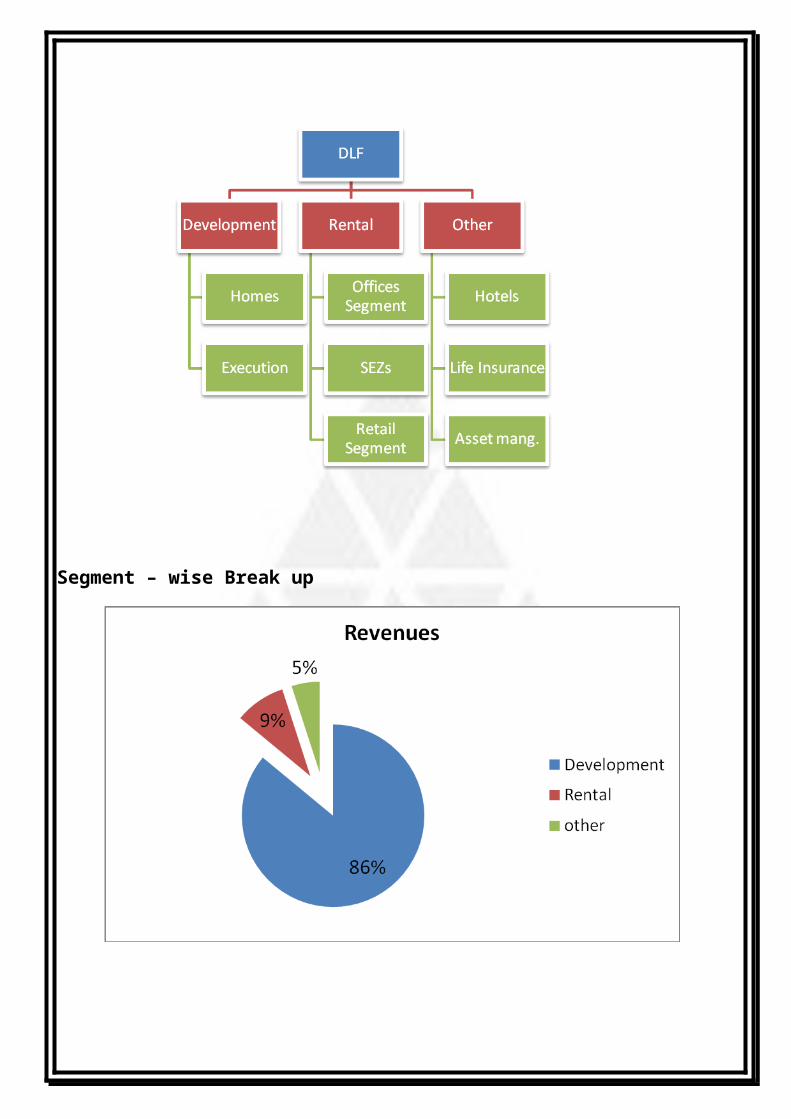

Business Review

Segment – wise Break up

(A) Development Business

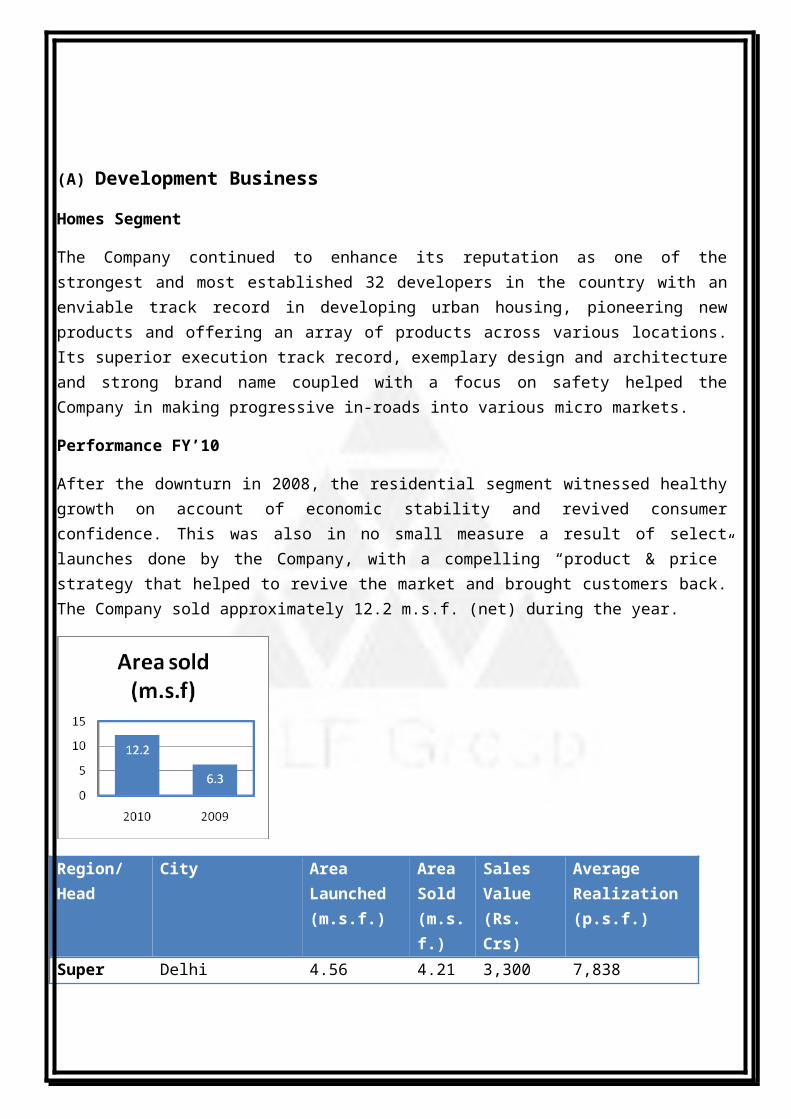

Homes Segment

The Company continued to enhance its reputation as one of the strongest and most established 32 developers in the country with an enviable track record in developing urban housing, pioneering new products and offering an array of products across various locations. Its superior execution track record, exemplary design and architecture and strong brand name coupled with a focus on safety helped the Company in making progressive in-roads into various micro markets.

Performance FY’10

After the downturn in 2008, the residential segment witnessed healthy growth on account of economic stability and revived consumer confidence. This was also in no small measure a result of select launches done by the Company, with a compelling “product & price” strategy that helped to revive the market and brought customers back. The Company sold approximately 12.2 m.s.f. (net) during the year.

Region/Head City AreaLaunched (m.s.f.)

Area Sold(m.s.f.)

Sales Value(Rs. Crs)

AverageRealization (p.s.f.)

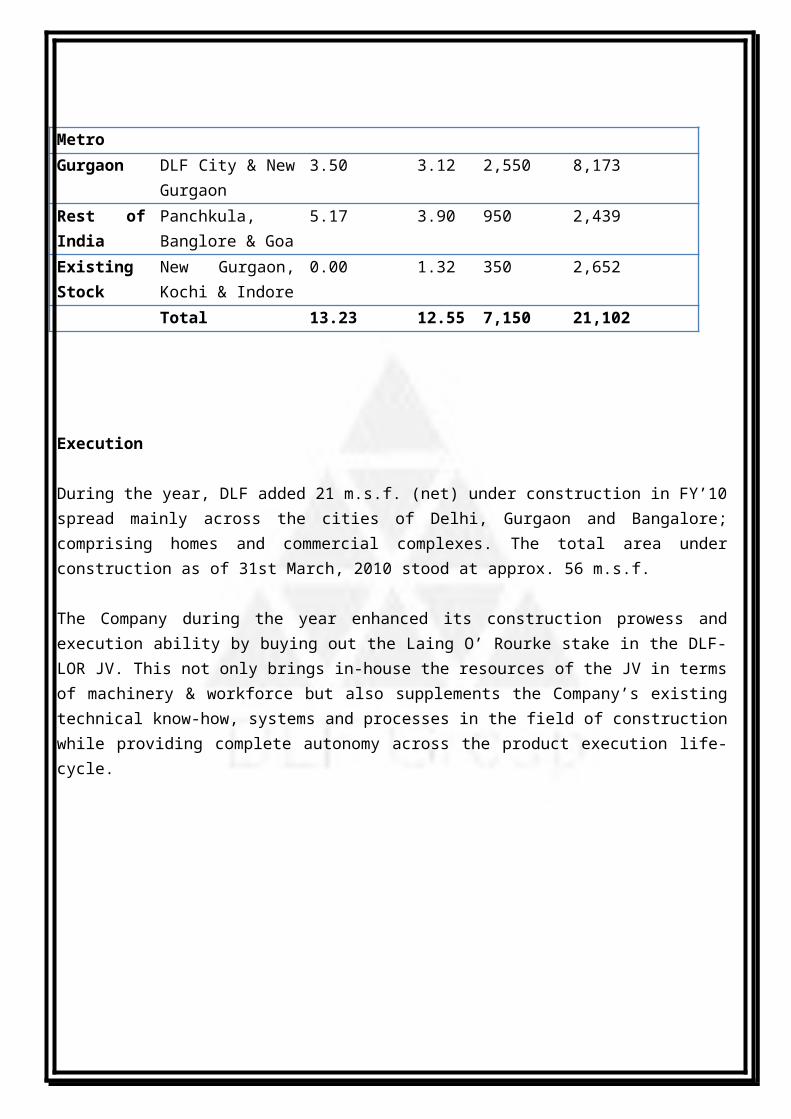

Super Metro Delhi 4.56 4.21 3,300 7,838

Gurgaon DLF City & New Gurgaon

3.50 3.12 2,550 8,173

Rest of India Panchkula, Banglore & Goa

5.17 3.90 950 2,439

Existing Stock

New Gurgaon, Kochi & Indore

0.00 1.32 350 2,652

Total 13.23 12.55 7,150 21,102

Execution

During the year, DLF added 21 m.s.f. (net) under construction in FY’10 spread mainly across the cities of Delhi, Gurgaon and Bangalore; comprising homes and commercial complexes. The total area under construction as of 31st March, 2010 stood at approx. 56 m.s.f.

The Company during the year enhanced its construction prowess and execution ability by buying out the Laing O’ Rourke stake in the DLF-LOR JV. This not only brings in-house the resources of the JV in terms of machinery & workforce but also supplements the Company’s existing technical know-how, systems and processes in the field of construction while providing complete autonomy across the product execution life-cycle.

(B) Rental Business

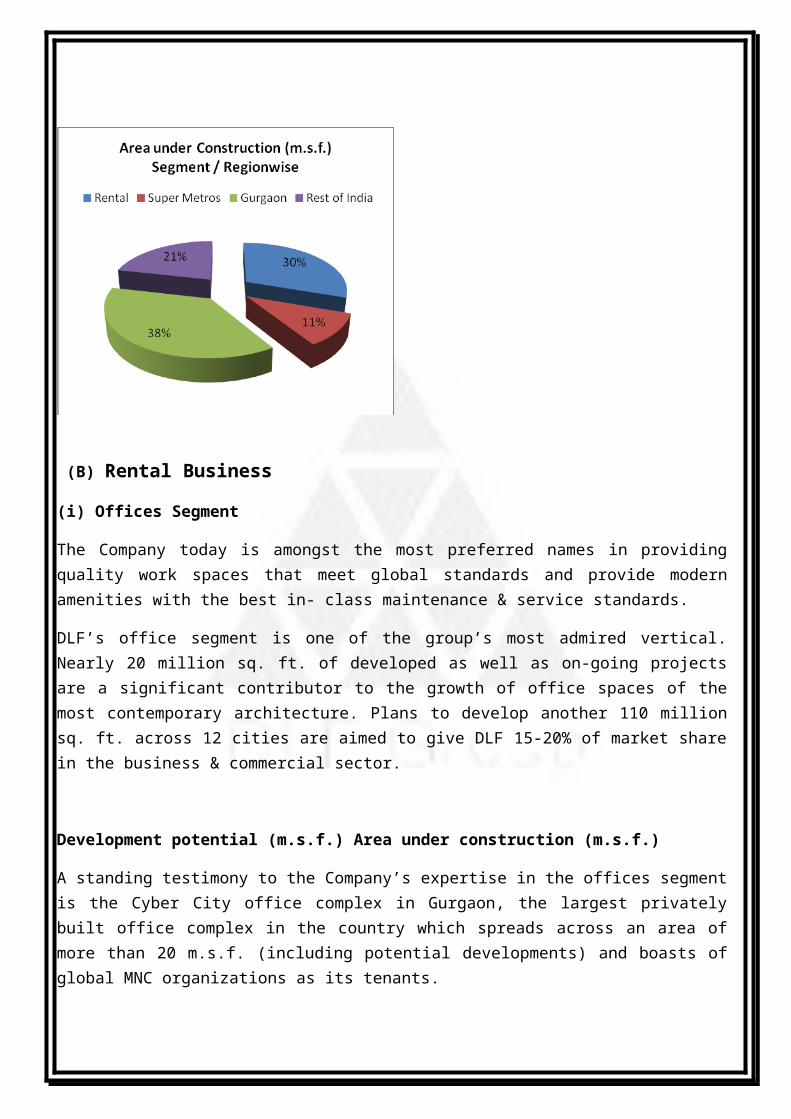

(i) Offices Segment

The Company today is amongst the most preferred names in providing quality work spaces that meet global standards and provide modern amenities with the best in- class maintenance & service standards.

DLF’s office segment is one of the group’s most admired vertical. Nearly 20 million sq. ft. of developed as well as on-going projects are a significant contributor to the growth of office spaces of the most contemporary architecture. Plans to develop another 110 million sq. ft. across 12 cities are aimed to give DLF 15-20% of market share in the business & commercial sector.

Development potential (m.s.f.) Area under construction (m.s.f.)

A standing testimony to the Company’s expertise in the offices segment is the Cyber City office complex in Gurgaon, the largest privately built office complex in the country which spreads across an area of more than 20 m.s.f. (including potential developments) and boasts of global MNC organizations as its tenants.

Performance FY’10

Outlook

With India Inc.’s aggressive hiring plans and the buoyancy in the economy, demand for office leasing is expected to improve in the coming years. For the Company, the first quarter of fiscal 2011 has seen leasing of 0.9 m.s.f., higher than the whole of last year. However, while volumes are expected to show a recovery, given the existing and oncoming supply of office space, market rents are unlikely to increase in the short to medium term.

The year gone by was challenging in terms of leasing activity as Company’s postponed business expansion plans and new ventures were delayed or shelved due to the uncertainty in the environment and lack of business confidence. Rentals corrected sharply and existing available inventory forced developers to stall or postpone ongoing constructions. With the revival in the economy, leasing enquiries gradually picked up pace and rentals stabilized. As clarity emerged on business growth prospects, the office segment started showing signs of revival in the last quarter of FY’10. The office leasing environment has been steadily improving with the Company having leased 0.7 m.s.f. area in FY’10 (after accounting for cancellations). Deliveries of approx. half a m.s.f. were made during the year.

Outlook

The office segment, though exhibiting signs of initial pickup, is subject to the continuing recovery in the economy and the crystallization of the Indian industry’s growth and expansion plans. Given the ongoing pressures on the Government, the current macro environment may witness policy actions that could hamper the current growth momentum. Any withdrawal of the stimulus measures in global powerhouses such as U.S.A. & China along with the troubles in the European Union could impact the leasing momentum in the office space. Another major factor that could potentially favour or impede growth in the office leasing environment would be the impact of the proposed Direct Tax Code and its effect on the IT SEZ’s. Clarity on this front is yet to emerge. With its superior locations and strong client relationships, the Company is well positioned to take advantage of the India growth story and is expected to be amongst the biggest beneficiaries as and when the leasing demand strengthens. The Company expects to lease 3-4 m.s.f. of office space during FY’10-11 across various locations.

(ii) SEZ

Special Economic Zones (SEZ) have acquired special status of importance from the Government of India as they have been categorized to bring infrastructural development and economic growth in that region. DLF has also taken the stride to develop SEZ across the country which will showcase world-class, state-of-the-art infrastructure and will include utilities such as roads and other public services, commercial centers, residential facilities and institutional facilities like schools, hospitals, etc.

Their first SEZ by DLF, proposed to be developed in Amritsar spreading over an expanse of 1100 acres, will comprise of four sector-specific individual SEZs for the textile and garments industry, engineering industry, food processing industry and a free trade and warehousing zone. It also has investment plans to develop an Rs 10,000 crore multi-product SEZ in Tamil Nadu.

(iii) Retail Segment

In the Retail segment, the Company has the expertise to cater to different retail formats. The Company was amongst the earliest one’s to realize & recognize the changing consumer preferences of the Indian customer and resultant spending patterns. With higher disposable incomes, a global exposure to aspiration and luxury products and the increasing influence & desire of a premium lifestyle by the Indian urban youth, the retail industry witnessed a paradigm shift.

With a booming retail environment on the horizon, this is a major thrust area for the Group and DLF is actively creating new shopping and entertainment spaces all over the country. There are over 42 million sq. ft. of quality retail space developed and under development in metros and other urban destinations across the country. These include categories of prime downtown shopping districts, shopping centers and super luxury malls.

With the benefits of an established brand name and strong track record coupled with a quality portfolio of premium locations across India, the Company was able to serve the needs of customers with different buying patterns and purchasing power. With pioneering the retail revolution in early 2000, the Company today has well proven expertise in providing a “one stop shop” shopping and entertainment experience by providing a discernible set of shopping labels and brands intermingled with an array of recreational & leisure options 35 in thoughtfully conceived and aesthetically designed premium architectural and commercial landmarks.

The Company today has approx. 1 m.s.f. of operational Malls located in the cities/ regions of NCR, Delhi, Chandigarh, Kolkata etc. Amongst its prominent retail malls are the Emporio, DLF Promenade & DLF Place, Saket all based in New Delhi and having an enviable tenant profile comprising luxury, premium and semi premium brands as its tenants.

Performance FY’10

The year gone by has seen the retail segment as the most challenging due to lower consumer spending and preference towards basic necessities rather than luxury offerings, hence impacting tenant business. Rentals corrected sharply and a host of ongoing developments were stopped mid-way due to the complete lack of leasing demand. Brands postponed their expansion plans and existing tenants exited unviable outlets. Revenue sharing agreements between developers and anchor stores emerged as a new trend in the industry where many such transactions were witnessed in the year gone by.

The first half of 2009-10 witnessed complete lack of movement in the demand for retail space; the second half saw the emergence of enquiries in select locations. The current focus for the Company would be to consolidate its position in the segment and increase its occupancy levels in existing operational malls.

Outlook

While still subdued, the revival in the economy and growing consumer confidence is expected to result in a gradual pickup in leasing transactions. The Governments FDI policy in multi-brand retail could be a significant growth driver in the short to medium term.

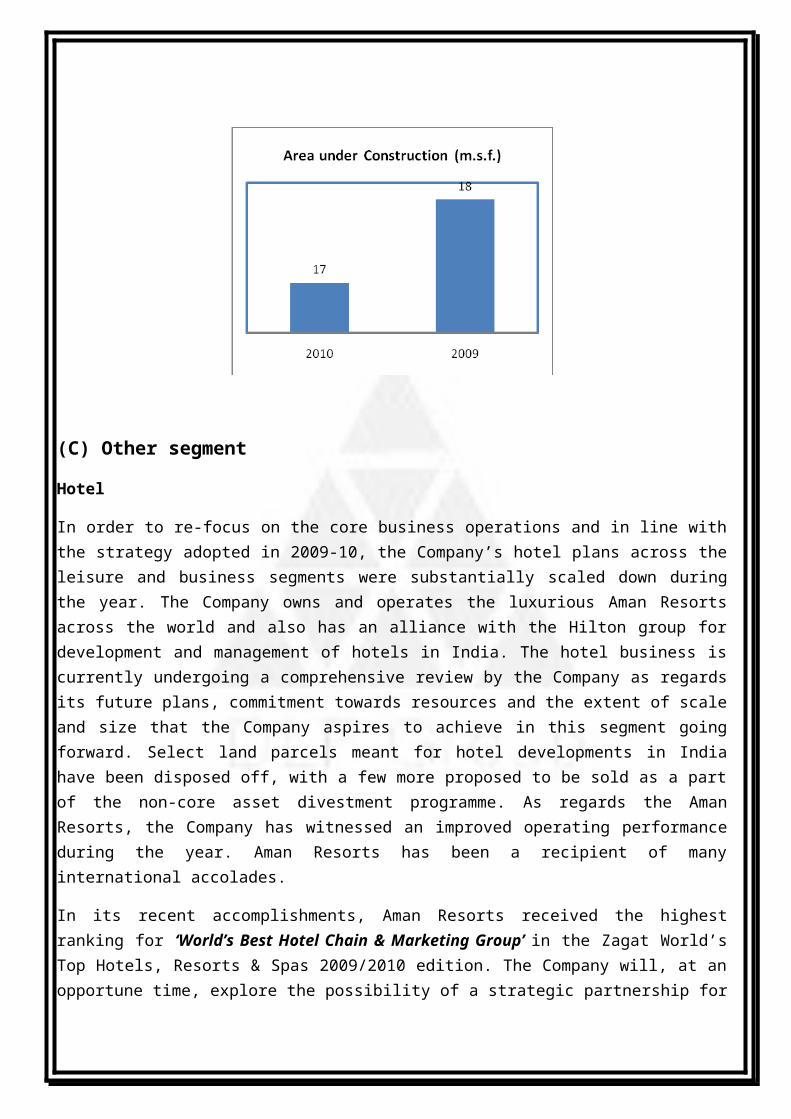

Project Execution Status and Development Potential

The Company as on 31st March, 2010 has 17 m.s.f. of area under construction in the Rentco. The area available for potential development in the Rentco (including area under construction) stood at 90 m.s.f.

(C) Other segment

Hotel

In order to re-focus on the core business operations and in line with the strategy adopted in 2009-10, the Company’s hotel plans across the leisure and business segments were substantially scaled down during the year. The Company owns and operates the luxurious Aman Resorts across the world and also has an alliance with the Hilton group for development and management of hotels in India. The hotel business is currently undergoing a comprehensive review by the Company as regards its future plans, commitment towards resources and the extent of scale and size that the Company aspires to achieve in this segment going forward. Select land parcels meant for hotel developments in India have been disposed off, with a few more proposed to be sold as a part of the non-core asset divestment programme. As regards the Aman Resorts, the Company has witnessed an improved operating performance during the year. Aman Resorts has been a recipient of many international accolades.

In its recent accomplishments, Aman Resorts received the highest ranking for ‘World’s Best Hotel Chain & Marketing Group’ in the Zagat World’s Top Hotels, Resorts & Spas 2009/2010 edition. The Company will, at an opportune time, explore the possibility of a strategic partnership for Aman Resorts in order to further strengthen the current business model.

Life Insurance

DLF Pramerica Life Insurance Company Ltd. (DPLI), a 74:26 JV between DLF Limited and Prudential International Insurance Holdings (PIIH) commenced operations in September, 2008 with a purpose to market and sell life insurance products in the country.

The Company has completed one full year of commercial operations as on 31st March, 2010. With a consistent focus on a steady strategy of capital conservation, sound liquidity and enhancement of operational and cost efficiencies, the overall financial performance during the last year was in line with the business plans envisaged.

Asset Management

The Company exited its asset management JV during the year. The Company’s decision to exit the business was triggered due to the changes by SEBI in its evaluation criteria for granting approval to the joint venture mutual fund to commence business in India. This primarily involved both the partners to have a five year track record in the financial services sector precluding DLF from partnering Prudential Financial Inc. in the business.

DLF partener

Construction

In February 2006, DLF entered into a joint venture with UK's leading construction company,

Laing O'Rourke Plc. The joint venture company will improve the quality of construction in all

the developments and help in setting new benchmarks in the real estate sector. The JV Company

is currently executing prestigious projects like- The Magnolias, The Mall of India, IT Parks and

many of DLF's retail destinations. DLF-LOR will construct the Group's infrastructure projects,

including roads, bridges, tunnels, pipelines, harbors, runways and power plants, through this JV.

Laing O'Rourke operates worldwide, in Asia, Europe, the Far East and Australia and employs

more than 23,000 people. Their best know projects include Terminal 5 at London Heathrow

airport , a terminal at the Dubai international airport, the Millennium Dome in the UK and a

Convention Centre in Hong Kong

Hospitality

DLF's hospitality arm, DLF Hotels, has signed an LoI with Four Seasons Hotels and Resorts to

operate a proposed luxury hotel at DLF Golf Links in DLF City, Gurgaon in Delhi's southern

borders. In November 2006, DLF Hotels announced its first joint venture with The Hilton

Hotels to acquire and develop 50 to 75 hotels and serviced apartments throughout India.

The joint venture hotels will represent several brands from Hilton Hotels Corporation's brand

portfolio, including Hilton Hotels, Hilton Garden Inn, Homewood Suites by Hilton and Hilton

Residences. The JV Company will develop and build these properties, while Hilton will manage

them.

DLF will hold 74 per cent in the joint venture company, and Hilton will hold the remaining

stake as its commitment to the venture. Over the next 5 to 7 years, Hilton has committed to

invest up to $ 143 million.

The initial stage of the joint venture will involve 20 hotels in a number of key locations

including, Chennai, Kochi, Bhubaneshwar, Hyderabad, Kolkata and Delhi. Some of these hotels

are planned to be Hilton Garden Inns and Hilton Hotels. Beyond the initial 20, the JV continues

to identify and acquire sites and undertake new hotel developments.

IT Infrastructure

DLF has partnered with IBM to outsource all its IT requirements to the global IT infrastructure

giant. Under this partnership IBM will be responsible for the helpdesk services for all the DLF

employees across India towards the IT infrastructure requirements. The partnership will support

the current IT requirements as well as identify and deploy new solutions for DLF and Indian real

estate industry.

At DLF joint ventures and strategic alliances are another facet of the Group's determined growth

with some of the best names globally.

Asset Management

DLF and Prudential Financial Inc. (PFI) of US, have signed a joint venture to provide a broad

array of mutual fund and investment products, including domestic and eventually international

mutual funds to Indian retail and institutional clients. The JV has been formulated on a 61:39

shareholding pattern between PFI and DLF. This agreement allows PFI to expand its

international investments business and marks its official entry into the Indian mutual fund

market.

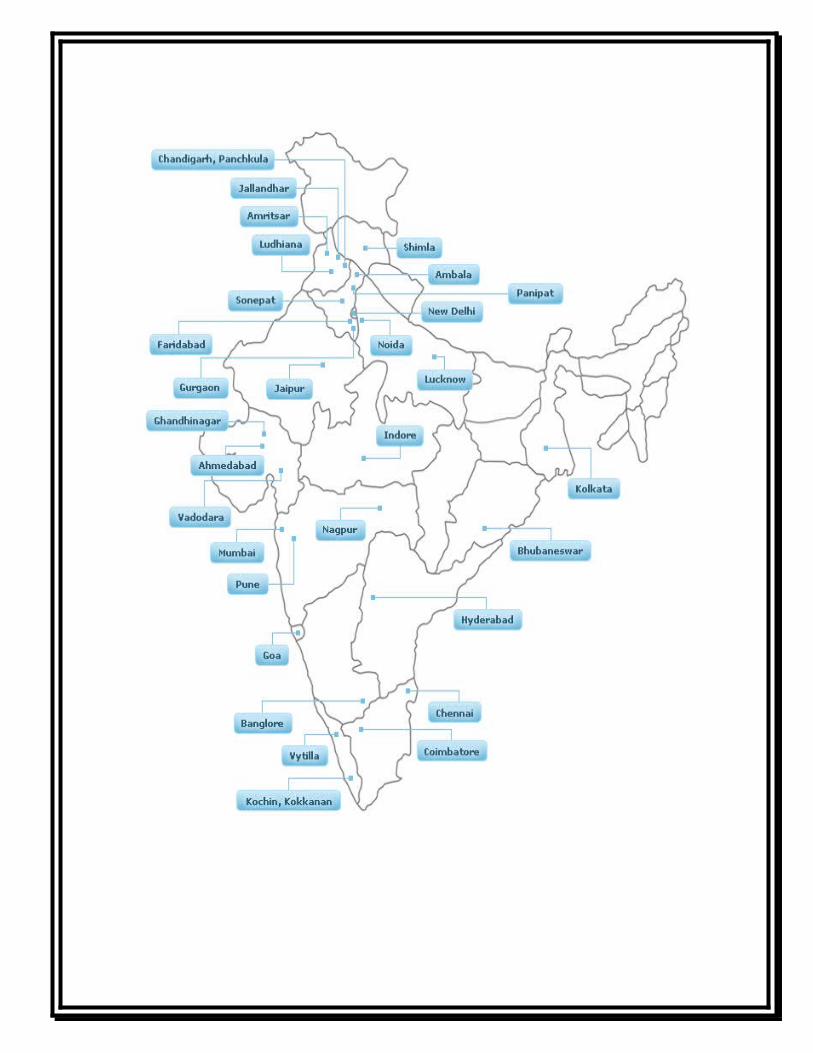

1.4.2 DLF's Presence

The following map shows the locations of our developments, projects and lands across India

1.4.3 Vision, Mission & Values

DLF Vision

To contribute significantly to building the new India and become the world’s most valuable real

estate company.

DLF Mission

To build world-class real-estate concepts across six business lines with the highest standards of

professionalism, ethics, quality and customer service

DLF Values

Sustained efforts to enhance customer value and quality

Ethical and professional service

Compliance and respect for all community, environmental and legal requirements.

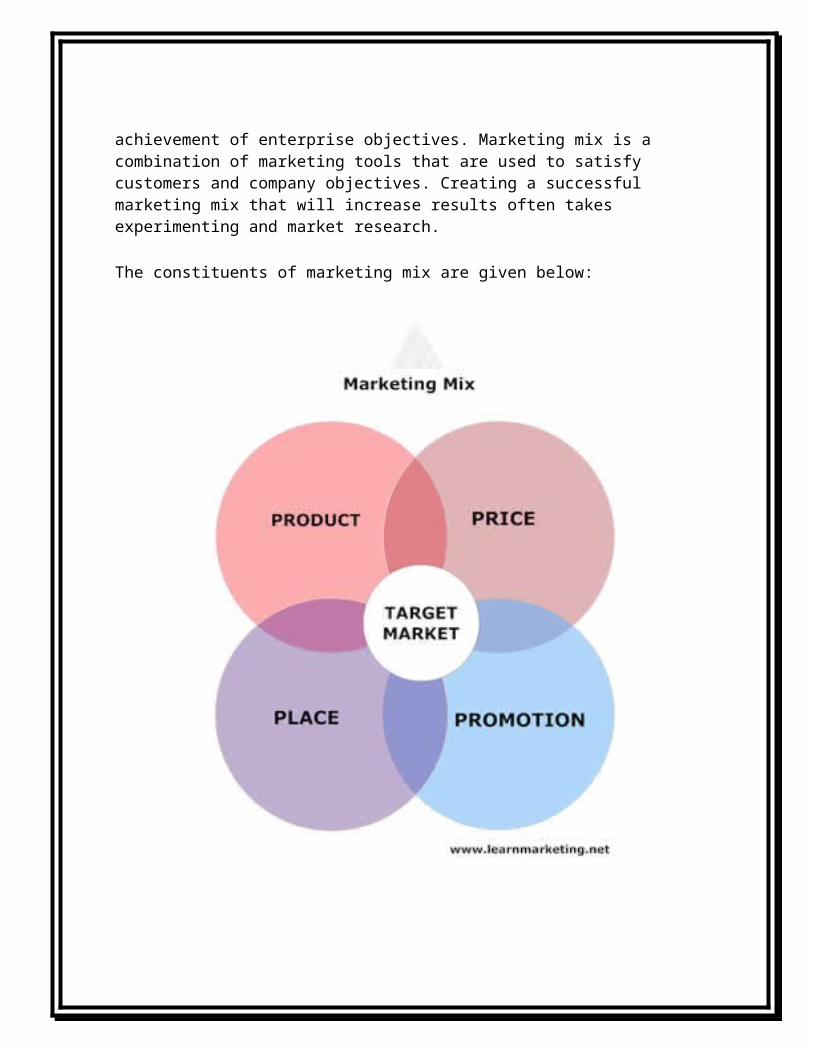

MARKETING MIX: 4-P STRATERGY

Marketing mix is the process of designing and integrating various elements of marketing in such a way as to ensure the achievement of enterprise objectives. Marketing mix is a combination of marketing tools that are used to satisfy customers and company objectives. Creating a successful marketing mix that will increase results often takes experimenting and market research.

The constituents of marketing mix are given below:

PRODUCT:

Product refers to a physical product or a service or an idea which a consumer needs and for which he is ready to pay. Physical products include tangible goods like grocery items, garments etc. Services are intangible products which are offered and purchased by consumers. Services may involve also an innovative idea on any aspect of operation. A product is the key element of any marketing mix. The decisions concerning product may relate to –

Product attributes Branding Packaging and labeling Product support service Product mix.

India is blessed with one of the fastest growing real estate markets in the world. It is not only attracting domestic real estate developers but also the foreign investors. But despite all these facts, the ever growing Indian population is always putting up the pressures on housing creating the shortage of houses in India. Also the recession period during 2008-2009, the real estate sector saw around 50% reduction in prices. This prompted the realtors to take effective measures to take control of the situation. Due to all this Low Cost Housing became the new buzz word in real industry. From buyers to the sellers to the realtors and investors, everyone is pitching for affordable quality homes in India.

We planned Low cost housing as the new product for our company DLF.DLF is India's largest real estate company in terms of revenues, earnings, market capitalization and developable area. DLF's primary business is development of residential, commercial and retail properties. The company has a unique business model with earnings arising from development and rentals. Its exposure across businesses, segments and geographies, mitigates any down-cycles in the market. DLF has also forayed into infrastructure, SEZ and hotel businesses.

Low cost housing will include construction of 1 or 2 BHK houses set up in the colony system. These low cost houses will be the constructed in Tier-2 cities of India like Chandigarh, Jaipur, Hyderabad, Luknow etc.According to Indicus Analytics, An Economics Research Firm,90% of the urban households have incomes under 5 lakhs.Going by this our category of housing is best suited to this group of households. The area of construction of these houses would be 250 – 500 square feet. We will be targeting both mixed and lower income group customers.

This looks a good venture for DLF as it has an advantage over its competitors due to the following factors:

BRANDING: DLF has the advantage of being the number 1 player in the real estate market. It is having huge capital reserves to fund this new project line.

QUALITY: DLF is in this sector for 62 years. It has given quality infrastructure to the corporate and household ever since. This fact has been substantiated by the following awards received by the company like ‘Most Trusted Brand’ by the

Reader’s Digest magazine,’ Most diversified Real Estate Developer’ by CRISIL etc.

FUNCTIONALITY: The target customers of our low cost housing will be the mixed and lower income groups. These houses will provide all the basic amenities required in a home but there will be no frills attached.

SERVICE: DLF will be providing excellent after sale service like maintenance,security,water and power solutions to the customers.

PRICING:

Price is the amount charged for a product or service. It is the consideration paid by consumers for the benefit of using any product or service. Price fixation is an important aspect of marketing. There may be two types of Price fixation:

Cost based approach: This is the simplest method of pricing. Generally companies add a certain percentage of Profit, to the total cost of the product. The total cost of the product is calculated after taking all types of costs into consideration. While following this approach, no other factors e.g. prices of substitute goods, nature of demand, etc. are considered.

Competition-based approach : The prices are determined on the basis of conditions in the market. Companies may follow any one of the following three approaches.

a) Price-in-lineb) Market-plusc) Market-minus

Price-in-line means prices fixed nearly equal to the prices of close alternatives. Generally this happens under free market conditions i.e. when the number of buyers and sellers is so large that they cannot affect the prices.

When companies charge (fix up) a price which is more than the price of existing substitutes, it is called market plus pricing. This approach is adopted when the quality of a product is better, or it has a popular brand name, or its packaging is attractive and useful. Consumers will pay more only when they find distinctive differences in the product and its substitutes.

Sometimes business enterprises get ready to supply products at a price lower than the market price. It may be adopted to grab a larger market share or to make a newly introduced product more popular. This approach is called market-minus approach. Companies having shorter channels of distributions or direct selling facilities can afford to fix a price lower than the prevailing market price.

Our low cost housing will be targeting the lower and mixed income group customers. So, pricing will be around 1000 – 3000 per square feet. The total price of a house will be around 15 -25 lakhs.This will be made possible by the reduction in prices of cement by over 40% and in that of steel by over 20% in the past two years.DLF will tie up with land owners and provide them share of profit in lieu of low cost land. We can also seek subsidies from Government by taking up projects in Tier B cities on the SEZ concept.We can reduce the cost of our project yet give customers a quality product by adopting following techniques:

Reducing plinth area by reducing the wall thickness.E.g.15 cms thick solid concrete block wall.

Use locally available material in an innovative form like soil cement blocks in place of burnt brick.

Use energy efficiency materials which consume less energy like concrete block in place of burnt brick.

Use environmentally friendly materials which are substitute for conventional building components like use R.C.C. Door and window frames in place of wooden frames.

Preplan every component of a house and rationalize the design procedure for reducing the size of the component in the building.

By planning each and every component of a house the wastage of materials due to demolition of the unplanned component of the house can be avoided.

Each component of the house shall be checked whether if it’s necessary, if it is not necessary, then that component should not be use.

PROMOTION:

Promotion refers to using methods of communication with two objectives: (i) informing the existing and potential consumers about a product, and (2) to persuade consumers to buy the product. It is an important element of marketing mix. In the absence of communication, consumers may not be aware of the product and its potential to satisfy their needs and desires.

Techniques used in the promotion of project:

SALES PROMOTION:

a) We will offer discounts on first 50 bookings of the houses.b) We will give extra incentives to the dealers who will book maximum

houses.c) We will tie up with various banks and financing institutions to provide the

customers low interest loans.d) Also we can give free insurance to the customers.

ADVERTISING:

a) We will put huge advertising budget for our product.b) We will hugely endorse our product in newspapers, magazines and

also in TV and radio.c) We will put interactive billboards on critical places in all important

cities of India.

Direct Marketing:

Direct marketing is the use of consumer direct channels to reach and deliver goods and services to customers without using marketing middlemen. DLF can use a number of channels to reach target customers, namely

a) We will send the information about low cost housing cans to their target customers by sending brochures and magazines describing our product.

b) DLF’s customer support will be contacting the customers by phone and explaining features of the product thereafter.

c) We can upload the complete information of our new product on the main website of DLF so that anyone accessing the homepage of DLF must also be accessible to that information. Basically this method is useful in promoting the product among the existing customers of DLF.

d) Catalogs offer consumers a wide range of products of either a generalized or specialized nature. So we can add the low cost housing in the existing list of products so offered and present that catalog to their customers.

PUBLICITY:

Publicity takes place when a favorable presentation is made through mass media about a product or service. People believe more on such news than in advertising. It covers people who do not entertain personal selling and sales promotion approaches. It is a non-paid form of communication but sometimes it is not regarded as a promotional tool within the reach of a company.

PLACE:

Place is another important aspect of 4P strategy. This refers to how an organization will distribute the product or service they are offering to the end user. The organization must distribute the product to the user at the right place at the right time. Efficient and effective distribution is important if the organization is to meet its overall marketing objectives. If an organization underestimates demand and customers cannot purchase products because of it, profitability will be affected.

DLF will use its extensive network of offices all around the country. It has the required presence in every big city of the country. This is a housing project so we will also use our network of existing dealers and brokers. We will first of all target the upcoming developing cities for our project. This will include cities like Chandigarh, Hyderabad, Luknow, Ahmadabad etc.We will build these houses in the concept of SEZ with Govt. approval so that we can avail tax benefits also. Then after this we will target the big metropolitan cities of our country like Delhi, Mumbai, Kolkata, and Chennai. In these cities availability of land is a big concern, so we will construct houses in the outskirts of the city. DLF will have to place the product very efficiently to beat the competitors like TATA, Sobha Developers, Omaxe, Panchsheel developers etc.

SWOT ANALYSIS

Swot analysis:

It is the study of factors that affects the organization or the industry in both positive and negative ways.

Strength:Strength is defined as any internal asset, technology, motivation,finance, business links, etc that can help to exploit opportunities and tofight off threats.

Weakness:It is an internal condition which hampers the competitiveposition or exploitation of opportunities.

Opportunity:It is any external circumstance or characteristic which favoursthe demand of the system or where the system is enjoying acompetitive advantage.

Threat: It is a challenge of an unfavorable trend or of any externalcircumstance which will unfavorably influence the position of thesystem.

STRENGTHS:

Due to the boom in IT/ITES sector in India, there is a tremendous growth in the private sector housing and commercial building demands.

Good structured national network infrastructure like highways, expressways etc. have also facilitated the boom in real estate industry.

DLF is the largest real estate company in India, so it has got the required expertise and brand value. It has around 54% market share in Indian real estate market.

DLF has a huge supplier base ensuring fixed raw material cost which helps them in bringing the cost down.

A large quantity of low cost and skilled labor is available in north India,which is very ably utilized by DLF.

India is full of natural resources and raw materials which is required for the real estate industry.

WEAKNESS:

The biggest problem for DLF is that there is no parallel product in their product profile to support during periods of recession.

There are very small amount of projects with DLF in other parts of India other than the northern part.

DLF mostly deals in mega projects, and it becomes very difficult to allocate such large projects to external vendors.

This sector requires huge amount of capital investment and it will be very difficult for DLF to raise capital in recession periods.

OPPURTUNITIES:

The biggest opportunity for DLF is to expand in other parts of India like south India and to tap that underutilized market.

It can invest more in Power generation projects like hydroelectric or Wind power. DLF can also tap the Public sector infrastructure due to the rise in the expansion of

public sector companies like BHEL, NTPC etc. DLF can also concentrate on improving the supply chain management of raw

materials to cut down cost and increase the efficiency.

THREATS:

DLF will have to face a lot of competition in the future as the competitors in this industry are increasing by leaps and bounds, eg, sobha developers, parsvnath developers etc.

Long term market instability may damage the expansion and training development opportunities.

Natural calamities like earthquakes and foods can always prevent this industry to grow at a normal pace.

Political unrest and security concerns in India are a big threat for DLF to expand rapidly.

MARKET RESEARCH STRATEGY:

SURVEY LOCATION- NOIDA

VOLUME OF SURVEY NUMBER- 50

MODE OF CONDUCT OF SURVEY-INTERVIEWING EMPLOYED PEOPLE AGE

GROUP OF 30-40 YEARS.

PERSONAL VISIT TO THE OFFICE OF PROPERTY DEALER AND

INTERVIEWING THE PEOPLE.

OTHER Domestic Players in Real Estate

Unitech

• Operating various asset classes in residential, commercial and retail

segment

• Developed more than 7 million sq.ft. Of built up area (BUA)

• Specialises in planning residential, commercial, SEZ development, retail and

hospitality, integrated townships

• 430 million sq.tf. Of BUA under planned projects

• Major presence in National Capital Region and other areas such as Kolkata,

Chennai and Hyderabad

K Raheja Corp

• Present in Commercial, Retail & Residential asset classes

• Developed over 5 million sq. ft. of BUA

• Developing 15 self-contained townships and 10 hotels

• Planning to construct 13.2 million sq. ft. of BUA

• Major presence in Mumbai with operations in Banglore, Ahamedabad, Goa,

Pune and Hyderabad.

Ansal Properties

• Operates primarily in Residential & Commercial asset classes

• Developed over 2850 acres in Gurgaon and Delhi

• Developing integrated townships, malls, hotels IT parks and SEZs

• Plan to construct 157.6 million sq.ft. Of BUA

• Pan-India footprint with major presence in 16 North-Indian cities acress 4

states

Sobha Developers

• Asset classes include Residential, Commercial, Development of plots and

Contractual projects

• Developed over 4.5 million sq. ft. of BUA

• Planning residential and retail projects

• 101 million sq. ft. of BUA is planned under various projects

• Major concentration in Banglore with presence in other areas such as

Cochin, Chennai and Pune.

Parsvnath Developers

• Presence in Residential, Retail Commercial asset classes

• Developed over 3.8 million sq. ft. of BUA

• Plans to develop IT Parks and 12 SEZs across the country

• Plannin to construct around 46.5 million sq. ft. of BUA

• Major Presence in National Capital Region

• Increasing Pan-India Footprint, active in over 46 cities across 17 states

Conclusion:

We have a hold on DLF with it their aggressive plans for the future and focused on

selling existing inventory along with selective launching of new projects across all categories

of real estate development. However, there will be a specific focus on strengthening margins

across all projects.

Having built a strong asset base of rental assets, DLF will continue to focus on growing the

rental business of the Company to capture the growth in leasing demand to generate stable

cash flows. Though demand drivers continue to drive longer term growth prospects, higher

inflationary concerns and the Governments initiatives to control inflation through monetary

& fiscal measures could result in an interest rate up cycle impacting affordability of

customers.

BIBLIOGRAPHY

WEB LINKS

http://www.dlf.in/jsp

http://www.wikipedia.com/mediakit.jsp

Case Study:DLF India’s Leading Real Estate Company in Trouble

DLF Limited or DLF (originally Delhi Land and Finance) is India’s biggest real estate developer based in New Delhi, India. The DLF Group was founded by Raghuvendra Singh in 1946. The company is currently headed by Indian billionaire Kushal Pal Singh. DLF builds residential, office and retail properties.

This case study is about India’s largest real estate company DLF Limited’s (DLF) struggle in the stressed market conditions due to the global financial crises which started in the year 2007. The company which created India’s biggest IPO in history, raising more than US$ 2 billion, was counting on the continued growth of realty sector in the country.

However, the depressed economic situation coupled with credit crunch led to a significant decline in the demand and property prices. While the company had ambitions plans to launch several properties ranging from Special Economic Zones (SEZs), large townships, hotels, and convocation centers, the market conditions took its toll on the business. These factors disturbed the cash flow cycle of DLF, making it difficult for it to repay its debt on time. The debt to equity ratio of the company increased to all time of high of 0.7 in June, 2010, with inadequate debt paying capacity.

In light of these factors, DLF had to exit from many of its projects either before, or even in middle of starting the operations. The company devised several strategies overcome the prevailing situation. By the mid-2010, DLF had a much leaner business structure, but it still facing various challenges in bringing its business back into shape.

Issues:» Understand the real estate sector in India and issues and challenges faced by the market leader in this sector.

» Understand the impact of global financial crises on business dynamics.

» To analyze how macro and micro economic factors influences the success of an organization.

» Determine the internal competencies of business though SWOT analysis.

» Examine the role of external factors influencing business thorough PESTEL analysis.

» Appreciate the importance of healthy cash flow cycle for a business. » Determine the best product mix, thorough analysis of demand, revenue streams, and profitability from different verticals of business.

» Understand the criticality of decision making process in business, especially during stressed market conditions.

» Scrutinize the impact of increasing debts on planning, execution, and evaluation of business strategy.

» Understand the importance of tailoring business tactics and strategy to fit specific industry and company situations.

» Appreciate the role of corporate restructuring and turnaround strategies.

As on June 12, 2010, DLF Limited (DLF), India’s largest real estate company, had accumulated an outstanding debt of more than US$3100 million, marginally below the record high of US$3635 million in the month of March 2009. The net profit of the company also plunged by more than 60%, falling from US$993.25 million in financial year 2008-2009 to US$384.44 million in financial year 2009-2010. In addition to decreasing profits, DLF was struggling with an enormous outstanding debt and a high debt to equity ratio which stood at around 0.70 in the month of June 2010. To reduce its debt burden, DLF was considering selling 97% of its stake in Aman Resorts, a hotel chain it had acquired in November 2007 for about US$400 million, to Khazanah.If completed, this deal was expected to release between US$300 million and US$350, helping DLF cut its heavy debt pile. The company was also implementing many other strategies with an eye on reducing its debt burden and managing its cash flow efficiently.

According to analysts, DLF had been doing well since liberalization and had witnessed strong growth as a private company in the growing Indian economy. It went public in July 2007 with one of the biggest IPOs (Initial Public Offering) in India. DLF raised capital of more than US$2 billion to further strengthen its growth. This made it the eighth most valuable company in India and its promoters, KP Singh and his family, the fourth richest Indians, just behind the two Ambani brothers and Lakshmi Mittal.

It was expected that after this IPO, DLF would be able to grow much faster and change growing Indian real estate sector, which was growing rapidly along with the Indian economy. The funds raised from the IPO enabled DLF to reduce its prevailing debt and acquire additional land to develop properties in the years to come. However, the global financial crisis in 2008 created a grim situation, and hampered the anticipated growth of DLF…

![DLF - BROFER DIF DIAGRAMMA SCELTA RAPIDA / QUICK SELECTION DIAGRAM DLF 8-1000 DLF 7-1000 DLF 6-1000 DLF 5-1000 DLF 4-1000 DLF 3-1000 DLF 2-1000 DLF 1-1000 0 500 1000 1500 2000 Q [m3/h]](https://static.fdocuments.in/doc/165x107/5b06b1047f8b9ad5548d39b5/dlf-dif-diagramma-scelta-rapida-quick-selection-diagram-dlf-8-1000-dlf-7-1000.jpg)